Embed Size (px)

Citation preview

THE CASE OF EOLICAS DE PORTUGAL‘Local Strategies for Greening jobs and skills’

GABRIELA PRATA DIASOECD LEED Trento Centre for Local Development

9-11 June 2010

Topics

• National & local context 1

• Wind energy cluster – Eólicas de Portugal2

• Conclusions and results3

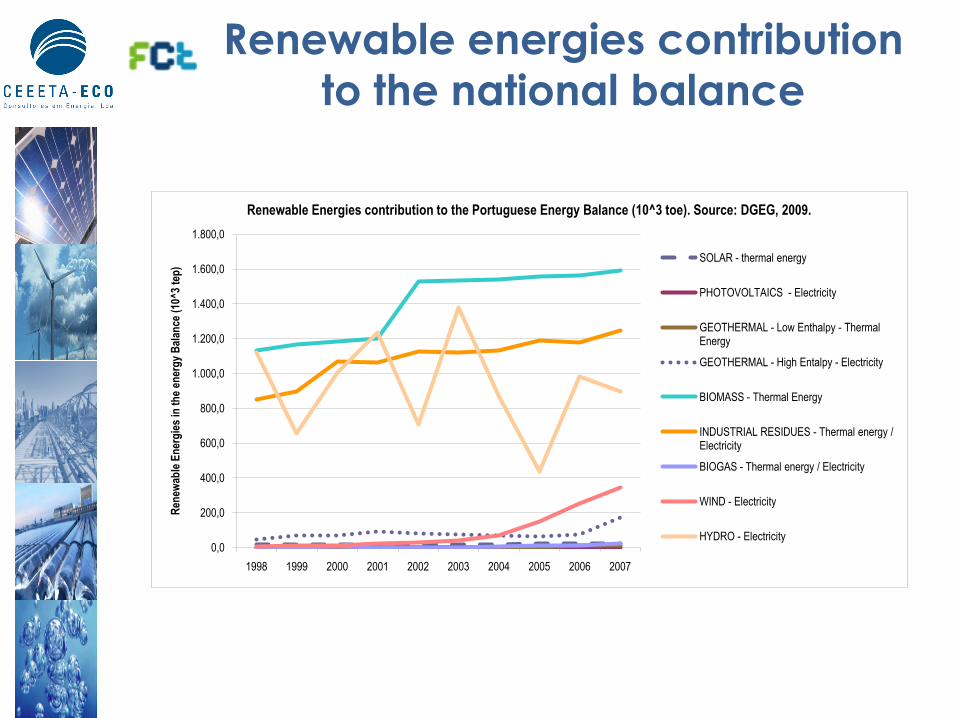

Renewable energies contribution to the national balance

0,0

200,0

400,0

600,0

800,0

1.000,0

1.200,0

1.400,0

1.600,0

1.800,0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Rene

wabl

e Ene

rgies

in th

e ene

rgy B

alanc

e (10

^3 te

p)

Renewable Energies contribution to the Portuguese Energy Balance (10^3 toe). Source: DGEG, 2009.

SOLAR - thermal energy

PHOTOVOLTAICS - Electricity

GEOTHERMAL - Low Enthalpy - Thermal Energy

GEOTHERMAL - High Entalpy - Electricity

BIOMASS - Thermal Energy

INDUSTRIAL RESIDUES - Thermal energy / Electricity

BIOGAS - Thermal energy / Electricity

WIND - Electricity

HYDRO - Electricity

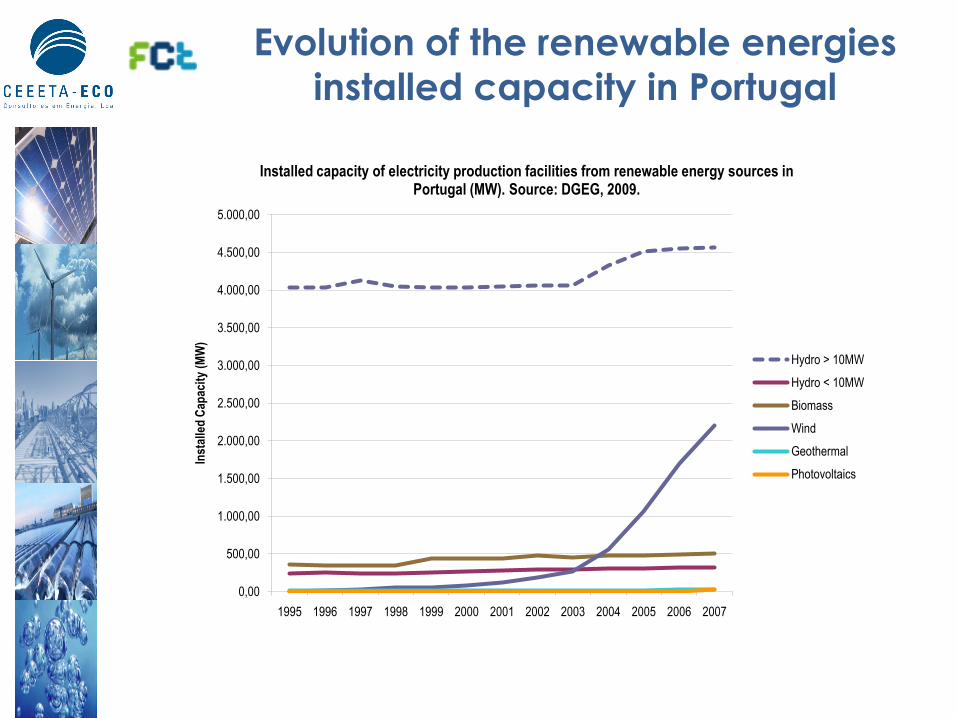

Evolution of the renewable energies installed capacity in Portugal

0,00

500,00

1.000,00

1.500,00

2.000,00

2.500,00

3.000,00

3.500,00

4.000,00

4.500,00

5.000,00

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Inst

alled

Cap

acity

(MW

)

Installed capacity of electricity production facilities from renewable energy sources in Portugal (MW). Source: DGEG, 2009.

Hydro > 10MWHydro < 10MWBiomassWindGeothermalPhotovoltaics

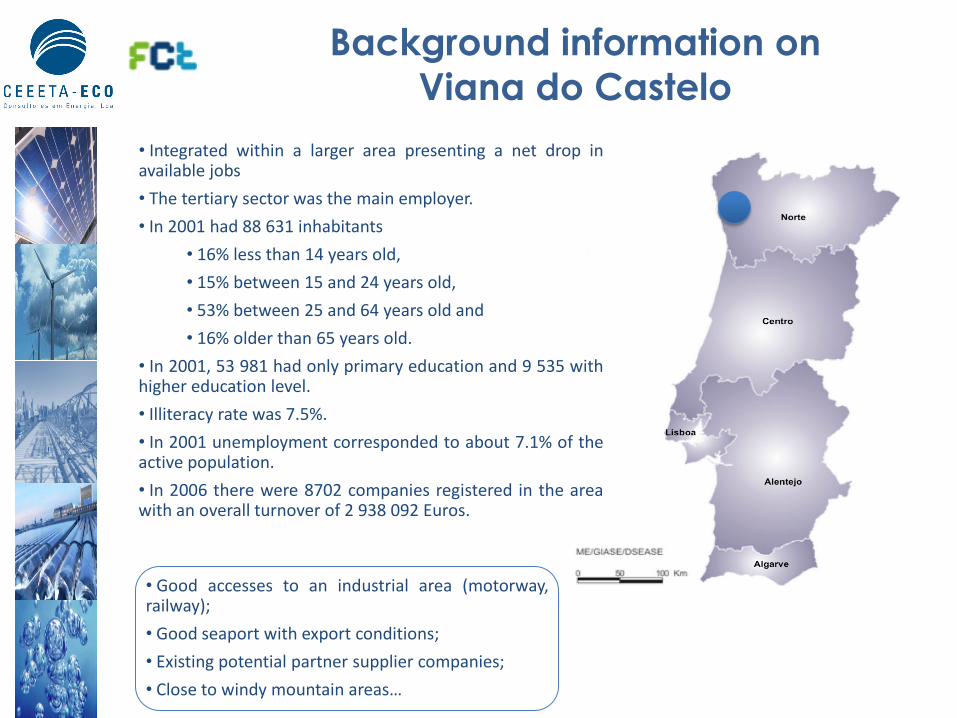

Background information on Viana do Castelo

• Integrated within a larger area presenting a net drop inavailable jobs

• The tertiary sector was the main employer.

• In 2001 had 88 631 inhabitants

• 16% less than 14 years old,

• 15% between 15 and 24 years old,

• 53% between 25 and 64 years old and

• 16% older than 65 years old.

• In 2001, 53 981 had only primary education and 9 535 withhigher education level.

• Illiteracy rate was 7.5%.

• In 2001 unemployment corresponded to about 7.1% of theactive population.

• In 2006 there were 8702 companies registered in the areawith an overall turnover of 2 938 092 Euros.

• Good accesses to an industrial area (motorway,railway);

• Good seaport with export conditions;

• Existing potential partner supplier companies;

• Close to windy mountain areas…

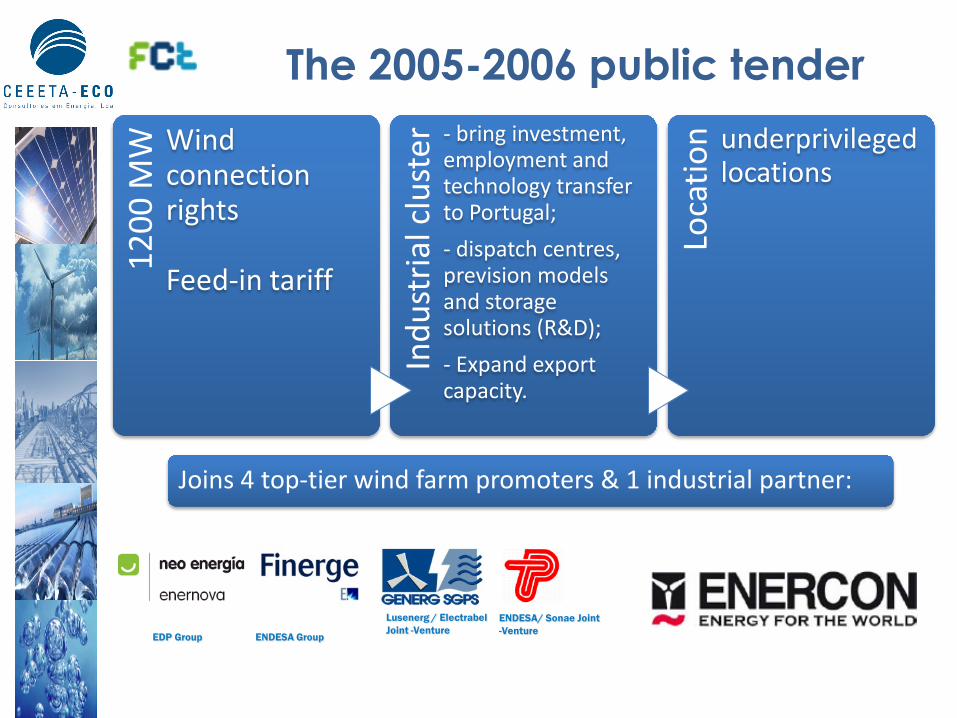

The 2005-2006 public tender12

00 M

W Wind connection rights

Feed-in tariff

Indu

stri

al c

lust

er - bring investment, employment and technology transfer to Portugal;

- dispatch centres, prevision models and storage solutions (R&D);

- Expand export capacity.

Loca

tion underprivileged

locations

Joins 4 top-tier wind farm promoters & 1 industrial partner:

EDP Group ENDESA Group

Lusenerg / Electrabel Joint -Venture

ENDESA/ Sonae Joint -Venture

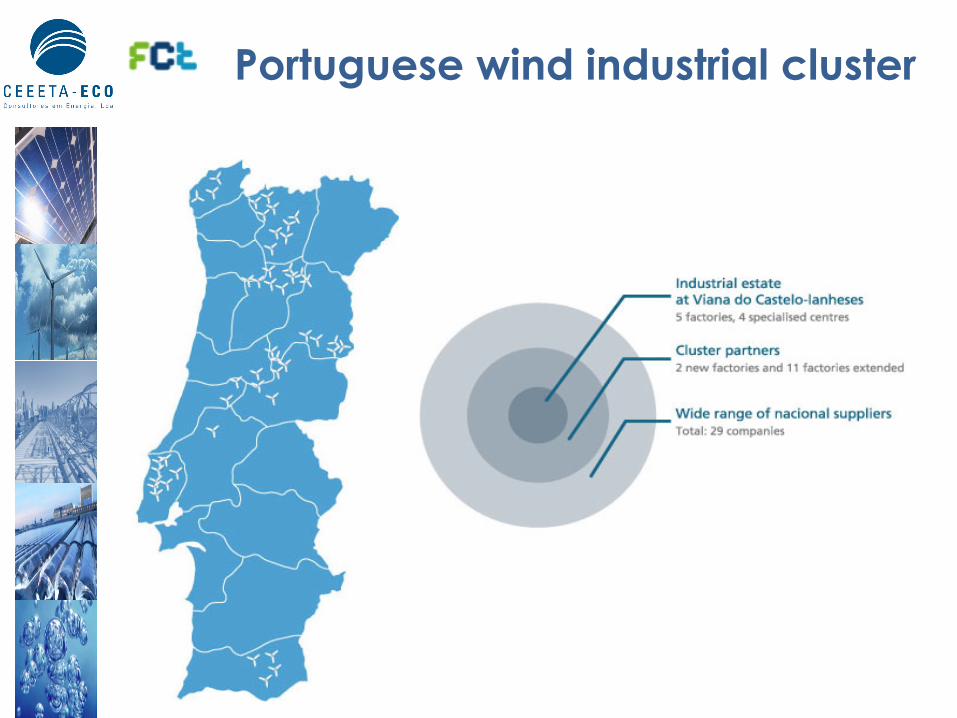

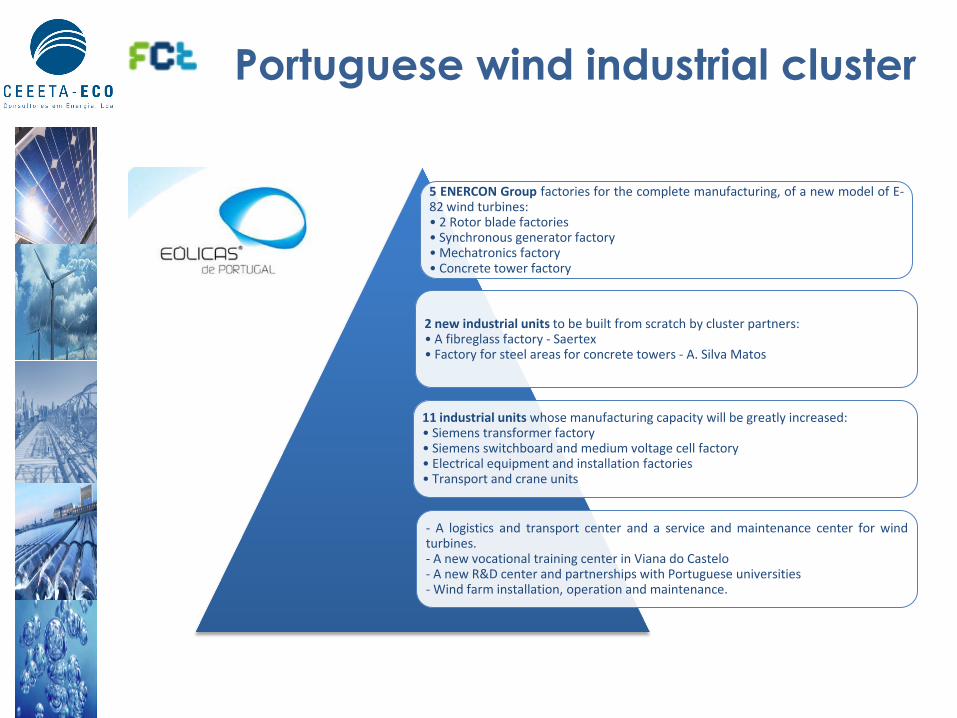

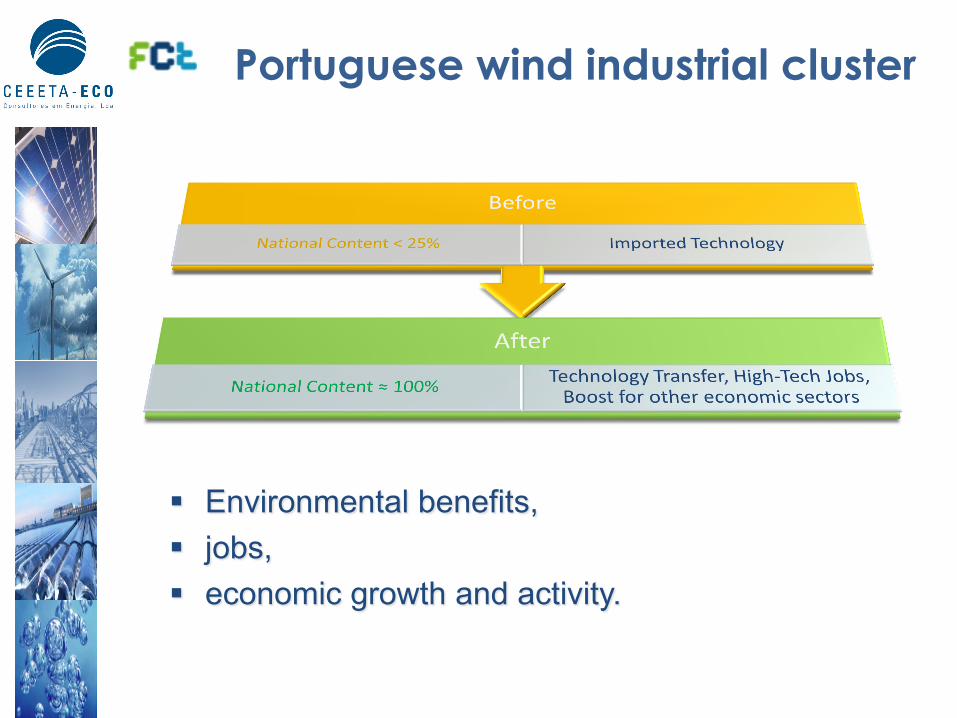

Portuguese wind industrial cluster

Portuguese wind industrial cluster

Portuguese wind industrial cluster

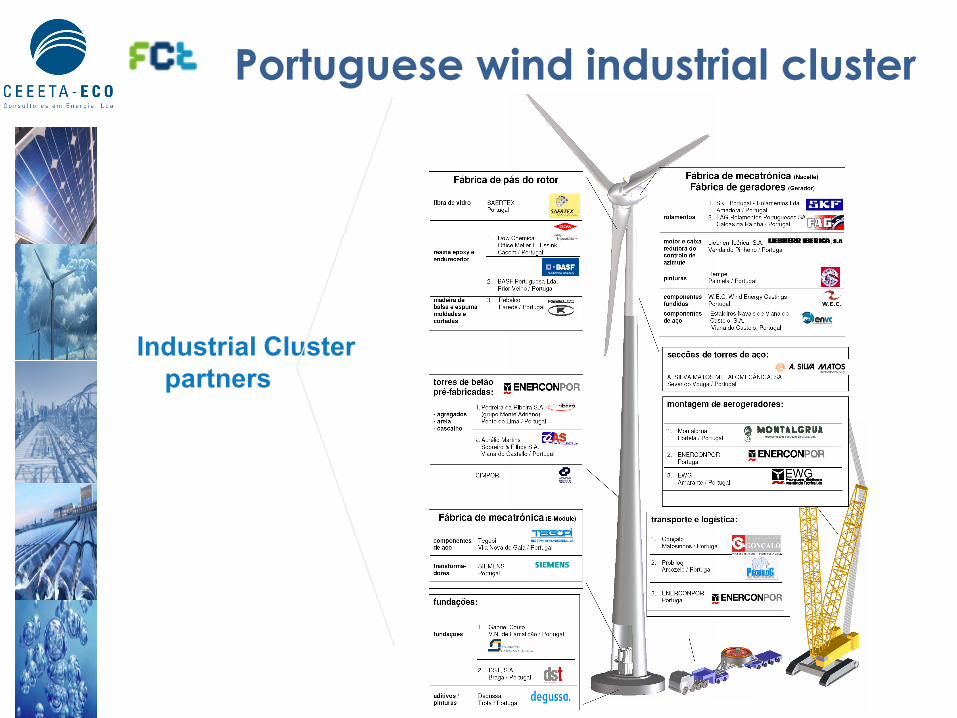

5 ENERCON Group factories for the complete manufacturing, of a new model of E-82 wind turbines:• 2 Rotor blade factories• Synchronous generator factory• Mechatronics factory• Concrete tower factory

2 new industrial units to be built from scratch by cluster partners:• A fibreglass factory - Saertex• Factory for steel areas for concrete towers - A. Silva Matos

11 industrial units whose manufacturing capacity will be greatly increased:• Siemens transformer factory• Siemens switchboard and medium voltage cell factory• Electrical equipment and installation factories• Transport and crane units

- A logistics and transport center and a service and maintenance center for windturbines.- A new vocational training center in Viana do Castelo- A new R&D center and partnerships with Portuguese universities- Wind farm installation, operation and maintenance.

Portuguese wind industrial cluster

Industrial Cluster partners

Portuguese wind industrial cluster

ENERCON Rotor Blades (1, 12, 13) – ENERCON Concrete Towers (5, 7, 9) – ENERCON Synchronous Generators (10) – SAERTEX Glass Fiber (11) – A. SILVA MATOS Steel Towers (3, 6, 15) – SIEMENS Transformers and Electrical Panels (8, 14) – JAYME DA COSTA Electrical Equipments (4)

Portuguese wind industrial cluster

1. Enercon Rotor Blades ready for export in the port of Viana do Castelo – 2 & 15. Special transport of Enercon E-82 blades (Transportes Laso) – 3. Building a power substation (Painhas) – 4 & 7. Installing electric lines (Painhas) – 5 & 8. Erecting the wind turbines (Montalgrua) – 6. Building the electric pylons (Painhas) – 9 & 12. Special transport of Enercon towers and nacelles ( Transportes Gonçalo)

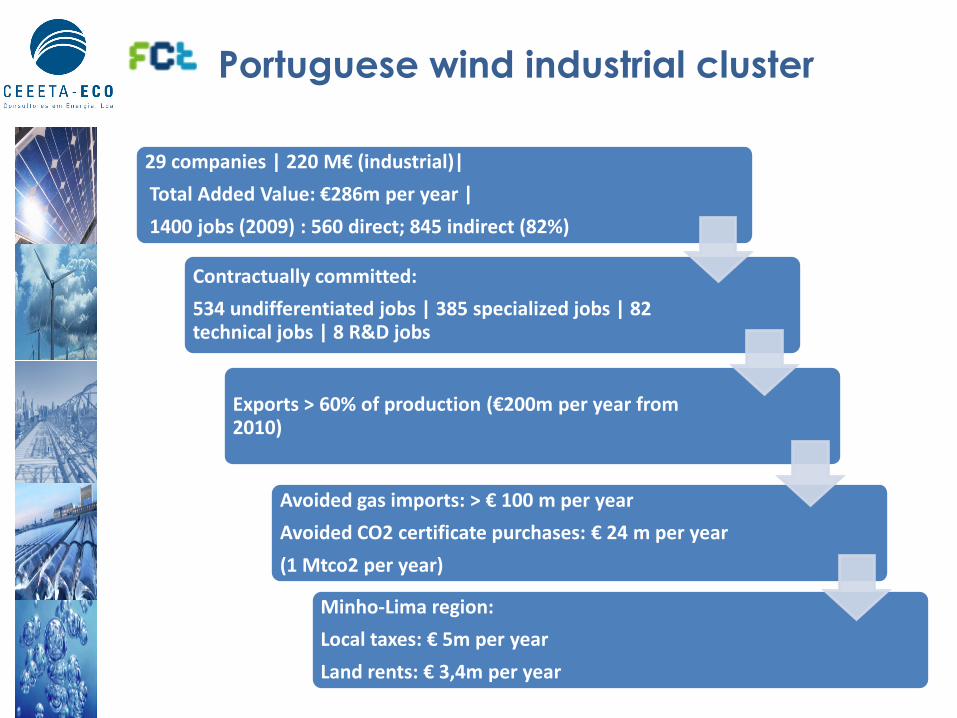

29 companies | 220 M€ (industrial)|

Total Added Value: €286m per year |

1400 jobs (2009) : 560 direct; 845 indirect (82%)

Contractually committed:

534 undifferentiated jobs | 385 specialized jobs | 82 technical jobs | 8 R&D jobs

Exports > 60% of production (€200m per year from 2010)

Avoided gas imports: > € 100 m per year

Avoided CO2 certificate purchases: € 24 m per year

(1 Mtco2 per year)

Minho-Lima region:

Local taxes: € 5m per year

Land rents: € 3,4m per year

Portuguese wind industrial cluster

Portuguese wind industrial cluster

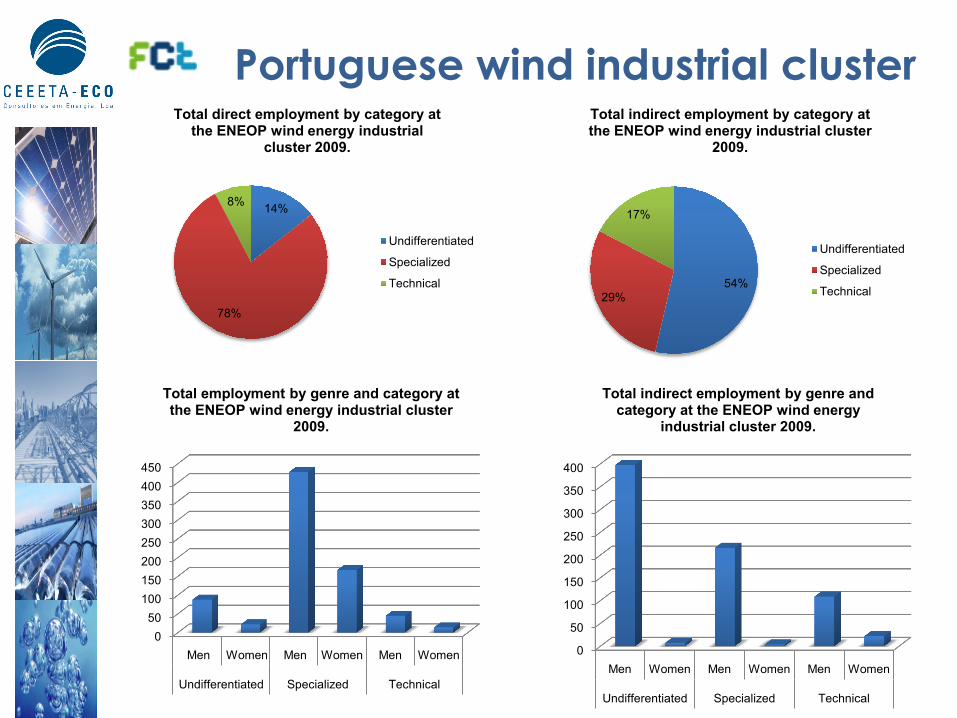

14%

78%

8%

Total direct employment by category at the ENEOP wind energy industrial

cluster 2009.

Undifferentiated

Specialized

Technical 54%29%

17%

Total indirect employment by category at the ENEOP wind energy industrial cluster

2009.

Undifferentiated

Specialized

Technical

050

100150200250300350400450

Men Women Men Women Men Women

Undifferentiated Specialized Technical

Total employment by genre and category at the ENEOP wind energy industrial cluster

2009.

0

50

100

150

200

250

300

350

400

Men Women Men Women Men Women

Undifferentiated Specialized Technical

Total indirect employment by genre and category at the ENEOP wind energy

industrial cluster 2009.

Portuguese wind industrial cluster

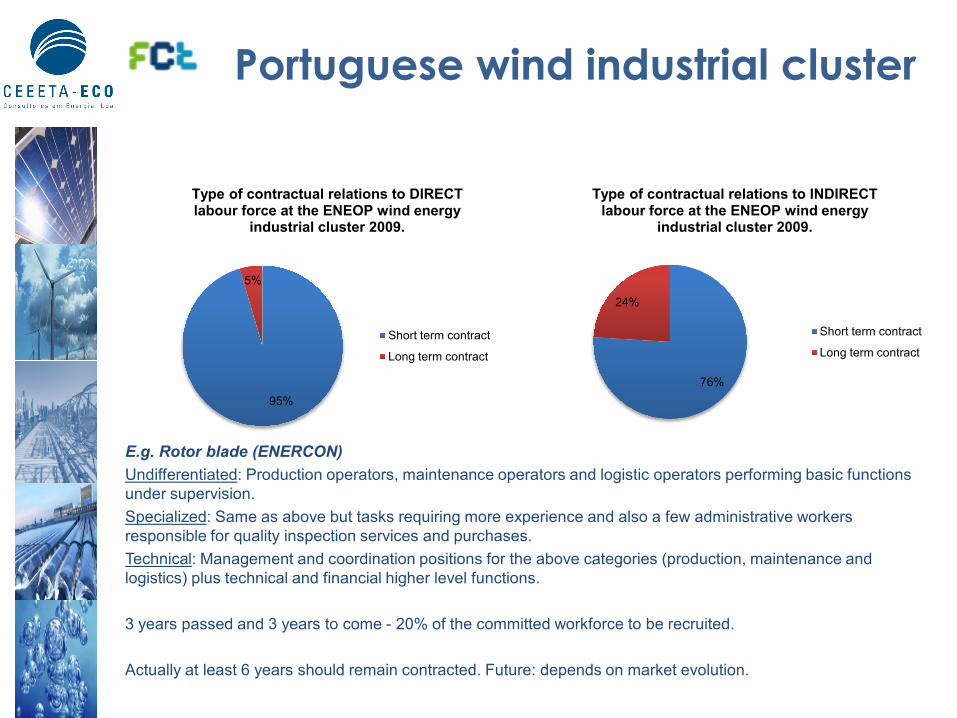

76%

24%

Type of contractual relations to INDIRECT labour force at the ENEOP wind energy

industrial cluster 2009.

Short term contract

Long term contract

95%

5%

Type of contractual relations to DIRECT labour force at the ENEOP wind energy

industrial cluster 2009.

Short term contract

Long term contract

E.g. Rotor blade (ENERCON)Undifferentiated: Production operators, maintenance operators and logistic operators performing basic functions under supervision.Specialized: Same as above but tasks requiring more experience and also a few administrative workers responsible for quality inspection services and purchases.Technical: Management and coordination positions for the above categories (production, maintenance and logistics) plus technical and financial higher level functions.

3 years passed and 3 years to come - 20% of the committed workforce to be recruited.

Actually at least 6 years should remain contracted. Future: depends on market evolution.

Portuguese wind industrial cluster

Environmental benefits, jobs, economic growth and activity.