Embed Size (px)

Citation preview

THE CASE OF SAUDI ARABIA

INTRODUCTION OF THE GROUP

Members of the group1) Majid Alfarsi (Actuarial Analyst, Ministry of Defense Pension

Fund, Oman)2) Jaser Aljaser (Specialist Actuary, Public Pension Agency, Saudi

Arabia)3) Abdullah Albahouth (Statistician Specialist, Public Pension

Agency, Saudi Arabia)4) Ghassan Alkhoja (Sr. operations officer, World Bank, Lebanon)5) Zaina Dawani (Iraq Pension Reform Project Coordinator, World

Bank, Lebanon)

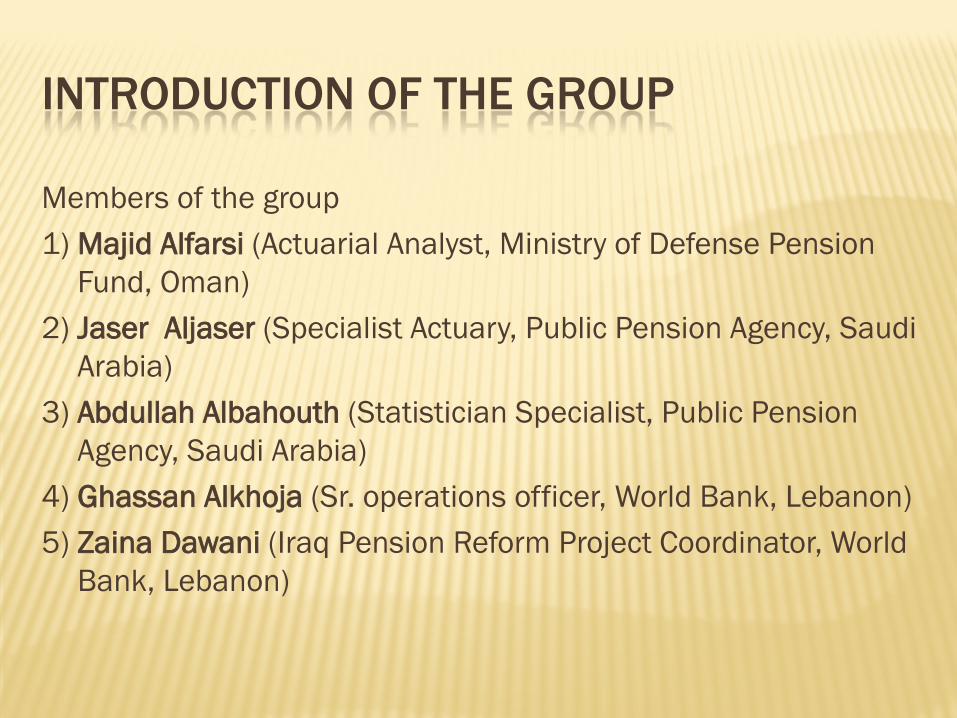

COUNTRY DEMOGRAPHIC AND ECONOMIC CHARACTERISTICS

Population growth rate among the population in 2004 and 2010 census 3,2 %

Population 2010 (people) 27,136,977GDP growth at constant prices 2009 0.6The contribution of the private sector in GDP at constant prices 2009 48%

Per capita GDP at current prices in 2009 (SAR) 52,853Growth rate of GDP per employed person (2008) 19.3The proportion of the working population to population (2009 m) 32.1

Rate and infant mortality (per thousand live births) 2009 14

FertilityThe population projection starts with a total fertility rate of 3.35 children per woman in 2005, decreasing gradually to 1.85 children per woman in 2050, remaining constant at 1.85 thereafter. The ratio of male births to female births is set at 1.03 for the whole projection period.

Mortalitylife expectancies at birth of 70.9 years for males and 75.3 years for females in 2005. These figures gradually increase to 79.4 years for males and 84.3 years for females in 2070.

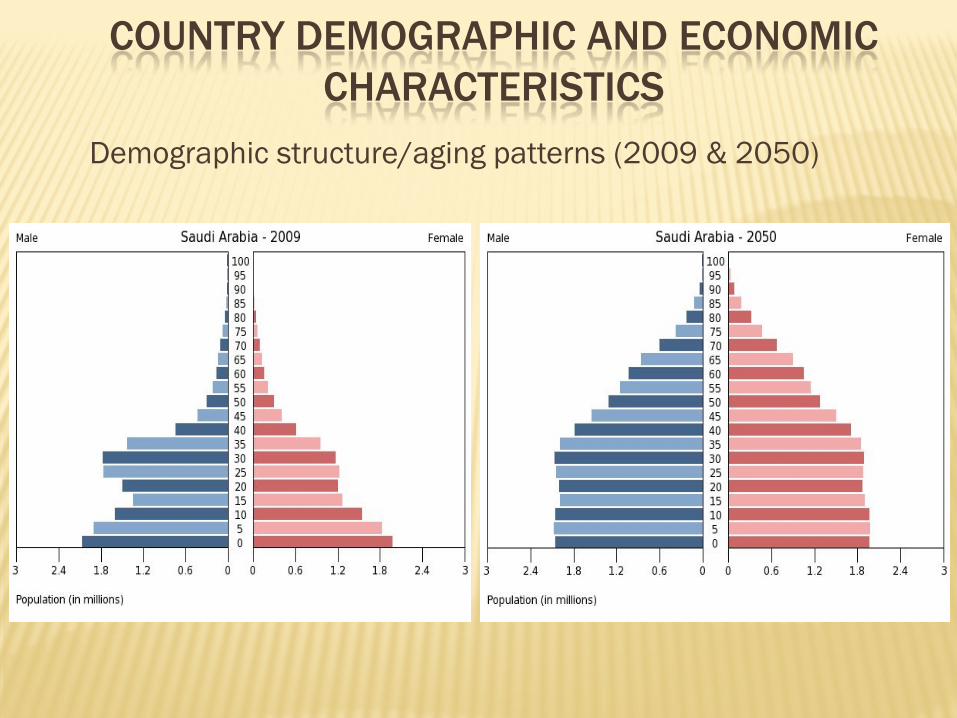

COUNTRY DEMOGRAPHIC AND ECONOMIC CHARACTERISTICS

Demographic structure/aging patterns (2009 & 2050)

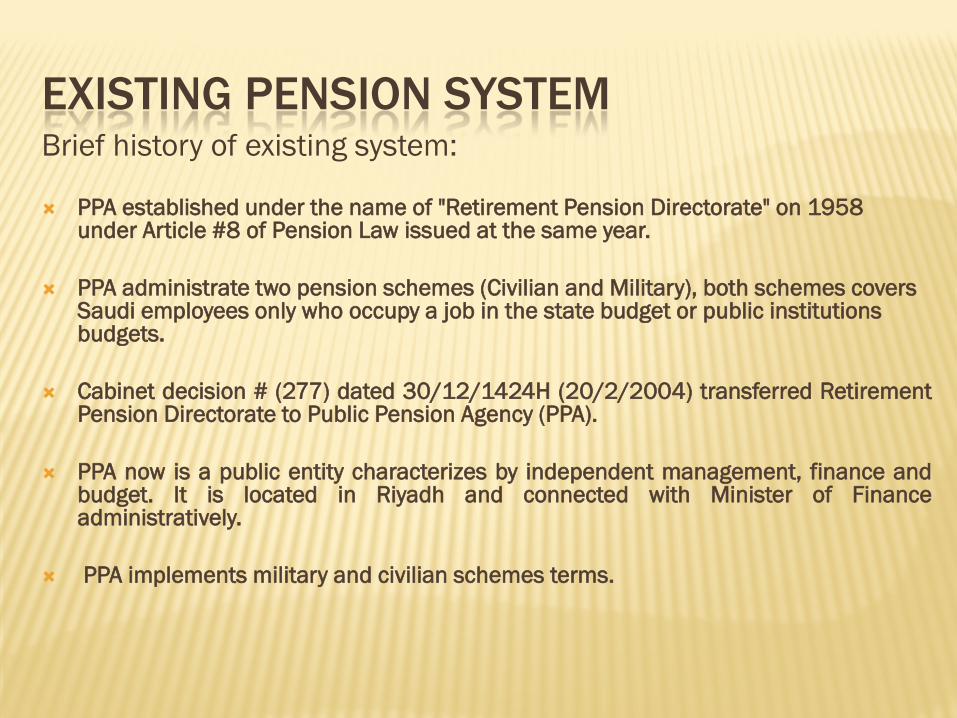

EXISTING PENSION SYSTEMBrief history of existing system:

PPA established under the name of "Retirement Pension Directorate" on 1958 under Article #8 of Pension Law issued at the same year.

PPA administrate two pension schemes (Civilian and Military), both schemes covers Saudi employees only who occupy a job in the state budget or public institutions budgets.

Cabinet decision # (277) dated 30/12/1424H (20/2/2004) transferred RetirementPension Directorate to Public Pension Agency (PPA).

PPA now is a public entity characterizes by independent management, finance andbudget. It is located in Riyadh and connected with Minister of Financeadministratively.

PPA implements military and civilian schemes terms.

EXISTING PENSION SYSTEM

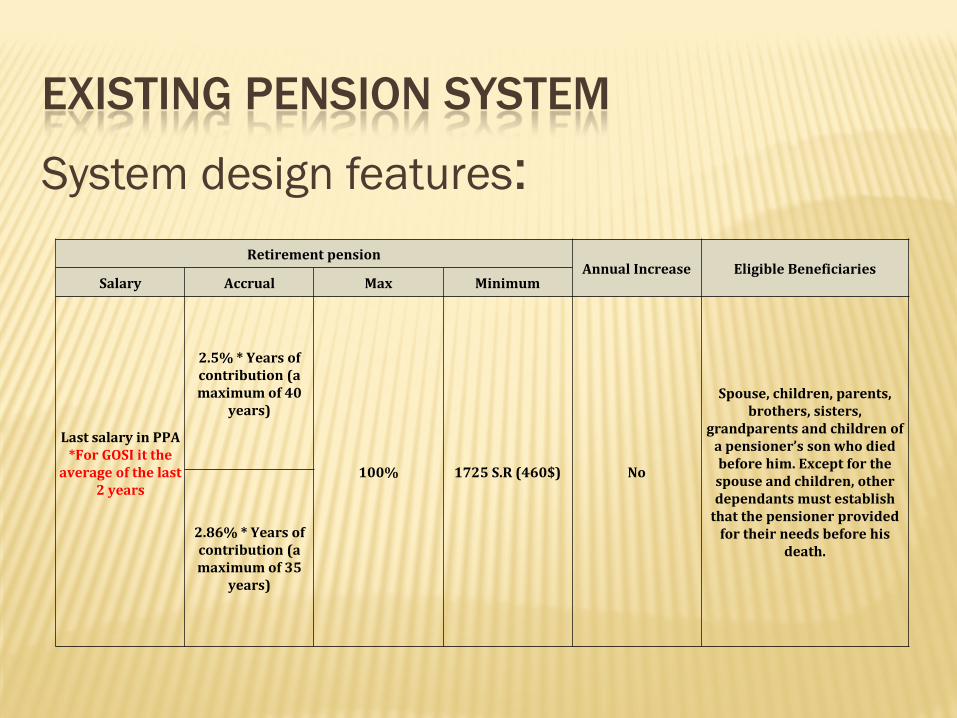

System design features:Retirement pension

Annual Increase Eligible Beneficiaries Salary Accrual Max Minimum

Last salary in PPA*For GOSI it the

average of the last 2 years

2.5% * Years of contribution (a maximum of 40

years)

100% 1725 S.R (460$) No

Spouse, children, parents, brothers, sisters,

grandparents and children of a pensioner’s son who died before him. Except for the spouse and children, other dependants must establish

that the pensioner provided for their needs before his

death. 2.86% * Years of contribution (a maximum of 35

years)

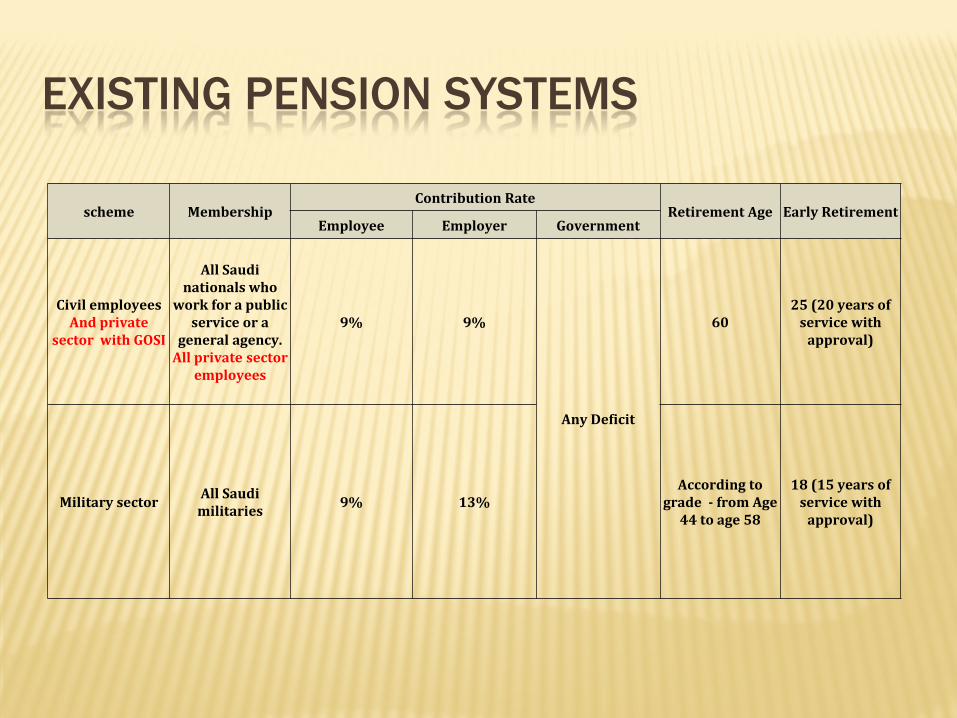

EXISTING PENSION SYSTEMS

scheme MembershipContribution Rate

Retirement Age Early RetirementEmployee Employer Government

Civil employeesAnd private

sector with GOSI

All Saudi nationals who

work for a public service or a

general agency.All private sector

employees

9% 9%

Any Deficit

6025 (20 years of

service with approval)

Military sector All Saudi militaries 9% 13%

According to grade - from Age

44 to age 58

18 (15 years of service with

approval)

EXISTING PENSION SYSTEM

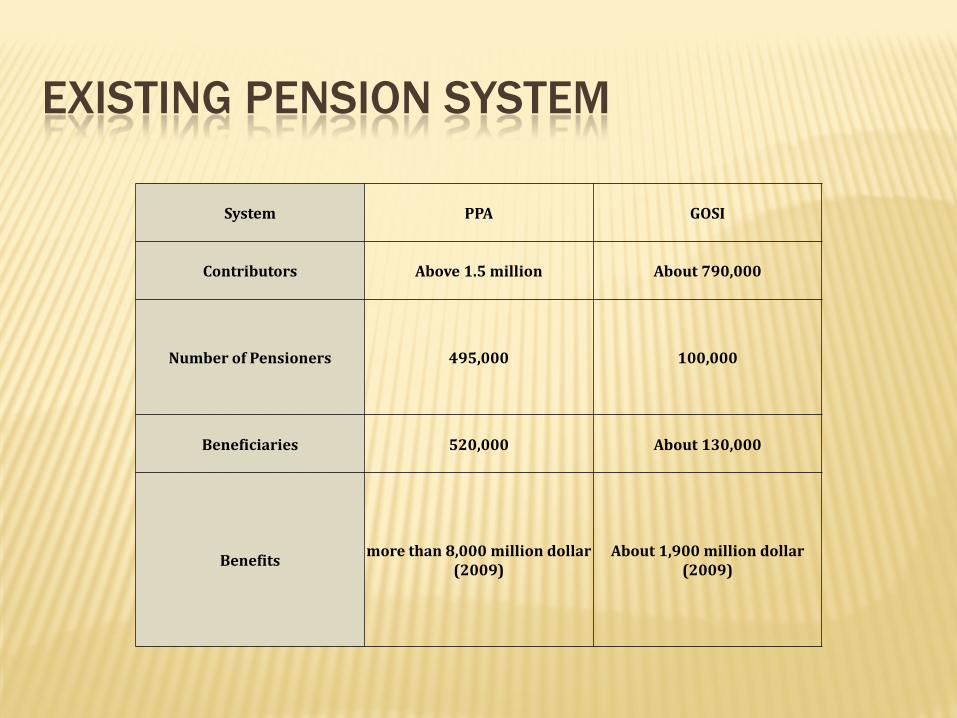

System PPA GOSI

Contributors Above 1.5 million About 790,000

Number of Pensioners 495,000 100,000

Beneficiaries 520,000 About 130,000

Benefits more than 8,000 million dollar (2009)

About 1,900 million dollar (2009)

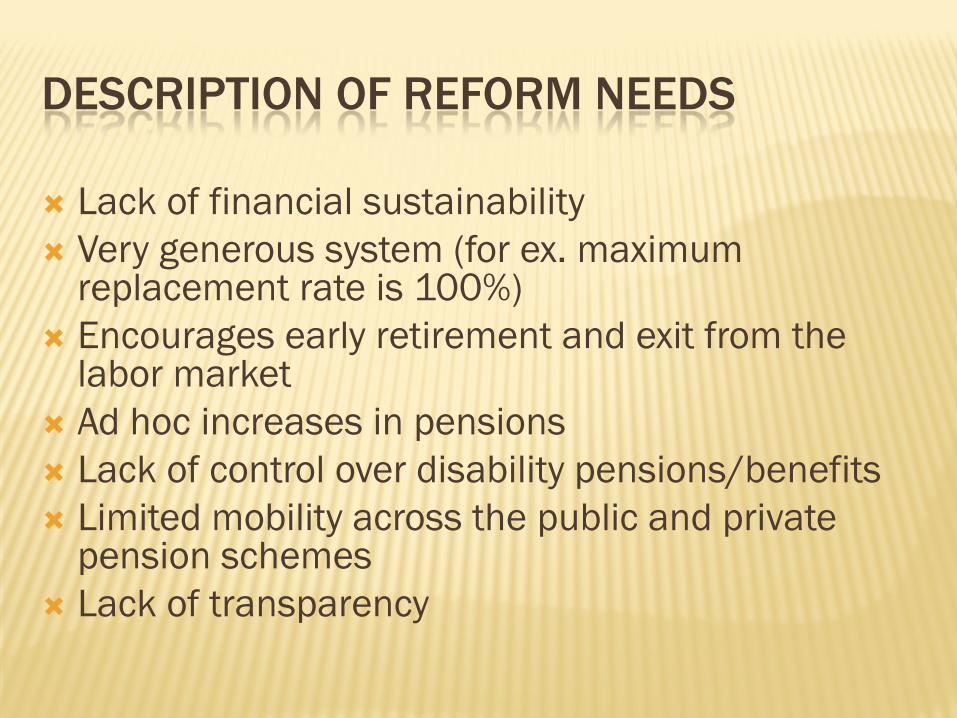

DESCRIPTION OF REFORM NEEDS

Lack of financial sustainability Very generous system (for ex. maximum

replacement rate is 100%) Encourages early retirement and exit from the

labor market Ad hoc increases in pensions Lack of control over disability pensions/benefits Limited mobility across the public and private

pension schemes Lack of transparency

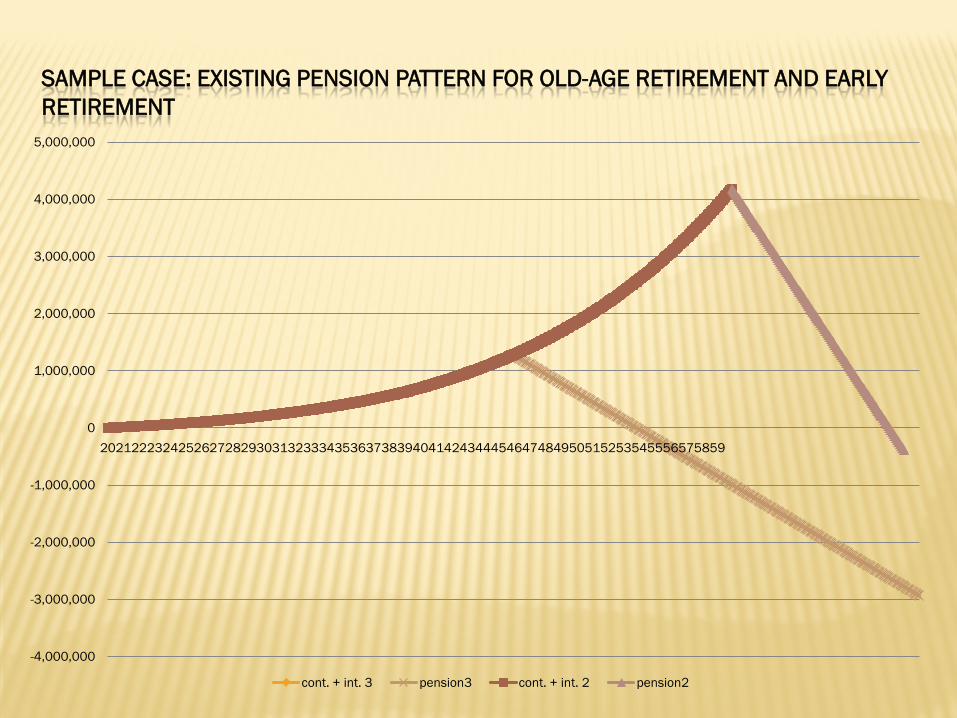

SAMPLE CASE: EXISTING PENSION PATTERN FOR OLD-AGE RETIREMENT AND EARLY RETIREMENT

-4,000,000

-3,000,000

-2,000,000

-1,000,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

20212223242526272829303132333435363738394041424344454647484950515253545556575859

cont. + int. 3 pension3 cont. + int. 2 pension2

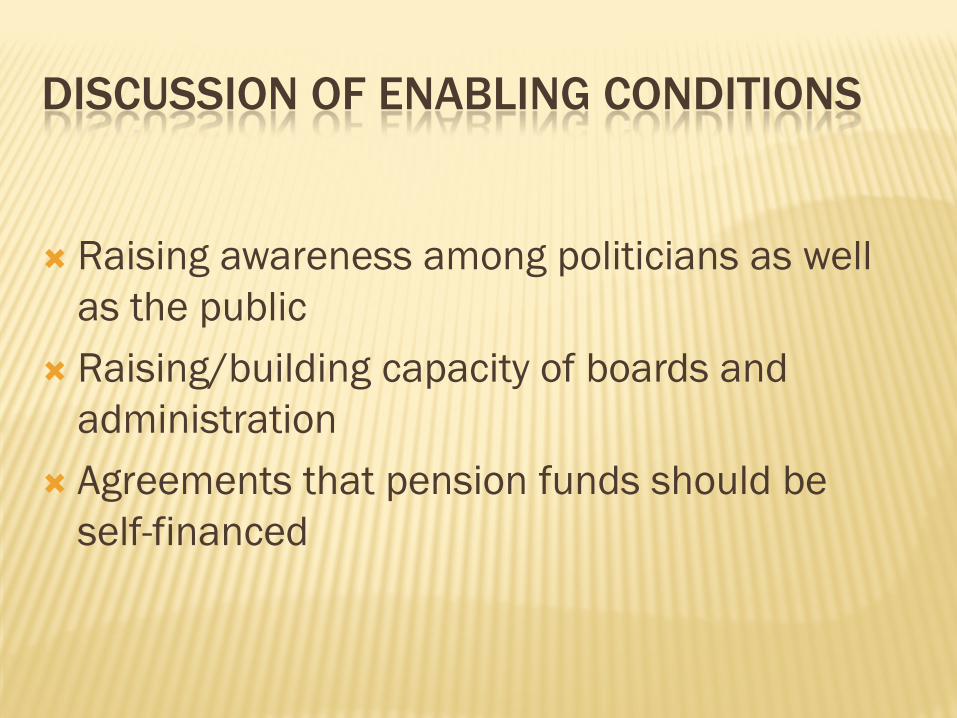

DISCUSSION OF ENABLING CONDITIONS

Raising awareness among politicians as well as the public

Raising/building capacity of boards and administration

Agreements that pension funds should be self-financed

DISCUSSION OF REFORM OPTIONS

Parametric reform to include: Gradual increase of retirement age Gradual increase of vesting periods Introducing penalties for early retirement Exponential accrual rate Change of reference wage Strengthening means of verification with

respect to disability pension

TECHNICAL FEASIBILITY OF REFORM OPTIONS

Too early to assess the technical feasibility, but the following steps are proposed for conducting a feasibility assessment:

To focus on awareness raising using simplified models which can demonstrate the lack of sustainability of the existing system

To develop several reform options with the assistance of actuarial analysis/advisors

More transparency would be needed on implicit pension liabilities

PROPOSED COALITION/CONSENSUS BUILDING STRATEGY

Starting with the Boards and administration (staff)

MoF and other concerned ministries Consultative councils (Parliament) Press and media International organizations

COMMUNICATION/PUBLIC INFORMATION STRATEGY

Emphasizing the importance of work in economic, social and religious terms

Innovative ways to focus on/reach the new beneficiary groups of the reform

Tailoring messages to different target groups Utilize the press/media for conveying

messages

THANK YOU