Embed Size (px)

Citation preview

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 1

The Chamber of Tax Consultants

Case studies Analysis – Domestic Transfer Pricing

30 March 2013

Sanjay Kapadia

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 2

Agenda

• Analysis on case studies – Domestic Transfer Pricing Regulations

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 3

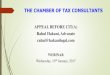

Case Study 1 : Applicability of Domestic TP to transactions between non-residents

FCo

Mr. X Director of FCO

PE in India

Outside India

India Salary paid in India

Salary paid outside India

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 4

Case Study 1 : Applicability of Domestic TP to transactions between non-residents

Analysis: Salary paid to Mr. X is not an Int Tr. in terms of s. 92B r.w.s. 92A since Mr. X is not an AE of

FCO as defined under s. 92A.

Mr. X is a director of FCO and hence covered as a related party under s. 40A(2)(b)(ii)

Since PE is liable to tax in India on net basis, it can claim deduction for salary paid to Mr. X for services rendered in India for the PE.

Since Mr. X renders services in India, the salary cost does not constitute ‘HO expenditure’ in terms of s. 44C and full deduction is available in respect thereof.

Since payment is made to related party covered by s. 40A(2)(b), the transaction constitutes SDT in terms of s. 92BA(i) if aggregate value of all transactions of PE referred under s. 92BA exceeds Rs. 5 Cr.

Being SDT, salary payment to Mr. X will be liable to Domestic TP and PE will be required to benchmark it to ALP, maintain documentation and furnish TP audit report. Incidentally, if PE is subject to tax audit, books of account will be required to be maintained.

The fact that both FCO and Mr. X are non-residents is not relevant. All in all SDT can overreach transactions with / between NR/s.

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 5

Case Study 2 - Applicability of TP for royalty paid by Indian and foreign subsidiaries to Indian parent

Sub 2 LtdSub 1 Ltd Sb 3 Ltd

Hold Co Ltd

Owns brand ‘XYZ’

Outside India India

Royalty paid(>5 Cr)

Royalty paid(>5 Cr)

Royalty paid(>5 Cr)

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 6

Case Study 2 - Applicability of TP for royalty paid by Indian and foreign subsidiaries to Indian parent

AnalysisApplicability of Domestic TP for Hold Co Hold Co receives royalty from its subsidiaries. It is not eligible for any profit linked tax

holiday.

Though subsidiaries are related parties covered under s 40A(2)(b)(vi), the royalty income received from subsidiaries is not covered by provisions of Domestic TP.

S.92BA(i) merely covers payments made to related parties under s. 40A(2)(b) and not incomes received from related parties.

Hence Hold Co is not liable for Domestic TP in respect of royalty income from domestic subsidiary.

However Sub 1 is an AE for Hold Co. Royalty income from Sub 1, therefore, constitutes IntTr. for Hold Co and it is required to benchmark royalty received from Sub 1 to ALP, maintain documentation and furnish TP audit report.

Applicability of Domestic TP to Sub 1 Sub 1 has no presence in India and is not liable to tax in India.

Hence S. 40A(2)(b) and Domestic TP provisions are not applicable to Sub 1.

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 7

Case Study 2 - Applicability of TP for royalty paid by Indian and foreign subsidiaries to Indian parentAnalysisApplicability of Domestic TP to Sub 2 and Sub 3 Hold Co is a related party for Sub 2 and Sub 3 covered under s 40A(2)(b)(iv).

The value of royalty paid by Sub 2 does not exceed Rs. 5 Cr.

Hence, though royalty paid by Sub 2 is covered by S. 40A(2)(b), it does not constitute SDT for Sub 2, if it is assumed that sub.2 did not have any other transaction covered by S. 92BA.

The value of royalty paid by Sub 3 exceeds Rs. 5 Cr. Hence, royalty paid by Sub 3 constitutes SDT and Sub 3 is liable for Domestic TP.

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 8

Case Study 3 - Applicability of Domestic TP to intra-group loans

A2 LtdA1 Ltd

Interest paid @ 18% (ALP 11%)

Loan given

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 9

Case Study 3 - Applicability of Domestic TP to intra-group loansAnalysis:For A1 Ltd Receipt of interest from related party under s 40A(2)(b) does not constitute SDT and hence

A1 Ltd is not liable to Domestic TP.

Even assuming ALP adjustment is made in hands of A2 Ltd to disallow interest in excess of ALP i.e. 7% (18% - 11%), there will be no correlative adjustment in hands of A1 Ltd.

For A2 Ltd Payment of interest to related party under s 40A(2)(b) constitutes SDT and hence A2 Ltd will

be liable to Domestic TP.

A2 Ltd can make voluntary TP adjustment by disallowing excess interest of 7% while filing its return.

If A2 Ltd does not voluntarily disallow the excess interest, the Tax Authority can, having regard to the facts, make TP adjustment to disallow excess interest of 7%.

In such a case, A2 Ltd will be exposed to penalty under s 271(1)(c) in respect of addition to income by way of TP adjustment.

A2 Ltd "may" also be exposed to penalty under s 271G if it has defaulted on maintenance of TP documentation and/or under s 271BA if it has defaulted on furnishing of TP audit report.

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 10

Case Study 4 - Applicability of Domestic TP to intra-group interest-free loans

A2 LtdA1 Ltd

No InterestPaid (ALP 11%)

Loan given

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 11

Case Study 4 - Applicability of Domestic TP to intra-group interest-free loansAnalysis:For A1 Ltd Presently, income transactions from related parties under s 40A(2)(b) are not covered under

s 92BA as SDT.

Hence A1 Ltd is not liable to Domestic TP. In other words, no notional interest income can be imputed in hands of A1 Ltd on the basis of ALP rate of or on any other basis.

However, if A1 Ltd has used interest bearing borrowed funds to give interest free loan to A2 Ltd, issue of disallowance of corresponding interest expenditure "may" arise in hands of A1 Ltd.

For A2 Ltd Since no interest is paid by A2 Ltd, provisions of S. 40A(2)(b) r.w.s. 92BA are not applicable.

Hence A2 Ltd is also not liable for Domestic TP.

The TP provisions do not permit adjustment favourable to the taxpayer. Hence no notional interest expenditure in the hands of A2 Ltd can be imputed in this case.

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 12

Case Study 5 - Applicability of Domestic TP to intra-group interest-free loans used for profit linked tax holiday qualifying unit

A2 LtdA1 LtdInterest free loan

Profit linked tax holiday qualifying

unit

Loan used

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 13

Analysis:For A1 Ltd Presently, income transactions from related parties under s 40A(2)(b) are not covered under

s 92BA as SDT.

Hence A1 Ltd is not liable to Domestic TP. In other words, no notional interest income can be imputed in hands of A1 Ltd on the basis of ALP rate of or on any other basis.

However, if A1 Ltd has used interest bearing borrowed funds to give interest free loan to A2 Ltd, issue of disallowance of corresponding interest expenditure "may" arise in hands of A1 Ltd.

For A2 Ltd If it can be established that the motivating reason for provision of interest free loan by

A1 Ltd to A2 Ltd was to enable A2 Ltd to earn more than ordinary profits, the Tax Authority may invoke provisions of s.10AA(9) r.w.s. 80-IA(10) r.w.s. 92BA(v) to deny deduction under s 10AA.

If such be the case, It is possible for A2 Ltd to avoid adverse consequences of TP adjustment by making voluntary TP adjustment in its return

Case Study 5 - Applicability of Domestic TP to intra-group interest-free loans used for profit linked tax holiday qualifying unit

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 14

Case study 6 - Eligible business

AB Ltd.

SEZ unit Non SEZ unit

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 15

Approach suggested

Determine whether the SEZ unit and non-SEZ unit businesses should be regarded as separate businesses

Evaluate whether there is transfer of goods/ services by non-SEZ unit to SEZ unit

Evaluate whether common cost allocation is required under general principles or under SDT provisions and manner in which allocation is to be made

Undertake functional analysis to determine appropriate characterization of the relationship between SEZ unit and non-SEZ unit

Undertake economic analysis to determine appropriate arm’s length approach for pricing the transactions

Consider opportunities to optimize tax holiday benefits

Consider approach to compliance/ disclosure

Case study 6 - Eligible business

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 16

Case study 7 - Eligible business

AB Ltd.

Unit claiming

80-IE

Ineligible unit 2

Ineligible unit 1

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 17

Approach suggested

Evaluate whether allocation of interest to 80-IE unit required under general principles for determining tax holiday or in view of SDT provisions and the manner in which the allocation is to be made.

Determine whether the transaction relating to inter unit temporary use of funds could be regarded as provision of services by ineligible business to an eligible business

If so, evaluate the approach for determining arm’s length charge for the service

Consider approach to compliance/ documentation

Case study 7 - Eligible business

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 18

Owner of IP

Case study 8 - Eligible business/Section 40A(2)

HC Ltd.

S1 Ltd. Ineligible

S3 Ltd.Ineligible

S2 Ltd. Eligible

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 19

Approach suggested

Undertake bench-marking exercise to identify comparable uncontrolled royalty transactions. In the absence of such data, evaluate application of other methods for establishing arm’s length royalty rate

Evaluate whether not charging arm’s length royalty to S2 could be subjected to provisions of 80-IA(10) and assess whether economic analysis could support not charging royalty having regard to facts and circumstances.

Consider approach to compliance/ documentation

Case study 8 - Eligible business/Section 40A(2)

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 20

Eligible business – Case study 9

IC Ltd.

Unit1 – RMIneligible

HOIneligible

Unit2 – FGEligible

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 21

Approach suggested

Evaluate whether allocation of HO costs required under general principles for determining tax holiday or in view of SDT provisions and the manner in which the allocation is to be made.

Undertaking functional analysis to allocate functions/ assets/ risks between unit 1 and unit 2 and whether HO should be treated as a separate business for purpose of SDT

Determine appropriate characterization of units for application of arm’s length principle for inter-unit transfer of goods.

Undertake a search for comparable data for determining pricing for inter-unit transfer

Consider opportunities to optimize tax holiday eligibility

Consider approach to compliance/ documentation

Case study 9 - Eligible business

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 22

Case study 10 - Eligible business and Section 40A(2)

MNC Inc.

M Ltd. Eligible

D Ltd.Ineligible

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 23

Approach suggested

Undertake functional analysis to determine the appropriate characterization of the entities/ transactions

Evaluate whether arm’s length testing at one of the entities could be relied upon for establishing arm’s length price for sale by M Ltd and purchase by D Ltd and if so testing for which of the entities is more appropriate.

Determine application of most appropriate TP method to test arm’s length pricing

If necessary, evaluate and document the factors which justify the profits earned by M Ltd to demonstrate that the same is not on account of an arrangement between M Ltd and D Ltd

Consider opportunities to optimize tax holiday eligibility

Consider approach to compliance/ documentation

Case study 10 - Eligible business and Section 40A(2)

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 24

Questions ??

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 25

Contact Details

Sanjay KapadiaPartner, Transfer Pricing,Ernst & Young Private Limited,MumbaiPh No: +91 9892400222E-mail – [email protected]

Case studies – Domestic Transfer Pricing Presenter : Sanjay KapadiaPage 26

All the views expressed during the presentation are personal opinions of the presenter and the presenter is not liable for any consequences arising out of reliance on the same