Embed Size (px)

Citation preview

The changing claims

environment

Tim AndrewsFinity Consulting

18-20 May 2016

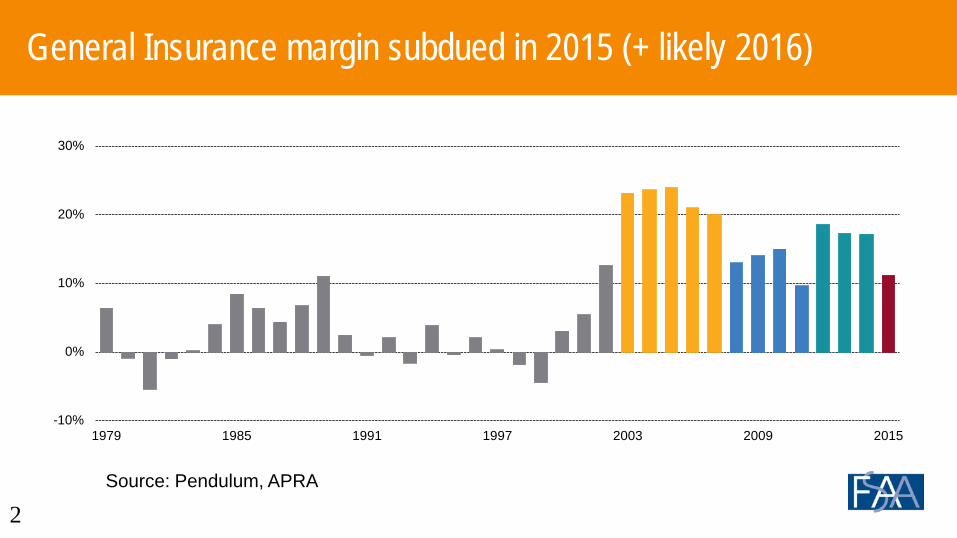

General Insurance margin subdued in 2015 (+ likely 2016)

2

-10%

0%

10%

20%

30%

1979 1985 1991 1997 2003 2009 2015

Source: Pendulum, APRA

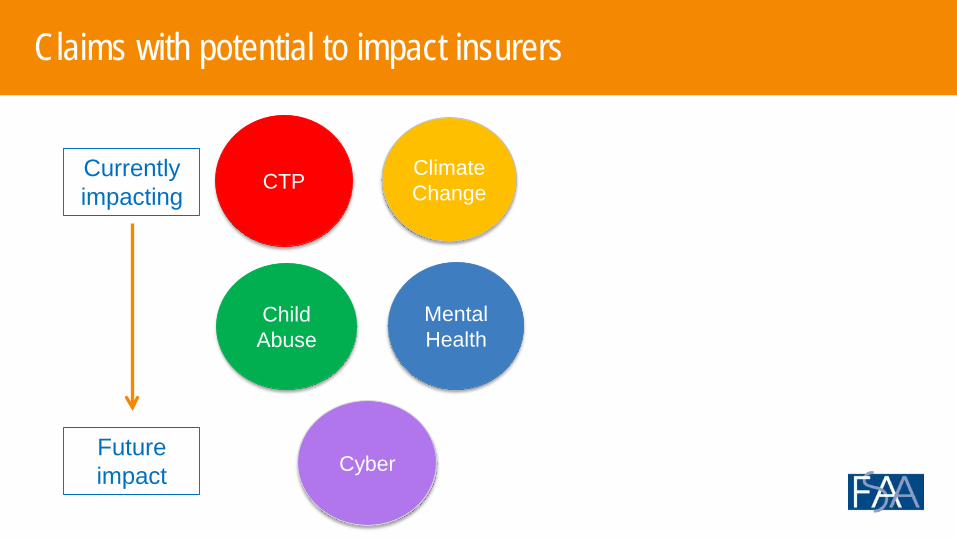

Claims with potential to impact insurers

ClimateChange

Child Abuse

Mental Health

CTP

Cyber

Currently impacting

Future impact

Claims with potential to impact insurers

Natural Perils

Child Abuse

Mental Health

CTP

Cyber

Currently impacting

Future impact

CTP

0%

10%

20%

30%

40%

50%

60%

70%

80%

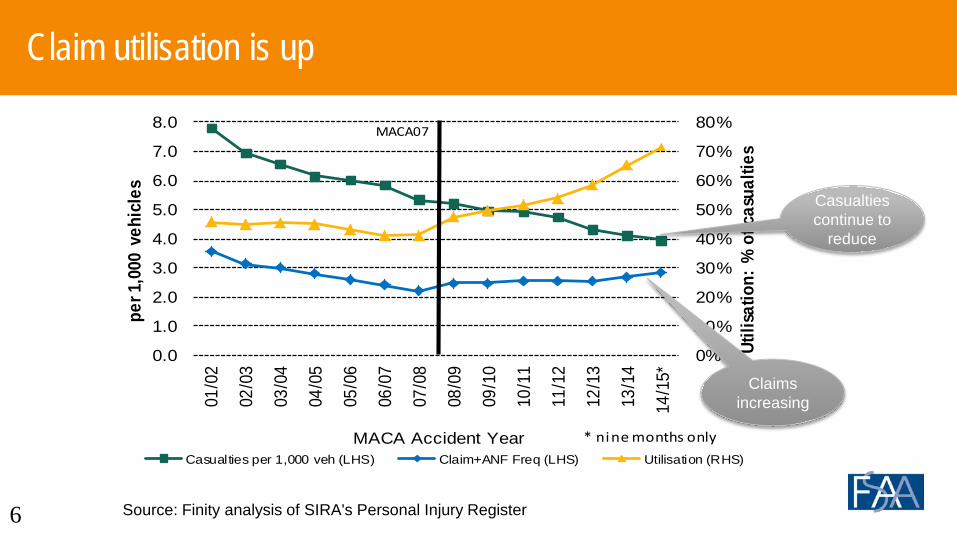

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

01/0

2

02/0

3

03/0

4

04/0

5

05/0

6

06/0

7

07/0

8

08/0

9

09/1

0

10/1

1

11/1

2

12/1

3

13/1

4

14/1

5*

Utili

satio

n: %

of c

asua

lties

per 1

,000

veh

icle

s

MACA Accident YearCasualties per 1,000 veh (LHS) Claim+ANF Freq (LHS) Utilisation (RHS)

MACA07

* nine months only

Casualties continue to

reduce

Claims increasing

Claim utilisation is up

6 Source: Finity analysis of SIRA's Personal Injury Register

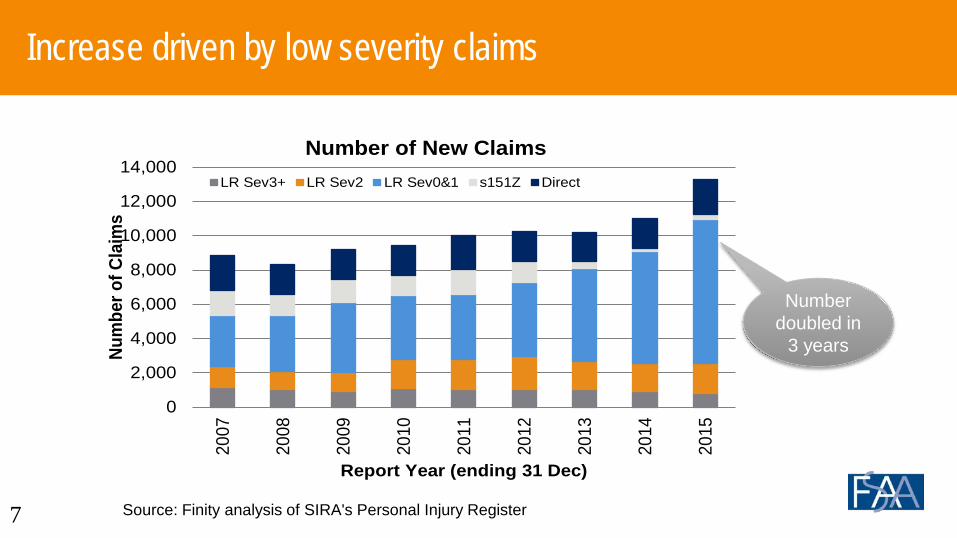

Increase driven by low severity claims

7

Number doubled in

3 years

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2007

2008

2009

2010

2011

2012

2013

2014

2015

Num

ber o

f Cla

ims

Report Year (ending 31 Dec)

Number of New ClaimsLR Sev3+ LR Sev2 LR Sev0&1 s151Z Direct

Source: Finity analysis of SIRA's Personal Injury Register

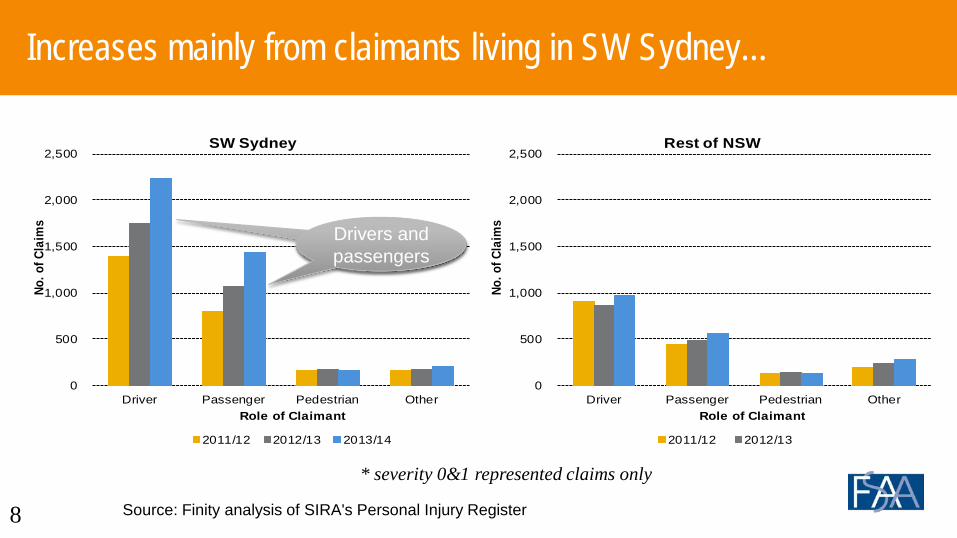

Increases mainly from claimants living in SW Sydney…

8

0

500

1,000

1,500

2,000

2,500

Driver Passenger Pedestrian Other

No. o

f Cla

ims

Role of Claimant

Rest of NSW

2011/12 2012/13

0

500

1,000

1,500

2,000

2,500

Driver Passenger Pedestrian Other

No. o

f Cla

ims

Role of Claimant

SW Sydney

2011/12 2012/13 2013/14

* severity 0&1 represented claims only

Drivers and passengers

Drivers and passengers

Source: Finity analysis of SIRA's Personal Injury Register

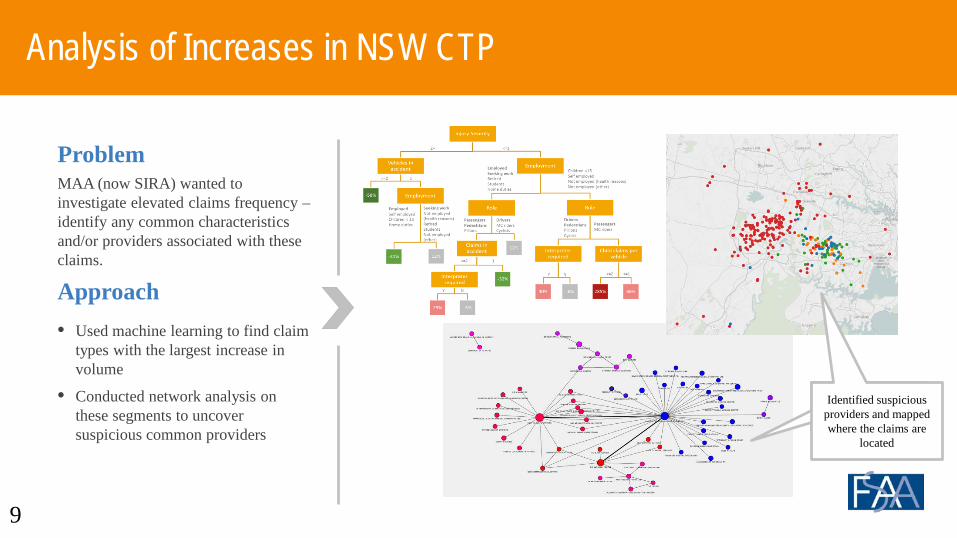

Analysis of Increases in NSW CTP

9

ProblemMAA (now SIRA) wanted to investigate elevated claims frequency –identify any common characteristics and/or providers associated with these claims.

• Used machine learning to find claim types with the largest increase in volume

• Conducted network analysis on these segments to uncover suspicious common providers

Approach

Identified suspicious providers

Identified suspicious providers and mapped where the claims are

located

10

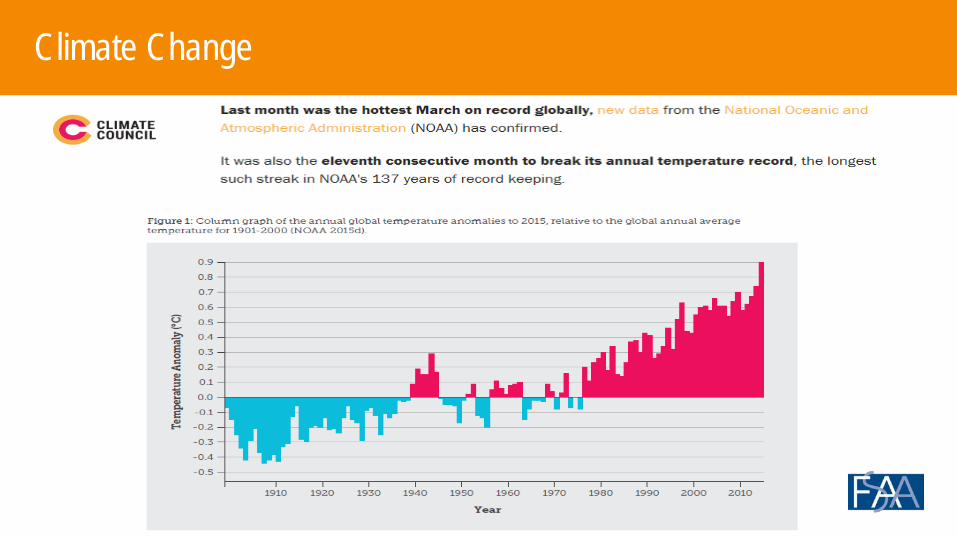

Climate Change

What chance?

Climate Change

Climate Change

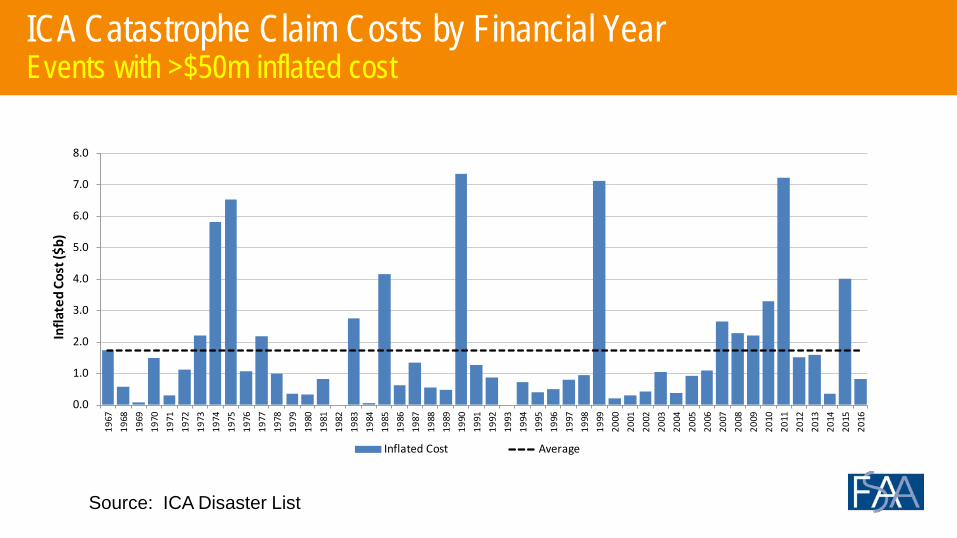

ICA Catastrophe Claim Costs by Financial YearEvents with >$50m inflated cost

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Infla

ted

Cost

($b)

Inflated Cost Average

Source: ICA Disaster List

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Infla

ted

Cost

($b)

Capped Incurred Average

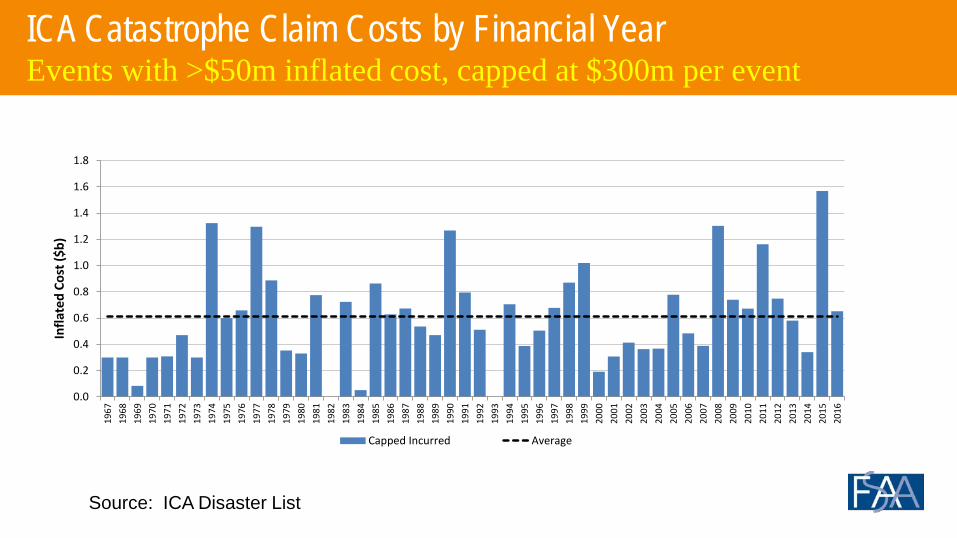

ICA Catastrophe Claim Costs by Financial YearEvents with >$50m inflated cost, capped at $300m per event

Source: ICA Disaster List

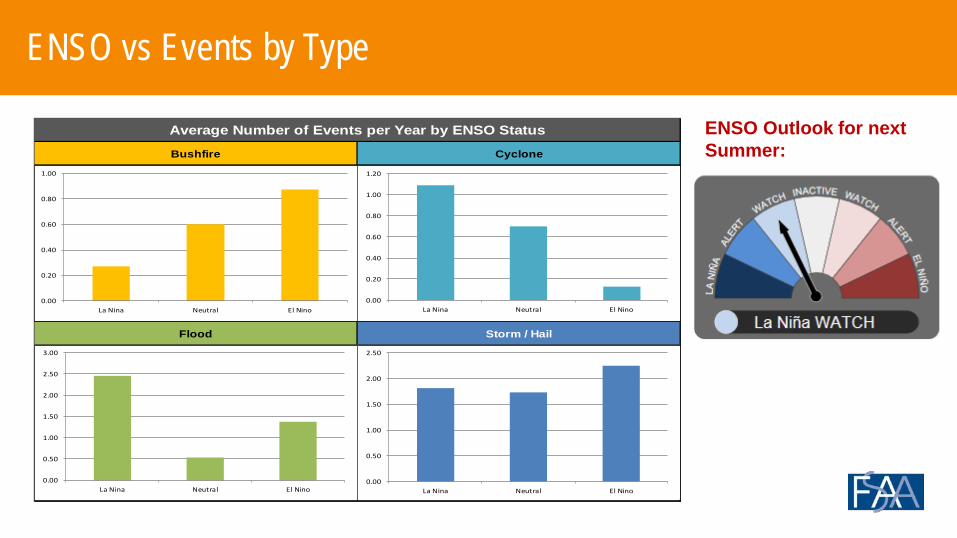

ENSO vs Events by Type

Bushfire Cyclone

Flood Storm / Hail

Average Number of Events per Year by ENSO Status

0.00

0.20

0.40

0.60

0.80

1.00

La Nina Neutral El Nino0.00

0.20

0.40

0.60

0.80

1.00

1.20

La Nina Neutral El Nino

0.00

0.50

1.00

1.50

2.00

2.50

3.00

La Nina Neutral El Nino0.00

0.50

1.00

1.50

2.00

2.50

La Nina Neutral El Nino

ENSO Outlook for next Summer:

Impacts by peril

• Vary by region• More bushfires• More intense rainfall• Fewer cyclones, but more intense• Wind / Hail – not clear

Impacts by peril

• Vary by region, emerge over a long period• More bushfires• More intense rainfall• Fewer cyclones, but more intense• Wind / Hail – not clear

• More actions of the sea

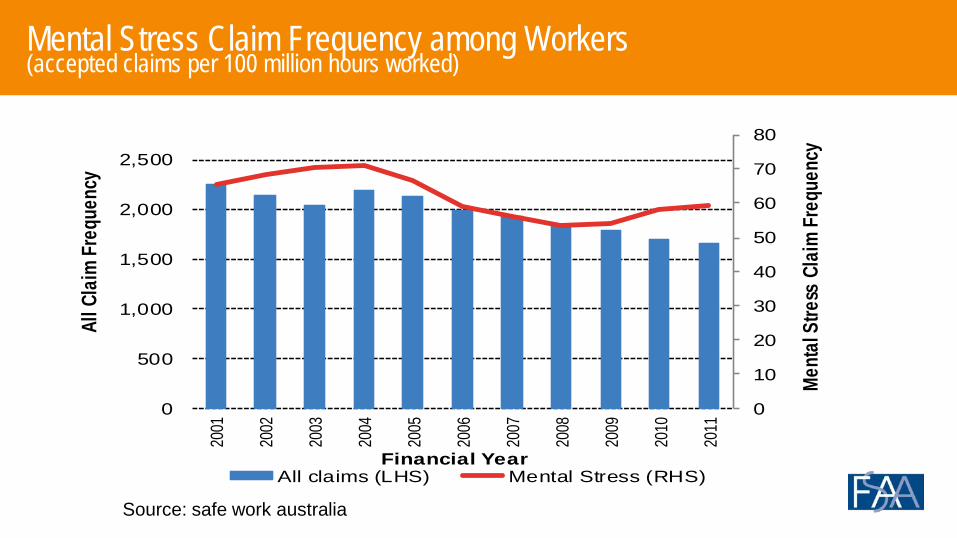

Mental Health

Identical twins

0

10

20

30

40

50

60

70

80

0

500

1,000

1,500

2,000

2,500

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Ment

al S

tress

Cla

im Fr

eque

ncy

All C

laim

Freq

uenc

y

Financial YearAll claims (LHS) Mental Stress (RHS)

Mental Stress Claim Frequency among Workers (accepted claims per 100 million hours worked)

Source: safe work australia

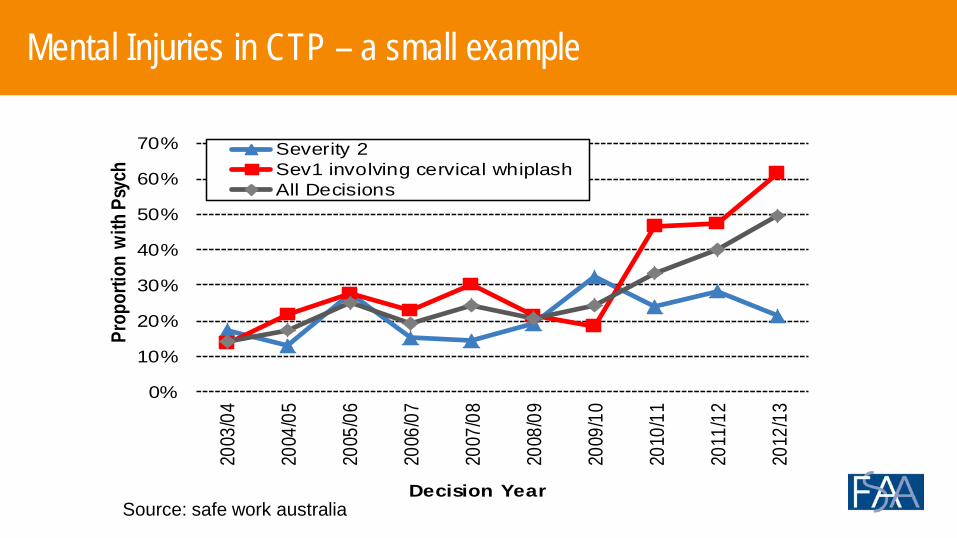

Mental Injuries in CTP – a small example

0%

10%

20%

30%

40%

50%

60%

70%

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

Prop

ortio

n wi

th P

sych

Decision Year

Severity 2Sev1 involving cervical whiplashAll Decisions

Source: safe work australia

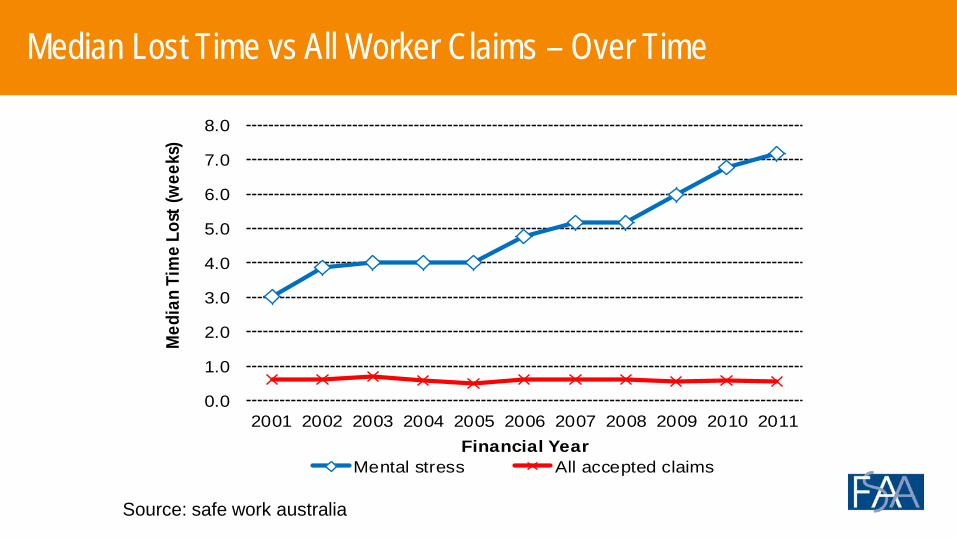

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Med

ian

Tim

e Lo

st (w

eeks

)

Financial YearMental stress All accepted claims

Median Lost Time vs All Worker Claims – Over Time

Source: safe work australia

Ella Ingram vs QBE Insurance

• Hospitalised with depression, cancelled overseas trip• Travel insurance claim denied on basis of mental health exclusion• Ingram claimed unlawfully discriminated against under Equal

Opportunities Act and Disability Discrimination Act• Acts allow insurers to discriminate on basis of statistical data

• Decided by Victorian Civil and Administrative Tribunal (VCAT)

Ella Ingram vs QBE Insurance

• Hospitalised with depression, cancelled overseas trip• Travel insurance claim denied on basis of mental health exclusion• Ingram claimed unlawfully discriminated against under Equal

Opportunities Act and Disability Discrimination Act• Acts allow insurers to discriminate on basis of statistical data

• Decided by Victorian Civil and Administrative Tribunal (VCAT)• Decision against QBE – failed to show that relied on statistical data

when denied indemnity. Hence not allowed to discriminate

Ella Ingram vs QBE Insurance

Environment

• Senate enquiry into financial advice• Separate investigation by ASIC• Labour suggest consideration of a Royal Commission into life

insurance• ASIC’s report on motor dealers selling life insurance• NDIS impacts?

Child Abuse

Unlucky brothers

Compensation for Child Sex Abuse

• Royal Commission final report on redress and civil litigation (09/15)• Recommended national redress scheme for victims

• eligibility on a reasonable likelihood basis• scale of damages relating to severity and impact of abuse (maximum of $200,000)

• Commission also recommended changes to civil liability• limitation periods abolished (retrospective)• identifying a proper defendant (retrospective)• reverse onus of proof (prospective)

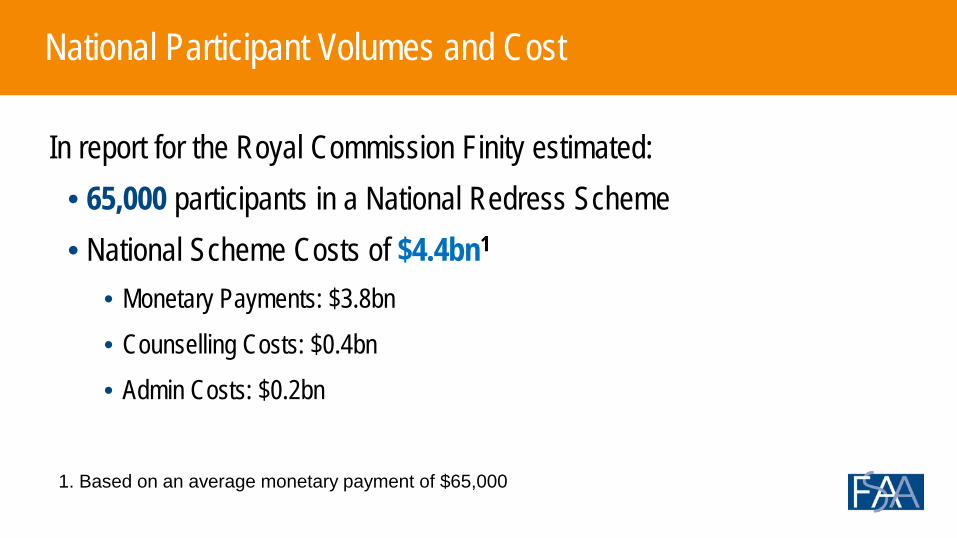

National Participant Volumes and Cost

In report for the Royal Commission Finity estimated:• 65,000 participants in a National Redress Scheme• National Scheme Costs of $4.4bn1

• Monetary Payments: $3.8bn• Counselling Costs: $0.4bn• Admin Costs: $0.2bn

1. Based on an average monetary payment of $65,000

Considerations for Insurers

• Unlikely a legal liability for Redress: Insurance Contracts not likely to trigger• BUT, existence of redress scheme likely to impact on behaviour of survivors

• will depend heavily on structure and design of redress scheme• If Statute of Limitations and Duty of Care rules changed there could be large

impacts for insurers

Titan vs Titanic

Cyber

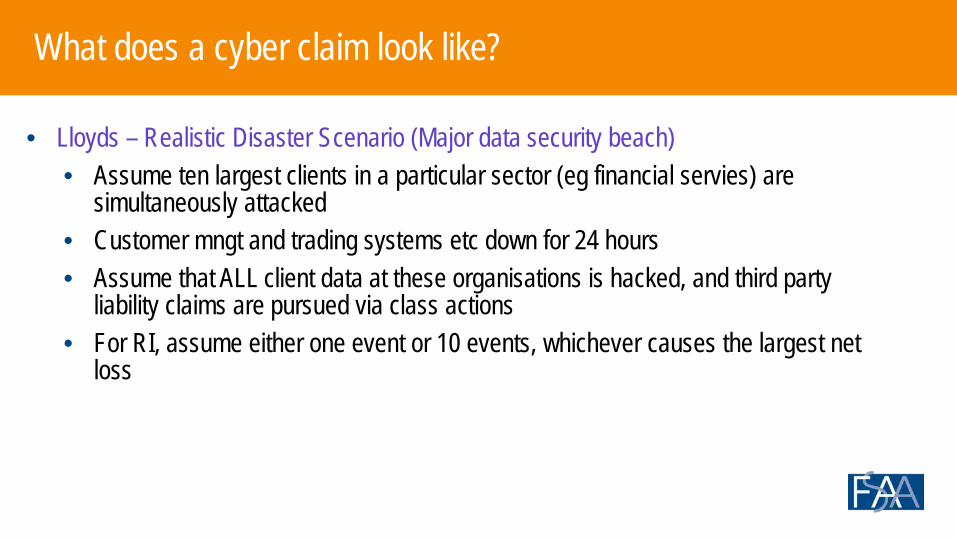

What does a cyber claim look like?

• Lloyds – Realistic Disaster Scenario (Major data security beach)• Assume ten largest clients in a particular sector (eg financial servies) are

simultaneously attacked• Customer mngt and trading systems etc down for 24 hours• Assume that ALL client data at these organisations is hacked, and third party

liability claims are pursued via class actions• For RI, assume either one event or 10 events, whichever causes the largest net

loss

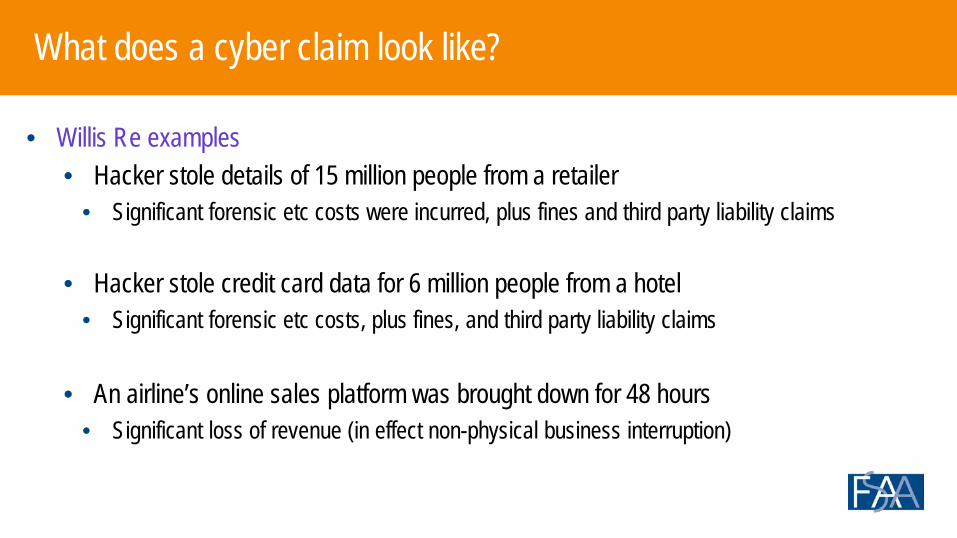

What does a cyber claim look like?

• Willis Re examples• Hacker stole details of 15 million people from a retailer

• Significant forensic etc costs were incurred, plus fines and third party liability claims

• Hacker stole credit card data for 6 million people from a hotel• Significant forensic etc costs, plus fines, and third party liability claims

• An airline’s online sales platform was brought down for 48 hours• Significant loss of revenue (in effect non-physical business interruption)

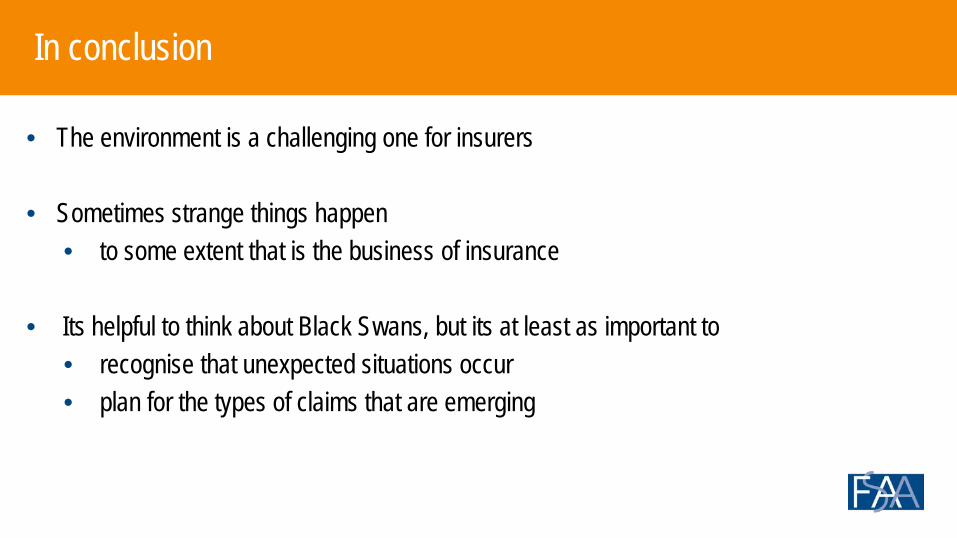

In conclusion

• The environment is a challenging one for insurers

• Sometimes strange things happen• to some extent that is the business of insurance

• Its helpful to think about Black Swans, but its at least as important to • recognise that unexpected situations occur • plan for the types of claims that are emerging

Distribution & UseThis presentation has been prepared for the FSAA conference, held on 19/20 May 2016. It is not intended, nor necessarily suitable, for any other purpose.

Third parties should recognise that the furnishing of this presentation is not a substitute for their own due diligence and should place no reliance on this presentation or the data contained herein which would result in the creation of any duty or liability by Finity to the third party.

Reliances & LimitationsFinity wishes it to be understood that the information presented at the seminar is of a general nature and does not constitute actuarial advice or investment advice. While Finity has taken reasonable care in compiling the information presented, Finity does not warrant that the information provided is relevant to a particular reader’s situation, specific objectives or needs.

Finity does not have any responsibility to any attendee at the conference or to any other party arising from the content of this presentation. Before acting on any information provided by Finity in this presentation, readers should consider their own circumstances and their need for advice on the subject – Finity would be pleased to assist.