Embed Size (px)

Citation preview

THE CHEMICAL INDUSTRY IN THE NEXT

INDUSTRIAL REVOLUTION, THE “SUSTAINABLE ONE”

MR. RAFAEL CAYUELA TWITTER @CAYUELARAFAEL

AUTHOR

“THE CHEMICAL INDUSTRY BY 2050”

7th October 2015

All rights reserved to WILEY - VCH

Energy Exchange Series Breakfast

Disclaimer

• The information in this presentation is based on information extracted from the book on “The Future of the Chemical Industry by 2050” edited by Mr. Rafael Cayuela and published by WILEY-VCH. WILEY does not warrant the accuracy, reliability, completeness or timeliness of the information and undertakes no obligation to revise or update this presentation.

• Mr. Rafael Cayuela act as an individual and author and non as an DOW Chief Economist or Employee. Dow Chemical (including its directors, officers, employees, agents and subcontractors) hereby waives any and all liability for damages of whatever kind and nature which may occur or be suffered as a result of the use of this presentation or reliance on the information therein.

• This presentation contains forward-looking information within the meaning of any applicable securities laws ("Forward-Looking Information"). The purpose of the Forward-Looking Information is to provide audience expectations and a logical framework about future developments on the industry, trends, business prospects and opportunities and may not be appropriate for other purposes and must not be relied on.

• All rights reserved (including those of translation into other languages). No part of this presentation and book may be reproduced in any form, not transmitted or translated into a machine language without written permission from the publisher. Registered names, trademarks, etc.. used in this presentation even when not specifically marked as such, are not to be considered un protected by law.

2 All rights reserved to WILEY - VCH

Strategy vs. Tactics

Q 1 : What was the world population in 1970?

A) 2, 5 B) 3,5 C) 4,5 2010 : 7 billion

Q 2 : What was the world life expectancy in 1970?

A) 35 B) 45 C) 55 2010 : 65 years

Q 3 : What was the World $US GDP in 1970?

A) 15 B) 25 C) 35 2010 : $US73 trillion

Q 4 : What was the world oil demand in 1970?

A) 28 B) 45 C) 65 2010 : 88 million barrel

3 All rights reserved to WILEY - VCH

TIME TO REFLECT

Strategy vs. Tactics

Q 1 : What was the world population in 1970?

A) 2, 5 B) 3,6 C) 4,5 2010 : 7 billion

Q 2 : What was the world life expectancy in 1970?

A) 35 B) 45 C) 55 2010 : 65 years

Q 3 : What was the World $US GDP in 1970?

A) 15 B) 25 C) 35 2010 : $US73 trillion

Q 4 : What was the world oil demand in 1970?

A) 28 B) 44 C) 65 2010 : 88 million barrel

4 All rights reserved to WILEY - VCH

100%

44%

387%

100%

TIME TO REFLECT – TIME FOR STRATEGY

During the next decades and on light of all the upcoming challenges our world need to face, strategy will play a much bigger role industry will need to move from “quantitative growth” into “quantitative & qualitative” growth. In other words the focus will shift from “operations” and incremental improvements into pure innovation.

GLOBAL MEGATRENDS

SOCIAL

“A WORLD WITH MORE THAN 9 BILLION PEOPLE, HIGHER QUALITY OF LIFE AND LIFE EXPECTANCY,

MOVING INTO CITIES”

5 All rights reserved to WILEY - VCH

Social Megatrends – Population

9 to 10 billion people by 2050, with the REST adding 1.8 billion and India

440 million. Japan, Russia, China & EU will face shrinking & older populations

Source : United Nations - World Population Prospect – 2007 Revision

Mill

ion

peo

ple

World Population Scenarios World Population per Area - Base World Population per Area in %

Lower case Base scenario High scenario

6 All rights reserved to WILEY - VCH

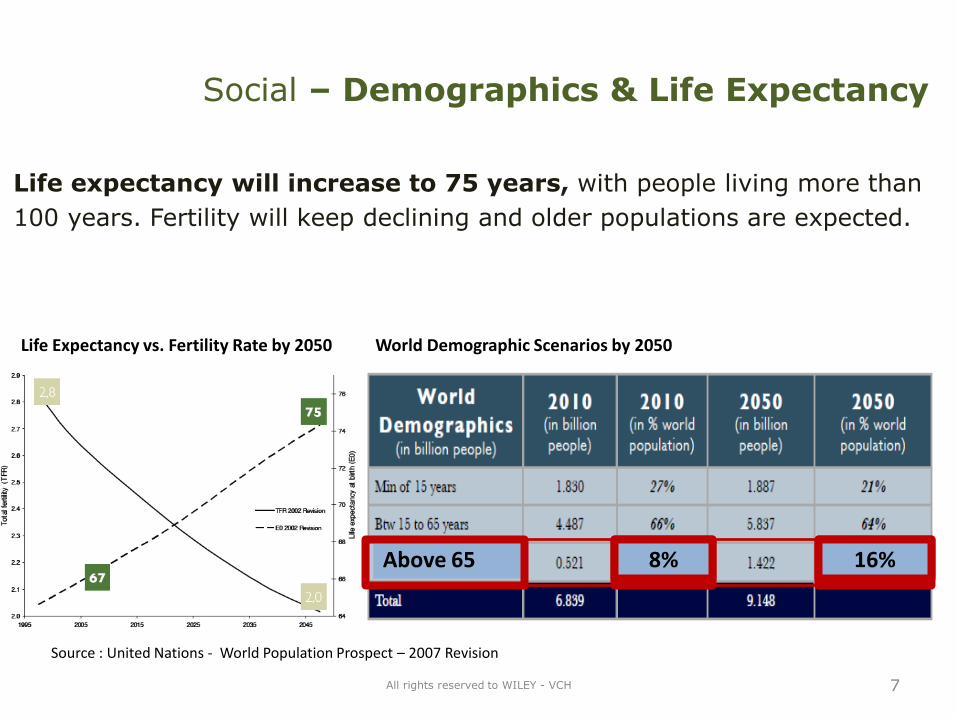

Life expectancy will increase to 75 years, with people living more than

100 years. Fertility will keep declining and older populations are expected.

Life Expectancy vs. Fertility Rate by 2050 World Demographic Scenarios by 2050

Source : United Nations - World Population Prospect – 2007 Revision

7 All rights reserved to WILEY - VCH

Above 65 8% 16%

Social – Demographics & Life Expectancy

GLOBAL MEGATRENDS

ECONOMY

“THE LARGEST MIDDLE CLASS IN HUMAN HISTORY”

8 All rights reserved to WILEY - VCH

Economic Megatrends - GDP

World GDP expected to quadruple to $US281 trillion by 2050; BRIC

will double their market share & Advanced Economies their size

Source : IMF and PWC and PriceWaterHouseCoopers for long term economic projections

9 All rights reserved to WILEY - VCH

Economic Megatrends - GDP

Source : IMF and PWC and PriceWaterHouseCoopers for long term economic projections

China & India might become the largest economies in the world,

while China, India & USA alone could host 50% of the world GDP.

50%

50%

$US 20 to 25 trillion gap

10 All rights reserved to WILEY - VCH

GLOBAL MEGATRENDS

CLIMATE CHANGE

“A WORLD IN A DIET OF 4,000 GRAMS OF CO2 PER CAPITA AND DAY, REPRESENTS A ENORMOUS TECHNOLOGICAL / POLITICAL CHALLENGE,

BUT ALSO AN HUGE BUSINESS OPPORTUNITY

“CLIMATE CHANGE IS THE “WAR” OF THE 21ST CENTURY”

11 All rights reserved to WILEY - VCH

Climate Change – Fundamentals

Scientific evidences correlate Greenhouse Emissions with higher

temperatures, eventually triggering “climate change”.

12 All rights reserved to WILEY - VCH

Historical C02 Emissions Historical World Temperature Variations Emissions vs. Temperature Fluctuations

2nd

May 2

01

3

Climate Change – Root causes

13 All rights reserved to WILEY - VCH

World Green House Emissions

72% = C02 19% Methane 9% Nitrous Oxide

World CO2 Emissions reached

33 Gigaton in 2010

72% C02 related.

29% Power stations

20% Ind. Processes

19% Transportation

12% residential

18% Methane

40% Agricultural

9% Nitrous Oxide

60% agricultural

14 All rights reserved to WILEY - VCH

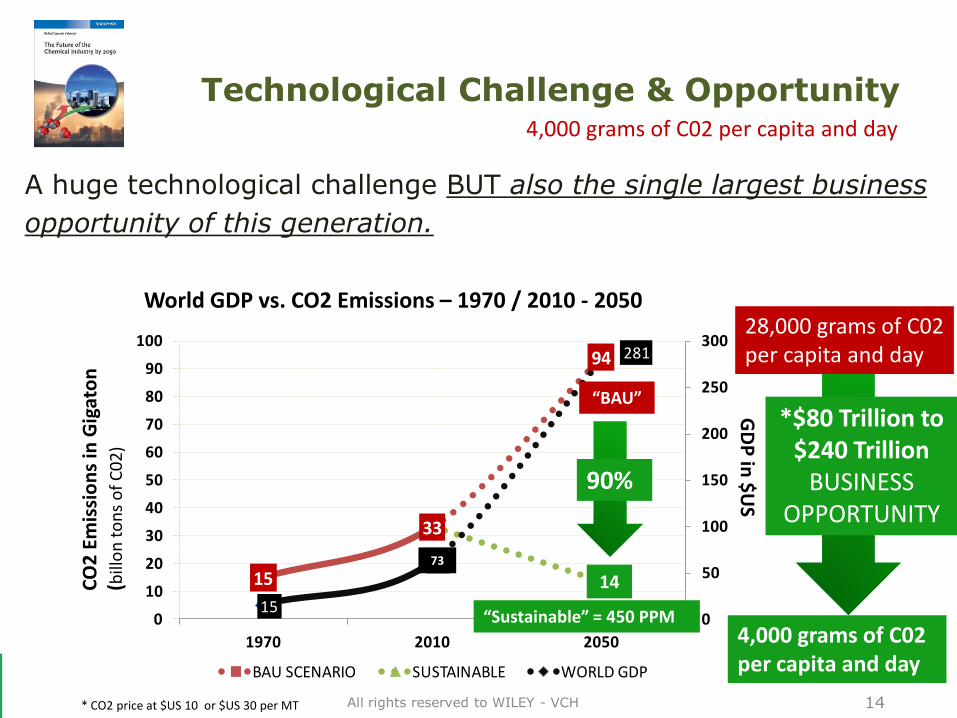

A huge technological challenge BUT also the single largest business

opportunity of this generation. G

DP

in $

US

15

33

94

1415

63

281

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

80

90

100

1970 2010 2050

BAU SCENARIO SUSTAINABLE WORLD GDP

90%

CO

2 E

mis

sio

ns

in G

igat

on

(b

illo

n t

on

s o

f C

02

)

“BAU”

“Sustainable” = 450 PPM

14

World GDP vs. CO2 Emissions – 1970 / 2010 - 2050

73

4,000 grams of C02 per capita and day

*$80 Trillion to $240 Trillion

BUSINESS OPPORTUNITY

4,000 grams of C02 per capita and day

28,000 grams of C02 per capita and day

* CO2 price at $US 10 or $US 30 per MT

Technological Challenge & Opportunity

Living with 4,000 grams of C02 per capita & day

BRAZIL, 16035

CHINA, 4,978

USA, 54,475

USA, 5,320

EU, 22,605

CHINA, 17058

INDIA, 3995

BRAZIL, 6,519

JAPAN, 28126

CANADA, 48751

RUSSIA, 32861

EU, 3788JAPAN, 3941

CANADA, 4,231 INDIA, 4,235 BRAZIL, 4942 RUSSIA, 4905

USA, 43034

CANADA, 32,829

EU, 16605

JAPAN, 20305

CHINA, 40111

INDIA, 49095

RUSSIA, 72236

CHEMICAL INDUSTRY, 545INDUSTRY, 982

INDUSTRY, 142-4,000

0

4,000

8,000

12,000

16,000

20,000

24,000

28,000

32,000

36,000

40,000

44,000

48,000

52,000

56,000

60,000

64,000

68,000

72,000

76,000

80,000

$(5,000) $5,000 $15,000 $25,000 $35,000 $45,000 $55,000 $65,000 $75,000 $85,000 $95,000 $105,000

CO

2 EM

ISSI

ON

S -

GR

AM

S P

ER C

AP

ITA

& D

AY

GDP PER CAPITA IN $ US

Sustainable Scenario 2050 - CO2 Emissions - 4,000 Grams Per Capita & Day

Daily Emissions per Capita in Grams of C02

11 times

14 times

8 times

8 times

8 times

3 times 4 times

5 times

7 times

ISSUE 2 – Economic / Wealth Challenge

All rights reserved to WILEY - VCH

GLOBAL LONG TERM MEGATRENDS

ENERGY MEGATRENDS

“IN A ENVIRONMENT OF MASSIVE ENERGY GROWTH, ENERGY TRANSITIONS OCCUR EVEN WHEN THE INCUMBENT ENERGY IT IS STILL AVAILABLE, AND THE NEW ONE IS MORE EFFICIENT, CHEAPER AND SUSTAINABLE” “CRUDE OIL PRICES MIGHT HAVE PEAKED FOREVER IN 2011 – PRICE SHOCKS ARE GOOD INDICATORS OF ENERGY TRANSITIONS”

16 All rights reserved to WILEY - VCH

Energy Transitions – Price “Shocks”

Price Shocks are tremendous “source” of information.

17

2010

Nominal Crude Oil Prices

Real Crude Oil Prices

HISTORICAL CRUDE OIL PRICES 1860 - 2010

All rights reserved to WILEY - VCH

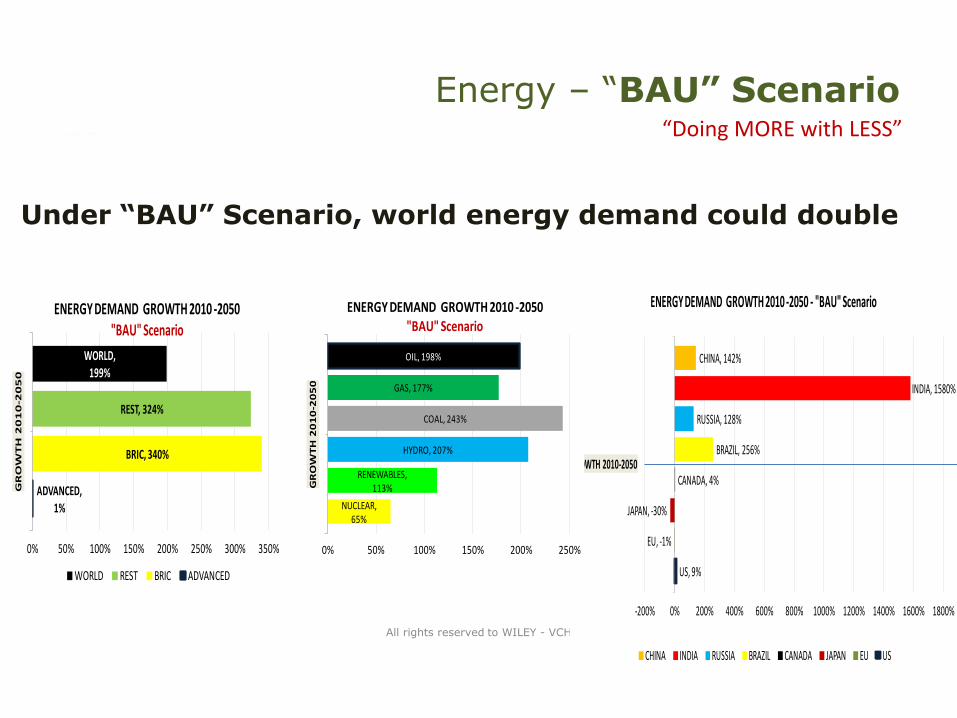

Energy – “BAU” Scenario

18 All rights reserved to WILEY - VCH

US, 9%

EU, -1%

JAPAN, -30%

CANADA, 4%

BRAZIL, 256%

RUSSIA, 128%

INDIA, 1580%

CHINA, 142%

-200% 0% 200% 400% 600% 800% 1000% 1200% 1400% 1600% 1800%

GROWTH 2010-2050

ENERGY DEMAND GROWTH 2010 -2050 - "BAU" Scenario

CHINA INDIA RUSSIA BRAZIL CANADA JAPAN EU US

ADVANCED, 1%

BRIC, 340%

REST, 324%

WORLD, 199%

0% 50% 100% 150% 200% 250% 300% 350%

GR

OW

TH

20

10

-20

50

ENERGY DEMAND GROWTH 2010 -2050 "BAU" Scenario

WORLD REST BRIC ADVANCED

NUCLEAR, 65%

RENEWABLES, 113%

HYDRO, 207%

COAL, 243%

GAS, 177%

OIL, 198%

0% 50% 100% 150% 200% 250%

GR

OW

TH

20

10

-20

50

ENERGY DEMAND GROWTH 2010 -2050 "BAU" Scenario

Under “BAU” Scenario, world energy demand could double

“Doing MORE with LESS”

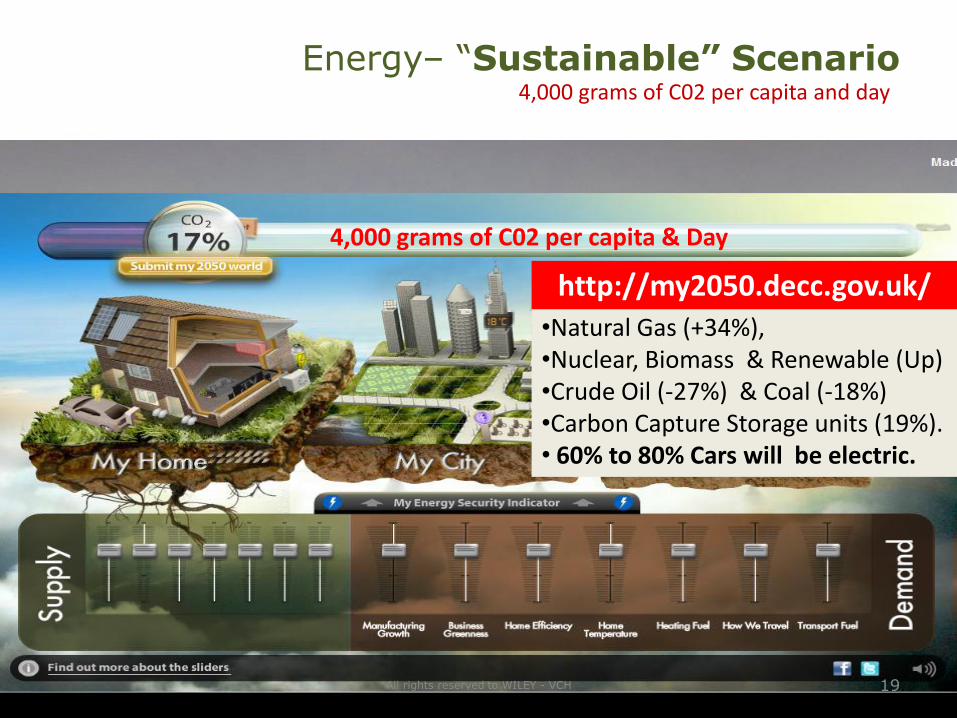

Energy– “Sustainable” Scenario

19 All rights reserved to WILEY - VCH

4,000 grams of C02 per capita and day

4,000 grams of C02 per capita & Day

•Natural Gas (+34%), •Nuclear, Biomass & Renewable (Up) •Crude Oil (-27%) & Coal (-18%) •Carbon Capture Storage units (19%). • 60% to 80% Cars will be electric.

http://my2050.decc.gov.uk/

GLOBAL LONG TERM MEGATRENDS

SINGULARITY

“INFORMATION TECHNOLOGY & COMPUTATIONAL PROGRESS WILL ACCELERATE AND CHANGE ALL ASPECTS OF OUR LIFE, THE WAY WE WORK, LIVE, AND COMMUNICATE”

20 All rights reserved to WILEY - VCH

All rights reserved to WILEY - VCH

Singularity

21

Computational Progress and Tech. Convergence accelerate Human Progress Exponentially

Digital Revolution

Singularity

22

Digital Revolution

All rights reserved to WILEY - VCH

Digitized – more information is becoming digitized, opening the door for a layer of analytics (e.g. machine learning) to be placed on top of it

Deceptive – early stages of exponential growth processes may be deceptively linear

Disruptive – once exponential growth reaches the inflection point, or “knee of the

curve,” they become truly disruptive

Dematerialized – no longer do you have to buy a flashlight or digital camera, you can

simply purchase an app on your phone to accomplish these tasks

Demonetized – as manufacturing techniques improve, technologies are becoming

less expensive at an alarming pace

Democratized –3 billion more people on the Internet by 2020

Exponential Growth – 6 Ds

THE CHEMICAL INDUSTRY LONG TERM DINAMICS

BY 2050

“THE CHEMICAL INDUSTRY / SCIENCE / ENGINEERING WOULD BE AT THE CORE OF THE NEXT INDUSTRIAL REVOLUTION – THE SUSTAINABLE & DIGITAL ONE”

23 All rights reserved to WILEY - VCH

Structure – Growth & Markets

China and India will become the largest chemical markets with 50% share.

24 All rights reserved to WILEY - VCH

BAU SCENARIO

27%

47%

1

Structure – Growth & Markets

India will be the fastest growing chemical market in world.

25 All rights reserved to WILEY - VCH

BAU SCENARIO

GROWTH RANKING in % - 2010 - 2050

ADJUSTED "BAU" SCENARIO - 2050

RANK COUNTRY INDUSTRY % GROWTH

TOP 1 INDIA CHEMICAL 3816%

TOP 2 INDIA PHARMA 3409%

TOP 3 CHINA PHARMA 1905%

TOP 4 CHINA CHEMICAL 431%

TOP 5 RUSSIA PHARMA 609%

TOP 6 BRAZIL PHARMA 527%

TOP 7 RUSSIA CHEMICAL 401%

TOP 8 BRAZIL CHEMICAL 372%

TOP 9 USA PHARMA 189%

TOP 10 USA CHEMICAL 164%

TOP 11 CANADA PHARMA 140%

TOP 12 EUROPE 27 PHARMA 132%

TOP 13 CANADA CHEMICAL 111%

TOP 14 EUROPE 27 CHEMICAL 105%

TOP 15 JAPAN PHARMA 61%

TOP 16 JAPAN CHEMICAL 38%

LARGEST WORLD MARKETS

CHEMICALS

CHINA CHINA 4,048$

EUROPE INDIA 2,903$

USA USA 1,385$

JAPAN EUROPE 1,332$

BRAZIL BRAZIL 474$

INDIA JAPAN 281$

CANADA RUSSIA 211$

RUSSIA CANADA 93$

PHARMA

USA USA 925$

EUROPE CHINA 752$

JAPAN EUROPE 566$

CHINA INDIA 456$

CANADA BRAZIL 128$

BRAZIL JAPAN 114$

RUSSIA RUSSIA 96$

INDIA CANADA 56$

763$

651$

524$

203$

100$

74$

44$

42$

2050

2,010 2050

320$

244$

71$

37$

2,010

24$

20$

14$

13$

1

2nd

4th

Feedstock Lighter, Renewable & Bio

Lighter, renewable and bio but still dependent in Naphtha.

All rights reserved to WILEY - VCH

BAU SCENARIO

2

51%

56%

55%

31%

36%

35%

30%

48%

14%

9%

15%

20%

0% 20% 40% 60% 80% 100%

WORLD

REST

BRIC

ADV

NAPHTHA & OIL ETHANE PROPANE / BUTANE / REST

BAU – Petrochemical Feedstock 2010 BAU – Petrochemical Feedstock 2050

56%

44%

75%

44%

30%

47%

10%

38%

13%

9%

15%

19%

0% 20% 40% 60% 80% 100%

WORLD

REST

BRIC

ADV

NAPHTHA & OIL ETHANE PROPANE / BUTANE / REST

Industry need for cheaper energy, feedstock and lower emissions will

accelerate the transition into lighter feedstock

All rights reserved to WILEY - VCH

BAU SCENARIO

30% less CO2 emissions

Feedstock Lighter, Renewable & Bio 2

Industry– Climate Change

The Chemical Industry remains a great contributor to emissions reductions.

In 2005, the industry released 3 Gigaton of C02e while “abating” 6 Gigaton

All rights reserved to WILEY - VCH

EMISSIONS vs. ABATEMENT = 1 to 2

X 2 times Abatement

3

Regulation – Global & Stringer

More global and stringent regulation, with higher C02 prices.

All rights reserved to WILEY - VCH

4,000 grams of C02 per capita & day

EMISSION TRADING SCHEMES

•2005 Europe Mandatory •2005 Japan Voluntary •2008 Canada Voluntary •2008 N. Zealand Voluntary •2010 UK Mandatory •2010 US States* Mandatory •2012 Australia* Mandatory •2015 China Mandatory •2015 Korea Mandatory

•Note“: WCI Western Climate Initiative

4

Regulation – Global, Stringer, Unbearable

“Under the new perspective many companies and industries will peril”

All rights reserved to WILEY - VCH

4,000 grams of C02 per capita & day

4

Exxon Mobile uses $60 tonne

as internal carbon price for C02

Expected EBITDA

annual lost of

$US 8 Billion!!

Sustainable?

INNOVATION – Technology

31

THE 3rd INDUSTRIAL REVOLUTION 5

1850 1900 1950 2000 2050 2100

INNOVATION Level 2

OPERATIONAL EFFICIENCY

NEXT INDUSTRIAL REVOLUTION “The Sustainable / Digital One”

4,000 grams per capita & day

2nd INDUSTRIAL REVOLUTION Enormous Growth - Fossil Fuel

1,2 1,7 2,5 6.0 9,0 12 Billion people

Technological CONVERGENCE

Business COLLABORATION

INNOVATION Level 3

R&D in Chemical Industry in 2010 - 25% new chemistry - 75% in incremental innovation -Source: McKinsey

INNOVATION – Technology

• Circular Economy, Technological Convergence and Collaboration will be at the core of the next industrial revolution.

• This require new biz models, new skills (employees/leaders), regulatory systems (IP protection, patents, antitrust) and technological frameworks.

32

THE 3rd INDUSTRIAL REVOLUTION

5

• Companies will be valued by the innovation pipeline of its value chain;

not only by their own innovation, financials or R&D pipeline.

• Innovation will become disruptive and exponential rather than incremental (Singularity)

Energy Chemical

Pharmaceutical

Consumer

Bank

SHELL DOW DOW

BMW

Information

Natural

MICHELIN

EXXON

PFIZER GOOGLE

APPLE NIKE APPLE

MICROSOFT

Natural SHANGAI

Health Mobility Industry

JPMORGAN AIRBUS UBS

All rights reserved to WILEY - VCH

Conclusions

• We are leaving historical and strategic times. During this transition the world is poised to witness another period of massive transformation. A world with 9 billion people and $US 280 trillion GDP; the world will have the potential to host “the largest, wealthiest and healthiest societies in human history”.

• China, USA & India will become the largest world economies but also the largest chemical and pharmaceutical markets. World avg. life expectancy will to 75 by 2050, with millions of people living more than 100 and up to 130 years.

• During this transition world GDP per capita will triple to US$ 30,675; creating a massive middle class and pulling millions of people our of poverty.

• Singularity and the Digital Revolution will accelerate and change most of the aspects of our life, the way we work, live, and communicate.

• However our world will not be sustainable. A world poised to live with just 4,000 grams of CO2 per capita an day it is not only a moral obligation and technological and political challenge, but also a large business opportunity.

34 All rights reserved to WILEY - VCH

UNDER THE 3rd INDUSTRIAL REVOLUTION

Conclusions

• Emissions reductions, resource scarcity and digitalization will trigger the Next Industrial Revolution – “Sustainable & Digital one” – moving the industry from operational efficiencies into innovation and fostering “technical convergence, business collaboration and the “circular economy”.

• The industry will be ‘‘called into action’’. New companies and industries will blossom, others will disappear. Massive growth and disrupting changes (markets, feedstock, products & technologies); combined with stringent emissions reductions , will stretch the industries to levels never seen before.

• Addressing emissions and energy reductions is not only a huge technological challenge and a moral obligation; but also it is a enormous business opportunity, at least $100 trillion dollars.

• This is an historical opportunity for the chemical industry to shine on what it does best: technology and innovation!

• The Chemical Industry will be at the core of the 3rd Industrial Revolution, I hope this time we will not forget it very soon.

35

UNDER THE 3rd INDUSTRIAL REVOLUTION

THANKS

“Welcome to a much larger and sustainable world thanks to chemistry”

All rights reserved to WILEY - VCH

![Title Advancing small-molecule-based chemical …...1 Advancing Small-Molecule-Based Chemical Biology With Next-Generation Sequencing Technologies Chandran Anandhakumar,[a] Seiichiro](https://img.pdfslide.net/doc/110x75/5fc86aa017ed2d10ca7bca2c/title-advancing-small-molecule-based-chemical-1-advancing-small-molecule-based.jpg)