Embed Size (px)

Citation preview

HOUSE OF LORDS

Committee for Privileges and Conduct

11th Report of Session 2010–12

The Conduct of Lord Avebury

Ordered to be printed 12 January 2012

Published by the Authority of the House of Lords

London : The Stationery Office Limited

£price

HL Paper 246

2 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

The Committee for Privileges and Conduct The Committee for Privileges and Conduct is appointed each session by the House to consider questions regarding its privileges and claims of peerage and precedence and to oversee the operation of the Code of Conduct. Detailed consideration of matters relating to the Code of Conduct is undertaken by the Sub-Committee on Lords’ Conduct.

Current Membership The Members of the Committee for Privileges and Conduct are: Baroness Anelay of St Johns Lord Bassam of Brighton Lord Brabazon of Tara (Chairman) Lord Brooke of Sutton Mandeville Lord Eames Lord Howe of Aberavon Lord Irvine of Lairg Lord Laming Lord Mackay of Clashfern Lord McNally Baroness Manningham-Buller Baroness Royall of Blaisdon Baroness Scotland of Asthal Lord Scott of Foscote Lord Shutt of Greetland Lord Strathclyde The Members of the Sub-Committee on Lords’ Conduct are: Lord Cope of Berkeley Lord Dholakia Lord Irvine of Lairg Baroness Manningham-Buller (Chairman) Baroness O’Neill of Bengarve The Code of Conduct and the up-to-date Register of Lords’ Interests are on the Internet at http://www.publications.parliament.uk/pa/ld/ldreg.htm.

General Information General information about the House of Lords and its Committees can be found at http://www.parliament.uk/lords/index.cfm.

Contacts General correspondence should be addressed to the Clerk of the Committee for Privileges and Conduct, House of Lords, London, SW1A 0PW (telephone 020 7219 8796). Correspondence relating to the work of the Sub-Committee on Lords’ Conduct should be addressed to the Clerk of the Sub-Committee on Lords’ Conduct, House of Lords, London SW1A 0PW (telephone 020 7219 1228).

THE CONDUCT OF LORD AVEBURY

1. The Committee has considered a report by the Commissioner for Standards on the conduct of Lord Avebury. The report arises out of a complaint, received on 13 September 2011, regarding Lord Avebury’s entry in the Register of Lords’ Interests.

2. The Commissioner has concluded that he is “satisfied that Lord Avebury has complied with the Code of Conduct in relation to registering relevant interests”. He has therefore dismissed the complaint.

3. The Sub-Committee on Lords’ Conduct, to which, in accordance with the Guide to the Code of Conduct, the Commissioner presents his reports, notes that Lord Avebury’s entry in the Register did not disclose the fact that a partnership in which he had an indirect interest derived income from waste disposal into a landfill site. However, the Sub-Committee accepts the Commissioner’s conclusion that this did not constitute a breach of the Code of Conduct.

4. In light of the Commissioner’s and the Sub-Committee’s conclusions, which we endorse, no further action is required.

5. We make this Report to the House for information.

4 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

APPENDIX 1: REPORT FROM THE SUB-COMMITTEE ON LORDS’ CONDUCT

Letter to the Chairman of Committees from the Chairman of the Sub-Committee on Lords’ Conduct

I am writing with the agreement of the Sub-Committee on Lords’ Conduct to submit a report by the Commissioner for Standards dismissing a complaint against Lord Avebury. The complaint raised the question of whether Lord Avebury’s entries in the Register of Lords’ Interests were sufficient to disclose the full nature of his business and land holdings.

Lord Avebury has registered a Directorship of “CL Projects Ltd (computer hardware & software; provides management advice to Cook Lubbock & Co, a partnership in which it has a 50% interest)”. The Sub-Committee note that Lord Avebury’s entry in the Register did not disclose that Cook Lubbock & Co derives most of its income from waste disposal into a landfill site which was on land rented to it by Lord Avebury and described as “arable” in the Register. However we accept the Commissioner’s judgement that this does not break the Code.

I would like to draw your attention to paragraph 22 of the Commissioner’s report in which he supports Lord Avebury’s request that financial information should be kept confidential.1 We would also support that request, but consider that the report should otherwise be published.

Manningham-Buller

16 December 2011

1 Lord Avebury emailed the Clerk of the Select Committee on 1 January 2012 indicating that “I have

decided that in the interests of transparency I don’t want any redactions”. The Commissioner’s report is accordingly reprinted in full.

ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT 5

APPENDIX 2: REPORT FROM THE HOUSE OF LORDS COMMISSIONER FOR STANDARDS ON THE CONDUCT OF LORD AVEBURY

Introduction

1. The complainant (Mr John Cook) initially wrote to the Registrar of Lords’ Interests on 13 September 2011.1 He highlighted his view that Lord Avebury’s “Declaration of Interests” omitted certain information and was in conflict with the obligations set out in the Code of Conduct. The Registrar acknowledged receipt and advised Mr Cook that he was forwarding his letter to the Commissioner for Standards.

2. My office wrote to the complainant on 21 September,2 providing a copy of the Code of Conduct for Members of the House of Lords and Guide to the Code of Conduct. Mr Cook replied on 23 September, making it clear that he was making a complaint and attaching an edited version of his original letter.3 I wrote to Mr Cook on 9 November,4 advising him that I had decided that his complaint fell within my terms of reference and that I had requested a full and accurate account from Lord Avebury of the matters in question. I naturally wrote to Lord Avebury on the same date.5 Mr Cook supplied additional information in a letter dated 22 November 2011.6

Summary

3. In essence, Mr Cook claimed that Lord Avebury’s entry/entries in the Register of Lords’ Interests suffered from omissions. He specifically highlighted that the entry did not reveal Lord Avebury’s involvement in the waste disposal industry, was insufficiently open in relation to his sources of income and could conceivably allow Lord Avebury to pose as an environmental champion, notwithstanding his waste disposal activity.

4. I requested that Lord Avebury respond in writing with a full and accurate account of the matters in question. I drew his attention to the following sections of the 2010 Code of Conduct, which the complaint suggests may have been broken:

“7. In the conduct of their parliamentary duties, Members of the House shall base their actions on consideration of the public interest, and shall resolve any conflict between their personal interest and the public interest at once, and in favour of the public interest.

8. Members of the House:

(a) must comply with the Code of Conduct;

(b) should always act on their personal honour ...

10. In order to assist in openness and accountability Members shall:

1 Annex A 2 Annex B 3 Annex C 4 Annex D 5 Annex E 6 Annex H

6 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

(a) register in the Register of Interests all relevant interests, in order to make clear what are the interests that might reasonably be thought to influence their parliamentary actions ...

12. The test of relevant interest is therefore not whether a Member’s actions in Parliament will be influenced by the interest, but whether a reasonable member of the public might think that this might be the case. Relevant interests include both financial and non-financial interests.”

The facts

5. Lord Avebury’s entry in the Register of Lords’ Interests is set out at Annex F. The entry is exactly as it was on 13 September, the date Mr Cook first wrote to the Registrar.

6. For the purposes of this investigation, only the entries under Categories 1, 2, 4 and 5 are relevant.

7. For ease of reference, I have set out under each Category Lord Avebury’s entry followed by Mr Cook’s observations/allegations (italicised).

Category 1 Directorships

CL Projects Ltd (computer hardware & software; provides management advice to Cook Lubbock & Co, a partnership in which it has a 50% interest)

The entry does not mention that the partnership is a two man partnership which derives most of its income from waste disposal into a landfill site. No information on quantum of income derived from this source. It is also highlighted that the entry contains no information re expenses claimed from the limited company and any potential duplication with Parliamentary expense claims.

Category 2 Remunerated employment etc.

Chartered Engineer (non-practising)

No mention of true remunerated employment.

Category 4 Shareholdings

Controlling interest in CL Projects Ltd (computer hardware & software; provides management advice to Cook Lubbock & Co, a partnership in which it has a 50% interest)

Category 5 Land and property

390 acres arable land in Northamptonshire

No mention that the land is fully leased to the partnership company at an annual rent of £23,716. Nor that the partnership then further leases the land to a national waste management company and is utilised for mineral extraction and waste disposal activities.

8. Mr Cook concluded his concerns by highlighting the potential for Lord Avebury to present himself as an environmental champion whilst deriving his income from the waste disposal industry. Mr Cook supposed that the entry could be construed as being tantamount to an attempt to mislead both Parliament and the general public as to Lord Avebury’s true outside interests and remuneration therefrom.

ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT 7

Lord Avebury’s response

9. Lord Avebury initially engaged with my office on 14 September by telephone and then wrote to me on 16 September.1

10. Lord Avebury informed me, in an effort to place Mr Cook’s complaint in context, that he and Mr Cook constituted the “two man partnership” which formerly owned Cook Lubbock & Co, mentioned in both Lord Avebury’s Register entry and also in Mr Cook’s letters. Lord Avebury further advised that the partnership is in the process of dissolution. Cook Lubbock & Co is held by limited companies and has been since 1997/98 when that structure replaced a true two man partnership. Lord Avebury states that the change came about because Mr Cook was declared bankrupt.

11. Lord Avebury openly acknowledged that Cook Lubbock derives most of its income from waste disposal into a landfill site, though he highlighted that income is also produced by electricity generation and through farm rental.

12. Lord Avebury disputes the amounts of income Mr Cook suggests he received. He also made it clear that he has no remunerated employment, received no salary and that his income is made up of farm rental payments, dividends and pensions (including the state pension).

13. Lord Avebury argued that he had not breached the Code of Conduct and specifically the seven principles set out at Paragraph 9 of the Code, as well as Paragraphs 7, 8 and 12, which I had brought to his attention in my letter (Annex E).

Analysis and findings

14. I have sought to follow the pattern established in the above Facts section, namely that I have looked at the complaint and Lord Avebury’s response category by category.

Category 1

15. Lord Avebury did register his remunerated directorship(s) and gave a broad indication of the company’s business. He was not required to provide additional detail and it should be noted that Paragraph 48 of the ‘Guide to the Code of Conduct’ (the Guidance) explicitly makes it clear that the amount of remuneration is not required.

16. No evidence whatsoever was supplied in connection with Mr Cook’s assertion that there was scope to submit claims in respect of parliamentary duties to another financial sponsor.

Category 2

17. Lord Avebury has discretion to register his former employment/profession. Thus his entry of Chartered Engineer (non-practising) is perfectly acceptable. He has dealt with the issue of remuneration by means of his Category 1 entry.

Category 4

18. His entry meets the requirements of Category 4(a).

1 Annex G

8 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

Category 5

19. Again, Lord Avebury’s entry fulfils the requirements set out in the Guidance. Specifically, Paragraph 66 states: “Only the nature of the property and a general indication of its location should be indicated (e.g. ‘farm in Norfolk’…) the value of the property and the income received need not be registered, unless it falls under part (b).”

20. I note that Mr Cook’s letters to me both use the phrase “Declaration of Interests” but then make it clear that he is in fact talking about Lord Avebury’s entry in the Register of Lords’ Interests. My investigation deals with the registration issue. I note Mr Cook’s concerns re Lord Avebury’s involvement in the waste disposal industry and the potential scope for misrepresentation, given that there is no explicit reference to that involvement in the Register of Lords’ Interests. However, that involvement would, I suggest, properly be a matter for declaration in line with the provisions of Paragraphs 85–90 of the Guidance. Mr Cook has not claimed that Lord Avebury ever misrepresented his interests and I would expect Lord Avebury to have regard to that requirement, particularly now that such a concern has been highlighted.

21. I am satisfied that Lord Avebury has complied with the Code of Conduct in relation to registering relevant interests and thus has not breached its provisions. In accordance with Paragraph 123 of the Guidance, I dismiss the complaint.

22. I have incorporated all documentation received in to this report in an unedited form. If the Committee for Privileges and Conduct were minded to publish a report, then I would respectfully draw their attention to a verbal request from Lord Avebury that financial information should be kept confidential. In the circumstances of this case I support that request.

Paul Kernaghan CBE QPM

Commissioner for Standards

13 December 2011

ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT 9

Annex A: Letter from Mr John Cook to the Registrar of Lords’ Interests, 13 September 2011

Possible Breach of the House of Lords Code of Practice

I have recently had passed to me Lord Avebury’s Declaration of Interests and I was surprised by what I perceived to be certain omissions. As a consequence I feel it is my duty to refer the matter to you as it seems to me to conflict in many respects with the “Code of Conduct” expected of members of the House of Lords.

I would appreciate any help and guidance you can give me in this matter. As a matter of courtesy I have copied this letter to Lord Avebury’s Solicitors.

I will set out the situation as I see it (having full regard to the “Peers Code of Conduct”) and based on Lord Avebury’s Statutory Declaration of Interests.

Under the following headings he states:

Directorships

He declares a controlling interest in a limited company and states in brackets (computer hardware and software; provides management advice to a partnership (without further description) in which it has a 50% interest).

He does not mention the fact that it is a two-man partnership which derives most of its income from waste disposal into a landfill site and of which the partnership is the beneficial owner. This is, as far as I am aware, his major source of income and in one year recently provided him with £400,000 although it probably now averages in excess of £150,000 p.a. This information is not mentioned in his declaration. Neither, at this moment in time, is it possible to ascertain that his Parliamentary claim for expenses is being in any way duplicated through the expenses claimed from his limited company. There is no evidence one way or the other.

Remunerated employment, office, profession etc.

He declares his profession as being an ‘Engineer’ (non-practising). No mention again of his true Remunerated employment.

Land & Property

He simply declares 390 acres of arable land. He makes no reference to the fact that it is fully leased by him, to the company of which he is a partner at an annual rent of £23,716 increasing with the RPI each year.

He does not mention that this in turn is leased by the Partnership to a national waste management company and that it comprises a large Landfill waste site, a waste disposal operation, a recycling plant, large scale stone and mineral extraction, an energy from waste plant and other ancillary activities connected to the waste industry. This currently provides the income, I have drawn your attention to, under “Directorships” and shows his total income from the waste industry to be approaching £200,000 p.a.

Relying simply on his “Statutory Declaration of Interests”, it would be difficult for anyone, to be able to discover or ascertain, that he has a substantial interest in, and, derives a massive income from, the Waste Industry. There doesn’t appear to be any clue whatsoever to this fact. Consequently from his Statutory Declaration

10 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

he could conceivably, present himself as a champion of all matters environmental without anyone having the slightest suspicion of, or being able to ascertain what some may see as an apparent conflict of interest (and in the general public’s eyes, the possible hypocrisy of it).

I would welcome your view, on my supposition that such a case, however one looks at it, might be construed as being tantamount to an attempt to mislead both Parliament and the general public at large as to his true outside interests.

I should also add that although the waste industry is a much maligned activity, it is one that I have been proud to be associated with for over 40 years. For a Peer to hide from the general public, for whatever reason, his own connection with the industry, does a great disservice to those who strive so hard, on no more than average wages, to maintain this important Public Service.

Annex B: Email from the Clerk to the Commissioner for Standards to Mr Cook, 21 September 2011

The Registrar of Lords’ Interests copied your letter dated 13 September 2011 to the Lords Commissioner for Standards (Mr Paul Kernaghan), who has noted your request for help and guidance. He has asked me to forward a copy of the Code of Conduct and associated Guidance to you (see attached link). The role and mandate of the Lords Commissioner for Standards is clearly set out in the Guidance (see paragraphs 102 onwards). I hope this will assist you.

http://www.publications.parliament.uk/pa/ld/ldcond/code.pdf

Annex C: Letter from Mr Cook to the Clerk, 23 September 2011

Possible Breach of the House of Lords Code of Practice

I acknowledge receipt of your communication dated 21st September 2011 and I appreciate your drawing my attention to the specific sections of the “Code of Conduct” relevant to my complaint.

I have noted sections 102 and 103 which appear to be only applicable to Members of the House of Lords.

Section 104: On the 13th September 2011 my Solicitors sent to Lord Avebury’s Solicitors a copy of my complaint. As far as I am aware there has been no reaction from him to date.

Section 105: My complaint was made in writing in accordance with this section.

Section 106: In order to further clarify my complaint I am forwarding herewith a slightly amended copy of it, highlighting in red my concerns [see below]. The only evidence I can produce (should these be required) are copies of the invoices submitted to the Partnership by Lord Avebury together with the annual accounts showing the payments that have a been made to him.

Section 107: I have made every effort to ensure this correspondence has been treated in a completely confidential manner. I have no wish to publicise it.

Finally, I would like to express my appreciation of your kind assistance in this matter and I look forward to hearing from you in due course.

ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT 11

Revised version of letter from Mr Cook to the Registrar of Lords’ Interests1

Possible Breach of the House of Lords Code of Practice

I have recently had passed to me Lord Avebury’s Declaration of Interests’ and I was surprised by what I perceived to be certain omissions. As a consequence I feel it is my duty to refer the matter to you as it seems to me to conflict in many respects with the “Code of Conduct” expected of members of the House of Lords.

I would appreciate any help and guidance you can give me in this matter. As a matter of courtesy I have copied this letter to Lord Avebury’s Solicitors.

I will set out the situation as I see it (having full regard to the “Peers Code of Conduct”), and based on Lord Avebury’s Statutory Declaration of Interests.

Under the following headings he states:

Directorships

He declares a controlling interest in a limited company and states in brackets (computer hardware and software; provides management advice to a partnership, (without further description) in which it has a 50% interest).

He does not mention the fact that it is a two-man partnership which derives most of its income from waste disposal into a landfill site and of which the partnership is the beneficial owner. This is, as far as I am aware, his major source of income and in one year recently provided him with £400,000 although it probably now averages in excess of £150,000 p.a. This information is not mentioned in his declaration. Neither, at this moment in time, is it possible to ascertain that his Parliamentary claim for expenses is being in any way duplicated through the expenses claimed from his limited company. There is no evidence one way or another.

Remunerated employment, office, profession etc.

He declares his profession as being an ‘Engineer’ (non-practising). No mention again of his true Remunerated employment.

Land & Property

He simply declares 390 acres of arable land. (He makes no reference to the fact that it is fully leased, by him, to the company of which he is a partner at an annual rent of £23,716 increasing with the RPI each year.)

He does not mention that this in turn is leased by the Partnership to a national waste management company and that it comprises a large Landfill waste site, a waste disposal operation, a recycling plant, large scale stone and mineral extraction, an energy from waste plant and other ancillary activities connected to the waste industry. This currently provides the income I have drawn your attention to, under “Directorships” and shows his total income from the waste industry to be approaching £200,000 p.a.

Relying simply on his “Statutory Declaration of Interests”, it would be difficult for anyone to be able to discover, (or ascertain), that he has a substantial interest in, and, derives a massive income from, the Waste Industry. There doesn’t appear to be any clue whatsoever to this fact. Consequently from his Statutory Declaration he

1 Text added to the earlier version of Mr Cook’s letter is given in italics.

12 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

could, conceivably, present himself as a champion of all matters environmental without anyone having the slightest suspicion of, or being able to ascertain what some may see as an apparent conflict of interest (and in the general public’s eye, the possible hypocrisy of it).

I would welcome your view, on my supposition that such a case, however one looks at it, might be construed as being tantamount to an attempt to mislead both Parliament and the general public at large as to his true outside interests and remuneration therefrom.

I should also add that although the waste industry is a much maligned activity, it is one that I have been proud to be associated with for over 40 years. For a Peer to hide from the general public, for whatever reason, his own connection with the industry, does a great disservice to those who strive so hard, on no more than average wages, to maintain this important Public Service.

Annex D: Letter from the Commissioner for Standards to Mr Cook, 9 November 2011

Your letter to the Registrar of Lords’ Interests dated 13/9/11 and your subsequent letter to my Clerk dated 23/9/11 refer.

I note that your complaint is made in compliance with the requirements of the ‘Guide to the Code of Conduct’. I am of the view that your complaint falls within my terms of reference and I have written to Lord Avebury supplying full details of your complaint. I have invited him to provide a full and accurate account of the matters in question.

I note and appreciate your personal commitment to the principle of confidentiality. I will in due course advise you of the outcome of my investigation. However, it may be several weeks before I am in a position to so advise you. If in the interim you require any information from me, or indeed wish to supply additional evidence, please do not hesitate to contact me.

Annex E: Letter from the Commissioner for Standards to Lord Avebury, 9 November 2011

I am writing to you in my capacity as the Commissioner for Standards. I have to advise you that I have received a complaint against you; namely, that you have breached the Code of Conduct by reason of your ‘limited’ declarations of interest.

I attach for your information copies of the two letters I have received from the complainant (Mr John Cook).

It appears on the basis of the complaint that you may have breached the following provisions of the 2010 Code of Conduct:

7. In the conduct of their parliamentary duties, Members of the House shall base their actions on consideration of the public interest, and shall resolve any conflict between their personal interest and the public interest at once, and in favour of the public interest.

8. Members of the House:

(a) must comply with the Code of Conduct;

ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT 13

(b) should always act on their personal honour ...

10. In order to assist in openness and accountability Members shall:

(a) register in the Register of Interests all relevant interests, in order to make clear what are the interests that might reasonably be thought to influence their parliamentary actions ...

12. The test of relevant interest is therefore not whether a Member’s actions in Parliament will be influenced by the interest, but whether a reasonable member of the public might think that this might be the case. Relevant interests include both financial and non-financial interests.

I would also draw your attention to the seven general principles of conduct identified by the Committee on Standards in Public Life and incorporated in to the Code of Conduct.

I have conducted a preliminary assessment of the complaint and believe it is appropriate and in the interests of all concerned that I investigate it. Therefore, I now invite you to respond in writing with a full and accurate account of the matters in question. A response by 30/11/11 would greatly assist me in investigating this matter in a timely fashion.

I attach for ease of reference a copy of the ‘Code of Conduct for Members of the House of Lords and Guide to the Code of Conduct.’

Annex F: Lord Avebury’s entry in the Register of Lords’ Interests as at 13 September 2011

Category 1: Directorships

CL Projects Ltd (computer hardware & software; provides management advice to Cook Lubbock & Co, a partnership in which it has a 50% interest)

Category 2: Remunerated employment, office, profession etc.

Chartered Engineer (non-practising)

Category 4: Shareholdings (a)

Controlling interest in CL Projects Ltd (computer hardware & software; provides management advice to Cook Lubbock & Co, a partnership in which it has a 50% interest)

Category 5: Land and property

390 acres arable land in Northamptonshire

Category 10: Non-financial interests (d)

President, Kurdish Human Rights Project

President, TAPOL (Indonesian Human Rights)

President, Advisory Council for the Education of Romanies and Travellers (ACERT)

President, Peru Support Group

14 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

Chairman, Cameroon Campaign Group

Co-chair, Chittagong Hill Tracts Commission

Category 10: Non-financial interests (e)

Trustee, Silbury Fund

Trustee, Friends of Alola Foundation

Chairman, Maurice Lubbock Memorial Fund

Annex G: Letter from Lord Avebury to the Commissioner for Standards, 16 November 2011

Thank you for your letter of November 9 enclosing copies of the two letters you received from Mr John Cook. I have considered these letters in the light of the Code of Conduct

I must also draw your attention to the context in which Mr Cook’s “complaint” has come forward, since it gives colour to his motivations and intent. I then set out the facts pertinent to his correspondence so that you may make your own assessment against the terms of the Code of Conduct.

Mr Cook refers firstly to a partnership called Cook Lubbock & Co (“CLCo”). Mr Cook and the company of which he is sole director, C.L.A.W. Investments Pension Fund Limited have retained a respectable firm of solicitors to advise on the CLCo partnership and earlier this year; those solicitors served on behalf of their client(s) a notice dated 29 July 2011 to determine the CLCo partnership 12 months hence.

Mr Cook, contrary it seems to his own solicitors’ advice, seems to maintain his own view that the CLCo partnership is one between me and him personally, notwithstanding the vesting of the partnership assets in corporate entities, and notwithstanding the accounting of the partnership for many years. I need make no further detailed comment on that for the purpose of this letter, but you should be aware that regrettably Mr Cook and/or his company are ultimately a disgruntled party who have an axe to grind over the break up of the CLCo partnership. This seems to have found a new dimension of expression in his letter to you.

Turning to the facts pertinent to your enquiry, the company referred to in my declaration of interest is C L Projects Ltd, (“CLP”) in which I am the registered holder of 50% of the shares. The company has a 50% interest in CLCo, which was a two man partnership between myself and Mr Cook many years ago, but the personal interests we each had in the partnership were transferred to limited companies in 1997/98. These changes came about as a result of Mr Cook’s bankruptcy

Mr Cook states correctly that CLCo derives most of its income from waste disposal into a landfill site, though it also receives payment from an electricity generator on the site, and from a contract farmer. The landfill site was a small area of the farmland and a new lease was issued to the operator to develop more of the surrounding farmland.

Mr Cook is not aware of the other activities of CLP, which holds investments in quoted companies.

ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT 15

His statement that I received £400,000 in a particular year from CLCo is incorrect, see attachment, and so is his assertion that I receive anything like £150,000 a year. I personally receive a rental income of about £25,000 from the partnership, retail price indexed, in respect of the partnership’s lease of Storefield Lodge Farm. I own the freehold of this farm, which is the 390 acres of arable land referred to in my declaration of interest.

Mr Cook says that there is ‘no mention again of his true remunerated employment’. I have no remunerated employment, having taken no salary from CLP, though I may do so in the future. I derive my income from the dividends CLP pays from time to time; rent of the farm; state pension; pensions from previous employments, and personal investments, and I enclose statements from my present and previous accountants setting out the total amounts.

Of course I totally reject the allegation that I have in any way said or done anything that contravened the Code of Conduct, and in particular, the seven principles and paragraphs 7, 8 and 12 which you quote. What Mr Cook seems to be saying is that my indirect interest in the waste disposal operations on my land, through my 50% shareholding in CLP, and that company’s 50% interest in the partnership which in turn leases part of the land to the operators of the waste disposal operator, was material enough to have warranted separate mention, among the other sources of my income. May I respectfully urge you to reject that proposition.

Attachment: Email from Leslie Cox FCA, R E Jones & Co, to Lord Avebury

Following our telephone conversation I am pleased to set out below the share of partnership income attributable to C L Projects Ltd and your personal income.

1. C L Projects:

a. Turnover included the following income from the partnership:

Year ended 31 May 2010 £103,841

Year ended 31 May 2009 £253,567 (the profits for this year were, however, overstated)

Year ended 31 May 2008 £70,535

Year ended 31 May 2007 £50,593

Year ended 31 May 2006 £29,211

b. Actual amounts received from the partnership:

Year ended 31 May 2010 £186,428

Year ended 31 May 2009 £167,500

Year ended 31 May 2008 £47,500

Year ended 31 May 2007 £50,250

Year ended 31 May 2006 £30,000

2. Your personal income from C L Projects Ltd, as declared on your tax returns, has been as follows:

a. Dividends, being 50% of the total:

Year ended 5 April 2010 Gross £25,666.67, Net £23,100

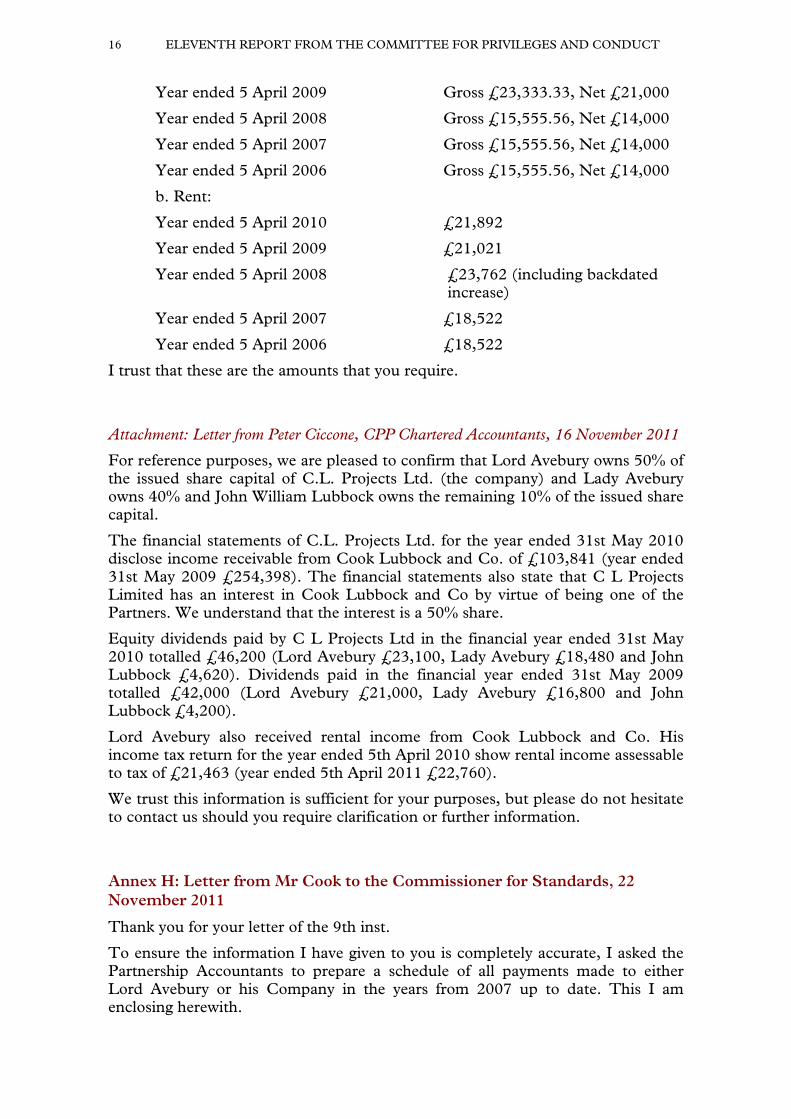

16 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

Year ended 5 April 2009 Gross £23,333.33, Net £21,000

Year ended 5 April 2008 Gross £15,555.56, Net £14,000

Year ended 5 April 2007 Gross £15,555.56, Net £14,000

Year ended 5 April 2006 Gross £15,555.56, Net £14,000

b. Rent:

Year ended 5 April 2010 £21,892

Year ended 5 April 2009 £21,021

Year ended 5 April 2008 £23,762 (including backdated increase)

Year ended 5 April 2007 £18,522

Year ended 5 April 2006 £18,522

I trust that these are the amounts that you require.

Attachment: Letter from Peter Ciccone, CPP Chartered Accountants, 16 November 2011

For reference purposes, we are pleased to confirm that Lord Avebury owns 50% of the issued share capital of C.L. Projects Ltd. (the company) and Lady Avebury owns 40% and John William Lubbock owns the remaining 10% of the issued share capital.

The financial statements of C.L. Projects Ltd. for the year ended 31st May 2010 disclose income receivable from Cook Lubbock and Co. of £103,841 (year ended 31st May 2009 £254,398). The financial statements also state that C L Projects Limited has an interest in Cook Lubbock and Co by virtue of being one of the Partners. We understand that the interest is a 50% share.

Equity dividends paid by C L Projects Ltd in the financial year ended 31st May 2010 totalled £46,200 (Lord Avebury £23,100, Lady Avebury £18,480 and John Lubbock £4,620). Dividends paid in the financial year ended 31st May 2009 totalled £42,000 (Lord Avebury £21,000, Lady Avebury £16,800 and John Lubbock £4,200).

Lord Avebury also received rental income from Cook Lubbock and Co. His income tax return for the year ended 5th April 2010 show rental income assessable to tax of £21,463 (year ended 5th April 2011 £22,760).

We trust this information is sufficient for your purposes, but please do not hesitate to contact us should you require clarification or further information.

Annex H: Letter from Mr Cook to the Commissioner for Standards, 22 November 2011

Thank you for your letter of the 9th inst.

To ensure the information I have given to you is completely accurate, I asked the Partnership Accountants to prepare a schedule of all payments made to either Lord Avebury or his Company in the years from 2007 up to date. This I am enclosing herewith.

ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT 17

You will see that the figures vary to some extent from those I provided with my original complaint. This was partly due to there being a difference between the accounting years for each partner, and I apologise for any difficulties this may cause. However, I do not think it in any way diminishes the basis of my complaint.

Should Lord Avebury dispute these figures, the Accountants have agreed for you to contact them for verification. They have also agreed to maintain complete secrecy until your investigations are complete.

Attachment: Letter from RE Jones & Co, Chartered Accountants, 21 November 2011

As requested I am pleased to enclose the following schedules:

1. Payments to C.L. Projects Limited from January 2007 to October 2011.

The total amounts paid, other than VAT, are in the Net Drawn column, although these figures are split between Consultancy Fees and Drawings in the accounts.

2. Payments to Lord Avebury as Rent.

I trust that these are clear but please do not hesitate to contact me if further explanation is required.

I also enclose a further copy of the accounts for the year ended 31 January 2011 as the original signed copy has not been received by us.

Please sign the front page and return it to me.

[See over the page for schedules]

18 ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT

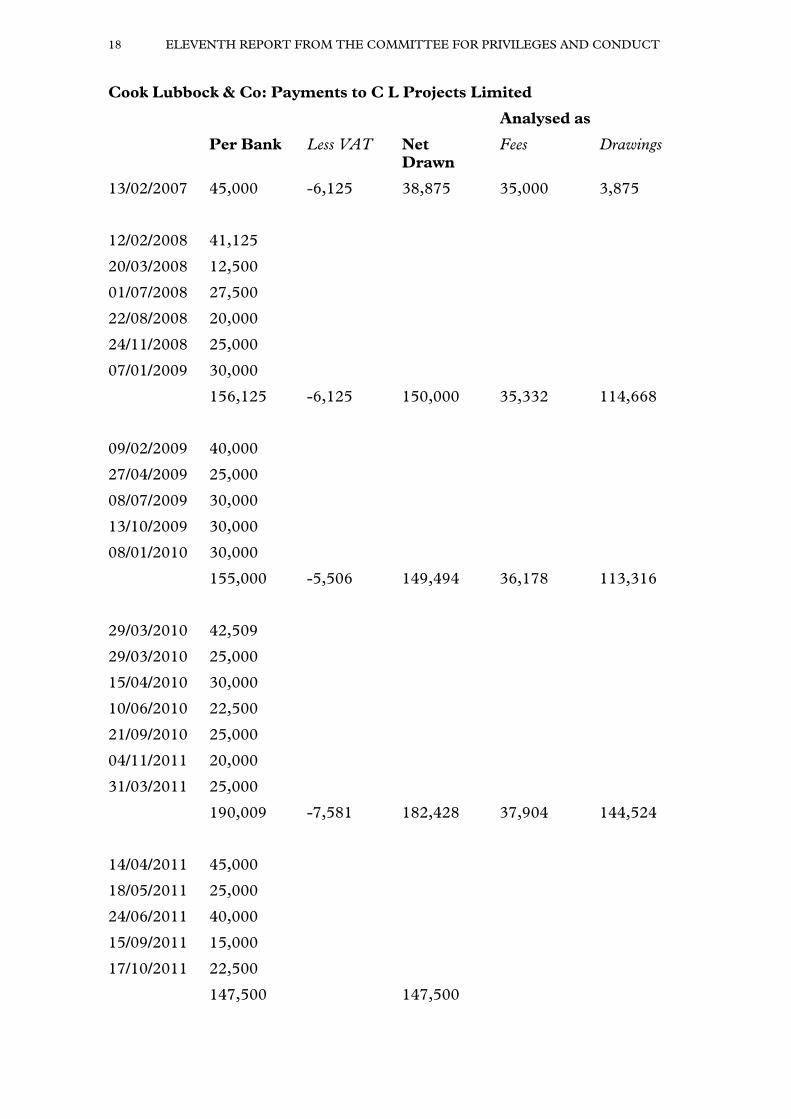

Cook Lubbock & Co: Payments to C L Projects Limited

Analysed as

Per Bank Less VAT Net Drawn

Fees Drawings

13/02/2007 45,000

-6,125 38,875 35,000 3,875

12/02/2008 41,125

20/03/2008 12,500

01/07/2008 27,500

22/08/2008 20,000

24/11/2008 25,000

07/01/2009 30,000

156,125 -6,125 150,000 35,332 114,668

09/02/2009 40,000

27/04/2009 25,000

08/07/2009 30,000

13/10/2009 30,000

08/01/2010 30,000

155,000 -5,506 149,494 36,178 113,316

29/03/2010 42,509

29/03/2010 25,000

15/04/2010 30,000

10/06/2010 22,500

21/09/2010 25,000

04/11/2011 20,000

31/03/2011 25,000

190,009 -7,581 182,428 37,904 144,524

14/04/2011 45,000

18/05/2011 25,000

24/06/2011 40,000

15/09/2011 15,000

17/10/2011 22,500

147,500 147,500

ELEVENTH REPORT FROM THE COMMITTEE FOR PRIVILEGES AND CONDUCT 19

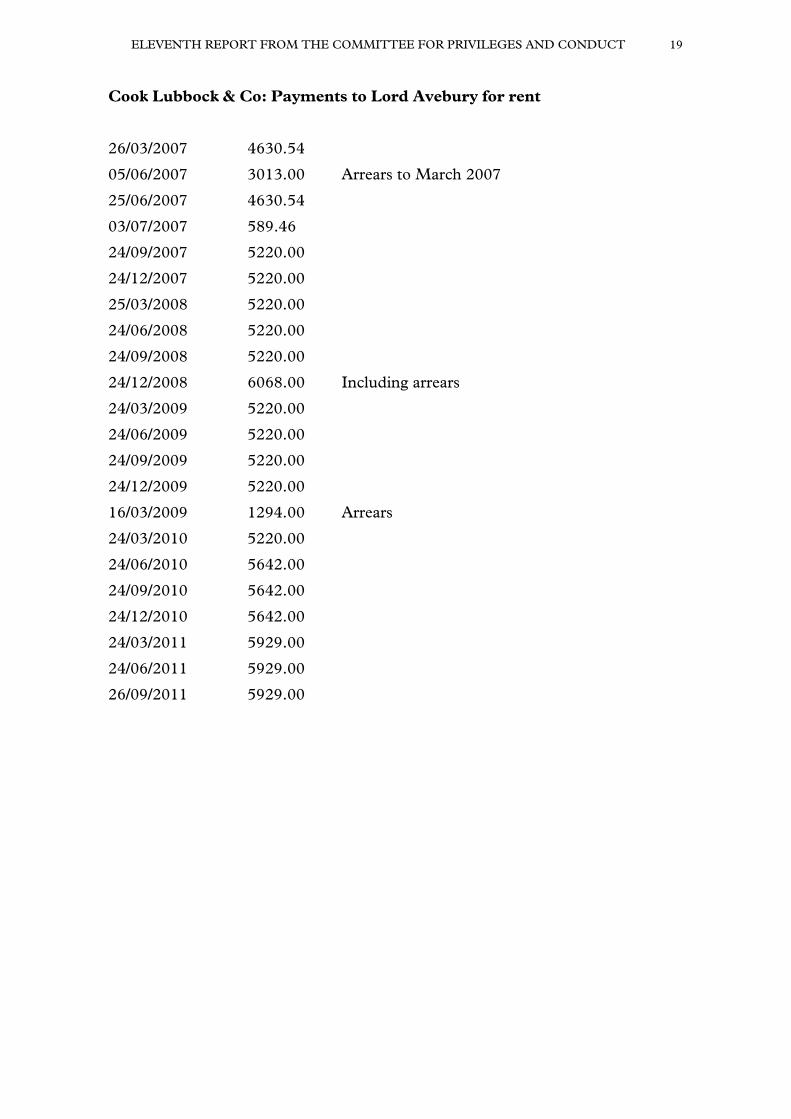

Cook Lubbock & Co: Payments to Lord Avebury for rent

26/03/2007 4630.54

05/06/2007 3013.00 Arrears to March 2007

25/06/2007 4630.54

03/07/2007 589.46

24/09/2007 5220.00

24/12/2007 5220.00

25/03/2008 5220.00

24/06/2008 5220.00

24/09/2008 5220.00

24/12/2008 6068.00 Including arrears

24/03/2009 5220.00

24/06/2009 5220.00

24/09/2009 5220.00

24/12/2009 5220.00

16/03/2009 1294.00 Arrears

24/03/2010 5220.00

24/06/2010 5642.00

24/09/2010 5642.00

24/12/2010 5642.00

24/03/2011 5929.00

24/06/2011 5929.00

26/09/2011 5929.00