Embed Size (px)

DESCRIPTION

The Cost of Doing Business in Africa Evidence from the Investment Climate Survey Data. Vijaya Ramachandran* - PowerPoint PPT Presentation

Citation preview

The Cost of Doing Business in AfricaEvidence from the Investment Climate Survey Data

Vijaya Ramachandran*

*This presentation is based on research jointly carried out with Alan Gelb, Benn Eifert, and Manju Kedia Shah, based on investment climate surveys carried out by the Regional Program on Enterprise Development, Africa Private Sector Group, The World Bank. The views expressed in this presentation are those of the authors, and not necessarily of the institutions they are affiliated with.

Investment Climate Surveys

This presentation is based on research using the World Bank’s Investment Climate Database.

Since 2001, private enterprises in South Africa, Senegal, Mali, Madagascar, Mauritius, Nigeria, Mozambique, Uganda, Kenya, Tanzania, Zambia, Ethiopia, and Eritrea have been surveyed; a sub-sample of these countries is used for this presentation.

Information is collected on cost of production, access to credit, labor, and the business environment (including infrastructure, government regulations, and crime and corruption), for about 400 firms in each country.

The focus of today’s presentation…

In this presentation, I will look at some key aspects of the investment climate, including access to infrastructure and government regulations.

I will argue that “factory-floor” productivity in Africa is not that low compared with China, but when investment climate variables are factored into costs, Africa’s productivity falls to very low levels.

I will also argue that small and indigenous firms face greater constraints, which need to be addressed via targeted interventions.

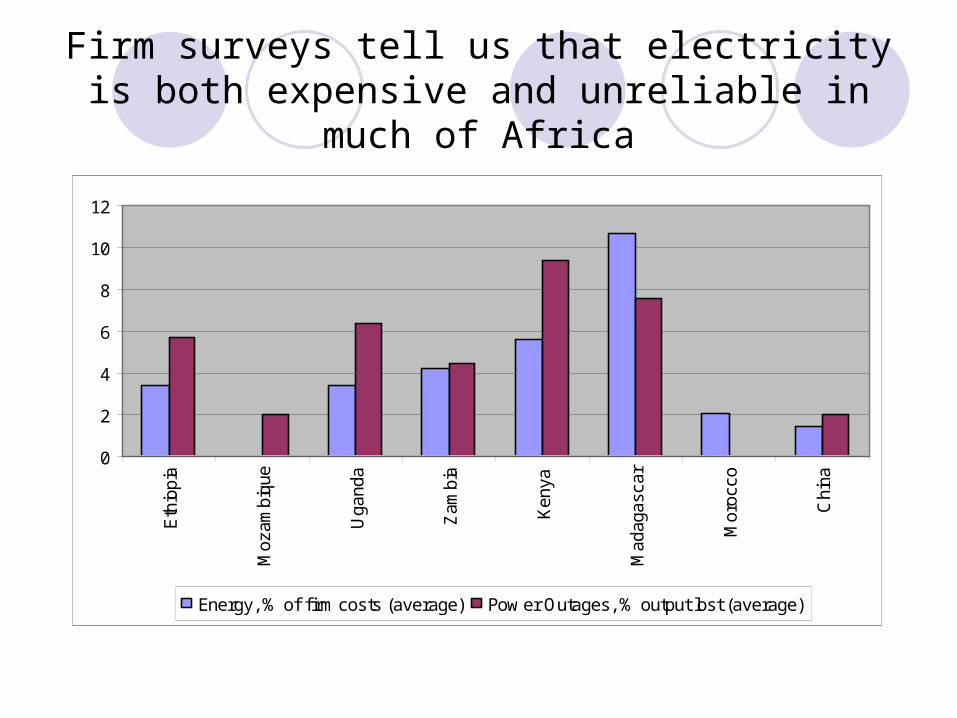

Firm surveys tell us that electricity is both expensive and unreliable in much of Africa

0

2

4

6

8

10

12

Eth

iopi

a

Moz

ambi

que

Uga

nda

Zam

bia

Ken

ya

Mad

agas

car

Mor

occo

Chi

na

Energy, % of f irm costs (average) Pow er Outages, % output lost (average)

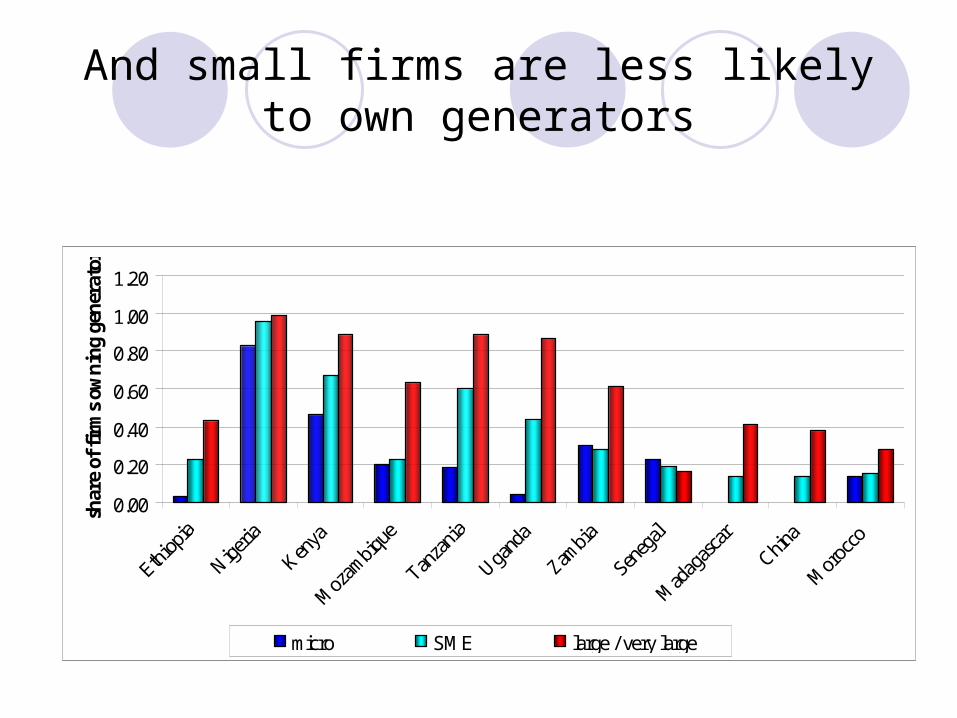

And small firms are less likely to own generators

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Ethiop

ia

Nigeria

Kenya

Moz

ambiq

ue

Tanza

nia

Ugand

a

Zambi

a

Seneg

al

Mad

agas

car

China

Mor

occo

shar

e of

fir

ms

own

ing

gen

erat

or

micro SME large / very large

0

10

20

30

40

50

60

Phone lines Electricityconnection

Water connection

The waiting time for utility connections is very long in Africa compared to China….

(median value in days, in the past 2 years)

Kenya

Tanzania

Uganda

Zambia

China

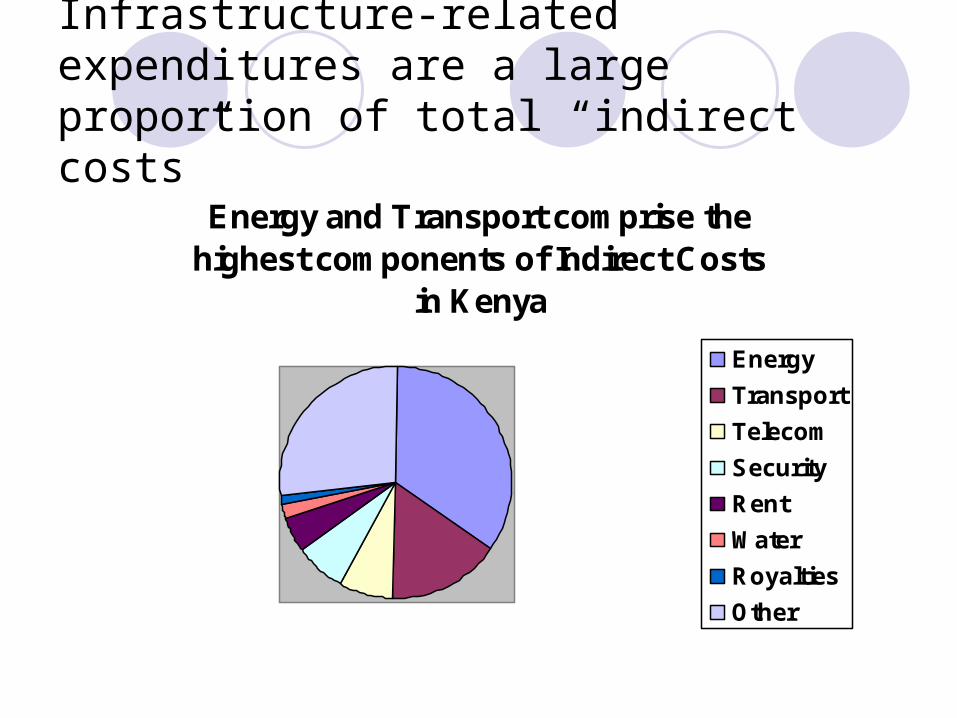

Infrastructure-related expenditures are a large proportion of total “indirect costs”

Energy and Transport comprise the highest components of Indirect Costs

in Kenya

Energy

Transport

Telecom

Security

Rent

Water

Royalties

Other

The time to clear goods at port is several days in many countries in Africa

02468

101214161820

Ethiop

ia

Moz

ambiq

ue

Nigeria

Ugand

a

Zambia

Kenya

Mad

agas

car

Mor

occo

China

India

Days to clear imports, median Days to clear exports, median

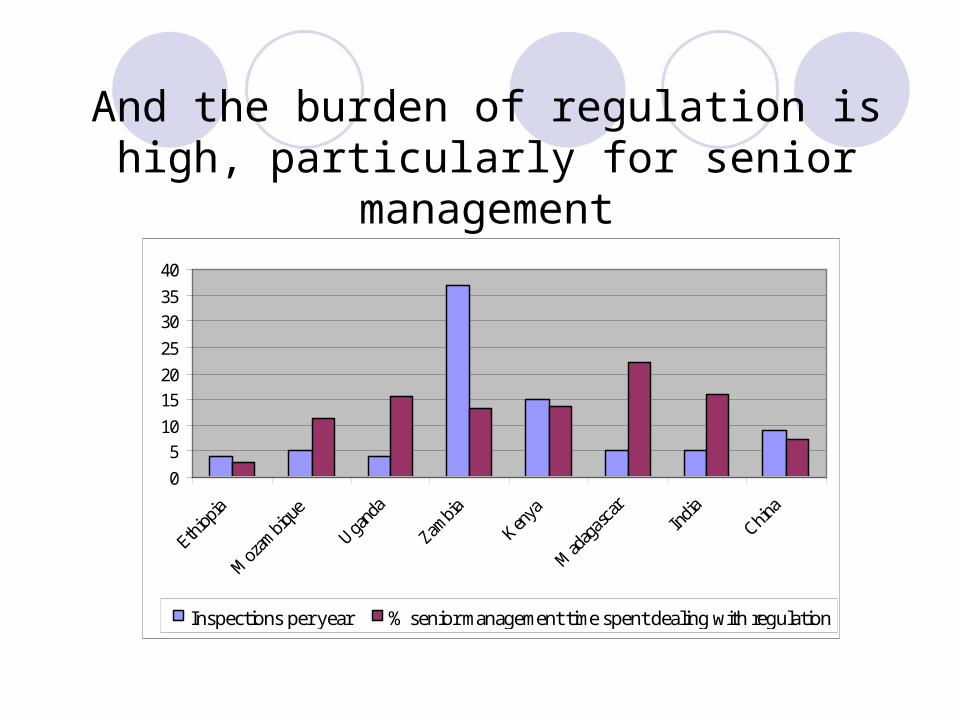

And the burden of regulation is high, particularly for senior management

0

5

10

15

20

25

30

35

40

Inspections per year % senior management time spent dealing with regulation

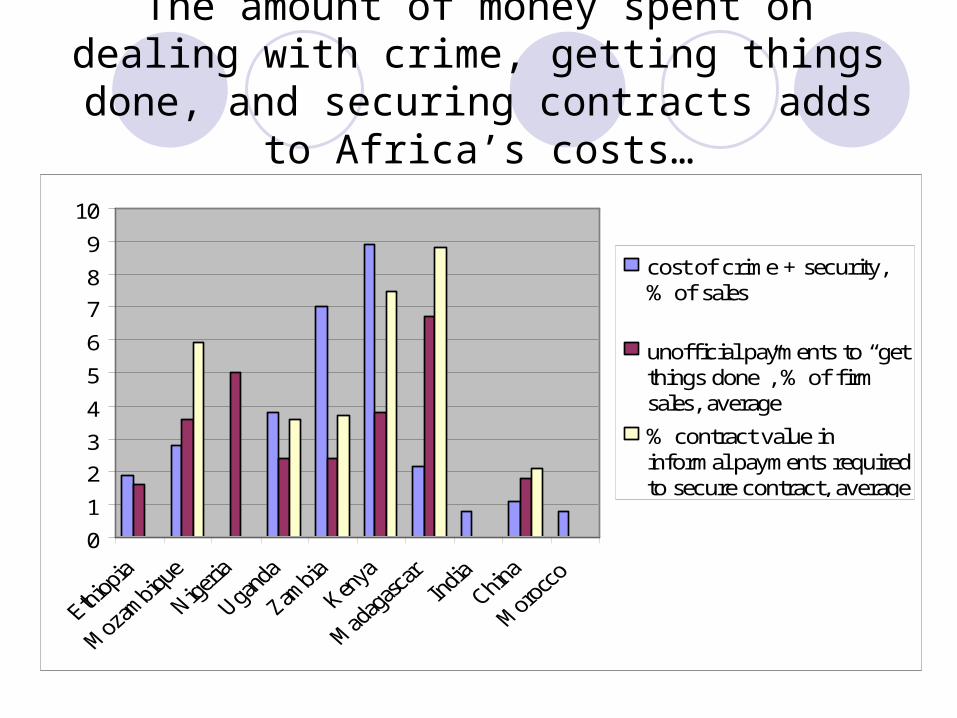

The amount of money spent on dealing with crime, getting things done, and securing

contracts adds to Africa’s costs…

Unofficial Payments and Informal Payments

0

1

2

3

4

5

6

7

8

9

10

cost of crime + security,% of sales

unofficial payments to “getthings done”, % of firmsales, average

% contract value ininformal payments requiredto secure contract, average

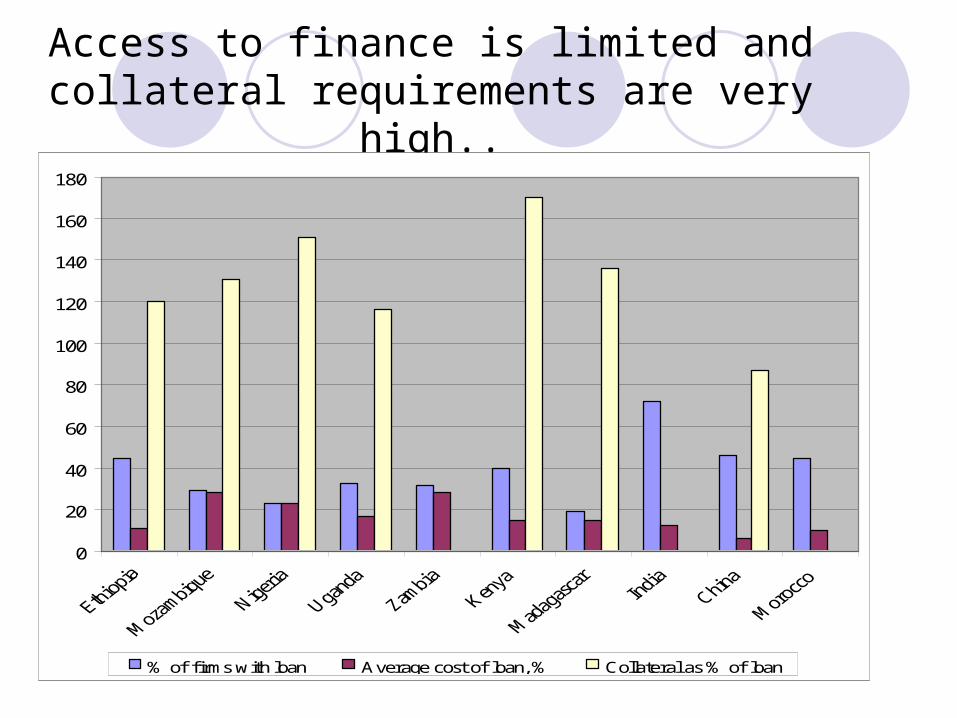

Access to finance is limited and collateral requirements are very high..

0

20

40

60

80

100

120

140

160

180

% of firms with loan Average cost of loan, % Collateral as % of loan

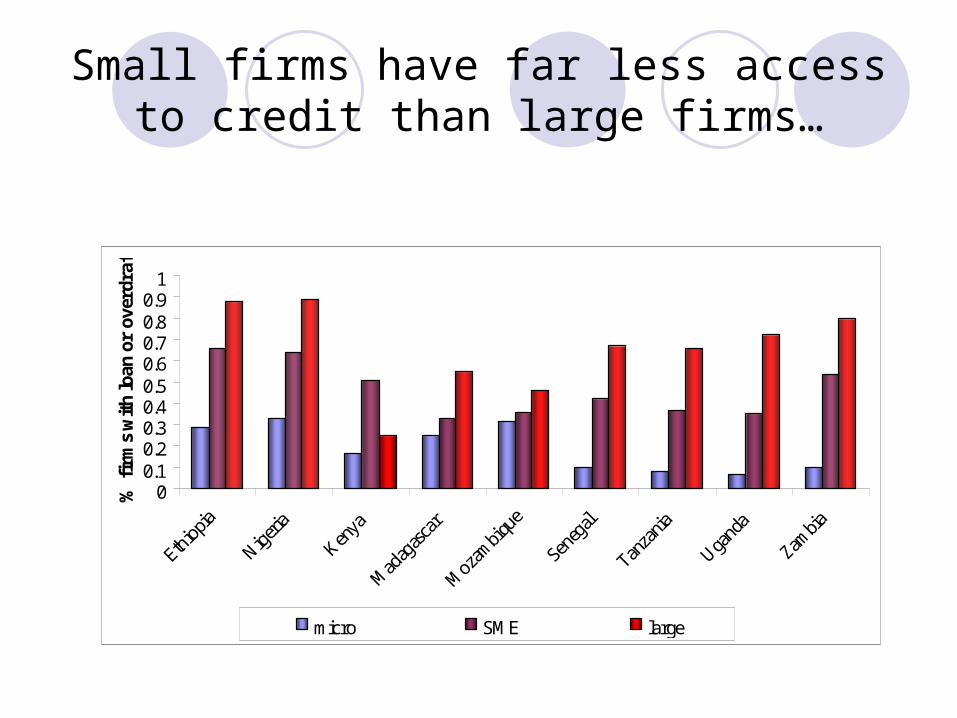

Small firms have far less access to credit than large firms…

00.10.20.30.40.50.60.70.80.9

1

Ethio

pia

Nigeri

a

Kenya

Mad

agas

car

Moza

mbi

que

Seneg

al

Tanza

nia

Uganda

Zambia

% f

irm

s w

ith

loan

or

over

draf

t

micro SME large

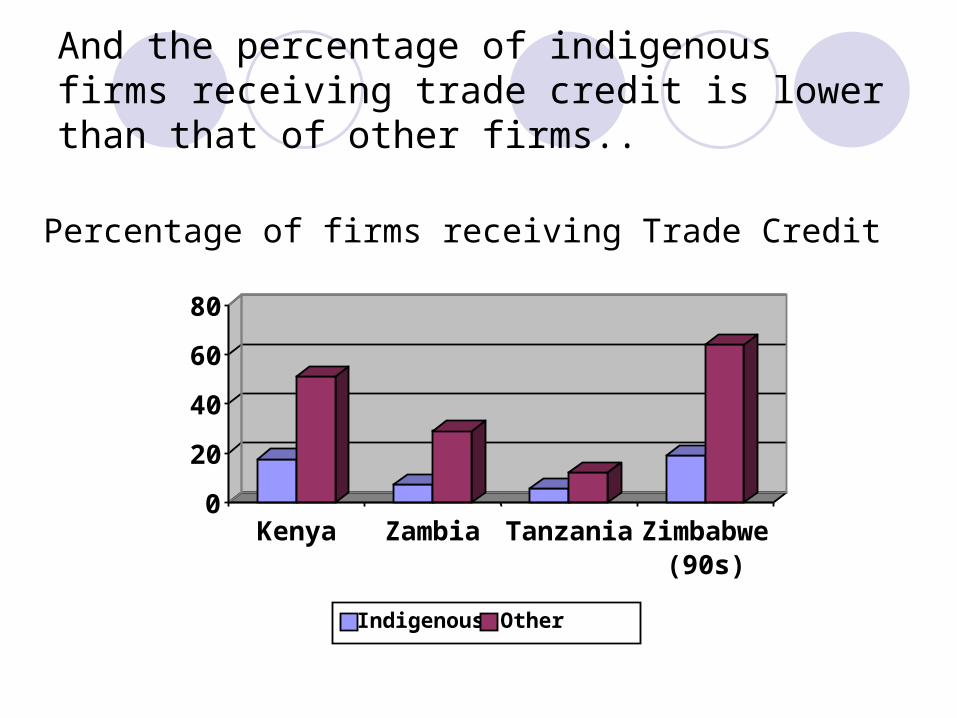

And the percentage of indigenous firms receiving trade credit is lower than that of other firms..

0

20

40

60

80

Kenya Zambia Tanzania Zimbabwe(90s)

Percentage of firms receiving Trade Credit

Indigenous Other

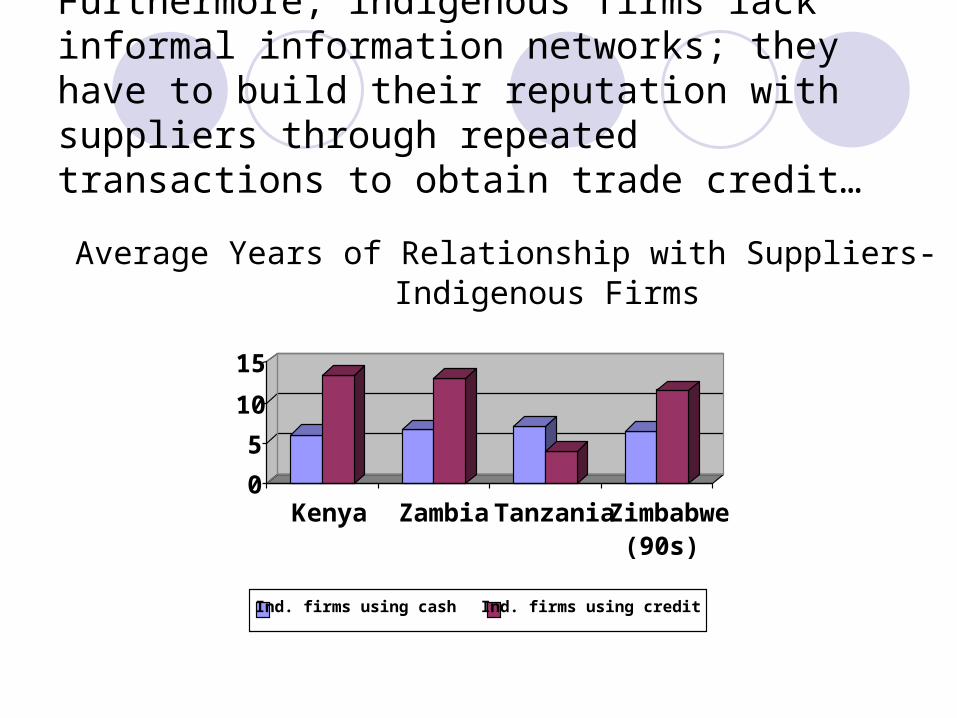

Furthermore, indigenous firms lack informal information networks; they have to build their reputation with suppliers through repeated transactions to obtain trade credit…

0

5

10

15

Kenya Zambia TanzaniaZimbabwe(90s)

Average Years of Relationship with Suppliers- Indigenous Firms

Ind. firms using cash Ind. firms using credit

What are the consequences of these investment climate characteristics for the African private sector?

Let us look at the impact on the productivity of firms, measuring Africa in comparative perspective…

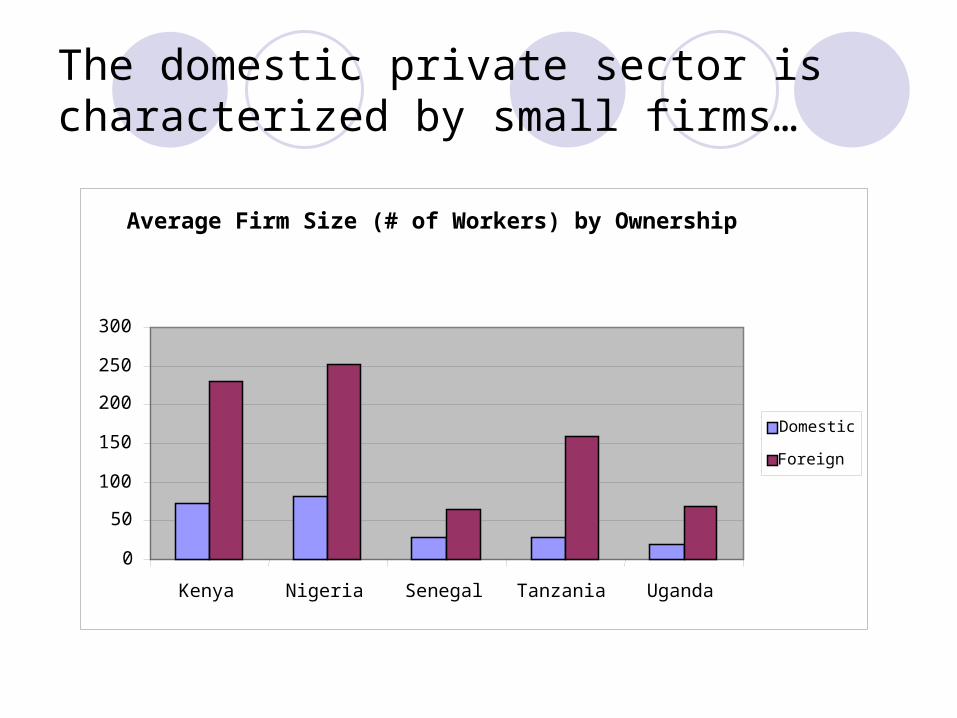

The domestic private sector is characterized by small firms…

Average Firm Size (# of Workers) by Ownership

0

50

100

150

200

250

300

Kenya Nigeria Senegal Tanzania Uganda

Domestic

Foreign

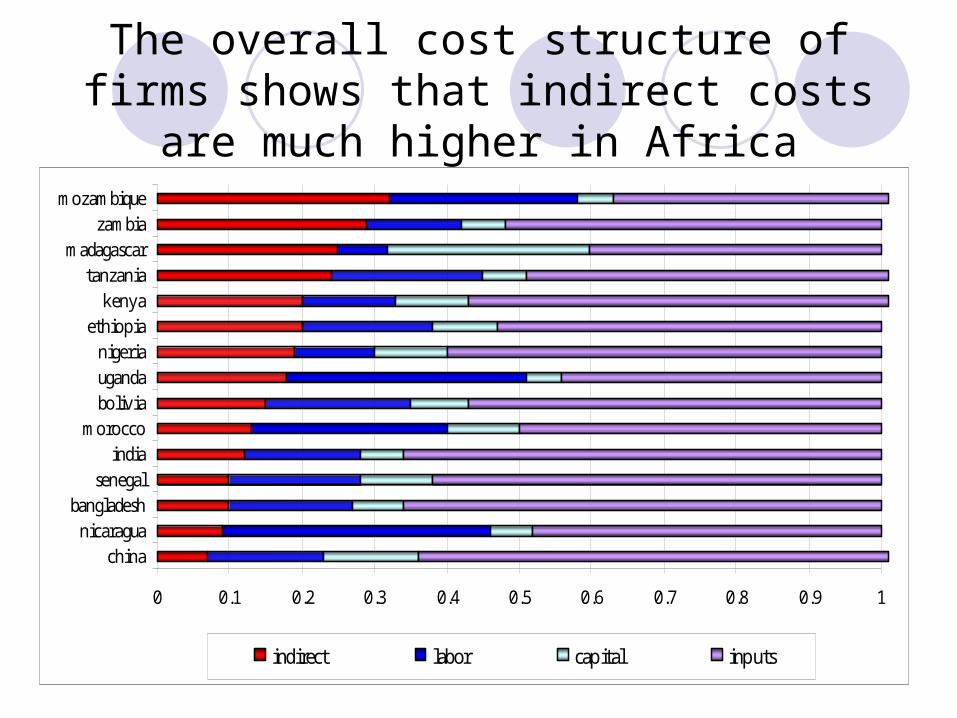

The overall cost structure of firms shows that indirect costs are much higher in Africa

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

chinanicaragua

bangladeshsenegal

indiamorocco

boliviaugandanigeria

ethiopiakenya

tanzaniamadagascar

zambiamozambique

indirect labor capital inputs

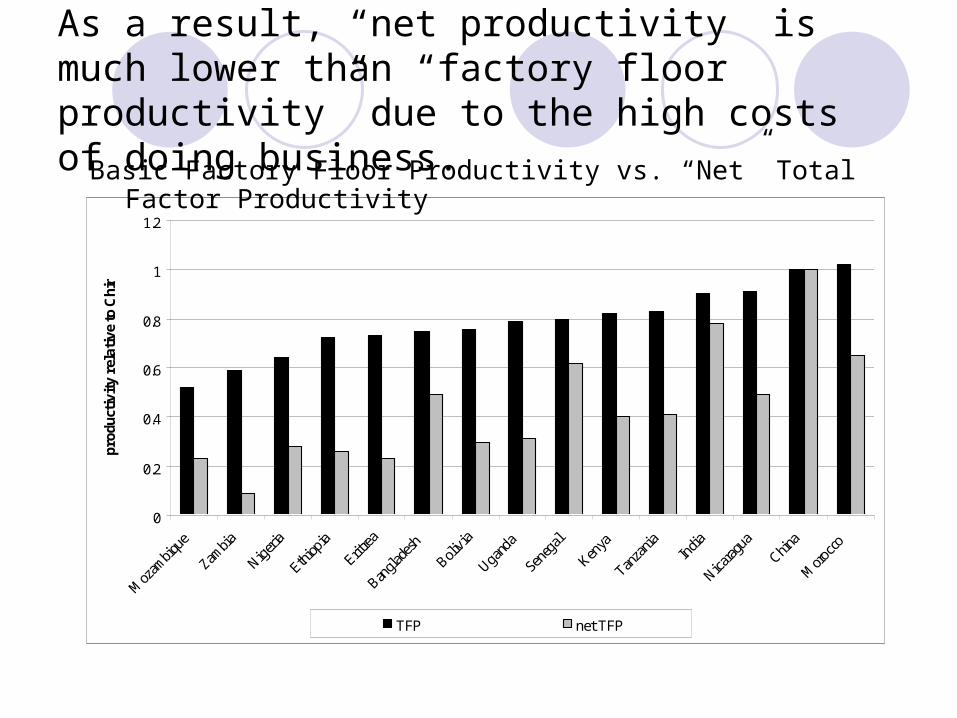

As a result, “net productivity” is much lower than “factory floor productivity” due to the high costs of doing business.

0

0.2

0.4

0.6

0.8

1

1.2

Moz

ambiq

ue

Zambia

Nigeri

a

Ethiop

ia

Eritrea

Bangla

desh

Bolivia

Uganda

Seneg

al

Kenya

Tanza

niaIn

dia

Nicarag

uaChin

a

Moro

cco

prod

ucti

vity

rel

ativ

e to

Chi

na

TFP net TFP

Basic Factory Floor Productivity vs. “Net” Total Factor Productivity

What are some of the key interventions that are necessary to raise productivity in Africa?

Scaling up infrastructure, to lower energy and transport costs, will benefit ALL firms.

Of particular interest is the INGA hydropower scheme, led by Eskom and other utility companies.

Advantage of low-cost labor often offset by poor power supply, resulting in investors going elsewhere—we need more generating capacity.

Improving Access to Finance

Targeted interventions towards helping small and medium sized firms get access to loans (e.g. the World Bank/IFC Small and Medium Enterprise Project or the very innovative kiva.org)

Increasing access to finance by creating credit bureaus or other mechanisms by which firms can be properly evaluated.

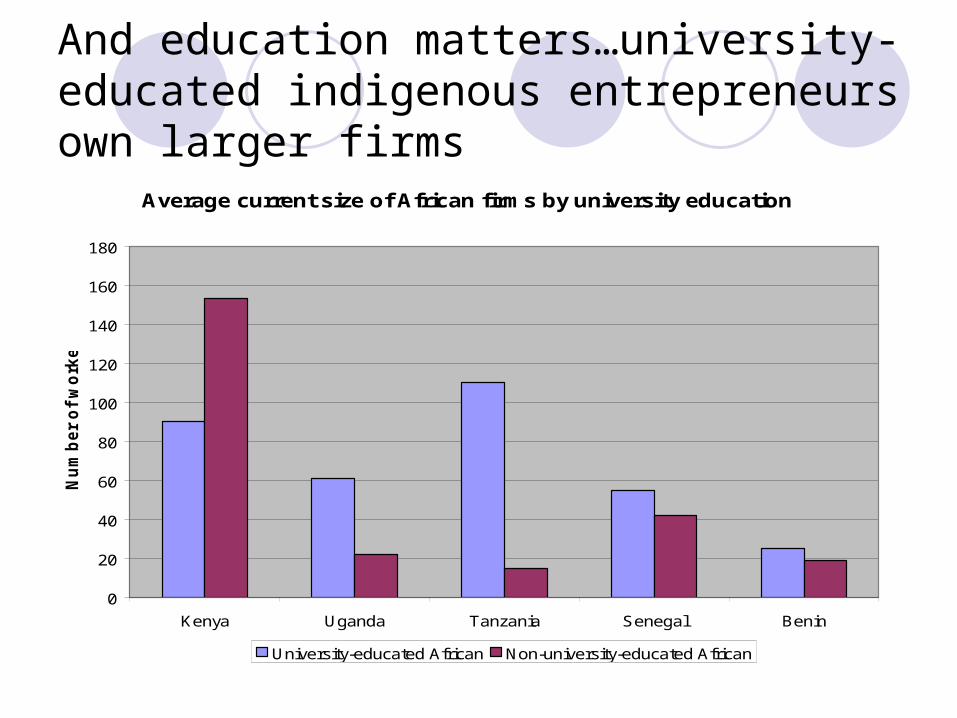

And education matters…university-educated indigenous entrepreneurs own larger firms

Average current size of African firms by university education

0

20

40

60

80

100

120

140

160

180

Kenya Uganda Tanzania Senegal Benin

Nu

mb

er

of

wo

rkers

University-educated African Non-university-educated African

Education Matters…

The International Finance Corporation has launched the Global Business School Network--a public-private partnership to strengthen and expand managerial education in Africa and elsewhere (http://www.ifc.org/gbsn)

Institutions such as WPI can play a role in training entrepreneurs

We have also found that relevant training, provided by the firm, increases productivity

Conclusion

The importance and centrality of the private sector must be continuously stressed by the various parties involved in African development.

We need unwavering government commitment, active private sector participation, and engagement by researchers, donors, and civil society.

For more information, please visit www.worldbank.org/rped