Embed Size (px)

Citation preview

The East Asian Crisis:Causes and Effects

Joseph E. StiglitzSenior Vice President and Chief Economist,

World Bank

Outline of the Talk

I. Key Aspects of the East Asian Crisis

II. Prospects for East Asia

III. Impact on the U.S. Economy

IV. Impact on Developing Countries

Key Aspects of the East Asian Crisis

1. Not public sector profligacy, but private sector borrowing.

2. Not overall indebtedness, but the type of borrowing and use of funds.

3. Not just borrowers, but also lenders.

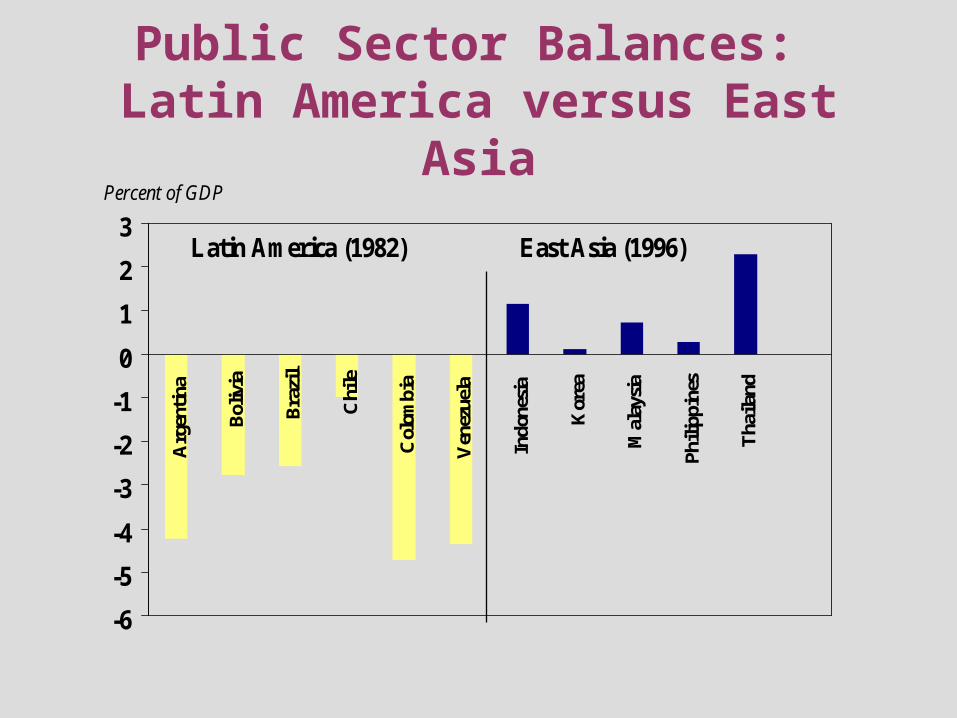

Public Sector Balances: Latin America versus East Asia

-6

-5

-4

-3

-2

-1

0

1

2

3

Arg

entin

a

Bol

ivia

Bra

zil

Chi

le

Col

ombi

a

Ven

ezue

la

Indo

nesi

a

Kor

ea

Mal

aysi

a

Phili

ppin

es

Tha

iland

Latin America (1982) East Asia (1996)

Percent of GDP

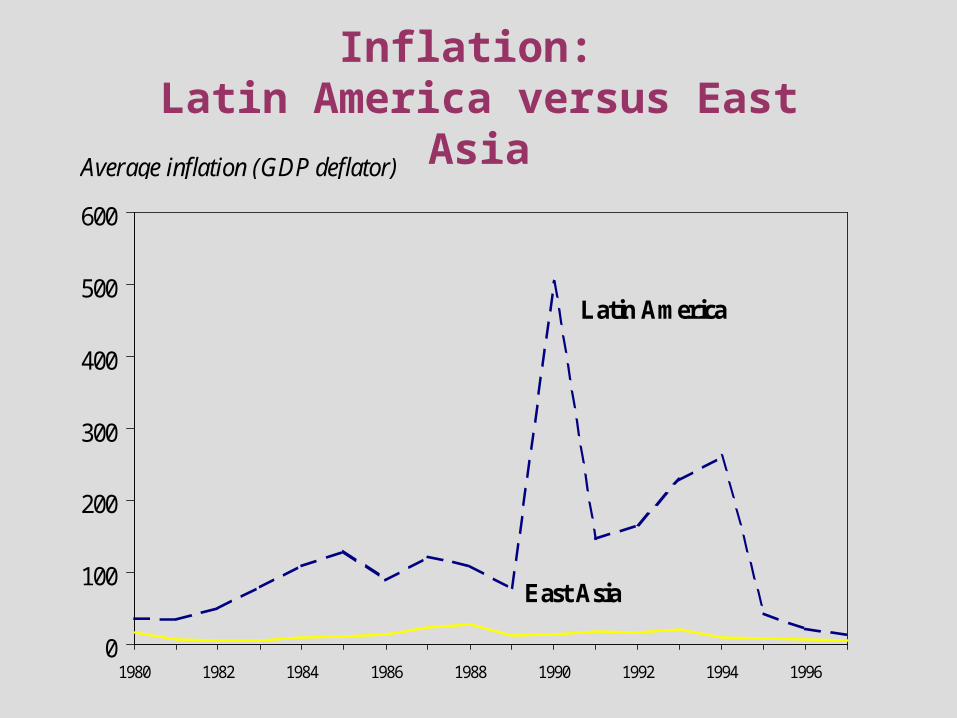

Inflation: Latin America versus East Asia

0

100

200

300

400

500

600

1980 1982 1984 1986 1988 1990 1992 1994 1996

Latin America

East Asia

Average inflation (GDP deflator)

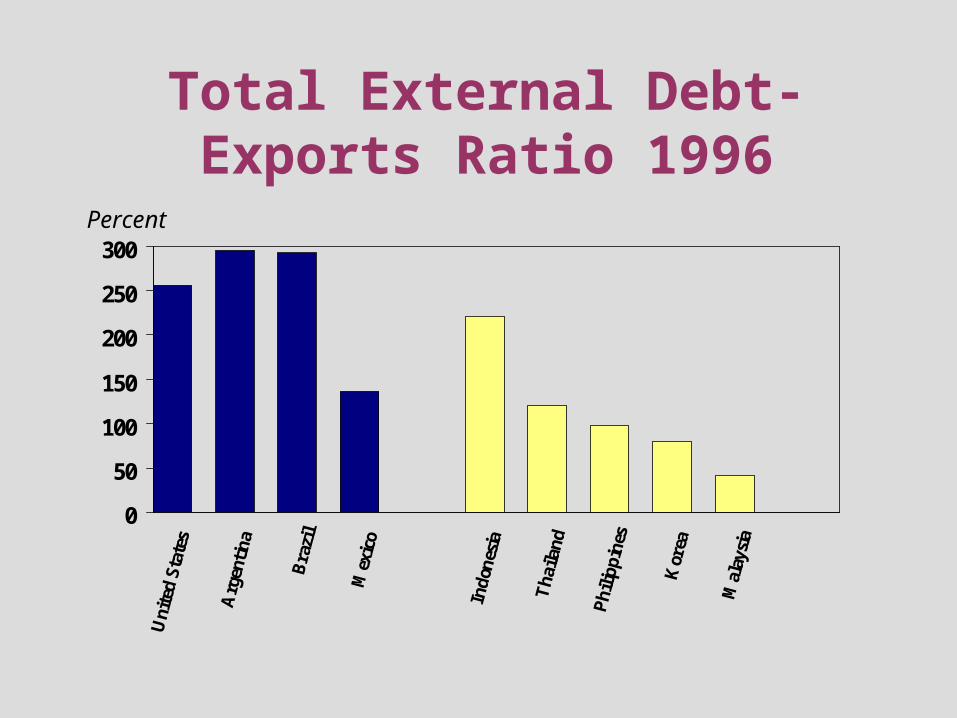

Total External Debt-Exports Ratio 1996

0

50

100

150

200

250

300

Uni

ted

Stat

es

Arg

enti

na

Bra

zil

Mex

ico

Indo

nesi

a

Tha

iland

Phi

lippi

nes

Kor

ea

Mal

aysi

a

Percent

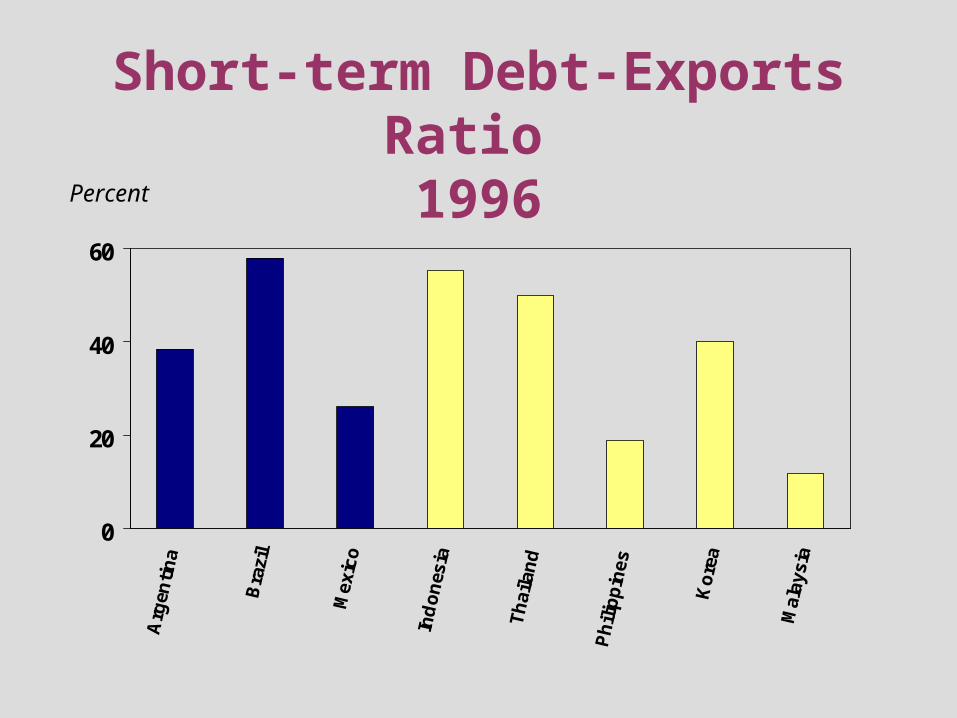

Short-term Debt-Exports Ratio 1996

0

20

40

60

Arg

enti

na

Bra

zil

Mex

ico

Ind

on

esia

Th

aila

nd

Ph

ilip

pin

es

Ko

rea

Mal

aysi

a

Percent

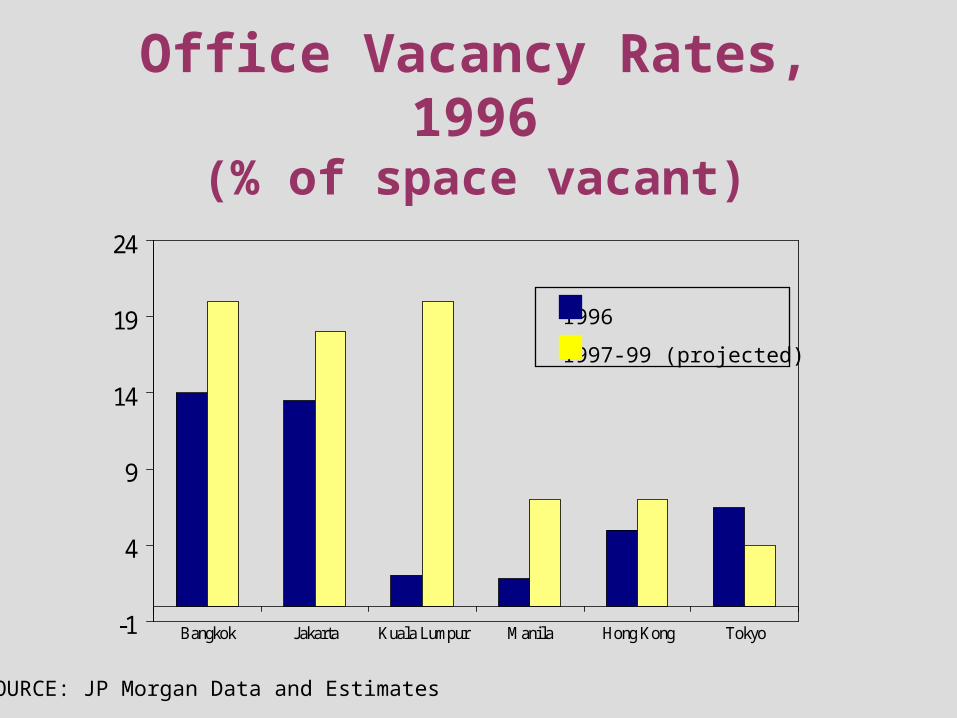

Office Vacancy Rates, 1996(% of space vacant)

-1

4

9

14

19

24

Bangkok Jakarta Kuala Lumpur Manila Hong Kong Tokyo

SOURCE: JP Morgan Data and Estimates

1996

1997-99 (projected)

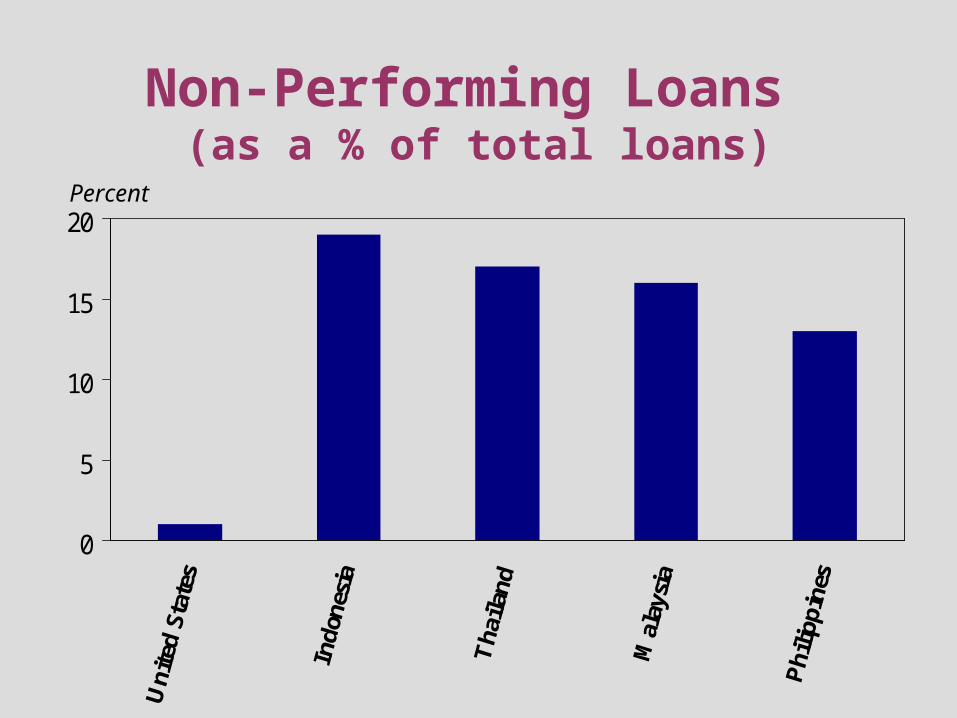

Non-Performing Loans (as a % of total loans)

0

5

10

15

20Percent

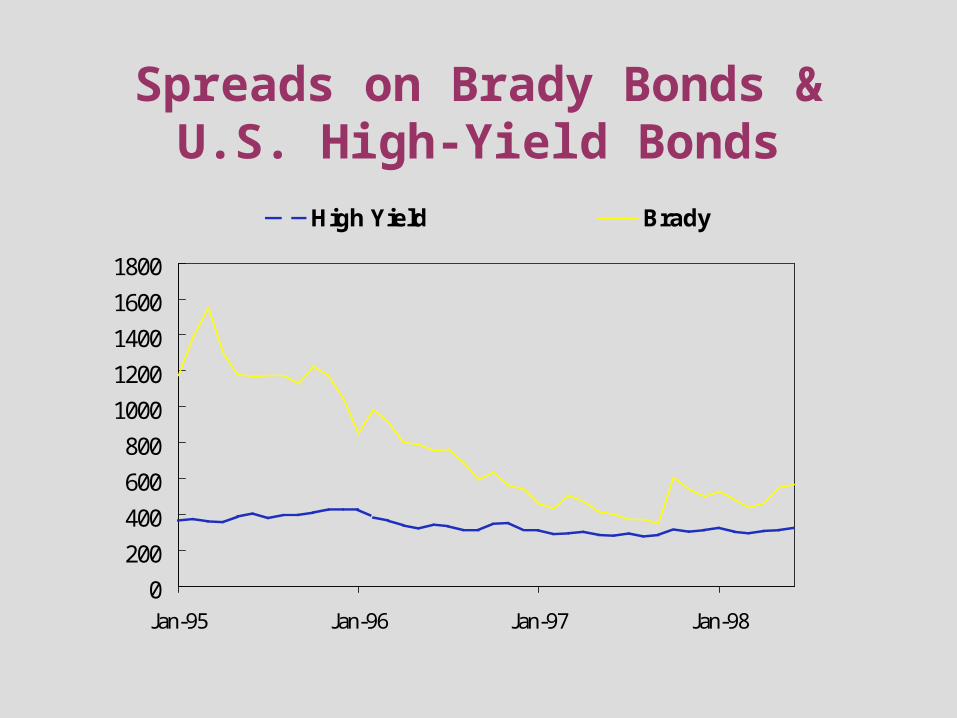

Spreads on Brady Bonds & U.S. High-Yield Bonds

0

200

400

600

800

1000

1200

1400

1600

1800

Jan-95 Jan-96 Jan-97 Jan-98

High Yield Brady

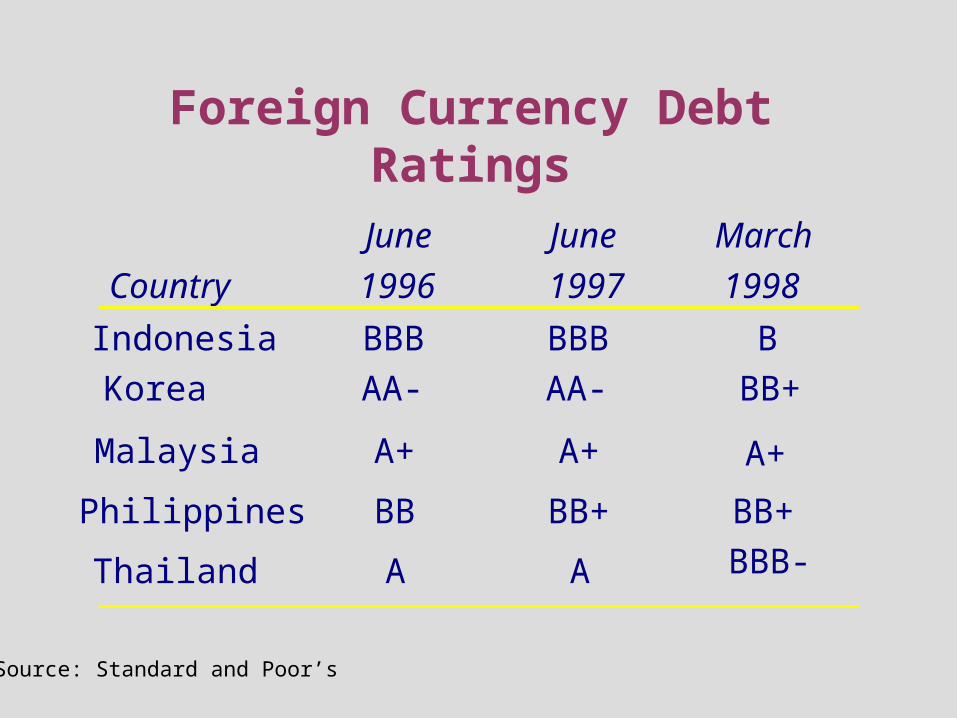

Foreign Currency Debt Ratings

Country

June

1996

June

1997

March

1998

Indonesia BBB BBB B

Korea AA- AA- BB+

Malaysia A+ A+ A+

Philippines BB BB+ BB+

Thailand A A BBB-

Source: Standard and Poor’s

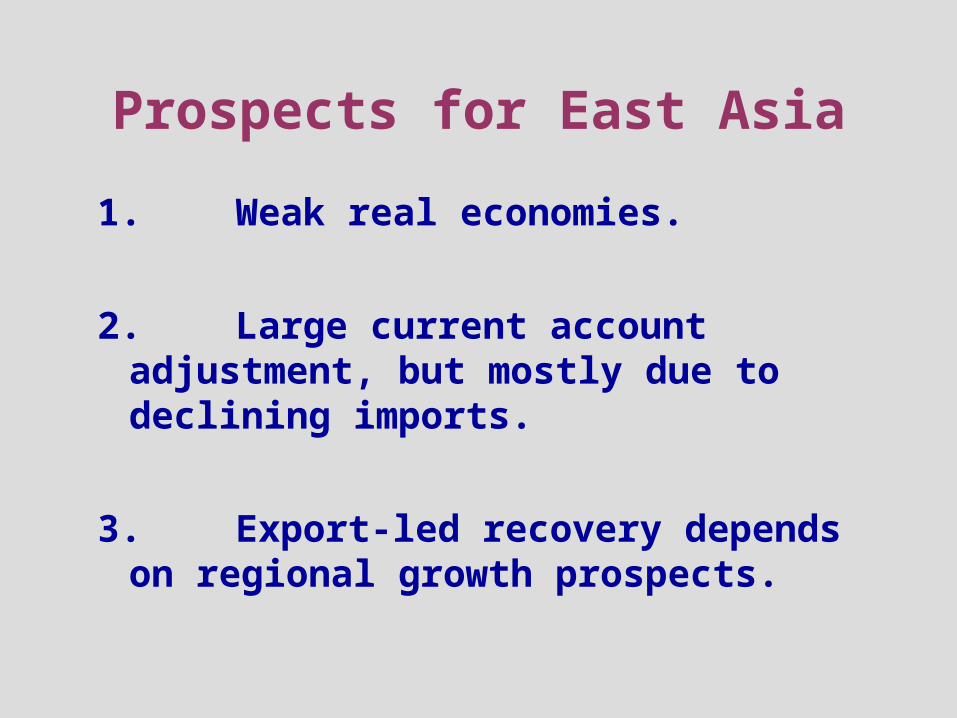

Prospects for East Asia

1. Weak real economies.

2. Large current account adjustment, but mostly due to declining imports.

3. Export-led recovery depends on regional growth prospects.

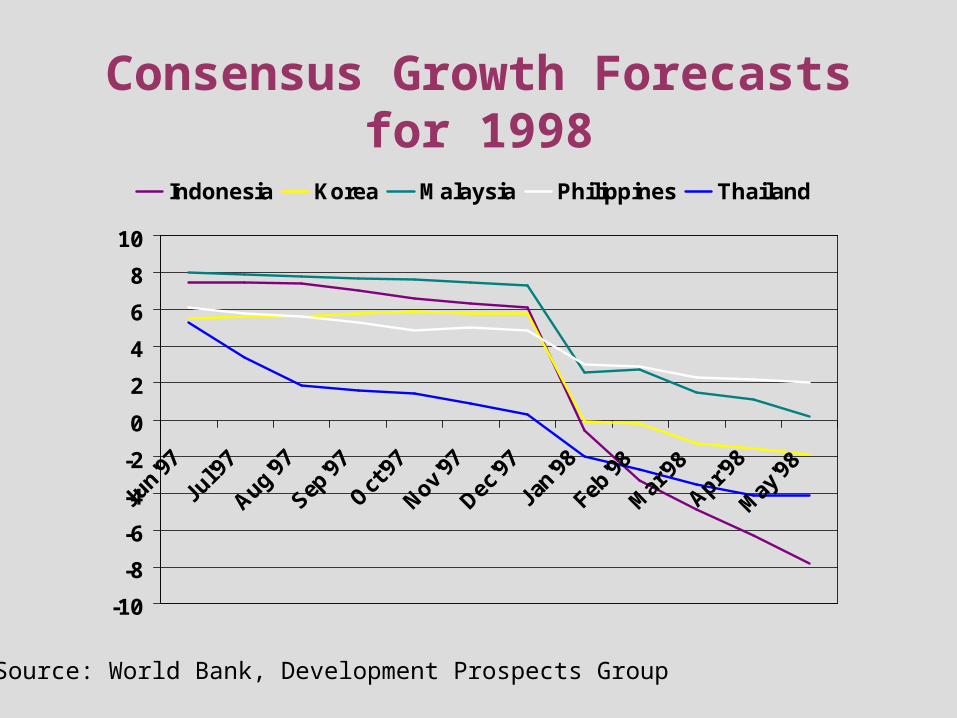

Consensus Growth Forecasts for 1998

-10

-8

-6

-4

-2

0

2

4

6

8

10

Jun'97

Jul'9

7

Aug'97

Sep'9

7

Oct'97

Nov'97

Dec'9

7

Jan'9

8

Feb'98

Mar

'98

Apr'98

May

'98

Indonesia Korea Malaysia Philippines Thailand

Source: World Bank, Development Prospects Group

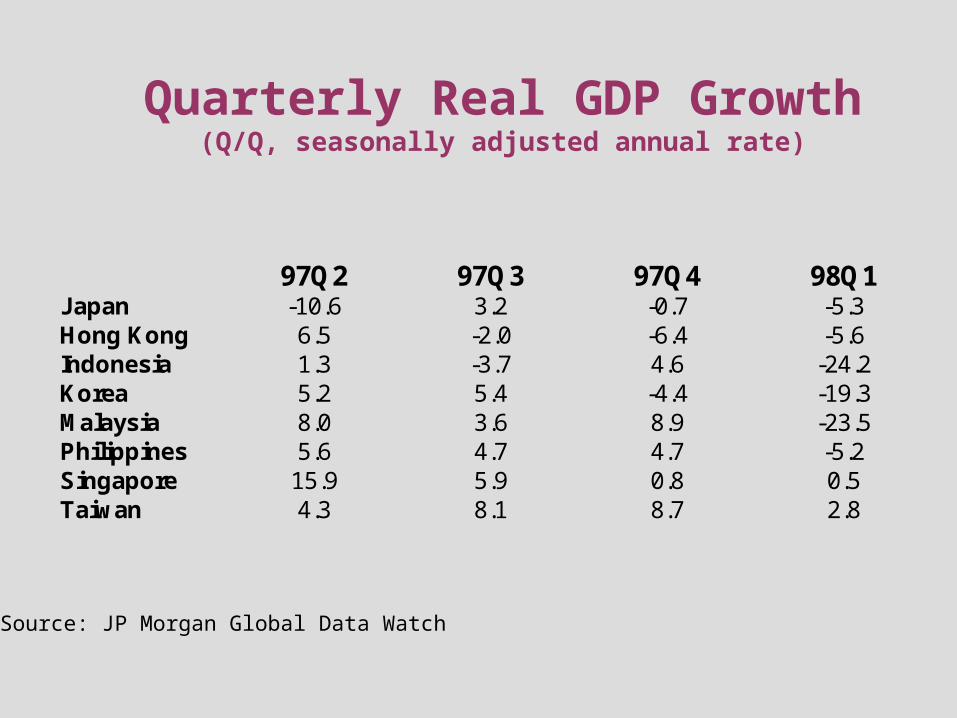

Quarterly Real GDP Growth(Q/Q, seasonally adjusted annual rate)

Source: JP Morgan Global Data Watch

97Q2 97Q3 97Q4 98Q1Japan -10.6 3.2 -0.7 -5.3Hong Kong 6.5 -2.0 -6.4 -5.6Indonesia 1.3 -3.7 4.6 -24.2Korea 5.2 5.4 -4.4 -19.3Malaysia 8.0 3.6 8.9 -23.5Philippines 5.6 4.7 4.7 -5.2Singapore 15.9 5.9 0.8 0.5Taiwan 4.3 8.1 8.7 2.8

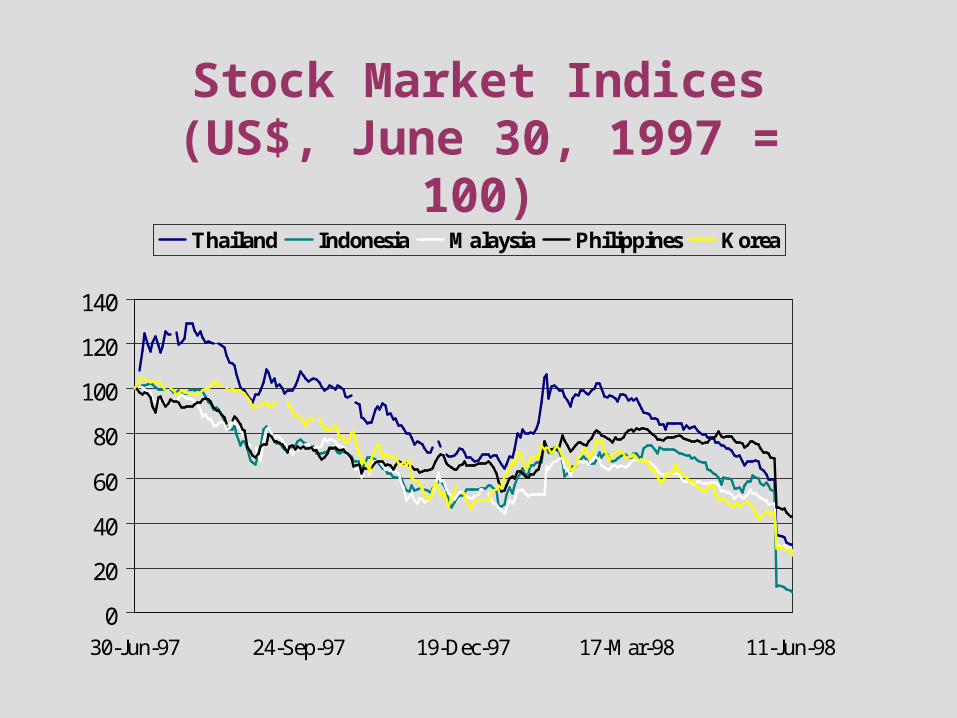

Stock Market Indices(US$, June 30, 1997 = 100)

0

20

40

60

80

100

120

140

30-Jun-97 24-Sep-97 19-Dec-97 17-Mar-98 11-Jun-98

Thailand Indonesia Malaysia Philippines Korea

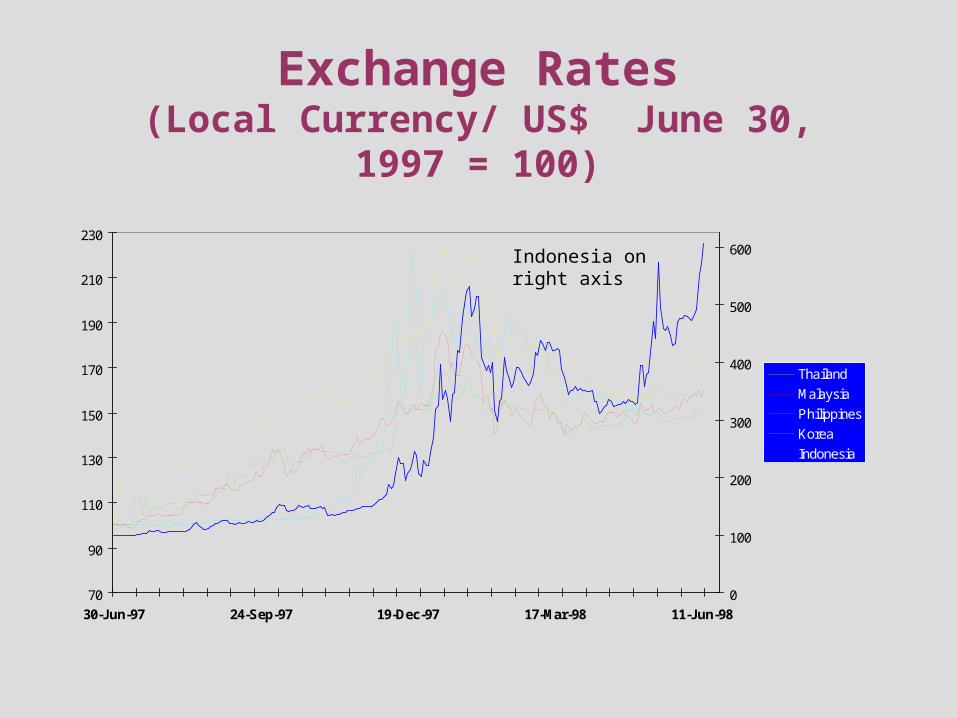

Exchange Rates(Local Currency/ US$ June 30, 1997 = 100)

70

90

110

130

150

170

190

210

230

30-Jun-97 24-Sep-97 19-Dec-97 17-Mar-98 11-Jun-98

0

100

200

300

400

500

600

Thailand

Malaysia

Philippines

Korea

Indonesia

Indonesia on right axis

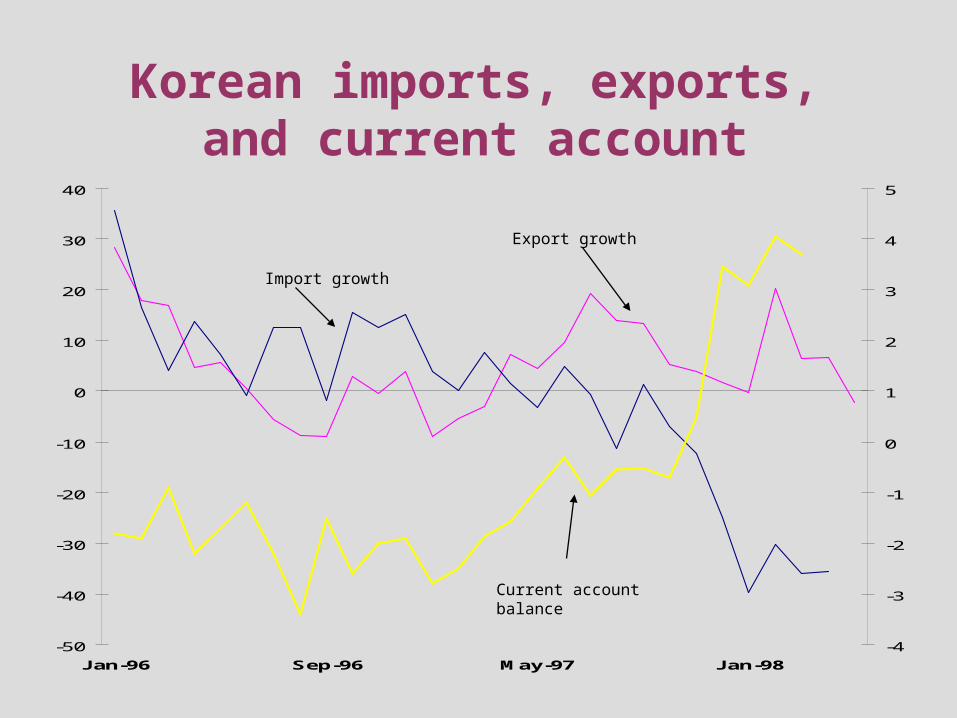

Korean imports, exports, and current account

-50

-40

-30

-20

-10

0

10

20

30

40

Jan-96 Sep-96 May-97 Jan-98

-4

-3

-2

-1

0

1

2

3

4

5

Import growth

Export growth

Current account balance

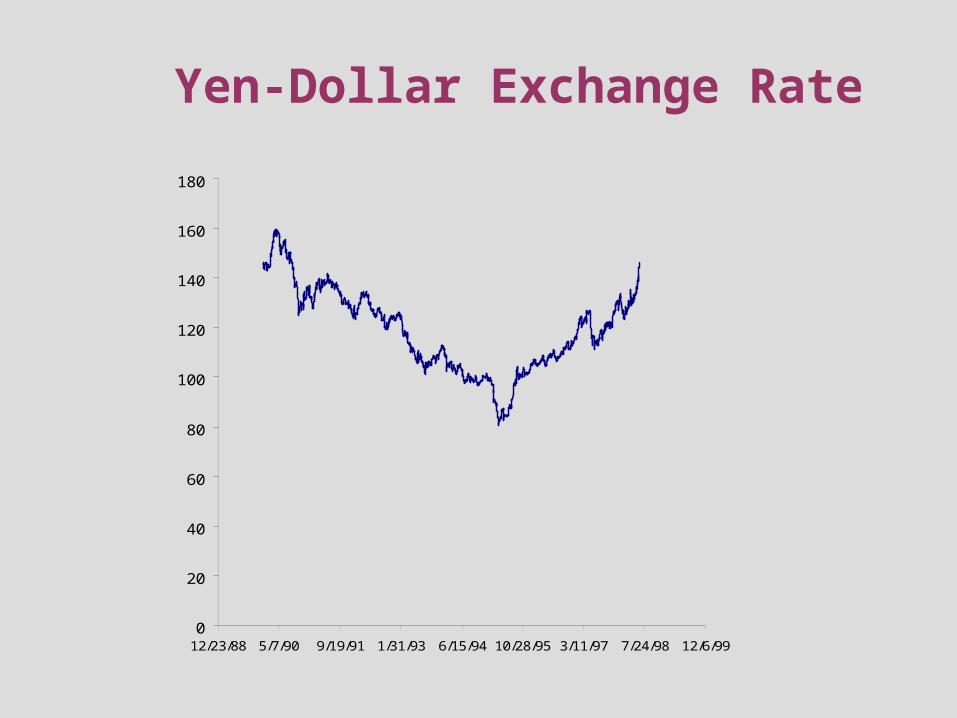

Yen-Dollar Exchange Rate

0

20

40

60

80

100

120

140

160

180

12/23/88 5/7/90 9/19/91 1/31/93 6/15/94 10/28/95 3/11/97 7/24/98 12/6/99

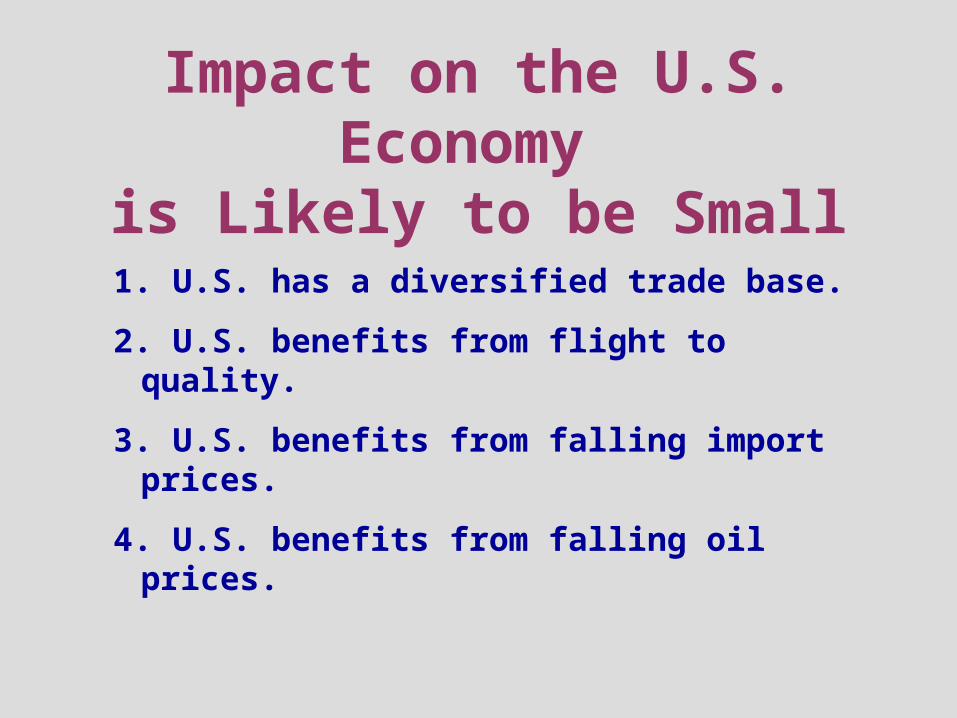

1. U.S. has a diversified trade base.

2. U.S. benefits from flight to quality.

3. U.S. benefits from falling import prices.

4. U.S. benefits from falling oil prices.

Impact on the U.S. Economy is Likely to be Small

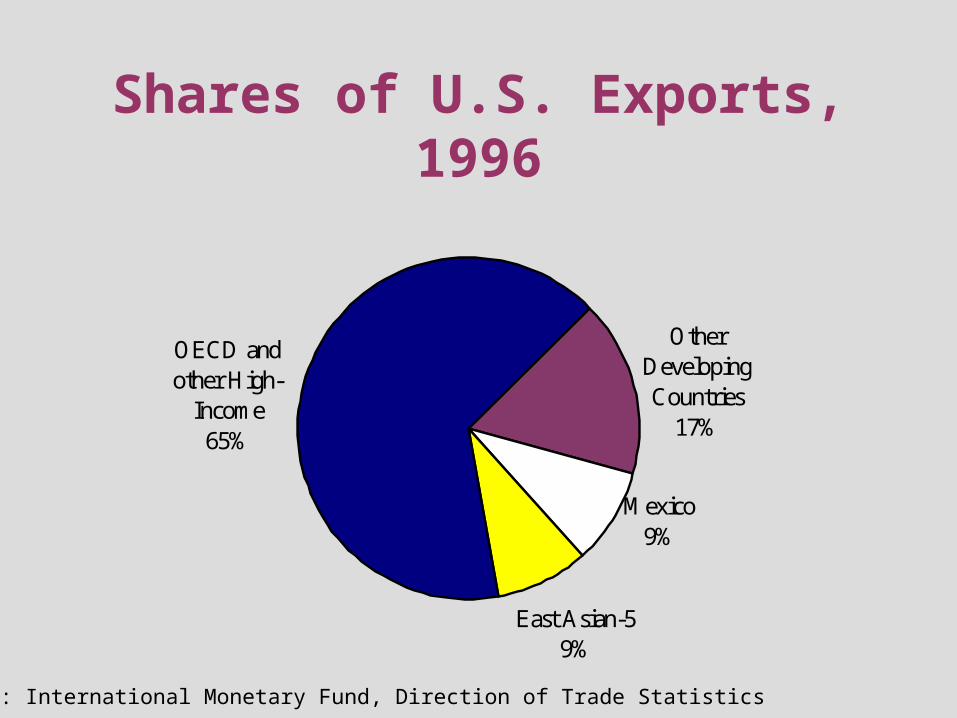

Shares of U.S. Exports, 1996

Other Developing Countries

17%

Mexico9%

East Asian-59%

OECD and other High-

Income65%

SOURCE: International Monetary Fund, Direction of Trade Statistics

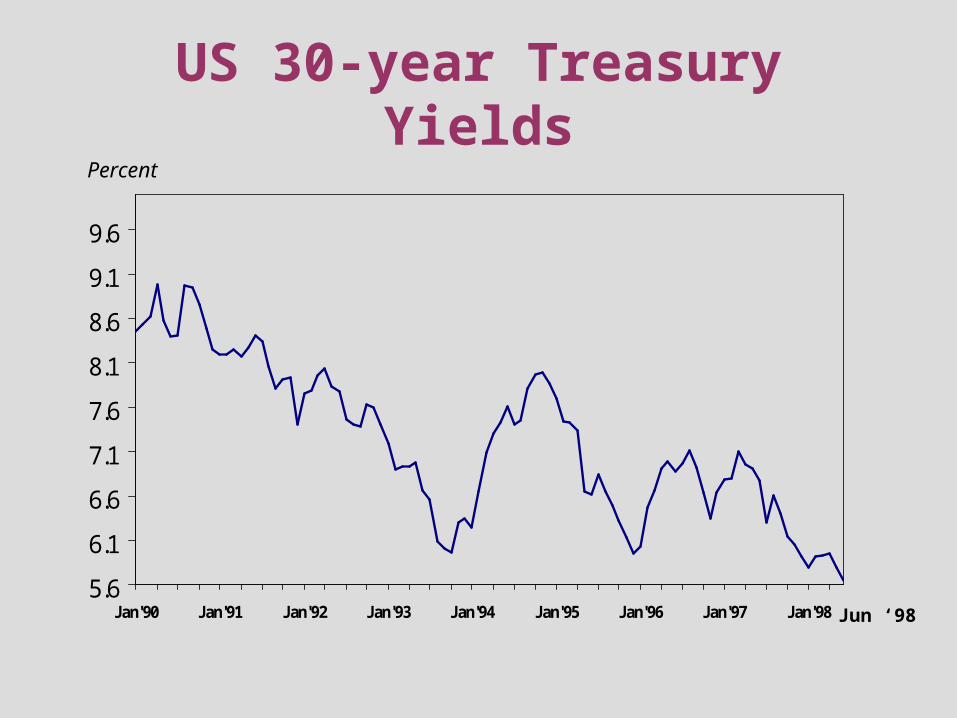

US 30-year Treasury Yields

5.6

6.1

6.6

7.1

7.6

8.1

8.6

9.1

9.6

Jan'90 Jan'91 Jan'92 Jan'93 Jan'94 Jan'95 Jan'96 Jan'97 Jan'98

Percent

Jun ‘98

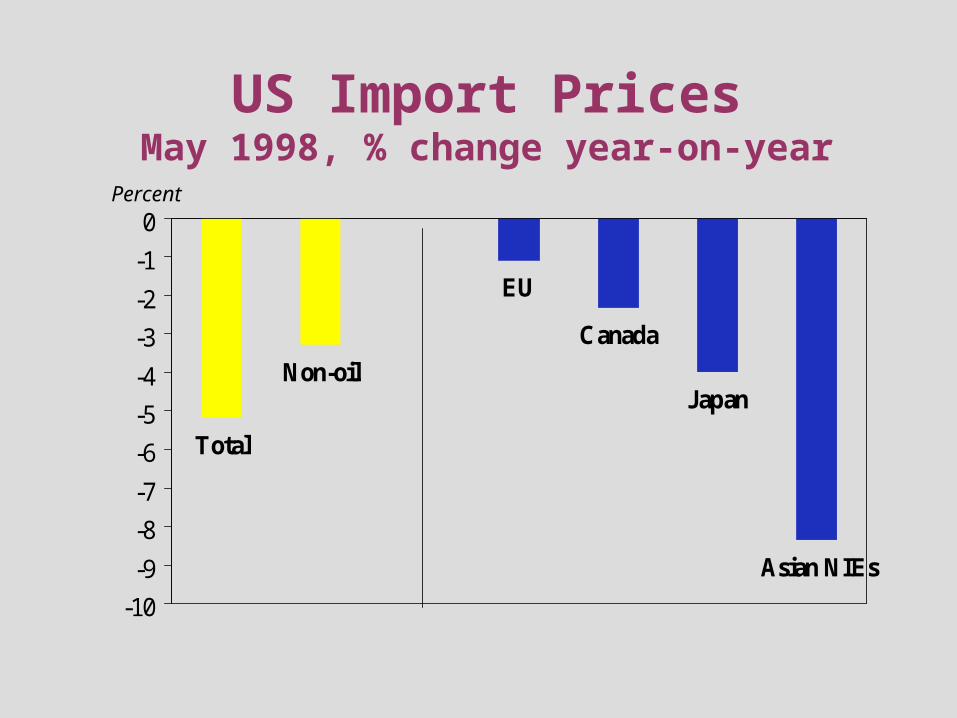

US Import PricesMay 1998, % change year-on-year

Total

Non-oil

EU

Canada

Japan

Asian NIEs

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0Percent

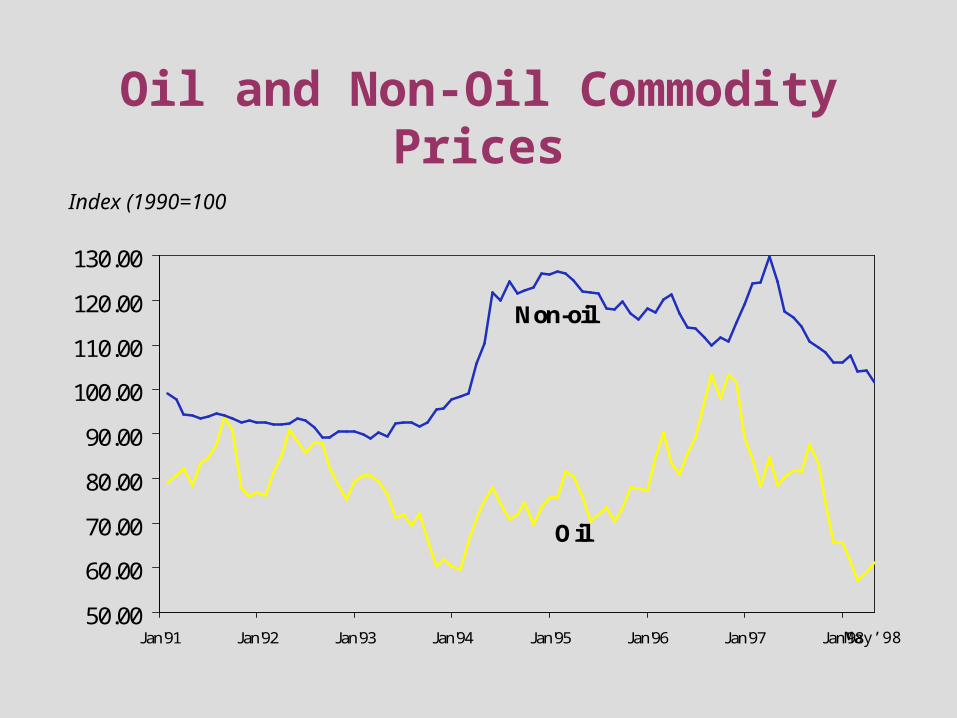

Oil and Non-Oil Commodity Prices

50.00

60.00

70.00

80.00

90.00

100.00

110.00

120.00

130.00

Jan'91 Jan'92 Jan'93 Jan'94 Jan'95 Jan'96 Jan'97 Jan'98

Non-oil

Oil

Index (1990=100

May’98

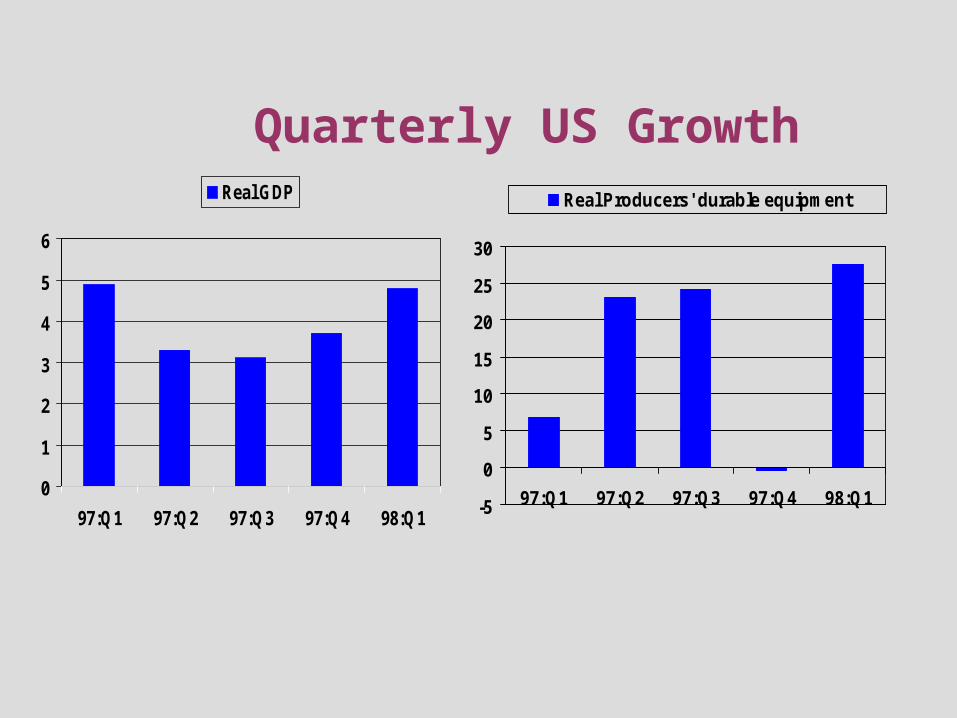

Quarterly US Growth

0

1

2

3

4

5

6

97:Q1 97:Q2 97:Q3 97:Q4 98:Q1

Real GDP

-5

0

5

10

15

20

25

30

97:Q1 97:Q2 97:Q3 97:Q4 98:Q1

Real Producers' durable equipment

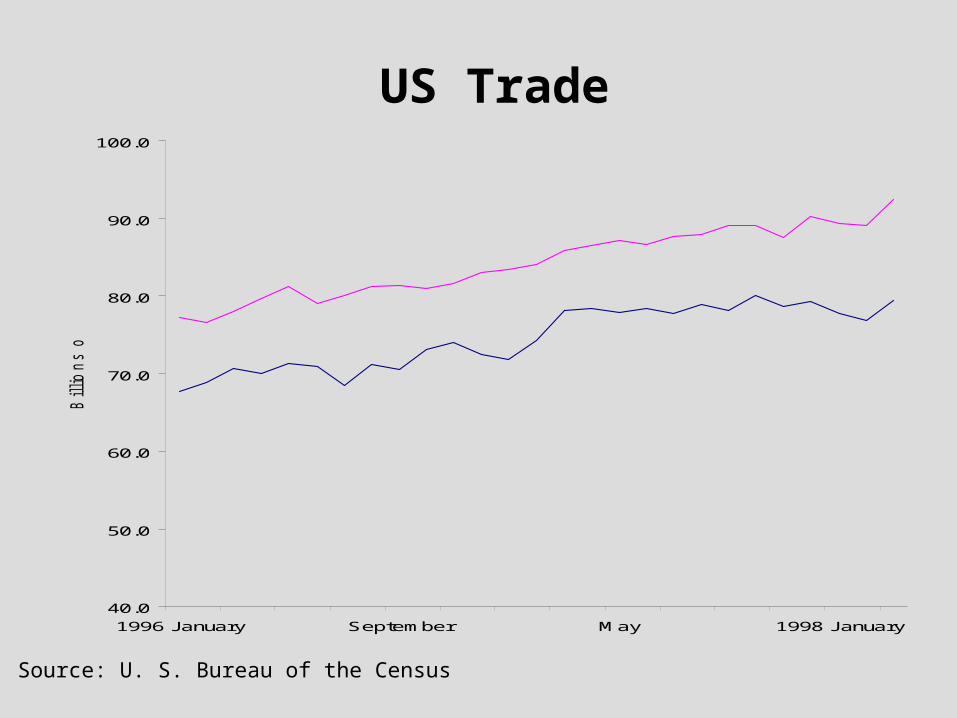

US Trade

Source: U. S. Bureau of the Census

40.0

50.0

60.0

70.0

80.0

90.0

100.0

1996 January September May 1998 January

Billio

ns o

f U

S $

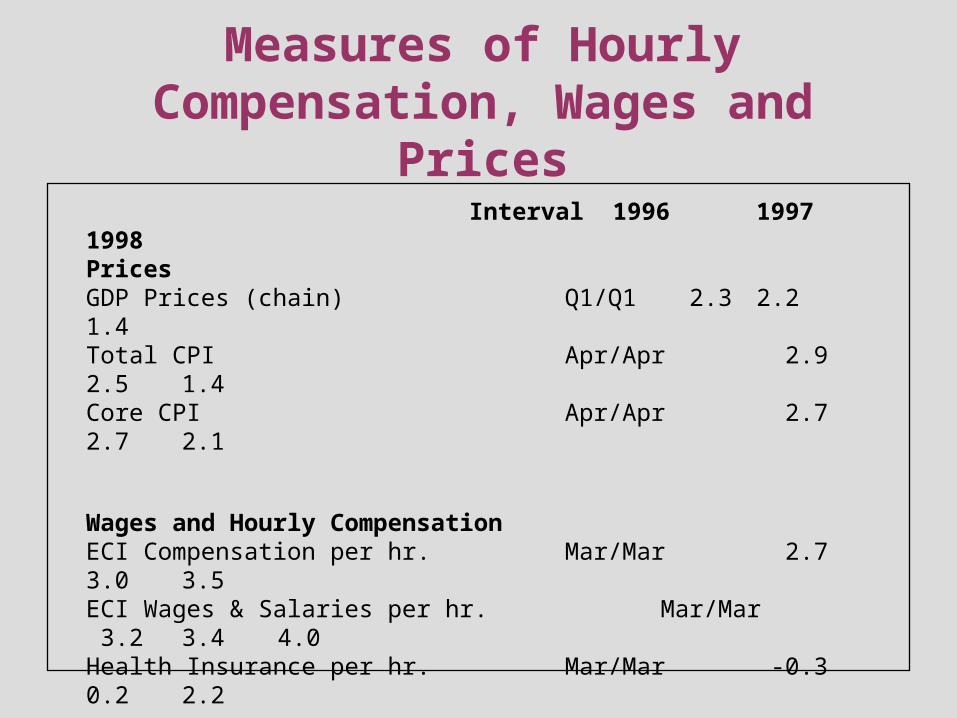

Measures of Hourly Compensation, Wages and

PricesInterval 1996 1997 1998

PricesGDP Prices (chain) Q1/Q1 2.3 2.2 1.4Total CPI Apr/Apr 2.9 2.5 1.4Core CPI Apr/Apr 2.7 2.7 2.1

Wages and Hourly CompensationECI Compensation per hr. Mar/Mar 2.7 3.0 3.5ECI Wages & Salaries per hr. Mar/Mar 3.2 3.4 4.0Health Insurance per hr. Mar/Mar -0.3 0.2 2.2

ProductivityNon-farm business Q1/Q1 1.8 1.3 2.1

1. High trade volume multipliers

2. Adverse terms of trade

3. Fall-off in capital flows and rising spreads

4. Forced policy response

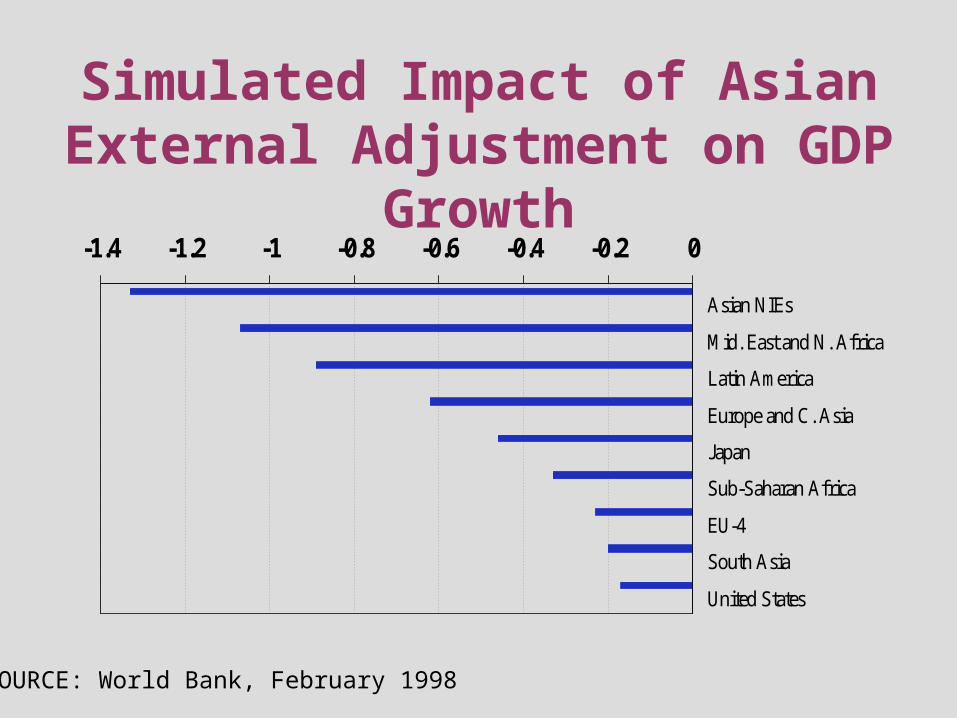

Adverse Impact on Developing Countries Greater Than on OECD

Simulated Impact of Asian External Adjustment on GDP Growth

-1.4 -1.2 -1 -0.8 -0.6 -0.4 -0.2 0

Asian NIEs

Mid. East and N. Africa

Latin America

Europe and C. Asia

Japan

Sub-Saharan Africa

EU-4

South Asia

United States

SOURCE: World Bank, February 1998

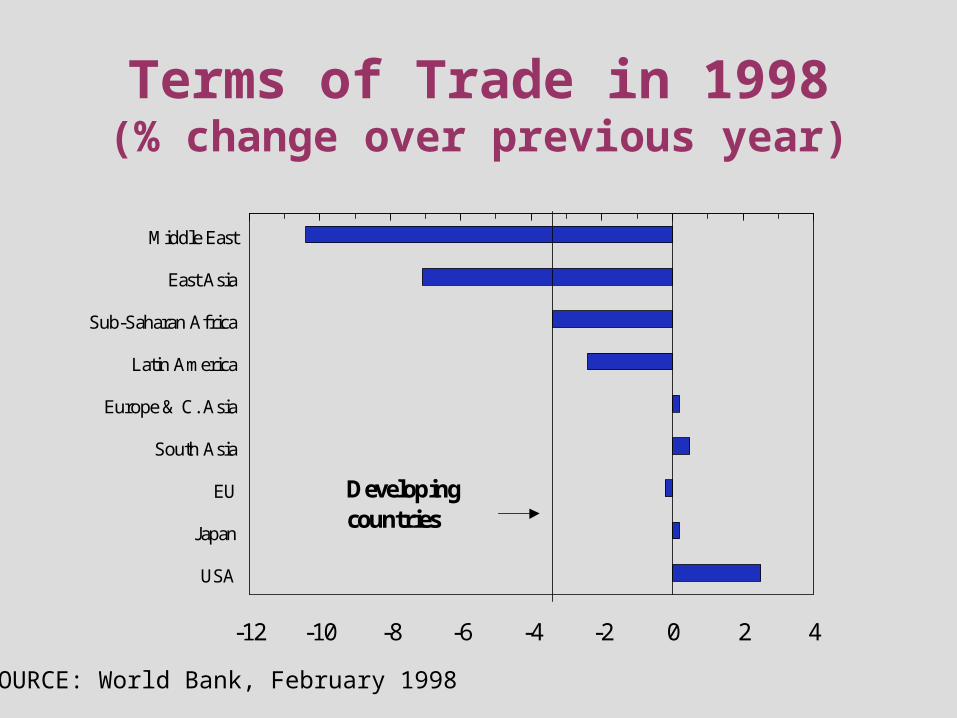

Terms of Trade in 1998(% change over previous year)

-12 -10 -8 -6 -4 -2 0 2 4

Middle East

East Asia

Sub-Saharan Africa

Latin America

Europe & C. Asia

South Asia

EU

Japan

USA

Developing countries

SOURCE: World Bank, February 1998

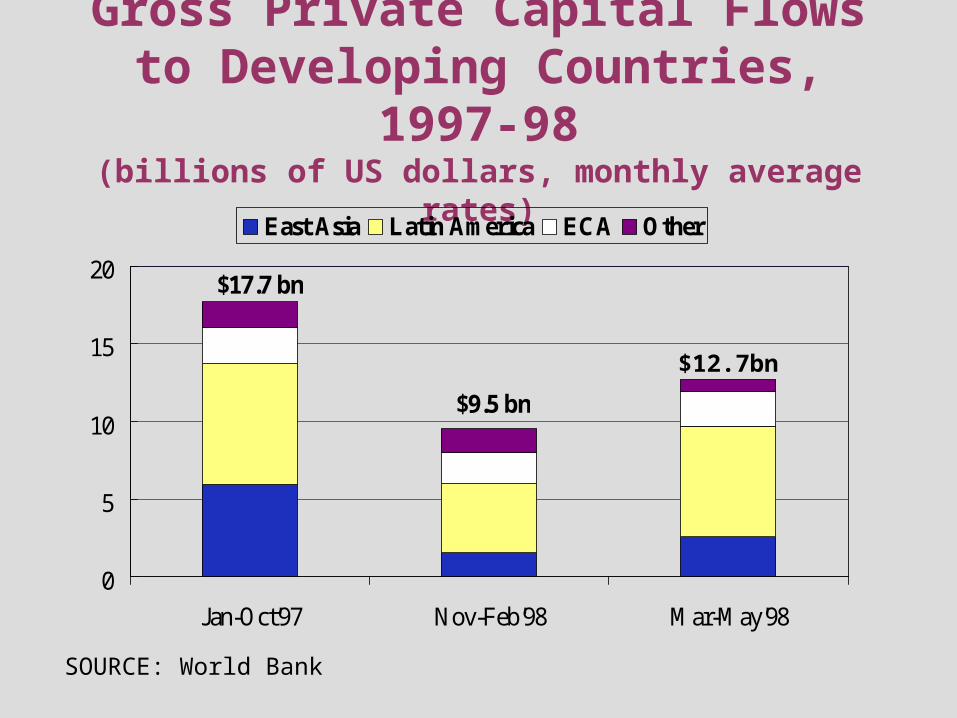

Gross Private Capital Flows to Developing Countries, 1997-98(billions of US dollars, monthly average rates)

0

5

10

15

20

Jan-Oct'97 Nov-Feb'98 Mar-May'98

East Asia Latin America ECA Other

$17.7 bn

$9.5 bn

SOURCE: World Bank

$12.7bn

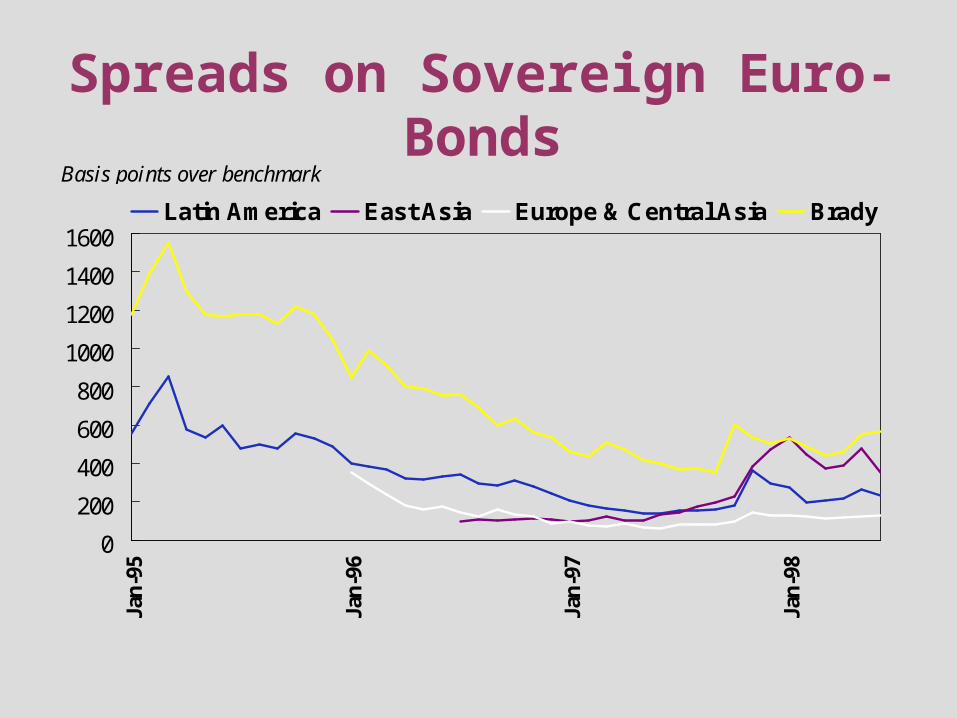

Spreads on Sovereign Euro-Bonds

0

200

400

600

800

1000

1200

1400

1600

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Latin America East Asia Europe & Central Asia Brady

Basis points over benchmark

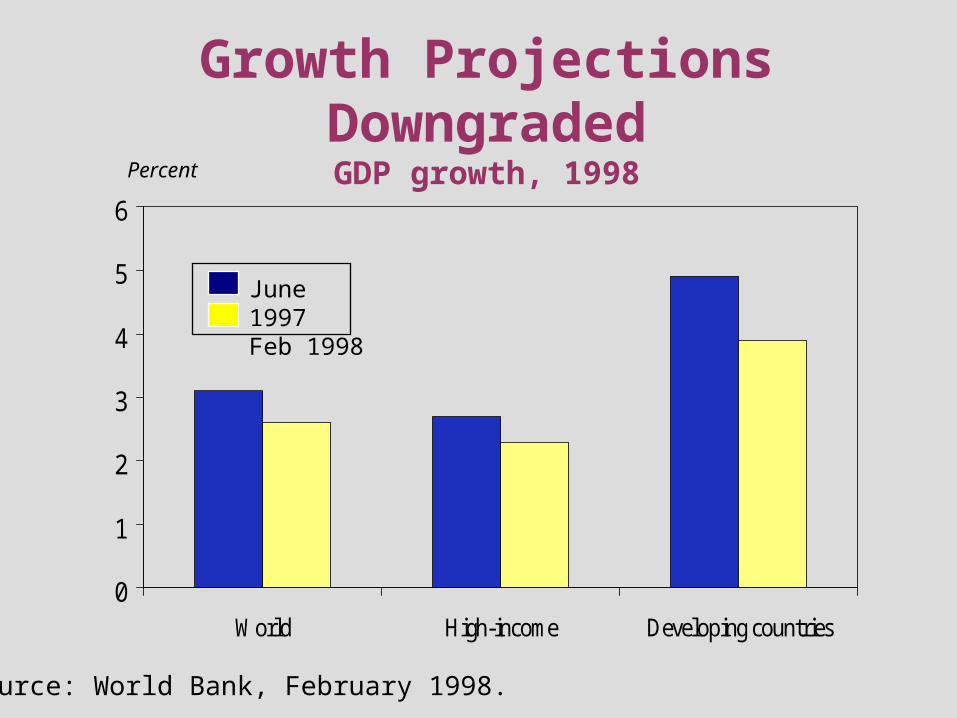

Growth Projections DowngradedGDP growth, 1998

0

1

2

3

4

5

6

World High-income Developing countries

Percent

June 1997Feb 1998

Source: World Bank, February 1998.

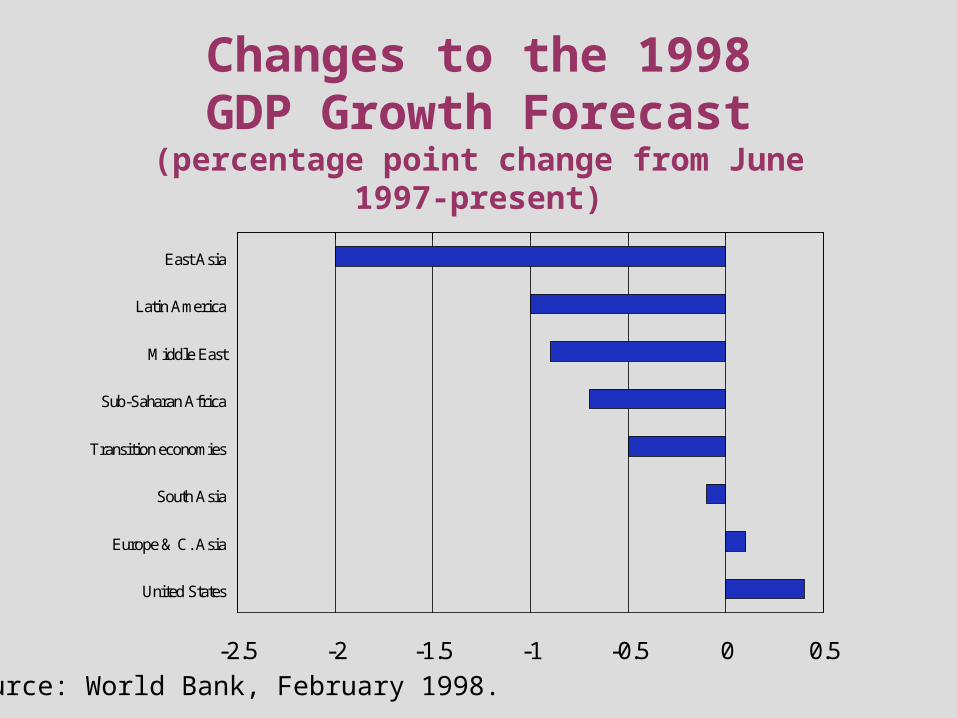

Changes to the 1998GDP Growth Forecast

(percentage point change from June 1997-present)

-2.5 -2 -1.5 -1 -0.5 0 0.5

East Asia

Latin America

Middle East

Sub-Saharan Africa

Transition economies

South Asia

Europe & C. Asia

United States

Source: World Bank, February 1998.

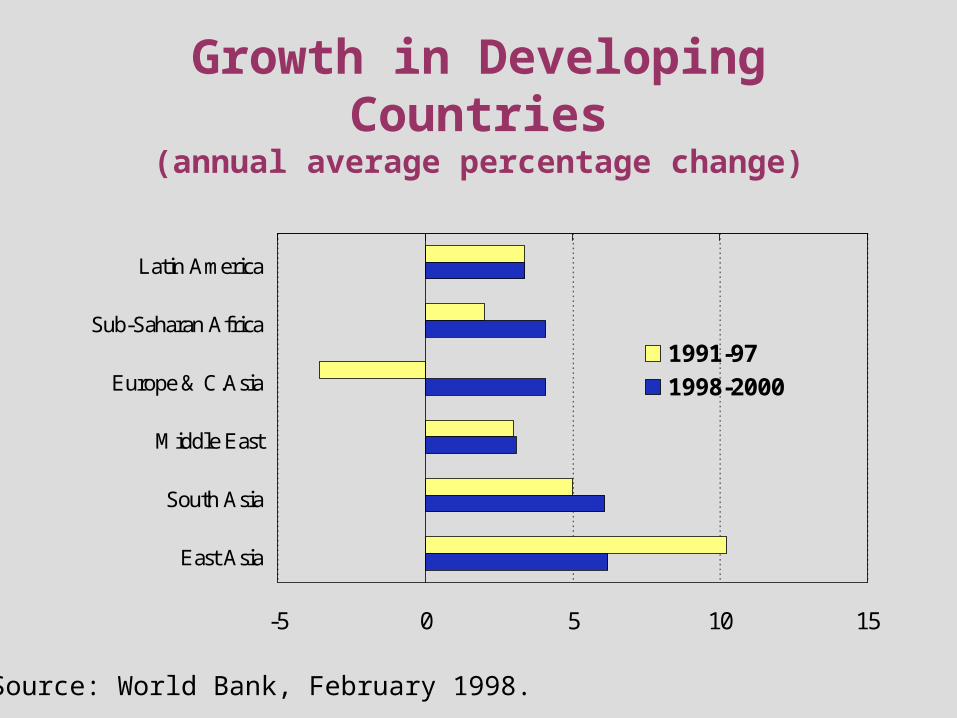

Growth in Developing Countries(annual average percentage change)

-5 0 5 10 15

Latin America

Sub-Saharan Africa

Europe & C.Asia

Middle East

South Asia

East Asia

1991-97

1998-2000

Source: World Bank, February 1998.