Embed Size (px)

Citation preview

Michelle R. Garfinkel

Michelle R. Garfinkel is a senior economist at the FederalReserve Bank of St. Louis. Scott Leitz provided researchassistance.

The Economic Consequencesof Reducing Military Spending

JILSEFORE THE CRISIS in the Middle East thissummer, the easing of international tensionshad reduced, for many, the urgency for theUnited States to continue building or even main-tain its military strength. As support for allo-cating the nation’s resources to defense weak-ened, people began to argue about the potentialfor a significant “peace dividend” available tothe U.S. economy.’

How should the savings from reduced defensespending be put to use to enhance our nation’swelfare? Many analysts, concerned primarilyabout the effects of large public deficits, haveargued that the savings should be applied toreduce the government’s need to borrow.2Others have voiced concern that a reduction indefense expenditures will generate unemploy-ment, at least temporarily, while resources arereallocated to productive activities in the civiliansector.3 Consequently, they have argued the in-itial savings should be used to ease this adjust-ment—perhaps by increasing expenditures on

training programs.4 Many other policy recom-mendations have been made.

Although the current situation in the MiddleEast raises doubt that there will be any signifi-cant dividend in the near term, it does not de-tract from the relevance of such recommenda-tions. Instead, it provides us with more time toevaluate the various options associated withfuture defense cuts.

In reviewing the economic implications ofreduced military spending, this article examinessome issues that have been overlooked by thosein search of ways to use the “peace dividend.”The article begins with a brief analysis of re-cent trends and the prospects for future cuts inmilitary spending to see how large a dividendmight be. Some simple economic principles arethen employed to assess how the peace dividend,regardless of its actual magnitude, might be usedto achieve diverse economic goals.

‘For example, see Pennar and Mandel (1989).2See, for example, Schultze (1990).3For example, see “Peace Dividend or Recession?” (1990).Also see Pennar and Mandel (1989), who report the resultsof a study of the short- and long-term effects of reducingthe defense budget by 5 percent a year in real terms from1991 to 1994 and keeping it constant thereafter. Althoughthis study predicts enhanced economic growth in the longrun, it also predicts some short-term losses. Also see Ellis

and Schine (1990), who report the results of a study in-dicating that as many as 1 million defense-related jobs (or20 percent of all jobs in defense-related activities) could belost by 1995. Although other analysts have argued that theemployment losses could be insignificant (see, for exam-ple, Uchitelle (1990)), some defense contractors havealready begun to cut production and employment.

4See, for example, the bill proposed recently by SenatorPeIl (S.2097).

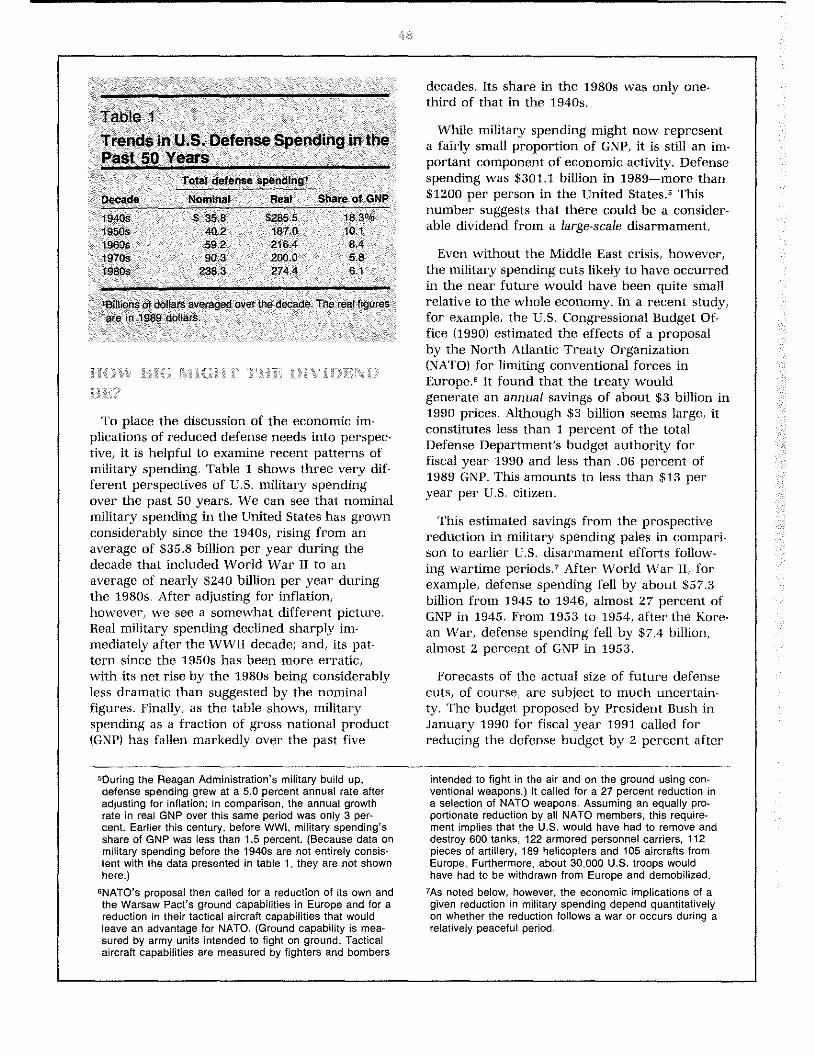

Table 1

Trends in U.S. Defense Spending in thePast 50 Years

Total defense spending’Decade Nominal Real Share of GNP

1940s $ 35.8 5285.5 18.3°’o1950s 402 187.0 10.11960s 59.2 216.4 8.41970s 90.3 200.0 581980s 238.3 274.4 6 I

‘Billions of dollars averaged over the decade. Tho real figuresare in 1989 dollars.

To place the discussion of the economic im-plications of reduced defense needs into perspec-tive, it is helpful to examine recent patterns ofmilitary spending. Table 1 shows three very dif-ferent perspectives of U.S. military spendingover the past 50 years. We can see that nominalmilitary spending in the United States has grownconsiderably since the 1940s, rising from anaverage of $35.8 billion per year during thedecade that included World War II to anaverage of nearly $240 billion per year duringthe 1980s. After adjusting for inflation,however, we see a somewhat different picture.Real military spending declined sharply im-mediately after the WWII decade; and, its pat-tern since the 1950s has been more erratic,with its net rise by the 1980s being considerablyless dramatic than suggested by the nominalfigures. Finally, as the table shows, militaryspending as a fraction of gross national product(GNP) has fallen markedly over the past five

decades. Its share in the 1980s was only one-third of that in the 1940s.

While military spending might now representa fairly small proportion of GNP, it is still an im-portant component of economic activity. Defensespending was $301.1 billion in 1989—more than$1200 per person in the United States.~Thisnumber suggests that there could be a consider-able dividend from a large-scale disarmament.

Even without the Middle East crisis, however,the military spending cuts likely to have occurredin the near future would have been quite smallrelative to the whole economy. In a recent study,for example, the U.S. Congressional Budget Of-fice (1990) estimated the effects of a proposalby the North Atlantic Treaty Organization(NATO) for limiting conventional forces inEurope.° It found that the treaty wouldgenerate an annual savings of about $3 billion in1990 prices. Although $3 billion seems large, itconstitutes less than 1 percent of the totalDefense Department’s budget authority forfiscal year 1990 and less than .06 percent of1989 GNP. This amounts to less than $13 peryear per U.S. citizen.

This estimated savings from the prospectivereduction in military spending pales in compari-son to earlier U.S. disarmament efforts follow-ing wartime periods.~After World War II, forexample, defense spending fell by about $57.3billion from 1945 to 1946, almost 27 percent ofGNP in 1945. From 1953 to 1954, after the Kore-an War, defense spending fell by $7.4 billion,almost 2 percent of GNP in 1953.

Forecasts of the actual size of future defensecuts, of course, are subject to much uncertain-ty. The budget proposed by President Bush inJanuary 1990 for fiscal year 1991 called forreducing the defense budget by 2 percent after

5During the Reagan Administration’s military build up,defense spending grew at a 5.0 percent annual rate afteradjusting for inflation; in comparison, the annual growthrate in real GNP over this same period was only 3 per-cent. Earlier this century, before WWI, military spending’sshare of GNP was less than 1.5 percent. (Because data onmilitary spending before the 1940s are not entirely consis-tent with the data presented in table 1, they are not shownhere.)

6NATO’s proposal then called for a reduction of its own andthe Warsaw Pact’s ground capabilities in Europe and for areduction in their tactical aircraft capabilities that wouldleave an advantage for NATO. (Ground capability is mea-sured by army units intended to fight on ground. Tacticalaircraft capabilities are measured by fighters and bombers

intended to fight in the air and on the ground using con-ventional weapons.) It called for a 27 percent reduction ina selection of NATO weapons. Assuming an equally pro-portionate reduction by all NATO members, this require-ment implies that the U.S. would have had to remove anddestroy 600 tanks, 122 armored personnel carriers, 112pieces of artillery, 189 helicopters and 105 aircrafts fromEurope. Furthermore, about 30,000 U.S. troops wouldhave had to be withdrawn from Europe and demobilized.

7As noted below, however, the economic implications of agiven reduction in military spending depend quantitativelyon whether the reduction follows a war or occurs during arelatively peaceful period.

adjusting for inflation over the fiscal years 1991to 1995.~Others argued for defense spendingcuts as much as 5 percent in real terms peryear from fiscal years 1992 to 1994, achievingan annual savings of about $60 billion (in 1989prices) starting in 1994.~If cuts of this magni-tude were implemented, the implied savingswould constitute about 1.2 percent of GNP forthe year 1989, nearly $250 per year on a percapita basis.

And the savings could be even larger. Indeed,on the day of the Iraqi invasion of Kuwait,President Bush announced that, although the in-vasion indicates a need to maintain a strongmilitary force, U.S. armed forces could bereduced by 25 percent over five years given therecent changes in Soviet-U.S. relations.’°

tn:.iqJI~(~irrc~(7fF 1•JII.•i•7 •[qJjIflF~~frp~

S(.JNIF: BAS.IC F(XJNI} 1111

Generally speaking, the trade-off betweencompeting uses of resources implies that a re-duction in real military spending would providea “dividend” in the form of increased real privateand public consumption and investment oppor-tunities—that is, increased resources availablefor the production of consumption and invest-ment goods. To quantify these increased oppor-tunities over time, the annual peace dividend isdefined here simply as the annual reduction inreal military spending.”

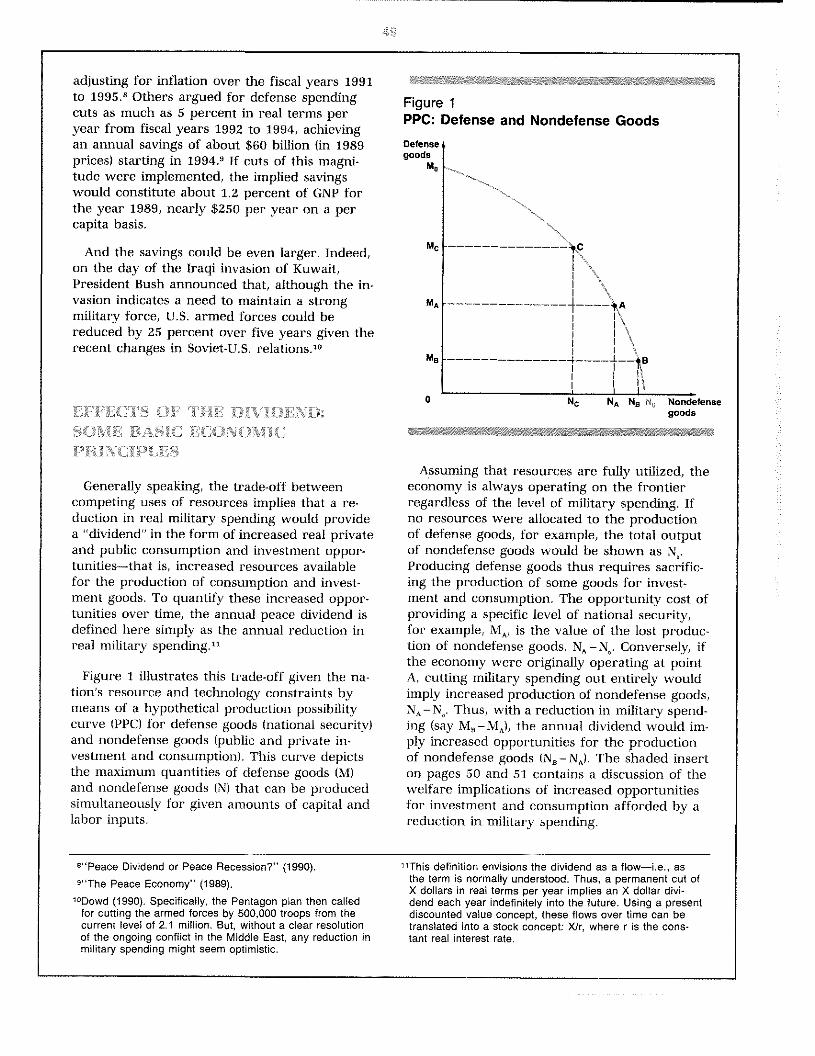

Figure 1 illustrates this trade-off given the na-tion’s resource and technology constraints bymeans of a hypothetical production possibilitycurve (PPC) for defense goods (national security)and nondefense goods (public and private in-vestment and consumption). This curve depictsthe maximum quantities of defense goods (M)and nondefense goods (N) that can be producedsimultaneously for given amounts of capital andlabor inputs.

Figure 1PPC: Defense and Nondefense GoodsDefensegoods

N

Ii0 Nc NA N9 N0 Nondefense

goods

Assuming that resources are fully utilized, theeconomy is always operating on the frontierregardless of the level of military spending. Ifno resources were allocated to the productionof defense goods, for example, the total outputof nondefense goods would be shown as N,.Producing defense goods thus requires sacrific-ing the production of some goods for invest-ment and consumption. The opportunity cost ofproviding a specific level of national security,for example, MA, is the value of the lost produc-tion of nondefense goods, NA — N,. Conversely, ifthe economy were originally operating at pointA, cutting military spending out entirely wouldimply increased production of nondefense goods,NA — N,. Thus, with a reduction in military spend-ing (say MB—MA), the annual dividend would im-ply increased opportunities for the productionof nondefense goods (NB—NA). The shaded inserton pages 50 and 51 contains a discussion of thewelfare implications of increased opportunitiesfor investment and consumption afforded by areduction in military spending.

8”Peace Dividend or Peace Recession?” (1990).9”The Peace Economy” (1989).

‘°Dowd(1990). Specifically, the Pentagon plan then calledfor cutting the armed forces by 500,000 troops from thecurrent level of 2.1 million. But, without a clear resolutionof the ongoing conflict in the Middle East, any reduction inmilitary spending might seem optimistic.

liThis definition envisions the dividend as a flow—i.e., asthe term is normally understood. Thus, a permanent cut ofX dollars in real terms per year implies an X dollar divi-dend each year indefinitely into the future. Using a presentdiscounted value concept, these flows over time can betranslated into a stock concept: Xlr, where r is the cons-tant real interest rate.

Mc

MA -

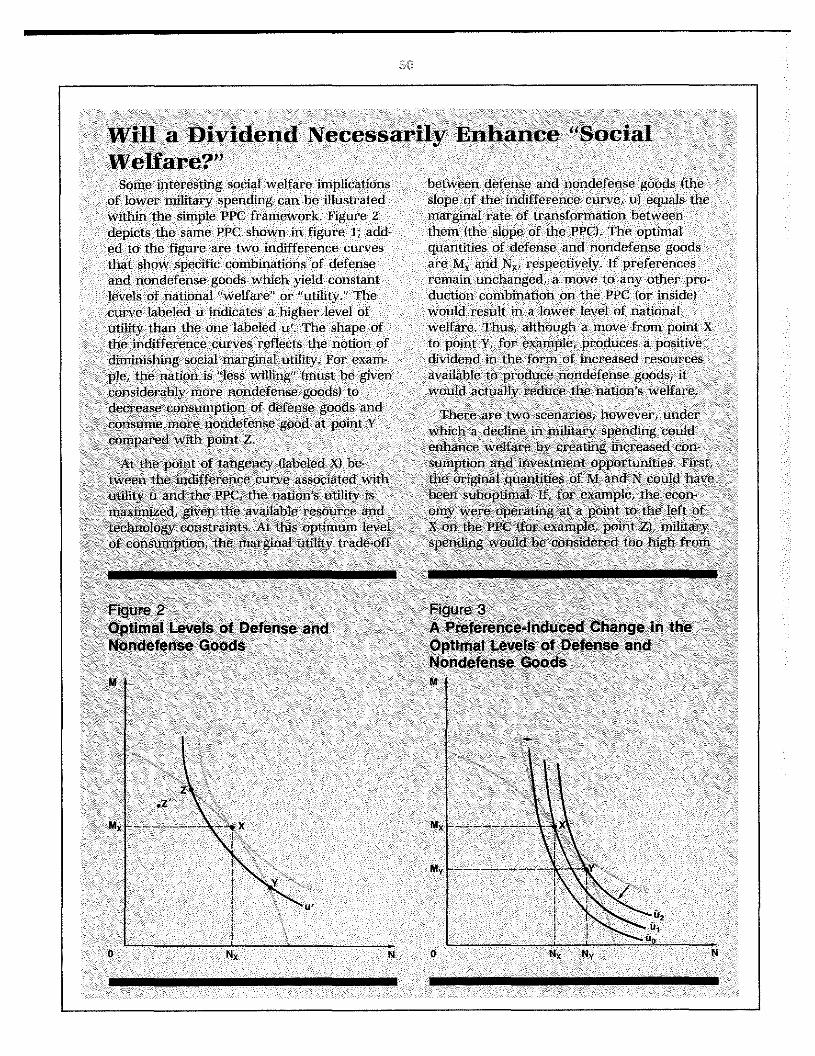

a ~,orta1u-ella IC’ iRlilit of en - \lteI-uati\ ely. general c’lock’vise mm c’n,ent iii the indif-the original point could un t’ been inside the fci’ence c’ui’vns. ihis I~I.I~C’iiiC’lit i~lutist ratedl’l’( ahot e Iioirit N. ‘,u(h .15 I,’. lii this c.aw, ill Figure 3. n’hei’e the mu indifferenceruilitan- ‘~peridil1gis ako lot) high and. riiore rui\ es are labt’Iecl ii if hat iohlai sccuritv canimportant, the econonn is opei’ating below its be maintained with it’’~.,mIlitary ~peuding apotential output h’~’els. smaller’ (liffintity of \t u itli the sanile qti.intit~

of \ tN,, I p rodii ce’~the same ti til iIv levelsecond, a cut in military spendinc~could — . . ‘ —

ii = ii - l-urthem’ the i’narginal value ot itu yeas—‘~emlii Ni te well art’ gil ins ii it were associattedirig \ I relat lfl’ to I he cost of to regone CC)! -

~ ith an unanticipated dec line iii I he se~’t’rmt~- .

stimption of N taIls. I he neu welfare may-o! e.~tema I threats. Hits ~eems to he the ex- ...muting to iii 1)1! Ui I mon of NI and N a torig thearnplt’ most relet ant to lilt’ t-urrent situation .

P ‘C. is denoted ii ~- \ , where \ increast’s to N -in t-olvu ig [‘b- Soviet me a tions. I he reduc ed . -and \ I decreases IC) NI ~. [ he net ‘‘well are eI

vat tie of ma ihit alum” e.\ is Ling I - S. In! Ii tars’ .- ‘ I ect ol the dlviden ci, Xl,. — Xl ,,, woud be

st men ‘‘th in the lace of det eme can be cap- . . . . —

reflec-t ed in the increase Iroi n ii to LI..iiired best bv presu muig there has been a

The concave shape of the PPC reflects dimin-ishing marginal returns in productive transfor-mation. That is, the amount of nondefensegoods that must be sacrificed to produce onemore defense good increases as M increases.For example, in the figure, the move from C toA and the move from A to B involve identicalreductions in military spending. Starting at thepoint with a higher level of military spending(Me), however, that reduction in military spend-ing implies greater additional production of non-defense goods than when starting at point B.(That is, NA — N~>N0 — NA.) Hence, assumingresources are fully employed, a given reductionin the production of defense goods when thecurrent level is low—for example, duringpeacetime—would imply smaller additions toconsumption and investment opportunities thanwhen the current level is high—for example,during wartime.

These allocative effects of the peace dividendcan also have implications for the amount ofresources available for production in general.

Specifically, any additional investment adds tothe future resource base, thereby enhancingfuture output growth and investment and con-sumption opportunities. Hence, even if the de-cline in military spending were temporary, forexample lasting only one year, its benefits interms of increased productive capacity could berealized over many years. This longer-term ef-fect can be modeled in the framework presentedabove by an outward shift of the PPC curveover time.”

Some analysts believe that, in recent decades,military spending has been excessive, reducingthe residual supply of productive resources (thatis, capital and labor) available for private andnondefense public investment and thereby weak-ening the economy.’3 According to this “deple-tion” theory, the effects of higher levels ofmilitary spending are reflected in lower rates ofinvestment and, consequently, lower rates ofeconomic growth. Thus, the principal result ofreduced military spending would be greater in-vestment and economic growth.

Evidence on the “crowding-out” effect ofmilitary spending is based primarily on empiricalanalyses relating changes in military spending’sshare of GNP to the GNP shares of other broadcategories of expenditures; typically, the studiesfocus on the effect on private investment’s

l2Of course, one might argue that the level of military spen-ding could positively influence the position of the PPC.Because military spending enhances a nation’s ability toprotect its resources, it might serve to increase the na-tion’s future resource base by encouraging moreinvestment.

“See, for example, Dumas (1987), Melman (1988) and DuBoff (1989). In contrast, Weidenbaum (1990) argues that,as defense spending has fallen relative to GNP, the effectsof such spending on the U.S. economy have become lesssignificant.

tures, not just real private domestic investment.

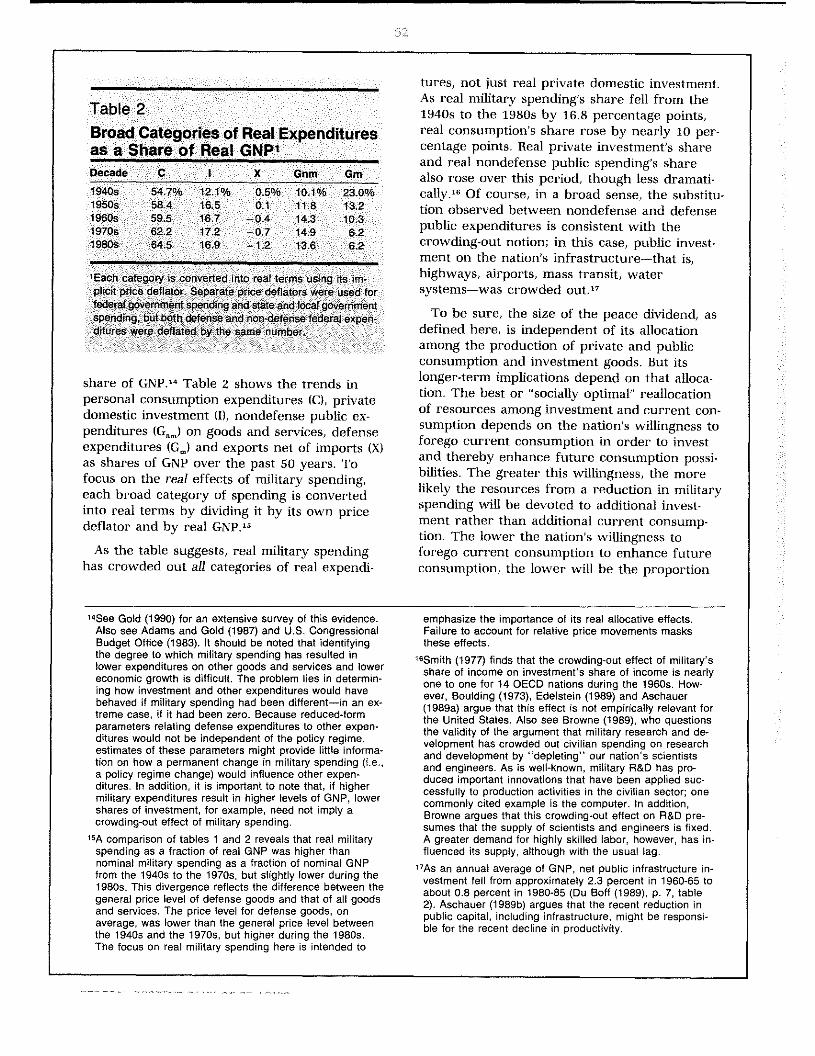

Table 2

Broad Categories of Real Expendituresas a Share of Real GNP’Decade C I X Gnm Gm

1940s 547% 12.1°/n 05% 101% 23.0%1950s 58.4 16.5 0.1 11.8 13.21960s 59.5 167 -0.4 14.3 10.31970s 62.2 172 -0.7 14.9 6.21980s 645 16.9 —1.2 13.6 6.2

1Each category is converted into real terms using its im-plicit price deflator. Separate price deflators were used forfederal government spending and state and local governmentspending, but both defense and non-defense federal expen-dilures were deflated by the same number

share of GNP.’4 Table 2 shows the trends inpersonal consumption expenditures (C), privatedomestic investment (I), nondefense public ex-penditures (Gnm) on goods and services, defenseexpenditures (Gm) and exports net of imports (X)as shares of GNP over the past 50 years. Tofocus on the rea/ effects of military spending,each broad category of spending is convertedinto real terms by dividing it by its own pricedeflator and by real GNP.’°

As the table suggests, real military spendinghas crowded out all categories of real expendi-

As real military spending’s share fell from the1940s to the 1980s by 16.8 percentage points,real consumption’s share rose by nearly 10 per-centage points. Real private investment’s shareand real nondefense public spending’s sharealso rose over this period, though less dramati-cally.16 Of course, in a broad sense, the substitu-tion observed between nondefense and defensepublic expenditures is consistent with thecrowding-out notion; in this case, public invest-ment on the nation’s infrastructure—that is,highways, airports, mass transit, watersystems—was crowded out.”

To be sure, the size of the peace dividend, asdefined here, is independent of its allocationamong the production of private and publicconsumption and investment goods. But itslonger-term implications depend on that alloca-tion. The best or “socially optimal” reallocationof resources among investment and current con-sumption depends on the nation’s willingness toforego current consumption in order to investand thereby enhance future consumption possi-bilities. The greater this willingness, the morelikely the resources from a reduction in militaryspending will be devoted to additional invest-ment rather than additional current consump-tion. The lower the nation’s willingness toforego current consumption to enhance futureconsumption, the lower will be the proportion

l4See Gold (1990) for an extensive survey of this evidence.Also see Adams and Gold (1987) and U.S. CongressionalBudget Office (1983). It should be noted that identifyingthe degree to which military spending has resulted inlower expenditures on other goods and services and lowereconomic growth is difficult. The problem lies in determin-ing how investment and other expenditures would havebehaved if military spending had been different—in an ex-treme case, if it had been zero. Because reduced-formparameters relating defense expenditures to other expen-ditures would not be independent of the policy regime,estimates of these parameters might provide little informa-tion on how a permanent change in military spending (i.e.,a policy regime change) would influence other expen-ditures. In addition, it is important to note that, if highermilitary expenditures result in higher levels of GNP, lowershares of investment, for example, need not imply acrowding-out effect of military spending.

ISA comparison of tables 1 and 2 reveals that real militaryspending as a fraction of real GNP was higher thannominal military spending as a fraction of nominal GNPfrom the 1940s to the 1970s, but slightly lower during the1980s. This divergence reflects the difference between thegeneral price level of defense goods and that of all goodsand services. The price level for defense goods, onaverage, was lower than the general price level betweenthe 1940s and the 1970s, but higher during the 1980s.The focus on real military spending here is intended to

emphasize the importance of its real allocative effects.Failure to account for relative price movements masksthese effects.

‘6Smith (1977) finds that the crowding-out effect of military’sshare of income on investment’s share of income is nearlyone to one for 14 OECD nations during the 1960s. How-ever, Boulding (1973), Edelstein (1989) and Aschauer(1989a) argue that this effect is not empirically relevant forthe United States. Also see Browne (1989), who questionsthe validity of the argument that military research and de-velopment has crowded out civilian spending on researchand development by “depleting” our nation’s scientistsand engineers. As is well-known, military R&D has pro-duced important innovations that have been applied suc-cessfully to production activities in the civilian sector; onecommonly cited example is the computer. In addition,Browne argues that this crowding-out effect on R&D pre-sumes that the supply of scientists and engineers is fixed.A greater demand for highly skilled labor, however, has in-fluenced its supply, although with the usual lag.

hAs an annual average of GNP, net public infrastructure in-vestment fell from approximately 2.3 percent in 1960-66 toabout 0.8 percent in 1980-85 (Du Boff (1989), p. 7, table2). Aschauer (1989b) argues that the recent reduction inpublic capital, including infrastructure, might be responsi-ble for the recent decline in productivity.

of the savings that is allocated to investment.Thus, in contrast to the suggestion of the deple-tion theory briefly described above, the divi-dend from reduced military spending need notresult in significantly greater rates of invest-ment and economic growth. The extent towhich the dividend will affect economic growthdepends on how it is allocated among the pro-duction of investment and consumption goods.

.‘•U~.1.

In recent decades, decreases in nominalmilitary spending typically have been associatedwith increases in other public expenditures innominal terms. Indeed, after falling to 19.5 per-cent in the 1950s from 25.1 percent during the1940s, total public spending (federal plus stateand local) on goods and services has remainedroughly constant as a fraction of nominal GNP,around 20 percent; only the composition ofthose expenditures changed. Although therecould be reasons why this pattern might persistin the upcoming decades, many analysts havequestioned whether a continuation of this pat-tern is either likely or even desirable. Never-theless, the basic question to be addressedshould be couched in real terms: What shouldbe done with the peace dividend?

ii~crease NOntheiènse PublicExpenditures

Some analysts have argued that leavingnondefense public expenditures alone and usingthe reduction in military spending to eitherdecrease the deficit or lower taxes is not thebest use of the peace dividend. Instead, many ofthem believe that at least part of the savingsfrom arms reduction might best be used to in-crease nonmilitary government spending—specifically, to rebuild the nation’s infrastruc-ture.18 In terms of the economic frameworkabove, this policy would shift out the PPC, in-

creasing future production and consumptionopportunities.

Others have argued that, unless the fall inmilitary spending is somehow offset, resourceutilization and, hence, economic activity will fallas well.19 In this view, which lies within thestandard “Keynesian” paradigm, the governmentshould use part (or all) of the savings to financeadditional public expenditures, including nonin-frastructure expenditures, such as welfare pro-grams, to offset the negative effect of reducedmilitary spending on aggregate demand.

This argument assumes that military spendingin particular or public expenditures in generalenhance social welfare not only by providingadditional public goods, but by increasingemployment and thereby stimulating the econo-my—that is, by inducing the use of idle resources.It implies that, without the increases in militaryspending or, more generally, public expendituresduring the post-WWII period, the economywould have operated below its potential outputcapability (that is, inside its PPC).

Although there is evidence that a permanentdecrease in military spending can produce apermanent decline in aggregate output,’° thedecline in output could be generated, in part,by a voluntary reduction in the supply of labor.In other words, this evidence does not necessari-ly imply that a permanent decline in militarydemand, without an increase in other publicspending, would cause these productive re-sources to become involuntarily idle on a per-manent basis.

Reduce Taxes

Some analysts would like us to consider analternative policy that leaves other governmentexpenditures unchanged and uses the dividendto reduce taxes. By increasing individuals’ after-tax income, this policy might induce individualsto decrease their supply of labor, which wouldin turn decrease output without leaving laborresources involuntarily idle.2’

‘°Forexample, see Du Boff (1989) and Melman (1988).19For example, see Bolton (1966), especially pp. 37-41.205ee Barro (1981). In studying the output effects of govern-

ment expenditures in the United States, he distinguishespermanent from temporary components of military spen-ding. He finds that the effect of increases in temporarymilitary spending (essentially wartime expenditures) onoutput was nearly one-for-one; increases in permanentmilitary spending also increased output, but by less thanthe change in military spending.

21See Barro (1981) for a theoretic discussion of the effectsof government expenditures on output. In support of this

line of reasoning, Dunne and Smith (1990) find that for theUnited States, military spending does not “cause”unemployment. Riddell (1988) argues, in a more Marxianspirit, that the government’s apparent bias for military overnon-military expenditures is driven by its objective to main-tain international order so as to maximize the profitabilityof U.S. capital. This possible endogeneity of military spen-ding calls many empirical analyses that treat military spen-ding as exogenous into question. Also see Garfinkel(1990a), who uses a game-theoretic model to show howmilitary spending can be driven by aggregate economicactivity through the government’s motive to prevent othernations from extracting its citizens’ resources.

NOVEMBER/DECEMBER 1990

It should be noted that a permanent declinein measured output, triggered by the impact ofreduced military spending (and reduced taxes)on leisure, does not necessarily reflect a deterio-ration in social welfare. Because leisure hasvalue, welfare could increase even if consump-tion did not. Further, the theory describedabove suggests that, although individuals wouldwork less, they might actually consume morenondefense private goods because theirdisposable income has increased (their taxliabilities have declined). On net, their welfarewould have increased as long as this new out-come were chosen voluntarily.”

Some analysts, who view large public deficitsas harmful to the economy, have argued thatthe government should use the peace savings toreduce the public deficit.” In particular, thelarge deficits (public dissavings) of the pastdecade are thought to have caused a decline intotal national savings—that is, the sum ofprivate and public savings. Since a decline intotal savings decreases the residual supply ofcredit available to private borrowers, largepublic deficits are considered by many to havepushed up expected real interest rates (interestrates adjusted for expected inflation).’~Thus,using the dividend to reduce the public deficitwould decrease expected real interest rates andthereby stimulate both investment activity andthe production of goods, such as exports andnew homes, whose sales are sensitive tomovements in interest rates.

Although the U.S. savings rate appears tohave declined in recent years, how much of thisdecline can be blamed on large public deficits is

unclear.” The argument that public deficits in-fluence the national savings rate is based on anumber of potentially questionable assumptions.One is that individuals do not view tax cuts thatincrease public borrowing (holding the level ofgovernment spending constant) as increasingtheir future tax liabilities. Instead, individualsfeel wealthier and increase their consumption inresponse to such tax cuts. Although they alsomight respond by increasing their savings, theincrease in private savings is assumed to be in-sufficient to keep total savings from falling. Inthis view, for a given level of government ex-penditures, public deficits decrease total savingsand increase aggregate demand.26

Other analysts argue that individuals believereductions in current taxes associated with addi-tions to public debt must be financed eventuallywith additional future taxes. In light of the in-crease in their future tax liabilities, individualsincrease their savings. Conversely, they respondto a decrease in the public deficit, for a givenlevel of government expenditures, by decreasingtheir savings. In either case, consumption isunaffected.

In this view, often referred to as the “Ricar-dian” view, individuals behave as if a decreasein the public deficit results in an equal decreasein the present discounted value of their futuretax liabilities. This argument builds on theassumption that public debt will be retiredeventually out of future taxes. If this view isvalid, private and public savings for a givenlevel of government expenditures should beperfectly negatively correlated, while total sav-ings should be unrelated to public savings.’7

22As discussed below, however, labor and capital resourcescould be left involuntarily idle temporarily as the economyadjusts to the reduced military demand.

23See, for example, Schultze (1990). Also, see Chrystal andThornton (1988) for a related discussion of the effects ofdeficit spending.24lndeed, this effect on interest rates is thought to be themechanism through which military spending has crowded-out investment. By enhancing the productivity of privatecapital, however, military spending could have had a“crowding-in” effect that would have offset its crowding-out effect. But Aschauer (1989a,b) presents evidence thatdoes not support the notion that additions to the stock ofmilitary capital add to the productivity of private capital.Moreover, the references cited in footnotes 14 and 16 pro-vide evidence that military spending does not crowd outprivate investment.

‘5Schultze (1990) estimates that national savings as apercentage of national income (i.e., net national product)has fallen from an average of 8 percent during the three

decades before 1980 to 3.3 percent during the first threequarters of 1989. Some analysts, however, question thenotion that savings is too low in the United States; theirskepticism is based on problems with the conventionalmeasurements of savings. Cullison (1990) provides auseful survey of this literature.

26See Thornton (1990) for a theoretical discussion of the linkbetween total national savings and public deficits.

“Against this Ricardian view, one might argue that deficitscould be financed either through increased seigniorage orincome taxes in future generations. In either case, the“burden” of the current deficit could be shifted andbudget deficits, holding government expenditures fixed,could affect economic activity. See Barro (1989) for a briefdiscussion of the empirical evidence on the effects ofbudget deficits. While recognizing the problems associatedwith testing the Ricardian proposition, Barro argues thatthe existing evidence lends more support to the Ricardianview than to the alternative view (p. 52).

DO

To be sure, using part of the annual dividendto reduce the public deficit could increase totalinvestment and total consumption. According tothe Ricardian view, however, the amounts ofthese increases do not depend on whether taxesare cut or the deficit is reduced. A cut in thedeficit reduces future tax liabilities, but the tim-ing of the tax cuts does not matter.

Because of the distorting nature of the incometax system, however, the equivalence betweentaxes and debt creation implied by the Ricardianview would be, at best, a rough approximation.Economic theory predicts that proportional in-come taxation distorts individuals’ decisionsabout consumption and labor supply. Thesedistortions are costly and, other things beingequal, the severity of the distortion increases asthe tax rate increases. Consequently, if thefederal government wants to minimize the costsassociated with these distortions, given the pathof future government expenditures, it shouldsmooth income taxes over time.28 This modifiedversion of the Ricardian view suggests that taxreductions, rather than deficit reductions,would be a preferable use for the peace divi-dend.’°

~ ~I•~•~

W~1rV((D.11Lf’ ,/4tJJtJ&i:xitt,~:1s1~

In thinking about how the savings from re-duced military spending could be used, it is im-portant to consider how the economy adjusts tounanticipated changes in resource uses. Reducedmilitary spending will produce a negative short-run effect on production, as labor and capitalresources are shifted from military to civilianuses. During the transition period, some re-sources will be unemployed or underemployed.

Previous disarmaments have been associatedwith sizable reductions in economic activity.~°

From the first quarter of 1945 to the first quar-ter of 1946 (peak to trough), for example,nominal GNP fell at a seasonally adjusted an-nualized rate of $22.8 billion or 10.3 percent.These numbers understate the magnitude of thedecline in output as, during this period, therewas a considerable acceleration in inflation.” Inreal terms, GNP fell 18 percent over this period,and it was not until the third quarter of 1952that the level of real GNP had fully recovered.Although this decline in real GNP is large, it isan overstatement of the drop in national wel-fare. While the level of employment fell sub-stantially, the unemployment rate rose very little -

Instead, a substantial number of workers, partic-ularly women, voluntarily withdrew from thelabor force.

The transition to peacetime after WWII wasfacilitated, in part, by government policies. Taxreductions and transfer payments (unemploy-ment and veteran benefits) left disposable (netof taxes) income nearly unaffected by the mas-sive reduction in military spending. Thus, de-mand for consumption goods rose to offset par-tially the decline in military demand.

The sharp decline in military spending thatfollowed the end of the Korean War was asso-ciated with a mild recession. From the secondquarter of 1953 to the second quarter of 1954(peak to trough), real GNP fell 3.2 percent. De-clines in defense spending and other federalgovernment expenditures, combined with inven-tory decumulations, were the driving forceshere. By the first quarter of 1955, however, realGNP had climbed well above its previous peak.

I i ~.

flit/al. Pasts

The aggregate adjustment cost for any reduc-tion in military spending can be measured bythe real value of resources (labor and capital)left idle involuntarily during the transition. Fora given cut in defense spending, the magnitude

28See Barro (1979). Also see Garfinkel (199Gb) for an exten-sion of this theory to include conscription as an additionaltool for financing public expenditures to avoid the distor-tions of income taxes, particularly during periods of severemilitary needs.

“In this view, deficits are necessary to smooth out thedistortionary effects associated with taxes. Hence, a tem-porary increase in government spending should be financedwith debt and a temporary decrease in government spend-ing should result in a budget surplus; this tax-smoothingview of debt creation predicts that deficits are temporaryphenomena. Although historical evidence supports this

positive theory of debt creation—see Barro (1979), forexample—it is unclear whether the current deficit is only atemporary phenomenon. Indeed, the magnitude and per-sistence of the peacetime deficits during the 1980s are un-precedented in U.S. history.

‘°SeeBolton (1966) and references cited therein for a moredetailed examination of these periods of disarmament.Much of the discussion here draws from this work. Dataare taken from Balke and Gordon (1986).

3hThis acceleration was driven, in part, by the removal ofprice controls in 1946.

of these costs depends on the speed with whichlabor and capital resources can be transformedto meet new demands.

The speed of resource transformation, in turn,depends on the degree of specialization ofresources used in the military sector. This spe-cialization has two dimensions. First, certain in-dustries, occupations and firms are highly de-pendent on military demand. Second, militaryproduction is highly concentrated in severalregions of the United States. Such specializationwill slow the adjustment process.

A given reduction in military demand nowmight generate relatively greater adjustmentcosts than those associated with large-scale dis-armaments following wartime periods. Duringwartime periods, resources normally used toproduce nondefense goods are mobilized quick-ly and, presumably, on a temporary basis; afterthe war, resources are rechanneled easily intotheir original civilian productive activities. Incontrast, during peacetime defense firms andtheir employees expect that demand for theirproduct is essentially permanent. To the extentthat these firms and employees have a compara-tive advantage in the production of defensegoods, they are less likely either to diversifytheir operations into civilian markets or be ableto do so in the event of an unanticipated perma-nent reduction in military spending.”

nl(/Io.1l];r:xJri .~yJ’j~Jipr[%z1/:

till (I ZIP .15/IS

To evaluate society’s options for using the sav-ings from reduced military spending, we mustaddress two related economic issues. ‘I’he firstissue, already discussed, concerns what are thebest uses of the dividend or the new “highest-valued” uses of the resources previously used inthe military (presumably their previous highest-valued uses). The second issue concerns how torechannel resources efficiently from their mili-tary uses to their new highest-valued uses.

Some people have advocated establishing publicprograms—for example, training programs—tolessen the costs of adjustment borne solely bythose closely linked to the military sector. A billintroduced recently by Senator Pell (S.209 7), forexample, seeks to establish a program throughwhich grants would be made to assist state andlocal governments in developing economic ad-justment plans—for example, job retraining andfinding alternative uses for defense facilities.These grants would be funded, in part, from thesavings from reduced military spending.” Anoth-er bill introduced by Senator Coats (S.2682) isintended to aid defense contractors in diversify-ing their operations into nondefense markets.Through tax incentives, this bill would encouragedefense contractors and their employees to adoptemployee stock ownership plans (ESOPs) to fi-nance the corporate restructuring necessary toadjust to the reduction in military demand.

These programs are aimed at distributing theadjustment costs and the benefits of reducedmilitary spending equitably; however, they areunlikely to effect an efficient reallocation ofresources.’4 Consider, for example, a programthat increases public nondefense expenditureson goods that are most easily produced by thecapital and labor resources originally employedfor the production of defense goods. While thisprogram might well limit the adverse impact ofreduced military spending otherwise borne bythose firms and individuals highly dependent onmilitary demand, it is clearly inefficient fromthe nation’s point of view. Unless increasedspending on these other goods were deemeddesirable on a permanent basis, this policywould not provide firms and individuals withthe incentives to channel their resources to newhigher-valued uses. Instead, it would merelyprolong the process of adjustment and delay therealization of the full benefits from a perma-nent reduction in military spending.

Nevertheless, the redistributive effects ofreduced military spending should not be

“In contrast, one might believe that defense contractors,having learned from past experience with sharp declinesin military demand, would have diversified their operationsto exploit commercial opportunities. While such diversifica-tion would provide insurance against large losses to thesefirms and their employees in the event of an unexpecteddecline in military demand, past efforts in this directionhave not been particularly successful. See Weidenbaum(1973) and Ellis and Schine (1990).

their firms unless a contract has been canceled. Thestates of Washington and California already have initiatedadjustment plans. See Ellis and Schine (1990).

‘4Although the evidence on the effectiveness of manpowerprograms (for example, the Manpower Development andTraining Act) is mixed, some studies find that manpowerpolicies have been successful in raising the earnings oftraining program participants. See, for example,Ashenfelter (1978).

“Representative Boxer’s proposal (HR5327) is similar;however, it would penalize defense contractors who close

dismissed as unimportant or irrelevant in choos-ing how the peace dividend ultimately will beused. The question of who reaps the gains andwho bears the costs of an unanticipated reduc-tion in military spending is an important aspectof the problem and will play an important rolein the solution.

P5/111)5/S

This article has examined some possible ef-fects of a permanent reduction in military spen-ding. In principle, the present discounted valueof the implied dividends from such a reduction,in terms of increased consumption and invest-ment opportunities, could be substantial.Through increased private and public invest-ment, reduced military spending implies greatereconomic growth and, hence, greater consump-tion and investment opportunities in the future.The important economic questions are, How canthese resources be reallocated efficiently to non-military uses? and, How can we identify whatthese uses should be? This article has introduc-ed and discussed the economic issues that mustbe addressed in answering these questions;much further analysis and discussion will clear-ly be needed before these questions can beanswered adequately.

Of course, given the recent course of eventsin the Middle East, the reduction in militaryspending in the near future might not be largeenough to generate any sizable dividend. Thus,debate over whether the savings from reducedmilitary spending should be used to reduce thepublic deficit, redistributed to taxpayersthrough tax cuts or be used to rebuild the in-frastructure might seem premature. Becausemany communities, firms and individuals are af-fected by even small reductions in militaryspending, however, the “micro” costs of theseadjustments will not be ignored in the politicaldecision-making process.

But temporary transitional costs do not justifyabandoning the effort to reduce the amount ofresources allocated to military spending. More-over, the Middle East situation is not a perma-nent obstacle to realize a large dividend in thefuture. While cuts in defense spending are notexpected to be particularly large now, a resolu-tion of the Middle East conflict will permit amuch larger dividend in the future.

Adams, Gordon, and David Gold. Defense Spending and theEconomy: Does the Defense Dollar Make a Difference?(Washington, D.C.: Defense Budget Project at the Centeron Budget and Policy Priorities, July 1987).

Aschauer, David. “Does Public Capital Crowd Out PrivateCapital?” Journal of Monetary Economics (September1989a), pp. 171-88.

_______- “Is Public Expenditure Productive?” Journal ofMonetary Economics (March 198gb), pp. 177-200.Ashenfelter, Orley. “Estimating the Effect of Training Pro-

grams on Earnings,”Review of Economics and Statistics(February 1978), pp. 47-57.

Balke, Nathan S. and Robert J. Gordon. “Historical Data,” inRobert J. Gordon, ed., The American Business Cycle: Con-tinuity and Change (Chicago: The University of ChicagoPress, 1986), pp. 781-850.

Barro, Robert J. “The Ricardian Approach to BudgetDeficits,” Joumal of Economic Perspectives (Spring 1989),pp. 37-54.

_______- “Output Effects of Government Purchases’ Jour-nal of Political Economy (December 1981), pp. 1086-121.

_______- “On the Determination of the Public Debt:’ Journalof Political Economy (October 1979), pp. 940-71.

Bolton, Roger E. “Defense Spending: Burden or Prop?” inRE. Bolton, ed., Defense and Disarmament (Prentice-Hall,Inc., 1966), pp. 1-53.

Boulding, Kenneth E. “The Impact of the Defense Industryon the Structure of the American Economy,” in BernardUdis, ed., The Economic Consequences of Reduced MilitarySpending (Toronto: D.C. Heath and Company, 1973), pp.225-52.

Browne, Lynn E. “Defense Spending and High TechnologyDevelopment: National and State Issues:’ New EnglandEconomic Review, Federal Reserve Bank of Boston(September/October 1988), pp. 3-22.

Chrystal, K. Alec, and Daniel L. Thornton. “TheMacroeconomic Effects of Deficit Spending: A Review,” thisReview (November/December 1988), pp. 48-60.

Cullison, William E. “Is Saving Too Low in the UnitedStates?” Federal Reserve Bank of Richmond EconomicReview (May/June 1990), pp. 20-35.

Dowd, Maureen. “Bush Says Military Can Be Cut 25% in 5Years’ New York Times, August 3, 1990.

Du Boff, Richard B. “What Military Spending Really Costs,”Challenge (SeptemberlOctober 1989), pp. 4-10.

Dumas, Lloyd J. “National Security and Economic Delu-sion:’ Challenge (March/April 1987), pp. 28-33.

Dunne, Paul, and Ron Smith. “Military Expenditure andUnemployment in the OECD,” Delänce Economics: ThePolitical Economy of Defence, Disarmament and Peace, Vol.1, No. 1 (1990), pp. 57-74.

Edelstein, Michael. “What Price Cold War: Military Expen-ditures and Private Investment in the U.S., 1890-1980,”mimeo (January 1989).

Ellis, James E., and Eric Schine. “Who Pays For Peace?”Business Week (July 2, 1990), pp. 64-70.

Garfinkel, Michelle R. “Arming as a Strategic Investment in aCooperative Equilibrium,” American Economic Review(March 1990a), pp. 50-68.

_______- “The Role of the Military Draft in Optimal FiscalPolicy’ Southern Economic Journal (January 199Gb),pp. 718-31.

Gold, David. The Impact of Defense Spending on Investment, _______. “Military Expenditure and Capitalism: A Reply:’Productivity and Economic Growth (Washington, D.C.: Cambridge Journal of Economics (September 1978),Defense Budget Project at the Center on Budget and pp. 299-304.Policy Priorities, February 1990). Stevenson, Richard W. “Suppliers Brace for Arms Cuts:’

Melman, Seymour. “Economic Consequences of the Arms New York Times, June 18, 1990.Race: The Second-Rate Economy,” American Economic Thornton, Daniel L. “Do Government Deficits Matter?” thisReview (May 1988), pp. 55-59, Review (SeptemberlOctober 1990), pp. 25-39.

“Peace Dividend or Peace Recession?” The Economist (April Uchitelle, Louis. “Economy Expected to Absorb Effects of7, 1990), pp. 31-32. Military Cuts:’ New York Times (April 15, 1990).

U.S. Congressional Budget Office. Defense Spending and thePennar~Karen, and Michael J. Mandel. “The Peace Economy (Government Printing Office, February 1983).Economy: How Defense Cuts Will Fuel America’s Long-Term Prosperity:’ Business Week (December 11, 1989), - Budgetary and Military Effects of a Treaty Limitingpp. 50-55. Conventional Fbrces in Europe, Special Study (January

1990).Riddell, Tom. “U.S. Military Power, the Terms of Trade, and

the Profit Rate:’ American Economic Review (May 1988), Weidenbaum, Murray. “Defense Outlays Have Declining Im-pp. 60-65. pact on Economy:’ Christian Science Monitor February 7,

1990.Schultze, Charles L. “Using the Peace Dividend to Increase

Saving’ Challenge (MarchlApril 1990), ~ 11-17. - “Industrial Adjustments to Military ExpenditureShifts and Cutbacks:’ in Bernard Uris, ed., The Economic

Smith, Ron P “Military Expenditure and Capitalism:’ Cam- Consequences of Reduced Military Spending (Toronto: D.C.bridge Journal of Economics (March 1977), pp. 61-76. Heath and Company, 1973), pp. 253-87.