Embed Size (px)

Citation preview

The Economic Way of Thinking

What is economics? • Economics is the study of how

people choose to use their limited resources to satisfy their seemingly unlimited wants.

Why is the study of economics important? • Economics is about how and why we make choices.

• It is not just about money. It concerns how we allocate scarce resources.

• Its study helps broaden our understanding of events in the news and how they affect you.

How does economics affect your life?

Describe what economists do. • Economists collect and interpret

information about economic activity.

• They conduct surveys, construct models and make predictions about how we use our resources and spend money.

• They also analyze the possible and actual economic effects of government actions.

• They often specialize in different branches of micro- and macroeconomics.

What is microeconomics?

• Microeconomics is the study of the economy at the level of individuals, households, and businesses.

• It is concerned with the supply and demand of goods and services, the determinants of price, consumer behavior, and the different types of businesses.

What is macroeconomics? • Macroeconomics is the study

of the workings of the economy as a whole.

• It is concerned with important aspects of national and global economic activity, such as GDP, unemployment, economic growth, national debt and international trade.

• It is particularly interested in the effect of government actions on economic activity.

What is positive economics? •Positive economics is the branch of economics that

uses objective analysis to find out how the economy actually works.

• It is concerned with studying the economy as it is, not as it ought to be.

What is normative economics? • Normative economics is the

branch of economics that makes value judgments about the economy.

• Its focus is on which economic policies should be implemented.

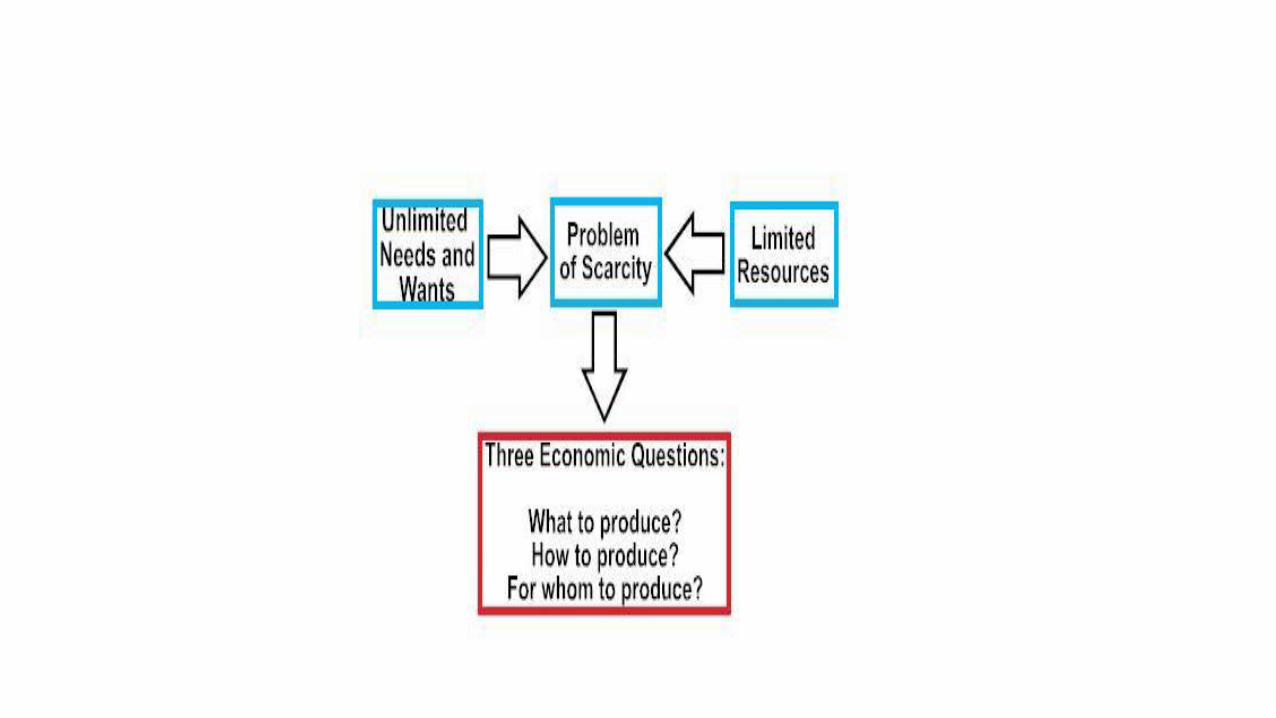

What is scarcity? •Scarcity is the condition that results from the fact that people have limited resources but unlimited wants.

What is “opportunity cost?” • Opportunity cost is the

value of the next best alternative that is given up when making a choice.

• It is a measure of what you must give up in order to get what you want.

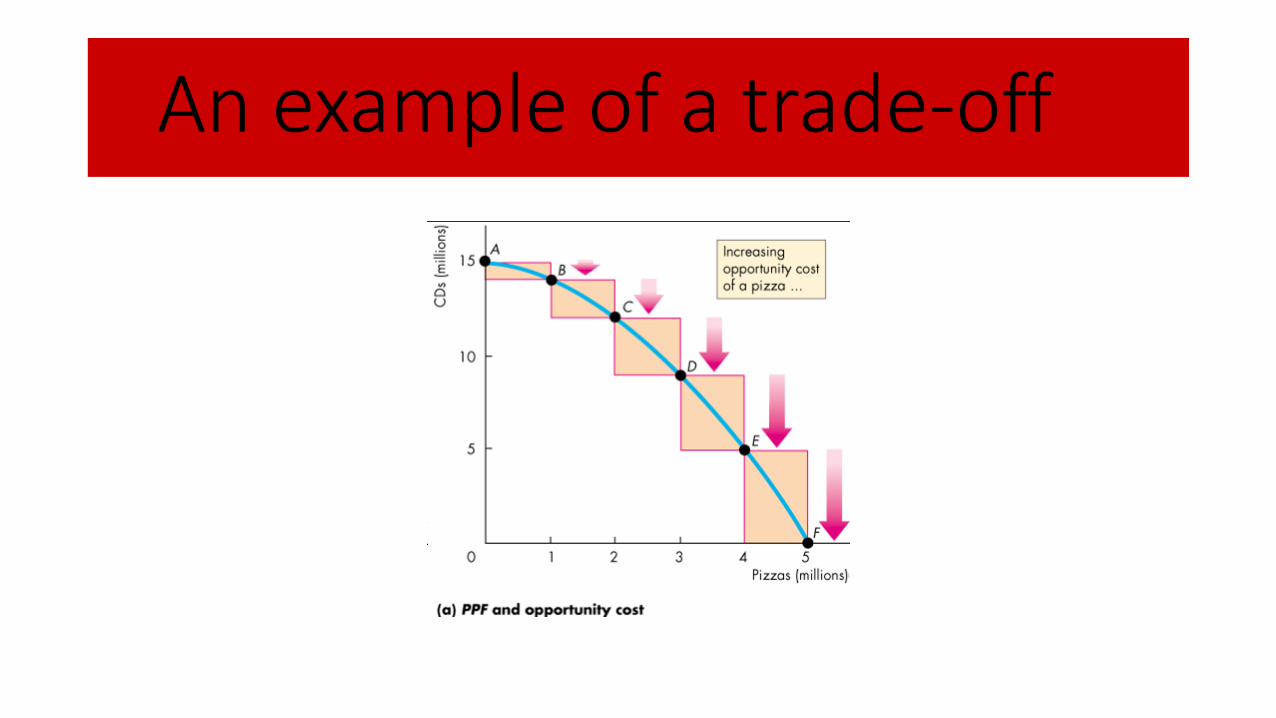

Explain how scarcity (of goods, e.g.) forces choices/ trade-offs.

• Limited resources force people to make choices and face trade-offs when they choose

• Sometimes these choices are binary in nature. You pick either A or B. If you pick A, you do not get any B.

• Other times it is a question of how many of each item you choose. Decisions are based on one more or one less of some item. In this instance you can be said to be deciding at the margin. This is sometimes referred to as marginal utility.

An example of a trade-off

Identify the 4 resource types used to produce goods and services in an economy?

•Land

•Labor

•Capital (i.e., Tools, Machines, and Buildings)

•Entrepreneurship (or Entrepreneurial Skills)

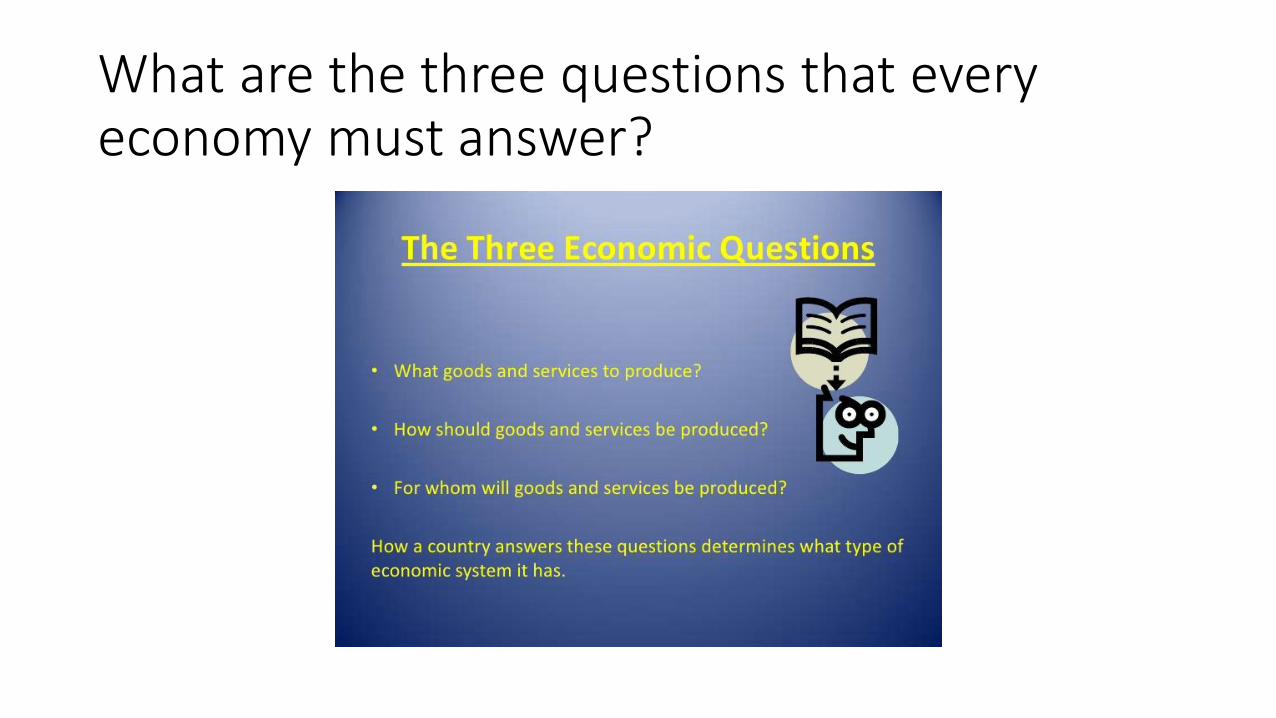

What are three questions that every economy must answer?

What are the three questions that every economy must answer?

What is an explicit cost? • An explicit cost is a direct payment made to others in the course of

running a business.

• Wages, rents, utility payments and other costs for inputs are explicit costs.

What is an implicit cost?

• An implicit cost refers to the opportunity cost of business decisions.

• An example of an implicit cost is the interest income that the owner of a business would get from his money if he were not to put it into his business.

How do economists describe and/or measure an economy?