Embed Size (px)

DESCRIPTION

jurnal

Citation preview

DOI: 10.1111/j.1475-679X.2010.00390.xJournal of Accounting Research

Vol. 49 No. 1 March 2011Printed in U.S.A.

The Effect of Mandatory IFRSAdoption on Financial Analysts’

Information Environment

D O N A L B Y A R D , ∗ Y I N G L I , † A N D Y O N G Y U ‡

Received 8 May 2009; accepted 15 October 2010

ABSTRACT

This paper examines the effect of the mandatory adoption of International Fi-nancial Reporting Standards (IFRS) by the European Union on financial ana-lysts’ information environment. To control for the effect of confounding con-current events, we use a control sample of firms that had already voluntarilyadopted IFRS at least two years prior to the mandatory adoption date. We findthat analysts’ absolute forecast errors and forecast dispersion decrease relativeto this control sample only for those mandatory IFRS adopters domiciled incountries with both strong enforcement regimes and domestic accountingstandards that differ significantly from IFRS. Furthermore, for mandatoryadopters domiciled in countries with both weak enforcement regimes anddomestic accounting standards that differ significantly from IFRS, we find

∗Baruch College—CUNY; †The George Washington University; ‡University of Texas atAustin. We thank an anonymous referee and the editor, Richard Leftwich, for many help-ful suggestions and comments. We also thank Bill Baber, Anna Brown, Jay Dahya, MasakoDarrough, Paquita Davis-Friday, Angela Gore, Nicole Heron, Gilles Hilary, Thomas Jeanjean,Sok-Hyon Kang, Krishna Kumar, Fred Lindahl, Carol Marquardt, Yun Zhang and seminarparticipants at George Washington University, the 2008 AAA annual meetings, and the 2010European Accounting Association annual meetings. Additionally, we are also grateful to MariaHelena Almeida, Ingrid Engshagen, Julie Erhardt, Frank-Thomas Graefe, David Grunberger,Virpi Haaramo, Jitka Hrudova, Liza McAndrew-Mobery, Paul Munter, Emmanuel Paret, Flem-ming Petersen, and Siw-Mette Thomassen for providing valuable input regarding institutionaldetails. We acknowledge the contribution of IBES International Inc. for providing earningsper share forecast data; Donal Byard also gratefully acknowledges the financial support pro-vided by a PSC-CUNY grant from the City University of New York (PSC-CUNY # 61815-00 39).

69

Copyright C©, University of Chicago on behalf of the Accounting Research Center, 2010

70 D. BYARD, Y. LI, AND Y. YU

that forecast errors and dispersion decrease more for firms with stronger in-centives for transparent financial reporting. These results highlight the im-portant roles of enforcement regimes and firm-level reporting incentives indetermining the impact of mandatory IFRS adoption.

1. Introduction

The adoption of International Financial Reporting Standards (IFRS) in Eu-rope and around the world represents perhaps the most important account-ing regulatory change in recent years. In 2002, the European Union (EU)required all firms listed in its 27 member countries to switch to IFRS forfinancial reporting purposes for fiscal years beginning on or after January1, 2005. This move forced over 7,000 public companies to replace variousdomestic accounting standards with IFRS. Despite the widespread manda-tory adoption of IFRS, there is relatively little evidence as to the relatedeconomic consequences (see Ball [2006], Daske et al. [2008]).

This study examines the effect of the EU-wide mandatory adoption ofIFRS on financial analysts’ information environment. Ex ante, it is unclearhow mandatory IFRS adoption would affect analysts’ information environ-ment. On the one hand, IFRS adoption may improve analysts’ informationenvironment by enhancing disclosure and transparency or by increasingthe comparability of financial reports (e.g., Bae, Tan, and Welker [2008],Barth, Landsman, and Lang [2008]). On the other hand, if the “one sizefits all” IFRS are suboptimal relative to firms’ domestic accounting stan-dards in reflecting firm performance, IFRS adoption may render financialreporting less informative, thereby reducing the quality of analysts’ infor-mation. In addition, earnings may become more volatile and thus moredifficult for analysts to forecast under IFRS ( Ball [2006]). However, it is alsopossible that mandatory IFRS adoption may have little impact on analysts’information environment. If mandatory adopters already optimize their fi-nancial reporting strategies under their domestic standards, they may lackincentives to rigorously implement IFRS. This lack of incentive can be fur-ther exacerbated by the weak enforcement regimes in many EU countries.As a result, firms may adopt IFRS in name only and make little change totheir financial reporting practices. Further, even if IFRS are properly imple-mented, the adoption effect should be small in EU countries with domesticaccounting standards similar to IFRS (Ashbaugh and Pincus [2001]).

We employ a difference-in-difference research design to examine the im-pact of mandatory IFRS adoption. Our test sample includes 1,168 manda-tory IFRS adopters in Europe. To control for the effect of concurrent con-founding events such as the EU’s ongoing efforts to strengthen the enforce-ment of accounting standards (Hail and Leuz [2007]), we identify a controlsample of 250 European firms that had already voluntarily adopted IFRS atleast two years prior to the mandatory adoption date. Because these con-trol firms use IFRS both before and after mandatory adoption, changes forthese firms likely reflect the impact of concurrent economic and regulatory

THE EFFECT OF MANDATORY IFRS ADOPTION 71

changes, but not mandatory IFRS adoption. To test the impact of manda-tory IFRS adoption, we focus on the difference between the test and controlfirms in the change in analysts’ information environment from the two-yearpre-mandatory-adoption period to the two-year post-mandatory-adoption pe-riod. We capture the properties of analysts’ information environment usingabsolute forecast errors, forecast dispersion, and analyst following, wheresmaller absolute forecast errors, smaller forecast dispersion, or higher ana-lyst following generally indicates a richer information environment.

We perform three levels of analysis: (1) an examination of the averageeffect of mandatory IFRS adoption, (2) an examination conditioned oncountry-level institutional characteristics, and (3) an examination condi-tioned on firm-level reporting incentives. In the first analysis, we find thatmandatory adopters exhibit no statistically significant change relative tothe control firms in analysts’ forecast errors, forecast dispersion, or ana-lyst following, thus providing no evidence that mandatory IFRS adoptionchanges analysts’ information environment on average. In the second anal-ysis, we partition mandatory adopters into groups based on the strength ofcountry-level enforcement regimes and the extent to which their domesticaccounting standards differ from IFRS. For mandatory adopters domiciledin countries with both strong enforcement regimes and domestic account-ing standards that differ substantially from IFRS, we find statistically andeconomically significant decreases relative to the control firms in both fore-cast errors and dispersion. In contrast, we find no statistically significant dif-ferences between the control firms and the mandatory adopters based inother countries. In the third analysis, we explore how firm-level incentivesfor transparent financial reporting affect the adoption effect. To increasethe power of our test, we focus on mandatory adopters domiciled in coun-tries with both weak enforcement environments and domestic accountingstandards that differ significantly from IFRS. For such firms, the changesrequired by IFRS adoption are substantial, and weak country-level enforce-ment allows firm-level reporting incentives to play a relatively greater rolein shaping reporting outcomes (Daske et al. [2008], Holthausen [2009]).We find larger decreases in analysts’ forecast errors and dispersion forfirms with stronger reporting incentives (i.e., more growth opportunities,a smaller proportion of closely held shares, or higher-quality auditors). Inaddition to these three analyses, further tests suggest that mandatory IFRSadoption improves analysts’ information environment by increasing bothanalysts’ public and private information. Taken together, our results sug-gest that the adoption effect is uneven across countries and firms, and thatanalysts’ information environment improves only when the changes man-dated by IFRS are both substantial and rigorously enforced.

Our findings highlight that simply mandating IFRS is not sufficient toensure actual changes to firms’ financial reporting practices. Our studymay be of interest to policy makers in evaluating the costs and benefitsof mandatory IFRS adoption and to financial statement users who wish tounderstand the effect of mandatory IFRS adoption.

72 D. BYARD, Y. LI, AND Y. YU

Two caveats are in order. First, our control sample has some limitations.Our results would understate the adoption effect if the changes for thecontrol firms are attributable to either concurrent changes in IFRS require-ments or positive externalities arising from mandatory IFRS adoption. Onthe other hand, if the control sample does not fully control for contempo-raneous changes unrelated to mandatory IFRS adoption (e.g., due to somefundamental differences between the test and control samples), our resultswould overstate the adoption effect. Second, we examine only two yearsfollowing the adoption, so our results may not shed light on the long-termadoption effect. It is possible that in the long run, IFRS adoption may resultin an across-the-board improvement for all firms.

2. Hypotheses

Our first hypothesis, stated in the null form, is:

H1: On average, the EU-wide mandatory adoption of IFRS is not associ-ated with a change in the quality of analysts’ information environment.

We next exploit cross-country differences to identify countries where theadoption effect is likely to be greater. The adoption effect, if any, is likely tobe more pronounced for mandatory adopters domiciled in countries withboth strong enforcement regimes and domestic accounting standards thatdiffer substantially from IFRS.1 For these firms, mandatory IFRS adoptionrequires substantial accounting changes, while strong enforcement forcesfirms to comply with these changes. Our second hypothesis, stated in thenull form, is thus:

H2: In countries with both strong enforcement regimes and domesticaccounting standards that differ significantly from IFRS, the EU-widemandatory adoption of IFRS is not associated with a change in the qual-ity of analysts’ information environment.

Holding country-level enforcement constant, the adoption effect likelyvaries with firm-level incentives for transparent financial reporting. If IFRSadoption improves financial reporting, we expect firms with stronger re-porting incentives to implement IFRS more rigorously, leading to a greaterimprovement in analysts’ information environment for these firms. Con-versely, if IFRS adoption does not improve financial reporting, we expectno relation between firm-level reporting incentives and the change in ana-lysts’ information environment. Therefore, our third hypothesis examineshow the adoption effect varies with firm-level reporting incentives. Becausefirms’ reporting incentives likely play a more prominent role in determin-ing reporting outcomes when country-level enforcement is weak and the

1 However, as long as there is discretion in financial reporting and firms have differingreporting incentives, strong enforcement will not eliminate all variation in reporting qualityacross firms (Leuz [2006]).

THE EFFECT OF MANDATORY IFRS ADOPTION 73

changes required by IFRS are larger, we focus on firms domiciled in coun-tries with both weak enforcement and domestic accounting standards thatdiffer significantly from IFRS. Our third hypothesis, stated in the null form,is thus:

H3: For firms domiciled in countries with both weak enforcement anddomestic accounting standards that differ significantly from IFRS, theimpact of the EU-wide mandatory adoption of IFRS on analysts’ infor-mation environment is not related to firm-level reporting incentives.

3. Sample Selection and Study Design

3.1. SAMPLE SELECTION

We obtain analysts’ forecast data from the IBES international (split unad-justed) database and accounting and market data from the Global Compus-tat or Datastream/Worldscope database. European firms subject to manda-tory IFRS adoption were required to switch to IFRS for financial report-ing purposes for fiscal years beginning on or after January 1, 2005. Sincewe study the change in analysts’ information environment after mandatoryIFRS adoption, we divide the sample period into two reporting regimes: thepre-mandatory-adoption window is the last two fiscal years a firm reportedusing its domestic accounting standards, while the post-mandatory-adoptionwindow is the first two fiscal years a firm reported using IFRS. For example,for a December year-end firm, the pre-mandatory-adoption window is 2003and 2004, while the post-mandatory-adoption window is 2005 and 2006.

We begin our sample-selection process by selecting from I/B/E/S allpublic companies domiciled in Europe with analysts’ annual earnings fore-casts for our four-year sample period.2 We exclude firms that were cross-listed in the United States as American Deposit Receipts (ADRs) during oursample period based on the ADR databases of the Bank of New York andCitibank. We also exclude firms that changed their country of domicile orprimary exchange listing during our sample period. We require that annualearnings announcements be made no later than 240 calendar days after thefiscal year-end. For each firm-year, we retrieve all annual earnings forecastsissued during the 12-month period prior to the year-end from each analystcovering the firm. If an analyst issues more than one annual forecast fora firm-year, we retain only the last forecast. We further require each ana-lyst to issue at least one annual forecast for a firm within both the pre- andpost-mandatory-adoption windows. Thus, our sample is composed of a con-stant set of analyst-firm pairs matched across the pre- and post-mandatory-adoption windows. This alleviates potential concerns that any changesin analysts’ information environment are driven by changes in sample

2 Our sample includes two non-EU-member countries (Norway and Switzerland) that alsomandated IFRS adoption. Our results are robust to excluding these two countries.

74 D. BYARD, Y. LI, AND Y. YU

composition, as both firm and analyst characteristics can affect propertiesof analysts’ forecasts.

Next, to identify mandatory IFRS adopters, we obtain information onfirms’ accounting standards from both Global Compustat and Datastream/Worldscope, and retain firms that reported under their domestic account-ing standards during the two-year pre-mandatory-adoption window. WhenGlobal Compustat and Datastream/Worldscope provide conflicting infor-mation as to which accounting standards a firm used, we verify data fromthe firm’s annual reports. Finally, we exclude firms with missing accountingor market data from both Global Compustat and Datastream/Worldscopethat are needed to construct the variables we use in our analyses (discussedbelow). Our final test sample contains 1,168 firms.

To control for the impact of potentially confounding concurrent events,we select a control sample of European firms that voluntarily adopted IFRSat least two years before the mandatory adoption deadline. We also requirethe control sample to have a constant analyst-firm composition over the pre-and post-mandatory-adoption windows. For each voluntary adopter, we de-fine the pre-mandatory-adoption window as the last two fiscal years endingbefore mandatory adoption, and the post-mandatory-adoption window asthe first two fiscal years beginning on or after January 1, 2005, the manda-tory adoption date. The two windows for the control sample are thus con-current with the windows for the mandatory adopters. All other data re-quirements for the control sample are the same as those for the test sample.The control sample contains 250 firms.3

The control firms use IFRS during both windows, while the test firmsswitch accounting standards between the two windows. To the extent thatIFRS requirements are unchanged around the mandatory adoption, thechange for the control firms likely reflects the impact of concurrent eco-nomic and regulatory changes, but not the impact of mandatory IFRSadoption. To identify the impact of mandatory IFRS adoption, we there-fore focus on the difference in the change from the pre- to post-mandatory-adoption window between the test and control firms.

The first two columns of table 1, panel A, provide the distributions of ourtest and control samples by country. The test (control) sample representsfirms from 20 (15) different countries, with heavy concentrations in theUnited Kingdom and France (Germany and Switzerland).4 We note thatthe country distributions of our test and control samples differ substantially,so we later explore the robustness of our results to this feature of the data.

3 December year-end firms account for 75% (88%) of the test (control) sample.4 Our control sample includes firms domiciled in European countries (i.e., Hungary,

France, Poland, and Sweden) that did not allow voluntary IFRS adoption for domestic listedfirms. We inspected the annual reports of these firms to confirm that these firms voluntar-ily released IFRS financial statements in addition to the required domestic GAAP financialstatements in the pre-mandatory-adoption period. Our results are, however, robust to remov-ing these firms from our control sample. In addition, our inferences remain unchanged if weexclude UK firms from both the test and control samples.

THE EFFECT OF MANDATORY IFRS ADOPTION 75

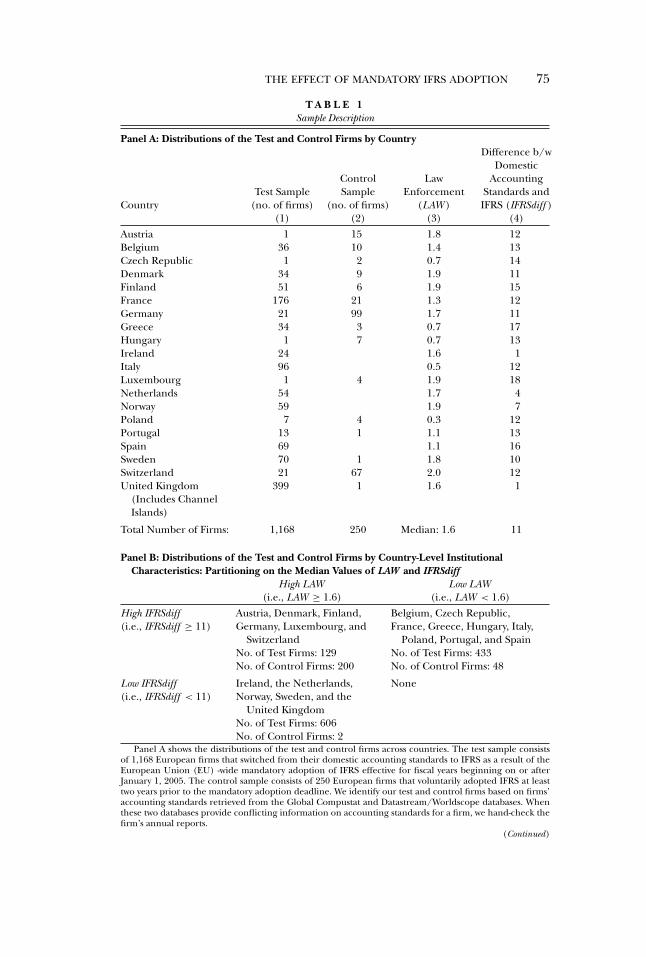

T A B L E 1Sample Description

Panel A: Distributions of the Test and Control Firms by Country

CountryTest Sample

(no. of firms)

ControlSample

(no. of firms)

LawEnforcement

(LAW )

Difference b/wDomestic

AccountingStandards andIFRS (IFRSdiff )

(1) (2) (3) (4)Austria 1 15 1.8 12Belgium 36 10 1.4 13Czech Republic 1 2 0.7 14Denmark 34 9 1.9 11Finland 51 6 1.9 15France 176 21 1.3 12Germany 21 99 1.7 11Greece 34 3 0.7 17Hungary 1 7 0.7 13Ireland 24 1.6 1Italy 96 0.5 12Luxembourg 1 4 1.9 18Netherlands 54 1.7 4Norway 59 1.9 7Poland 7 4 0.3 12Portugal 13 1 1.1 13Spain 69 1.1 16Sweden 70 1 1.8 10Switzerland 21 67 2.0 12United Kingdom

(Includes ChannelIslands)

399 1 1.6 1

Total Number of Firms: 1,168 250 Median: 1.6 11

Panel B: Distributions of the Test and Control Firms by Country-Level InstitutionalCharacteristics: Partitioning on the Median Values of LAW and IFRSdiff

High LAW Low LAW(i.e., LAW ≥ 1.6) (i.e., LAW < 1.6)

High IFRSdiff Austria, Denmark, Finland, Belgium, Czech Republic,(i.e., IFRSdiff ≥ 11) Germany, Luxembourg, and

SwitzerlandFrance, Greece, Hungary, Italy,

Poland, Portugal, and SpainNo. of Test Firms: 129 No. of Test Firms: 433No. of Control Firms: 200 No. of Control Firms: 48

Low IFRSdiff Ireland, the Netherlands, None(i.e., IFRSdiff < 11) Norway, Sweden, and the

United KingdomNo. of Test Firms: 606No. of Control Firms: 2

Panel A shows the distributions of the test and control firms across countries. The test sample consistsof 1,168 European firms that switched from their domestic accounting standards to IFRS as a result of theEuropean Union (EU) -wide mandatory adoption of IFRS effective for fiscal years beginning on or afterJanuary 1, 2005. The control sample consists of 250 European firms that voluntarily adopted IFRS at leasttwo years prior to the mandatory adoption deadline. We identify our test and control firms based on firms’accounting standards retrieved from the Global Compustat and Datastream/Worldscope databases. Whenthese two databases provide conflicting information on accounting standards for a firm, we hand-check thefirm’s annual reports.

(Continued)

76 D. BYARD, Y. LI, AND Y. YU

T A B L E 1 — Continued

Panel B shows the partition of our sample firms into groups based upon two country-level institutionalvariables: LAW and IFRSdiff . LAW is the measure of the quality of a country’s legal and enforcement envi-ronment for 2005 from Kaufmann, Kraay, and Mastuzzi [2007]. Higher values of LAW represent strongerlegal and enforcement regimes. IFRSdiff is the GAAP difference measure from Bae, Tan, and Welker [2008,table 1]. IFRSdiff measures differences between countries’ domestic accounting standards and IFRS along21 key accounting items; higher values of IFRSdiff indicate greater differences. We partition countries basedon the median values of IFRSdiff and LAW , which are 11 and 1.6, respectively. This partitioning scheme re-sults in three country groups: (1) a High LAW-High IFRSdiff group; (2) a Low LAW-High IFRSdiff group;and (3) a High LAW-Low IFRSdiff group. Note that no country has below-median values of both LAW andIFRSdiff .

3.2. MEASURING THE QUALITY OF ANALYSTS’ INFORMATION ENVIRONMENT

We use three measures to capture analysts’ information environment fora firm: absolute forecast errors, forecast dispersion, and the number of an-alysts following a firm. We focus on these three proxies because they aremore direct measures of the impact of mandatory IFRS adoption on ana-lysts’ information environment than other analyst-related measures (e.g.,stock recommendations, forecast revisions, and forecast frequency). Forexample, analysts’ stock recommendations reflect both accounting andnonaccounting information, and there is no clear benchmark to assess theaccuracy of stock recommendations. Price reactions to stock recommen-dations or forecast revisions can be difficult to interpret, because if IFRSadoption enhances firm disclosures, this could result in an increase or a de-crease in market reactions, depending on whether more disclosures primar-ily crowd out analysts’ private information or help analysts develop moreunique insights. Similarly, because forecast timeliness reflects the amountof analysts’ private information and forecast frequency captures analysts’effort to generate private information, it is debatable whether an increasein forecast frequency or timeliness indicates an improvement or a deterio-ration in analysts’ information environment.

For each firm, we calculate the changes in the three proxies for analysts’information environment between the pre- and post-mandatory-adoptionwindows. We obtain the change in analysts’ absolute forecast error (�AFE)by first calculating analysts’ absolute forecast error (AFEit) for each firm-year as: |Actual Earningsit − Median Forecastit |/Stock Priceit , where ActualEarningsit is the actual I/B/E/S annual EPS for firm i in year t, MedianForecastit is the median of forecasts made by analysts in our sample duringthe 12-month period prior to the fiscal year-end for firm i and year t, andStock Priceit is the stock price of firm i at the beginning of year t.5 We thencompute each firm’s average AFE for the pre- and post-mandatory-adoptionwindows, respectively, and calculate the difference as �AFE . We similarlycompute the change in forecast dispersion (�DISP). For each firm-year,we first calculate forecast dispersion as: Standard Deviation of Forecasts/Stock

5 The results are similar using the mean forecast rather than the median forecast. We win-sorize continuous variables at the 1% and 99% levels to mitigate the influence of outliers.

THE EFFECT OF MANDATORY IFRS ADOPTION 77

Price. We then calculate �DISP as the difference between the averages ofDISP for the pre-and post-mandatory-adoption windows. For each firm-year,we measure analyst following (FOLLOW ) as the total number of analystswho issue at least one annual forecast for that firm-year. Note that we in-clude all analysts following a firm, not just the analysts included in our con-stant analyst-firm sample. For each firm, we then calculate the change inanalyst following, �LogFOLLOW , as the difference in the log of averageanalyst following between the pre- and post-mandatory-adoption windows.6

Because a minimum of two analysts’ forecasts in each firm-year is needed tomeasure dispersion, the sample size is slightly smaller for �DISP than for�AFE and �LogFOLLOW . For ease of exposition, we multiply both �AFEand �DISP by 100.

3.3. TESTING THE AVERAGE EFFECT OF MANDATORY IFRS ADOPTION (H1)

To test H1, we estimate the following model7

�Info. Environmenti = α0 + a1DMANDi + α j �Controlsi + εi , (1)

where the subscript i refers to firm i. The dummy variable DMAND equals one(zero) for the test (control) firms, and �Info. Environment refers to �AFE,�DISP, or �LogFOLLOW . The intercept, α0, captures the change aroundmandatory IFRS adoption for the control firms. The key coefficient of in-terest, α1, captures the difference in the change in analysts’ informationenvironment between the test and control firms and, thus, the impact ofmandatory IFRS adoption.

We control for changes in firm size, analyst following, and forecast hori-zon (i.e., the number of days between the forecast issuing date and the earn-ings announcement date) in the �AFE and �DISP regressions.8 Largerfirms and firms with greater analyst following tend to have smaller fore-cast errors and forecast dispersion (Bhushan [1989]); forecast errors anddispersion also decrease as forecast horizon shortens. We control for thechange in firm size in the �logFOLLOW regression, because larger firmstend to attract a larger analyst following (Bhushan [1989]). To measure thechange in firm size (�logSIZE), we first calculate the beginning-of-the-yearmarket capitalization in U.S. dollars for each firm-year using the exchangerate in effect at the beginning of the year from I/B/E/S. We then compute

6 We use a log transformation to reduce the skewness in FOLLOW . Our results are robustto reestimating the change in analyst following using an ordered-probit model.

7 The results are robust to allowing the coefficients on the control variables to vary betweenthe test and control firms.

8 Our results are robust to including three additional control variables used by Lang andLundholm [1996]: the standard deviation of return on assets, the return-earnings correlation,and earnings surprise based on a random-walk model. We do not include these variables inour reported results because the first two require a long time-series of data to compute, andearnings surprise constructed based on actual earnings is mechanically associated with forecasterrors (Hope[2003]). In addition, our results are also robust to controlling for the change infirm risk, measured by the standard deviation of monthly stock returns.

78 D. BYARD, Y. LI, AND Y. YU

the difference in the log of average market capitalization between the pre-and the post-mandatory-adoption windows.9 Since multiple forecasts mayexist for a firm-year, we first compute the average horizon (i.e., the numberof days between the forecast issuing date and the earnings announcementdate) across all forecasts for that firm-year. Then for each firm, we compute�logHORIZON as the change in the log of average horizon between the pre-and post-mandatory-adoption windows.

3.4. TESTS CONDITIONAL ON COUNTRY-LEVEL INSTITUTIONALCHARACTERISTICS (H2)

We use the “Rule of Law” (LAW ) variable for 2005 from Kaufmann,Kraay, and Mastuzzi [2007] as a proxy for the quality of countries’ legaland enforcement regimes. Higher values of LAW indicate stronger en-forcement. We base our measure of the difference between a country’s ac-counting standards and IFRS on the gaapdiff1 measure of Bae, Tan, andWelker[2008, table 1]. This is a comprehensive measure that captures dif-ferences between domestic accounting standards and IFRS along 21 key ac-counting items. We relabel this measure IFRSdiff to emphasize that it mea-sures differences between domestic accounting standards and IFRS. Highervalues of IFRSdiff indicate greater difference. Columns (3) and (4) of table1, panel A, show the LAW and IFRSdiff scores for each country in our sam-ple.

We classify sample firms into country groups based on the median valuesof LAW (1.6) and IFRSdiff (11) as follows:

(1) a High LAW-High IFRSdiff group (LAW ≥ 1.6 and IFRSdiff ≥ 11),(2) a Low LAW-High IFRSdiff group (LAW ≤ 1.6 and IFRSdiff ≥ 11), and(3) a High LAW-Low IFRSdiff group (LAW ≥ 1.6 and IFRSdiff ≤ 11).

No country is below the median values of both LAW and IFRSdiff . PanelB of table 1 shows the distributions of the test and control firms across thesethree country groups. The numbers of test and control firms are highly un-balanced within the High LAW-Low IFRSdiff and the Low LAW-High IFRSdiffgroups: in the former (latter) group, there are only 2 (48) control firms, farfewer than the 606 (433) test firms. Hence, the distribution of the data re-stricts meaningful comparisons within each group. As a result, we comparemandatory adopters in each of the three country groups with the controlfirms pooled across all countries using the following equation:

�Info. Environmenti = β0 + β1DMANDi ∗ DHLAW −HDIFFi

+β2DMANDi ∗ DLLAW −HDIFFi + β3DMANDi ∗ DHLAW −LDIFFi

+β j �Controlsi + εi , (2)

9 We measure firm size by market value of equity because financial analysts mainly serveequity investors. However, the results are robust to measuring firm size by enterprise value(defined as the sum of market value of equity and book value of debt).

THE EFFECT OF MANDATORY IFRS ADOPTION 79

where the subscript i refers to firm i. �Info. Environment refers to �AFE,�DISP, or �LogFOLLOW . DHLAW −HDIFF is a dummy variable coded one ifa test or control firm is from the High LAW-High IFRSdiff country group;similarly, DLLAW −HDIFF and DHLAW −LDIFF are dummy variables indicating testor control firms from the Low LAW-High IFRSdiff and High LAW-Low IFRSdiffgroups. The controls are the same as in equation (1). The intercept, β0,reflects the change in analysts’ information environment for the controlfirms. The coefficient of interest, β1, reflects the difference between the testfirms in the High LAW-High IFRSdiff group and the control firms. Similarly,β2 (β3) capture the difference between the test firms in the Low LAW-HighIFRSdiff (High LAW-Low IFRSdiff ) group and the control firms.

3.5. TESTS OF FIRM-LEVEL REPORTING INCENTIVES (H3)

Prior research (e.g., Ashbaugh [2001], Pagano et al. [2002], Leuz [2006],Christensen, Lee, and Walker [2007], Daske et al.[2007], Barth, Landsman,and Lang [2008]) suggests that firms that: (1) are more profitable, (2) havemore growth opportunities, (3) are more highly leveraged, (4) have a lessconcentrated ownership structure, (5) are more international, and (6) havehigher-quality auditors have stronger incentives to provide high-quality fi-nancial reporting. We measure these firm characteristics using account-ing and market data from Global Compustat or Datastream/Worldscope.We measure profitability by return on assets (ROA), defined as net in-come/total assets; growth opportunities by Tobin’s q (TOBIN Q), definedas market value of assets/book value of assets, where the numerator ismeasured as (book value of assets + market value of common equity –book value of common equity – balance sheet deferred taxes). Financialleverage (LEVERAGE) is measured as total liabilities/total assets, owner-ship concentration is the percentage of closely held shares (CLOSEHELD)as reported by Datastream/Worldscope, and international diversificationis the percentage of foreign sales (FOREIGNSALES) reported by Datas-tream/Worldscope. These variables are all measured as the mean valuesfor the two-year pre-mandatory-adoption period. Finally, we use a dummyvariable to indicate the presence of a big four auditor (BIG4) in the yearimmediately preceding mandatory IFRS adoption.

To test H3, we estimate the following model using mandatory adoptersdomiciled in countries with both weak enforcement regimes and domesticaccounting standards that differ significantly from IFRS (i.e., the Low LAW-High IFRSdiff group)

�Info. Environmenti = δ0 + δ1ROAi + δ2TOBIN Qi + δ3LEVERAGEi

+ δ4CLOSEHELDi + δ5FOREIGNSALESi + δ6BIG4i

+ δ j �Controlsi + εi , (3)

where the subscript i refers to mandatory adopter i. �Info. Environmentrefers to �AFE, �DISP, or �LogFOLLOW ; the control variables are thesame as in equations (1) and (2). We estimate this equation using only

80 D. BYARD, Y. LI, AND Y. YU

test firms because our focus is on the cross-sectional variation in reportingincentives within the sample of mandatory adopters. As long as concur-rent confounding events have the same effect on all mandatory adopters,this effect is cancelled out in this within-mandatory-sample comparison. Iffirms with stronger reporting incentives experience a greater improvementin analysts’ information environment, we expect the coefficients on ROA,TOBIN Q , LEVERAGE , FOREIGNSALE , and BIG4 to be negative for the�AFE and �DISP regressions, and positive for the �LogFOLLOW regres-sion; additionally, we expect the coefficient on CLOSEHELD to be positivefor the �AFE and �DISP regressions, and negative for the �LogFOLLOWregression.

4. Results

4.1. DESCRIPTIVE STATISTICS

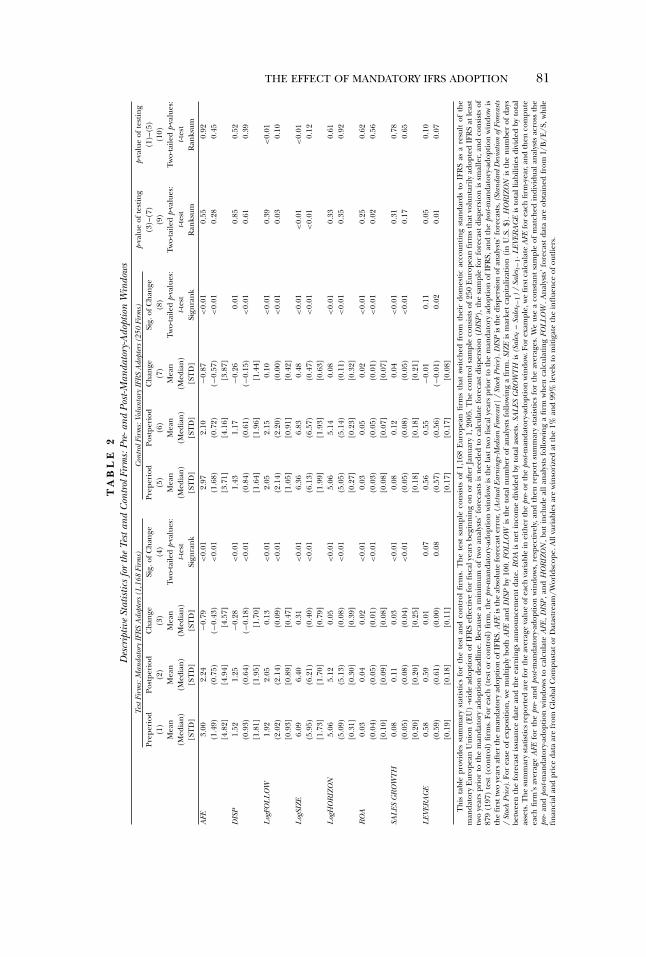

Table 2 provides descriptive statistics for the test and control samples, andpresents univariate comparisons across the two samples to explore poten-tial differences. For the test sample, the means (medians) of �AFE, �DISP,and �LogFOLLOW are −0.79 (−0.43), −0.28 (−0.18), and 0.13 (0.09), re-spectively; these changes are all statistically significant (two-tailed p ≤ 0.01).The reductions in analysts’ forecast errors and dispersion and increase inanalyst following suggest an improvement in analysts’ information environ-ment. However, we also observe a similar improvement for the control sam-ple: the means (medians) of �AFE, �DISP, and �LogFOLLOW are −0.87(−0.57), −0.26 (−0.15), and 0.10 (0.00), respectively, for the control firms;again, these changes are all statistically significant (two-tailed p ≤ 0.01).More importantly, Column (9) shows that �AFE, �DISP, and �LogFOLLOWare not statistically different between the test and control firms, except forthe median �LogFOLLOW , which is higher for the test sample (two-tailedp = 0.03). Thus, table 2 provides little evidence of an incremental change inanalysts’ information environment for the test firms relative to the controlfirms. However, because these univariate comparisons do not control forcorrelated factors that potentially influence the change in analysts’ infor-mation environment (e.g., changes in firm size), the results only providepreliminary evidence on H1 and should be interpreted with caution.

The improvement in analysts’ information environment for the controlfirms could reflect: (1) concurrent economic or regulatory shocks suchas the EU’s efforts to improve the enforcement of accounting standards,(2) IFRS changes between the pre- and post-mandatory-adoption windows,and/or (3) some positive externality—such as increased comparability—arising from mandatory IFRS adoption. It is difficult to distinguish amongthese effects in our setting. To the extent that the improvement for thecontrol firms is attributable to either IFRS changes around mandatoryadoption or to some positive externality arising from the adoption, exam-ining the difference between the test and control firms may understate theadoption effect.

THE EFFECT OF MANDATORY IFRS ADOPTION 81

TA

BL

E2

Des

crip

tive

Stat

istic

sfo

rth

eTe

stan

dC

ontr

olFi

rms:

Pre-

and

Post

-Man

dato

ry-A

dopt

ion

Win

dow

sTe

stFi

rms:

Man

dato

ryIF

RS

Ado

pter

s(1

,168

Firm

s)C

ontr

olFi

rms:

Volu

ntar

yIF

RS

Ado

pter

s(2

50Fi

rms)

p-va

lue

ofte

stin

gp-

valu

eof

test

ing

Prep

erio

dPo

stpe

riod

Cha

nge

Sig.

ofC

hang

ePr

eper

iod

Post

peri

odC

hang

eSi

g.of

Cha

nge

(3)–

(7)

(1)–

(5)

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Mea

nM

ean

Mea

nTw

o-ta

iled

p-va

lues

:M

ean

Mea

nM

ean

Two-

taile

dp-

valu

es:

Two-

taile

dp-

valu

es:

Two-

taile

dp-

valu

es:

(Med

ian)

(Med

ian)

(Med

ian)

t-tes

t(M

edia

n)(M

edia

n)(M

edia

n)t-t

est

t-tes

tt-t

est

[ST

D]

[ST

D]

[ST

D]

Sign

rank

[ST

D]

[ST

D]

[ST

D]

Sign

rank

Ran

ksum

Ran

ksum

AFE

3.00

2.24

−0.7

9<

0.01

2.97

2.10

−0.8

7<

0.01

0.55

0.92

(1.4

9)(0

.75)

(−0.

43)

<0.

01(1

.68)

(0.7

2)(−

0.57

)<

0.01

0.28

0.45

[4.8

2][4

.94]

[4.5

7][3

.71]

[4.1

6][3

.87]

DIS

P1.

521.

25−0

.28

<0.

011.

431.

17−0

.26

0.01

0.85

0.52

(0.9

3)(0

.64)

(−0.

18)

<0.

01(0

.84)

(0.6

1)(−

0.15

)<

0.01

0.61

0.39

[1.8

1][1

.95]

[1.7

0][1

.64]

[1.9

6][1

.44]

Log

FOL

LO

W1.

922.

050.

13<

0.01

2.05

2.15

0.10

<0.

010.

39<

0.01

(2.0

2)(2

.14)

(0.0

9)<

0.01

(2.1

4)(2

.20)

(0.0

0)<

0.01

0.03

0.10

[0.9

3][0

.89]

[0.4

7][1

.05]

[0.9

1][0

.42]

Log

SIZE

6.09

6.40

0.31

<0.

016.

366.

830.

48<

0.01

<0.

01<

0.01

(5.9

5)(6

.21)

(0.4

0)<

0.01

(6.1

3)(6

.57)

(0.4

7)<

0.01

<0.

010.

12[1

.73]

[1.7

0][0

.79]

[1.9

9][1

.93]

[0.6

3]L

ogH

OR

IZO

N5.

065.

120.

05<

0.01

5.06

5.14

0.08

<0.

010.

330.

61(5

.09)

(5.1

3)(0

.08)

<0.

01(5

.05)

(5.1

4)(0

.11)

<0.

010.

350.

92[0

.31]

[0.3

0][0

.39]

[0.2

7][0

.23]

[0.3

2]R

OA

0.03

0.04

0.02

<0.

010.

030.

050.

02<

0.01

0.25

0.62

(0.0

4)(0

.05)

(0.0

1)<

0.01

(0.0

3)(0

.05)

(0.0

1)<

0.01

0.02

0.56

[0.1

0][0

.09]

[0.0

8][0

.08]

[0.0

7][0

.07]

SAL

ESG

RO

WT

H0.

080.

110.

03<

0.01

0.08

0.12

0.04

<0.

010.

310.

78(0

.05)

(0.0

8)(0

.04)

<0.

01(0

.05)

(0.0

8)(0

.05)

<0.

010.

170.

65[0

.20]

[0.2

0][0

.25]

[0.1

8][0

.18]

[0.2

1]L

EVER

AG

E0.

580.

590.

010.

070.

560.

55−0

.01

0.11

0.05

0.10

(0.5

9)(0

.61)

(0.0

0)0.

08(0

.57)

(0.5

6)(−

0.01

)0.

020.

010.

07[0

.19]

[0.1

8][0

.11]

[0.1

7][0

.17]

[0.0

8]

Thi

sta

ble

prov

ides

sum

mar

yst

atis

tics

for

the

test

and

cont

rol

firm

s.T

hete

stsa

mpl

eco

nsis

tsof

1,16

8E

urop

ean

firm

sth

atsw

itche

dfr

omth

eir

dom

estic

acco

untin

gst

anda

rds

toIF

RS

asa

resu

ltof

the

man

dato

ryE

urop

ean

Uni

on(E

U)

-wid

ead

optio

nof

IFR

Sef

fect

ive

for

fisca

lyea

rsbe

ginn

ing

onor

afte

rJa

nuar

y1,

2005

.The

cont

rols

ampl

eco

nsis

tsof

250

Eur

opea

nfir

ms

that

volu

ntar

ilyad

opte

dIF

RS

atle

ast

two

year

spr

ior

toth

em

anda

tory

adop

tion

dead

line.

Bec

ause

am

inim

umof

two

anal

ysts

’for

ecas

tsis

need

edto

calc

ulat

efo

reca

stdi

sper

sion

(DIS

P),

the

sam

ple

for

fore

cast

disp

ersi

onis

smal

ler,

and

cons

ists

of87

9(1

97)

test

(con

trol

)fir

ms.

For

each

(tes

tor

cont

rol)

firm

,the

pre-

man

dato

ry-a

dopt

ion

win

dow

isth

ela

sttw

ofis

caly

ears

prio

rto

the

man

dato

ryad

optio

nof

IFR

S,an

dth

epo

st-m

anda

tory

-ado

ptio

nw

indo

wis

the

first

two

year

saf

ter

the

man

dato

ryad

optio

nof

IFR

S.A

FEis

the

abso

lute

fore

cast

erro

r,(A

ctua

lEar

ning

s-Med

ian

Fore

cast

|/St

ock

Pric

e).D

ISP

isth

edi

sper

sion

ofan

alys

ts’f

orec

asts

,(St

anda

rdD

evia

tion

ofFo

reca

sts

/St

ock

Pric

e).F

orea

seof

expo

sitio

n,w

em

ultip

lybo

thA

FEan

dD

ISP

by10

0.FO

LL

OW

isth

eto

taln

umbe

rof

anal

ysts

follo

win

ga

firm

.SIZ

Eis

mar

ket

capi

taliz

atio

n(i

nU

.S.$

).H

OR

IZO

Nis

the

num

ber

ofda

ysbe

twee

nth

efo

reca

stis

suan

ceda

tean

dth

eea

rnin

gsan

noun

cem

ent

date

.RO

Ais

net

inco

me

divi

ded

byto

tala

sset

s.SA

LES

GR

OW

TH

is(S

ales

t–

Sale

s t−1

)/

Sale

s t−1

.LEV

ERA

GE

isto

tall

iabi

litie

sdi

vide

dby

tota

las

sets

.The

sum

mar

yst

atis

ticsr

epor

ted

are

for

the

aver

age

valu

eof

each

vari

able

inei

ther

the

pre-

orth

epo

st-m

anda

tory

-ado

ptio

nw

indo

w.Fo

rex

ampl

e,w

efir

stca

lcul

ate

AFE

for

each

firm

-yea

r,an

dth

enco

mpu

teea

chfir

m’s

aver

age

AFE

for

the

pre-

and

post

-man

dato

ry-a

dopt

ion

win

dow

s,re

spec

tivel

y,an

dth

enre

port

sum

mar

yst

atis

tics

for

the

aver

ages

.We

use

aco

nsta

ntsa

mpl

eof

mat

ched

indi

vidu

alan

alys

tsac

ross

the

pre-

and

post

-man

dato

ry-a

dopt

ion

win

dow

sto

calc

ulat

eA

FE,D

ISP

,and

HO

RIZ

ON

,but

incl

ude

alla

naly

sts

follo

win

ga

firm

whe

nca

lcul

atin

gFO

LL

OW

.Ana

lyst

s’fo

reca

stda

taar

eob

tain

edfr

omI/

B/E

/S,w

hile

finan

cial

and

pric

eda

taar

efr

omG

loba

lCom

pust

ator

Dat

astr

eam

/Wor

ldsc

ope.

All

vari

able

sar

ew

inso

rize

dat

the

1%an

d99

%le

vels

tom

itiga

teth

ein

flue

nce

ofou

tlier

s.

82 D. BYARD, Y. LI, AND Y. YU

In table 2, we also compare other financial and analyst variables acrossthe test and control samples to gauge whether and how the two samplesdiffer. We find a statistically significant increase in firm size and analysts’forecast horizon for both the test and control samples. Although the in-crease in analysts’ forecast horizon is not statistically different across thetwo samples, the increase in firm size is statistically greater for the controlfirms. Both return on assets and sales growth increase for the test and con-trol samples, but the increases are not statistically different across the twosamples. We find that leverage increases for the test sample, but there isweak evidence that it decreases for the control sample. Column (10) com-pares the pre-mandatory-adoption levels of all these variables across the testand control samples: control firms tend to be larger and have higher ana-lyst following and lower leverage, but differences between the two samplesin forecast errors, dispersion, analysts’ forecast horizons, sales growth, orfirm performance are statistically insignificant.

Overall, the results in tables 1 and 2 indicate that our test and controlfirms differ in important ways, most prominently country of origin and firmsize. Although our results are robust to comparing test and control firmswithin country groups and to controlling for various firm characteristics,we cannot rule out the possibility that some unknown difference betweenthe test and control firms may cause them to react differently to confound-ing concurrent events, and, consequently, our control firms may not fullycapture the impact of these events on our test firms.

4.2. THE AVERAGE EFFECT OF MANDATORY IFRS ADOPTION (H1)

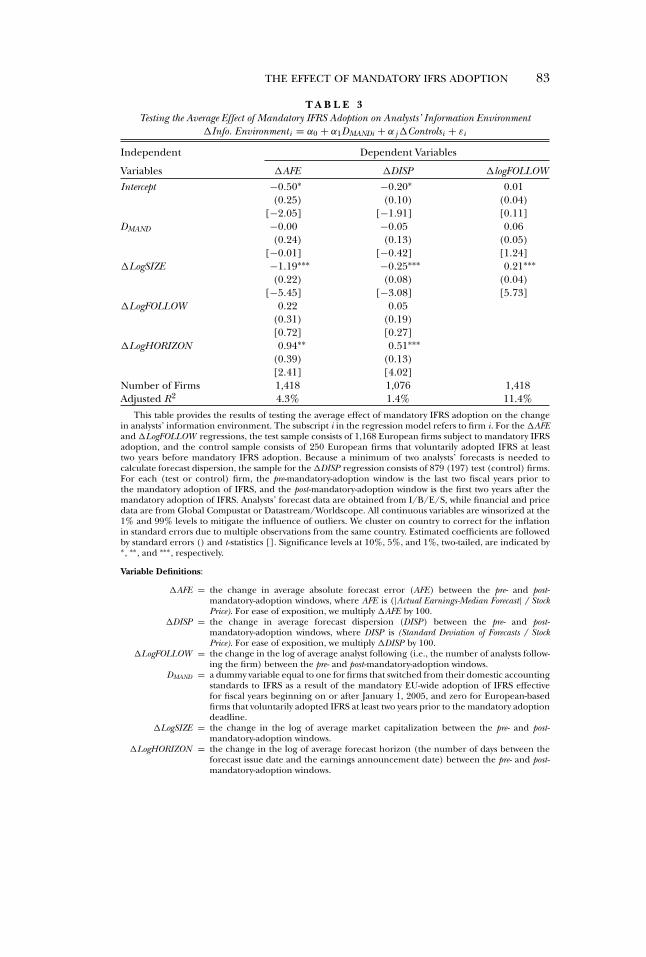

Table 3 reports the results of estimating equation (1), which regressesthe change in analysts’ information environment (measured by �AFE,�DISP, or �LogFOLLOW ) on a dummy variable indicating mandatory IFRSadopters (DMAND) and the control variables. The estimated coefficients onDMAND are: −0.00 (t-stat = −0.01), −0.05 (t-stat = −0.42), and 0.06 (t-stat= 1.24) for the �AFE, �DISP, and �logFOLLOW regressions, respectively.These results indicate that on average mandatory adopters exhibit no incre-mental change in analysts’ information environment relative to the controlfirms. Thus, we are unable to reject H1.

The sum of the intercept and the coefficient on DMAND is negative andstatistically significant for both the �AFE and �DISP regressions (untab-ulated), indicating that mandatory adopters experience decreases in bothforecast errors and dispersion. The intercept, which captures the changefor the control firms, is negative and statistically significant for both the�AFE and �DISP regressions, indicating an improvement in analysts’ infor-mation environment for the control firms (see section 4.1 for a discussionof possible reasons). Overall, the regression results in table 3 confirm theunivariate results in table 2.

THE EFFECT OF MANDATORY IFRS ADOPTION 83

T A B L E 3Testing the Average Effect of Mandatory IFRS Adoption on Analysts’ Information Environment

�Info. Environmenti = α0 + α1DMANDi + α j �Controlsi + εi

Independent Dependent Variables

Variables �AFE �DISP �logFOLLOW

Intercept −0.50∗ −0.20∗ 0.01(0.25) (0.10) (0.04)

[−2.05] [−1.91] [0.11]DMAND −0.00 −0.05 0.06

(0.24) (0.13) (0.05)[−0.01] [−0.42] [1.24]

�LogSIZE −1.19∗∗∗ −0.25∗∗∗ 0.21∗∗∗(0.22) (0.08) (0.04)

[−5.45] [−3.08] [5.73]�LogFOLLOW 0.22 0.05

(0.31) (0.19)[0.72] [0.27]

�LogHORIZON 0.94∗∗ 0.51∗∗∗(0.39) (0.13)[2.41] [4.02]

Number of Firms 1,418 1,076 1,418Adjusted R2 4.3% 1.4% 11.4%

This table provides the results of testing the average effect of mandatory IFRS adoption on the changein analysts’ information environment. The subscript i in the regression model refers to firm i. For the �AFEand �LogFOLLOW regressions, the test sample consists of 1,168 European firms subject to mandatory IFRSadoption, and the control sample consists of 250 European firms that voluntarily adopted IFRS at leasttwo years before mandatory IFRS adoption. Because a minimum of two analysts’ forecasts is needed tocalculate forecast dispersion, the sample for the �DISP regression consists of 879 (197) test (control) firms.For each (test or control) firm, the pre-mandatory-adoption window is the last two fiscal years prior tothe mandatory adoption of IFRS, and the post-mandatory-adoption window is the first two years after themandatory adoption of IFRS. Analysts’ forecast data are obtained from I/B/E/S, while financial and pricedata are from Global Compustat or Datastream/Worldscope. All continuous variables are winsorized at the1% and 99% levels to mitigate the influence of outliers. We cluster on country to correct for the inflationin standard errors due to multiple observations from the same country. Estimated coefficients are followedby standard errors () and t-statistics []. Significance levels at 10%, 5%, and 1%, two-tailed, are indicated by∗, ∗∗, and ∗∗∗, respectively.

Variable Definitions:

�AFE = the change in average absolute forecast error (AFE) between the pre- and post-mandatory-adoption windows, where AFE is (|Actual Earnings-Median Forecast| / StockPrice). For ease of exposition, we multiply �AFE by 100.

�DISP = the change in average forecast dispersion (DISP) between the pre- and post-mandatory-adoption windows, where DISP is (Standard Deviation of Forecasts / StockPrice). For ease of exposition, we multiply �DISP by 100.

�LogFOLLOW = the change in the log of average analyst following (i.e., the number of analysts follow-ing the firm) between the pre- and post-mandatory-adoption windows.

DMAND = a dummy variable equal to one for firms that switched from their domestic accountingstandards to IFRS as a result of the mandatory EU-wide adoption of IFRS effectivefor fiscal years beginning on or after January 1, 2005, and zero for European-basedfirms that voluntarily adopted IFRS at least two years prior to the mandatory adoptiondeadline.

�LogSIZE = the change in the log of average market capitalization between the pre- and post-mandatory-adoption windows.

�LogHORIZON = the change in the log of average forecast horizon (the number of days between theforecast issue date and the earnings announcement date) between the pre- and post-mandatory-adoption windows.

84 D. BYARD, Y. LI, AND Y. YU

4.3. RESULTS CONDITIONAL ON COUNTRY-LEVEL INSTITUTIONALCHARACTERISTICS (H2)

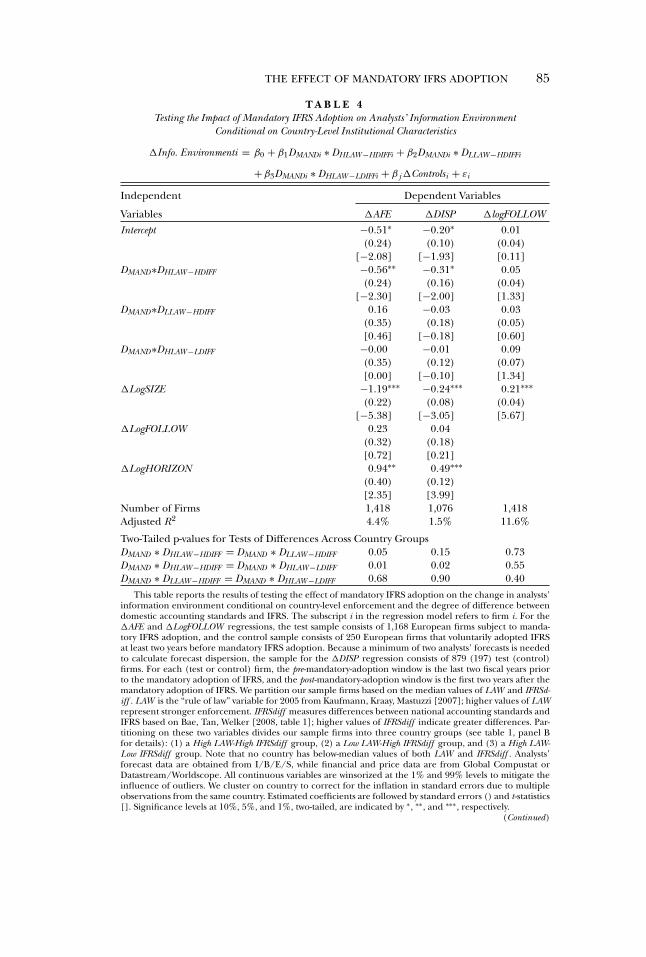

4.3.1. Primary Analyses. Table 4 reports the results of estimating equa-tion (2), which regresses the change in analysts’ information environment(measured by �AFE, �DISP, or �LogFOLLOW ) on the dummy variable in-dicating mandatory IFRS adopters (DMAND) interacted with three dummyvariables — DHLAW −HDIFF , DLLAW −HDIFF , and DHLAW −LDIFF — that identify thethree different country-groups, in addition to the control variables. Thecoefficient of interest is on DMAND ∗DHLAW −HDIFF , which captures the differ-ence between the test firms domiciled in High Law-High IFRSdiff countriesand all the control firms. The estimated coefficients on this interactionterm are: −0.56 (t-stat = −2.30), −0.31 (t-stat = −2.00), and 0.05 (t-stat= 1.33) for the �AFE, �DISP, and �logFOLLOW regressions, respectively.Thus, we reject H2 in favor of the alternative hypothesis that, followingmandatory IFRS adoption, analysts’ information environment improves forfirms in High Law-High IFRSdiff countries.

The estimated effects of mandatory IFRS adoption on analysts’ forecasterrors and dispersions also appear to be economically significant. For testfirms domiciled in High Law-High IFRSdiff countries, the means of AFE andDISP in the pre-mandatory-IFRS-adoption window are 2.86 and 1.53, respec-tively (untabulated). Thus, the results in table 4 indicate that mandatoryIFRS adoption is associated with a 22% (i.e., −0.56/2.86) reduction in ana-lysts’ forecast error and a 20% (i.e., −0.31/1.53) reduction in analysts’ fore-cast dispersion for mandatory adopters domiciled in High Law-High IFRSdiffcountries.

For mandatory adopters domiciled in the other two country groups, wefind no evidence that the change in analysts’ information environment dif-fers from that for the control firms: the coefficients on DMAND ∗ DLLAW −HDIFF

and DMAND ∗ DHLAW −LDIFF are statistically insignificant in any regression.Comparing across the three groups of mandatory adopters, we find thatin the �AFE regression the coefficient on DMAND∗DHLAW −HDIFF is statisti-cally more negative than DMAND ∗ DLLAW −HDIFF or DMAND ∗ DHLAW −LDIFF ; inthe �DISP regression the coefficient on DMAND ∗ DHLAW −HDIFF is statisti-cally more negative than DMAND ∗ DHLAW −LDIFF . Thus, the adoption effectis greater for mandatory adopters domiciled in the High Law-High IFRSdiffcountries than in other countries.

The above results are based on a simultaneous partition of the test sam-ple using the median values of both LAW and IFRSdiff . To evaluate therelative importance of these two partitioning variables, we split the test sam-ple by the median value of each variable, one at a time. We find some im-provement in analysts’ information environment for mandatory adoptersin either high LAW or high IFRSdiff countries, but the magnitudes of theimprovement (untabulated) are smaller and the statistical significance lev-els are lower than our reported results. These results suggest that both highIFRSdiff and high LAW contribute to our main findings reported in table 4.

THE EFFECT OF MANDATORY IFRS ADOPTION 85

T A B L E 4Testing the Impact of Mandatory IFRS Adoption on Analysts’ Information Environment

Conditional on Country-Level Institutional Characteristics

�Info. Environmenti = β0 + β1DMANDi ∗ DHLAW −HDIFFi + β2DMANDi ∗ DLLAW −HDIFFi

+β3DMANDi ∗ DHLAW −LDIFFi + β j �Controlsi + εi

Independent Dependent Variables

Variables �AFE �DISP �logFOLLOW

Intercept −0.51∗ −0.20∗ 0.01(0.24) (0.10) (0.04)

[−2.08] [−1.93] [0.11]DMAND∗DHLAW −HDIFF −0.56∗∗ −0.31∗ 0.05

(0.24) (0.16) (0.04)[−2.30] [−2.00] [1.33]

DMAND∗DLLAW −HDIFF 0.16 −0.03 0.03(0.35) (0.18) (0.05)[0.46] [−0.18] [0.60]

DMAND∗DHLAW −LDIFF −0.00 −0.01 0.09(0.35) (0.12) (0.07)[0.00] [−0.10] [1.34]

�LogSIZE −1.19∗∗∗ −0.24∗∗∗ 0.21∗∗∗(0.22) (0.08) (0.04)

[−5.38] [−3.05] [5.67]�LogFOLLOW 0.23 0.04

(0.32) (0.18)[0.72] [0.21]

�LogHORIZON 0.94∗∗ 0.49∗∗∗(0.40) (0.12)[2.35] [3.99]

Number of Firms 1,418 1,076 1,418Adjusted R2 4.4% 1.5% 11.6%

Two-Tailed p-values for Tests of Differences Across Country GroupsDMAND ∗ DHLAW −HDIFF = DMAND ∗ DLLAW −HDIFF 0.05 0.15 0.73DMAND ∗ DHLAW −HDIFF = DMAND ∗ DHLAW −LDIFF 0.01 0.02 0.55DMAND ∗ DLLAW −HDIFF = DMAND ∗ DHLAW −LDIFF 0.68 0.90 0.40

This table reports the results of testing the effect of mandatory IFRS adoption on the change in analysts’information environment conditional on country-level enforcement and the degree of difference betweendomestic accounting standards and IFRS. The subscript i in the regression model refers to firm i. For the�AFE and �LogFOLLOW regressions, the test sample consists of 1,168 European firms subject to manda-tory IFRS adoption, and the control sample consists of 250 European firms that voluntarily adopted IFRSat least two years before mandatory IFRS adoption. Because a minimum of two analysts’ forecasts is neededto calculate forecast dispersion, the sample for the �DISP regression consists of 879 (197) test (control)firms. For each (test or control) firm, the pre-mandatory-adoption window is the last two fiscal years priorto the mandatory adoption of IFRS, and the post-mandatory-adoption window is the first two years after themandatory adoption of IFRS. We partition our sample firms based on the median values of LAW and IFRSd-iff . LAW is the “rule of law” variable for 2005 from Kaufmann, Kraay, Mastuzzi [2007]; higher values of LAWrepresent stronger enforcement. IFRSdiff measures differences between national accounting standards andIFRS based on Bae, Tan, Welker [2008, table 1]; higher values of IFRSdiff indicate greater differences. Par-titioning on these two variables divides our sample firms into three country groups (see table 1, panel Bfor details): (1) a High LAW-High IFRSdiff group, (2) a Low LAW-High IFRSdiff group, and (3) a High LAW-Low IFRSdiff group. Note that no country has below-median values of both LAW and IFRSdiff . Analysts’forecast data are obtained from I/B/E/S, while financial and price data are from Global Compustat orDatastream/Worldscope. All continuous variables are winsorized at the 1% and 99% levels to mitigate theinfluence of outliers. We cluster on country to correct for the inflation in standard errors due to multipleobservations from the same country. Estimated coefficients are followed by standard errors () and t-statistics[]. Significance levels at 10%, 5%, and 1%, two-tailed, are indicated by ∗, ∗∗, and ∗∗∗, respectively.

(Continued)

86 D. BYARD, Y. LI, AND Y. YU

T A B L E 4 — Continued

Variable Definitions:

�AFE = the change in average absolute forecast error (AFE) between the pre- and post-mandatory-adoption windows, where AFE is (|Actual Earnings-Median Forecast| / StockPrice). For ease of exposition, we multiply �AFE by 100.

�DISP = the change in average forecast dispersion (DISP) between the pre- and post-mandatory-adoption windows, where DISP is (Standard Deviation of Forecasts / StockPrice). For ease of exposition, we multiply �DISP by 100.

�LogFOLLOW = the change in the log of average analyst following (i.e., the number of analysts follow-ing the firm) between the pre- and post-mandatory-adoption windows.

DMAND = a dummy variable equal to one for firms that switched from their domestic accountingstandards to IFRS as a result of the mandatory EU-wide adoption of IFRS effectivefor fiscal years beginning on or after January 1, 2005, and zero for European-basedfirms that voluntarily adopted IFRS at least two years prior to the mandatory adoptiondeadline.

DHLAW −HDIFF = a dummy variable equal to one if a firm (test or control) is domiciled in a High LAW-High IFRSdiff country, and zero otherwise.

DLLAW −HDIFF = a dummy variable equal to one if a firm (test or control) is domiciled in a Low LAW-High IFRSdiff country, and zero otherwise.

DHLAW −LDIFF = a dummy variable equal to one if a firm (test or control) is domiciled in a High LAW-Low IFRSdiff country, and zero otherwise.

�LogSIZE = the change in the log of average market capitalization between the pre- and post-mandatory-adoption windows.

�LogHORIZON = the change in the log of average forecast horizon (the number of days between theforecast issue date and the earnings announcement date) between the pre- and post-mandatory-adoption windows.

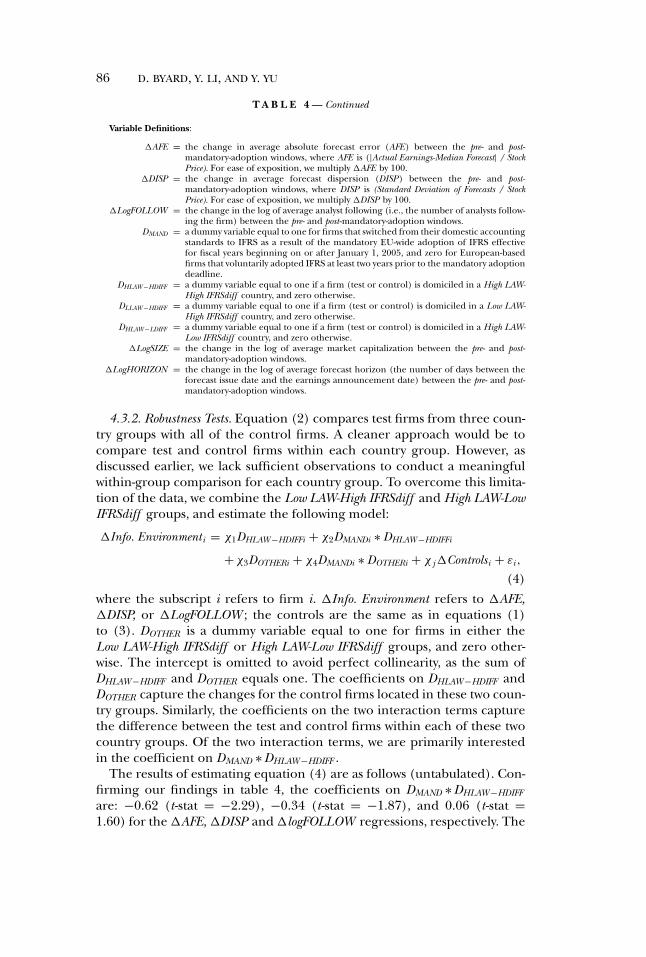

4.3.2. Robustness Tests. Equation (2) compares test firms from three coun-try groups with all of the control firms. A cleaner approach would be tocompare test and control firms within each country group. However, asdiscussed earlier, we lack sufficient observations to conduct a meaningfulwithin-group comparison for each country group. To overcome this limita-tion of the data, we combine the Low LAW-High IFRSdiff and High LAW-LowIFRSdiff groups, and estimate the following model:

�Info. Environmenti = χ1DHLAW −HDIFFi + χ2DMANDi ∗ DHLAW −HDIFFi

+χ3DOTHERi + χ4DMANDi ∗ DOTHERi + χ j �Controlsi + εi ,

(4)where the subscript i refers to firm i. �Info. Environment refers to �AFE,�DISP, or �LogFOLLOW ; the controls are the same as in equations (1)to (3). DOTHER is a dummy variable equal to one for firms in either theLow LAW-High IFRSdiff or High LAW-Low IFRSdiff groups, and zero other-wise. The intercept is omitted to avoid perfect collinearity, as the sum ofDHLAW −HDIFF and DOTHER equals one. The coefficients on DHLAW −HDIFF andDOTHER capture the changes for the control firms located in these two coun-try groups. Similarly, the coefficients on the two interaction terms capturethe difference between the test and control firms within each of these twocountry groups. Of the two interaction terms, we are primarily interestedin the coefficient on DMAND ∗ DHLAW −HDIFF .

The results of estimating equation (4) are as follows (untabulated). Con-firming our findings in table 4, the coefficients on DMAND ∗ DHLAW −HDIFF

are: −0.62 (t-stat = −2.29), −0.34 (t-stat = −1.87), and 0.06 (t-stat =1.60) for the �AFE, �DISP and �logFOLLOW regressions, respectively. The

THE EFFECT OF MANDATORY IFRS ADOPTION 87

coefficients on DMAND ∗ DOTHER are statistically insignificant in all regres-sions, indicating that the change in analysts’ information environment doesnot differ between the test and control firms domiciled in Other countries.We also compare the adoption effect across the two country groups. Con-sistent with the results in table 4, the coefficients on DMAND ∗ DHLAW −HDIFF

are statistically more negative than DMAND∗DOTHER in the �AFE and �DISPregressions.10

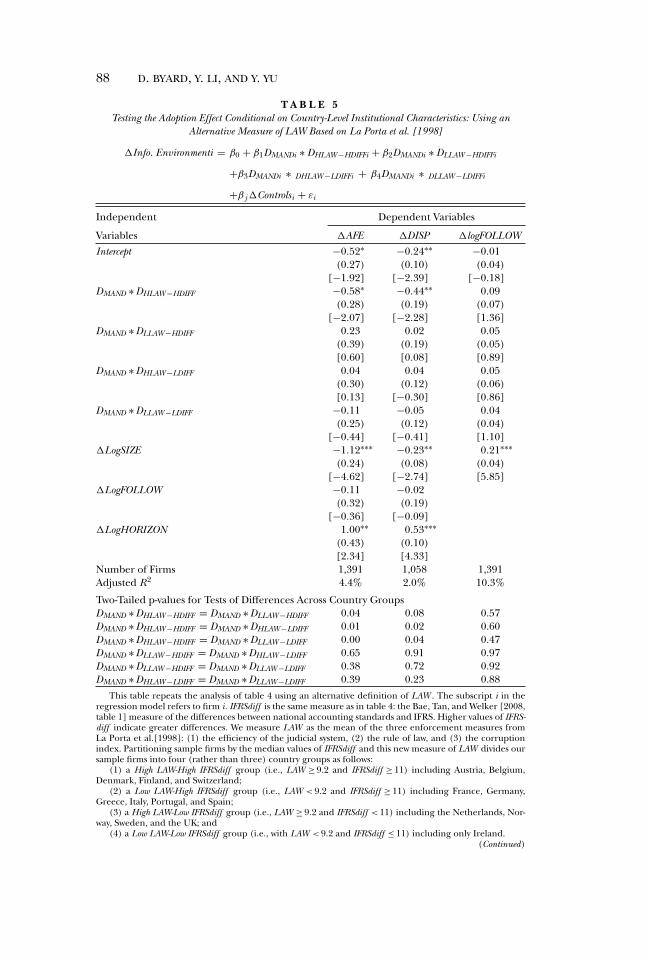

To further test the robustness of our results, table 5 reestimates equa-tion (2) using IFRSdiff and an alternative measure of LAW used by Leuzet al. [2003] and DeFond and Hung [2004]— the mean of the three legalvariables from La Porta et al. [1998]: the efficiency of the judicial system,the rule of law, and the corruption index. Note table 5 now has four (ratherthan three) country groups using this alternative measure of LAW , with Ire-land being the only country included in the Low LAW-Low IFRSdiff group.The results using this alternative partition are similar to our main results intable 4.

Our results are also robust to using the following alternative proxies forthe quality of country-level enforcement environment (untabulated): (1)Kaufmann, Kraay, and Mastuzzi [2007] “rule of law” score for 2004, 2005,or 2006, as well as the average of the three years, and (2) the “governanceeffectiveness” score, the “regulatory quality” score, or the average of the sixgovernance scores for 2005 from Kaufmann, Kraay, and Mastuzzi [2007].In addition, when we partition the sample firms using mean (rather thanmedian) values of both LAW and IFRSdiff , we find similar results (untabu-lated).11

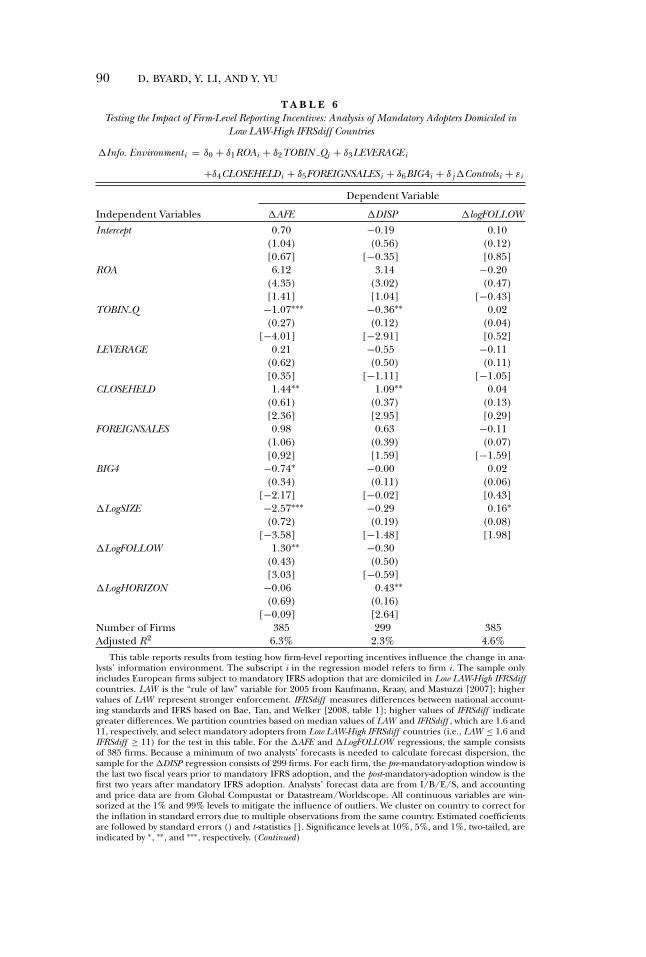

4.4. RESULTS FOR FIRM-LEVEL REPORTING INCENTIVES (H3)

Table 6 reports the results of estimating equation (3), which regresses thechange in analysts’ information environment (measured by �AFE, �DISP,or �LogFOLLOW ) on our proxies for firm-level reporting incentives andthe control variables, for mandatory adopters domiciled in the Low LAW-High IFRSdiff countries. We find that TOBIN Q is negatively related to both

10 We undertake a one-to-one matching of test and control firms within each country (e.g.,on pre-mandatory-adoption firm size). The maximum number of within-country matched pairsis only 102. Using this approach, we find that the key coefficients of interest are statisticallyinsignificant.

11 In untabulated analyses, we also test the effect of the transition year (i.e., the first yearunder IFRS reporting) on our results. On the one hand, a number of firms, particularly largeones, provided significant interim guidance in the transition year. This may have temporarilyreduced analysts’ forecast errors and dispersion. On the other hand, the transition year maybias against finding our results, because the “one-time” adjustments coinciding with the first-time adoption of IFRS may temporarily increase the difficulty of forecasting earnings. Wefind that the results are similar when we remove the transition year from the post-mandatory-adoption window. We also find no statistically significant change in forecast errors, dispersion,or analyst following across the two years in the post-mandatory-year window. Thus, our resultsare unlikely to be confounded by the effect of the transition year.

88 D. BYARD, Y. LI, AND Y. YU

T A B L E 5Testing the Adoption Effect Conditional on Country-Level Institutional Characteristics: Using an

Alternative Measure of LAW Based on La Porta et al. [1998]

�Info. Environmenti = β0 + β1DMANDi ∗ DHLAW −HDIFFi + β2DMANDi ∗ DLLAW −HDIFFi

+β3DMANDi ∗ DHLAW −LDIFFi + β4DMANDi ∗ DLLAW −LDIFFi

+β j �Controlsi + εi

Independent Dependent Variables

Variables �AFE �DISP �logFOLLOW

Intercept −0.52∗ −0.24∗∗ −0.01(0.27) (0.10) (0.04)

[−1.92] [−2.39] [−0.18]DMAND ∗ DHLAW −HDIFF −0.58∗ −0.44∗∗ 0.09

(0.28) (0.19) (0.07)[−2.07] [−2.28] [1.36]

DMAND ∗ DLLAW −HDIFF 0.23 0.02 0.05(0.39) (0.19) (0.05)[0.60] [0.08] [0.89]

DMAND ∗ DHLAW −LDIFF 0.04 0.04 0.05(0.30) (0.12) (0.06)[0.13] [−0.30] [0.86]

DMAND ∗ DLLAW −LDIFF −0.11 −0.05 0.04(0.25) (0.12) (0.04)

[−0.44] [−0.41] [1.10]�LogSIZE −1.12∗∗∗ −0.23∗∗ 0.21∗∗∗

(0.24) (0.08) (0.04)[−4.62] [−2.74] [5.85]

�LogFOLLOW −0.11 −0.02(0.32) (0.19)

[−0.36] [−0.09]�LogHORIZON 1.00∗∗ 0.53∗∗∗

(0.43) (0.10)[2.34] [4.33]

Number of Firms 1,391 1,058 1,391Adjusted R2 4.4% 2.0% 10.3%

Two-Tailed p-values for Tests of Differences Across Country GroupsDMAND ∗ DHLAW −HDIFF = DMAND ∗ DLLAW −HDIFF 0.04 0.08 0.57DMAND ∗ DHLAW −HDIFF = DMAND ∗ DHLAW −LDIFF 0.01 0.02 0.60DMAND ∗ DHLAW −HDIFF = DMAND ∗ DLLAW −LDIFF 0.00 0.04 0.47DMAND ∗ DLLAW −HDIFF = DMAND ∗ DHLAW −LDIFF 0.65 0.91 0.97DMAND ∗ DLLAW −HDIFF = DMAND ∗ DLLAW −LDIFF 0.38 0.72 0.92DMAND ∗ DHLAW −LDIFF = DMAND ∗ DLLAW −LDIFF 0.39 0.23 0.88

This table repeats the analysis of table 4 using an alternative definition of LAW . The subscript i in theregression model refers to firm i. IFRSdiff is the same measure as in table 4: the Bae, Tan, and Welker [2008,table 1] measure of the differences between national accounting standards and IFRS. Higher values of IFRS-diff indicate greater differences. We measure LAW as the mean of the three enforcement measures fromLa Porta et al.[1998]: (1) the efficiency of the judicial system, (2) the rule of law, and (3) the corruptionindex. Partitioning sample firms by the median values of IFRSdiff and this new measure of LAW divides oursample firms into four (rather than three) country groups as follows:

(1) a High LAW-High IFRSdiff group (i.e., LAW ≥ 9.2 and IFRSdiff ≥ 11) including Austria, Belgium,Denmark, Finland, and Switzerland;

(2) a Low LAW-High IFRSdiff group (i.e., LAW < 9.2 and IFRSdiff ≥ 11) including France, Germany,Greece, Italy, Portugal, and Spain;

(3) a High LAW-Low IFRSdiff group (i.e., LAW ≥ 9.2 and IFRSdiff < 11) including the Netherlands, Nor-way, Sweden, and the UK; and

(4) a Low LAW-Low IFRSdiff group (i.e., with LAW < 9.2 and IFRSdiff ≤ 11) including only Ireland.(Continued)

THE EFFECT OF MANDATORY IFRS ADOPTION 89

T A B L E 5 — Continued

This alternative measure of LAW is not available for four countries: the Czech Republic, Hungary, Lux-embourg, and Poland. As a result, the sample size is reduced by 27 firms for the �AEF and �LogFOLLOWregressions, and by 18 firms for the �DISP regression compared with the sample used in table 4. For the�AFE and �LogFOLLOW regressions, the total number of sample firms (test and control) is 1,391; for the�DISP regression, the total number of sample firms (test and control) is 1,058. Analysts’ forecast data arefrom I/B/E/S, while financial and price data are from Global Compustat or Datastream/Worldscope. Foreach (test or control) firm, the pre-mandatory-adoption window is the last two fiscal years prior to manda-tory IFRS adoption, and the post-mandatory-adoption window is the first two years after mandatory IFRSadoption. All continuous variables are winsorized at the 1% and 99% levels to mitigate the influence of out-liers. We cluster on country to correct for the inflation in standard errors due to multiple observations fromthe same country. Estimated coefficients are followed by standard errors () and t-statistics []. Significancelevels at 10%, 5%, and 1%, two-tailed, are indicated by ∗, ∗∗, and ∗∗∗, respectively.

Variable Definitions:

�AFE = the change in average absolute forecast error (AFE) between the pre- and post-mandatory-adoption windows, where AFE is (|Actual Earnings-Median Forecast| / StockPrice). For ease of exposition, we multiply �AFE by 100.

�DISP = the change in average forecast dispersion (DISP) between the pre- and post-mandatory-adoption windows, where DISP is (Standard Deviation of Forecasts / StockPrice). For ease of exposition, we multiply �DISP by 100.

�LogFOLLOW = the change in the log of average analyst following (i.e., the number of analysts follow-ing the firm) between the pre- and post-mandatory-adoption windows.

DMAND = a dummy variable equal to one for firms that switched from their domestic accountingstandards to IFRS as a result of the mandatory EU-wide adoption of IFRS effectivefor fiscal years beginning on or after January 1, 2005, and zero for European-basedfirms that voluntarily adopted IFRS at least two years prior to the mandatory adoptiondeadline.

DHLAW −HDIFF = a dummy variable equal to one if a firm (test or control) is domiciled in a High LAW-High IFRSdiff country, and zero otherwise.

DLLAW −HDIFF = a dummy variable equal to one if a firm (test or control) is domiciled in a Low LAW-High IFRSdiff country, and zero otherwise.

DHLAW −LDIFF = a dummy variable equal to one if a firm (test or control) is domiciled in a High LAW-Low IFRSdiff country, and zero otherwise.

DLLAW −LDIFF = a dummy variable equal to one if a firm (test or control) is domiciled in a Low LAW-Low IFRSdiff country, and zero otherwise.

�LogSIZE = the change in the log of average market capitalization between the pre- and post-mandatory-adoption windows.

�LogHORIZON = the change in the log of average forecast horizon (the number of days between theforecast issue date and the earnings announcement date) between the pre- and post-mandatory-adoption windows.

�AFE and �DISP (t-stat = −4.01 and −2.91, respectively), CLOSEHELDis positively related to both �AFE and �DISP (t-stat = 2.36 and 2.95, re-spectively), and BIG4 is negatively related to �AFE (t-stat = −2.17). Theseresults indicate that firms with stronger reporting incentives (i.e., firms withmore growth opportunities, a smaller proportion of closely held shares, orhigher-quality auditors) exhibit larger decreases in analysts’ forecast errorsand dispersion around mandatory IFRS adoption. These results are con-sistent with mandatory adopters with stronger reporting incentives imple-menting the changes mandated by IFRS more rigorously and, thus, exhibit-ing a greater improvement in analysts’ information environment.

For completeness, we also estimate equation (3) for mandatory adoptersin the other two country groups (untabulated). As expected, the results aremuch weaker. To compare regression coefficients across the three groups,we estimate equation (3) for the three country groups pooled in a Seem-ingly Unrelated Regression (SUR) model. Untabulated results show that

90 D. BYARD, Y. LI, AND Y. YU

T A B L E 6Testing the Impact of Firm-Level Reporting Incentives: Analysis of Mandatory Adopters Domiciled in

Low LAW-High IFRSdiff Countries

�Info. Environmenti = δ0 + δ1ROAi + δ2TOBIN Qi + δ3LEVERAGEi

+δ4CLOSEHELDi + δ5FOREIGNSALESi + δ6BIG4i + δ j �Controlsi + εi

Dependent Variable

Independent Variables �AFE �DISP �logFOLLOW

Intercept 0.70 −0.19 0.10(1.04) (0.56) (0.12)[0.67] [−0.35] [0.85]

ROA 6.12 3.14 −0.20(4.35) (3.02) (0.47)[1.41] [1.04] [−0.43]

TOBIN Q −1.07∗∗∗ −0.36∗∗ 0.02(0.27) (0.12) (0.04)

[−4.01] [−2.91] [0.52]LEVERAGE 0.21 −0.55 −0.11

(0.62) (0.50) (0.11)[0.35] [−1.11] [−1.05]

CLOSEHELD 1.44∗∗ 1.09∗∗ 0.04(0.61) (0.37) (0.13)[2.36] [2.95] [0.29]

FOREIGNSALES 0.98 0.63 −0.11(1.06) (0.39) (0.07)[0.92] [1.59] [−1.59]

BIG4 −0.74∗ −0.00 0.02(0.34) (0.11) (0.06)

[−2.17] [−0.02] [0.43]�LogSIZE −2.57∗∗∗ −0.29 0.16∗

(0.72) (0.19) (0.08)[−3.58] [−1.48] [1.98]

�LogFOLLOW 1.30∗∗ −0.30(0.43) (0.50)[3.03] [−0.59]

�LogHORIZON −0.06 0.43∗∗(0.69) (0.16)

[−0.09] [2.64]Number of Firms 385 299 385Adjusted R2 6.3% 2.3% 4.6%

This table reports results from testing how firm-level reporting incentives influence the change in ana-lysts’ information environment. The subscript i in the regression model refers to firm i. The sample onlyincludes European firms subject to mandatory IFRS adoption that are domiciled in Low LAW-High IFRSdiffcountries. LAW is the “rule of law” variable for 2005 from Kaufmann, Kraay, and Mastuzzi [2007]; highervalues of LAW represent stronger enforcement. IFRSdiff measures differences between national account-ing standards and IFRS based on Bae, Tan, and Welker [2008, table 1]; higher values of IFRSdiff indicategreater differences. We partition countries based on median values of LAW and IFRSdiff , which are 1.6 and11, respectively, and select mandatory adopters from Low LAW-High IFRSdiff countries (i.e., LAW ≤ 1.6 andIFRSdiff ≥ 11) for the test in this table. For the �AFE and �LogFOLLOW regressions, the sample consistsof 385 firms. Because a minimum of two analysts’ forecasts is needed to calculate forecast dispersion, thesample for the �DISP regression consists of 299 firms. For each firm, the pre-mandatory-adoption window isthe last two fiscal years prior to mandatory IFRS adoption, and the post-mandatory-adoption window is thefirst two years after mandatory IFRS adoption. Analysts’ forecast data are from I/B/E/S, and accountingand price data are from Global Compustat or Datastream/Worldscope. All continuous variables are win-sorized at the 1% and 99% levels to mitigate the influence of outliers. We cluster on country to correct forthe inflation in standard errors due to multiple observations from the same country. Estimated coefficientsare followed by standard errors () and t-statistics []. Significance levels at 10%, 5%, and 1%, two-tailed, areindicated by ∗, ∗∗, and ∗∗∗, respectively. (Continued)

THE EFFECT OF MANDATORY IFRS ADOPTION 91

T A B L E 6 — Continued

Variable Definitions:

�AFE = the change in average absolute forecast error (AFE) between the pre- and post-mandatory-adoption windows, where AFE is (|Actual Earnings-Median Forecast| / StockPrice). For ease of exposition, we multiply �AFE by 100.

�DISP = the change in average forecast dispersion (DISP) between the pre- and post-mandatory-adoption windows, where DISP is (Standard Deviation of Forecasts / StockPrice). For ease of exposition, we multiply �DISP both by 100.

�LogFOLLOW = the change in the log of average analyst following (i.e., the number of analysts follow-ing the firm) between the pre- and post-mandatory-adoption windows.

ROA = average return on assets (net income / total assets) for the pre-mandatory-adoptionwindow.

TOBIN Q = average Tobin’s q for the pre-mandatory-adoption window. Tobin’s q is market valueof assets / book value of assets, where the numerator is measured as (book value ofassets + market value of common equity – book value of common equity – balancesheet deferred taxes).

LEVERAGE = average leverage (total liabilities / total assets) for the pre-mandatory-adoption win-dow.

CLOSEHELD = average percentage of closely hold shares (number of closely held shares / commonshares outstanding) as reported by Datastream/Worldscope in the pre-mandatory-adoption window.

FOREIGNSALES = average percentage of foreign sales (foreign sales / total sales) for the pre-mandatory-adoption window as reported by Datastream/Worldscope.

BIG4 = a dummy variable indicating the presence of a big-four auditor in the year immedi-ately before switching to IFRS.

�LogSIZE = the change in the log of average market capitalization between the pre- and post-mandatory-adoption windows.

�LogHORIZON = the change in the log of average forecast horizon (the number of days between theforecast issue date and the earnings announcement date) between the pre- and post-mandatory-adoption windows.

the effects of TOBIN Q , CLOSEHELD, and BIG4 are statistically larger forthe Low LAW-High IFRSdiff group than the other two groups. These resultsconfirm our expectation that in countries with weak enforcement regimes,firm-level reporting incentives play a relatively greater role in determiningthe effect of mandatory IFRS adoption.

4.5. ANALYSIS OF ANALYSTS’ PUBLIC AND PRIVATE INFORMATION