Embed Size (px)

Citation preview

The Effect of the Use of International Tax Systems on Developing Countries: An African

Perspective

Tax Justice, Poverty and Development

19/11/09 Attiya Waris, University of Nairobi, Kenya 2

An African Approach to:

1.Paying Tax and Receiving Benefits

2.Avoiding and Evading Taxes

3.State Failure to Provide Benefits

4.Tax Havens

5.Advantages of Tax Havens

6.Users of Tax Havens

7.Effects of Tax Havens

19/11/09 Attiya Waris, University of Nairobi, Kenya 4

1. Paying Taxes and Receiving Benefits

The French Declaration on the Rights of Man 1789

13. A common contribution is essential for the maintenance of the public forces and for the cost of administration. This should be equitably distributed among all the citizens in proportion to their means.

14. All the citizens have a right to decide, either personally or by their representatives, as to the necessity of the public contribution; to grant this freely; to know to what uses it is put; and to fix the proportion, the mode of assessment and of collection and the duration of the taxes.

19/11/09 Attiya Waris, University of Nairobi, Kenya 5

Tax revenue and tax expenditure

State Resources

International Donors (Aid and Loans)

Government Business

Taxation

International Trade

State Expenditure

Infrastructure

Health

Education

Social Security

Defence

Housing

Judiciary

Parliament

Executive

19/11/09 Attiya Waris, University of Nairobi, Kenya 6

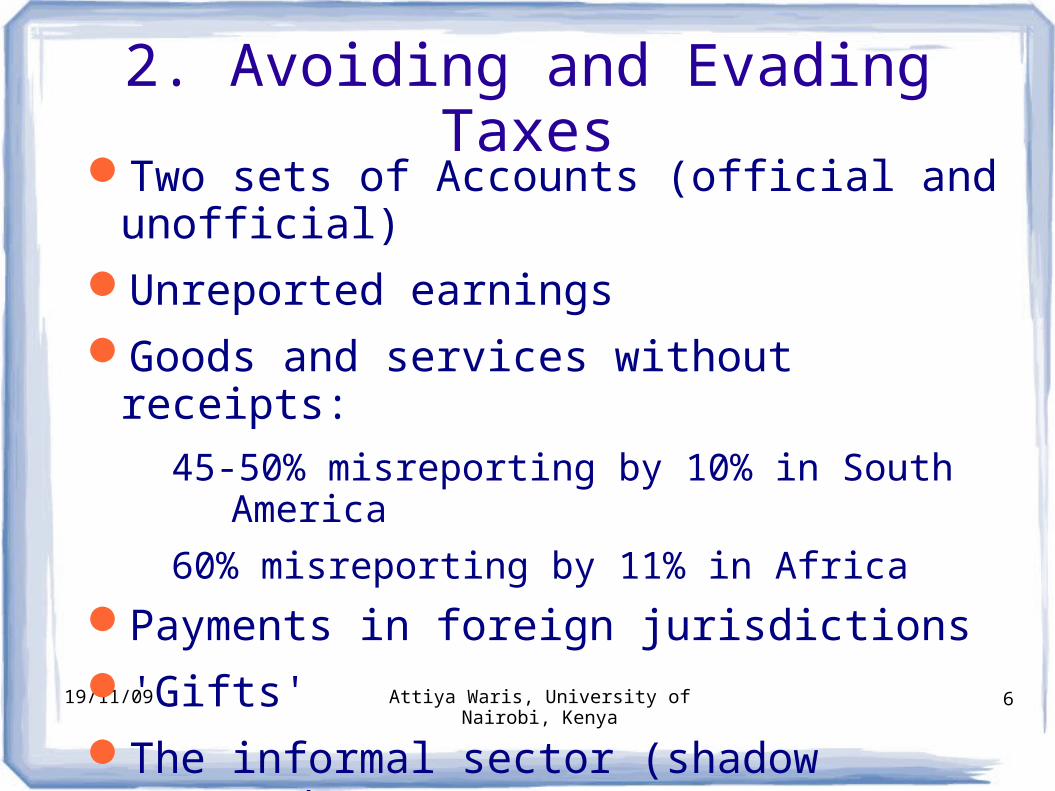

2. Avoiding and Evading TaxesTwo sets of Accounts (official and unofficial)

Unreported earnings

Goods and services without receipts:

45-50% misreporting by 10% in South America

60% misreporting by 11% in Africa

Payments in foreign jurisdictions

'Gifts'

The informal sector (shadow economy)

19/11/09 Attiya Waris, University of Nairobi, Kenya 8

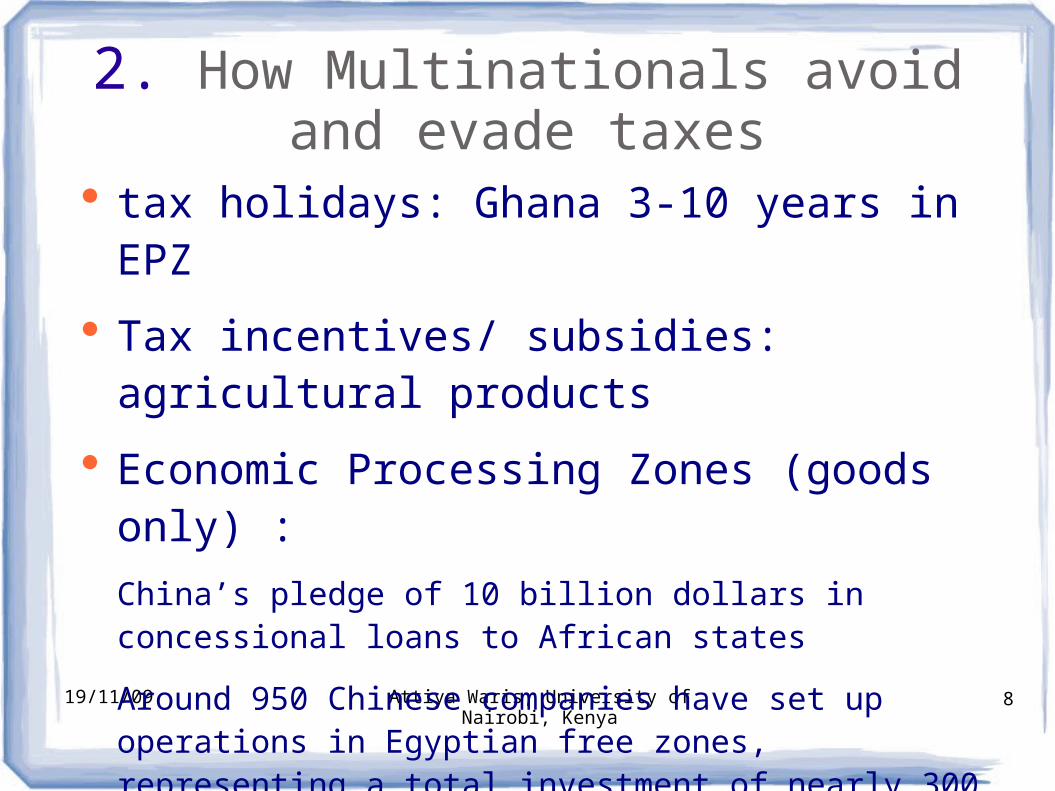

2. How Multinationals avoid and evade taxes

tax holidays: Ghana 3-10 years in EPZ

Tax incentives/ subsidies: agricultural products

Economic Processing Zones (goods only) :

China’s pledge of 10 billion dollars in concessional loans to African states

Around 950 Chinese companies have set up operations in Egyptian free zones, representing a total investment of nearly 300 million dollars (17th November 2009)

2. How Multinationals avoid and evade taxes

• Industrial Processing Zones (goods and services)

• Use of Tax havens: Mauritius

• Freedom of Information and Confidential agreements

• Use of legal loopholes/tax planning/exemptions: Tanzanite in Tanzania

• Corruption

2. Comparing FDI v Profits Leaving Africa

1995-2003 US$ million loss

• DRC 1,150

• Nigeria 1,603

• Botswana 4,678

• Angola 3,592

• Cameroon 156

• Kenya 50

19/11/09 Attiya Waris, University of Nairobi, Kenya 11

2. Case Study: Unilever Case

Arms length pricing

Transfer pricing

Decision: Application of OECD Guidelines

Whether in the absence of specific guidelines from the Kenya Revenue Authority the OECD (The Organization for Economic Co-operation and Development) guidelines and the methods prescribed there under for the calculation of an arm’s length price are proper basis for the determination of an arm’s length price as required under section 18() - when the Act provides no guidelines, other guidelines should be looked at a tax payer is entitled to demand that his liability to a higher charge should be made out with reasonable clarity, before he is adversely affected

19/11/09 Attiya Waris, University of Nairobi, Kenya 12

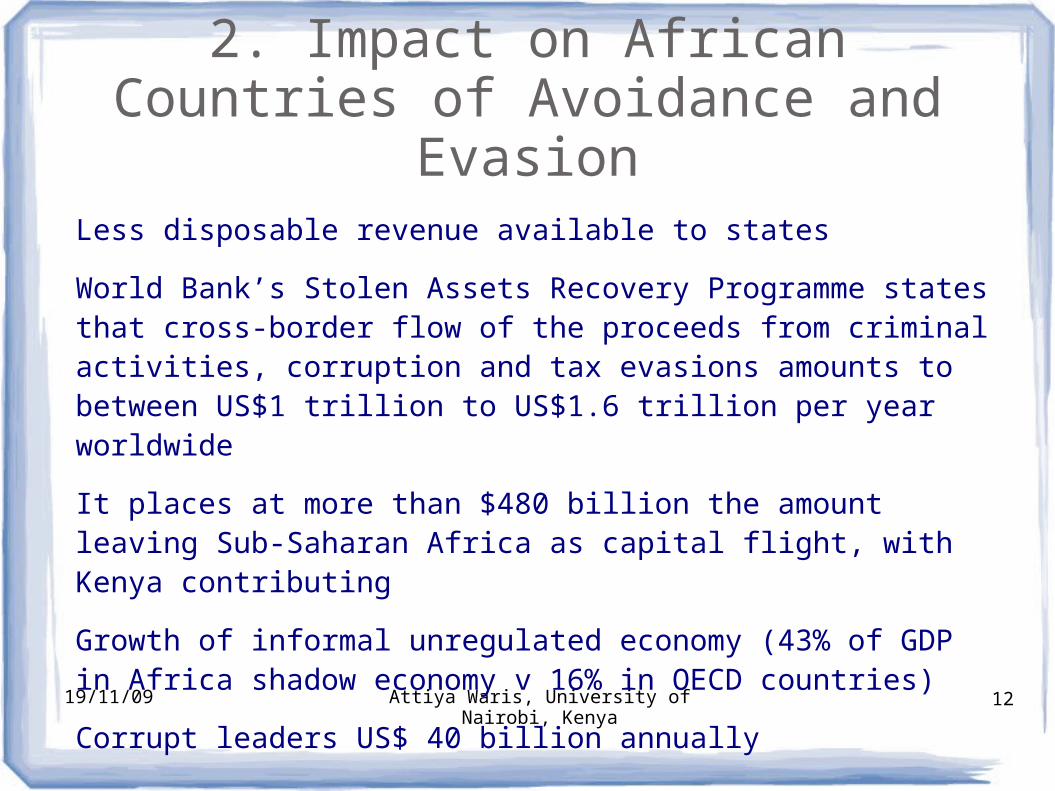

2. Impact on African Countries of Avoidance and Evasion

Less disposable revenue available to states

World Bank’s Stolen Assets Recovery Programme states that cross-border flow of the proceeds from criminal activities, corruption and tax evasions amounts to between US$1 trillion to US$1.6 trillion per year worldwide

It places at more than $480 billion the amount leaving Sub-Saharan Africa as capital flight, with Kenya contributing

Growth of informal unregulated economy (43% of GDP in Africa shadow economy v 16% in OECD countries)

Corrupt leaders US$ 40 billion annually

19/11/09 Attiya Waris, University of Nairobi, Kenya 13

3. State Failure to Provide Benefits

Poor policies

Foreign imposed policies (WB, IMF)

Loan Conditionalities

No independent contextualised policy development

Globalisation and trade liberalisation

Poverty Share

Legend:

41 1 0

(No data

)

1 India: 41.01 % of world's poor

2 China: 22.12 % of world's poor

3 Nigeria: 8.03 % of world's poor

4 Pakistan: 3.86 % of world's poor

5 Bangladesh: 3.49 % of world's poor

6 Brazil: 1.82 % of world's poor

6 Ethiopia: 1.82 % of world's poor

8 Indonesia: 1.49 % of world's poor

9 Mexico: 1.43 % of world's poor

10 Russia: 0.99 % of world's poor

11 Ghana: 0.78 % of world's poor

11 Nepal: 0.78 % of world's poor 13 Colombia: 0.76 % of world's poor 14 Kenya: 0.72 % of world's poor 15 Mali: 0.71 % of world's poor 16 Madagascar: 0.68 % of world's poor 17 Burkina Faso: 0.62 % of world's poor 18 Mozambique: 0.61 % of world's poor 18 Tanzania: 0.61 % of world's poor 20 Niger: 0.59 % of world's poor

19/11/09 Attiya Waris, University of Nairobi, Kenya 17

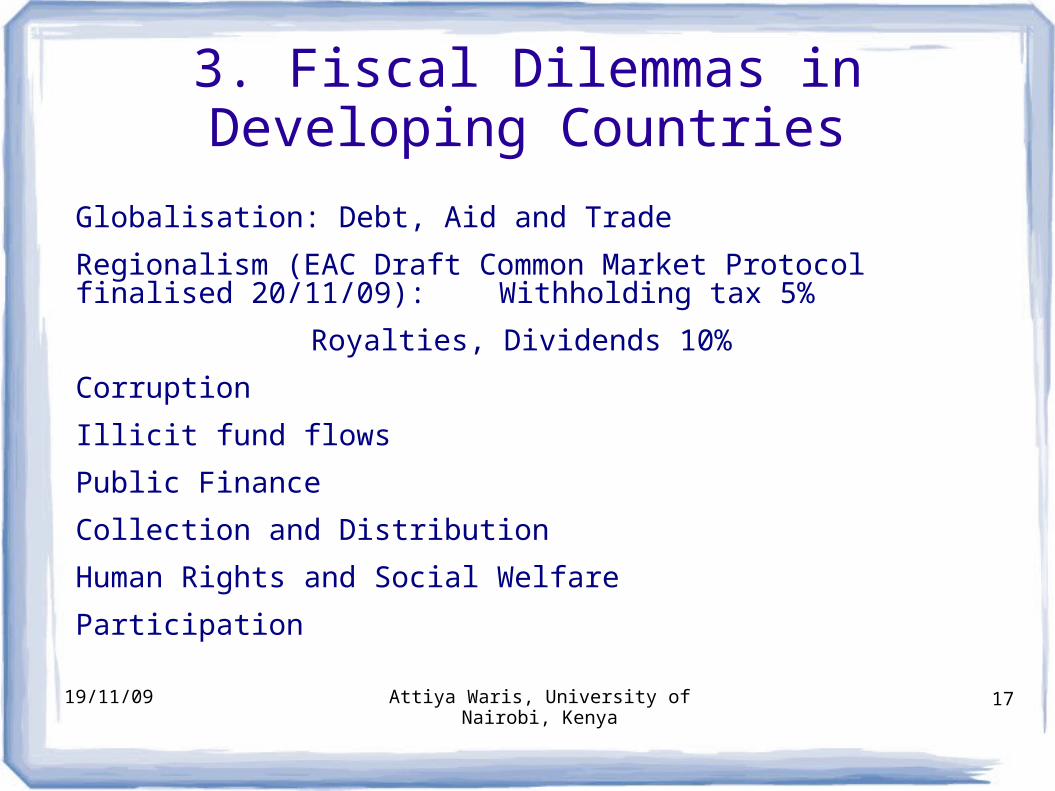

3. Fiscal Dilemmas in Developing Countries

Globalisation: Debt, Aid and Trade

Regionalism (EAC Draft Common Market Protocol finalised 20/11/09): Withholding tax 5%

Royalties, Dividends 10%

Corruption

Illicit fund flows

Public Finance

Collection and Distribution

Human Rights and Social Welfare

Participation

19/11/09 Attiya Waris, University of Nairobi, Kenya 18

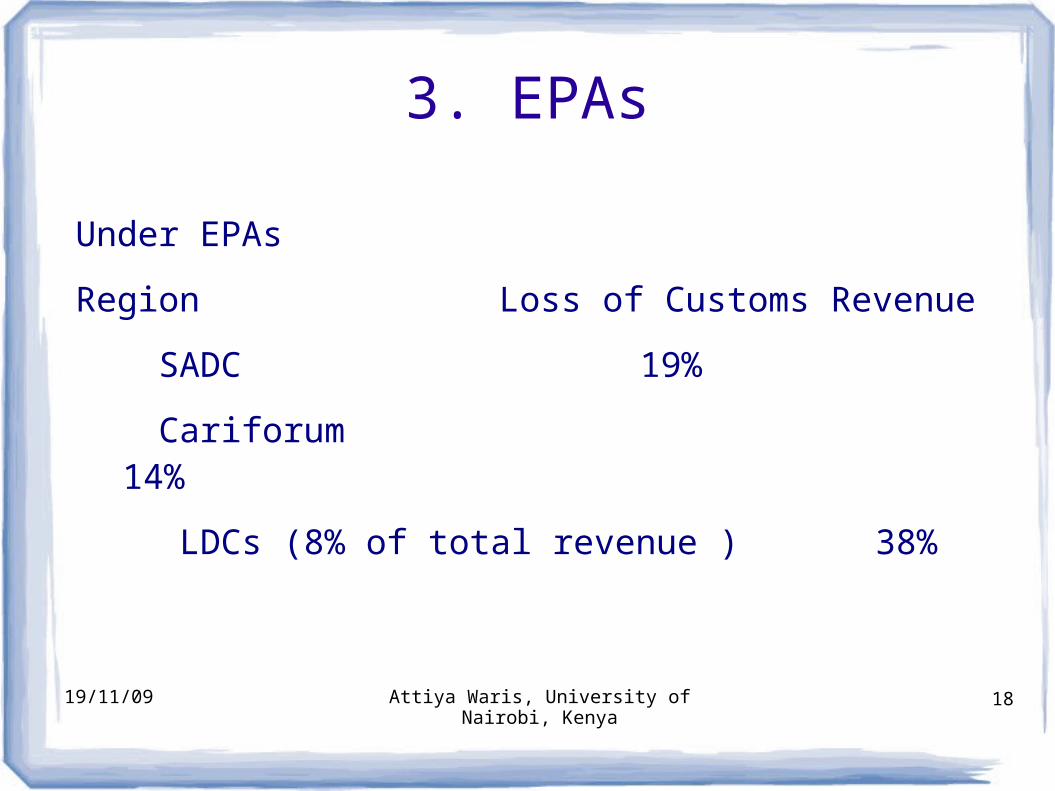

3. EPAs

Under EPAs

Region Loss of Customs Revenue

SADC 19%

Cariforum 14%

LDCs (8% of total revenue ) 38%

19/11/09 Attiya Waris, University of Nairobi, Kenya 19

4. Tax Havens

Tax efficiency=denying sovereign governments their income

Allen Kagina Customs Commissioner Rwanda noted capital flight, presence of tax havens and the continent’s dependence on foreign assistance and indebtedness as some of the most pressing issues of the revenue sector. “Billions of dollars leave the African continent each year. Between 1961 and 2004, these outflows are estimated at around 7.6 per cent of the annual GDP of the region and in effect make African countries net creditors of donor countries,”

19/11/09 Attiya Waris, University of Nairobi, Kenya 20

5. Users of Tax Havens

Ordinary citizens with a certain income level

Scared citizens (unstable state)

Foreigners (expatriat workers)

Tax evaders: Corporations

Criminals (drug dealers)

Corrupt persons

19/11/09 Attiya Waris, University of Nairobi, Kenya 21

6. Effects of Tax Havens

Fiscal drain from one state to another

Bloating of economies

Instability of economies

Encouraging corruption/criminal activity

Poverty

19/11/09 Attiya Waris, University of Nairobi, Kenya 22

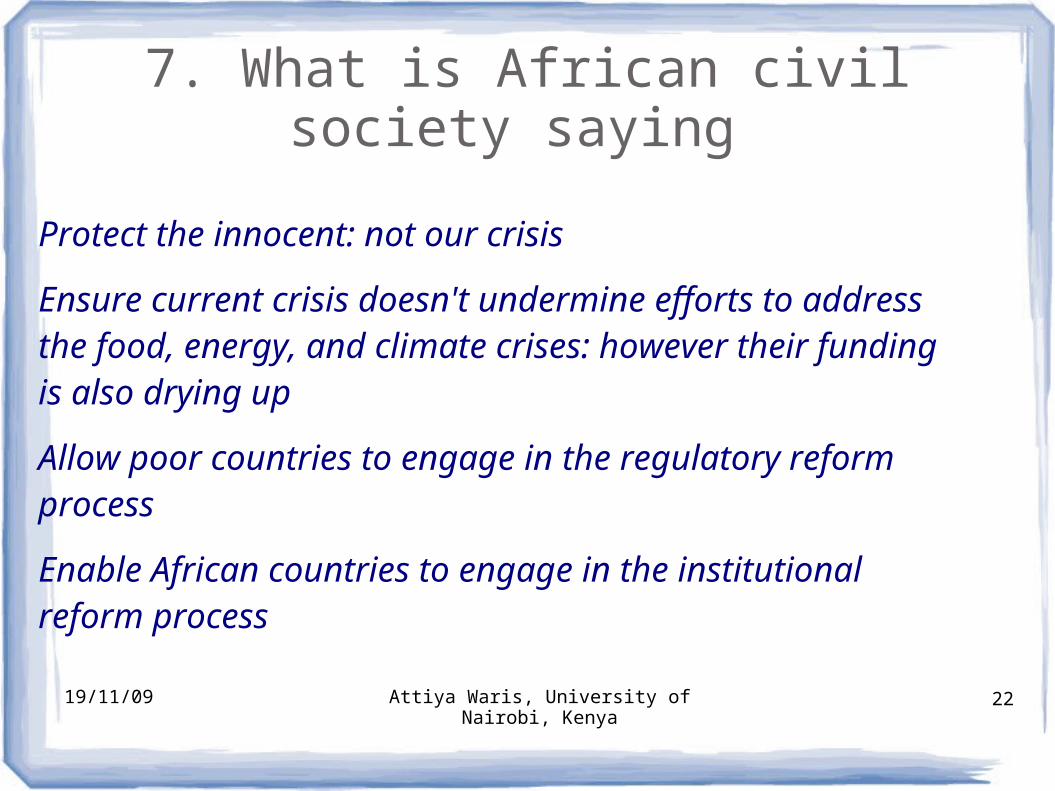

7. What is African civil society saying

Protect the innocent: not our crisis

Ensure current crisis doesn't undermine efforts to address the food, energy, and climate crises: however their funding is also drying up

Allow poor countries to engage in the regulatory reform process

Enable African countries to engage in the institutional reform process

19/11/09 Attiya Waris, University of Nairobi, Kenya 23

8. Recommendations

Support the debt campaign

Asking for more direct income redistribution schemes from the natural resources.

Strengthening public finances

Accountability, responsibility and transparency

Equity in redistribution

19/11/09 Attiya Waris, University of Nairobi, Kenya 24

Recommendations

Constitutionalisation of participation

Financial crisis: break the globalisation trend

Develop more regionalism

Selective decoupling of economies

Pay taxes but demand re-distribution

Tack för er uppmärksamhet