Embed Size (px)

Citation preview

The Effects of CDS Trading on Information Asymmetry in Syndicated Loans

Dan Amiram Columbia Business School

Columbia University

William Beaver Graduate School of Business

Stanford University

Wayne R. Landsman* Kenan-Flagler Business School

University of North Carolina and

Securities and Exchange Commission

Jianxin Zhao Kenan-Flagler Business School

University of North Carolina

October 2016

Journal of Financial Economics, Forthcoming

We thank Mary Barth, Nittai Bergman, Robert Bushman, Ilya Dichev, Miguel Ferreira, Fabrizio Ferri, Jon Glover, Bjorn Jorgensen, Alon Kalay, Doron Nissim, Martin Oehmke, Shiva Rajgopal, an anonymous reviewer, and workshop participants at the Cambridge Financial Accounting Symposium, Catolica-Nova Lisbon Accounting Conference, Columbia University, the European Accounting Association Annual Congress, Emory University, IDC Herzliya, London School of Economics, Temple University, the University of Toronto Rotman Research Conference, the UNC-Duke Fall Camp, and the University of North Carolina Chapel Hill for helpful comments. We appreciate funding from the Center for Finance and Accounting Research, Kenan-Flagler Business School, the Center for Global Business and the Economy, Stanford Graduate School of Business, and Columbia Business School. We thank Ki-Soon Choi for research assistance. * Corresponding author at: 300 Kenan Drive, Chapel Hill, NC 27599, USA. Tel.: +1-919-962-3221; fax: +1-919-962-4727, E-mail address: [email protected]. The Securities and Exchange Commission, as a matter of policy, disclaims responsibility for any private publication or statement by any of its employees. The views expressed herein are those of Wayne Landsman and do not necessarily reflect the views of the Commission or of the study’s other coauthors upon the staff of the Commission.

The Effects of CDS Trading on Information Asymmetry in Syndicated Loans

Abstract This study shows that initiation of CDS trading for an entity’s debt increases the share of loans retained by loan syndicate lead arrangers and increases loan spread. These findings are consistent with CDS initiation reducing the effectiveness of a lead arranger’s stake in the loan to serve as a mechanism to address the adverse selection and moral hazard problems in the loan syndicate. Additional findings corroborate this interpretation by revealing a moderating effect for firms with greater transparency, for loans originated by a lead arranger with a strong reputation in this market, and for firms with relatively liquid CDS markets. JEL Classifications: G10, G21, G32 Keywords: CDS, Syndicated loans, Adverse selection, Moral hazard, Information asymmetry

1

1. Introduction

Syndicated loans are the largest source of US corporate financing activity (Sufi, 2007;

Ivashina, 2009). Globally, the syndicated loan market plays a similarly leading role in corporate

financing, with volume growing from nearly $3 trillion in 2010 to $4.7 trillion in 2014, and

shows no signs of slowing down (Thomson and Reuters, 2014). An important friction in this

market is information asymmetry between the lead arranger, who originates the loan with a

borrower, and the participants within the syndicate. This friction impedes the ability of the lead

arranger to find syndicate participants, which can restrict loan amounts or raise the cost of

borrowing. A well known solution to the information asymmetry problem is for the lead

arranger to have ‘skin in the game’ by holding a share of each originated loan (Sufi, 2007;

Ivashina, 2009; Gopalan, Nanda, and Yerramilli, 2011).

Many believed that the development of the credit default swaps (CDSs) potentially

benefited the lending market by providing the lead arranger with more opportunities to hedge

credit risk, thereby reducing the price of risk. However, initiation of CDS trading also could

have created unintended costs in the lending market. These instruments, which pay their holders

the face value in a case of a reference entity (i.e., borrower) credit event (e.g., debt default) in

return for a premium, were issued first in the early 1990s and reached a peak of $62.2 trillion of

notional outstanding value in 2007 (ISDA, 2013). The introduction of CDS trading potentially

can impede the effectiveness of the lead arranger’s ‘skin in the game’ to resolve the information

asymmetry problem inherent in the loan syndicate. Because the syndicated loan market is a key

source of corporate financing and CDS trading has become widespread, we investigate whether

the initiation of CDS trading exacerbates the information asymmetry problem within the loan

syndicate.

2

In contrast to a traditional bank loan, which involves a single lender, a syndicated loan

involves a group of lenders. Loan syndication has evolved as an efficient mechanism that

permits the lead arranger to share risk with syndicate participants, who depend on the lead

arranger to screen borrowers before loan syndication and monitor borrowers throughout the life

of the loans. Because screening and monitoring efforts are costly and unobservable, the loan

syndication process suffers from information asymmetry problems that can adversely affect the

loan syndication process. The information asymmetry between the lead arranger and syndicate

participants creates an adverse selection problem, in which the lead arranger has an incentive to

misrepresent the quality of syndicated loans, and creates a moral hazard problem, in which the

lead arranger has an incentive to underperform on its monitoring. To mitigate these information

asymmetry problems, syndicate participants can require the lead arranger to retain a larger share

of a loan, i.e., have ‘skin in the game,’ than would otherwise be optimal from a pure risk-sharing

perspective. This ‘skin in the game’ serves as a commitment for the lead arranger to set loan

terms that accurately reflect the riskiness of the loan and to exert monitoring effort after loan

origination.

Initiation of a CDS market introduces a potential positive externality to the syndicated

loan market by providing the lead arranger with an alternative mechanism to hedge exposure to

credit risk associated the portion of the loan it retains. However, the ability of the lead arranger

to hedge credit risk using CDSs introduces a potential negative externality in that CDS trading

reduces the effectiveness of lead arranger ownership to serve as a mechanism to mitigate the

information asymmetry problems of adverse selection and moral hazard. CDS initiation

introduces another negative externality by increasing the default risk of the reference entity

3

because speculators that hold CDSs on the borrower may have incentives to encourage it to

default (e.g., Che and Sethi, 2013; Subrahmanyam, Tang, and Wang, 2014).

We begin our study by first developing a framework for understanding the economic

effects of CDS initiation on loan syndication, which enables us to gain insight into whether CDS

initiation exacerbates adverse selection and moral hazard problems within the syndicate. We do

this by building on Ivashina (2009), which develops an equilibrium model of loan syndication in

which the observed loan spread and a lead bank’s share of a loan corresponds to the intersection

of two pricing schedules representing the syndicate participants’ demand for a proportional share

of a loan and the lead bank’s willingness to retain a proportional share of a loan. We show that

CDS initiation can lead to a variety of new equilibrium combinations of loan share retained by

the lead arranger and borrower loan spread. However, an important observation is that an

increase in neither loan share retained nor loan spread following CDS initiation is sufficient for

evidence of an increase in adverse selection and moral hazard (hereafter information asymmetry)

associated with loan syndication. Observing simultaneous increases in both loan share retained

and loan spread are necessary for there to be an economically significant increase in information

asymmetry.

To analyze empirically the effect of CDS trading initiation on the loan share retained and

loan spread of the syndicated loan market, we obtain CDS trading information from Markit and

collect a sample of 22,406 loan contracts from Dealscan over the period 1993-2014. We

investigate the effects of CDS initiation on the share retained by the lead arranger using a

research design borrowed from Bertrand and Mullainathan (2003) that controls for borrower and

time fixed effects. In all tests we also include as controls firm- and loan-specific characteristics.

We find that CDS initiation is associated with an increase in the loan share retained by the lead

4

arranger. This finding is consistent with two alternative explanations. The first is that CDS

initiation introduces a positive externality arising from the availability to the lead arranger of an

alternative means to diversify credit risk exposure to a loan. The second is that CDS initiation

introduces a negative externality arising from the reduced effectiveness of lead arranger

ownership to serve as a mechanism to mitigate the information asymmetry problems.

To help distinguish whether the ownership structure changes more likely arise from the

lead arranger’s diversification benefit or an increase in information asymmetry problems, we

also test for the effect on loan spreads arising from CDS initiation. Findings from this test

indicate that average loan spread increases. As we explain in section 2, finding an increase in

both loan share retained by the lead arranger and loan spread is evidence consistent with CDS

initiation introducing a negative externality arising from an increase in information asymmetry

that more than offsets any possible positive externality from diversification.

A research design problem common to studies on CDS initiation is that CDS initiation is

possibly endogenously related to an increase in credit risk or change in some other unobservable

time varying characteristics of the reference entity. To address this possibility, following prior

literature, we conduct additional tests including the use of a propensity score matched sample, an

entropy balanced sample, and instrumental variable approaches (two-stage least squares and

Heckman correction) that utilize an instrument used in related prior studies (e.g., Saretto and

Tookes, 2013; Subarhmanyam et al., 2014). Findings from these tests reveal the same inferences

as those based on our primary tests. Because we base our tests on a difference-in-differences

research design, we also conduct additional analyses to test whether there is a pre-determined

trend in the dependent variables for the CDS traded firms relative to the non-CDS traded firms,

and whether our findings are robust to limiting the sample to loans immediately before and after

5

CDS initiation. Findings reveal no evidence of a pre-determined trend and that inferences are

robust to estimating the models with the short window sample.

Finally, to mitigate the potential for alternative explanations for our results, we also

conduct cross-sectional tests to determine whether the effects of CDS initiation on syndicated

loan structure and loan spread vary with borrower transparency and lead arranger reputation, two

factors that prior literature shows moderate the effects of the information asymmetry problems

within the loan syndicate. Regarding borrower transparency, if a borrower’s risks and activities

are more transparent, then the information asymmetry problems are less severe and monitoring

by lead arrangers is less important to syndicate participants. As a result, the information

asymmetry problems created by CDS trading is likely to be less severe for more transparent

firms. We test our prediction of a moderating influence of a borrower’s transparency using a

measure of the debt-contracting value of borrowers’ accounting information in explaining credit

ratings (Ball et al., 2008). Findings from these tests support our prediction that for firms with

higher transparency there are smaller increases in loan share retained by the lead arranger and

loan spreads following CDS initiation. Similarly, we also find that, as predicted, our

documented effects of CDS initiation on loan share retained and loan spreads are less

pronounced when the lead arranger has a strong reputation in the syndicated loan market. This is

because lead arrangers with a strong reputation to protect have greater incentives to screen and

monitor borrowers, which mitigates the information asymmetry problems.

A key assumption in our use of CDS initiation as an indication that the cost of

anonymously hedging its retained credit risk in the borrower decreases for the lead arranger is

predicated on the existence of a liquid CDS market. As a result, we predict and find evidence of

larger share retained by the lead arranger and higher loan spreads relating to loans for which

6

CDS contracts are relatively liquid. These findings suggest that existence of a liquid CDS

market better enables the lead arranger to hedge its retained credit risk using CDS, thereby

exacerbating information asymmetry effects of CDS initiation.

Our study contributes to the literature by documenting the effects of CDS initiation on the

information asymmetry problems in the syndicated loan market. Although prior studies find that

CDS initiation is associated with an increase in reference entity bankruptcy risk (Subarhmanyam

et al., 2014), an increase in loan spread for relatively opaque reference entities (Ashcraft and

Santos, 2009), and an increase in lead arranger ownership (Streitz, 2016), our study is the first to

provide evidence that CDS initiation exacerbates the moral hazard and adverse selection

problems in the syndicated loan market. Finding an increase in both loan share retained by the

lead arranger and loan spread and that these increases are larger for borrowers with lower

transparency and for loans originated by a lead arranger with a relatively low reputation in the

syndicated loan market enable us to infer that CDS initiation results in an increase in information

asymmetry that more than offsets possible diversification benefits to the lead arranger. Thus,

CDS initiation reduces the effectiveness of a lead arranger’s stake in the loan to serve as a

mechanism to address the information asymmetry problems.

The remainder of the paper is organized as follows. The next section discusses the

institutional background, related literature, and provides our predictions. Section 3 presents our

research design, section 4 describes our sample and data, and section 5 presents our results.

Section 6 provides concluding remarks.

2. Background and predictions

A credit default swap (CDS) is essentially an insurance contract that provides that the

seller of the CDS compensates the buyer in the event of a debt default or other specified credit

7

event relating to a specific entity. The CDS contract typically requires the buyer of the CDS to

make a series of payments to the seller throughout the life of the debt and, in exchange, the buyer

receives a payoff if the debt defaults. The availability of a CDS market can significantly reduce

the cost of hedging credit risk exposure to a borrower for holders of the borrower’s debt

securities. CDS transactions are conducted through an over-the-counter market and thus are

unobservable to parties outside of the deal. Therefore, if a CDS market for a firm’s debt is

available, the lead arranger anonymously can purchase CDSs to lay off credit risk associated

with the portion of the loan it holds.1 Although there are so-called “loan-only” CDS contracts,

LCDS, credit protection buyers—including lead arranger banks—typically use CDS contracts as

a means to hedge credit risk of the borrower because the market for LCDS contracts is relatively

illiquid.2

The ability of the lead arranger to lay off credit risk has several potential economic

effects on loan syndication, particularly syndicate ownership structure and loan spread. To

understand these economic effects and develop predictions, we build on Ivashina (2009), which

develops an equilibrium model of loan syndication in which the observed loan spread and a lead

bank’s share of a loan correspond to the intersection of two pricing schedules representing the

syndicate participants’ demand for a proportional share of a loan and the lead bank’s willingness

to retain a proportional share of a loan. Fig. 1, which plots loan spread and share retained by the

1 The lead arranger’s actions are, in principle, observable to the CDS seller only, i.e., its actions are unobservable by syndicate participants. To the extent that the lead arranger is concerned about maintaining anonymity with all parties, including the seller, it can arrange for a third party to purchase the CDS directly from the seller and then acquire the CDS from the third party. 2 The most prevalent form of CDS contracts are those written on bonds. Such contracts have been written since inception of CDS market. However, since 2007 LCDS have begun to be traded with some degree of frequency and it is generally the case that since 2007 LCDS markets continue to be less liquid than CDS markets (Choudhry, 2011). Because LCDS contracts are linked to secured loans with higher recovery rates than unsecured bonds, spreads for LCDS contracts generally are smaller than those for CDS contracts for the same reference entity. However, because loan and bond contracts typically are cross-referenced with respect to a defining default event, the default event date is normally the same for CDS and LCDS.

8

lead arranger, illustrates the model. In the presence of adverse selection arising from syndicate

participants being unable to observe the creditworthiness of the borrower and the moral hazard

problem arising from their inability to assess whether the lead arranger monitors the borrower’s

activities throughout the life of the loan, the syndicate participants’ demand curve is downward-

sloping. Other things equal, syndicate participants demand a higher loan spread the greater are

the information asymmetry problems. The downward slope of their demand curve, DSynd,

reflects their requiring a lower loan spread when the lead arranger retains a larger proportion of

the loan, which reduces the information asymmetry problems. Because of the lead arranger’s

desire to diversify loan portfolio risk, as the share retained increases, the greater must be the loan

spread to compensate the lead arranger for the greater risk exposure. Hence, the lead arranger’s

demand curve, DLeadA, is upward sloping. The intersection of the two demand curves yields

the equilibrium loan spread and share retained by the lead arranger given by E(0).

The first economic effect of CDS initiation on loan syndication relates to a shift in the

syndicate participants’ demand curve resulting from an increase in information asymmetry risk.

The ability of lead arrangers to anonymously lay off credit risk using CDS reduces their

incentive to screen and monitor borrowers (e.g., Morrison, 2005). As a result, holding a portion

of the loan no longer provides as credible commitment as before CDS initiation that the lead

arranger will provide a fair assessment of the riskiness of the loan and exert monitoring effort.

Moreover, because CDSs allow banks and creditors to transfer risk exposure to third parties

through the purchase of CDS protection, an “empty creditor” problem is created in that creditors

with CDS insurance are better off when the borrowing firm defaults and may even have

incentives to push the borrower into default (Hu and Black, 2008a, 2008b) or inefficient

9

bankruptcy because the lender’s total pay-off would be higher in that event (Bolton and Oehmke,

2011).

Thus, CDS initiation exposes syndicate participants to increased information asymmetry

risk. Of course, loan syndicate participants are likely to take actions to protect themselves from

these increased risks arising from CDS initiation, resulting in a new equilibrium loan spread and

share retained by the lead arranger. In the context of the Ivashina (2009) framework, for a given

level of lead bank’s share in the loan, syndicate participants will demand higher spreads because

of CDS initiation, which results in a shift of the syndicate demand curve to the right. This is

shown in Fig. 2, where DSynd_pre and Dsynd_post are the demand curves before and after CDS

initiation.3 Note that in the absence of a shift in the lead arranger’s demand curve, DLeadA, the

resulting equilibrium, E(1), is a greater share retained by the lead arranger after CDS initiation

and a larger loan spread. We refer to this shift in the syndicate participants’ demand curve as the

adverse selection/moral hazard effect arising from CDS initiation. In the limit, if the increase in

the adverse selection/moral hazard effect is sufficiently large, the lead arranger will have to

retain the entire loan, i.e., the loan will be issued as a sole lending loan, and the syndicate

structure fully breaks down.

The second and third economic effects of CDS initiation on loan syndication relate to

shifts in the lead arranger’s demand curve. The first shift arises from the lead arranger’s reduced

cost of hedging exposure to the borrower’s credit risk after CDS initiation. Development of the

CDS market for a borrower provides the lead arranger (and other holders of a borrower’s debt)

with an additional way to hedge or lay off credit risk exposure to the borrower without having to

3 For ease of exposition and because there is no effect on our predictions, we do not consider the slope and potential changes in the slope of the Dsynd and the DLeadA curves after CDS initiation.

10

sell its stake in the loan.4 This enables the lead arranger to reduce the cost of hedging the

borrower’s credit risk while maintaining a lending relationship with the borrower (Saretto and

Tookes, 2013) and provides the lead arranger with an opportunity to reduce regulatory capital

requirements (Martin and Roychowdhury, 2015). Even if lenders do not purchase CDSs

immediately, the existence of CDS markets provides a liquid resale option and makes holding

credit risk more attractive. Because CDS initiation provides an additional way for the lead

arranger to reduce the risk exposure from holding a share in a loan, in the context of the Ivashina

(2009) framework, for each level of shares retained by the lead arranger, the lead arranger is

willing to charge a lower level of loan spread. As shown in Fig. 3, this implies a shift of the lead

arranger’s demand curve to the right, where DLeadA_pre and DLeadA_post_1 are the lead

arranger’s demand curves before and after CDS initiation. Note that in the absence of a shift in

the syndicate participants’ demand curve, Dsynd, after CDS initiation the resulting equilibrium,

E(1), is a greater share retained by the lead arranger but a lower loan spread faced by the

borrower. We refer to this shift in the lead arranger’s demand curve as the diversification effect.

In the limit, if the diversification effect is sufficiently large, the new equilibrium can result in the

lead arranger retaining 100% of the loan, i.e., the loan is issued as a sole lending loan.

The second shift in the lead arranger’s demand curve arises from the fact that CDS

initiation also reduces the cost of speculation for investors who are not creditors. Such investors

may have incentives to cause the borrower to default on its loans (Soros, 2009; Stulz, 2010;

Portes, 2010; Markose et al., 2012; Che and Sethi, 2013), which increases the credit risk of loans

4 Even though, in principle, syndicate participants also can purchase CDSs to reduce their exposure to the borrower’s credit risk, they have less incentive than the lead arranger to do so. Typically the lead arranger’s primary objective in arranging debt financing for the borrower is to generate origination fees, and therefore prefers to have minimal exposure to the borrower’s credit risk. In contrast, syndicate participants purchase shares of the syndicated loans with the objective of generating interest revenue from the loans. Purchasing CDSs by syndicate participants would reduce their exposure to loans at a cost of sacrificing their net revenue.

11

in the lead arranger’s portfolio.5 However, this increase in credit risk likely is idiosyncratic to

the lead arranger and not borne by the syndicate participants. Whereas the lead bank typically

retains a large share of the loan, each syndicate participant typically holds a small proportion and

can diversify away the extra risk arising from CDS initiation (Ivashina, 2009). The increase in

default risk on the lead arranger’s portfolio will shift the lead arranger’s curve to the left, as the

lead arranger will want to diversify more for a given level of interest spread. We refer to this

shift in the lead arranger’s demand curve as the credit risk effect. Thus, despite the potential

benefits of diversification brought about by CDS initiation, it is possible that this credit risk

effect arising from CDS initiation could result in the lead arranger’s curve shifting on net to the

left, which is illustrated as DLeadA_post_2 in Fig. 3. Note that in contrast to the equilibrium

associated with the diversification effect, E(1), the equilibrium associated with the credit risk

effect, E(2), is a smaller share retained by the lead arranger but a greater loan spread faced by the

borrower. That is E(1) and E(2) have opposite effects on share retained by the lead arranger and

loan spread when compared to E(0).

The resulting equilibrium following CDS initiation depends on the relative magnitude of

the adverse selection/moral hazard effect. Returning to Fig. 3, if there is little or no adverse

selection/moral hazard effect, then as noted above, the resulting equilibrium is either E(1) or

E(2). In the case of the first equilibrium, E(1), the diversification effect causes DLeadA_pre to

shift to the right, which results in an increase in the share retained by the lead arranger but a

decrease in the borrower’s loan spread. Conversely, in the case of the second equilibrium, E(2),

the credit risk effect dominates the diversification effect, causing DLeadA_pre to shift to the left

5 To see this, consider the hypothetical example of insurers issuing homeowner policies that provide a payoff to the policyholder in the event of a house fire for a home not owned by the policyholder. Although CDS holders cannot necessarily directly cause a borrower to default on a loan (or, by analogy, “burn down” a home), actions they take collectively in the credit markets—including “bear raiding,” i.e., spreading negative information about a borrower—can make it difficult for a borrower to secure future borrowing.

12

such that there is a decrease in the share retained by the lead arranger but an increase in the

borrower’s loan spread.

However, CDS initiation can result in an increase in the adverse selection/moral hazard

effect such that it is sufficiently large so as to dominate the diversification effect (a shift to the

right) or the credit risk effect (a shift to the left). In this case, as Fig. 3 illustrates, the shift in the

syndicate participants’ demand curve from DSynd_pre to DSynd_post results in increases in

share retained by the lead arranger and loan spread. That is, in Fig. 3, for both of the new

equilibria, E(3) and E(4), share of a loan retained by the lead arranger and loan spread are higher

than are the amounts for E(0). Thus, we will observe an increase in both share of a loan retained

by the lead arranger and loan spread only if there also is an adverse selection/moral hazard effect

that causes a shift to the right in the syndicate participants’ demand curve.

Taken together, Fig. 3 illustrates that CDS initiation can lead to a variety of new

equilibrium combinations of changes in loan share retained by the lead arranger and loan spread.

However, two other observations based on the figures are noteworthy. First, as Fig. 3 makes

clear, an economically significant adverse selection/moral hazard effect following CDS initiation

will lead to an increase in both loan share retained and loan spread. Second, observing either an

increase in loan share retained or loan spread alone is not sufficient for determining whether

there is an adverse selection/moral hazard effect.

One caveat is in order regarding our predictions. As noted above, we expect that the

credit risk effect of CDS initiation will only affect the lead arranger’s demand schedule and not

the syndicate participants’ demand schedule. This assumption may not hold empirically if the

syndicate participants cannot diversify away the credit risk increase. If this is the case, then the

syndicate demand curve could also shift to the right. Such a shift could result in observing an

13

increase in loan spread regardless of the effect of credit risk on the lead arranger’s pricing

schedule, although it is unclear what would be the resulting equilibrium share retained by the

lead arranger. In addition, observing an increase in both loan share and loan spread no longer

would imply that CDS initiation creates a net adverse selection/moral hazard effect that is caused

by lead arranger using CDSs to hedge credit risk. As a result, following Ivashina (2009) and as

described in the section below, we include a proxy for credit risk when conducting our empirical

tests as a control for the impact of change in credit risk on the syndicate participants’ pricing

schedule.

3. Research design

In this section we describe the empirical relations between CDS initiation and changes in

loan syndication ownership structure and loan spread. Following Ashcraft and Santos (2009)

and others, we assume that the first trading date is associated with an economically significant

reduced cost of hedging credit risk and speculation. Because the cost of hedging may not fall

substantially until the CDS market for the borrower becomes liquid enough to make it practical

to hedge credit risk, using the first date can mismeasure when the cost of hedging credit risk

falls, which would make it more difficult to detect effects of CDS initiation on syndicate

ownership structure and spread. In addition, use of the binary event—initiation of CDS

trading—precludes us from exploiting the cross-sectional and intertemporal variation in the

liquidity of the CDS market. Although it is difficult to develop a continuous measure of change

in the cost of hedging credit risk based on CDS market liquidity because standard liquidity

measures such as bid-ask spread and trading volume generally are not publicly available, in

section 5.5.3 below, we extend our tests to include a measure of CDS market liquidity based on

the number of CDS dealers.

14

3.1. The effect of CDS trading on syndicate ownership structure

To test whether CDS initiation leads to an increase, decrease, or no change in the share

retained by the lead arranger, we estimate the following linear regression model given by Eq. (1):

_ it it i i t t itLEAD OWN TradedPost Controls D Dβ γ α α ε= + + + + (1)

_LEAD OWN is percentage of a loan retained by lead arrangers. TradedPost is an indicator

variable that equals one if a loan is issued after the month of CDS initiation, and zero otherwise.

Di, and Dt are firm, and year-month fixed effects, where subscripts i and t refer to borrower and

year and month at loan origination. This methodology, which follows Bertrand and

Mullainathan (2003) and is used in prior studies that examine the effects of events on loan

contracting terms (e.g., Sapienza 2002; Valta, 2012), controls for fixed differences between firms

that have CDS contracts traded and those that do not via the firm fixed effects, and controls for

aggregate fluctuations via the year-month fixed effects. As such, Eq. (1) is essentially a

difference-in-differences research design.6 If CDS initiation is associated with an increase

(decrease, no change) in the share retained by the lead arranger, then 0 ( 0, 0)β β β> < = .

Controls is a set of control variables for a variety of firm- and loan-specific

characteristics suggested by prior research to affect loan syndication. The firm characteristics

include return on assets, ROA; profit margin, Profit; the debt-to asset-ratio, Leverage; firm size

as measured by the natural logarithm of total assets, Log_asset; and a set of indicator variables

corresponding to each of 22 possible credit ratings (e.g., AAA, AA+, AA, etc.).7 Loan

6 Because we cannot assign a specific treatment date for each control firm, we estimate Eq. (1) and Eq. (2) using the Bertrand and Mullainathan (2003) difference-in-differences design. In section 5.4 below, we present findings in which we match each CDS traded firm to a non-CDS traded firm and use the loan immediately before and after CDS initiation for the CDS traded firm. This enables us to use a standard difference-in-differences design because we can identify a treatment date for the non-CDS traded firms. 7 For firms without credit ratings, we follow the approach in Barth et al. (1998) to use accounting measures to generate credit ratings. We also estimated a version of Eqs. (1) and (2) that include an indicator variable for whether

15

characteristics, include loan spread, LoanSpread, revolver lines, Revolver; term loan B or below,

TermLoanB; and presence of guarantors, Guarantor; the loan dollar amount in billions,

LoanAmt; the loan term in months, Maturity; the number of financial covenants, NCOV; an

indicator variable that equals one if a loan is secured and zero otherwise, Securdum; and a set of

30 indicator variables for loan purpose, e.g., whether a loan is used to finance an acquisition or

whether a loan is used to execute a leveraged buyout.8 All firm firm-level variables are

measured as of the most recent quarterly financial reporting date. We cluster standard errors at

the firm level.

3.2. The effect of CDS trading on loan pricing

To examine the effect of CDS initiation on loan pricing, we estimate the following

regression model:

it it i i t t itLoanSpread TradedPost Controls D Dβ γ α α ε= + + + + (2)

The dependent variable, LoanSpread, is loan spread based on the all-in-drawn spreads over

LIBOR at issue date for loans issued to firm i in year t. Because loan spreads are highly skewed,

following prior studies (e.g., Graham, Li, and Qiu, 2008; Chava et al., 2009), we measure

LoanSpread as the natural logarithm of the actual loan spread. If CDS initiation is associated

with an increase (decrease, no change) in the loan spread, then 0 ( 0, 0)β β β> < = . Eq. (2)

includes the same set of control variables as those in Eq. (1), omitting LoanSpread.9 In addition,

we include in Eq. (2) an additional loan characteristic, the number of lenders, Lender_num.

a firm has a credit rating, and do not estimate credit ratings for firms that are not rated. Untabulated findings from these estimates result in the same inferences as those based on tabulated findings. 8 To the extent that changes in ownership structure and loan spread are simultaneously determined, inclusion of loan characteristics, particularly LoanSpread, in Eqs. (1) and (2), can mitigate the effects of potential simultaneity bias on the TradedPost coefficient. 9 We also estimate versions of Eq. (2) in which we replace LoanSpread with each of four non-price loan terms, LoanAmt, Maturity, NCOV, and Securdum, to examine whether there is any trade-off between price and non-price terms. For example, after CDS initiation borrowers may be charged a higher loan spread—CDS initiation is costly,

16

4. Data and sample

We start by merging the quarterly CRSP-Compustat database with Dealscan to identify a

sample of non-financial US firms that have private loan information and accounting and price

information.10 Each observation in the analysis corresponds to a separate loan agreement, i.e.,

loan deal. We use the following steps to identify CDS initiations for the firms in our sample.

First, we identify all the firms in our merged sample that ever had a CDS traded on their debt

according to Markit. Next, following Ashcraft and Santos (2009), for every firm we identify the

first date on which a five-year-to maturity, U.S.-dollar-denominated CDS contract is traded. We

use this date as the date of the onset of CDS trading. We eliminate all firms that have a CDS

initiation date in January 2001 because the Markit database begins its coverage then and thus the

CDS initiation date for these firms is ambiguous. We use all loans in the period 1993-2014 with

available data necessary to estimate Eqs (1) and (2). The resulting sample includes 836 CDS

traded firms with 7,046 loans issued by these firms over the period 1993-2014. This is CDS

traded sample we use for estimation of Eq. (2), the loan spread model.

Using the Markit database to identify the initiation of CDS trading as a means to assess

when the cost of hedging credit risk changed for lead arrangers posses a few challenges. First,

Markit is a contributor-based database. Markit’s CDS User Guide states that as of March 2012,

22 global banks contributed data, with over one million data points are being contributed daily

across approximately 3,000 entity-tiers. For a given contract, Markit calculates a composite

CDS spread if Markit has received prices from at least 3 distinct dealers, of which at least 2 have

but may be able to get expanded access to bank lending capital—CDS initiation is beneficial. If this is the case, then the effect of CDS initiation on loan contract terms is ambiguous. However, following prior research, we can interpret the effect of CDS initiation on loan pricing more definitively if the inferences are consistent across the LoanSpread and four non-price loan term estimations. Untabulated findings indicate that there is no evidence of any such trade-off between spreads and these non-price terms after CDS initiation. 10 Financial firms are those with two-digit SIC between 60 and 64, inclusive (Ivashina, 2009).

17

passed all data cleaning tests that are proprietary to Markit. As a result, the actual date when

CDS trading begins for a firm may not be the same as date trade information first appears on the

Markit database. This is unlikely to be a serious problem because syndicated loan originations

are infrequent, averaging 22 months between consecutive originations for our sample firms.

Therefore, the time lag between the date of initial trading and appearance on the Markit database

would have to be several months or more to misclassify a loan originating before or after CDS

trading.

Second, the Markit database only includes CDS contracts written on bonds, i.e., it does

not include LCDS contracts. Because CDS spreads generally exceed LCDS spreads, it is

possible that the initiation of CDS trading did not lower the cost of hedging for lead arrangers,

and they had to wait until LCDS contracts appeared (if at all) later in our sample period to hedge

credit risk. Nonetheless, as noted above, because the market for LCDS contracts is relatively

illiquid compared to the market for CDS contracts, banks and other purchasers of credit

protection typically use CDS contracts to hedge credit risk of the borrower.11

To develop the sample for estimation of Eq. (1) we exclude observations for which shares

retained by the lead arranger are unavailable. We generally follow Sufi (2007) to identify who

the lead arranger is for a loan deal.12 Lenders’ commitments, including the lead bank’s share, are

settled at the end of loan syndication. As with Ivashina (2009), information regarding shares

11 Whether the cost of hedging for the lead arranger is significantly lower using LCDS than CDS depends on whether they have substantially different spreads as well as the relative liquidity of the two markets. Regarding spreads, untabulated statistics reveal that 93% of our sample CDS contracts are written on senior unsecured bonds, 2% are written on senior secured bonds, and 5% are written on subordinated bonds. Recovery rates for senior bonds are closer to those for loans than for other subordinated bonds. As a result, spreads for our sample firms’ CDS contracts are likely to be closer to those for LCDS than those for other subordinated bonds. 12 We use two variables to classify lenders as either lead arrangers or participants. Both are available from Dealscan. One variable is “Lead arranger credit” and the other is “Lender role”. We designate as lead arrangers any lender for which the field “lead arranger credit” is marked “Yes”. If this field is unavailable, then lenders that act as an administrative agent, agent, arranger, bookrunner, lead arranger, lead bank, or lead manager are defined to be lead arrangers. When a loan has more than one lead arranger, following Ivashina (2009), we treat them as a single entity when calculating share retained by the lead arranger.

18

retained by the lead arranger is available for only approximately 30% of loans for which we can

identify a lead arranger. Ivashina (2009) notes that there is a reporting bias regarding lead

arranger share in DealScan towards large loans, which implies that the sample loans we use in

our tests are likely to relate to relatively large and transparent borrowers. Other things equal, this

will make it difficult to detect changes in share retained by lead arranger and loan spread

following CDS initiation.13 The resulting sample for the lead arranger’s ownership analysis, Eq.

(1), contains 616 CDS traded firms and 2,321 loans issued by these firms. Because lead bank

share is missing more than 70% of the time when loan spread is available, the sample size for the

lead arranger’ ownership analysis is smaller than that for the loan spread analysis, Eq. (2), which

as discussed above contains 836 CDS traded firms with 7,046 loans.14

We obtain our control sample using all US private loans issued by non-CDS-traded firms

with available data in Dealscan. The sample of loans for firms that never have CDS traded

contracts during our sample period includes 4,974 firms with 15,360 loans issued by these firms

over the same period. Thus, for the loan spread analysis, Eq. (2), our sample comprises 22,406

loans (7,046 for CDS traded firms and 15,360 loans for non-CDS traded firms) from 5,810

unique firms (836 CDS traded and 4,974 non-CDS traded firms). For the lead arranger’s

ownership analysis, Eq. (1), there are 6,201 syndicated loans (2,321 and 3,880 loans for CDS and

non-CDS traded firms) from 2,599 firms (616 CDS traded and 1,983 non-CDS traded firms).

Syndicated loans can be structured in several facilities. As a result, following Ivashina (2009),

when there is more than one facility in a loan package, we use the loan characteristics of the

13 Ivashina (2009) also provides evidence that the reporting bias grows stronger over time. Ivashina (2009) suggests that inclusion of time fixed effects mitigates the effects of this bias. Therefore, we include time fixed effects in our research design. 14 Untabulated findings relating to our loan spread analysis using the same sample as the lead arranger’s analysis yield the same inferences as those based on the tabulated findings.

19

largest facility. Specifically, we measure loan spread, loan amount, maturity, and other facility

level variables based on the largest facility.

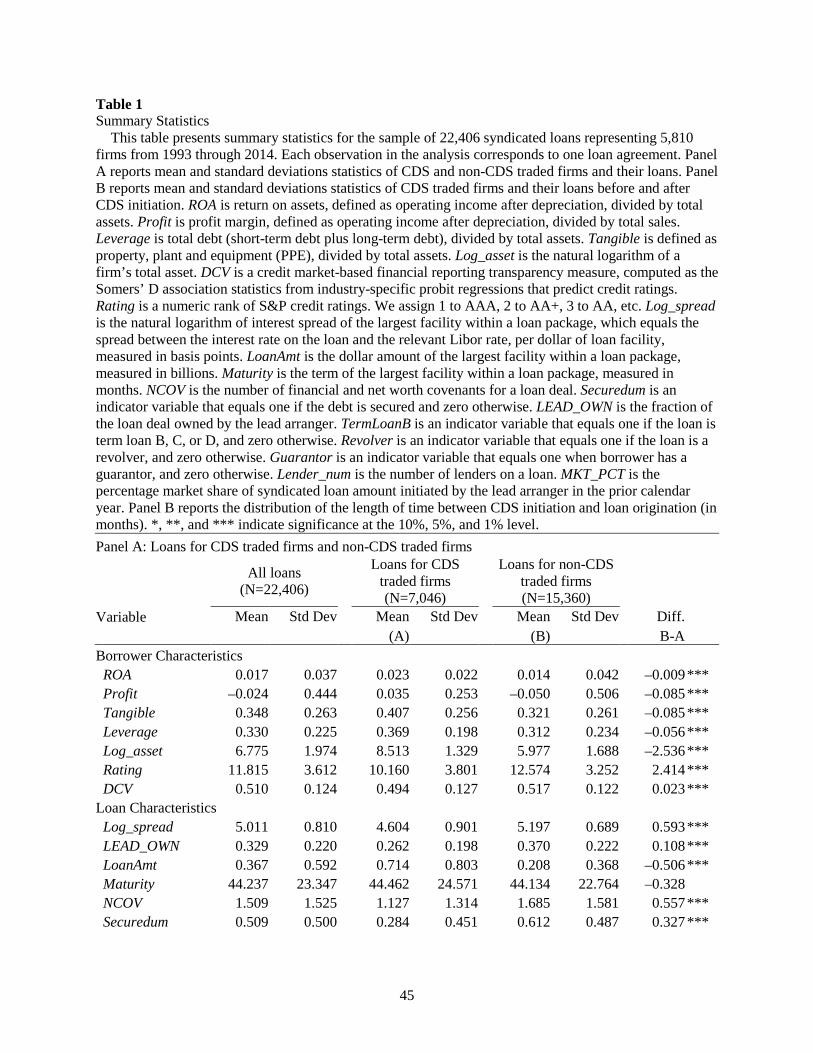

Table 1, Panel A, presents mean and standard deviation statistics for the full sample, as

well as separate statistics for CDS traded and non-CDS traded firms. The statistics indicate that

there are significant mean differences in firm and loan characteristics between the two groups.

Notably, the CDS traded firms are larger (Log_asset: 8.513 vs. 5.977), more profitable (ROA:

0.023 vs. 0.014), and have better credit ratings (Rating: 10.160 vs. 12.574). In addition, mean

log loan spread and share of the loan retained by the lead arranger are significantly smaller for

CDS traded firms (4.604 vs. 5.197 and 26.2% vs. 37%).

Table 1, Panel B, which presents mean and standard deviation statistics for CDS traded

firms before and after CDS trading, reveals that mean log loan spread and share of the loan

retained by the lead arranger are significantly larger after CDS trading (4.726 vs. 4.490 and

30.5% vs. 22.5%). In addition, there are significant differences in each of the borrower and loan

characteristics. Notably, two credit risk measures, credit ratings and leverage, Rating and

Leverage, are consistent with firms’ credit quality improving slightly after CDS trading, which

taken at face value is inconsistent with the observed increase in loan share retained and spreads

following CDS trading being attributable to an increase in credit risk. In addition, average loan

size and average loan maturity, LoanAmt and Maturity, increase, and the number of financial

covenants for a loan and the likelihood of collateral, NCOV and Securedum, also decrease.

The statistics in Panel B showing that loans within CDS traded firms differ significantly

before and after CDS trading along dimensions suggests the possibility that the firms before and

after CDS initiation fundamentally differ in other unobservable dimensions. If the key

assumption of this design, i.e., the dependent variables in Eqs. (1) and (2) follow parallel trends

20

for CDS and non-CDS traded firms, is valid, then employing our difference-in-differences design

with firm and time fixed effects helps to mitigate the effect on our inferences of such

unobservable differences. However, the statistics in Panel A showing that CDS traded firms

differ significantly from non-CDS traded firms along several dimensions suggests the possibility

that the parallel trend assumption may not hold. Therefore, as discussed in section 5.3 below, we

conduct additional tests to address these issues, including estimation of Eqs. (1) and (2) using a

propensity score-matched sample and an entropy balanced sample.

Finally, Table 1, Panel C, which presents descriptive statistics relating to the distribution

of the number of months between CDS initiation and loan origination, indicates that few sample

loans are originated in the months surrounding CDS initiation. For example, 75% of all loans are

originated at least 23 months before or after CDS initiation. Moreover, the loan origination

distributions before and after CDS initiation are fairly symmetric. These Panel C findings

suggest that CDS initiation does not appear to arise endogenously in anticipation of an increase

in loan origination.

5. Results

5.1. Main Results

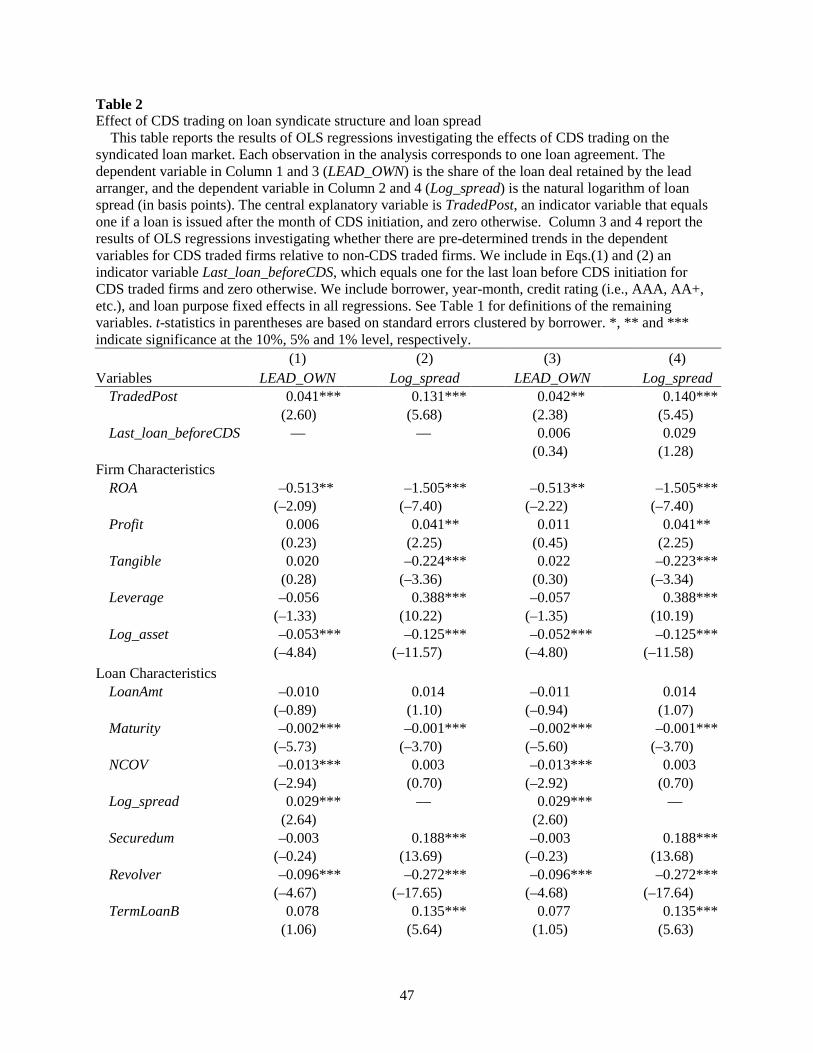

Table 2, Columns 1 and 2, reports the regression summary statistics associated with

estimation of Eqs. (1) and (2) using all loans as described in section 4. Regarding Eq. (1), the

key finding is that the TradedPost coefficient, 0.041, is significantly positive (t-statistic =

2.60).15 The magnitudes of the coefficients are also economically significant. In particular, the

TradedPost coefficient implies that the onset of CDS trading leads to an incremental increase in

15 Throughout, when discussing a coefficient, we use the term significant to denote a 5% significance level under a two-sided alternative.

21

the percentage of the loan retained by the lead arranger in excess of 4.1%, which is 12.5% of the

sample mean for loan share retained by CDS traded firms, 30.5%.

This finding is consistent with CDS initiation increasing the loan share retained by the

lead arranger. As explained in the prior section, these increases after CDS initiation could reflect

the positive effect of a more efficient alternative diversification mechanism for the lead arranger

or because the negative effect of reducing the effectiveness of ownership in mitigating

information asymmetry problems. To identify which effect most likely accounts for such an

increase, we now turn to observing the effect of CDS initiation on loan spreads.

Regarding Eq. (2), the key finding in Column 2 is that the TradedPost coefficient is

significantly positive (coefficient = 0.131; t-statistic = 5.68). The magnitude of the coefficient is

also economically significant, implying that the onset of CDS trading leads to an increase of

approximately 13% of loan spreads. This implies that for a firm that faced a loan spread of

197bp before CDS initiation, the average loan spread for firms in our sample, its loan spread

increased to approximately 228bp after CDS initiation. Finding an increase in loan spread

following CDS initiation, together with the finding in Column 1 showing an increase in loan

share retained by the lead arranger, is indicative of a significant increase in the adverse

selection/moral hazard effect.16 Moreover, the findings suggest that CDS initiation results in an

increase in an information asymmetry cost that more than offsets possible diversification benefits

to the lead arranger. Thus, CDS initiation reduces the effectiveness of a lead arranger’s stake in

the loan to serve as a mechanism to address the information asymmetry problems.

16 Although Ashcraft and Santos (2009) does not examine the effect of CDS initiation on the share retained by the lead arranger, viewed in isolation the study’s finding of no effect of CDS trading on loan spreads for the average sample firm suggests that the adverse selection/moral hazard and diversification effects are, on average, offsetting. There are several sample and research design differences between Ashcraft and Santos (2009) and our study that likely account for different loan spread results. For example, relative to our study, Ashcraft and Santos (2009) is limited to a smaller sample (approximately 1/5 our sample size) comprised of mostly larger borrowers that, other things equal, are relatively transparent and less likely to be affected by CDS initiation.

22

The majority of the control variables’ coefficients are significant, with signs that are

largely consistent with prior research. For example, firms with high return on assets, ROA, on

average have a lower cost of debt. Larger firms (Log_asset) and firms with more tangible assets

(Tangible) enjoying lower load spreads, and more highly leveraged firms (Leverage) paying

higher spreads; the significantly negative coefficient on Revolver and significantly positive

coefficient on TermLoanB indicate that revolver loans and term loans B (i.e., those in which

syndicate participants are non-bank institutions) face lower and higher rates (Harjoto et al., 2004;

Zhang, 2008; Nandy and Shao, 2010; Lim et al., 2013).

Regarding the four non-price loan terms, the loan amount (LoanAmt) and the number of

covenants (NCOV) coefficients are insignificant. However, there is a significantly positive

relation between the loan spread and collateral (Securedum) (Berger and Udell, 1990; Bradley

and Roberts, 2004), and a significantly negative relation between loan spread and maturity,

which perhaps reflects the endogenous determination of loan contractual terms.17

We also estimated Eqs. (1) and (2) decomposing Leverage into bank debt leverage and

non-bank debt leverage, which effectively relaxes the constraint that these two sources of

leverage have the same effects on loan syndicate structure and loan spread. We do so to mitigate

the concern that CDS initiation could be correlated with the extent there is a change in firm’s

debt structure, i.e., bank debt vs. non-bank debt, which also could affect loan syndicate structure

and spread. Untabulated findings reveal that although the coefficients on bank debt and non-

bank debt leverage differ from each other, the TradedPost coefficients in the LEAD_OWN and

Log_spread estimations, 0.039 and 0.130 (t-statistics = 2.54 and 5.63), are similar in magnitude

17 Untabulated findings from estimations of Eq. (2) that exclude the four non-price loan terms yield the same inference regarding the association between TradedPost and loan spread, i.e., the TradedPost coefficient is significantly positive. These additional findings are consistent with simultaneous determination of loan terms not being the cause of the positive relation.

23

to those reported in Table 2.18 Relatedly, we also test whether loans are more likely to be used

for refinancing purposes after CDS initiation by estimating a linear probability model of loan

refinancing using the same independent variables and same design as in Eq. (2). Untabulated

statistics reveal that there is no significant difference in the likelihood of loans being used for

refinancing before and after CDS initiation (t-statistic = 1.04).

5.2. Testing for a pre-determined trend

The finding in Table 1 showing that CDS traded firms have different firm characteristics

before and after CDS initiation raises the question of whether there is a pre-determined trend in

the share retained by the lead arranger and loan spread for the CDS traded firms relative to the

non-CDS traded firms. Existence of such a trend could call into question the parallel trend

assumption that underlies the difference-in-differences design of Eqs. (1) and (2). If there is a

pre-determined trend, then such a trend likely begins before CDS initiation, which should

manifest as an increase in loan share retained and spread for loans immediately preceding CDS

initiation (e.g., Heider and Ljungvist, 2015). Therefore, we modify and estimate Eqs. (1) and (2)

by including an indicator variable, Last_loan_beforeCDS, that equals one if the loan is the last

loan originated before CDS initiation, and zero otherwise. In these estimations, the coefficient

on this indicator variable reflects the difference in the loan share retained and spread between the

last loan before CDS initiation and the loans that preceded it. Therefore, finding that this

coefficient is not different from zero provides evidence in support of the parallel trend

assumption in our tests.

18 We construct bank debt and non-bank debt as of the most recent financial reporting date preceding each loan origination date using loan amount and maturity information from Dealscan. Following Ozelge and Saunders (2012), we set bank debt equal to total loans outstanding, and set non-bank debt equal to total debt less total loans outstanding. This approach for calculating loans outstanding using Dealscan is similar to that used by Ivashina et al. (2009) and Gopalan et al. (2011) for calculating the exposure particular banks have to particular borrowers.

24

Table 2, Columns 3 and 4, presents the findings from these estimations. The findings

reveal that the coefficients on the indicator variable, Last_loan_beforeCDS, are insignificant

(coefficients = 0.006 and 0.029, t-statistics = 0.34 and 1.28), which means that the share retained

and spread of the last loans immediately before CDS initiation are not significantly different

from those of the prior loans. The findings also reveal that the indicator variable’s coefficients

are significantly smaller than the TradedPost coefficients, 0.042 and 0.140, which means that

loans following CDS initiation have significantly larger share retained and spread than the last

loans originated before CDS initiation. Taken together these findings not only increase our

confidence that the observed increases in share retained by the lead arranger and loan spread are

not attributable to pre-determined trends, but also increase our confidence that CDS initiation is

the underlying event that affected the observed changes in syndicated loan market structure and

loan pricing.

5.3. Endogeneity: matched sample and instrumental variable approaches

A key assumption of the regression approach represented by Eqs. (1) and (2) and

similarly employed in prior literature (Ashcraft and Santos, 2009; Subarhmanyam et al., 2014) is

that the timing of CDS introduction is exogenous. However, it is possible that the initiation of

CDS trading for a reference entity is the result of an increase in its credit risk or other

unobservable changes. Hence, changes in syndicate ownership structure and loan terms could be

the result of these changes and not CDS initiation. If this is the case, then the estimated

parameters in Eqs. (1) and (2) are subject to endogeneity bias.

We address potential endogeneity bias when assessing the effect of CDS initiation on

loan share retained and loan pricing in two approaches: by estimating Eqs. (1) and (2) using

matched sample approaches and instrumental variables approaches.

25

5.3.1 Matched sample approaches

Regarding the propensity score matched sample approach, we match each CDS traded

firm with a non-CDS traded firm based on propensity scores, and then use the loan observations

of the CDS traded firms and matched non-CDS traded firms to estimate Eqs. (1) and (2). We do

this by first estimating a Probit model with TradedPost as the dependent variable and the firm-

specific variables as independent variables, and then using the estimated model parameters to

calculate propensity scores for each firm.19 We match each CDS firm to the non-CDS trading

firm whose propensity score is closest, doing so without replacement.20 Untabulated statistics

reveal that CDS traded and matched non-CDS traded firms differ significantly only along two

dimensions. In particular, as in prior research (Ashcraft and Santos, 2009; Subrahmanyam et al.,

2014) we find that CDS traded firms are significantly larger and have significantly higher credit

ratings than matched non-CDS traded firms. The effects of these two differences are mitigated

by including firm size and credit rating when estimating Eqs. (1) and (2).

Table 3, Panel A, reports the regression summary statistics associated with estimation of

Eqs. (1) and (2) using the propensity score-matched sample. The key finding is that the

TradedPost coefficient is significantly positive in both estimations (coefficients = 0.031 and

0.064; t-statistics = 2.07 and 2.71). As in Table 2, the magnitudes of the coefficients are also

economically significant, although they are somewhat smaller. In particular, the TradedPost

19 Also, although the unit of analysis for Eqs. (1) and (2) is at the loan level, following Ashcraft and Santos (2009) and Subrahmanyam et al. (2014), we match each CDS traded firm to a non-CDS traded firm based on firm characteristics for both sets of firms as of the quarter in which CDS initiation occurs. To obtain a sample for estimating propensity scores, we use firm-quarter observations. We estimate the propensity score model using all CDS traded firms’ quarterly observations between 2001 and the date of CDS initiation for each firm; and all potential control firms’ quarterly observations between 2001 and the last sample quarter, quarter 4 of 2014. Following Ashcraft and Santos (2009), we begin the propensity score estimation sample in 2001 because this is the earliest year in which a CDS initiation occurs in our sample. 20 Untabulated statistics reveal that the number of CDS traded firms used in the propensity score matched sample tests are 582 and 783 for Eqs. (1) and (2). The loss of 34 and 53 firms is largely attributable to missing data for CDS-traded firms necessary to estimate the Probit model of the likelihood of CDS trading.

26

coefficient implies that the onset of CDS trading leads to an incremental increase in the

percentage of the loan retained by the lead arranger of 3.1% and an increase in loan spread of

approximately 12.8 basis points for the average sample loan.

As noted above, on average the CDS traded firms are larger and have higher credit

ratings than their matched non-CDS traded firms. To mitigate the influence these differences

could have on our inferences, we also estimated Eqs. (1) and (2) using an alternative matching

process, entropy balancing, that by design ensures that the treatment and control groups’

covariates, i.e., firm characteristics, are balanced at the mean (Hainmueller, 2012). Untabulated

findings result in the same inferences regarding the TradedPost coefficients as those based on the

Tables 2 findings. In particular, the TradedPost coefficient is significantly positive in both Eqs.

(1) and (2) (coefficients = 0.032 and 0.065; t-statistics = 1.97 and 2.68).

5.3.2 Instrumental variable approaches

We also apply instrumental variable approaches to mitigate further the concern that CDS

initiation arises endogenously. Following Saretto and Tookes (2013) and Subarhmanyam et al.

(2014), we use the foreign exchange (FX) hedging position of lenders, Lender_FX, as an

instrument for Tradedpost. A lender’s use of foreign exchange hedging is related to its general

propensity to hedge risk. Lenders with larger FX hedging positions are more likely to trade the

CDS of their borrowers. However, because the aggregate FX hedging interests of a bank are

unlikely to be related to the credit quality or other characteristics of a particular borrower,

Lender_FX likely satisfies the exclusion restriction requirement (Saretto and Tookes, 2013;

Subarhmanyam et al., 2014).

To construct Lender_FX, we first identify lenders for our sample firms based on

Dealscan. We then obtain foreign exchange derivative positions of the bank holding companies

27

of borrowers’ lead banks using Federal Reserve Call Reports. For each borrower in each quarter,

Lender_FX is constructed as the ratio of the notional volume of foreign exchange derivatives

used for hedging purposes to total assets, averaged across the banks that served as a lead arranger

for the firm over the previous five years. For each loan origination, we use the Lender_FX from

the most recent quarter. Because our key independent variable, TradedPost, is an endogenous

binary variable, following Bharath et al. (2011) and Saretto and Tookes (2013), we implement

our instrumental variable approach using the method described by Wooldrige (2010).

Specifically, we use a first-stage probit model to estimate the predicted value for TradedPost,

which is then used as an instrument in the standard two-stage least squares estimation.21 When

estimating the probit model for Eqs (1) and (2), in addition to Lender_FX we include all control

variables in the respective equations.22 Untabulated statistics reveal that the probit models for

Eqs (1) and (2) indicate that Lender_FX is not weak. In particular, as predicted, the coefficient

on Lender_FX is positive and significant and the incremental Wald 2χ -statistics are 15.7 and

44.1, and are significant at less than the 0.001 level.

Table 3, Panel B, reports the regression summary statistics associated with estimation of

Eqs. (1) and (2) using the two-stage approach. The key finding is that the coefficient for the

fitted TradedPost coefficient is significantly positive in both estimations (coefficients = 0.161

and 0.411; t-statistics = 5.13 and 9.46). These findings suggest that a one standard deviation

increase in the fitted value of TradedPost from the probit model implies increases in loan share

retained and loan spread of 4.4% and 9.7%, which are consistent with the findings in Table 2.

21 Wooldridge (2010) shows that two-stage least squares coefficients are consistent and their standard errors are still asymptotically valid. 22 Estimating this two-stage procedure with firm fixed effects when the endogenous variable is binary may result in biased coefficients. Therefore, following Saretto and Tookes (2013), we also estimate the two-stage least squares models using industry fixed effects. Inferences from this alternative estimation are identical to the ones reported in the paper.

28

Following Subarhmanyam et al. (2014) we also use the instrumental variable to

implement the Heckman-correction procedure, which involves estimating a probit model using

Lender_FX as an instrumental variable in the first-stage probit model. Untabulated findings

indicate that the effects of CDS initiation on share retained by the lead arranger and loan pricing

are similar to those based on the Table 2 findings. In particular, the TradedPost coefficients are

positive and significant for both Eqs. (1) and (2). In addition, we implemented the propensity

score matched sample approach by including Lender_FX in the probit model used to predict

CDS trading. Untabulated findings yield the same inferences as those based on the Table 3,

Panel A, findings.

Taken together, the findings in Table 3 provide additional support that the inferences we

draw from the Table 2 findings—that CDS initiation has adverse effects on the syndicated loan

market structure and loan pricing—are not the result of the potential endogeneity in the onset of

CDS trading for a firm.

5.4. Loans immediately before and after CDS initiation

The main findings in Table 2 are based on using all loans available during our sample

period. Table 1, Panel C, indicates that the median length of time between CDS initiation date

and loan origination based on all loans is approximately four years. This distance in time

increases the likelihood that other events unrelated to CDS initiation that occur before and after

CDS initiation could be the underlying reason for the increases in the share retained by the lead

arranger and loan spread documented in Table 2. To address this issue, we estimate versions of

Eqs. (1) and (2) that use as observations one loan immediately before and after CDS initiation for

the CDS traded firm and its match. This approach increases our confidence that changes in the

29

share retained by the lead arranger and loan spread for CDS traded firms are attributable to CDS

initiation rather than other events that are unrelated to CDS initiation.

To implement this approach, we first identify four non-CDS traded firms with propensity

scores closest to each CDS traded firm, and assign the CDS initiation date to its four potential

matched firms. Second, from this set of potential matches, we select the non-CDS traded firm

that has loan origination dates closest to the loan dates for the CDS traded firm.23 Minimizing

time differences when selecting a match mitigates the confounding effect of loan differences

arising from being originated at different dates. Limiting the sample of loans to two each for the

CDS traded and its matched non-CDS traded firm results in there being a narrow window of

observation that minimizes the influence of other events on share retained by the lead arranger

and loan spread.24 The median length of time between CDS initiation date and loan origination

for CDS traded firms based on this sample is approximately 1 year (10 and 9 months for loans

before and after CDS initiation). Because each resulting matched pair has the same event date,

i.e., the CDS traded firm’s CDS initiation date, we modify Eqs. (1) and (2) by including an

indicator variable, Post, which equals one if a loan is after the CDS initiation date and zero

otherwise, and an indicator variable, Traded, which equals one if a firm is a CDS traded firm and

zero otherwise, and by replacing firm fixed effects with industry fixed effects (Dj) and year-

month fixed effects with year fixed effects (Dt). The resulting equations are as follows:

1 2 3_ it it it it j j t t itLEAD OWN Post Traded TradedPost Controls D Dβ β β γ α α ε= + + + + + + (3)

23 To do this, for the CDS traded and each potential matched firm, we calculate the number of months between loan origination dates for the two loans immediately before CDS initiation, and repeat this procedure for the two loans immediately after CDS initiation. We then compute the average of the two time differences. We select that non-CDS traded firm with the shortest average time difference. Untabulated statistics reveal the mean (median) average time difference for the resulting matched sample is 10.7 (7.3) months. 24 Untabulated statistics reveal that for both CDS traded and non-CDS traded firms, mean firm characteristics, e.g., ROA, Leverage, and Rating, generally are not statistically or economically different before and after CDS initiation. This is not surprising because the loans, by design, relate to observations that are closer together in time than those for all loans in Table 1.

30

1 2 3it it it it j j t t itLoanSpread Post Traded TradedPost Controls D Dβ β β γ α α ε= + + + + + + (4)

Table 4 presents the regression summary statistics associated with estimation of Eqs. (3)

and (4). There are 231 and 509 matched pairs for Eqs. (3) and (4), comprising 924 and 2,036

loans. The key findings are that the TradedPost coefficients are significantly positive in both

estimations (coefficients = 0.068 and 0.099; t-statistics = 3.15 and 2.94) and, as in Table 2, the

magnitudes of the coefficients are also economically significant. Hence, the findings in Table 4

provide additional support that the inferences we draw from the Table 2 findings—that CDS

initiation has adverse effects on the syndicated loan market structure and loan pricing—are not

the result of other events that are unrelated to the onset of CDS trading for a firm.

5.5. Additional tests: transparency, reputation and liquidity

In this section we present findings from cross-sectional tests to determine whether the

effects of CDS initiation on syndicated loan structure and loan spread vary with borrower

transparency and lead arranger reputation, two factors that prior literature shows moderate the

effects of information asymmetry problems within the loan syndicate. We also present findings

from cross-sectional tests to determine whether the effects of CDS initiation on loan syndication

structure and loan spread vary with CDS market liquidity.

5.5.1. Effect of borrower transparency

The findings in Tables 2 indicate that following CDS initiation there is a significant

increase in the information asymmetry problems. However, if a borrower’s risks and activities

are readily transparent, then the adverse selection problem is less severe and monitoring by lead

arrangers is less important to syndicate participants (Sufi, 2007; Ball et al., 2008). As a result, if

a borrower’s activities are readily transparent, CDS initiation is less likely to have any effect on

adverse selection or moral hazard. In the context of the syndicate analysis in Fig. 3, other things

31

equal, CDS initiation creates less severe information asymmetry problems for a transparent

borrower than for an opaque borrower. As a result, there is a smaller shift to the right of the

syndicate participants’ demand curve, DSynd, for a transparent borrower. Thus, we predict that

CDS initiation causes a smaller increase in share retained by lead arranger and a smaller increase

in loan spread for more transparent firms.

To test our prediction that greater borrower transparency leads to a smaller increase in

shares retained by the lead arranger and a smaller increase in loan spreads, we estimate Eqs. (1)

and (2) separately for firms above and below the sample median, by year, of our financial

reporting transparency measure, DCV. DCV is the debt-contracting value of borrowers’

accounting information developed in Ball, Bushman, and Vasvari (2008) and extended by Dou

(2012). Our DCV measure reflects the inherent ability of firms’ public accounting information to

capture credit quality. DCV is the Somers’ D-statistic derived from the explanatory power of

accounting variables (i.e., earnings, leverage, equity book value and interest coverage) in an

industry-specific probit model of firm credit ratings and ranges from zero—low transparency—

to one—high transparency. As such, DCV reflects the inherent ability of firms’ accounting

amounts to capture credit quality measured at the industry rather than the firm level (see

Appendix for details of how DCV is constructed). If, as we predict, financial reporting

transparency mitigates the adverse effect of CDS trading on loan syndication ownership structure

and loan spread, then the TradedPost coefficient will be smaller for firms with relatively high

DCV.

We use DCV, a measure of financial statement transparency, rather than equity bid-ask

spread or analysts’ coverage (Ashcraft and Santos, 2009) as our measure of transparency for

several reasons. First, whereas DCV relates specifically to the credit market, equity bid-ask

32

spread and analysts’ coverage relate primarily to the equity market. Second, DCV is particularly

relevant to the credit markets at the time of loan initiation because accounting information is the

primary source of information lenders use when they initiate loans. In this regard, prior studies

provide consistent evidence that accounting information plays an important role in the design of

debt contracts (e.g., Ball et al., 2008; Graham et al., 2008; Armstrong et al., 2010; Amiram,

2013). In particular, Ball et al. (2008) demonstrates that when a borrower’s public accounting

information possesses higher DCV, information asymmetry between the lead arranger and other

syndicate participants is lower, which results in lead arrangers being required to retain a lower

loan share.

Table 5, Panel A, reports summary statistics associated with estimation of Eqs. (1) and

(2) for the subsamples of high and low financial reporting transparency, DCV, i.e., firms for

which DCV is above or below the sample median, by year. The key finding in Panel A is that the

TradedPost coefficients are significantly higher for low transparency firms for both analyses,

which is consistent with our prediction that transparency has a moderating influence on the

adverse effect of CDS initiation on the loan syndication market.

Regarding share retained by the lead arranger, Panel A reveals that the TradedPost

coefficients for low and high DCV firms are 0.068 and 0.005, and the difference is significantly

positive ( 2χ -statistic = 10.22, p-value < 0.001).25 These findings imply that CDS trading is

associated with an increase in the percentage of the loan retained by the lead arranger that is

6.3% smaller (= 0.068 – 0.005) for high DCV firms relative to low DCV firms.

25 Because we have a signed prediction for the difference in TradedPost coefficients between low and high transparency firms, we use a 5% significance level under a one-sided alternative. For ease of exposition, the reported p-values in Table 5 assume a two-sided alternative.

33

Finally, regarding loan spread, Panel A reveals that the TradedPost coefficients for low

and high DCV firms are 0.160 and 0.091, and the difference is significantly positive ( 2χ -statistic

= 5.61, p-value = 0.017). This finding implies that CDS trading is associated with an increase in

loan spread that is 6.9% (= 0.160 – 0.091) smaller for high DCV firms relative to low DCV firms,

which is consistent with the finding in Ashcraft and Santos (2009) that opaque firms pay a higher

loan spread following CDS initiation.

We also estimated versions of Eqs. (1) and (2) that use analysts’ coverage, a measure of

transparency used in Ashcraft and Santos (2009), in place of DCV. In particular, we estimate

Eqs. (1) and (2) separately for firms above and below the top quintile of number of analysts

based on each firm’s average number of analysts that follow the firm during our sample period.

Regarding Eq. (1), untabulated findings reveal that the TradedPost coefficients for firms with

number of analysts below and above the top quintile are 0.139 and 0.014, and the difference is

significantly positive ( 2χ -statistic = 18.1, p-value < 0.001). Regarding Eq. (2), untabulated

findings reveal that the TradedPost coefficients for firms with number of analysts below and

above the top quintile are 0.045 and 0.007, and the difference is significantly positive ( 2χ -