Embed Size (px)

Citation preview

DIRECTORATE-GENERAL FOR EXTERNAL POLICIES POLICY DEPARTMENT

POLICY BRIEFING

The EU automotive sector in a globalised market

Abstract

Over the past decade the global car industry has undergone a gradual but significant shift in sales and production numbers from developed into developing markets This shift has plunged many European car manufacturers into a particularly difficult structural crisis as they have had to grapple with falling domestic sales and growing overcapacity issues The economic importance of Europersquos car sector underscores the potential damage that this crisis may inflict on many EU member states

Increasing the volume of exports has been suggested as a solution to the current predicament of Europersquos car industry This policy briefing provides an in-depth analysis of recent trends and possible future developments in nine mature and growing car markets concluding that Europersquos car sector could expand its share in a number of these markets

Tariff and non-tariff barriers however pose a significant obstacle to this scenario and their timely removal is of utmost importance for the European car industry The European Commission included improved market access in its CARS 2020 Action Plan yet the relative ease with which countries can introduce non-tariff barriers remains a cause for concern

DG EXPOBPolDepNote2012_349 December 2012

PE 491464 EN

Policy Department Directorate-General for External Policies

This Policy Briefing is an initiative of the Policy Department DG EXPO

AUTHOR Lukas GAJDOS (Roberto BENDINI sup) Directorate-General for External Policies of the Union Policy Department WIB 06 M 55 rue Wiertz 60 B-1047 Brussels

Feedback to robertobendinieuroparleuropaeu is welcome

Editorial Assistant Jakub PRZETACZNIK

LINGUISTIC VERSIONS Original EN

ABOUT THE PUBLISHER Manuscript completed on 4 December 2012 copy European Union 2012 Printed in Belgium

This Policy Briefing is available on the intranet site of the Directorate-General for External Policies in the Regions and countries or Policy Areas section

To obtain paper copies please send a request by e-mail to poldep-expoeuroparleuropaeu

DISCLAIMER Any opinions expressed in this document are the sole responsibility of the authors and do not necessarily represent the official position of the European Parliament

Reproduction and translation except for commercial purposes are authorised provided the source is acknowledged and provided the publisher is given prior notice and supplied with a copy of the publication

2

The EU automotive sector in a globalised market

Table of contents

1 Introduction 4

2 The global car industry 4

3 The European car industry 8

4 Export markets 16 41 Trade deficit 16

411 Japan 16 412 South Korea 17 413 India 18

42 Trade surplus 19 421 United States 19 422 China 20 423 Russia 21 424 Brazil 22 425 Argentina 23 426 Indonesia 23

5 Tariff and non-tariff barriers 24 51 Tariff barriers 25 52 Non-tariff barriers 25

6 Conclusion 27

3

Policy Department Directorate-General for External Policies

1 Introduction The European car sector is experiencing a particularly difficult period Sales and production numbers have decreased significantly since the onset of the continentrsquos economic difficulties imposing a considerable burden on EU carmakers This burden is two-fold and its effects are closely interlinked as the collapse in car sales is responsible not only for the carmakersrsquo financial difficulties but also for the growing overcapacity problem in certain EU15 countries

Falling sales in Europe contrast with rising sales in developing markets suggesting that further increasing the volume of car exports could be a solution to the European sectorrsquos current woes Numerous tariff and non-tariff barriers however prevent EU car exporters from increasing their sales in growing and more mature markets and restrict their exports to high-end cars

This paper will provide an overview of the global and European car industries with a specific focus on recent trends and problems It will then analyse a number of key European car export market markets and conclude with an overview of trade barriers that hamper market access to these markets

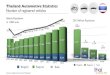

2 The global car industry The automotive industry enjoyed a period of steady growth before the onset of the global financial crisis Production rates increased from 4122 million units in 2000 to 532 million units in 2007 interrupted only by a mild downturn in 2001 The industry was badly affected by the global economic recession and the subsequent decrease in global demand as production slowed down in the final months of 2008 and fell sharply in 2009 by nearly 5 million units It should be noted that this decrease was more pronounced that the contraction of the world economy highlighting the automotive sectorrsquos vulnerability to adverse economic conditions An important turning point for car manufacturers occurred in 2010 when the fall in production numbers halted Production rates exceeded their pre-crisis levels by a considerable margin with 5834 million cars produced worldwide The industry grew by 3 in 2011 with 5995 million units produced The International Organisation of Motor Vehicle Manufacturers (OICA) the principal industry body expects this rate of growth to be maintained in the current year

4

The EU automotive sector in a globalised market

Source OICA data

The recent growth in global demand for passenger cars has been geographically uneven Sales have yet to recover in the region traditionally seen as responsible for demand mdash the Triad (Japan the USA and the EUWestern Europe) particularly in the US and the EU Increasing affluence and demand in developing countries in general and in China in particular sustains the sectorrsquos recent recovery and projected future growth New car registrations in China doubled in two years reaching 1255 million units in 2010 Sales in India grew by two thirds and by one quarter in Brazil during the same period

Sources ACEA Bureau of Transport National Bureau of Statistics of China JAMA Fenabrave SIAM

The changing geographic distribution of passenger car demand has directly influenced changes in the geographic distribution of car manufacturersrsquo output Although the EU has retained its position as the leading global car producer output in Japan and the US has fallen South Korea is perhaps the only developed country not to have decreased car production its production rates have rather significantly increased In this South Korea resembles a number of emerging economies Car production in India has increased five-fold and China which produced only some 700 000 cars in 2001 has become the global number two producer with 1449 million units in 2011 Output in Brazil grew more

5

Policy Department Directorate-General for External Policies

The changing geographic distribution of passenger car demand has directly influenced changes in the geographic distribution of car manufacturersrsquo output

moderately and the country added just over a million units over the last decade These developments were spurred in part by increases in FDI as foreign car producers expanded their operations and joint ventures in emerging countries Volkswagen has invested in Brazil Maruti Suzuki in India and GAC Toyota in China Domestic car manufacturers in China (such as BYD) and India (Tata Motors) have also become more important The automotive industry has therefore become more dispersed with more countries producing cars than a decade ago

Source OICA data

Source OICA data

Although production may have diversified geographically the global car industry remains dominated by a limited group of suppliers and these carmakers command a significant presence on most continents in terms of both sales and production For example Toyota Volkswagen and General Motors were responsible for more than one third of global car production in 20101 Volkswagen in particular is projected to strengthen its leading position over the coming years courtesy of its growing output in Europe

1 OICA data

6

The EU automotive sector in a globalised market

China India Brazil Mexico and Russia

Overcapacity is casting a long shadow over the future of global car industry

Source The Economist

As far as the industryrsquos future is concerned the issue of overcapacity is casting a long shadow2 In just ten years car production in Japan decreased by almost a million of units US car production fell by two million units within the same time period and General Motors and Chrysler were forced to file for Chapter 11 restructuring (reorganisation bankruptcy) Many European car manufacturers are also struggling with overcapacity Although manufacturers such as Volkswagen and Toyota have been able to weather the crisis by increasing their production in emerging markets these markets are expected to reach saturation at some point in the future3 China for example which was responsible for nearly one quarter of the global car production in 2011 had an estimated six million units of unutilised capacity in the same year mdash nearly twice the size of the German car market4 Global overcapacity is forecast to reach 20shy30 by 20165 mdash a rate similar to those already reported by many of Europersquos struggling car manufacturers Given the car industryrsquos importance mdash both in terms of industrial output and employment mdash to many national economies many governments may attempt to further protect their industries in the future

2 Overcapacity occurs when the installed productive capacity in a given factory or industry exceeds output eg when domestic sales fall It can be solved by adjusting the existing installed capacity or increasing the volume of exports to foreign markets 3 It should be noted that certain markets might reach their saturation point in terms of high car ownership rates but still manage retain high levels of annual sales especially under favourable economic conditions (due to high car replacement rates) The US serves as a prime example of this 4 KPMG Overcapacity ndash Global Automotive Executive Survey 2012 Xinhua Chinarsquos auto sector faces overcapacity problem (01 September 2012) 5 KPMG Overcapacity ndash Global Automotive Executive Survey 2012

7

Policy Department Directorate-General for External Policies

In sum the global car industry has recovered from the world financial crisis and annual production rates have reached unprecedented numbers An important geographical shift in sales and output has occurred from the Triad towards countries such as China and India Global overcapacity is expected to become a major problem in the near future

3 The European car industry Car production in Europe has generally mirrored developments caused by the global economic slowdown as European output declined by 67 to 1595 million units in 2008 and by 128 to 139 million units the following year Production rates increased with the global car marketrsquos recovery in 2010 and 2011 by 99 and 27 respectively but remain over a million units short of their 2007 output Europersquos automotive industry consists of major indigenous car-making groups including Volkswagen Daimler BMW Fiat PSA and Renault which run car plants in their home countries as well as in new EU Member States (Fiat in Poland for example or PSA in Slovakia) Overseas carmakers also operate assembling plants in Europe General Motors (Opel) in Germany Nissan in the UK and Hyundai in the Czech Republic As the graph below indicates car production in the EUs newer Member States has increased significantly over the past five years but traditional car-producing countries such as Germany and France continue to be responsible for the bulk of European car production

8

The EU automotive sector in a globalised market

New passenger car registrations in the EU have not risen on a year-to-year basis since 2007

Source ACEA

While Europersquos car output has recently risen the European car industry has had to deal with decreasing domestic demand for cars New passenger car registrations have not risen on a year-to-year basis since 2007 with demand falling by as much as 79 in 2008 and 56 in 2010 Recent statistical evidence suggests that the decrease in sales is far from over compared to sales one year earlier sales in September 2012 fell in France by 18 in Italy by 26 and in Spain by 37 6 This plunge compounds a number of existing difficulties For example PSA lost EUR 819 million before tax in the first half of this year while Renault had a negative cash flow of EUR 200 million7 Financial problems prompted some carmakers to dispose of parts of their European operations Ford sold Jaguar Land Rover to Indiarsquos Tata Motors in 2008 and Volvo was sold to Chinarsquos Geely in 20108 Overcapacity which has plagued many developed countries (as described in Section 2) is another by-product of Europes falling domestic demand Fiat PSA and Renault have estimated Europersquos oversupply at 20 as of March 20129 This in turn has taken a toll on factory operations according to other estimates approx 30 of Europersquos 98 assembly plants are operating below 70 of their capacity10 The financial implications of these related problems are particularly dramatic for those carmakers with

6 The Financial Times France and Spain car sales slide further (01 October 2012) 7 The Financial Times Peugeot and Renault line up a cavalcade (25 September 2012) 8 Bloomberg Geely Seals Takeover of Volvo From Ford (02 August 2010) 9 The Financial Times Fiat chief calls for EU intervention (06 March 2012) 10 The Financial Times Car industry rattles on old Europersquos roads (04 October 2012)

9

Policy Department Directorate-General for External Policies

weak sales in the premium car segment andor growing overseas markets where demand for higher-end cars of European origin remains high11

European car manufacturers have been faced with falling domestic sales

Source ACEA

In addition to falling car sales many European car manufacturers have had to grapple with a declining market share As the graph below indicates PSA Peugeot Citroen Renault Opel and Fiat each lost approx 08 of their share in the western European market in less than two years Volkswagen on the other hand gained 13 within the same time period and South Korearsquos Kia gained 05 Hyundairsquos market share grew over the past two years by 04 extending its period of uninterrupted growth to 41 consecutive months as of July 201212 Significantly the sales of Volkswagen Group Kia and Hyundai grew in the low-cost end of the market which offers margins as high as 6 mdash two to three times higher than in the sector as a whole13 A number of car manufacturers are however losing their domestic markets For example new registrations of Peugeots and Renaults in France dropped by 20 in September 2012 while year-on-year sales of Hyundai and Kia were up by 24 14

11 This has been made apparent by the contrasting fortunes of high-end German car makers (Audi BMW Mercedes-Benz) and other European car makers (Fiat Opel PSA Peugeot Citroen Renault) 12 Reuters Analysis Carmakers dampen EU free-trade drive (06 July 2012) 13 Renault Group cited in The Financial Times Peugeot and Renault line up a cavalcade (25 September 2012) 14 The Financial Times France and Spain car sales slide further (01 October 2012)

10

The EU automotive sector in a globalised market

The European car industry is still a major employer

Source ACEA data15

The economic importance of the European car industry cannot be overlooked The car sector directly employs 63 of Europersquos manufacturing labour force mdash 2 million people mdash and another 39 mdash 12 million people mdash through its suppliers Most of Europersquos car assembly plants are concentrated in a handful of regions such as Bavaria in Germany Piedmont in Italy western Slovakia and central Bohemia The automotive industry is also the largest private investor in research and development (RampD) in Europe having invested EUR 26 billion in innovation in 2011 The loss of these jobs and investments would have significant economic and political repercussions Yet closing plants and laying off workers may be the only way for European carmakers to escape their current predicament as the productivity of car plants within the EU varies greatly For example in 2009 Fiatrsquos 22 000 workers in Italy produced 650 000 cars in five assembly plants while 6 100 of their Polish counterparts produced 600 000 cars in a single Fiat plant in Tychy16 Similarly PSA Peugeot Citroen produced 127 million motor vehicles in 2010 in France where the company employed approximately 104 465 employees (15 000 of them engaged in RampD) its Slovak plant produced more than 186 000 vehicles with only 3 000 employees17 Faced with declining sales poor financial results and overcapacity PSA Peugeot Citroen announced earlier this year that it would make 8 000 workers redundant and close the Aulnay plant near Paris by 201418

15 Up to September 2012 16 The Financial Times France and Spain car sales slide further (01 October 2012) 17 OICA for car production data Autoevolution Peugeot cuts 5700 jobs in France for PSA France employment data SARIO for PSA Slovakia employment data 18 BBC News Peugeot Citroen plans 8000 job cuts (12 July 2012)

11

Policy Department Directorate-General for External Policies

Consolidation may be the way forward for many European car makers Some industry insiders including Fiat CEO Sergio Marchionne have argued that this would help to address the overcapacity issue by shutting down underused plants and create savings by manufacturing cars on common platforms19 In February 2012 Peugeot and Opel (GM) announced plans for a strategic alliance which would enable each manufacturer to save close to EUR 1 billion per year The partners are currently discussing deepening their ties to make even more substantial savings20 Daimler is reportedly on its way to becoming the third member of Renault-Nissan alliance while Fiat and Chrysler have also embarked on a strategic partnership which has been described as a potential merger21 While consolidating European car makers should increase their competitiveness and help address current financial difficulties

19 The Financial Times Carmakers must merge says Fiat chief (11 January 2012) 20 Reuters GM and Peugeot weighting deeper tie-up sources (12 October 2012) 21 The Economist Despite the troubles in past alliances carmakers are embracing their rivals (06 October 2012) Reuters Fiat-Chrysler merger still on track despite lawsuit CEO (27 September 2012)

12

The EU automotive sector in a globalised market

manufacturing jobs are likely to be lost in the process

Source The Financial Times

The European Commission has recently issued its CARS 2020 Action Plan aimed at reinforcing this industryrsquos competitiveness and sustainability towards 202022 The Plan advocates four concrete measures

promoting investment in advanced technologies and innovation

improving market conditions

supporting industry access to the global market

promoting investment in skills and training to accompany structural change and anticipate employment and skills needs

The third pillar (concerning the global market) clearly involves targeting tariff and non-tariff barriers as it promises the conclusion of balanced trade deals and intensifying the work on international harmonisation of vehicle requirements Industry response to this initiative has been lukewarm the European Automobile Manufacturers Association (ACEA) Secretary-General Ivan Hodac called it necessary but not sufficient and argued that the EU should also explore ways to improve labour flexibility and support the affected workers and regions23

22 European Commission CARS 2020 a strong competitive and sustainable European car industry (08 November 2012) 23 ACEA Press Release European Automobile Manufacturers Call for EU Policy Automotive Industry to be Translated into Urgent Action (08 November 2012)

13

Policy Department Directorate-General for External Policies

Source Eurostat

European carmakers provide a sizeable proportion of EU exports

In addition to employment European carmakers provide a sizeable proportion of EU exports As of 2011 the value of passenger car exports to countries outside the EU reached EUR 938 billion a rise of 229 in comparison with the previous year24 The EU is the worldrsquos largest car exporter and the industryrsquos export orientation is underscored by its positive and increasing trade balance which reached EUR 696 billion in 2011 a one-year increase of 287 These figures gain further significance when placed in a comparative perspective Manufactured goods in general were responsible for around 80 of total EU exports in 2011 generating a trade surplus of EUR 264 billion25 The car industry was thus responsible for more than one quarter of the surplus in trade of manufactured goods Increasing car exports to emerging markets could help Europersquos carmakers to address the issue of falling domestic demand as well as their growing overcapacity problem in many EU plants The tariff and non-tariff barriers that European car exporters face are therefore of crucial importance both in countries that are already significant recipients of European car exports mdash such as the United States China and Russia mdash and more importantly in those countries in which existing tariff and non-tariff barriers play a role in limiting the volume of European car exports

24 Eurostat 25 Ibid

14

The EU automotive sector in a globalised market

Figure 1

Extra EU-27 trade of motor cars main trading partners shares of imports 2011

Source EurostatComext

The European car industry is currently facing significant challenges

In sum the European car industry is currently facing significant challenges falling domestic sales and overcapacity Not all European carmakers have however been equally affected Volkswagen and South Korean companies with assembly plants in Europe have in fact steadily increased their market share On the other hand PSA Peugeot Citroen Renault Opel and Fiat have experienced much greater structural and financial difficulties as well as a declining market share Industry consolidation has been suggested as a solution to their current woes increased exports another

Against this backdrop and in order to understand the likely benefits of different approaches the following sections will offer an analysis of various export markets and the various tariff and non-tariff barriers that European car producers face in these markets

Figure 2 Extra EU-27 trade of motor cars main trading partners shares of exports 2011

Source EurostatComext

15

Policy Department Directorate-General for External Policies

4 Export markets

41 Trade deficit

411 Japan

Europersquos car export markets can be divided into two broad categories according to trade balance Japan South Korea and India are three important markets with which EUrsquos trade balance in cars is negative mdash the result of the countriesrsquo export performance and the trade barriers they have put in place The EU maintains a trade surplus with other major countries yet its market share varies The EU is the leading exporter in Russia and China second to Japan in the US and far behind regional export powerhouses Brazil Argentina and Indonesia The premium car sector is responsible for the bulk of EU exports in most countries

The EUrsquos trade deficit in passenger cars with Japan is substantial but gradually decreasing having fallen by 75 between 2008 and 2011 to USD 283 billion26 Falling demand in Europe the strong Japanese yen and the shift of production of Japanese cars to Europe were responsible for the drop of Japanese exports EU car exports to Japan grew by one quarter within the same period cementing the Unions position as the leading car exporter worldwide

Imports of foreign cars have increased in Japan defying the more general and long-term Japanese trend of falling car sales While only 1 in 20 cars in use in Japan in 2011 was of foreign origin (most of these European) the total number of European cars in Japan is relatively high by comparison only 39 of all cars in use within the EU are Japanese imports27 The market share of foreign carmakers in Japan is relatively strong for standard cars (155 ) while negligible in the two thirds of the market occupied by small and kei micro cars28 High-end German carmakers command the majority of the Japanese foreign car market and the market share of Europersquos struggling carmakers mdash Renault Peugeot Citroen and Fiat mdash remains insignificant these four manufacturers together exported fewer cars into Japan in 2011 than did Audi29

European carmakers remain wary of the looming EU-Japan FTA fearing that it would be used by Japanese carmakers to offset the losses incurred by falling domestic sales30 ACEA has called for a level-playing field mdash the

26 UN Comtrade 27 Prof Yorizumi Watanabe European Parliament Workshop ndash Towards a Free Trade Agreement with Japan (11 September 2012) 28 Out of 582 million cars in use in Japan in 2011 29 were classified as lsquostandardrsquo 40 as lsquosmallrsquo and 31 as lsquokeirsquo (JAMA data) 29 Audirsquos exports in 2011 were 21166 units The total number of the four aforementioned carmakers was 18225 units Total imports into Japan in 2011 were 260707 units 30 The Financial Times EU and Japan to start trade deal talks (29 November 2012)

16

412 South Korea

The EU automotive sector in a globalised market

removal of all non-tariff barriers impeding the EUrsquos access to the Japanese car market31

The EUrsquos trade deficit in passenger cars with South Korea halved between 2008 and 2011 dropping to USD 229 billion EU exports nearly doubled while imports from South Korea especially in the more lucrative medium and large engines category declined by over USD 1 billion The most recent statistics confirm these trends32

The EU is the dominant car exporter to South Korea Sales of imported cars have been on the rise in South Korea growing from 52 of total sales in 2009 to 87 in 201133 This 72 increase represents a more rapid rte of growth than in Japan where sales of foreign cars grew by 553 in the same span34 As in Japan sales of foreign cars in South Korea defied the domestic trend of falling sales In general the growth of car sales in South Korea levelled off in 2011 and fell by 7 on a year-to-year basis in 201235

Further parallels exist between Japan and South Korea in terms of market share In 2011 the high-end German carmakers Mercedes-Benz BMW and Audi were responsible for more than one half of all sales of imported cars in South Korea Struggling European carmakers have either no market presence mdash as is the case with Fiat mdash or an insignificant market share mdash as is the case with PSA Peugeot Citroen (25 )

The EU-South Korea Free Trade Agreement which has been in force since 1 July 2011 is to eliminate the custom duty in medium and large cars by 2014 as well as the tariff on small cars by 2016 European car makers have been concerned about what they called asymmetrical trade flow relations sales of South Korean cars have in their view risen in Europe in general Believing that its market was particularly affected France asked the European Commission to monitor car imports from South Korea36 This request was rejected on the grounds of a lack of evidence that the increase in imports was concentrated in France37 Moreover the South

31 ACEA EU-Japan FTA Tentative beginnings uncertain gains (29 September 2012) 32 Korean car exports to the EU fell by 165 in September 2012 on a year-on-year basis while EU exports grew by over 20 Korea Customs Service Trade Statistics (September 2012) 33 Authorsrsquo calculations based on KAIDA data 34 Authorsrsquo calculations based on KAIDA and JAMA data 35 2012 data between up to August 2012 KAMA data 36 Hyundai sales in the EU were up by 12 Kia sales by 25 in Q1 2012 while the EU car market was down by 8 year-on-year imports to France grew by 50 in Jan-Feb 2012 sales of small South Korean cars grew by nearly 150 between January and June 2012 The Financial Times Ford Europe hits at EU-Korea trade deal (01 May 2012) Embassy of France in Washington European Commission Car imports from South Korea factsheet FranceEU-South-Korea FTA (03 August 2012) 37 The Wall Street Journal EU Rejects Call to Monitor South Korean Auto Imports (22 October 2012)

17

Policy Department Directorate-General for External Policies

Korean car manufacturer Hyundai maintained that there was no link with the free trade agreement since less than 12 of its more than 230 000 cars registered in Europe in the first half of 2012 were imported from Korea 70 of Hyundai cars registered in Europe within this period were manufactured in its plants in the Czech Republic and Turkey38

413 India

In relative terms the EUrsquos USD 198 billion trade deficit in passenger cars with India dwarfs its deficits with Japan and South Korea European car exports grew by mere USD 20 million between 2008 and 2011 while car imports from India increased within the same period by 150 to USD 215 billion European car exports to India in 2011 were eight times lower than imports India profited from a low 65 import tariff a weak Indian rupee and the increasing local availability of compact cars by non-European manufacturers mdash Hyundai Suzuki and Nissan EU exports to India remain low courtesy of high tariff barriers

Sales of passenger cars in India doubled between 2005 and 2011 and are projected to grow to 673 million units by 2020 which will transform India into the second-largest car market in Asia after China in the not so distant future39 The short-term outlook is however less positive as the generalised economic slowdown combined with increases in tariffs and financing costs resulted in a 19 year-on-year decrease in output in August 201240 Predictions for this yearrsquos growth in sales of passenger cars in India are 1-3 down from a previous estimate of 9-11 41 Given the substantial market access barriers in place most European carmakers export completely knocked-down units which are assembled locally and thereby subject to a substantially lower tariff Europersquos carmakers are paying close attention to India For example one in five vehicles launched by Renault between May 2011 and December 2012 is designed principally for the Indian market42 High-end carmakers are expected to benefit from the projected trebling in sales of luxurious vehicles in India by 202043

The car sector has proven to be a contentious element in the EU-India FTA negotiations Indiarsquos car sector has very little incentive to open up as it benefits from low EU import tariffs and might well suffer from the removal of protective tariffs at home European car manufacturers have called for

38 Reuters EU mulls French request for surveillance of South Korea car imports (06 August 2012) 39 The Wall Street Journal Corporate News India to Overtake Japan in Car Sales (15 March 2012) 40 The Financial Times Indian car market suffers sharp slowdown (03 October 2012) 41 The Financial Times Car sales rebound in India and China (09 November 2012) 42 The Financial Times India Renault makes up for lost time (12 September 2011)

43 The Financial Times Three-way race for Indiarsquos luxury market (28 August 2012)

18

The EU automotive sector in a globalised market

42 Trade surplus

421 United States

an unrestricted market access on a zero-for-zero tariff basis rejecting a number of Indian proposals that maintain import tariffs44

With the onset of the countryrsquos subprime mortgage crisis the US car market suffered a significant decline In a mere two years the US went from being the largest market in the world with 165 million units sold in 2007 to 106 million units in 2009 The country was overtaken by China one year later45 The market has been gradually recovering since with over 13 million units sold in 2011 The outlook for future growth is positive as sales reached their highest number in four years in September 2012 up by 145 for the first nine months of the year in comparison with the previous year46 Increasing fuel prices prompting consumers to replace old vehicles with newer more fuel-efficient models have been identified as one of the principal causes of this growth in car sales Sales of small cars increased by 50 on a year-on-year basis in September 2012 whereas sales of SUVs were down by 36 47 Higher availability of low-interest credit and the improving US housing market have also boosted car sales48 Some doubts remain about the markets strength given low consumer confidence levels and fears of a contagion of the deterioration of Europersquos car industry but the outlook for the current year is generally positive49

The EU balance of trade in cars with the US reached USD 181 billion down 124 from 2010 but up by a third from 2009 when EU exports hit their record low EU car imports from the US grew by 576 between 2009 and 2011 contrary to the downturn in car sales within the EU EU exports valued at USD 247 billion in 2011 still lag behind their pre-crisis levels of USD 303 billion The EU is the second-biggest car exporter to the US ranked behind Japan which exported USD 309 billion worth of cars into the US in 2011 The US demand for imported cars in the year up to September 2012 was 24 Some European carmakers have been

44 Examples include the reduction of Indiarsquos car imports duties to 30 in return for immediate duty-free access to the EU with a possibility of introducing a fixed quota of cars on which a lowered 10 tariff would apply for a period of five years The Financial Times Europersquos carmakers hit out at India trade deal (29 January 2012) The Economic Times You may have to pay just 10 duty on Porsche and BMW India in talks with EU to slash tariff (30 July 2012) 45 WardsAuto data 46 The New York Times Auto Sales Are Highest In 4 Years (02 October 2012) 47 The Wall Street Journal Whatrsquos Moving US Auto Sales (02 October 2012) 48 Generally speaking improving housing market tends to have a positive impact on consumer spending 49 Reuters US new-car sales in August seen up as much as 20 percent (04 September 2012)

19

Policy Department Directorate-General for External Policies

particularly successful with Volkswagenrsquos volume of exports to the US growing by 117 within the same time period50

422 China

The growth of Chinarsquos market for passenger cars has been unprecedented The number of units sold more than doubled in three years rising from 676 million in 2008 to 145 million in 2011 The market showed some signs of slowing down with sales increasing by only 51 between 2010 and 2011 due to the withdrawal of a 2009 government stimulus package which favoured cars with smaller engine sizes and the gradual tightening of credit policy by the central government51 Car sales have risen over recent months up by nearly 7 year on year in October with 1257 million units sold in the year up to October 2012 spurred by recent fuel price cuts and the rush to buy a car before more Chinese cities introduce expected licence plate restrictions52 These sales figures do not however reflect sales to end consumers and inventories at car dealerships are reportedly rising The single-digit growth that has recently characterised the Chinese car market is seen as signalling a period of adjustment from hyper-growth towards a more sustainable growth in line with the countrys GDP growth53 The potential of Chinarsquos car market remains enormous as its vehicle ownership rates remain relatively low 58 units per 1 000 people compared to 600 units per 1 000 in the G7 countries54

Foreign brand ownership is high Foreign brands are estimated to have accounted for 709 of car sales in 2011 up 18 from 201055 Moreover while the Chinese car market grew by approximately 115 between 2008 and 2011 imports from the triad countries grew by almost 190 within the same period56 EU car exports to China increased by 223 from USD 68 billion in 2008 to USD219 billion in 2011 exceeding exports from other major car-exporting countries by USD 69 billion Total EU exports of goods to China reached EUR 1362 billion in 2011 meaning that the car sector provided approximately 12 the yearrsquos goods exports to China European luxury-car manufacturers have been particularly successful in China For example BMW recorded a 335 increase between January and September 2012 well ahead of the market average of 7 and the companys Chinese sales have accounted for almost 50 of its EUR 18 billion improvement in revenues since 200957

50 The Wall Street Journal Whatrsquos Moving US Auto Sales (02 October 2012) 51 Reuters China 2011 car sales rise at slowest annual pace (12 January 2012) 52 The Financial Times Car sales rebound in India and China (09 November 2012) 53 The Financial Times China car sales defy broader slowdown (09 August 2012) 54 The Financial Times Carmakers itrsquos all about China (21 March 2012) 55 Reuters China 2011 car sales rise at slowest annual pace (12 January 2012) The Financial Times GM sales buck trend for China slowdown (09 January 2012) 56 CAAM and UN Comtrade data 57 The Financial Times Asia shifts BMWrsquos confidence up a gear (11 October 2012)

20

The EU automotive sector in a globalised market

423 Russia

The Russian car market collapsed in the aftermath of the financial crisis with sales falling between 2008 and 2009 by over 14 million units to 147 million units58 The market has since then steadily improved with sales figures as high as 265 million in 2011 Sales are expected to grow by 124 this year exceeding 2008 sales If this rate of growth were to continue Russia would become the largest car market in Europe by 2016 exceeding even Germany (currently the largest market in Europe)59 Total industry sales in Russia were estimated at USD 65 billion in 2011 up by 55 from the previous year60 Economic recovery (linked to high oil prices) and government stimulus measures mdash such as the extension of a car scrapping scheme until the end of 2010 mdash and the greater availability of loans have been identified as the key drivers of this growth Russiarsquos vehicle density of 250 units per 1 000 people is lower than that of many key European markets offering significant potential for growth61

Imports in 2011 were estimated at 34 of total car sales Cars and other vehicles constitute the main EU export to Russia and European export volume reached USD 89 billion in 2011 The EU was the leading car exporter to Russia in 2011 exporting USD 18 billion more than Japan although the EUs 2011 volume was only 68 of its 2008 figure nearly USD 13 billion Although Russia entered the WTO in August 2012 EU exporters are not likely to benefit in any significant way from the gradual decrease of import duties that will accompany Russias accession as the introduction of a car recycling fee by the Russian government will offset the lowering of import duties62 According to an initial analysis from the Commission the recycling fee will result in a decrease of more than EUR 1 billion per year in the value of the EUs export of vehicles to Russia

Since 2005 Russia has also introduced an aggressive localisation policy measures in the automotive sector This principally consists of an ldquoindustrial assemblyrdquo regime which imposes local content requirements that gradually increase to 60 by 2016 as well as a minimum capacity of 300000 units per year for entities establishing new production capacities and 350000 units per year for entities modernising existing capacities Other requirements include for example the establishment or modernisation of RampD centres in Russia and reaching a minimum average annual level of production localisation in the Russian Federation63 These developments will only compound the existing overcapacity problem in

58 Ernst amp Young An overview of the Russian and CIS automotive industry (February 2012) 59 Russia Today Russia in high gear to become top car market in Europe (24 September 2012) 60 Ernst amp Young An overview of the Russian and CIS automotive industry (February 2012) 61 Ibid 62 The Moscow Times After WTO Carmakers Still Protected (30 August 2012) 63 WTO Report of the Working Party on the Accession of the Russian Federation to the World Trade Organization section 1080 (17 November 2011)

21

Policy Department Directorate-General for External Policies

the EU

Renault is the only European brand that figures among the top five car brands in Russia behind Chevrolet and Hyundai but ahead of KIA and Nissan Each one of these car producers has plants in Russia German high-end manufacturers are well entrenched in the Russian market and the Volkswagen Group recently recorded a 50 sales increase in Russia well ahead of its other markets64 Nevertheless all EU vehicle producers except Fiat (currently negotiating a new investment) have invested in production capacity in Russia most of them under the assembly regime requiring high levels of local content

424 Brazil

The EU managed to reverse its trade deficit in cars with Brazil going from a deficit of USD 290 million in 2008 to a USD 162 billion surplus in 2011 EU exports nearly doubled while imports from Brazil declined by 90 due to the strong Brazilian currency the real and falling demand in Europe

European car exporters were able to capitalise on Brazils surging demand for imported cars which grew between 2008 and 2011 by 153 reaching nearly 580 000 units Car sales in Brazil increased between 2008 and 2010 by 206 to 264 million units65 Although growth stalled in 2011 the outlook for the Brazilian car market remains positive borrowing costs have decreased and the government recently cut excise taxes resulting in an 189 increase in car registrations in July 2012 compared to one year previous66 The rate of growth of imported cars has however declined from 26 in 2011 to mere 52 in August 201267 This decline is a direct consequence of an increased number of protectionist measures aimed at curbing the rising number of imports considered threatening to Brazilrsquos domestic manufacturers and industrialisation efforts For example in March 2012 Brazil imposed a quota on car imports from Mexico which had risen by 70 in 201168 Previously in December 2011 a tax on cars with less than 65 local content had been increased by 30 to 55 allegedly to safeguard against imports from China which had risen fiveshyfold in 201169 The scheme was modified in October 2012 becoming the Inovar-auto program but it retains its discriminatory character towards imports and builds upon tax exemption incentives for the localisation of production RampD and engineering This may have a particularly negative effect on EU car components exports to Brazil

Fiat and Volkswagen sell two in five cars in Brazil but sales are forecast to

64 The Financial Times VW hit by Europe slowdown (24 October 2012) 65 ANFAVEA data 66 The Financial Times Tax breaks boost Brazilian car production (06 August 2012) 67 ANFAVEA data 68 Reuters Mexico bows to Brazilian pressure on auto exports (15 March 2012) 69 The Economist Brazilrsquos trade policy Seeking protectionism (14 January 2012)

22

The EU automotive sector in a globalised market

425 Argentina

426 Indonesia

drop by 83 and 84 respectively for each manufacturer in 2013 when Brazilrsquos local car production capacity will receive a major boost from new factories for Hyundai Chery and JAC Motor70 Other European carmakers including BMW and Mercedes-Benz are reportedly interested in investing in Brazil in order to circumvent trade barriers and profit from the growing car market71

Argentinarsquos passenger car market contracted in the immediate aftermath of the world financial crisis dropping to around 453 000 units in 2009 but went on to make a strong recovery with 673 900 units sold in 201172 The increase in supply was met by growing domestic production which reached record levels of around 840 000 cars in 2011 and increased imports from Brazil which increased by 60 to USD 362 billion between 2008 and 201173 EU car exporters largely did not profit from this recovery to the same extent as their Brazilian counterparts did EU exports grew by only 23 within the three-year period although they declined by USD 45 million between 2010 and 2011 In 2011 EU exports to Brazil were valued at USD 480 million

The Argentinean car industry is showing signs of slowing down Car production decreased by 21 on a year-to-year basis up to September 2012 This was mainly due to the depreciation of Brazilrsquos currency which rendered Argentinean cars in Brazil mdash Argentinarsquos principal car export market mdash more expensive74 Moreover Argentinas has faced an own economic slowdown with GDP growth halving to 34 in 2012 and placing capital at risk of flight75 Car sales as a result have fallen by 96 in the year up to October 2012 The Argentinean government has tried to partially shield its industry from imports and has renegotiated its automotive accord with Mexico which has led car imports to decrease by 166 76

Indonesia the fourth most populous country in the world has car ownership rates as low as 4 and thus promises an enormous potential for future growth77 Indonesiarsquos economy fuelled by rising domestic

70 Bloomberg Fiat Faces Challenge as Hyundai Threatens Profit (22 October 2012) 71 The Financial Times BMW eyes plans for Brazil factory (19 October 2012) The Wall Street Journal Mercedes-Benz May Decide on New Brazil Factory by Year End (22 October 2012) 72 ADEFA data 73 ADEFA data UNCTAD 74 The Financial Times Argentine autos bumpy road ahead (07 November 2011) 75 Bloomberg Argentine Budget Sees 34 GDP Growth in 2012 44 in 2013 (20 September 2012) 76 The Financial Times Auto fight Argentina wants a piece of Mexico too (21 March 2012) ADEFA data 77 The Economist Indonesiarsquos car market Stuck in the fifth gear (01 September 2012)

23

Policy Department Directorate-General for External Policies

consumption grew by 65 in 2011 with GDP per capita reaching USD 3 500 mdash a threshold considered the take-off point for car sales78 Sales of all motor vehicles grew by 17 in 2011 contrasting with falling sales in other ASEAN countries79 Sales of motor vehicles in Indonesia are projected to reach 106 million units this year and double to 2 million units by 201880 Indonesia is expected to become the biggest car market in Southeast Asia

EU car exports to Indonesia grew by 44 between 2008 and 2011 reaching USD 1335 million in 2011 This figure was only about one quarter of Japanese car exports to Indonesia and only slightly higher than that of South Korean exports which increased eight-fold within the same time period Thailand used as a regional car-manufacturing hub by Japanese carmakers remains the most significant car exporter into Indonesia with exports higher than those of all other countries combined

Japanese carmakers control over 90 of the Indonesian car market They will likely maintain their leading position given their plans to USD 2 billion by the end of this year to expand their manufacturing capacity in Indonesia81 General Motors is investing USD 150 million to reactivate a defunct Indonesian plant in a bid to recapture a share of the growing Indonesian market82 European carmakers on the other hand have been much less active Peugeot was reportedly interested in investing USD 150 million in Indonesia in 2011 but its plans have been delayed by the companyrsquos on-going financial difficulties and there has been no official confirmation of this investment83

5 Tariff and non-tariff barriers As the above survey of various markets demonstrates European car exporters maintain a leading position in a high number of geographically diverse markets with luxury cars constituting the key segment in the majority of these markets Market openness however remains an issue EU car exports to developing markets such as India and Indonesia and to certain developed markets such as Japan and South Korea remain low andor restricted to more expensive cars only Tariff and non-tariff barriers in many countries have had a major impact on the overall volume of EU car exports as well as on segmentation which makes EU exports of standard and lower-end cars less competitive

78 The Financial Times Boom time for Indonesiarsquos car industry (10 October 2012) 79 ASEAN Automotive Federation 80 Reuters Indonesia Sept car sales jump back to near record levels (15 October 2012) The Financial Times Boom time for Indonesiarsquos car industry (10 October 2012) 81 The Financial Times Boom time for Indonesiarsquos car industry (10 October 2012) 82 The Jakarta Globe GM Peugeot to Revive Plants for Production (12 August 2011) 83 BSD Indonesia Trade amp Investment News 0612 (June 2012)

24

The EU automotive sector in a globalised market

51 Tariff barriers

Import duties faced by European car exports in developed car markets are relatively low ranging from 0 in Japan to 56 in South Korea and 10 in the US The EU import tariff itself is 10 or 65 with the lower rate applying to developing countries On the other hand a number of growing automotive markets including those listed below apply import tariffs that vary from 25 in Russia and China to 75 in India and even 83 in Vietnam India is a very specific case as its automotive industry has clearly profited from the low EU duty applied to Indian exports the country exports a high number of cars to the EU as well as to other countries

Figure 3 China 25 India 75 Argentina 35 Malaysia 30

Automotive peak tariffs in selected markets November Russia 2584 Indonesia 50 Brazil 35 Vietnam 83 2012

The European Commission has repeatedly promised to address these tariff imbalances in trade negotiations with its partners by concluding balanced trade deals as reiterated in the CARS 2020 Action Plan85 European car manufacturers have for their part frequently called for securing a level playing field in any future trade agreements such as the FTA with India currently being negotiated86

52 Non-tariff barriers

Non-tariff barriers take many different forms and can often pose an even more formidable obstacle to car exports than tariff barriers

Non-tariff barriers (NTBs) can in many cases pose even more formidable obstacle to car exports than tariff barriers This is certainly the case with Japan and South Korea where EU car exporters face low mdash and sometimes no mdash import duties while their export volume remains relatively low As far as developing markets are concerned NTBs tend to significantly increase the price of imported cars which are already expensive and attract high import duties

NTBs take many differing forms which makes them hard to fully eliminate Technical regulations are among the most common NTBs Their effect can be particularly strong due to the growing gap between EU regulations and foreign regulations which often results in significant costs for EU car manufacturers The EU-South Korea FTA which entered into force in July 2011 includes ambitious provisions that would make a number of EU technical requirements apply to the Korean market In spite of this ACEA which represents European manufacturers reports and lists a number of

84 More than 30 if the recycling fee is taken into account 85 European Commission CARS 2020 a strong competitive and sustainable European car industry (08 November 2012) 86 The Financial Times Europersquos carmakers hit out at India trade deal (29 January 2012)

25

Policy Department Directorate-General for External Policies

regulatory issues in South Korea as pending Examples include test procedures conditions and criteria for certification post-market surveillance and vehicle width87 Other countries mdash most notably Indonesia mdash are also introducing their own national standards According to the provisions of the Indonesian National Standard (SNI) SNI certifications will be required for car components (such as braking systems) and for completely built cars (such as tyre and windscreen certifications) This trend towards greater local regulations is worrying for European carmakers which control only a small fraction of the market as SNI certification and testing proved to be lengthy and costly88

Homologation procedures closely related to technical regulations can be equally thorny For example motor vehicles imported into China are subject to more than one type-approvalhomologation requirement by different uncoordinated regulators89 Moreover under the provisions of the 2002 China Compulsory Certification system each automotive product and component that has been type-approved in Europe must be re-tested in Chinese laboratories imposing a further burden on importers90

Tax structures in certain countries may also discourage customers from purchasing imported cars Examples of such structures include the luxury car tax in Indonesia and the Brazilian industrial tax (IPI) The IPI which was initially re-introduced in December 2011 and extended to 2013-2017 in April 2012 is as high as 30 The tax applies to motor vehicles unless their manufacturers comply with at least three out of four prescribed rules for example adhering to content requirements (ie meeting an onshore-manufacturing threshold) or making RampD investments in Brazil91

Other NTBs vary widely For example the recycling fee on imported cars to be introduced in Russia will more than offset the planned lowering of tariffs An importer declaration system in Argentina requires that imports be reported in advance In China draft public procurement rules for official party and government cars only feature vehicles from Chinese carmakers Finally in Japan owners of Japanese kei cars mdash domestically manufactured micro-cars with a market share of over 30 mdash enjoy

87 ACEA EU-South Korea FTA Resolution of Remaining Issues (20102011) European Commission Report of the meeting of the Market Access Working Group on Cars and Car parts and Market Access Working Group on Tyres (09 February 2012) 88 European Business Chamber of Commerce in Indonesia Automotive Position Paper 2012 (27 July 2012) 89 Automotive Working Group European Chamber of Commerce in China European Business in China Position Paper 20122013 (12 September 2012) 90 Ibid 91 European Commission The Ninth Report on Potentially Trade Restrictive Measures (06 June 2012) 92 Ibid ACEA EU-Japan FTA Tentative beginnings uncertain gains (29 September 2012) 93 Hosuk Lee-Makiyama FTAs and the crisis in the European car industry (2012) 94 European Commission CARS 21 High Level Group ndash Final Report (06 June 2012)

26

The EU automotive sector in a globalised market

financial benefits92 It has even been remarked that low market penetration by foreign carmakers can be an NTB in itself creating a vicious circle The total cost of owning a foreign car in Japan for example has been calculated at 30 more than that of comparable domestic models purely due to the low availability of spare parts diagnostic equipment and technical expertise In such conditions customers opt for domestically manufactured models especially in the lower-end segments of the market where cost is a primary consideration93

The strategy of the European Commission for removing NTBs is centred on facilitating worldwide acceptance of technical requirements and conformity assessment procedures defined by the UNECE 1958 Agreement94 FTAs are seen as useful tools for ensuring legislative equivalence but they might not always accomplish the goal of removing NTBs This was for example the case of the EU-South Korea FTA Bilateral discussions such as the EU-China Dialogue may be of some help Yet any successful elimination of NTBs can easily be reversed with the introduction of new NTBs The range of possible NTBs is so broad that they pose an ongoing threat to future market access in any car export destination

6 Conclusion The global automotive industry has been affected by two significant developments in the past decade The first was short-term as global sales and production numbers temporarily dropped following the onset of the world financial crisis The industry has however since recovered and its current production levels exceed those of the pre-crisis era The second development on the other hand is ongoing Both sales and production have been shifting from the countries of the triad (the EU US and Japan) to developing markets Demand for passenger cars in countries such as China and India has soared Although these markets have experienced short-term fluctuations in demand their long-term outlook is quite positive

The EU the worldrsquos leading car exporter has been able to capitalise on this shift Nearly every fifth car exported from the EU is destined for China Passenger cars are responsible for a sizeable portion of EU exports of manufactured goods to the worldrsquos second largest economy

At the same time many European carmakers are experiencing major financial and structural difficulties caused by stagnating domestic markets A number of carmakers have suffered losses at home within the very market segment that was traditionally one of their strongpoints Among sales of small cars in France for example the market share of French brands has fallen unlike that of their South Korean counterparts The impact on struggling carmakers has been severe as confirmed by their financial results and plans to lay off workers and close plants

Overcapacity has often been cited as the principal cause of the current predicament Addressing this issue however is no simple matter and the

27

Policy Department Directorate-General for External Policies

Increasing the levels of car exports appears to be the only plausible solution to Europersquos overcapacity problem

Tariff and non-tariff barriers present a significant impediment to possible increases in the volume and segmentation of EU exports

range of potential solutions is limited The car industry is a major employer within the EU and further lay offs resulting for example from alliances between different EU carmakers would create serious problems for many national governments already battling growing unemployment rates Given this context increasing the levels of car exports appears to be the only plausible solution to addressing the issue of overcapacity in the short-run

Our analysis of numerous important export markets has demonstrated that there is scope for such an increase The EU despite being the worldrsquos leading car exporter has only managed to incrementally reduce its trade deficit with other major car exporters namely Japan South Korea and mdash particularly mdashIndia Foreign car ownership rates in Japan and South Korea remain low India is adamantly shielding its domestic market from exports while becoming an ever-more productive car exporter in its own right Those countries with which the EU maintains a trade surplus are either still growing (as is the case for China Brazil and Indonesia) or gradually recovering (the US) Russiarsquos recovery has also been significant as the country is poised to become the biggest car market in Europe perhaps as early as this year

Tariff and non-tariff barriers however present a significant impediment to possible increases in the volume and segmentation of EU exports to these markets Lower import duties mdash which the EU has vowed to secure by concluding FTAs mdash merely offer a partial solution as countries tend to protect their domestic automotive industries andor force carmakers to open plants at home Non-trade barriers are both difficult to remove and easy to introduce and they tend to offset any gains in the removal of trade barriers More than a year has passed since the EU-South Korea FTA entered into force for example and European carmakers still voice their concerns about South Korean NTBs The EUs car exports to Russia have not benefited from Russias WTO membership (and the resulting 10 reduction in car import duties) because a new car recycling fee applied to imported vehicles will ensure that these cars remain as expensive as before Examples of NTBs vary but they all share an ease of implementation Ensuring proper market openness to car exports will therefore remain a major challenge for the EU for many years to come

28

Policy Department Directorate-General for External Policies

This Policy Briefing is an initiative of the Policy Department DG EXPO

AUTHOR Lukas GAJDOS (Roberto BENDINI sup) Directorate-General for External Policies of the Union Policy Department WIB 06 M 55 rue Wiertz 60 B-1047 Brussels

Feedback to robertobendinieuroparleuropaeu is welcome

Editorial Assistant Jakub PRZETACZNIK

LINGUISTIC VERSIONS Original EN

ABOUT THE PUBLISHER Manuscript completed on 4 December 2012 copy European Union 2012 Printed in Belgium

This Policy Briefing is available on the intranet site of the Directorate-General for External Policies in the Regions and countries or Policy Areas section

To obtain paper copies please send a request by e-mail to poldep-expoeuroparleuropaeu

DISCLAIMER Any opinions expressed in this document are the sole responsibility of the authors and do not necessarily represent the official position of the European Parliament

Reproduction and translation except for commercial purposes are authorised provided the source is acknowledged and provided the publisher is given prior notice and supplied with a copy of the publication

2

The EU automotive sector in a globalised market

Table of contents

1 Introduction 4

2 The global car industry 4

3 The European car industry 8

4 Export markets 16 41 Trade deficit 16

411 Japan 16 412 South Korea 17 413 India 18

42 Trade surplus 19 421 United States 19 422 China 20 423 Russia 21 424 Brazil 22 425 Argentina 23 426 Indonesia 23

5 Tariff and non-tariff barriers 24 51 Tariff barriers 25 52 Non-tariff barriers 25

6 Conclusion 27

3

Policy Department Directorate-General for External Policies

1 Introduction The European car sector is experiencing a particularly difficult period Sales and production numbers have decreased significantly since the onset of the continentrsquos economic difficulties imposing a considerable burden on EU carmakers This burden is two-fold and its effects are closely interlinked as the collapse in car sales is responsible not only for the carmakersrsquo financial difficulties but also for the growing overcapacity problem in certain EU15 countries

Falling sales in Europe contrast with rising sales in developing markets suggesting that further increasing the volume of car exports could be a solution to the European sectorrsquos current woes Numerous tariff and non-tariff barriers however prevent EU car exporters from increasing their sales in growing and more mature markets and restrict their exports to high-end cars

This paper will provide an overview of the global and European car industries with a specific focus on recent trends and problems It will then analyse a number of key European car export market markets and conclude with an overview of trade barriers that hamper market access to these markets

2 The global car industry The automotive industry enjoyed a period of steady growth before the onset of the global financial crisis Production rates increased from 4122 million units in 2000 to 532 million units in 2007 interrupted only by a mild downturn in 2001 The industry was badly affected by the global economic recession and the subsequent decrease in global demand as production slowed down in the final months of 2008 and fell sharply in 2009 by nearly 5 million units It should be noted that this decrease was more pronounced that the contraction of the world economy highlighting the automotive sectorrsquos vulnerability to adverse economic conditions An important turning point for car manufacturers occurred in 2010 when the fall in production numbers halted Production rates exceeded their pre-crisis levels by a considerable margin with 5834 million cars produced worldwide The industry grew by 3 in 2011 with 5995 million units produced The International Organisation of Motor Vehicle Manufacturers (OICA) the principal industry body expects this rate of growth to be maintained in the current year

4

The EU automotive sector in a globalised market

Source OICA data

The recent growth in global demand for passenger cars has been geographically uneven Sales have yet to recover in the region traditionally seen as responsible for demand mdash the Triad (Japan the USA and the EUWestern Europe) particularly in the US and the EU Increasing affluence and demand in developing countries in general and in China in particular sustains the sectorrsquos recent recovery and projected future growth New car registrations in China doubled in two years reaching 1255 million units in 2010 Sales in India grew by two thirds and by one quarter in Brazil during the same period

Sources ACEA Bureau of Transport National Bureau of Statistics of China JAMA Fenabrave SIAM

The changing geographic distribution of passenger car demand has directly influenced changes in the geographic distribution of car manufacturersrsquo output Although the EU has retained its position as the leading global car producer output in Japan and the US has fallen South Korea is perhaps the only developed country not to have decreased car production its production rates have rather significantly increased In this South Korea resembles a number of emerging economies Car production in India has increased five-fold and China which produced only some 700 000 cars in 2001 has become the global number two producer with 1449 million units in 2011 Output in Brazil grew more

5

Policy Department Directorate-General for External Policies

The changing geographic distribution of passenger car demand has directly influenced changes in the geographic distribution of car manufacturersrsquo output

moderately and the country added just over a million units over the last decade These developments were spurred in part by increases in FDI as foreign car producers expanded their operations and joint ventures in emerging countries Volkswagen has invested in Brazil Maruti Suzuki in India and GAC Toyota in China Domestic car manufacturers in China (such as BYD) and India (Tata Motors) have also become more important The automotive industry has therefore become more dispersed with more countries producing cars than a decade ago

Source OICA data

Source OICA data

Although production may have diversified geographically the global car industry remains dominated by a limited group of suppliers and these carmakers command a significant presence on most continents in terms of both sales and production For example Toyota Volkswagen and General Motors were responsible for more than one third of global car production in 20101 Volkswagen in particular is projected to strengthen its leading position over the coming years courtesy of its growing output in Europe

1 OICA data

6

The EU automotive sector in a globalised market

China India Brazil Mexico and Russia

Overcapacity is casting a long shadow over the future of global car industry

Source The Economist

As far as the industryrsquos future is concerned the issue of overcapacity is casting a long shadow2 In just ten years car production in Japan decreased by almost a million of units US car production fell by two million units within the same time period and General Motors and Chrysler were forced to file for Chapter 11 restructuring (reorganisation bankruptcy) Many European car manufacturers are also struggling with overcapacity Although manufacturers such as Volkswagen and Toyota have been able to weather the crisis by increasing their production in emerging markets these markets are expected to reach saturation at some point in the future3 China for example which was responsible for nearly one quarter of the global car production in 2011 had an estimated six million units of unutilised capacity in the same year mdash nearly twice the size of the German car market4 Global overcapacity is forecast to reach 20shy30 by 20165 mdash a rate similar to those already reported by many of Europersquos struggling car manufacturers Given the car industryrsquos importance mdash both in terms of industrial output and employment mdash to many national economies many governments may attempt to further protect their industries in the future

2 Overcapacity occurs when the installed productive capacity in a given factory or industry exceeds output eg when domestic sales fall It can be solved by adjusting the existing installed capacity or increasing the volume of exports to foreign markets 3 It should be noted that certain markets might reach their saturation point in terms of high car ownership rates but still manage retain high levels of annual sales especially under favourable economic conditions (due to high car replacement rates) The US serves as a prime example of this 4 KPMG Overcapacity ndash Global Automotive Executive Survey 2012 Xinhua Chinarsquos auto sector faces overcapacity problem (01 September 2012) 5 KPMG Overcapacity ndash Global Automotive Executive Survey 2012

7

Policy Department Directorate-General for External Policies

In sum the global car industry has recovered from the world financial crisis and annual production rates have reached unprecedented numbers An important geographical shift in sales and output has occurred from the Triad towards countries such as China and India Global overcapacity is expected to become a major problem in the near future

3 The European car industry Car production in Europe has generally mirrored developments caused by the global economic slowdown as European output declined by 67 to 1595 million units in 2008 and by 128 to 139 million units the following year Production rates increased with the global car marketrsquos recovery in 2010 and 2011 by 99 and 27 respectively but remain over a million units short of their 2007 output Europersquos automotive industry consists of major indigenous car-making groups including Volkswagen Daimler BMW Fiat PSA and Renault which run car plants in their home countries as well as in new EU Member States (Fiat in Poland for example or PSA in Slovakia) Overseas carmakers also operate assembling plants in Europe General Motors (Opel) in Germany Nissan in the UK and Hyundai in the Czech Republic As the graph below indicates car production in the EUs newer Member States has increased significantly over the past five years but traditional car-producing countries such as Germany and France continue to be responsible for the bulk of European car production

8

The EU automotive sector in a globalised market

New passenger car registrations in the EU have not risen on a year-to-year basis since 2007

Source ACEA

While Europersquos car output has recently risen the European car industry has had to deal with decreasing domestic demand for cars New passenger car registrations have not risen on a year-to-year basis since 2007 with demand falling by as much as 79 in 2008 and 56 in 2010 Recent statistical evidence suggests that the decrease in sales is far from over compared to sales one year earlier sales in September 2012 fell in France by 18 in Italy by 26 and in Spain by 37 6 This plunge compounds a number of existing difficulties For example PSA lost EUR 819 million before tax in the first half of this year while Renault had a negative cash flow of EUR 200 million7 Financial problems prompted some carmakers to dispose of parts of their European operations Ford sold Jaguar Land Rover to Indiarsquos Tata Motors in 2008 and Volvo was sold to Chinarsquos Geely in 20108 Overcapacity which has plagued many developed countries (as described in Section 2) is another by-product of Europes falling domestic demand Fiat PSA and Renault have estimated Europersquos oversupply at 20 as of March 20129 This in turn has taken a toll on factory operations according to other estimates approx 30 of Europersquos 98 assembly plants are operating below 70 of their capacity10 The financial implications of these related problems are particularly dramatic for those carmakers with

6 The Financial Times France and Spain car sales slide further (01 October 2012) 7 The Financial Times Peugeot and Renault line up a cavalcade (25 September 2012) 8 Bloomberg Geely Seals Takeover of Volvo From Ford (02 August 2010) 9 The Financial Times Fiat chief calls for EU intervention (06 March 2012) 10 The Financial Times Car industry rattles on old Europersquos roads (04 October 2012)

9

Policy Department Directorate-General for External Policies

weak sales in the premium car segment andor growing overseas markets where demand for higher-end cars of European origin remains high11

European car manufacturers have been faced with falling domestic sales

Source ACEA

In addition to falling car sales many European car manufacturers have had to grapple with a declining market share As the graph below indicates PSA Peugeot Citroen Renault Opel and Fiat each lost approx 08 of their share in the western European market in less than two years Volkswagen on the other hand gained 13 within the same time period and South Korearsquos Kia gained 05 Hyundairsquos market share grew over the past two years by 04 extending its period of uninterrupted growth to 41 consecutive months as of July 201212 Significantly the sales of Volkswagen Group Kia and Hyundai grew in the low-cost end of the market which offers margins as high as 6 mdash two to three times higher than in the sector as a whole13 A number of car manufacturers are however losing their domestic markets For example new registrations of Peugeots and Renaults in France dropped by 20 in September 2012 while year-on-year sales of Hyundai and Kia were up by 24 14

11 This has been made apparent by the contrasting fortunes of high-end German car makers (Audi BMW Mercedes-Benz) and other European car makers (Fiat Opel PSA Peugeot Citroen Renault) 12 Reuters Analysis Carmakers dampen EU free-trade drive (06 July 2012) 13 Renault Group cited in The Financial Times Peugeot and Renault line up a cavalcade (25 September 2012) 14 The Financial Times France and Spain car sales slide further (01 October 2012)

10

The EU automotive sector in a globalised market

The European car industry is still a major employer

Source ACEA data15

The economic importance of the European car industry cannot be overlooked The car sector directly employs 63 of Europersquos manufacturing labour force mdash 2 million people mdash and another 39 mdash 12 million people mdash through its suppliers Most of Europersquos car assembly plants are concentrated in a handful of regions such as Bavaria in Germany Piedmont in Italy western Slovakia and central Bohemia The automotive industry is also the largest private investor in research and development (RampD) in Europe having invested EUR 26 billion in innovation in 2011 The loss of these jobs and investments would have significant economic and political repercussions Yet closing plants and laying off workers may be the only way for European carmakers to escape their current predicament as the productivity of car plants within the EU varies greatly For example in 2009 Fiatrsquos 22 000 workers in Italy produced 650 000 cars in five assembly plants while 6 100 of their Polish counterparts produced 600 000 cars in a single Fiat plant in Tychy16 Similarly PSA Peugeot Citroen produced 127 million motor vehicles in 2010 in France where the company employed approximately 104 465 employees (15 000 of them engaged in RampD) its Slovak plant produced more than 186 000 vehicles with only 3 000 employees17 Faced with declining sales poor financial results and overcapacity PSA Peugeot Citroen announced earlier this year that it would make 8 000 workers redundant and close the Aulnay plant near Paris by 201418

15 Up to September 2012 16 The Financial Times France and Spain car sales slide further (01 October 2012) 17 OICA for car production data Autoevolution Peugeot cuts 5700 jobs in France for PSA France employment data SARIO for PSA Slovakia employment data 18 BBC News Peugeot Citroen plans 8000 job cuts (12 July 2012)

11

Policy Department Directorate-General for External Policies

Consolidation may be the way forward for many European car makers Some industry insiders including Fiat CEO Sergio Marchionne have argued that this would help to address the overcapacity issue by shutting down underused plants and create savings by manufacturing cars on common platforms19 In February 2012 Peugeot and Opel (GM) announced plans for a strategic alliance which would enable each manufacturer to save close to EUR 1 billion per year The partners are currently discussing deepening their ties to make even more substantial savings20 Daimler is reportedly on its way to becoming the third member of Renault-Nissan alliance while Fiat and Chrysler have also embarked on a strategic partnership which has been described as a potential merger21 While consolidating European car makers should increase their competitiveness and help address current financial difficulties

19 The Financial Times Carmakers must merge says Fiat chief (11 January 2012) 20 Reuters GM and Peugeot weighting deeper tie-up sources (12 October 2012) 21 The Economist Despite the troubles in past alliances carmakers are embracing their rivals (06 October 2012) Reuters Fiat-Chrysler merger still on track despite lawsuit CEO (27 September 2012)

12

The EU automotive sector in a globalised market

manufacturing jobs are likely to be lost in the process

Source The Financial Times

The European Commission has recently issued its CARS 2020 Action Plan aimed at reinforcing this industryrsquos competitiveness and sustainability towards 202022 The Plan advocates four concrete measures

promoting investment in advanced technologies and innovation

improving market conditions

supporting industry access to the global market

promoting investment in skills and training to accompany structural change and anticipate employment and skills needs