Embed Size (px)

Citation preview

This is an electronic reprint of the original article.This reprint may differ from the original in pagination and typographic detail.

Powered by TCPDF (www.tcpdf.org)

This material is protected by copyright and other intellectual property rights, and duplication or sale of all or part of any of the repository collections is not permitted, except that material may be duplicated by you for your research use or educational purposes in electronic or print form. You must obtain permission for any other use. Electronic or print copies may not be offered, whether for sale or otherwise to anyone who is not an authorised user.

Lähteenmäki, JarnoThe evolution paths of neutral host businesses: antecedents, strategies, and business models

Published in:Telecommunications Policy

DOI:10.1016/j.telpol.2021.102201

Published: 01/11/2021

Document VersionPublisher's PDF, also known as Version of record

Published under the following license:CC BY

Please cite the original version:Lähteenmäki, J. (2021). The evolution paths of neutral host businesses: antecedents, strategies, and businessmodels. Telecommunications Policy, 45(10), [102201]. https://doi.org/10.1016/j.telpol.2021.102201

Telecommunications Policy 45 (2021) 102201

Available online 25 June 20210308-5961/© 2021 The Author. Published by Elsevier Ltd. This is an open access article under the CC BY license(http://creativecommons.org/licenses/by/4.0/).

The evolution paths of neutral host businesses: Antecedents, strategies, and business models

Jarno Lahteenmaki Aalto University, Konemiehentie 2, PL11000, 00076, AALTO, Finland

A R T I C L E I N F O

Keywords: Neutral host Strategy Antecedents Regulation Business model Ownership Path dependence

A B S T R A C T

A neutral host company provides wholesale infrastructure sharing services through digital plat-forms to the downstream-markets enabling customers to take advantage of economies of scale and to access knowledge assets. Through a qualitative study of more than 50 businesses, the analysis of neutral host business antecedents, emergent company strategies, and ecosystem business models reveal that the markets of data and communications are highly fragmented, different, and diversified, but the categorization of business traits suggests the attribution of typical underlying business and investment decisions. The policy implication is that to enable asset sharing, the markets should not be constrained through a local-monopoly prohibiting regulation, but addi-tional innovation fostering practices shall be implemented to provide further social benefits and business consolidation opportunities before dominant designs emerge. On the global level, increased collaboration among policy makers is needed to ensure the parallel evolution of local digital platform regulatory frameworks.

1. Introduction

Throughout the history of industries, the strategic decisions of market participants have played a crucial role in shaping how in-dustry assets are utilized. In telecommunications markets, for more than 100 years, providers have made decisions to share their infrastructure with others to enable end-to-end network coverage instead of building their own global networks (Dunnewijk & Hulten, 2007). And in the data markets, analysis firms have decided to buy and sell datasets with each other to expand data coverage (Koutroumpis et al., 2020). These strategic decisions have in turn created local wholesale markets that have opened a wide range of business opportunities. When these markets have matured, however, they have required regulatory frameworks to prevent, e.g., anti-competitive behaviour, violation of personal privacy, and discriminatory pricing. Moreover, the initiatives of authorities have steered market evolution, e.g., in means of telecommunications privatization to enhance competition (Ros & Banerjee, 2000) or the act of general data protection regulation to enhance the market power of individuals (Kramer & Wohlfarth, 2018).

Demand for digital services in modern societies has increased dramatically in recent years, which in turn has increased the need to expand infrastructure sharing practices on the telecommunications and data markets. Infrastructure sharing capabilities have evolved through technological evolution, but this development has also created a need for a dedicated business entity called a neutral host provider. The extant literature acknowledges three major domains where a neutral host business, and the corresponding infrastructure sharing, can take place; wide area infrastructure requiring sharing due to scale (e.g., Kibilda & DaSilva, 2013); urban area infra-structure requiring data collection for better decision making (e.g., Anttiroiko et al., 2014); and local micro environments with special

E-mail address: [email protected].

Contents lists available at ScienceDirect

Telecommunications Policy

journal homepage: www.elsevier.com/locate/telpol

https://doi.org/10.1016/j.telpol.2021.102201 Received 4 December 2020; Received in revised form 16 June 2021; Accepted 16 June 2021

Telecommunications Policy 45 (2021) 102201

2

circumstances (e.g., Kibria et al., 2017). Although the literature agrees that the role of a neutral host is to aggregate downstream needs and to build corresponding technology platforms for sharing (Paglierani et al., 2020; Yrjola, 2020), these studies also tend to focus on modern urban areas utilizing 5G technologies as a contextual factor. The literature dismisses, however, the other structural and environmental factors of these neutral host companies.

Although infrastructure sharing has a long history, the term neutral host is a relatively new concept in the area of data and com-munications businesses as it emerged in the mid 2000s. The original need was stemming from passive infrastructure sharing opera-tions, where distributed antenna systems (DAS) required an operator independent company to run the infrastructure (Muir et al., 2006). First the concept diffused to the science literature (Ramachandran, 2008) and then later to the business literature (e.g.; Rayal, 2013) resulting in a fragmented use of the term. There have been some recent studies related to the concept unification, but it seems that the paradigm has not settled yet due to the fact that there are still several alternative definitions for the neutral host concept (e.g.,; Benseny, Walia, Finley, & Hammainen, 2019; Paglierani et al., 2020; Paolino, 2019). Hence, the existing literature is inconclusive of what ‘neutral host’ actually means.

Policy makers may find it hard to set effective rules and incentives on novel neutral host markets if it is unknown what these markets and its stakeholders actually are. As some scholars have pointed out, the regulation of neutral host ecosystems is a multi- dimensional endeavour resulting in a complex interplay of policies (Korpisaari et al., 2020, p.90-91), for example on the areas of personal data protection and privacy, network and spectrum regulation, competition law, and public procurement legislation. This raises two major topics to be addressed. First, as the term is used differently by several stakeholders, including scholars, policy makers, and industry players, that allows mixed interpretations of market structures and market powers, and it may even lead to misaligned policies, the study finds it important to clarify the terminology in the neutral host literature. Second, as some business evolution scholars have pointed out (David, 1994; Reynolds, 1981), it is crucially important to understand the history of a business due to the fact that the path-dependent nature of business decisions steer individual company strategies, but it also shapes the whole market evo-lution. The historical insights, in terms of company evolution, may provide paramount views to the organization level factors of neutral host markets. Addressing these topics together allow this study to elaborate further the antecedents and future directions of neutral host markets and implications for policy makers.

This study formulates a dense form of the neutral host definition and defines that a neutral host is a service provider that builds and operates an integrated technology platform that is solely for sharing purposes. This generic definition allows the broader use of a neutral host model in various context as it strives to minimize the role of technological factor, and this perspective allows this study to research existing markets and interpret the future directives on the higher levels of ecosystems rather than focusing on platform assets which are subject to technological evolution and rapid obsolescence.

In this line, the context of this study is the strategic factors of neutral host market companies. In this context, technology platforms are seen as enablers for businesses and regulatory landscape of telecommunications, spectrum allocation, and data privacy policies as a framer. The technological context and scope of this study span across all major standards in use, including mobile and fixed tech-nologies such as 3 GPP 4G/5G and IEEE 802.11 in the fields of communications, and including different kinds of data platforms such as IoT sensor networks and big data platforms. The reason why this research is needed is because of the need for better structural un-derstanding of markets. As the neutral host models diffuse into various markets, various stakeholders should identify the decision- making criteria and the background factors that affect them. Moreover, it has become clear that neutral host markets are subject to consolidation as the activity on mergers and acquisitions has gained momentum. How the most important assets of modern digital societies become distributed and who holds the controlling power of it are not superfluous questions, but these require increasing attention to ensure the socially optimal development of the policy landscape. This study sets the research question as: On what paths neutral host companies have emerged and what strategies those companies have taken?

Through an empirical study of more than 50 existing organizations utilizing the neutral host model, this paper categorises and analyses strategies and business models seen in the market. Moreover, the study categorises typical ownership structures and in-vestment strategies to gain an understanding of company antecedents on the markets. This paper concludes that data and commu-nications business models are significantly different, implying that these are two separate markets, and there are very few neutral host companies that operate on both of these markets. Moreover, it turns out that the original line of a business and company ownership structures impact first to company level strategies and then to corresponding ecosystem level business models.

This paper contributes to the literature on neutral host market structures, neutral host strategies, and neutral host models. First, this paper contributes to the neutral host market structure literature by igniting the research on the categorization and elaboration of distinctive emergence paths. While existing research explains extant roles and relationships through abstract and static value network configuration models (Benseny, Walia, Finley, & Hammainen, 2019), this paper deepens this understanding empirically by showing how organizations actually have evolved. Moreover, the contribution of this study includes a clarification of the neutral host concept terminology. Second, this study advances the research on neutral host strategies. While existing research has been limited to explaining the choices made by a neutral host company through characteristic business logic (Ahokangas et al., 2019), this paper broadens this research stream by categorizing strategic choices and ownership structures. Third, this research contributes to the understanding of firm level behaviour differences in the market through linking the investment strategies of shareholders to company strategies, and by doing so this study strives to explain neutral host business antecedents better. While existing research identifies only a few alternative typical ownership categories for neutral host companies (Kibria et al., 2017), this research identifies ten categories for owners with their characteristic investment strategies.

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

3

2. The concept of neutral host

Several business scholars have studied the asset sharing practices on data and communications markets, and they have observed the need for a strategic business entity to enhance the efficient use of infrastructure assets. However, as the focus has been in details, the bigger picture has remained ambiguous.

2.1. Review of the neutral host literature

This section reviews the most important part of the literature related to the business models and sharing economies and strategies of a neutral host company. These streams build the bigger picture of a neutral host landscape. First in the stream of neutral host business models, review reveals that although being highly fragmented and inconclusive of several aspects, the extant body of literature builds on the idea that through infrastructure sharing, local communication ecosystems can improve efficiencies and, thus, reduce costs. Second in the stream of neutral host strategies, it is well known that when neutral host models are applied, it also has strategic consequences for others, but only a few of those other areas have been actually studied. Third, the sharing economics literature of digital platforms acknowledges that sharing is not just dividing costs between multiple stakeholders, but it is also dividing knowledge, created value, and risks among platform stakeholders.

The term neutral host is a relatively new concept in the area of data and communications businesses. The term emerged in the mid 2000s from passive infrastructure sharing operations, where distributed antenna systems (DAS) required an operator independent company to run the infrastructure (Muir et al., 2006). First the concept diffused to the science literature (Ramachandran, 2008) and then later to the business literature (e.g.; Rayal, 2013) resulting in a fragmented use of the term. There have been some studies related to the concept recently, but it seems that the paradigm has not settled yet due to the fact that there are still several alternative def-initions for the neutral host concept (e.g.; Benseny, Walia, Finley, & Hammainen, 2019; Paglierani et al., 2020; Paolino, 2019). However, there are some patterns within the literature that is reviewed next.

First, the business model literature is highly segregated through spatial factors, meaning that urban area, rural area, and special venue differences have been the main contextual factor in several studies. Most of the studies focus on urban areas, where the pop-ulation density is the highest. Paglierani et al. (2020) propose a neutral host model where a small cell operator with cloud capabilities provides full featured connectivity services in urban areas. Their extensive analysis of neutral host enabled connectivity services suggests that neutral host business models are most applicable in specific venues, such as stadiums. Neokosmidis et al. (2018) proposes a model where a local municipality acts as a neutral host by sharing the local infrastructure for MNOs in a local wholesale market. Their model supports active network sharing, but it is limited to the eNodeB level as it assumes that the ownership of spectrum assets is held by MNOs. Benseny, Walia, Hammainen, and Salmelin (2019) also propose a municipality driven approach to the neutral host ownership. Their work builds on the scenario where a local neutral host company operates a local small cell-based network. However, their techno-economic analysis shows almost ten years break-even time when comparing a traditional MNO model and the neutral host model, which suggests an unfeasible scenario. Later, Neokosmidis et al. (2020) presented a techno-economic analysis of their business model for a 5G small based network operator. In their results, the payback time of the scenario is also rather slow for investments, which may indicate the lack of scale in these scenarios.

There are also studies which focus on rural areas. Kumar et al. (2020), for example, analyse a scenario where the neutral host model is seen as an industry configuration rather than a role of some individual business entity. In their model, a separate infrastructure provider holds ownership of wide-area network assets and shares it among industry stakeholders to motivate ecosystem members to provide services to areas which were unattractive other vice. Although these rural area studies are rare, these show high potential as monetary incentives have not always been able to motivate incumbents to build services (Kontio, 2020).

Special regions and venues have also been studied through the neutral host perspective. Walia et al. (2017), for example, study campus network options and conclude that small-cell based micro-operator approach can both decrease a number of required base stations in an area, and in turn it can increase network efficiency. However, they also acknowledge that these micro-operator-based approaches are subject to regulation uncertainty as it is still unresolved if these private network operators are subject to public network regulation or not. Moreover, Kibria et al. (2017), proposes the use of a neutral host model in the context of tailored services for different venues. Their model is based on a micro-operator approach and it utilizes a shared spectrum model. In addition, Ahokangas et al. (2019) propose two distinctive dominant business models for a neutral host operating in a micro-operator role; the vertical business model provides tailored services for specific cases; the horizontal business model provides local hosted connectivity for extant MNOs in a feasible and cost-efficient way. This body of literature shows the third important context where the neutral host business model has been applied.

The second stream of literature, neutral host strategies, is very short. Those few papers that handle strategy topics in the context of a neutral host model tend to examine strategic impact for stakeholders in the environment of a neutral host company, but not the strategy of the neutral host company itself. Benseny, Walia, Hammainen, and Salmelin (2019) provide two characteristic strategies for cities to deploy a small-cell network using a neutral host model. The study assumes that MNOs rely on cost-efficiency strategies, which implies that the neutral host strategies have to support that path. Neokosmidis et al. (2019) argues that incumbent MNOs have to change their strategy to utilize neutral host infrastructure where present. It remains a question why incumbents have to do it. If this would be the case in the presence of a high regulatory regime, a neutral host company could then just build a natural monopoly infrastructure and let customers come. But this is hardly the case in modern competitive markets. There seems to be a major lacking in the literature in terms of neutral host strategies.

Third, the sharing economy literature covers a significant number of studies related to digital platforms in general, but it mostly

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

4

lacks the neutral host perspective in detail. The study of Munoz and Cohen (2017) includes both telecommunications and data cases, and their analysis reveals that instead of having just one type of a sharing business or economic impact, it turns out that there are at least five distinctive configurations of how a sharing economy may be realized. Configurational factors, such as collaboration governance, mission, resource efficiency, access to funding, ecosystem peer-collaboration, and leverage on technology, influence how the business logic functions within that configuration. Hence, these turn out to be strategic factors which are influenced by both historical aspects of a company and environment (e.g., ownership). The authors also discuss the policy implications of these factors, and conclude that typically sharing economy businesses lead to inclusion and more socially optimal situations. Yrjola (2019) proposes utilization related economy factors in terms of infrastructure sharing. Moreover, he proposes sharing of knowledge and sharing of created value in ecosystems. While the former factor explains decreasing transaction costs through larger scale and increasing effi-ciency, the latter factors stem from knowledge exploration initiatives within alliance partnerships (Stettner & Lavie, 2014), and seek for complementarity (Gulati & Gargiulo, 1999, p. 1460). However, in some cases also competition, organizational structures and market configuration create or prevent synergies related to the sharing economy to happen. Moreover, Lehr and Sicker (2019) discuss the implications of forcing infrastructure sharing by policies, and propose a framework to address sharing issues in public utility services. The authors notice that technological flexibility and adaptability have diversified business opportunities which in turn have increased the range of substitutions for consumers.

The neutral host term has also been referenced by several other studies beyond these three areas. These other studies are not specifically addressing the aspects of infrastructure sharing, but they illustrate the contexts where the term has been applied. Scholars on techno-economics have studied, for example, value network configurations (Walia et al., 2017) giving alternative industry structure guidelines for local micro-operators, and small-cell provisioning practices (Paglierani et al., 2020) providing guidelines for local neutral host operators introducing innovative 5G services. Moreover, scholars on neutral host technologies have studied emerging aspects, such as block-chains (Di Pascale et al., 2020), architectures (Colman-Meixner et al., 2019; Foukas et al., 2019), radio-access network slicing features (Ferrús et al., 2019), cloud computing at the mobile edge (Giannoulakis et al., 2016), and network function virtualization implementations (Baldoni et al., 2018; Paolino et al., 2019). Furthermore, scholars on legal and regulatory consider-ations have studied, for example, micro licensing policies focusing on 5G technologies (Matinmikko et al., 2018), spectrum ownership options (Neokosmidis et al., 2019), spectrum management practices (Massaro & Beltran, 2020), and licensed shared access practices (Yrjola & Kokkinen, 2017). All these studies focus on the communications services and also to the 5G related aspects of the neutral host concept.

Some scholars have found it useful to study different use-cases to reveal the impact of contextual factors, such as, deployments in ports (Ahokangas et al., 2020), expanding neutral host networks to rural areas (Cowie et al., 2020), or the use of in vehicle applications (C–V2X) (Basaure & Benseny, 2020). In addition to the interest of academia towards the topic, also industry forums have been active. Organizations, such as Small Cell Forum (SCF, 2021), Alliance for Telecommunications Industry Solutions (ATIS, 2019), GSM Asso-ciation (GSMA, 2018), and International Telecommunications Union (ITU-T, 2018), have published their views regarding neutral host implementations, regulation, and business models. Through these studies the understanding of the concept has gradually improved but novelty and fragmentation of the topic indicates that there are several opportunities for further studies.

Although the extant literature mostly considers the neutral host model technologically neutral, meaning that the model itself does not constraint which technology is utilized, however, it turns out that the most of the research on the field actually posits neutral hosts

Table 1 Definitions of a neutral host have evolved over the years.

Source Definition

Muir et al. (2006) One entity operates a network on behalf of multiple cellular carriers. Ramachandran (2008) A neutral host is a system that allows multiple wireless carriers to share the same infrastructure. Rayal (2013) The small cell network can be operated by a neutral host service provider which leases capacity to multiple mobile

network operators SCF (2021) A neutral host is a firm that provides services for a number of operators wishing to deploy infrastructure in a particular

location. Giannoulakis et al. (2016) A neutral host shares IT and network resources at the edge of the mobile network Walia et al. (2017) A neutral host is responsible for deployment, operation and managing of indoor small cell networks in an MNO neutral

manner. ITU-T (2018) A neutral host is an independent wireless operator on a wholesale basis to mobile operators. GSMA (2018) In a neutral host model two or more operators rent a single network infrastructure that is deployed and operated by a

non-operator 3rd party (may be affiliated with operator(s)). ATIS (2019b, p. 10) A neutral host obtains and manages resources, and provides facilities and/or interconnection allowing hosted clients to

make use of the platform(s) to provide continuous services to their end user customers. Paolino et al. (2019) A neutral host slices its compute and networking resources according to the needs of verticals providing services for end

users. Benseny, Walia, Finley, and

Hammainen (2019) The NHO offers a network resource that MNOs can use to extend 3.5 GHz-based (and potentially 26 GHz-based) outdoor capacity and coverage.

Colman-Meixner et al. (2019) A neutral host can offer its infrastructure to the third parties, and these can create new instances of virtualized services in the neutral operator’s equipment.

Paglierani et al. (2020) The neutral host is the owner of the radio and IT infrastructure deployed in a venue. Di Pascale et al. (2020) A neutral host deploys and maintains a small cell network, and provides a common infrastructure that can be used by

multiple MNOs, and by other stakeholders enabled by smart-contracts.

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

5

to the 3 GPP mobile service context. Li et al. (2020), for example, study DAS implementations in a neutral host context and they acknowledge 5G opportunities. Although their results could be generalized to any wireless standard, however, this study assumes that the neutral host concept as such is technologically agnostic although all use-cases are anchored into some specific technology context.

To synthesize the literature findings, it can be said that the technological side of neutral host models is dominating the literature. At the same time, business strategy and business model related studies are relatively rare. In these few studies, some propose antecedents of the platform-based ecosystemic business models (Yrjola, 2020), which can be considered a historical perspective of a neutral host, while some provide techno-economic models for analysing business feasibility (Paglierani et al., 2020), which can be considered an emergent strategy perspective. However, none of these studies explores these strategies in depth, nor have focused on comparing neutral host models of data and connectivity. This is a clear gap that needs to be addressed in order to reveal how neutral host companies form and how they evolve in their environment. Moreover, the fragmented landscape of neutral host terminology cries for unification. These are important topics to be addressed because, for scholars, without a proper ontological base, academia is struggling to find a common language for this emerging concept, and, for policy makers, without an understanding of structures and evolution paths of neutral host businesses authorities may find it impossible to set effective incentives or appropriately binding regulatory constraints for local markets. As the extent of installed infrastructure and collected data continues to increase, the challenge to find socially optimal policies is becoming harder.

2.2. The model of neutral host

The literature review results in fragmented definitions of the neutral host concept. The extant literature is also inconclusive in the fact if a neutral host concept is a technology specific concept or if it is technology agnostic. The neutral host literature, however, agrees that a neutral host builds its infrastructure for sharing purposes and it operates on the wholesale part of a value chain. Table 1 gives examples of how different scholars and organizations have defined the neutral host term. These illustrative samples show that there is certain development of the term over the years, but also increasing diversity.

This paper takes a dense form of definition and defines a neutral host is a service provider that builds and operates an integrated technology platform that is solely for sharing purposes. The theoretical context is defined through this definition for this study.

The definition, this study proposes, contains four key characteristics. First, the service provider part proposes that a neutral host offers continuous services for its customers in the area of its operations. Second, the builds and operates part defines neutral host value adding activities, implying that the service provider constructs required infrastructure together with its key partners and it maintains and develops the infrastructure to meet varying needs of downstream customers. Third, the integrated technology platform part scopes and constraints the area of operations. Last, the solely for sharing purposes part steers the way how the built infrastructure is leveraged on the business-vice. To elaborate this further, it could be said that the scope defines that a neutral host strives to consolidate required technological components so that those can be delivered to wholesale customers as a one uniform environment. It is also good to notice that the definition does not limit what kind of technological components or applications are actually used, but the definition allows the use of all data and communications related components as long as those support sharing. Hence, it can be assumed that striving to seek economies of scale, innovation through collaboration, and efficiency in markets push business decisions to seek maximized fair uti-lization. However, this definition does not limit a company utilizing a neutral host model to pursue other businesses that do not fit into the definition. Consultancy services, and retailing or whole-selling of equipment, for example, are businesses that a company may pursue, but are not considered a part of the neutral host business.

3. Theoretical foundation

This study utilizes several theoretical frameworks, such as the concepts of strategy, business models, path dependency, ecosystems, and digital platforms. This section summarizes the most important of those.

This research focuses on analysing a realized company behaviour on a market. This selection implies that this study examines realized company strategies and then interprets the characteristic general model, which fits the real-world data. Generally, a business model and business strategy are variedly understood concepts (e.g. Ansoff, 1957; Mintzberg & Waters, 1985; Osterwalder, 2013; Porter, 1997). Several scholars have strived to clarify the concepts (e.g. Casadesus-Masanell & Ricart, 2010; Seddon & Lewis, 2003), and typical propositions have been that while strategy defines a business logic of one individual company within its environment in several ways (answering to the questions such as, ‘what’, ‘how’, ‘when’, ‘why’, and ‘where’), a business model defines the business logic of some group in more simple way (answering just to the questions such as, ‘what’ and ‘how’). In recent studies, Lanzolla and Markides (2021) discuss the roles of a business model and business strategy, and they propose that a business model can be seen as an analysis view of strategy extending resource-based view and market positioning perspectives. This approach is also in line with Seddon and Lewis (2003) work, which posits the concept of strategy to the level of ‘real-world’ and the concept of business model to the level of ‘model-world’. Adapting this perspective to social constructivism’s ontological stances, this study interprets a business model as an abstract description of typical business-related characteristics, which very seldom realize as such in the real world, but rather are simplifying characteristics of such business. At the same time, this study interprets strategy as ‘a pattern in a stream of decisions’ (Mintzberg & Waters, 1985), implying that these patterns, either deliberate or emergent, can be directly seen in the real-world company behaviour.

The previously described perspective of a strategy implies that there is an infinite number of different distinctive strategies that a company can utilize. However, it turns out that there are three main paths that most of these strategies lay on, the strategies of dif-ferentiation, cost leadership, and market focus (Porter, 1980). By utilizing the path of differentiation, a company selects novel product

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

6

areas and novel customer segments where to pursue the business (Ansoff, 1957). However, the utilization of differentiation strategies also causes decreasing operational efficiency due to lower average utilization of assets (Schommer et al., 2019). The profit seeking nature of companies pushes them to improve financial results (Coase, 1991), which motivates them to utilize the second path of a cost leadership strategy – i.e. operational efficiency. A company utilizing an operational efficiency strategy seeks economies of scale and scope (Stigler, 1958; Teece, 1980) and strives to maximize the utilization of assets (Majumdar, 1998). The third optional strategic path is the focusing on certain niche market segments in terms of customer needs and demands by providing superior quality and features (Whiteley, 1991). However, this strategy implies that the company needs to constraint its business to certain customers and it may find it challenging to grow or change amid industry changes (Arasa & Gathinji, 2014).

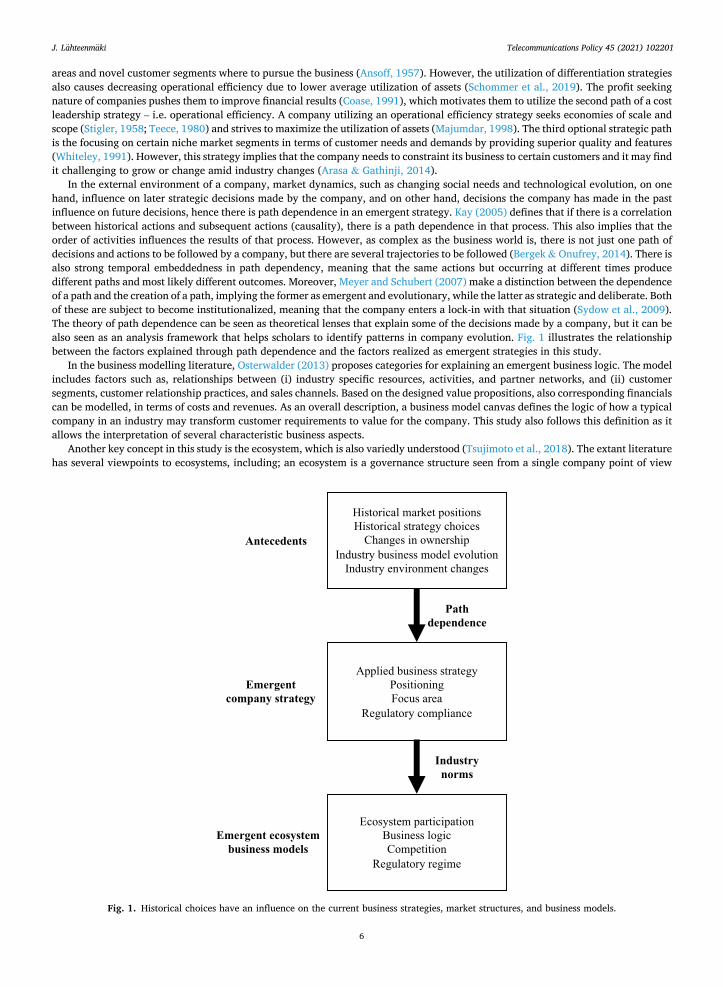

In the external environment of a company, market dynamics, such as changing social needs and technological evolution, on one hand, influence on later strategic decisions made by the company, and on other hand, decisions the company has made in the past influence on future decisions, hence there is path dependence in an emergent strategy. Kay (2005) defines that if there is a correlation between historical actions and subsequent actions (causality), there is a path dependence in that process. This also implies that the order of activities influences the results of that process. However, as complex as the business world is, there is not just one path of decisions and actions to be followed by a company, but there are several trajectories to be followed (Bergek & Onufrey, 2014). There is also strong temporal embeddedness in path dependency, meaning that the same actions but occurring at different times produce different paths and most likely different outcomes. Moreover, Meyer and Schubert (2007) make a distinction between the dependence of a path and the creation of a path, implying the former as emergent and evolutionary, while the latter as strategic and deliberate. Both of these are subject to become institutionalized, meaning that the company enters a lock-in with that situation (Sydow et al., 2009). The theory of path dependence can be seen as theoretical lenses that explain some of the decisions made by a company, but it can be also seen as an analysis framework that helps scholars to identify patterns in company evolution. Fig. 1 illustrates the relationship between the factors explained through path dependence and the factors realized as emergent strategies in this study.

In the business modelling literature, Osterwalder (2013) proposes categories for explaining an emergent business logic. The model includes factors such as, relationships between (i) industry specific resources, activities, and partner networks, and (ii) customer segments, customer relationship practices, and sales channels. Based on the designed value propositions, also corresponding financials can be modelled, in terms of costs and revenues. As an overall description, a business model canvas defines the logic of how a typical company in an industry may transform customer requirements to value for the company. This study also follows this definition as it allows the interpretation of several characteristic business aspects.

Another key concept in this study is the ecosystem, which is also variedly understood (Tsujimoto et al., 2018). The extant literature has several viewpoints to ecosystems, including; an ecosystem is a governance structure seen from a single company point of view

Fig. 1. Historical choices have an influence on the current business strategies, market structures, and business models.

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

7

(Adner, 2017); an ecosystem can be a cannon for network-centric innovation, rendering it a network of knowledge sharing (Nambisan & Sawhney, 2011); and in an urban context, an ecosystem can embed a public authority driven governance and sustainability seeking business networks through private sector participation and collaboration (Diaz-Diaz et al., 2017). The common aspects in these are the central coordination by a focal organization, and there are mutual interests among stakeholders. This study utilizes the term ecosystem as a perspective to interpret the external environment of a company. This implies that not all ecosystems are deliberate or even acknowledged by ecosystem stakeholders, but those may be highly emergent and latent for them. This study also applies the popu-lation ecology view (Hannan & Freeman, 1977) to interpret ecosystems, as it allows the analysis to consider emerging sub-groups as sub-populations of a wider ecosystem, but it also explains factors such as competition and product selection in these sub-populations. These perspectives allow this study to combine, for interpretation, the strategy as a company level decision making structure and the ecosystem as an external value-creating business network.

When discussing neutral host concepts, one cannot avoid discussing the use of digital platforms. One could say that setting up a digital platform has several similarities to setting up a traditional manufacturing factory, both economically and operationally. These modern information factories have become the norm in several industries, including telecommunications and data. A digital platform allows decreasing transaction costs through increasing scale, and it also allows increasing network effects through more integrated value creation (Kiesling, 2018). A platform typically combines latest digital technological enablers with a suitable and sustainable business logic, that open the sharing of costs and revenues between the focal platform company and its customers (de Reuver et al., 2018; Smedlund, 2012). The digital platform term is a generic concept. It refers to any set of digital technology assets, built and operated by a platform company. In that concept, the focal company leverages high asset specificity in the form of physical assets or knowledge. It may also, under high asset specificity circumstances, gain a natural monopoly position that in turn allows it to price the services and to control access to the platform for its own benefit.

Hence, while a digital platform is a tangible asset that a company holds, it also becomes a subject to obsoletion. To be able to keep up with technological evolution, a company not only needs to be able to renew the platform, but it also needs to be able to renew its market position, ecosystem configurations, and business models to ensure alignment with stakeholders (Agarwal & Helfat, 2009). This strategic renewal capability allows the company to change amid industry evolution.

Epistemologically, it becomes a cross-level interpretation of how strategy, an industry business model, and ecosystems intercon-nect. At a macro-level, a business model represents how a market is served by market participants. At a meso-level, an ecosystem represents how a network of market participants co-create value. And at a micro-level, strategy represents the path of company level decisions to fulfil the meso and macro-level goals. In this chain of thought, a platform can be seen as a core resource (see resource-based view by Wernerfelt, 1984) that the selected strategy leverages.

The puzzle is, due to the high growth of digital services in demand and the fast pace of technological evolution in recent years, it has become evident that the trend of diffusing digital technologies will remain. At the same time, the underlying market structures change as markets try to seek increasing efficiency. The role of a neutral host company in this change has been ambiguous, and it has become urgent to address two major questions. First, this study strives to answer the question of what a neutral host actually is? Second, through the analysis of empirical data, it also seeks to answer the question of on what paths neutral host companies have emerged and what strategies those companies have taken?

4. Methods

The general research question that this study seeks to answer is: “on what paths neutral host companies have emerged and what strategies those companies have taken?” Since the study puts neutral-host companies to the focal point in trying to identify differentiating characteristics, decision patterns, and their surroundings, qualitative research was preferred above quantitative techniques (Lee & Lee, 1999, pp. 21-22). The reason to do so is that it is not well known what are the lower-level market structures in the neutral host markets and what company level characteristics drive these markets. Specifically, this study utilizes qualitative comparative analysis together with active categorization to reveal underlying aspects. This study assumes that market structures, including business models, are socially constructed, which is in line with the views of Porac et al. (1995). Based on this social constructivism ontological stances, this study also acknowledges that the interpretations made by a scholar actually influence how reality emerges. As discussed in the pre-vious section, this study interprets business strategy and business model as two different concepts. Moreover, it explores environmental factors through the ecosystem view described earlier.

4.1. Sample

This study examines the historical developments and current state of neutral host markets to gain understanding on how markets have formed. To gain an understanding of the neutral host market evolution and company level characteristics, this study reviews a sample of companies on the neutral host markets. In this research, the selection criteria are induced from the theoretical context; hence the study relies on theoretical sampling rather than statistical sampling (Glaser & Strauss, 1967). The context implies that a qualifying

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

8

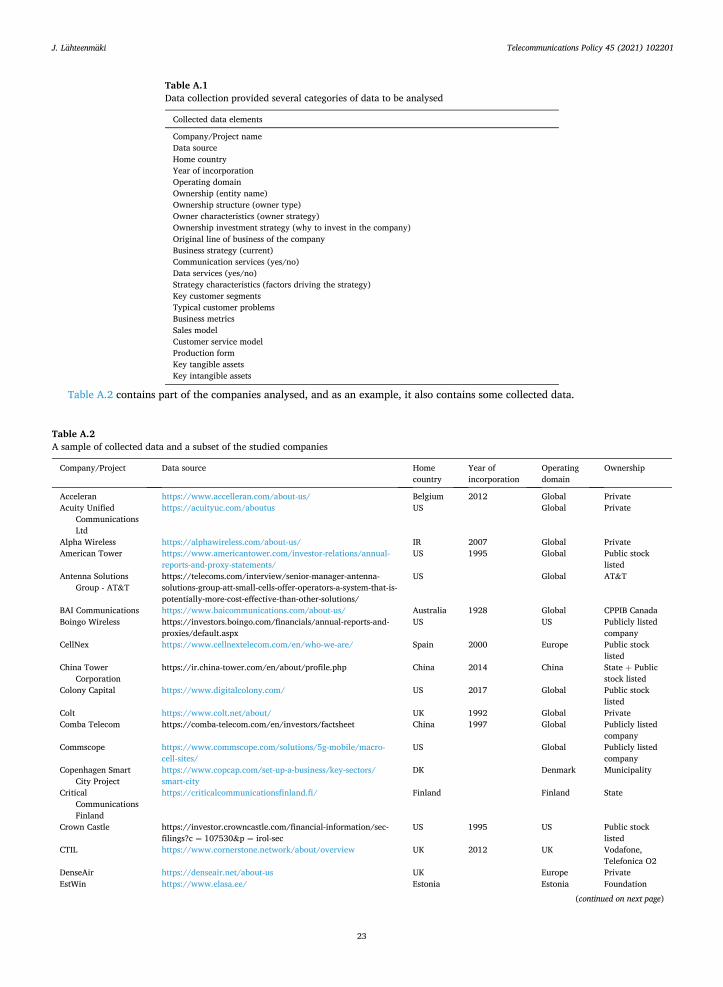

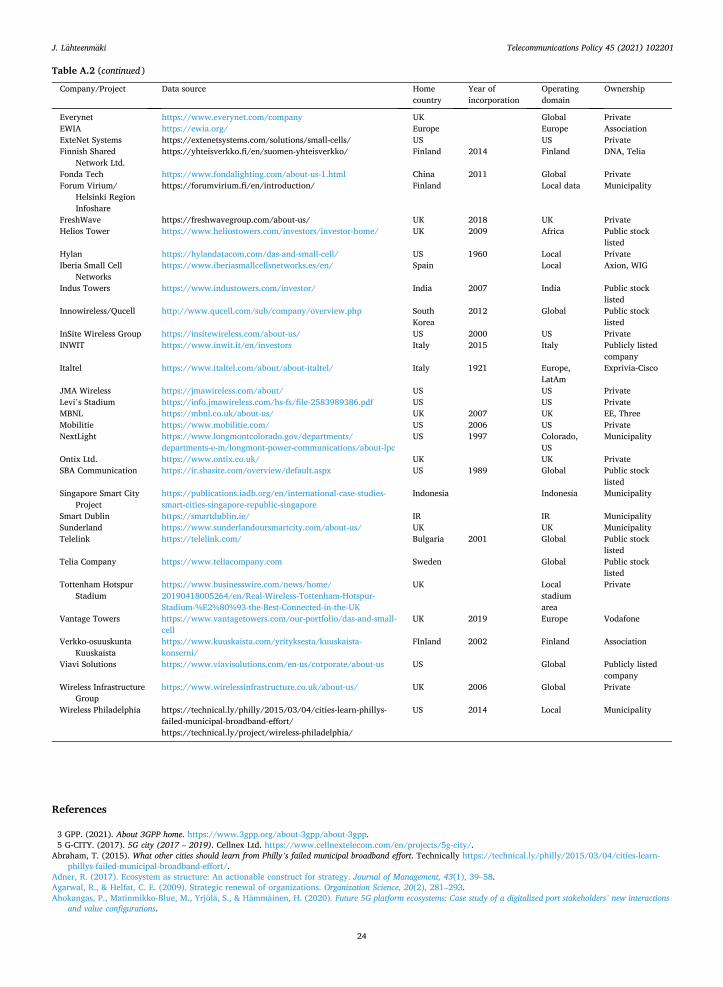

company needs to provide data or communication services for other service companies without striving to compete on end-user markets. In this setting, a neutral host company does not deliver services for end-users, but only for other wholesale type organiza-tions that process services further. For sampling purposes, the author extracted the full list of communication and data service companies from the Orbis database,1 then any company that provided services for end-users were filtered out. The list was supple-mented by collecting public authority driven initiatives that were not present in the commercial database.2 As the author wanted to reveal differences between companies, hence to select polar cases, which allows the study to explore the phenomenon of interest, the author selected business entities to the sample one by one from the long-list until he felt that the saturation point has been reached and adding a new firm to the sample would not add significantly new information. Eventually the study reached the list of more than 50 companies and public organizations, and based on the author’s interpretation, it represented well the neutral host domain.

4.2. Research data

As the study uses inductive means to interpret generalizable propositions, thus has no predefined hypothesis to be tested, the author strived to collect as diverse a set of data as possible to ensure trustworthiness of the results without going to the actual firms. The author wanted to understand organizational behaviour on the market level and the structures of these entities. Hence, this study collected a diverse set of public data related to the sample companies, such as public relations materials, annual reports, financial reports, marketing materials, press-releases, and public interview records. Company web-pages provided basic information related to business offerings, customer segments, and value propositions. News articles and press-releases provided information related to historical events a company has gone through. Marketing materials revealed the reasons why and how a customer may use the service being offered. Not all material was available for all companies, for example, only publicly listed companies disclosed annual reports, thus this study did not have similar detailed information available for non-publicly listed companies and the author was not able to make any interpretation on those cases. On the other hand, some organizations did not provide a detailed list of provided services, hence such information was interpreted through customer testimonials or white papers, for example. The data collection was done between November 2019 and October 2020. Orton (1997) proposes interleaving data collection and analysis phases to enable iteration between data and interpretation, which turned out to be a good practice also in this study as it allowed the author to find missing information as those occurred. The author downloaded all online material to the local repository for coding. The data collection phase yielded more than 400 documents.

4.3. Analyses

The author started the analysis by familiarizing himself with the context seen through the data, to the historical backgrounds of companies, and the overall development of markets. The first observation was that the communications market is actually much older than initially assumed, as, for example, one of the companies utilizing a neutral host model was established as early as 1989 (SBA, 1998), which is two decades before the 4G-LTE network era that was considered as a starting point of the market. This fact triggered the author to go even further to the history and to seek older events related to the neutral host type operations, but it turned out that the study did not find any older telecommunications related neutral host operations than 1989, which was then decided to be the starting point of the market.

This study used several qualitative analysis methods to interpret the data. For example, this study used qualitative data analysis and categorization methods to identify emergent themes and dimensions among the data (Grodal et al., 2020). Moreover, as the data in this study is mostly a written text, which holds an implicit narrative value, the author also used discourse analysis methods to gain un-derstanding on the actors, their activities, and the relationships between these in the given context (Powers, 2001). These methods allowed the author to extract the needed insights from the data.

The qualitative data analysis method is based on an iterative textual coding procedure (Bazeley, 2013, pp. 125-132). First, the author coded the data using short labels, such as ‘provides small-cell services’ or ‘owned by an investment fund’. The selected criteria were the strategic choices made by the company and different characteristics of the company. The author collected these codes to a table. In the second phase the author searched common dependencies between codes to form second order elements. The author identified that, for example, a company providing services with an end-to-end focus strived to specialise into one specific context (vertical focus), and thus selected a diversification strategy, while a company with a narrow product focus strived to specialise in a limited set of technologies and processes (horizontal focus), thus selected the economics of scale strategy. The author reviewed these categories, the original data, and supporting literature to improve coherence among dimensions. The author selected three key di-mensions for further development, (i) business models, which reflect the overall ecosystem level business logics, (ii) the original lines of businesses, which reflect path dependent nature of a company strategies, and (iii) ownership structures, which reflect the

1 Orbis is a commercial business information database, which contains a wide range of qualitative and quantitative information provided by local authorities and listed companies itself. The accuracy and quality of data in the database cannot be evaluated as the data collection procedures are not disclosed, but we think that the database is a trustworthy source for sampling purposes. https://www.bvdinfo.com/en-gb/our-products/data/ international/orbis.

2 The author collected public authority driven initiatives through extensive search from public websites. The author used search keywords, such as, “smart city; city development program; city data program”, to identify potential candidates, and the author reviewed each of those before including them into the sample.

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

9

governance of company strategies. On the business models, the author defined two characteristics models using the Osterwalder (2013) framework, one for data and one for communications offerings. On the original line of business dimension, the author defined four categories that emerged from the data. The ownership structure development phase yielded ten categories that emerged from the data. After defining these dimensions, the author compared the emergent categories with the original data and validated if the analysis was able to abduct all relevant aspects of the companies. When data allowed, the author also looked at the temporal dimensions of different events to reveal the causal order of actions. For example, change in company ownership was found to influence the business decisions the company makes. The final review did not result in any major changes, thus the author concluded that the analysis has progressed to the end. Now let us move to elaborate the findings further.

5. Results

This study asks, on what paths neutral host companies have emerged and what strategies those companies have taken? To address that question, this study analysed the data, which resulted in three overarching dimensions. First two dimensions, historical market po-sitions and ownership structures, together with direct observations of company strategies, build the view of emergent company strategies and their corresponding evolution paths. The third dimension, the ecosystem level business models illustrate the business logic within the ecosystem, which can be considered as an institutional constraint for a company within that ecosystem. Fig. 1 il-lustrates the structure of the results. First, this section shows the antecedent factors, such as historical market positions and ownership structures, which act as historical and path dependent factors for emergent strategies. Second, this section elaborates on the emergent neutral host company strategies, which leads to formation of industry norms and rules, and emergent ecosystem level business models. In this ecosystem context, this section elaborates on the implications to the regulatory regime. Together these can enlighten the emergence paths of neutral host companies, and market structures.

5.1. Antecedents of neutral host businesses

The results of the business structure analysis suggest that there is a path dependence in neutral host strategies. The assessed neutral host companies are divided into four separate categories, so that the grouping criterion is the historical business logic. The emerging categories are; (i) infrastructure leasing, (ii) specialization to a certain domain, (iii) incumbent MNOs ally to share costs, (iv) and public stakeholder intervention. Now let us discuss each of these categories and give some typical characteristics for a company in the category.

5.1.1. Infrastructure leasing Infrastructure leasing is found to be the oldest form of neutral host businesses. Companies, such as China Tower Corporation,3

Crowne Castle,4 and Helios Towers,5 all provide the full range of different infrastructure services from passive cablings to active small- cell services. Part of the infrastructure leasing companies have emerged when mobile network operators (MNO) corporatized their cell tower operations to separate units and divested the unit eventually to free the capital for other investments (Rasay & Shah, 2019). Infrastructure funds have acquired and financed several such new ventures, (e.g. DIF, 2020). Some independent infrastructure leasing companies have been founded by industry specialists together with infrastructure investment funds to challenge incumbents (e.g. WIG, 2020). These cases represent a bottom-up approach, in which the starting point of a company’s business is in the simple infrastructure elements and then the business has been expanded to other network elements.

It turns out that these companies are actually competing in two different markets. First, as these companies seek economies of scale, they typically also provide highly standardized services in terms of features and quality, which in turn increases rivalry between these companies on the downstream customer side. Second, as these companies have adopted merger and acquisition tactics as a growth strategy to find new opportunities for business expansion, they also need to compete for the acquisitions. The annual report 2019 of American Tower,6 for example, states “We compete, both for new business and for the acquisition of assets.“. Hence, these companies require a constant stream of funding to support both the construction of widening infrastructure and acquiring access to new regions. In turn this has resulted in a situation where all infrastructure leasing companies have eventually become publicly listed. Moreover, the process of market consolidation keeps the number of competitors decreasing as the entry barriers constraint new entries heavily.

5.1.2. Specialization to a certain domain The second category is specialization to a certain domain including companies that leverage special knowledge on some niche. The

domains in this category include areas such as railways, metro tunnels, airports, large sport venues, shopping malls, and exhibition centres. Companies typically develop their business gradually over the years by accumulating the domain knowledge that allows them to transform the business to network operator areas while still having their special domain knowledge. Through these explicit domain choices, companies are able to tighten customer relationships, use direct sales channels, and access strong customer references. Such choices provide an opportunity for companies to increase their business growth while introducing new lower-level value propositions.

3 https://ir.china-tower.com/en/about/profile.php. 4 https://investor.crowncastle.com/financial-information/sec-filings?c=107530&p=irol-sec. 5 https://www.heliostowers.com/investors/investor-home/. 6 https://americantower.gcs-web.com/static-files/abaea648-59f3-4884-a186-4e5c57cccf55, page 7.

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

10

The analysis suggests that due to these diversified paths and lack of competition between the domains, the market has become highly fragmented and it may not be easy to find synergies between the domains. BAI Communications,7 for example, operated in the consultancy area by specializing into the public transportation domain before becoming a neutral host, and by utilizing that knowl-edge, the company developed its business gradually towards active network services. Another example, Iberia Small Cell Networks8

was formed as a spin-off from Wireless Infrastructure Group9 and Axion when the companies realized that they required deepening knowledge on the domain of airport facilities. As the use of next generation connectivity services and data-based applications in-creases, it can be assumed that the companies in this category will keep diversifying also in the future.

There are some early signs that also the domain specialization area has started to consolidate. Although the specialized companies have not used merger and acquisition tactics as a primary source for growth, some of them have acquired similar companies to extend their knowledge and to get access to new customer cases. Moreover, this fragmented area has been a good opportunity for pension funds, infrastructure investment funds, and other investors to invest in. This has enabled neutral host companies to scale their in-novations and to expand the business beyond the original geographical area.

5.1.3. Alliances of incumbents for cost sharing The third category is strategic alliances including companies that use, e.g., joint-ventures, to seek synergies between ecosystem

incumbents. The analysis suggests that the main motivation is to seek economies of scale, thus to decrease production costs. Moreover, it actually turns out that horizontal integration can only take place in the upstream direction as agreeing downstream factors would be considered as a cartel. Allying in the upstream direction allows owner enterprises, for example, to reduce the costs of network op-erations and be compliant with strict spectrum license terms. Finnish Shared Network10, for example, was established in 2013 by DNA and Telia in Finland to build and operate mobile networks in the north-east part of the country where the population is sparse. Two examples from the UK, MBNL11 was established in 2007 by EE and Three to ensure nationwide coverage of the services, and CTIL12 was established in 2012 by O2 and Vodafone to decrease operational costs of the urban network operations. Although a strategic alliance seems to be a common way to improve operational efficiency by sharing the costs of network operations amongst neutral host companies, and some of these have had liberal customer policies, however, some these have been very selective who can become a customer and it can be argued that these are not as neutral as other categories.

5.1.4. Public stakeholders intervene Several public authorities around the globe have identified that there is a need for public authority driven data and communi-

cations services. In several cases, cities have carried out development projects that strived to build a collaboration ecosystem that in turn would provide city-wide services utilizing a neutral host model. Some of these projects targeted data related services, e.g. Copenhagen Smart City project,13 while others focused more on the communications, e.g. Wireless Philadelphia.14 Moreover, some projects strived to address both of these, e.g. Singapore Smart City Project15 and the Sunderland Our Smart City project.16 These projects can be seen as public stakeholder interventions that steered market evolution by policing how the neutral host ecosystem emerges. The analysis suggests that cities do not pursue their data and communications initiatives primarily for profit, but they want to provide enablers for the well-being of society and to provide business opportunities for companies and to enhance operational effi-ciency through new technologies. These objectives in turn guide how projects are implemented.

In some cases, the communications services of a municipality area have been combined with other utility services. NextLight17 in the US, for example, is part of the Longmont utility company, and these units provide combined electricity network services and broadband services. However, this approach implies that the local broadband service provider holds a monopoly position preventing others from enter the market.

As many cities rather choose to act as an orchestrator for ecosystem operations than to be a full featured service provider, ecosystem collaboration models become crucial (Lenkenhoff et al., 2018). In the horizontal collaboration model, a city can choose to establish a dedicated city-owned neutral host company to provide services and to allow infrastructure and knowledge to be shared (the case NextLight). At the same time, using a vertical collaboration model, some cities have outsourced service operations to allow MNOs and other companies to participate as a neutral host, e.g. Dublin in Ireland.18 In short, collaboration models chosen by cities are highly dependent on regional ecosystem conditions.

To get an access to horizontal resources and knowledge sources, public stakeholder initiated neutral hosts can seek partnering

7 https://www.baicommunications.com/our-services/transit-communications/. 8 https://www.iberiasmallcellsnetworks.es/en/. 9 https://www.wirelessinfrastructure.co.uk/about-us/.

10 https://yhteisverkko.fi/suomen-yhteisverkko/. 11 https://mbnl.co.uk/about-us/. 12 https://www.cornerstone.network/about/overview. 13 https://www.copcap.com/set-up-a-business/key-sectors/smart-city. 14 https://technical.ly/philly/2015/03/04/cities-learn-phillys-failed-municipal-broadband-effort/. 15 https://publications.iadb.org/en/international-case-studies-smart-cities-singapore-republic-singapore. 16 https://www.sunderlandoursmartcity.com/about-us/. 17 https://www.longmontcolorado.gov/departments/departments-e-m/longmont-power-communications/about-lpc. 18 https://smartdublin.ie/.

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

11

through joint-ventures. However, cities and neutral host companies can also partner vertically to get access to knowledge and re-sources. For instance, Barcelona City19 agreed to collaborate with Huawei in late 2019. The city is looking for a partner in the digital transformation industry that can help city businesses leverage 5G and build smart city applications. This collaboration can accelerate the adoption of smart city services in Barcelona, but it may also introduce a vendor lock-in.

In some cases, regulatory decisions have created natural monopolies for certain services. For example, in 2006, Digita20 acquired an exclusive right to operate 450 MHz spectrum for wireless broadband services in Finland. One of the decision criteria was that Digita clearly stated that it uses a neutral host type position in their ecosystem and it provides wholesale services only. Regulatory authority interpreted that this kind of approach enhances ecosystem openness which has more advantages than the monopolistic situation has drawbacks.

All these public authority driven actions have shaped ecosystem structures by influencing company level decisions, i.e. strategies. The list of characteristic strategies is not all-inclusive, but it gives some hints how authority interventions take place. Moreover, it should be noticed that actual regulatory frameworks and explicit industry policies shape market structures further, but those regulate the market as a whole rather than only some specific entity of it.

These four characteristics emergence paths proposed here provide a historical perspective to the emergence of neutral host type companies. This study acknowledges that some companies may actually posit themselves in several of these categories, and there may be companies that actually do not fit any of these. Data markets are especially emerging and characteristic patterns may not have formed yet. Next, let us discuss how the ownership structures are found to influence neutral-host company operations.

5.2. On the ownership structures of neutral host companies

Shareholders of a company can be seen as investors who have varying investment strategies (Slater & Zwirlein, 1992) and they also differ in the level of bearable risk-taking (Hoffmann et al., 2015). Several studies suggest that the ownership structure of a company actually affects its market entry strategies (Amihud & Lev, 1999), which in turn affect its economic performance (Thomsen & Pedersen, 2000). American Tower Corporation,21 a publicly listed company in the New York Stock Exchange (NYSE), for example, is mainly owned by institutional investors who expect a relatively stable stream of dividends.22 On the other hand, a neutral host company Kuuskaista,23 for example, is owned by the members and the users of the services, and while keeping service pricing low it invests excess profits back for the service development and for the society. Hence, in general, it can be assumed that public stock listed companies have the most aggressive ROI expectations, while associations, foundations, and community-based models have the least aggressive ROI expectations.

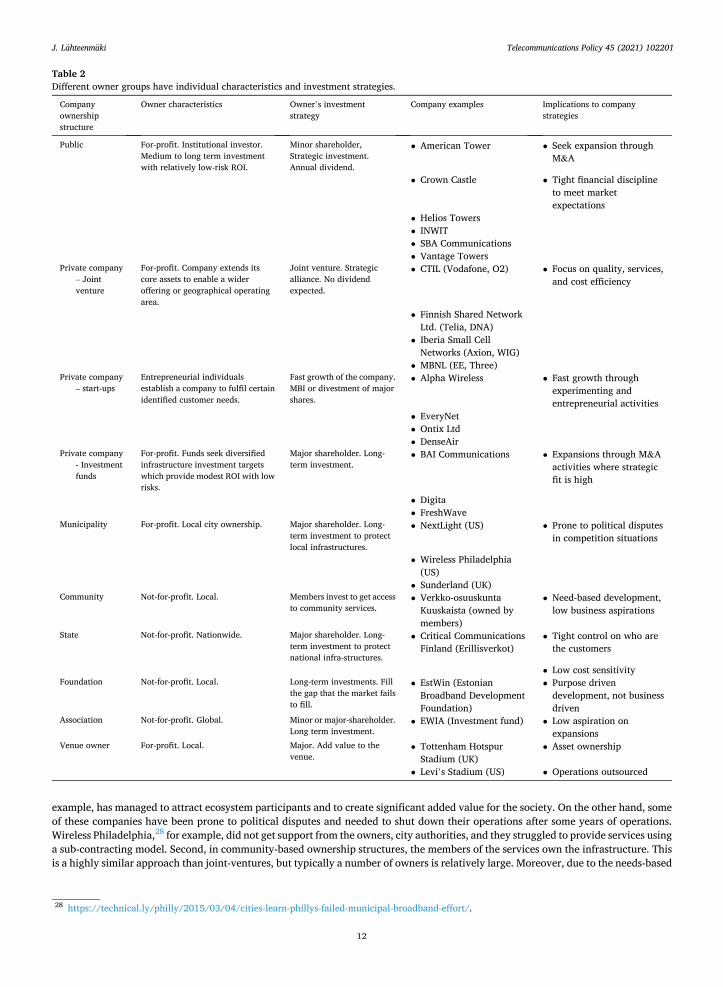

The analysis phase finds ten categories of ownership structures. Each of these structures has its own characteristic investment strategy of an owner. Table 2 summarizes these categories.

The neutral host companies, that are listed in public stock exchange, are typically majorly owned by institutional investors. These investor brokers typically have the investment strategy of above average profits, and the investors typically require dividends when the company has matured. This in turn increases the need for strict financial targets, which in turn leads to the seek for economies of scale.

The study finds four types of privately owned companies. Joint-ventures formed by incumbent MNOs, early phase challengers, enterprises backed by strong investment funds, and venue owners. First, joint-ventures typically focus on the cost efficiency aspect of the services. As the owners are also the users of the services, they have clear requirements and quality targets for the services. Second, challengers typically seek fast growth through some service niche on a global scale. These companies are led by founder CEOs, and these typically do not have strong financing behind them. DenseAir,24 for example, provides mobile network services in radically different ways than its competitors. Third, already matured companies typically have a strong financing partner or owner who can ensure growth in the previously identified niche. BAI Communications, for example, has expanded its operations through acquisitions to several areas. Fourth, the owners of different venues are typically large real-estate funds. These companies see local venue specific data and communication operations as value-added services, which increase customer retention and brand-value, which in turn in-crease financial results. Tottenham Hotspur Stadium,25 for example, is owned by the football club Spurs.26 While owners of joint- ventures and venues expect long term investments and stable operations without an exit plan, owners of challengers and already matured companies expect exit opportunities, which implies that the company operations need to show increasing value for owners and market legitimacy.

Rest of the owner categories are non-profits, municipalities or states. First, some of the municipalities have established separate companies for data and communications operations. In these arrangements, the neutral host companies have had relatively small regional scope, but ambitious objectives set by owners. Some of these have been highly successful, Forum Virium27 in Helsinki, for

19 https://www.smartcitiesworld.net/news/news/huawei-seals-smart-city-deal-with-barcelona-4804. 20 https://yle.fi/uutiset/3-5752451. 21 https://www.americantower.com/investor-relations/stock-information/. 22 https://www.marketwatch.com/story/two-dividend-stock-income-ideas-as-the-fed-works-against-you-2019-07-29. 23 https://www.kuuskaista.com/yrityksesta/kuuskaista-konserni/. 24 https://denseair.net/about-us. 25 https://footballpredictions.net/blog/who-owns-tottenhams-stadium. 26 https://eventmasters.tottenhamhotspurtravelclub.tickets/who-owns-tottenham/. 27 https://forumvirium.fi/en/ceo-review-2020/.

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

12

example, has managed to attract ecosystem participants and to create significant added value for the society. On the other hand, some of these companies have been prone to political disputes and needed to shut down their operations after some years of operations. Wireless Philadelphia,28 for example, did not get support from the owners, city authorities, and they struggled to provide services using a sub-contracting model. Second, in community-based ownership structures, the members of the services own the infrastructure. This is a highly similar approach than joint-ventures, but typically a number of owners is relatively large. Moreover, due to the needs-based

Table 2 Different owner groups have individual characteristics and investment strategies.

Company ownership structure

Owner characteristics Owner’s investment strategy

Company examples Implications to company strategies

Public For-profit. Institutional investor. Medium to long term investment with relatively low-risk ROI.

Minor shareholder, Strategic investment. Annual dividend.

• American Tower • Seek expansion through M&A

• Crown Castle • Tight financial discipline to meet market expectations

• Helios Towers • INWIT • SBA Communications • Vantage Towers

Private company – Joint venture

For-profit. Company extends its core assets to enable a wider offering or geographical operating area.

Joint venture. Strategic alliance. No dividend expected.

• CTIL (Vodafone, O2) • Focus on quality, services, and cost efficiency

• Finnish Shared Network Ltd. (Telia, DNA)

• Iberia Small Cell Networks (Axion, WIG)

• MBNL (EE, Three) Private company

– start-ups Entrepreneurial individuals establish a company to fulfil certain identified customer needs.

Fast growth of the company. MBI or divestment of major shares.

• Alpha Wireless • Fast growth through experimenting and entrepreneurial activities

• EveryNet • Ontix Ltd • DenseAir

Private company - Investment funds

For-profit. Funds seek diversified infrastructure investment targets which provide modest ROI with low risks.

Major shareholder. Long- term investment.

• BAI Communications • Expansions through M&A activities where strategic fit is high

• Digita • FreshWave

Municipality For-profit. Local city ownership. Major shareholder. Long- term investment to protect local infrastructures.

• NextLight (US) • Prone to political disputes in competition situations

• Wireless Philadelphia (US)

• Sunderland (UK) Community Not-for-profit. Local. Members invest to get access

to community services. • Verkko-osuuskunta

Kuuskaista (owned by members)

• Need-based development, low business aspirations

State Not-for-profit. Nationwide. Major shareholder. Long- term investment to protect national infra-structures.

• Critical Communications Finland (Erillisverkot)

• Tight control on who are the customers

• Low cost sensitivity Foundation Not-for-profit. Local. Long-term investments. Fill

the gap that the market fails to fill.

• EstWin (Estonian Broadband Development Foundation)

• Purpose driven development, not business driven

Association Not-for-profit. Global. Minor or major-shareholder. Long term investment.

• EWIA (Investment fund) • Low aspiration on expansions

Venue owner For-profit. Local. Major. Add value to the venue.

• Tottenham Hotspur Stadium (UK)

• Asset ownership

• Levi’s Stadium (US) • Operations outsourced

28 https://technical.ly/philly/2015/03/04/cities-learn-phillys-failed-municipal-broadband-effort/.

J. Lahteenmaki

Telecommunications Policy 45 (2021) 102201

13

investments of the company, the service development activity is typically rather low and the company does not have high business aspirations. Verkko-osuuskunta Kuuskaista,29 for example, is owned by the members. It builds and operates passive and active infrastructure in one specific area in Finland, and it has opened the infrastructure for other service companies for service provisioning. Third, in some cases, the state holds the ownership of the company. Typically, there is some critical requirement to directly regulate and control the services and to ensure that the critical infrastructure follows the needs of that state. Critical Communications Finland30, for example, is tightly controlled by different ministries of Finland. Moreover, it is tightly regulated who can become a customer.

As these different categories depict, the objectives of different owner groups are different. The strategic guidance given by owners have direct influence on the strategic choices the company makes, which in turn influence the market level business model evolution.

5.3. Society level influencers to neutral host markets

Governmental actions have allowed new businesses to emerge, but also have forced some incumbents to react; let us take the United Kingdom as an example region. In the late 2010s, the UK government set ambitious targets. The aim is to provide fibre-access to all premises and ubiquitous access to 5G by 2035 (UK, 2018). Achieving this target using the traditional MNO model would increase investment needs to a high level due to multi-operator redundancies. This results in an opportunity for local neutral network operators who may share investment needs and share network assets in certain regions. For example, MBNL and CTIL are two of those neutral host operators in the UK which are going to leverage the opportunity. By setting ambitious objectives, the government signals the market that there are new investment opportunities available, which results in new investment money and emergence of new players. For example, Wireless Infrastructure Group (WIG) (WIG, 2020) was established in 2006 to operate on the cell-tower-leasing market and to introduce competition to the mobile-network-infrastructure market. WIG has changed their strategy to a more co-operational way towards MNOs as WIG’s customers are mainly large MNOs. The shift happened after the UK government decided to bet more on the ubiquitous 5G access. The company is privately owned but is nowadays backed by large global infrastructure investment funds.31

WIG has expanded the service offering from cell-towers to cover all relevant mobile network infrastructure components. Furthermore, the company seeks new domains for a business. WIG is a major investor in an autonomous vehicle test-bed platform which is the UKs largest. Such a shift to higher tier applications may result in WIG being one of the earliest neutral host operators operating in both the communications and data markets.

Government-led 5G promotions have also taken place in other countries. The Danish Energy Agency has a nationwide plan to promote the use of modern communications technologies and to find ways to create smarter cities (Kokkegård, 2019). Their 5G plan clearly states that the aim is the creation of new markets for independent small-cell operators. The plan contains several actions, such as site-rental, network-sharing, network-slicing, and network-neutrality. Furthermore, the EU funded research project called 5 G-CITY (2017) pilots the neutral host model in three different cities, Barcelona in Spain, Bristol in the UK and Lucca in Italy. Although the consortium of the pilot projects in Lucca and Bristol are entirely on public funding, Cellnex Telecom is participating as a private partner in the Barcelona project. The planned business model is largely based on infrastructure sharing, where street cabinets, lightning poles, and passive and active components of the mobile network all are intended for rental purposes. Although these publicly funded projects aim to create feasible business opportunities, it is open if the projects actually produce them.

There are several initiatives that did not end so well. Some projects, especially in Western countries, faced disputes, MNO ob-jections, and even legal actions when an incumbent operator tried to prevent infrastructure owners and municipalities from becoming a network operator. For example, incumbent lobbying and public debate did prevent Philadelphia City in the US from improving its network operations (Abraham, 2015). On the other hand, some cities previously had active network services for citizens, but have decided to shut down the network due to the emergence of 4G and 5G networks; for example, San Francisco,32 Dublin,33 and Sydney.34

Several municipality managed ecosystems have opted for the open ecosystem model and have also opted for free-pricing. For instance, Helsinki is classified as one of the most functional smart cities in Europe (Helsinki, 2018). The merit comes from the availability of open data sets. At the time of this study, more than 1000 open data sets are available (FV, 2019). Any company can continue to use them in their applications at no extra charge. Data is collected from applications related to urban use, such as tram location information. Using the data as a platform for new innovations, Helsinki aims to create new data-based markets. Typical goals for cities are to improve operational efficiency, improve the well-being of citizens, improve the visitors experience and enable business growth. The challenge for the data operator is to acquire relevant data and attract new ecosystem members to the platform.

As these examples illustrate, the emergence of neutral host opportunities is highly influenced by political and society level factors. Moreover, regional economic conditions and technology diffusion may influence the business decisions that emerging neutral host companies take.