-

8/14/2019 The External Economy

1/15

VI. THE EXTERNAL ECONOMY

In dias ba lan ce of pa ymen ts position rem ained com fortab le

du ring 20 07 -08,

notwi ths tanding a sharp increase in merchandise t rade def ici

t on account of

sus tained demand for non-oi l impor ts and escalat ion in

internat ional crude oi l

prices. Net surplus under invisibles remained buoyant, led by

high growth in

private transfers and software exports , thereby offset t ing a

s ignif icant part of

the trade defici t . Consequently, the current account defici t

was contained at

1.5 per cent of GDP during the year . Net capital inflows

increased substantial ly

during 2007-08, led by foreign direct investment, portfolio

investments and

external commercial borrowings (ECBs) . Outward foreign di rect

inves tment

increased, ref lect ing the global expansion by Indian

companies. Signif icantly

larger net capital inflows over the current account deficit

resulted in an accretion

of US $ 110.5 bil l ion to the foreign exchange reserves during

2007-08 (US $

47.6 billion du rin g 200 6-07).

Inte rnat ional Developme nts

The global economy expanded by 5.0 per cent in 2007 as agains t

5.1 per

cent in 2006. Af ter a s t ronger than expected growth in the

thi rd quar ter of

2007, most of the advanced economies recorded a sharp decelerat

ion in thei r

growth towards the end of the year 2007 driven mainly by the f

inancial cr is iswhich spread beyond the US sub-prime mortgage

market (Table 52). According

to the projections released by the International Monetary Fund

(IMF) in July

2008, the slowdown in global growth, which started in the middle

of last year ,

i s expected to cont inue through the second hal f of 2008, wi

th only a gradual

recovery during 2009. However, the fears of a significant

slowdown did not

come t ru e in the fir s t qu ar ter of 2008 . Cou ntr ies /

regions like Eu ro area, th e

US and Korea registered more or less same growth rates in the f

irs t quarter of

2008 as in the previous quar ter . The UK and the Japanese

economy exhibi ted

decelerat ion in the f irs t quarter of 2008. In contrast ,

emerging and developingeconomies continued to grow above trend

despite some slackening of growth

rates in the f irs t quarter of 2008.

The IMF has projected the US economy to grow by 1.3 per cent in

2008

(2.2 per cent in 2007). The US growth prospects , according to

the IMF, would

hinge upon the future course of the housing correction, extent

of f inancial

sector dis locat ion, an d th e ensu ing imp act on hou sehold a

nd bu s iness fina nces .

8 6

-

8/14/2019 The External Economy

2/15

8 7

The Externa l Economy

Table 5 2 : Growth Rat es - Global Sce nario(Per cent )

P : IMF Projections .

Note : Data for Ind ia in column s 2 an d 3 refer to fiscal

years 2006-07 an d 2007 -08, respectively.

Source : Intern ational Monetary Fun d; The Economist; an d the

OECD.

Region / Cou n try 2006 2007 2008P 2009P 20 07 2008

Q1 Q2 Q3 Q4 Q1

1 2 3 4 5 6 7 8 9 10

Advanced Econom ies

Eu ro a rea 2 .8 2 .6 1 .7 1 .2 3 .0 2 .5 2 .7 2 .2 2 .1

J a pa n 2 .4 2 .1 1 .5 1 .5 2 .6 1 .6 1 .9 2 .0 1 .3

Korea 5 .1 5 .0 4 .2 4 .4 4 .0 5 .0 5 .2 5 .7 5 .8

UK 2.9 3 .1 1 .8 1 .7 3 .0 3 .1 3 .3 2 .8 2 .5

US 2.9 2 .2 1 .3 0 .8 1 .9 1 .9 2 .8 2 .5 2 .5

OECD Cou n tr ies 3 .1 2 .7 1 .8 1 .7 2 .8 2 .5 3 .0 2 .7 2

.6

Emerging Economie s

Argen tin a 8 .5 8 .7 7 .0 4 .5 8 .0 8 .7 8 .7 9 .1 8 .4

Brazil 3 .8 5 .4 4 .9 4 .0 4 .3 5 .4 5 .7 6 .2 5 .8

Ch in a 11.6 11 .9 9 .7 9 .8 11.1 1 1.9 11 .5 11 .2 10.6

In d ia 9 .6 9 .0 8 .0 8 .0 9 .7 9 .2 9 .3 8 .8 8 .8

In don es ia 5 .5 6 .3 6 .1 6 .3 6 .0 6 .3 6 .5 6 .3 6 .3Ma la

ys ia 5 .9 6 .3 5 .0 5 .3 5 .3 5 .7 6 .7 7 .3 7 .1

Th a ila n d 5.1 4 .8 5 .3 5 .6 4 .3 4 .4 4 .9 5 .7 6 .0

The Euro Area is expected to grow by 1.7 per cent in 2008 (2.6

per cent in

2007), while there are increasing concerns that with spil lovers

from the US,

t i g h t e n i n g c r e d i t c o n d i t i o n s a n d r i s

i n g r i s k s p r e a d s m a y h a v e a d v e r s e

impl icat ions for the domest ic demand. The growth momentum in

Japan is

projected to decelerate to 1.5 per cent in 2008 (2.1 per cent in

2007) on account

of expected moderation in export growth and consumption. Growth

projection

for developing Asia by the IMF is placed at 8.4 per cent for

2008 as against

10.0 per cent in 2007 (Table 53). Growth in emerging Asia during

the f irs t

quar ter of 2008 was led by China and India. GDP in China grew

by 10.6 per

cent in the f irs t quarter of 2008. The IMF has projected that

growth in China

would moderate to 9.7 per cent in 2008 (11.9 per cent in

2007).

Going forward, the growth in global economy is projected to

moderate to

4.1 per cent in 2008 mainly on account of expected slowdown in

most of the

advanced economies, part icularly the US. The overall balance of

r isks to the

short- term global growth outlook remains t i l ted to the

downside. Interaction

between negat ive f inancial shocks and the domest ic demand

remains a ser ious

downside r isk for the US and to some extent in Western Europe

and elsewhere.

However, there is some upside potential for projected domestic

demand in

emerging economies . The emerging market and developing

economies are

-

8/14/2019 The External Economy

3/15

8 8

Macroeconomic an d Monetary Developmen ts : Fi rs t Qu ar ter

Review 2008 -09

expected to remain the key factor in support ing the global

economy and in

cushioning global downturns mainly because of their l imited

direct exposure to

su b-pr ime related secur i t ies . Consu mp t ion a ct ivity su

ppor ted domest ic dema nd

in other emerging Asian economies while export growth began to

show some

signs of moderation. The strength of domestic demand in the

region combined

with rising food and energy prices, however, led to the build-up

of inflationary

pressures in a number of countr ies in emerging Asia. Apart from

the possibil i ty

of further credit crunch, downside r isks to global growth,

therefore, include

contagion from the l ikely US recession, increased inflat ionary

pressures driven

by r is ing food and energy prices, and persist ing global

imbalances.

Table 5 3 : Sele ct Econ om ic Indicato rs - World

Item 2002 2003 2004 2005 2006 2007 2008P 2 009P

1 2 3 4 5 6 7 8 9

I. World Outpu t (Per ce nt ch ange ) # 2.8 3 .6 4 .9 4 .4 5 .1

5 .0 4 .1 3 .9

(1 .9) (2 .6) (4 .0) (3 .4) (3 .9) (3 .7) (2 .6 ) (2 .6)

i) Adva n ced Econ om ies 1 .6 1 .9 3 .2 2 .6 3 .0 2 .7 1 .7 1

.4

ii) Other Emerging Marke t and

Developin g Cou n tr ies 4 .7 6 .2 7 .5 7 .1 7 .9 8 .0 6 .9 6

.7

of w hich: Developin g As ia 6 .9 8 .1 8 .6 9 .0 9 .9 10.0 8 .4

8 .4

II. Consum er Price Inflation (Per cent)

i) Adva n ced Econ om ies 1 .5 1 .8 2 .0 2 .3 2 .4 2 .2 3 .4 2

.3

ii) Oth er Emergin g Market an d Developing Cou ntries 6 .7 6 .6

5 .9 5 .7 5 .4 6 .4 9 .1 7 .4

of w hich: Developin g As ia 2 .0 2 .5 4 .1 3 .8 4 .1 5 .3 5 .9

4 .1

III. Net Capital Flows * (US $ billion )

i) Net Pr iva te Cap ita l Flows (a +b+c)** 89.8 168.6 241.9

251.8 231.9 605.0 330.7 441.5

a ) Net Pr iva te Direct In ves tm en t 157.2 166.2 188.7 259.8

250 .1 309.9 306.9 322 .4

b) Net Pr iva te Por tfolio In ves tm en t -9 2 .2 -13 .2 16 .4

-1 9 .4 -1 03.8 48.5 -72 .2 31 .0

c) Net Oth er Pr iva te Ca p ita l Flows 25 .1 17 .1 38.5 13.3

87 .5 2 48.8 98.0 90.0

ii) Net Officia l Flows -0 .6 -5 0 .0 -70 .7 -109.9 -160.0

-149.0 -162.3 -1 49.8

IV. World Trade @

i) Volu m e 3.5 5 .4 10.7 7 .6 9 .2 6 .8 5 .6 5 .8

ii) Pr ice Defla tor 1 .1 10 .4 9 .6 5 .5 4 .9 8 .2 8 .6 1

.1

V. Current Accoun t Balance (Per ce nt to GDP)

i) US -4 .4 -4 .8 -5 .5 -6 .1 -6 .2 -5 .3 -4 .3 -4 .2

ii) Ch in a 2 .4 2 .8 3 .6 7 .2 9 .4 11 .1 9 .8 10.0

iii) Mid dle Ea s t 4 .8 8 .3 11.8 1 9.7 20 .9 19.8 23 .0

19.4

P : IMF P roje ct ion s .

# : Growth ra tes a re based on exchange ra tes a t pu rchas ing

power pa r i ties . F igures in pa renth eses a re growth ra

tes

a t m arke t exchan ge ra tes .

* : Ne t capita l flows to emerging marke t and deve loping coun

tr ie s .

** : On a ccoun t of dat a limitations, flows listed u nd er Net

Private Cap ital Flows ma y inclu de som e official flows.

@ : Average of an nu al percenta ge chan ge for world exports an

d imports of goods a nd s ervices.

Source : World E conomic Outlook, April 2008; World Econom ic

Outlook Upda te, J uly 2008 , Internat iona l Monetary Fu nd.

-

8/14/2019 The External Economy

4/15

8 9

The Externa l Economy

According to the IMF, growth in world trade is expected to

moderate to

5.6 per cent in volume terms in 2008 from 6.8 per cent in 2007

(see Table 53).

Exports of other emerging market and developing countr ies are

projected to

grow by 7.1 per cent in 2008 (8.9 per cent a year ago), while

those of advanced

countries are expected to grow by 4.5 per cent (5.8 per cent a

year ago).

World merchandise exports ( in US dollar terms) in the f irs t

quarter of

2008 (January-March) recorded a growth of 22.9 per cent , as

agains t 13.2 per

cent a year ago. Emerging and developing economies recorded a

growth of 26.0

per cent , showing a sharp r ise from 13.0 per cent a year ago.

Exports from

indust r ial countr ies grew at an accelerated rate of 20.4 per

cent in January-

March 2008, as compared with 13.5 per cent in January-March 2007

(Table 54).

Balance of Payment s : 200 7-08

According to the provisional data released by the Directorate

General of

Comm ercial In telligen ce an d Sta tistics (DGCI&S), In

dias m erch an dise exports

recorded a growth of 25.8 per cent dur ing 2007-08 as compared

wi th 22.6 per

cent d u ring 2006 -07. Growth of In dias imp orts a ccelerated

to 29.0 p er cent in

2007 -08 from 2 4.5 per cent in 2006 -07 (Char t 40).

Comm odity-wise da ta on In dias m ercha n dise exports for 200

7-08 s h owed

a n a c c e l e r a t e d g r o w t h i n p r i m a r y p r o d

u c t s a n d m a n u f a c t u r e d p r o d u c t s

Table 5 4 : Growt h in Exports - Global Sce nario

(Per cen t)

Source : Intern ationa l Finan cial Stat istics, Int erna tional

Money Fun d; DGCI&S for Ind ia.

Region / Cou n try 2006 2007 2007-Q1 2008-Q1

1 2 3 4 5

World 1 5 .3 1 5 .0 1 3 .2 2 2 .9

Indus trial Countrie s 1 2 .4 1 3 .6 1 3 .5 2 0 .4

Em e rging and De ve loping Ec onom ie s 1 9 .1 1 6 .8 1 3 .0 2

6 .0

Ch in a 27.2 25.6 2 7.8 21.3

Fra n ce 9 .9 1 2.0 10 .3 22.9

Germ a n y 14.7 1 8.5 2 1.2 20.9

In dia 2 1 .4 2 0.3 15 .2 33.8

In don es ia 18 .3 16.8 9 .7 34.2

J a pa n 9 .2 9 .2 5 .4 28.7

Korea 14 .4 14 .2 14 .6 17.4

Malays ia 14 .0 9 .6 7 .6 19.1

Sin gapore 18.4 10.1 9 .9 21.3

Th a ila n d 18.5 16.8 1 7.2 21.3

US 14 .7 12 .2 10.8 17.1

-

8/14/2019 The External Economy

5/15

9 0

Macroeconomic an d Monetary Developmen ts : Fi rs t Qu ar ter

Review 2008 -09

(Table 55). Agriculture and allied products, engineering goods,

gems and jewellery,

and pet roleum products were the main contr ibutors of expor t

growth dur ing

2007-08. Within primary products , exports of agriculture and al

l ied products

showed a sharp increase of 42.4 per cent (24.2 per cent a year

ago). Exports of

manufactured goods increased by 19.1 per cent (17.0 per cent a

year ago) .

Within manufactured goods, gems and jewellery, texti les and

texti le products ,

and chemicals and related products recorded higher growth whi le

engineer ing

goods exhibited moderation. Growth in exports of petroleum

products during

2007-08 decelerated to 33.1 per cent from 60.5 per cent a year

ago.

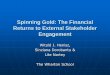

Chart 40: India's Merchandise Trade

Exports Imports

0

Growthrate

(perc

ent)

Apr-06

Jun-06

Aug-06

Oct-06

Dec-06

Feb-07

Apr-07

Jun-07

Aug-07

Oct-07

Dec-07

Feb-08

10

20

30

40

50

60

70

Apr-08

Table 55 : Exports of Princ ipal Com m oditie s

Com m odity Grou p US $ b illion Va r ia t ion (p er cen t )

2006-07 2007-08 2006-07 2007-08

1 2 3 4 5

1 . Prim ary Product s 1 9 .7 2 7 .1 2 0 .2 3 7 .5

of wh ich:

a ) Agr icu ltu re a n d Allied Prod u cts 12 .7 18 .1 24.2 4

2.4

b) Ores a n d Min era ls 7 .0 9 .0 13.6 2 8.6

2 . Manufact ured Goods 8 4 .9 1 0 1 .1 1 7 .0 1 9 .1

of wh ich:a ) Ch em ica ls a n d Rela ted Prod u cts 17 .3 20 .5

17.4 1 8.0

b) En gin eer in g Goods 29 .6 3 6.7 36.1 24.2

c) Text iles a n d Text ile Produ cts 17 .4 19 .0 5 .9 9 .5

d) Gem s a n d J ewellery 16 .0 19.7 2 .9 2 3.0

3 . Pe trole um Produc ts 1 8 .7 2 4 .9 6 0 .5 3 3 .1

4 . Tot al Export s 1 2 6 .4 1 5 9 .0 2 2 .6 2 5 .8

Memo:

Non -oil Exports 107.7 134 .1 17.7 24.6

Source : DGCI&S.

-

8/14/2019 The External Economy

6/15

9 1

The Externa l Economy

Dest inat ion-wise, al though the US remained the pr incipal

expor t market ,

i t s share decl ined to 13.0 per cent dur ing 2007-08 f rom

14.9 per cent a year

ago (Table 56). The other major destinations were the UAE (9.7

per cent), China

(6.8 per cent), Singapore (4.3 per cent), the UK (4.1 per cent),

Hong Kong (4.0

per cent) , Germany (3.2 per cent) and the Netherlands (3.0 per

cent) . During2007-08, exports to the EU, North America, Eastern

Europe and Asian developing

countries showed an accelerated growth, while that to OPEC,

African developing

countries and Latin American developing countr ies showed

decelerat ion.

Growth in imports of petroleum, oil and lubricants (POL)

accelerated to

39.4 per cent dur ing 2007-08 f rom 30.0 per cent dur ing

2006-07, main ly

reflecting the spurt in the Indian basket of international crude

oil prices (higher

by 27.4 per cent in 2007-08 than 12.0 per dur ing 2006-07) .

Growth in non-oi l

impor ts was placed at 24.4 per cent dur ing 2007-08 (22.2 per

cent a year ago)

an d contr ibuted a bout 66.8 p er cent to the overal l imp or t

growth.

Commodity wise data on non-oil imports for 2007-08 indicated

that gold

and si lver recorded a lower growth of 21.9 per cent (29.4 per

cent during 2006-

07). Non-oil imports net of gold and si lver increased at an

accelerated rate of

24.7 per cent . The other major non-oil products which recorded

accelerated

growth in imports were, inter alia , edible oi l , pearls ,

precious and semi-precious

stones and chemicals . Capital goods imports recorded a growth

of 24.1 per

cent , marginally lower than that of 2006-07 (Table 57).

Source-wise, China was the principal source of imports , consti

tut ing 11.3

per cent of total imports (oil plus non-oil) during 2007-08. The

other major

Table 5 6 : Direc tion o f Indias Exports

Grou p / Cou n try US $ b illion Va ria t ion (p er cen t )

2006-07 2007-08 2006-07 2007-08

1 2 3 4 5

1 . OECD Count rie s 5 2 .0 6 1 .7 1 3 .5 1 8 .6

of wh ich:

a ) EU 2 5.8 32.2 15 .1 24.9

b) North Am er ica 20.0 2 2.0 8 .7 1 0.0

US 18 .9 20.7 8 .7 9 .7

2 . OPEC 2 0 .7 2 6 .2 3 5 .8 2 6 .4of wh ich:

UAE 12 .0 15.4 40 .0 27.7

3 . Deve loping Countrie s 5 0 .8 6 7 .2 2 7 .8 3 2 .4

of wh ich:

Asia 37 .6 50.1 21 .4 33.2

Peop les Repu blic of Ch in a 8 .3 10 .8 22 .7 3 0.0

Sin ga p ore 6 .1 6 .9 11 .9 12.9

4 . Total Exports 1 2 6 .4 1 5 9 .0 2 2 .6 2 5 .8

Source : DGCI&S.

-

8/14/2019 The External Economy

7/15

9 2

Macroeconomic an d Monetary Developmen ts : Fi rs t Qu ar ter

Review 2008 -09

sources were Saudi Arabia (8.1 per cent) , the UAE (5.6 per

cent) , the US (5.5

per cent) , Iran (4.6 per cent) , Switzerland (4.1 per cent) ,

Germany (4.0 per

cent) and Singapore (3.4 per cent) .

In dias m erch an dise trad e deficit, on a ba lan ce of pa ymen

ts ba sis, widen ed

from US $ 63.2 billion in 2006-07 to US $ 90.1 billion in

2007-08. As proportion

to GDP, the trade defici t increased from 6.9 per cent to 7.7

per cent .

Curren t Acc oun t

Net s u r p l us under i nv i s i b l e s ( s e r v i ces , t r

ans f e r s and i ncome t aken

together) expanded to US $ 72.7 bil l ion in 2007-08 (US $ 53.4

bil l ion in

2006-07), ref lect ing mainly the r ise in remittances from

overseas Indians, large

receipts from software exports , h igher interest in come on

reserves an d relat ively

moderate decl ine in payments of bus iness services (Table 58) .

Growth in

invis ible receipts at 26.2 per cent dur ing 2007-08 was broadly

comparable

with tha t of 28.3 per cent in 2006-07, ma inly du e to the m

omentu m ma inta ined

in the growth of software services exports , t ravel , t

ransportat ion, along withthe s teady inf low of remit tances f rom

overseas Indians . Invis ible payments

grew by 17.7 per cent in 2007-08 (29.3 per cent in 2006-07) ,

ref lect ing the

ma jor payments on accou nt of t ravel, t ransp or tat ion, bu s

iness an d m an agemen t

consul tancy, engineer ing and other technical services ,

dividend, prof i t and

interes t . The moderat ion in growth rate of invis ible

payments dur ing 2007-08

was mainly due to moderate payments relat ing to a number of bus

iness and

professional services.

Table 5 7 : Im ports of Princ ipal Com m oditie s

Com m odity Grou p US $ b illion Va r ia t ion (p er cen t )

2006-07 2007-08 2006-07 2007-08

1 2 3 4 5

Petroleu m , Petroleu m Produ cts a n d Rela ted Mater ia l 5 7

.1 7 9.6 3 0.0 3 9.4

Ed ib le Oil 2 .1 2 .6 4 .2 2 1.3

Iron a n d Steel 6 .4 8 .7 4 0.5 3 5.2

Ca pita l Goods 47 .1 5 8.4 25 .0 24.1

Pea rls , Preciou s a n d Sem i-Preciou s Ston es 7 .5 8 .0 -18

.0 6 .5

Ch em ica ls 7 .8 9 .9 1 2.1 26.2

Gold a n d Silver 1 4 .6 17 .8 29.4 2 1.9

Total Imports 185.7 239.7 24.5 29.0

Memo:

Non -oil Im ports 12 8.6 160.0 22 .3 24.4

Non -oil Im p or ts exclu din g Gold a n d Silver 114.0 142.2

21.4 24.7

Main ly In d u s t r ia l In pu ts* 104.7 130.0 19.6 24.2

* : Non-oil imports net of gold and si lver , bulk consumption

goods, manufactured fer t i l isers and professional

ins t ruments .

Source : DGCI&S.

-

8/14/2019 The External Economy

8/15

9 3

The Externa l Economy

During 2007-08, the widening of the trade defici t mainly led by

imports ,

resulted in a widening of current account defici t to US $ 17.4

bil l ion (1.5 per

cent of GDP) f rom US $ 9 .8 b i l l ion (1 .1 per cent of GDP)

in 2006-07,

notwi ths tanding a large net surplus in the invis ible account

(6.2 per cent of

GDP in 2007-08 as agains t 5.8 per cent in 2006-07) (Table 59

and Char t 41) .

The net invisible surplus offset 80.7 per cent of the trade

deficit during 2007-08

as compared to 84.5 per cent dur ing 2006-07. Net of remit

tances , the current

account defici t was US $ 58.2 bil l ion or 5.0 per cent of GDP

during 2007-08

(US $ 37.7 billion and 4.1 per cent of GDP in 2006-07).

Capital Flows

Capi tal inf lows to India, both debt and non-debt , remained

large dur ing

2007-08. Within non-debt f lows, FDI inflows at US $ 32.4 bil l

ion during 2007-

08 (US $ 22.1 bil l ion in 2006-07) reflected the continued

strength of sustained

domestic act ivi ty and posit ive investment cl imate. FDI

inflows were channeled

mainly into f inancial , manufactur ing and cons t ruct ion

sectors . Country-wise

detai l s of FDI f lows revealed the cont inued predominance of

Maur i t ius as the

major inves tor in India. Net outward FDI were US $ 16.8 bi l l

ion dur ing 2007-

08 (US $ 13.5 bi llion in 20 06 -07), reflect in g th e expan

sion by In dian

companies in global markets (Table 60).

Table 5 8 : Invis ibles Acc oun t (Net )

(US $ m illion)

1 2 3 4 5 6 7 8

Services 31 ,810 37,550 10,079 8,729 7,608 10,430 10,783

Tra vel 2 ,43 8 2,118 1,251 207 145 905 861

Tran sporta tion -18 -2 ,107 230 -587 -649 -293 -578

In su ra n ce 560 543 198 185 36 191 131

Govern m en t n ot in clu ded els ewh ere -153 -51 -43 -16 -62

16 11

Softwa re 29,033 37,0 51 8,775 8,040 7,667 9,257 1 2,087

Oth er Services -50 -4 -332 900 471 354 -1 ,729

Tra n s fers 28 ,16 8 41,017 8,463 7,518 9,265 10,86 6 1

3,368

In ves tm en t In com e -6 ,018 -5 ,239 -1 ,284 -1 ,719 -1 ,142

-1 ,161 -1 ,217

Com p en sa t ion of Em p loyees -555 -671 -136 -128 -201 -160

-182

Tot al 5 3 ,4 0 5 7 2 ,6 5 7 1 7 ,1 2 2 1 4 ,4 0 0 1 5 ,5 3 0 1

9 ,9 7 5 22 ,7 5 2

PR : Pa rt ia lly Revis ed . P : Prelim in ary.

Item

J a n . -

March

2007-08

July-

Sept. PR

Oct.-

Dec.PR

J a n . -

Mar. P

2006-07PR

April-

Ju n e PR

2007-08P2006-07PR

April-March

-

8/14/2019 The External Economy

9/15

9 4

Macroeconomic an d Monetary Developmen ts : Fi rs t Qu ar ter

Review 2008 -09

Table 5 9 : Indias Balance of Paym en ts

1 2 3 4 5 6 7 8

Exports 1 ,28 ,083 158,461 35,700 35 ,752 37,595 42 ,284 42,83

0

Im port 1 ,91 ,2 54 248,521 48,570 56 ,453 58,069 67,376

66,623

Tra d e Ba la n ce -63 ,171 -90 ,060 -12 ,870 -20 ,701 -20 ,474

-25 ,092 -23 ,793

(-6 .9 ) (-7 .7)

In vis ib le Receip ts 1 ,15 ,074 145,257 35,715 29,100 32,322

38,764 45,071

In vis ib le Pa ym en ts 61 ,669 72,600 18,593 14 ,700 16,792

18,789 22,319

In vis ib les , n et 53 ,405 72,657 17,122 14 ,400 15,530 19,975

22,752

(5 .8) (6 .2)

Cu rren t Accou n t -9 ,766 -17 ,403 4,252 -6 ,301 -4 ,944 -5

,117 -1 ,041

(-1 .1 ) (-1 .5)

Ca pita l Accou n t (n et )* 46 ,372 109 ,567 16,200 17,501

34,180 31,855 26,031

of wh ich:

Foreign Direct In ves tm en t 8 ,479 15,545 899 2,658 2,808

3,729 6,350

Por tfolio In ves tm en t 7 ,062 29,261 1,849 7,458 10,876

14,662 -3 ,735Extern a l Com m ercia l Borrowin gs + 16,155 22,165

6,343 6,990 4,136 6,212 4,827

Sh ort Term Tra d e Credit 6 ,612 17,683 934 1,804 4,886 4,691

6,302

Extern a l Ass is tan ce 1 ,7 67 2,114 764 241 468 565 840

NRI Dep os its 4 ,321 179 648 -447 369 -853 1,110

Ch a n ge in Res erves # -36 ,606 -92 ,164 -20 ,452 -11 ,200 -29

,236 -26 ,738 -24 ,990

Memo:

Current Ac coun t -3 7 ,7 0 7 -5 8 ,1 8 1 -4 ,1 6 7 -1 3 ,8 3 2

-1 4 ,1 6 2 -1 5 ,9 0 9 -1 4 ,2 7 8

ne t of Private Trans fers (-4 .1 ) (-5 .0 )

PR : Pa rt ia lly Revis ed . P : Prelim in a ry

* : In clu des errors a n d om is s ion s . + : Med iu m a n d

lon g-term b or rowin gs .

# : On a ba lance of payments bas is (exc luding va lua t ion);

(- ) ind ica tes inc rease .

Note : Figures in pa renth eses are percenta ges to GDP

(US $ million)

Item

J a n . -

March

2007-08 P

July-

Sept.

Oct.-

Dec.

J a n . -

MarchApril-March

2006-07PR

April-

J u n e

2007-08P2006-07 PR

Foreign inst i tut ional investors (FIIs) made net purchases in

the Indian

s tock market dur ing 2007-08, despi te net out f lows dur ing

August , November ,

Chart 41 : Movement in Current Account Balance

Trade Balance Invisible Balance Current Account Balance

Apr-

Jun

2004

Jul-Sep

2004

Oc

t-Dec

2004

Jan-M

ar

2005

Apr-

Jun

2005

Jul-Sep

2005

Oc

t-Dec

2005

Jan-M

ar

2006

Apr-

Jun

2006

Jul-Sep

2006

Oc

t-Dec

2006

Jan-Mar

2007

Apr-

Jun

2007

Oc

t-Dec

2007

Jul-Sep

2007

US$billion

-25

-20

-15

-10

-5

0

5

10

15

20

25

Jan-M

ar

2008

-

8/14/2019 The External Economy

10/15

9 5

The Externa l Economy

February and March. The large FII inflows (net) in 2007-08 at US

$ 20.3 billion

as against US $ 3.2 bil l ion in 2006-07 also reflected

increased part icipation of

FIIs in the primary market . Reflecting the buoyant s tock

markets , the resources

m obilised b y the In dian comp an ies th rou gh th eir globa l

offerin gs of ADRs/ GDRs

abroad also remained large amounting to US $ 8.8 bil l ion in

2007-08 (US $ 3.8

billion in 2006-07).Among debt flows, the inflows (net) under

external commercial borrowings

were higher at US $ 22.2 bil l ion during 2007-08 enabled by f

iner spreads on

ECBs and r is ing f inancing requirements. Net short term trade

credit was at US

$ 1 7.7 billion (in clu sive of su pp liers credit u p to 1 80

da ys) du ring 200 7-08 as

against US $ 6.6 bil l ion during the previous year . The signif

icant r ise reflected

the increased f inancing requirements of crude oil imports led

by higher crude

prices. Ou t of total short- term tra de credit , th e su

ppliers credit up to 18 0 da ys

amounted to US $ 6.8 bil l ion during 2007-08 (US $ 3.3 bil l

ion in 2006-07).

NRI deposits recorded a marginal net inflow (US $ 179 million)

during 2007-08

as compa red with a large in flow of US $ 4.3 billion in 20 06

-07, on a ccoun t of

prevai l ing interes t rates on such deposi ts and large wi

thdrawals f rom the

NR(E)RA for domestic use.

With net capital f lows being substantial ly higher than the

current account

def ici t , the overal l balance of payments recorded a surplus

of US $ 92.2

bi l l ion dur ing 2007-08, as compared wi th a surplus US $

36.6 bi l l ion dur ing

2006-07.

Table 6 0 : Capital Flows

(US $ million)

2006-07 2007-08 2007-08 2008-09

April-May

1 2 3 4 5

Foreign Direct In ves tm en t in to In dia 22 ,07 9 32,435 3,763

7,681

Foreign Direct In ves tm en t a broa d -13 ,512 -16 ,782 ..

..

FIIs (n et) 3 ,2 25 20,328 8,417 * -5 ,648 *

ADRs / GDRs 3,776 8,769 16 998

Extern a l Ass is ta n ce (n et ) 1 ,767 2,114 .. ..

Extern al Commercial Borrowings (net)

(Mediu m a n d lon g-term ) 16,155 22,165 .. ..

Sh or t-term Tra de Credit (n et) 6 ,612 17,683 .. ..

Non -NRI Ba n k in g Ca pita l (n et ) -2 ,408 11,578 .. ..

NRI Depos it s (n et) 4 ,321 179 -559 292

Oth er Ca pita l 3 ,95 3 9 ,62 7 .. ..

* : Up to J u ly 11 , 2008.

Note : Data on FIIs p resented in this t able represent inf lows

into the cou ntry. They may differ from da ta re la ting to

net investmen t in st ock excha nges by FIIs in Ch apter V.

-

8/14/2019 The External Economy

11/15

9 6

Macroeconomic an d Monetary Developmen ts : Fi rs t Qu ar ter

Review 2008 -09

In dias foreign exch an ge reserves were US $ 3 09 .7 billion a

s a t en d-March

2008, showing an increase of US $ 110.5 bil l ion over end-March

2007. The

increase in reserves was mainly due to an increase in foreign

currency assets .

Valuation gain, ref lect ing the appreciat ion of major

currencies against the US

dollar , accounted for US $ 18.3 bil l ion in total reserves

during 2007-08 as

against a valuation gain of US $ 11.0 bil l ion during the

previous year .

External Debt

In dias tota l externa l debt was placed a t US $ 2 21.2 billion

a t en d-March

2008, recording an increase of US $ 51.5 bil l ion (30.4 per

cent) over end-

March 2007 (Table 61). The increase in external debt during the

period was

mainly on account of higher external commercial borrowings,

followed by higher

short-term trade credit. This was mainly due to financing

requirements of Indian

compan i es a r i s i ng on accoun t o f t echno l og i ca l

upgr ada t i on and capac i t y

expan sion . Fu rth erm ore, ou t of th e in creas e of US $

51.5 billion in externa l

debt during the year 2007-08, valuation effect ref lect ing the

depreciat ion of the

Table 6 1 : Indias Exte rnal De bt

(US $ million)

Item En d- En d- En d- En d- En d- En d- En d-Ma rch Ma rch Ma

rch J u n e Sept. Dec. Ma rch

2005 2006 2007 2007 2007 2007 2008

1 2 3 4 5 6 7 8

1. Mu lt ila tera l 31 ,744 32 ,620 35,337 36,058 37,068 37,944

39,312

2. Bila tera l 17 ,034 15 ,761 16,061 15,841 16,774 17,269

19,613

3. In tern a tion a l Mon eta ry Fu n d 0 0 0 0 0 0 0

4. Tra de Cred it (a bove 1 yea r) 5 ,022 5,420 7,051 7,441

8,202 8,887 10,267

5. Extern a l Com m ercia l Bor rowin gs 2 6,405 26,452 41,657

47,918 52 ,123 57,012 62,0 19

6. NRI Dep os it 32 ,743 36 ,282 41,240 42,603 43,679 43,034

43,672

7. Ru p ee Deb t 2 ,302 2,059 1,947 2,023 2,071 2,097 2,016

8. Lon g-term (1 to 7) 115 ,250 118,594 143,29 3 15 1,884

159,917 166,2 43 17 6,899

9. Sh or t-term 17,723 19 ,539 26,376 28,295 33,276 38,229

44,313

Tota l (8+9) 132 ,973 13 8,13 3 1 69,6 69 1 80,179 193,193

204,47 2 221 ,212

Memo : (p er cen t )

Tota l d ebt / GDP 1 8.6 1 7.2 17 .8 .. .. . . 18 .8

Sh ort -term / Tota l deb t 13 .3 14 .1 15.5 1 5.7 17 .2 18 .7

20.0

Sh ort -term d ebt / Reserves 12 .5 12 .9 13.2 1 3.3 13 .4 13.9

14.3

Con ces s ion a l deb t/ Tota l deb t 30 .9 28 .6 23.3 2 1.9 21

.1 20 .2 19.9

Reserves / Tota l deb t 106.4 109.8 117.4 118.4 128.2 134.6

140.0

Debt Service Ra tio 6 .1 9 .9 4 .8 4 .6 5 .6 5 .9 5 .4

.. : Not available.

-

8/14/2019 The External Economy

12/15

9 7

The Externa l Economy

US do l l a r aga i ns t o t he r ma j o r i n t e r na t i ona

l cu r r enc i es and I nd i an r upee

accou n ted for US $ 9 .9 billion of th e in creas e. Su pp

liers credits u p to 1 80

days maturi ty and investment by foreign inst i tut ional

investors in short- term

debt ins t ruments have been included in shor t - term debt of

India for the per iods ince March 2005. The shor t - term debt outs

tanding increased to US $ 44.3

billion at end-March 2008 from US $ 26.4 billion at end-March

2007, accounting

for 34.8 per cent of the total increase in external debt . The

US dollar remained

the leading curren cy in which In dias external debt was denom

ina ted, accoun ting

for about 57.1 per cent of total debt .

Debt sustainabil i ty indicators remained at comfortable levels

during 2007-

08. The external debt to GDP rat io rose to 18.8 per cent at

end-March 2008

from 17.8 per cent at end-March 2007; this rat io was 30.8 per

cent at end-March 1995. The debt service rat io was placed at 5 .4

per cent dur ing 2007-08

as agains t 4.8 per cent dur ing 2006-07. Ref lect ing the r i

se in shor t term debt

dur ing 2007-08, the rat io of shor t - term to total debt and

shor t term debt to

reserves in creas ed to 20 .0 per cent an d 14.3 per cent ,

respectively. In dias

foreign exchange reserves exceeded the external debt by US $

88.5 bil l ion

providing a cover of 140.0 per cent to the external debt s tock

at end-March

2008.

Inte rnat ional Inves tm ent Posi t ion

In dias n et in tern at ion al liabilities in crea sed by US $

11 .6 billion b etween

end-March 2007 and end-December 2007, as the increase in in

terna t ional

liabilities (US $ 98.0 billion) exceeded the increase in

international assets (US $

86.4 billion) (Table 62). Whereas the increase in international

liabilities was

mainly on account of increased inflows under external commercial

borrowings,

foreign direct investment and portfolio investment, the increase

in international

assets was at t r ibuted to the increase in reserve assets and

di rect inves tment

ab road . Th e ma jor part of coun trys externa l fin an cial

assets wa s in th e form

of reserve assets constituting around 83.0 per cent, followed by

direct investment

an d other investm ent a ccou nting for 11.7 per cent a nd 5.1

per cent , respectively,

at en d-December 2 007 . Arou n d 44 .1 per cent of coun trys

externa l fin an cial

liabilities were in the form of other investment in India (trade

credits, loans,

currency and deposits and other liabilities), followed by

portfolio investment at

30.7 per cent and di rect inves tment at 25.2 per cent .

-

8/14/2019 The External Economy

13/15

9 8

Macroeconomic an d Monetary Developmen ts : Fi rs t Qu ar ter

Review 2008 -09

Developmen ts during 200 8-09

Accordin g to DGCI&S d ata , In dias m ercha n dise exports

p osted a growthof 21.7 per cent during April-May 2008 (24.2 per

cent during April-May 2007).

Impor ts grew at 31.8 per cent as compared wi th 37.9 per cent a

year ago.

Petroleu m , oil an d lu brican ts (POL) im ports grew by 48.6

per cent du ring April-

May 2008 as against 25.7 per cent in April-May 2007, largely due

to the spurt

in international crude oil prices. Non-oil imports at US $ 32.3

bil l ion recorded

a growth of 24.6 per cent (43.8 per cent a year ago).

Merchandise trade defici t

Table 6 2 : Int ernation al Inve stm en t Posit ion of India

(US $ billion )

Item March March J u n e Septem ber Decem ber

2 00 6 PR 2 00 7 PR 20 07 PR 2007P 2007P

1 2 3 4 5 6A. Ass ets 1 8 4 .0 2 4 5 .3 2 6 1 .4 2 9 9 .8 3 3 1

.7

(2 2 .9 ) (2 5 .8 ) . . . . . .

1. Direct In ves tm en t 15 .9 2 9.4 3 4.0 35.4 38.9

2 . Por tfolio In ves tm en t 1 .0 0 .8 0 .8 0 .6 0 .6

2 .1 Equ ity Secu r it ies 0 .5 0 .4 0 .4 0 .4 0 .4

2 .2 Deb t s ecu rit ies 0 .5 0 .4 0 .4 0 .2 0 .2

3 . Oth er In ves tm en t 15 .5 1 5.9 13 .2 16.0 1 6.9

3 .1 Trad e Credits -0 .3 0 .6 -1 .0 1 .2 2 .4

3 .2 Loan s 2 .4 3 .0 2 .0 3 .8 3 .1

3 .3 Cu rren cy a n d Depos its 1 0 .0 8 .1 8 .1 6 .6 6 .9

3 .4 Oth er Assets 3 .4 4 .2 4 .1 4 .4 4 .5

4 . Res erve Ass ets 151.6 199.2 213.4 247.8 2 75.3(18 .9) (20

.9) . . . .

B. Liabilit ie s 2 4 3 .7 3 0 7 .7 3 4 1 .7 3 7 2 .5 4 0 5

.6

(3 0 .4 ) (3 2 .4 ) . . . . . .

1. Direct In ves tm en t 52 .4 7 6.2 88.1 94.4 102.4

(6 .5) (8 .0) . . . . . .

2 . Por tfolio In ves tm en t 64 .2 7 9.5 93.8 108 .5 124 .5

(8 .0) (8 .4) . . . . . .

2 .1 Equ ity Secu rit ies 5 4 .7 63.3 75.2 88.2 103.5

2 .2 Deb t s ecu rit ies 9 .5 16 .1 18.6 20 .3 21.0

3 . Oth er In ves tm en t 127.1 152.0 159.8 169.6 1 78.7

(15 .8) (16 .0) . . . . . .

3 .1 Trad e Credits 21 .2 2 7.7 29 .1 32.4 3 6.13 .2 Loa n s 68

.0 8 0.9 8 5.7 9 0.9 97.2

3 .3 C u rren cy a n d Dep os it s 37 .3 42.3 4 3.8 44.8 4

4.1

3 .4 Oth er Lia bilit ies 0 .6 1 .1 1 .2 1 .5 1 .3

C. Net Pos it ion (A-B) -5 9 .7 -6 2 .4 -8 0 .3 -7 2 .7 -7 3

.9

(-7 .4) (-6 .6) . . . . ..

PR: Pa rtia lly Revised . P: Provis ion a l. .. : Not a va ila b

le.

Note: Figur es in paren theses are percentages to GDP.

-

8/14/2019 The External Economy

14/15

9 9

The Externa l Economy

Table 6 3 : Indias Merch andis e Trade

(US $ billion )

Item 2006-07 2007-08 2007-08 2008-09

April-May

1 2 3 4 5

Exports 126.4 159.0 2 3.1 28.2

Im p orts 1 85.7 23 9.7 37 .1 48.8

Oil 57 .1 79 .6 11.1 16 .5

Non -oil 128 .6 160 .0 26 .0 32.3

Tra de Ba la n ce -59 .4 -8 0 .7 -13 .9 -20 .7

Non -Oil Tra de Ba la n ce -20 .9 -25 .9 -7 .1 ..

Variation (per cen t)

Exports 22 .6 2 5.8 2 4.2 21.7

Im ports 2 4 .5 2 9.0 37.9 31.8

Oil 30 .0 39 .4 2 5.7 48.6

Non -oil 22 .2 24 .4 4 3.8 24.6

.. : Not Available.

Source : DGCI&S.

during April-May 2008 increased to US $ 20.7 billion from US $

13.9 billion a

year ago (Table 63).

Available information on capital flows indicates that the strong

momentum

observed in FDI inf lows dur ing the year 2007-08 cont inued dur

ing 2008-09 so

far, with inflows during April-May 2008 amounting to US $ 7.7

billion. In respect

of FIIs, h owever, th ere were n et ou tflows of US $ 5 .6 b

illion u p to J u ly 11 ,

2008. NRI deposits recorded net inflows of US $ 292 million

during April-May

2008 as against net outf lows of US $ 559 mill ion during

April-May 2007 (see

Table 60).

As on J u ly 18, 200 8, In dias foreign excha n ge reserves a m

oun ted to US $

307.1 billion, showing a decline of US $ 2.6 billion over

end-March 2008 level,

on account of the decrease in foreign currency assets and the

decl ine in the

value of gold. As at end-May 2008, the outstanding net forward

purchases of

US dollar by the Reserve Bank were US $ 15.5 billion (Table

64).

Th e overal l ap proach to th e m an agemen t of In dias foreign

exch an ge

reserves in recent years reflects the changing composit ion of

the balance of

payments and the liquidity risks associated with different types

of flows and

other r equ iremen ts. Taking thes e factors in to accou n t, In

dias foreign excha n ge

reserves continued to be at a comfortable level and consistent

with the rate of

growth, the size of external sector in the economy and the size

of r isk-adjusted

capital flows.

-

8/14/2019 The External Economy

15/15

1 00

Macroeconomic an d Monetary Developmen ts : Fi rs t Qu ar ter

Review 2008 -09

Table 6 4 : Foreign Exchange Reserves

Mem o :

Mon th Gold SDR Foreign Res erve Tota l Ou ts ta n din g Net

Cu rren cy Pos it ion (2+3+4+5) Forwa rd Sa les (-) /

Assets in th e IMF Pu rch a se (+) of USdollar by the

Reserve

Bank a t the end

of the m onth

1 2 3 4 5 6 7

Ma rch 2000 2,974 4 35,058 658 38 ,694 (-) 67 5

Ma rch 2 005 4 ,5 00 5 135,5 71 1 ,438 141 ,514 -

Ma rch 2 006 5 ,7 55 3 145,108 756 151,622 -

Ma rch 2 007 6 ,7 84 2 191,924 469 199,179 -

April 2 007 7 ,03 6 11 196,899 463 204,409 -

Ma y 2 007 6,911 1 200,697 459 208,068 -

J u n e 2 00 7 6 ,787 1 206,114 460 213 ,362 -

J u ly 2 00 7 6,887 12 219,753 455 227,107 -

Au gu s t 20 07 6 ,881 2 221,509 455 228 ,847 -

Septem ber 20 07 7 ,367 2 239,955 438 247 ,762 -

October 2 00 7 7,811 13 256,427 441 26 4,6 92 (+) 4 ,9 90

Novem b er 20 07 8,357 3 264,725 435 27 3,5 20 (+) 7 ,5 53

Decem ber 20 07 8,328 3 266,553 432 27 5,3 16 (+) 8 ,2 38

J a n u a ry 2 00 8 9,199 9 283,595 437 29 3,24 0 (+) 1 6 ,6

29

Febru a ry 2 00 8 9,558 - 291,250 427 30 1,23 5 (+) 1 6 ,1

78

Ma rch 200 8 10,039 1 8 299 ,23 0 436 30 9,72 3 (+) 1 4 ,7

35

April 20 08 9,427 1 8 304 ,22 5 485 31 4,15 5 (+) 1 7 ,0 95

Ma y 2 008 9,202 11 30 4,8 75 526 31 4,61 4 (+) 1 5 ,4 70

J u n e 2 00 8 9,208 11 302,340 528 312,087 ..

J u ly 2008* 9,20 8 11 297,371 517 307,107 ..

* : As on J uly 18, 2008 .

(US $ million)