Embed Size (px)

Citation preview

パーソナルファイナンス研究No.3

55

The Financial Activities of Households, and US Financial Institutions

Abstract Households’ financial transactions have been increasing in recent years. In the United States, the

household as a fund raiser has increased borrowing in the forms of mortgages and consumer credit.

Households, as asset holders, own a great deal of stocks and real estate, such as housing. The borrowing

of households has become greatly affected by their asset value fluctuation, as financial instruments by

which to borrow against the collateral assets held by households have become more popular in recent

years.

US financial institutions have been expanding their financial business in those areas that target house-

holds. Financial institutions have increased lending to households, while expanding the volume of target

customers and the auspices of loan collateral. At that time, financial institutions attempted to reduce their

credit risk by using securitization; however, the credit cost of US financial institutions increased rapidly

during the 2008 financial crisis. In looking at its content, credit cost increased rapidly—not only with

respect to mortgages, but also in other areas, such as credit cards. To date, financial institutions have

applied credit risk management to each distinct loan product; however, at the time of the financial crisis,

increased credit risk with respect to mortgages (i.e., due to the decrease in housing prices) also affected

credit risk with respect to credit cards and other products. As such, the risk management undertaken by

financial institutions—which has previously been done through the use of traditional financial instru-

ments and business lines—may have become insufficient. Overall, I do believe that financial institutions

require an integrated risk management strategy with respect to the financial transactions of households

and individuals.

Shinichiro MaedaMeijo University

56

パーソナルファイナンス研究No.3

1 Introduction

Does an expansion in household financial activity in-

crease macro-level financial instability? The finance busi-

ness, in catering to an unspecified number of households

or individuals, has developed into a stable profit source

for financial institutions.1 That financial business tar-

geting households has promoted a small amount of risk

dispersion, although its cost is high. However, since the

2008 global financial crisis—which presumably stemmed

from subprime mortgages in the United States—the busi-

ness results of financial institutions have largely wors-

ened, not only in the United States, but internationally.2

A home mortgage loan is a loan made at the household or

individual level, and US commercial banks have pushed

and promoted home mortgage loans since approximately

the 1930s.3 In addition, the securitization of home mort-

gages has been pushed since the 1970s, and the results

of that push are only manifesting now.4 The financial

development and innovation of management methods

helped expand financial activities at the household level;

on the other hand, we can also see qualitative changes

in the financial activities of households. In this study, I

analyze the influence that changes to and expansion in fi-

nancial activities among US households have had on the

management of financial institutions, within the context

of the outbreak of the financial crisis. I want to clarify

the relationship seen, even today, between households

and financial institutions, by analyzing the influence of

increased financial activity among US households on the

management of financial institutions.

Financial activities of US household

2. 1 Money flows of US households

Let us look at the financial behavior of US households,

by examining macro-level data. The US household sec-

tor saw a funding surplus (net lending), mainly until the

late 1990s. However, the household sector saw a lack

of funding (net borrowing) in both the 2000–2003 and

2005–2006 periods (Figure 1). The US household sector

again saw a funding surplus after the 2008 financial cri-

sis, as the financial institutions reduced their loans and

households repaid their debts. The money flows of US

households have fluctuated in recent years; in addition,

the household sector has not always seen a financial sur-

plus.

Figure 1 Net lending or borrowing in the United States(as a percentage of GDP, 1946–2015)

2

57

The Financial Activities of Households, and US Financial Institutions

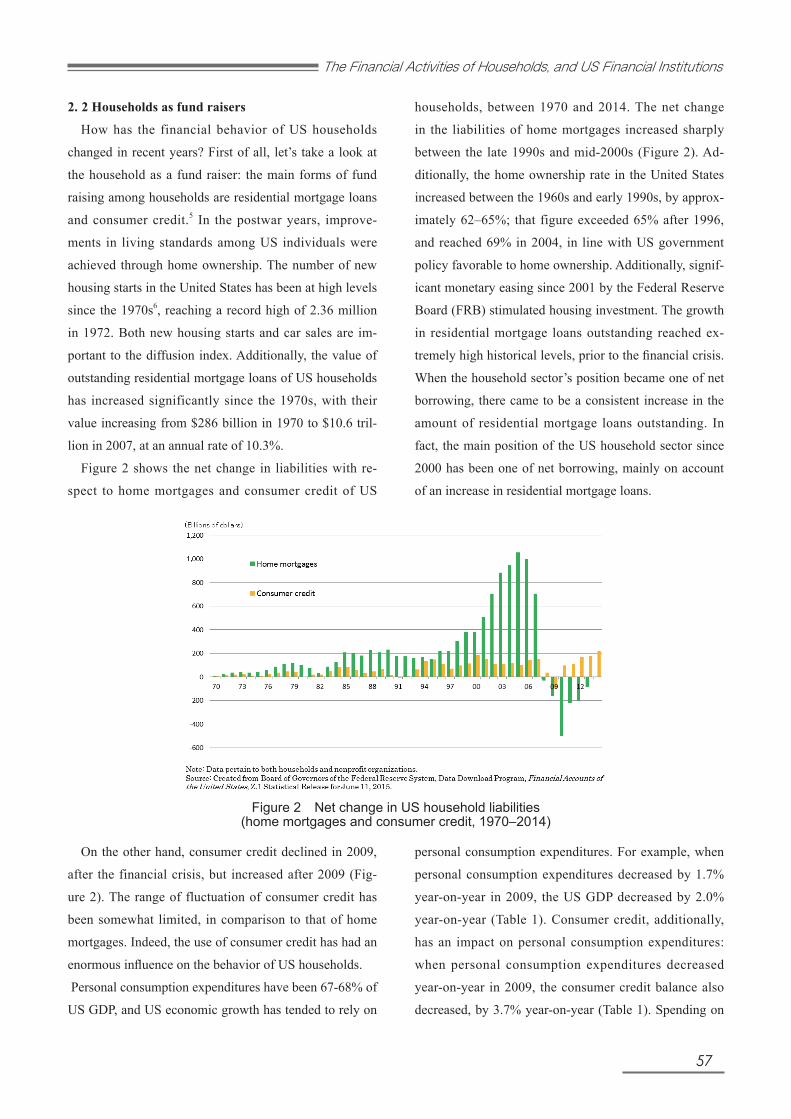

Figure 2 Net change in US household liabilities(home mortgages and consumer credit, 1970–2014)

2. 2 Households as fund raisers

How has the financial behavior of US households

changed in recent years? First of all, let’s take a look at

the household as a fund raiser: the main forms of fund

raising among households are residential mortgage loans

and consumer credit.5 In the postwar years, improve-

ments in living standards among US individuals were

achieved through home ownership. The number of new

housing starts in the United States has been at high levels

since the 1970s6, reaching a record high of 2.36 million

in 1972. Both new housing starts and car sales are im-

portant to the diffusion index. Additionally, the value of

outstanding residential mortgage loans of US households

has increased significantly since the 1970s, with their

value increasing from $286 billion in 1970 to $10.6 tril-

lion in 2007, at an annual rate of 10.3%.

Figure 2 shows the net change in liabilities with re-

spect to home mortgages and consumer credit of US

households, between 1970 and 2014. The net change

in the liabilities of home mortgages increased sharply

between the late 1990s and mid-2000s (Figure 2). Ad-

ditionally, the home ownership rate in the United States

increased between the 1960s and early 1990s, by approx-

imately 62–65%; that figure exceeded 65% after 1996,

and reached 69% in 2004, in line with US government

policy favorable to home ownership. Additionally, signif-

icant monetary easing since 2001 by the Federal Reserve

Board (FRB) stimulated housing investment. The growth

in residential mortgage loans outstanding reached ex-

tremely high historical levels, prior to the financial crisis.

When the household sector’s position became one of net

borrowing, there came to be a consistent increase in the

amount of residential mortgage loans outstanding. In

fact, the main position of the US household sector since

2000 has been one of net borrowing, mainly on account

of an increase in residential mortgage loans.

On the other hand, consumer credit declined in 2009,

after the financial crisis, but increased after 2009 (Fig-

ure 2). The range of fluctuation of consumer credit has

been somewhat limited, in comparison to that of home

mortgages. Indeed, the use of consumer credit has had an

enormous influence on the behavior of US households.

Personal consumption expenditures have been 67-68% of

US GDP, and US economic growth has tended to rely on

personal consumption expenditures. For example, when

personal consumption expenditures decreased by 1.7%

year-on-year in 2009, the US GDP decreased by 2.0%

year-on-year (Table 1). Consumer credit, additionally,

has an impact on personal consumption expenditures:

when personal consumption expenditures decreased

year-on-year in 2009, the consumer credit balance also

decreased, by 3.7% year-on-year (Table 1). Spending on

58

パーソナルファイナンス研究No.3

both durable consumer goods and nondurable consumer

goods decreased year-on-year in 2009. Purchases of cars

in consumer durables spending, for example, has tended

to be contingent on the use of consumer credit.7 As such,

consumer credit trends are thought to affect personal con-

sumption expenditures.

6

Table 1. US personal consumption expenditures and consumer credit balance (2005–2014)

(Billions of dollars)2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

GDP 13,094 13,856 14,478 14,719 14,419 14,964 15,518 16,155 16,663 17,348 y-y (%) 6.7 5.8 4.5 1.7 -2.0 3.8 3.7 4.1 3.1 4.1 Personal consumption expenditures 8,794 9,304 9,750 10,014 9,847 10,202 10,689 11,051 11,392 11,866 y-y (%) 6.5 5.8 4.8 2.7 -1.7 3.6 4.8 3.4 3.1 4.2 the ratio to GDP (%) 67.2 67.1 67.3 68.0 68.3 68.2 68.9 68.4 68.4 68.4 Durable goods 1,127 1,156 1,185 1,102 1,023 1,071 1,125 1,192 1,238 1,280 y-y (%) 4.4 2.6 2.5 -6.9 -7.2 4.6 5.1 5.9 3.9 3.4 Nondurable goods 1,953 2,080 2,177 2,273 2,175 2,292 2,471 2,547 2,599 2,668 y-y (%) 7.3 6.5 4.7 4.4 -4.3 5.4 7.8 3.1 2.0 2.7 Services 5,714 6,068 6,389 6,638 6,649 6,839 7,093 7,312 7,556 7,918 y-y (%) 6.6 6.2 5.3 3.9 0.2 2.9 3.7 3.1 3.3 4.8

Consumer credit 2,321 2,461 2,615 2,650 2,552 2,647 2,755 2,923 3,099 3,317 y-y (%) 4.5 6.1 6.2 1.3 -3.7 3.7 4.1 6.1 6.0 7.1

Source: Created from Board of Governors of the Federal Reserve System, Financial Accounts of the United States, Flow of Funds, Balance Sheets, andIntegrated Macroeconomic Accounts, Historical Annual Tables 1995―2004, Historical Annual Tables 2005―2014 (data for March 12, 2015 andDecember 10, 2015). In modern times, there have been two major changes in the financial activities of US households, from the viewpoint of consumer credit. One is the rapid expansion of, and subsequent reduction in, home equity loans. Home equity loans are loans secured by residential properties, for purposes other than the purchase of a house (i.e., first-mortgage loans). Normally, second-mortgage loans are secured by residential properties, and loans are secured by net housing assets (=present value of the house – unpaid balance of the mortgage). Therefore, home equity loans tend to be used when housing prices increase. The value of outstanding home equity loans increased from $214.7 billion in 1990 to $1,133.2 billion in 2007—the highest such figure to date (Table 2). The value of outstanding home equity loans began to decrease after the financial crisis, to $673.0 billion in 2014 (Table 2). Home equity loans are used to secure consumption, rather than housing investment; in fact, borrowing secured by housing—such as home equity loans—has a push-up effect on consumption expenditures 8 . Therefore, in modern times, we are no longer able to accurately understand behavioral changes among households solely by tracking consumer credit trends. The second major change in the financial activities of US households has been the expansion of student loans in consumer credit. According to FRB statistics, the amount of student loans has been disclosed since 2006, and the value of total outstanding student loans increased from $517.2 billion in 2006, to $1,230.1 billion in 2014, at an annual rate of 11.4%. As the value of outstanding auto loans and credit card loans in

Table 1 US personal consumption expenditures and consumer credit balance (2005–2014)

In modern times, there have been two major changes

in the financial activities of US households, from the

viewpoint of consumer credit. One is the rapid expan-

sion of, and subsequent reduction in, home equity loans.

Home equity loans are loans secured by residential prop-

erties, for purposes other than the purchase of a house

(i.e., first-mortgage loans). Normally, second-mortgage

loans are secured by residential properties, and loans

are secured by net housing assets (=present value of the

house – unpaid balance of the mortgage). Therefore,

home equity loans tend to be used when housing prices

increase. The value of outstanding home equity loans

increased from $214.7 billion in 1990 to $1,133.2 billion

in 2007—the highest such figure to date (Table 2). The

value of outstanding home equity loans began to decrease

after the financial crisis, to $673.0 billion in 2014 (Table

2). Home equity loans are used to secure consumption,

rather than housing investment; in fact, borrowing se-

cured by housing—such as home equity loans—has a

push-up effect on consumption expenditures.8 Therefore,

in modern times, we are no longer able to accurately un-

derstand behavioral changes among households solely by

tracking consumer credit trends.

The second major change in the financial activities of

US households has been the expansion of student loans

in consumer credit. According to FRB statistics, the

amount of student loans has been disclosed since 2006,

and the value of total outstanding student loans increased

from $517.2 billion in 2006, to $1,230.1 billion in 2014,

at an annual rate of 11.4%. As the value of outstanding

auto loans and credit card loans in 2014 was $957.8 bil-

lion and $890.0 billion respectively, student loans now

constitute the greatest proportion of the balance of con-

sumer credit (Table 2). Historically, in the United States,

consumer credit has proliferated from loans for durable

consumer goods (e.g., car loans) to elsewhere, including

free-to-use credit cards. The contents of consumer credit

have changed significantly in recent years, largely on ac-

count of the rapid expansion of student loans.

59

The Financial Activities of Households, and US Financial Institutions

7

2014 was $957.8 billion and $890.0 billion respectively, student loans now constitute the greatest proportion of the balance of consumer credit (Table 2). Historically, in the United States, consumer credit has proliferated from loans for durable consumer goods (e.g., car loans) to elsewhere, including free-to-use credit cards. The contents of consumer credit have changed significantly in recent years, largely on account of the rapid expansion of student loans.

Table 2. US household liabilities (2005–2014) (Billions of dollars)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Home mortgages (Household sector) 8,913 9,910 10,613 10,580 10,419 9,915 9,696 9,486 9,398 9,397 y-y (%) 13.4 11.2 7.1 -0.3 -1.5 -4.8 -2.2 -2.2 -0.9 0.0 Home equity loans 917 1,068 1,133 1,116 1,033 929 854 770 703 673 y-y (%) 18.2 16.4 6.1 -1.5 -7.4 -10.1 -8.1 -9.8 -8.6 -4.3

Consumer credit 2,321 2,461 2,615 2,650 2,552 2,647 2,755 2,923 3,099 3,317 y-y (%) 4.5 6.1 6.2 1.3 -3.7 3.7 4.1 6.1 6.0 7.1 Credit card loans 857 924 1,002 1,004 916 840 841 846 858 890 y-y (%) 3.9 7.9 8.4 0.2 -8.8 -8.4 0.2 0.6 1.5 3.7 Auto loans 823 785 801 777 719 714 751 809 879 958 y-y (%) 3.2 -4.6 2.1 -3.0 -7.5 -0.8 5.3 7.7 8.6 9.0 Student loans N.A. 517 584 666 760 844 943 1,051 1,142 1,230 y-y (%) - - 12.9 14.0 14.1 11.0 11.7 11.4 8.6 7.8 Other consumer credit 641 235 228 203 157 250 220 217 220 239

Security credit 232 292 326 165 203 278 239 304 339 370 y-y (%) -12.0 25.7 11.4 -49.4 23.2 37.0 -14.1 27.1 11.7 8.9

Home equity loans + Consumer credit 3,238 3,529 3,748 3,766 3,586 3,575 3,609 3,692 3,802 3,990 y-y (%) 8.1 9.0 6.2 0.5 -4.8 -0.3 0.9 2.3 3.0 4.9

Home equity loans + Consumer credit +Security credit 3,470 3,821 4,074 3,931 3,789 3,854 3,848 3,996 4,141 4,360

y-y (%) 6.5 10.1 6.6 -3.5 -3.6 1.7 -0.2 3.9 3.6 5.3

Home mortgages charge-offs N.A. N.A. 32 138 239 186 154 142 92 53 Charge-off ratio (%) - - 0.3 1.2 2.2 1.8 1.5 1.4 0.9 0.5

Note: Other consumer credit includes student loans in 2005. Data of home mortgages charge-offs begin in 2007. Home equity loans and homemortgages charge-offs include data for nonfinancial corporate business and nonfinancial noncorporate business.Source: Created from Board of Governors of the Federal Reserve System, Financial Accounts of the United States, Flow of Funds, Balance Sheets, andIntegrated Macroeconomic Accounts, Historical Annual Tables 1995―2004, Historical Annual Tables 2005―2014 (data for March 12, 2015 andDecember 10, 2015). 2.3. Households as asset holders Next, let us take a look at households as asset holders. Modern households and individuals have tended to hold considerable assets: in 2014, US households held tangible assets and financial assets valued at $29 trillion and $68 trillion, respectively, for a total of $97 trillion in assets. Typical assets held by US households are housing and stock. First, let us look at tangible assets. Real estate held by US households in 2014 was valued at $20.6 trillion; in fact, housing constitutes the majority of tangible assets held by US households. The value of real estate held by US households has continued to

Table 2 US household liabilities (2005–2014)

2. 3 Households as asset holders

Next, let us take a look at households as asset hold-

ers. Modern households and individuals have tended to

hold considerable assets: in 2014, US households held

tangible assets and financial assets valued at $29 trillion

and $68 trillion, respectively, for a total of $97 trillion in

assets. Typical assets held by US households are housing

and stock.

First, let us look at tangible assets. Real estate held by

US households in 2014 was valued at $20.6 trillion; in

fact, housing constitutes the majority of tangible assets

held by US households. The value of real estate held by

US households has continued to increase since the 1960s,

reaching a value of $22.5 trillion in 2006—the highest

such figure to date (Figure 3). The total value of real es-

tate has been in decline since 2007, and since 2011 has

again been on the rise (Figure 3). Since the late 1990s,

real estate prices have increased in line with increases in

the value of home mortgage loans. One should bear in

mind the fact that individuals in the United States buy

housing aggressively, by borrowing: the ratio of the value

of home mortgage loans to that of real estate, which had

been hovering at around 40% around 2006, has increased

rapidly since 2007, finally exceeding 60% during the

2008–2011 period (Figure 3). When real estate prices

began to fall in the late 2000s, the debt burden of US

households became very much apparent.

60

パーソナルファイナンス研究No.3

Figure 3 Real estate and home mortgages of US households (1960–2014)

Figure 4 Financial assets of US households (1945–2014)

Next, let us look at financial assets. In 2014, the fi-

nancial assets held by US households were valued at

$68 trillion—a value equivalent to 2.3 times that of their

tangible assets. Among financial assets held by house-

holds, the value of stocks and investments (corporate

equities + equity in noncorporate business) was $22.7

trillion; that of mutual funds including the money market

mutual funds (MMFs) was $8.9 trillion. The total amount

of stocks, investments, and mutual funds held by house-

holds (i.e., $31.6 trillion) exceeded the $9.1 trillion in de-

posits (excluding the MMFs). When we think of stocks,

investments, and mutual funds as risk assets, we find that

the ratio of risk assets to total US household financial

assets was 47% (Figure 4). It becomes clear, just why an

increase or decrease in financial assets is influenced by

the stock market.

61

The Financial Activities of Households, and US Financial Institutions

2. 4 US households’ asset holding and financial activities

One characteristic of modern US economy is that

households’ consumption activities closely relate to the

assets they hold. In what follows, I attempt to describe

this in terms of the housing and stock held by house-

holds.

Specific examples based on housing are home equity

loans. Statistically, home equity loans are considered

home mortgage loans, as they are secured by housing;

additionally, they are distinguished from consumer credit.

However, funds derived through home equity loans have

primarily been directed toward consumption, rather than

housing investments. There are two types of home equity

loan. One is the traditional loan, which is executed by

contract. The other one is the credit line (or open-ended

type), which can be used multiple times as needed, so

long as the balance remains within lending limits. As the

credit-line type involves borrowing on a revolving basis

and is accessed through an automated teller machine

(ATM), it is materially identical to a credit card. As the

payment of interest is deducted from taxable income in

the case of loans secured by housing, the actual interest

rate is suppressed significantly lower, relative to that for

consumer credit. For this reason, home equity loans are

frequently used as alternative means of consumer credit.

A specific example that is based on stock is securities

backed loans (security credit). In the United States, one

opportunity for individuals to access the equity invest-

ment market came in 1971, with the sale of money mar-

ket mutual funds (MMFs) by securities companies. The

sale of MMFs began to increase explosively with the ad-

vent of cash management accounts (CMAs), which were

developed in 1977 by Merrill Lynch in partnership with

Bank One of Columbus. At that point, individuals could

write checks and use credit cards attached to CMAs;

individuals were also able to receive loans as collateral

securities if the MMF balance were deemed insufficient

at the time of fund settlement. The security credit bal-

ance exceeded $200 billion in 1999, and exceeded $300

billion in 2007 and after 2011 (Table 2). Security credit

is not necessarily used to make securities investments:

today, it is used also to fund consumption. Since the

Gramm–Leach–Bliley (GLB) Act was enacted in 1999,

major securities companies have typically strengthened

the lending business by using deposits of subsidiary

banks. For example, Merrill Lynch has since 2000 incor-

porated the deposits of subsidiary banks into CMA, and

has induced short-term funds from MMFs to deposit cov-

ered by deposit insurance. Merrill Lynch also introduced

in April 2004 the multi-purpose account known as the

loan management account (LMA), which consolidates

more than one security credit. The purpose of introducing

this product was to extend comprehensive management

services to assets and liabilities at the individual level,

to encompass all of their financial assets and liabilities.

The state of the security credit market depends largely on

the price of securities, which are used as collateral. It is

possible for individuals to use security credit for short-

term borrowing, even if they have invested in securities

for long-term purposes. This is a characteristic of the US

market, and it proliferated among individual investors.

Receivers of consumer credit look to obtain credit, based

on future income, to fund consumption expenditures.

Individuals who have available-for-sale assets will find

it bankroll consumption by selling their assets. However,

even if it were necessary for individuals to borrow for

some reason, they can continue to hold assets and carry

out effective asset management by using their held assets

as borrowing collateral.9 As home equity loans are se-

cured by housing, and security credit by securities, both

can be statistically distinguished from consumer credit;

however, their purposes relate to consumption, and they

are also used similarly. We can consider home equity

loans and security credit as comprising consumer cred-

it—in the broad, modern sense—when we pay attention

to consumer credit and how it allows for intertemporal

consumption selection and contributes to the maximiza-

tion of utility among households and individuals. Indeed,

in modern times—at least in the United States—consum-

er credit has expanded while changing its format.

62

パーソナルファイナンス研究No.3

3. 1 US households and US commercial banks

US financial institutions have helped enhance finan-

cial transactions at the household level. For example, the

loan balance composition ratio of consumer lending (i.e.,

the total of consumer credit and home mortgage loans)

is higher than that of corporate lending by US commer-

cial banks.10 There is the factor that, within this context,

households have borrowed to raise funds and built up

their financial assets. US capital markets are well devel-

oped, and commercial banks have historically found it

difficult to expand corporate lending. Commercial banks

have been working to improve credit assessments and

develop financial instruments so as to expand loans made

to individuals; in recent years, those banks have followed

two processes to increase the loans made to households

and individuals.

One such process involves enlarging the circle of

lending target customers—that is, the extension of loans

to relatively low-creditworthy customers (e.g., subprime

loans). Some credit card companies in the United States

also offer loans to relatively low-creditworthy customers.

In the past, regulators have crafted separate regulations

with respect to subprime loans, but those regulations

have not stopped such large-scale problems as the 2008

financial crisis from occurring. Financial institutions need

a new mechanism by which to reduce their credit risk, if

they wish to extend loans to relatively low-creditworthy

individuals. Therefore subprime loans are being made

not only through credit cards, but also in a form collat-

eralized by housing. In the background, subprime loans

through credit cards were strictly regulated by regulators;

when extending loans to low-creditworthy individuals,

financial institutions have been focusing on house prices,

which have continuously increased since 2000.

The second process involved the extension of loan

collateral. Housing loans extended to low-creditworthy

individuals differ from traditional housing loans: in the

former, financial institutions put up as collateral future

increases in housing prices, rather than the present value

of a house. Additionally, home equity loans have also

been extended, based on the net assets of a house (=pres-

ent value of house – unpaid balance of the mortgages).

This serves also as an example of how loan collateral has

expanded.

3. 2 Bank loans and financing

Commercial banks have increased lending to individu-

als, in forms such as home mortgage loans and consumer

credit; they have also extended the loan period. The loan

period of home mortgages is long-term, and the loan pe-

riod of consumer credit, at least in the case of installment

credit, is usually more than one year. The loan period of

commercial banks increases as the composition ratio of

home mortgage loans and consumer credit increases, and

the increase in medium and long-term loans has created

liquidity problems among commercial banks.

The Housing and Urban Development Act of 1968 was

established in the United States, and on account of it, the

federal government has been found to support the secu-

ritization of home mortgage loans held by thrift institu-

tions.11 The Government National Mortgage Association

(GNMA) first issued MBSs in 1970. The Federal Home

Loan Mortgage Corporation (FHLMC) started in 1971

to issue pass-through securities where the monthly prin-

cipal and interest repayment of the mortgage was paid to

security holders. The use of securitization was required,

given the fact that financial institutions need to mitigate

the risk that comes with holding long-term loan receiv-

ables. Commercial banks began to use securitization in

the process of increasing consumer lending: the US home

mortgage loan market, for example, began to expand

rapidly through its use. As a result of the extensive use

of securitization, commercial banks now hold only in the

vicinity of 25% of all home mortgage balances (Table

3); on the other hand, government-sponsored enterprises

(GSEs) such as FNMA ((A) of Table 3) and agency and

GSE-backed mortgage pools ((B) of Table 3) hold the

majority of home mortgages.

3 US households and financial institution management

63

The Financial Activities of Households, and US Financial Institutions

Table 3 Holders of home mortgages in the United States (2005–2014)

3. 3 Profit fluctuations among financial institu-

tions

Since the 1990s, US commercial banks have seen

increasing profit levels (Figure 5). One reason for this

is the expansion of retail finance. Nonetheless, US com-

mercial banks slipped into the red in 2009, following the

financial crisis (Figure 5). The cause of the deficit has

been thought to derive from losses caused by a fall in the

prices of securitized products held in the trading book,

and by general loan losses related to home mortgages.12

Figure 5 Net income and provision for loan and lease losses of US commercial banks (1980–2014)

13

commercial banks increases as the composition ratio of home mortgage loans and consumer credit increases, and the increase in medium and long-term loans has created liquidity problems among commercial banks. The Housing and Urban Development Act of 1968 was established in the United States, and on account of it, the federal government has been found to support the securitization of home mortgage loans held by thrift institutions11. The Government National Mortgage Association (GNMA) first issued MBSs in 1970. The Federal Home Loan Mortgage Corporation (FHLMC) started in 1971 to issue pass-through securities where the monthly principal and interest repayment of the mortgage was paid to security holders. The use of securitization was required, given the fact that financial institutions need to mitigate the risk that comes with holding long-term loan receivables. Commercial banks began to use securitization in the process of increasing consumer lending: the US home mortgage loan market, for example, began to expand rapidly through its use. As a result of the extensive use of securitization, commercial banks now hold only in the vicinity of 25% of all home mortgage balances (Table 3); on the other hand, government-sponsored enterprises (GSEs) such as FNMA ((A) of Table 3) and agency and GSE-backed mortgage pools ((B) of Table 3) hold the majority of home mortgages.

Table 3. Holders of home mortgages in the United States (2005–2014) (Billions of dollars, %)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Home mortgages (Total) 9,421 10,501 11,240 11,154 10,939 10,447 10,201 9,972 9,877 9,881 y-y (%) 13.6 11.5 7.0 -0.8 -1.9 -4.5 -2.4 -2.2 -1.0 0.05 U.S.-chartered depository institutions 2,730 2,934 3,069 2,885 2,693 2,616 2,538 2,504 2,386 2,402 y-y (%) 11.9 7.4 4.6 -6.0 -6.6 -2.9 -3.0 -1.4 -4.7 0.7 The ratio to home mortgages 29.0 27.9 27.3 25.9 24.6 25.0 24.9 25.1 24.2 24.3

454 458 448 457 433 4,691 4,588 4,476 4,546 4,538 (B) Agency- and GSE-backedmortgage pools 3,446 3,749 4,372 4,864 5,267 1,069 1,217 1,322 1,421 1,472

(A)+(B) 3,900 4,207 4,820 5,321 5,700 5,760 5,805 5,798 5,967 6,010 The ratio to home mortgages 41.4 40.1 42.9 47.7 52.1 55.1 56.9 58.1 60.4 60.8

Source: Created from Board of Governors of the Federal Reserve System, Financial Accounts of the United States, Flow of Funds,Balance Sheets, and Integrated Macroeconomic Accounts, Historical Annual Tables 1995―2004, Historical Annual Tables 2005―2014(data for March 12, 2015 and December 10, 2015).

Table 3. Holders of home mortgages in the United States (2005-2014)

Note: Mortgages on 1–4 family properties including mortgages on farm houses. Total of household sector, nonfinancial corporatebusiness and nonfinancial noncorporate business.

3.3. Profit fluctuations among financial institutions Since the 1990s, US commercial banks have seen increasing profit levels (Figure 5). One reason for this is the expansion of retail finance. Nonetheless, US commercial

(A) Government-sponsored enterprises

64

パーソナルファイナンス研究No.3

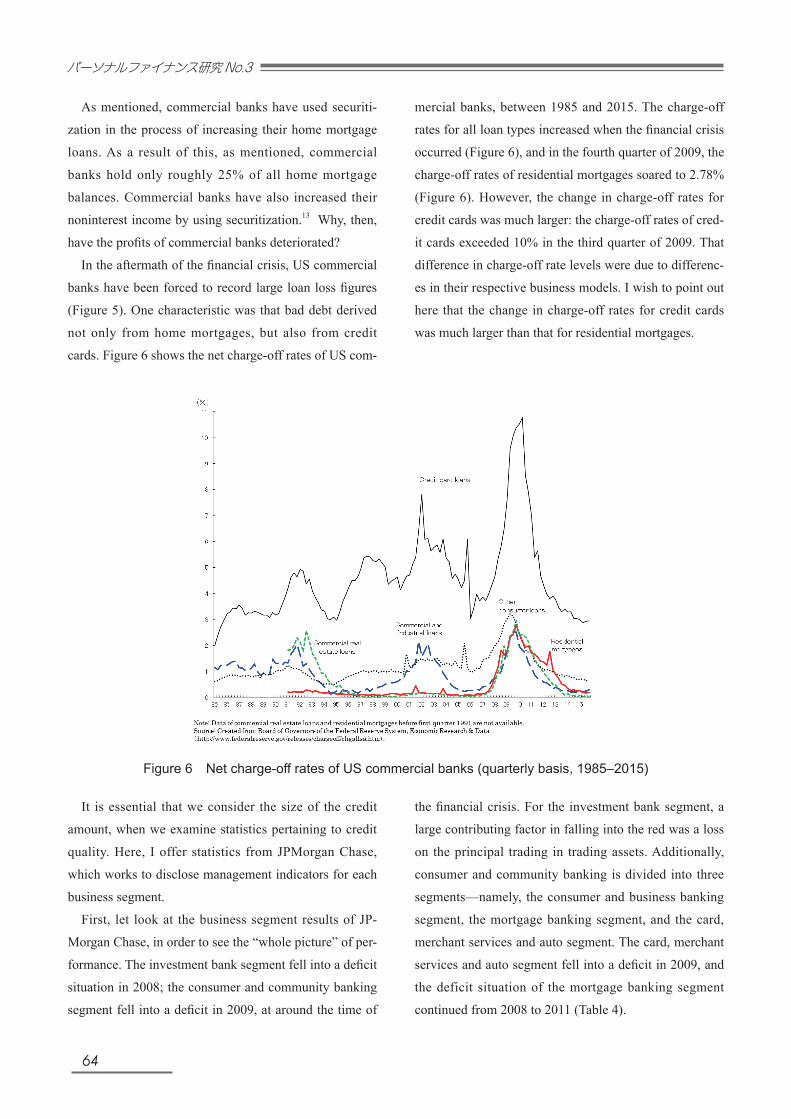

As mentioned, commercial banks have used securiti-

zation in the process of increasing their home mortgage

loans. As a result of this, as mentioned, commercial

banks hold only roughly 25% of all home mortgage

balances. Commercial banks have also increased their

noninterest income by using securitization.13 Why, then,

have the profits of commercial banks deteriorated?

In the aftermath of the financial crisis, US commercial

banks have been forced to record large loan loss figures

(Figure 5). One characteristic was that bad debt derived

not only from home mortgages, but also from credit

cards. Figure 6 shows the net charge-off rates of US com-

mercial banks, between 1985 and 2015. The charge-off

rates for all loan types increased when the financial crisis

occurred (Figure 6), and in the fourth quarter of 2009, the

charge-off rates of residential mortgages soared to 2.78%

(Figure 6). However, the change in charge-off rates for

credit cards was much larger: the charge-off rates of cred-

it cards exceeded 10% in the third quarter of 2009. That

difference in charge-off rate levels were due to differenc-

es in their respective business models. I wish to point out

here that the change in charge-off rates for credit cards

was much larger than that for residential mortgages.

It is essential that we consider the size of the credit

amount, when we examine statistics pertaining to credit

quality. Here, I offer statistics from JPMorgan Chase,

which works to disclose management indicators for each

business segment.

First, let look at the business segment results of JP-

Morgan Chase, in order to see the “whole picture” of per-

formance. The investment bank segment fell into a deficit

situation in 2008; the consumer and community banking

segment fell into a deficit in 2009, at around the time of

the financial crisis. For the investment bank segment, a

large contributing factor in falling into the red was a loss

on the principal trading in trading assets. Additionally,

consumer and community banking is divided into three

segments—namely, the consumer and business banking

segment, the mortgage banking segment, and the card,

merchant services and auto segment. The card, merchant

services and auto segment fell into a deficit in 2009, and

the deficit situation of the mortgage banking segment

continued from 2008 to 2011 (Table 4).

Figure 6 Net charge-off rates of US commercial banks (quarterly basis, 1985–2015)

65

The Financial Activities of Households, and US Financial Institutions

For both the card, merchant services and auto segment

and the mortgage banking segment, the main contribut-

ing factor in falling into the red was an increase in credit

costs. The provision for credit losses in the card, mer-

chant services and auto segment surged to $11.0 billion

in 2008 and $19.6 billion in 2009 (Figure 7). Originally,

the credit card business was highly profitable, but it fell

into a deficit situation in 2009, largely due to huge credit

costs. On the other hand, the provision for credit losses

in the mortgage banking segment increased to $8.6 bil-

lion in 2008 and $13.6 billion in 2009 (Figure 8). What I

want to highlight here is the level of credit cost involved.

The credit amount of credit cards is smaller than that of

home mortgages. As for the loans outstanding of JPMor-

gan Chase as of the end of 2008, those of credit cards

were valued at $104.7 billion, while the sum of home

mortgage loans was $292.6 billion (home equity, $142.9

billion; prime mortgages, $87.0 billion; subprime mort-

gages, $22.1 billion; and option adjustable-rate mortgag-

es (ARMs), $40.6 billion).14 Against this loan amount,

in 2009, the provision for credit losses in the card, mer-

chant services and auto segment was significantly larger

($6.1 billion) than that in the mortgage banking segment,

at the same time that the consumer and community bank-

ing segment had fallen into a deficit (Figures 7 and 8).

The largest contributing factor to the rapid increase in

credit cost was the bad debt burden of credit cards after

the financial crisis, although it is necessary also to take

into consideration differences in accounting standards

among loan products.

Table 4 Business segment results of JPMorgan Chase (2005–2014)

16

mortgage banking segment continued from 2008 to 2011 (Table 4).

Table 4. Business segment results of JPMorgan Chase (2005–2014) (Millions of dollars)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014LINE OF BUSINESS NET INCOMEInvestment Bank 3,673 3,674 3,139 -1,175 6,899 6,639 6,789Retail Financial Services 3,427 3,213 2,925 880 -335 1,728 1,678Card Services & Auto 1,907 3,206 2,919 780 -1,793 2,872 4,544Commercial Banking 951 1,010 1,134 1,439 1,271 2,084 2,367Treasury & Securities Services 863 1,090 1,397 1,767 1,226 1,079 1,204Asset Management 1,216 1,409 1,966 1,357 1,430 1,710 1,592Corporate / Private Equity -3,554 842 1,885 557 3,030 1,258 802Net Income 8,483 14,444 15,365 5,605 11,728 17,370 18,976 21,284 17,923 21,762

Consumer & Community Banking 5,334 6,419 5,844 1,660 -2,128 4,578 6,202 10,791 11,061 9,185 Consumer & Business Banking 2,780 1,922 2,245 2,982 3,915 3,630 3,796 3,224 2,943 3,443 Mortgage Banking 379 945 385 -2,102 -4,250 -1,924 -2,138 3,468 3,211 1,668 Card, Merchant Services & Auto 2,175 3,552 3,214 780 -1,793 2,872 4,544 4,099 4,907 4,074

Source: Created from JPMorgan Chase & Co., Annual Report and Earnings Release Financial Supplement.

Disclosure standards have beenchanged.

Note: Some figures of Consumer & Community Banking segment before 2010 are estimated. The figures of the Retail Financial Services segment before 2009inlcude auto and student loans. The figure of the Card, Merchant Services & Auto segment in 2008 doesn't include auto and student loans, and the figures before2008 don't include student loans. The figure of the Mortgage Banking segment in 2008 includes auto and student loans, and the figures in 2007 and 2006 includestudent loans. The figure of the Consumer & Business Banking segment in 2005 includes a part of mortgage loans and home equity loans.

For both the card, merchant services and auto segment and the mortgage banking segment, the main contributing factor in falling into the red was an increase in credit costs. The provision for credit losses in the card, merchant services and auto segment surged to $11.0 billion in 2008 and $19.6 billion in 2009 (Figure 7). Originally, the credit card business was highly profitable, but it fell into a deficit situation in 2009, largely due to huge credit costs. On the other hand, the provision for credit losses in the mortgage banking segment increased to $8.6 billion in 2008 and $13.6 billion in 2009 (Figure 8). What I want to highlight here is the level of credit cost involved. The credit amount of credit cards is smaller than that of home mortgages. As for the loans outstanding of JPMorgan Chase as of the end of 2008, those of credit cards were valued at $104.7 billion, while the sum of home mortgage loans was $292.6 billion (home equity, $142.9 billion; prime mortgages, $87.0 billion; subprime mortgages, $22.1 billion; and option adjustable-rate mortgages (ARMs), $40.6 billion)14. Against this loan amount, in 2009, the provision for credit losses in the card, merchant services and auto segment was significantly larger ($6.1 billion) than that in the mortgage banking segment, at the same time that the consumer and community banking segment had fallen into a deficit (Figures 7 and 8). The largest contributing factor to the rapid increase in credit cost was the bad debt burden of credit cards after the financial crisis, although it is necessary also to take into consideration differences in accounting standards among loan products.

66

パーソナルファイナンス研究No.3

Figure 7 Provision for credit losses in the card, merchant services and auto segment of JPMorgan Chase (2005–2014)

Figure 8 Provision for credit losses in the mortgage banking segment and the consumer and business banking segment of JPMorgan Chase (2005–2014)

67

The Financial Activities of Households, and US Financial Institutions

Figure 9 Net charge-offs classified by loan products of JPMorgan Chase (2005–2014)

Source: Mitsubishi UFJ Financial Group, MUFG Report 2015(2) disclosure documents 2015 references, p.52.

Looking also at the charge-offs of JPMorgan Chase,

those of the mortgage banking segment increased from

$3.9 billion in 2008 to $8.4 billion in 2009. Within the

mortgage banking segment, the charge-offs of subprime

mortgages increased from $0.9 billion in 2008 to $1.6

billion in 2009, and those of home equity loans surged

from $2.4 billion in 2008 to $4.7 billion in 2009 (Figure

9). The charge-offs of home equity loans were larger than

those of subprime mortgages, due to differences in the

outstanding loans held. When we look at charge-off rates,

we see that those of subprime mortgages rose to 11.9%

in 2009. It is true that among the various loan products

available, the charge-off rates of subprime mortgage were

quite high; however, I want to point out that the charge-

off amount of home equity loans was larger than that of

subprime mortgages, because securitization has been

widely used for subprime mortgages.15

Financial institutions have largely managed credit risk

for each individual product. For example, the exposure

category for retail financials, as per Basel III, is divided

into three categories—namely, residential mortgage,

qualifying revolving retail, and other retail exposures.

Large financial institutions have managed credit risk by

analyzing delinquencies and risk characteristics in each

product category.

Table 5 Exposure category for retail financials, based on Basel III

19

Table 5. Exposure category for retail financials, based on Basel III

Asset classification based on BaselⅢ Explanation

Residential mortgage exposures Including loans for individuals who live in the residential real estatepurchased.

Qualifying revolving retail exposures Including card loans for individuals who meet certain requirements.

Other retail exposures

Including nonbusiness credit exposures for individuals other thanresidential mortgage and qualifying revolving retail exposures and smallcredit exposures for business corporations that do not have obligorratings.

Source: Mitsubishi UFJ Financial Group, MUFG Report 2015 (2 )disclosure documents 2015 references , p.52. However, the increased credit risk in home mortgages—due largely to the decline in housing prices—affected the credit risk in credit cards; credit costs then sharply increased at the time of the financial crisis. A larger amount of charge-offs has occurred in home equity loans than in subprime loans within total home mortgage loans, as households and individuals holding mortgages also concurrently use credit cards and home equity loans. As has been described in this paper, US financial institutions expanded financial transactions at the household level, all while developing new financial products. Credit risk management has differed between home mortgage loans secured by housing, and unsecured credit cards; however, those product borrowers are single individuals. Financial institutions’ means of risk management may become insufficient when they are applied to financial products and business segments as per usual. The management of financial institutions tends to be affected more by the financial activities of households as households expand their financial transactions. I believe financial institutions are facing a need for integrated risk management, in terms of the financial transactions of households and individuals. I also believe that discussion on this point will lead to a reconsideration of the significance of financial services; this will compel us to look at both the assets and liabilities of households and individuals. It is essential that financial institutions further develop management techniques with respect to retail financial services, especially in the aftermath of the financial crisis. 4. Conclusion Financial institutions make economic activity more dynamic, chiefly by offering loans and extending consumer-spending opportunities to a larger circle of households and individuals, including relatively low-creditworthy customers. More individuals who are given credit opportunities should naturally behave to increase their personal utility; nevertheless, individuals may face difficulties when confronting a level of debt that

68

パーソナルファイナンス研究No.3

However, the increased credit risk in home mortgages—

due largely to the decline in housing prices—affected the

credit risk in credit cards; credit costs then sharply increased

at the time of the financial crisis. A larger amount of charge-

offs has occurred in home equity loans than in subprime

loans within total home mortgage loans, as households

and individuals holding mortgages also concurrently use

credit cards and home equity loans. As has been described

in this paper, US financial institutions expanded financial

transactions at the household level, all while developing

new financial products. Credit risk management has differed

between home mortgage loans secured by housing, and

unsecured credit cards; however, those product borrowers

are single individuals. Financial institutions’ means of

risk management may become insufficient when they are

applied to financial products and business segments as per

usual. The management of financial institutions tends to be

affected more by the financial activities of households as

households expand their financial transactions.

I believe financial institutions are facing a need for

integrated risk management, in terms of the financial

transactions of households and individuals. I also believe

that discussion on this point will lead to a reconsideration

of the significance of financial services; this will compel

us to look at both the assets and liabilities of households

and individuals. It is essential that financial institutions

further develop management techniques with respect to

retail financial services, especially in the aftermath of the

financial crisis.

Financial institutions make economic activity more dy-

namic, chiefly by offering loans and extending consum-

er-spending opportunities to a larger circle of households

and individuals, including relatively low-creditworthy

customers. More individuals who are given credit oppor-

tunities should naturally behave to increase their personal

utility; nevertheless, individuals may face difficulties

when confronting a level of debt that exceeds their ability

to repay, if that credit provision is excessive.

Financial institutions do not make loans in consideration

of their own bad debt. However, one of the contributing

factors of the current financial crisis is that financial in-

stitutions are inclined to make certain financial transac-

tions accessible to households and individuals, all in an

attempt to derive greater profits. Global financial institu-

tions have been limited in terms of their scale and scope

of business, by virtue of growing regulation; however,

severe regulation will change the behavior of those fi-

nancial institutions, as they search out their next revenue

source. Financial institutions need to assume the risk re-

lated to obtaining profits; the current financial crisis has

raised the issue of where to find the source of risk taking

and revenue inherent in financial institutions at the micro

level.

*On proceeding with this study, I received a 2013 re-

search grant from Japan Academy of Personal Finance. I

would like to thank all concerned.

4 Conclusion

69

The Financial Activities of Households, and US Financial Institutions

【Notes】

1 Please refer to Maeda, 2014, chapter 5.2 For example, large Japanese financial institu-

tions—such as Mitsubishi UFJ Financial Group,

Sumitomo Mitsui Financial Group, and Mizuho

Financial Group—fell into a consolidated deficit

position in fiscal year 2008.3 In the United States, Federal Housing Adminis-

tration (FHA) insurance was introduced in 1934

to offer public insurance with respect to principal

and interest payments on home mortgage loans.4 The Government National Mortgage Associa-

tion issued the first Mortgage Backed Securities

(MBSs), in 1970. Please refer to Maeda, 2004,

chapter 5.5 In the United States, housing loans have been re-

ferred to as home mortgage loans. 6 Please refer to Maeda, 2014, pp.121–123.7 In the United States, the correlation between du-

rable goods consumption expenditures and con-

sumer credit is high. Please refer to Maeda, 2014,

pp.35–38.8 According to a 2007 paper co-authored by FRB

Greenspan and economists, finances backed by

housing are estimated to have increased personal

consumption expenditures by an annual average

of 1.1% between 1991 and 2000, and by an annu-

al average of 3% between 2001 and 2005 (Green-

span and Kennedy, 2007, p.10).9 In the case of holding assets, if the asset value

increases, the individual is considered to have

consumed more, even when personal income re-

mains unchanged. The effect of the size asset on

consumption expenditures is known as the wealth

effect.10 Please refer to Maeda, 2014, chapter 4, section 3.11 Please refer to Maeda, 2004, p.135.12 As for the cause of the financial crisis, please

refer to Japan Society of Monetary Economics,

2013, chapter 4.

13 Please refer to Maeda, 2014, pp.200–202.14 Please refer to JPMorgan Chase & Co., 2010,

p.69.15 About 75% of the total loan amount of the sub-

prime mortgage loans had been securitized.

Please refer to the International Monetary Fund,

2008, p.59.

【References】

Allen, Franklin and Douglas Gale (2004). “Financial

Fragility, Liquidity, and Asset Prices,” Journal of

the European Economic Association, 2(6), 1015-

1048.

Brunnermeier, Markus K. and Lasse Heje Pedersen

(2009). “Market Liquidity and Funding Liquid-

ity,” Review of Financial Studies, 22(6), 2201-

2238.

Diamond, Douglas W. and Philip H. Dybvig (1983).

“Bank Runs, Deposit Insurance, and Liquidity,”

Journal of Political Economy, 91(3), 401-419.

Diamond, Douglas W. and Raghuram G. Rajan (2005).

“Liquidity Shortages and Banking Crises,” Jour-

nal of Finance, 60(2), 615-647.

Diamond, Douglas W. and Raghuram Rajan (2009). “The

Credit Crisis: Conjectures about Causes and Rem-

edies,” NBER Working Paper, No.14739.

Diamond, Douglas W. and Raghuram G. Rajan (2001).

“Liquidity Risk, Liquidity Creation, and Financial

Fragility: A Theory of Banking,” Journal of Polit-

ical Economy, 109(2), 287-327.

Financial Crisis Inquiry Commission (2011).The Finan-

cial Crisis Inquiry Report: Final Report of the

National Commission on the Causes of the Fi-

nancial and Economic Crisis in the United States,

Official Government Edition, United States of

America.

Greenspan, Alan and James Kennedy (2007). “Sourc-

es and Uses of Equity Extracted from Homes,”

Finance and Economics Discussion Series, Di-

visions of Research & Statistics and Monetary

70

パーソナルファイナンス研究No.3

Affairs, Federal Reserve Board, Washington, D.C.

Hector, Gary (1988). Breaking The Bank: The Decline of

BankAmerica, Little Brown and Company.

Hirtle, Beverly J. and Kevin J. Stiroh (2005). “The

Return to Retail and the Performance of U.S.

Banks,” Federal Reserve Bank of New York Staff

Reports, No.233, 1-37.

Imura, Shinya (2002). Evolution of the American Hous-

ing Finance System, University of Tokyo Press.

(originally written in Japanese)

International Monetary Fund (2008). Global Financial

Stability Report, Containing Systemic Risks and

Restoring Financial Soundness, World Economic

and Financial Surveys, International Monetary

Fund.

Japan Securities Research Institute (2013). Securities

Market in the USA 2013, Japan Securities Re-

search Institute. (originally written in Japanese)

Japan Society of Monetary Economics (2013). Review

of Monetary and Financial Studies, Special Issue

January 2013, Why Financial Crises Occur?:

Frontiers of Monetary and Financial Studies, Ja-

pan Society of Monetary Economics. (originally

written in Japanese)

JPMorgan Chase & Co. (2010). Annual Report 2009.

Maeda, Shinichiro (2004). Successful Retail Strategies

for Financial Services Companies, Toyo Keizai

Inc. (originally written in Japanese)

Maeda, Shinichiro (2014). A Study of Retail Finance

in the United States: Historical Development in

Consumer Credit, Nippon Hyoron Sha Co., Ltd.

(originally written in Japanese)

McDonald, Larry and Patrick Robinson (2009). A Co-

lossal Failure of Common Sense: The Incredible

Inside Story of the Collapse of Lehman Brothers,

Crown Business.

Mian, Atif and Amir Sufi (2014). House of Debt: How

They (and You) Caused the Great Recession, and

How We Can Prevent It from Happening Again,

The University of Chicago Press.

Minsky, Hyman P. (1986). Stabilizing an Unstable Econ-

omy, Yale University Press.

Wolfson, Martin H. (1994). Financial Crises: Under-

standing the Postwar U.S. Experience, Second

Edition, M.E. Sharpe Inc., New York.

Accepted: 31 October 2016