Embed Size (px)

Citation preview

The Financial Crisis: An Actuarial Perspective

Paul EmbrechtsDepartment of Mathematics

Director of RiskLab, ETH Zurich Senior SFI Chair

www.math.ethz.ch/~embrechts

(*)

(*) Rather personal!

Before we start, some words on:

ETH Zurich

RiskLab

swiss:finance:institute

This talk is very much based on the following 2009 RiskLab publication (*):

Catherine Donnelly and Paul Embrechts, The devil is in the tails: actuarial

mathematics and the subprime crisis Astin Bulletin 2010, to appear

(*) It contains more technical details

Mathematics and Financial Crises

• 1987: (October 19, Black Monday) electronic/algorithmic trading, portfolio insurance, Value-at-Risk (VaR), …

• 1995: (Barings Bank) Financial Enginee- ring, off-balance products (derivatives), …

• 1998: (LTCM disaster) normal-based risk management systems (VaR again), leverage, personalities, too big to fail, …

• 2007 - ???: (Subprime Crisis) numerous accusations, main content of this talk!

And since our memory is so short:

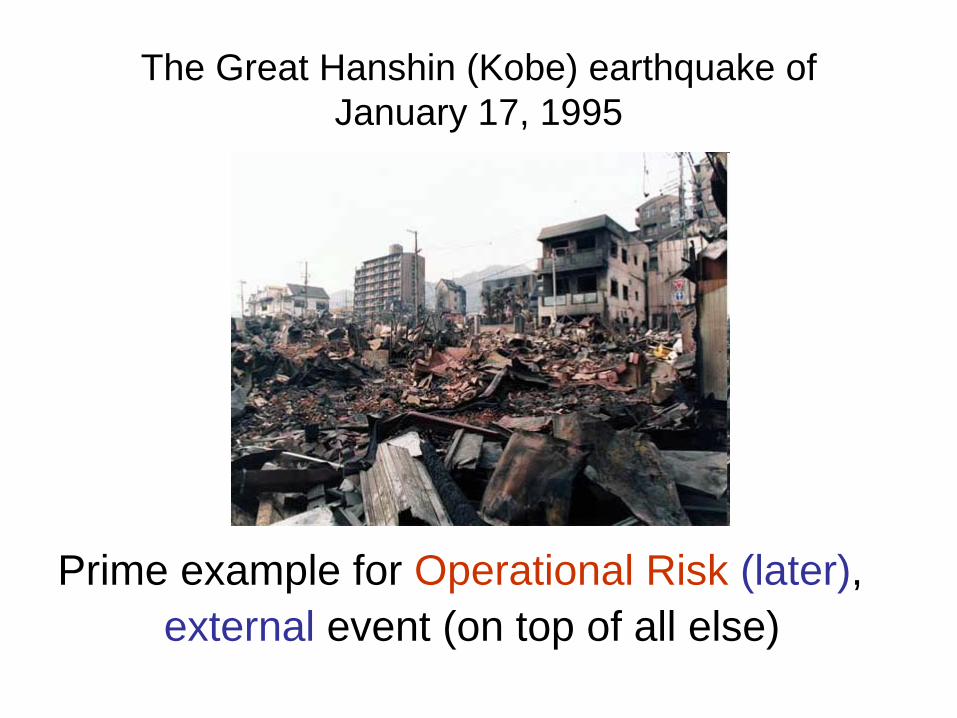

Example 1: February 1995

The Great Hanshin (Kobe) earthquake of January 17, 1995

Prime example for Operational Risk (later),external event (on top of all else)

How Kobe earthquake and a straddle position finally broke the back of Barings bank

Straddle = Short Call and Short Put on Common Strike

Volume of Nikkei Futures

The main ingredients of this example are:

Derivatives: calls, puts, futures, …

“One person can bring the bank down”

Total collapse of Risk Management Functions

And as a result:

Value-at-Risk was introduced through the Amendment to Basel I (more on this later!)

Financial Derivatives: where it all started (*)

• Black, F., and M. Scholes (1973): “The Pricing of Options and Corporate Liabilities,” Journal of Political Economy, 81, 637–654.

• Merton R. C. (1973): “Theory of Rational Option Pricing,” Bell Journal of Economics and Management Science, 4, 141–183.

• However, L. Bachelier (1900), V. Bronzin (1908), E.O. Thorp (1969)!

(*) More interesting question: why then?

A brief answer to the latter question:

1. The end of Bretton-Woods Agreement (1973)

2. The successive oil-shocks (1973 Oil Crisis)

3. Geopolitical instabilities

4. Internationalization & Global Networks

5. Increase in Information Technology

But let us have a very short excursion to the world of derivatives!

Example 2: The Black-Scholes Formula(s)

TdT

TrKSd

TTrKSd

dNSdNeKp

dNeKdNScrT

rT

10

2

01

102

210

)2/2()/ln(

)2/2()/ln(

)()(

)()(

where

Conditions

The Black-Scholes Model and Model Uncertainty

Just waiting for disaster to strike!

And then indeed disaster struck in September 1998

Nobel Prize 1997

March 1998!

But first

By that time we should have learned about:

• (I)liquidity• Leverage• Model Uncertainty• Non-normality, Extreme Events• Regulatory Arbitrage• Off-Balance Positions• Greed, Non-rationality, Human Factors • Accounting Deficiencies• Global Financial Networks• Etc …

Well we didn’t, previous events were justpeanuts compared to the Perfect Stormthat came to us around late 2007, and isstill going on!

Some covers and a cartoon from The Economist

…

Chavez-Demoulin, V., Embrechts, P.: Revisiting the edge, ten years on. To appear in Communications in Statistics - Theory and Methods (2008/9)

Embrechts, P., Resnick, S., Samorodnitsky, G.: Living on the Edge. RISK, January 1998, 96-100.

Humpty Dumpty sat on a wall, Humpty Dumpty had a great fall,

All the King's horses and all the King's men, Couldn't put Humpty together again.

The Economist

March 14, 2008, Bear Stearns …

An early victim:

!!!!!

In the wake of the unfolding Subprime Crisis

others were to follow!

And many more!!!

We not only became very well aware of

Too big to fail

But much more importantly

Too big to save!

And indeed the feeling very much was one of “SOS for the World’s Financial System”:

Or “The scream” of the banker:

“Blame the mathematicians!” (*)

For some it was however clear:

Here are some examples:

(*) financial engineers, quants, …

Recipe for Disaster: The Formula That Killed Wall Street

By Felix Salmon 23 February, 2009 Wired Magazine

Error, )

Maar ook in KNACK Extra, 18/12/2009 (Bewerking Luc Baltussen)

PE, David Li, Pat Brockett and Harry Panjer at Harry’s retirement party at the University of Waterloo April 11, 2008

The Turner ReviewA regulatory response to theglobal banking crisisMarch 2009, FSA, London (126 pages)

1.1 (iv) Misplaced reliance on sophisticated mathsThere are, however, fundamental questions about The validity of VAR as a measure of risk (see Section 1.4 (ii) below). And the use of VAR measures based on relatively short periods of historical observation (e.g. 12 months) introduced dangerous procyclicality into the assessment of trading-book risk for the reasons set out in Box 1A (deficiencies of VAR).

The very complexity of the mathematics used to measure and manage risk, moreover,made it increasingly difficult for top management and boards to assess and exercisejudgement over the risks being taken. Mathematical sophistication ended up not con-taining risk, but providing false assurance that other prima facie indicators of increa-sing risk (e.g. rapid credit extension and balance sheet growth) could be safely ignored.

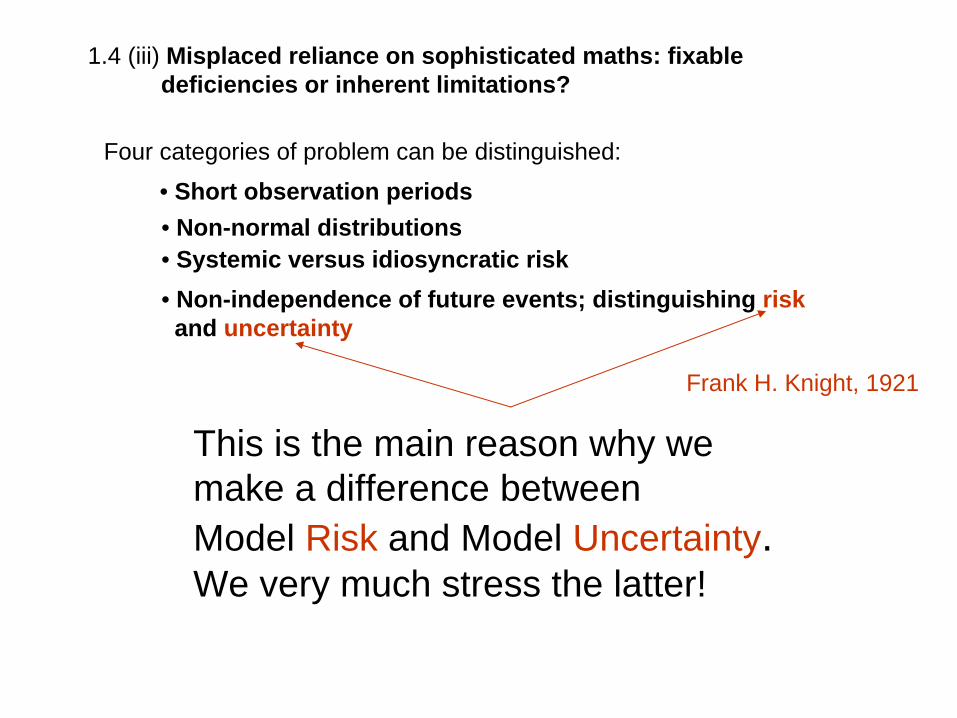

1.4 (iii) Misplaced reliance on sophisticated maths: fixable deficiencies or inherent limitations?

Four categories of problem can be distinguished:

• Short observation periods• Non-normal distributions• Systemic versus idiosyncratic risk• Non-independence of future events; distinguishing risk and uncertainty

This is the main reason why we make a difference between Model Risk and Model Uncertainty. We very much stress the latter!

Frank H. Knight, 1921

The Financial Times:

Of couples and copulas by Sam Jones (April 24, 2009)

In the autumn of 1987, the man who would become the world’s most influential actuary landed in Canada on a flight from China.He could apply the broken hearts maths to broken companies.Li, it seemed, had found the final piece of a risk ma-nagement jigsaw that banks had been slowly piecingtogether since quants arrived on Wall Street.

Why did no one notice the formula’s Achilles heel? Johnny Cash and June Carter

Wall Street’s Math Wizards Forgot a Few Variables,

Steve Lohr, September 12, 2009, NY Times

• From 3 to N Dimensions (mean, variance, …)• Social Networks, Global Networks• Market Psychology, Irrationality, Human Factor • More RM, Less Complex Products• New Frontiers for FE and RM• More Dimensions of Uncertainty• The Adaptive (not Efficient) Market Hypothesis• Understanding of Contagion• …

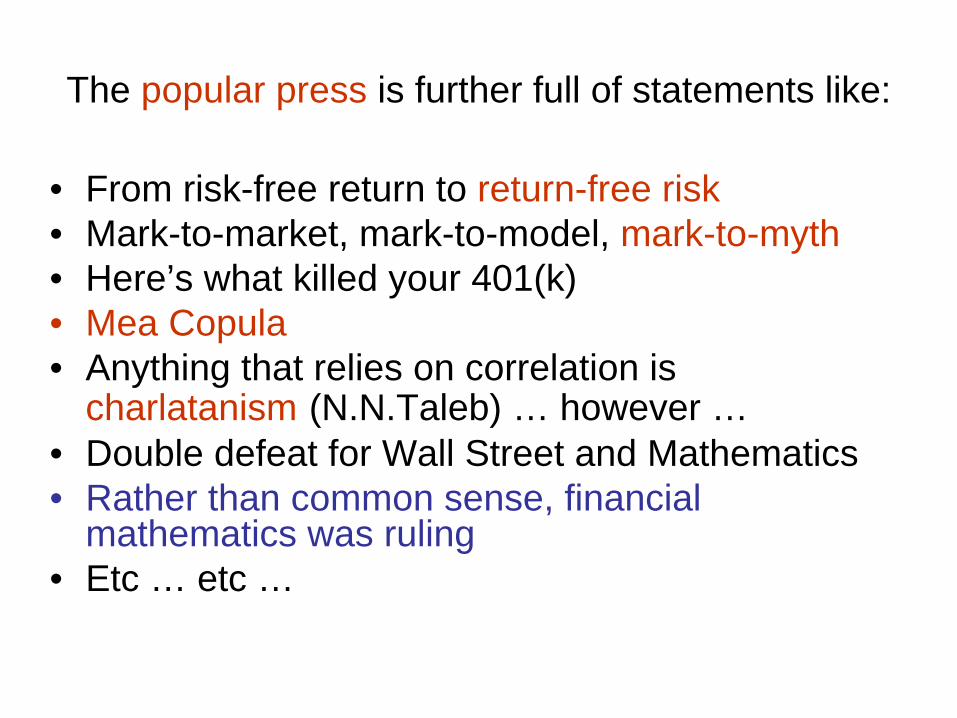

The popular press is further full of statements like:

• From risk-free return to return-free risk• Mark-to-market, mark-to-model, mark-to-myth• Here’s what killed your 401(k)• Mea Copula• Anything that relies on correlation is

charlatanism (N.N.Taleb) … however …• Double defeat for Wall Street and Mathematics• Rather than common sense, financial

mathematics was ruling• Etc … etc …

Others voice their criticism in a somewhat more subtle way:

“With respect to the current economic crisis mathematicians are innocent … and this in both meanings of the word.”

Roger Guesnerie, Collège de France

(Paris, March 20, 2009)

These are rather serious allegations, so let us look at some examples of financial products (*) and

investigate where the mathematics “went wrong”

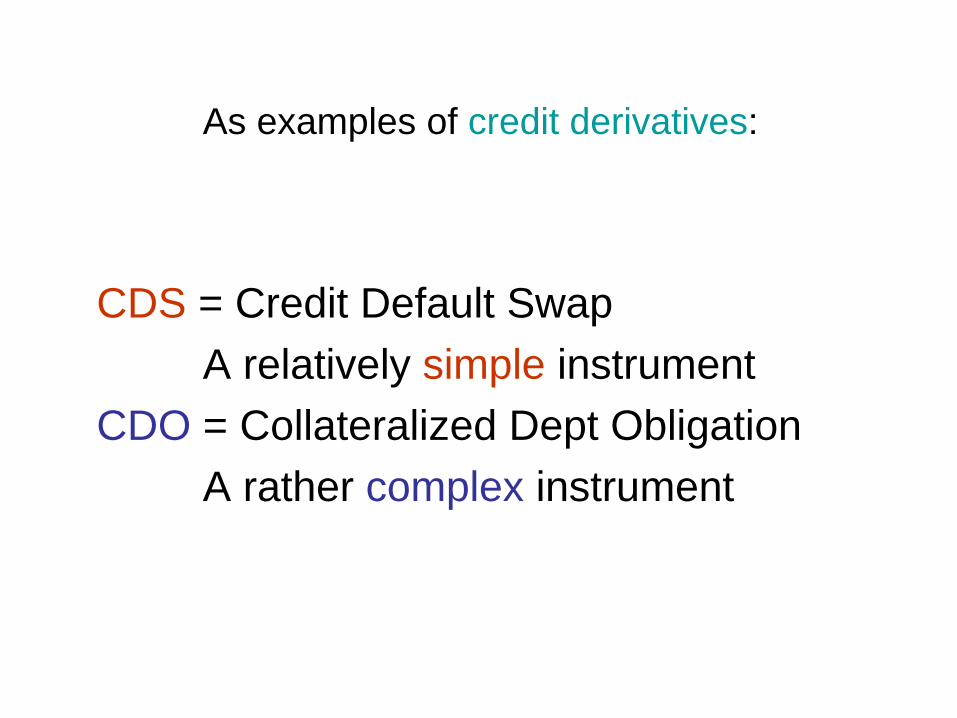

(*) Credit Derivatives

As examples of credit derivatives:

CDS = Credit Default SwapA relatively simple instrument

CDO = Collateralized Dept ObligationA rather complex instrument

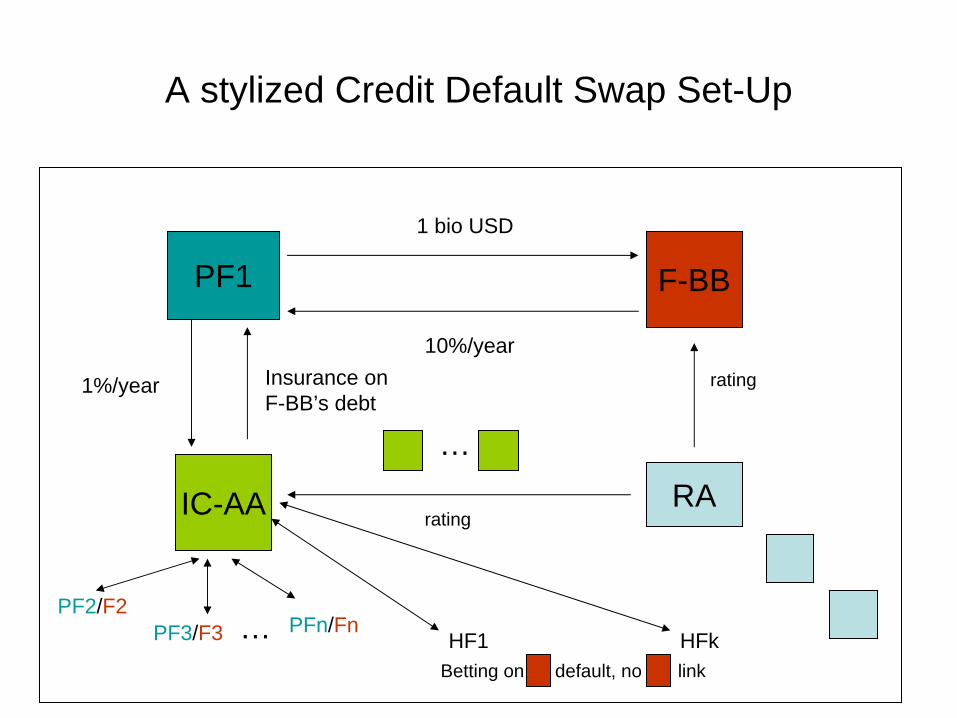

A stylized Credit Default Swap Set-Up

PF1 F-BB

RAIC-AA rating

rating

1 bio USD

10%/year

1%/year Insurance on F-BB’s debt

PF2/F2PF3/F3 PFn/Fn… HF1 HFk

…

Betting on default, no link

A sure road for disaster

• In the previous picture, problems occur if several corporations default at the same time, in that case the insurance companies have to pay, may loose their high rating causing the pension funds (investors) more problems, etc, etc … someone at some time will blame the rating agencies

• But what about the hedge funds … ?• In the end all depends on default correlation …

enters the Gauss-copula and Mr Li.But only marginally!

Complexity, Opacity, Distance,

Greed, Economic

and Political Stupidity,

Regulatory Blindness,

Academic Naivity, and Arrogance

… We are all to blame!

CDOs

Before we say something about pricing, let us first reflect about volume(*), in particular

what order of magnitude are we talking about for these markets?

(*) “Where is all the credit risk hiding?” (+/- 2005)

50 000 000 000 000 $ *• CDS is almost a brand new investment vehicle, but the

market is already 20 times its size in 2000. The principal amount of CDS outstanding equals $50 trillion, or more than three times the U.S. Gross Domestic Product and bigger than all the U.S. credit markets put together. And the CDS has been a huge source of "financial engineering" profits, both for Wall Street and the hedge fund community over the last few years.

• World GDP is about $66 trillion.• First CDS about 1995.• Total nominal volume of OTC derivatives 550 Tri. $

* 3.7 Tri. $ after netting

And yet

“The four most expensive words in investment are ‘This time it’s different’.” (xyz)

Mr Greenspan so described this “New World” in 2002(!):

“The use of a growing array of derivatives and the related application of more sophisticated methods for measuring and managing risk are key factors underpinning the enhanced resilience of our largest financial institutions. As a result, not only have individual financial institutions become less vulnerable to shocks from underlying risk factors, but also the financial system as a whole has become more stable.”

Was it really “A Brave New World for Valuation Methodologies”(Mary Meeker) and “a time to be rationally reckless (*)”?

(*) John Kay (FT, 28/12/09), chiding Mr Greenspan

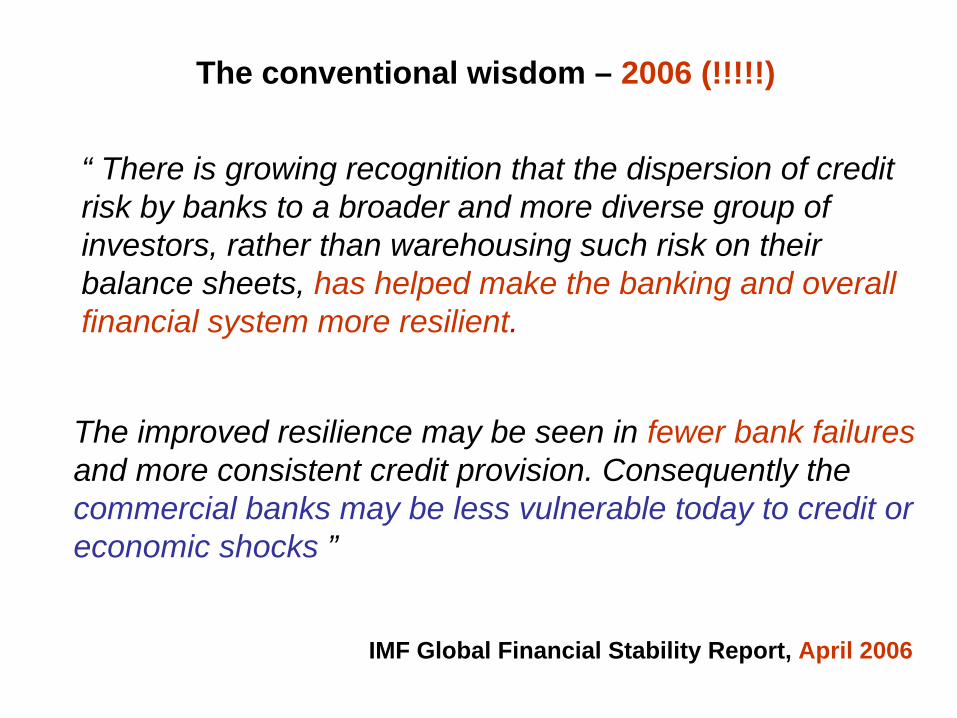

The conventional wisdom – 2006 (!!!!!)

“ There is growing recognition that the dispersion of credit risk by banks to a broader and more diverse group of investors, rather than warehousing such risk on their balance sheets, has helped make the banking and overall financial system more resilient.

The improved resilience may be seen in fewer bank failures and more consistent credit provision. Consequently the commercial banks may be less vulnerable today to credit or economic shocks ”

IMF Global Financial Stability Report, April 2006

This very much clashed with an older (*) view:

(*) Sadly neglected and/or forgotten

Economists’ Voice: www.bwpress.com/ev November, 2008

“I went on to explain how securitization can give rise to perverse incentives …Has the growth in securitization been result of more efficient transactions tech-nologies, or an unfounded reduction in concern about the importance of scree-ning loan applications? … we should at least entertain the possibility that it isthe latter rather than the former.”

At the very least, the banks have demonstratedan ignorance of two very basic aspects of risk:(a) the importance of correlation, and(b) the possibility of price decline.

So according to Stiglitz (1992!) the issues to concentrate on are:

• Downside risk: extremes• Correlation: dependence

And let me add as an Intermezzo:

Chapter on Extreme Value Theorybeyond Normality

Chapter on Dependence Modellingbeyond Linear Correlation

… (2005) contains

and much more …

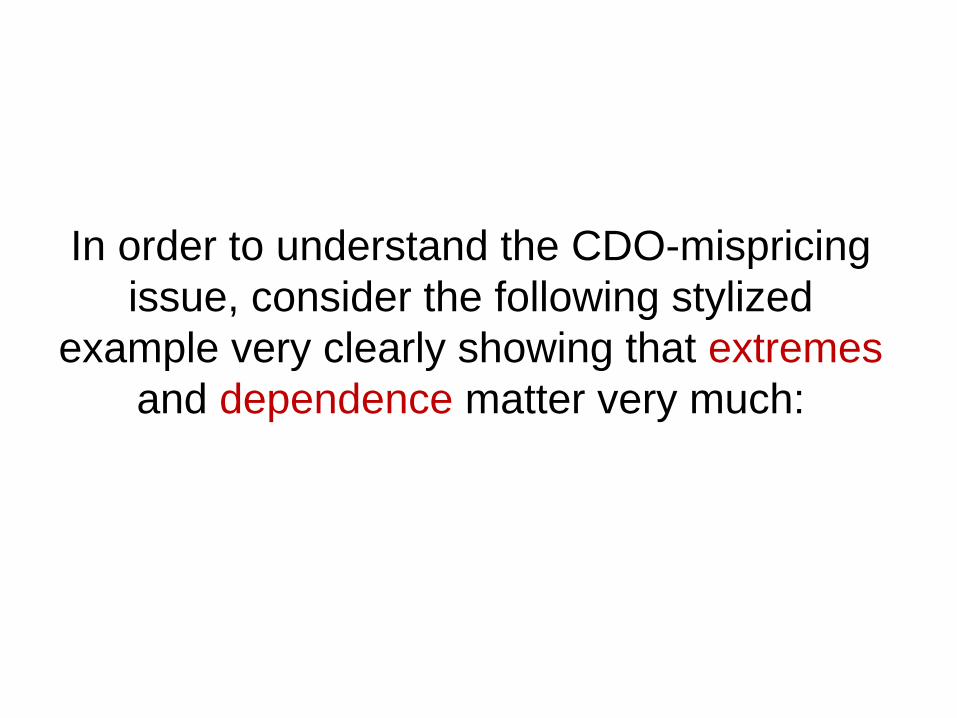

In order to understand the CDO-mispricing issue, consider the following stylized

example very clearly showing that extremes and dependence matter very much:

The normal distribution

Extremes matter

Correlation matters

Credit Default Swaps Securitisationconstruction

The investors

(Synthetic)

?Eq. Mez. Sen.

The waterfall principle

The AIG-story:

• AIGFP sold protection on super-senior tranches of CDOs, where the underlying portfolio con- sisted of loans, debt securities, asset-backed securities and mortgage-backed securities.

• “The likelihood of any payment obligation by AIGFP under each transaction is remote, even in severe recessionary market scenarios“ (2006, AR)

• “It is hard for us, without being flippant, to even see a scenario within any kind of realm of reason that would see us losing one dollar in any of those transactions.“(8/2007, CEO of AIGFP)

And yet:

• AIG, a company of around 100,000 employees brought to its knees by a small subsidiary of 400 employees, is an example of a failure of risk management, both at the division and the group level. AIG almost went bankrupt because it ran out of cash.

• As at December 31 2007, AIG had assets of $1,000 billion dollars.

• Problems with collateral posting and securities lending pro- gram also affecting its credit rating, etc …

• On September 16 2008, the Federal Reserve Board, with the support of the U.S. Department of the Treasury, announced that it had authorized the Federal Reserve Bank of New York to lend up to $85 billion to AIG.

Liquidity – Speed – Size

Back to “Recipe for Disaster: The Formula That Killed Wall Street”

Why did no one notice the formula’s Achilles heel?

We did, but nobodylistened!

Two results from the 1998 RiskLab report

Remark 1: See Figure 1 next page

Remark 2: In the above paper it is shown that

A very early warning!

1960

Indeed we did warn about the Achilles heel!

Standard - model Stress - model(3) (12)

Some comments by mathematicians:

• (L.C.G. Rogers) The problem is not that mathematics was used by the banking industry, the problem was that it was abused by the banking industry. Quants were instructed to build models which fitted the market prices. Now if the market prices were way out of line, the calibrated models would just faithfully reproduce those wacky values, and the bad prices get reinforced by an overlay of scientific respectability!

And Rogers continues:

• The standard models which were used for a long time before being rightfully discredited by (some) academics and the more thoughtful practitioners were from the start a complete fudge; so you had garbage prices being underpinned by garbage modelling.

• (M.H.A. Davis) The whole industry was stuck in a classic positive feedback loop which no party could (P.E. “wanted to”) walk away from.

Indeed only some!

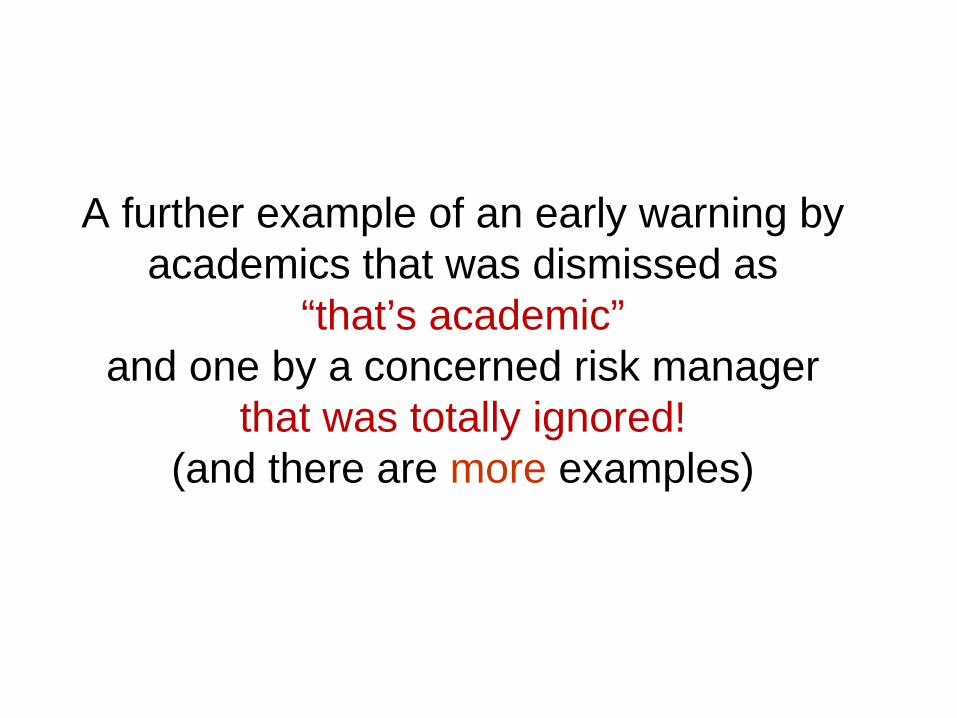

A further example of an early warning by academics that was dismissed as

“that’s academic” and one by a concerned risk manager

that was totally ignored! (and there are more examples)

Charles Ponzi1910

Harry Markopolos

Embrechts, P. et al. (2001): An academic response to Basel II. Financial Markets Group, London School of Economics. (Mailed to the Basel Committee)

(Critical on VaR, procyclicality, systemic risk)

Markopolos, H. (2005): The world’s largest hedge fund is a fraud. (Mailed to the SEC)

(Madoff runs a Ponzi scheme)

Bernard Madoff

Quote from the LSE-RiskLab report to the Basel Committee:

The Basel II regulations fail to consider the fact that risk is en-dogonous. VaR can destabilise an economy and induce cra-shes when they would not otherwise occur.

Statistical models used for forecasting risk have been proven togive inconsistent and biased forecasts, namely under-estimating the joint downside risk of different assets. The Basel Com-mittee has chosen poor quality measures of risk when betterrisk measures are available.

Heavy reliance on credit rating agencies for the standard ap-proach to credit risk is misguided as they have been shown toprovide conflicting and inconsistent forecasts of individual clients’ creditworthiness. They are unregulated and the quality of their risk estimate is largely unobservable.

…Financial regulation is inherently procyclical. Our view is thatthis set of proposals will, overall, exacerbate this tendencysignificantly. In so far as the purpose of financial regulationIs to reduce the likelihood of systemic crisis, these propos-sals will actually tend to negate, not promote this useful purpose.

Perhaps our most serious concern about these proposals, takenall together, will enhance both the procyclicality and the suscep-tibility of the financial system to systemic crisis, thus negating thecentral purpose of the whole exercise.

Reference: An academic response to Basel II. RiskLab-LSEFMG 2001 report to the Basel Committee.

Reconsider before it is too late!

I felt that I had to react to all the nonsense written on Mathematics and The Crisis

and wrote a letter to the Financial Times:

Dear SirThe article "Of couples and copulas", published on 24 April 2009, suggests that David Li's formula is to blame for the current financial crisis. For me, this is akin to blaming Einstein's E=mc² formula for the destruction wreaked by the atomic bomb.

Feeling like a risk manager whose protestations of imminent danger were ignored, I wish to make clear that many well-respected academics have pointed out the limitations of the mathematical tools used in the finance industry, including Li's formula. However, these warnings were either ignored or dismissed with a desultory response: "It's academic".

We hope that we are listened to in the future, rather than being made a convenient scapegoat.

Yours Faithfully, Professor Paul Embrechts Director of RiskLab ETH Zurich

The overall societal relevance, importance and success of mathematics is beyond any doubt:

• Medical Statistics and Epidemiology• Actuarial Mathematics (Life, Non-Life, Re, Health, …)• Statistical Quality Control• Maxwell’s Theory of Electromagnetism• Calculus and Newtonian Mechanics• Number Theory and Cryptography• Differential Geometry and Einstein’s Relativity Theory

(GPS-application)• Markov Chain Theory and Web based Search Engines

like Google• …

And likewise:

Mathematical Finance – Financial Mathematics is of key importance for

• understanding and clarifying models used in economics

• making heuristic methods mathematically precise

• highlighting model conditions and restrictions on applicability

• working out numerous explicit examples • leading the way for stress testing and

robustness properties• … a relevant mathematical theory on its own

(Hans Föllmer)

Some of the research coming from RiskLab, see also www.math.ethz.ch/~embrechts

1997 2005 2007

Chuck Prince (former CEO of Citygroup) “So long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

Warren Buffett “The giddy participants all planned to leave just seconds before midnight. There’s a problem, though: they’re dancing in a room in which the clocks have no hands.”

Alan Greenspan “The whole intellectual edifice [the modern risk manage-ment paradigm] collapsed in the summer of last year.”

Isaac Newton (the South Sea Bubble) “I can predict the motion of heavenly bodies, but not the madness of crowds.”

Perhaps that old cynic, Adam Smith, should have the final words on past and present financial follies: “The chance of gain is by every man more or less overvalued, and the chance of loss is by most men undervalued and by scarce any man who is in tolerable health and spirits valued more than it is worth.”

Some quotes from Kay’s FT article:

“Who cares for you?” said Alice, (she had grown to her full size by this time.) “You’re nothing but a pack of cards!” At this, the whole pack rose up into the air, and came flying down upon her.

Alice’s Summary

Alexander Pope “They have dreamed out their dream and awaking have found nothing in their hands.”

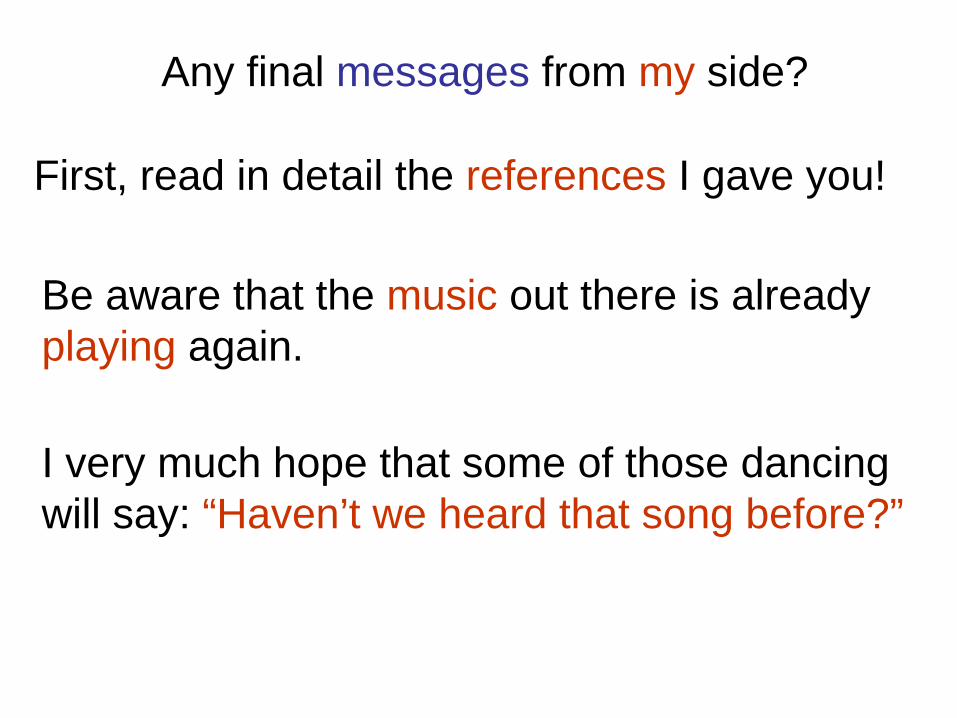

Any final messages from my side?

First, read in detail the references I gave you!

Be aware that the music out there is alreadyplaying again.

I very much hope that some of those dancingwill say: “Haven’t we heard that song before?”

New generations of students will have to use the tools and techniques of QRM wisely in a world where the rules of the game will (may?) have been changed.

Always be scientifically critical, as well as socially honest, adhere to the highest ethical principles, especially in the face of temptation … which will come!

A message for my students

And on the boundedness of our knowledge:

There are more things in heaven and earth, Horatio, than are dreamt of in your philosophy!

William Shakespeare(Hamlet I.v. 166)

Thank You!