Embed Size (px)

Citation preview

NEW ZEALAND ECONOMICS

MARKET FOCUS

ANZ RESEARCH

15 June 2015

INSIDE

Economic Overview 2

Data Preview 6

Interest Rate Strategy 7

Currency Strategy 9

Data Event Calendar 11

Local Data Watch 13

Key Forecasts 14

NZ ECONOMICS TEAM

Cameron Bagrie Chief Economist Telephone: +64 4 802 2212 E-mail: [email protected] Twitter @ANZ_cambagrie Philip Borkin Senior Economist Telephone: +64 9 357 4065 Email: [email protected]

David Croy Senior Rates Strategist Telephone: +64 4 576 1022 E-mail: [email protected] Peter Gardiner Economist Telephone: +64 4 802 2357 E-mail: [email protected] Mark Smith Senior Economist Telephone: +64 9 357 4096 E-mail: [email protected] Sam Tuck Senior FX Strategist Telephone: +64 9 357 4086 E-mail: [email protected] Con Williams Rural Economist Telephone: +64 4 802 2361 E-mail: [email protected] Sharon Zöllner Senior Economist Telephone: +64 9 357 4094 E-mail: [email protected]

THE FIRST CUT IS THE DEEPEST

ECONOMIC OVERVIEW

Given the shifting tone of the economic data, we expect a follow-up cut in July

and the risk is for more beyond that. This week, the main data reads are largely

backward-looking, with Q1 GDP growth expected to be below trend given the

impact of drought. The global dairy market is highly uncertain at present and

price movements are difficult to predict, but many indicators are pointing to a

modest bounce. We’ll take it, although the levels will tell the real story – they are

low.

DATA PREVIEW – Q1 GDP & BALANCE OF PAYMENTS

A positive goods and services balance is expected to temper the size of the

annual current account deficit, although the declining goods terms of trade will

help deliver circa 5% deficits by the end of the year. Q1 GDP is expected to show

a modest pace of growth, with lifting services sector activity offsetting drought-

related dips in primary and goods valued-added.

INTEREST RATE STRATEGY

Short-term rates have rallied considerably since last week’s MPS. The direction of

rates is wedded to the economic outlook and we expect pending data to support a

follow-up cut in July. The yield curve remains under pressure to steepen further.

Longer-term rates have edged higher, and while the published “dot plots” from

this week’s FOMC meeting suggest the market is underestimating the speed of

policy normalisation, we expect a gradual path of US policy normalisation and

abundant global liquidity will help cap rises in global yields. Local yields remain

high in relation to global peers, and with the policy outlooks pointing in differing

directions there is scope for local rates to narrow in relation to global peers.

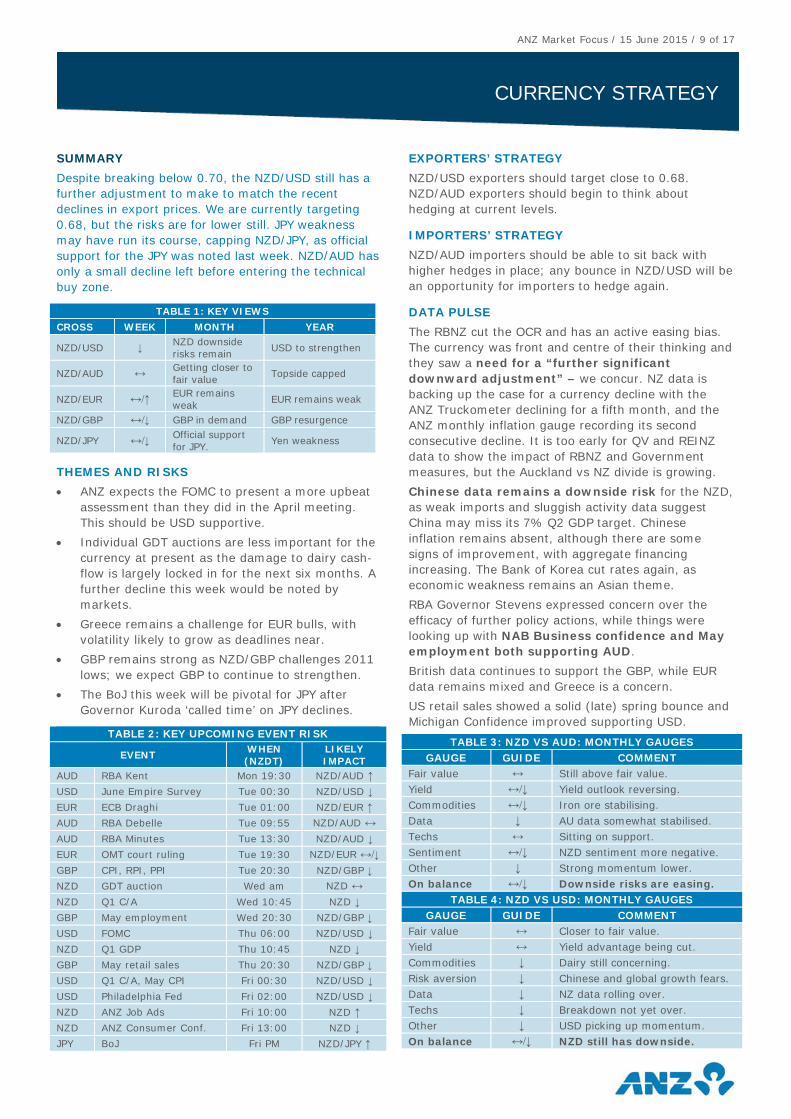

CURRENCY STRATEGY

Despite breaking below 0.70, the NZD/USD still has a further adjustment to make

to match the recent declines in export prices. We are currently targeting 0.68, but

the risks are for lower still. JPY weakness may have run its course, capping

NZD/JPY, as official support for the JPY was noted last week. NZD/AUD has only a

small decline left before entering the technical buy zone.

THE ANZ HEATMAP

Variable View Comment Risk profile (change to view)

GDP

2.9% y/y

for 2016

Q2

Economic momentum is beginning to soften from an above-trend to a

below-trend pace as previous supports begin to wane.

Unemployment

rate

5.5% for

2016 Q2

Unemployment rate to gradually trend lower. Wage inflation

contained.

OCR 3.0% by

Jun 2016

The RBNZ is now responding to a weaker macro backdrop. We

expect a further 25bp cut in July, with risks skewed to more.

CPI

1.3% y/y

for 2016

Q2

Sub-1% annual inflation over 2015. Benign global backdrop;

domestic pricing pressures contained so far.

Positive Negative

Neutral

Positive Negative

Neutral

Up Down

Neutral

Positive Negative

Neutral

ANZ Market Focus / 15 June 2015 / 2 of 17

ECONOMIC OVERVIEW

SUMMARY Given the shifting tone of the economic data, we

expect a follow-up cut in July and the risk is for more

beyond that. This week, the main data reads are

largely backward-looking, with Q1 GDP growth

expected to be below trend given the impact of

drought. The global dairy market is highly uncertain

at present and price movements are difficult to

predict, but many indicators are pointing to a modest

bounce. We’ll take it, although the levels will tell the

real story – they are low.

FORTHCOMING EVENTS GlobalDairyTrade auction results (early am,

Wednesday, 17 June). We do believe we are close to

the trough in prices, although uncertainty is high.

Most indicators point to a modest bounce.

Balance of Payments – Q1 (10:45am, Wednesday,

17 June). In unadjusted terms, we expect a small

current account surplus ($100m), although base

effects should see the annual deficit widen to 3.9% of

GDP – the largest in 18 months.

GDP – Q1 (10:45am, Thursday, 18 June). We expect

modest quarterly growth of 0.5% (3.0% y/y). This is

led by services sector outperformance, and offsets

contractions from primary and goods sector value

added.

ANZ Job Ads – June (10:00am, Friday, 19 June).

ANZ Roy Morgan Consumer Confidence – June (1:00pm, Friday, 19 June).

WHAT’S THE VIEW? We’ll start by making a few observations following the RBNZ’s decision to cut the OCR last week:

The decision itself was clearly about responding to macro developments, and the weaker terms of trade in particular. The

RBNZ is assuming the terms of trade falls 7%

from here (13% peak-to-trough), which all else

being equal represents a 2% point headwind for

GDP growth [we assume each 1% change in the

terms of trade impacts GDP growth to the tune of

0.15%pt]. That is spread over a couple of years

but is still a massive headwind. Along with the

low inflation staring point and better supply-side

capacity, the reality is that the previous

combination of monetary conditions (a slowly

declining TWI and a flat-lined OCR) was

insufficient to get inflation back to 2%.

Whether or not price and wage setting outcomes “settle” at a low level (one of the

conditions from April) is still a question in the background and highly relevant for monetary policy going forward. If inflation

nuances remain weak, the RBNZ will cut more

than just an extra 25bps. But first and foremost,

the decision to cut last week was about a weaker

macro backdrop. Markets (NZD and interest

rates) will keep pushing for more than one more

cut as the “settle” scenario is additional to the

weaker macro one.

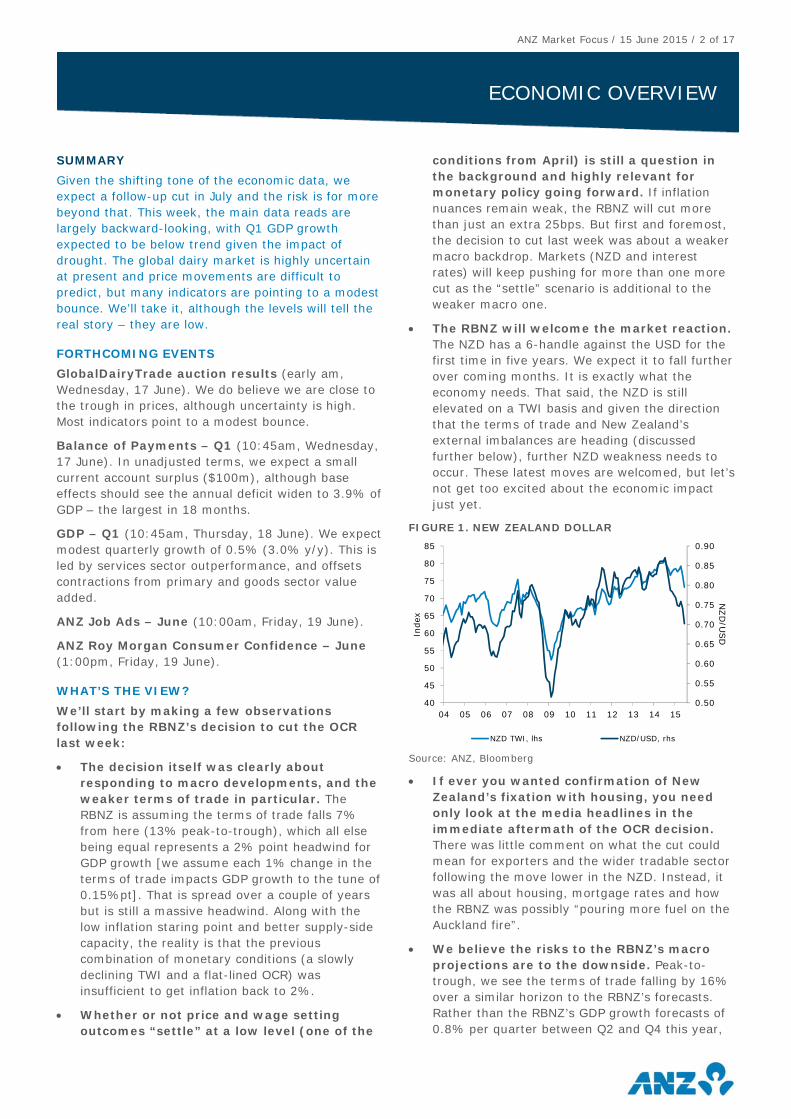

The RBNZ will welcome the market reaction. The NZD has a 6-handle against the USD for the

first time in five years. We expect it to fall further

over coming months. It is exactly what the

economy needs. That said, the NZD is still

elevated on a TWI basis and given the direction

that the terms of trade and New Zealand’s

external imbalances are heading (discussed

further below), further NZD weakness needs to

occur. These latest moves are welcomed, but let’s

not get too excited about the economic impact

just yet.

FIGURE 1. NEW ZEALAND DOLLAR

Source: ANZ, Bloomberg

If ever you wanted confirmation of New Zealand’s fixation with housing, you need only look at the media headlines in the immediate aftermath of the OCR decision. There was little comment on what the cut could

mean for exporters and the wider tradable sector

following the move lower in the NZD. Instead, it

was all about housing, mortgage rates and how

the RBNZ was possibly “pouring more fuel on the

Auckland fire”.

We believe the risks to the RBNZ’s macro projections are to the downside. Peak-to-

trough, we see the terms of trade falling by 16%

over a similar horizon to the RBNZ’s forecasts.

Rather than the RBNZ’s GDP growth forecasts of

0.8% per quarter between Q2 and Q4 this year,

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

40

45

50

55

60

65

70

75

80

85

04 05 06 07 08 09 10 11 12 13 14 15

NZD

/USDIn

dex

NZD TWI, lhs NZD/USD, rhs

ANZ Market Focus / 15 June 2015 / 3 of 17

ECONOMIC OVERVIEW

we see below-trend outcomes as much more

likely, with Q2 activity certainly looking on the

weak side.

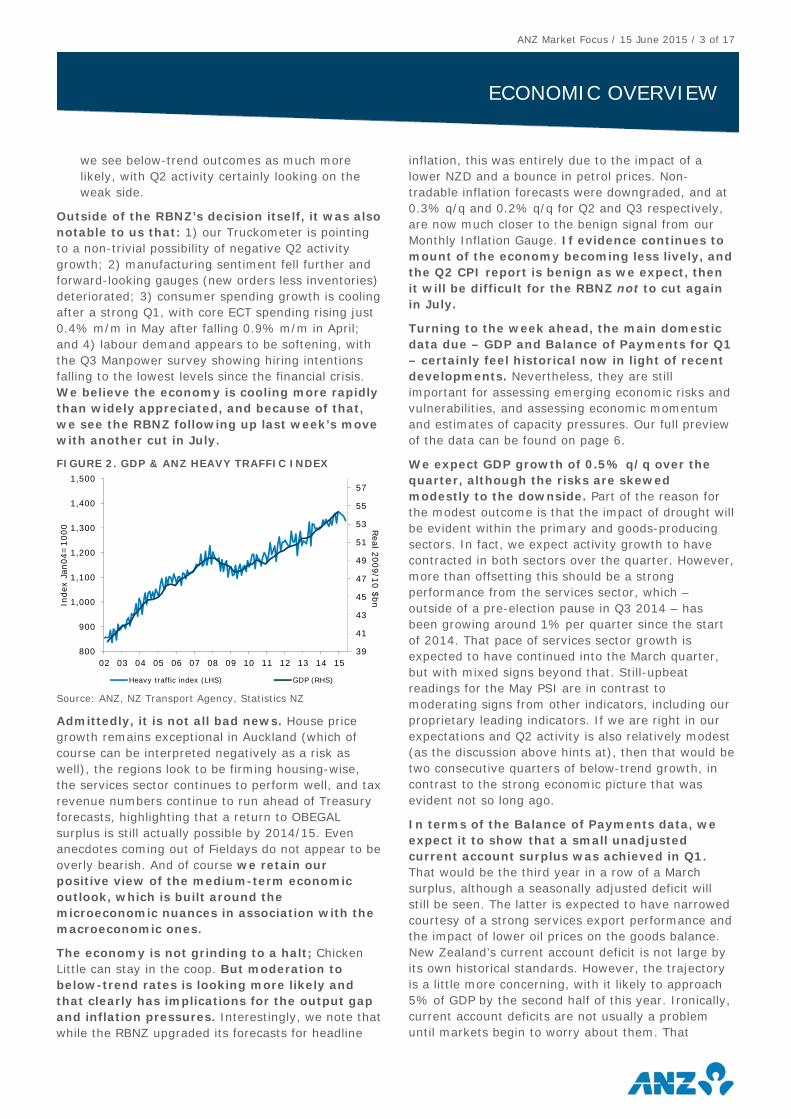

Outside of the RBNZ’s decision itself, it was also notable to us that: 1) our Truckometer is pointing

to a non-trivial possibility of negative Q2 activity

growth; 2) manufacturing sentiment fell further and

forward-looking gauges (new orders less inventories)

deteriorated; 3) consumer spending growth is cooling

after a strong Q1, with core ECT spending rising just

0.4% m/m in May after falling 0.9% m/m in April;

and 4) labour demand appears to be softening, with

the Q3 Manpower survey showing hiring intentions

falling to the lowest levels since the financial crisis.

We believe the economy is cooling more rapidly than widely appreciated, and because of that, we see the RBNZ following up last week’s move with another cut in July.

FIGURE 2. GDP & ANZ HEAVY TRAFFIC INDEX

Source: ANZ, NZ Transport Agency, Statistics NZ

Admittedly, it is not all bad news. House price

growth remains exceptional in Auckland (which of

course can be interpreted negatively as a risk as

well), the regions look to be firming housing-wise,

the services sector continues to perform well, and tax

revenue numbers continue to run ahead of Treasury

forecasts, highlighting that a return to OBEGAL

surplus is still actually possible by 2014/15. Even

anecdotes coming out of Fieldays do not appear to be

overly bearish. And of course we retain our positive view of the medium-term economic outlook, which is built around the microeconomic nuances in association with the macroeconomic ones.

The economy is not grinding to a halt; Chicken

Little can stay in the coop. But moderation to below-trend rates is looking more likely and that clearly has implications for the output gap and inflation pressures. Interestingly, we note that

while the RBNZ upgraded its forecasts for headline

inflation, this was entirely due to the impact of a

lower NZD and a bounce in petrol prices. Non-

tradable inflation forecasts were downgraded, and at

0.3% q/q and 0.2% q/q for Q2 and Q3 respectively,

are now much closer to the benign signal from our

Monthly Inflation Gauge. If evidence continues to mount of the economy becoming less lively, and the Q2 CPI report is benign as we expect, then it will be difficult for the RBNZ not to cut again in July.

Turning to the week ahead, the main domestic data due – GDP and Balance of Payments for Q1 – certainly feel historical now in light of recent developments. Nevertheless, they are still

important for assessing emerging economic risks and

vulnerabilities, and assessing economic momentum

and estimates of capacity pressures. Our full preview

of the data can be found on page 6.

We expect GDP growth of 0.5% q/q over the quarter, although the risks are skewed modestly to the downside. Part of the reason for

the modest outcome is that the impact of drought will

be evident within the primary and goods-producing

sectors. In fact, we expect activity growth to have

contracted in both sectors over the quarter. However,

more than offsetting this should be a strong

performance from the services sector, which –

outside of a pre-election pause in Q3 2014 – has

been growing around 1% per quarter since the start

of 2014. That pace of services sector growth is

expected to have continued into the March quarter,

but with mixed signs beyond that. Still-upbeat

readings for the May PSI are in contrast to

moderating signs from other indicators, including our

proprietary leading indicators. If we are right in our

expectations and Q2 activity is also relatively modest

(as the discussion above hints at), then that would be

two consecutive quarters of below-trend growth, in

contrast to the strong economic picture that was

evident not so long ago.

In terms of the Balance of Payments data, we expect it to show that a small unadjusted current account surplus was achieved in Q1. That would be the third year in a row of a March

surplus, although a seasonally adjusted deficit will

still be seen. The latter is expected to have narrowed

courtesy of a strong services export performance and

the impact of lower oil prices on the goods balance.

New Zealand’s current account deficit is not large by

its own historical standards. However, the trajectory

is a little more concerning, with it likely to approach

5% of GDP by the second half of this year. Ironically,

current account deficits are not usually a problem

until markets begin to worry about them. That

39

41

43

45

47

49

51

53

55

57

800

900

1,000

1,100

1,200

1,300

1,400

1,500

02 03 04 05 06 07 08 09 10 11 12 13 14 15

Real 2

009/1

0 $

bnIn

dex J

an04=

1000

Heavy traffic index (LHS) GDP (RHS)

ANZ Market Focus / 15 June 2015 / 4 of 17

ECONOMIC OVERVIEW

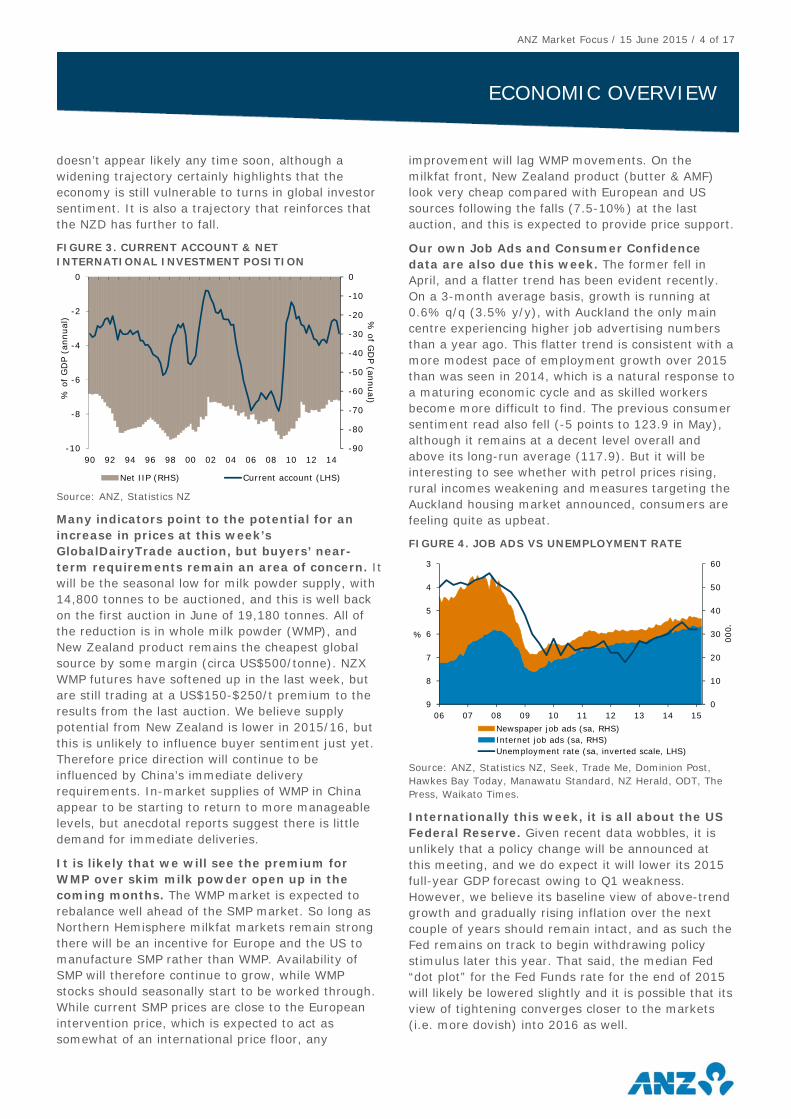

doesn’t appear likely any time soon, although a

widening trajectory certainly highlights that the

economy is still vulnerable to turns in global investor

sentiment. It is also a trajectory that reinforces that

the NZD has further to fall.

FIGURE 3. CURRENT ACCOUNT & NET INTERNATIONAL INVESTMENT POSITION

Source: ANZ, Statistics NZ

Many indicators point to the potential for an increase in prices at this week’s GlobalDairyTrade auction, but buyers’ near-term requirements remain an area of concern. It will be the seasonal low for milk powder supply, with

14,800 tonnes to be auctioned, and this is well back

on the first auction in June of 19,180 tonnes. All of

the reduction is in whole milk powder (WMP), and

New Zealand product remains the cheapest global

source by some margin (circa US$500/tonne). NZX

WMP futures have softened up in the last week, but

are still trading at a US$150-$250/t premium to the

results from the last auction. We believe supply

potential from New Zealand is lower in 2015/16, but

this is unlikely to influence buyer sentiment just yet.

Therefore price direction will continue to be

influenced by China’s immediate delivery

requirements. In-market supplies of WMP in China

appear to be starting to return to more manageable

levels, but anecdotal reports suggest there is little

demand for immediate deliveries.

It is likely that we will see the premium for WMP over skim milk powder open up in the coming months. The WMP market is expected to

rebalance well ahead of the SMP market. So long as

Northern Hemisphere milkfat markets remain strong

there will be an incentive for Europe and the US to

manufacture SMP rather than WMP. Availability of

SMP will therefore continue to grow, while WMP

stocks should seasonally start to be worked through.

While current SMP prices are close to the European

intervention price, which is expected to act as

somewhat of an international price floor, any

improvement will lag WMP movements. On the

milkfat front, New Zealand product (butter & AMF)

look very cheap compared with European and US

sources following the falls (7.5-10%) at the last

auction, and this is expected to provide price support.

Our own Job Ads and Consumer Confidence data are also due this week. The former fell in

April, and a flatter trend has been evident recently.

On a 3-month average basis, growth is running at

0.6% q/q (3.5% y/y), with Auckland the only main

centre experiencing higher job advertising numbers

than a year ago. This flatter trend is consistent with a

more modest pace of employment growth over 2015

than was seen in 2014, which is a natural response to

a maturing economic cycle and as skilled workers

become more difficult to find. The previous consumer

sentiment read also fell (-5 points to 123.9 in May),

although it remains at a decent level overall and

above its long-run average (117.9). But it will be

interesting to see whether with petrol prices rising,

rural incomes weakening and measures targeting the

Auckland housing market announced, consumers are

feeling quite as upbeat.

FIGURE 4. JOB ADS VS UNEMPLOYMENT RATE

Source: ANZ, Statistics NZ, Seek, Trade Me, Dominion Post,

Hawkes Bay Today, Manawatu Standard, NZ Herald, ODT, The

Press, Waikato Times.

Internationally this week, it is all about the US Federal Reserve. Given recent data wobbles, it is

unlikely that a policy change will be announced at

this meeting, and we do expect it will lower its 2015

full-year GDP forecast owing to Q1 weakness.

However, we believe its baseline view of above-trend

growth and gradually rising inflation over the next

couple of years should remain intact, and as such the

Fed remains on track to begin withdrawing policy

stimulus later this year. That said, the median Fed

“dot plot” for the Fed Funds rate for the end of 2015

will likely be lowered slightly and it is possible that its

view of tightening converges closer to the markets

(i.e. more dovish) into 2016 as well.

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

-10

-8

-6

-4

-2

0

90 92 94 96 98 00 02 04 06 08 10 12 14

% o

f GD

P (a

nnual)%

of

GD

P (

annual)

Net IIP (RHS) Current account (LHS)

0

10

20

30

40

50

603

4

5

6

7

8

9

06 07 08 09 10 11 12 13 14 15

'000%

Newspaper job ads (sa, RHS)

Internet job ads (sa, RHS)

Unemployment rate (sa, inverted scale, LHS)

ANZ Market Focus / 15 June 2015 / 5 of 17

ECONOMIC OVERVIEW

Why is this important for New Zealand? Well

clearly the direction of Fed policy and the

performance of the US economy more generally will

have a huge bearing on the NZD/USD. The RBNZ has

played its part (and is expected to continue doing

so), but if the Fed does begin “lift-off” then this

should reinforce a downward NZD/USD trend.

LOCAL DATA

ANZ Truckometer – May. The Heavy Traffic Index

fell 1.1% m/m – the fifth consecutive monthly

decline. The Light Traffic Index fell 0.6% m/m.

Government Financial Statements – Apr. The

OBEGAL was in surplus to the tune of $448m, over

$1bn better than forecast.

Economic Survey of Manufacturing – Q1. Total

manufacturing sales volumes fell 0.3% q/q, with

meat and dairy sales volumes down 1.5% q/q.

QV House Prices – May. Nationwide sales prices

rose 3.1% over the past three months, with annual

growth rising to 9.0% y/y.

ANZ Monthly Inflation Gauge – May. The Gauge

fell 0.1% m/m, the second consecutive fall after a

0.2% m/m fall in April.

Electronic Card Transactions – May. Total retail

spending rose 1.2% m/m, led by fuel retailing. Core

retail spending rose a more modest 0.4% m/m.

RBNZ Monetary Policy Statement. The RBNZ cut

the OCR by 25bps to 3.25% and signalled the

possibility of additional easing this year.

REINZ Housing Market Statistics – May. Sales

volumes fell 1.4% sa, while the median sales price

rose 1.2% sa, with annual inflation rising to 7% y/y.

Auckland prices are running at 20% y/y.

BNZ-Business NZ PMI – May. The headline index

dipped 0.2 points to 51.5.

Food Price Index – May. Food prices rose 0.4%

m/m, although annual growth eased to 0.8% y/y.

BNZ-Business NZ PSI – May. The PSI rose 1.5

points to 58.0 – the highest reading since July 2014.

ANZ Market Focus / 15 June 2015 / 6 of 17

DATA PREVIEW

SUMMARY A positive goods and services balance is expected to

temper the size of the annual current account deficit,

although the declining goods terms of trade will help

deliver circa 5% deficits by the end of the year. Q1

GDP is expected to show a modest pace of growth,

with lifting services sector activity offsetting drought-

related dips in primary and goods valued-added.

CURRENT ACCOUNT – 2015Q1 (Wednesday 17 June, 10.45am)

Current Account ANZ Market Quarter (nsa) +$100m +$282m

Quarter (sa) -$2,240m --

Annual -$9.2bn -$9.1bn

% of GDP -3.9% -3.8%

We expect a small (unadjusted) current account surplus in Q1 ($100m), which would be the third

year in a row of such a Q1 outcome. However, due to

base effects (largely within the goods balance), the

annual current account deficit is expected to widen to

3.9% of GDP – the largest in 18 months.

Stronger services exports and lower goods import values are expected to deliver a larger seasonally adjusted goods and services surplus in Q1. Services exports are being boosted by a

strong performance from the tourism sector (both

arrivals and spending), while lower import values are

in part a result of weaker global oil prices. Over the

quarter, the goods terms of trade posted a modest

1.4% q/q lift. With the income deficit expected to

remain at $2.8bn, due to slightly lower debt servicing

costs offset by stronger profitability of foreign firms

operating in New Zealand, the broader seasonally adjusted current account deficit is expected to narrow from $2.6bn to $2.2bn.

However, base effects are still likely to see the annual current account widen towards at least 5% of GDP by 2015 H2. Moreover, we believe the

improvement in the seasonally adjusted deficit in Q1

could prove temporary. With the terms of trade

forecast to fall a further 8% over the remainder of

the year, the goods deficit is forecast to widen.

This widening in New Zealand’s external balances is a

reminder of what the economy still sorely needs – a

lower currency. That said, there are some offsetting

forces to take into account and it shouldn’t be

forgotten that structural progress has been made

over recent years. Net external debt sits at an 11-

year low (60.4% of GDP) and the maturity profile of

its gross liabilities continues to lengthen. The

economy is therefore less vulnerable to shocks than it

was in, say, 2008. But it is not bulletproof.

GROSS DOMESTIC PRODUCT – 2015Q1 (Thursday 18 June, 10.45am)

GDP ANZ RBNZ Market QoQ +0.5% +0.6% +0.6%

YoY +3.0% +3.1% +3.1%

Ann. Ave. +3.3% +3.3% +3.3%

We expect a 0.5% lift in production-based GDP (+3.0% y/y), slightly below the median market

expectation and the June MPS pick. Risks around our pick are slightly to the downside.

Rescuing the economy from a negative quarter is a resurgent services sector, with a close to 1%

q/q outturn expected. Retail trade growth was strong,

with surging visitor numbers lifting accommodation.

Paid hours from the services sector registered

another strong quarterly increase (+2.2%), with the

major beneficiaries being finance & insurance, and

real estate & business services. Higher paid hours

should also support activity in the government sector.

We expect a Cricket World Cup boost to be evident in

media & communications activity. Tempering the

result will be flat outturns for wholesale trade and

transport (consistent with the Truckometer).

Primary value added is expected to fall close to 2% q/q largely due to a drought impact on

agricultural production. A small fall is expected for goods sector value added, which is largely the

result of drought-related falls in food manufacturing.

Rising wholesale electricity prices suggest a further

fall in electricity value added. The remainder of the

manufacturing sector is expected to be flat, with

offsetting movements amongst the components. A

1.5% increase is expected for construction, with

increases for both residential and non-residential.

Expenditure GDP is still expected to convey a strong domestic demand backdrop. A circa 1%

consumption print is expected, with public

consumption also up in Q1. Circa 1% increases are

also expected for residential and other investment

activity despite expected falls for plant & machinery

and intangibles asset investment. A positive

contribution is expected from net trade, which should

be more than offset by a rundown in inventories.

MARKET IMPLICATIONS Market implications from the Q1 data are limited

given their historical nature and the swift change in

the risk profile that has eventuated. The short-term

outlook has softened and there is a strong likelihood

of another sub-trend GDP print in Q2. The lower NZD

is acting as a release valve for the economy, but the

worsening trajectory for the external accounts

suggests it has further to go.

ANZ Market Focus / 15 June 2015 / 7 of 17

INTEREST RATE STRATEGY

SUMMARY Short-term rates have rallied considerably since last

week’s MPS. The direction of rates is wedded to the

economic outlook and we expect pending data to

support a follow-up cut in July. The yield curve remains

under pressure to steepen further. Longer-term rates

have edged higher, and while the published “dot plots”

from this week’s FOMC meeting suggest the market is

underestimating the speed of policy normalisation, we

expect a gradual path of US policy normalisation and

abundant global liquidity will help cap rises in global

yields. Local yields remain high in relation to global

peers, and with the policy outlooks pointing in differing

directions there is scope for local rates to narrow in

relation to global peers.

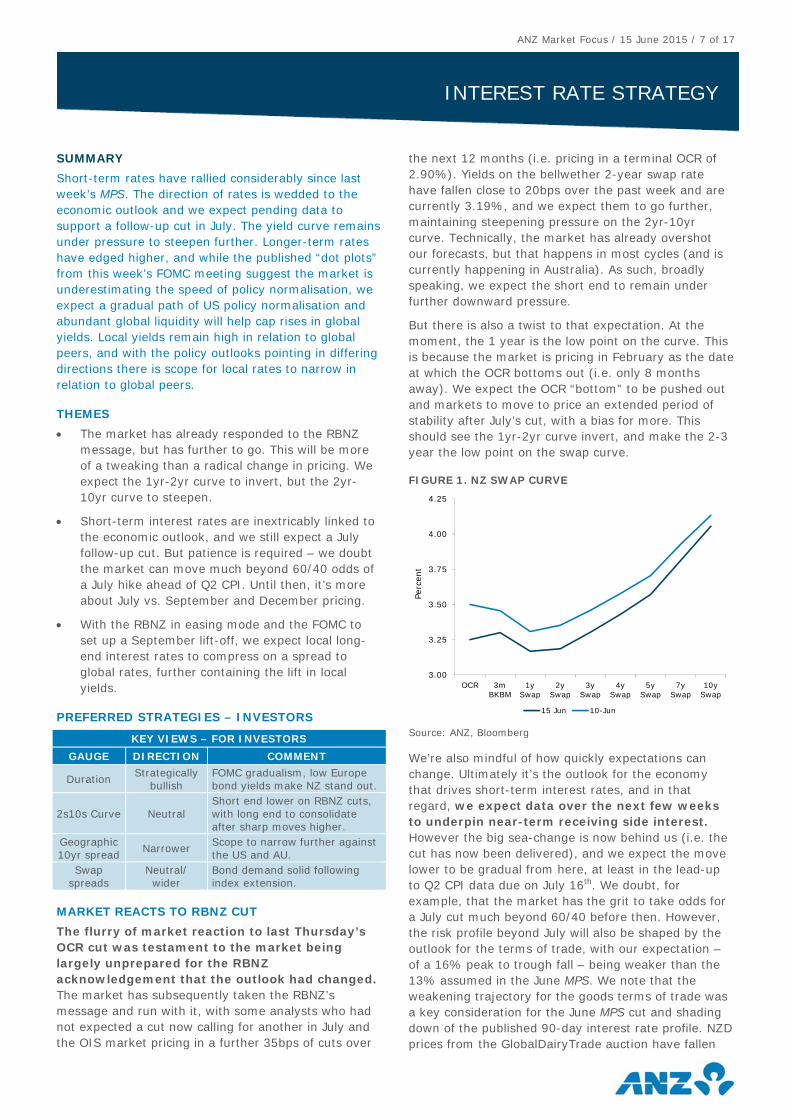

THEMES The market has already responded to the RBNZ

message, but has further to go. This will be more

of a tweaking than a radical change in pricing. We

expect the 1yr-2yr curve to invert, but the 2yr-

10yr curve to steepen.

Short-term interest rates are inextricably linked to

the economic outlook, and we still expect a July

follow-up cut. But patience is required – we doubt

the market can move much beyond 60/40 odds of

a July hike ahead of Q2 CPI. Until then, it’s more

about July vs. September and December pricing.

With the RBNZ in easing mode and the FOMC to

set up a September lift-off, we expect local long-

end interest rates to compress on a spread to

global rates, further containing the lift in local

yields.

PREFERRED STRATEGIES – INVESTORS

KEY VIEWS – FOR INVESTORS GAUGE DIRECTION COMMENT

Duration Strategically

bullish

FOMC gradualism, low Europe

bond yields make NZ stand out.

2s10s Curve Neutral

Short end lower on RBNZ cuts,

with long end to consolidate

after sharp moves higher.

Geographic

10yr spread Narrower

Scope to narrow further against

the US and AU.

Swap

spreads

Neutral/

wider

Bond demand solid following

index extension.

MARKET REACTS TO RBNZ CUT The flurry of market reaction to last Thursday’s OCR cut was testament to the market being largely unprepared for the RBNZ acknowledgement that the outlook had changed. The market has subsequently taken the RBNZ’s

message and run with it, with some analysts who had

not expected a cut now calling for another in July and

the OIS market pricing in a further 35bps of cuts over

the next 12 months (i.e. pricing in a terminal OCR of

2.90%). Yields on the bellwether 2-year swap rate

have fallen close to 20bps over the past week and are

currently 3.19%, and we expect them to go further,

maintaining steepening pressure on the 2yr-10yr

curve. Technically, the market has already overshot

our forecasts, but that happens in most cycles (and is

currently happening in Australia). As such, broadly

speaking, we expect the short end to remain under

further downward pressure.

But there is also a twist to that expectation. At the

moment, the 1 year is the low point on the curve. This

is because the market is pricing in February as the date

at which the OCR bottoms out (i.e. only 8 months

away). We expect the OCR “bottom” to be pushed out

and markets to move to price an extended period of

stability after July’s cut, with a bias for more. This

should see the 1yr-2yr curve invert, and make the 2-3

year the low point on the swap curve.

FIGURE 1. NZ SWAP CURVE

Source: ANZ, Bloomberg

We’re also mindful of how quickly expectations can

change. Ultimately it’s the outlook for the economy

that drives short-term interest rates, and in that

regard, we expect data over the next few weeks to underpin near-term receiving side interest. However the big sea-change is now behind us (i.e. the

cut has now been delivered), and we expect the move

lower to be gradual from here, at least in the lead-up

to Q2 CPI data due on July 16th. We doubt, for

example, that the market has the grit to take odds for

a July cut much beyond 60/40 before then. However,

the risk profile beyond July will also be shaped by the

outlook for the terms of trade, with our expectation –

of a 16% peak to trough fall – being weaker than the

13% assumed in the June MPS. We note that the

weakening trajectory for the goods terms of trade was

a key consideration for the June MPS cut and shading

down of the published 90-day interest rate profile. NZD

prices from the GlobalDairyTrade auction have fallen

3.00

3.25

3.50

3.75

4.00

4.25

OCR 3mBKBM

1ySwap

2ySwap

3ySwap

4ySwap

5ySwap

7ySwap

10ySwap

15 Jun 10-Jun

Perc

ent

ANZ Market Focus / 15 June 2015 / 8 of 17

INTEREST RATE STRATEGY

25% in NZD terms since early March, with few signals

of imminent recovery evident in whole milk powder

futures contracts.

GLOBAL YIELDS REMAIN VOLATILE Global bond yields have generally moved higher over

the past week and remain close to the top of recent

trading ranges. Investor expectations for higher

interest rates, thin liquidity, and elevated issuance of

corporate debt have been contributors. US 10-year

yields are around 50bp higher than in mid-April at

2.40%. The question that must be asked is, how high could yields go? Our expectation is that the rise in global yields will be gradual given that we

believe the global tightening cycle will be elongated,

gradual and cautious.

Thursday’s Fed meeting is effectively live and the US

activity data has been improving, but with the Fed

signalling to the market it will be taking its time, the

general consensus is for a September start to Fed fund

hikes. The tone of Thursday’s statement is expected to

be more upbeat relative to April but the published

growth and fed fund “dot plots” are likely to be shaded

down relative to March. The large gap between the Fed and market’s view argues for caution. While

we fully expect the Fed to hike in September, we

expect the cycle to be gradual, resulting in 10-year

yields remaining sub-3% until the end of 2017.

Policy support and a brittle global scene are also expected to cap rises in global yields. Yields for 10-

year German bunds at 0.83% were little changed over

the week, but are streets above the 0.08% April 20

low. Safe-haven demand, concerns over the Greek

situation, and signals that the ECB is unlikely to soon

withdraw QE have prevented a break higher. Yields for

the Eurozone periphery have blown out of late, but

remain low. This week’s BOJ meeting is expected to

see it maintain its commitment to increase the

monetary base by 80 trillion yen per annum. Activity

data has disappointed in China, with ANZ expecting a

further rate cut this month and a 100bp relaxation in

the RRR over the remainder of the year.

The increasingly stark divergence with local rates is

likely to result in a steeper local yield curve and tighter

spreads to other markets, particularly the US. New Zealand yields remain head and shoulders above those of comparable OECD economies and have the added advantage of being underpinned by a sound fiscal position. Last week’s $300m tender for

the April 2017 bond was well subscribed with a high bid

to cover ratio (3.74). The average yield at 3.87%

remained streets above rates on offer offshore, with

the weaker NZD making NZ assets cheaper. Hence, our

bias is for local rates to converge to (lower) global

yields.

PREFERRED STRATEGIES – BORROWERS Our preference is to watch and wait. Short-end rates

are biased lower given the strong likelihood of a follow-

up cut in the next few months. Long-end yields are still

comparatively low but the recent steepening in the

curve makes hedging a progressively less attractive

proposition for the majority of borrowers. Given that

we expect subsequent rises in global rates to be

gradual, borrowers have the luxury of waiting and

could benefit from a potential snap lower in yields if

that occurs. With the RBNZ in easing mode, we expect

local long-end interest rates to compress on a spread

to global rates, further containing the lift in local yields.

KEY VIEWS – FOR BORROWERS

GAUGE VIEW COMMENT

Hedge ratio Majority

hedged

Historic hedges more than

adequate. No immediate

reason to add to them now.

Value Cheap Longer-term rates are still low

despite recent climb.

Uncertainty Elevated

Global markets volatile and

policy outlook unclear, but rate

cuts here suggest caution.

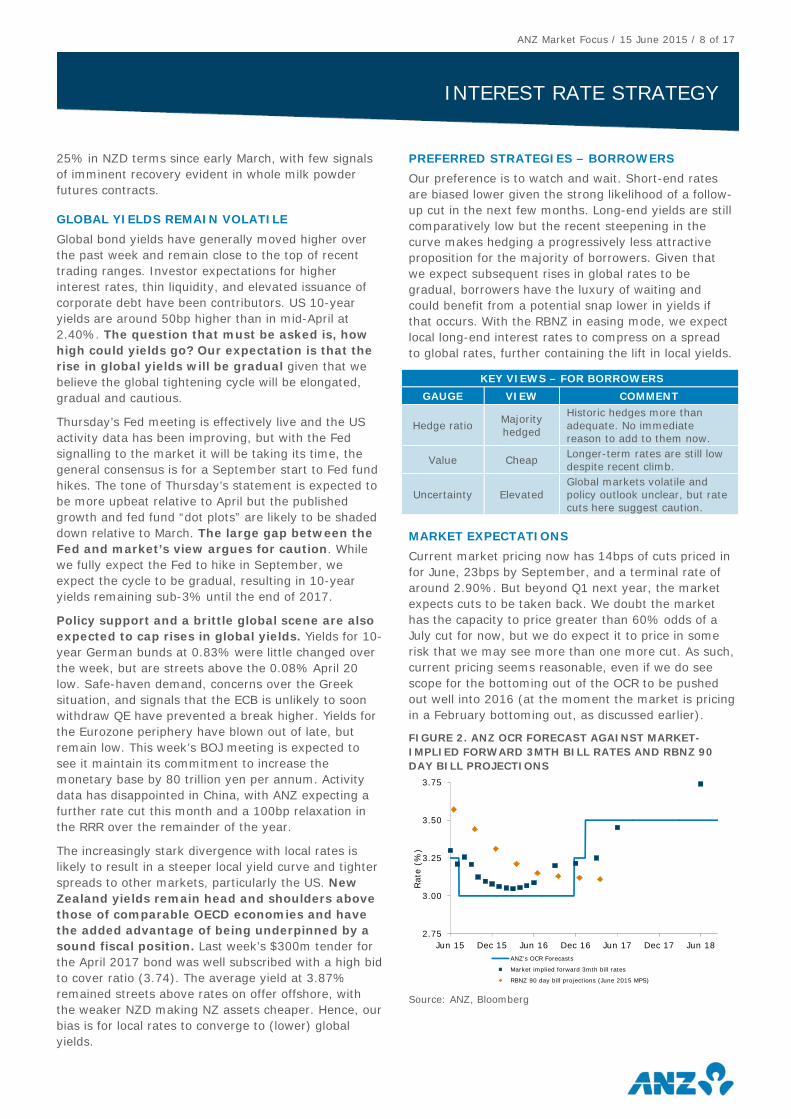

MARKET EXPECTATIONS

Current market pricing now has 14bps of cuts priced in

for June, 23bps by September, and a terminal rate of

around 2.90%. But beyond Q1 next year, the market

expects cuts to be taken back. We doubt the market

has the capacity to price greater than 60% odds of a

July cut for now, but we do expect it to price in some

risk that we may see more than one more cut. As such,

current pricing seems reasonable, even if we do see

scope for the bottoming out of the OCR to be pushed

out well into 2016 (at the moment the market is pricing

in a February bottoming out, as discussed earlier).

FIGURE 2. ANZ OCR FORECAST AGAINST MARKET-IMPLIED FORWARD 3MTH BILL RATES AND RBNZ 90 DAY BILL PROJECTIONS

Source: ANZ, Bloomberg

2.75

3.00

3.25

3.50

3.75

Jun 15 Dec 15 Jun 16 Dec 16 Jun 17 Dec 17 Jun 18

Rate

(%

)

ANZ's OCR Forecasts

Market implied forward 3mth bill rates

RBNZ 90 day bill projections (June 2015 MPS)

ANZ Market Focus / 15 June 2015 / 9 of 17

CURRENCY STRATEGY

SUMMARY Despite breaking below 0.70, the NZD/USD still has a

further adjustment to make to match the recent

declines in export prices. We are currently targeting

0.68, but the risks are for lower still. JPY weakness

may have run its course, capping NZD/JPY, as official

support for the JPY was noted last week. NZD/AUD has

only a small decline left before entering the technical

buy zone.

TABLE 1: KEY VIEWS CROSS WEEK MONTH YEAR

NZD/USD ↓ NZD downside

risks remain USD to strengthen

NZD/AUD ↔ Getting closer to

fair value Topside capped

NZD/EUR ↔/↑ EUR remains

weak EUR remains weak

NZD/GBP ↔/↓ GBP in demand GBP resurgence

NZD/JPY ↔/↓ Official support

for JPY. Yen weakness

THEMES AND RISKS ANZ expects the FOMC to present a more upbeat

assessment than they did in the April meeting.

This should be USD supportive.

Individual GDT auctions are less important for the

currency at present as the damage to dairy cash-

flow is largely locked in for the next six months. A

further decline this week would be noted by

markets.

Greece remains a challenge for EUR bulls, with

volatility likely to grow as deadlines near.

GBP remains strong as NZD/GBP challenges 2011

lows; we expect GBP to continue to strengthen.

The BoJ this week will be pivotal for JPY after

Governor Kuroda ‘called time’ on JPY declines.

TABLE 2: KEY UPCOMING EVENT RISK

EVENT WHEN (NZDT)

LIKELY IMPACT

AUD RBA Kent Mon 19:30 NZD/AUD ↑

USD June Empire Survey Tue 00:30 NZD/USD ↓

EUR ECB Draghi Tue 01:00 NZD/EUR ↑

AUD RBA Debelle Tue 09:55 NZD/AUD ↔ AUD RBA Minutes Tue 13:30 NZD/AUD ↓

EUR OMT court ruling Tue 19:30 NZD/EUR ↔/↓

GBP CPI, RPI, PPI Tue 20:30 NZD/GBP ↓

NZD GDT auction Wed am NZD ↔

NZD Q1 C/A Wed 10:45 NZD ↓

GBP May employment Wed 20:30 NZD/GBP ↓

USD FOMC Thu 06:00 NZD/USD ↓

NZD Q1 GDP Thu 10:45 NZD ↓

GBP May retail sales Thu 20:30 NZD/GBP ↓

USD Q1 C/A, May CPI Fri 00:30 NZD/USD ↓

USD Philadelphia Fed Fri 02:00 NZD/USD ↓

NZD ANZ Job Ads Fri 10:00 NZD ↑

NZD ANZ Consumer Conf. Fri 13:00 NZD ↓

JPY BoJ Fri PM NZD/JPY ↑

EXPORTERS’ STRATEGY

NZD/USD exporters should target close to 0.68.

NZD/AUD exporters should begin to think about

hedging at current levels.

IMPORTERS’ STRATEGY NZD/AUD importers should be able to sit back with

higher hedges in place; any bounce in NZD/USD will be

an opportunity for importers to hedge again.

DATA PULSE

The RBNZ cut the OCR and has an active easing bias.

The currency was front and centre of their thinking and

they saw a need for a “further significant downward adjustment” – we concur. NZ data is

backing up the case for a currency decline with the

ANZ Truckometer declining for a fifth month, and the

ANZ monthly inflation gauge recording its second

consecutive decline. It is too early for QV and REINZ

data to show the impact of RBNZ and Government

measures, but the Auckland vs NZ divide is growing.

Chinese data remains a downside risk for the NZD,

as weak imports and sluggish activity data suggest

China may miss its 7% Q2 GDP target. Chinese

inflation remains absent, although there are some

signs of improvement, with aggregate financing

increasing. The Bank of Korea cut rates again, as

economic weakness remains an Asian theme.

RBA Governor Stevens expressed concern over the

efficacy of further policy actions, while things were

looking up with NAB Business confidence and May employment both supporting AUD.

British data continues to support the GBP, while EUR

data remains mixed and Greece is a concern.

US retail sales showed a solid (late) spring bounce and

Michigan Confidence improved supporting USD.

TABLE 3: NZD VS AUD: MONTHLY GAUGES GAUGE GUIDE COMMENT

Fair value ↔ Still above fair value.

Yield ↔/↓ Yield outlook reversing.

Commodities ↔/↓ Iron ore stabilising.

Data ↓ AU data somewhat stabilised.

Techs ↔ Sitting on support.

Sentiment ↔/↓ NZD sentiment more negative.

Other ↓ Strong momentum lower.

On balance ↔/↓ Downside risks are easing. TABLE 4: NZD VS USD: MONTHLY GAUGES

GAUGE GUIDE COMMENT Fair value ↔ Closer to fair value.

Yield ↔ Yield advantage being cut.

Commodities ↓ Dairy still concerning.

Risk aversion ↓ Chinese and global growth fears.

Data ↓ NZ data rolling over.

Techs ↓ Breakdown not yet over. Other ↓ USD picking up momentum.

On balance ↔/↓ NZD still has downside.

ANZ Market Focus / 15 June 2015 / 10 of 17

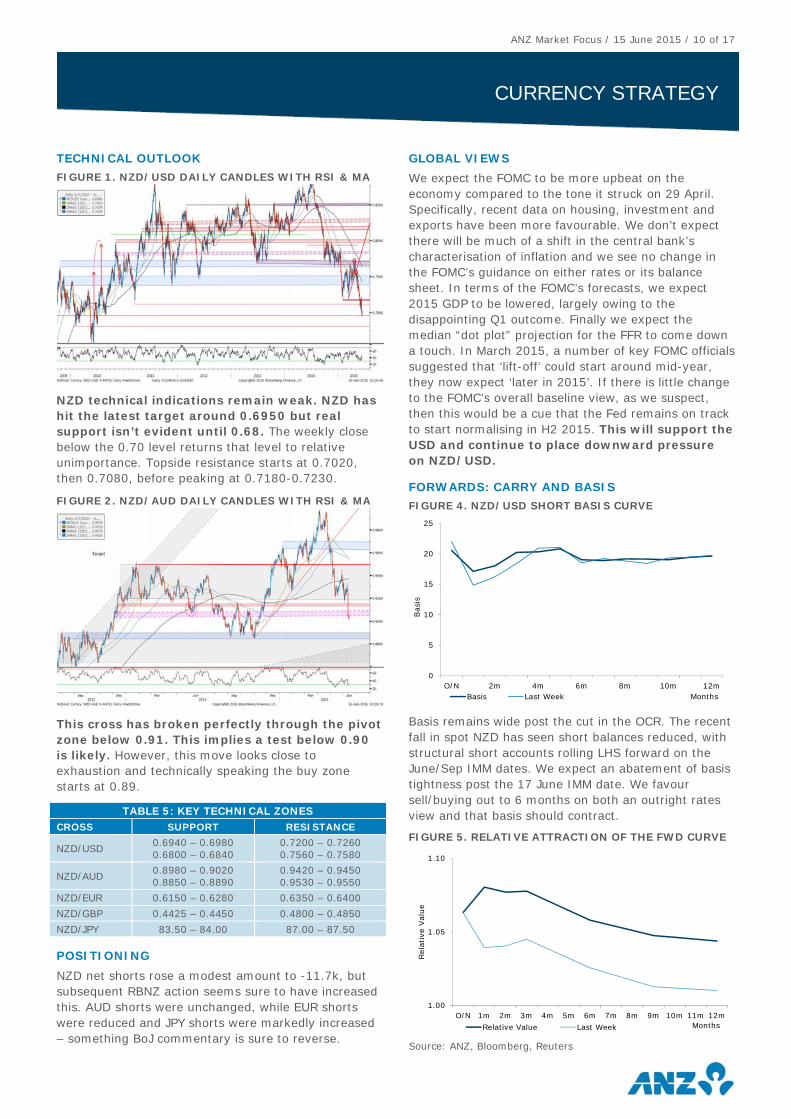

CURRENCY STRATEGY

TECHNICAL OUTLOOK FIGURE 1. NZD/USD DAILY CANDLES WITH RSI & MA

NZD technical indications remain weak. NZD has hit the latest target around 0.6950 but real support isn’t evident until 0.68. The weekly close

below the 0.70 level returns that level to relative

unimportance. Topside resistance starts at 0.7020,

then 0.7080, before peaking at 0.7180-0.7230.

FIGURE 2. NZD/AUD DAILY CANDLES WITH RSI & MA

This cross has broken perfectly through the pivot zone below 0.91. This implies a test below 0.90 is likely. However, this move looks close to

exhaustion and technically speaking the buy zone

starts at 0.89.

TABLE 5: KEY TECHNICAL ZONES CROSS SUPPORT RESISTANCE

NZD/USD 0.6940 – 0.6980

0.6800 – 0.6840

0.7200 – 0.7260

0.7560 – 0.7580

NZD/AUD 0.8980 – 0.9020 0.8850 – 0.8890

0.9420 – 0.9450 0.9530 – 0.9550

NZD/EUR 0.6150 – 0.6280 0.6350 – 0.6400

NZD/GBP 0.4425 – 0.4450 0.4800 – 0.4850

NZD/JPY 83.50 – 84.00 87.00 – 87.50

POSITIONING NZD net shorts rose a modest amount to -11.7k, but

subsequent RBNZ action seems sure to have increased

this. AUD shorts were unchanged, while EUR shorts

were reduced and JPY shorts were markedly increased

– something BoJ commentary is sure to reverse.

GLOBAL VIEWS We expect the FOMC to be more upbeat on the

economy compared to the tone it struck on 29 April.

Specifically, recent data on housing, investment and

exports have been more favourable. We don’t expect

there will be much of a shift in the central bank’s

characterisation of inflation and we see no change in

the FOMC’s guidance on either rates or its balance

sheet. In terms of the FOMC’s forecasts, we expect

2015 GDP to be lowered, largely owing to the

disappointing Q1 outcome. Finally we expect the

median “dot plot” projection for the FFR to come down

a touch. In March 2015, a number of key FOMC officials

suggested that ‘lift-off’ could start around mid-year,

they now expect ‘later in 2015’. If there is little change

to the FOMC’s overall baseline view, as we suspect,

then this would be a cue that the Fed remains on track

to start normalising in H2 2015. This will support the USD and continue to place downward pressure on NZD/USD.

FORWARDS: CARRY AND BASIS FIGURE 4. NZD/USD SHORT BASIS CURVE

Basis remains wide post the cut in the OCR. The recent

fall in spot NZD has seen short balances reduced, with

structural short accounts rolling LHS forward on the

June/Sep IMM dates. We expect an abatement of basis

tightness post the 17 June IMM date. We favour

sell/buying out to 6 months on both an outright rates

view and that basis should contract.

FIGURE 5. RELATIVE ATTRACTION OF THE FWD CURVE

Source: ANZ, Bloomberg, Reuters

0

5

10

15

20

25

O/N 2m 4m 6m 8m 10m 12m

Basis

MonthsBasis Last Week

1.00

1.05

1.10

O/N 1m 2m 3m 4m 5m 6m 7m 8m 9m 10m 11m 12m

Rela

tive V

alu

e

MonthsRelative Value Last Week

ANZ Market Focus / 15 June 2015 / 11 of 17

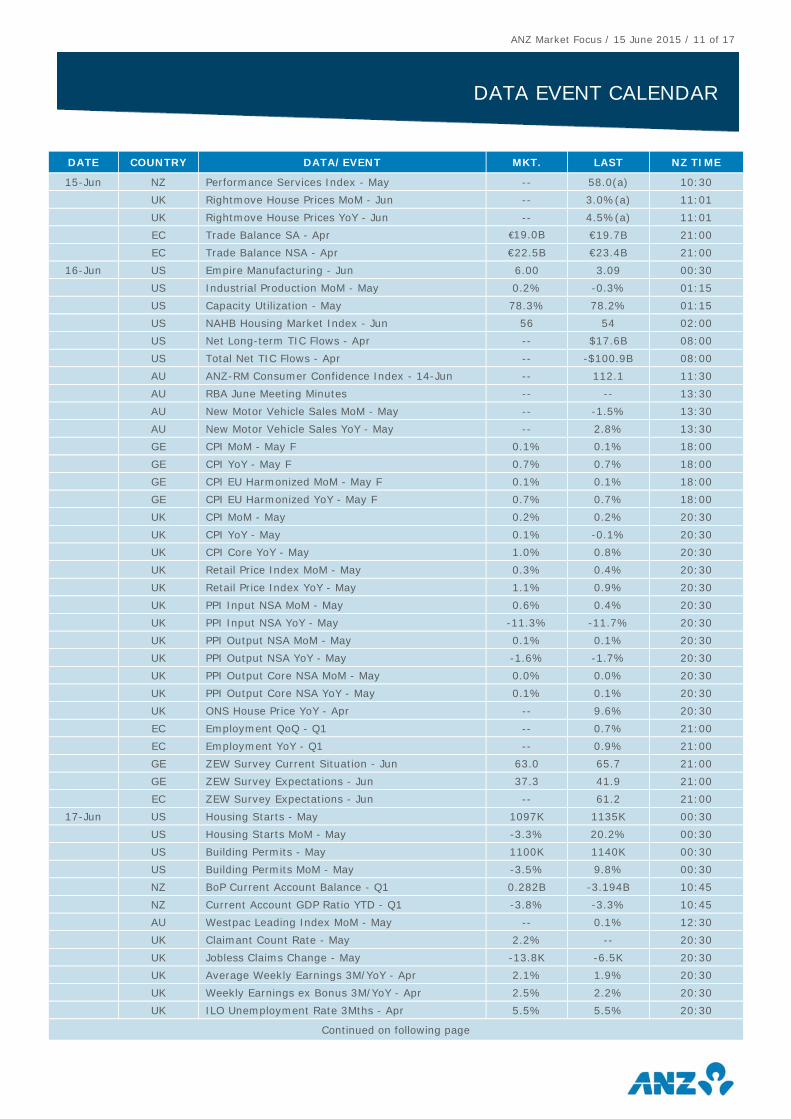

DATA EVENT CALENDAR

DATE COUNTRY DATA/EVENT MKT. LAST NZ TIME

15-Jun NZ Performance Services Index - May -- 58.0(a) 10:30

UK Rightmove House Prices MoM - Jun -- 3.0%(a) 11:01

UK Rightmove House Prices YoY - Jun -- 4.5%(a) 11:01

EC Trade Balance SA - Apr €19.0B €19.7B 21:00

EC Trade Balance NSA - Apr €22.5B €23.4B 21:00

16-Jun US Empire Manufacturing - Jun 6.00 3.09 00:30

US Industrial Production MoM - May 0.2% -0.3% 01:15

US Capacity Utilization - May 78.3% 78.2% 01:15

US NAHB Housing Market Index - Jun 56 54 02:00

US Net Long-term TIC Flows - Apr -- $17.6B 08:00

US Total Net TIC Flows - Apr -- -$100.9B 08:00

AU ANZ-RM Consumer Confidence Index - 14-Jun -- 112.1 11:30

AU RBA June Meeting Minutes -- -- 13:30

AU New Motor Vehicle Sales MoM - May -- -1.5% 13:30

AU New Motor Vehicle Sales YoY - May -- 2.8% 13:30

GE CPI MoM - May F 0.1% 0.1% 18:00

GE CPI YoY - May F 0.7% 0.7% 18:00

GE CPI EU Harmonized MoM - May F 0.1% 0.1% 18:00

GE CPI EU Harmonized YoY - May F 0.7% 0.7% 18:00

UK CPI MoM - May 0.2% 0.2% 20:30

UK CPI YoY - May 0.1% -0.1% 20:30

UK CPI Core YoY - May 1.0% 0.8% 20:30

UK Retail Price Index MoM - May 0.3% 0.4% 20:30

UK Retail Price Index YoY - May 1.1% 0.9% 20:30

UK PPI Input NSA MoM - May 0.6% 0.4% 20:30

UK PPI Input NSA YoY - May -11.3% -11.7% 20:30

UK PPI Output NSA MoM - May 0.1% 0.1% 20:30

UK PPI Output NSA YoY - May -1.6% -1.7% 20:30

UK PPI Output Core NSA MoM - May 0.0% 0.0% 20:30

UK PPI Output Core NSA YoY - May 0.1% 0.1% 20:30

UK ONS House Price YoY - Apr -- 9.6% 20:30

EC Employment QoQ - Q1 -- 0.7% 21:00

EC Employment YoY - Q1 -- 0.9% 21:00

GE ZEW Survey Current Situation - Jun 63.0 65.7 21:00

GE ZEW Survey Expectations - Jun 37.3 41.9 21:00

EC ZEW Survey Expectations - Jun -- 61.2 21:00

17-Jun US Housing Starts - May 1097K 1135K 00:30

US Housing Starts MoM - May -3.3% 20.2% 00:30

US Building Permits - May 1100K 1140K 00:30

US Building Permits MoM - May -3.5% 9.8% 00:30

NZ BoP Current Account Balance - Q1 0.282B -3.194B 10:45

NZ Current Account GDP Ratio YTD - Q1 -3.8% -3.3% 10:45

AU Westpac Leading Index MoM - May -- 0.1% 12:30

UK Claimant Count Rate - May 2.2% -- 20:30

UK Jobless Claims Change - May -13.8K -6.5K 20:30

UK Average Weekly Earnings 3M/YoY - Apr 2.1% 1.9% 20:30

UK Weekly Earnings ex Bonus 3M/YoY - Apr 2.5% 2.2% 20:30

UK ILO Unemployment Rate 3Mths - Apr 5.5% 5.5% 20:30

Continued on following page

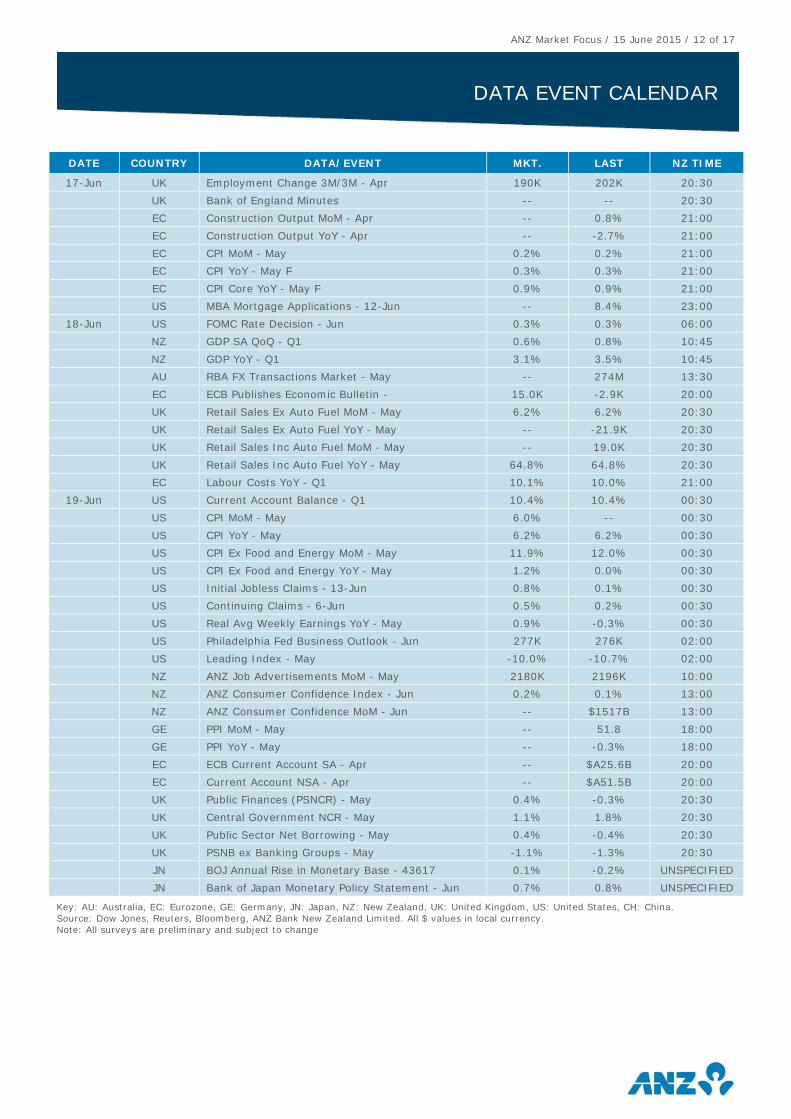

ANZ Market Focus / 15 June 2015 / 12 of 17

DATA EVENT CALENDAR

Key: AU: Australia, EC: Eurozone, GE: Germany, JN: Japan, NZ: New Zealand, UK: United Kingdom, US: United States, CH: China. Source: Dow Jones, Reuters, Bloomberg, ANZ Bank New Zealand Limited. All $ values in local currency. Note: All surveys are preliminary and subject to change

DATE COUNTRY DATA/EVENT MKT. LAST NZ TIME

17-Jun UK Employment Change 3M/3M - Apr 190K 202K 20:30

UK Bank of England Minutes -- -- 20:30

EC Construction Output MoM - Apr -- 0.8% 21:00

EC Construction Output YoY - Apr -- -2.7% 21:00

EC CPI MoM - May 0.2% 0.2% 21:00

EC CPI YoY - May F 0.3% 0.3% 21:00

EC CPI Core YoY - May F 0.9% 0.9% 21:00

US MBA Mortgage Applications - 12-Jun -- 8.4% 23:00

18-Jun US FOMC Rate Decision - Jun 0.3% 0.3% 06:00

NZ GDP SA QoQ - Q1 0.6% 0.8% 10:45

NZ GDP YoY - Q1 3.1% 3.5% 10:45

AU RBA FX Transactions Market - May -- 274M 13:30

EC ECB Publishes Economic Bulletin - 15.0K -2.9K 20:00

UK Retail Sales Ex Auto Fuel MoM - May 6.2% 6.2% 20:30

UK Retail Sales Ex Auto Fuel YoY - May -- -21.9K 20:30

UK Retail Sales Inc Auto Fuel MoM - May -- 19.0K 20:30

UK Retail Sales Inc Auto Fuel YoY - May 64.8% 64.8% 20:30

EC Labour Costs YoY - Q1 10.1% 10.0% 21:00

19-Jun US Current Account Balance - Q1 10.4% 10.4% 00:30

US CPI MoM - May 6.0% -- 00:30

US CPI YoY - May 6.2% 6.2% 00:30

US CPI Ex Food and Energy MoM - May 11.9% 12.0% 00:30

US CPI Ex Food and Energy YoY - May 1.2% 0.0% 00:30

US Initial Jobless Claims - 13-Jun 0.8% 0.1% 00:30

US Continuing Claims - 6-Jun 0.5% 0.2% 00:30

US Real Avg Weekly Earnings YoY - May 0.9% -0.3% 00:30

US Philadelphia Fed Business Outlook - Jun 277K 276K 02:00

US Leading Index - May -10.0% -10.7% 02:00

NZ ANZ Job Advertisements MoM - May 2180K 2196K 10:00

NZ ANZ Consumer Confidence Index - Jun 0.2% 0.1% 13:00

NZ ANZ Consumer Confidence MoM - Jun -- $1517B 13:00

GE PPI MoM - May -- 51.8 18:00

GE PPI YoY - May -- -0.3% 18:00

EC ECB Current Account SA - Apr -- $A25.6B 20:00

EC Current Account NSA - Apr -- $A51.5B 20:00

UK Public Finances (PSNCR) - May 0.4% -0.3% 20:30

UK Central Government NCR - May 1.1% 1.8% 20:30

UK Public Sector Net Borrowing - May 0.4% -0.4% 20:30

UK PSNB ex Banking Groups - May -1.1% -1.3% 20:30

JN BOJ Annual Rise in Monetary Base - 43617 0.1% -0.2% UNSPECIFIED

JN Bank of Japan Monetary Policy Statement - Jun 0.7% 0.8% UNSPECIFIED

ANZ Market Focus / 15 June 2015 / 13 of 17

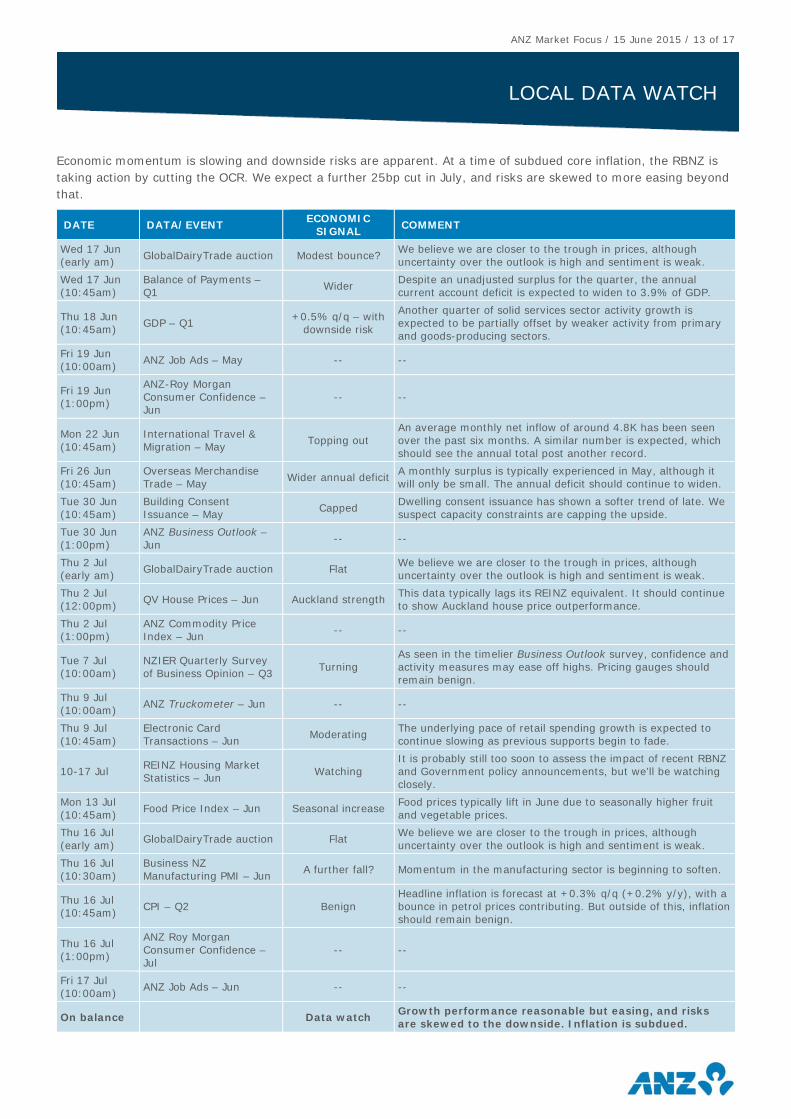

LOCAL DATA WATCH

Economic momentum is slowing and downside risks are apparent. At a time of subdued core inflation, the RBNZ is

taking action by cutting the OCR. We expect a further 25bp cut in July, and risks are skewed to more easing beyond

that.

DATE DATA/EVENT ECONOMIC SIGNAL COMMENT

Wed 17 Jun

(early am) GlobalDairyTrade auction Modest bounce?

We believe we are closer to the trough in prices, although

uncertainty over the outlook is high and sentiment is weak.

Wed 17 Jun

(10:45am)

Balance of Payments –

Q1 Wider

Despite an unadjusted surplus for the quarter, the annual

current account deficit is expected to widen to 3.9% of GDP.

Thu 18 Jun

(10:45am) GDP – Q1

+0.5% q/q – with

downside risk

Another quarter of solid services sector activity growth is

expected to be partially offset by weaker activity from primary

and goods-producing sectors.

Fri 19 Jun

(10:00am) ANZ Job Ads – May -- --

Fri 19 Jun

(1:00pm)

ANZ-Roy Morgan

Consumer Confidence –

Jun

-- --

Mon 22 Jun

(10:45am)

International Travel &

Migration – May Topping out

An average monthly net inflow of around 4.8K has been seen

over the past six months. A similar number is expected, which

should see the annual total post another record.

Fri 26 Jun

(10:45am)

Overseas Merchandise

Trade – May Wider annual deficit

A monthly surplus is typically experienced in May, although it

will only be small. The annual deficit should continue to widen.

Tue 30 Jun

(10:45am)

Building Consent

Issuance – May Capped

Dwelling consent issuance has shown a softer trend of late. We

suspect capacity constraints are capping the upside.

Tue 30 Jun

(1:00pm)

ANZ Business Outlook –

Jun -- --

Thu 2 Jul

(early am) GlobalDairyTrade auction Flat

We believe we are closer to the trough in prices, although

uncertainty over the outlook is high and sentiment is weak.

Thu 2 Jul

(12:00pm) QV House Prices – Jun Auckland strength

This data typically lags its REINZ equivalent. It should continue

to show Auckland house price outperformance.

Thu 2 Jul

(1:00pm)

ANZ Commodity Price

Index – Jun -- --

Tue 7 Jul

(10:00am)

NZIER Quarterly Survey

of Business Opinion – Q3 Turning

As seen in the timelier Business Outlook survey, confidence and

activity measures may ease off highs. Pricing gauges should

remain benign.

Thu 9 Jul

(10:00am) ANZ Truckometer – Jun -- --

Thu 9 Jul

(10:45am)

Electronic Card

Transactions – Jun Moderating

The underlying pace of retail spending growth is expected to

continue slowing as previous supports begin to fade.

10-17 Jul REINZ Housing Market

Statistics – Jun Watching

It is probably still too soon to assess the impact of recent RBNZ

and Government policy announcements, but we’ll be watching

closely.

Mon 13 Jul

(10:45am) Food Price Index – Jun Seasonal increase

Food prices typically lift in June due to seasonally higher fruit

and vegetable prices.

Thu 16 Jul

(early am) GlobalDairyTrade auction Flat

We believe we are closer to the trough in prices, although

uncertainty over the outlook is high and sentiment is weak.

Thu 16 Jul

(10:30am)

Business NZ

Manufacturing PMI – Jun A further fall? Momentum in the manufacturing sector is beginning to soften.

Thu 16 Jul

(10:45am) CPI – Q2 Benign

Headline inflation is forecast at +0.3% q/q (+0.2% y/y), with a

bounce in petrol prices contributing. But outside of this, inflation

should remain benign.

Thu 16 Jul

(1:00pm)

ANZ Roy Morgan

Consumer Confidence –

Jul

-- --

Fri 17 Jul

(10:00am) ANZ Job Ads – Jun -- --

On balance Data watch Growth performance reasonable but easing, and risks are skewed to the downside. Inflation is subdued.

ANZ Market Focus / 15 June 2015 / 14 of 17

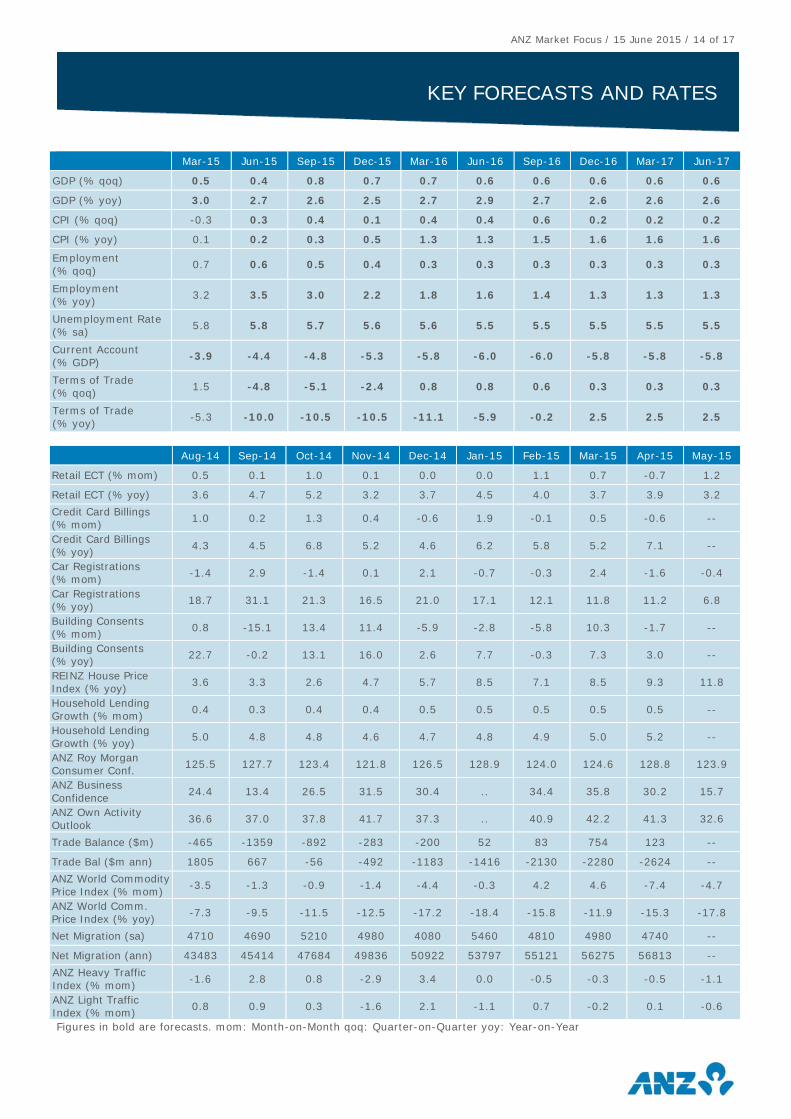

KEY FORECASTS AND RATES

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17

GDP (% qoq) 0.5 0.4 0.8 0.7 0.7 0.6 0.6 0.6 0.6 0.6

GDP (% yoy) 3.0 2.7 2.6 2.5 2.7 2.9 2.7 2.6 2.6 2.6

CPI (% qoq) -0.3 0.3 0.4 0.1 0.4 0.4 0.6 0.2 0.2 0.2

CPI (% yoy) 0.1 0.2 0.3 0.5 1.3 1.3 1.5 1.6 1.6 1.6

Employment

(% qoq) 0.7 0.6 0.5 0.4 0.3 0.3 0.3 0.3 0.3 0.3

Employment

(% yoy) 3.2 3.5 3.0 2.2 1.8 1.6 1.4 1.3 1.3 1.3

Unemployment Rate

(% sa) 5.8 5.8 5.7 5.6 5.6 5.5 5.5 5.5 5.5 5.5

Current Account

(% GDP) -3.9 -4.4 -4.8 -5.3 -5.8 -6.0 -6.0 -5.8 -5.8 -5.8

Terms of Trade

(% qoq) 1.5 -4.8 -5.1 -2.4 0.8 0.8 0.6 0.3 0.3 0.3

Terms of Trade

(% yoy) -5.3 -10.0 -10.5 -10.5 -11.1 -5.9 -0.2 2.5 2.5 2.5

Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15

Retail ECT (% mom) 0.5 0.1 1.0 0.1 0.0 0.0 1.1 0.7 -0.7 1.2

Retail ECT (% yoy) 3.6 4.7 5.2 3.2 3.7 4.5 4.0 3.7 3.9 3.2

Credit Card Billings

(% mom) 1.0 0.2 1.3 0.4 -0.6 1.9 -0.1 0.5 -0.6 --

Credit Card Billings

(% yoy) 4.3 4.5 6.8 5.2 4.6 6.2 5.8 5.2 7.1 --

Car Registrations

(% mom) -1.4 2.9 -1.4 0.1 2.1 -0.7 -0.3 2.4 -1.6 -0.4

Car Registrations

(% yoy) 18.7 31.1 21.3 16.5 21.0 17.1 12.1 11.8 11.2 6.8

Building Consents

(% mom) 0.8 -15.1 13.4 11.4 -5.9 -2.8 -5.8 10.3 -1.7 --

Building Consents

(% yoy) 22.7 -0.2 13.1 16.0 2.6 7.7 -0.3 7.3 3.0 --

REINZ House Price

Index (% yoy) 3.6 3.3 2.6 4.7 5.7 8.5 7.1 8.5 9.3 11.8

Household Lending

Growth (% mom) 0.4 0.3 0.4 0.4 0.5 0.5 0.5 0.5 0.5 --

Household Lending

Growth (% yoy) 5.0 4.8 4.8 4.6 4.7 4.8 4.9 5.0 5.2 --

ANZ Roy Morgan

Consumer Conf. 125.5 127.7 123.4 121.8 126.5 128.9 124.0 124.6 128.8 123.9

ANZ Business

Confidence 24.4 13.4 26.5 31.5 30.4 .. 34.4 35.8 30.2 15.7

ANZ Own Activity

Outlook 36.6 37.0 37.8 41.7 37.3 .. 40.9 42.2 41.3 32.6

Trade Balance ($m) -465 -1359 -892 -283 -200 52 83 754 123 --

Trade Bal ($m ann) 1805 667 -56 -492 -1183 -1416 -2130 -2280 -2624 --

ANZ World Commodity

Price Index (% mom) -3.5 -1.3 -0.9 -1.4 -4.4 -0.3 4.2 4.6 -7.4 -4.7

ANZ World Comm.

Price Index (% yoy) -7.3 -9.5 -11.5 -12.5 -17.2 -18.4 -15.8 -11.9 -15.3 -17.8

Net Migration (sa) 4710 4690 5210 4980 4080 5460 4810 4980 4740 --

Net Migration (ann) 43483 45414 47684 49836 50922 53797 55121 56275 56813 --

ANZ Heavy Traffic

Index (% mom) -1.6 2.8 0.8 -2.9 3.4 0.0 -0.5 -0.3 -0.5 -1.1

ANZ Light Traffic

Index (% mom) 0.8 0.9 0.3 -1.6 2.1 -1.1 0.7 -0.2 0.1 -0.6

Figures in bold are forecasts. mom: Month-on-Month qoq: Quarter-on-Quarter yoy: Year-on-Year

ANZ Market Focus / 15 June 2015 / 15 of 17

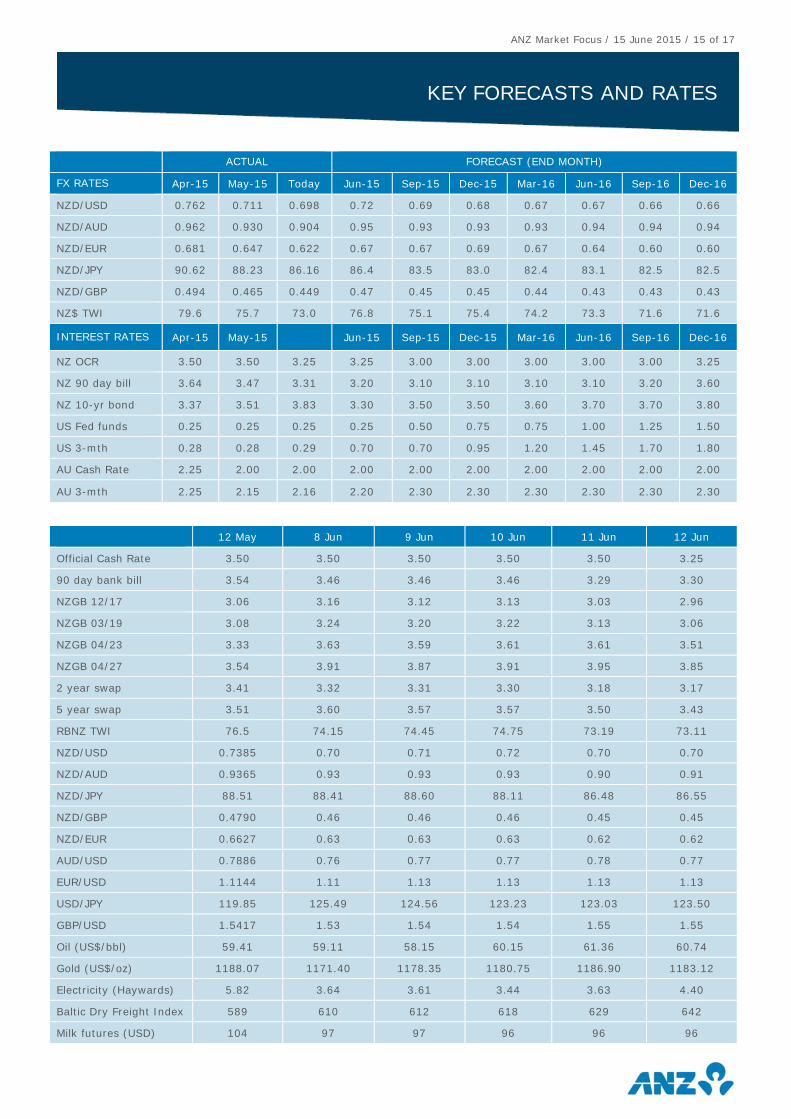

KEY FORECASTS AND RATES

ACTUAL FORECAST (END MONTH)

FX RATES Apr-15 May-15 Today Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

NZD/USD 0.762 0.711 0.698 0.72 0.69 0.68 0.67 0.67 0.66 0.66

NZD/AUD 0.962 0.930 0.904 0.95 0.93 0.93 0.93 0.94 0.94 0.94

NZD/EUR 0.681 0.647 0.622 0.67 0.67 0.69 0.67 0.64 0.60 0.60

NZD/JPY 90.62 88.23 86.16 86.4 83.5 83.0 82.4 83.1 82.5 82.5

NZD/GBP 0.494 0.465 0.449 0.47 0.45 0.45 0.44 0.43 0.43 0.43

NZ$ TWI 79.6 75.7 73.0 76.8 75.1 75.4 74.2 73.3 71.6 71.6

INTEREST RATES Apr-15 May-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

NZ OCR 3.50 3.50 3.25 3.25 3.00 3.00 3.00 3.00 3.00 3.25

NZ 90 day bill 3.64 3.47 3.31 3.20 3.10 3.10 3.10 3.10 3.20 3.60

NZ 10-yr bond 3.37 3.51 3.83 3.30 3.50 3.50 3.60 3.70 3.70 3.80

US Fed funds 0.25 0.25 0.25 0.25 0.50 0.75 0.75 1.00 1.25 1.50

US 3-mth 0.28 0.28 0.29 0.70 0.70 0.95 1.20 1.45 1.70 1.80

AU Cash Rate 2.25 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00

AU 3-mth 2.25 2.15 2.16 2.20 2.30 2.30 2.30 2.30 2.30 2.30

12 May 8 Jun 9 Jun 10 Jun 11 Jun 12 Jun

Official Cash Rate 3.50 3.50 3.50 3.50 3.50 3.25

90 day bank bill 3.54 3.46 3.46 3.46 3.29 3.30

NZGB 12/17 3.06 3.16 3.12 3.13 3.03 2.96

NZGB 03/19 3.08 3.24 3.20 3.22 3.13 3.06

NZGB 04/23 3.33 3.63 3.59 3.61 3.61 3.51

NZGB 04/27 3.54 3.91 3.87 3.91 3.95 3.85

2 year swap 3.41 3.32 3.31 3.30 3.18 3.17

5 year swap 3.51 3.60 3.57 3.57 3.50 3.43

RBNZ TWI 76.5 74.15 74.45 74.75 73.19 73.11

NZD/USD 0.7385 0.70 0.71 0.72 0.70 0.70

NZD/AUD 0.9365 0.93 0.93 0.93 0.90 0.91

NZD/JPY 88.51 88.41 88.60 88.11 86.48 86.55

NZD/GBP 0.4790 0.46 0.46 0.46 0.45 0.45

NZD/EUR 0.6627 0.63 0.63 0.63 0.62 0.62

AUD/USD 0.7886 0.76 0.77 0.77 0.78 0.77

EUR/USD 1.1144 1.11 1.13 1.13 1.13 1.13

USD/JPY 119.85 125.49 124.56 123.23 123.03 123.50

GBP/USD 1.5417 1.53 1.54 1.54 1.55 1.55

Oil (US$/bbl) 59.41 59.11 58.15 60.15 61.36 60.74

Gold (US$/oz) 1188.07 1171.40 1178.35 1180.75 1186.90 1183.12

Electricity (Haywards) 5.82 3.64 3.61 3.44 3.63 4.40

Baltic Dry Freight Index 589 610 612 618 629 642

Milk futures (USD) 104 97 97 96 96 96

ANZ Market Focus / 15 June 2015 / 16 of 17

IMPORTANT NOTICE

The distribution of this document or streaming of this video broadcast (as applicable, “publication”) may be restricted by law in certain jurisdictions. Persons who receive this publication must inform themselves about and observe all relevant restrictions.

1. Disclaimer for all jurisdictions, where content is authored by ANZ Research: Except if otherwise specified in section 2 below, this publication is issued and distributed in your country/region by Australia and New Zealand Banking Group Limited (ABN 11 005 357 522) (“ANZ”), on the basis that it is only for the information of the specified recipient or permitted user of the relevant website (collectively, “recipient”). This publication may not be reproduced, distributed or published by any recipient for any purpose. It is general information and has been prepared without taking into account the objectives, financial situation or needs of any person. Nothing in this publication is intended to be an offer to sell, or a solicitation of an offer to buy, any product, instrument or investment, to effect any transaction or to conclude any legal act of any kind. If, despite the foregoing, any services or products referred to in this publication are deemed to be offered in the jurisdiction in which this publication is received or accessed, no such service or product is intended for nor available to persons resident in that jurisdiction if it would be contradictory to local law or regulation. Such local laws, regulations and other limitations always apply with non-exclusive jurisdiction of local courts. Certain financial products may be subject to mandatory clearing, regulatory reporting and/or other related obligations. These obligations may vary by jurisdiction and be subject to frequent amendment. Before making an investment decision, recipients should seek independent financial, legal, tax and other relevant advice having regard to their particular circumstances. The views and recommendations expressed in this publication are the author’s. They are based on information known by the author and on sources which the author believes to be reliable, but may involve material elements of subjective judgement and analysis. Unless specifically stated otherwise: they are current on the date of this publication and are subject to change without notice; and, all price information is indicative only. Any of the views and recommendations which comprise estimates, forecasts or other projections, are subject to significant uncertainties and contingencies that cannot reasonably be anticipated. On this basis, such views and recommendations may not always be achieved or prove to be correct. Indications of past performance in this publication will not necessarily be repeated in the future. No representation is being made that any investment will or is likely to achieve profits or losses similar to those achieved in the past, or that significant losses will be avoided. Additionally, this publication may contain ‘forward looking statements’. Actual events or results or actual performance may differ materially from those reflected or contemplated in such forward looking statements. All investments entail a risk and may result in both profits and losses. Foreign currency rates of exchange may adversely affect the value, price or income of any products or services described in this publication. The products and services described in this publication are not suitable for all investors, and transacting in these products or services may be considered risky. ANZ and its related bodies corporate and affiliates, and the officers, employees, contractors and agents of each of them (including the author) (“Affiliates”), do not make any representation as to the accuracy, completeness or currency of the views or recommendations expressed in this publication. Neither ANZ nor its Affiliates accept any responsibility to inform you of any matter that subsequently comes to their notice, which may affect the accuracy, completeness or currency of the information in this publication. Except as required by law, and only to the extent so required: neither ANZ nor its Affiliates warrant or guarantee the performance of any of the products or services described in this publication or any return on any associated investment; and, ANZ and its Affiliates expressly disclaim any responsibility and shall not be liable for any loss, damage, claim, liability, proceedings, cost or expense (“Liability”) arising directly or indirectly and whether in tort (including negligence), contract, equity or otherwise out of or in connection with this publication. If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. ANZ and its Affiliates do not accept any Liability as a result of electronic transmission of this publication. ANZ and its Affiliates may have an interest in the subject matter of this publication as follows: They may receive fees from customers for dealing in the products or services described in this publication, and their staff and introducers

of business may share in such fees or receive a bonus that may be influenced by total sales. They or their customers may have or have had interests or long or short positions in the products or services described in this

publication, and may at any time make purchases and/or sales in them as principal or agent. They may act or have acted as market-maker in products described in this publication. ANZ and its Affiliates may rely on information barriers and other arrangements to control the flow of information contained in one or more business areas within ANZ or within its Affiliates into other business areas of ANZ or of its Affiliates. Please contact your ANZ point of contact with any questions about this publication including for further information on these disclosures of interest.

2. Country/region specific information: Australia. This publication is distributed in Australia by ANZ. ANZ holds an Australian Financial Services licence no. 234527. A copy of ANZ's Financial Services Guide is available at http://www.anz.com/documents/AU/aboutANZ/FinancialServicesGuide.pdf and is available upon request from your ANZ point of contact. If trading strategies or recommendations are included in this publication, they are solely for the information of ‘wholesale clients’ (as defined in section 761G of the Corporations Act 2001 Cth). Persons who receive this publication must inform themselves about and observe all relevant restrictions. Brazil. This publication is distributed in Brazil by ANZ on a cross border basis and only following request by the recipient. No securities are being offered or sold in Brazil under this publication, and no securities have been and will not be registered with the Securities Commission - CVM. Brunei. Japan. Kuwait. Malaysia. Switzerland. Taiwan. This publication is distributed in each of Brunei, Japan, Kuwait, Malaysia, Switzerland and Taiwan by ANZ on a cross-border basis. European Economic Area (“EEA”): United Kingdom. ANZ in the United Kingdom is authorised by the Prudential Regulation Authority (“PRA”). Subject to regulation by the Financial Conduct Authority (“FCA”) and limited regulation by the PRA. Details about the extent of our regulation by the PRA are available from us on request. This publication is distributed in the United Kingdom by ANZ solely for the information of persons who would come within the FCA definition of “eligible counterparty” or “professional client”. It is not intended for and must not be distributed to any person who would come within the FCA definition of “retail client”. Nothing here excludes or restricts any duty or liability to a customer which ANZ may have under the UK Financial Services and Markets Act 2000 or under the regulatory system as defined in the Rules of the PRA and the FCA. Germany. This publication is distributed in Germany by the Frankfurt Branch of ANZ solely for the information of its clients. Other EEA countries. This publication is distributed in the EEA by ANZ Bank (Europe) Limited (“ANZBEL”) which is authorised by the PRA and regulated by the FCA and the PRA in the United Kingdom, to persons who would come within the FCA definition of “eligible counterparty” or “professional client” in other countries in the EEA. This publication is distributed in those countries solely for the information of such persons upon their request. It is not intended for, and must not be distributed to, any person in those countries who would come within the FCA definition of “retail client”. Fiji. For Fiji regulatory purposes, this publication and any views and recommendations are not to be deemed as investment advice. Fiji investors must seek licensed professional advice should they wish to make any investment in relation to this publication. Hong Kong. This publication is distributed in Hong Kong by the Hong Kong branch of ANZ, which is registered at the Hong Kong Monetary Authority to conduct Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) regulated activities. The contents of this publication have not been reviewed by any regulatory authority in Hong Kong. If in doubt about the contents of this publication, you should obtain independent professional advice. India. This publication is distributed in India by ANZ on a cross-border basis. If this publication is received in India, only you (the specified recipient) may print it provided that before doing so, you specify on it your name and place of printing. Further copying or duplication of this publication is strictly prohibited.

ANZ Market Focus / 15 June 2015 / 17 of 17

IMPORTANT NOTICE