Embed Size (px)

Citation preview

22/10/2014

1

The Future Challenges for Global expansion:

Uncertain grounds Tenuous pathways

Gayle Allard

IE Business School

Seoul, October 2014

The financial crisis was one of the worst in history…

22/10/2014

2

...and the world will feel its effects for some time

• Developed nations face

– High debt and painful deleveraging

– Rising inequality

– A search for competitiveness and sources of growth

• The emerging world also faces difficult issues:

– Sharp slowdown and financial instability in China, other BRICS

– Conflict in the Middle East and Ukraine

– Disease, instability in Africa

The United States is leading the way back to global growth

22/10/2014

3

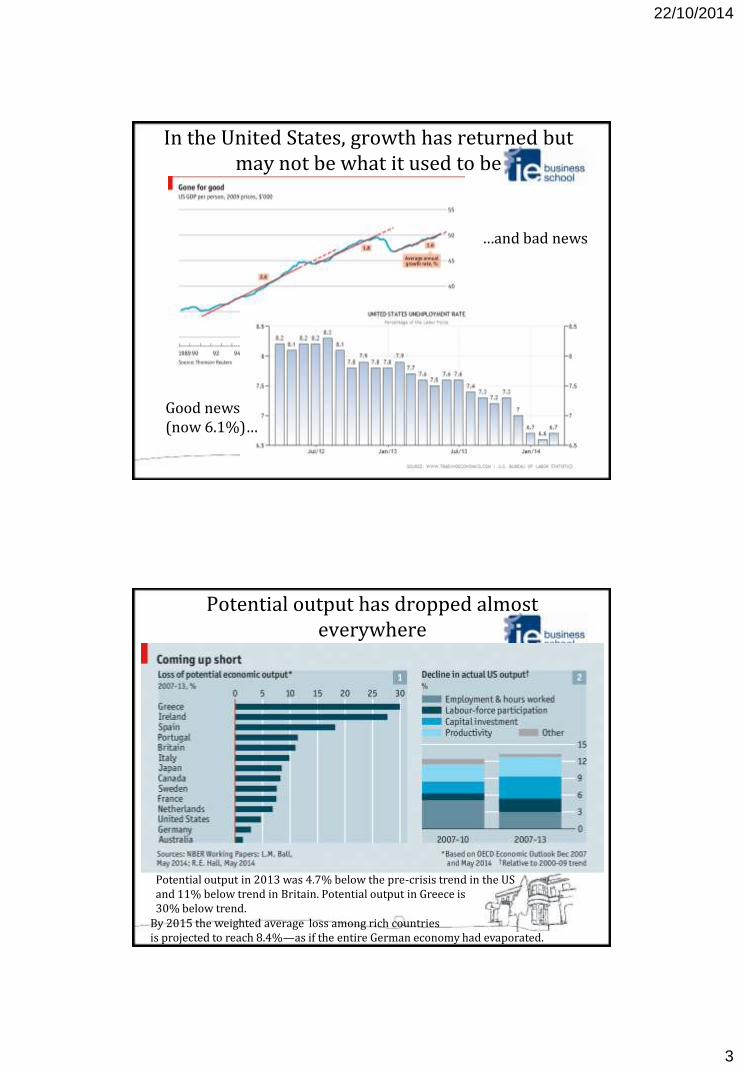

In the United States, growth has returned but may not be what it used to be

Good news (now 6.1%)…

…and bad news

Potential output has dropped almost everywhere

Potential output in 2013 was 4.7% below the pre-crisis trend in the US and 11% below trend in Britain. Potential output in Greece is 30% below trend.

By 2015 the weighted average loss among rich countries is projected to reach 8.4%—as if the entire German economy had evaporated.

22/10/2014

4

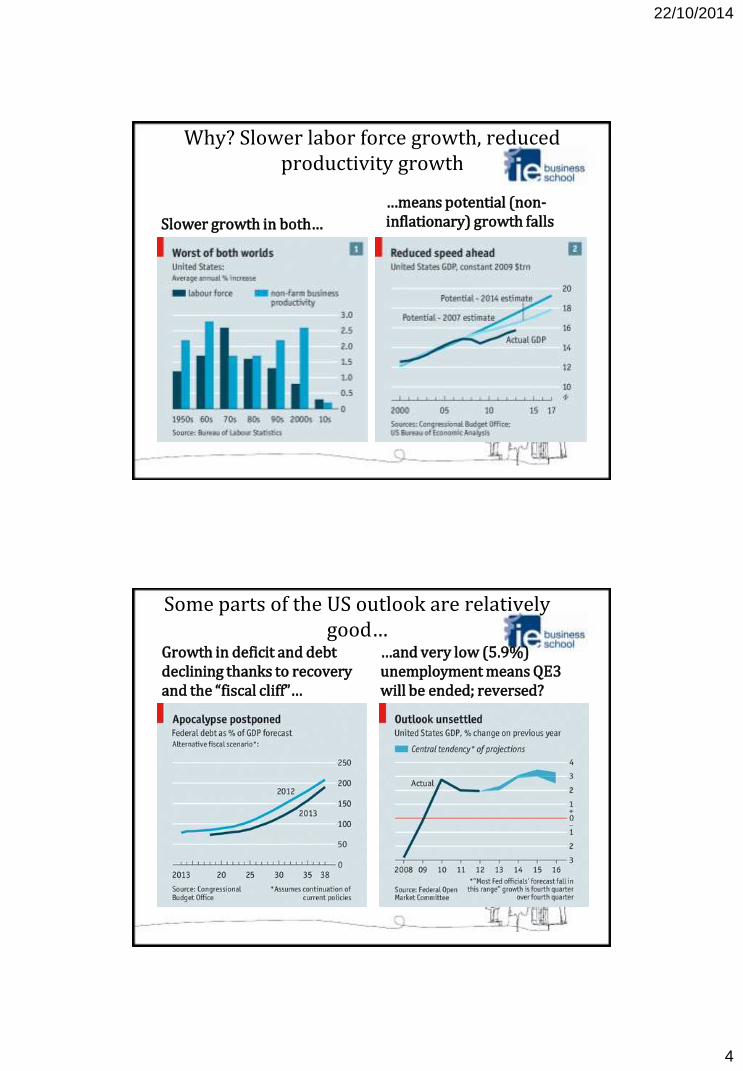

Why? Slower labor force growth, reduced productivity growth

Slower growth in both…

…means potential (non-inflationary) growth falls

Some parts of the US outlook are relatively good…

Growth in deficit and debt declining thanks to recovery and the “fiscal cliff”…

…and very low (5.9%) unemployment means QE3 will be ended; reversed?

22/10/2014

5

…but major fiscal and energy issues are on the horizon

The US has major fiscal issues to face

• It needs a credible, long-term plan to address social programs and stabilize spending

• It also needs higher and more progressive taxes

• The tax system is overly complex and needs overhaul

• Only a bipartisan effort can achieve this

Becoming self-sufficient in oil will affect the world

• In the next decade the US should again become the world s largest producer of liquid hydrocarbons

• Already, imports are only 47% (60% in 2005)

• This will help reduce the deficit, shield it from supply disruptions

• But energy still needs to be priced correctly

Japan is betting everything on the success of Abenomics

22/10/2014

6

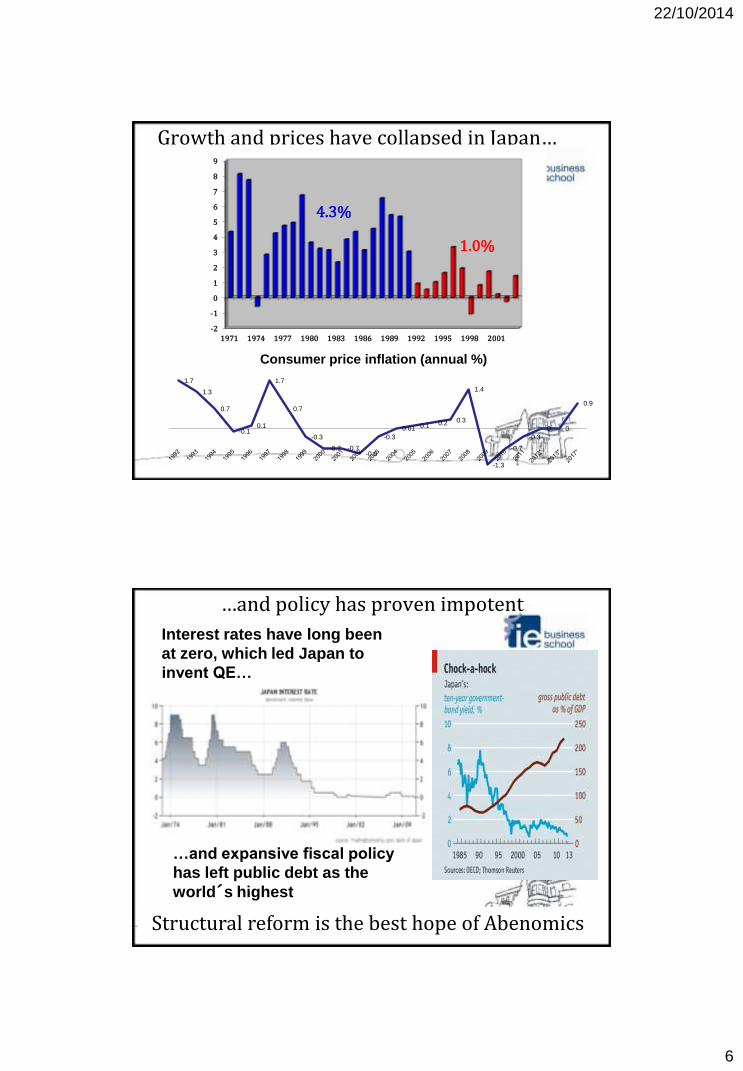

Growth and prices have collapsed in Japan…

-2

-1

0

1

2

3

4

5

6

7

8

9

1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001

4.3%

1.0%

1.7

1.3

0.7

-0.1 0.1

1.7

0.7

-0.3

-0.7 -0.7 -0.9

-0.3

0.01 0.1 0.2 0.3

1.4

-1.3

-0.7

-0.3

0 0

0.9

Consumer price inflation (annual %)

…and policy has proven impotent

Interest rates have long been

at zero, which led Japan to

invent QE…

…and expansive fiscal policy

has left public debt as the

world s highest

Structural reform is the best hope of Abenomics

22/10/2014

7

For Europe, recovery is not yet a reality and the specter of deflation looms

Japanese-style deflation is the greatest concern in the eurozone

Debt is high and deflation makes it worse…

…as recovery still fails to materialize

Greek debt will reach175% of GDP this year A look at the Eurozone economies

22/10/2014

8

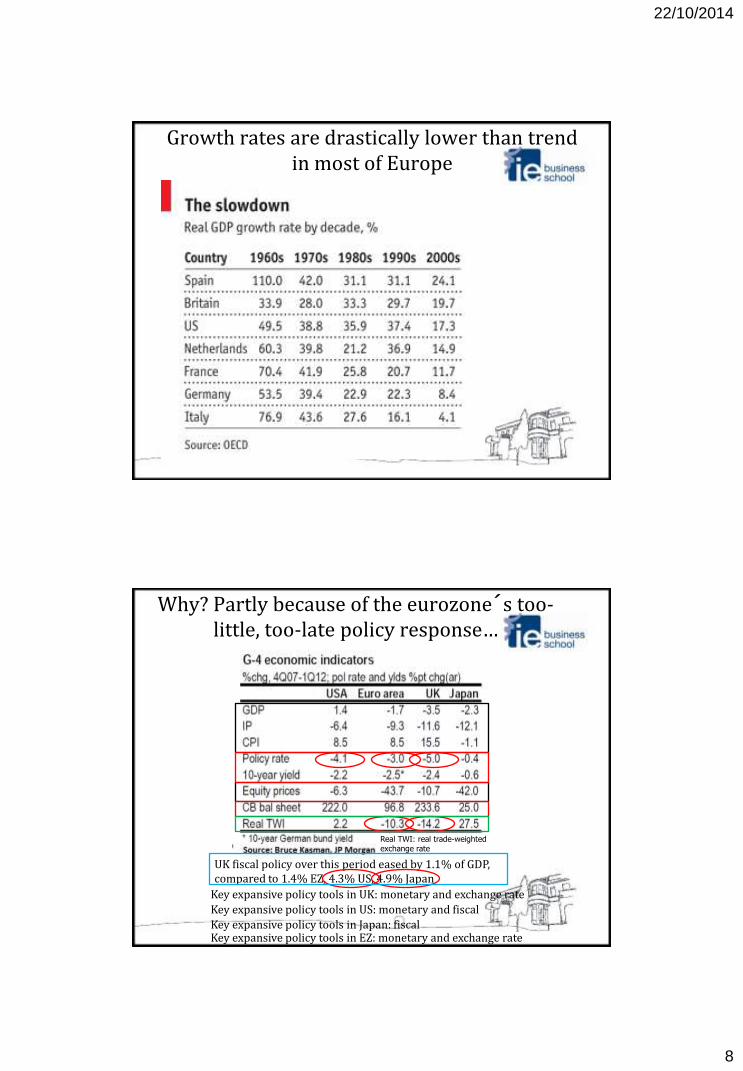

Growth rates are drastically lower than trend in most of Europe

Why? Partly because of the eurozone s too-little, too-late policy response…

Key expansive policy tools in UK: monetary and exchange rate

UK fiscal policy over this period eased by 1.1% of GDP, compared to 1.4% EZ, 4.3% US, 4.9% Japan

Real TWI: real trade-weighted exchange rate

Key expansive policy tools in US: monetary and fiscal

Key expansive policy tools in Japan: fiscal Key expansive policy tools in EZ: monetary and exchange rate

22/10/2014

9

…and partly due to the same structural issues facing the US, plus special institutional ones

• Sorting out banks and creating a real banking union

• Adapting institutions and attitudes to a single currency…many years after it began to circulate!

• Finding a way to correct euro-wide cyclical and external imbalances

• Saving the welfare state

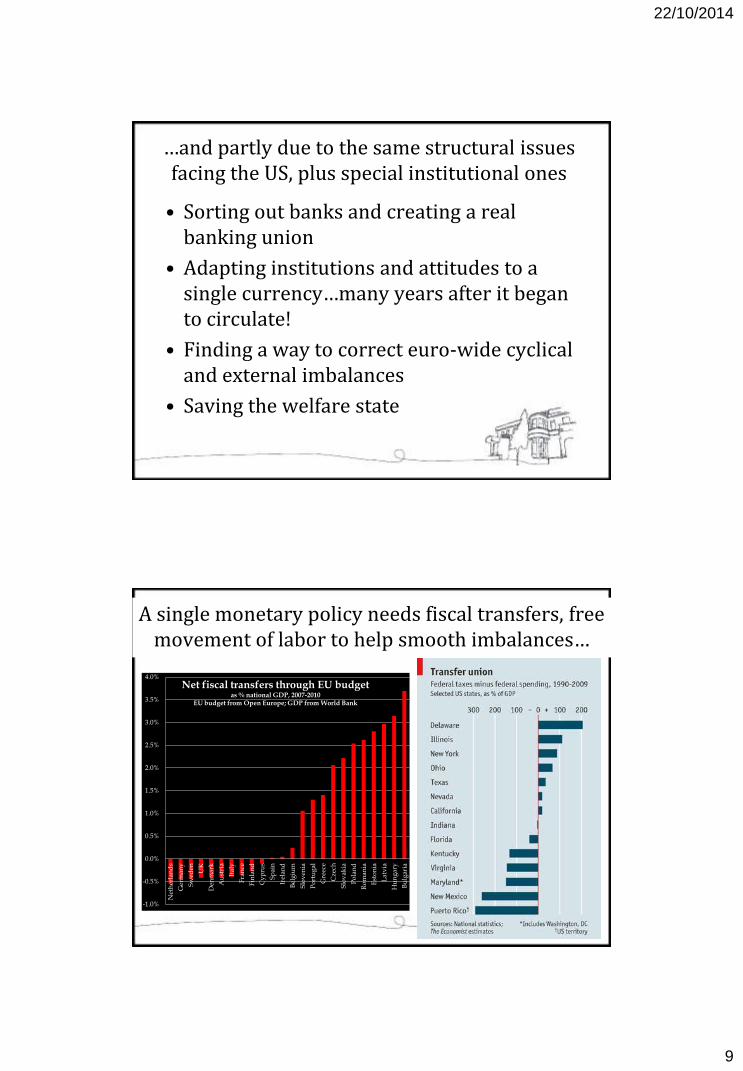

A single monetary policy needs fiscal transfers, free movement of labor to help smooth imbalances…

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Net

her

lan

ds

Ger

man

y

Sw

eden

UK

Den

mar

k

Au

stri

a

Ital

y

Fra

nce

Fin

lan

d

Cy

pru

s

Sp

ain

Irel

and

Bel

giu

m

Slo

ven

ia

Po

rtu

gal

Gre

ece

Cze

ch

Slo

vak

ia

Po

lan

d

Ro

man

ia

Est

on

ia

Lat

via

Hu

ng

ary

Bu

lgar

ia

Net fiscal transfers through EU budget as % national GDP, 2007-2010

EU budget from Open Europe; GDP from World Bank

22/10/2014

10

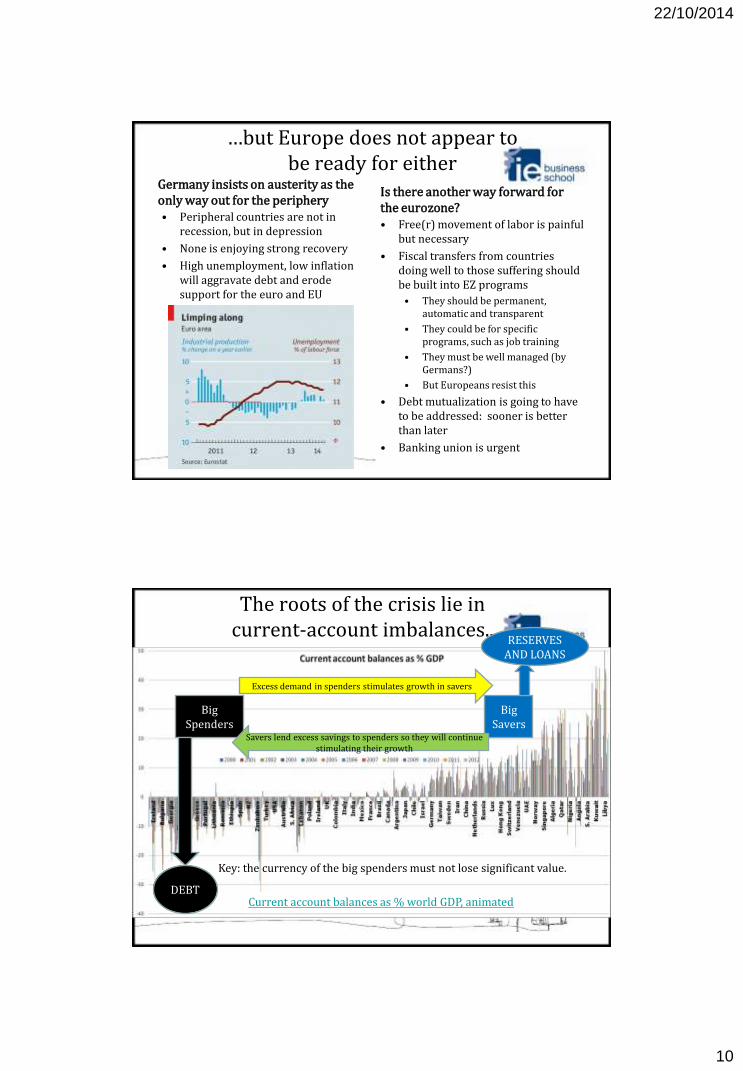

…but Europe does not appear to be ready for either

Germany insists on austerity as the only way out for the periphery • Peripheral countries are not in

recession, but in depression

• None is enjoying strong recovery

• High unemployment, low inflation will aggravate debt and erode support for the euro and EU

Is there another way forward for the eurozone? • Free(r) movement of labor is painful

but necessary

• Fiscal transfers from countries doing well to those suffering should be built into EZ programs

• They should be permanent, automatic and transparent

• They could be for specific programs, such as job training

• They must be well managed (by Germans?)

• But Europeans resist this

• Debt mutualization is going to have to be addressed: sooner is better than later

• Banking union is urgent

The roots of the crisis lie in current-account imbalances...

Global imbalances over time

Big Spenders

Big Savers

Excess demand in spenders stimulates growth in savers

Savers lend excess savings to spenders so they will continue stimulating their growth

DEBT

RESERVES AND LOANS

Current account balances as % world GDP, animated

Key: the currency of the big spenders must not lose significant value.

22/10/2014

11

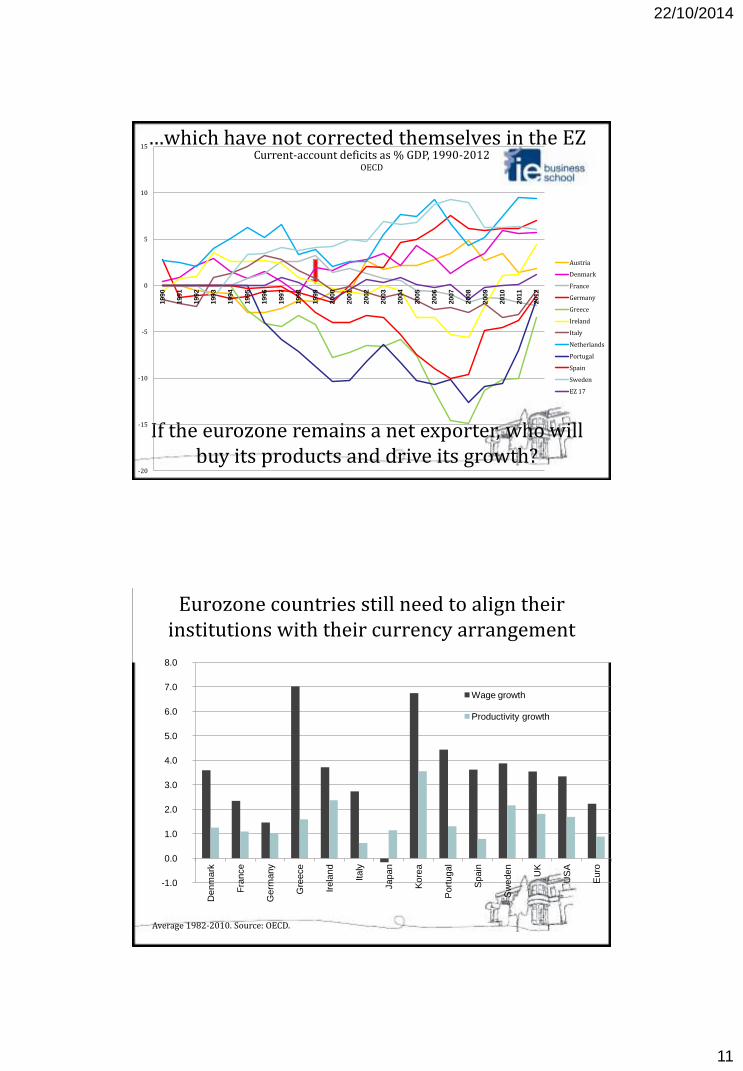

…which have not corrected themselves in the EZ

If the eurozone remains a net exporter, who will buy its products and drive its growth?

-20

-15

-10

-5

0

5

10

15

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Current-account deficits as % GDP, 1990-2012 OECD

Austria

Denmark

France

Germany

Greece

Ireland

Italy

Netherlands

Portugal

Spain

Sweden

EZ 17

Eurozone countries still need to align their institutions with their currency arrangement

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Denm

ark

Fra

nce

Germ

any

Gre

ece

Irela

nd

Italy

Japan

Kore

a

Port

ugal

Spain

Sw

eden

UK

US

A

Euro

Wage growth

Productivity growth

Average 1982-2010. Source: OECD.

22/10/2014

12

Certain key challenges are shared by all developed countries

• Where will we get growth?

• How will we pay our public debts?

• How will we face the costs of our changing demography?

• How will we respond to environmental stresses?

• What will we do about the collateral effects of technological change?

• Above all, what are we looking for?

Meanwhile, the “emerging” world is half or more of global economic activity…

22/10/2014

13

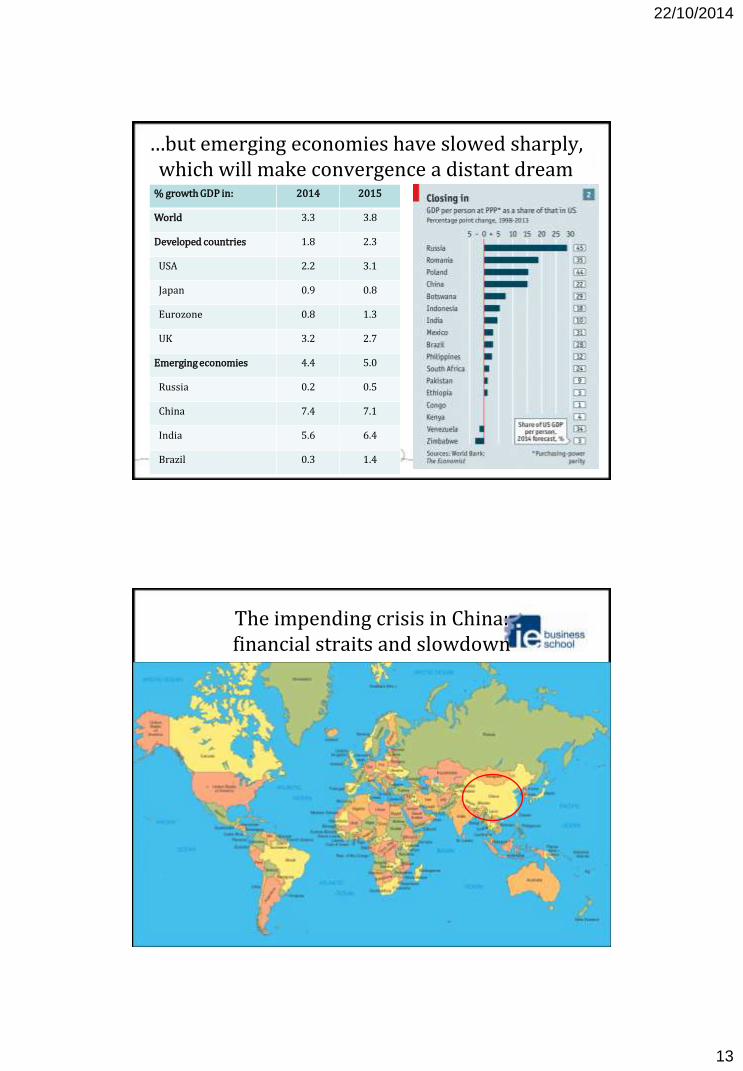

…but emerging economies have slowed sharply, which will make convergence a distant dream

% growth GDP in: 2014 2015

World 3.3 3.8

Developed countries 1.8 2.3

USA 2.2 3.1

Japan 0.9 0.8

Eurozone 0.8 1.3

UK 3.2 2.7

Emerging economies 4.4 5.0

Russia 0.2 0.5

China 7.4 7.1

India 5.6 6.4

Brazil 0.3 1.4

The impending crisis in China: financial straits and slowdown

22/10/2014

14

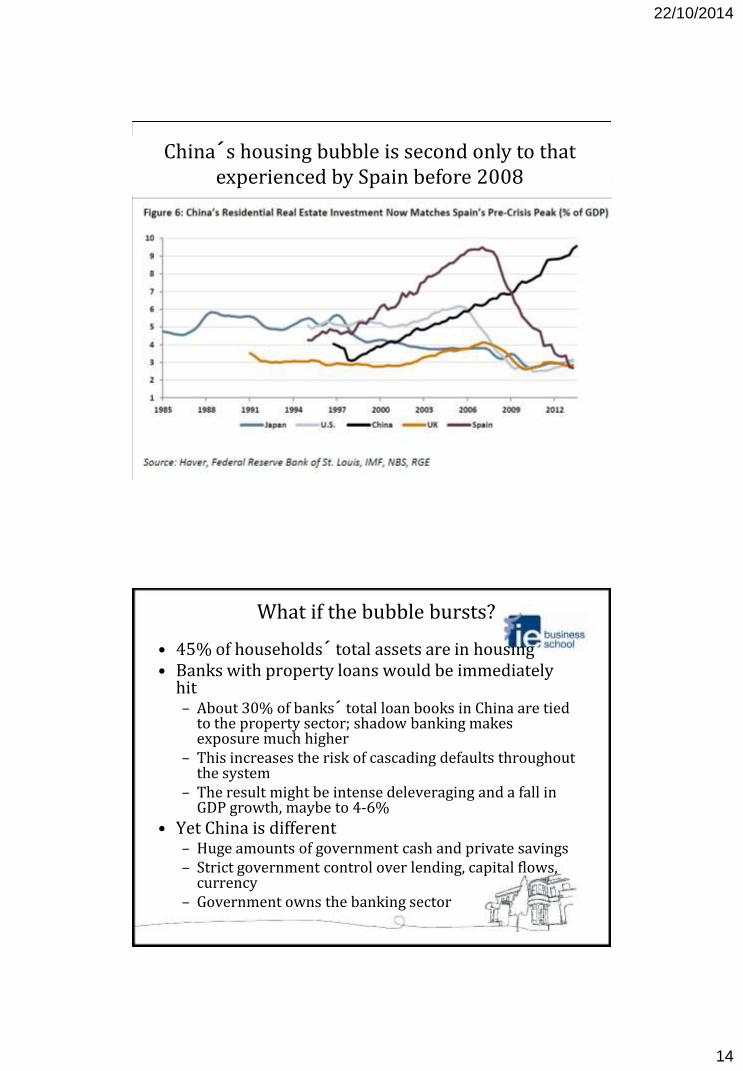

China s housing bubble is second only to that experienced by Spain before 2008

What if the bubble bursts?

• 45% of households total assets are in housing • Banks with property loans would be immediately

hit – About 30% of banks total loan books in China are tied

to the property sector; shadow banking makes exposure much higher

– This increases the risk of cascading defaults throughout the system

– The result might be intense deleveraging and a fall in GDP growth, maybe to 4-6%

• Yet China is different – Huge amounts of government cash and private savings – Strict government control over lending, capital flows,

currency – Government owns the banking sector

22/10/2014

15

There may be a financial crisis;

there will be a steady slowdown • Monetary and fiscal expansion and credit growth are

sustaining GDP growth

• Private sector debt in China is now as big as it was in the United States in 2007 (Fitch); and growth is slowing down (10% to 7%)

• Demography will also slow China down: fertility rate is the lowest in the world, and working aged population is now declining – Demographic dividend represented 15-25% of China s

economic growth between 1980-2000

– China s population will hit its peak in less than 15 years and begin a long decline and rapid ageing

• As Japan demonstrates, it is difficult to manage the transition from a high-growth to a lower-growth economy in an export-led model

Roubini s view on China:

“Our structural view of China’s economy remains the same—debt-fueled, investment-led growth is unsustainable and a shift toward a growth model that relies less on financial leverage and capacity expansion and more on private consumption and productivity improvements is inevitable.

This was controversial four years ago, but is conventional wisdom now. Yet, the question remains—how will this rebalancing process play out?”

22/10/2014

16

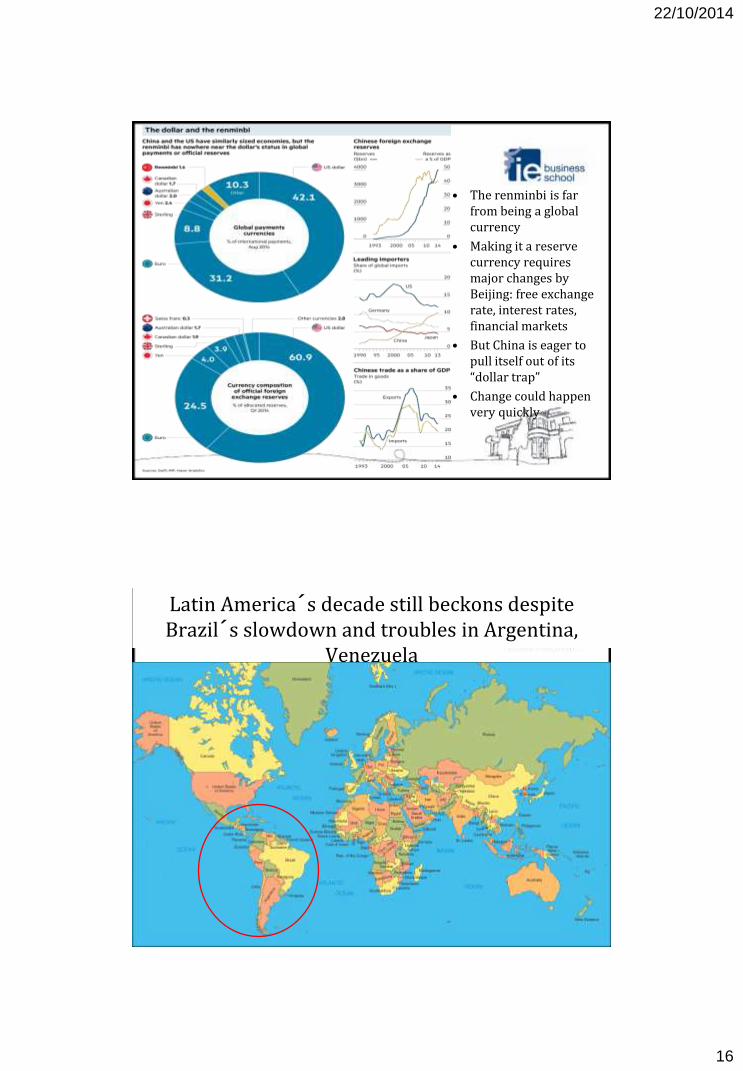

• The renminbi is far from being a global currency

• Making it a reserve currency requires major changes by Beijing: free exchange rate, interest rates, financial markets

• But China is eager to pull itself out of its “dollar trap”

• Change could happen very quickly

Latin America s decade still beckons despite Brazil s slowdown and troubles in Argentina,

Venezuela

22/10/2014

17

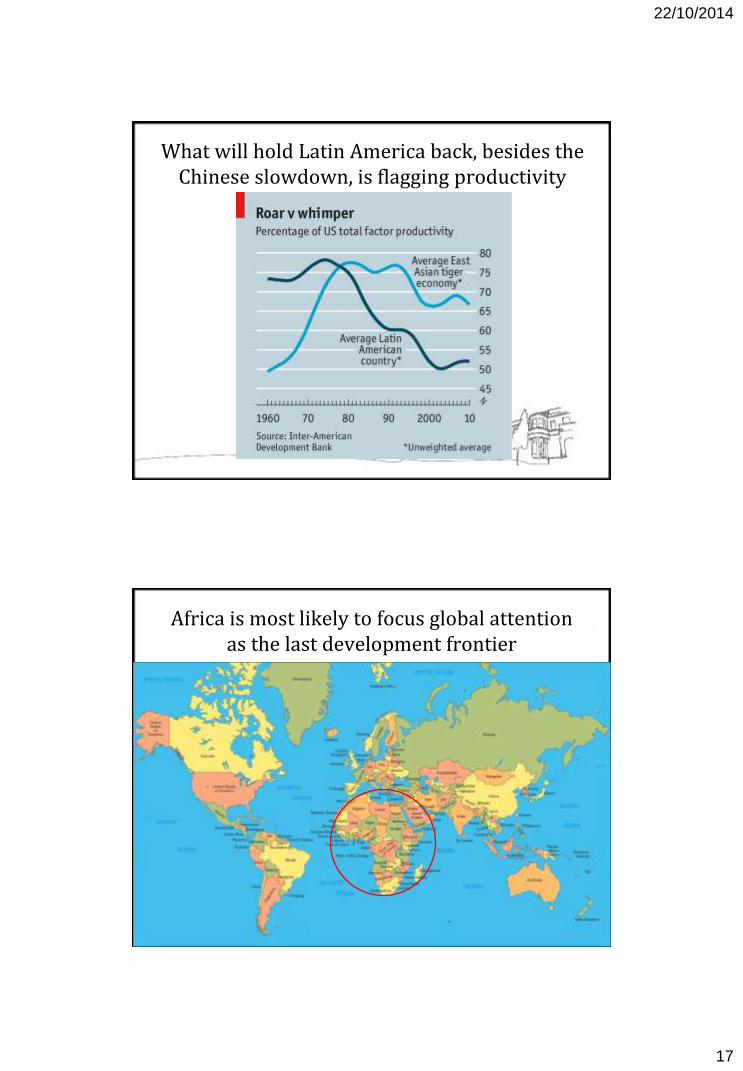

What will hold Latin America back, besides the Chinese slowdown, is flagging productivity

Africa is most likely to focus global attention as the last development frontier

22/10/2014

18

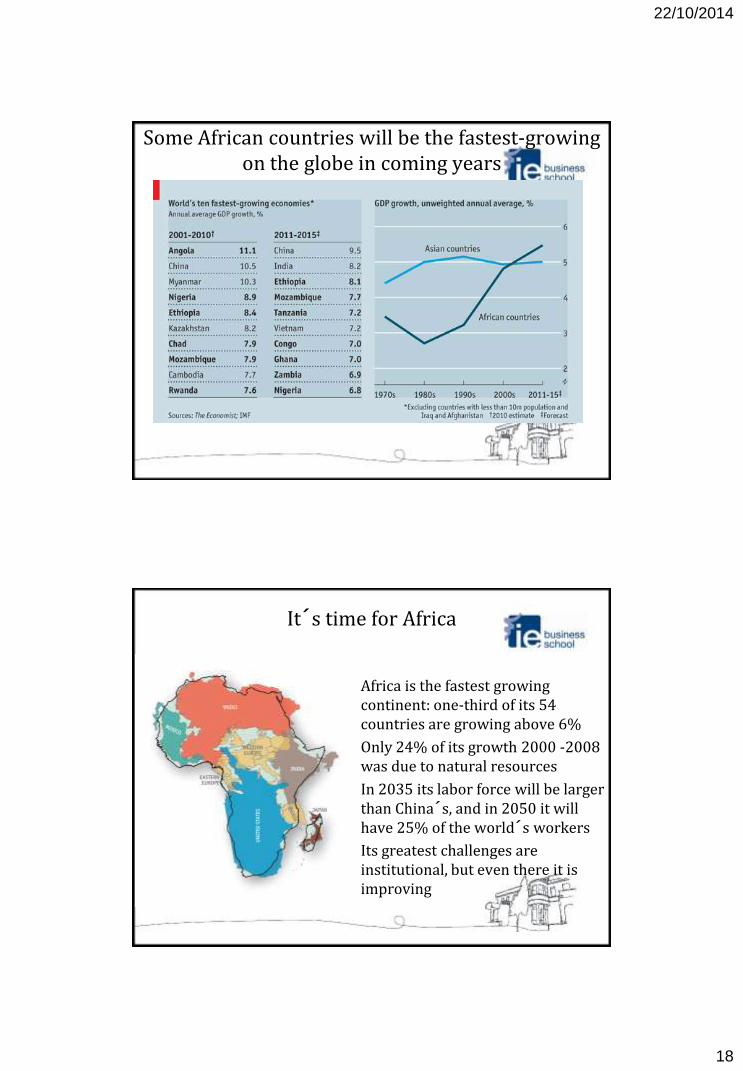

Some African countries will be the fastest-growing on the globe in coming years

It s time for Africa

• Africa is the fastest growing continent: one-third of its 54 countries are growing above 6%

• Only 24% of its growth 2000 -2008 was due to natural resources

• In 2035 its labor force will be larger than China s, and in 2050 it will have 25% of the world s workers

• Its greatest challenges are institutional, but even there it is improving

22/10/2014

19

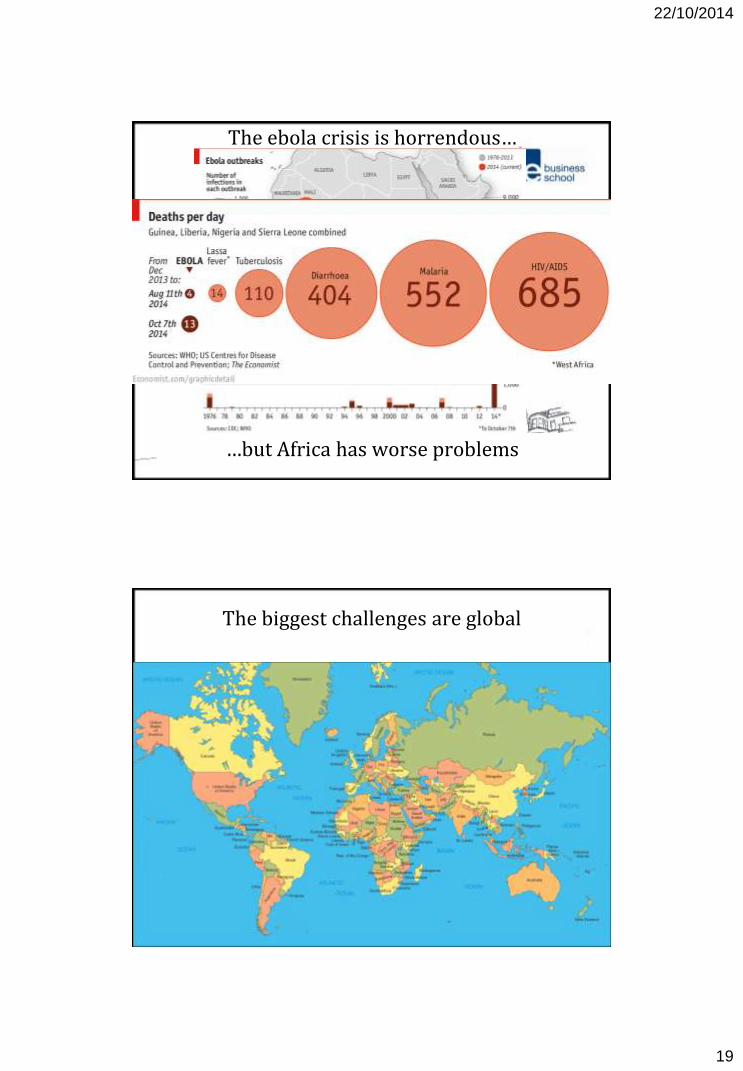

The ebola crisis is horrendous…

…but Africa has worse problems

The biggest challenges are global

22/10/2014

20

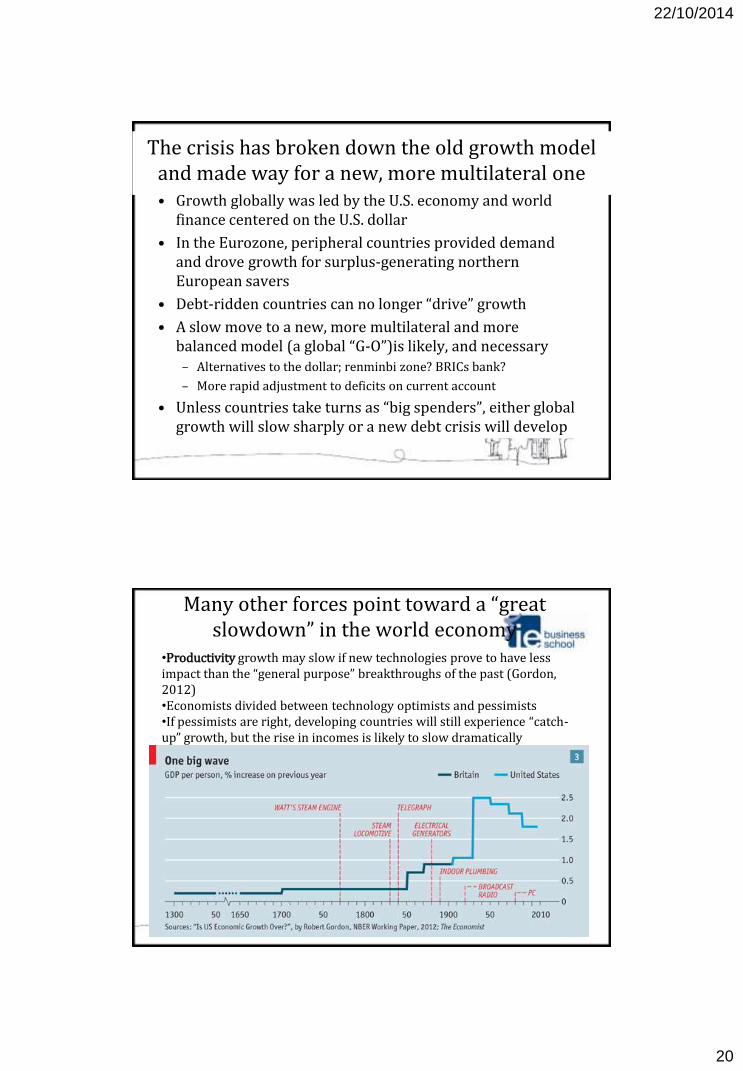

The crisis has broken down the old growth model and made way for a new, more multilateral one • Growth globally was led by the U.S. economy and world

finance centered on the U.S. dollar

• In the Eurozone, peripheral countries provided demand and drove growth for surplus-generating northern European savers

• Debt-ridden countries can no longer “drive” growth

• A slow move to a new, more multilateral and more balanced model (a global “G-O”)is likely, and necessary

– Alternatives to the dollar; renminbi zone? BRICs bank?

– More rapid adjustment to deficits on current account

• Unless countries take turns as “big spenders”, either global growth will slow sharply or a new debt crisis will develop

Many other forces point toward a “great slowdown” in the world economy

•Productivity growth may slow if new technologies prove to have less impact than the “general purpose” breakthroughs of the past (Gordon, 2012) •Economists divided between technology optimists and pessimists •If pessimists are right, developing countries will still experience “catch-up” growth, but the rise in incomes is likely to slow dramatically

22/10/2014

21

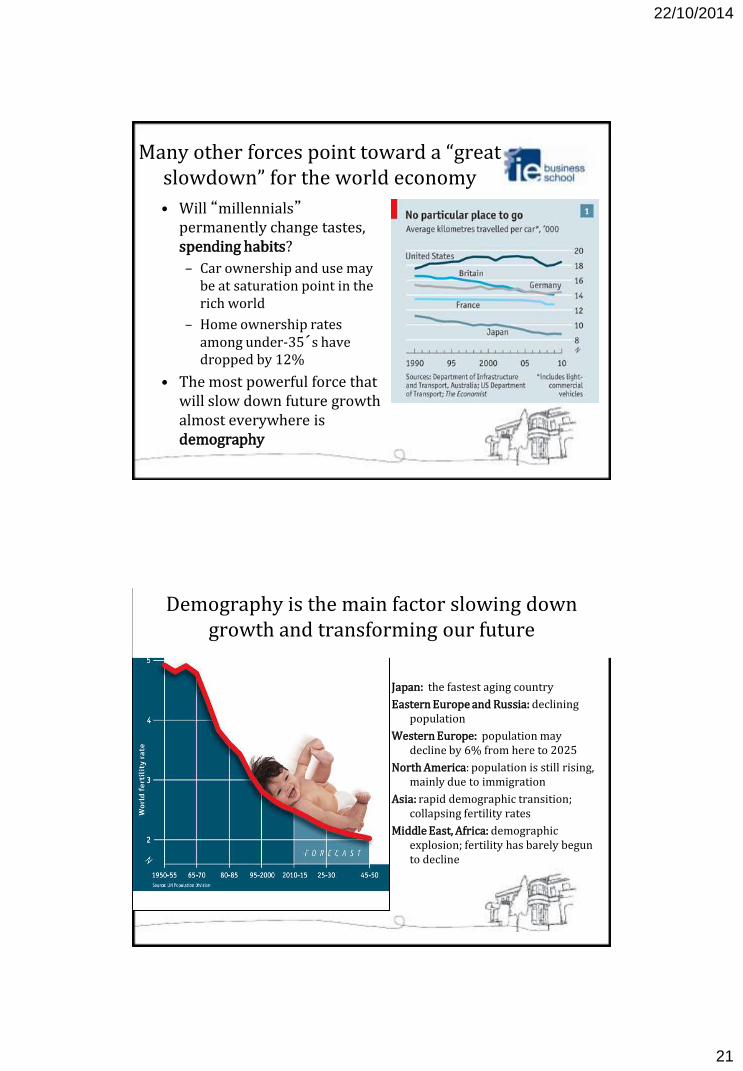

Many other forces point toward a “great slowdown” for the world economy

• Will “millennials” permanently change tastes, spending habits?

– Car ownership and use may be at saturation point in the rich world

– Home ownership rates among under-35 s have dropped by 12%

• The most powerful force that will slow down future growth almost everywhere is demography

Japan: the fastest aging country

Eastern Europe and Russia: declining population

Western Europe: population may decline by 6% from here to 2025

North America: population is still rising, mainly due to immigration

Asia: rapid demographic transition; collapsing fertility rates

Middle East, Africa: demographic explosion; fertility has barely begun to decline

Demography is the main factor slowing down growth and transforming our future

22/10/2014

22

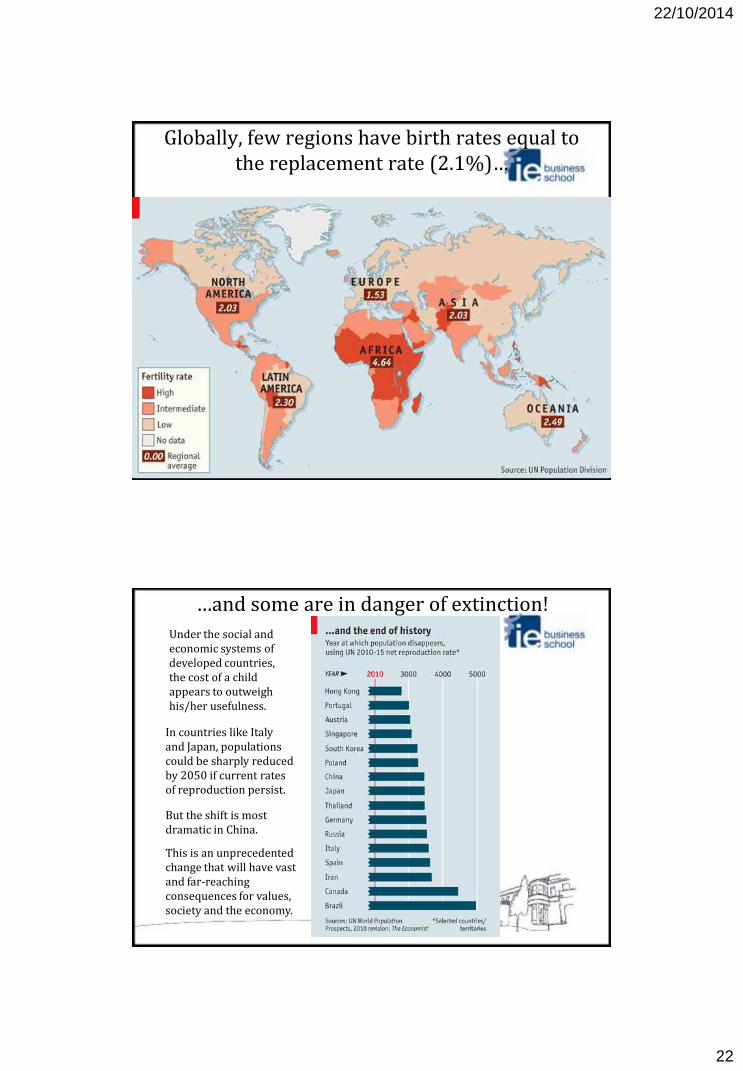

Globally, few regions have birth rates equal to the replacement rate (2.1%)…

…and some are in danger of extinction!

Under the social and economic systems of developed countries, the cost of a child appears to outweigh his/her usefulness.

In countries like Italy and Japan, populations could be sharply reduced by 2050 if current rates of reproduction persist.

This is an unprecedented change that will have vast and far-reaching consequences for values, society and the economy.

But the shift is most dramatic in China.

22/10/2014

23

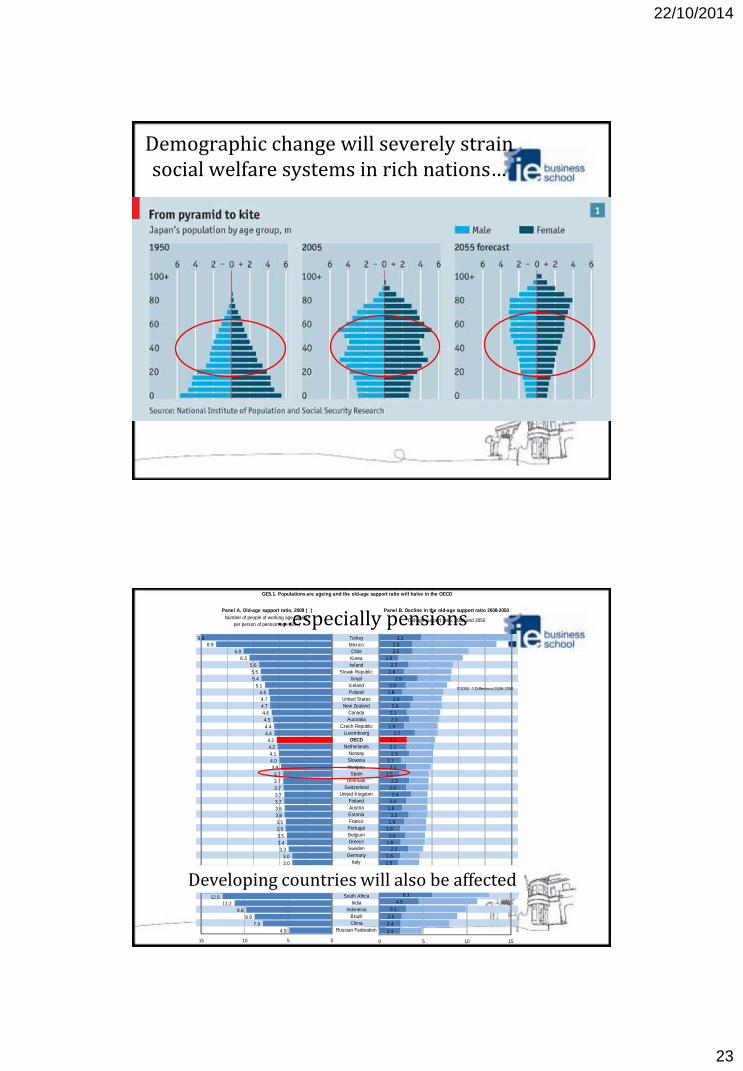

Demographic change will severely strain social welfare systems in rich nations…

…especially pensions Turkey

Mexico

Chile

Korea

Ireland

Slovak Republic

Israel

Iceland

Poland

United States

New Zealand

Canada

Australia

Czech Republic

Luxembourg

OECD

Netherlands

Norway

Slovenia

Hungary

Spain

Denmark

Switzerland

United Kingdom

Finland

Austria

Estonia

France

Portugal

Belgium

Greece

Sweden

Germany

Italy

Japan

South Africa

India

Indonesia

Brazil

China

Russian Federation

Number of people of working age (20-64)

per person of pension age (65+)

GE5.1. Populations are ageing and the old-age support ratio will halve in the OECD

Panel A. Old-age support ratio, 2008 (

↘

) Panel B. Decline in the old-age support ratio 2008-2050

Old-age support ratio, 2008 and 2050

9.9

8.9

6.8

6.3

5.6

5.5

5.4

5.1

4.8

4.7

4.7

4.6

4.5

4.4

4.4

4.2

4.2

4.1

4.0

3.9

3.7

3.7

3.7

3.7

3.7

3.6

3.6

3.5

3.5

3.5

3.4

3.3

3.0

3.0

2.8

0246810

3.2

2.5

2.5

1.5

2.2

1.9

2.9

2.0

1.8

2.6

2.4

2.1

2.3

1.9

2.7

2.1

2.1

2.3

1.7

2.1

1.5

2.3

2.0

2.4

2.0

1.8

2.2

1.9

1.6

2.0

1.6

2.2

1.6

1.5

1.2

0 2 4 6 8 10

2050 Difference 2008-2050

12.5

11.2

9.8

8.9

7.9

4.9

051015

6.1

4.5

3.1

2.6

2.4

2.4

0 5 10 15

Developing countries will also be affected

22/10/2014

24

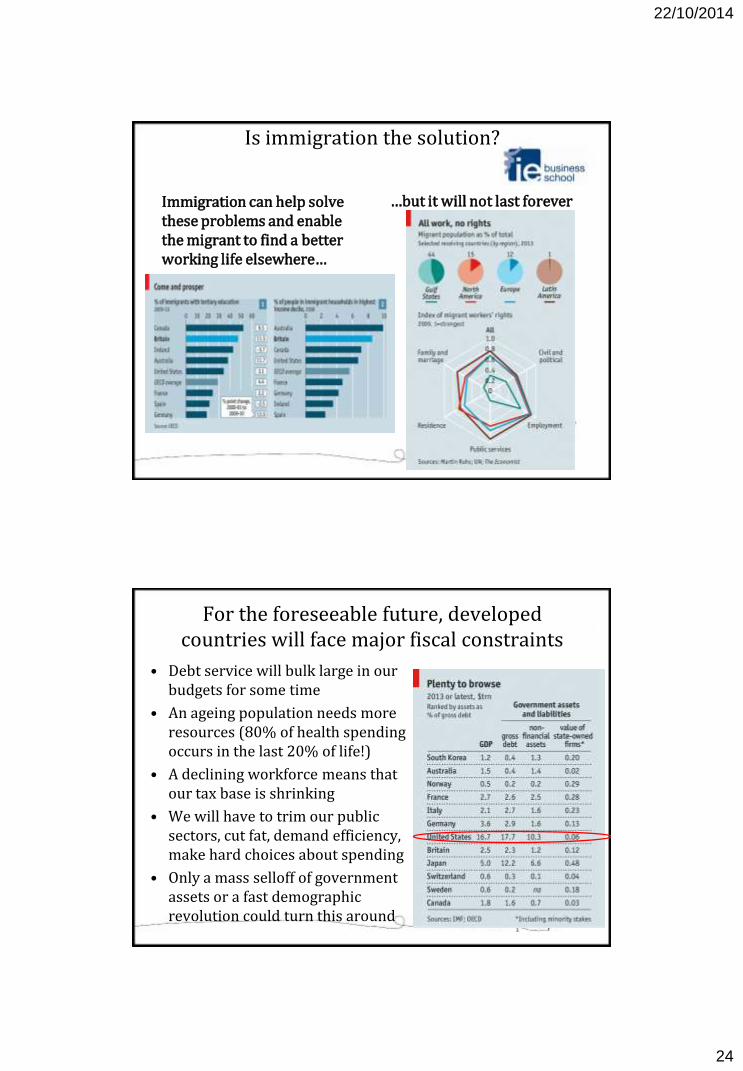

Is immigration the solution?

Immigration can help solve these problems and enable the migrant to find a better working life elsewhere…

…but it will not last forever

For the foreseeable future, developed countries will face major fiscal constraints

• Debt service will bulk large in our budgets for some time

• An ageing population needs more resources (80% of health spending occurs in the last 20% of life!)

• A declining workforce means that our tax base is shrinking

• We will have to trim our public sectors, cut fat, demand efficiency, make hard choices about spending

• Only a mass selloff of government assets or a fast demographic revolution could turn this around

22/10/2014

25

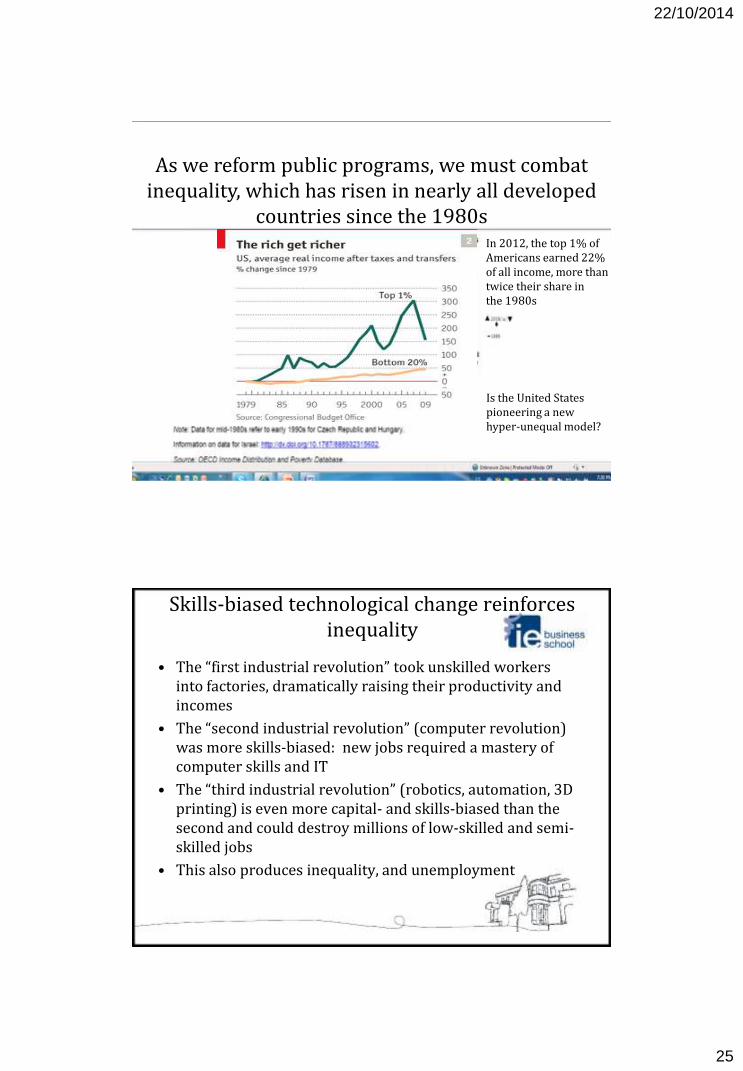

As we reform public programs, we must combat inequality, which has risen in nearly all developed

countries since the 1980s In 2012, the top 1% of Americans earned 22% of all income, more than twice their share in the 1980s

Is the United States pioneering a new hyper-unequal model?

Skills-biased technological change reinforces inequality

• The “first industrial revolution” took unskilled workers into factories, dramatically raising their productivity and incomes

• The “second industrial revolution” (computer revolution) was more skills-biased: new jobs required a mastery of computer skills and IT

• The “third industrial revolution” (robotics, automation, 3D printing) is even more capital- and skills-biased than the second and could destroy millions of low-skilled and semi-skilled jobs

• This also produces inequality, and unemployment

22/10/2014

26

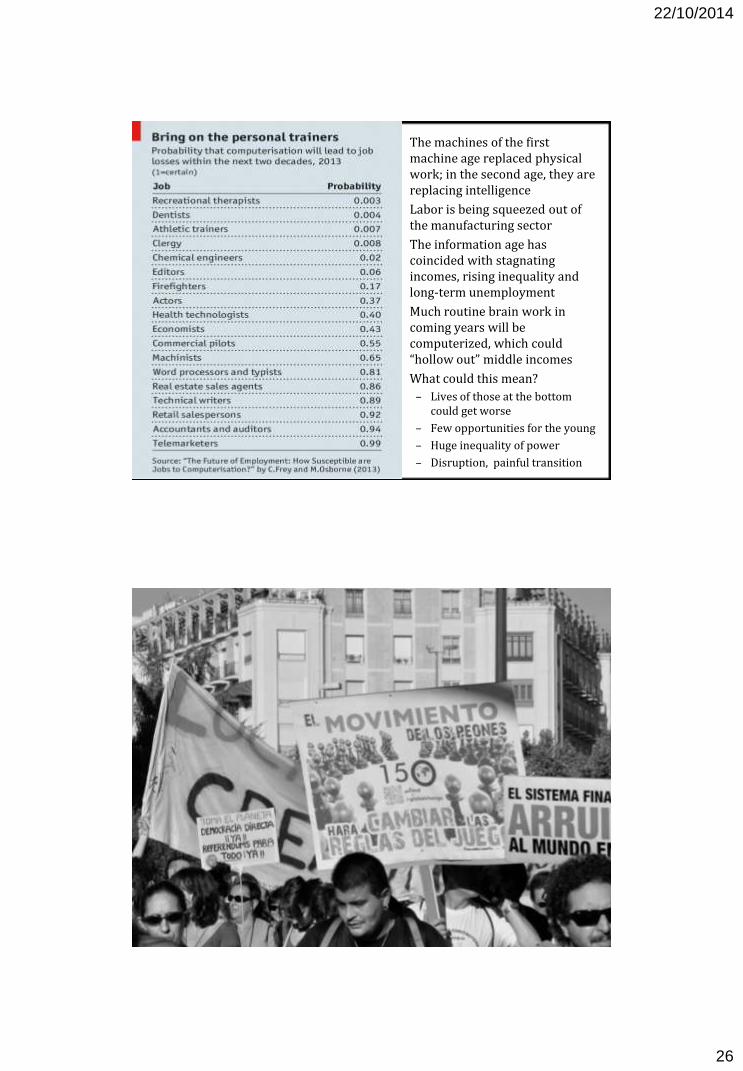

Automation could make many educational

professionals obsolete...and many

others

• The machines of the first machine age replaced physical work; in the second age, they are replacing intelligence

• Labor is being squeezed out of the manufacturing sector

• The information age has coincided with stagnating incomes, rising inequality and long-term unemployment

• Much routine brain work in coming years will be computerized, which could “hollow out” middle incomes

• What could this mean?

– Lives of those at the bottom could get worse

– Few opportunities for the young

– Huge inequality of power

– Disruption, painful transition

What are they protesting? What is wrong with inequality? Apart from ethical considerations, it causes

instability

22/10/2014

27

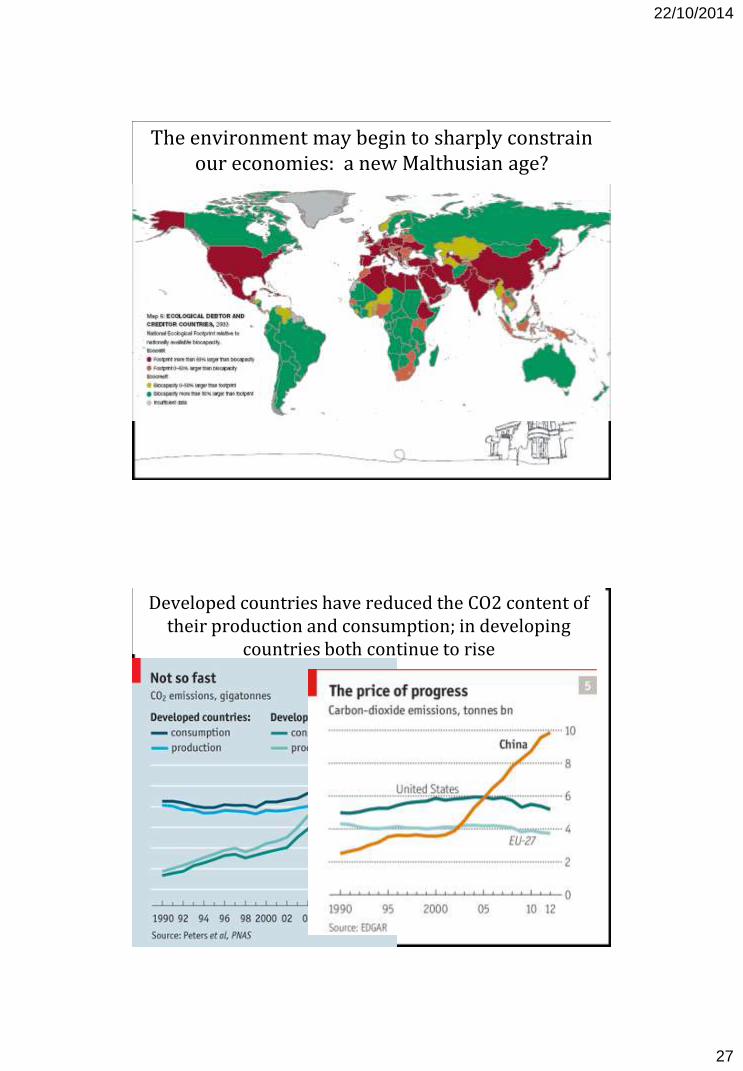

The environment may begin to sharply constrain our economies: a new Malthusian age?

• Currently, we are consuming 1.5 times the planet s capacity, and development will only raise this figure

• The latest UN report predicts that at current emissions rates, world temperatures will rise 2∘C by 2030 and 3.7-4.8∘C by 2030

• If climate change plays out as projected, new factors emerge that would slow down growth:

– Higher temperatures (linked to slower growth)

– Lower farm yields

– The cost of extreme weather events

• Barring technological change, developed-world living standards probably cannot be extended to all the world

Developed countries have reduced the CO2 content of their production and consumption; in developing

countries both continue to rise

22/10/2014

28

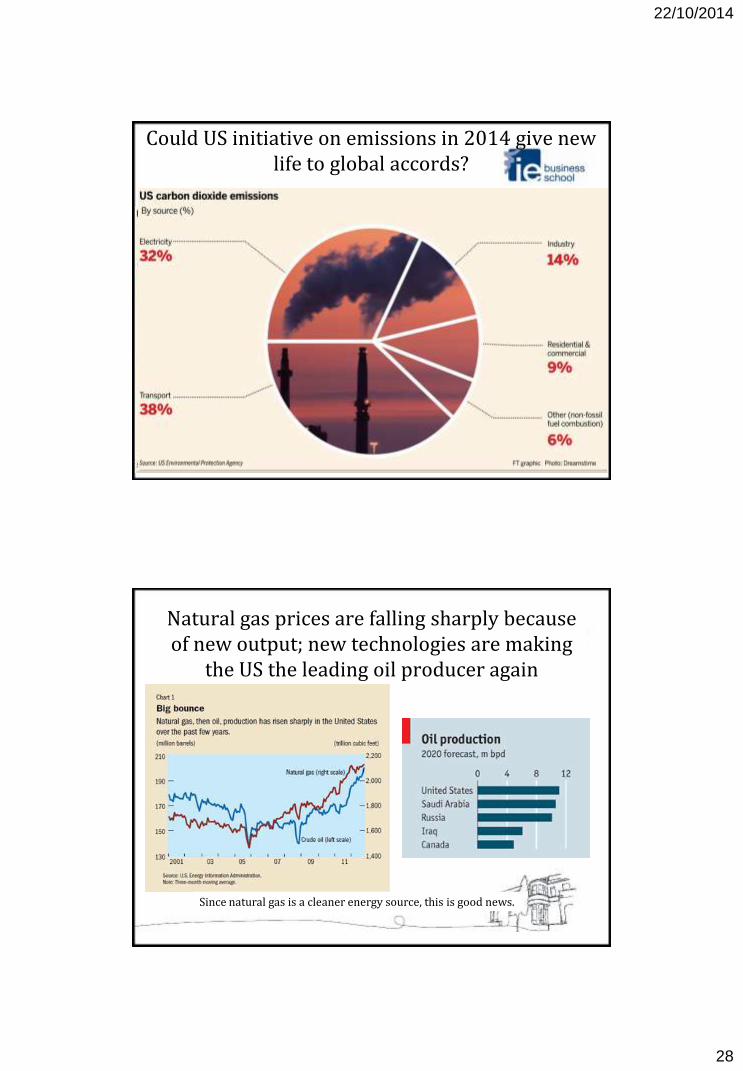

Could US initiative on emissions in 2014 give new life to global accords?

Natural gas prices are falling sharply because of new output; new technologies are making

the US the leading oil producer again

Since natural gas is a cleaner energy source, this is good news.

22/10/2014

29

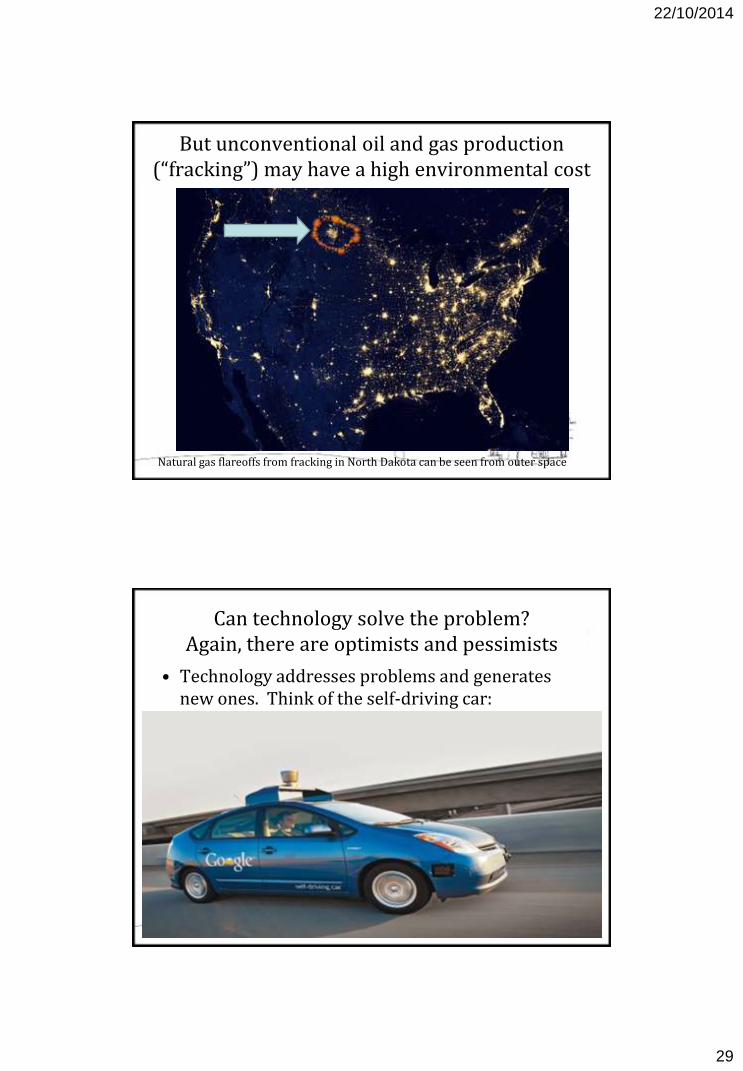

But unconventional oil and gas production (“fracking”) may have a high environmental cost

Natural gas flareoffs from fracking in North Dakota can be seen from outer space

Can technology solve the problem? Again, there are optimists and pessimists

• Technology addresses problems and generates new ones. Think of the self-driving car:

– Less reckless driving, fewer accidents, better traffic flows

– Young adults might decide to return to driving

– Roads and parking areas could bear more cars

– New models could be lighter, hence turned out faster and at lower cost

– Commutes could become longer; suburbs may spread

– Jobs for taxi and bus drivers, policemen, insurers and even hospital workers and lawyers might be destroyed

22/10/2014

30

The “no-brainer” for emissions reduction is to cut subsidies to fossil fuels

• Energy subsidies distort the economy, fuel corruption, strain government budgets and benefit the rich far more than the poor

• Ending them would save governments worldwide up to $500bn and cut global carbon emissions by 6% by 2020

• But as Egypt, Nigeria, Indonesia and others have shown, ending them can be political suicide; India, Iran have shown that slowly phasing them out can work

• The issue needs to be depoliticized and media campaigns are needed to explain the change

• Ending petroleum subsidies and raising the gas tax could transform energy use in the United States

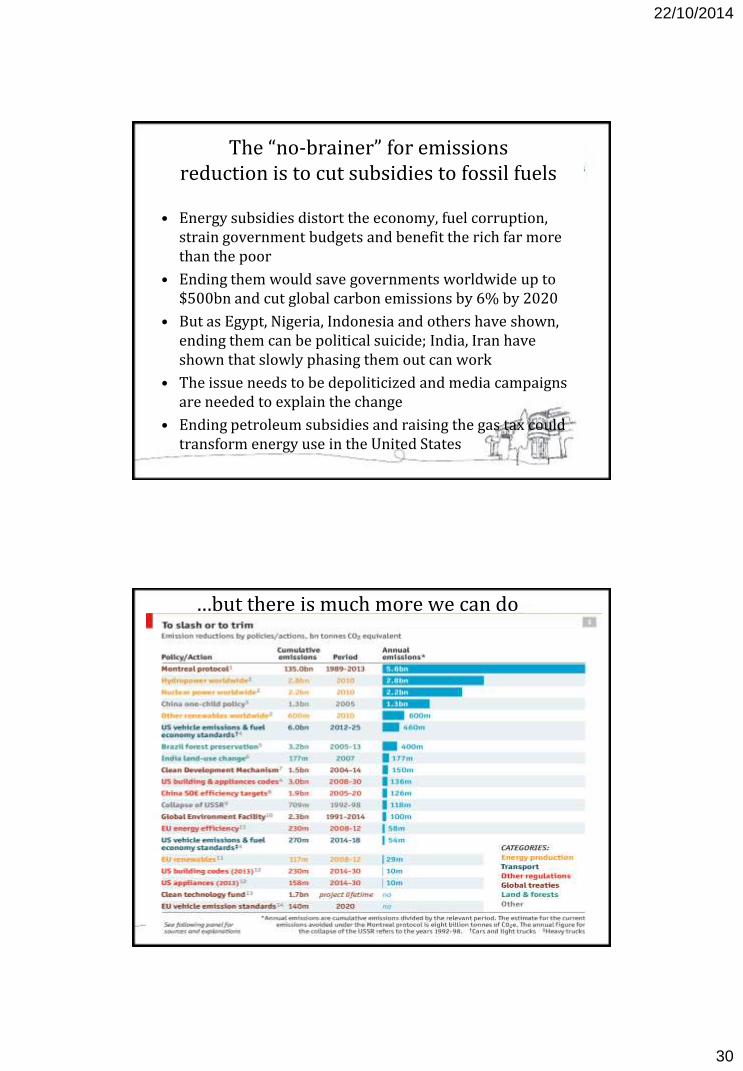

…but there is much more we can do

22/10/2014

31

If growth slowed down sharply, would this be entirely negative?

• The growth rates of the 1990s and 2000s were not normal in a historical context

• Slower growth makes sense as populations decline

• Fast growth has many negative consequences: bubbles, irrational investments, unsustainable practices, lack of time to really think and plan for fear the “train” will leave the station, lack of leisure time and higher stress levels, inequality?

• Slower growth is better for the environment…and probably for the human spirit

• We can learn to do business well in a different growth environment; maybe better than before

An economic life story: When I was born, GDP per capita in the United States was $2,400; or

nearly $18,000 in constant 2005 prices (similar to Poland today)

• We lacked nothing.

22/10/2014

32

When I finished university, GDP per capita in the United States was about $9,000, or $27,000 in constant prices.

We were already discussing how to stop growth to protect the environment, because our living standards were more than adequate.

During my lifetime, US GDP has been multiplied by 34 and global GDP by 72 (current prices)

In my experience, this has not made us, or me, truly better off.

22/10/2014

33

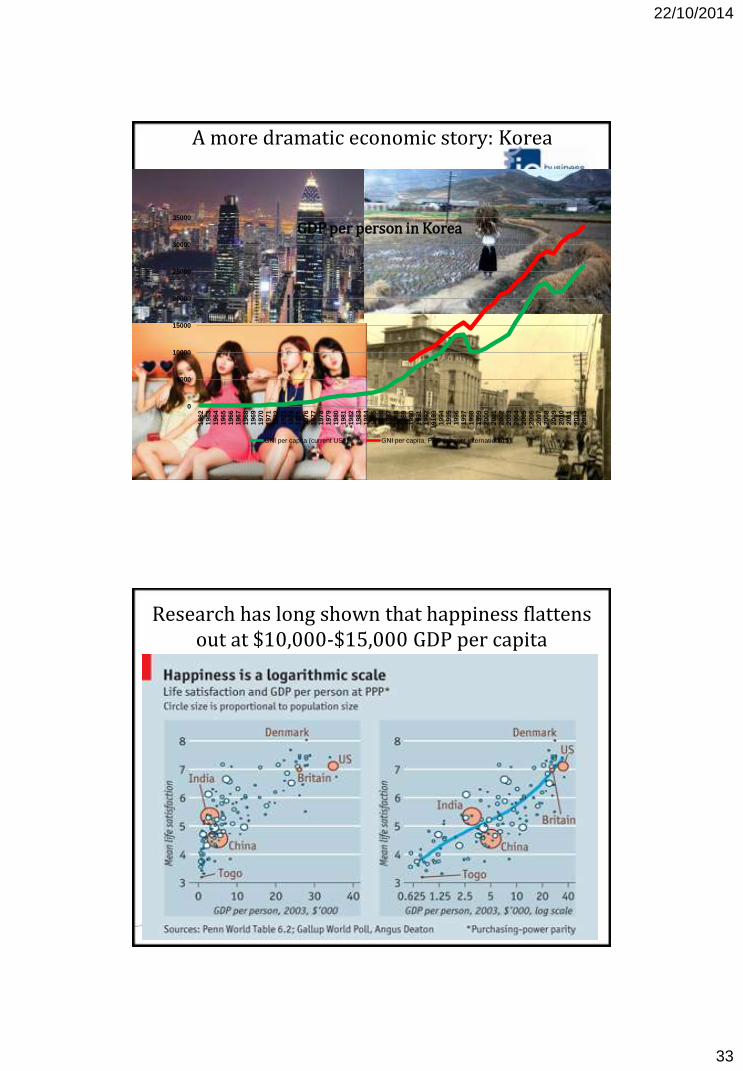

A more dramatic economic story: Korea

0

5000

10000

15000

20000

25000

30000

35000

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1972

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

19193

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

GDP per person in Korea

GNI per capita (current US$) GNI per capita, PPP (current international $)

Research has long shown that happiness flattens out at $10,000-$15,000 GDP per capita

22/10/2014

34

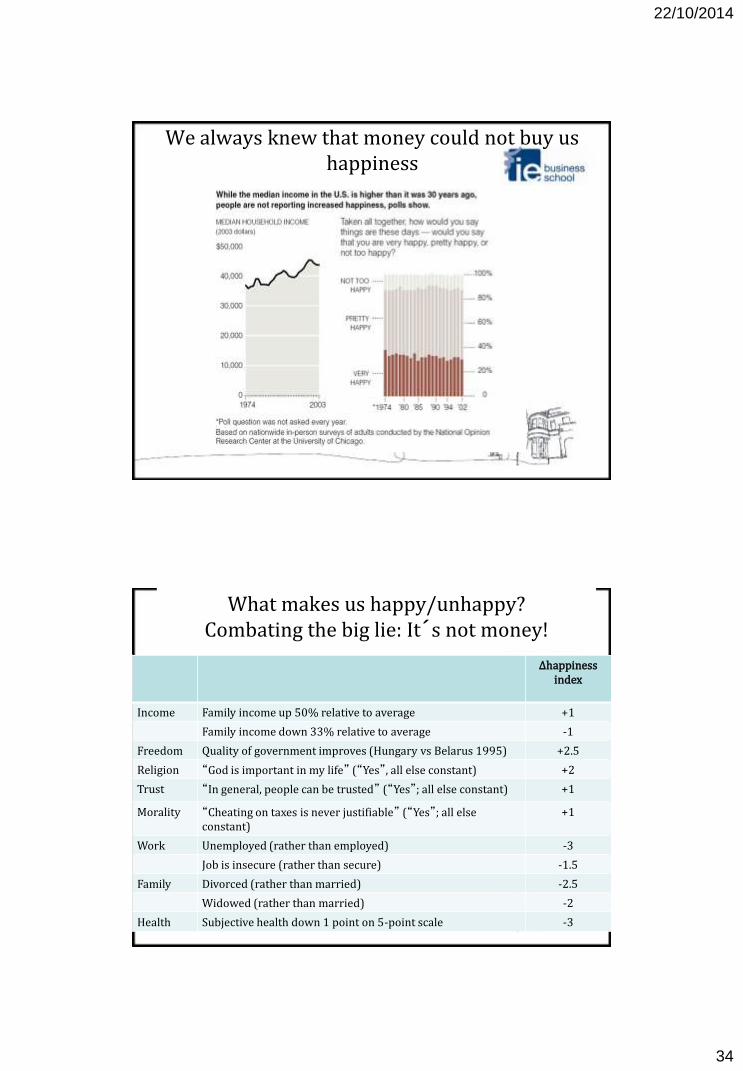

We always knew that money could not buy us happiness

What makes us happy/unhappy? Combating the big lie: It s not money!

∆happiness index

Income Family income up 50% relative to average +1

Family income down 33% relative to average -1

Freedom Quality of government improves (Hungary vs Belarus 1995) +2.5

Religion “God is important in my life” (“Yes”, all else constant) +2

Trust “In general, people can be trusted” (“Yes”; all else constant) +1

Morality “Cheating on taxes is never justifiable” (“Yes”; all else constant)

+1

Work Unemployed (rather than employed) -3

Job is insecure (rather than secure) -1.5

Family Divorced (rather than married) -2.5

Widowed (rather than married) -2

Health Subjective health down 1 point on 5-point scale -3

22/10/2014

35

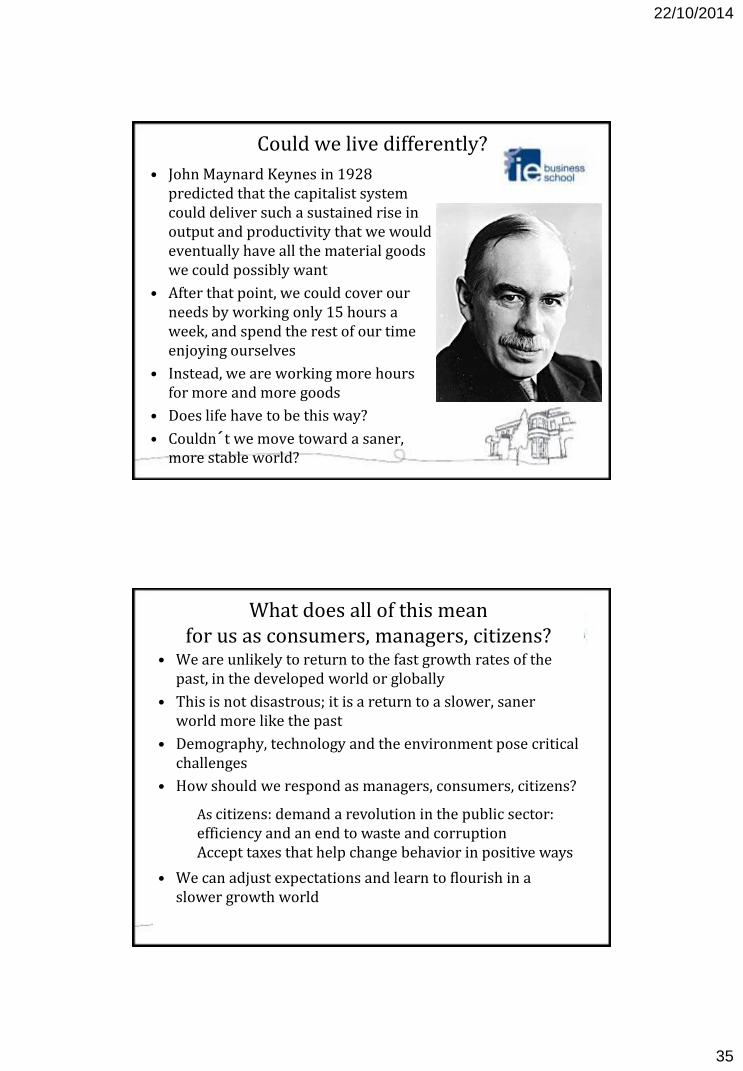

Could we live differently?

• John Maynard Keynes in 1928 predicted that the capitalist system could deliver such a sustained rise in output and productivity that we would eventually have all the material goods we could possibly want

• After that point, we could cover our needs by working only 15 hours a week, and spend the rest of our time enjoying ourselves

• Instead, we are working more hours for more and more goods

• Does life have to be this way?

• Couldn t we move toward a saner, more stable world?

What does all of this mean for us as consumers, managers, citizens?

• We are unlikely to return to the fast growth rates of the past, in the developed world or globally

• This is not disastrous; it is a return to a slower, saner world more like the past

• Demography, technology and the environment pose critical challenges

• How should we respond as managers, consumers, citizens?

• We can adjust expectations and learn to flourish in a slower growth world

As businesses: new definitions of success ; quality, service, excellence, sustainability rather than focusing on numerical targets? Voluntary limits on destructive marketing

As consumers: more informed, conscientious and ethical spending habits Use “dollar votes” to promote change

As citizens: demand a revolution in the public sector: efficiency and an end to waste and corruption Accept taxes that help change behavior in positive ways

22/10/2014

36

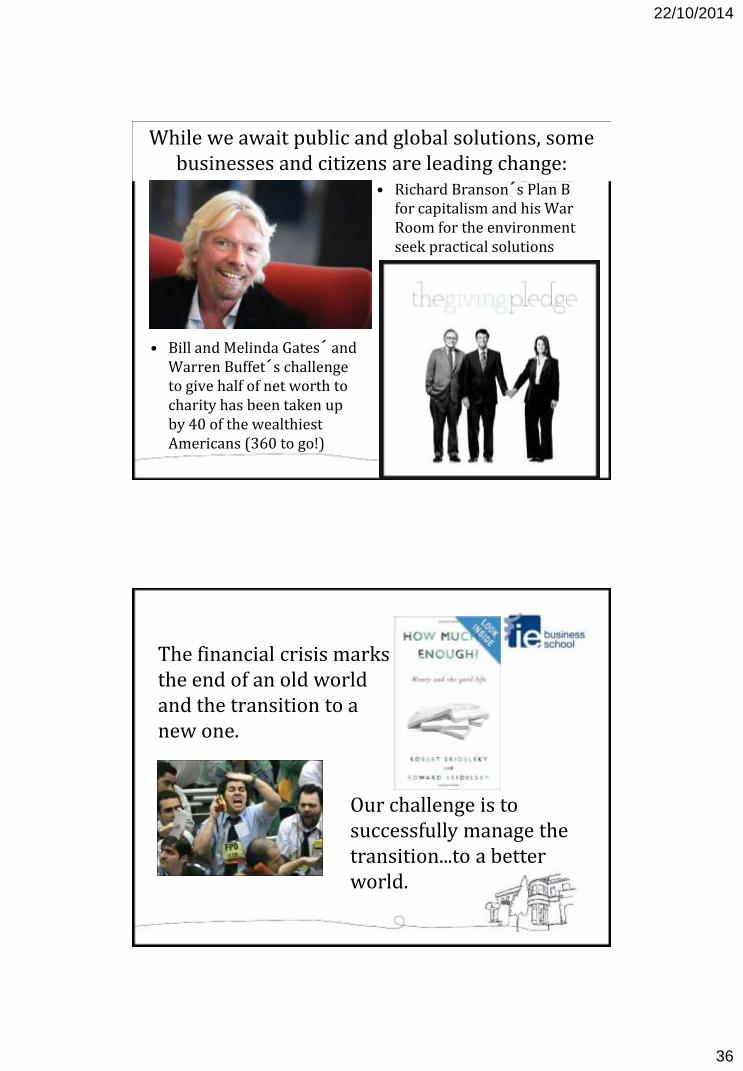

While we await public and global solutions, some businesses and citizens are leading change:

• Richard Branson s Plan B for capitalism and his War Room for the environment seek practical solutions

• Bill and Melinda Gates and Warren Buffet s challenge to give half of net worth to charity has been taken up by 40 of the wealthiest Americans (360 to go!)

The financial crisis marks the end of an old world and the transition to a new one.

Our challenge is to successfully manage the transition...to a better world.

22/10/2014

37

THANK YOU.

Questions?