Embed Size (px)

Citation preview

THE FUTURE LANDSCAPE OF THE HONG KONG DATA CENTRE MARKET

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Rosanna TangHead of Research |

Hong Kong SAR and Southern China+852 2822 0514

Anthony WongAssistant Manager | Research |

Hong Kong SAR+852 2822 0588

2

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Market entry strategy - government supportive measures

Data centres have recently captured interest from Hong Kong investors and other stakeholders in the real estate market, despite the current market downcycle and economic uncertainty the city is facing.

The outbreak of COVID-19 has raised the awareness of agile working ande-commerce, while growing broadband penetration, increasing adaptation of cloud services and the soon-to-be-launched 5G technology, are all pointing to increasing demand for data centres.

Currently, over half of the data centrespace in Hong Kong (8 million sq ft or 743,000 sq m) is clustered in the TseungKwan O area, and we estimate the total data centre stock will grow by 23% over the next three years.

The nature of this sector, with high barriers to entry and long repayment-periods, means it is dominated by a few key players. The lack of available sites remains one of the key challenges for investors. We recommend investors to look at Kwai Chung and Tseung Wan for conversion opportunities, and we believe Tuen Mun and Lok Ma Chau should be better-positioned as the longer-term data centre options.

Insights & Recommendations

Rosanna TangHead of ResearchHong Kong SAR and South China

The growth of cloud computing, the development of the Internet of Things (IoTs) and the growth of data consumption from emerging industries, such as fintech, digital media, and e-commerce, have become the catalyst for the growing demand for colocation (or offsite third-party) data centres in Hong Kong.

In 2020, the Hong Kong government plans to launch its 5G network infrastructure on the back of the ongoing smart city initiative. The enhancement of internet speed and stability should increase the confidence of corporates moving towards cloud storage and computing, while the media and telecommunications sector will likely continue expanding its use of these technologies.

Currently, the data centre market in Hong Kong has been dominated by a relatively small group of local and international operators. To cater to the strong growing demand, more data centres are required, which suggests investors and operators should tap into the sector through wholesale conversion or redevelopment strategies of existing industrial buildings amid the limited land supply.

Hannah JeongHead of Valuation and Advisory ServicesHong Kong SAR

Source: Colliers International; *Note: Developers are charged the land premium when they apply for rezoning their lands to other land use.

Note: 10.76 sq ft = 1 sq m. This report covers the Hong Kong Special Administrative Region of the People’s Republic of China.

Wholesale conversion –change in use of parts of existing industrial buildings

> No fee for waiving any conditions through the change of use

> The data centre conversion must take place in an existing industrial building which is 15 years or older

> The proposed building must be in

− Industrial (I), – Commercial (C) or – Other Specified Uses

(Business) (OUB) zones

Lease modification –redevelopment to high-tier data centres

> The data centre portion of the redevelopment should be at least:

– 40% of the maximum permissible development GFA or,

– a plot ratio of 2.5, whichever is higher

> Land premium* assessed based on high-tier data centre use for the data centre portion

> The redevelopment must take place on an Industrial lot

> Acquire government sites from land sale programme that are allowed to be developed for data centre use

Land acquisition –government land sales for data centres

Industrial buildings into data centres

3

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Cost comparison, wholesale conversion vs. redevelopmentRECOMMENDATIONS Kwai Tsing for near-term opportunitiesKwai Tsing, Kwai Chung and Tsing Yi, located in the western New Territories, is currently the largest industrial cluster, and the second largest data centrehub in Hong Kong following Tseung Kwan O. Although key players such as PCCW solutions, Equinix and Grand Ming Group have already entered the market, we believe the districts still offer great opportunities for data centreconversions given the large amount of industrial stock. For instance, the new data centre project developed by Hon Kwok should be completed this year, which should push Kwai Tsing to further evolve into a more mature data centre cluster.

Source: Colliers International; *The substation connects the data centre to its electric supply.

Wholesale conversion Redevelopment

Acquisition cost HKD4,000-7,000 (USD513-897) per sq ft

Land PremiumNo land premium cost involved

HKD2,500-3,500(USD321-449) per sq ft

Foundation and Construction Not applicableHKD2,500(USD321) per sq ft

Substation Cost* Around HKD300-800 (USD38-103) per sq ft

Wholesale conversion vs. redevelopment

There are three key channels for investors to enter the market: apply for wholesale conversion, redevelopment of industrial lots through modifications, or acquire government lands for data centre usage.

New supply for tailor-made data centres

Government sites would be predeveloped for high-tier data centres in terms of planning and infrastructure. However, new lands for data centres have been very limited, while the development size and cost is usually higher. We recommend this to investors with deep pockets including major operators and developers, absorbing the demand from large tech companies.

Redevelopment for large scale high-tier data centres

Redevelopment of industrial buildings through lease modification would be an option against the limited new land supply. Investors, similarly, can tailor-made or built-to-suit through redevelopment. Additional cost, however, would be involved for acquiring existing properties, demolition and the land premium involved during application for lease modification.

Wholesale conversion as a “quick-win” option

Wholesale conversion from industrial properties into data centres is regarded as an easier option for immediate availability. A larger flexibility is provided that any buildings located in areas zoned “I”, “C” or “OU(B)” are also allowed for data centre installation. This option would be suitable for landlords who want to better utilize their industrial buildings without involving redevelopment costs.

Tuen Mun and Lok Ma Chau as the potential clusters for longer-term optionsWe recommend Tuen Mun and Lok Ma for longer-term data centreredevelopment options. This is in part to cope with demand, but also to offer greater geographic distribution in Hong Kong.

The Lok Ma Chau Loop, a new site for HKSTP’s innovation park

Lok Ma Chau is close to the Hong Kong-mainland China border, which may be desirable by tech companies just across the border such as Tencent, Baidu, and Huawei. The proposed 87-hectare Hong Kong-Shenzhen Innovation and Technology Park in Lok Ma Chau, specifically catering to R&D, technology and start-up incubators, will likely benefit the development of data centres.

Tuen Mun as the next opportunity with new infrastructure

Tuen Mun serves as a strategic location, with the Tuen Mun-Chek Lap Kok Link scheduled to be completed in 2020. This area is suitable for longer-term redevelopment opportunities, although the land premium is one of key factors determined by investors and developers. We recommend investors focus on long-term growth, while expecting stable returns once developed, despite the high cost of market entry.

Tuen Mun

Lok Ma Chau

TseungKwan O

Shatin, Tai Po & Fanling

Kwai Chung & Tsing Yi

Lantau Island

Tuen Mun – Chek Lap Kok Link

4

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Lack of supply

> There is a growing demand from the mainland and international companies looking for service expansions in Hong Kong.

> The supply-demand gap offers investment opportunities, given data centre supply remains limited in the next 2-3 years.

High property prices

> Hong Kong remains as one of the most expensive places in terms of business occupancy cost.

> MNCs in Hong Kong have been actively increasing the ultilisation rate or efficiency of their workplace. Demand for colocation data centres should likely stay firm.

Value-add opportunities

> According to the government figure, vacancy rate of flatted factories stood at 6% as at end-2019, suggesting that some industrial spaces could be better-utilized.

> The current market downcycle coupled with the Revitalization Scheme 2.0 could mean the right time for investors to consider data centre conversions.

High customer stickiness

> Frequent relocation is not preferable for data centres, as it involves high switching costs, and the risk of data loss or service disruption.

> Although operators may take time to achieve a high occupancy rate, customers of data centres will likely stay with the same operator for a long period.

Stable and predictable income stream

> The lease period for data centres ranges from eight to 10 years or longer, which will likely translate into stable recurring income for operators.

> We believe the stable streams of income makes data centres attractive investments.

The Greater Bay Area initiatives

> While the Greater Bay Area (GBA) is planned to be an integrated economic cluster, Hong Kong is well-positioned to leverage its geographical and data protection advantages as a regional data centrehub.

OPPORTUNITIES, RISK AND CHALLENGES

Opportunities

5

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Strong growing rivals

> As a gateway to Southeast Asia, Singapore shares similar advantages including robust data privacy regulation.

> Singapore also edges Hong Kong with the fastest internet speed among the APAC region, with fewer unplanned power cuts, which may shift the regional data centre demand away from Hong Kong.

Local instability

> In 2019, Fitch Ratings and Moody's both downgraded Hong Kong’s credit rating due to rising doubts on its political stability and local governance, which could impact occupier sentiment.

> Facebook and Google have halted plans to activate their international submarine cable, the Pacific Light Cable Network (PLCN), between the US and Hong Kong, turning their attention to the Philippine's and Taiwan instead*.

* Source: Techcrunch, 7 February 2020

Shortage of new land supply

> In the past 10 years, the government has sold only two data centre sites with no new supply in upcoming financial year.

High investment costs

> Investment costs are relatively high as it requires a large floor plate, high-floor loading, high-ceilings and sufficient power supply as well as suitable surrounding area and site access.

Lack of suitable properties

> Almost half of the industrial buildings in Hong Kong are strata-titled, requiring additional costs to unify the ownership, making conversion or redevelopment opportunities in those buildings difficult.

Long investment cycles

> Investing in data centres involves a longer investment cycle while their liquidity is lower compare to other assets, which pushes some investors away.

Risks

.

Challenges

6

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

BOOM IN DATA CENTRE DEMANDData centres have been emerging as one of the most appealing asset types in the real estate market. New technology advancement and cloud computing adoption have driven demand for data centres in the Asia region. According to Cisco’s projection, the Asia Pacific region will have 13.5 billion networked devices/connections by 2023, up from 8.6 billion in 2018, while the number of internet users should grow from 2018’s 2.1 billion to 3.1 billionby 20231.

Whilst Hong Kong is one of the most important global financial centres in Asia, data centredemand is not only coming from cloud services, but a wider-spectrum of drivers including the banking and finance sector, the multimedia and telecoms sector, and the IoT. Internet has also become an important means of communication for enterprises and individuals. According to government figures, the number of organizations using cloud-based services reached 292,100 in 20192, which represented 20% growth from 2017. Meanwhile, the household broadband penetration rate reached 93% as of October 20193, while Statista forecasts the penetration rate to reach 95% by 20234.

Forecast of technology usage in Asia Pacific and Hong Kong

Source: Cisco, Statista

Cloud computing and Internet of Things (IoT)

• Cloud computing is the delivery of computing resources (processing power and software) by a service provider over the internet to a user.

• Around 85% of the enterprises in Hong Kong used cloud computing services in 20192. 99% of information and communications sector enterprises are using cloud computing services.

• The tech giants Intel Corp. and Nvdia had strong revenue growth of 8% and 41% YOY, respectively, in Q4 20195, thanks to a big jump in the sales of chips for data centres and cloud computing.

Banking and Finance

• Traditional banks and financial institutions have been gradually moving towards e-banking and reducing physical service centres and offices.

• Banks are also diversifying services by providing innovative and enterprise solutions which involve additional demand for data storage and analysis.

• The rise of fintech companies and virtual banks require advanced data and network infrastructure to ensure data security and low latency.

Big data and data analytics

• Data has become the most valuable asset a company owns, playing an increasingly important role in decision making and business strategies, measuring and quantitating companies’ goals and success.

• With information becoming more transparent and accessible, trustworthy data has become the major distinguish factor in any industries. The private sectors are encouraged to store large amount of data on cloud with low costs, increasing the demand for data centres from cloud service providers.

5G: a game changer

• Gartner forecasts worldwide 5G network infrastructure revenue to reach USD6.8 billion by 2021, increasing 208% from 2019.

• Hong Kong’s government is adopting a multi-pronged approach in facilitating the development and application of the 5G network and plans 5G services to be fully launched in 2020.

• The improvement of latency will likely drive the demand for cloud storage, real-time data and streaming. Data centres will likely not only expand but also need upgrades amid the network transformation.

Industries

Asia Pacific Hong Kong

1 Cisco; 2 Report on the Survey on Information Technology Usage and Penetration in the Business Sector for 2019; 3 OGCIO; 4 Statista; 5 Intel, Nvdia

Networked devices Internet users Internet penetration

+57% +48%

(Bill

ion

)

13.5

8.6

3.12.1

95%93%

+2pps

7

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

GROWING DATA CENTRE DEMAND FROM MAINLAND COMPANIESThe tech-savvy nature of China has boosted the development of cloud computing, IoT and e-commerce. With its proximity to China, Hong Kong should benefit from the growing demand for secure data centre services from mainland companies. Chinese technology giants, such as Tencent, Baidu and Alibaba, have also been driving the growth of the data centremarket in Hong Kong. For instance, Alibaba Cloud has had a data centre in Hong Kong since 2014, while doubling its capacity in just five years6. Tencent Cloud, which set up its first data centre in Hong Kong in 2013, also opened a second data centre in 2018 for expanding service coverage to the Greater Bay Area7.

CORONAVIRUS AS A WAKE-UP CALL FOR BUSINESSESAccording to Colliers’ recent Coronavirus: Impact On Chinese Real Estate report, 80% of data centre operators surveyed believe they will benefit from a growth in telecommuting demand.

Remote office solutions and cloud computing

The coronavirus outbreak has forced world’s largest work-from-home experiment, triggering the acceleration of digitalization and automation of international banks and MNCs. Corporates, with a higher proportion of staff working from home, will likely increase the use of tools such as Microsoft MyAnalytics that collect data for tracking the efficiency and wellbeing of staff working from home.

Online retail and e-commerce

Consumer demand is increasingly shifting towards online shopping, and retailers should invest in online shopping platforms, enhancing omnichannel distribution strategies, as well as tools for data collection to analyseshopping patterns.

Source: Colliers’ report Coronavirus: Impact On Chinese Real Estate

Alibaba Cloud Tencent Cloud

Data centre TGT Hong Kong Data Centre 2 HGC Global Centre

Location Tseung Kwan O Wong Chuk Hang

Operator Towngas TelecomHutchison Global Communications

Launch date May 2014 October 2013

Examples of mainland companies’ data centres in Hong Kong

Source: Towngas Telecom; HGC

6 DataCenterNews, 18 January 2019. 7 Tencent, 26 March 2018.

Limited clarity

11%Yes

80%

No

9%

Percent of respondents, will the coronavirus outbreak boost demand for telecommuting and data centres?

8

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

HONG KONG’S COMPETITIVE ADVANTAGE

0 50 100 150 200 250

Singapore

Hong Kong (SAR)

Monaco

Romania

Switzerland

France

Sweden

United States

Thailand

Denmark

Mbps

Average download speeds over fixed broadband

Source: Ookla Speedtest, as of Jan 2020

02468

101214161820

Min

ute

s p

er y

ear

Unplanned power interruptions

Source: CLP Holdings 2018 Sustainability Report (page 114).Note: 2016-2018 average for CLP Power was 10.3 minutes, but 8.9 minutes was due to the impact of typhoon Mangkhut, otherwise the three-year average would be 1.4 minutes. Figures for other cities are the average in 2015-2017.

Hong Kong (HK) has been vulnerable to typhoons due to geographical location. However, Hong Kong is unlikely to see earthquakes, volcanos, tornados and large-scale wildfires. In addition, Hong Kong has a reputation for using best practices for data reliability and protection, as well as having a stable power supply. These factors combine to make Hong Kong one of the best locations for data centres.

Source: Ookla Speedtest, Office of the Government Chief Information Officer8,9 CLP Information Kit; 10 Office of the Communications Authority; 11 Ookla, Speedtest Global Index, as of January 2020

Why Hong Kong for data centres?

Reliable Power supply

CLP Power Hong Kong Limited (CLP),

one of two electricity suppliers in Hong

Kong, achieves over 99.9%8 supply reliability for

Kowloon and the New Territories.

Low electricity costs

HK (CPL Power) charges the lowest

electricity tariffs among major cities such as Singapore,

Sydney, London and New York, at only

HKD1.15 (USD0.13) per kilowatt-hour

(kWh)9.

Network connectivity

Over 250 internet service providers

licensed to provide broadband services in

HK10. HK has the world’s second fastest

internet download speed over fixed broadband (170

Mbps)11.

Data protection

HK has implemented The Personal Data

(Privacy) Ordinance to protect personal data collection. This

attracts demand from mainland firms

emphasizing the internationalisation

of their service.

Climate

HK’s temperature ranges between 10

and 35 degrees Celsius. Moreover, HK is

located in a zone with low risk of natural calamities such as earthquakes and

tornadoes.

9

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Shatin

Tai Po

Tsuen Wan & Tsing Yi

Kowloon Bay

Chai Wan

Lantau IslandAAGAPCN-2FEA

Tong FukFLAG/REACH NAL

Deep Water BaySeeMeWe-3TGN-IAPLCN

Chung Hom KokEAC-C2CSJCHK-ASJC-2BTOBE

Cape D’AguilarAAE-1

Tsueng Kwan OEAC-C2CAPGHK-GASE/Chaya Malaysia

Aberdeen

Central

TsuengKwan O

WELL ESTABLISHED INTERNET INFRASTRUCTUREBy January 2019, Hong Kong was linked to the internet through 11 submarine cables12, increasing from six in 2012. As a major regional telecommunications hub, Hong Kong has robust data centre demand from telecom companies and enterprises.

Hong Kong has eight cable landing stations, located in Tseung Kwan O, Deep Water Bay, Chung Hom Kok, Cape D’Aguilar, and Tong Fuk. As development sites for data centres are limited in most of these areas except Tseung Kwan O, demand from submarine cable and telecommunications operators for high-tier* data centres and has increased along with demand from their end-users, enterprises and telecommunications customers.

Source: Office of the Communications Authority

0

20,000

40,000

60,000

80,000

Mar

-05

Sep

-05

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

Sep

-16

Mar

-17

Sep

-17

Mar

-18

Sep

-18

Mar

-19

Sep

-19

Gig

abit

per

sec

on

d

Data centres: The missing puzzle

Despite the well-established internet infrastructure and the rising demand for data centres, data centre supply and capacity, one of major factors in MNCs’ location strategy, has been lacking.

Due to a shortage of land, the government has prioritised residential land for development. However, the commercial land supply has also been increased recently with the development of CBD2 in Kowloon. Land for data centres has been limited in government land sale programmes. Over the past 10 years, the government only sold two data centre sites13, which were both acquired by SUNeVision, the largest data centre operator in Hong Kong.

Hong Kong, locations of cable landing stations and cable names

12 Landing of Submarine Cables in Hong Kong, OFCA13 Lands Department*Data centres are classified into four tiers in general, the higher tier the better performance. Please see Data Center Site Infrastructure Tier Standard: Topology by Uptime Institute for more details.

Servers with appropriate security

and backup equipment that stores, manages

and disseminates data

Insufficient

Cloud computing/ IoT/ e-commerce

The source of demand for data centres

Increasing

Landing stations and telecom cables within and across regions; to connect

between end-users and data centres

Established

Telecom infrastructure Data centre

Capacity of external telecommunications facilities (activated cable)

Source: Data Centre Facilitation Unit

Cable Landing Stations

Data Centre Clusters

10

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Wholesale conversion –change in use of parts of existing industrial buildings

> No fee for waiving any conditions through the change of use

> The data centre conversion must take place in an existing industrial building which is 15 years or older

> The proposed building must be in

– Industrial (I),

– Commercial (C) or

– Other Specified Uses (Business) (OUB) zones

Lease modification –redevelopment to high-tier data centres

> The data centre portion of the redevelopment should be at least:

– 40% of the maximum permissible development GFA or,

– a plot ratio of 2.5, whichever is higher

> For the data centre component, the land premium** assessed based on high-tier data centre use

> The redevelopment must take place on an Industrial lot

> Acquire government sites from land sale programme that are allowed to be developed for data centre use

Source: Developing Data Centres in Hong Kong. *See also: Lease Modification for Development of High-tier Data Centre on an Industrial Lot. **Developers are charged the land premium when they apply for rezoning their lands to other land use.

Adequate space for cooling infrastructure, transformers and petrol or gas storage

Must be in Industrial (I), Commercial (C) or Other Specified Uses (Business) (OUB) zone*

HIGH-TIER DATA CENTRE REQUIREMENTS

MARKET ENTRY STRATEGY - GOVERNMENT SUPPORTIVE MEASURESThere are three main types of data centre incentives in Hong Kong, which are detailed in the Measures to Facilitate the Development of Data Centres,promulgated by the Office of the Government Chief Information Officer (OGCIO). Investors and data centre operators in Hong Kong can leverage the measures that allow the redevelopment or conversion, in whole or in part, of industrial buildings into data centres.

Distance away from petrol stations and oil depots

Sufficient distance from any other hazardous businesses or goods

Industrial buildings into data centres

Land acquisition –government land sales for data centres

11

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Hong Kong Island

Kowloon Tseung Kwan O

Shatin, Tai Po & Fanling

Kwai Chung & Tsuen Wan

Geographical distribution of data centres in Hong Kong (%)

Source: Companies, Colliers International

CURRENT DATA CENTRE TREND Data centres clusters mainly in the New TerritoriesCurrently, there are around 8 million sq feet (743,224 sq meter) of datacentre facilities in Hong Kong, with more than half (56%) of them located inTseung Kwan O. Most high-quality and sophisticated Tier IV14 data centresare also clustering in Tseung Kwan O Industrial Estate. Given the scarcity ofthe new data centre plots in the government land sale market, prices for datacentre sites have been growing rapidly over the last few years. The averageland prices for the last two high-tier data centre plots, both in Tseung Kwan OIndustrial Estate, have vastly expanded by five times, from HKD904 (USD116)per sq feet in 2013, to HKD4,500 (USD577) per sq feet in 2018. Meanwhile,Kwai Chung and Tsuen Wan secured the second-largest (21%) data centrecluster, according to our data.

Local operators dominate the marketDue to the nature of high barriers to entry and long repayment-period, data centre remained a niche sector in Hong Kong. The requirement of sophisticated technologies and facilities, and the substantial development cost involved may have sidelined some small and individual investors to explore opportunities in other asset type. According to Colliers’ estimate, the top five data centre operators already accounted for over half of the market shares (in terms of data centre floor area) in Hong Kong, with key players including SUNeVision, PCCW Solutions, NTT Communications, China Unicom and Telehouse.

Government policies in support of data centresApart from the aforementioned incentive measure discussed on page 10 inthis report, the government also announced in the latest 2020-21 BudgetSpeech, the scheduled completion of the 290,700 sq feet (27,000 sq meter)Data Technology Hub15 in Tseung Kwan O Industrial Estate by H1 2020.Developed by Hong Kong Science and Technology Park, the facility should befocusing to support data technology, information, and telecommunications,including services to support data centre and disaster recovery plans.Meanwhile, the government also plans to launch Smart City Blueprint forHong Kong 2.0 in 2020 to further promote smart city development.

14 Tier IV defines as facility events affecting the computer room are empirically reduced to 0.8 hours on an annual basis. Tier IV sites consistently demonstrate 99.99% availability.15 Hong Kong Science Park and Technology Corporation

Hong Kong Island

Tseung Kwan O

Kwai Chung & Tsuen Wan

Shatin, Tai Po & Fanling

Kowloon

56%

21%

11%

9%

3%

12

COLLIERS RADAR DATA CENTRE | RESEARCH | HONG KONG | 8 APRIL 2020

Tsuen Wan

Kwai Tsing

Shatin

Kowloon East

TseungKwan O

Island East

Island South

Tai Po

0

2

4

6

8

10

12

2018 2019 2020 E 2021 E 2022 E

New supply

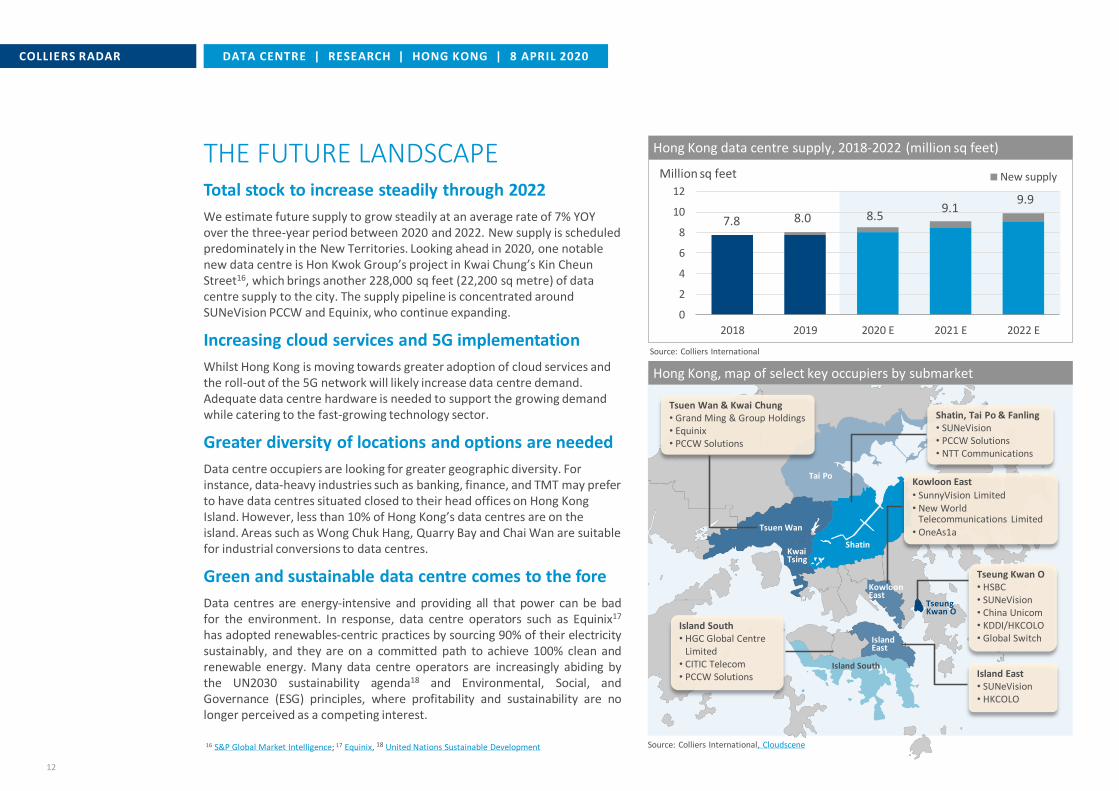

THE FUTURE LANDSCAPE Total stock to increase steadily through 2022

We estimate future supply to grow steadily at an average rate of 7% YOY over the three-year period between 2020 and 2022. New supply is scheduled predominately in the New Territories. Looking ahead in 2020, one notable new data centre is Hon Kwok Group’s project in Kwai Chung’s Kin CheunStreet16, which brings another 228,000 sq feet (22,200 sq metre) of data centre supply to the city. The supply pipeline is concentrated around SUNeVision PCCW and Equinix, who continue expanding.

Increasing cloud services and 5G implementation

Whilst Hong Kong is moving towards greater adoption of cloud services and the roll-out of the 5G network will likely increase data centre demand. Adequate data centre hardware is needed to support the growing demand while catering to the fast-growing technology sector.

Greater diversity of locations and options are needed

Data centre occupiers are looking for greater geographic diversity. For instance, data-heavy industries such as banking, finance, and TMT may prefer to have data centres situated closed to their head offices on Hong Kong Island. However, less than 10% of Hong Kong’s data centres are on the island. Areas such as Wong Chuk Hang, Quarry Bay and Chai Wan are suitable for industrial conversions to data centres.

Green and sustainable data centre comes to the fore

Data centres are energy-intensive and providing all that power can be badfor the environment. In response, data centre operators such as Equinix17

has adopted renewables-centric practices by sourcing 90% of their electricitysustainably, and they are on a committed path to achieve 100% clean andrenewable energy. Many data centre operators are increasingly abiding bythe UN2030 sustainability agenda18 and Environmental, Social, andGovernance (ESG) principles, where profitability and sustainability are nolonger perceived as a competing interest.

Source: Colliers International

Hong Kong data centre supply, 2018-2022 (million sq feet)

Hong Kong, map of select key occupiers by submarket

Million sq feet

7.8 8.0 8.59.1

9.9

Source: Colliers International, Cloudscene16 S&P Global Market Intelligence; 17 Equinix, 18 United Nations Sustainable Development

Tsuen Wan & Kwai Chung• Grand Ming & Group Holdings• Equinix• PCCW Solutions

Shatin, Tai Po & Fanling• SUNeVision• PCCW Solutions• NTT Communications

Tseung Kwan O• HSBC• SUNeVision• China Unicom• KDDI/HKCOLO• Global Switch

Island East• SUNeVision• HKCOLO

Island South • HGC Global Centre

Limited• CITIC Telecom• PCCW Solutions

Kowloon East

• SunnyVision Limited• New World

Telecommunications Limited• OneAs1a

About Colliers International

Colliers International (NASDAQ, TSX: CIGI) is a leading real estate professional services and investment management company. With operations in 68 countries, our more than15,000 enterprising professionals work collaboratively to provide expert advice and services to maximize the value of property for real estate occupiers, owners and investors. Formore than 25 years, our experienced leadership, owning approximately 40% of our equity, has delivered compound annual investment returns of almost 20% for shareholders. In2019, corporate revenues were more than $3.0 billion ($3.5 billion including affiliates), with $33 billion of assets under management in our investment management segment. Learnmore about how we accelerate success at corporate.colliers.com, Twitter or LinkedIn

Copyright © 2020 Colliers International

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it.No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

Primary Authors:

Rosanna TangHead of Research | Hong Kong SAR and Southern China+852 2822 [email protected]

Anthony WongAssistant Manager | Research | Hong Kong SAR+852 2822 [email protected]

For further information, please contact:

Nigel SmithManaging Director | Hong Kong SAR+852 2822 [email protected]

Andrew HaskinsExecutive Director | Research | Asia+852 2822 [email protected]

Hannah JeongHead of Valuation and Advisory Services | Hong Kong SAR+852 2822 0589 [email protected]