Embed Size (px)

Citation preview

Page 1 of 239

Title: Understanding IRAs

Difficulty: Beginner

Description: As an investment professional, Individual Retirement Accounts

(IRAs) are a natural place to start helping your clients with

retirement planning. The IRA is a powerful tool to help clients retire

in dignity. What is the difference between Traditional and Roth

IRAs? How can the Stretch IRA help with estate planning? This

series gives you a better understanding of Traditional and Roth

IRAs and some of the decisions your clients may face in planning

for retirement.

The Genesis of Individual Retirement Accounts

Employee Retirement Income Security Act of 1974 (ERISA)

The Employee Retirement Income Security Act of 1974 (known as “ERISA”) established legal

standards for employee benefit plans, and introduced tax-deductible Individual Retirement

Accounts (IRAs) as a way for Americans to save for retirement. In the decades since IRAs

were created, IRA contribution limits and personal tax deductions have increased; employers

can establish special IRA plans for employees; and Roth IRAs were created, allowing

nondeductible contributions that can accumulate tax-exempt earnings for years to come.

IRA Definition

An IRA is a tax-favored personal retirement savings plan to which the account owner may

make contributions up to limits permitted per year (indexed for inflation). An account owner

may “rollover” a qualified pension, profit sharing, or Keogh account to an IRA when no longer a

participant in a former plan (or roll an IRA account into a qualified plan in some situations).

There are two basic types of IRAs: (a) traditional and (b) Roth. Let’s get started with some

basics in the law:

There is always a written IRA trust or custodial account document. Individuals cannot be

IRA fiduciaries. Trustees and custodians must be financial institutions such as banks,

federally insured credit unions, broker-dealers, or other organizations that demonstrate

trustworthiness to the IRS. [CFR §1.408-2(e)(2)(i)(A)]

Page 2 of 239

IRA issuers must provide account owners a “disclosure” statement and a copy of the

plan (and any projections or guarantees), within seven days of purchase.

Compensation includes salary, wages, commissions, self-employment income, alimony,

separate maintenance, or nontaxable combat pay. Compensation doesn’t include

deferred compensation, earnings and profits from property, interest and dividend

income, pension or annuity income, income from certain partnerships, or Conservation

Reserve Program payments.

Contributions may be made as late as April 15th (excluding any extensions) of the year

following the tax year on behalf of which the contribution is made. For example,

contributions for 2016 may be made until April 17 of 2017.

Contributions must be in cash and are limited to the lesser of (a) 100% of compensation

included in gross income or (b) the maximum contribution limit.

An account owner can make a contribution for a non-working spouse if (a) they file a

joint return, and (b) the “non-working” spouse’s compensation is less than the working

spouse’s compensation included in his gross income for the year.

Within seven days of purchase, the account owner may revoke an IRA plan without

paying sales commissions or administrative expenses.

An IRA account owner will normally have an option to complete a beneficiary

designation form. If there is no beneficiary form, the plan itself determines who receives

everything at death.

Anyone can establish an IRA. But to claim a tax deduction for contributions, the account

owner must have compensation and must not have attained age 70½ during the year

for which the contribution is made.

Contributions cannot be invested in life insurance, artwork, rugs, metals, gems, stamps,

antiques, coins, alcoholic beverages, and certain other tangible property. However, a

plan may invest in certain gold and silver US coins, coins issued by states, and some

platinum coins. A plan may purchase certain gold, silver, platinum and palladium bullion

if the bullion remains in the physical possession of an IRA trustee.

Contributions must be nonforfeitable under the plan.

Contributions in excess of those permitted under current contribution limits will incur a

6% excise tax even if made inadvertently.

Page 3 of 239

The excise tax can be avoided if the excess contribution (and any income attributed to

it) is withdrawn before the due date (April 15th, plus extensions, if any) of filing an

income tax return.

IRA investments can include cash (such as an IRA savings account or CD), mutual

funds, and variable or fixed annuity contracts, among others.

IRA accounts are exempt from an owner’s creditors if necessary for the support of the

owner and his or her dependents

The Bankruptcy Abuse Protection and Consumer Protection Act of 2005 (BAPCPA)

provides a $1 million (adjusted periodically for inflation) exemption for contributory IRAs

regardless of the need for support. Qualified retirement plan assets that are rolled over

into an IRA are completely protected from bankruptcy proceedings even if the amount

exceeds $1 million. SEP and SIMPLE IRAs are also excluded from bankruptcy

proceedings.

The law permits another personal retirement savings account. It is an Individual

Retirement Annuity, and is subject to the same rules as IRAs. The annuity contract must

not permit (a) assignment of the policy to cover a loan, or (b) forfeitability for missing a

premium payment. Someone other than the owner may make annuity payments, but

only the owner or surviving beneficiaries may receive benefits from the annuity contract.

Without paying an income tax, an IRA may be transferred directly to a spouse (or a

former spouse) under a divorce or separate maintenance decree. The IRA is then

maintained solely for the former mate.

An IRA pledged as collateral for a loan is taxable to the extent of the assignment.

The income tax on taxable IRA withdrawals before turning 59½-years of age is

increased by 10% of the portion of the amount includible in gross taxable income. This

is the commonly referred to “penalty tax on premature distributions.”

A nondeductible cash contribution of $2,000 annually is permitted to a Coverdell

Education Savings Account (ESA) – formerly known as an “Education IRA” – for

designated beneficiaries. All distributions are tax-free if they are for qualified higher

educational expenses of the beneficiary paid in the same year the distribution is made.

Page 4 of 239

In the past, workers counted on employer pensions to see them through retirement. Today,

Americans have become increasingly responsible for their own retirement plans so they can

retire and have more control over their financial future. IRAs represent one of the largest and

fastest growing shares of the US retirement market; and it is expected that IRAs’ share will

continue to grow. Here are a few reasons why:

Contribution Limits - IRA contributions limits rise gradually. For 2016, the maximum

contribution to all of a client’s traditional and Roth IRAs if you’re under 50 is $5,500. The IRA

contribution limit does not apply to rollover contributions or qualified reservist repayments.

Catch-Up Provisions for Those Over 50 Years of Age - There are “catch-up” provisions

where those 50 and over can increase their annual contribution. For 2016, if you are 50 and

over you can contribute $6,500.

Control Over Investments and Account Features - Individuals control their personal IRA

investments, beneficiary designations and payout options; that makes IRAs much more flexible

than most 401(k) and pension programs, which tend to provide limited opportunities for

creative financial and estate planning.

Protection From Creditors – As of April 1, 2016, the first $1,283,025 (adjusted periodically for

inflation) inside traditional and Roth IRA accounts, under most circumstances, is fully exempt

from creditors of an account owner in bankruptcy. The amount over the exemption is subject to

state laws regarding creditor protection. Generally, these plans are protected because of the

penalties and costs incurred by the account owner to access the funds.

It should be noted, there are a handful of States that treat Roth IRAs differently. Roth IRAs are

funded with after-tax dollars, which limits the penalties and costs a debtor may incur by

accessing the funds within a Roth.

This is an industry hot topic. IRA protection from creditors does not apply to all

circumstances. In 2014, the U.S. Supreme Court ruled that funds from an inherited IRA are not

“retirement funds” and, therefore, do not qualify for an exemption from the debtor’s bankruptcy

Page 5 of 239

estate (Clark v. Rameker, STc., June 12, 2014). The best protection you can provide your

client is to ensure IRA accounts are protected based on the laws of the State in which your

client resides or holds the IRA.

U.S. Treasury Rules - The U.S. Treasury finalizes the rules for distributions from IRAs and

qualified retirement plans. The Treasury makes regulations as they pertain to defined benefit

plans and annuity contracts providing benefits from qualified plans, IRAs and 403(b) contracts.

Traditional IRAs

Traditional IRAs give account owners tax deductions with the benefit of tax-deferred income

earned for the account. Here are some additional rules for these IRAs:

1. Individual tax deductions are limited to the contributions limits (under “the ground rules”

supra), on his or her own behalf to a traditional IRA. However, if an account owner is an “active

participant” in a qualified corporate or Keogh pension, profit sharing, stock bonus or annuity

plan, simplified employee pension, 403(b) tax sheltered annuity, simple IRA or governmental

plan, deductions are reduced or eliminated depending on the taxpayer’s filing status and

Modified Adjusted Gross Income (MAGI).

2. MAGI for purposes of the IRA deduction is adjusted gross income before the IRA deduction

increased by certain excluded income or deductions (such as student loan interest).

3. Deductions for contributions by a married person for a spouse are limited by the lesser of:

The maximum contribution limits of $5,500 (in 2016 [adjusted periodically]) for those

under 50; and

100% of the non-working spouse’s includable compensation, less (i) the amount of any

IRA deduction taken by the working spouse, and (ii) the amount of any contribution to a

Roth IRA by or for the non-working spouse.

4. Once 70½, contributions are no longer permitted to a person's traditional IRA.

5. An IRA deduction is available even though other deductions aren’t itemized. It is an “above

the line” deduction.

6. IRA administrative or trustee fees paid separately are deductible. Sales commissions paid

separately are not.

7. An account owner may elect not to deduct contributions otherwise deductible.

Nondeductible contributions are limited to the excess of the maximum deductible contribution

Page 6 of 239

over the amount actually claimed as a deduction. (And, nondeductible amounts are reduced by

contributions made that year to a Roth.) The sum not deducted builds a "cost basis" for the

account. Later, when distributions are made from this traditional IRA, the account owner

excludes a portion from taxes.

Example: At age 70½, George has $1 million in traditional IRAs; this includes a nondeductible

contribution of $10,000 (1%). He withdraws $40,000. Accordingly, $400 (1%) of his distribution

is tax-free. Each year that George makes withdrawals from his traditional IRA, he will repeat

this calculation until these exclusions equal $10,000; and then, all withdrawals are taxable.

8. There may be a 10% penalty tax on pre-age 59½ distributions, which will be explained later.

9. Distributions must begin by April 1st following the taxable year an account owner attains age

70½.

Roth IRAs

Roth Rules

Roth IRAs are personal retirement savings plans that don’t give tax deductions for

contributions, but permit accumulations to build up tax-free. (This makes Roth IRAs attractive

to those who expect to have a higher tax rate at retirement.) Here are some additional rules

applicable to Roth IRAs:

Roth IRAs must be designated clearly when established.

Unlike traditional IRAs, contributions to Roth IRAs are permitted after 70½.

Contributions to individual and spousal Roth IRAs (disregarding any active participant

restrictions) are reduced by any contributions (deductible or nondeductible) for the year

made to traditional IRAs.

The Examples within the course rely on more simple, rounded

figures for the purpose of teaching the concept rather than

requiring memorization of numbers from life expectancy tables,

contribution charts, annual estate exemptions, tax rates, etc.

Further, the examples rely on the values assigned to the year for

which the example applies. It is incumbent on you, in your

practice, to use the most recently issued IRS values.

Page 7 of 239

For 2016, the Roth IRA contribution limit is phased out as indicated in this IRS illustration:

Excess contributions incur a 6% penalty tax. Internal Revenue Code (IRC) Section 4973

imposes a 6% penalty tax on certain excess contributions to a traditional or Roth IRA.

If the account owner is not a married person filing a separate return, he or she can

transfer a traditional IRA to a Roth IRA (technically, a “conversion”). A surviving spouse

beneficiary can also convert to a Roth. The amount rolled over is included in income as

if the traditional IRA was cancelled. Therefore, if only deductible contributions were

made to a former traditional IRA, the entire account value is taxable when rolled to the

Roth.

A Roth conversion is made from either:

A distribution from a traditional IRA to a Roth, within 60 days, or

A direct transfer to that Roth by an IRA trustee.

After five taxable years, distributions from a converted Roth IRA to an account owner

are income tax-free if he or she is 59½ or older; disabled; or the funds are used to

acquire, construct or reconstruct a first residence (or to pay its closing costs) up to

$10,000. The five year period isn’t waived simply because the account owner dies –

even though a beneficiary must usually begin taking withdrawals from the account in the

year following the year of death. However, these distributions are tax-free (up to the

original account owner’s original contribution). Once the five-year period expires, all

distributions are tax-free.

Unlike traditional IRAs, distributions needn’t commence at 70½ (or a spouse’s age 70½,

if he or she rolls over the account at the IRA owner’s death); in other words, Roth IRAs

o Your filing status is married filing jointly or qualifying widow(er) and your modified AGI is at least $184,000. You cannot make a Roth IRA contribution if your modified AGI is $194,000 or more.

o Your filing status is single, head of household, or married filing separately and you did not live with your spouse at any time in 2016 and your modified AGI is at least $117,000. You cannot make a Roth IRA contribution if your modified AGI is $132,000 or more.

o Your filing status is married filing separately, you lived with your spouse at any time during the year, and your modified AGI is more than -0-. You cannot make a Roth IRA contribution if your modified AGI is $10,000 or more. [IRS Pub 590]

Page 8 of 239

aren’t subject to the age 70½ required minimum distribution (RMD) rules for traditional

IRA account owners.

Rollover IRAs - The Basics

Congress Viewpoint on IRAs

Plain and simple, Congress wants taxpayers to use their IRA for retirement and not as an

emergency fund along the way. Consequently, IRA owners really need to know how to

navigate the rules on:

Withdrawals made before age 59½

RMDs after age 70½

Let’s look first at eligible rollovers, which are taxable distributions from retirement accounts that

can actually be put back into a tax-protected environment. Rollovers are transfers of funds

received from qualified plans, 403(b) annuities, eligible 457 government plans, and IRAs to

another qualified plan or IRA and which follow the requirements set out in the Internal Revenue

Code and Regulations. Rollovers are important because income taxes on the distribution

“rolled-over” are deferred into the future. Here are some of the rules:

When someone receives a distribution from an IRA, 403(b) annuity, eligible 457

government plans or qualified plan, a rollover must be completed within 60 days of

payment.

Since there is a mandatory income tax owed or withheld on all taxable distributions, a

taxpayer pays taxes on the amount of tax retained if he or she doesn’t personally add

this amount to the rollover. For instance, when Harry terminates employment, his

payout from the company’s 401(k) plan is $100,000. After the trustee withholds

$20,000 in taxes, Harry receives $80,000 net. He rolls over only his $80,000

distribution to an IRA. The result: Harry pays taxes on $20,000. And, he may owe a

10% early distribution penalty of $2,000. The solution: To avoid these taxes, Harry

must add $20,000 to his $80,000 distribution and rollover a full $100,000 to his IRA.

The reason: The law considers the $20,000 in withheld funds a “distribution eligible

for a rollover.” If the total amount of Harry’s payout isn’t rolled over it is taxed.

Qualified plans and 403(b) annuities must offer participants the option to have eligible

distributions transferred directly to an IRA or other retirement plan [a qualified defined

Page 9 of 239

contribution plan, e.g., profit sharing, 401(k) or money purchase pension] that accepts

rollovers. (In Harry’s situation, he could authorize a direct transfer of $100,000 to his

IRA, and there would be no income tax withheld.)

Rollover funds can be divided among several IRAs.

A participant can roll over all or part of any distribution from an IRA except: 1) a required

minimum distribution (RMD), or 2) a distribution of excess contributions and related

earnings.

As long as the RMDs are met, rollovers by individuals who have attained 70½ are

allowed.

A participant who received funds from a qualified retirement plan and placed them in his

wife’s traditional IRA, but not pursuant to a valid Qualified Domestic Relation Order

(QDRO) did not make a valid rollover.

What is a Qualified Domestic Relations Order?

A "qualified domestic relation order" (QDRO) is:

An IRA owner may receive funds from a traditional IRA and roll them into a qualified plan,

regardless of source. For example, someone with a large IRA might establish a new company

that creates a profit sharing plan. Then, she makes a direct rollover of the IRA into her qualified

plan account. As long as a surviving spouse is the sole beneficiary with an unlimited right to

withdraw amounts from her spouse’s IRA (or a portion of it), she may roll it over to her own IRA

at his death. Be aware: The trustee of a trust for her benefit has no automatic rollover right,

even if she is the only beneficiary of the trust.

A domestic relations order that creates or recognizes the existence of an "alternate payee's" right to receive, or assigns to an alternate payee the right to receive, all or a portion of the benefits payable with respect to a participant under a pension plan, and that includes certain information and meets certain other requirements. In divorce, a spouse or former spouse of a plan participant may rollover taxable funds received pursuant to a qualified domestic relations order (QDRO).

Page 10 of 239

This is an industry hot topic. “60 day rollovers”, i.e., indirect rollovers that allow a taxpayer to

receive the funds outright and re-contribute the same amount distributed within a sixty day

period to a new or the same IRA, are only permitted once per twelve month period. (Note that

this has nothing to do with the calendar year. Such rollovers can only be made once every

twelve months, regardless of how many IRA accounts an individual may have.) However, any

number of direct rollovers can be made that are trustee-to-trustee transfers between plans.

The Penalty Period, Up to Age 59½

Early Distribution from 401(k) and IRA Plans

If a client withdraws money from a traditional individual retirement account (IRA), 401(k),

403(b), or other qualified retirement plan before age 59½, he/she may be subject to an early

distribution penalty of 10%. There are exceptions. This penalty does not apply to Roth IRAs as

long as it has been at least five years since the Roth account was opened. Here's what you

need to know about the early distribution tax.

The additional tax on a distribution prior to turning 59½ is10% of the taxable distribution. The

taxable amount is also included in taxable income. This 10% tax is in addition to regular

income taxes. This is sometimes referred to as the premature or early withdrawal tax penalty,

because it is similar to the penalty banks charge when a savings account is liquidated early.

This can be avoided if the client meets certain criteria, but the withdrawal cannot avoid

inclusion in the taxable income. So you need to make sure clients consider the tax impact

before tapping into retirement accounts for short-term financial emergencies. When Congress

invented traditional and Roth IRAs as long-term retirement savings programs, it was meant to

discourage "early" withdrawals. The result: Most casual early distributions incur a 10% excise

tax, in addition to any regular ordinary income tax. In fairness, however, the law allows IRA

owners some basic exemptions from the tax on premature withdrawals. For example, there is

no 10% premature distribution tax on “early” IRA payments—

To an account owner, after he or she attains 59½;

To a beneficiary, or the owner’s estate, on or after the owner’s death;

After the account owner’s permanent disability; for an account owner’s medical

expenses that exceed the applicable percentage-of-adjusted gross income floor,

regardless of whether the account owner itemizes deductions on his or her tax return;

Page 11 of 239

For an unemployed account owner’s health insurance premiums;

For "qualified higher education expenses" (tuition, room and board, fees, books,

supplies and equipment - even graduate courses) for the account owner, her spouse

and their children or grandchildren;

For a "qualified" (no home ownership in prior two years) first-time homebuyer’s

expenses of acquiring, constructing or reconstructing a personal residence (including

settlement, financing and closing costs), – up to a maximum of $10,000 during the

account owner’s lifetime;

The portion of a distribution that is not included in taxable income because it constitutes

an account owner’s nondeductible contributions to the IRA;

On account of a federal tax levy;

Distribution to reservists while serving on active duty for at least 180 days; and

One-time (once in a lifetime) rollover distribution to a Health Savings Account.

Real Life Examples

Congress also protects “all substantially equal payments” from an IRA paid over the lifetime of

the account owner (or joint lifetimes of the owner and a beneficiary). What follows are three

real-life situations that show how this exemption might help the taxpayer:

Example One

Let’s say Agnes is 55, and needs $50,000 for a family emergency. Her $300,000 IRA has the

money, but a $50,000 distribution wouldn’t be protected from the 10% penalty tax under the

basic exemptions. Use the following strategy:

Step one: Agnes borrows $50,000 from a commercial lender, friend or relative. Assume

the lender charges 8% interest and her loan obligation is $12,500 annually for five years

- a total payback of $62,500.

Step two: She begins taking a series of “substantially equal payments” from her IRA that

simply amortizes the $300,000 account over her IRS life expectancy. The interest rate

must not exceed a reasonable interest rate (the IRS considers a reasonable rate to be

any rate that does not exceed 120% of the mid-term applicable federal rate (AFR) –

assume 1.5% – on the date payments commence, and the arrangement can’t be

Page 12 of 239

modified during the next 60 months unless the account owner dies or becomes

disabled.

Observations: Using a 1.5% interest rate (and say, a 29-year IRS unisex single life expectancy

under the Single Life Table –29.6 years rounded downwards), the taxable (but penalty-free)

IRA distribution is $12,834 annually; and this is nearly equal to her loan payment of $12,500

annually. The law requires a period of five years before ceasing or modifying this arrangement,

but (a) then she’ll be 60, and (b) the $50,000 loan will be fully repaid.

Example Two

Norman is 55 and wants to acquire a $500,000 life insurance policy payable to a charity. The

projected tax-deductible annual premium is $21,000 for a 10-year period. He has a $500,000

IRA and a 29.6 year IRS unisex single life expectancy. Use this strategy:

Applying a 1.5% interest rate over 29 years, Norman can withdraw $21,389, annually

from the $500,000 account. This “coincidentally” covers his tax-deductible premium of

$21,000, and is penalty tax-free. After 10 years when his policy is paid-up, he’ll cease

withdrawals. If the IRA has earned say, 8% interest (a 6.5% net gain) consistently, the

account will actually increase from $500,000 to about $770,000.

Example Three

At 55, John’s $300,000 personal residence (the basis is $50,000) is debt-free; and he wants to

upgrade to a $500,000 model. A $400,000 mortgage is available at a 5% interest rate

amortized over 30 years, and the mortgage payment is $25,767 annually (or about $2,147 paid

monthly). He has a $600,000 IRA. Use this strategy:

Step one: Calculate John’s IRS unisex single life expectancy which is 29.6 years.

Applying a 1.5% interest rate over 29 years, a “substantially equal” amortized payment

is $25,667 annually (and this nearly covers his mortgage payment). This distribution is

penalty tax-free.

Step two: John sells his present home tax-free because the gain of $250,000 ($300,000

less $50,000) isn’t taxable.

Page 13 of 239

Step three: John obtains the $400,000 home loan and will repay a total of $773,024,

including interest of $373,024 - $12,434 annually on average over 30 years. The tax-

deductible interest offsets about 48% of the yearly IRA taxable distributions of $25,667.

Step four: John reinvests (outside his IRA) $300,000 in sales proceeds from his home;

here are possibilities that make some “tax sense:”

Acquire a life insurance policy because of its tax-free inside buildup

Purchase a non-qualified, tax-deferred annuity where there are no RMDs at

70½. And, a surviving spouse beneficiary can also continue the contract (and its

tax deferral) until death or its maturity date

Buy growth oriented securities or real estate that has a basis step-up at death

Use a combination of each option

The result: John has “removed” much of his taxable IRA and sheltered almost half of the

taxable distributions. And, there is no 10% penalty tax. He’ll have $300,000 in tax-free funds

invested outside the IRA, and there won’t be any out-of-pocket mortgage payment. Finally, if

the $600,000 IRA can earn more than 1.5% interest, it will continue building on a tax-sheltered

basis.

Summary

Some words of caution: When recommending a series of payments to avoid the 10% penalty

on premature distributions, you don’t want to assume responsibility for how “reasonable” the

interest rate; ask your client’s tax adviser to make this determination. In summary, use your

imagination! There are many creative strategies to obtain IRA funds pre-59½. The penalty tax

is avoidable; this money can solve a number of financial problems and bring happy smiles to

many IRA client-owners.

Planning Period, 59½ to 70½

Income Tax Considerations

After age 59½, there are no more 10% penalty taxes to pay on premature IRA distributions.

(And, once a five-year “substantially equal payment period” expires and the owner is 59½, a

previous IRA distribution plan can be modified or cancelled without a tax penalty.)

Page 14 of 239

On the way to 70½, it’s time to plan ahead. Here’s why: Let’s say at 60, Mary has a $1 million

IRA to which she has contributed merely $100,000. The good news: By the time she is 70½,

this should double to about $2 million. The bad news: A maturing, traditional IRA is simply a

pile of taxable income that will be worth much less after income taxes and any transfer taxes at

her death. Mary needs a pre-70½ planning strategy to eventually gain maximum tax and

financial benefits under the law.

The federal estate tax was is part of the permanent tax code since implementation of the

American Taxpayer Relief Act (ATRA) of 2012 (passed in January 2013). ATRA makes the

estate tax permanent and is automatically indexed for inflation. The amount exempt from tax

per person in 2016 is $5.45 million (remember, automatically indexed for inflation) and the top

tax rate on amounts over the exemption is 40%.

Well, Mary is 60 and she has been contributing to an IRA over several decades. Her account is

worth $1 million; and is projected to be worth $2 million in about 10 years. Should she continue

the account and take RMDs beginning at 70½, or is it better to cancel and pay the taxes now?

The answer depends on her objectives and personal philosophy; it also hinges on some

common sense. If you think about it, this IRA has been financed with tax deductions on Mary’s

contributions and has only saved her the amount of her 30% tax bracket (contributions

multiplied by .30). In retrospect, would Mary do it again (or would she purchase tax-deferred

annuities instead)? The real issue though is probably what to do now given her needs,

personal philosophy and circumstances. Here is an analysis of how two advisers might look at

her $1 million IRA in its present form.

The Case for IRA Liquidation

Some believe rates are moving higher and income taxes will continue indefinitely. We already

know the federal estate tax is permanent and automatically indexed for inflation. Since a

traditional IRA doesn’t have a basis step-up at death, they also discount its value as an

inheritance fund. Therefore — Assuming Mary’s Gross Estate is $7 million, including $2 million

in an IRA, it could cost $620,000 in estate taxes and $552,000 in income taxes to pass the

account to the family. Here’s how these taxes are calculated:

Page 15 of 239

The Tax Calculation

$7,000,000 Gross Estate

- $5,450,000 Federal Estate Tax Deduction

= $1,550,000 Taxable Estate

+ $620,000 Estate Taxes at 40%

+ $552,000 Income Taxes on $1.38 million

IRA at 40%

= 1,172,000 Total Estate and Income Tax

The decedent’s estate will pay the estate taxes. The beneficiary (heir) will pay income tax on

the distributions from the IRA. Luckily, the beneficiary will receive an IRC section 691(c)

deduction for estate taxes paid which are allocable to the IRA. In our example, since all the

estate tax is attributable to the IRA, the beneficiary should pay no income tax on roughly the

first $620,000 of distributions. The remaining 1,380,000 would be taxable.

The Case for IRA Liquidation if the Client’s Goal is Inheritance Planning

A suggestion: It may be best to liquidate the $1 million IRA now and simply pay an income tax

of $400,000 on $1 million. Then, use the remaining $600,000 to purchase a one-pay life

insurance policy for say, $2 million, assuming reasonable mortality and interest projections.

The result: Since the insurance death benefit is income tax-free, a $2 million face amount is

worth more than $2 million in an IRA, before income taxes and the policy’s full value is

available immediately whenever death occurs. Therefore, if inheritance planning is the goal,

liquidating the IRA to buy replacement life insurance is worth considering. As with all

recommendations, the client must be made aware of the costs, fees and downsides of this

approach.

IRA Continuation

If an IRA is liquidated gradually (potentially in a lower tax bracket) – over, say, a 10-year period

– this may result in a gradually lowering tax bracket and reduce income taxes on distributions.

Of course, an insurance policy could be funded gradually over the liquidation period as well.

When (a) cash premiums are gifted to family to fund the policy; and (b) they own the contract,

presumably the death proceeds will be estate tax-free. Alternatively, the death proceeds from a

life insurance policy inside an irrevocable life insurance trust (ILIT) will be estate tax-free.

Page 16 of 239

The Case for IRA continuation

The second adviser, believes what counts now is tax deferral into the future. Why pay taxes to

liquidate an IRA currently if you don’t have to? (Actually, the same reasoning applies when

paying taxes to convert a traditional IRA to a Roth.) This adviser always focuses on building as

much as possible in tax-deferred investments such as IRAs. When emergencies come up,

theory says spend “outside” funds instead. It may even be best to borrow when extra cash is

needed for personal use. IRAs become the cornerstone to income at retirement and beyond. In

short, IRAs may never be taxed, and protected from creditors. They should be cherished for

generations to come. The name of the game is defer, defer and defer - and protect, shelter and

safeguard. A suggestion: There is a middle ground. An IRA owner can balance the

possibilities; she can take out a portion of her IRA accumulation and acquire life insurance for

inheritance planning purposes. At age 70½, she’ll take what’s necessary for personal use. If

the IRA runs-out, she can withdraw or borrow tax-free funds from the life insurance policy.

Summary

In summary, clients 59½ - 70½ have a 1-to-11-year window to make imaginative, long-range

decisions for themselves and families. They basically have two choices: (1) Liquidate their IRA

and reinvest in life insurance, annuities, or buy-and-hold securities, or (2) build-up the account;

then at 70½ take RMDs (or greater amounts, if necessary) and continue tax deferral as long as

possible. It might be beneficial to hold seminars that appeal to 59½ - 70½, preretirement

prospects that need a distribution plans of action.

The Retirement Period, 70½ Until Death

IRA Distribution Plan

Eventually, some traditional IRA owners don’t cash-out, attain 70½ and begin taking RMDs

under the rules. Let’s look at Harry and Mary Jensen. Here are their facts and circumstances:

Harry and Mary are a married couple, ages 70 and 67. Actually, he turned 70½ in January of

2015; their actual ages on December 31, 2016, will be 71 and 68. His traditional IRA account is

worth $1 million as of their December 31, 2014, year-end statement. The Jensens ask you to

design an effective IRA payout strategy. You accept the assignment.

Page 17 of 239

Some additional facts: Presently, the Jensens live comfortably on Social Security and a

$50,000 income from non-IRA investments. Their taxable income is also $50,000, and they

have good health insurance, credit and access to funds in an emergency. They really don’t

need an IRA income but are aware of the need to take distributions in the near future.

Eventually, they’ll pass what’s left to family. For now, they want to strengthen their

circumstances.

An IRA Distributions Plan of Action For Mr. & Mrs. Harry Jensen

Harry has $1 million in his traditional IRA. At 70½, he must take at least minimum distributions

from the account. If not, he’ll owe (1) regular income taxes, and (2) a 50% penalty tax on what

he doesn’t take. From Harry’s $1 million IRA, let’s say the RMD is (the statement balance as of

December 31, 2014 divided by life expectancy) $36,496. Unfortunately, he takes only $16,000.

Later, when his income tax return is audited, the missing amount is discovered. He’ll be

assessed a $10,248 (50%) penalty on the shortfall. The reason: Congress insists that account

owners start paying taxes on the tax-deferred buildup accumulated over the years when the

account owner reaches 70½. Since the government means business, it’s essential to have an

IRA distribution plan of action that conforms to your clients’ financial objectives.

Here are four payout possibilities to consider:

Strategy One: RMDs

At 70½, Harry must take at least a minimal amount from the IRA. Here is what you need to

know about the relevant regulations:

Harry may take the first IRA payment in the year (2016) following the year (2015) in

which he turned 70½ – but it must be received by April 1, 2016 – then, he must receive

a second distribution by year’s end on December 31, 2016, a third payment by

December 31, 2017, etc.

Or, he may take the first payment sometime in 2015; receive the second payment

anytime in 2016; the third payment in 2017, etc.

Each payment must be at least a set percentage of the value as of December 31st of

the previous year, the year for which the payment is made. Here’s how this works using

the IRS Life Expectancy Tables:

Page 18 of 239

The first minimum payment (in 2015 or by April 1, 2016) is calculated by

dividing the IRA value indicated on the December 31, 2014 statement by

Harry’s life expectancy for a 71-year old of 26.5 years ($37,735);

The second minimum payment uses the new IRA balance (as of December

31, 2015) divided by the adjusted life expectancy of 25.6 years; and

The third minimum payment uses the prior year’s December 31st balance

divided by the adjusted life expectancy of 24.7 years, etc.

Strategy One Summary

An RMD strategy is helpful when the client wants:

Less IRA money now;

To reduce income taxes now;

To have an increasing income that may keep pace with a rising cost of

living standard;

To pass a significant account at death to family or charity; or believes

income taxes in the future will be lowered or eliminated.

It may be unwise if the client:

Needs more cash-flow now;

Will be in a higher tax bracket later;

Believes income and estate taxes in the future will be higher;

Has other funds that will be sufficient for family and charity; or

Is unable to manage the IRS minimum payments.

Strategy Two: Level Distributions

Instead of taking Required Minimum Distributions, let’s say Harry needs more IRA income

now – perhaps a steady, predictable amount. Consider this approach: Determine a reasonable

payout period. For instance, you might use Harry’s IRS life expectancy at age 71 of 26.5 years;

or age 70 of 27.4 years.

Next, assume an average rate of return on investments you believe can be achieved easily.

Finally, calculate a level amount, which will bring the $1 million IRA’s value to zero by either

Harry’s life expectancy or his and his wife’s combined life expectancies.

Page 19 of 239

Advantages

Here are some advantages to this level distributions payout approach:

Presuming Harry is comfortable with (and achieves) the assumed rate of return, level

distributions give him a long, steady, significant payment from the IRA (and a much

higher amount in the early years) than an RMD strategy with smaller payments at the

beginning.

If Harry makes conservative withdrawals initially, and actually achieves a rate of return

higher than the assumed rate, this will extend the payout period. For instance, a 5%

assumed payout rate over 16 years pays $91,000 annually. If the account actually earns

8%, that would increase the payout period to about 20 years. (A lower rate of return

would shorten the payout period, so the client should be shown a variety of scenarios in

order to make an informed decision.)

Observations

Under these scenarios, Harry could end up paying taxes on two distributions made in

2016; or he can elect to pay taxes on one distribution in 2015 and one in 2016.

Although there are required minimum disbursements set by the IRS, one can always

take more. But, if one takes less, the 50% penalty tax is assessed on the shortfall.

If Harry withdraws only the required minimum, which turns out to be about 3.5% in each

of the first few years, and his account earns a higher percentage rate of return (say, 8%

annually), his account grows in value. But, if his account earns less (say, 2.5%), it will

decline in value.

Disadvantages

However, there are some disadvantages to a level distributions strategy where more is taken

from an IRA than the required minimum under the law, and this must be explained to the client:

You may pay more taxes because you’ve taken more income in the early years.

You reduce the advantages of tax-deferred buildup on the remaining balance.

You may run out of money early, if the assumed rate of return isn’t achieved.

There is a reduced inheritance kitty for your family (unless you replace it outside the

IRA).

Page 20 of 239

If you choose a 16 year period over merely Harry’s life expectancy, there may be

nothing left in the IRA for Mary at his death.

Eventually, there may be a shortfall (subject to a 50% penalty tax), if RMDs exceed the

level payment. The withdrawal plan should be monitored closely to prevent this result.

You must keep some extra liquidity in the IRA for higher distributions in the early years.

Strategy Three: Guaranteed Level Distributions from a Commercial Annuity

In strategy two, we looked at distribution approaches that involved minimum distributions

based on the IRS RMD Life Expectancy Table:

Since there are no guarantees whether an IRA will lose money or earn less than the assumed

rate of return, you must also manage the investments and cash flow in and from the account.

A solution: Insurance companies assume the management function and guarantee payments

from fixed annuity policies. Let’s say a 15-year guaranteed fixed annuity pays $89,000, with

payments beginning one year after purchase. If this policy is purchased March 1, 2016, the

cash will be liquidated and the annual payments will cease on March 1, 2032.

Page 21 of 239

Advantages

There are no financial or investment worries; the annuity check arrives on time, every

time, and it follows the client anywhere in the world.

As long as a commercial annuity satisfies IRS regulations, there is no possibility of a

50% penalty tax under the RMD rules.

By including a lifetime feature to a fixed period of annuity payments, you guarantee

clients an income that can’t be outlived. This is only available contractually in annuity

policies offered by insurance companies licensed and regulated in the 50 states.

Strategy Four: Variable Distributions from a Commercial Annuity

In strategy three, we reviewed fixed annuity options. If a client is willing to accept more risk and

seek stock market-like rates of return, a variable payout annuity provides distributions that

fluctuate with its underlying investments.

Example: At age 71, assume that a 15-year, $1 million, fixed annuity will pay $89,000

annually. A variable annuity might offer a reduced payment of say, $80,000 the first year and

subsequent amounts that vary depending on how a select portfolio of securities fluctuates in

value. The result: You have a potential upside. Of course, there is unlimited downside as well,

unless limited by provisions within the annuity contract. Always review the policy and

prospectus carefully and insist your clients do the same. Payments always continue for life, a

term certain, or life and a term certain guaranteed in the annuity contract.

Strategy Five: Combination of Strategies

If clients own more than one IRA, an RMD is necessary from each account. However, the full

amount may be taken from any one or more of the IRAs. Consider this illustration, an

imaginative strategy for managing a $1 million IRA:

Example: For your client, age 71½, divide $1 million equally and place into three separate

IRAs, which might be structured as follows:

IRA #1 ($333,000) is invested in aggressive securities projected to earn say, 12%

annually. Observation: $333,000 x 12% equals $40,000, an amount sufficient to at least

pay the first year’s RMD (on all the accounts) of $37,735.

Page 22 of 239

IRA #2 ($333,000) is invested in somewhat more value-oriented securities. If cash flow

from IRA #1 cannot support the RMDs (based on all three IRAs), the client can use IRA

#2 to make up the shortfall.

IRA #3 ($334,000) is invested in a fixed annuity that earns a guaranteed 5% interest for

five years. Plan to allow this policy to accumulate for 13½ years or so when it may

double in value to about $650,000. Then, take a life and term-certain annuity payout

determined for someone age 84.

Using Two-Directional Savings Strategies

RMDs from an IRA Account

Many IRA owners think of these accounts as cushions at 70½. In some instances, an IRA will

be the primary source of retirement income. In others, the account owner will reluctantly take

RMDs into her taxable income. Let’s assume your client, Mark Thompson, has worked hard to

build his $1 million IRA’s tax-free accumulation over the years. He has attained 70½, and it’s

time to take RMDs (starting at about $37,735 annually). Since Mark already has a comfortable

$50,000 income from bonds and CDs (also worth about $1 million), he views the IRA

payments as a nuisance that increases his taxes “unnecessarily.” He should consider this

planning idea: When Mark’s taxable IRA distributions begin, he cashes-in the non-IRA

investments and acquires a tax-deferred accumulation annuity. (Alternatively, Mark could

convert these funds into a single-premium life insurance policy, a growth-oriented stock

portfolio, investment real estate, or a combination of these approaches.) In other words, Mark

(a) eliminates taxes on income formerly taxable just as (b) new IRA withdrawals are taken into

his taxable income.

The bottom line: RMDs from an IRA account at 70½ shouldn’t be a problem; they should be an

opportunity to shift non-IRA cash into a cottage in the mountains, some needed life insurance

or a more creative, tax-favored savings portfolio. As the IRA is liquidated, the non-IRA monies

are accumulated or gifted to family. In summary, an account owner and the adviser should use

Mark’s account creatively, throughout his lifetime. There will be emergencies pre-59½, a

planning period 59½ - 70½, and an RMD period after 70½.

Page 23 of 239

Who Should be an IRA Beneficiary?

Questions the IRA Owner Should Consider

Assume a client’s first IRA starts innocently enough with a few hundred dollars. There is a

second IRA and also, a rollover from a 401(k) plan years later. The IRA accounts get larger

and larger. Along the way, family members marry, have children, and divorce. They may have

children from other relationships or unmarried partners. Some have money worries, others are

financially secure, and a few will die before the IRA owner. Are the beneficiary designations

up-to-date? Does your client have copies of each form (or, is paperwork misplaced or lost)?

Ask for this information. Then, prepare probing questions about beneficiaries, heirs and loved

ones. Here are a few eye openers:

Can the beneficiaries manage large sums of money?

Can each of them make financial decisions easily?

Will they understand tax consequences of cashing in, or continuing the account with

RMDs under the law?

Is there a shaky marriage where the money can be lost in divorce?

Is someone in financial trouble where there may be pressure to cash-in the account?

Are they professionals or successful persons who may be targets for litigation?

Could a gifted or impaired loved one be a ward of the state someday and could IRA

money be attached to pay for his care?

Do you want beneficiaries to share the account, or should it be divided into separate

portions? By you? Or, by them?

If the primary beneficiary dies after she receives the IRA, are you concerned about

who succeeds to the money?

Will you name a beneficiary to what’s left at the primary beneficiary’s death? Or, will

your designee?

If a primary beneficiary predeceases you, could the contingent beneficiary be a

minor?

If the beneficiary is a minor, could a guardian of the account be an estranged parent

or in-law?

When a child or grandchild dies, should a spouse receive something or should the

heir’s share pass to his or her children?

Page 24 of 239

The Bottom Line: It’s really not enough to name a beneficiary and let the “chips fall where they

may.” Have a serious discussion about beneficiaries with IRA clients; this is an opportunity to

bond with them in a meaningful way.

Examples

Here are a few beneficiary designations that can cause trouble.

The beneficiary is “my spouse, Mary.” But, Mary is no longer married to Harry. Since

beneficiary designations aren’t revoked automatically when a marriage is dissolved,

Mary will legally receive the account at Harry’s death.

If Mary is still Harry’s spouse at his death and receives the IRA outright, would it

disturb Harry if she later remarries and names her new spouse as beneficiary at her

death? If so, perhaps the IRA should be left in trust where children and grandchildren

take what’s left eventually.

When IRAs are payable to parents, children, brothers and sisters, and other relatives,

there may be transfer taxes as each dies and bequeaths what’s left of the account. A

well-crafted, multi-generational trust can provide for everyone without ever changing

ownership of the account. The funds will pass intact and estate tax-free if trust

beneficiaries change over time.

If the beneficiary is “lawful surviving children in equal shares,” the portion belonging

to a child who predeceases an IRA owner simply passes to the other children. That

child’s offspring receives nothing. Is this what your client really wants?

The designation, “lawful surviving issue, per stirpes,” leaves a deceased child’s share

to his or her children. Are they minors? If so, there’s always a possibility an estranged

parent or in-law may control the account as guardian. The solution: A trust-payee for

potentially younger beneficiaries.

Whenever children or issue are the named beneficiaries, and they predecease a

benefactor, their spouses receive nothing from the account. Ask if these widows or

widowers should be entitled to at least an income for a period of time. Some creative

trust planning solves the problem. Beneficiary planning is a legacy for loved ones and

should be taken seriously.

Page 25 of 239

Although outright designations (where IRA accounts pass directly to someone) may seem the

best tax planning method, trusts are often the answer, especially when an owner is concerned

about control over distributions. A properly licensed attorney should handle the legal advice

given to clients.

Who Can Be an IRA Beneficiary?

What the IRA plan document says, i.e., it could actually state that all beneficiaries must

be, “your spouse, if any, and if none — your lawful surviving issue, per stirpes.” If this

plan sponsor won’t accept an alternate beneficiary designation, the account owner

should establish another IRA that permits more flexible beneficiary arrangements.

As provided on a plan beneficiary form completed by the account owner, i.e., the

account owner freely names any individual, estate, charity, trust or other entity

beneficiary of the IRA. Most IRA sponsors provide or require these forms, as well as

“Change of Beneficiary” forms (often available on the sponsor’s website). Treat this

opportunity with care. In some cases, you or your client may be best served to have a

lawyer draft the Appointment of Beneficiary language to reflect family objectives.

Some words of caution: Read the plan document. It may not permit spouses to rollover the

account to their own IRA. Or when the beneficiary is a group of individuals, e.g., children, the

plan might not allow a division into separate shares. The recourse: Select another IRA.

There is No "Designated" Beneficiary

Tax Concept of a Designated Beneficiary

Once IRA owners are clear about whom the beneficiary will be, and what is permitted by the

plan document, make them aware of the tax concept of a designated beneficiary.

By definition, designated beneficiaries are individuals

and certain trusts defined in the law. Estates,

charitable organizations and all other trusts are not

designated beneficiaries.

Page 26 of 239

Here’s why: If an IRA owner wants the possibility of maximum extended tax deferral over long

periods after her death, he or she must select an appropriate designated beneficiary. If no

beneficiary is designated, the IRA may pass according to state law.

In the following situations, assume there is no designated beneficiary: An account owner dies

before April 1st of the year following the year in which he attains 70½. Let’s assume Harry was

70½ in 2015 (and actual age 71); he will take a first IRA distribution just prior to April 1, 2016.

His account balance on December 31, 2014, is $1 million, and his first payment for 2015 will

be $36,496 ($1 million divided by a 27.4 year life expectancy). Thereafter, the plan is to take

only the minimum payments over the next few years. These amounts will be determined by

dividing the prior December 31st account balance by life expectancy based on Harry’s age.

Unfortunately, Harry dies on February 1, 2016, at age 71, and there is no designated

beneficiary. (Perhaps his IRA beneficiary form is silent or it names “Harry’s estate” recipient of

the account.) The consequence: Since Harry’s death occurs before April 1st (the April 1st

following the year in which he attained 70½), his account must be liquidated by December 31,

2021; in other words, there is no tax deferral past this five-year window after Harry’s death.

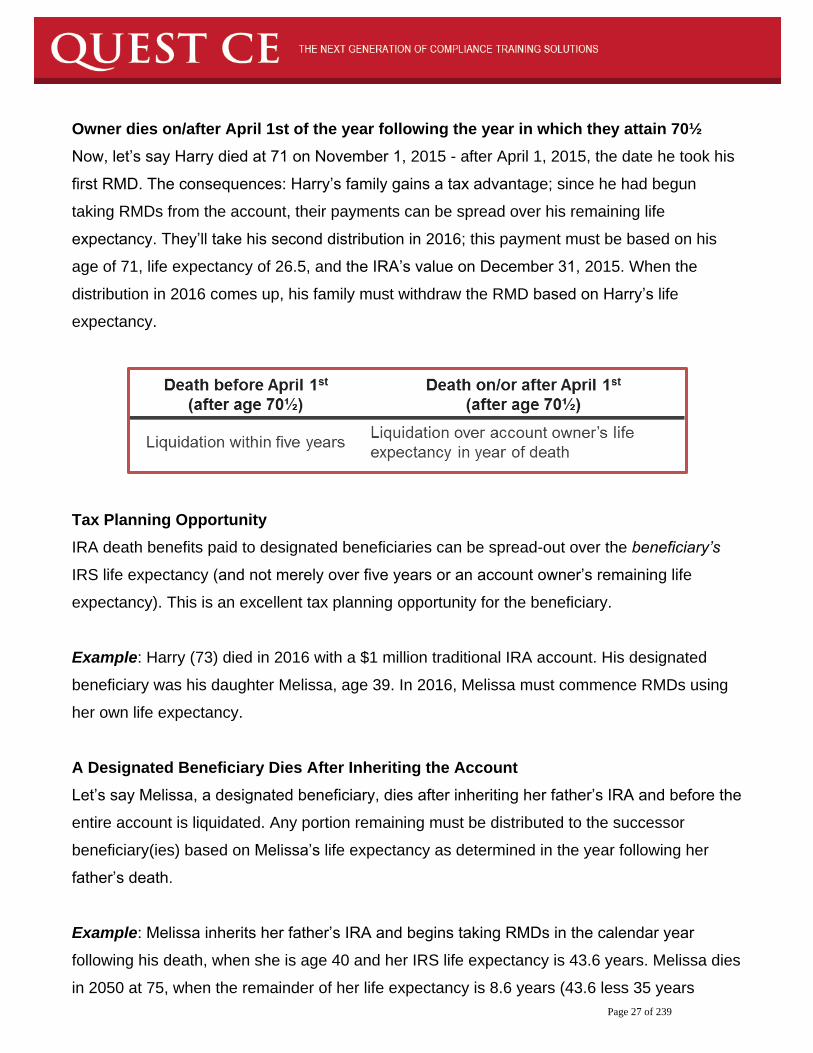

Page 27 of 239

Owner dies on/after April 1st of the year following the year in which they attain 70½

Now, let’s say Harry died at 71 on November 1, 2015 - after April 1, 2015, the date he took his

first RMD. The consequences: Harry’s family gains a tax advantage; since he had begun

taking RMDs from the account, their payments can be spread over his remaining life

expectancy. They’ll take his second distribution in 2016; this payment must be based on his

age of 71, life expectancy of 26.5, and the IRA’s value on December 31, 2015. When the

distribution in 2016 comes up, his family must withdraw the RMD based on Harry’s life

expectancy.

Tax Planning Opportunity

IRA death benefits paid to designated beneficiaries can be spread-out over the beneficiary’s

IRS life expectancy (and not merely over five years or an account owner’s remaining life

expectancy). This is an excellent tax planning opportunity for the beneficiary.

Example: Harry (73) died in 2016 with a $1 million traditional IRA account. His designated

beneficiary was his daughter Melissa, age 39. In 2016, Melissa must commence RMDs using

her own life expectancy.

A Designated Beneficiary Dies After Inheriting the Account

Let’s say Melissa, a designated beneficiary, dies after inheriting her father’s IRA and before the

entire account is liquidated. Any portion remaining must be distributed to the successor

beneficiary(ies) based on Melissa’s life expectancy as determined in the year following her

father’s death.

Example: Melissa inherits her father’s IRA and begins taking RMDs in the calendar year

following his death, when she is age 40 and her IRS life expectancy is 43.6 years. Melissa dies

in 2050 at 75, when the remainder of her life expectancy is 8.6 years (43.6 less 35 years

Page 28 of 239

elapsed). Melissa’s son, Tom, the successor beneficiary, can then begin taking distributions

using Melissa’s adjusted life expectancy.

A Group of Individuals Sharing the Account

Beneficiaries Establishing Separate Shares

Let’s say Harry, an account owner, names a group of designated beneficiaries such as:

“My lawful surviving children;”

“My lawful surviving children, in joint tenancy with right of survivorship;”

“My lawful surviving children, in tenants-in-common;” or

“My lawful surviving issue, per stirpes.”

When the account owner has not actually established separate shares during life, the group

creates separate shares by December 31st of the year following the year of Harry’s death.

Then each beneficiary can use their individual life expectancies for their own accounts.

However, if the group remains intact, the shortest life expectancy (that of the oldest beneficiary

in the group) is used for the entire IRA. When an account owner has more than one

beneficiary, it’s natural to think in terms of trusts, perhaps one for each child family unit.

Example

Harry has a $1 million IRA and his beneficiary list includes children Melissa and Melinda who

have one child each. He wants to treat each family unit equally and secure protection and

professional management for them. Here’s the recommendation: Harry divides the IRA equally

into two accounts A and B. One is payable to Trust A for Melissa and children; the other is

payable to Trust B for Melinda and children. Distributions to each trust are based on the life

expectancies of its oldest beneficiaries, Melissa and Melinda. At their deaths, RMDs are paid

to the trusts for the balance of their life expectancies as calculated in the year following Harry’s

death.

Note: This example shows how an IRA can be stretched-out over the life expectancy of

someone whose share is held in trust. In the sections that follow, we will look at stretch or

multigenerational IRAs, a strategy for maximum tax deferral possibly over several generations-

to-come and other planning strategies available by state law.

Page 29 of 239

To summarize, all IRA owners (and their beneficiaries), can be viewed as joint venturers

regarding a significant IRA. This is a great time to be a major contributor: Work with clients to

obtain and update current beneficiary designations. Then, test everything to determine what

happens if a first or second beneficiary inherits the account.

IRA Owner Leaves Account Directly to a Spouse

Primary Designated Beneficiary

In most families, the primary designated beneficiary is the IRA owner’s spouse. The law favors

this and gives the greatest tax advantages when a spouse assumes full control of the account

– a rollover IRA. In this chapter we will explore various approaches for leaving IRAs to

surviving spouses.

The list of possibilities includes:

Inherited IRAs

Rollover IRAs

Annuities and trusts

Each of these possibilities can benefit the surviving marital partner. Spouses who inherit and

maintain traditional IRAs have choices that hinge on the date the first spouse dies.

For instance, Harry asks about what happens when his wife, Mary, receives his $1 million IRA.

You tell him Mary’s first option is to keep the account intact (a so-called “inherited IRA”). If she

does, everything depends on Harry date of death:

He dies before 70½. Let’s say the owner dies on February 1, 2016; He was 65, and

his wife was 60. Since his wife is Harry’s sole beneficiary, Mary can defer taking any

money from the account until 2021, the year he would have attained 70½ had he

lived, keeping the account titled in Harry’s name. She must receive the first payment

by December 31st of that year. An added bonus: As sole spouse beneficiary of an

inherited IRA, Mary can re-determine her life expectancy in each succeeding year,

and reduce her RMD.

Page 30 of 239

Harry attains age 70½ but dies before April 1st of the following year. Assume he

attained age 70½ on November 1, 2016, and died on December 1, 2016 (before April

1st of the following year). His spouse, as sole beneficiary, may defer her first

distribution until December 31, 2017, the year following her husband’s death. The

reason: Technically, a spouse beneficiary must commence RMDs by the later of (a)

December 31st of the calendar year in which her spouse would have been 70½, or

(b) December 31st of the year following his death. In this instance, December 31,

2017 is her required beginning date. Again, her Single Life Table expectancy (based

on her attained age in 2017 and re-determined in each succeeding year), is the basis

for computing her RMDs.

Harry dies on or after April 1st following the year he attains 70½. Assume Harry died

in 2017 at age 75, after commencing RMDs from his IRA. Any unpaid amounts for

2016 must still be distributed. Then, his spouse’s first distribution would be due by

December 31, in the year following his death. Mary’s life expectancy in that year (re-

determined in each succeeding year) is the basis for her RMDs.

A spouse dies after the IRA owner. Assume the Mary, the surviving wife, takes some

withdrawals from her late husband’s IRA, and then Mary dies. Harry’s remaining

account balance will be distributed according to the plan document. Normally, the

next beneficiary will be whomever the account owner specifies on his beneficiary

form. (However, the plan could permit the surviving spouse to name a successor.) If

no one is mentioned, the plan will probably specify the new beneficiary, e.g., the

owner’s issue, per stirpes (or his estate).

The next beneficiary (successor beneficiary) takes RMDs over the widow’s IRS unisex single

life expectancy, based on the age she had attained or would have attained in the year of her

death. (In other words, a successor divides 1 by this life expectancy to obtain an applicable

percentage; then, she multiplies the account’s value on December 31st of the year of her

death by this percentage.) There is no recalculation, and her life expectancy is reduced by one

in each succeeding year.

Page 31 of 239

Example

After the account owner’s death, his widow inherits his IRA, but she dies a few years later at

77 when her IRS life expectancy of 12.1 years is frozen because of her death. After any

amounts due to her are paid, the distributions thereafter will be based on this 12.1 expectancy

less one year each year.

Note: When a spouse dies, a subsequent beneficiary calculates the decedent’s life expectancy

determined by her year of death, and takes distributions over that period of time. When a non-

spouse beneficiary dies, a successor continues with the non-spouse’s life expectancy

determined in the year following the original account owner’s death.

Spouse Rolls it Over to Her Own IRA Spouse Assumes Control

Earlier, we described situations where Mary assumes control of Harry’s IRA – an inherited IRA.

There are several reasons why she may do this. For instance:

She wants to follow Harry’s wishes. Let’s say he names children from a former

marriage, as successor beneficiaries after Mary dies. She decides voluntarily (or

perhaps by a written agreement) to keep the account and not to change his designation.

She is under 59½, and any distributions are exempt from the 10% early distributions tax

penalty; if she rolls over the account, what she receives pre-59½ can be subject to this

penalty.

She is older than Harry, and need not commence RMDs until he would have been 70½;

if the account is rolled over (when she is over 70½), she is immediately subject to the

RMD rules. In most cases, however, she will roll over his account to her own IRA. This

is accomplished by simply retitling the account in her name.

Here is the Rationale

Let’s say Harry is older than Mary, and he dies at 65 when Mary is 60. If she rolls over

his account to her own IRA, she can defer distributions until April 1st following the year

she attains 70½ - approximately 10 or 11 years from now. If she simply maintains

Harry’s account as an inherited IRA, she must commence RMDs by the end of the year

he would have attained 70½ - about five years from now.

Page 32 of 239

After the rollover, when taking RMDs she uses the Uniform Lifetime Table each year

based on (a) her actual age, and (b) the age of someone hypothetically 10 years

younger. If she keeps Harry’s IRA, she uses her actual life expectancy, but it is re-

determined each year.

Example: Harry (65) dies, and Mary (60) decides to maintain Harry’s IRA. Mary is permitted to

defer distributions until the end of the calendar year Harry would have attained 70½, when she

is 65.

Mary’s first payment is based on Harry’s life expectancy and the statement’s balance on

December 31st of the year before Harry died. If instead, she rolls over the account to her own

IRA, she can defer taking payments until April 1st of the year following her age 70½. Her first

payment would be based on the larger balance on the December 31st statement the year

before Mary’s first RMD and her life expectancy. The decision is critical in Mary’s long-term

estate planning.

When Mary rolls over Harry’s account and designates a new primary (and contingent or

successor) beneficiary, e.g., a young child or grandchild, the family gains an additional

tax deferral opportunity. The reason: After Mary’s death, the youngster’s life expectancy

in the following year is the basis for RMD calculations. When this beneficiary dies, a

successor uses any remaining years to calculate ongoing RMDs.

Example: Mary rolls over Harry’s IRA account and names Tommy, her 9-year-old

grandson (or his custodian or trust), primary beneficiary at her death. (Of course, she

can always leave the account in separate shares to several beneficiaries or to a group

of them.) When Mary dies a year later, Tommy’s life expectancy in the year following

her death (71.8 years for the now 11-year old) determines RMDs in succeeding years,

even after his death.

Observations: When Mary dies, Tommy’s life expectancy of 71.8 years will result in a

low RMD and a long distribution period. If Mary had simply kept Harry’s account active,

her remaining life expectancy based on her age in the calendar year of her death -

reduced by one in each year thereafter – would be used to calculate RMDs for Tommy.

Page 33 of 239

Perhaps Harry has named a subsequent beneficiary for his account, to occur after Mary

dies (but Mary doesn’t agree with his selection and she can’t change the designation). If

she rolls over to her own IRA, the account is totally under her control and she can name

new primary and contingent beneficiaries.

Mary may prefer a completely different IRA, or she has personal reasons for rolling over

the account.

The rollover of several accounts may simplify overall investment and administration by

combining everything into one IRA. As long as it is allowed under the IRA plan

document, there is no time limit on the rollover. A surviving spouse’s rollover after her

mate dies is permitted even if (a) he was already receiving RMDs, or (b) she has

attained the date for taking them. If the deceased former account owner dies after April

1st following the year he attained 70½, she (a) waits until the year following death, (b)

rolls over the account, and (c) takes any RMD in the rollover year. If she is under 70½,

she can always defer distributions from the rollover account until April 1st after her age

70½.

In summary, a surviving IRA spouse beneficiary has options: She may take at least RMDs

based on her recalculated life expectancy (or the plan may allow her to forego distributions

under the five year rule). Or, she may (a) roll over the account, (b) withdraw amounts at her

age 70½ under the Uniform Lifetime Table, and (c) designate new beneficiaries who can use

their life expectancies for RMDs after her death.

Owner Leaves Account “for the benefit” of Surviving Spouse

Surviving Spouse Options

Earlier we discussed a surviving spouse’s options when she receives an IRA directly, by

beneficiary designation. We looked at the inherited IRA concept where Mary merely takes

distributions from Harry’s account. We also discussed when she rolls over his IRA and treats

the new account as her own. However, there are circumstances where an IRA owner may

prefer not to leave an account outright to a spouse. For instance, she needs help with

investments or managing money. Asset and creditor protection is an issue. Or, he doesn’t want

what’s left to pass to her “next” mate eventually. Finally, this may be a second or third

marriage, and he wants the remainder of the account for children from a prior union. When

Page 34 of 239

someone indicates reluctance to give full control of the account to a surviving spouse, the

following are alternatives to an outright beneficiary designation.

A survivor’s annuity - At Harry’s death, he wants Mary to have maximum cash flow from

the account, without investment or management worries. He also wants a practical

solution that is easy to implement. Consider this idea: Harry’s IRA acquires a

commercial accumulation annuity contract that names Mary income beneficiary. He

selects a settlement option arrangement, which annuitizes the policy at his death. Any

payments remaining at her death are paid automatically to their daughter, Melissa.

A general power of appointment (GPA) marital deduction trust - Harry doesn’t want a

set annuity payout for Mary that pays any more than the gradually increasing RMDs

under the law. Or, he prefers a more flexible arrangement where Mary can choose how

their descendants will receive what’s left in the IRA eventually. Here’s the

recommendation: Harry’s lawyer drafts a trust solely for Mary that gives her a right to

name who receives what’s left from the trust at her death – a general power of

appointment (GPA) trust. The objective is to qualify the trust for a marital deduction for

estate tax purposes and to provide management help for Mary.

Let’s say Harry died at age 65 when Mary was 60; he left a $1 million IRA and a $1

million apartment house to her GPA trust. In the year following his death when she was

66, the IRA earns $100,000 in accounting income and the apartment house had a

$10,000 accounting loss. The question: What did the trustee owe Mary? The answer: It

depends. There are a couple options.

Possibilities

First, to obtain a marital deduction, she clearly is entitled to the trust’s net accounting

income of $90,000 ($100,000 from the IRA, less the apartment’s $10,000 loss).

Therefore, her trustee must presumably withdraw up to $90,000 from the IRA and pay it

to her – even though this exceeds any RMD in the law.

Actually, at age 66, Mary’s IRS unisex life expectancy is 20.2 years – accordingly, the

trustee’s minimum withdrawal for her from a $1 million IRA would be only $49,505 ($1

million ÷ 20.2.) And, the minimum withdrawal for her (and successor beneficiaries after

Page 35 of 239

her death), would be based on the elapsed years method by subtracting one year in

each succeeding year until her 20.2 life expectancy is “used up.”

Fortunately, Mary’s GPA trust probably won’t have to withdraw a full $90,000 from the

IRA. As long as she can compel her trustee to withdraw all of its accounting income and

make a distribution to her of that amount the trust should still qualify for the marital

deduction. And, if Mary’s trust gives her this right, her trustee can withdraw as little as

her minimum distribution ($49,505), and this would probably be the payment.

Some creative financial and legal planning can reduce Mary’s trust distribution even more. If

Mary’s trust document requires that she receive all IRA income actually paid to the trust (so

these amounts will never be accumulated in the trust for remaindermen), a so-called conduit

trust, she will be deemed the IRA’s sole beneficiary and treat the account as an inherited IRA.

The result: IRA distributions can be deferred until Harry would have attained 70½. Thereafter,

Mary’s IRS life expectancy can be re-determined annually until her death when it is frozen (and

reduced by one year, each year, thereafter). Although her trustee can always withdraw up to

the IRA’s full accounting income and pay this to Mary, this trust language can reduce her

required taxable distributions to zero for five or six years, and markedly thereafter. Mary’s GPA

trust might be drafted with even greater imagination.

Second, let’s say this trust gives Mary an unlimited and continuing right to withdraw all

assets of the trust, including the IRA. Consequently, it effectively gives her a general

power of appointment in favor of herself. Although this withdrawal right may be

inconsistent with the purpose of the trust (which is, say, to provide investment

management for Mary), the trustee should now be able to exercise an IRA rollover on

Mary’s behalf.

The result: After the rollover, no RMDs are necessary until Mary is 70½. At her death,

Mary’s beneficiary can use his or her own life expectancy to spread-out distributions

gradually over many years into the future.

The bottom line: Harry’s attorney must be thoroughly aware of the regulations when

drafting a GPA trust that is named beneficiary of an IRA. And, if the objective is to slow-

down taxable distributions for Mary and her successors, this trust can always enhance

Page 36 of 239

Mary’s authority over her trustee – even to the extent of giving her the ability to make a

rollover of the account.

QTIP Definition

Qualified terminable interest property (QTIP) is property in a decedent's estate that, even

though subject to certain restrictions, can still qualify for the estate tax marital deduction. The

term also includes property given to a spouse during life that qualifies for the gift tax marital

deduction, even though it is subject to similar restrictions.

Brief Review of the Marital Deduction

When people leave property to others at death -- or give property away during life that exceeds

or does not qualify for the annual gift tax exclusion -- that property is generally subject to

federal estate tax (death transfer) or a federal gift tax (lifetime transfer) if the total transfer

exceeds the applicable exclusion amount sheltered from federal estate tax by the applicable

credit amount. However, when property is left (or given) to a surviving spouse, the "unlimited

marital deduction," allows a spouse to transfer any amount of property between him or herself,

during life or at death, without triggering the federal estate tax or the federal gift tax.

Terminable Interests

Property left (or given) to the spouse cannot be a "terminable interest" if it is to qualify for the

marital deduction. So, what is a "terminable interest"? Basically, it is an interest in property that

can expire due to the passage of time, or that can terminate due to the occurrence of some

future event, or the failure of some event to occur.

Example One: Husband leaves wife a 10-year income interest in a trust. After ten