Embed Size (px)

Citation preview

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 1/84

Verein Deutscher Werkzeugmaschinenfabriken

Die deutsche Werkzeugmaschinen-

industrie im Jahr 2011The German Machine Tool Industry in 2011

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 2/84

3 Zukunftsfähigkeit der Hochtechnologieorientierung7 Aktuelle Situation und Perspektiven

17 Werkzeugmaschinen-Produktion29 Werkzeugmaschinen-Außenhandel

43 Stellung auf dem Weltmarkt59 Strukturdaten der Werkzeugmaschinenindustrie65 Statistischer Anhang, methodische Hinweise, VDW-Mitgliedsfirmen

3 Bright prospects for the future of high-tech orientation7 Current situation and perspectives

17 Machine tool production29 Foreign trade in machine tools43 Position on the world market59 Structural data of the machine tool industry65 Statistical appendix, methodical comments, VDW member companies

Titelseite: Beim Wälzschälen handelt es sich um ein innovatives Verfahren. Ein neu entwickeltes Werkzeugsystem erlaubt es, Wälzschälen auf Kegel radfräsmaschinen erfolgreichanzuwenden und garantiert eine produktive, prozesssichere und präzise Fertigungstechnologie insbesondere von Innenverzahnungen. Vorteile sind unter anderem eine bis zuzehnfach schnellere Bearbeitung im Vergleich zum Stoßen und hohe Bauteilqualität durch exakte Werkzeuge und dynamische Maschinen.

Front cover: Skiving is an innovative process. A newly developed tool system makes it possible to use skiving successfully on bevel gear cutting machines, and guaranteesproductive, stable and precise manufacturing technology, especially for internal gears. Benefits include up to ten-fold faster machining as compared with shaping along withhigh component quality through precise tools and dynamic machines.

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 3/84

1

Auftragsflut 2011 bis weit in 2012 wirksam, weltweiteIndustrie produktion und Investitionstätigkeit wenigerbeeinträchtigt, Hochtechnologieorientierung der Branchebleibt tragfähiges Modell

Nach 85 % Plus im Auftragseingang des Jahres 2010 legtdie auf deutsche Werkzeugmaschinen gerichtete Nach-frage um weitere 45% auf ein spektakuläres Volumen von16,7 Mrd. EUR zu! Das ehemals als kaum wiederholbaresRekordergebnis betrachtete Niveau 2007 wird souveränüberboten.

Primär ist es die Auslandsnachfrage, welche die erwähnteReferenz mit fast 2 Mrd. EUR Abstand distanziert und denentscheidenden Unterschied ausmacht. Zwar stehen die

Orders aus Europa für einen hohen zweistelligen Steiger-ungssatz, aber die Partizipation der über Jahrzehnte wich-tigsten Absatzregion am Gesamtwert der Auslandsbe-stellungen wird durch die Teilhabe Asiens sehr deutlichüberflügelt.

Folge ist Produktionsausweitung in 2011 um ein sattes Drittelgegenüber dem Referenzjahr auf über 13 Mrd. EUR. Trotz-dem bleibt es zu Jahresbeginn 2012 bei einer durchschnitt-lichen Reichweite der Auftragsbestände von 9 Monaten.Dieser Auftragsüberhang geht zurück auf stattliche Anteile

der durch lange Durchlaufzeiten geprägten kundenspezifi-schen Sondermaschinen sowie des Projektgeschäfts mitGroßanwendern am gesamten Auftragsvolumen 2011. Dieserwichtige Einfluss dürfte in Kombination mit anhaltendenFortschritten hinsichtlich der Eindämmung finanz- undrealwirtschaftlicher Risiken zu einem neuerlichen Produk-tionsplus deutscher Werkzeugmaschinenhersteller vonetwa 5 % führen. Vorhersagen für die weltweite Industrie-produktion und die international in den wichtigstenAbnehmer industrien unserer Branche getätigten Anlagein-vestitionen sind spürbar nach oben angepasst worden.Damit bewegt man sich deutlich über dem noch im Spät-herbst 2011 als Risikovariante durchgespielten Szenarium.

Im Halbjahresmuster des Auftragseingangs der deutschenWerkzeugmaschinenindustrie sind im laufenden Jahr über-proportionale Abstriche während der ersten 6 Monate undanschließend bereits in der 2. Jahreshälfte erfolgende Kon-solidierung vorgezeichnet. Hinsichtlich der Produktionsent-wicklung nehmen sich die Dinge umgekehrt aus: Hier giltnach einem weiteren starken 1. Halbjahr ein moderates

zweistelliges Minus als wahrscheinlich.

Flood of orders effective in 2011 and well into 2012, world -wide industrial production and investment activity lessimpaired, high-tech orientation of the sector remainsviable model

Following 85% growth in incoming orders in 2010, Germanmachine tools posted another 45% increase in demand,rising to a spectacular volume of EUR 16.7 billion! Consideredas a virtually unbreakable record result at the time, thelevel of 2007 was exceeded by a large margin.

Foreign demand, which outpaced the aforementioned ref-erence year by nearly EUR 2 billion, primarily made thedecisive difference. While orders from Europe – which hasbeen the most important consumption region for decades –

grew at a high two-digit rate, its participation as a share of the total value of foreign orders was very clearly outpacedby the Asian fraction.

As a consequence, production expanded by a full third rela-tive to the reference year to more than EUR 13 billion in2011. Nevertheless, the average range of order backlogs wasstill nine months at the start of 2012. That backlog arosefrom the ample shares of the total order volume in 2011which involved customer-specific special machines (char-acterised by long turnaround times) and project business

with major customers. This important factor, in combina-tion with continued progress in limiting finance risks andreal economy risks, should serve to increase German ma-chine tool manufacturers’ production by about another 5%.Predictions for worldwide industrial production have beenadjusted perceptibly upward together with plant and equip-ment investment activity in the major customer industriesof our sector. As a result, we are already well beyond thescenario which was still considered as the risk variant in thelate autumn of 2011.

The half-year pattern of incoming orders received by theGerman machine tool industry anticipates disproportion-ately high declines during the first six months of the current

year followed by consolidation activity in the second half.With regard to production trends, things will be the otherway round: Here a continued strong first half-year is likelyto be followed by a moderate two-digit decrease.

It is likely that emerging countries, and especially China,will become increasingly oriented towards higher qualityproducts which are potentially suitable for export. This will,

VorwortPreface

Programmstruktur und regionale Verteilungder Nachfrage sind Assets der Branche

Programme structure and regional distributionof demand are assets of the sector

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 4/84

in turn, raise the demands on manufacturing technology,thereby offering German manufacturers good opportunitiesto benefit disproportionately from the new procurementpractices.

This is also precisely the argumentation underlying a jointstudy by VDW and PricewaterhouseCoopers: While made-to-order special solutions and projects represent nearlyhalf of the production volume of the German machine toolindustry, its international competitors dedicate only about30% of their order volume to customisation of this type.

The current composition of German manufacturers’ port-folio of foreign orders will also have beneficial effects. Thisas a consequence of the weight of Asia – already a high 46%share and still growing – where significantly less reductionin machine tool consumption is also generally necessary,even during weaker periods.

The present publication aims to provide professional ana-lyses and consider industry trends of topical interest realis-tically within the expectations described and regardless of whether or not the reporting period offers attractive growthrates. The VDW considers its target audience to comprisemainly decision-makers from politics, the banking sector, at

trade union level, in the media landscape and in researchand teaching. The VDW’s regularly revised view of the worldmarket, which differs from ones based on other sources invarious respects, represents a traditional focal point of thisseries of brochures started in 1998.

Frankfurt am Main, April 2012German Machine Tool Builders’ AssociationEconomy and Statistics Division

Die in den Schwellenländern, hier insbesondere in China, zuerwartende Hinwendung zu höherwertigen, potenziellexportfähigen Erzeugnissen wird den Anspruch an Ferti-gungstechnologie nach oben verschieben und damit deut-

schen Herstellern gute Chancen bieten, vom verändertenBeschaffungsverhalten überproportional zu profitieren.

Bei exakt dieser Argumentation setzt auch eine gemeinsameStudie von VDW und PricewaterhouseCoopers an. Währendnämlich knapp die Hälfte des Produktionsvolumens derdeutschen Werkzeugmaschinenindustrie auf nachgefragteSonderlösungen und Projekte entfällt, bedient die interna-tionale Konkurrenz lediglich mit einem Wertanteil von etwa30% Auftragsvolumina derartigen Zuschnitts.

Günstig wird sich auch die gegebene Zusammensetzungder Auslandsorders deutscher Hersteller auswirken. Dies in-folge des mit derzeit 46% Anteil bereits hohen und weiterwachsenden Gewichts Asiens, mit den dort in aller Regelauch in schwächeren Phasen deutlich geringer erforder-lichen Abstrichen am Werkzeugmaschinenverbrauch.

Die vorliegende Publikation will sachlich unterrichten undaktuell diskutierte Branchenentwicklungen aufgreifen. Rea-listisch in den geschilderten Erwartungen und unabhängig

davon, ob der Berichtszeitraum attraktive Wachstumsratenbietet oder nicht. Als Zielgruppe sieht der VDW vornehmlichEntscheider aus der Politik, im Bankenbereich, auf Gewerk-schaftsebene, in der Presselandschaft oder in Forschungund Lehre. Die vom VDW regelmäßig überarbeitete und inverschiedener Hinsicht begründet von anderen Quellen ab-weichende Weltmarktbetrachtung bildet traditionell einenSchwerpunkt dieser 1998 begonnenen Broschürenreihe.

Frankfurt am Main, April 2012

Verein Deutscher Werkzeugmaschinenfabriken e. V. (VDW)Bereich Wirtschaft und Statistik

2

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 5/84

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 6/84

4

Zukunftsfähigkeit der Hochtechnologie-Orientierungder deutschen Werkzeugmaschinenindustrie

Der deutsche Werkzeugmaschinenbau ist als globaler

Technologieführer sehr gut positioniert und verfolgt denExport von Hochtechnologie im Sinne eines klar ausge-richteten Geschäftsmodells. Gleichzeitig verschieben sichdie internationalen Gravitationszentren der Nachfrage zu-gunsten der BRIC-Staaten und anderer Schwellenländer.Die Untersuchung des genannten Geschäftsmodells auf Nachhaltigkeit vor dem Hintergrund dieser schwerwie-genden Veränderungen sowie Ableitung von strategischenHandlungsempfehlungen sind Anliegen einer gemeinsamenUntersuchung von VDW und PricewaterhouseCoopers(PwC) gewesen. Ausgewählte Erkenntnisse haben diePartner des Projekts im Zuge der Mitgliederversammlungdes Verbands sowie einer Pressekonferenz im Rahmen derEMO Hannover 2011 vorgestellt. Das besondere Interessegerade solcher Mitgliedsfirmen, die Business-Pläne vor-legen und rechtfertigen sollen, belegt die Sinnhaftigkeitder Studie.

PwC hat in den vergangenen Jahren zahlreiche Projekteim Maschinen- und Anlagenbau durchgeführt. Entspre-chende Erfahrungen beziehen sich, neben der klassischen

Wirtschaftsprüfung, vor allem auf Transaktionsberatungbei Unternehmensübernahmen oder Restrukturierungs -vorhaben. Die Prüfungsgesellschaft treibt derzeit die Aus-weitung von Beratungskompetenzen auf zukunftsträchtigeTechnologiefelder voran. Motivation des VDW ist zumeinen das gezielte Aufgreifen hochaktueller strate-gischer Fragestellungen, zum anderen der während derWeltwirtschaftskrise oft formulierte Wunsch, der Verbandmöge dazu beitragen, das Verständnis für branchenspe-zifische Besonderheiten der mittelständischen Werkzeug-maschinenindustrie bei Finanzdienstleistern zu vertiefen.

Intensiv geführte Gespräche und ein Workshop mit Füh-rungskräften aus geografisch breit aufgestellten Unter-nehmensgruppen des Mitgliederkreises galten Szenarien-basierten Absicherungs- und Expansionsstrategien fürunterschiedliche Marktkontexte. Will heißen: sowohl fürHochlohnmärkte mit Sättigungstendenzen, als auch fürüberproportional wachsende Schwellenmärkte. Die zwi-schen April und September 2011 zusammengetragenenInformationen und Bewertungen haben eine Überprüfungund weitere Unterlegung durch Expertise im Zuge einerschriftlichen Intensivbefragung mit repräsentativemErgebnis erfahren.

Bright prospects for the future of the German machinetool industry’s high-tech orientation

German machine tool builders are very well positioned as

global technology leaders and export high-tech systemswithin the context of a clearly structured business model.At the same time, the international centres of gravity of demand are shifting in favour of the BRIC states and otheremerging countries. Against the background of theseserious changes, a joint study by the VDW and Pricewater-houseCoopers (PwC) was carried out to examine thesustainability of the business model mentioned aboveand to derive recommendations for strategic action. Theproject partners presented selected findings during thegeneral assembly of the association and at a press confer-ence in connection with the EMO Hannover 2011. The specialinterest shown particularly by member companies requiringto submit and justify business plans provides clear evidenceof just how meaningful the study is.

Over the years, PwC has carried out a large number of projects in machinery and plant construction. Along withclassic auditing services, relevant experience also primarilyinvolves transaction consulting in company takeovers orrestructuring projects. The audit firm is currently expand-

ing its consulting competence to include seminal technol-ogy fields. The motivation of the VDW was two-fold: first,to focus attention on a highly topical strategic question,and second, to address the request often expressed duringthe global economic crisis that the association should helpgive financial service providers a deeper understanding of industry-specific particularities relative to medium-sizecompanies in the machine tool industry.

Intensive meetings and a workshop with managers froma broad geographic spectrum of member corporations

generated valid scenario-based risk management andexpansion strategies for different market contexts. Thatmeans both for high-salary markets which are showingsigns of saturation and also for emerging markets whichare growing at disproportionately high rates. The infor-mation and assessments compiled between April andSeptember 2011 were reviewed and further refined throughexpertise as part of an intensive written survey withrepresentative results.

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 7/84

Zukunftsfähigkeit der HochtechnologieorientierungBright prospects for the future of high-tech orientation

5

Wertmäßig knapp die Hälfte des Produktionsvolumens

deutscher Werkzeugmaschinenhersteller geht auf Nach-frage zurück, die sich auf kundenspezifische Sonderma-schinen und Projektgeschäft richtet, während lediglichetwa 30 % der Weltnachfrage auf Spitzentechnologieabzielt. Der globale Marktanteil der Branche in Deutsch-land bewegte sich in den letzten Jahren nahe der 20 Prozent- Marke. In Westeuropa und Russland hält man sehr hoheAnteile von 38 % bzw. 24 %, in China, dem Leitmarktschlechthin, sind es beachtliche 9 % und in Brasilienund Italien jeweils 8 %.

Für 2015 ist in Westeuropa, den USA und dem Einzugs-gebiet der BRIC-Staaten ein durchschnittliches jährlichesWachstum von fast 18 % zu erwarten, vorausgesetzt dieaktuelle Staatsschulden-Krise in Europa und in den USAeskaliert nicht weiter. Impulse ergeben sich für die primärtechnologiegetriebenen westeuropäischen Märkte sowiedie auf Modernisierung des bestehenden Maschinenparksangewiesenen USA aus Nachholeffekten mit Blick auf dentiefen Fall 2008/2009. In China und Indien treibt anhaltendüberproportionales Wachstum dieser Volkswirtschaften

breit angelegte Industrie- und Infrastrukturinvestitionen.Der brasilianische Markt ist durch die Automobilindustriedominiert. Im Vorfeld sportlicher Großveranstaltungenstehen Infrastrukturvorhaben bedeutender Dimension an.In Russland werden Investitionen in die Grundstoffgewin-nung zunehmend durch solche in die verarbeitendeIndustrie flankiert. Steigende Konsumfähigkeit der Be-völkerung verlangt nach höherwertigen Produkten, wassteigende Ansprüche an die Fertigungstechnik auslöst.

Technologiesegmentmix begünstigt deutsches Angebot

Der deutsche Werkzeugmaschinenbau wird sich in dennächsten Jahren im Spannungsverhältnis zwischen einerdie eigene Position stärkenden Verschiebung im Tech-nologiesegmentmix zugunsten von Mid Tech sowie HighTech und längerfristigen Unsicherheitsfaktoren bewegen,wie Fachkräftemangel, technologischer Konvergenz asia-tischer Wettbewerber oder technologischem Wandel inHaupt-Anwenderindustrien. Hinzu tritt die Tatsache, dasssich die Wertschöpfung der Branche entsprechend ihremExportmodell noch zu ganz überwiegendem Teil in Deutsch-land konzentriert. Local-Content-Anforderungen oder dieprotektionistische Nutzung anderer handelspolitischer„Stellschrauben“ können rasch zu Friktionen führen.

In terms of value, customer-specific special machines and

project business represent nearly half of the total produc-tion volume of Germany’s machine tool manufacturers,while advanced technology comprises only about 30% of world demand. In recent years, Germany’s share of theglobal market has fluctuated near the 20% mark. WesternEurope and Russia maintain very high shares of 38% and24%, respectively; the undisputed leading market Chinahas a respectable 9%, and Brazil and Italy hold 8% each.

In Western Europe, the USA and the catchment area of theBRIC states, average growth of nearly 18% is expected in2015, provided the current public debt crisis in Europe andthe USA does not escalate further. Catch-up effects in thewake of the steep declines in 2008 / 2009 give impetus tothe primarily technology-driven markets of Western Europeand also in the USA, which must modernise its existingmachine base. The national economies in China and Indiacontinue to grow at disproportionately high rates, therebydriving broad-based investments in industry and infrastruc-ture. The Brazilian market is dominated by the automotiveindustry. In advance of upcoming major athletic events,

infrastructure projects of significant scope are in the works.In Russia, investments in raw material extraction are in-creasingly flanked by their counterparts in the processingindustries. Growth in the buying power of the populationis increasing the demand for high-quality products, there-by necessitating enhancements in manufacturing tech-nology.

Combination of technology segments favoursGerman offering

In the years ahead, German machine tool constructionwill have to strike a dynamic balance between a technologysegment mix which is shifting (to the benefit of its ownposition) in favour of mid-tech and high-tech on the onehand, and longer term uncertainty factors on the other –such as the lack of skilled labour, the technological con-vergence of Asian competitors, or technological changesin major user industries. It is also true that, in accordancewith its export model, the value creation of the sectorremains concentrated to a very large extent in Germany.Local content requirements or the protectionist use of other trade policy “adjustment screws” can rapidly createfriction.

Zur Ausgangslage:Export von Hochtechnologie ist Erfolgsmodell!

Starting point:Exporting high technology is a successful model!

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 8/84

6

Die ausschließlich für Mitgliedsunternehmen von VDWund Fachverband Werkzeugmaschinen und Fertigungs-systeme verfügbare Studie greift dieses Szenarium in Formvon Handlungsoptionen auf, die einer vierstufigen Stra-

tegie folgen: Absicherung des High-Tech-Segments inKernmärkten, Durchdringung des High-Tech-Segmentsin BRIC-Märkten, Eintritt in das Mid-Tech-Segment derBRIC-Märkte und schließlich Durchdringung von MidTech in den Kernmärkten. Jede Stufe wird durch einenMaßnahmenkatalog vertieft.

Prinzipiell handelt es sich um zwei Untersuchungsmodule:eine ausführlich kommentierte Fassung der während derMitgliederversammlung vorgestellten Erkenntnisse, idealfür die Führungs- und Leitungsebene, sowie eine deutlichbreitere Backup-Version mit zusätzlichem Tabellen- undGrafikmaterial für die unmittelbar befasste Arbeitsebene.

The study, which is exclusively available for member com-panies of the VDW and the Sector Association Machine Toolsand Manufacturing Systems, casts this scenario in theform of action options as part of a four-pronged strategy:

consolidation of the high-tech segment in core markets,penetration of the high-tech segment in BRIC markets,entry into the mid-tech segment of the BRIC markets and,finally, penetration of mid-tech in the core markets. A listof actions develops each of these elements in detail.

There are two main analytical modules: a fully commentedsummary of the findings presented during the generalmeeting, which is ideal for the management and executivelevels, and a much broader back-up version with additionaltables and diagrams for the working level directly concerned.

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 9/84

Aktuelle Situation und PerspektivenCurrent situation and perspectives

Individuelle Prozesslösungen für die multifunktionale Werkstückfertigung: Drehen, Hartdrehen, Rotationsdrehen, Unrund-Feindrehen,Endenbearbeitung, Bohren, Gewinden, Fräsen, Schleifen, Finishen, Induktionshärten. Im Mittelpunkt steht die Entwicklung eines komplettenSystems bei uneingeschränkter Prozessbeherrschung. Die Komplett-Werkstückbearbeitung durch Verfahrensintegration in einemArbeitsraum bietet maximale Flexibilität, hohe Qualität, geringere Stückkosten und größtmögliche Effizienz.

Individual process solutions for multifunctional workpiece manufacturing: turning, hard turning, rotational turning, out-of-round precisionturning, end machining, boring, thread-cutting, milling, grinding, finish cutting and induction hardening. At the centre of it all is thedevelopment of a complete system capable of handling an unlimited range of processes. Complete workpiece machining through processintegration in a single workspace provides tremendous flexibility, high quality, low piece costs and maximum efficiency.

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 10/84

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 11/84

0

100

120

3-Monats-Durchschnitte: %-Veränderung zum Vorjahr (nominal)

%

3 monthly averages: %-change to previous year (nominal)

80

60

40

20

-80

-60

-40

-20

02 03 04 05 06 07 08 09 10 11

140

Situation/PerspektivenSituation/Perspectives

9

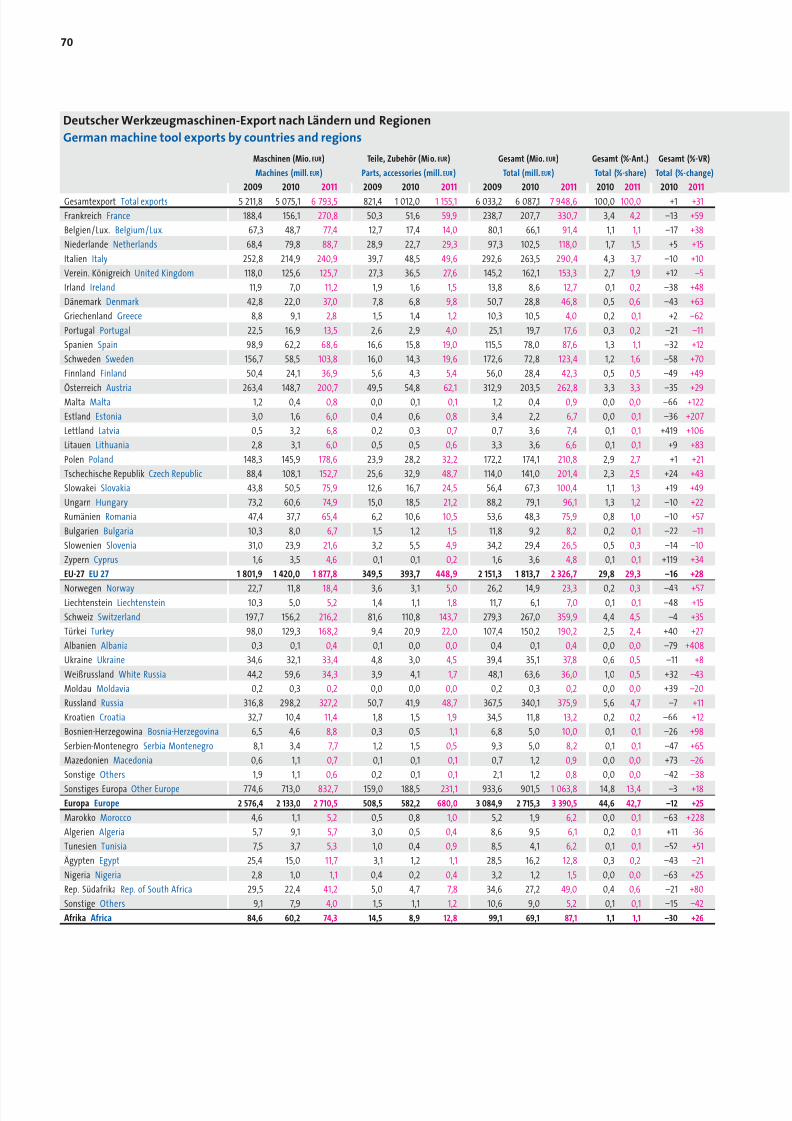

Anteile am gesamten Ausfuhrvolumen stehen sich Asienund Europa in bislang nicht gekannter Weise mit jeweils45 % Quote auf Augenhöhe gegenüber!

Parallel zum noch geschwächten Inlandsverbrauch 2010,wo ohne Berücksichtigung von Dienstleistungen nochmals10 % Minus auf 6,9 Mrd. EUR zu verbuchen sind, verbleibtauch der deutsche Werkzeugmaschinenimport mit 7 %Abschlag und 2,8 Mrd. EUR im negativen Bereich. Dertraditionellen Struktur noch folgend, decken europäischeKonkurrenten mit über 70 % Anteil einen Großteil desEinfuhrvolumens ab, wobei allerdings Lieferverflechtungenzwischen deutschen Führungsgesellschaften und ihrenTochterfirmen im Ausland eine wesentliche Rolle spielen.

Im Dezember 2010 liegt die Anzahl der Beschäftigten imWerkzeugmaschinenbau am Standort Deutschland mitrund 63.800 Personen um etwas mehr als 3% unter demJahresendstand 2009 (damals –8%). Hatte der Auslastungs-gradder Kapazitäten im Oktober 2009 bei nur mehr 67%gelegen, notiert die Branche im gleichen Monat desaktuellen Referenzjahres 2010 mit 86 %. Erwartungsgemäßähnliche Tendenz zeigt auch der Auftragsbestand: DemNiveau von 5,5 Monaten in 2009 stehen im Oktober 2010schon fast 8 Monate Reichweite gegenüber.

Still weakened in 2010, domestic consumption lost another10% excluding services (EUR 6.9 billion), while machinetool imports to Germany also remained in the negative

range with a 7% decline (EUR 2.8 billion). Maintaining thetraditional structure, European competitors covered a largepart of the import volume with more than a 70% share,whereby supply link-ups between leading German com-panies and their local subsidiaries abroad played a major role.

In December 2010, the number of employees in machinetool construction in Germany (slightly over 63,800 people)was somewhat more than 3% below the level at the endof 2009 (which was –8% at the time). If the utilisation of capacities was still only 67% in October of 2009, the indus-

try posted 86% utilisation in the same month of the cur-rent reference year of 2010. As expected, the order backlogalso demonstrated a similar tendency: The level of 5.5 monthsin 2009 contrasted with a range of nearly eight monthsalready in October 2010.

Auftragseingang der deutschen WerkzeugmaschinenindustrieOrder intake of the German machine tool industry

Quelle: VDMASource: VDMA

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 12/84

02 03 04 05 07 08 09

70

75

100

0 2 0 3 04 0 5 0 6 07 0 8 0 9

4

5

6

7

8

9

Kapazitätsauslastung (%)*Capacity utilization (%)*

Auftragsbestand (Monate)Order backlog (months)

10 11

10

10 11

95

90

85

80

65

60

06

10

Auftragseingang 2011 stößt in historisch einmaligeDimensionen vor

Der Auftragseingang deutscher Werkzeugmaschinenher-steller legt im Jahresverlauf 2011 um weitere 45 % auf ein Volumen von spektakulären 16,7 Mrd. EUR zu! Dasbislang als einsames Rekordniveau betrachtete Ergebnis2007 wird nicht allein wieder erreicht, sondern übertroffen.Allerdings ergibt sich im Quartalsmuster der Nachfragemit zunehmend stärkeren Referenzwerten 2010 deutlichabnehmende Entwicklungsdynamik. Während für die1. Jahreshälfte, mit 130 % Plus im 1. Vierteljahr und 83 %Zuwachs im 2. Quartal, noch eine satte wertmäßige Ver-doppelung verbucht werden darf, steht das 3. Vierteljahrfür noch 29 % Wachstum und das Schlussquartal kommtmit 6% Minus erstmals auf ein moderat negatives Ergebnis.

Die Differenzierung der Bestelltätigkeit nach Inlands- undAuslandsorders unterstreicht trotz sehr ähnlicher prozen-tualer Wachstumsbeiträge zuvor nicht vorstellbare Höhenin der Auslandsnachfrage (11,2 Mrd. EUR), selbst gegenüberextremer Ausweitung wie in 2007. Man distanziert dieseReferenz mit fast 2 Mrd. EUR Abstand. Die Inlandskompo-nente der Nachfrage 2011 steuert im Volumen 5,5 Mrd. EUR

bei und hält entsprechend deutlichen Abstand zum vor-stehend erwähnten Level 2007.

Incoming orders in 2011 take on uniquely historicdimensions

Over the course of 2011, German machine tool manufac-turers’ incoming orders increased by another 45%, reach-ing the spectacular volume of EUR 16.7 billion! Previouslyconsidered as a record which could never be repeated, the2007 result was not only attained again, but exceeded.However, in the quarterly pattern of demand with increas-ingly strong reference values in 2010, the dynamic rate of development was clearly diminishing. With a 130% increasein the first quarter and 83% growth in the second quarter,the full double in total value could be posted for the firsthalf of the year. There was only 29% growth in the thirdquarter, however, and the final quarter’s 6% decline markedthe first moderately negative result.

Despite very similar percentage growth rates, the differ-entiation of order activity according to domestic andforeign orders underscores the previously unimaginablescale of foreign demand (EUR 11.2 billion), even by compari-son with huge expansion as experienced in 2007. Thatbenchmark was outdistanced by nearly EUR 2 billion. Thedomestic component of demand contributed a volume of

EUR 5.5 billion in 2011 with a similarly unequivocal distancefrom the aforementioned level of 2007.

Kapazitätsauslastung und Auftragsbestand der deutschen WerkzeugmaschinenindustrieCapacity utilization and order backlog of the German machine tool industry

* Okt. 11 = 95,5 %,Jan. 12 = 95,6 %Quellen: Ifo-Institut, VDMA* Oct. 11 = 95.5%,Jan. 12 = 95.6%Sources: Ifo institute, VDMA

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 13/84

Situation/PerspektivenSituation/Perspectives

11

Nach wirtschaftsgeografischen Regionen untergliedert,ergibt sich für die Nachfrage aus Europa gegenüber der

aus Asien zwar ein überproportional hoher Steigerungs-satz von 43%, die Ablösung Europas als wichtigste Absatz-region (38% Anteil bezogen auf die Auslandsorders ins-gesamt) ist indessen angesichts von fast 46% Teilhabe imFalle Asiens bereits vollzogen! Das Nachfragevolumen ausAmerika hat sich um 44 % aufstocken lassen, der Anteil istum knapp einen Prozentpunkt auf 15,6 % angestiegen.

Die Betrachtung der nachfragestärksten Auslandskundenzeigt folgendes Bild: Der „Steigflug“ von durch China er-teilten Orders ist schlicht ohne Beispiel, das hervorragendeErgebnis 2010 lässt sich um ein weiteres Drittel überbieten,und das für die USA als Nummer 2 im Ranking verbuchteVolumen wird mit fast Faktor 4 distanziert. Im asiatischenRaum fungieren ferner Indien, Korea und Taiwan alsWachstumsmotoren. Auch die Nachfrage aus Japan legtum ein reichliches Fünftel zu. Abgesehen vom kraftvollanziehenden Aufkommen der in starkem Maße automobilgetriebenen „Klassiker“ wie Frankreich, Italien und Groß-britannien wird Europa durch hochdynamische Entwick-lungen im Osten gestützt, sprich: erneut durch Automotive

Business in Russland, Ungarn, Tschechien und der Slowakei.Der fokussierte Blick auf Amerika zeigt die USA und denNAFTA-Standort Mexiko, welcher ebenfalls den Absatz-

Broken down according to geo-economic regions, Europe’s43% growth in demand was disproportionately high versus

that of Asia, but the mantle of the biggest consumptionregion had already passed from Europe (38% share of totalforeign orders) to Asia, with its share of nearly 46%. Thedemand volume from the Americas increased by 44% whileits world share rose by barely one percentage point to 15.6%.

Analysis of the foreign customers with the highest demandshowed the following picture: The take-off and continuedclimb in orders placed by China simply has no precedent.The outstanding result of 2010 was exceeded by one thirdagain, and the volume posted for second-ranked USA wasoutdistanced by a factor of four. India, South Korea andTaiwan also served as growth engines in Asia. And Japanesedemand increased by a full fifth as well. Besides burgeoningdemand from the “classic” markets largely fuelled by theautomotive sector – including France, Italy and GreatBritain – support also came in the form of highly dynamicdevelopment in Eastern Europe: once again from the auto-motive business in Russia, Hungary, the Czech Republic andSlovakia. Turning the focus to the Americas, the lead pos-itions were held by the USA and its NAFTA partner Mexico,

which also reflected the sales boom in the internationalautomotive industry and took advantage of structurallyinduced procurement measures promoting the develop-

Wichtige Zahlen der deutschen WerkzeugmaschinenindustrieKey figures of the German machine tool industry

Mrd.EURBill.EUR %-Veränderung%-Change2007 2008 2009 2010 2011 2009/08 2010/09 2011/10

ProduktionProduction 12,6 14,2 10,2 9,9 13,1 –28 –3 +33Spanende MaschinenCutting machines 7,1 8,2 5,6 5,1 7,1 –31 –10 +41Umformende MaschinenForming machines 2,4 2,5 2,1 2,1 2,6 –15 –2 +23Teile, ZubehörParts, accessories 2,3 2,5 1,6 1,9 2,4 –36 +14 +27Installationen, Reparaturen etc.Installation, repairs etc. 0,9 0,9 0,8 0,9 1,1 –15 +10 +21AuftragseingangOrder intake 16,0 13,7 6,2 11,5 16,7 –55 +85 +45InlandDomestic 6,7 5,6 2,2 3,8 5,5 –61 +75 +46AuslandForeign 9,3 8,1 4,1 7,7 11,2 –50 +90 +45(ohne Installation, Reparaturenexcl. installation, repairs)Produktion Production 11,8 13,3 9,4 9,0 12,1 –29 –4 +34– Export – Exports 7,8 8,2 6,0 6,1 7,9 –26 +1 +31+ Import + Imports 3,3 3,7 2,1 2,0 2,8 –43 –7 +42= Inlandsverbrauch= Domestic consumption 7,4 8,8 5,5 4,9 6,9 –37 –10 +41Exportquote (%)Export quota (%) 65,9 61,9 64,3 67,5 66,0Importquote (%)Import quota (%) 45,4 42,4 38,7 40,4 40,7BeschäftigteEmployment 66 369 70 839 69 614 64 10865 877 –1,7 –7,9 +2,8Kapazitätsauslastung (%)Capacity utilization (%) 93,6 94,7 72,6 75,4 93,8Auftragsbestand (Monate)Order backlog (months) 7,5 8,7 6,2 7,1 9,3

Daten 2011 teilweise geschätztHinweise:– Daten beziehen sich auf Werkzeugmaschinen inklusive Teile/Zubehör– Auftragseingang: Hochrechnung auf Basis Verbandsstatistik– Beschäftigte, Kapazitätsauslastung, Auftragsbestand: JahresdurchschnitteQuellen: Statistisches Bundesamt, Ifo-Institut, VDMA, VDW

Data 2011 partly estimatedNote:– Figures include parts/accessories– Order intake: projection based on associations’ statistics– Employment, capacity utilization, order backlog: average of yearSources: German Statistical Office, Ifo-Institute, VDMA, VDW

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 14/84

12

boom in der internationalen Automobilindustrie wider-spiegelt und von strukturell induzierten Beschaffungs-maßnahmen für z. B. energieeffizientere Motoren- und

Getriebekonzepte profitiert, sowie natürlich das aufstre-bende Brasilien und Argentinien in den Spitzenpositionen.

Bei quartalsweise relativ gleich verteilten Wachstumsbei-trägen, die den hohen Auslastungsgrad der Firmen undabnehmende Kapazitätsspielräume signalisieren, stehenschließlich für das gesamte Jahr 2011 sage und schreibe

33% Produktionsplus auf 13,1 Mrd. EUR zu Buche (erneuteinschließlich Teile/Zubehör und Dienstleistungen). In der„Netto-Betrachtung“ allein für die Maschinenfertigungsind es 35 % Plus. Hinter der Rekordausbringung desJahres 2008 bleibt die Branche insgesamt um etwa 8 %zurück, wobei aber Hersteller spanender Werkzeugma-schinen bereits den unmittelbaren Anschluss herstellenkönnen.

In der Gegenüberstellung der Ergebnisse für spanendeund umformende Technologien kommen die unterschied-lichen Beschaffungsmodalitäten zum Ausdruck. In demSinne nämlich, dass sich die überproportionale Dynamikim spanenden Bereich stärker in konjunkturellem Zusam-

ment of more energy efficient engines and transmissionconcepts, for example – together with the ambitious Braziland Argentina, of course.

Relatively constant quarterly growth rates were indicativeof companies’ consistently higher utilisation and dimin-ishing flexibility in terms of capacity. Believe it or not, theyultimately accounted for a 33% increase in production toEUR 13.1 billion for the full year 2011 (once again includingparts and accessories, and services). In the “net analysis”

for machinery production alone, there was a 35% increase.Overall the sector remained about 8% behind the recordoutput of 2008, whereby manufacturers of metal-cuttingmachine tools already came within striking distance.

A comparison of the results for metal-cutting and metal-forming technologies reflects their different procurementmodalities. Which is to say that the disproportionatelydynamic activity in the metal-cutting sector, with itsmuch broader market segment orientation, primarilyfollowed the general economic climate. By contrast, themetal-forming sector is driven to a large extent by (heavyduty) press construction. As a result it is closely tied to theprocurement activity of the automotive industry, so its

2011 = VDW-SchätzungHinweis: Ab 1995 Werteverfügbar für Installation,ab 2002 zusätzlich fürReparatur/InstandhaltungQuellen: StatistischesBundesamt, VDW, VDMA2011 = VDW estimateNote: since 1995 figuresavailable for installation,since 2002 additionallyfor repair/maintenanceSources: German StatisticalOffice, VDW, VDMA

Werkzeugmaschinen-Produktion DeutschlandMachine tool production Germany

Maschinen MachinesTeile, Zubehör Parts, accessoriesInstallation, Reparatur/Instandhaltung Installation, repair/maintenance

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Mrd.eur Bill.eur

0

3

6

9

12

15

09 10 11

Auftragsflut des Jahres 2011 lässt sichhinsichtlich der Umsetzung im Produktionswertnur mit Zeitversatz bändigen

The overwhelming flood of orders in 2011cannot be converted into production valuewithout a time delay

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 15/84

Situation/PerspektivenSituation/Perspectives

13

menhang mit deutlich bereiterer Aufstellung nach Bran-chen versteht, während der durch den (Groß-)Pressenbaugeprägte umformende Bereich eng dem Beschaffungs-verhalten der Automobilindustrie folgt, entsprechende

Pro jekte sehr lange Durchlaufzeiten haben und sich dieRealisierung von Auftragsvolumen in Produktion und Um-satz oft „paukenschlagartig“ und das jeweilige Berichts jahrüberschreitend vollziehen kann. Auch der mit Umformtech-nik verbundene positive Basiseffekt – man arbeitet bereits2010 fast wieder auf Vor jahresniveau – bremst Zuwachsein.Speziell die Blechbearbeitungmit und ohne Laserverwen-dung hat im Gegensatz zum projektorientierten Pressen-bau 2010 für schnellen Durchsatz gesorgt.

Der Werkzeugmaschinenexport setzt seinen Wachstums-kurs im 4. Quartal 2011 gebremst, aber mit Zuwachs umein Fünftel souverän fort. Das Jahresergebnis steht fürkraftvolles Plus von 31% auf ein Volumen von 7,9 Mrd. EUR,gleicht den Einbruch aus dem Krisenjahr 2009 im Konzertmit 2010 fast vollständig aus und kommt somit direkt anden Rekordwert 2008 heran. Treibsätze für das Ausfuhr-wachstum 2011 sind mit 57% Steigerungssatz das Amerika-geschäft und die mit 29 % Plus (nach +22% im Referenzjahr)notierende Dynamik Asiens. Zwar legt auch der europäischeMarkt um 25% zu, doch läuft sein Anteil am Gesamtexport

von 45% in 2010 auf aktuell 43% zurück. Asien hingegenhält seinen Anteil von 41 % konstant. Amerika weitet seinePartizipation von 12% auf knapp 15% aus. Für China alleinesind im aktuellen Berichtsjahr 34 % Zuwachs und ein mo-derat ausgebauter Anteil von 29% am gesamten Ausfuhr-volumen deutscher Herstellerfirmen zu konstatieren. DieStellung als zweitgrößter Markt können die USA mit 66%Plus und einem Anteilsgewinn von 2 Punkten auf 9% aus-bauen. Trotz gegenüber 2010 vergleichsweise schmalemZuwachs um 11 % steht Russland für die drittstärkste Auf-nahmefähigkeit für deutsche Werkzeugmaschinen, noch

vor der klassischen europäischen Kundschaft in der Schweiz,Frankreich und Italien.

Wegen der im Universalmaschinenbereich eingefordertenkurzen Lieferzeiten, hauptsächlicher Lost-Order-Grund fürdie voll ausgelastete Branche in Deutschland, partizipiertder Werkzeugmaschinenimport 2011 mit 42 % Plus auf rund 2,8 Mrd. EUR (ohne Dienstleistungen) voll am Inlands-verbrauch, der sich auf 6,9 Mrd. EUR beläuft. Der auf euro-päische Konkurrenz entfallende Anteil sinkt von fast 72 %im Vorjahr auf 68 %, die Teilhabe Asiens nimmt hingegenvon 22 % auf wenig unter 26% zu. Im Falle der Schweiz(alleine 32% Anteil), Italiens (Partizipation von knapp 8%),Tschechiens und Polens (gemeinsamer Anteil von gut 7 %)

projects typically have very long turnaround times and thecontract volumes it realises as production and turnoverwith great “fanfare” often extend beyond the year currentlyunder review. And the basic positive effect underlying

metal-forming technology – already in 2010 work wasproceeding almost at the level of the previous year again –also inhibited growth. Unlike the project-oriented pressconstruction, sheet-metal machining, with and withoutthe use of lasers, provided particularly rapid throughput.

In the fourth quarter of 2011, machine tool exports continu-ed to grow at a somewhat slower pace, increasing by asolid 20% nevertheless. The results over the course of the

year increased by an impressive 31% to a volume of EUR7.9 billion. Together with 2010, this compensated completelyfor the collapse from the crisis year of 2009, thereby closelyapproaching the 2008 record value. The driving forcesbehind export growth in 2011 comprised trade with theAmericas (+57%) and the dynamic activity in Asia (+29%,following a 22% increase in the reference year). The Euro-pean market also grew by 25%, but its share of total worldexports fell from 45% in 2010 to its current level of 43%.Asia, on the other hand, maintained its 41% share. TheAmericas extended their share from 12% to nearly 15%. Onits own, China posted 34% growth and a moderately higher

29% share of the total volume exported by German manu-facturers in the current reporting year. As the second lar-gest market, the USA was able to extend its position with+66% and a two-point gain in world share to 9%. Despitecomparatively modest 11% growth over 2010, Russia repre-sented the third strongest absorption capacity for Germanmachine tools, still ahead of the traditional Europeancustomer base in Switzerland, France and Italy.

Due to the short delivery times demanded by the universalmachine sector – the primary reason for lost orders in

Germany, where the sector was operating at full capacity –the 42% increase in machine tool imports to about EUR 2.8billion in 2011 (without services) was used exclusively tosupport domestic consumption, which totalled EUR 6.9billion. The share corresponding to the European competi-tors fell from nearly 72% in the previous year to 68%, whileAsia’s share rose from 22% to just below 26%. In the caseof Switzerland (a 32% share all to itself), Italy (nearly an 8%share), the Czech Republic and Poland (common share of afull 7%), mention should once again be made of the supplylink-ups between leading German companies and localsubsidiaries. Following a 12% increase in 2010, the volumeof rapidly deliverable universal machines imported fromJapan increased by 55% in the current reporting year, and

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 16/84

14

ist erneut auf Lieferverflechtungen deutscher Führungs-gesellschaften mit dortigen Tochterfirmen zu verweisen.Der Import schnell lieferbarer Universalmaschinen ausJapan steigt nach 12% Zunahme 2010 im aktuellen

Berichts jahr um 55% und erreicht einen Anteil von knapp13 % an der Gesamteinfuhr. Koreanische, taiwanesische undchinesische Standardmaschinen aus dem Basissegment,vielfach über den Handel re-exportiert, legen gegenüber2010 jeweils über 80% bzw. im letztgenannten Fall um 52 %zu und realisieren gemeinsam einen im Vergleich mit demReferenzjahr gleichgebliebenen Anteil von 12%.

Branche geht selbstbewusst ins Geschäftsjahr 2012,weiteres Produktionsplus vorgezeichnet

Natürlich ist die Vorausschau wegen des gerade in letzterZeit sehr heftig auftretenden Korrekturbedarfs bei denPrognosegrundlagen ein heikles Unterfangen. Es herrschennach wie vor, trotz eingeläuteter Entspannung in dergestörten Kreditversorgung ganzer Volkswirtschaften,unsichere Erwartungen. Die Abschätzung der Aufnahme-fähigkeiten wichtiger Märkte für Investitionsgüter bleibtüberlagert durch den sorgenvollen Blick auf das weltweiteFinanzsystem. Die Prognose an sich bewegte sich währendder vergangenen drei Jahre in einem denkbar ungünstigen,

weil stark volatilen Umfeld. Trendverschiebungen imVerlauf der globalen Bruttoinlandsprodukte, der Industrie-produktionen und insbesondere Anlageinvestitionen inHaupt-Anwenderindustrien führender Märkte bleiben auf der Tagesordnung.

Ausgelöst durch die am aktuellen Rand fühlbaren finanz-und realwirtschaftlichen Konsolidierungstendenzen dürftensich das Produktionsgeschehen und der Invest aber stabilerals erwartet entwickeln. Weltweite Industrieproduktionund Investitionstätigkeit sind vom Prognosepartner des

VDW, der britischen WirtschaftsforschungsgesellschaftOxford Economics, im Frühjahr des laufenden Jahres vonStagnation bzw. lediglich 3% Steigerungsrate auf knapp 4%Plus bzw. 7% Zuwachs neu justiert worden. Entsprechendbewegten sich diese Sätze deutlich über dem noch im Spät-herbst 2011 als Risikovariante durchgespielten Szenarium.

Im Halbjahresmuster des Auftragseingangs deutscherWerkzeugmaschinenhersteller sind im laufenden Jahrüberproportionale Abstriche während der ersten 6 Monateund anschließende Konsolidierung in der 2. Jahreshälftevorgezeichnet. In Sachen deutscher Werkzeugma -schinenproduktion dürfte sich die Entwicklung imJahresverlauf naturgemäß umgekehrt ausnehmen: Hier

their share of total imports was just below 13%. SouthKorean, Taiwanese and Chinese standard machines fromthe basic segment, in many cases re-exported through thetrade, increased more than 80% over 2010 – +52% in the

case of the latter – and achieved together a 12% share, whichremained constant relative to the reference year.

The industry heads into the business year 2012 withconfidence – further increase in production anticipated

The frequent need to correct basic data underlying prog-noses in recent times has made predicting the futurerather difficult, of course. Uncertainty continues to reigndespite initial relief in the disrupted credit supply of entirenational economies. Estimations of the absorption capaci-ties of major markets for investment goods remain over-shadowed by worrisome prospects for the global financesystem. During the past three years, prognoses themselvesinvolved the least favourable conditions imaginable – whichis to say, highly volatile ones. Shifting trends in global GDPdevelopment and industrial production and especially withregard to equipment investments in the major user indus-tries of leading markets are still on the agenda.

Currently on the margins, however, there are perceptible

consolidation tendencies in finance and real economy. Theproduction activity and investment they induce should bestabler than once feared. In the spring of the current year,the VDW’s prognosis partner, the British economic researchinstitute Oxford Economics, readjusted its assessments of global industrial production and investment activity fromstagnation and a mere 3% growth rate, respectively, tonearly +4% and 7% growth, respectively. So these rateshave already risen well above the scenario which was stillconsidered as the risk variant in the late autumn of 2011.

The half-year pattern of incoming orders received by Ger-man machine tool manufacturers anticipates dispropor-tionately high declines during the first six months of thecurrent year followed by consolidation activity in thesecond half. Regarding German machine tool production,the development over the course of the year should natur-ally turn out the other way round: Here a continued strongfirst half-year is likely to be followed by a moderate one-digit decrease. The composition of its portfolio of foreignorders will effectively support the sector in Germany. Thisis because of the weight of Asia, which is high and stillgrowing, and the much lower loss of momentum in machinetool consumption required here in 2012 (–5%). Moreover,the Chinese (and now the Indians as well) see a growing

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 17/84

Situation/PerspektivenSituation/Perspectives

15

darf nach dem noch starken 1. Halbjahr ein moderateseinstelliges Minus als wahrscheinlich gelten. Für die Branchein Deutschland stützend wird sich die Zusammensetzungihrer Auslandsorders auswirken. Dies wegen des hohen

und weiter wachsenden Gewichts Asiens und der hier mit5% Minus deutlich geringer erforderlichen Dynamikverlusteim Werkzeugmaschinenverbrauch 2012. Hinzu tritt die auschinesischer Sicht (letztlich auch aus indischem Blickwinkel)notwendige Hinwendung zu hochwertigen, potentziellexportfähigen Erzeugnissen, was den Anspruch an Ferti-gungstechnologien nach oben verschiebt. Deutsche Her-steller haben gute Chancen, überproportional an solchenTrends zu partizipieren. Der hohe Auftragsbestand vondeutlich über 9 Monaten wird die „Nachfragedelle“ imÜbergangsjahr 2012 ebenfalls ein gutes Stück einebnen.

VDW und Oxford Economics haben ihre Prognose für dieProduktion 2012 der deutschen Werkzeugmaschinen-industrie deshalb auf 5% Plus gesetzt. Die gesamte durch-schnittliche Auftragsreichweite darf nicht als über dieBranche gleich verteilt unterstellt werden. Insofernmarkiert eine um 5 % gesteigerte Ausbringung aus Sichtvon Universalmaschinenherstellern im Volumengeschäfteine außerordentlich fordernde Marke. Andererseits wirdder hohe Anteil kundenspezifischer Sonderanlagen und

des Projektgeschäfts mit langen Durchlaufzeiten amgesamten Auftragseingangsvolumen 2011 (45 % Plus) starkdurchschlagen. Diese firmenkonjunkturellen Unter-scheidungsmerkmale hat der VDW in seinerÖffentlichkeitsarbeit wiederholt unterstrichen.

need for high-quality, potentially exportable products, andthis is raising the standards of manufacturing technologyfurther. German manufacturers are well positioned tobenefit disproportionately from such trends. The high order

backlog (well over nine months) will also go a long waytowards smoothing the “demand dip” during the transition

year of 2012.

For this reason, the VDW and Oxford Economics have settheir prognosis for the production of the German machinetool industry in 2012 to +5%. It would be a mistake to assumethat the overall average order backlog is evenly distributedthroughout the industry. In that respect, 5% more outputwould be an extraordinarily challenging target from theperspective of universal machine manufacturers in thevolume business. On the other hand, the high share of cus-tomised special units and of project business with longturnaround times will heavily penetrate the overall volumeof 2011 incoming orders (+45%). In its public relations work,the VDW has repeatedly stressed these distinguishingcharacteristics with regard to the economic conditions of companies.

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 18/84

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 19/84

Werkzeugmaschinen-Produktion Machine tool production

Maximale Zerspanleistungen und Schnittgeschwindigkeiten durch den Einsatz von hochproduktiven Werkzeugen mit Wendeschneid-platten-Technologie auf einer Wälzfräsmaschine.

Maximum metal removal rates and cutting speeds through the use of high productivity tools with tipped tool insert technology on a gear hobbing machine.

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 20/84

18

Referenz für aktuelle Bewertungen: 2010 läuft wegenNachfrageboom aus Asien deutlich besser als zuJahresbeginn erwartet

Der typische Zeitversatz zwischen wieder hochlaufenderProduktion beim Kunden und nachfolgendem Invest inneue Anlagen bleibt 2010 weitgehend aus oder erweistsich doch als in bislang nicht gekannter Weise verkürzt.Weder für das ansatzlose Auftreten und die Intensität desNachfrageausfalls zu Krisenbeginn im Herbst 2008 undwährend des frühen Jahresverlaufs 2009 noch hinsichtlichdes nicht minder unmittelbaren und drastischen Anzie-hens der Orders 2010 gibt es Vorbilder in der Branchenhis-torie. Beim extremen Steigungswinkel der Bestelltätigkeitim Referenzjahr dieser Publikation spielen natürlich dieTiefe der zuvor erreichten Talsohle und vergleichsweisebescheiden gewordene Volumina der betreffenden Aggre-gate eine nicht unwesentliche Rolle. Im Frühjahr 2010wird der dynamische Aufschwung und die Extrapolierbar-keit dieser Entwicklung auf den weiteren Jahresverlauf mitvorsichtiger Skepsis gesehen. Die Möglichkeit des Auftre-tens eines inzwischen „legendär“ gewordenen V-förmigenKonjunkturmusters gilt zu diesem Zeitpunkt als eherunrealistisch.

Dann aber kommt die deutsche Werkzeugmaschinenin-dustrie Quartal für Quartal in den Genuss zweistelligerZuwächse im Auftragseingang. Im 2. Halbjahr 2010 notierenmehrere Monate mit sogar dreistelligem Plus, das 4. Quar-tal verdoppelt den Referenzwert nahezu, und im Gesamt-

jahr 2010 darf ein um 85% höherer Auftragswert verbuchtwerden. Getrieben ist diese Entwicklung zunächst vorallem durch die Auslandsnachfrage, insbesondere ausChina, Südkorea und Indien. Diese Länder haben die Krisedeutlich schneller abgeschüttelt, sind frühzeitig auf denWachstumspfad zurückgekehrt und unterstützen somit

initial die Erholung des Werkzeugmaschinenbaus inDeutschland. Der Aufschwung in der Auslandsnachfragegewinnt danach zügig an Breite. Während der ersten dreiQuartale 2010 verzeichnen praktisch alle Regionen zwei-stellige Zuwächse, Südamerika und Südostasien glänzendreistellig.

Schon im August 2010 stehen erstmals wieder „schwarze“Umsatzresultate zu Buche! Bis Jahresende erfreut sich dieBranche Monat für Monat zweistelliger Zuwächse. Schließ-lich zeigt der Produktionswert im gesamten Jahresverlauf

Reference for current assessments: 2010 results areconsiderably better than expected at the start of theyear due to boom in demand from Asia

The typical time lag between the re-launch of productionat the customer and their subsequent investment in newequipment remained largely absent in 2010, or certainlyturned out to be far shorter than ever before. No historicalmodels from the industry exist for the sudden emergenceand intensity of the loss in demand at the start of the crisisin the autumn of 2008 and during the early part of 2009 –nor do models exist for the no less immediate and drasticrise in orders in 2010. The depth of the preceding valleyand the volumes of the aggregates concerned, which hadbecome relatively modest, played a significant role in theextremely steep increase in order activity in the reference

year of this publication, of course. In the spring of 2010,the dynamic recovery and the validity of extrapolating thatdevelopment to the rest of the year were met with cautiousscepticism. The possibility of experiencing what has mean-while become a “legendary” V-shaped economic curve wasconsidered rather unrealistic at that point in time.

But then, quarter after quarter, the German machine toolindustry enjoyed two-digit growth rates in incoming orders.

Several months during the second half of 2010 even postedthree-digit increases, and the reference value was nearlydoubled in the fourth quarter. The sector finished 2010with an 85% higher order value for the year. This trend wasdriven primarily by demand from abroad, especially fromChina, South Korea and India. These countries shook off the effects of the crisis much faster than the others. Theyreturned to a path of growth early, thereby providing initialsupport for the recovery of machine tool construction inGermany. The upswing in demand from abroad broadenedrapidly thereafter. During the first three quarters of 2010,

practically every region posted two-digit growth rates.South America and Southeast Asia outshined the restwith three-digit performance.

In terms of turnover, results already started to be in theblack again by August of 2010. By the end of the year, thesector was enjoying two-digit growth rates month aftermonth. Ultimately the production value over the courseof 2010 still posted a slight 3% loss relative to 2009. Thehealthy expansion of output was supported by metal-forming technology, which represented about 30% of the

Contrary to past experience, turnover alsobegan to increase much sooner

Auch der Umsatz dreht entgegen frühererErfahrungen viel schneller ins Plus

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 21/84

ProduktionProduction

19

2010 noch ein schmales Minus von 3 % im Vergleich mit2009. Gestützt wird die sich gut entwickelnde Ausbringungdurch die Umformtechnik, die für etwa 30% des Geschäftsmit Werkzeugmaschinen steht. Besonders positiv hebt

sich dabei die Blechbearbeitung ab, die im Gegensatz zurstark projektorientierten Pressentechnik wesentlich kürzereDurchlaufzeiten realisieren kann. Dies treibt die Produkti-onsleistung hier wieder fast auf Vorjahresniveau. Die Zer-spanungstechnik indessen notiert noch mit 7% im Minus.

Produktionsvolumen 2011 bricht sämtliche Rekorde

Nicht umsonst ist in Übersichtskapitel 2 bereits auf tradi-tionell hohe Anteile kundenspezifisch ausgelegter Sonder-maschinen bzw. des Projektgeschäfts, in beiden Fällen mitlangen Durchlaufzeiten verbunden, am gesamten Auftrags-eingang deutscher Werkzeugmaschinenhersteller hinge-wiesen worden. So ist dies insbesondere auch in 2010 derFall – und: für den gesamten Jahresverlauf ergibt sich einum 85 % über 2009 notierender Auftragseingang. ImOktober 2010 verfügt der deutsche Werkzeugmaschinen-bau bereits wieder über durchschnittlich fast 8 MonateReichweite der Auftragsbestände. Es liegt also auf der Hand,dass ein ganz erheblicher Anteil der insgesamt eingegan-genen Bestellungen erst in 2011 produktiv bzw. umsatz-

wirksam werden kann. Derart hoher Auftragsüberhangund anhaltend florierende laufende Orders im Berichts- jahr 2011 selbst (+45 %) führen zu Produktionswachstumvon 41% im reinen Maschinengeschäft während des 1. Halb-

jahres, von 38% im 3. Vierteljahr und somit leicht nachvoll-ziehbar auch von fast 40% über die ersten drei Quartale2011.

Nach Blick auf die monatlich vom VDMA durchgeführte,als Trendaussage gut taugliche Fortschreibung der Um-satzindizes für Oktober bis Dezember 2011 lässt sich die

Ausbringung des gesamten Jahres 2011 guten Gewissensmit 35 % Plus im Maschinengeschäft bzw. 33% Plus auf hochgerechnet 13,1 Mrd. EUR Volumen einschließlichTeile/Zubehör und Dienstleistungen beziffern.

VDW und Oxford Economics avisieren weiteresProduktionsplus 2012

Für den Ausblick auf 2012 relevant ist die Feststellung, dasssich der Auftragsbestand im Oktober 2011, trotz zum gleichenZeitpunkt 96 % Kapazitätsauslastung, nach wie vor beideutlich über 9 Monaten bewegt! Der Personalstandnotiert im Dezember 2011 mit rund 67.700 Beschäftigtenreichlich 6% über Vorjahresmonat. Ausgelöst durch die

machine tool business. One particularly positive highlighthere was the sheet-metal machining segment, which, unlikethe highly project-oriented press technology, was able toachieve significantly shorter turnaround times. This drove

the production performance here almost back up to thelevel of the previous year. Cutting machine tools, however,still posted a 7% decline.

Production volume in 2011 breaks all records

The overview chapter 2 has already indicated – and withgood reason – that the incoming orders received by Germanmachine tool manufacturers traditionally include a highshare of special machines designed according to customerspecifications, and also a high share of project business,both of which involve long turnaround times. This wasalso the case in 2010 in particular – and over the courseof the entire year, incoming orders exceeded the level of 2009 by 85%. In October of 2010, German machine toolconstruction had already established an average orderbacklog of nearly eight months again. So it goes withoutsaying that a very significant share of the total ordersreceived could not become productive or affect turnoveruntil 2011. An order backlog of this amplitude and continu-ously flourishing open orders in the reporting year 2011

itself (+45%) led to a 41% increase in production in the puremachinery business during the first half of the year, a 38%increase in the third quarter, and therefore also an easilycomprehensible increase of nearly 40% over the course of the first three quarters of 2011.

The continued sales indices that the VDMA prepares on amonthly basis are well suited for predicting trends. In viewof their figures for October through December 2011, thetotal output for 2011 can be estimated in good consciencewith a 35% increase for the machine business alone, and

with a 33% increase including parts and accessories, andservices to a projected volume of EUR 13.1 billion.

VDW and Oxford Economics predict a further increasein production in 2012

Regarding the prospects for 2012, it is appropriate to notethat although production was operating at 96% of capacityat the time, the order backlog in October 2011 remainedwell over nine months! With some 67,700 employees, staff-ing in December 2011 was a full 6% higher than in the samemonth of the previous year. Currently on the margins,however, there are perceptible consolidation tendenciesin finance and real economy. The production activity and

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 22/84

20

Spanende Werkzeugmaschinen*Metal cutting machine tools*

Umformende Werkzeugmaschinen*Metal forming machine tools*

Mrd.eur

Bill.eur

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

0

1

2

3

4

5

6

7

8

9

09 10 11

am aktuellen Rand fühlbaren finanz- und realwirtschaft-lichen Konsolidierungstendenzen dürften sich Produktions-geschehen und Invest stabiler als zuvor angenommen

entwickeln. Weltweite Industrieproduktion und Investiti-onstätigkeit sind vom Prognosepartner des VDW, derbritischen Wirtschaftsforschungsgesellschaft OxfordEconomics, deutlich über den Ansätzen liegend justiertworden, die noch im Spätherbst 2011 für ein Risiko-Szena-rium galten. Entsprechend konnte die aktuellste Voraus-schau für die Produktion 2012 der deutschen Werkzeug-maschinenindustrie auf 5 % Plus gesetzt werden. Eineausführlichere Herleitung dieses neuen Eckwertes findetsich gegen Ende des vorangegangenen Kapitels „AktuelleSituation und Perspektiven“.

Internationale Präsenz der Branche

Zunehmend weniger Sinn macht es auch für die Werkzeug-maschinenindustrie, alleine auf Datenmaterial für denStandort Deutschland abzustellen. Schließlich steht dieAuslandsproduktion deutscher Hersteller mit Blick aufdie Gesamtleistungsfähigkeit der Branche mittlerweilefür weit mehr als einen „Added Value“. Die Abschätzungder Auslandsproduktion wirft verschiedene Probleme auf.

So muss alles außen vor bleiben, was als Umsatz im deut-schenStammhaus fakturiert und somit bereits an natio-nale statistische Behörden gemeldet worden ist. Ferner

investment they induce should be stabler than initiallyassumed. The VDW’s prognosis partner, the British economicresearch institute Oxford Economics, has adjusted its assess-

ments of global industrial production and investmentactivity well above the estimates which were still consid-ered as a risk scenario in the late autumn of 2011. As a result,the production of the German machine tool industry isnow projected to increase by 5% in 2012. A complete deri-vation of this new benchmark appears at the end of theprevious chapter “Current situation and perspectives”.

International presence of the sector

It is becoming less and less useful to gear analyses to dataconcerning Germany alone. This also applies in connectionwith the machine tool industry. After all, in view of theoverall capacity of the sector, German manufacturers’ pro-duction abroad stands for far more than just an “addedvalue”. The analysis of production abroad raises a series of issues. For instance, all sales invoiced by the German headoffice – and thereby previously reported to national statis-tical authorities – must be excluded from consideration.Furthermore, the significance of components and modulesprovided from abroad and of basic machines supplied from

Germany that are then customised abroad and recordedthere separately as sales must be sufficiently clarified.

2011 = VDW-Schätzung* ohne Teile, ZubehörQuellen: StatistischesBundesamt, VDW, VDMA2011 = VDW estimate* excluding parts,accessoriesSources: German StatisticalOffice, VDW, VDMA

Produktion spanender und umformender Werkzeugmaschinen in DeutschlandProduction of metal cutting and forming machine tools in Germany

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 23/84

21

Deutsche Werkzeugmaschinen-Produktion nach Technologien (Mio. eur )German machine tool production by technologies (mill. eur )

%-Anteil %-Veränd. %-Anteil %-Veränd.%-Share %-Change

Jan.–Sept.%-Share %-Change

2007 2008 2009 2010 2010 2010/09 2010 2011 2011 2011/10Laser-, Ionen- und UltraschallmaschinenLaser-, ion beam-, ultrasonic machines

480 469 231 264 2,7 +14 192 253 2,8 +32

ErodiermaschinenElectrical discharge machines

75 74 46 56 0,6 +20 23 29 0,3 +28

Bearbeitungszentren, Flexible SystemeMachining centres, flexible systems

1 542 1 913 1 269 1 081 10,9 –15 6201 137 12,7 +83

Mehrwege-, TransfermaschinenUnit construction machines, transfer machines

465 564 516 453 4,6 –12 345 398 4,4 +15

Drehmaschinen, DrehzentrenTurning machines, turning centres

1 370 1 565 1 062 960 9,7 –10 606 1 011 11,3 +67

Bohr-, Ausbohrmaschinen, komb. Ausbohr- und FräsmaschinenDrilling machines, boring machines, boring-milling machines

188 215 146 162 1,6 +11 109 126 1,4 +16

FräsmaschinenMilling machines 996 1 086 703 668 6,8 –5 456 555 6,2 +22Schleif-, Hon-, Läpp- und PoliermaschinenGrinding, honing, lapping and polishing machines

1 120 1 226 853 710 7,2 –17 405 689 7,7 +70

Verzahnmaschinen, ZahnfertigbearbeitungsmaschinenGear cutting and finishing machines

543 748 619 528 5,3 –15 379 385 4,3 +2

Säge- und TrennmaschinenSawing and cutting-off machines

238 268 145 149 1,5 +3 95 143 1,6 +50

Sonstige spanende WerkzeugmaschinenOther metal cutting machine tools

71 86 50 51 0,5 +0 28 34 0,4 +18

Spanende WerkzeugmaschinenMetal cutting machine tools

7 089 8 214 5 642 5 080 51,4 –10 3 257 4 759 53,1 +46

Schmiedemaschinen und Hämmer (einschl. Pressen)Forging machines and hammers (incl. presses)

88 160 232 299 3,0 +29 217 190 2,1 –12

Biege-, Abkant- und Richtmaschinen (einschl. Pressen)Bending, folding and straightening machines (incl. presses)

505 543 409 384 3,9 –6 260 324 3,6 +25

Scheren, Lochstanzen, Ausklinkmaschinen (einschl. Pressen)Shearing, punching, notching machines (incl. presses)

446 432 328 341 3,5 +4 243 318 3,6 +31

Andere PressenOther presses

623 605 562 578 5,8 +3 412 514 5,7 +25

Drahtbe- und -verarbeitungsmaschinenWire working machines

286 299 211 184 1,9 –13 125 176 2,0 +41

Sonstige umformende WerkzeugmaschinenOther metal forming machine tools

403 462 382 300 3,0 –22 212 313 3,5 +48

Umformende WerkzeugmaschinenMetal forming machine tools

2 352 2 501 2 125 2 086 21,1 –2 1 468 1 835 20,5 +25

Werkzeugmaschinen insgesamtTotal machine tools

9 441 10 715 7 767 7 166 72,5 –8 4 7256 594 73,6 +40

Teile und ZubehörParts and accessories

2 328 2 537 1 623 1 851 18,7 +14 1 2901 630 18,2 +26

Installation, Reparatur, Instandhaltung von WerkzeugmaschinenInstallation, repair, maintenance of machine tools

855 925 788 865 8,8 +10 612 736 8,2 +20

Werkzeugmaschinen inkl. Teile und Zubehör,Installation, Reparatur, InstandhaltungMachine tools incl. parts and accessories,

12 624 14 178 10 177 9 881 100,0 –3 6 6278 961 100,0 +35

installation, repair, maintenance

vorläufigQuellen: Statistisches Bundesamt, VDW, VDMA

preliminarySources: German S tatistical Office, VDW, VDMA

ProduktionProduction

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 24/84

22

muss die Bedeutung aus dem Ausland beigestellter Kompo-nenten und Baugruppen bzw. aus Deutschland gelieferterRumpfmaschinen, die im Ausland veredelt werden unddort separat als Umsatz anfallen, hinreichend geklärt sein.

Die geografische Orientierung am global tätigen Großan-wender Automobilindustrie hat zum Aufbau von Produkti-onsstätten vor allem in Westeuropa (Frankreich, Großbri-tannien, Italien, Österreich, Schweiz), Osteuropa (Tschechien,Polen), den USA und Brasilien geführt. Auch in LändernAsiens, wo die Volksrepublik China die Entwicklung domi-niert, gibt es bereits Standorte mit noch bescheidener, aberkräftig wachsender Ausbringung. Hier steht das Engage-ment noch eher am Anfang, wird aber künftig insbeson-dere in China, wegen verschärfter Local-Content-Anforde-rung und dem gezielten Zurückdrängen von Einfuhrenzugunsten der Eigenproduktionen, zu intensivieren sein.Nahezu alle großen Werkzeugmaschinenhersteller unter-halten einen oder mehrere Produktions- bzw. Montage-standorte im Ausland. Vor dem Hintergrund des mittel-ständischen Charakters der Branche (mehr als die Hälfteder Betriebe beschäftigt höchstens 250 Mitarbeiter) stößtProduktionsverlagerung an finanzielle und personelleGrenzen.

Einmal abgesehen von mehreren hundert Vertriebs- undServiceniederlassungen bzw. Repräsentanzen deutscherWerkzeugmaschinenhersteller in aller Welt, dürften derzeitweniger als 20 deutsche Unternehmensgruppen kompletteAnlagen im Ausland produzieren. Zuletzt sind 51 Produkti-onsstätten in 13 Ländern ermittelt worden. Mit rund 1,1 Mrd.EUR Volumen im Jahr 2010 hat der Teilnehmerkreis einerentsprechenden VDW-Erhebung das in 2009 erzielte Er-gebnis knapp gehalten. Auffällig dabei ist die Heterogenitätder Firmenergebnisse: Während verschiedene meldendeUnternehmen Zuwächse im zweistelligen Bereich ver-

zeichnen, notieren 8 Melder mit teilweise schmerzlichenRückgängen im ebenfalls zweistelligen Bereich.

Der Auslandsanteil, gemessen an der weltweiten Werk-zeugmaschinenproduktion im Teilnehmerkreis, notiert2010 ähnlich wie im Referenzjahr mit 28 %. Dabei stehtEuropa in Bezug auf die regionale Struktur der Auslands-standorte mit 61% Anteil (2009: 62%) und 670 Mio. EURProduktionsvolumen an der Spitze, vor Nordamerika, mitwieder ausgeweitetem Abstand gefolgt von Südamerika(Brasilien) und schließlich den rasant aufschließenden Län-dern Asiens als dritter Region der Triade. Mit Blick auf dieTechnologien entfallen rund 580 Mio. EUR auf spanendeVerfahren, die somit 53 % des insgesamt im Ausland

Geographical alignment to the automotive industry, amajor consumer segment with global operations, has ledto the establishment and expansion of production facilitiesmainly in Western Europe (France, Great Britain, Italy, Austria

and Switzerland), Eastern Europe (Czech Republic and Po-land), the USA and Brazil. Also in Asian countries, wherethe Peoples Republic of China is dominating development,there are already locations where output is still modestbut growing rapidly. Although commitment here tends tobe in its early stages, it will intensify in the future, particu-larly in China, due to heightened local content requirementsand specifically targeting import barriers favouring domes-tic production. Nearly every major machine tool manufac-turer operates one or more production facilities or assem-bly plants abroad. Inasmuch as the sector is predominatedby medium-sized companies (more than half of the busi-nesses employ 250 people or less), financial and staffingconstraints limit production outsourcing.

Apart from several hundred sales and service subsidiariesor branch offices of German machine tool manufacturersthroughout the world, there are probably less than 20German corporations producing complete units abroad atthis time. Recently, 51 production sites in 13 countries wereidentified. With a volume of about EUR 1.1 billion in 2010,

the companies that participated in a related VDW surveybarely maintained the result they achieved in 2009. Theheterogeneous character of the company results herewas striking: While various companies reported two-digitgrowth, eight businesses reported sometimes painfullosses also in the two-digit range.

In 2010, production abroad as a share of worldwide machinetool production was, at 28%, similar among participantsto that of the reference year. Europe led here with regardto the regional structure of foreign locations with a 61%

share (2009: 62%) and a production volume of EUR 670million. Second place North America was followed – at agreater distance again – by South America (Brazil), andfinally by the rapidly encroaching countries of Asia as thethird region of the triad. With regard to technologies, metal- cutting processes accounted for about EUR 580 million,which represented 53% of the total production value gen-erated abroad. Production abroad by manufacturers of metal-forming machines (EUR 510 million) declined muchmore than that of companies specialised in cuttingmachinery.

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 25/84

23

erzielten Produktionswerts reklamieren können. Die Aus-landsproduktion der Hersteller umformender Anlagen(510 Mio. EUR) ist gegenüber der Entwicklung bei denauf Zerspanung spezialisierten Firmen deutlich gesunken.

Spanende und umformende Technologie:Andere Kundenstruktur prägt unterschiedlicheNachfrageverläufe

Als im Zeitablauf üblicherweise recht konstant dürfen dieBeiträge beider Aggregate zur deutschen Werkzeugma-schinenproduktion gelten. Im Zeitraum Januar bis Sep-tember 2011 belaufen sich diese Anteile auf „klassische“72% (4,8 Mrd. EUR) und 28% (1,8 Mrd. EUR). Die für Oktoberbis Dezember ausgewiesene Umsatzentwicklung gemäßVDMA-Indexstatistik (das letzte Vierteljahr der amtlichenProduktionsstatistik liegt noch nicht vor) belegt allerdings,dass die Realisierung von Auftragsvolumen im Umsatzdes Schlussquartals 2011 bei den Herstellern von Umform-technik mit deutlich überproportionaler Dynamik verläuft.Alle Wertangaben beziehen sich hier, wie oben schon aus-geführt, allein auf Werkzeugmaschinen. Die Differenzbe-träge gegenüber den an anderer Stelle genannten Gesamt -volumina verstehen sich als Wert von Teilen und Zubehörbzw. als Umsätze in Dienstleistungen.

Der oft auftretende Phasenversatz zwischen dem Beschaf-fungsverhalten der Automobilindustrie, mit lange vorge-planten Projekten und strategischer Ausrichtung, und derviel stärker konjunkturabhängigen Nachfrage im Mittel-stand kann zu recht unterschiedlichen Verläufen in derProduktionsentwicklung bei umformenden (Großpressen!)und spanenden Werkzeugmaschinen führen.

Das Produktionsgeschehen 2010 belegt dies, mit 8 % Minusfür spanende/abtragende Technologien und lediglich

2 % Minus im Ergebnis für die Umformtechnik. Die erstendrei Quartale 2011 sind weniger geeignet, einen stützen-den Einfluss der Umformtechnik zu unterstreichen. Ins-gesamt 40% Produktionswachstum steht im Bereich derUmformtechnik eine Ausweitung um 25 % gegenüber.Dabei sorgt der zweite Kernbereich der Umformtechnik,die Blechbearbeitung mit und ohne Lasereinsatz, fürüberproportional ausgeprägte Impulse.

Mit technologischem Strukturwandel oder Gefälle in derInnovationsfähigkeit hat der eingeschränkte oder aucheinmal gänzlich ausbleibende Gleichschritt der beidengroßen Werkzeugmaschinenaggregate nichts zu tun!

Metal-cutting and metal-forming technologies: customerstructure variant affects different demand patterns

As usual over time, the two elements of German machine

tool production made essentially constant contributionsto earnings. During the period from January to September2011 they assumed the “classic” proportions of 72% (EUR4.8 billion) and 28% (EUR 1.8 billion). For October throughDecember, however, the turnover trend listed according toVDMA index statistics (the last quarter of official productionstatistics has not been released yet) confirms that themanufacturers of metal-forming machinery clearly demon-strated disproportionately high momentum in the realisa-tion of order volume as turnover in the final quarter of 2011. As already indicated above, all values here relate tomachine tools only. The differences versus the total volumeslisted elsewhere comprise the value of parts and acces-sories or as sales relative to services.

The procurement behaviour of the automotive industry –with its projects planned well in advance and its strategicorientation – often differs sharply from the demand of small and medium-sized companies, which is far moredependent on economic conditions. The resulting phaseshift can create rather different production development

patterns with metal-forming (large-scale presses!) andmetal-cutting machine tools.

Production activity in 2010 confirmed this with an 8% de-crease for metal-cutting/EDM technologies and only a2% decline in the result for metal-forming machinery. Thefirst three quarters of 2011 were less apt to underscoremetal-forming technology’s supportive effect. There was40% production growth in the metal-forming machineryarea overall as compared with 25% expansion. Sheet-metalmachining (with and without the use of lasers), the second

core area of metal-forming technology, provided dispro-portionately strong momentum here.

The partial or even total dissimilarity in performancebetween the two major machine tool segments hasnothing to do with structural transformation of technol-ogy or diminished innovative capacity!

ProduktionProduction

8/15/2019 The German Machine Tool Industry in 2011

http://slidepdf.com/reader/full/the-german-machine-tool-industry-in-2011 26/84

24