Embed Size (px)

Citation preview

INVESTOR RELATIONSCorporate Planning Division, Samsung Fire & Marine Insurance. Co., Ltd.

Samsung Insurance Bldg. 87, Euljiro -1ga, Jung-gu, Seoul, Korea, 100-782

E-mail: [email protected]

Telephone: 82-2-758-7535

Facsimile: 82-2-758-7831

View our interactive on-line annual report at

ir.samsungfire.com

We always care our customers and shareholderswww.samsungfire.com http://ir.samsungfire.com

This report is printed on an Fsc certified paper in Soyink

THE GLOBAL PIONEERA n n u a l R e p o r t 2 0 0 8

PROFILE

01 CORPORATE OVERVIEWMESSAGE FROM THE CEO

CORPORATE DIRECTORY

02 CORPORATE STORYVISION & STRATEGY

BRAND STRATEGY

HIGHLIGHTS

2008 AWARDS

03 REVIEW OF OPERATIONAUTOMOBILE INSURANCE

LONG-TERM INSURANCE

COMMERCIAL INSURANCE

ENTERPRISE RISK MANAGEMENT

04 SUSTAINABILITY MANAGEMENTETHICAL & ENVIRONMENTAL MANAGEMENT

CORPORATE COMMUNITY RELATIONS

SPORTS

CULTURE

05 FINANCIAL SECTIONMD&A

FINANCIAL STATEMENTS

WORLDWIDE NETWORK & SAMSUNG AFFILIATES

12

15

Corportate

Story

20

22

24

26

30

32

34

36

41

50

102

Contents

An

nu

al Rep

ort

20

08

TH

E G

LOB

AL P

ION

EE

R

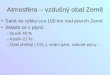

18,490

20,741

23,092

06FY FY FY07 08

Total Assets(In billions of Korean Won)

Net Profit(In billions of Korean Won)

06FY FY FY07 08

341

477

599

SF&MI realized a a record-high pre-tax profit for the fiscal year. Net profit totaled KRW598.7 billion, which was secondto none in the industry. Direct premiums written were up 6.4% year-on-year to KRW9,744.9 billion, net profit climbed by25.6% to KRW598.7 billion, and adjusted net profit including an increase in catastrophe reserves jumped 27.2% toKRW671.3 billion. Total assets grew 11.3% to KRW23,092.2 billion while catastrophe reserves increased 7.3% toKRW1,059.3billion.

Financial Hightlights

Direct Premiums Written

Increase in Catastrophe Reserves

Investment Profit

Operating Profit

Adjusted EPS (in KRW)

6.4%

41.5%

14.9%

18.4%

31.2%

Summary ofIncome Statements(In billions of Korean Won)

Summary ofBalance Sheet(In billions of Korean Won)

9,74573

888856

15,408

Cash & Equivalents

Stocks

Real Estate

Total Assets

Total Liabilities

Total Liabilities andShareholders’Equity

5.2%

-2.8%

4.9%

11.3%

11.0%

11.3%

5961,9751,088

23,09219,22923,092

102/10305.3 Worldwide Network & Samsung AffiliatesSamsung Fire & Marine Insurance Annual Report 2008

SAMSUNG AFFILIATES

Samsung Fire & Marine Insurance Co., Ltd.

has affiliates in the Samsung Group which includes the below companies.

Finance

Samsung Fire & Marine Insurance Co., Ltd.

Samsung Life Insurance Co., Ltd.

Samsung Card Co., Ltd.

Samsung Securities Co., Ltd.

Samsung Investment Trust Management Co., Ltd.

Samsung Venture Investment Corporation

Other Samsung Companies

Samsung Corporation

Samsung Engineering Co., Ltd.

Cheil Industries Inc.

Samsung Everland Inc.

The Shilla Hotels & Resorts

Cheil Communications Inc.

S1 Corporation

Samsung Lions

Samsung Medical Center

Samsung Economic Research Institute

Samsung Advanced Institute of Technology

Samsung Foundation of Culture

Samsung Welfare Foundation

Electronics

Samsung Electronics Co., Ltd.

Samsung SDI Co., Ltd.

Samsung Electro-Mechanics Co., Ltd.

Samsung Corning Co., Ltd.

Samsung Corning Precision Glass Co., Ltd.

Samsung SDS Co., Ltd.

Samsung Networks Inc.

Chemicals

Samsung Total Petrochemicals Co., Ltd.

Samsung Petrochemical Co., Ltd.

Samsung Fine Chemicals Co., Ltd.

Samsung BP Chemicals Co., Ltd.

Machinery

Samsung Heavy Industries Co., Ltd.

Samsung Techwin Co., Ltd.

The Global Pioneer

SF&MI aims to be the best property/casualty insurance in the 21st century. It willachieve this goal with a customer-oriented attitude and unmatched financialsoundness. SF&MI is undisputed No.1 non-life insurance company in Korea interms of size, financial condition and management practices. We have partneredwith leading global insurance companies by actively expanding all around theworld, including the U.S., Europe, Indonesia, China, Japan and Vietnam, so as toachieve steady growth and become a global competitive financial serviceprovider. SF&MI will continue efforts to strengthen its competitiveness byadopting advanced financial skills, enhancing product development capability andinnovating insurance marketing practices.

The corporate values of SF&MI stem from distinct strategies and passionate “newpioneer” spirit for the benefit of our customers. SF&MI is undeniably the finestinsurance company in Korea, which always provides high quality insurance servicewith the first priority being put on its customers and complies with regulations andstandards to set an example of honest and responsible business practices.

Card ofPioneer

01

We will be a global financial service provider that

ushers the world into a better future.

Global Power

year1978

15

The first-ever overseas office

SF&MI opened its first overseas office in London on May 25,1978. It was a bold and preemptive move for a Korean financialcompany at that time. It also opened an office in Indonesia in1997 and in Vietnam in 2003, and established a local subsidiaryin China in 2005 for the first time as an insurance companyaround the world.

Locations World-Wide

SF&MI, after planting its flag in London, has opened offices andlocal subsidiaries in 15 regions in eight countries including theU.S., China, Japan, Indonesia, India, Singapore and Vietnam. Indoing so, we have geared up to be the No. 1 financial group notonly in Korea but in the global marketplace.

We are committed to growing as an exemplary and ideal company that

can be a role model for others around the world.

Global Standard

25.2%

A+

year-on-year growth in net profit in 2008.

SF&MI posted KRW598.7bill ion or a 25.2% year-on-yearincrease in net profit in 2008, which was the highest record in thecompany’s history. As a result, the company’s total assetstopped the KRW21,000 billion mark, further fueling its growthengine to become a global player.

A.M. Best Company for Seven Years in a Row Ratingfrom S&P for Six Consecutive Years

SF&MI earned a seventh straight A+ (Superior) rating from A.M.Best Company, a world- renowned insurance rating andinformation agency. We also received an A+ rating from S&P forsix years in a row. Such recognition is clear evidence that we area globally competitive financial firm.

We will make the world a better place for

everyone rather than merely indulging in profit taking.

Global Mind

126 126 guide dogs from the SF&MI guide dog schoolhave been donated for the blind

SF&MI’s guide dog school is the only one in the world that issponsored by a private business. For its valuable efforts, theschool received an official certificate from Korea’s Ministry ofHealth and Welfare. Since donating the first guide dog in 1994, ithas provided guide dog training programs two or three times peryear. So far, 126 guide dogs have been donated, and 54 of themare currently helping blind people.

336 336 children of traffic accident victims are providedwith support for living

Since 1993, SF&MI has supplemented the living costs of primary,middle and high school students who lost their parents in trafficaccidents. We also have provided gifts upon their entrance toschool or on national holidays. As many as 234 such childrenhave grown up to become responsible members of our society,and another 102 are currently provided with assistance fromSF&MI.

Message from the CEO

We sincerely thank our shareholders for their continued support and

encouragement in this unprecedented time of global economic hardship.

Corporate Overview

To Our Shareholders:

With the early summer heat building to a crescendo, two months have passed since fiscal year 2009 began. In fiscal 2008, a

global economic cataclysm reverberated around the world. The spill-over of the credit crisis that started in the U.S. was felt in

global financial markets and on Main Street. Domestically, we also suffered from declining exports, reduced consumption,

unemployment, and foreign exchange and stock market volatility.

It was a turbulent year for the industry, as well, as competition tightened due to diversification of sales channels with the cross-

selling of life and non-life products. Price competition also intensified with e auto insurers.

Nevertheless, despite such difficulties, Samsung Fire and Marine Insurance (SF&MI) reported earnings of KRW9,744.9 billion in

direct written premiums, up 6.4% from the previous year, and an increase of KRW122.2 billion in net profit as we reached a

record profit of KRW598.7 billion.

Total assets soared to KRW23,092.2 billion, up KRW2,351.7 billion from last year, and catastrophe reserves surged 41.5% to

KRW72.6 billion, adding to the robustness of our financial condition.

On top of this, SF&MI has enjoyed a rating of A+ from S&P for six straight years, a testimony to the strong financial soundness

and credit worthiness of the company. We are the only financial firm in the country to have been ranked first for eight years in a

row in the National Consumer Satisfaction Index (NCSI). Built on the company’s excellence in business, we have also been

committed to fulfilling our social responsibilities of sharing what we have with our neighbors in need. To this end, we have

assisted the children of traffic accident victims, donated guide dogs for the blind, partnered with rural communities, and raised

donations through the “KRW500 Gift of Hope” fund, a voluntary initiative of risk consultants (RC) to improve the living conditions

of people with disabilities.

My Fellow Shareholders,

In fiscal 2009, it is considered unlikely that the global economy will experience a strong rebound from financial instability and the

economic downturn.

The local insurance industry is also expected to be mired in a vicious cycle, in which corporate restructuring and a decrease in

disposable income will force people to reduce consumption and investment. This could lead to fewer new insurance contracts

being signed and possibly, even to the surrendering of existing policies. At the same time, competition among insurers will

become fiercer with implementation of the Capital Market Consolidation Act, changes in regulations, diversification of sales

channels and the breaking down of barriers between areas of business.

2010

쪾Solidify foundation for profitability쪾Improve direct communication

channel

쪾Strengthen core business areas

2015

쪾Improve business structure쪾Attain sound profit structure

쪾Become an outstanding globalfinancial institution

2020

쪾Expanding business areas쪾Attain advanced

competitiveness in the financialmarket

쪾Attain global capability

SYSTEMATICAPPROACHSTRATEGY

12/1301.1 Message from the CEOSamsung Fire & Marine Insurance Annual Report 2008

June 4, 2009

DaeSub Chi

President and CEO Samsung Fire & Marine Insurance

In response, with a new pioneering spirit full of passion, enthusiasm and the pursuit of excellence, SF&MI has set clear priorities to

continue its march to the top in the global marketplace.

First, we will be committed to enhancing our global competitiveness to keep abreast of globalization.We aim to compete with global players by training our staff professionals in the knowledge and skills required to compete at the

global level and to have global perspectives, while upgrading our existing capacities to global standards. Utilizing our core

competencies, we will go beyond the already saturated domestic market to seek new growth engines in wider markets.

Second, we will build enduring corporate value by securing cost competitiveness.The insurance industry will not be immune from the economic turmoil roiling the world’s markets. We may face challenges such as

decreases in profitability and new contracts, but through a sobering reality check, the management and employees of SF&MI will

work for comprehensive improvement and innovation in sales, compensation, underwriting, risk management, asset management,

and sales channels. We will also seek to reduce costs so as to gain a distinct competitive edge in terms of pricing that cannot be

duplicated by others. With the launch of new services and products such as the company’s “My anycar”online auto insurance,

introduced in March, we will strengthen our leadership position in the industry and lay a foundation for becoming a global leading

company in every aspect.

Third, we will turn the crisis into new opportunities while remaining honest and sincere with our customers.Our clients are the root of the company’s existence and are the reason SF&MI is here. The best way to turn the crisis into new

opportunities in these troubling times is to put ourselves in the customers’ shoes. In initiating each and every managerial activity, we

will place a top priority on building customer confidence and customer satisfaction. We will work to the best of our ability to

continue exploring new markets, develop new products, and enhance the competencies of our employees, thus maximizing

customer satisfaction and strengthening the company’s platform for future growth.

In fiscal 2009, as in the past, SF&MI employees will be creative contrarians with a mindset based on the concept, “From crisis comes

opportunity.” SF&MI’s employees have the passion, confidence and spirit to take up the challenge of creating excellence as the

company seeks to join the ranks of the world’s top financial firms in the 21st century.

To make a more promising future for the company, we need and ask for your continued support and guidance. As we look to a brighter

future for the company, I wish you and your family the all the best in happiness and success.

Sincerely,

Corporate Overview

President & CEO

쪾DaeSub Chi

Executive VP

쪾YongAm Yoon쪾HyungMo Yoon 쪾kyeHa Lee쪾SungZin Lim

Outside Director

쪾YoungChul Kim쪾KangJung Kim 쪾WonChang Lee 쪾HeonCheol Shin

Senior Vice President

쪾MoonPyo Chae 쪾JaeHo Nam 쪾NamKu Yoh 쪾YoungSoo Cha 쪾JaeHong Park 쪾JongSung Rhee 쪾HaiSun Hwang 쪾TaeHwan Kim쪾YoungChang Ko

Vice Presidnet

쪾YoungHwan Cho쪾KeeChul Shin 쪾JungIl Park쪾EuiHyeon Kim쪾HoKyung Bae쪾YounGil Kim쪾SungJun Kim 쪾SunSeol Hwang 쪾WonGwyn Jang쪾JeongCheol Kim 쪾DaeKyung Kim

Vice Presidnet

쪾HoeYong Jung 쪾TaeMyung Kwon 쪾YoungMoo Choi 쪾JongWoo Kim쪾JungBin Ko쪾YoungKap Choi쪾SeongGyu Kim쪾HoonTaek Oh쪾HagGeun Whoang쪾ByungSeok Choi 쪾YangHee Lee

Vice Presidnet

쪾SukHan Lee쪾ChoonWeon Park쪾Beom Lee쪾HyungKoo Kang쪾SangKyung Lee쪾HyunJun Jeong쪾YouSang Kim 쪾KiJae Seong쪾ByungHo Chun

* Current executives as of July 31, 2009

Auditing Diresctor

쪾GwangKi Son

CorporateDirectory

14/1501.2 Coporate DirectorySamsung Fire & Marine Insurance Annual Report 2008

Journey as a Pioneer

02

The journey of SF&MI is a living witness of the history of Korea’s insurance industry. To fulfill its responsibilities and obligations as the nation’s leading insurer and, above all,to set an example in our society, SF&MI takes a meaningful step forward every day.

★

Earned an A+ (Superior) rating from A.M. Best Company forseven consecutive years

★ Received an A+ (Stable) rating from S&P for six straight years

★ Ranked 1st in the National Customer Satisfaction Index (NCSI)for eight years in a row in 2008

★ Ranked 1st in the Non-Life Insurer category of the KoreaStandard-Service Quality Index (KS-SQI) for seven straightyears in 2008

★ Ranked 1st in the auto insurer category in the KoreaCustomer Satisfaction Index(KCSI) for 11 consecutive yearsin 2008

★ Received the Grand Prize of the Korea Service Awards for sixyears in a row in 2009

★ Received the Grand Prize of the Korea Customer SatisfactionManagement Awards for three consecutive years in 2008

★ Honored as the Best Insurance Company for the twoconsecutive years in 2008 by the Korea Insurance ConsumerFederation

★ SF&MI Chinese subsidiary obtained an A rating from S&P in2008

CorporateStory

2008 Awards

June 24“KRW 500 Gift of Hope” fund donates study room forhospitalized children

SF&MI risk consultants (RC) and sales outlets raised money and opened anew study room, named “Nuribom Class,” at a school in the HanyangUniversity Hospital for children undergoing long-term hospitalization to treatcancer and other diseases. The fund also paid for the refurbishment of thehouse of a child attending the hospital school. The study room and the homerefurbishment were the 53rd and 54th projects of the “KRW 500 Gift of Hope”fund, a voluntary initiative of RCs who seek to improve the living conditions ofpeople with disabilities.

July 17Branch opens in Suzhou, China

In an effort to strengthen sales in China, SF&MI’s Chinese subsidiaryestablished a triangular sales network linking its branches in Suzhou, Beijingand Shenzhen. The company now provides upgraded and tailored insuranceservices to Korean businesses, expatriates and foreign corporations in theHuadong region, a key center for China’s rapid economic growth.

December 16Ceremony held for donation of five guide dogs to the blind

A ceremony attended by 60 persons included SF&MI CEO DaeSub Chi, fiveblind people to receive guide dogs and volunteers who had trained the dogsfor a year. The dogs were handed over to five blind persons including Mr.

KIM Sang Joon who, despite his disability, studied social welfare in collegeand is now helping other disabled people to receive job training and stand ontheir own feet. The dogs are expected to be new and great guiding eyes indaily lives of the blind people. SF&MI is determined to continue guide dogsdonation as a vital part of the company’s social responsibility programs.

November 21FP Center opens for the first time in the industry

SF&MI became the first non-life insurance company in the country to open aFinancial Planning (FP) center. It offers a “comprehensive asset manage-ment service” and an “Financial Advisory Service” for its VIP customers and a“corporate risk-management service” to CEO customers. The center boastsa top level advisory group composed of the nation’s most renowned CFPs,lawyers, tax attorneys and real estate specialists. VIP customers are providedwith one-on-one comprehensive asset management service which goes farbeyond simple risk management. The service includes inheritance,disposition, tax-saving, possession of real property, asset allocation, financialinvestment, legal advices and etc.

Samsung anycar, the Finest Auto Insurance in Korea.

In 2002, SF&MI’s “anycar” was launched as the first branded auto insurance in Korea. It has since earned an undisputedleadership position in the industry through proactive communications with clients, and is hailed as a new, viable model ofbrand development and improvement of customer service for financial companies.

“anycar” was the first consulting-type auto insurance in Korea. It is a customized auto insurance service designed by aspecialized consulting and sales force, known as risk consultants (RC). In addition, to reinforce the leadership of thebrand, we have maintained the largest compensation network in the industry enabling the speediest settlement of claims.More than a mere insurer, we aim to be an “auto life consultant” that takes care of every aspect of car ownership andusage.

We are extending our services to bring about a full spectrum of benefits to our customers even on a global level. Forinstance, we recently signed an agreement with Farmers Insurance Group, a Los Angeles based automobile insurer, toensure that anycar’s premium customers can enjoy the same level of benefits in the U.S.

Allife- From Life to Living, All That You Need

When the line between life and property/casualty insurance has been blurred because of the diversification of saleschannels and convergence of insurance products, long-term insurance can be a key growth engine for a non-life insurer.

Allife was launched in September 2005 with an aim to strengthen our competitiveness by renewing our brand leadershipin the long-term insurance market.

Allife, a portmanteau of the words, “All, Always+Life,” means that it will cover all forms of disaster in life such as disease,accident, fire, property loss and general liability.

In other words, Allife’s inherent strength as a long-term, non-life insurance is that it insures against not only death andincurable diseases, but also minor illnesses, property damage, nursing costs, and after-retirement living costs, as well asmisfortunes that may strike parents or children in everyday life.

We introduced a new term, “living insurance,” in the industry to help our customers better understand our services whileincreasing brand recognition with the promotion of the concept, “From Life to Living.”

SF&MI’s family of brands, “anycar” is a leading automobile insurance, and “Allife”is a premier long-term insurance.

“anyhome” is a new general insurance product targeted at individual customers. This product adds to SF&MI’s well-defined hierarchy of products and brands.

Samsung Fire & Marine Insurance is taking steps toward becoming a world classfinancial services conglomerate

STRENGTHENING THE CORE COMPETENCY

Meet the demands of the rapidly evolving market and develop adif ferent iated status in areas of core competency throughstrengthening profitability in existing business areas and securing corecompetency for the future.

- Strengthen insurance competency (products, underwriting,reinsurance)

- Organize direct communication sales channel and cultivatefinancial consulting skills

- Strengthen the compliance system

DIVERSIFICATION OF BUSINESS AREAS

Leverage core competency to diversify into new markets andstrengthen overseas competency in preparation for competition withnon-financial and global players, such as banks, securities and lifeinsurance companies.

- Improve asset management

- Introduce new risk management competency (health, retirement,group)

- Strengthen global business competency

Strategies

COMPREHENSIVE FINANCIAL SERVICES COMPANY

Through differentiated competitiveness and various business areas weaim to become a total finance service company that provides acombination of high quality services to clients in the areas ofinsurance, finance and additional services

- Achieve economy of scale through mergers

- Pursue competitive multi-channel structure

- Provide total risk solutions that cater to clients’ needs

Vision Samsung Fire & Marine Insurance will strive to strengthen its core competency to secure a broad profit base anddiversify into other business areas to become a leading global corporation.

2008

January 23Seventh straight A+ (Superior) rating from A.M. Best Company

SF&MI earned the highest possible A+ rating (Superior) for the seventhconsecutive year from A.M. Best Company, one of the largest insurancerating and information agencies in the world. A.M. Best Company reviewedSF&MI’s operations thoroughly, with a special focus on our capital capacity,profit-centered strategies and risk-management capability. As a result, wereceived a “Superior”grade in financial soundness, profitability, safety andpayment capacity.

February 2English camp for the children of premium customers

SF&MI held a winter vacation English camp for the children of its premiumcustomers at the SF&MI Human Resource Training Center in Yuseong,Daejeon city. A total of 100 elementary, middle and high school studentsparticipated in the program which offered them abundant opportunities toimprove their English as they spoke only in the international languagethroughout the four-day program with native English teachers from Australia.

February 17Launch of the Internet auto insurance serviceSF&MI initiated a change in its sales practice to attract customers in their 20sand 30s by introducing a new type of auto insurance. “My anycar” autoinsurance, on sale only on the company’s Internet website, www.myanycar.com,offers 15% lower premium rates than existing “anycar” insurance. Though the

rates are lower, the Internet insurance provides the same compensationservice, emergency road service, and “anycar land” network service asexisting SF &MI products.

February 26Opening of the 4th branch of the Chinese subsidiary inQingdaoThe branch office in Qingdao is the fourth sales office of SF&MI’s subsidiaryin China, following the opening of branches in Beijing (2006), Shenzhen(2008) and Suzhou (2008). The Qingdao office will focus on sales ofcorporate insurance products that target Korean businesses and expatriates,as well as foreign corporations in the region. It also will provide high qualityand tailored insurance services as well as an upgraded and com-prehensiverisk management to our corporate customers in China. SF&MI is poised tosharpen its competitive edge in the global insurance market by implementingbusiness strategies aimed at increasing sales networks in China based onthorough market research and analysis.

April 2Singapore office opensSF&MI held a ceremony to open its office at the Samsung Hub Building onChurch Street in Singapore. The Singapore office is responsible for studyingthe insurance market in Singapore, exploring new business opportunities andpromoting partnerships with aforeign insurers and reinsurance companiesbased in Southeast Asia.

2009

HighlightsBrand StrategyVision & Strategy

Group Brand

auto insurance long-term insurance others

Independen Brand

- Economic plan

- VIP plan

- Weekend/Leisure Plan

Family Brand

Brand Modifier

- Allife Health PartnerInsurance for theElderly

- Allife TOP DriverInsurance

- Allife NewBusiness Insurance

- All kinds of long-term insurance andpension products

Coporate Brand

New Channel Products

1950sJanuary 26, 1952Founded as Anbo Fire & Marine InsuranceCo., Ltd.

1960sJanuary 31, 1963Acquired Ankuk Fire & Marine InsuranceCo., Ltd.

March 2, 1963Company name changed to Ankuk Fire &Marine Insurance Co., Ltd.

1970sJune 1, 1975Initial Public Offering

February 24, 1978Opened offices in Masan, Dongbu (east),Nambu (south)

February 4, 1979Established a risk management institute-afirst among Korean non-life insurers

1980sOctober 1, 1983Launched auto insurance division

September 1, 1985Opened office in New York (U.S.)

October 17, 1987Construction of head office building completed

May 26, 1989Increased capital to KRW8.4 billion

1990sFebruary 10, 1990Increased capital to KRW10.0 billion

March 17, 1990Increased capital to KRW 11.7 billion

April 1, 1990Opened branch in U.S.

May 29, 1990Increased capital to KRW12.8 billion

April 1, 1992Opened Seoul Customer Service Center

March 26, 1993Selected as domestic lead manager forKoreasat Insurance

November 29, 1993Opened Jakarta office (Indonesia)

2000sJanuary 30, 2000Increased capital to KRW25 billion

May 30, 2000Paid dividend on account of capital increase

April 24, 2001Opened branch in Shanghai (China)

July 1, 2001Established Samsung Traffic SafetyResearch Institute

December 31, 2001Selected as one of Asia’s “Top 200Companies” by the Far Eastern EconomicReview, a Hong Kong-based political andeconomic weekly magazine

July 10, 2008Opened Suzhou office of China subsidiary

November 20, 2008Opened the first FP Center in the industry

December 12, 2008Opened office in Singapore

2009February 26, 2009Opened Qingdao office of China subsidiary

March 3, 2009Launched Internet auto insurance service

December 6, 1993Company name changed to Samsung Fire & Marine Insurance Co., Ltd.

January 10, 1994Opened office in Tokyo (Japan)

May 9, 1994Opened Yuseong Training Center

Oct, 1994Launched Social Service Team of SF&MI

April 20, 1995Opened Beijing office (China)

July 15, 1995Opened office in Ho Chi Minh City (Vietnam)

August 28, 1996Opened office in Hanoi (Vietnam)

September 20, 1996Opened office in Shanghai (China)

November 7, 1996Established a local subsidiary in Indonesia

April 4, 1998Increased capital to KRW 14.8 billion

October 15, 1998Established Samsung Fire & MarineInsurance Claim Adjustment Service Co., Ltd.

January 19, 1999Increased capital to KRW 20.0 billion

July 3, 1999Stock split to KRW500 per value

January 18, 2002Declared 2002 as the first year for “SamsungFire & Marine Insurance Ethical Management”

January 26, 2002Unveiled time capsule in commemoration of the50th anniversary of the company

April 2, 2002Launched Samsung “anycar” auto insurancebrand

April 26, 2002Won the “Most Respected property/casualtyInsurer Award” at “The First in Korea” awardssponsored by Korea Minting and SecurityPrinting Corporation

November 14, 2002Established “Samsung Vina Insurance CompanyLimited (SVIC)” as a local subsidiary in Vietnam

March 26, 2003Selected as the “fairest trader” by KoreaFair Trade Commission

May 26, 2003Opened office in Qingdao (China)

December 10, 2003Launched Samsung Super Insurance, theindustry’s first integrated insurance product

December 30, 2003Signed an MOU for Cooperation andExchange with China Price InformationNetwork, a Chinese insurer

August 19, 2004Introduced “Socially Contributing Brand” a first in the industry

August 19, 2004Changing its name into “Samsung AnycarSocial Service Team”

January 3, 2005Opened Samsung Loss Control Center,the first of its kind in the history of theprivate sector

April 25, 2005Established Samsung Fire & MarineInsurance (China), the first local subsidiaryestablished by a foreign insurer in China

July 22, 2005Opened office in London (U.K.)

September 30, 2005Launched “Allife” as a flagship brand forlong-term insurance

February 27, 2006Renewed the 2006 Samsung anycarVolunteer Group

April 4, 2006Introduced the slogan “Living Insurance” inlong-term insurance

July 27, 2006Opened Beijing office of China subsidiary

November 27, 2006Unveiled the Metro Pole 50, a neon sculpture

November 29, 2006Won “Presidential Award” at “Korea BrandAwards”

December 12, 2006Received “Presidential Citation” at the Firstand Foremost Movement for Persons withDisabilities Awards

December 20, 2006Won “Presidential Award” at the “DigitalKnowledge Management Awards”

January 9, 2007Samsung Traffic Safety Research Institute(STSRI) received “Samsung Award of Honor”

January 18, 2007Named an “Asian Fab 50” company in theAsia Pacific Region by Forbes

February 21, 2007Opened Railroad Wing at the SamsungTransportation Museum

December 21, 2007Opened Shenzhen office of China branch

Corporate Historysee the widest 촻

SF&MI’s philosophy is embedded in all of the company’s insurance products-a principlethat customers are our first priority in any case and a promise to deliver top-level servicethat surpasses anything our competitors offer

PioneeringPhilosophy

03

Review of Operation

1 AUTOMOBILE INSURANCE2 LONG-TERM INSURANCE3 COMMERCIAL INSURANCE4 ENTERPRISE RISK MANAGEMENT

2,760.4

3,112.3

Direct Premiums(In billions of Korean Won)

FY2008FY2007

FY2006

SF&MI, with its “anycar”auto insurance brand, is the one and onlyfinancial company in Korea ranked first in the Korean Customer SatisfactionIndex (KCSI) for 11 straight years.

28.0%

Market Share :

MoonSeog So I Senior Manager

Review of Operation

3,060.5

FY2006

Auto insurance market in 2008 and SF&M’sstrategies and results

Undeterred by rapidly changing market conditions such asthe diversification of sales channels, we maintained a healthymarket share of 28.0% in the auto insurance industry in fiscal2008. With a 2% growth in the market share of online autoinsurance from 16.4% in 2007 to 18.4% in 2008, SF&MIentered the market with its own online auto insurance servicein March 2009. This will enable us to build a strongerpresence in the online market in the future.

In an effort to strengthen our profit structure, we introducedmodel-specific rates and profit-oriented pricing policies,which resulted in a loss rate of 67.2% in 2008.

Implement pricing policy reflecting actual cost

In the face of rapid growth of the online insurance market, wedid not take refuge in price competition. Rather, we havemaintained a pricing policy that reflects the actual costs indelivering quality products and services to customers.Premiums are determined by the risk factors of eachcustomer to ensure fairness for all customers while a positiveand advanced underwrit ing (U/W) system has beenstrengthened.

Strenghten competitiveness through productdifferentiation

We have a wide range of differentiated products that enableus to strengthen sales competitiveness and introduceproducts tailored to each customer. For example, our anycarFamily Service, launched in August 2008 to provide freemaintenance and repairs at auto service centers associatedwith SF&MI, was hailed by our customers. Such innovationhas led anycar to top the Korean Customer SatisfactionIndex (KCSI) for 11straight years, the only brand of a financialcompany to do so.

Reinforce car accident prevention programs

Recognizing our social responsibility to seek a reduction incar accidents, the Samsung Traffic Safety Research Institute(STSRI) was founded in July 2001. In 2008 alone, theorganization implemented a total of 148 publicity programs.

In addition, since 2006, we have produced and airedprograms introducing the best road traffic safety practices inother countries in partnership with a major TV station inKorea.

We also provide road safety training to 12,000 mothers ofprimary school students every year. As “honorary road safetyteachers,” the parents ensure the safety of their children onthe way to and from school. To support the road safetyinitiatives of local authorities, we conduct safety assessmentsof roads in medium- and small-sized cities as well as ofroads in downtown areas.

The business outlook for 2009, strategies and plans

With the growth of the online auto insurance market, SF&MIbegan its own online auto insurance service in March 2009.This service, along with our already strong face-to-face saleschannels, is expected to solidify the company’s leadingposition in the market.

We will continue to focus on profitability that reflecting theloss ratio and costs of doing business in our pricing. Thus wewill maintain realistic pricing and refrain from aggressive pricecompetition, while offering high quality products and servicesthat cover actual costs. This will enable us to build a stableand sustained profit-loss structure.

We also upgraded the insurance terms of use with expressionsthat are more easily understood by our customers, and willintroduce more products differentiated and catering to thevarious needs of customers. In addition, in the event that anyof our policyholders move to the U.S., we are working tohave their accident-free records recognized by U.S. insurers.In doing so, we will make anycar the most trusted autoinsurance among sales forces as well as customers.

In the last year, the STSRI increased the number of TVprograms about traffic safety practices in foreign countries toraise awareness of road safety and encourage thegovernment to invest more in relevant infrastructure.

We will continue our efforts to increase the profitability of autoinsurance while remaining true to our quest for excellence asa leading company in the industry.

SF&MI, with its “anycar” auto insurance brand, is the one and only financialcompany in Korea ranked first in the Korean Customer Satisfaction Index (KCSI) for11 straight years.

20/2103.1 Automobile InsuranceSamsung Fire & Marine Insurance Annual Report 2008

4,545.9

5,089.6

5,576.8

Direct Premiums(In billions of Korean Won)

FY2008FY2007

FY2006

insurance market by developing

products and underwriting policies in

a systematic and strategic manner.

Despite the

unfavorable market

conditions, SF&MI

realized sustained growth

in the

27.9%Market Share :

long-term

HyoEun Jang I Associate

Review of Operation

Long-term insurance market in 2008 and SF&MI’sstrategies and results

Since the global financial crisis began in 2008, there hasbeen possibility of a prolonged economic downturn andfinancial market volatility. The implementation of the CapitalMarket Consolidation Act is expected to break down barriersbetween business areas of financial companies and intensifycompetition in the industry. The insurance industry isundergoing a number of changes in its managementenvironment, including the crossselling of life and non-lifeproducts, the implementation of long-term nursing insurancefor the elderly as well as diversification of sales channelssuch as bancassurance, GA and mail order.

Maintain leadership in the market through sustainedgrowth based on strong profitability

Despite the unfavorable market conditions, SF&MI realizedsustained growth in the longterm insurance market bydeveloping products and underwri t ing pol ic ies in asystematic and strategic manner. At the same time, we havesecured profitability through sophisticated risk and profit/lossmanagement. To cope with the rapidly changing environmentin the financial market, we have sought new growth enginesthat can maximize customer values and provide the mostsuitable products for each sales channel with an aim toachieve balanced growth of all sales channels.

Enhance and leverage core competencies of long-term products

The long-term insurance of SF&MI is an important source ofcurrent and future revenue. Therefore, we have strengthenedefforts to stand tall in this field by developing new products,improving underwriting skills, optimizing our product portfolioand enhancing our compliance system. We also establisheda scientific and systematic statistical system to maintainproper risk rate, and a policy-renewal system to increasevalue for our customers and shareholders.

Strengthen strategies to deal with sales channeldiversification

We are focusing on developing products with an ideal fit foreach sales channel and differentiating sales strategies inresponse to the diversification of sales channels-for example,cross-selling of life and non-life products, GA and mail order.

We are committed to providing distinct products to eachcustomer and sales channel through a careful analysis of thecompetitiveness of each sales channel and the intensity ofcompetition in the market.

2009 outlook, strategies and plans

It appears that the economic downturn caused by the globalfinancial crisis will continue into this year. In the insuranceindustry, small and medium insurers are expected to addprice competition to the market with low-premium productsand rate cuts through diversified sales channels such asbancassurance, GA and mail order. Furthermore, the industryis bracing for a series of changes in the regulation of thepayment of medical costs borne by policy holders and theprovision of detailed product information.

Given this background, we will put in place long-terminsurance sales strategies that seek to sustain M/S growthbased on a stable profit/loss structure. We will analyzecustomers’ needs thoroughly, and develop and provideproducts from their viewpoints. We will develop products andmarketing methods that fully reflect the needs and purchasepatterns of our customers. In doing so, we will provideproducts that are highly responsive to the changing needs ofour customers and the market while maintaining our marketleadership.

We will be creative as we venture into new marketplaces,and develop innovative products and services. We also willconduct more precise and systematic analysis of risk rates toimprove our cost competitiveness.

Long-term insurance plays a key role in ensuring the company’s revenues andfuture profitability. Systematic and strategic product development paves the wayfor steady and long-term growth of our insurance business.

22/2303.2 Long-term insuranceSamsung Fire & Marine Insurance Annual Report 2008

29.3%

Operating profit from

KRW 40.3 billion over the

year to KRW 151.9 billion,

not with standing falling

premium rates in the

reinsurance market,

steep hikes in foreign

exchange rates and

a subsequent increase

in foreign currency O/S

commercialinsurance surged by

Market Share:

SeonGeel Seo I Manager

936.2

958.71,107.6

Direct Premiums(In billions of Korean Won)

FY2008FY2007

FY2006

Review of Operation

Commercial insurance market in 2008 and SF&MI’sstrategies and results

In fiscal 2008, revenue from commercial insurance reachedKRW1,107.6 billion, up 15.5% from the previous year.Operating profit surged by KRW40.3 billion over the year toKRW151.9 billion, notwithstanding falling premium rates inthe reinsurance market, steep hikes in foreign exchangerates and a subsequent increase in foreign currency O/S.

Such results are all the more remarkable given that one ofour rival companies posted an operating profit of negativeKRW118.1 billion. Our fine results can be attributed toSF&MI’s thorough risk analysis, strong managementcapacity, and retention of profitable policies.

To this end, we continued with professional training and riskanalysis to bolster our consulting-type sales, adopted in2007, in pursuit of service differentiation and competitiveadvantage. Innovations in management practices wererealized in scientific risk analysis, in the use of scientific andstat ist ical databases in decision-making and in theenhancement of infrastructure.

As for our overseas operations, we opened offices inQingdao in February 2009 under the direction of our Chinesesubsidiary and in Singapore in March 2009 to expand oursales and service portfolio in Asia. Built on the accom-plishments, we are moving forward so as to stand shoulder-to-shoulder with other top-notch insurers in the globalmarketplace.

2009 outlook, strategies and plans

It appears that another bumpy year lies ahead for commercialinsurance, as there are tantalizing signs of recovery in the realeconomy, and fears of another credit crunch linger inf inancial markets. However, based on SF&M’s pastexperience in overcoming difficulties, we will strive to sustainstable growth this year.

In recognition of the need for new growth engines andfundamental improvements in underwriting to cope withchallenges in the domestic market, we are set to driveforward with massive innovation focused on extending oursales reach from small-and mediumsized enterprises andindividuals to big business, reinforcing overseas operations,and strengthening underwriting capacity.

To expand our customer base, we will target “small in valuebut large in number” contracts with the launch of the firstproduct targeting the segment in July 2009. As for ouroverseas operations, we opened an office in India in May,and offices in Qingdao, China and Singapore earlier this year,after the necessary approvals were obtained. In the latter halfof this year, we will open an office in Brazil to expand thesales and services for commercial insurance overseas as away to strengthen the company’s new growth engine.

With a goal of developing a risk analysis capacity forunderwriting that is equal to that of leading foreign insurers,we are making considerable innovations to strengthenanalysis according to risk level, develop specialized areas ofunderwriting, create distinct pricing strategies and improveour ability in the calculation of rates. We will exert an all-outeffort to build our capacity for global competitiveness so asto take advantage of a diversified source of profits and tostrengthen our leadership in the market.

In commercial insurance, SF&MI is on the global frontier of efforts to build capacity to meet global standards and innovate management practices to strengthen serviceplatforms.

24/2503.3 Commercial InsuranceSamsung Fire & Marine Insurance Annual Report 2008

risk-related

Our Enterprise RiskManagement Committee isresponsible for addressingrisk and controlling for

issues in a timelyand appropriate manner.

Ross Ratio 76.6%Expense Ratio 23.0%

Underwriting Efficiency99.6%

Underwriting Efficiency(%)

Dedicated to identifying, assessing andmanaging potential threats

Ross Ratioa

Expense Ratio

Review of Operation

YeunJi Jung I Associate

FY 2007

FY 2008

21.7

78.1

99.8

23.0

76.6

99.6

Being a financial institution, active risk management is one ofthe crucial processes and core competencies of SF&MI.Managing risk is not just about avoiding or even minimizing it.Risk also needs to be considered as a potential opportunity.The ERM department manages the overall risk profile, aimingfor a good balance between risk and return.

SF&MI uses the Enterprise Risk Management (ERM) system,which has two functions: to ensure financial stability throughcontrolled risk-taking and to provide for adequate capitalizationthrough a broad range of risk analyses.

SF&MI's Enterprise Risk Management Principles

At SF&MI, Enterprise Risk Management (ERM) is based onthree principles that are applied throughout the company.

Early Warning Risk Identification:This involves risk management and analyses using projections for thefuture and requiring risk management forecasts and prognostications. KeyRisk Indicators (KRIs) allow SF&MI's risk managers to evaluate risk inadvance using real data.

Independent Risk Management Function:This is a specialized SF&MI department that is charged with managingpotential conflicts of interest.

Value-based Management Support:Embedded Value (EV) appraisals and the reporting of same enable SF&MIto practice Value-based Management (VBM) and measure the economicvalue of SF&MI's overall insurance operations.

Enterprise Risk Management Organization andStructure

The Board of Directors is responsible for establishing theframework, principles, and guidelines for Enterprise RiskManagement (ERM) at SF&MI. The Enterpr ise RiskManagement Committee is responsible for addressing riskand controll ing for risk-related issues in a timely andappropriate manner. The Chief Risk Officer (CRO) takesprimary responsibility for SF&MI’s risk management and hastwo staff departments, the Actuarial Department and ERMDepartment, which oversee Strategic Risk Planning, RiskControl, and Model Validation.

SF&MI’s Enterprise Risk Management Department monitorsrisk through analyses, reports, and risk modeling and istasked with identifying a wide range of possible risk scenariosin the company’s business units as well as company-wide. Byapplying these processes, the department assesses andmonitors each risk scenario, and implements appropriateaction plans.

Risk CategoriesThe major risks that SF&MI faces are as follows.

Asset-Liability Management (ALM) Risk:ALM manages structural risks (i.e., interest rate, equity, and liquidity) from

the perspective of optimized returns. Managing for ALM Risk involvesstrategizing from the dual viewpoints of assets and liabilities. StrategicAsset Allocation (SAA) involves the optimization of asset structures, whilethe Product Mix Strategy is concerned with the optimization of liabilitystructures.

Insurance Risk (Underwriting Risk): Insurance Risk refers to the danger of incurring a financial loss due toproperty, casualty, auto, or long-term insurance events. Our EnterpriseRisk Management Department manages for the transfer of such risks-including setting limits on underwriting authorizations and requiringapprovals for transactions involving new products. It also oversees themanagement of reinsurance and monitors emerging issues that may affectthe company’s overall exposure to risk.

Market Risk:Market Risk refers to the danger of being negatively impacted bymovements in financial markets-including equity market prices, creditspreads, foreign exchange rates, and real estate prices. Through scenario& sensitivity analysis, SF&MI measures the potential changes in expectedearnings based on an instantaneous increase/decrease in financial marketfactors.

Credit Risk:Credit Risk refers to the danger of incurring a financial loss due to thediminished credit-worthiness of counter-parties of SF&MI and/or thirdparties. To help mitigate the possibility of such occurrences, SF&MItransfers a portion of its new business to authorized reinsurers that arerated at least “A-.” For its investment portfolios, SF&MI maintains a well-diversified credit fixed-income portfolio across companies and industries.

Regulatory Perspective

SF&MI is engaged in the Risk Assessment & ApplicationSystem (RAAS) and in preparing for the introduction of theRisk-Based Capital (RBC) System, both of which arestatutory requirements of the Korean Financial SupervisoryService.

Strategic Risk Management Decision-Making

SF&M’s strategic decision-making is made by quanti-tative/qualitative analysis. Enterprise Risk Managementinvolves the company’s future earnings projection, NPV, IRR,and Capital collection periods using quantitative analysis.SWOT analysis and reputation/compliance risk assessmentsare also used to aid in the company’s strategic decision-making.

Strategic decisions are made by management committees orby the Board of Directors. Risk management analysis is oneof the major tools for strategic decision-making, in terms ofnot only the financial impact, but also reputation/compliancerisk reviews.

Strategic acquisitions, if necessary, will be made throughvaluations by actuarial and risk management concepts inaccordance with regional regulations.

26/2703.4 Enterprise Risk ManagementSamsung Fire & Marine Insurance Annual Report 2008

Sustainability Management1 ETHICAL & ENVIRONMENTAL MANAGEMENT2 CORPORATE COMMUNITY RELATIONS3 SPORTS4 CULTURE

Strong financial soundness, profitability, safety and payment capability are not the only elementsthat make SF&MI the finest insurance company in Korea. We are not only socially responsible,but also committed to making the world a better place to live for everyone.

PioneeringAction

04

Sustainability Management

By balancing our social,environmental andeconomic needs, SF&MI is striving totake greater responsibilityfor our environment andwork towards creating a cleaner future.

Ethical &Environmental

Management

Ethical Management

In 2002, SF&MI declared the year as a threshold year forethical management. The principles of SF&MI’s ethicalmanagement were set as 3Cs representing “Clean, Change,and Challenge.” Furthermore, key objectives of our code ofethics include “transparent managemen” trusted by thepeople, “fair trade” in respect of fair and free marketcompetition, and a “clean organizational culture” that fightscorruption.

With a strong belief and confidence in the value offered byinsurance, we have improved our sales practices to offermore detailed explanations of a product while providing moreaccurate compensation to the greater satisfaction of ourcustomers. In 2009, we adopted a code of conduct aimedat improving “customer orientation,” “a sense of ownership,”“a spirit of challenge,” “professionalism,” and “compliancewith laws.” We have also strengthened our commitment toethical management through in-company broadcasting andcampaign leaflets. In addition, every year all employees sign awritten oath to uphold the principles of ethical management.

SF&MI-from the CEO to entry-level employee- is clearlyaware that ethical management is not merely a matter ofchoice, but an obligation. We reiterated our dedication tosustainable ethical management practices at the 2007B.E.S.T (Business Ethics are the Source of Top Per-formance) Forum Seminar on March 7, 2007, jointly hostedby the B.E.S.T. Forum and the Institute for Industrial PolicyStudies and signed the forum’s CEO pledge.In 2001, we proclaimed our adherence to the principles andpractices of fair trade for the first time as a non-life insurer inthe country. Since then, we have developed a “ComplianceProgram” to translate our pledges into actions.

In 2005, we established an Internal Trade Commission,whose membership is l imited to outside directors, toexpedite transparent management. In 2009, we also foundeda Compliance Consulting Center to provide all employeeswith guidance on fair trade whenever needed. In addition, weenforce Jeongdo Jikimi, a whistleblower program, whichallows for anonymous reporting of non-compliance withguidelines or rules within the company. At the same time, theprogram places more emphasis on prevent ion thanpunishment. We also run an ethical management training

course for all employees throughout the year to sharelessons learned from whistle blowing cases, and best andworst practices for ethical management.

Environmental ManagementClimate change and environmental destruction is alreadyaffecting our lives and the places we live, and has thepotent ia l to dramatical ly impact the l ives of futuregenerat ions. SF&MI is committed to protect ing theenvironment, both as a responsible insurer and as anenvironmentally responsible corporation.

Green Bicycle InsuranceOn June 2009, SF&MI launched its 'green bicycle insurance',a bancassurance product that was jointly developed withKookmin Bank. In Korea, this is the first bicycle insurancethat provides personal and third-party liability protectionagainst the costs of damage or injury to other people orvehicles. This product is in line with ‘Low Carbon, GreenGrowth’, the core of the Korean government's new visionand helps reduce greenhouse gas emission andenvironmental pollution. In addition, it also meets the growingneeds of more than 8 million bicycle owners in Korea, whowere without such accident protection before this productlaunched.

Eco-OfficeIn order to become more environmentally friendly and cutdown paper use, SF&MI initiated a company-wide programto decrease the paper usage by 10%. From March 2009, wesuccessfully reduced 37 printers and 49 fax machines fromthe headquarters and decreased paper cup waste bypromoting the use of individual mugs. In addition, from July2009, SF&MI started reducing the energy expenditure on ourcomputers by setting the computer to go into standby modeif it has been inactive for 10 minutes.

Pollution Liability InsuranceSF&MI is helping conserve our nature with our pollutionliability insurance. This insurance product not only providesfinancial protection for damages caused by pollutionincidents, but also prevents the spread and facilitates theclean-up of the environmental hazard.

30/3104.1 Ethical & Environmental ManagementSamsung Fire & Marine Insurance Annual Report 2008

Sustainability Management

BoYoon Kook I Assistant

SF&MI is committed tocontributing to thecommunity to realizethe “management ofsharing” for a betterworld.

CorporateCommunity

Relations

SF&MI, since creating a volunteer group in 1994, has beenengaged in a number of community service activities, with aspecial focus on traffic safety and support for persons withdisabilities because they are closely linked to the nature ofour business. All employees and RCs (Risk Consultant) ofSF&MI have act ively part ic ipated in the company’scommunity service initiatives through volunteering anddonations.

Traffic Safety Promotion Initiatives

We selected Traffic Safety as our focus of attention and haveendeavored to prevent the occurrence of car accidentsinvolving children and raise awareness of accident preventionwhile initiating a wide range of road safety training programsand campaigns through the Samsung Traff ic SafetyResearch Institute (STSRI) and the Samsung TransportationMuseum. In addition, to a total of 102 children of trafficaccident victims including traffic police officers, we providesuch assistance as support in covering living costs, collegeentrance scholarships, graduation gifts, private tutoring aswell as emotional support by connecting each child with apart icular division of the company. In part icular, weintroduced a “Creating a Safer World Car Insurance” in July2007 to raise funds that go towards the “Health Voucher”initiative which provides about KRW300,000 worth ofmedicine per year to each child of traffic accident victims incoll-aboration with the Korean Pharmaceutical Association.

Support for Persons with Disabilities

We also provide an array of programs for persons withdisabilities such as donation of guide dogs for the blind,support for talented students with disabilities, assistance fora successful reintegration of the people into society, andincrease public awareness regarding people with disabilities.We have also donated a total of 126 specially trained guidedogs to the blind since 1995. The dogs are donated twice ayear after being trained at the Samsung Guide Dog School.With this, we are making a variety of efforts to increasepublic acceptance of the dogs in public areas and transitsystems.

In addit ion, we run “Talent Camp for Students withDisabilities” to provide systematic and professional educationto students who are gifted with musical talent. We also haveoffered the “SF&MI Scholarship” to visually challengedstudents and joined forces with a volunteer group, “First andForemost Movement for Persons with Disabilities” to helpvisually-impaired and wheelchair-bound persons successfullyreintegrate into society. In 2008, we signed a “SocialAgreement to Raise Public Awareness of Disability” with theMinistry of Education, Science and Technology and the Firstand Foremost Movement for Persons with Disabilities andaccordingly produced and distributed a campaign film “MyFriends” to 3,000 middle schools across the country.

Volunteering of SF&MI Employees

To better serve our community as a good corporate citizen,we formed the “Samsung anycar Volunteer Group” underwhich 180 sub-groups are actively engaged in communityservices across the nation. In 2008 alone, each employeeparticipated in volunteering for an average of 6.2 times or20.2 hours. Employees also raise KRW400 million a year inthe name of the Dream Fund. The company then matchesthese donations, which are used to lend a helping hand toneighbors in need. Since August 2005, we have set uppartnerships with 105 rural communities, in which each ofour divisions is partnered with one of them. Employees areencouraged to visit and purchase agricultural products at thelocal village partnered with their division.

KRW500 Gift of Hope

At the same time, SF&MI risk consultants (RC) have raised a“KRW500 Gift of Hope” fund by donating KRW500 per long-term insurance contract signed since May 2005. The fund isused to refurbish kitchens, restrooms, washstands, studyrooms, etc. at homes and facilities of the disabled to improvefunctionality and convenience for the residents of saidfacilities. So far, as many as 20,000 RCs have joined thecampaign to raise KRW1.36 billion and bring new hope to 67families of the disabled and 11 facilities. SF&MI is committedto contributing to the community to realize the “managementof sharing” for a better world.

32/3304.2 Corporate Community RelationsSamsung Fire & Marine Insurance Annual Report 2008

Sustainability Management

The passion of SF&MIstands out in sports. We progress and innovatefurther every year.

Sports

Samsung Fire & Marine Insurance BluefangsVolleyball Club

Since its launch in 1995, this volleyball club has made asensational debut by winning the title of the 2nd Korea GrandVolleyball League in 1996. The next year, the Korea VolleyballSuper League was created and the Samsung Fire & MarineInsurance Bluefangs won the title, too. The volleyball teamhas since swept the top spots in a number of series inKorea.

The triumphant march of the Bluefangs reflects the passionof SF&MI. In 2008, the club won the grand title of the nation’svolleyball leagues. The Bluefangs volleyball club is in full gearto win the 2009-2010 volleyball leagues with its new pioneerspirit. The team will bring fans lots of joy and excitementthrough well-mannered and thrilling games in the nextseason.

The 14th Samsung Cup World Baduk Masters1

The Samsung Cup World Baduk Masters , which marks its14th year in 2009, has upgraded the rules and prizes underthe slogan of “Change and Innovation - the Samsung CupEvolves.” “The Samsung Cup World Baduk Masters” refersto a traditional Korean board game also known as “Go”.

In the previous competitions, players from Korea, China andJapan constituted the majority of the participants. This year,however, players from Southeast Asia, Europe, and Americaare also invited. Therefore, the international reputation of theSamsung Cup is expected to be strengthened significantly.

As a result, for the first time in the competition’s history, thetop players from 10 countries including Singapore, Thailand,

Canada, France, Germany, the Netherlands, Hungary,Romania, Russia, and the Czech Republic will come toKorea to compete for the title.

Besides participating in the world’s largest “The SamsungCup World Baduk Masters” “championship, the players willbe given chances to have goodwill matches with KoreanBaduk clubs. The events are designed to offer opportunitiesfor the players to experience the excellence of Korean Badukand to raise awareness of it in countries of the players.

In the previous competitions, each country had the right torecommend their seed players. This year, however, only thewinners of major championships are invited so as to ensurethat the world’s top players join the games.

The rules of finals have also changed significantly. Instead ofa knockout tournament where defeated players in eachmatch are eliminated, double elimination2 will be applied forthe top 32 players. The format, which was used in the WorldBaseball Classic (WBC), aims to give another chance tolosers, reduce unexpectedness, and add more thrills to eachmatch.

In addition, a “Senior’s Group” was created for pros over 45years old. Online preliminaries are also adopted so thatamateur players can participate in the Samsung Cup moreeasily.

A Children’s Baduk competition will also be held on thesidelines of the Samsung Cup. Young Baduk playersadvancing to finals will have their matches in the place wherethe quarter-finals of the Samsung Cup are held and will beallowed to watch the games in person.

34/3504.3 SportsSamsung Fire & Marine Insurance Annual Report 2008

1) Masters competition:Competitions to which the winners and top players in major championships are invited.

2) Double elimination:A type of tournament where a player is eliminated upon losing two games. However, if the player loses one game and wins the other two, s/he will be eligibleto advance to the next round.

Sustainability Management

YeonHee Shin I Financal Specialist Ⅲ

SF&MI is committed toproviding valuable learningand special enjoyment byresearching automobileculture while contributing tothe advancement of thecountry’s traffic safetypractices.

Culture

Samsung Traffic Safety Research Institute (STSRI)

The Samsung Traffic Safety Research Institute (STSRI) wasestablished in July 2001 with 15 Ph.D. holders in tran-sportation safety. One hundred years have passed since thefirst car appeared on the street in the country and thenumber of registered cars now exceeds 14 million. Theinstitute was founded to improve driving and traffic practicesin Korea, which still records the highest death rate in caraccidents.

The STSRI has actively partnered with government agenciesand civic groups to pursue joint projects, improve road safetyregulations, propose relevant laws, and etc.

The institute is also committed to conducting research onICT development for road safety, theft-prevention systems,car safety systems and automobile product liability.

Samsung Loss Control Center

SF&MI formed a specialized organization for risk manage-ment in 1979 for the first time among domestic non-lifeinsurers. Since then, it has provided risk-managementservices for accident prevention to create disaster-freeworkplaces for our customers.

The specialists at our Loss Control Center have rich practicaland theoretical experience in the fields of construction, civilengineering, machinery, electronics, chemical engineeringand others. They have exerted their best efforts to safeguardour customers from accidents by developing new risk-prevention skills for highly industrialized fields, establishingpractical accident-prevention methods, holding seminars andpublishing reports.

Samsung Transportation Museum

The Samsung Transportation Museum, The SF&MI Tran-sportation Museum, the only automobile museum in Korea,aims to introduce the history and spirit of automobiles, andthus promote automobile culture that can be widely sharedby the public. Since the museum’s establishment in May1998, about 300,000 people visit there every year.

The transportation museum is playing three roles as below:

Social education on automobile cultureThe museum has collected, studied and preserved a widevariety of artifacts related to automobiles. It also has exhibitedits collections, run training programs and published books tofulfill the public desire to know more about automobileculture.

Preserve and promote the heritage of automobile cultureThe museum has preserved automobile-related artifacts in anoptimized environment and restored damaged ones, passingthis heritage down to our descendants.

Create and promote a new automobile cultureThe museum has introduced and explored automobileculture in all its forms and related information in an effort toprovide the public with opportunities to experience it whilecreating and promoting a new and better automobile culturein Korea.

36/3704.4 CultureSamsung Fire & Marine Insurance Annual Report 2008

SF&MI is robust. We are reliable. We never fall into complacency, and we are runningwell ahead of anyone else. Our customers are the beginning and end of our business.We will dedicate our efforts to creating stronger corporate values for many years tocome.

Table of aPioneeringCompany

05

Financial Section

1 MD&A2 FINANCIAL STATEMENTS3 WORLDWIDE NETWORK & SAMSUNG AFFILIATES

MANAGEMENT DISCUSSION & ANALYSIS

A. Operational Results

1. Overview

In fiscal 2008, the global economic meltdown ravaged the world economy. On the international front, the global financial market and the real

economy felt the squeeze of the credit crunch in the U.S. Meanwhile, on the domestic front, the economy was plagued by such woes as a

slackening of exports, weak consumption, sagging employment, and volatile currency and stock market swings.

The domestic non-life insurance industry was also marked by intense competition as sales channels were diversified with the implementation

of cross-selling of life and nonlife products and the growth of GA channels and the online auto insurance market. Despite the unfavorable

circumstances in and out of the country, SF&M made good progress as follows:

First, we posted a record-high net profit for the fiscal year. Net profit totaled KRW598.7 billion, which was second to none in the industry. In

so doing, we set a record of paying dividends to our shareholders for 33 years in a row, ever since the company’s listing on the stock

market in 1975. In addition, return on equity (ROE) rose 2.1%p to 16.5%, dwarfing that of major foreign insurers.

Second, tangible progress was made in strengthening SF&MI’s fundamental competitiveness. Auto insurance stemmed persistent losses by

achieving a combined ratio of 98.3%. Such improvements in the company’s efficiency contributed considerably to the growth in profit. In

long-term insurance, the loss ratio remained stable as the share of living benefit type coverage in product lines were kept to appropriate

levels. Despite the challenging investment environment, net investment yield was up 0.1%p from the previous year to 4.9% as a result of

focused efforts to improve the existing profit structure and extend debt-asset spreads through a preemptive high-yield bond investment.

Third, we realized the strongest financial soundness in the industry. SF&MI recorded the lowest non-performing loan ratio and delinquency

ratio in the industry. The solvency margin ratio, one of the major barometers of financial robustness, was 374.8% at the end of March,

showing a striking gap with other players in the market whose capital strength was undermined by losses from risky assets.

In addition, direct premiums written were up 6.4% year-on-year to KRW9,744.9 billion, net profit climbed by 25.6% to KRW598.7 billion, and

adjusted net profit including an increase in catastrophe reserves jumped 27.2% to KRW671.3 billion. Total assets grew 11.3% to

KRW23,092.2 billion while catastrophe reserves increased 7.4% to KRW1,059.3billion, thus enhancing the company’s already strong

financial stability.

Financial Section

2. Profit and Loss Summary

In fiscal 2008, direct premiums written and net premiums earned posted 6.4% and 7.9% year-on-year growth, or KRW9,744.9 billion and

KRW8,992.6 billion, respectively.

Increase in catastrophe reserves surged 41.5% from the previous year to KRW72.6 billion. Underwriting losses shrank KRW18.1 billion to

negative KRW31.8 billion owing to a significant improvement in the auto insurance loss ratio. Investment operations posted KRW887.6 billion

in profits, up KRW114.9 billion from a year earlier.

All in all, operating profit expanded by KRW133.1billion or 18.4% year-on-year to KRW855.9 billion. Non-operating profit improved by

KRW27.3 billion to negative KRW35.1 billion. In other words, pre-tax profit soared by KRW160.4 billion to KRW820.8 billion and net profit

grew KRW122.2 billion or 25.6% from the previous year to KRW598.7 billion. Adjusted net profit including catastrophe reserves was up

KRW143.5 billion to KRW671.3 billion. Adjusted EPS based on adjusted net profit increased 31.2% to KRW15,408.

40/4105.1 Management Discussion & AnalysisSamsung Fire & Marine Insurance Annual Report 2008

Income Statement Summary Korea Won / in billions

WonFY08Change

%FY07

Direct Premiums Written 9,744.9 9,160.6 584.3 6.4%

Net Premiums Earned 8,992.6 8,336.5 656.1 7.9%

Increase in Catastrophe Reserves 72.6 51.3 21.3 41.5%

Underwriting Profit -31.8 -49.9 18.1 N/A

Investment Profit 887.6 772.7 114.9 14.9%

Operating Profit 855.9 722.8 133.1 18.4%

Non-Operating Profit -35.1 -62.4 27.3 N/A

Pre-tax Profit 820.8 660.4 160.4 24.3%

Net Profit 598.7 476.5 122.2 25.6%

Adjusted Net Profit 671.3 527.8 143.5 27.2%

Adjusted EPS (In KRW) 15,408 11,742 3,666.5 31.2%

MANAGEMENT DISCUSSION & ANALYSIS

3. Earnings by Product Line

When it comes to the sales growth of product lines in fiscal 2008, general insurance recorded the biggest gain followed by long-term

insurance and auto insurance.

General insurance, which grew the most among the product lines, showed a 15.5% increase in sales mainly due to a growth in sales of hull

insurance.

Sales of long-term insurance reached KRW5,576.8 billion, up 9.6% from a year before. Initial premiums recorded a healthy 19.9% climb to

KRW195.4 billion as a result of focused efforts to launch innovative products, boost the productivity of solicitors’ channels, and increase the

number of high-performing solicitors on the heels of an overhaul of product and solicitors’ channels in the last year.

Auto insurance sales fell 1.7% compared to last year to KRW3,060.5 billion because of cuts in premium rates and new car registrations.

Our market share was slightly down by 1.1%p to 28.0% from a year earlier. By product line, our control of the auto insurance market was

weakened by the expansion of the online insurance market and a decrease in new contracts while market share in general insurance and

long-term insurance dropped slightly as we focused on improving the profitability of sales.

Financial Section

Direct Premiums Written by Line

Market Share by Line

General 1,107.6 11.4% 958.7 10.5% 148.9 15.5%

Long-term 5,576.8 57.2% 5,089.6 55.6% 487.2 9.6%

Initial Premiums 195.4 2.0% 163.0 1.8% 32.4 19.9%

Renewal Premiums 5,381.4 55.2% 4,926.6 53.8% 454.8 9.2%

Automobile 3,060.5 31.4% 3,112.3 34.0% -51.8 -1.7%

Total 9,744.9 100.0% 9,160.6 100.0% 584.3 6.4%

Korea Won / in billions

AmountFY08

% AmountFY07

% AmountChange

%

General 29.3% 28.2% 29.1% 1.1%p

Long-term 27.9% 29.7% 31.9% -1.8%p

Automobile 28.0% 28.8% 28.6% -0.8%p

Total 28.0% 29.1% 30.2% -1.1%p

FY08 Change %FY07 FY06

The loss ratio slipped 1.5%p to 76.6% in fiscal 2008. By product lines, the loss ratio in auto insurance showed a substantial improvement

among others. The figure was down by 3.2%p to 67.2% because the accident rate fell slightly and net premiums earned increased by 3.2%

on account of premium hikes over the last two years.

The loss ratio in long-term insurance also dipped to 83.8%, a 1.1% decrease from a year earlier, due to a decrease in the interest burden

from a decline in the legacy of high-fixed guarantees that were matured. In the meantime, the general line loss ratio went up by 1.9%p from

the last year to 56.2% by virtue of an increase in O/S reserves.

The overall expense ratio amounted to 23% or a 1.3%p rise year-on-year in the aftermath of changes in the commission payment method. In

fiscal 2008, commissions were paid in up front for major long-term products and this led to an increase in payments and, in turn, the overall

expense ratio.

By items, the wages and severance benefit ratio was up 0.2%p year-on-year to 5.3% while distribution costs went upward by 1.1%p.

Business administration costs increased 0.1%p to 7.3%, but the expense recovered ratio slid marginally. The overall expense ratio stood at

23%, a 1.3%p increase from the previous year.

42/4305.1 Management Discussion & AnalysisSamsung Fire & Marine Insurance Annual Report 2008

Underwriting Efficiency

Loss Ratio 76.6% 78.1% -1.5%p

General 56.2% 54.3% 1.9%p

Long-term 83.8% 84.9% -1.1%p

Automobile 67.2% 70.4% -3.2%p

Expense Ratio 23.0% 21.7% 1.3%p

General 16.3% 18.3% -2.0%p

Long-term 19.4% 17.4% 2.0%p

Automobile 31.1% 29.5% 1.7%p

Combined Ratio 99.6% 99.8% -0.1%p

Change %FY08 FY07

Miscellaneous Business Expense Ratio

Wages and Severance Benefits Ratio 5.3% 5.1% 0.2%p

Distribution Costs 1) 12.2% 11.1% 1.1%p

Business Administration Costs 7.3% 7.2% 0.1%p

Expenses Recovered 2) -1.9% -1.8% -0.1%p

Total 23.0% 21.7% 1.3%p

Change %FY08 FY07

1) acquisition and collection cost, transaction fees, deferred acquisition cost2) recovered commissions, recovered profit commissions

MANAGEMENT DISCUSSION & ANALYSIS

4. Profit from Investment Operations

The investment profit in fiscal 2008 was KRW887.6 billion, representing growth of 14.9% from KRW114.9 billion for the previous year. The

net investment yield was up 0.1%p year-on-year to 4.9% on the back of increased profit from fixed income type assets such as bonds and

loans.Profit from bonds surged by 13.5% or KRW62.5 billion to KRW524.2billion. Profit from loans grew by 19.2% or KRW52 billion to

KRW322.5 billion.

The overseas investment yield declined 2.3%p from last year because of KRW6.8billion in losses from the write-down of collateralized debt

obligation (CDO) bonds. The CDOs owned by SF&MI are not sub-prime loans, but are AAA-rated senior bonds which are safe from the risk

of default. However, a conservative accounting decision was made to write these off considering the extended CDO credit spread caused

by a scarcity of global credit while some of the CDOs were recovered as bonds.

5. Income Tax Expenses

In fiscal 2008, profit before income tax recorded a gain of KRW160.4billion or 24.3% year-on-year to KRW820.8 billion. Subsequently,

income tax increased by KRW38.2 billion from a year ago to KRW222.1 billion. The official corporate tax rate including residency tax was set

at 27.5%. However, the effective tax rate for the period was set at 27.1%, or a 0.7%p drop from the previous year.

Financial Section

Investment Income

Cash and Equivalents 29.6 20.0 9.5 48.0%

Stocks 59.2 55.3 3.9 7.0%

Bonds 524.2 461.8 62.5 13.5%

Loans 322.5 270.5 52.0 19.2%

Overseas 22.2 29.4 -7.2 -24.5%

Real Estate 13.1 12.0 1.0 9.2%

Total 970.7 849.0 121.7 14.3%

Investment Administration Expenses 1) 83.1 76.4 6.7 8.8%

Investment Income 887.6 772.7 115.0 14.9%

Net Investment Yield 4.9% 4.8% 0.1%p

FY08 FY07

1) Bad debt expenses and depreciation costs have been distributed by asset.

Won Change %

Income Tax Charges

Income Before Income Tax Charges 820.8 660.4 160.4 24.3%

Income Tax Charges 222.1 183.9 38.2 20.8%

Effective Tax Rate 27.1% 27.8% -0.7%p

FY08 FY07

Korea Won / in billions

Won Change %

Korea Won / in billions

B. Balance Sheet

1. Financial Conditions