Embed Size (px)

Citation preview

The Global Economy, Competency, and theEconomic Vote

Raymond M. Duch University of Oxford

Randy Stevenson Rice University

Working within a selection model of economic voting we propose explanations for the cross-national and dynamicvariations in the magnitude of the vote that have puzzled students of comparative voting behavior. Our theory suggeststhat unexpected shocks to the economy inform the economic vote which implies that voters are able to resolve a signalextraction problem: determine the extent to which these shocks are the result of incumbent competency as opposed toexogenous shocks to the economy. We assume that voters have information on the overall variance in shocks to themacroeconomy and that they use this signal to weight the importance of economic shocks in their vote decision. Votersare also hypothesized to recognize that higher exposure to global trade influences reduces the magnitude of theincumbent competency signal. We provide empirical evidence demonstrating that voters are able to discern significantvariation in macroeconomic outcomes in order to perform this signal extraction task: We analyze a six-nation surveyconducted by the authors that was designed to assess whether voters are attentive to variance in economic outcomes andwhether these in fact conditioned their economic vote. Secondly we examine economic time series from 19 countriesover the 1979–2005 period, demonstrating that variances in the macroeconomic series explain contextual variations inthe economic vote as our theory hypothesizes. Finally, the essay demonstrates that open economies, which are moresubject to exogenous economic shocks, have a smaller economic vote than countries with economies less dependent onglobal trade.

Is it rational for voters to ignore economic out-comes in making a vote decisions? That theyfrequently do has been established by many stu-

dents of both U.S. and comparative economic voting.Based on an extensive analysis of voter preferencestudies in the developed democracies, Duch andStevenson (2008) have established that there is con-siderable variation in the economic vote from onecountry to the next and even from one election tothe next. Some have argued that the evidence is sovariable as to call in question the notion of an eco-nomic vote (Cheibub and Przeworski 1999). Othershave been much more sanguine suggesting that thisinstability results from institutional or political con-texts that vary in terms of the clarity with whichvoters can determine responsibility for economicpolicy making (Hibbs 2006; Powell and Whitten1993). Neither of these perspectives suggests thisvariation in the economic vote results from rationalcalculations on the part of voters. In this essay wepropose an explanation for this contextual instability

in the economic vote that explicitly builds on a modelof instrumentally rational voting decisions.

While we are certainly not alone in drawingattention to this cross-national instability in the eco-nomic vote, we believe we have a persuasive explanationfor this variation. Our contribution is to derive explan-ations for this contextual instability from a competencytheory of the economic vote.1 This theory identifiespolitical and economic contexts in which we wouldnot expect rational voters to hold incumbents respon-sible for shocks to the macroeconomy. Working withina selection model of economic voting we propose ex-planations for the cross-national and dynamic varia-tions in the magnitude of the vote that has puzzledstudents of comparative voting behavior. This essaybegins with an overview of our selection or competencytheory of economic voting.

Our theory builds on rational expectations theoryand suggests that unexpected shocks to the economyinform the economic vote but in addition that votersare confronted with a signal extraction problem—to

The Journal of Politics, Vol. 72, No. 1, January 2010, Pp. 105–123 doi:10.1017/S0022381609990508

� Southern Political Science Association, 2010 ISSN 0022-3816

1We do not review the extensive literature on economic voting in this essay. For an excellent review see Lewis-Beck and Stegmaier (2000)and Lewis-Beck (1988).

105

what extent are these shocks the result of incumbentcompetency as opposed to exogenous shocks to theeconomy. We assume that voters have informationon the overall variance in shocks to the macro-economy and that they use this signal to weight theimportance of economic shocks in their vote deci-sion. Voters also recognize that higher exposure toglobal trade reduces the magnitude of the incumbentcompetency signal.

Two critical empirical implications of this theoryare explored in this essay employing quite distinct datasources. One assumption is that voters are able todiscern significant variation in macroeconomic out-comes in order to perform this signal extraction task.Hence one of our empirical goals is establishingwhether voters have the information necessary for thissignal extraction task. Our theory suggests that thesevariations in shocks to the macroeconomy conditionthe economic vote. Testing this argument constitutesthe second empirical focus of the essay. We organizethe empirical test into two different sections, oneemploying microlevel data and the other macro oraggregate-level data. The empirical section begins byanalyzing a six-nation survey that the authors designedto assess whether voters are attentive to variance ineconomic outcomes and whether these conditionedtheir economic vote. Secondly our analysis of eco-nomic time series from 19 countries between 1979 and2005 confirms our hypothesis that variances in themacroeconomic series explain contextual variations inthe economic vote. Finally, the essay demonstrates thatopen economies, which are more subject to exogenouseconomic shocks, have a smaller economic vote thancountries with economies less dependent on global trade.

Competency Theory of theEconomic Vote

Competency, or selection, models of economic votingstipulate that the vote decision entails more than asimple reward-punishment response to economicoutcomes. They suggest that instrumentally rationalvoters are motivated by the desire to select the mostcompetent candidates: voters use information abouteconomic outcomes to assess the future competenciesof competing candidates. An incumbent who is notperceived by the voter as having competency foreconomic outcomes should neither be rewarded for agood economy, nor punished for poor economicoutcomes. Selection models were not unfamiliar tothe early economic voting scholars. For example,

voters in Downs’ model are future oriented and com-pare the platforms of contending candidates; logicwhich more closely resembles a selection as opposedto a sanctioning model. Likewise, Kramer (1971)viewed voters as future oriented but unwilling tospend the resources to assess future promises. Whilethis early work clearly pointed the way toward arational model of economic voting based on theselection of competent politicians, informal modelsleft many questions unanswered, e.g., could it berational for voters to use the previous economy toinfer competence, if politicians had incentives tomanipulate the economy for electoral gain? Answersto these kinds of questions had to await the develop-ment of the rational expectations literature in eco-nomics; and it is this tradition that informs ourselection model of the economic vote.

How do voters with rational expectations abouteconomic outcomes use economic performance tomake their vote choice? Since a voter’s future utilitywill depend on choices she makes today, she mustforecast the likely economic future under differentpossible incumbents. Our assumption is that theseexpectations are formed rationally based on all theinformation available at the time of the election.Politicians in our model all care only about being inoffice and understand that voters will vote to max-imize their expected utility.2 The model, closely basedon Alesina and Rosenthal (1995), assumes that anincumbent competes for control of the executive andthat this executive can choose, for example, aninflation rate (pit) directly (i.e., their economicpolicy) that determines growth (yit) in the followingexpectations augmented Phillips curve:

yit 5 �y þ pit � peit þ hit ð1:1Þ

The equilibrium level, or average rate, of growth isrepresented by �y. The economic shock consists of twoparts as follows:

hit 5 eit þ jt ð1:2Þ

One part, eit, is simply an increment to growth thatdepends on the identity of the incumbent but not onher economic policy (which is captured in pit). Thisincrement to economic performance captures theeconomic impact of the incumbent administration’smanagerial competence. More specifically, this shock

2We could allow politicians to differ in their policy preferences,for example leftist politicians might prefer a nonzero inflationrate. As we will see, however, economic voting in the model doesnot in any way depend on the policy choices of politicians and sowe ignore this complication.

106 raymond m. duch and randy stevenson

includes any unobserved economic impact of thebehavior of the incumbent administration that is notconstant over time or administration.3 We refer tothis impact as a ‘‘competency shock.’’ The other partof the total shock to economic growth, jt, thoughalso unobserved and not constant over time, does notdepend on the identity of the administration. Werefer to it as an ‘‘exogenous’’ shock or sometimes as a‘‘nonpolitical’’ shock.

Voters cannot observe competence shocks or non-political shocks directly but can glean some informa-tion about incumbent competence from the fact thatthe observed economy is partially dependent on it. Ofcourse, to be useful in forecasting the future economy,the level of competence inferred from observed eco-nomic performance must provide some guide to theincumbent’s future level of competence. Consequently,we assume that competence is persistent over time inthe following way:4

eit 5 mit þ mit�1 ð1:3Þ

Thus, current competence is just a first-order movingaverage from a sequence of competency shocks. Eachof these competency shocks is drawn from an iden-tical distribution, with mean zero and finite vari-ance s2

m. Likewise, we assume that the nonpoliticalshocks, jt, are drawn from identical distributionseach with zero mean and finite variance s2

j . Weassume voters know the expected values and varian-ces of these distributions.

All voters in the model are identical and care aboutachieving the highest possible economic growth andlowest possible inflation in the next period. Specifi-cally, we will write the utility of a typical voter in periodt+1 as a function of which party is elected, whatpolicy that party pursues, and what the resulting levelof economic growth will be. Given some governingparty, i, that pursues a particular economic policy(a choice of pit+1), the voter’s utility in period t+1 isin part:5

u pitþ1; yitþ1ð Þ5 � 1

2p2

itþ1 þ byitþ1; b . 0 ð1:4Þ

where b indexes the voter’s preference for growthrelative to inflation. The particular functional form ofutility for inflation and growth is quite flexible: as wewill see, any choice that has the voter’s utility in-creasing in growth will produce the same substantiveimplications for rational economic voting given theother assumptions in the model. The one providedabove is a common formulation in the literature andso was chosen for its familiarity. Since utility is in-creasing in y and is maximized, for a given y, wheninflation equals zero, this expression says that thevoter prefers more growth and price stability and thatshe would be willing to trade price increases forgrowth at a rate governed by the size of b.

Since a voter’s future utility will depend onchoices she makes today, she must forecast the likelyeconomic future under different possible incumbents.Our assumption is that these expectations are formedrationally based on all the information available at thetime of the election. Politicians in the model all careonly about being in office and understand that voterswill vote to maximize their expected utility.

Since voters form expectations about inflationand growth rationally they know that incumbentpoliticians will pick the level of inflation (and cor-respondingly growth) that will maximize the incum-bent’s expected utility. Voters know current inflationand are never surprised by the government’s inflationpolicy. Consequently, politicians have nothing togain from doing anything but choosing the voter’soptimal inflation rate (zero). Thus, in this simpleversion of the model, all politicians, no matter howcompetent, will choose the same economic policyand differences in growth associated with differentpoliticians can only result from differences in theirtypes (which are exogenous to the model). Clearly,then, the decisions of the politicians play no real rolein the model and so it is equivalent to a reducedform, decision-theoretic version of the usual formu-lation that has been used to explore political businesscycles. Since our focus is on the decision of votersgiven the observed economy and not on the decisionsof politicians about policy, this seems an appropriatesimplification.

With this, the growth rate from equation (1.1) isjust the natural rate plus any shock. Further, voterscan actually observe the total shock, since they cancalculate it via equation (1.1). However, they cannotuse that equation to parse out how much of the

3If voters observe the impact of this behavior it cannot be part ofthe shock but is part of the observed policy represented by pit.Likewise, any unobserved impact of behavior on growth that isconstant is subsumed in the natural rate of economic growth.

4One can also discount the impact of past competence as long asit is at least partially persistent.

5It is possible to state the voter’s preferences more generally toinclude the whole sequence of time discounted future periods, e.g.,U ¼ E +‘

t¼0dtu pi;t; yi;t

� �� �; 0. However, the usual assumption

restricts the discount factors to make this equivalent to a voterwho looks into the future only so far as the next period ofincumbency. For our purposes, then, the simpler formulationgiven in the text is adequate.

the economic vote 107

observed shock is due to the incumbent’s compe-tence, since they do not observe the two shock termsseparately, but only overall growth.

The voters in the model form their expectationsabout the competence of the incumbent rationallyand because of the moving average structure of theerror term in equation (1.3), growth rates at time tthat differ from �y will provide voters with informa-tion regarding the competence of an incumbent re-elected for period t + 1. This follows from takingexpectations in equation (1.3) (recall that the uncon-ditional expectation of mit+1 is zero).

E eitþ1½ �5 E mitþ1

� �þ E mit j yit½ �

5 E mit j yit½ �ð1:5Þ

Voters form their expectations about the competence ofan incumbent reelected in period t+1 by evaluating mit

or, more precisely, the noisy signal provided by yit.A key assumption of Alesina and Rosenthal’s (1995)model is that voters learn the value of competency witha one-period delay—that is, in period t they knowmit21 but not mit. Hence voters base their forecast ofthe economic competence of the incumbent on both yit

and mit21. Specifically, in the current period votersknow the competency of the incumbent in the lastperiod, the natural rate of growth, the current realiza-tion of growth, and the current economic shock (whichis composed of some unknown mix of the currentcompetence of the incumbent and the nonpoliticalshock). Growth in the current period is thus:

yit ¼ �y þ hit

¼ �y þ mit þ mit�1 þ jt

ð1:6Þ

Rearranging this gives:

mit þ jt 5 yit � �y � mit�1 ð1:7Þ

Where everything on the right-hand side of thisequality is observed and so the sum of the terms onthe left is also observed, though not the individualcomponents. Denote the sum on the left hand side askit 5 mit þ jt. Since kit is observed, the voter cancompute her expectation about mit given kit (i.e., herexpectation about the incumbent’s current level ofcompetence, given the observed level of growth andthe incumbent’s competence in the last period). Tocalculate this conditional expectation, we need toknow the distribution of both kit and mit. kit is thesum of two normally distributed random variables,both with zero means and variances s2

m and s2j ,

respectively. The distribution of kit is thus:

kit 5 mit þ jtð ÞeN 0;s2m þ s2

j

� ð1:8Þ

Given that both, kit and mit are distributed normally,their joint distribution is bivariate normal and theoptimal forecast of mit given kit is just the conditionalexpectation, which is computed from the appropriateconditional distribution of the bivariate normal.Using standard results, this conditional expectationis (Greene 2003):6

E mit j kit½ � ¼ E½mit� þsm;k

s2k

yit � �y � mit�1ð Þ � E½kit �

¼s2

m

s2m þ s2

j

!yit � �y � mit�1ð Þ

ð1:9Þ

Since E mit j kit½ �5 E mit j yit½ �, this expression is therational voter’s assessment of the current competenceof the incumbent given the observed economy.7 Fur-ther, from equation (1.5), we have E mit j yit½ �5E eitþ1½ �, so we now have what we need to explore theimplications of the model for economic voting bycomparing the voter’s expected utility for voting for theincumbent in this model to her expected utility for anychallenger.

The voter will vote for the party that she expectsto deliver the most utility in the next period. So wecan write her expected utility for voting for incum-bent party i as equal to the expected utility the voterwill accrue in the next period if party i is in office.

E utþ1jvi½ � ¼ E u pitþ1; yitþ1ð Þ½ �

¼ 1

2E½p2

itþ1� þ bE½yitþ1�

¼ 0þ b �y þ E hitþ1

� �� �i

¼ 0þ b �y þ 0þ E eitþ1½ �ð Þ

¼ b �y þs2

m

s2m þ s2

j

ðyit � �y � mit�1Þ !

¼ b�y þ bs2

m

s2m þ s2

j

!ðyit � �y � mit�1Þ

ð1:10Þ

6In general, E x j y½ �5 rxyy�E y½ �

sysx þ E x½ �, where rxy is the corre-

lation between x and y.

7E mit j yit½ �5 sm;y

s2mþs2

j

yit � y� mit�1ð Þ by applying the same signalextraction solution as above. Further, it is easy to show thatsm;y 5 sm;k , so the claim in the text follows.

108 raymond m. duch and randy stevenson

Lacking any information about the challenger’s levelof competency, the voter’s expected utility for votingfor any challenger, k, is just:

E utþ1 j vk½ � ¼ E u pktþ1; yktþ1ð Þ½ �

¼ 1

2E½p2

ktþ1� þ bE½ykt þ 1�

¼ 0þ b �y þ E hktþ1

� �� �¼ b �y þ E jtþ1½ � þ E ektþ1½ �ð Þ¼ b�y

ð1:11Þ

Thus, the voter is more likely to vote for theincumbent when the expected utility in equation(1.10) is larger than that in equation (1.11). Thedifference is:

E utþ1jvi½ � � E utþ1jvk½ � ¼ b�y þ bs2

m

s2m þ s2

j

!3 ðyit � �y � mit�1Þi � b�y

¼ bs2

m

s2m þ s2

j

!ðyit � �y � mit�1Þ ð1:12Þ

This result makes it clear when voters can and cannotextract information from fluctuations in the previouseconomy in order to access the current competenceof an incumbent and cast an economic vote. Theterm yit � �y� mit�1 is simply observed economicperformance less the parts of economic growth whosesources are known to the voter. The term captureswhat the incumbent has ‘‘done for the voter lately’’(i.e., how the current period differs from the naturallevel of growth, discounted by the impact of theincumbent’s known level of competence in theprevious period). We can interpret the coefficient

on this term, i.e.,s2

m

s2mþs2

j

, as the ‘‘competency signal’’

that controls how much information about the com-petence of incumbents voters can extract from ob-served movements in the economy. This competencysignal will always be positive and will approach one asthe variance in the random (nonpolitical) shocks tothe economy, s2

j , goes to zero. In that case, the voterknows that growth above or below the natural rate iscompletely due to competency shocks—consequently,deviations from the natural rate of growth willperfectly identify competent and incompetent ad-ministrations. More generally, if sm

2, the variation inthe competence term mit, is large relative to variationin the nonpolitical component of growth, sj

2, thenchanges in the economy will provide a strong signal

about the competency of the incumbent and thevoter will weigh the retrospective economy moreheavily in her utility function. Alternatively, growththat is above or below the natural rate is a poor signalof the incumbent’s competence if observed growth ismore likely to result from nonpolitical shocks thanfrom competency shocks—i.e., if s2

j is high relativeto s2

m.In our economic vote model, like many other

models in the literature, voters focus on the mostrecent economic outcomes (Hibbs 2006; and for acritique, Achen and Bartels 2002).8 The voter’s assess-ment of economic performance is presumed to focuson most recent shocks to the economy yit � �yð Þwhich is similar to Hibbs (2006) although it is nota weighted sum of past outcomes (although Hibbsnotes that the weight is typically very high on themost recent outcome). In this formulation our voterfocuses only on recent unexpected shocks, so behav-ing in a decidedly more rational expectation fashionthan Hibbs’ economic voter. We go a step furtherthan many of the economic voting models in thatwe try to characterize precisely how voters use thisinformation, i.e., the most recent shock in theeconomy, in their vote preference function. Herewe argue that voters do use historical informationabout the economy (hence they pay attention tomore than just the most recent economic outcome).Based on historical fluctuation in these economicoutcomes voters are able to construct a competencyterm that they use to weight current economicshocks. Voters pay attention to historical outcomesbecause they inform them of the economic compe-tency of the incumbent.

Empirical Implications

In the rest of this essay we assess whether voters useglobal economic outcomes to inform themselvesabout the magnitude of the terms that make up this

competency signal,s2

m

s2mþs2

j

. We examine two macro-

economic outcomes, related to the global economy,that inform voters of competency: (1) fluctuations indomestic and global economic outcomes; and (2)exposure of the domestic economy to global trade.While these do not represent the totality of

8Although since the periodicity in our abstract theoretical modelis completely arbitrary—we refer to periods not months oryears—the reader is free to interpret yit � �y� mit�1ð Þ to applyto whatever period she thinks relevant.

the economic vote 109

information that informs voters of competency, theyconstitute two informative signals. Our goal is toprovide empirical evidence that voters are informedabout these signals and that this information con-ditions their economic vote.

Figure 1 illustrates in a stylized fashion the con-cepts summarized in equations (1.1) and (1.12), inaddition to introducing our two principal empiricalhypotheses. In each of the four quadrants the plottedlines correspond to shocks to the macroecono-my—we can think of these shocks as deviationsfrom expectations, yit � �y which are similar to theyit � �y� mit�1 term in equation (1.12). The first rowof the stylized graphs illustrates the hypothesizedimpact of domestic versus global fluctuations inshocks to GDP growth while the second row illus-trates the exposure to global trade effect. The firstcolumn represents a hypothetical high competencysignal condition while the second column illustrates ahypothetical low-competency signal condition.

Recall that we define the economic vote asa function of a shock to the macroeconomy,yit � �y� mit�1, weighted by a competency term,

s2m

s2mþs2

j

. The competency signal,s2

m

s2mþs2

j

, differs in Col-umn 1 versus 2 as a function of variation in shocks to

the domestic versus global economies (Row 1) and asa function of exposure to global trade shocks (Row 2).

In Row 1, voters have two pieces of informationon which to extract a competency signal: they knowthe historical variation in shocks to real GDP growthfor other countries (summarized by the variation inthe bold line), and they know the historical variationin shocks to domestic real GDP growth (captured bythe dashed line). In Quadrant 1, the two variances arevery different suggesting that variation in shocks toGDP growth in this country is quite distinct fromthose for other global economies. The fact that theshocks to the domestic economy vary quite distinctlyfrom those for other economies signals to voters thatthe national government, rather than exogenousglobal economic shocks, is affecting domestic eco-nomic outcomes. These differences provide the voterwith information that s2

m is high relative to s2j which

suggests a high-competency signal.Quadrant 2 suggests exactly the opposite: varia-

tion in shocks to the domestic economy’s GDPgrowth is very similar to that of the global economies,suggesting that exogenous factors, rather than na-tional government officials, are shaping domesticeconomic outcomes. Hence s2

j is high relative to

FIGURE 1 Hypothetical Competency Signals from Domestic and International Economies

110 raymond m. duch and randy stevenson

s2m and the overall competency signal is low. Our

operationalization of the voter’s signal extractionefforts is similar to the signal extraction that occursin the ‘‘benchmark competition’’ literature. In Besleyand Case (1995) voters, motivated by selection con-cerns, use tax increases that are out of line with thosein neighboring states to make vote choices. Theirinsight is that tax increases in general are not a signalof excessive rent seeking by incumbents but taxincreases that are out line with neighboring taxincrease do represent a signal to voters about ‘‘badtypes.’’

In this essay we test two theoretical argumentssummarized in Row 1: (1) Are voters knowledgeableabout variations in shocks to the economy and canthey discern whether variations in national shocks aredistinct from those in other countries? (2) Do differ-ences in these variations condition the vote assuggested by our theory?

Row 2 illustrates how variations in a country’sexposure to global trade inform the competencysignal that conditions the economic vote. In Quad-rant 3 and 4 the bold lines represent total variation inthe shocks to GDP growth while the dotted linesindicate that portion of the variance that is associatedwith goods and services produced and consumeddomestically. The difference represents variation inthat portion of GDP shocks associated with goodsand services that are produced domestically butconsumed by foreign markets. The distance betweenthese two lines represent a signal regarding themagnitude of the competency variance s2

m in thecompetency signal. A narrow distance between thesetwo lines, illustrated in Quadrant 3, suggests that s2

m

is high relative to s2j which indicates a high com-

petency signal. This would be a national context thathas relatively less exposure to the effects of globaltrade and where we would predict high levels ofeconomic voting. Quadrant 4 with a large differencesuggests that s2

m is low relative to s2j which indicates

a low competency signal case. This is a nationalcontext with high exposure to the global trade andwhere we predict low levels of economic voting.

We propose to test two aspects of the theoreticalargument summarized in Row 2: (1) Are votersknowledgeable about the exposure of their domesticeconomies to shocks from global economic influen-ces? (2) Do differences in exposure to global tradeinfluences condition the economic vote as suggestedby our theory?

In this essay we demonstrate how economicoutcomes—seen from a competency perspective—can help us explain contextual variation in the

economic vote. We make two empirical points: votershave information about the economy that allowsthem to engage in the hypothesized signal extraction,and the magnitude of the economic vote responds tothese economic competency signals as hypothesized.

Microfoundations: Evidence from aSix-Nation Survey

Our competency theory assumes that voters haveinformation on the overall variance in shocks to themacroeconomy, s2

m þ s2j , and have strategies for

distinguishing between s2m and s2

j . We first examinewhether voters really have well-formed beliefs aboutthe variance in competence shocks to the economy?Or even about the total variation in shocks to theeconomy? Given the often-touted ignorance of voterswhen it comes to political and economic matters,some skepticism is surely warranted. Still, little directevidence on these questions is available in the existingliterature, and so we explore a variety of originalevidence that we have collected that will help usanswer them. This evidence includes a survey that weconducted that quizzes voters on their knowledge ofeconomic variation and its sources.

The Availability of Information aboutVariance in the Macroeconomy

Do the voters get much information about thevariance in economic outcomes? There is extensiveevidence that the media plays an integral role inshaping economic evaluations, which of course arecritical to the economic voting model (De Boef andKellstedt 2004; Duch and Stevenson 2004; Erikson,Mackuen and Stimson 2002). An important portionof the information regarding the economy that istransmitted by the media helps voters assess overallvariance in shocks to the macroeconomy. Mediareports of economic performance typically includeextensive references to how the economy has changedand what most often captures the attention of mediaoutlets are unexpected changes in macroeconomicoutcomes.

Voter Attention to Information aboutVariance in the Macroeconomy

Is there any reason to believe that the average voter indeveloped democracies pays any attention to

the economic vote 111

information regarding variance in economic out-comes?9 Some have argued that in fact fluctuationsin economic outcomes attract an equal, if not higher,amount of attention than levels of economic perform-ance from the voter. Quinn and Woolley (2001) arguethat voters pay considerable attention to volatility inaddition to rates of change in the macroeconomy, al-though they draw different conclusions regarding itsimplication for the economic votes.

There is little data on whether the media messageabout variance in the economy registers with thetypical voter. As a result, in the spring of 2005, weconducted a six-nation survey that explored voters’beliefs about the variation in their national econo-mies and its sources.10 One of the questions in thissurvey asked respondents the following question:‘‘Over the last four years would you say that theeconomy in [country] has experienced very stablegrowth, somewhat stable growth, somewhat unstablegrowth, or very unstable growth?’’

Of initial interest is whether responses to thisquestion show any systematic variation or whetherthey are just random. We assess this by examiningwhether there is significant agreement among re-spondents in their answers. Random answers wouldshow no such clustering but should be distributedrelatively uniformly. Further, if voters have well-formed beliefs about variation in the economy, thenthe proportion of ‘‘don’t know’’ responses should besimilar to their proportion in other surveys thatcollect other kinds of economic information.

Results from each of the six countries clearlysuggest that the question is meaningful. Figure 2indicates that in each of the countries we see a clearmodal response and relatively small variances aroundthe modal response. In Denmark, for example, overhalf the respondents choose the ‘‘somewhat stablegrowth’’ response. In no case is the modal responseless than 40% of the sample. Furthermore, thenumber of ‘‘don’t know’’ responses compare favor-ably with levels in other surveys soliciting morestandard types of economic beliefs. The highest levelof ‘‘don’t know’’ responses was 8.7% of the Danish

sample and the lowest was 1.1% of the France sample.These compare quite favorably, for example, to therange of ‘‘don’t know’’ responses to the standardquestion concerning retrospective evaluations of thenational economy: the highest level, again, was 7.5%of the Danish sample and the lowest level was 1% ofthe French sample.

We are also interested in whether there is sig-nificant cross-national variation in the average per-ceptions of economic volatility—again, this variationis part of the competency weight that conditions themagnitude of the economic vote. The left-hand graphin Figure 3 shows that average citizen perceptions ofthe stability of economic outcomes in their countryvary quite significantly across European nations.Danish and British respondents clearly perceive theirnational economies as turning in very stable growthover the previous four years. By contrast the Germansand Italian report high levels of instability in growthoutcomes. In short, these individual-level data supportthe idea that contextual variation in the economic votecould come, in part, from differences in the compe-tency signal (or at least voters’ beliefs about thissignal).

Of particular interest is whether cross-nationalvariation in perceptions of economic stability isgrounded in real variation in the economies of thedifferent countries. We expect citizens in contextswith highly variable economic outcomes to perceiveeconomic outcomes to be highly unstable. This isconfirmed by the data in the right hand graph inFigure 4: citizens in contexts where the fluctuationsin real GDP growth were highly unstable over the2000–05 period have perceptions of economic insta-bility that are higher than citizens in contexts withmore stable economic outcomes. The exception hereis Denmark where citizens, in spite of high fluctua-tions in real GDP, perceived their economy as beingstable. Note though that the relationship includingDenmark (the dashed regression line) is quite strongalthough without Denmark (the solid regression line)is extremely strong.

One explanation for the Danish exception, di-rectly related to the empirical findings presented inthe next section, is that Denmark is a relatively smalleconomy that is highly exposed to global tradeinfluences. We argue that voters recognize the impactof these exogenous global factors on variations innational economic outcomes. What we may be seeingin Figure 3 is Danish responses about the nationaleconomy that discount fluctuations related to globaleconomic shocks. And, since Denmark is highlyaffected by these global shocks, its citizens may have

9Our focus on the developed democracies excludes, for the mostpart, countries that have experienced dramatic variances inmacroeconomic outcomes and where there is no question thatcitizens have been concerned with variance in addition to growth.

10The survey was pretested in the United States in the earlyspring. The actual survey was conducted in Great Britain, Spain,Denmark, France, Italy, and Germany. The items were includedon an Omnibus telephone survey administered in each countryand supervised by IFOP, France.

112 raymond m. duch and randy stevenson

perceptions of fluctuations that are relatively modestcompared to citizens in the other five sample coun-tries which have quite large and more insulatedeconomies.

Our evidence, though based only on six coun-tries, is unique in its focus on economic variation andsuggests that voters have well-formed beliefs aboutvariation in their national economies and that thesebeliefs on balance are grounded in economic reality.

Distinguishing Domestic and InternationalEconomic Fluctuation

In the competency theory, we assume that, inaddition to knowing the overall variance in macro-economic shocks, voters also know the relativecontributions of s2

m and s2j to that total. While

political economy models often make this assump-tion (for example, Cukierman and Meltzer 1989;Rogoff and Sibert 1988), there is little effort toexplore empirically whether citizens have perceptionsconsistent with this characterization.

If voters have a sense of the total variation ineconomic shocks (i.e., s2

m and s2j), then they can

distinguish between the relative contributions of thedifferent components of this total variation if theyhave well-formed beliefs about either one. So, forexample, if they know how important exogenousshocks are in their national economy (at a particulartime) and they know how much the economy variesin general, they should have a sense of how much‘‘room’’ there is for the competence of the electedgovernment to impact the economy.

Row 1 of Figure 1 illustrated one signal extractionstrategy that builds on voters’ knowledge aboutstability in the domestic and international macro-economies. Voters can inform themselves of therelative importance of exogenous versus competencyshocks in national economic outcomes by bench-marking fluctuations in domestic macroeconomicoutcomes against those in the overall global econ-omy. An interesting example here are the recentfindings of Ebeid and Rodden (2006): they establishthat voters in U.S. state elections condition theireconomic vote by making comparisons between stateand national economic outcomes.11 This, of course, isconsistent with Besley and Case (1995) who find thatvoters, motivated by selection concerns, use taxincreases that are out of line with those in neighbor-ing states to make vote choices.

We hypothesize that voters know whether toattribute shocks to the macroeconomy to competencerather than exogenous factors by observing howfluctuations in the domestic economy deviate signifi-cantly from those in the broader global economy.12

Our reasoning, illustrated in Row 1 of Figure 1, isthat if fluctuations in the domestic economic closelytrack fluctuations in the global economy voters areless likely to attribute fluctuations in macroecono-mic shocks to incumbent government policy makers.

FIGURE 2 Histogram of Volatility of Economic Perceptions, Europe

11Wolfers (2006) makes the opposite case using state-levelelection data. He suggests that voters reward/punish incumbentsfor economic outcomes beyond their control (such as oil priceshocks in oil producing states).

12This assumes that a significant portion of the exogenous shocksto an economy comes from the global economy.

the economic vote 113

On the other hand, if the fluctuations in the domesticeconomy differ significantly from the global economyvoters are more likely to attribute shocks to themacroeconomy to incumbent policy makers. We canuse our six-nation European survey to illustrate whatwe mean here and test whether, in fact, these devia-tions in perceptions result in higher levels of economicvoting.

We begin by using our six-nation survey resultsto explore how perceptions regarding fluctuations inthe domestic economy deviate from those regardingthe overall global economy—here we focus onEurope and treat the overall European economy asthe global referent. The survey asked respondents toassess the stability of both their national economiesand the overall European economy.13 Table 1 presentsa cross-tabulation of responses to these two questions.The entries are the numbers of respondents falling ineach cell. Respondents falling along the diagonal hadidentical responses for both their domestic economyand the European economy. Off-diagonal respondentsperceived domestic fluctuations as deviating fromthose of the overall European economy. Approximately

50% fall on the diagonal with the other 50% falling onthe off-diagonal cells.

One strategy that voters may employ for distin-guishing competency shocks from exogenous shocksto the macroeconomy is examining whether fluctua-tions in the domestic economy differ significantlyfrom those in the overall global economy—or, in thiscase, the overall European economy. To the extentthat domestic fluctuations are distinct from broaderglobal fluctuations, voters may attribute domesticmacroeconomic shocks to political initiatives, i.e.,competency, and have a higher propensity to cast aneconomic vote. This implies that respondents fallingin the off-diagonal cells of Table 1 are more likely toengage in economic voting.

We evaluate this argument empirically by againemploying the six-nation survey data. Respondentswere asked to report their likely vote choice if anelection were held in the coming days.14 Responses tothis question were used to create a dichotomousincumbent vote variable (respondents preferringparties in the governing coalition were coded as 1with the remaining respondents coded as 0). The firstcolumn of Table 2 reports the probit estimates forthis simple vote equation (country dummies are

FIGURE 3 Volatility of Real GDP and Economic Perceptions, Europe

22

.53

3.5

Me

an

Pe

rce

ptio

ns o

f E

co

no

mic

Sta

bili

ty 2

00

5

Denmark UK Spain France Germany Italy

Perceived Economic Volatility, Europe 2005

Denmark

France

Germany

Italy

Spain

UK

22

.53

3.5

.8 1 1.2 1.4 1.6

Standard Deviations of Real GDP Growth 2000-05

Perceived and Actual Economic Volatility

13The Europe economy question was worded as follows: ‘‘Overthe last four years would you say that the European economieshave experienced very stable growth, somewhat stable growth,somewhat unstable growth, or very unstable growth?’’

14The British questioning wording is as follows: ‘‘If a generalelection were held next Sunday which political party would youvote for?’’

114 raymond m. duch and randy stevenson

included in the regression). As we would expect,retrospective national economic evaluations arestrongly correlated with incumbent vote intention.

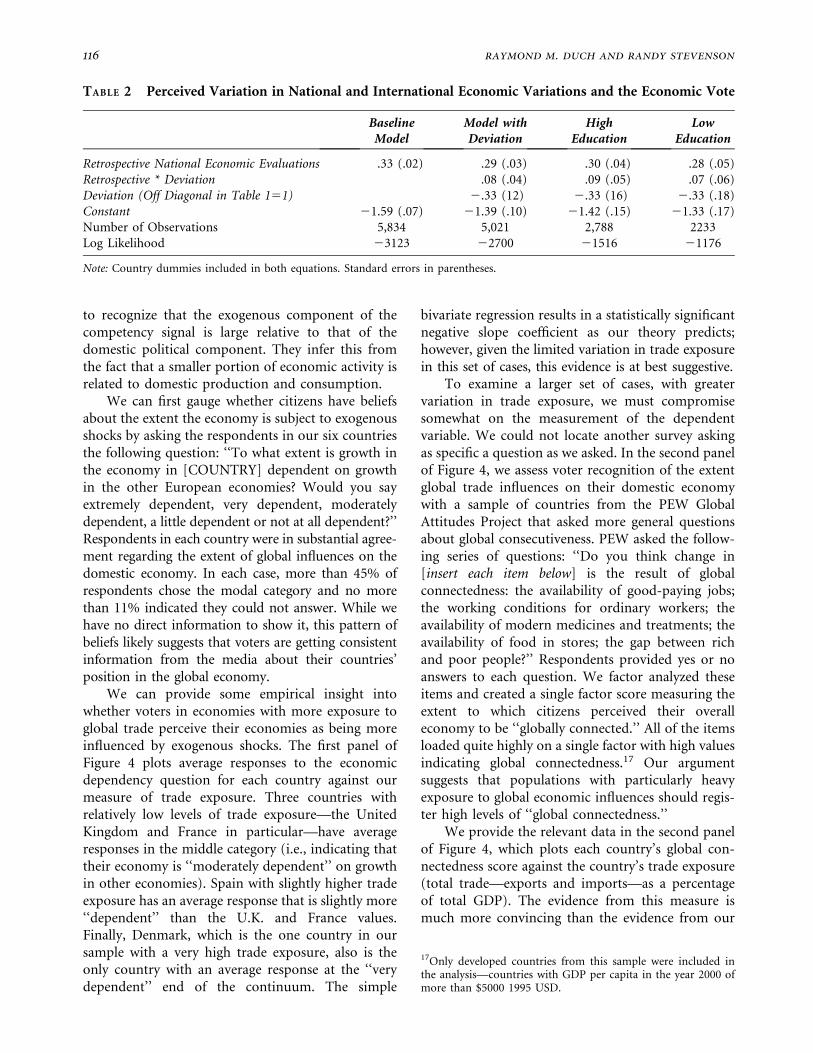

To test the notion that the off-diagonal respond-ents have a higher propensity to cast an economicvote we created a dummy variable (deviation) thathas a value of 1 for all those respondents falling inthe off-diagonal cells. This variable, interacted withthe economic evaluation variable, indicates whetherthe off-diagonal respondents have in fact higher levelsof economic voting as we hypothesis. The secondcolumn of Table 2 reports these results. As we hy-pothesized respondents who perceive distinct differ-ences in the fluctuations of their national economiesare more likely to exercise an economic vote.

In this essay we do not pretend to provide acomplete account of how voters acquire this infor-mation about variations in shocks to the global anddomestic economy. But our intuition, supported bysome preliminary analysis, suggests that voters live ina media context that informs them about the domesticand international economies.15 Our argument impliesthat the media respond to variations in macroeco-nomic outcomes as opposed to simply focusing on themagnitude of economic indicators. And we find, forexample, that the count of U.S. media stories con-cerning inflation or unemployment is higher duringperiods in which the standard deviations of actualinflation or unemployment outcomes are high (Duchand Stevenson 2008).

This suggests that the costs to voters of informingthemselves about exogenous and competency shocksto the macroeconomy are not high. The data (notshown here) suggest that in general this appears to bethe case. For each country we estimated bivariateprobit equations with deviation as the dependent

variable (0 for those on the diagonal and 1 for thoseoff the diagonal) and education as the explanatoryvariable. With one exception, Italy, the coefficients oneducation were statistically insignificant. These resultssuggest that the costs to voters of informing them-selves about exogenous and competency shocks to themacroeconomy are not particularly high.

A second issue is whether the conditioning of theeconomic vote based on the competency signal variesby levels of sophistication. There is some evidencethat more highly educated respondents are morelikely to condition their economic vote on informa-tion regarding competency shocks to the macro-economy. In Table 2 we estimate the interactionmodels for high- versus low-education groups in thepopulation. The interaction term remains just barelysignificant for the highly educated groups but is notstatistically significant for the low-educated groups.It may be the case—although this evidence is onlysuggestive—that more sophisticated voters are morelikely to learn about candidate competency.

One assumption of our competency theory is thatvoters know about the variance in exogenous shocks(relative to the variance in competency shocks) to themacroeconomy. Our evidence suggests that voters areinformed about how much the domestic economyis subject to exogenous shocks from the globaleconomy.16

Competency and Exposure to Global Trade

Row 2 of Figure 1 suggests a second signal extractionstrategy that voters can employ: In economies ex-posed to global trade shocks voters are hypothesized

TABLE 1 Perceptions of Stability of National and European Economies

European Economy

National Economy Very Stable Somewhat Stable Somewhat Unstable Very Unstable Total

Very Stable 86 143 116 27 372Somewhat Stable 105 1114 596 90 1905Somewhat Unstable 35 543 836 131 1545Very Unstable 27 286 446 484 1243Total 253 2086 1994 732 5065

15This is similar to the argument made by Besley and Case (1995)regarding benchmark competition regarding tax rates amongstneighboring states. They argue that the media provides voterswith benchmarked information about tax rates from neighboringstates.

16We realize, of course, that not all exogenous shocks to theeconomy arise from nondomestic sources. Indeed, the theoryonly distinguishes between governmental and nongovernmentalshocks, where the nongovernmental category includes shocksarising from the behavior of any economic actor who voters donot include in the government whose competency they wish toevaluate.

the economic vote 115

to recognize that the exogenous component of thecompetency signal is large relative to that of thedomestic political component. They infer this fromthe fact that a smaller portion of economic activity isrelated to domestic production and consumption.

We can first gauge whether citizens have beliefsabout the extent the economy is subject to exogenousshocks by asking the respondents in our six countriesthe following question: ‘‘To what extent is growth inthe economy in [COUNTRY] dependent on growthin the other European economies? Would you sayextremely dependent, very dependent, moderatelydependent, a little dependent or not at all dependent?’’Respondents in each country were in substantial agree-ment regarding the extent of global influences on thedomestic economy. In each case, more than 45% ofrespondents chose the modal category and no morethan 11% indicated they could not answer. While wehave no direct information to show it, this pattern ofbeliefs likely suggests that voters are getting consistentinformation from the media about their countries’position in the global economy.

We can provide some empirical insight intowhether voters in economies with more exposure toglobal trade perceive their economies as being moreinfluenced by exogenous shocks. The first panel ofFigure 4 plots average responses to the economicdependency question for each country against ourmeasure of trade exposure. Three countries withrelatively low levels of trade exposure—the UnitedKingdom and France in particular—have averageresponses in the middle category (i.e., indicating thattheir economy is ‘‘moderately dependent’’ on growthin other economies). Spain with slightly higher tradeexposure has an average response that is slightly more‘‘dependent’’ than the U.K. and France values.Finally, Denmark, which is the one country in oursample with a very high trade exposure, also is theonly country with an average response at the ‘‘verydependent’’ end of the continuum. The simple

bivariate regression results in a statistically significantnegative slope coefficient as our theory predicts;however, given the limited variation in trade exposurein this set of cases, this evidence is at best suggestive.

To examine a larger set of cases, with greatervariation in trade exposure, we must compromisesomewhat on the measurement of the dependentvariable. We could not locate another survey askingas specific a question as we asked. In the second panelof Figure 4, we assess voter recognition of the extentglobal trade influences on their domestic economywith a sample of countries from the PEW GlobalAttitudes Project that asked more general questionsabout global consecutiveness. PEW asked the follow-ing series of questions: ‘‘Do you think change in[insert each item below] is the result of globalconnectedness: the availability of good-paying jobs;the working conditions for ordinary workers; theavailability of modern medicines and treatments; theavailability of food in stores; the gap between richand poor people?’’ Respondents provided yes or noanswers to each question. We factor analyzed theseitems and created a single factor score measuring theextent to which citizens perceived their overalleconomy to be ‘‘globally connected.’’ All of the itemsloaded quite highly on a single factor with high valuesindicating global connectedness.17 Our argumentsuggests that populations with particularly heavyexposure to global economic influences should regis-ter high levels of ‘‘global connectedness.’’

We provide the relevant data in the second panelof Figure 4, which plots each country’s global con-nectedness score against the country’s trade exposure(total trade—exports and imports—as a percentageof total GDP). The evidence from this measure ismuch more convincing than the evidence from our

TABLE 2 Perceived Variation in National and International Economic Variations and the Economic Vote

BaselineModel

Model withDeviation

HighEducation

LowEducation

Retrospective National Economic Evaluations .33 (.02) .29 (.03) .30 (.04) .28 (.05)Retrospective * Deviation .08 (.04) .09 (.05) .07 (.06)Deviation (Off Diagonal in Table 151) 2.33 (12) 2.33 (16) 2.33 (.18)Constant 21.59 (.07) 21.39 (.10) 21.42 (.15) 21.33 (.17)Number of Observations 5,834 5,021 2,788 2233Log Likelihood 23123 22700 21516 21176

Note: Country dummies included in both equations. Standard errors in parentheses.

17Only developed countries from this sample were included inthe analysis—countries with GDP per capita in the year 2000 ofmore than $5000 1995 USD.

116 raymond m. duch and randy stevenson

more limited sample. Countries with high levels oftrade exposure tend to be those in which theirpopulation recognizes the extent to which the do-mestic economy is subject to global economic influ-ences. That said, the fact that this measure of ourdependent variable captures perceptions of globalconnectedness broadly defined, rather than the morespecific notion of economic connectedness, means weshould not expect its relationship with trade depend-ence to be perfectly linear. Specifically, since themeasure includes perceptions of global influenceson both economic outcomes and social outcomes,trade (a decidedly economic form of connectedness)may be sufficient to engender perceptions of con-nectedness using this measure, but is unlikely to benecessary. Even when trade is low, a given populationmight be connected to the rest of the world in otherways—reflecting, perhaps, a particular cultural andsocial orientation—that would be reflected in thisbroad ‘‘perceptions of global connectedness’’ meas-ure. The placement of Japan in the second panel ofFigure 4 may be a case in point. Japanese perceptionsof global connectedness are much higher than theirtrade exposure would predict and so is an outlierfrom the point of view of this paper. However, thisresult would hardly surprise to students of Japanesesociety, some of whom have demonstrated the exis-tence of specific perceptual biases (resulting from socialinstitutions and norms) that encourage the view that

society and the world more generally should be under-stood as highly interconnected (e.g., Nisbett 2003).

A Summary of the Microevidenceand Some Caveats

The competency model of rational retrospectiveeconomic voting makes two assumptions regardingvoter knowledge about the economy. First, the theoryassumes that voters know the total variance in shocksto the macroeconomy. Our six-nation survey resultssuggest that individual perceptions about the vola-tility of the macroeconomy are reasonably wellinformed: cross-national perceptions of macroeco-nomic variability correlate quite highly with themagnitudes of actual variations in real GDP.

Second, the theory assumes that voters are able todistinguish variations in competency shocks fromvariations in exogenous shocks to the macroecon-omy. If we assume that a large part of the exogenousshocks in the economy originate in global fluctua-tions and that a large part of domestic shocks areattributable to the competence of politicians, theresults of both our six-nation study and the PEWGAP suggest that voters do have the information tomake such distinctions. Specifically, voters appear tounderstand the extent to which their economies aresubject to shocks from the international economy.

FIGURE 4 Trade and Perceptions of Global Dependency

Denmark

FranceGermany

ItalySpain

UK

A Little Dependent

Very Dependent22.5

33.5

4

Perc

eiv

ed D

epedency o

n O

ther

Euro

pean E

conom

ies

50 60 70 80

Trade as Percent of GDP (2000)

Perceived Dependence=4.25(.54) - .02(.008)

X Trade/GDP R-Square=.48

Trade and Percpetions of Trade Dependency

argentina

canada

czech re

francegermany

italy

japan south koreagreat britain

us

-.6

-.4

-.2

0.2

Perc

eiv

ed G

lobal C

onnecte

dness F

acto

r S

core

s (

PE

W)

0 50 100 150

Trade as Percent of GDP (2000)

Perceived Global Connectedness=-.36(.10) + .004(.001)

X Trade/GDP R-Square=.41

Trade and Percpetions of Global Connectedness

the economic vote 117

Our individual-level analysis of differences inbeliefs (and economic voting) among voters addsfurther support to the plausibility of our contextualhypotheses, which is based on an individual-levelrelationship: voters who perceive that the variation inthe national economy differs from variation in theglobal economy seem to use the economy more in theirvote choice. This is certainly consistent with the ideathat these voters attribute a larger share of the variancein the economy to the actions of domestic politiciansrather than to exogenous shocks and so glean a re-latively stronger signal about the competence of theincumbent government from perceived fluctuations inthe economy. Finally, with respect to informationcosts: we find very little evidence that variations ineducation levels affect the ability of voters to distin-guish exogenous from competency shocks to themacroeconomy. On the other hand, we do find someevidence that the extent to which voters use thisinformation to condition their economic vote is moreprevalent amongst the more highly educated voters.

Macrolevel Findings from 163Election Studies

The previous section provided encouraging empiricalsupport for the microfoundations of our competencytheory of the economic vote. We now focus on theempirical evidence indicating that voters use thisinformation about the macroeconomy and structuralfeatures of the domestic economy to condition theireconomic vote. Again, we have two principal hypoth-eses here: (1) economic voting will be higher indomestic contexts in which variations in shocks tothe domestic economy deviate from those for theglobal economy; and (2) exposure of the domesticeconomy to global trade will reduce the magnitude ofthe economic vote.

The Data: Cross-National Mappingof the Economic Vote

The dependent variable in our macrolevel empiricalanalysis is the estimate of the Chief Executive economicvote for each of 163 voter preference surveys conductedin 19 countries during the 1979–2005 period. A de-tailed description of how these estimates are derivedand a discussion of our two-stage multi-level analy-sis approach are available in Duch and Stevenson(2005 and 2008) and at www.raymondduch.com/economicvoting. Hence, in this essay we only provide

a brief overview of how these estimates were derived.For each of the 163 voter preference studies in oursample we estimate the economic vote of the ChiefExecutive defined as any decrease (increase) in sup-port for the party of the incumbent Chief Executivethat is caused by worsening (improving) economicperceptions. Each of these 163 studies includes a votepreference question and the respondent’s retrospec-tive evaluation of the overall economy. These are thecore questions for our analysis, and they are roughlysimilar across all of the 163 studies. In addition, weinclude control variables in the estimation that reflectthe types of variables typically included in thespecification of vote choice equations: socioeconomiccleavages, policy measures, left-right self-placement,and partisanship where appropriate. In each coun-try’s logit model specification, we include the appro-priate set of control variables that are necessary toensure consistent estimates for the economic evalua-tion variable.18

We then use these estimated coefficients togenerate predicted changes in each individual’s voteprobabilities associated with a change in the individ-ual’s economic perceptions. We define a ‘‘meaningfulchange’’ as a change in opinion that results frommoving each respondent’s economic perception oneunit in the direction of a worsening economy. Thisrepresents a reasonable shift in economic perceptionsbased on our assessment of the distribution ofeconomic perceptions in the 163 surveys. The controlvariables are held constant at the values they take onfor each individual in the sample.19 This gives usestimates of the change in the Chief Executive party’svote probabilities associated with a unit deteriorationin economic perceptions.

Competency Signals from Variations inShocks to the Domestic and Global

Macroeconomies

Recall from Row 1 of Figure 1 that our theorysuggests that variation in shocks to the domesticeconomy that deviate from variations in globaleconomic shocks inform voters about the economic

18The models and the parameter estimates for each of theseelections studies are available at www.raymondduch.com/economicvoting.

19Our estimates of the impact of a change in economic percep-tions on vote probabilities is generated in a fashion that alsoproduces estimates of uncertainty about the economic votemeasure for each case. We accomplish this by sequentiallyapplying the simulation procedure detailed in King, Tomz, andWittenberg (2000) to each respondent in each sample. Weprovide details of this estimation in Duch and Stevenson (2008).

118 raymond m. duch and randy stevenson

competency of incumbent governments. At any pointin time the voter observes that an economic indicatoris high, low, or possibly in line with expectations. Theoverall global average outcome provides the voter withtwo important pieces of information. First, the coun-try may always experience higher (or lower) economicshocks and hence some of the difference between theglobal economic outcome and the country outcomecan be attributed to a country effect. This typicalcountry deviation from the global mean constitutesthe voters’ expectations regarding economic outcomes(it is constant and hence is factored into the long termequilibrium component, �y, of equation (1.1)). But atany point in time variation in economic shocks willdeviate from this expectation, or country effect. Hencesome of the deviation between the global mean andcountry outcome will be associated with a time orperiod effect—unique to that particular time point(but shared by all the countries). A period effect isvariation in economic shocks that is shared by allcountries and hence in our theory is attributed to s2

j ,the nonpolitical, or random, shocks to the macro-economy. It is a shock to the domestic economy thatresults from global economic factors that are notattributable to elected political decision makers.

But not all of the variation between the globalmean and the country outcome can be accounted forby a country effect (part of the voters’ long-termexpectations and hence uninformative about thecompetency signal) or by a time effect (variationsin economic shocks associated with random, non-political factors). There will be a residual compo-nent—after accounting for the country and periodeffects—which we associate with s2

m the competency,or political, term in the competency signal. This isunexpected variation in shocks to the macroeconomythat are neither associated with the country’s generalrelative performance compared to the global meannor with a period shock that is experienced by allcountries in the global economy.

Estimates of these three quantities—the countryeffect, period effect, and residual component—can beobtained from a variance components model in whichthe dependent variable is the particular economicindicator (CPI, real GDP growth, and the unemploy-ment rate); there are no covariates in the model and thegrouping of observations is by country and by time.20

Specifically, we estimate the following equation:

yit 5 aþ mi þ tt þ nit ð1:13Þ

where a is the mean of yit, mi is a random effect forcountry i, tt is a random effect for time t, and nit isthe remaining variation that is neither associated witha country effect (some countries are typically morevolatile than the overall global economy) or with atime effect (for example, all countries in 1992 mighthave experienced a shock). In the case of each of ourthree indicators we estimate a simple random effectsmodel that associates variation in the indicators witheach of the four components in equation (1.13).

As we pointed out earlier, the portion of thevariance that is time specific is not informative ofpolitical competency—this is essentially a periodshock effect that is experienced by all countries andhence is not associated with domestic political deci-sion makers (a classic example is the impact of oilprices on inflation rates). It is the residual portion ofthe variance that is neither associated with a countrynor a time effect that is informative of politicalcompetency.21 In the case of CPI, real GDP growthand unemployment there is in fact a relatively largeportion of the variance accounted for by the residualterm (15%, 27%, and 30%, respectively).

Recall from our theoretical proposition in equa-tion (1.12), that the political competency term is thevariation in shocks to the macroeconomy associatedwith the incumbent government. Hence it is notsimply the magnitude of the residual term, nit, for aparticular country i at time t, but rather s2

n for a par-ticular country i evaluated over some time period t.In order to explore the impact of the variations inthese economic shocks on the economic vote for eachof the three economic indicators we calculatethe standard deviation of the residual terms over12-month time periods for each of the countries inour sample.22 As a result, a country that has a residualterm that is relatively constant over these 12-monthperiods—regardless of its magnitude—would have a

20The model is estimated using Stata 10.0’s xtmixed function.

21We say informative because we recognize that this residual is anoisy measure of the competency signal. One could, for example,imagine overstating the extent of government competencybecause it characterizes what we label as domestic shocks asbeing indicators of governmental influence over the economy.We do not deny that some of the residual shocks will be non-governmental. We believe that, while noisy, the signal as we havemeasured it is compelling because it approximates the compe-tency signal term that is found in the formal model.

22We obtain these residuals from the model in equation . Foreach observation of the macroeconomic indicator in the data set(recall that the observations are monthly for CPI and unemploy-ment and quarterly for GDP growth), this model will apportionthe observed value amongst four components: a constant term(or grand mean); a country effect; a period effect; and theresidual. We then estimate how much this residual effect variesover each 12-month period in our data set.

the economic vote 119

small standard deviation. In contrast, a country thathad a residual term that was sometimes high andsometimes low would have a high standard deviation.Our theoretical expectations is that in the first case(a small standard deviation) voters would concludethat the policies of the incumbent have little impactbecause national outcomes, once controlling for theglobal mean and for country and period effects, alwaysessentially remain the same. We believe this constitutesone signal regarding the size of the variance ineconomic shocks attributable to the incumbent gov-ernment (s2

m) relative to the overall variance ineconomic shocks to the economy s2

m þ s2j

� .

We hypothesize that the magnitudes of thesevariances—our measure of the magnitude of theincumbent’s competence signal—are correlated withthe strength of economic voting in our sample ofdemocracies. In order to test this hypothesis wedefine the dependent variable as the economic voteof the Chief Executive measure described earlier thatis based on a total of 163 election studies in 19countries for the period 1979–2005. Our independentvariable is the sum of the standard deviations of thethree macroeconomic residual terms defined above(for CPI, unemployment, and real GDP Growth).The plot in Figure 5 of economic vote of the ChiefExecutive against our composite measure of variationin macroeconomic shocks supports our hypothesis—note the slope coefficient in the bivariate regression isstatistically significant at the 0.05 level with a t-statisticof 1.98. Variation in shocks to the macroeconomy thatare neither associated with a country or period effectprovide voters with a signal about competency of

domestic decision makers and hence result in higherlevels of economic voting.

Competency Signals from Variations inExposure to Global Trade

Our theoretical argument summarized in Row 2 ofFigure 1 suggests that exposure of the domesticeconomy to global trade has a negative impact onthe competency signal and reduces the magnitude ofthe economic vote. To evaluate this argument weemploy a measure of Trade Openness from theWorld Bank which is a ratio of total trade to grossdomestic product (GDP; World Bank 2004). Figure 6presents a plot of the economic vote of the ChiefExecutive against our measure of Trade Openness.First, there clearly is no evidence that the economicvote is higher in open economies as some haveclaimed (Scheve 2001). In fact, openness of theeconomy leads to a significantly smaller economicvote (the t-statistic for trade openness is 2.37 (sig-nificant at the 0.05 level).23 This lends support toour argument that the competency signal in open

FIGURE 5 Economic Vote and Fluctuations in Macro-economic Shocks

fr

fr

fr

frfr

fr

fr

frfr

fr

fr

fr

fr

nl

nl nlnl

nl

nl

dede

de

de

it

it

it

it

it

itit

dk dk

dk

dk

dkir

ukuk

uk

ukuk

uk

uk

uk

uk

uk

uk

uk

uk

uk

uk

uk

uk

gc

sp

sp

sp

pt

pt

no

nono

no

ca

ca

ca

ca

us

us

us

us

us

us

us

us

us

us

us

us

us

us

usus

us

us

us

us

-.1

-.05

0.0

5

Chie

f E

xecutive

Eco

no

mic

Vote

0 1 2 3

Standard Deviation of Macro-economic Shocks

Economic Vote= -0.02(0.007) + -0.01(.006) X Std Dev (GDP+CPI+Unemploy) R-Square=.03

23We have estimated a hierarchical model in which the dependentvariable is individual vote for or against the incumbent party andthe independent variables are economic evaluations along with anumber of controls (left-right identification in particular). In arandom coefficients specification the coefficients on economicevaluations are modelled as a function of trade openness. Theestimated trade-openness effects on economic evaluations arestatistically significant and in the expected direction, as are anumber of the control variables in these models. This suggeststhat while the relationship in Figure 6 appears fragile, in fact thehierarchical model suggests it is quite robust.

120 raymond m. duch and randy stevenson

economies is weaker than in closed economies whichin turn leads to lower levels of economic voting.

In this section we have addressed two macrolevelempirical implication of our competency theory ofthe economic vote: first, the theory presumes thatfluctuations in the macroeconomy provide the aver-age voter with signals regarding incumbent compe-tence and that our measure of the economic vote iscorrelated with these fluctuations in a fashion con-sistent with our theory. One operationalization of thecompetency signal is variation in macroeconomicshocks that is neither associated with unique countryfactors nor with temporal trends—essentially thevariation in the residuals of a variance decompositionmodel that controls for country and temporal effects.We demonstrate that in fact this variable (variation inthe residuals of GDP growth, CPI, and unemploy-ment) is correlated with the magnitude of the eco-nomic vote.

Second, our theory suggests that in an openeconomy the exogenous term in our competencysignal is high—more of the variation in shocks to the

macroeconomy result from factors unrelated toactions by elected decision makers—and hence eco-nomic outcomes should get less weight in the voteutility function. The empirical results support thiscontention also: economic voting is more subdued ineconomies with more exposure to global trade.

Conclusion

Economic voting is an important phenomenon inmature democracies. At the same time though themagnitude of the economic vote varies quite dra-matically, and there are contexts and periods inwhich there is no economic voting or a very weakeconomic vote. We summarize a competency theoryof rational economic voting that identifies the cir-cumstances in which we would expect high levels ofeconomic voting and those in which we would expectlow levels. If variation in what we are calling thecompetent, or political, component of economic

FIGURE 6 Trade Openness and Economic Vote

FR

FRFR

FRFR

FR

FRFR

FR

FR

FR

FR

BE

BE

BE

BE

BE

BEBE

BE

BE

BE

BE

BE

NL

NL

NL

NL

NL

NL

NL

NL

NL

NL

NL

NL

DE

DE

DE

DEDE

DE

DEDE

DE

DE

DE

DE

IT

IT

IT

IT

IT

IT

DK

DKDK

DK

DK

DK

DK

DK

DK

DK

DK

DK

DK

DK

IE

IE

IEIE

IE

IE

IE

IE

IE

IE

IE

GB

GB

GB

GB

GB

GBGB

GB

GB

GB

GB

GB

GB

GB

GB

GB

GR

GR

GR

GR

GR

GR

GR

GR

GR

GR

GR

ES

ES

ES

ESES

ES

ES

ESES

ES

PT

PT

PTPT

PT

PT

PT

PT

NO

NONO

NOSE

SESE

SE

CA

CA

CA

CA

AU

AU

AU

AUAU

NZ

NZ

NZ

USUS

US

US

US

US

IC

-0.1

5-0

.10

-0.0

50

.00

0.0

5

Econom

ic V

ote

for

Chie

f E

xecutive P

art

y

0 50 100 150

Trade Openness

Source: Total Trade as Percent of GDP; World Bank, 2004Equation: Chief Executive Economic Vote = -.07 (.01) + .0003 (.0001) * Trade Openness. Standard errors are in parentheses.The adjusted R-square is .04. N=151.

the economic vote 121

performance signals is large relative to variation inthe non-political component of these signals, thenchanges in the economy will provide a strong signalabout the competency of the incumbent and the voterwill weigh the retrospective economy more heavily inher utility function. Alternatively, perceived economicoutcomes that are above or below the natural rate are apoor signal of the incumbent’s competence if observedoutcomes are more likely to result from nonpoliticalshocks than from competency shocks. In this essay wefocus on demonstrating empirically how economiccontexts provide voters with information that allowsthem to assess the competency of incumbents forshocks to the macroeconomy (unexpected growth inthe economy, for example).

First, we present a body of individual-level datasuggesting that individual voters are informed aboutthe economy in a fashion consistent with the com-petency argument, and they use this information toinform their economic vote as our theory predicts:individual perceptions about the volatility of themacroeconomy are reasonably well informed; votersappear to understand the extent to which their eco-nomies are subject to shocks from the internationaleconomy; and voters who perceive that the variationin the national economy differs from variation in theglobal economy seem more inclined to exercise aneconomic vote.

Secondly, we demonstrate that fluctuations in thedomestic and global economies provide the averagevoter with information necessary to distinguishexogenous from political shocks to the macroecon-omy and hence to establish the competence of theincumbent policy maker. Two empirical findingsmake this case: We show that variations in shocksto the macroeconomy are correlated with the magni-tude of the economic vote in a fashion consistentwith our theory. And we demonstrate that the eco-nomic vote is more subdued in economies withhigher exposure to global trade.

The puzzle motivating this essay is the absence ofeconomic voting in some contexts. In our opinionselection theories gives us the most traction foridentify circumstances in which voters will minimizethe importance of economic evaluations in their votedecision. In this essay we summarize our competencytheory of economic voting; demonstrated that indi-vidual voters have the information necessary todetermine competency; and provided empirical evi-dence of the predicted relationship between ourmeasures of the competency signal and economicvoting. We believe this is a strong endorsement of acompetency theory of the economic vote.

Acknowledgments

This paper was originally prepared for presentation atthe 2006 annual meeting of the American PoliticalScience Association, Philadelphia. It was awarded theBest Paper in Political Economy presented at the2006 American Political Science Association Meeting.We acknowledge the generous support of the NationalScience Foundation that funded this project with grantSBR-0215633. Also we are very appreciated of the in-valuable comments we received from Jim Alt, RobFranzese, and Bing Powell. The assistance of DaveArmstrong and Jeff May on data issues was partic-ularly helpful. But of course any errors here are theresponsibility of the authors.

Manuscript submitted 9 May 2008Manuscript accepted for publication 23 April 2009

References

Achen, Christopher, and Larry Bartels. 2002. ‘‘Blind Retrospec-tion: Electoral Responses to Draught, Flu, and Shark Attacks.’’Presented at the annual meeting of the American PoliticalScience Association.

Alesina, A., and H. Rosenthal. 1995. Partisan Politics, DividedGovernment, and the Economy. Cambridge: Cambridge Uni-versity Press.

Besley, Timothy, and A. Case. 1995. ‘‘Incumbent Behavior: VoteSeeking, Tax Setting and Yardstick Competition.’’ AmericanEconomic Review 85 (1): 25–45.

Cheibub, Jose Antonio, and Adam Przeworski. 1999. ‘‘Democ-racy, Elections, and Accountability for Economic Outcomes.’’In Democracy, Accountability, and Representation, eds. AdamPrzeworski, Susan C. Stokes, and Bernard Manin. Cambridge:Cambridge University Press, 222–49.

Cukierman, Alex, and Allan H. Meltzer. 1989. ‘‘A Political Theoryof Government Debt and Deficits in a Neo-Ricardian Frame-work.’’ American Economics Review 79: 713–33.

De Boef, Suzanna, and Paul M. Kellstedt. 2004. ‘‘The Political(and Economic) Origins of Consumer Confidence.’’ AmericanJournal of Political Science 48 (4): 633–49.

Downs, Anthony. 1957. An Economic Theory of Democracy. NewYork: Harper and Row.

Duch, Raymond M., and Randy Stevenson. 2008. Votingin Context: How Political and Economic Institutions Con-dition Election Results. Cambridge: Cambridge UniversityPress.

Duch, Raymond M., and Randy Stevenson. 2005. ‘‘Using Multi-ple Surveys to Explore Contextual Variation in BehavioralRelationships: The Case of Economic Voting.’’ PoliticalAnalysis 13 (4): 387–409

Duch, Raymond M., and Randy Stevenson. 2004. ‘‘The Econ-omy: Do they get it Right and does it Matter?’’ Presented atthe annual meeting of the Midwest Political ScienceAssociation.

122 raymond m. duch and randy stevenson

Ebeid, Michael, and Jonathan Rodden. 2006. ‘‘Economic Geog-raphy and Economic Voting: Evidence from the U.S. States.’’British Journal of Political Science 36: 527–47.

Erikson, Robert S., Michael B. Mackuen, and James A. Stimson.2002. The Macro Polity. Cambridge: Cambridge University Press.

Greene, William H. 2003. Econometric Analysis Fifth Edition.Upper Saddle River, NJ: Prentice Hall.

Hibbs, Douglas A., Jr. 2006. ‘‘Voting and the Macro-economy.’’In The Oxford Handbook of Political Economy, eds. BarryWeingast and Donald Whittman. New York: Oxford Univer-sity Press, 565–86.