Embed Size (px)

Citation preview

Growing equity, realizing value

ManagementConsulting

Engineering

IT Services

HumanResources

MediaAgencies

The Global Management Consulting M&A Report 2017Vital research on global M&A trends for owners of consulting businesses.

The Global Management Consulting M&A Report 20172

3

Foreword 4

Your regional contacts 5

Management Consulting 8

At a glance 8

Overview of M&A activity 9

Deal size distribution 11

Regional review 12

Overview of equity market performance 13

Valuation multiples and trends 15

Strategic and private equity buyer trends 17

Selected M&A transactions 18

Appendix 22

Key definitions 22

A quick word on the data 23

About Equiteq 24

Further resources 24

Disclaimer 25

Contents

Contents© Equiteq Advisors Ltd. 2017

The Global Management Consulting M&A Report 20174

Foreword

Foreword

Welcome to our annual review of M&A and equity market trends within the Management Consulting industry.

This year’s report considers the global developments impacting M&A across the Management Consulting sector, together with a comprehensive analysis of the Equiteq Management Consulting Share Price Index, the only published share price index for the industry.

Management consulting capabilities are in strong demand across sectors, as strategic buyers in adjacent consulting segments use these services as a gateway to boardrooms to cross-sell and protect market share for their own offerings. This is part defensive, in response to the large global Management Consulting players own diversification strategies and part due to opportunities presented by digital transformation consulting firm’s innovation and deployment of advanced analytics tools, software, cloud solutions and managed services

M&A activity was robust against a backdrop of slow global economic growth and an unsettled political environment following the UK’s vote to Brexit and the US Presidential elections. Premium pricing and competition for assets is being supported by increasing valuations of listed Management Consulting firms, along with cash-rich buyer’s quests for new avenues of growth in rapidly changing segments of the market. These positive market trends bode well for those owners considering a sale in 2017.

We hope this edition of the Global Management Consulting M&A Report provides you with some useful market insights. Our regional teams would be delighted to explore these further with you in the context of your own strategic objectives.

Best regards,

David Jorgenson, CEO Equiteq

5

Your regional contacts

Nicodemo Esposito

NORTH AMERICA

Managing Director, Head of M&A and Strategic Advisory

Jean-Louis Michelet

ASIA-PACIFIC

Managing Director, Head of M&A and Strategic Advisory

Alex White

EUROPE

Managing Director, Head of M&A and Strategic Advisory

Pierre Briand

AUSTRALIA AND NEW ZEALAND

Managing Director, Head of M&A and Strategic Advisory

Your regional contacts© Equiteq Advisors Ltd. 2017

Christine Parry, Leadership Development Consultancy.

Sold.

The Global Management Consulting M&A Report 20178

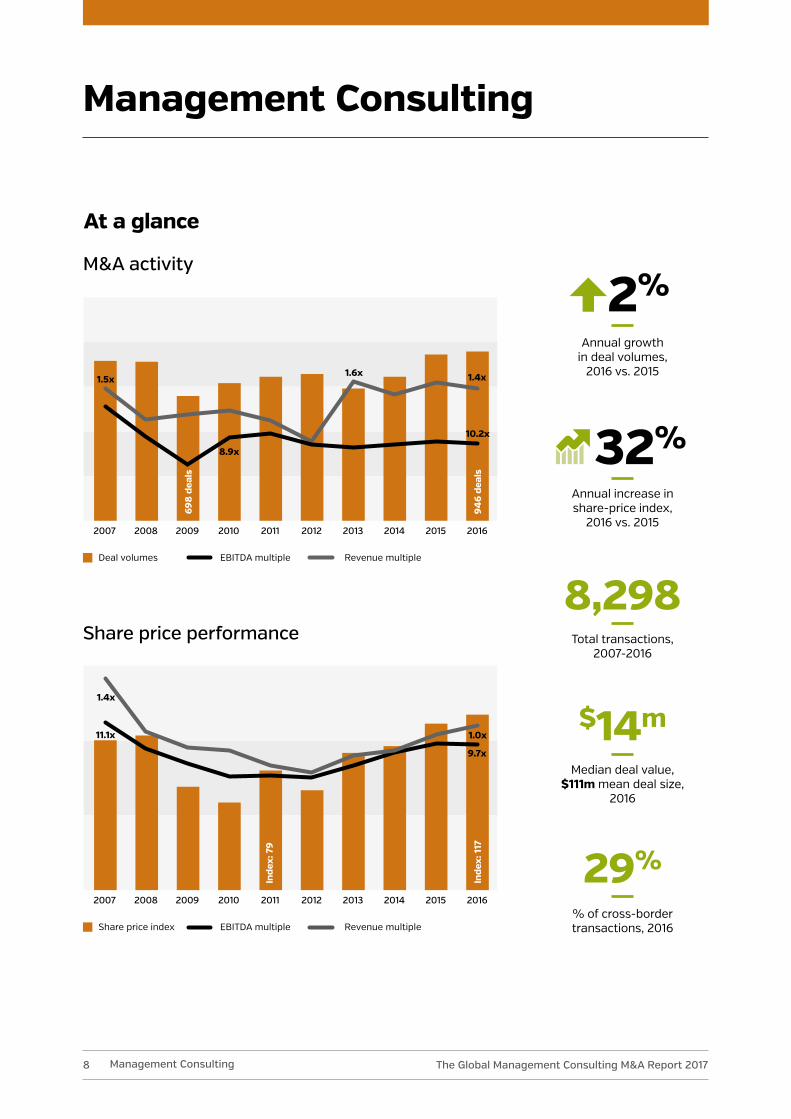

M&A activity

Share price performance

Management Consulting

2007 20122008 20132009 20142010 20152011 2016

Deal volumes Revenue multipleEBITDA multiple

698

dea

ls

1.5x1.6x 1.4x

8.9x

10.2x

94

6 de

als

Share price index Revenue multipleEBITDA multiple

2007 20122008 20132009 20142010 20152011 2016

Inde

x: 7

9

1.4x

9.7x

11.1x 1.0x

Inde

x: 1

17

Total transactions, 2007-2016

Median deal value, $111m mean deal size,

2016

% of cross-border transactions, 2016

Annual growth in deal volumes,

2016 vs. 2015

Annual increase in share-price index,

2016 vs. 2015

8,298

$14m

29%

2%

32%

Management Consulting

At a glance

9

Overview of M&A activity

M&A deal activity rose to a ten-year high, with strong demand from buyers across industries.

Looking ahead, we expect that strong industry drivers, such as digital disruption, as well as converging buyer demands, will continue to underpin strong M&A activity in the industry for the foreseeable future.

Strong demand for niche capabilities

Industry trends such as digital disruption, globalization and geo-political volatility are presenting challenges and opportunities for strategy and operational consultants. The opportunities are arising from large industry incumbents that are reconsidering their business and operating models, while looking to their advisors for best-in-class strategy-through-implementation consulting services. This is driving demand for varied functional and sector capabilities.

Accenture’s acquisition of Kurt Salmon was a notable deal in strategy, strengthening the buyer’s capabilities focused on the retail sector, following its acquisition of Javelin in 2015. The Boston Consulting Group also continued with its approach of making selective complementary acquisitions, by acquiring Inverto. This notable deal significantly bolstered the buyer’s procurement and operations capabilities in Germany.

Regulatory change and stronger enforcement

Strong demand for compliance and regulatory advisory services has been driven by new complex regulations in the financial sector, along with stronger enforcement across various jurisdictions, since the 2008 financial crisis.

Significant deals in the space over the year included the acquisition of Promontory by IBM, as well as the acquisition of CounselWorks by Duff & Phelps.

Consulting enhanced by advanced analytics

There is high demand for capabilities enhanced by advanced predictive and prescriptive data analytics solutions. This year contained a number of high-profile data analytics deals in the US healthcare services sector - an industry that is underpinned by powerful long-term drivers, which has benefited from the reforms created by the Affordable Care Act.

McKinsey’s acquisition of PriceMetrix and EQT’s acquisition of Press Ganey were noteworthy deals in the space. Press Ganey and Veritas Capital’s acquisition of Verisk’s health analytics unit formed part of a number of notable private equity (PE) backed deals in the healthcare analytics space.

Convergence with adjacent sectors

Management Consulting capabilities continue to have strong cross-sector appeal, which is driving convergence with complementary consulting segments and adjacent sectors like software and managed services.

Management Consulting© Equiteq Advisors Ltd. 2017

The Global Management Consulting M&A Report 201710

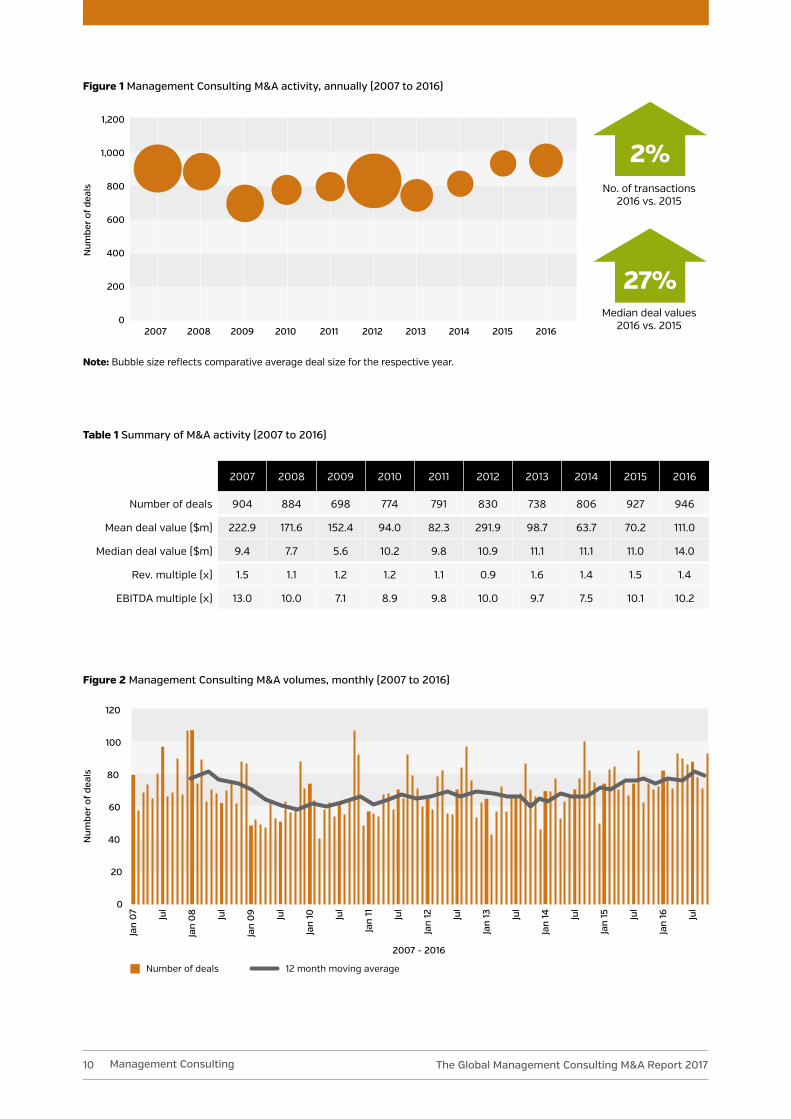

Figure 1 Management Consulting M&A activity, annually (2007 to 2016)

Figure 2 Management Consulting M&A volumes, monthly (2007 to 2016)

Table 1 Summary of M&A activity (2007 to 2016)

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Number of deals 904 884 698 774 791 830 738 806 927 946

Mean deal value ($m) 222.9 171.6 152.4 94.0 82.3 291.9 98.7 63.7 70.2 111.0

Median deal value ($m) 9.4 7.7 5.6 10.2 9.8 10.9 11.1 11.1 11.0 14.0

Rev. multiple (x) 1.5 1.1 1.2 1.2 1.1 0.9 1.6 1.4 1.5 1.4

EBITDA multiple (x) 13.0 10.0 7.1 8.9 9.8 10.0 9.7 7.5 10.1 10.2

2007 20122008 20132009 20142010 20152011 20160

600

400

200

800

1,000

1,200

Num

ber

of d

eals

Num

ber

of d

eals

120

100

80

60

40

20

0

Jan

07

Jul

Jan

08 Jul

Jan

09 Jul

Jan

10 Jul

Jan

11 Jul

Jan

12 Jul

Jan

13 Jul

Jan

14 Jul

Jan

15

Jan

16Jul

Jul

2007 - 2016

Number of deals 12 month moving average

No. of transactions 2016 vs. 2015

Median deal values 2016 vs. 2015

2%

27%

Management Consulting

Note: Bubble size reflects comparative average deal size for the respective year.

11

Deal size distribution

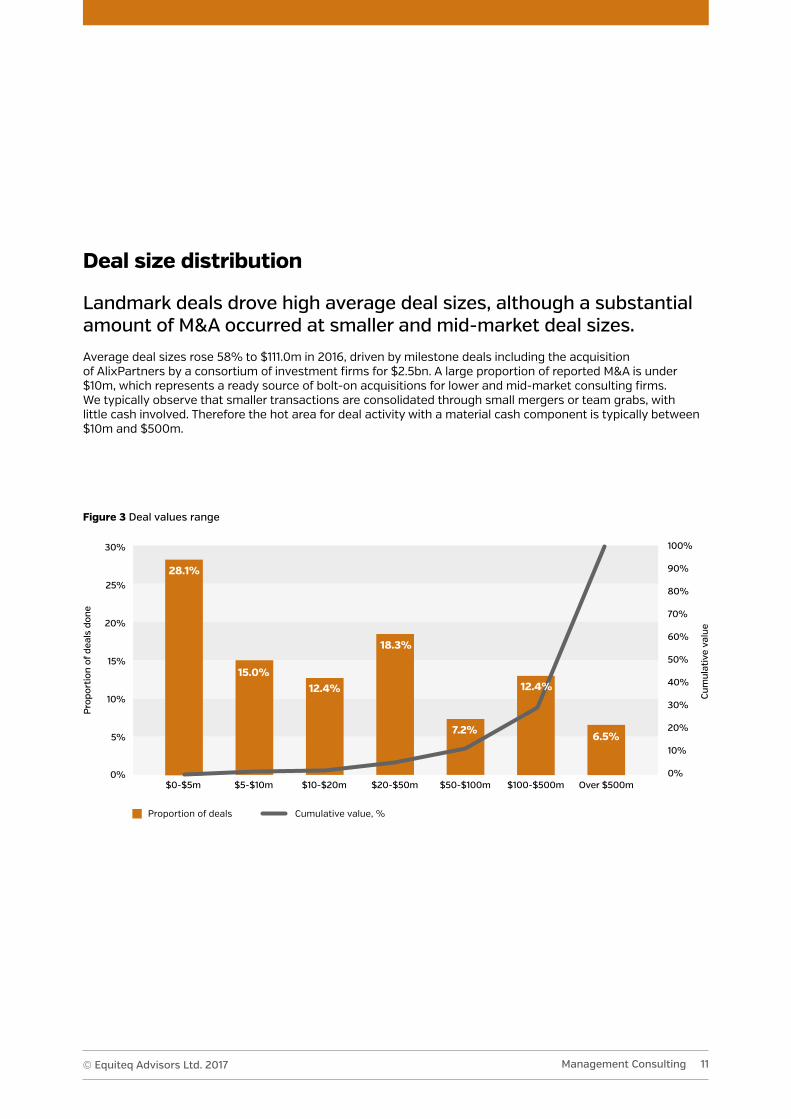

Landmark deals drove high average deal sizes, although a substantial amount of M&A occurred at smaller and mid-market deal sizes.

Average deal sizes rose 58% to $111.0m in 2016, driven by milestone deals including the acquisition of AlixPartners by a consortium of investment firms for $2.5bn. A large proportion of reported M&A is under $10m, which represents a ready source of bolt-on acquisitions for lower and mid-market consulting firms. We typically observe that smaller transactions are consolidated through small mergers or team grabs, with little cash involved. Therefore the hot area for deal activity with a material cash component is typically between $10m and $500m.

Figure 3 Deal values range

Pro

port

ion

of d

eals

don

e

Cum

ulat

ive

valu

e

30%

25%

20%

15%

10%

5%10%

0%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%$0-$5m $20-$50m$5-$10m $50-$100m$10-$20m $100-$500m Over $500m

Proportion of deals Cumulative value, %

28.1%

18.3%

15.0%

7.2%

12.4%

6.5%

12.4%

Management Consulting© Equiteq Advisors Ltd. 2017

The Global Management Consulting M&A Report 201712

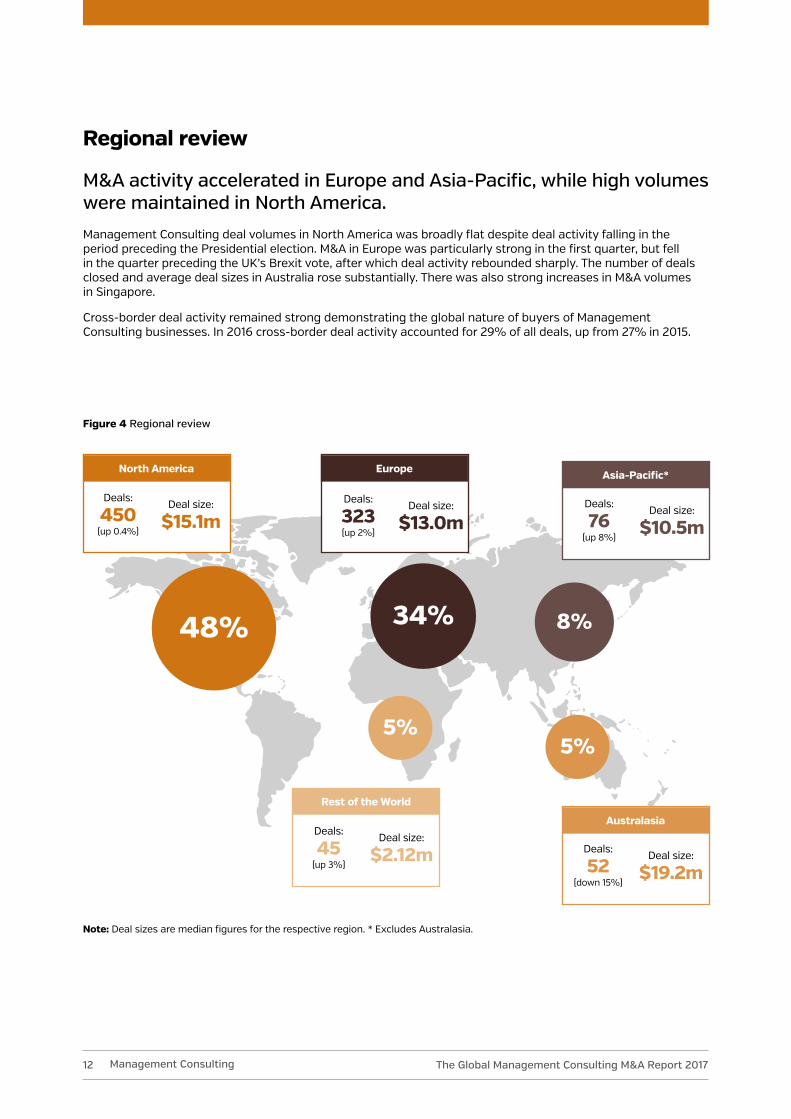

Regional review

M&A activity accelerated in Europe and Asia-Pacific, while high volumes were maintained in North America.

Management Consulting deal volumes in North America was broadly flat despite deal activity falling in the period preceding the Presidential election. M&A in Europe was particularly strong in the first quarter, but fell in the quarter preceding the UK’s Brexit vote, after which deal activity rebounded sharply. The number of deals closed and average deal sizes in Australia rose substantially. There was also strong increases in M&A volumes in Singapore.

Cross-border deal activity remained strong demonstrating the global nature of buyers of Management Consulting businesses. In 2016 cross-border deal activity accounted for 29% of all deals, up from 27% in 2015.

Figure 4 Regional review

North America

Deals:

450 (up 0.4%)

Deal size:

$15.1m

Europe Asia-Pacific*

Rest of the World

Australasia

48% 34% 8%

5%5%

Deals:

323 (up 2%)

Deals:

76 (up 8%)

Deals:

45 (up 3%)

Deals:

52 (down 15%)

Deal size:

$13.0mDeal size:

$10.5m

Deal size:

$2.12m Deal size:

$19.2m

Management Consulting

Note: Deal sizes are median figures for the respective region. * Excludes Australasia.

13

Overview of equity market performance

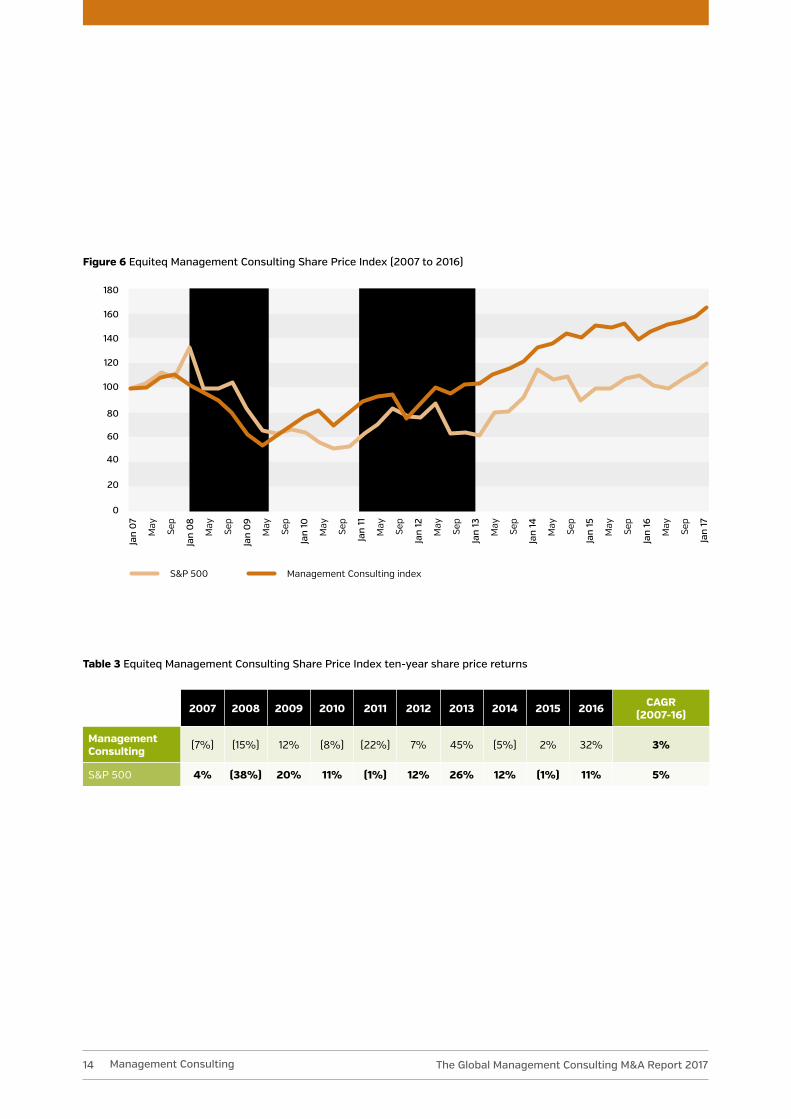

The Equiteq Management Consulting Share Price Index rose strongly to a ten-year high.

The Equiteq Management Consulting Share Price Index ended the year up 32%, outperforming the S&P 500. Its performance was supported by notable increases in the share prices of Navigant Consulting Inc (NYSE:NCI), FTI Consulting (NYSE:FCN), CRA International (NasdaqGS:CRAI) and ICF International (NasdaqGS:ICFI). The index has risen beyond its previous ten-year peak which was achieved at the end of 2015.

Figure 5 Equiteq Management Consulting Share Price Index

Table 2 Equiteq Management Consulting Share Price Index share price returns

Q1 Q2 Q3 Q4 Annual

Management Consulting 2% 1% 17% 12% 32%

S&P 500 1% 2% 5% 3% 11%

140

130

120

110

100

90

80

Jan-16 Feb-16 Apr-16Mar-16 Jun-16May-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16

Management Consulting© Equiteq Advisors Ltd. 2017

June 23: Britain votes to exit the EU and David Cameron plans to step down as PM.

Nov 8: The US Presidential election result.

The Global Management Consulting M&A Report 201714

Figure 6 Equiteq Management Consulting Share Price Index (2007 to 2016)

Table 3 Equiteq Management Consulting Share Price Index ten-year share price returns

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 CAGR(2007-16)

Management Consulting (7%) (15%) 12% (8%) (22%) 7% 45% (5%) 2% 32% 3%

S&P 500 4% (38%) 20% 11% (1%) 12% 26% 12% (1%) 11% 5%

120

140

160

180

100

80

60

40

20

0

S&P 500

Global financial crisis

European debt crisis

Management Consulting index

Jan

07

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

May

May

May

May

May

May

May

May

May

May

Jan

08

Jan

09

Jan

10

Jan

11

Jan

12

Jan

13

Jan

14

Jan

15

Jan

16

Jan

17

Management Consulting

15

Valuation multiples and trends

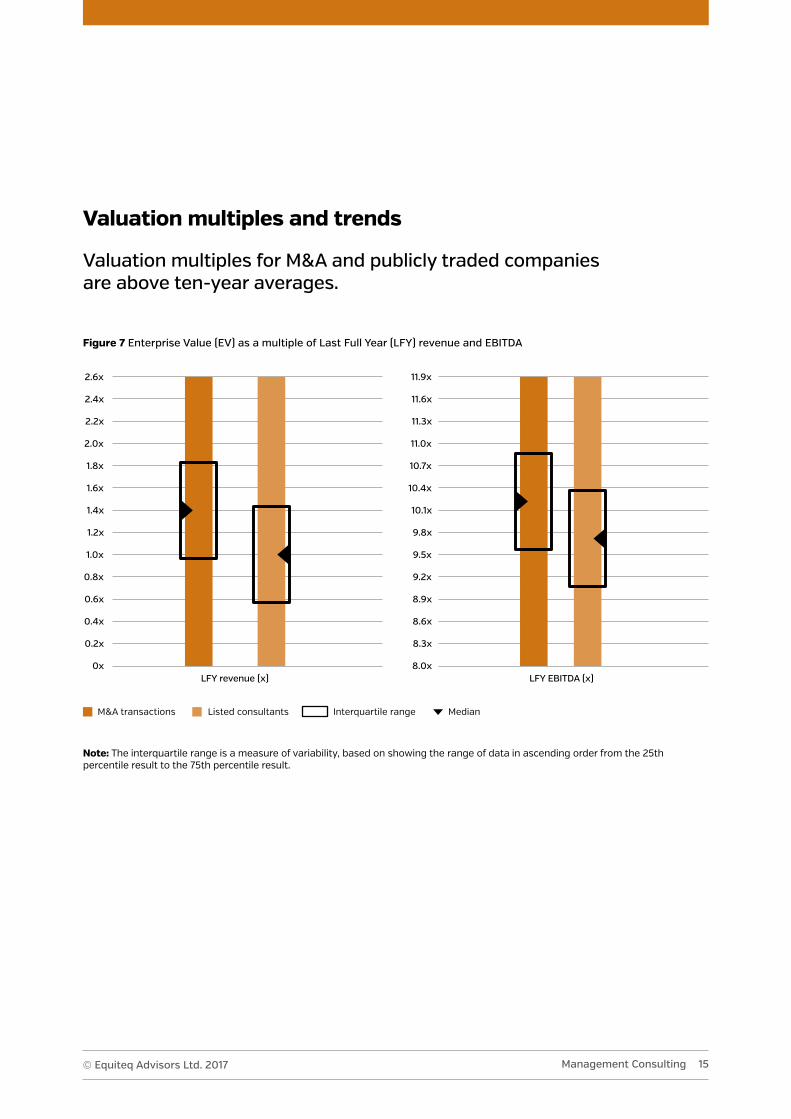

Valuation multiples for M&A and publicly traded companies are above ten-year averages.

Note: The interquartile range is a measure of variability, based on showing the range of data in ascending order from the 25th percentile result to the 75th percentile result.

Figure 7 Enterprise Value (EV) as a multiple of Last Full Year (LFY) revenue and EBITDA

Management Consulting

0.2x 8.3x

0x 8.0x

0.4x 8.6x

0.6x 8.9x

0.8x 9.2x

1.8x 10.7x

1.0x 9.5x

2.0x 11.0x

1.2x 9.8x

2.2x 11.3x

1.4x 10.1x

2.4x 11.6x

1.6x 10.4x

2.6x 11.9x

LFY revenue (x) LFY EBITDA (x)

© Equiteq Advisors Ltd. 2017

M&A transactions Listed consultants Interquartile range Median

The Global Management Consulting M&A Report 201716

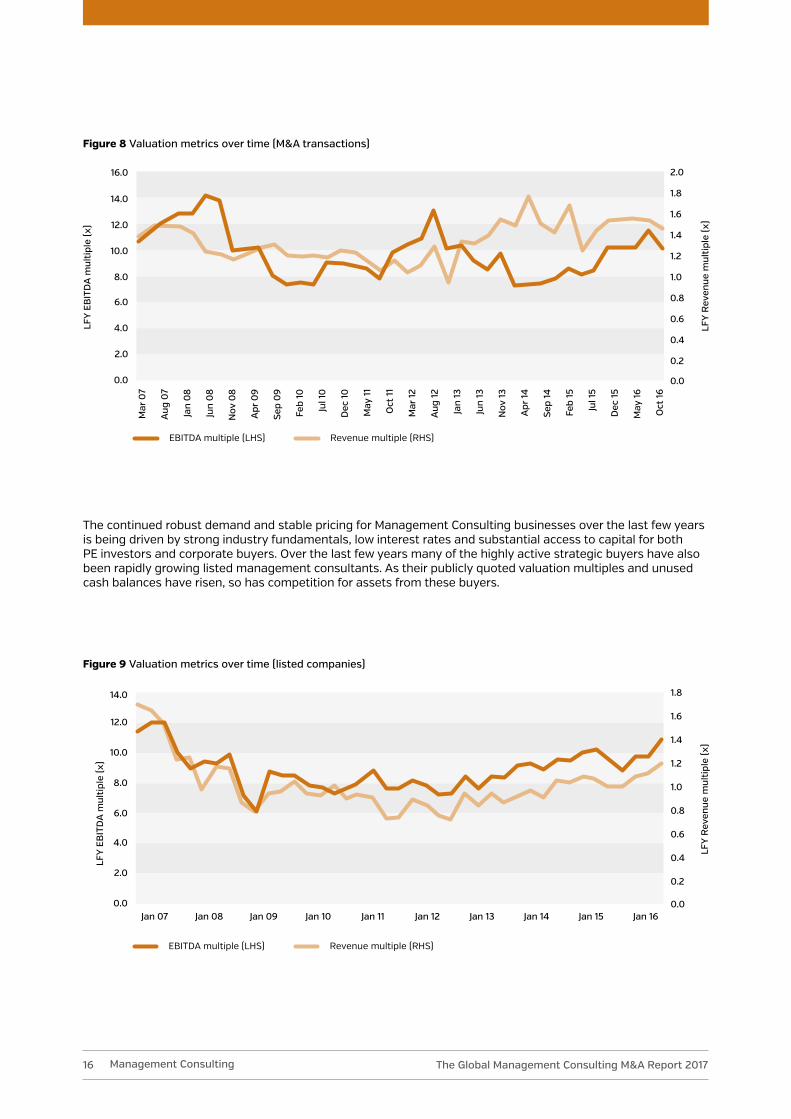

The continued robust demand and stable pricing for Management Consulting businesses over the last few years is being driven by strong industry fundamentals, low interest rates and substantial access to capital for both PE investors and corporate buyers. Over the last few years many of the highly active strategic buyers have also been rapidly growing listed management consultants. As their publicly quoted valuation multiples and unused cash balances have risen, so has competition for assets from these buyers.

Figure 8 Valuation metrics over time (M&A transactions)

LFY

EBIT

DA

mul

tipl

e (x

)

LFY

Rev

enue

mul

tipl

e (x

)

EBITDA multiple (LHS) Revenue multiple (RHS)

14.0

16.0

1.2

1.6

2.0

1.0

1.4

1.8

0.8

12.0

0.6

10.0

0.4

8.0

0.2

6.0

4.0

2.0

0.0 0.0

Mar

07

Mar

12

Aug

07

Aug

12

Jan

08

Jan

13

Jun

08

Jun

13

Nov

08

Nov

13

Apr

09

Apr

14

Sep

09

Sep

14

Feb

10

Feb

15

Jul 1

0

Jul 1

5

Dec

10

Dec

15

May

11

May

16

Oct

11

Oct

16

Figure 9 Valuation metrics over time (listed companies)

LFY

EBIT

DA

mul

tipl

e (x

)

LFY

Rev

enue

mul

tipl

e (x

)

EBITDA multiple (LHS) Revenue multiple (RHS)

12.0

14.0

1.4

1.2

1.6

1.8

1.0

0.8

10.0

0.6

8.0

0.4

6.0

0.2

4.0

2.0

0.0 0.0Jan 07 Jan 08 Jan 09 Jan 10 Jan 11 Jan 12 Jan 13 Jan 14 Jan 15 Jan 16

Management Consulting

17

Strategic and private equity buyer trends

Listed management consultants and growing accounting firms dominated the top buyers in the industry.

Selected top strategic buyers

PricewaterhouseCoopers

Following its transformational acquisition of Booz & Co in 2014, PwC has slowed its rate of reported Management Consulting acquisitions in the US. The buyer appears to now to be focused on integrating recent acquisitions in the region and focusing its M&A strategy on emerging territory consulting businesses. The Big Four firm made a number of acquisitions in 2016, which included IT and Management Consulting acquisitions by its network firms in the UK, Germany, France and Central & Eastern Europe.

Huron Consulting

The buyer has grown rapidly through acquisitions, with a focus on expanding into healthcare, which is now believed to represent over 60% of its business and technology practice. This sector expansion continued in 2016 with its acquisitions of MyRounding and HSM. Another interesting deal in the year was its acquisition of ADI Strategies, which will be used to create one of the largest and fastest growing Oracle application and analytics practices in the U.S.

BDO International

BDO continued to grow in the US, making 7 accounting and consulting acquisitions. There was also considerable deal activity across its global network, particularly within EMEA where notable deals occurred within accounting, business advisory, IT and cyber security.

Navigant Consulting

Navigant stepped up the pace of its acquisitions in 2016, acquiring 3 Management Consulting businesses across Europe and North America. This included acquisitions of consulting firms with specialisms in data-driven market analysis to the medical technology industry, energy and sustainability consulting, as well as strategy and optimization assistance for healthcare providers.

CliftonLarsonAllen

CliftonLarsonAllen made a string of M&A deals this year, as it continues to expand across the US. Its acquisition of CPWR significantly strengthened its presence in Texas with the addition of 130 professionals. Another notable deal, was the acquisition of Bray & Company, which will expand the buyer’s capabilities in the Midwest with 280 accountants and consultants in Wisconsin.

In 2016,

40.0% of all deals were by serial buyers

(down from 41% in 2015)

In 2016,

7.4% of buyers were financial buyers (up from 6.8% in 2015)

Management Consulting© Equiteq Advisors Ltd. 2017

The Global Management Consulting M&A Report 201718

Selected M&A transactions

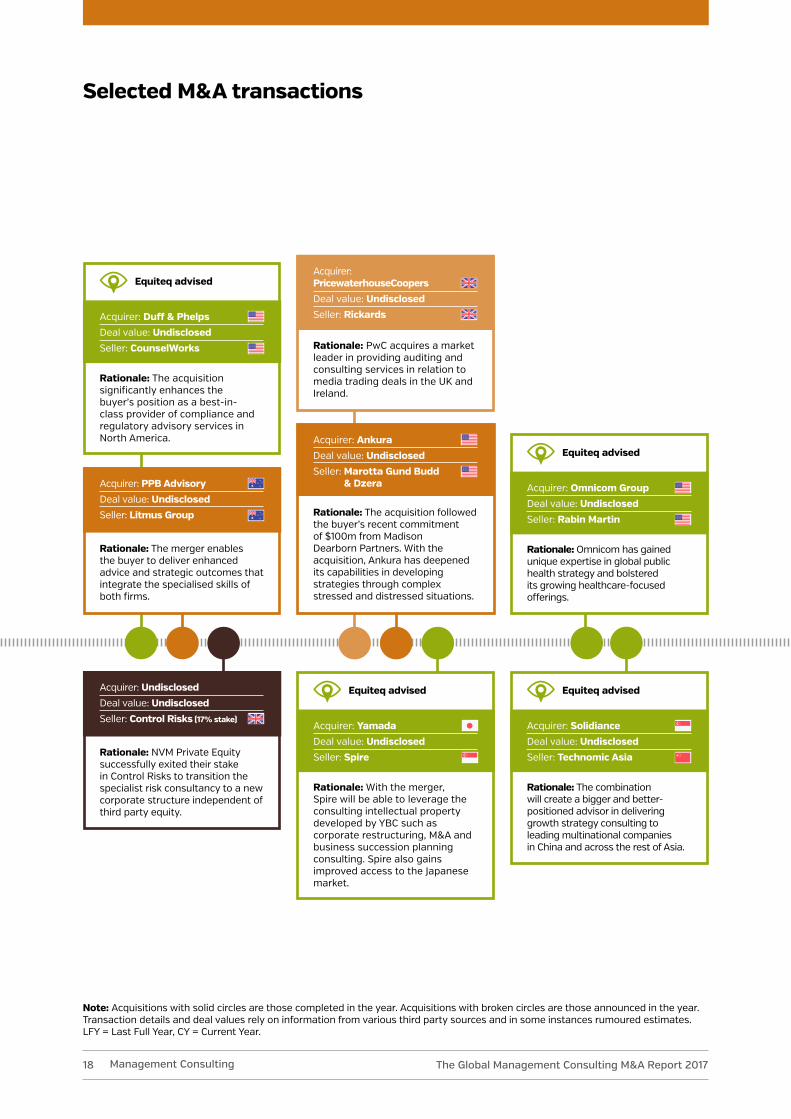

Acquirer: Solidiance Deal value: UndisclosedSeller: Technomic Asia

Rationale: The combination will create a bigger and better-positioned advisor in delivering growth strategy consulting to leading multinational companies in China and across the rest of Asia.

Equiteq advised

Acquirer: Omnicom Group Deal value: UndisclosedSeller: Rabin Martin

Rationale: Omnicom has gained unique expertise in global public health strategy and bolstered its growing healthcare-focused offerings.

Equiteq advised

Acquirer: Yamada Deal value: UndisclosedSeller: Spire

Rationale: With the merger, Spire will be able to leverage the consulting intellectual property developed by YBC such as corporate restructuring, M&A and business succession planning consulting. Spire also gains improved access to the Japanese market.

Equiteq advised

Acquirer: Duff & Phelps Deal value: UndisclosedSeller: CounselWorks

Rationale: The acquisition significantly enhances the buyer’s position as a best-in-class provider of compliance and regulatory advisory services in North America.

Equiteq advised

Note: Acquisitions with solid circles are those completed in the year. Acquisitions with broken circles are those announced in the year. Transaction details and deal values rely on information from various third party sources and in some instances rumoured estimates. LFY = Last Full Year, CY = Current Year.

Rationale: NVM Private Equity successfully exited their stake in Control Risks to transition the specialist risk consultancy to a new corporate structure independent of third party equity.

Acquirer: Undisclosed Deal value: UndisclosedSeller: Control Risks (17% stake)

Rationale: The merger enables the buyer to deliver enhanced advice and strategic outcomes that integrate the specialised skills of both firms.

Acquirer: PPB Advisory Deal value: UndisclosedSeller: Litmus Group Rationale: The acquisition followed

the buyer’s recent commitment of $100m from Madison Dearborn Partners. With the acquisition, Ankura has deepened its capabilities in developing strategies through complex stressed and distressed situations.

Acquirer: Ankura Deal value: UndisclosedSeller: Marotta Gund Budd & Dzera

Rationale: PwC acquires a market leader in providing auditing and consulting services in relation to media trading deals in the UK and Ireland.

Acquirer: PricewaterhouseCoopers Deal value: UndisclosedSeller: Rickards

Management Consulting

19

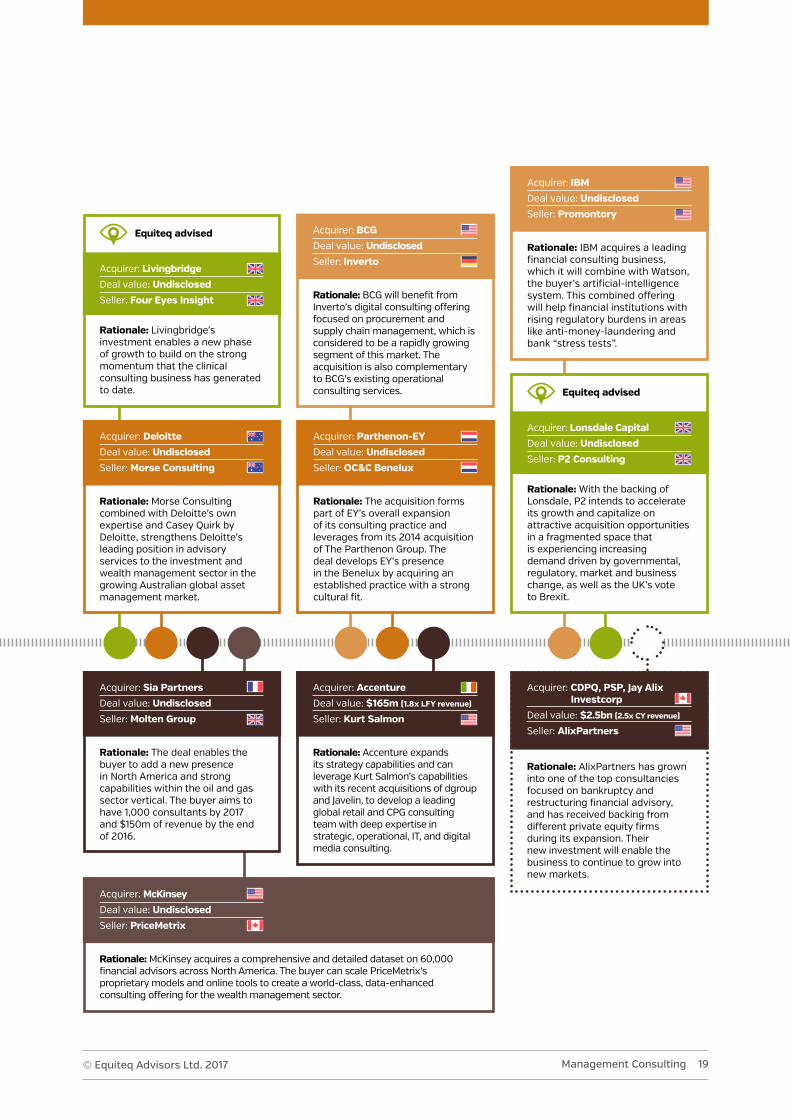

Rationale: The deal enables the buyer to add a new presence in North America and strong capabilities within the oil and gas sector vertical. The buyer aims to have 1,000 consultants by 2017 and $150m of revenue by the end of 2016.

Acquirer: Sia Partners Deal value: UndisclosedSeller: Molten Group

Rationale: The acquisition forms part of EY’s overall expansion of its consulting practice and leverages from its 2014 acquisition of The Parthenon Group. The deal develops EY’s presence in the Benelux by acquiring an established practice with a strong cultural fit.

Acquirer: Parthenon-EY Deal value: UndisclosedSeller: OC&C Benelux

Rationale: IBM acquires a leading financial consulting business, which it will combine with Watson, the buyer’s artificial-intelligence system. This combined offering will help financial institutions with rising regulatory burdens in areas like anti-money-laundering and bank “stress tests”.

Acquirer: IBM Deal value: UndisclosedSeller: Promontory

Rationale: Morse Consulting combined with Deloitte’s own expertise and Casey Quirk by Deloitte, strengthens Deloitte’s leading position in advisory services to the investment and wealth management sector in the growing Australian global asset management market.

Acquirer: Deloitte Deal value: UndisclosedSeller: Morse Consulting

Acquirer: Livingbridge Deal value: UndisclosedSeller: Four Eyes Insight

Rationale: Livingbridge’s investment enables a new phase of growth to build on the strong momentum that the clinical consulting business has generated to date.

Equiteq advised

Acquirer: Lonsdale Capital Deal value: UndisclosedSeller: P2 Consulting

Rationale: With the backing of Lonsdale, P2 intends to accelerate its growth and capitalize on attractive acquisition opportunities in a fragmented space that is experiencing increasing demand driven by governmental, regulatory, market and business change, as well as the UK’s vote to Brexit.

Equiteq advised

Rationale: McKinsey acquires a comprehensive and detailed dataset on 60,000 financial advisors across North America. The buyer can scale PriceMetrix’s proprietary models and online tools to create a world-class, data-enhanced consulting offering for the wealth management sector.

Acquirer: McKinsey Deal value: UndisclosedSeller: PriceMetrix

Rationale: Accenture expands its strategy capabilities and can leverage Kurt Salmon’s capabilities with its recent acquisitions of dgroup and Javelin, to develop a leading global retail and CPG consulting team with deep expertise in strategic, operational, IT, and digital media consulting.

Acquirer: Accenture Deal value: $165m (1.8x LFY revenue) Seller: Kurt Salmon

Rationale: AlixPartners has grown into one of the top consultancies focused on bankruptcy and restructuring financial advisory, and has received backing from different private equity firms during its expansion. Their new investment will enable the business to continue to grow into new markets.

Acquirer: CDPQ, PSP, Jay Alix Investcorp Deal value: $2.5bn (2.5x CY revenue)

Seller: AlixPartners

Rationale: BCG will benefit from Inverto’s digital consulting offering focused on procurement and supply chain management, which is considered to be a rapidly growing segment of this market. The acquisition is also complementary to BCG’s existing operational consulting services.

Acquirer: BCG Deal value: UndisclosedSeller: Inverto

Management Consulting© Equiteq Advisors Ltd. 2017

Marc Jantzen, Performance Improvement.

Sold.

The Global Management Consulting M&A Report 201722

Key definitions Equiteq segments the consulting sector into five key segments, which span a broad array of knowledge-intensive services. These sub-sectors are defined further below:

Appendix

Management ConsultingFirms engaged in strategic or operationally focused business advisory services.

IT ServicesFirms focused on IT architecture or strategy, IT implementation and maintenance.

Media AgenciesFirms in this space cover all the main disciplines relating to advertising and marketing process.

EngineeringFirms involved in professional services relating to engineering and construction.

Human ResourcesFirms engaged in human capital management or related technology consulting, leadership consulting, training and recruitment.

Appendix

23

A quick word on the dataTransaction data, share price data, company information and valuation multiples are taken from various sources, including the S&P Capital IQ and PitchBook databases, which have not been verified by us. The valuation multiples reflect a measure of aggregated deal values and historic financial performances where these were disclosed by the buyer and sellers. Many factors influence value which are not disclosed such as current year earnings, growth potential, synergies, non-recurring items and so on. Therefore the findings in this report should not be used by any party to value a business, for which we recommend you obtain independent financial advice.

Appendix

For the purposes of this report we have broken down buyers into three groups, defined further below:

Private equity or financial buyers are investment firms investing private capital into businesses, which are typically held and exited after a hold-period.

Strategic or corporate buyers are non-private equity investors who have existing businesses which will typically make acquisitions which form part of their existing operations.

Serial buyers are those buyers that have made multiple acquisitions over the last three years.

Private equity (PE) buyers differ from trade buyers in that the former acquire strictly to realize a cash return on their invested equity, usually after 3 to 5 years. Strategic buyers typically acquire to realize long-term strategic value. As a result, PE buyers will look for specific traits in a consulting acquisition and selling to a PE buyer will have different implications as compared with selling to a trade buyer.

© Equiteq Advisors Ltd. 2017

The Global Management Consulting M&A Report 201724

About Equiteq

Equiteq is the global leader in providing strategic advisory and Mergers & Acquisition services to consulting and IT Services firms.

We focus 100% on helping owners fulfil their exit goals. We do this by achieving successful sales that deliver maximum value for firm owners and by providing strategic advice on what will best yield value growth and shareholder returns against their objectives.

With offices in New York, London, Singapore and Sydney, we offer our clients true global reach.

Further resourcesJoin Equiteq Edge, our free source of information, advice and insight to help you prepare for sale and sell your consulting firm. Equiteq Edge gives you access to the findings of unique research conducted amongst buyers of consulting firms from around the world, insight from those who have sold their consulting firms and expert advice.

Join Equiteq Edge at equiteq.com/equiteq-edge

Appendix

Request a Strategy SessionBenefit from our insights on your value, market position and attractiveness to buyers, together with recommended actions which, if implemented, will transform value prior to an exit.

We specialize in working with owners of consulting, IT Services, agency and intellectual property enabled BPO businesses throughout their growth to exit journey. We are deeply invested in our knowledge of the buyer market and what counts in terms of acquisition attractiveness, value and transaction readiness. An Equiteq strategic review is more than a current analysis, it is the beginning of a journey together to maximize your firm’s potential value where we will provide the roadmap that best suits achieving your stated objectives.

Operational as well as financial, a review will typically cover:

• Operational assessment of the factors enhancing your value and dragging it down, together with how your firm compares to best practice.

• The buyer groups who will be attracted to your firm, how they approach transactions and current value.

• Recommended change program to enhance value and saleability of your firm and the potential future value if change is implemented.

• Your options, routes to exit and how shareholder alignment can be achieved.

If you would like to learn more, please get in touch for a confidential discussion by phone or email us at [email protected].

© Equiteq Advisors Ltd. 2017 25

Disclaimer Equiteq is an M&A and strategic advisory firm that exists to provide you, the owners of consulting and IT Services firms, with the best possible information, advice and experience to help you make decisions about selling your firm and preparing it for sale.

What follows is a legal disclaimer to ensure that you are aware that if you act on this advice, Equiteq cannot be held liable for the results of your decisions.

We have obtained the information provided in this report from sources which we believe to be reliable, and we have made reasonable efforts to ensure that it is accurate. However, the information is not intended to provide tax, legal or investment advice. We make no representations or warranties in regard to the contents of or materials provided in this report, and exclude all representations, conditions and warranties, express or implied arising by operation of law or otherwise, to the extent that these may not be excluded by law.

We shall not be liable in contract, tort (including negligence) or otherwise for indirect, special, incidental, punitive or consequential losses or damages, or loss of profits, revenue, goodwill or anticipated savings, or for any financial loss whatsoever, regardless of whether any such loss or damage would arise in the ordinary course of events or otherwise, or is reasonably foreseeable or is otherwise in the contemplation of the parties in connection with this report. No liability is excluded to the extent such liability may not be excluded or limited by law. Nothing in this statement shall limit or exclude our liability for death or personal injury caused by our negligence.

Appendix

Contact usIf you would like more information on our Global Consulting

M&A Report 2017, our company or the various services we offer please don’t hesitate to get in touch.

Email: [email protected]

Website: equiteq.com

Equiteq has global reach through its offices in New York, London, Singapore and Sydney.

equiteqedge.com

@consultingmanda

© 2017 Equiteq Advisors Ltd. April 2017