Embed Size (px)

Citation preview

1 CENTRAL BANK OF CHILE JUNE 2008

The Global Rise in Food Prices and the U.S. Slowdown: Issues and Challenges in Monetary Policy

The case of Chile

Pablo García SilvaDirector of Research, BCCh

2 CENTRAL BANK OF CHILE JUNE 2008

AgendaAgenda

•The nature of the inflation shock

Expectations and the policy response

Challenging times for Inflation Targeting

3 CENTRAL BANK OF CHILE JUNE 2008

AgendaAgenda

•The nature of the inflation shock

Expectations and the policy response

Challenging times for Inflation Targeting

4 CENTRAL BANK OF CHILE JUNE 2008

Impact on Annual CPI Inflation(*)(percentage points)

(*) In brackets, shares in the CPI basketSources: Central Bank of Chile and National Statistics Bureau.

A A highlyhighly significantsignificant shareshare ofof currentcurrent yy--oo--y y inflationinflation has has beenbeen drivendriven by by foodfood pricesprices

Public services (5,51%)Fuels (3,97%)

Food without fresh fruits and vegetables(23,5%)Fresh fruits and vegetables (3,77%)Rest (63,25%)

5 CENTRAL BANK OF CHILE JUNE 2008

Food price index(Annual change in local currency, percentage)

Source: Magendzo (2008) from Survey on increases in food prices,

This is not unique to ChileThis is not unique to Chile

Dec. 2006 to Dec. 2007 Dec. 2007 to Mar. 2008

0

10

20

30

40

50

Argentina Brasil Bolivia Chile Paraguay Perú Uruguay Venezuela

6 CENTRAL BANK OF CHILE JUNE 2008

Food prices affected by idiosyncraticidiosyncratic shocks

IdiosyncraticIdiosyncratic shocks shocks havehave occurredoccurred in in mostmostanalyzedanalyzed countriescountries

Argentina Brazil Bolivia Chile Paraguay Peru Uruguay Venezuela

Importanteffect:

Vegetablesand fruits

Kidneybeans

Tomato, beef andpea

Freshvegetables, fresh fruitsandvegetables

Papaya, freshvegetables, tomatoesand othervegetables

Fruits andvegetables

Moderateeffect:

Meat anddairy

Papayas, bananas, lettuce, carrot, onion, pepperandbroadbean

Preparedfood, tomatosauce andpreservedfruits

Vegetables Potatoes, tomatoesand citrus

Meat anddairy

Source: Magendzo (2008) from Survey on increases in food prices,

7 CENTRAL BANK OF CHILE JUNE 2008

5

2

1

DemandDemand pressurespressures havehave alsoalso playedplayed a role in a role in somesome economieseconomies

Source: Magendzo (2008) from Survey on increases in food prices,

7

1

Important effect Moderate effect Slight effect None

3

4

1

International increaseof food price

How far do the following factors explain the extraordinary rise of foodprices since December 2006

Idiosyncratic shocks Domestic demandpressures

8 CENTRAL BANK OF CHILE JUNE 2008

y = 0,642x - 29,788R 2 = 0,6475

(sin Argentina)

Change in the price of bread and exchange rate(Dec06 to Mar08 change, percentage)

Source: Magendzo (2008) from Survey on increases in food prices,

Bread prices have risen less in countries that have Bread prices have risen less in countries that have had a greater appreciation of their currencyhad a greater appreciation of their currency

Exchange rate

Bread price

Venezuela

Bolivia

Uruguay

Chile

Brasil

Paraguay

Perú

Argentina

-25

-20

-15

-10

-5

0

5

10 15 20 25 30 35 40 45

9 CENTRAL BANK OF CHILE JUNE 2008

ShiftShift in in generationgeneration awayaway fromfrom hydrohydro andand gas gas towardstowards diesel, diesel, alongalong withwith hikeshikes in oil in oil pricesprices, , havehave ledled toto sharpsharp increasesincreases in in energyenergy costscosts.

Energy cost measures(relative to GDP deflator, index)

Marginal cost Regulated distribution price

Source: Central Bank of Chile

0

2

4

6

8

10

12

89 91 93 95 97 99 01 03 05 070,6

0,8

1,0

1,2

1,4

10 CENTRAL BANK OF CHILE JUNE 2008

RecentRecent accelerationacceleration ofof corecore inflationinflation relatedrelated totofoodfood andand energyenergy costscosts, , notnot demanddemand pressurespressures.

Source: Central Bank of Chile

-6

-4

-2

0

2

4

6

95 96 97 98 99 00 01 02 03 04 05 06 07 08-2

0

2

4

6

8

10

Output Gap q-o-q s/a CPIX1

11 CENTRAL BANK OF CHILE JUNE 2008

AgendaAgenda

•The nature of the inflation shock

Expectations and the policy response

Challenging times for Inflation Targeting

12 CENTRAL BANK OF CHILE JUNE 2008

Sources: Monthly survey of Economic expectations, Central Bank of Chile.

InflationInflation surprisessurprises ledled toto a gradual a gradual shiftshift in in expectedexpected inflationinflation in in monthlymonthly surveysurvey

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

Ene.06 May.06 Sep.06 Ene.07 May.07 Sep.07 Ene.08 May.08

2.0

2.5

3.0

3.5

4.0

4.5

5.0

3 month ahead surprise current month surprise 12 month ahead expected inflation 24 month ahead expected inflation

13 CENTRAL BANK OF CHILE JUNE 2008

BreakBreak--eveneven inflationinflation tenorstenors havehave alsoalso risenrisen, , affectedaffected by by expectationsexpectations andand significantsignificantinflationinflation riskrisk premiapremia

Sources: Central Bank of Chile and Bloomberg.

1 on 1 3 on 2 5 on 5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

5,5

Ene.06 Jul.06 Ene.07 Jul.07 Ene.082,0

2,5

3,0

3,5

4,0

4,5

5,0

5,5

14 CENTRAL BANK OF CHILE JUNE 2008

Source: Central Bank of Chile.

MonetaryMonetary policypolicy stancestance has has beenbeen shiftedshifted by a by a cumulativecumulative 175bp 175bp sincesince midmid 20072007

Cumulative increase of 175bpover period of food price surprises

0

1

2

3

4

5

6

7

8

2002 2003 2004 2005 2006 2007 2008

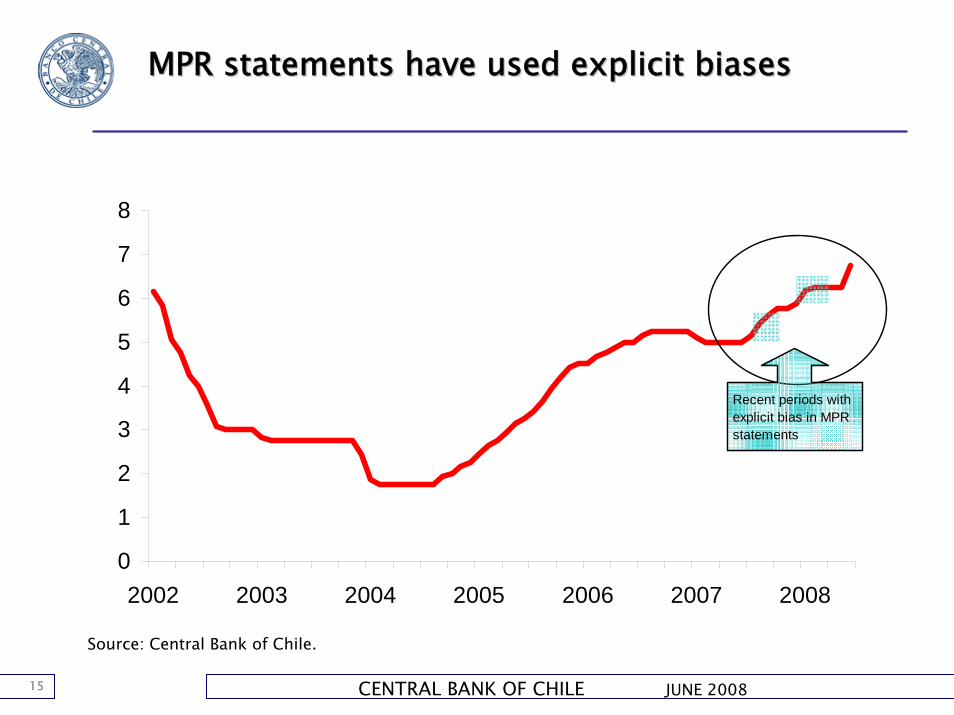

15 CENTRAL BANK OF CHILE JUNE 2008

Source: Central Bank of Chile.

MPR MPR statementsstatements havehave usedused explicitexplicit biasesbiases

0

1

2

3

4

5

6

7

8

2002 2003 2004 2005 2006 2007 2008

Recent periods with explicit bias in MPR statements

16 CENTRAL BANK OF CHILE JUNE 2008

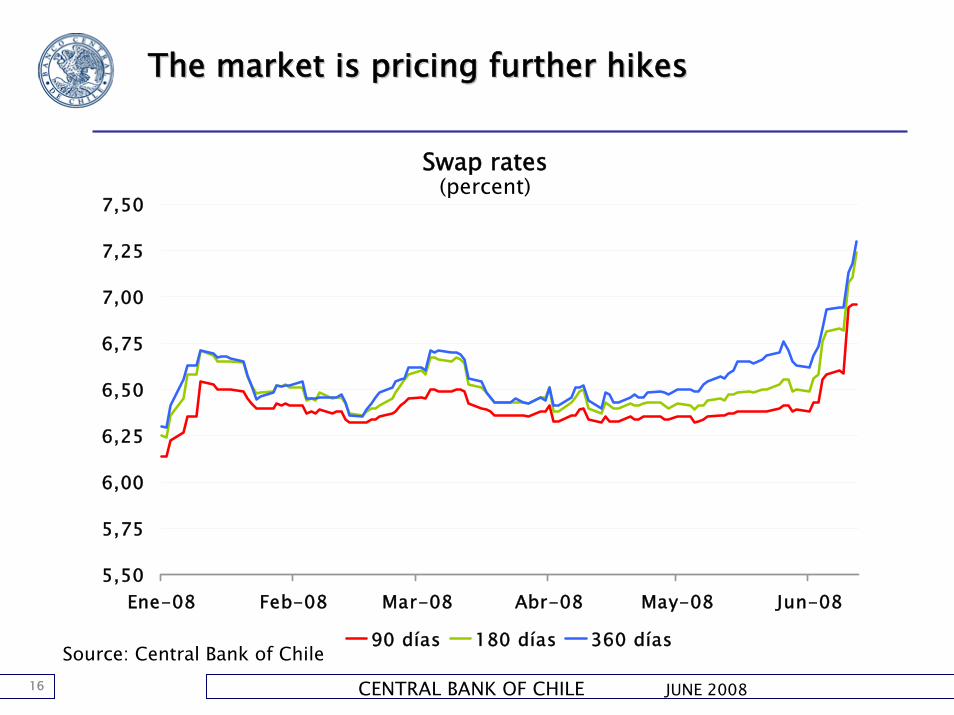

TheThe marketmarket isis pricingpricing furtherfurther hikeshikes

Swap rates(percent)

Source: Central Bank of Chile

5,50

5,75

6,00

6,25

6,50

6,75

7,00

7,25

7,50

Ene-08 Feb-08 Mar-08 Abr-08 May-08 Jun-08

90 días 180 días 360 días

17 CENTRAL BANK OF CHILE JUNE 2008

AgendaAgenda

•The nature of the inflation shock

Expectations and the policy response

Challenging times for Inflation Targeting

18 CENTRAL BANK OF CHILE JUNE 2008

ChallengesChallenges forfor InflationInflation TargetingTargeting

•Consistency with intervention policy

Adjusting communication to largedeviation from target

19 CENTRAL BANK OF CHILE JUNE 2008

ConsistencyConsistency withwith interventionintervention policypolicy

April 10th intervention package:

Announcement within window of opportunity given by neutral bias in MPR and lack of further inflation surprises during 2008:Q1

Rationale based on high uncertainty in global financial markets:- Investment in stability- Role of forex liquidity provision with the Central Bank, not the

fiscal authority through SWF- Mechanic implementation: USD50 million daily for eight months- No target for the exchange rate

Implications for monetary policy:- Mechanic implementations does not constrain monetary policy- Mechanic implementation avoids the discretion of using exchange

rate policy for disinflation purposes

20 CENTRAL BANK OF CHILE JUNE 2008

Source: Central Bank of Chile.

AdjustingAdjusting communicationcommunication toto largelargedeviationdeviation fromfrom targettarget

-1

01

23

45

67

89

10

04 05 06 07 08 09 10-1

01

23

45

67

89

10

21 CENTRAL BANK OF CHILE JUNE 2008

AdjustingAdjusting communicationcommunication toto largelargedeviationdeviation fromfrom targettarget

In normal times and under small shocks:

• IT under full credibility has a rolling policy horizon and is fully forward looking

• Supply shocks vs demand shocks distinction critical when tailoring monetary policy responses

In times under large shocks flexibility is curtailed:

• Little scope for postponement of disinflation to target• Little tolerance of further inflation surprises regardless of the

nature of the shock, difficult distinction between normal and undesired propagation

Shift in recent MPR statement: 50bp decision based on the need to avoid “undesired postponement” of convergence to target

22 CENTRAL BANK OF CHILE JUNE 2008

ConcludingConcluding remarksremarks

Inflation targeting has served emerging economies well during times of turmoil (2001-2003)

We live in challenging times for Inflation Targeting• Shocks at each country level are supply shocks• But worldwide we face a significant demand shock

It is not the time for tinkering for the framework (eg. increasing flexibility), but rather for simplification of the message and sticking to the basics: avoid the unhinging of inflationary expectations

23 CENTRAL BANK OF CHILE JUNE 2008

The Global Rise in Food Prices and the U.S. Slowdown: Issues and Challenges in Monetary Policy

The case of Chile

Pablo García SilvaDirector of Research, BCCh