Embed Size (px)

Citation preview

Corporate presentation - June, 2016

The HDL Company

Disclaimer

This document has been prepared by Cerenis Therapeutics (the "Company") and is for information purposes only.

The information and opinions contained in this document are provided as of the date of this document only and may be updated,supplemented, revised, verified or amended, and thus such information may be subject to significant changes. The Company is not underany obligation to update the information or opinions contained herein which are subject to change without prior notice.The information contained in this document has not been subject to independent verification. No representation, warranty orundertaking, express or implied, is made as to the accuracy, completeness or appropriateness of the information and opinions containedin this document. The Company, its subsidiaries, its advisors and representatives accept no responsibility for and shall not be held liablefor any loss or damage that may arise from the use of this document or the information or opinions contained herein.This document contains information on the Company’s markets and competitive position, and more specifically, on the size of its markets.This information has been drawn from various sources or from the Company’s own estimates. Investors should not base their investmentdecision on this information.This document contains certain forward-looking statements. These statements are not guarantees of the Company's future performance.These forward-looking statements relate to the Company's future prospects, developments and marketing strategy and are based onanalyses of earnings forecasts and estimates of amounts not yet determinable. Forward-looking statements are subject to a variety ofrisks and uncertainties as they relate to future events and are dependent on circumstances that may or may not materialize in the future.Forward-looking statements cannot, under any circumstance, be construed as a guarantee of the Company's future performance and theCompany’s actual financial position, results and cash flow, as well as the trends in the sector in which the Company operates, may differmaterially from those proposed or reflected in the forward-looking statements contained in this document. Even if the Company’sfinancial position, results, cash-flows and developments in the sector in which the Company operates were to conform to the forward-looking statements contained in this document, such results or developments cannot be construed as a reliable indication of theCompany's future results or developments. The Company does not undertake any obligation to update or to confirm projections orestimates made by analysts or to make public any correction to any prospective information in order to reflect an event or circumstancethat may occur after the date of this document.This document does not constitute an offer to sell or subscribe or a solicitation to purchase or subscribe for securities in France, theUnited States or any other jurisdiction. Securities may not be offered or sold in the United States absent registration under the USSecurities Act of 1933, as amended, or an exemption from registration thereunder. No public offering of securities may be conducted inFrance or abroad prior to the delivery by the French Autorité des marchés financiers (Financial Markets Authority) of a visa on aprospectus that complies with the provisions of Directive 2003/71/CE as amended. No offering of securities is contemplated in France orany jurisdiction outside France.

2Corporate Presentation| June 2016

Jean-Louis DASSEUX, PhD, MBA

Founder and CEO Over 25 years of experience in the pharmaceutical industry (Pfizer,

Esperion Therapeutics, Fournier Laboratories)

A leading world expert in lipid metabolism, atherosclerosis and cardiovascular diseases

Inventor of more than 60 patent families relating to HDL and the treatment of cardiovascular diseases

Cyrille TUPIN, CPA

CFO

Audit Director at Sygnatures, the largest private auditing and consulting company in Toulouse, France

More than 7 years at PWC working on high-profile business transactions

3

An experienced Management

Corporate Presentation| June 2016

Cardiovascular Disease: Still an unmet medical need after more than 30 years of existing therapy

4

ONLY ONE REAL SOLUTION: ELIMINATE CHOLESTEROL PLAQUE WITH CERENIS

1 out of 3 deaths worldwide (source: WHO)

The disease category with the greatest health expenditure:

– $107 bn in the United States, in 2010

– $110 bn in Europe, in 2009

Leading cause of death in the world

Only 1/3 of the cardiovascular risk is targeted by the best current treatments

A primary cause: atherosclerosis

Atherosclerosis: accumulation of cholesterol plaque in the arteries

Corporate Presentation| June 2016

How to eliminate the build-up of cholesterol plaque

5

HDL: THE SOLUTION FOR EFFICIENTLY REMOVING CHOLESTEROL

Food

Liver

Elimination

Artery

Badcholesterol: LDL 1

Goodcholesterol: HDL 2

Causes atherosclerosis Removes cholesterolfrom artery walls

1. LDL: Low Density Lipoprotein2. HDL: High Density Lipoprotein

Corporate Presentation| June 2016

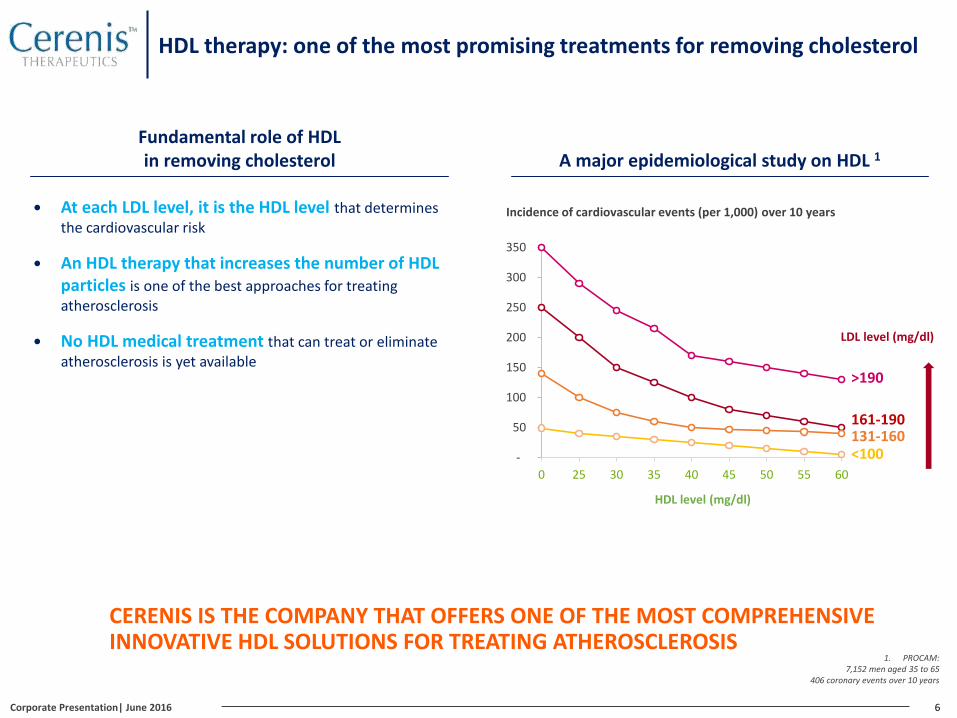

HDL therapy: one of the most promising treatments for removing cholesterol

6

Fundamental role of HDLin removing cholesterol

At each LDL level, it is the HDL level that determines the cardiovascular risk

An HDL therapy that increases the number of HDL particles is one of the best approaches for treating atherosclerosis

No HDL medical treatment that can treat or eliminate atherosclerosis is yet available

A major epidemiological study on HDL 1

Incidence of cardiovascular events (per 1,000) over 10 years

-

50

100

150

200

250

300

350

0 25 30 35 40 45 50 55 60

HDL level (mg/dl)

161-190131-160

>190

<100

LDL level (mg/dl)

CERENIS IS THE COMPANY THAT OFFERS ONE OF THE MOST COMPREHENSIVEINNOVATIVE HDL SOLUTIONS FOR TREATING ATHEROSCLEROSIS

1. PROCAM: 7,152 men aged 35 to 65

406 coronary events over 10 years

Corporate Presentation| June 2016

7

2005: creation of Cerenis 2015 2016 2017 2018

Product Indications

CER-001(HDLmimetic)

Post Acute Coronary Syndrome(ACS)

HDL genetic defects (FPHA 1)

CER-209(P2Y13 receptor agonist)

NAFLD/NASH/Atherosclerosis

Financing to date

Investors

Phase I

Phase II

Request for marketing approval

2nd Phase II

€25 m in 2005 €50 m in 2010€42 m in 2006

1st Phase II

Orphan disease designation

Preclinical development

POC 2

IPO:€53.4 m in 2015

POC 2

Preclinical development

Preclinical Clinical

Phase I Phase III

1. Familial Primary Hypoalphalipoproteinemia2. Proof of Concept

AMM

10 years of R&D to achieve one of the world’s most advanced HDL solutions

Preclinical development undergoing

POC 2 Clinical development plan to be defined

3 TARGETED INDICATIONS: ACS, FPHA AND NAFLD/NASH/ATHEROSCLEROSIS

Corporate Presentation| June 2016

Contents

Highlights since IPO

Potential for development in a large market

An HDL therapy with a validated manufacturing process

Compelling clinical results

1

2

3

4

8Corporate Presentation| June 2016

Part 1

Potential for development in a large market

10

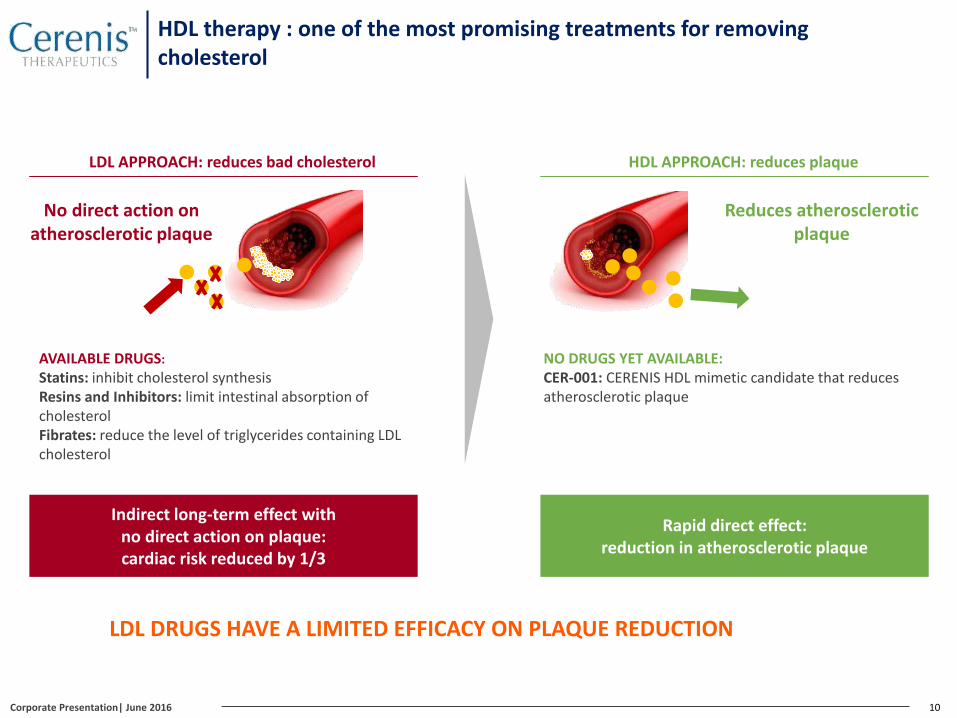

LDL DRUGS HAVE A LIMITED EFFICACY ON PLAQUE REDUCTION

Indirect long-term effect with no direct action on plaque:cardiac risk reduced by 1/3

LDL APPROACH: reduces bad cholesterol

Rapid direct effect: reduction in atherosclerotic plaque

HDL APPROACH: reduces plaque

Reduces atheroscleroticplaque

AVAILABLE DRUGS:

Statins: inhibit cholesterol synthesisResins and Inhibitors: limit intestinal absorption of cholesterolFibrates: reduce the level of triglycerides containing LDLcholesterol

No direct action on atherosclerotic plaque

NO DRUGS YET AVAILABLE:CER-001: CERENIS HDL mimetic candidate that reduces atherosclerotic plaque

HDL therapy : one of the most promising treatments for removing cholesterol

Corporate Presentation| June 2016

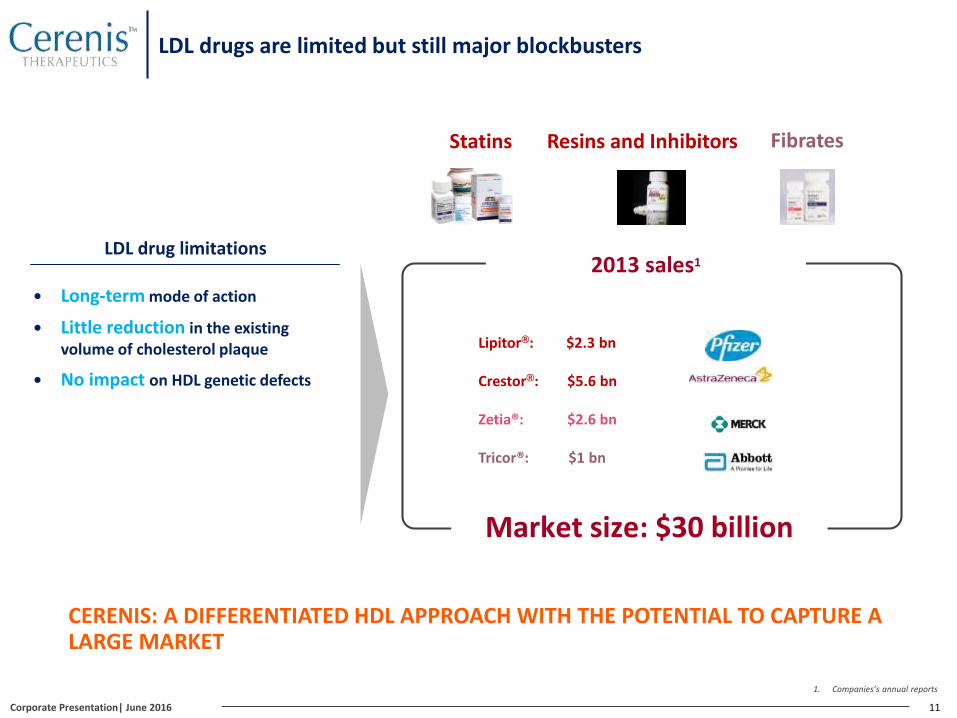

LDL drugs are limited but still major blockbusters

11

Lipitor®: $2.3 bn

Crestor®: $5.6 bn

Zetia®: $2.6 bn

Tricor®: $1 bn

Market size: $30 billion

2013 sales1

Statins Resins and Inhibitors Fibrates

LDL drug limitations

Long-term mode of action

Little reduction in the existing volume of cholesterol plaque

No impact on HDL genetic defects

CERENIS: A DIFFERENTIATED HDL APPROACH WITH THE POTENTIAL TO CAPTURE A LARGE MARKET

1. Companies’s annual reports

Corporate Presentation| June 2016

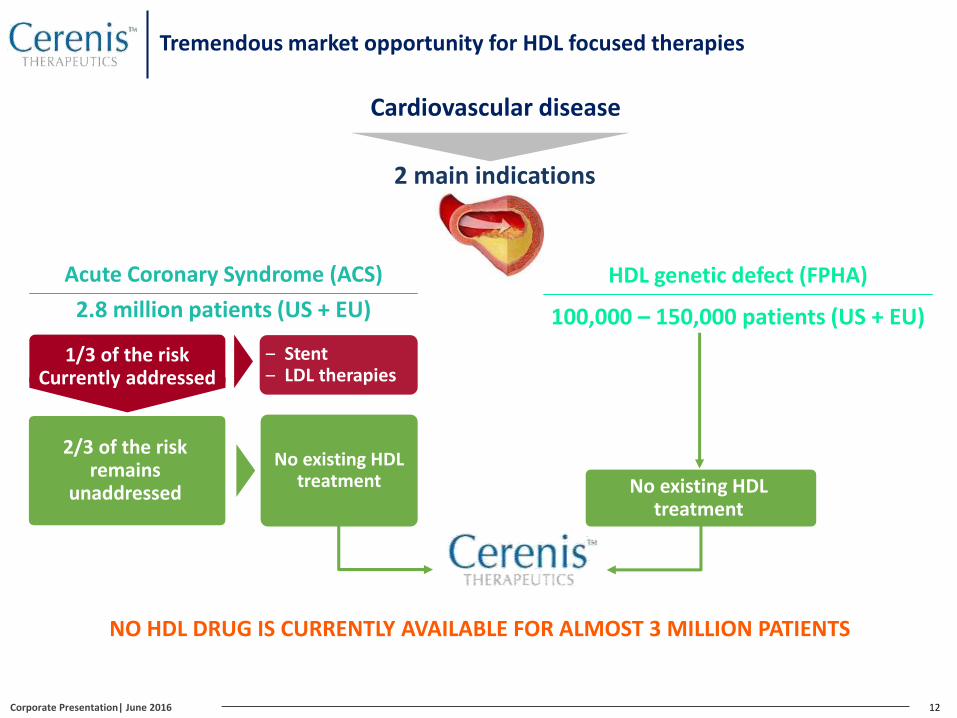

2 main indications

2.8 million patients (US + EU)

Acute Coronary Syndrome (ACS)

12

NO HDL DRUG IS CURRENTLY AVAILABLE FOR ALMOST 3 MILLION PATIENTS

Cardiovascular disease

100,000 – 150,000 patients (US + EU)

HDL genetic defect (FPHA)

No existing HDLtreatment

No existing HDLtreatment

‒ Stent‒ LDL therapies

2/3 of the risk remains

unaddressed

1/3 of the risk Currently addressed

Tremendous market opportunity for HDL focused therapies

Corporate Presentation| June 2016

13

12% 2 of patients relapse during the 12 months following an ACS, 2/3 of them during the first 2 months

19-26% 3 of patients over 45 years old die during the 12 months that follow a cardiovascular event

ACS hospitalization costs: $20,000 - $60,000 per patient per event

HDL THERAPY IS THE ONLY SOLUTION FOR THE CRITICAL 2-MONTH POST-ACS PERIOD

1. Vale N. et al Cochrane Database of Systematic Reviews 2014, Issue 9.2. PLATO clinical study, AstraZeneca

3. Source: AHS

Cardiovascular risk (relapse + mortality)

Critical period:the first 2 months

Rapid action Long-term action

1 year2 months

12%

HDL therapy:CERENIS LDL drugs (address 1/3 of the risk)

STATINS1, FIBRATES, RESINS

Value proposition: HDL therapy for ACS

Corporate Presentation| June 2016

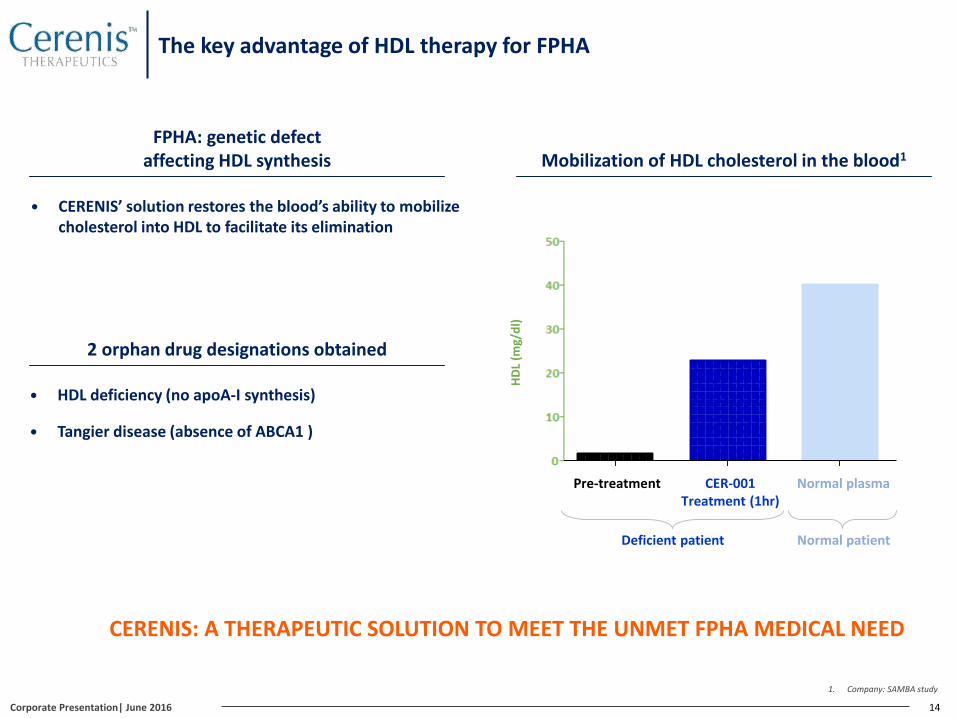

The key advantage of HDL therapy for FPHA

14

CERENIS: A THERAPEUTIC SOLUTION TO MEET THE UNMET FPHA MEDICAL NEED

HDL deficiency (no apoA-I synthesis)

Tangier disease (absence of ABCA1 )

FPHA: genetic defect affecting HDL synthesis

CERENIS’ solution restores the blood’s ability to mobilize cholesterol into HDL to facilitate its elimination

Mobilization of HDL cholesterol in the blood1

HD

L (m

g/d

l)

Pre-treatment CER-001 Treatment (1hr)

Normal plasma

Deficient patient Normal patient

2 orphan drug designations obtained

0

10

20

30

40

50

HD

L (

mg

/dl)

1. Company: SAMBA study

Corporate Presentation| June 2016

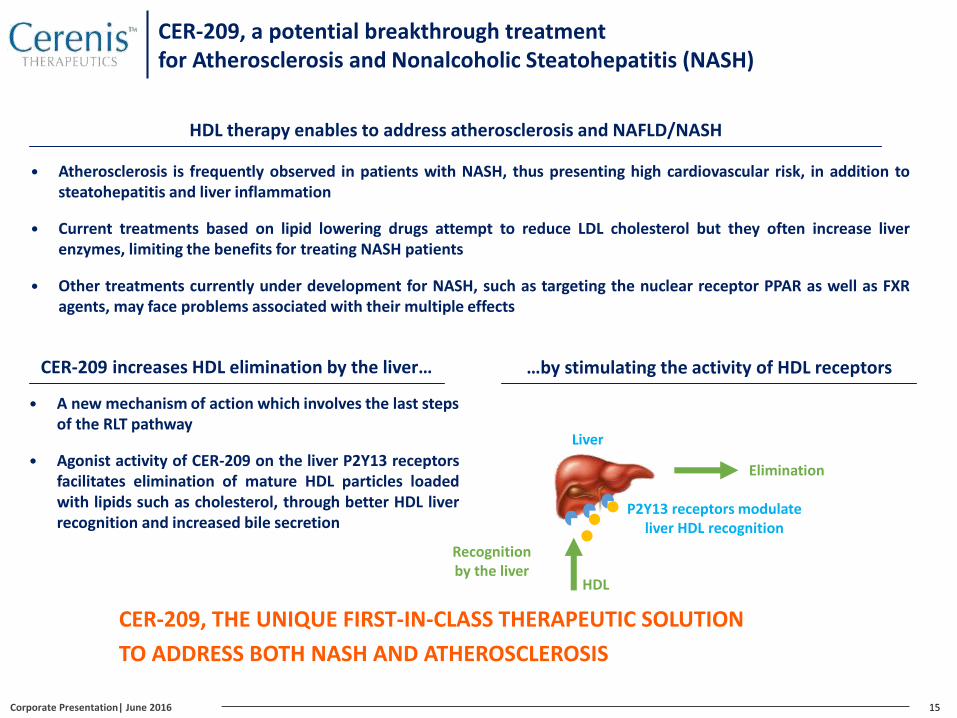

CER-209, a potential breakthrough treatmentfor Atherosclerosis and Nonalcoholic Steatohepatitis (NASH)

15

HDL therapy enables to address atherosclerosis and NAFLD/NASH

Atherosclerosis is frequently observed in patients with NASH, thus presenting high cardiovascular risk, in addition tosteatohepatitis and liver inflammation

Current treatments based on lipid lowering drugs attempt to reduce LDL cholesterol but they often increase liverenzymes, limiting the benefits for treating NASH patients

Other treatments currently under development for NASH, such as targeting the nuclear receptor PPAR as well as FXRagents, may face problems associated with their multiple effects

Liver

Elimination

P2Y13 receptors modulate liver HDL recognition

HDL

CER-209 increases HDL elimination by the liver…

A new mechanism of action which involves the last steps of the RLT pathway

Agonist activity of CER-209 on the liver P2Y13 receptorsfacilitates elimination of mature HDL particles loadedwith lipids such as cholesterol, through better HDL liverrecognition and increased bile secretion

CER-209, THE UNIQUE FIRST-IN-CLASS THERAPEUTIC SOLUTION

TO ADDRESS BOTH NASH AND ATHEROSCLEROSIS

…by stimulating the activity of HDL receptors

Recognition by the liver

Corporate Presentation| June 2016

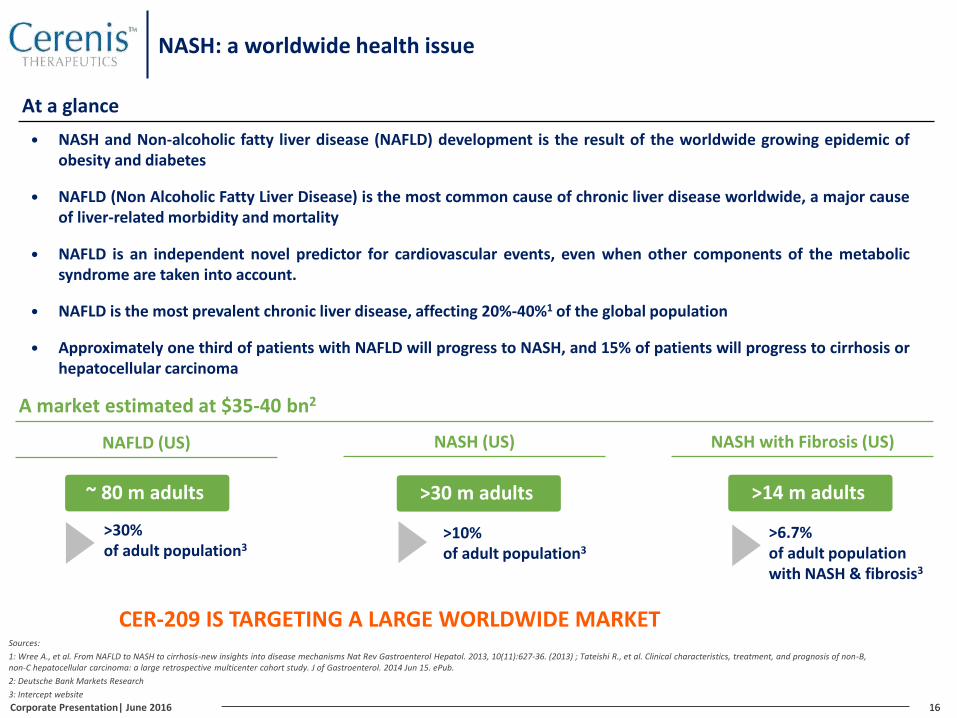

NASH: a worldwide health issue

16

A market estimated at $35-40 bn2

NAFLD (US)

>30% of adult population3

NASH (US)

>10% of adult population3

NASH with Fibrosis (US)

>6.7% of adult populationwith NASH & fibrosis3

NASH and Non-alcoholic fatty liver disease (NAFLD) development is the result of the worldwide growing epidemic ofobesity and diabetes

NAFLD (Non Alcoholic Fatty Liver Disease) is the most common cause of chronic liver disease worldwide, a major causeof liver-related morbidity and mortality

NAFLD is an independent novel predictor for cardiovascular events, even when other components of the metabolicsyndrome are taken into account.

NAFLD is the most prevalent chronic liver disease, affecting 20%-40%1 of the global population

Approximately one third of patients with NAFLD will progress to NASH, and 15% of patients will progress to cirrhosis orhepatocellular carcinoma

~ 80 m adults >30 m adults >14 m adults

At a glance

Sources:

1: Wree A., et al. From NAFLD to NASH to cirrhosis-new insights into disease mechanisms Nat Rev Gastroenterol Hepatol. 2013, 10(11):627-36. (2013) ; Tateishi R., et al. Clinical characteristics, treatment, and prognosis of non-B, non-C hepatocellular carcinoma: a large retrospective multicenter cohort study. J of Gastroenterol. 2014 Jun 15. ePub.

2: Deutsche Bank Markets Research

3: Intercept website

CER-209 IS TARGETING A LARGE WORLDWIDE MARKET

Corporate Presentation| June 2016

Part 2

An HDL therapy with a validated manufacturing process

18

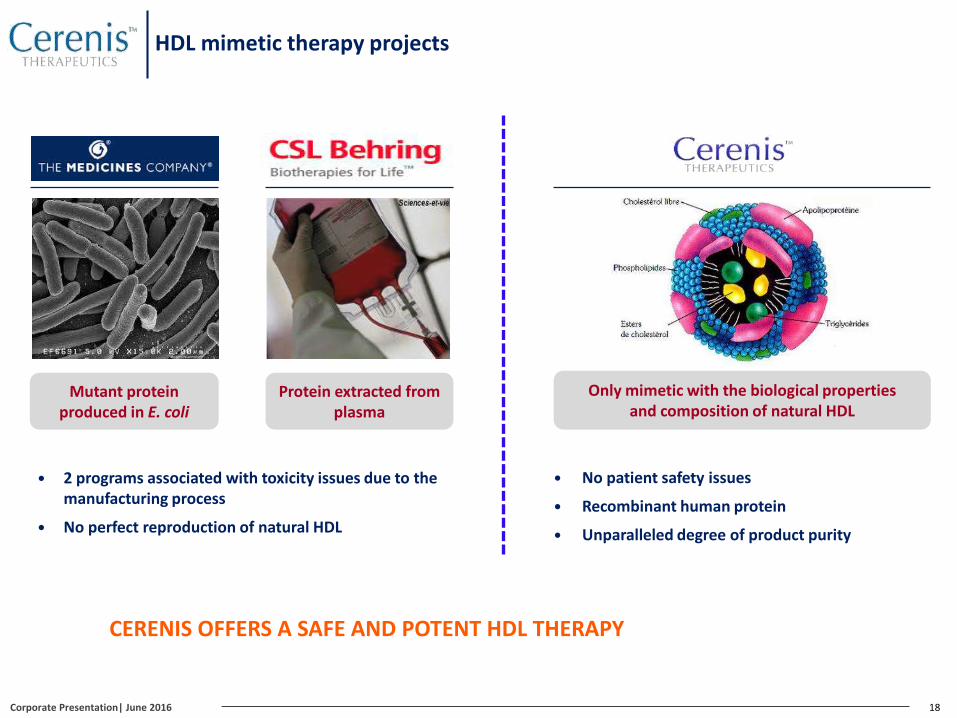

CERENIS OFFERS A SAFE AND POTENT HDL THERAPY

Mutant protein produced in E. coli

Protein extracted from plasma

Only mimetic with the biological properties and composition of natural HDL

2 programs associated with toxicity issues due to the manufacturing process

No perfect reproduction of natural HDL

No patient safety issues

Recombinant human protein

Unparalleled degree of product purity

HDL mimetic therapy projects

Corporate Presentation| June 2016

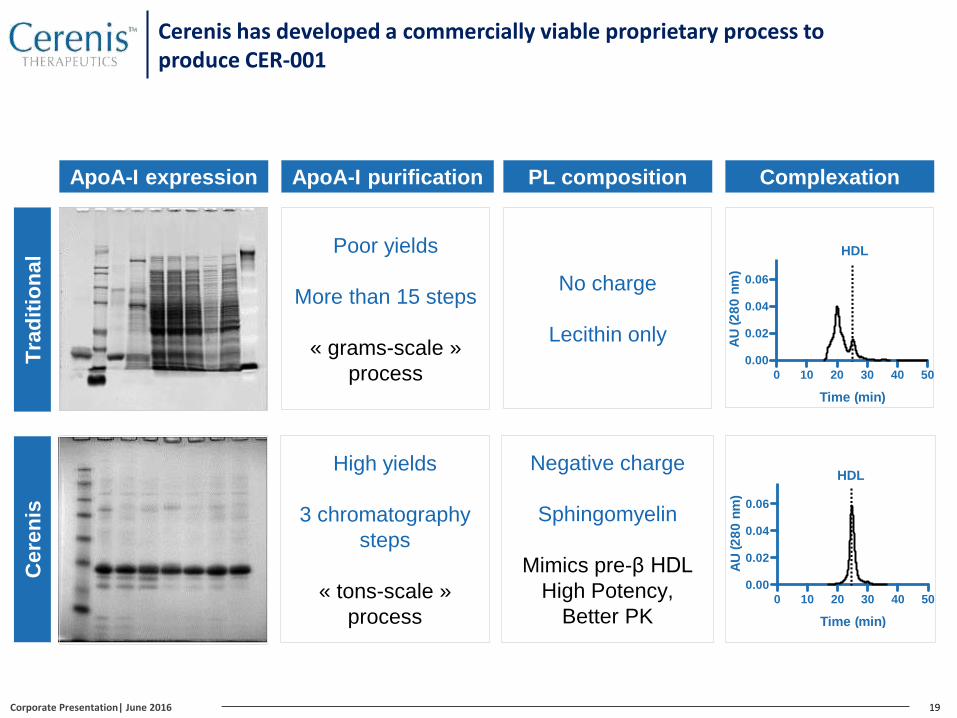

Cerenis has developed a commercially viable proprietary process to produce CER-001

19

Poor yields

More than 15 steps

« grams-scale »

process

High yields

3 chromatography

steps

« tons-scale »

process

Tra

dit

ion

al

Cere

nis

0 10 20 30 40 50

0.00

0.02

0.04

0.06

Time (min)

AU

(2

80

nm

)

0 10 20 30 40 50

0.00

0.02

0.04

0.06

Time (min)

AU

(2

80

nm

)

HDL

HDL

No charge

Lecithin only

Negative charge

Sphingomyelin

Mimics pre-β HDL

High Potency,

Better PK

ApoA-I purification ComplexationPL compositionApoA-I expression

Corporate Presentation| June 2016

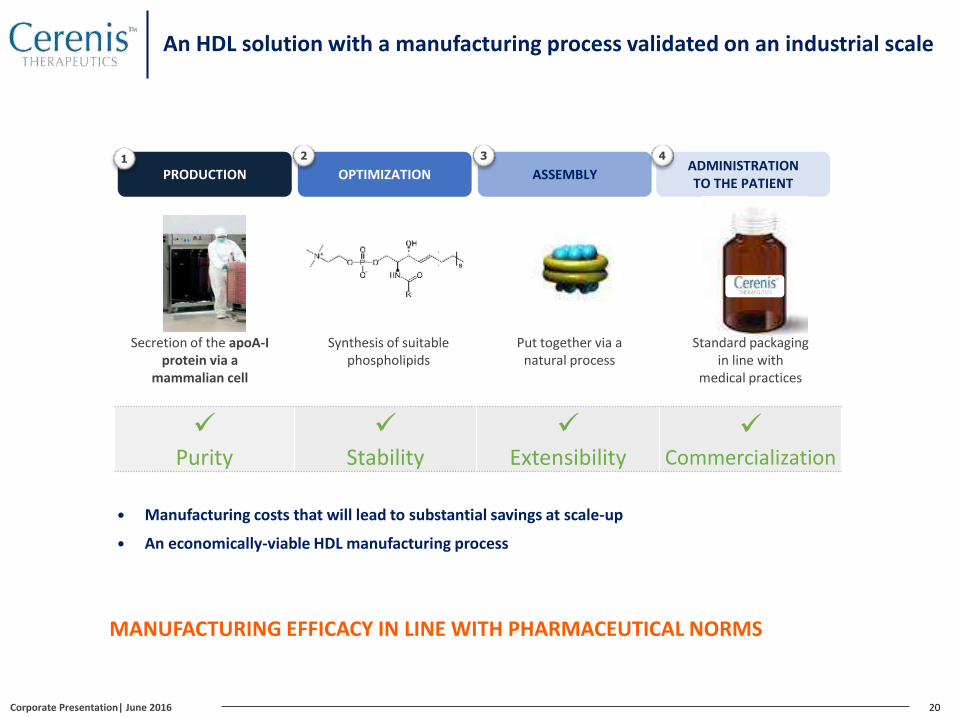

An HDL solution with a manufacturing process validated on an industrial scale

20

OPTIMIZATION

2

PRODUCTION ASSEMBLY

31

Purity

Stability

Extensibility

Commercialization

Secretion of the apoA-I protein via a

mammalian cell

Synthesis of suitable phospholipids

Put together via a natural process

ADMINISTRATION TO THE PATIENT

4

Manufacturing costs that will lead to substantial savings at scale-up

An economically-viable HDL manufacturing process

MANUFACTURING EFFICACY IN LINE WITH PHARMACEUTICAL NORMS

Standard packaging in line with

medical practices

Corporate Presentation| June 2016

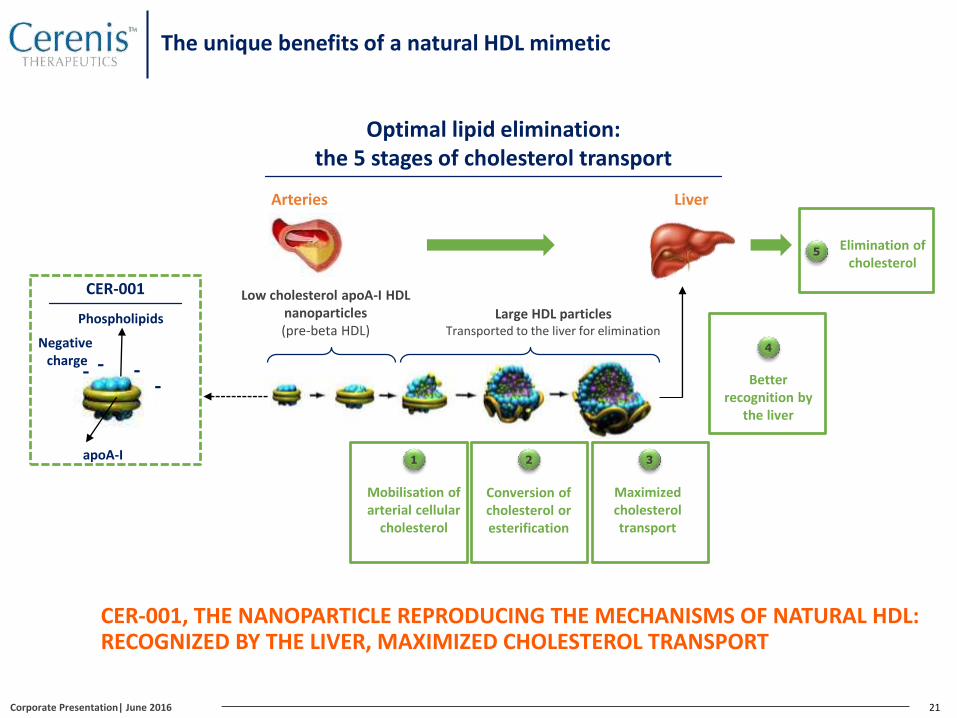

21

Optimal lipid elimination: the 5 stages of cholesterol transport

LiverArteries

Low cholesterol apoA-I HDL nanoparticles(pre-beta HDL)

1 2

Large HDL particlesTransported to the liver for elimination

3

Mobilisation of arterial cellular

cholesterol

Conversion of cholesterol or esterification

Maximized cholesterol transport

Better recognition by

the liver

4

Elimination of cholesterol

5

Phospholipids

apoA-I

CER-001

- --

-

Negative charge

CER-001, THE NANOPARTICLE REPRODUCING THE MECHANISMS OF NATURAL HDL: RECOGNIZED BY THE LIVER, MAXIMIZED CHOLESTEROL TRANSPORT

The unique benefits of a natural HDL mimetic

Corporate Presentation| June 2016

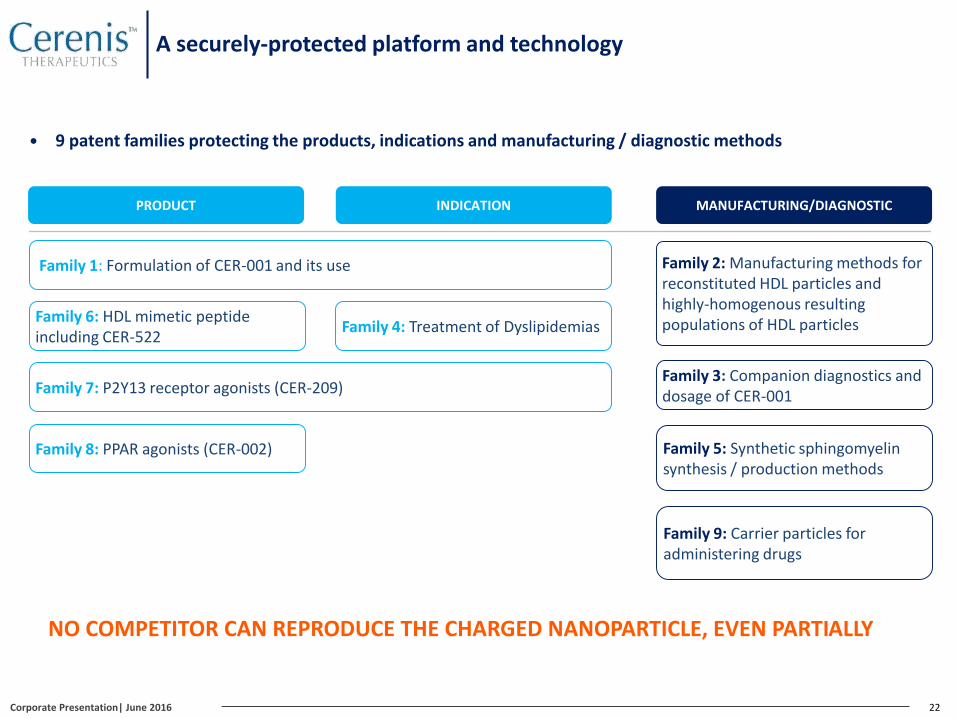

A securely-protected platform and technology

9 patent families protecting the products, indications and manufacturing / diagnostic methods

22

PRODUCT INDICATION MANUFACTURING/DIAGNOSTIC

Family 1: Formulation of CER-001 and its use Family 2: Manufacturing methods for reconstituted HDL particles and highly-homogenous resulting populations of HDL particles

Family 3: Companion diagnostics and dosage of CER-001

Family 4: Treatment of Dyslipidemias

Family 5: Synthetic sphingomyelinsynthesis / production methods

Family 6: HDL mimetic peptide including CER-522

Family 7: P2Y13 receptor agonists (CER-209)

Family 8: PPAR agonists (CER-002)

Family 9: Carrier particles for administering drugs

NO COMPETITOR CAN REPRODUCE THE CHARGED NANOPARTICLE, EVEN PARTIALLY

Corporate Presentation| June 2016

A safe and industrializable natural mimetic solution

CERENISThe Medicines

CompanyCSL

Product specificity

Only mimetic with the biological properties of natural HDL

Mutant protein produced in an E.colibacteria

Protein extracted from plasma

Composition of the nanoparticle

Natural HDL mimetic Mutant formMultiple forms of A-I apolipoprotein

Competitive advantage of CER-001

Purity Homogenous particle population

Mobilization of cholesterol / Efficacy Lower required dosage

Side effects/Toxicity No identified toxicity

Intellectual property Protection of the active principle blocking

any reproduction of the nanoparticle

Composition Only charged-complexnatural HDL mimetic

Manufacturing process Only 3 purification steps

23Corporate Presentation| June 2016

Part 3

Compelling clinical results

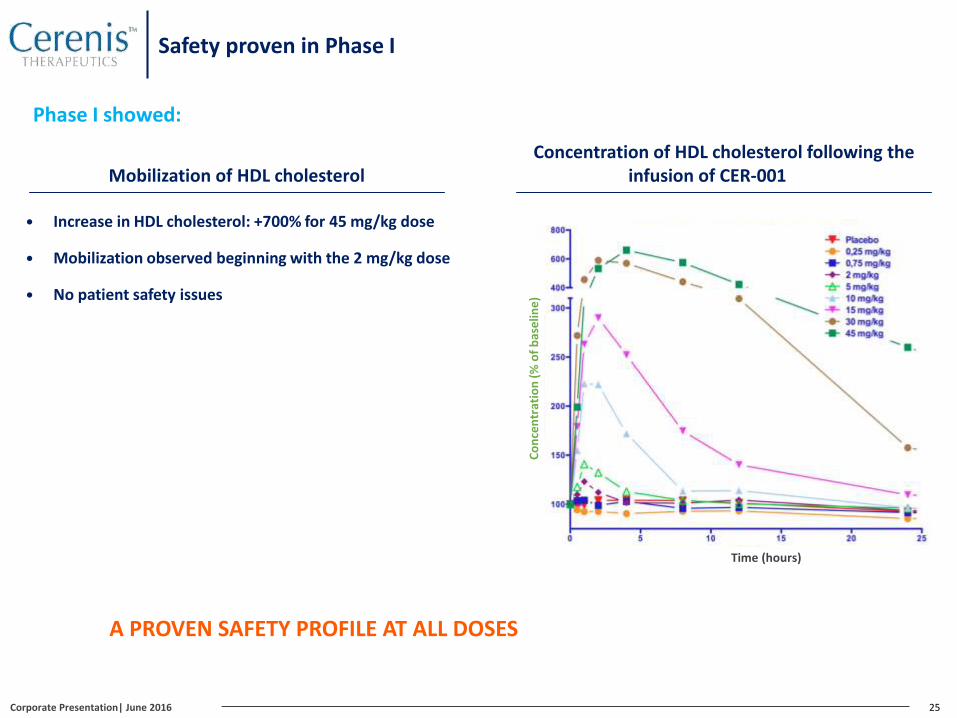

Safety proven in Phase I

25

A PROVEN SAFETY PROFILE AT ALL DOSES

Mobilization of HDL cholesterol

Increase in HDL cholesterol: +700% for 45 mg/kg dose

Mobilization observed beginning with the 2 mg/kg dose

No patient safety issues

Concentration of HDL cholesterol following the infusion of CER-001

Phase I showed:

Co

nce

ntr

atio

n (

% o

fb

ase

line

)

Time (hours)

Corporate Presentation| June 2016

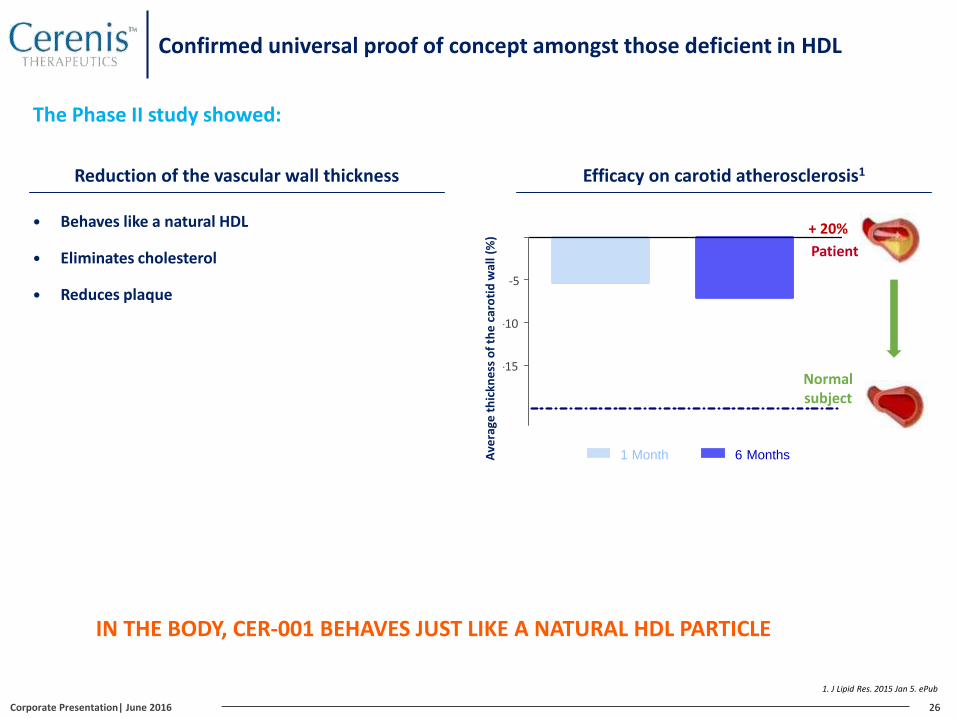

Confirmed universal proof of concept amongst those deficient in HDL

26

IN THE BODY, CER-001 BEHAVES JUST LIKE A NATURAL HDL PARTICLE

-15

-10

-5

1 Month 6 Months

+ 20%

Normal subject

Reduction of the vascular wall thickness

Behaves like a natural HDL

Eliminates cholesterol

Reduces plaque

The Phase II study showed:

Efficacy on carotid atherosclerosis1

Patient

Ave

rage

th

ickn

ess

of

the

car

oti

d w

all (

%)

1. J Lipid Res. 2015 Jan 5. ePub

Corporate Presentation| June 2016

27

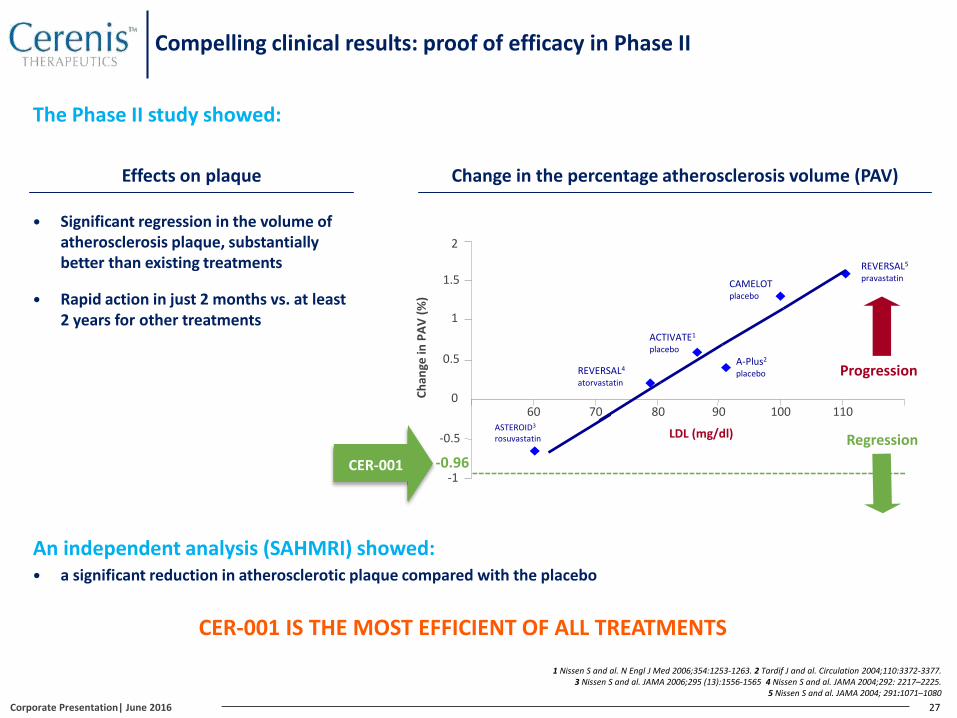

An independent analysis (SAHMRI) showed: a significant reduction in atherosclerotic plaque compared with the placebo

Change in the percentage atherosclerosis volume (PAV)

CAMELOT placebo

ACTIVATE1

placebo

REVERSAL4

atorvastatin

2

Ch

ange

in P

AV

(%)

-1

-0.5

0

0.5

1

1.5

60 70 80 90 100 110

A-Plus2

placebo

REVERSAL5

pravastatin

LDL (mg/dl)

Progression

ASTEROID3

rosuvastatin

CER-001

Regression

-0.96

CER-001 IS THE MOST EFFICIENT OF ALL TREATMENTS

Effects on plaque

Significant regression in the volume of atherosclerosis plaque, substantially better than existing treatments

Rapid action in just 2 months vs. at least 2 years for other treatments

The Phase II study showed:

1 Nissen S and al. N Engl J Med 2006;354:1253-1263. 2 Tardif J and al. Circulation 2004;110:3372-3377. 3 Nissen S and al. JAMA 2006;295 (13):1556-1565 4 Nissen S and al. JAMA 2004;292: 2217–2225.

5 Nissen S and al. JAMA 2004; 291:1071–1080

Compelling clinical results: proof of efficacy in Phase II

Corporate Presentation| June 2016

28

THE OPTIMAL DOSE HAS BEEN IDENTIFIED THE OPTIMAL NUMBER OF INFUSIONS STILL NEEDS TO BE DETERMINED

An independent analysis (SAHMRI) confirmed the optimal dose2 :

Conclusions of CHI-SQUARE, the 1st Phase II study:

Cholesterol mobilization by CER-001 at every dose level

Demonstrated patient safety profile

Primary endpoint, defined with 12 mg/kg dose, not achieved

Reduction in the total volume of atherosclerosis vs. baseline was statistically significant from 3 mg/kg

Too high a concentration of HDL induces a down-regulation of ABCA1 transporter, which is necessary for cholesterol efflux. The 12 mg/kg dose caused such a down-regulation whereas 3 mg/kg did not resulting in the highest efficacy

The optimal dose enabling a maximization of the plaque regression vs. placebo: 3 mg/kg Next study: number of infusions

Change in the percentage atherosclerosis volume (PAV)Patients with PAV≥30 at baseline

1. Statistically significant result2. Greater regression of coronary atherosclerosis with the pre-beta high-density

lipoprotein mimetic CER-001 in patients with more extensive plaque burden American Heart Association sessions 2015, S. Nicholls et al.

Compelling clinical results: identification of the optimal dose for treatment

ParameterPlacebo

(n=69)

3 mg/kg

(n=58)

6 mg/kg

(n=78)

12 mg/kg

(n=66)

PAV -0.259 -0.963 -0.619 +0.177

P value 0.038 1 0.287 0.587

Corporate Presentation| June 2016

29

CER-001 induced greater plaque regression in patients with baseline PAV≥ 30%

An inverse relationship was observed between CER-001 dose and effect on plaque burden

These findings identify patients who are most likely to benefit from CER-001 infusions and the most biologically active dose

Greater regression of coronary atherosclerosis with the pre-beta high-density lipoprotein mimetic CER-001 in patients with more extensive plaque burden

American Heart Association sessions 2015, S. Nicholls et al.

Corporate Presentation| June 2016

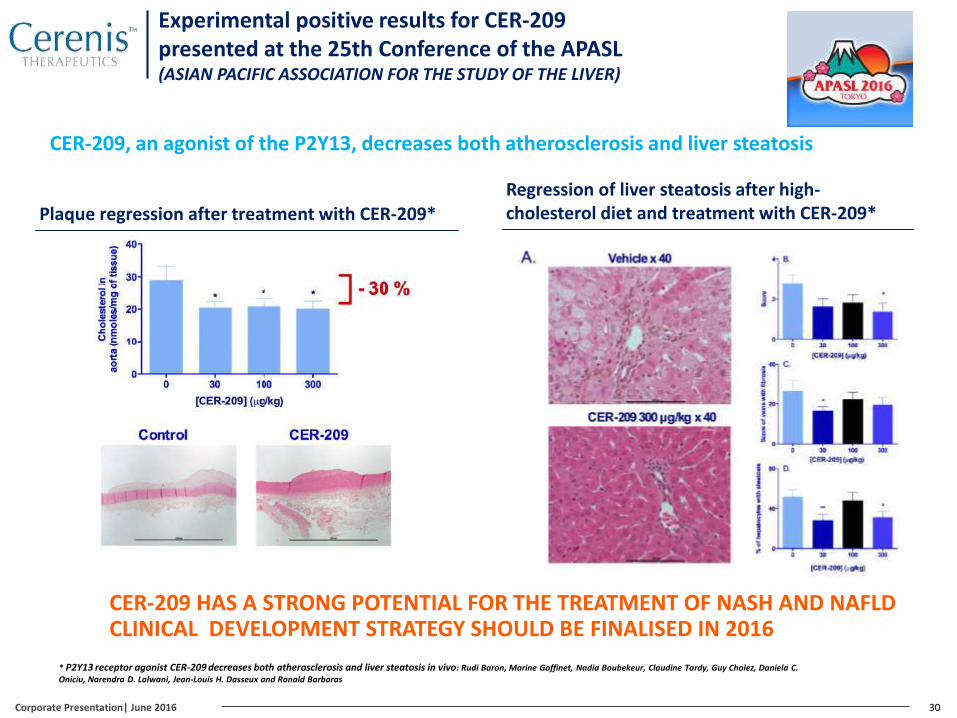

Experimental positive results for CER-209 presented at the 25th Conference of the APASL(ASIAN PACIFIC ASSOCIATION FOR THE STUDY OF THE LIVER)

CER-209, an agonist of the P2Y13, decreases both atherosclerosis and liver steatosis

30Corporate Presentation| June 2016

CER-209 HAS A STRONG POTENTIAL FOR THE TREATMENT OF NASH AND NAFLDCLINICAL DEVELOPMENT STRATEGY SHOULD BE FINALISED IN 2016

Plaque regression after treatment with CER-209*Regression of liver steatosis after high-cholesterol diet and treatment with CER-209*

* P2Y13 receptor agonist CER-209 decreases both atherosclerosis and liver steatosis in vivo: Rudi Baron, Marine Goffinet, Nadia Boubekeur, Claudine Tardy, Guy Cholez, Daniela C.

Oniciu, Narendra D. Lalwani, Jean-Louis H. Dasseux and Ronald Barbaras

Indications Preclinical Phase I Phase II Phase III

Products due to enter a new development phase

CER-001RecombinantHDL

Post-ACS

FPHA:Orphan diseaseApoA-I and ABCA1 deficiency

CER-209Stimulation of HDL receptors

Dyslipidemia with low HDL

Non-alcoholic steatohepatitis(NASH/NAFLD/Atherosclerosis)

Products in the portfolio

CER-522(back-up)

Peptide HDLMimetic

Aortic Valve Stenosis

CER-002Specific PPARdelta agonist

Dyslipidemia with low HDL

Non-alcoholic steatohepatitis (NASH)

Systemic Lupus Erythematosus (SLE)

Future growth drivers

31

A structured and diversified portfolio

Corporate Presentation| June 2016

Part 4

Highlights since IPO

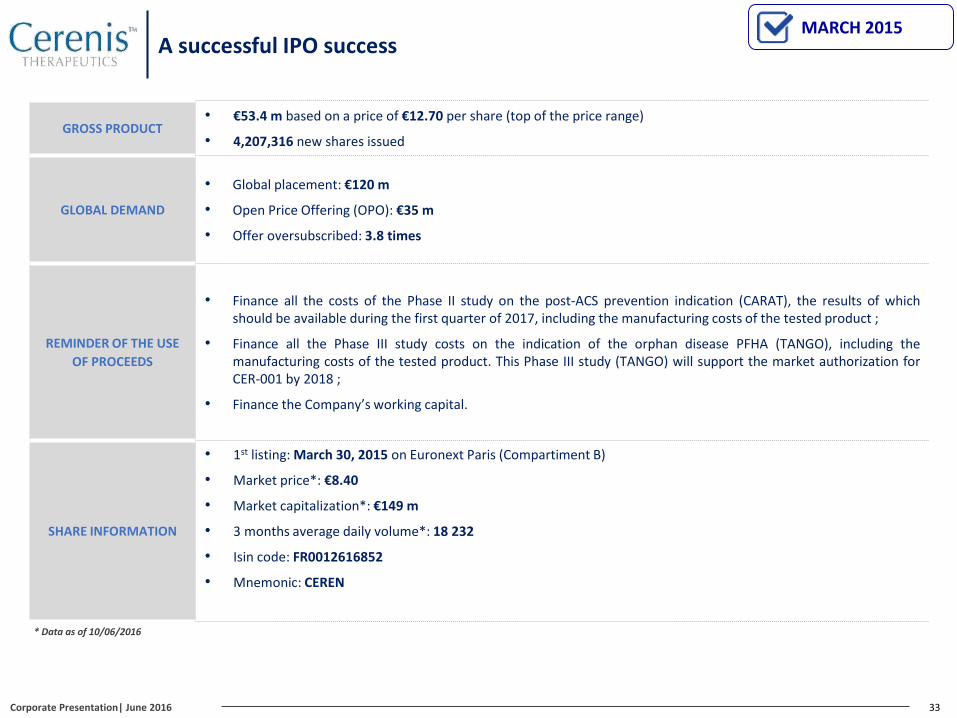

A successful IPO success

33

GROSS PRODUCT• €53.4 m based on a price of €12.70 per share (top of the price range)

• 4,207,316 new shares issued

GLOBAL DEMAND

• Global placement: €120 m

• Open Price Offering (OPO): €35 m

• Offer oversubscribed: 3.8 times

REMINDER OF THE USE

OF PROCEEDS

• Finance all the costs of the Phase II study on the post-ACS prevention indication (CARAT), the results of whichshould be available during the first quarter of 2017, including the manufacturing costs of the tested product ;

• Finance all the Phase III study costs on the indication of the orphan disease PFHA (TANGO), including themanufacturing costs of the tested product. This Phase III study (TANGO) will support the market authorization forCER-001 by 2018 ;

• Finance the Company’s working capital.

SHARE INFORMATION

• 1st listing: March 30, 2015 on Euronext Paris (Compartiment B)

• Market price*: €8.40

• Market capitalization*: €149 m

• 3 months average daily volume*: 18 232

• Isin code: FR0012616852

• Mnemonic: CEREN

* Data as of 10/06/2016

MARCH 2015

Corporate Presentation| June 2016

Poster presentation at the 2015 ISA*(International Symposium on Atherosclerosis, Amsterdam)

34

CER-209, A POTENTIAL FIRST-IN-CLASS TREATMENTADDRESSING BOTH NAFLD/NASH AND ATHEROSCLEROSIS

Validation of a promising new mechanism of action focused on the treatment of both atherosclerosis and non-alcoholic steatohepatitis (NASH). CER-209 acts as a selective novel agonist of the P2Y13r, responsible for HDL recognition by liver receptors which leads to increased cholesterol and triglyceride elimination by the liver

A good preclinical safety profile

Significant decrease of liver steatosis content in the liver (NASH)

Observable decrease of atherosclerotic plaques in aorta

Preclinical models conclusion for CER-209 :

Decrease of steatohepatitis*

* Validated preclinical models: CER-209 administration following a cholesterol-intensive diet

Decrease of atherosclerotic plaques

MAY 2015

Corporate Presentation| June 2016

Appointment of two new Board Members

35

STRENGTHENING THE COMPANY’S ABILITY TO SUPERVISE ITS STRATEGY

Catherine Moukheibir, MA, MBA (Yale University)

Dr. Laura A. Coruzzi Esq., Ph.D. (University of Fordham, Mount Sinai School of Medicine)

20 years of experience in finance including 15 in the biotechnology industry

Executive board member at Innate Pharma

CFO of Movetis : leading both Euronext Brussels IPO and takeover by Shire

Director Capital Markets at ZETIA

Executive Director : Salomon Smith Barney, Morgan Stanley

Senior Vice President of Intellectual Property at REGENXBIO. Prior she was a partner in the Intellectual Property practice at Jones Day

Deeply involved in developing patent strategies related to HDL mimetics and Reverse Lipid Transport (RLT) modulating drugs

Has represented clients in biotechnology and pharmaceuticals for 30 years, participating in numerous landmark cases

Extensive experience in patent prosecution, litigation and appeals before the USPTO Board of Appeals, the Federal Circuit, and the U.S. Supreme Court

JUNE 2015

Corporate Presentation| June 2016

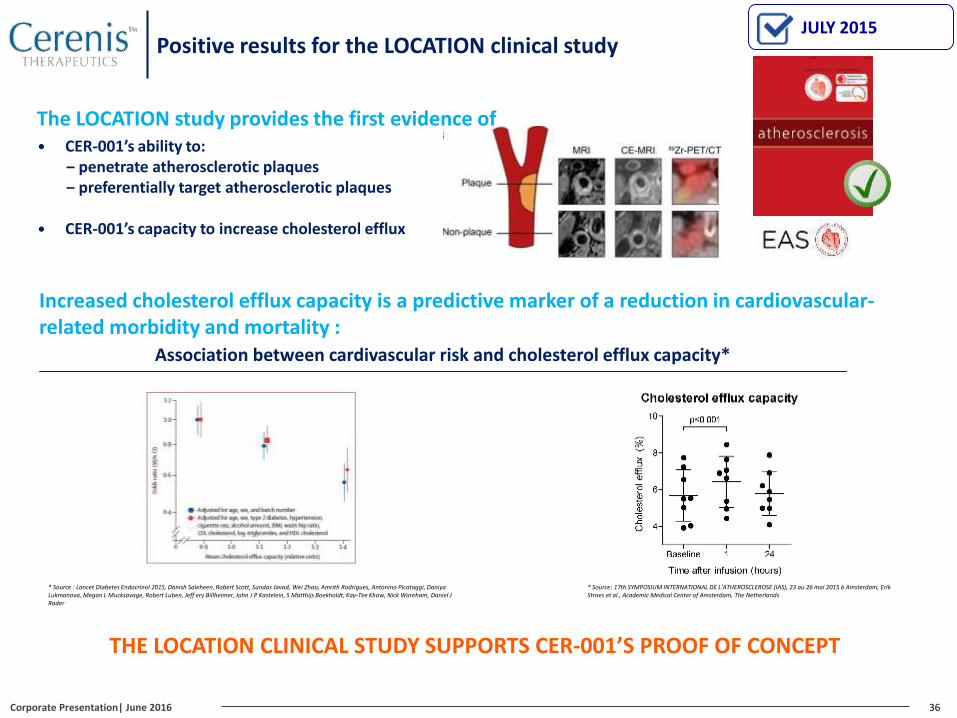

Positive results for the LOCATION clinical study

36

THE LOCATION CLINICAL STUDY SUPPORTS CER-001’S PROOF OF CONCEPT

The LOCATION study provides the first evidence of CER-001’s ability to:

‒ penetrate atherosclerotic plaques‒ preferentially target atherosclerotic plaques

CER-001’s capacity to increase cholesterol efflux

Increased cholesterol efflux capacity is a predictive marker of a reduction in cardiovascular-related morbidity and mortality :

Association between cardivascular risk and cholesterol efflux capacity*

* Source : Lancet Diabetes Endocrinol 2015, Danish Saleheen, Robert Scott, Sundas Javad, Wei Zhao, Amrith Rodrigues, Antonino Picataggi, DaniyaLukmanova, Megan L Mucksavage, Robert Luben, Jeff ery Billheimer, John J P Kastelein, S Matthijs Boekholdt, Kay-Tee Khaw, Nick Wareham, Daniel J Rader

JULY 2015

* Source: 17th SYMPOSIUM INTERNATIONAL DE L’ATHEROSCLEROSE (IAS), 23 au 26 mai 2015 a Amsterdam, Erik Stroes et al., Academic Medical Center of Amsterdam, The Netherlands

Corporate Presentation| June 2016

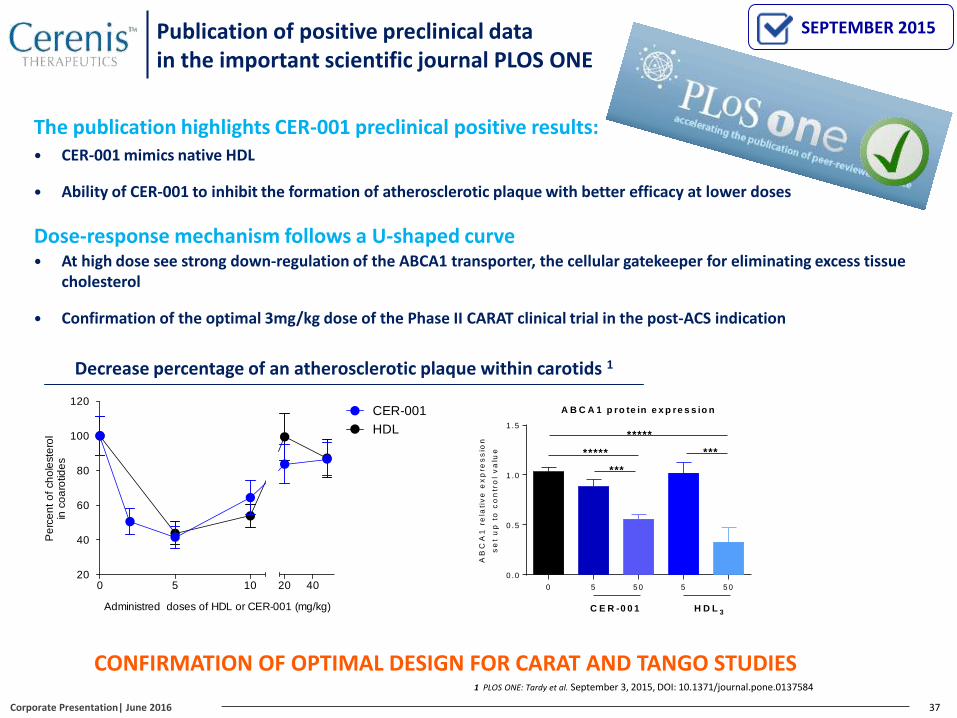

At high dose see strong down-regulation of the ABCA1 transporter, the cellular gatekeeper for eliminating excess tissue cholesterol

Confirmation of the optimal 3mg/kg dose of the Phase II CARAT clinical trial in the post-ACS indication

Dose-response mechanism follows a U-shaped curve

Publication of positive preclinical datain the important scientific journal PLOS ONE

37

CONFIRMATION OF OPTIMAL DESIGN FOR CARAT AND TANGO STUDIES

The publication highlights CER-001 preclinical positive results: CER-001 mimics native HDL

Ability of CER-001 to inhibit the formation of atherosclerotic plaque with better efficacy at lower doses

Decrease percentage of an atherosclerotic plaque within carotids 1

SEPTEMBER 2015

0 5 10 20 4020

40

60

80

100

120

Administred doses of HDL or CER-001 (mg/kg)

Pe

rce

nt

of

ch

ole

ste

rol

in c

oa

rotid

es

Percent of regression of atheroma plaques in carotides

CER-001

HDL

1 PLOS ONE: Tardy et al. September 3, 2015, DOI: 10.1371/journal.pone.0137584

A B C A 1 p ro te in e x p re s s io n

0 5 5 0 5 5 0

0 .0

0 .5

1 .0

1 .5

AB

CA

1 r

ela

tiv

e e

xp

res

sio

n

se

t u

p t

o c

on

tro

l v

alu

e *****

*****

C E R -0 0 1 H D L 3

***

***

Corporate Presentation| June 2016

CER-001: the future benchmark in HDL mimetic

Professor Stephen Nicholls“I’m particularly enthusiastic about collaborating with Cerenis

Therapeutics for the future Phase II CARAT clinical study of

CER-001. On the basis of our convincing analyses of the Phase

II CHI-SQUARE study highlighting the efficacy of the optimal

3mg/kg dose, I’m highly confident regarding the potential

success of this important clinical step to establish CER-001 as

the market benchmark in HDL mimetic.

38

Dr. John Kastelein

Dr. Béla Merkely

Dr. Stephen Nicholls, Principal Investigator

Dr. Steven Nissen

Dr. Kausik Ray

Dr. Gregory Schwartz

Dr. Stephen Worthley

A prestigious steering committee for the CARAT Study

Corporate Presentation| June 2016

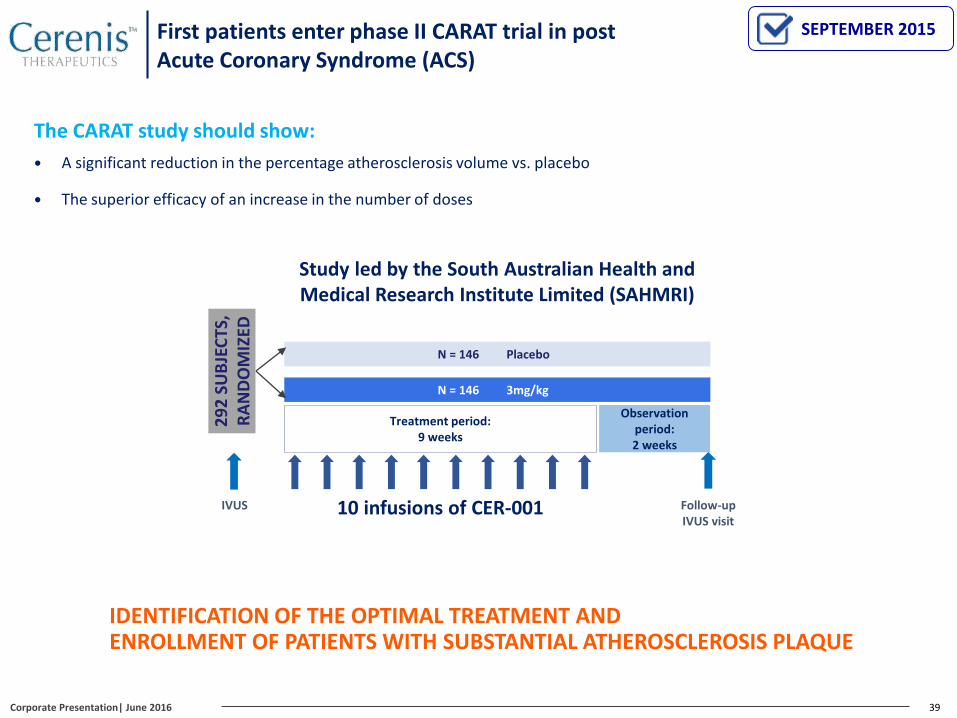

39

N = 146 Placebo

N = 146 3mg/kg

29

2 S

UB

JEC

TS,

RA

ND

OM

IZED

10 infusions of CER-001

Treatment period:9 weeks

Observation period:2 weeks

Follow-up IVUS visit

IDENTIFICATION OF THE OPTIMAL TREATMENT AND ENROLLMENT OF PATIENTS WITH SUBSTANTIAL ATHEROSCLEROSIS PLAQUE

The CARAT study should show:

A significant reduction in the percentage atherosclerosis volume vs. placebo

The superior efficacy of an increase in the number of doses

IVUS

Study led by the South Australian Health and Medical Research Institute Limited (SAHMRI)

First patients enter phase II CARAT trial in post Acute Coronary Syndrome (ACS)

SEPTEMBER 2015

Corporate Presentation| June 2016

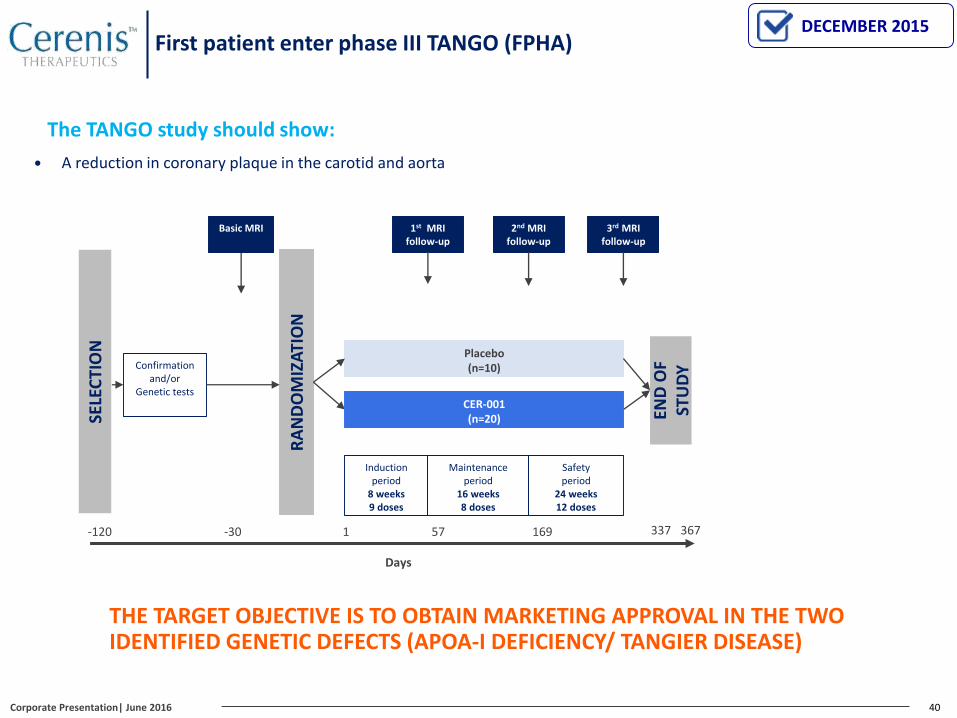

40

THE TARGET OBJECTIVE IS TO OBTAIN MARKETING APPROVAL IN THE TWO IDENTIFIED GENETIC DEFECTS (APOA-I DEFICIENCY/ TANGIER DISEASE)

SELE

CTI

ON

1st MRI follow-up

-120 1 57 337

Days

END

OF

STU

DY

169

Confirmation and/or

Genetic tests

RA

ND

OM

IZA

TIO

N

CER-001(n=20)

Placebo(n=10)

2nd MRI follow-up

3rd MRI follow-up

Induction period

8 weeks9 doses

Maintenance period

16 weeks8 doses

Safety period

24 weeks12 doses

367

Basic MRI

-30

The TANGO study should show:

A reduction in coronary plaque in the carotid and aorta

First patient enter phase III TANGO (FPHA)DECEMBER 2015

Corporate Presentation| June 2016

NAFLD/NASH/Atherosclerosis development

FPHA development, TANGO

Post-ACS development, CARAT

41

WEALTH CREATION PERSPECTIVE IN BOTH THE SHORT AND MEDIUM TERM

1st patient enrolled, FPHA study ✔

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

2017Q3

2017Q4

2018Q1

2018Q2

2018Q3

2018Q4

Last patient enrolled, FPHA study

Last visit for patients enrolled in the FPHA study

Application filed for orphan diseases

FPHA results

1st patient enrolled, CARAT study ✔

Q1CARAT results

Market approval

LOCATION study ✔

Board appointments ✔

Poster at the IAS ✔

PLOS ONE Publication✔

Done Upcoming

Solid short & medium-run newsflow

Published Newsflow

Timeline to be defined

Q3Last patient enrolled, CARAT

Q4Last IVUS visit CARAT

Corporate Presentation| June 2016

Two poster presentations on CER-209 at the APASL✔

Publication of the LOCATION clinical study results in Atherosclerosis journal ✔

42

A LISTED COMPANY WITH SUBSTANTIAL POTENTIAL IN HDL THERAPY

1. A therapy targeting 2/3 of the risk that is unmet with available medical treatments

2. Advanced and promising clinical developments

3. Compelling to big pharma (ex. of transactions, OMTHERA: $443 m, Esperion: $1.3 bn, KOS: $3.7 bn)1

4. A manufacturing process validated on an industrial level

CER-001: major potential in the treatment of patients post-ACS

In the short term: CER-001, a drug for treating orphan diseases

1. A potential of value creation in the short term

2. A major unmet medical need

3. Application for marketing approval before 2018

1. Press releases,OMTHERA: http://www.astrazeneca.com/Media/Press-releases/Article/20130528-omthera

Esperion: http://www.bloomberg.com/apps/news?pid=newsarchive&sid=apU2qcYCmkO4&refer=usKOS: http://www.bloomberg.com/apps/news?pid=newsarchive&sid=af_8tglk4fHE

Value proposition: why invest in CERENIS?

CER-209: major potential in the treatment of patients with atherosclerosis and NAFLD/NASH

1. A major unmet medical need

2. CER-209, a highly specific P2Y13 receptor agonist promoting lipid elimination

Corporate Presentation| June 2016

APPENDICES

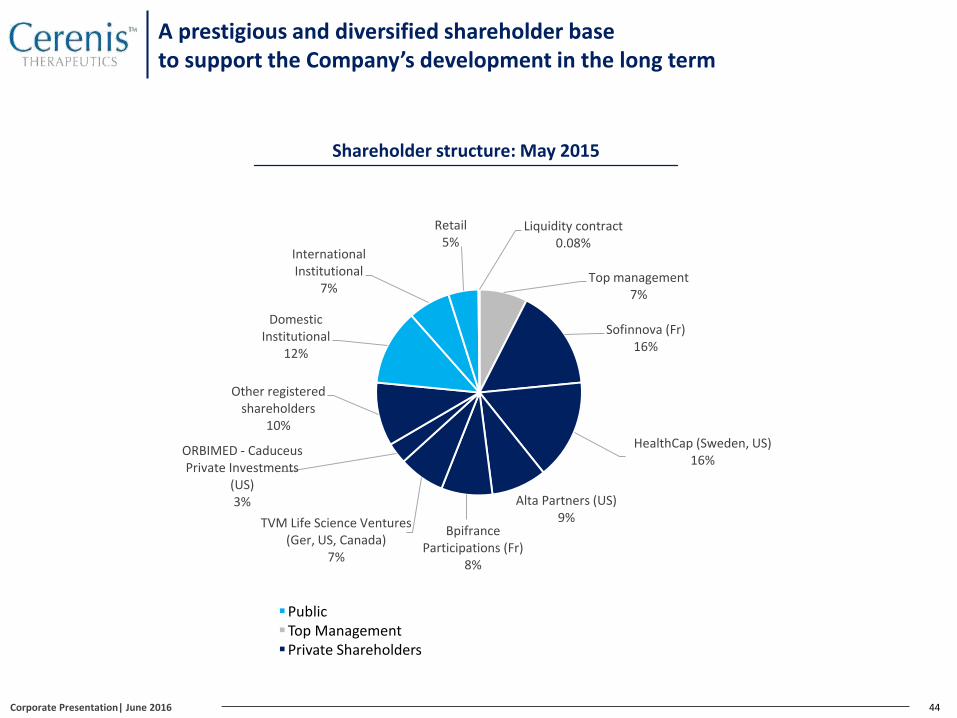

A prestigious and diversified shareholder base to support the Company’s development in the long term

44

Shareholder structure: May 2015

PublicTop ManagementPrivate Shareholders

Top management7%

Sofinnova (Fr)16%

HealthCap (Sweden, US)16%

Alta Partners (US)9%

Bpifrance Participations (Fr)

8%

TVM Life Science Ventures (Ger, US, Canada)

7%

ORBIMED - Caduceus Private Investments

(US)3%

Other registeredshareholders

10%

Domestic Institutional

12%

International Institutional

7%

Retail 5%

Liquidity contract0.08%

Corporate Presentation| June 2016

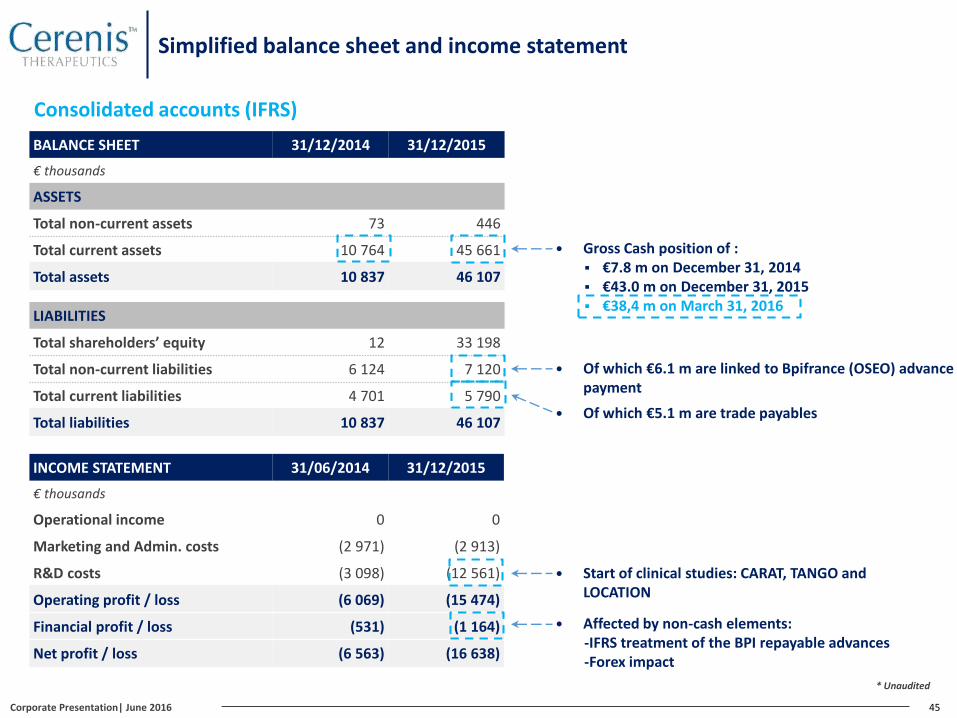

Simplified balance sheet and income statement

BALANCE SHEET 31/12/2014 31/12/2015

€ thousands

ASSETS

Total non-current assets 73 446

Total current assets 10 764 45 661

Total assets 10 837 46 107

LIABILITIES

Total shareholders’ equity 12 33 198

Total non-current liabilities 6 124 7 120

Total current liabilities 4 701 5 790

Total liabilities 10 837 46 107

INCOME STATEMENT 31/06/2014 31/12/2015

€ thousands

Operational income 0 0

Marketing and Admin. costs (2 971) (2 913)

R&D costs (3 098) (12 561)

Operating profit / loss (6 069) (15 474)

Financial profit / loss (531) (1 164)

Net profit / loss (6 563) (16 638)

Consolidated accounts (IFRS)

45

* Unaudited

Gross Cash position of : €7.8 m on December 31, 2014 €43.0 m on December 31, 2015 €38,4 m on March 31, 2016

Of which €6.1 m are linked to Bpifrance (OSEO) advancepayment

Affected by non-cash elements: -IFRS treatment of the BPI repayable advances-Forex impact

Start of clinical studies: CARAT, TANGO and LOCATION

Of which €5.1 m are trade payables

Corporate Presentation| June 2016

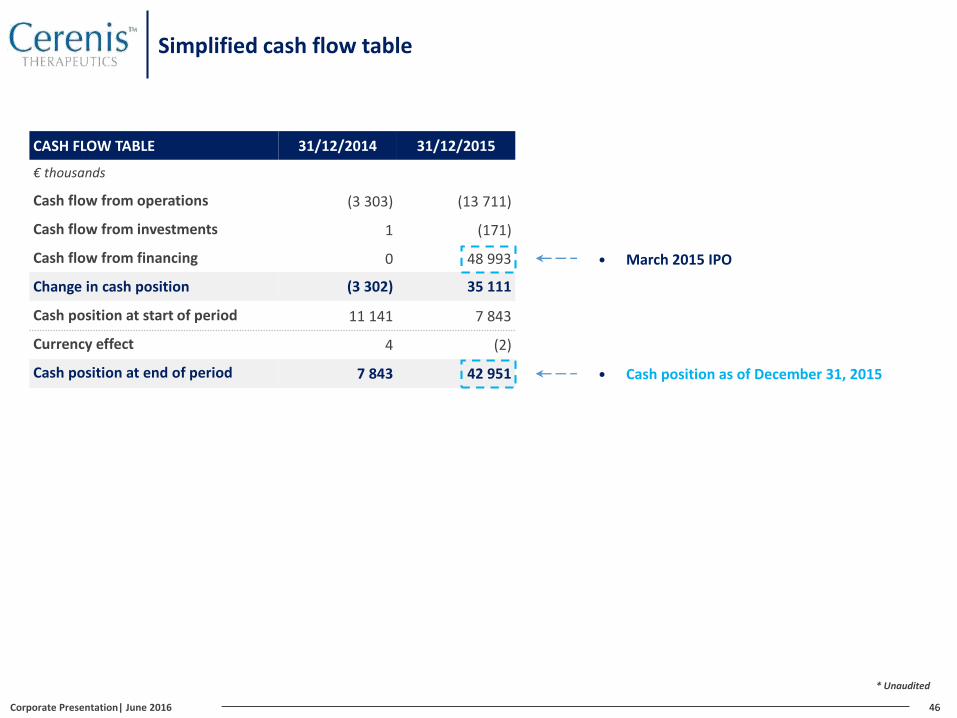

Simplified cash flow table

CASH FLOW TABLE 31/12/2014 31/12/2015

€ thousands

Cash flow from operations (3 303) (13 711)

Cash flow from investments 1 (171)

Cash flow from financing 0 48 993

Change in cash position (3 302) 35 111

Cash position at start of period 11 141 7 843

Currency effect 4 (2)

Cash position at end of period 7 843 42 951

46

* Unaudited

March 2015 IPO

Cash position as of December 31, 2015

Corporate Presentation| June 2016

Company’s funding

47

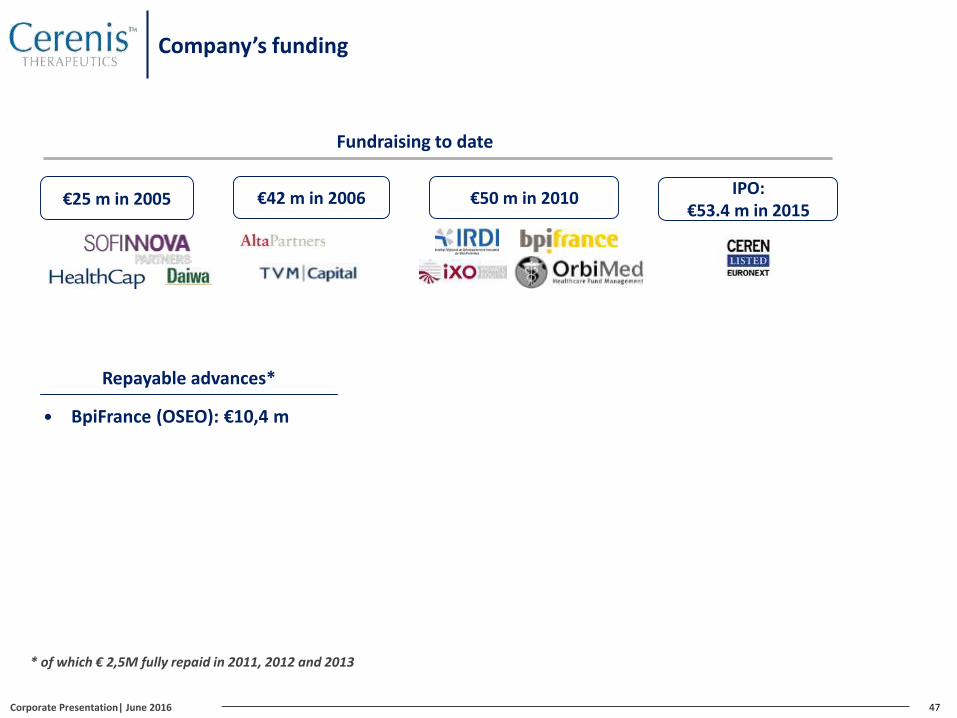

Repayable advances*

BpiFrance (OSEO): €10,4 m

€25 m in 2005 €50 m in 2010€42 m in 2006

Fundraising to date

* of which € 2,5M fully repaid in 2011, 2012 and 2013

IPO: €53.4 m in 2015

Corporate Presentation| June 2016