Embed Size (px)

Citation preview

THE HERITAGE INSURANCE COMPANY KENYA LIMITED

Annual Report & Financial Statements

2017A member of

Insurance CompanyHeritage

02

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

01CORPORATE INFORMATION 2 Corporate Information 7 Directors’ Report 8 Chairman’s statement21 Corporate Governance Report24 Statement of Directors’ Responsibilities26 Independent Auditors’ Report

02FINANCIAL STATEMENTS31 Statement of Profit or Loss32 Statement of other comprehensive income33 Statement of financial position35 Statement of changes in equity37 Statement of cash flows39 Accounting policies53 Notes to the financial statements

DIRECTORS

P.N. Gethi Kenyan ChairmanG.M. Kioi Kenyan Managing DirectorG.R. May British Non-ExecutiveM.L. du Toit South African Non-ExecutiveS. Sejpal (Ms) British Non-Executive (Resigned 20/11/2017)S.C. Wenman South African Non-ExecutiveC.W. Mwangi (Ms) Kenyan Non-Executive (Resigned 14/06/2017)Rachel Mbai Kenyan Non-Executive (Appointed 30/08/2017)Catherine Mitchem British Non-Executive (Appointed 17/11/2017)

SECRETARY

C. Kioni (Ms)P. O. Box 30390 - 00100Nairobi

SENIOR MANAGEMENT

G. M. Kioi Managing DirectorA. P. Ngunjiri Director (Medical)B. N. Hiuhu (Mrs) Director (Underwriting & Claims)L. Magambo General Manager (Finance)B. Irungu Senior Manager (Claims)I. K Kamau Senior Manager (IT)D. Mathenge Senior Manager (Finance)J. Maluki (Ms) Senior Manager (Medical)B. Maina Senior Manager (Underwriting)S. Chege Head of Retail Business

AUDITORS

KPMG KenyaCertified Public Accountants8th Floor, ABC TowersWaiyaki WayP. O. Box 40612 - 00100Nairobi

REGISTERED HEAD OFFICE

Liberty HouseMamlaka RoadP.O. Box 30390 - 00100Nairobi

PRINCIPAL BANKERS

Stanbic Bank LimitedStanbic CentreChiromo RoadP. O. Box 72833 - 00200Nairobi

Commercial Bank of Africa LimitedCBA Building Mara/ Ragati RoadP.O. Box 30437 - 00100Nairobi

CORPORATE INFORMATION0

4Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

MOMBASA Social Security HouseP.O. Box 84886 - 00100MOMBASA

ELDORET Imperial CourtP.O. Box 6120 - 30100ELDORET

NYALI Nyali CentreLinks RoadP.O. Box 84886 - 80100MOMBASA

MACHAKOS Town Plaza2nd FloorP.O. Box 211 - 90100MACHAKOS

KISII Royal Towers2nd Floor,Hospital RoadP. O. Box 3066 - 40200KISII

KISUMU Tuffoam Mall1st FloorJomo Kenyatta HighwayP.O. Box 1062 - 40100KISUMU

NAIVASHA CfC Heritage HouseMoi RoadP.O. Box 1319 - 20117NAIVASHA

NAIROBI Liberty HouseP.O. Box 30390 - 00100NAIROBI

NANYUKI Silver PlazaP.O. Box 1615 - 10400NANYUKI

NAKURU Polo CentreP.O. Box 4362 - 20100NAKURU

MERU NakumattMwitu Centre BuildingP.O. Box 1911 - 60200MERU

THIKA Zuri CentreKenyatta HighwayP.O. 7048 - 001000THIKA

KITENGELA Capital CentreP.O. Box 30390 - 00100NAIROBI

NAIROBI (CITY CENTRE) Lonrho HouseMezzanine 2, Standard StreetP.O. Box 30390 - 00100NAIROBI

EMBUNjue Plaza3rd Floor, Embu - Meru RoadP. O. Box 2607 - 60100EMBU

The Heritage Insurance Company (T) Limited4th Floor Masaki IkonBains Avenue- Msasani Peninsula PO Box 7390, Dar es Salaam, Tanzania.

BRANCHES

SUBSIDIARYTh

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

170

5

OUR VISIONWe will be the market leading wealth management company in Africa while entering growth markets which allow us to use our points of difference to make a meaningful contribution to the group.

We are a customer-focused organisation with a united, passionate and skilled workforce.

We have the foresight to respond to changing consumer needs through innovative solutions and technologically efficient processes.

OUR VALUES

• Be passionate about our work and utilise our talents to add value

• Take initiative and responsibility

• Respect and appreciate constructive criticism and the opinion of others

• Focus on set goals and deadlines

• Be proud ambassadors of our Company and Group

• Put our customers at the centre of our thinking and serve them with diligence

• Encourage teamwork, respect and trust for one another

• Take ownership of the consequences of our actions

• Perform our duties with care, integrity and honesty

• Deliver beyond expectations

• Constantly improve our skills and knowledge

• Embrace change and seek ways to do things better

06

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

MEDICAL INSURANCE

because the greatest gift is a healthy you

MARINE INSURANCE

because your businessmatters to you

The directors submit their report together with the audited financial statements for the year ended 31 December 2017 which disclose the state of affairs of The Heritage Insurance Company Kenya Limited and its subsidiary, Heritage Insurance Company Tanzania Limited (together the ‘Group’).

1. PRINCIPAL ACTIVITIESThe Group underwrites all classes of non life insurance risks as defined by the Insurance Act except Micro Insurance.

2. COMPANY RESULTS AND DIVIDEND

Profit after tax for the year ended 31 December 2017 of Shs 459 million (2016: Shs 524 million) has been added to retained earnings.During the year, the directors paid nil (2016: 60 million) as interim dividend. The directors do not propose payment of a final dividend (2016: nil).

3. DIRECTORS

The directors who held office during the year to the date of this report are as shown on page 2.

4. RELEVANT AUDIT INFORMATION

The Directors in office at the date of this report confirm that:

• There is no relevant information of which the company’s auditor is unaware; and

• Each director has taken all the steps that they ought to have taken as a Director so as to be aware of any relevant audit information and to establish that the Company’s auditor is aware of that information.

5. EMPLOYEES

The number of persons employed by the Company at the end of the year was 179 (2016: 174). Out of the 179 members of staff employed by Heritage Kenya as at 31 December 2017, 105 are male and 74 are female.

6. AUDITORS

The auditors, KPMG Kenya, continue in office in accordance with section 719 of the Kenyan Companies Act, 2015 and subject to the approval by the Commissioner of Insurance under Section 56(4) of the Insurance Act.

7. BUSINESS OVERVIEW

The group delivered solid results in the backdrop of a difficult trading environment. The Group’s heritage is built around a philosophy of quality business rather than top line growth. This has helped the Group weather a particularly difficult year. In Kenya, the Gross Written Premium grew by 11 percent though there was a disproportionate growth in reinsurance costs due to changes in business mix.

There was also an increase in bad debts provisioning reflective of a difficult trading environment where some of our customers were unable to pay premiums on time due to credit glut.

This had a negative effect on Kenya’s core underwriting results though expenses of management remained well under controlin the year. The Heritage Insurance Company Kenya Limited sold a non-strategic company Azali Limited, a special purpose vehicle created to manage Heritage House in Naivasha. The disposal contributed a net loss of KShs 10 million to Heritage Group earnings.

Tanzania business underwent multiple and fundamental regulatory changes in the year. The changes were mainly targeted at distribution and premium payment. This resulted in business slow down and as a result,

DIRECTORS’ REPORT

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

09

DIRECTOR’S REPORT (CONT’D)BUSINESS OVERVIEW (CONT’D)

the Gross Written premium was down on the prior year by 14%. On the flipside, the claims cost and management expenses both reduced to compensate for lower premium earnings.

In keeping with the Group’s strong Corporate Governance and risk management practices, all entities within the Group recorded improved solvency in the reporting period.

Key financial indicators of Group and Company are shown below:

THE GROUP THE COMPANY

Gross Written Premiums: up 9% up 11%

Investment Income: up 22% up 17%

Net assets: up 11% up 23%

Benefit payments: up 5% up 11%

Operating expenses up 6% flat

Profit for the year down 12% up 16%

(Loss)/ Gain on disposal of subsidiary (10m) 50m

8. APPROVAL OF FINANCIAL STATEMENTS

The financial statements set out on pages 39 to 103 were approved and authorized for issue at a meeting of Directors on 28 March 2018

By Order of the Board

Company Secretary28 March 2018

10Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

PROFESSIONAL INDEMNITY

because your careerbrings value to your life

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

11

CHAIRMAN’S STATEMENT DEAR SHAREHOLDERS

I am indeed very pleased to present the Heritage Insurance Company Kenya Limited Annual Report and Financial Statements for the year ended 31 December 2017.

I am particularly grateful to you, shareholders, for the level of support you continue to provide for your company as is evident from your active participation every year.

These occasions offer us a great opportunity to review

our financial performance and at the same time plan strategically ahead together.

On our part as the Board, together with the management and staff, we are always encouraged by the confidence bestowed upon us to steer the affairs of your company and remain committed to the realization of its full potential for growth in order to continue to deliver better returns.

Income Statement HIK HIT Azali Total Cons Adj. Group

2017Profit before taxation 770,982 77,449 2,912 851,343 (172,344) 679,001

Taxation (193,892) (25,493) (874) (220,259) - (220,259)

Total earnings 577,090 51,956 2,038 631,084 (172,344) 458,743

Change in earnings +16% (51%) 0% +4% (111%) (12%)

2016

Profit before taxation 705,079 155,941 2,934 863,954 (81,617) 782,337

Taxation (206,885) (50,306) (897) (258,089) - (258,089)

Total earnings 498,194 105,635 2,037 605,866 (81,617) 524,249

*Azali Limited was sold on 31 August 2017

GLOBAL BUSINESS OUTLOOK

The World Bank forecasts global economic growth to edge up to 3.1 percent in 2018 after a much stronger than expected 2017, as the recovery in investment, manufacturing, and trade continues.

Growth in advanced economies is expected to moderate slightly to 2.2 percent this year, as central banks gradually remove their post-crisis accommodation and the upturn in investment growth stabilizes.

Growth in emerging market and developing economies as a whole is projected to strengthen to 4.5 percent, as activity in commodity exporters continues to recover amid firming prices.

In oil-exporting economies, the 2014 - 16 oil price collapse has already prompted some reforms. Nevertheless, across all emerging market and developing economies (EMDEs), room for policy improvements remains. Policy initiatives to lift physical and human capital, encourage labour force participation, and improve institutions could help raise potential growth and reduce inequality.

12Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

“The Company’s overall financial performance in 2017 showed resilience in the midst of events outside our direct control”.

P N Gethi

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

13

CHAIRMAN’S STATEMENT (CONT’D)MACRO ECONOMIC ENVIRONMENT

World Bank 2018 report projects Kenya’s economic growth to rebound to 5.8 percent in 2018. The same report indicates the Gross Domestic Product (GDP) growth decelerated to 5.5 percent in 2017 because of drought, weak credit growth, security concerns, and a rise in oil prices.

Medium term GDP growth should rebound to 5.8 percent in 2018 and 6.1 percent in 2019 respectively, depending on the completion of ongoing infrastructure projects, the resolution of slow credit growth, and the strengthening of the global economy and tourism.

In the long term, the adoption of prudent macroeconomic policies will help safeguard Kenya’s robust economic performance, according to the World Bank. This includes the implementation of fiscal and monetary prudence and lowering the deficit down to 4.3 percent by financial year 2019/2020, as per the Medium Term Fiscal Framework. Fiscal consolidation needs to avoid compromising public investment in critical infrastructure key to unlocking the economy’s productive capacity.

On social development, Kenya met some Millennium Development Goals (MDGs) targets, including reduced child mortality, near universal primary school enrolment, and narrowed gender gaps in education. Interventions and increased spending on health and education are paying dividends. And, while the healthcare system has faced challenges, devolved health care and free maternal health care at all public health facilities will improve health care outcomes and develop a more equitable health care system.

Kenya’s youthful and growing population, dynamic private sector, highly skilled workforce, improved infrastructure, new constitution, and pivotal role in East Africa, give it the potential to be one of Africa’s great success stories. Addressing poverty, inequality, governance, and the skills gap (between market requirements and the education curriculum) will be major goals, as well as problems of climate change, low investment, and low productivity.

INSURANCE SECTOR OUTLOOK

Kenya represents one of Africa’s most well developed and best regulated insurance markets, with formidable historic growth and even better near term prospects. There are increasing regulatory capital requirements on the horizon, and there is growing scope for consolidation.

The 2018 Insurance Industry Outlook pinpoints key opportunities for growth. Foreign and local capital is likely to continue to flow into the sector, lured not only by the great domestic potential access to financial services is still modest but also by the chance to expand into the sizeable regional market. Currently, according to the Association of Kenyan

Insurers (AKI), Kenya represents 70 percent of the East African insurance market, which also includes Tanzania, Uganda, Rwanda and Burundi.

In recent years, insurance penetration and accessibility have been improving steadily. A number of major infrastructure plans have created investment opportunities in insurance. Some of the main ventures include the construction of the second runway and new terminal at Jomo KenyattaInternational Airport, the Lamu Transport Corridor project and the Standard Gauge Railway (SGR) project.The insurance penetration is about 2.9 percent of the Gross Domestic Product (GDP).

The worldwide insurance penetration is estimated at 6.5 percent of GDP. (Source IRA 2017 report)

As technology, innovation, higher customer expectations and disruptive newcomers redefine the marketplace, we remain focused on growing top line sales, bottom line profitability, addressing challenges, and competing responsibly in a dynamic industry.

INNOVATION AND TECHNOLOGYIn line with enhancing efficiency in various spheres of business operations, adoption of emerging technology trends has been a key area of focus for the company. The business has been aggressive in automating core areas of business including bank payment through a host to host system that has not only quickened payments but also reduced from a two-stage process to a one stage process.

In addition, we made it easier for customers to pay premiums by offering multiple online payment options. Customers can now pay premiums from the comfort of their homes or offices via m pesa or credit cards (Visa) by simply going to our website and selecting E Pay. Payment reference will be required for instantaneous receipting and allocating to a customer account.

The company also connected to the government’s Integrated Population Registration System (IPRS) which is registration bureau of identity cards.

This has enhanced speed of processing new business with an authenticated and accurate system. Cyber Security has been a key area of focus for the company. In the year, the business subscribed to Mimecast with a view to scan emails, thereby eliminating fraud and spam emails and filtering any viruses. The company also moved its email servers to the cloud thereby ensuring that all staff are able to access and provide timely service from any location with an internet connection.

On new product development, we introduced the Trade Credit policy that seeks to cover businesses that supply goods on credit against loss of revenue from buyers who do not honour their payment obligation.

14Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

CHAIRMAN’S STATEMENT (CONT’D)INNOVATION AND TECHNOLOGY (CONT’D)

Going forward, the company plans to introduce a groundbreaking motor insurance policy that will revolutionize motor insurance in Kenya. Through this product, clients will now pay their premiums based on how they drive.

CORPORATE SOCIAL INVESTMENTSIn 2017, the company drove a robust Corporate Social Responsibility (CSI) programme anchored on two main pillars of Education and Health as part of the wider Liberty Group CSI

Policy. On education, the company enrolled 10 new secondary school students in form one from across the country to bring to a total of 52 students under the Heritage Scholarship Programme that sponsors tuition fee for students in secondary and tertiary institutions. Other education programmes undertaken over the period include celebration of the 2017 Nelson Mandela Day with students from Kajiado Township Primary School. In marking this occasion, the company through its staff donated funds towards a school feeding programme that saw all the students get lunch through a Heritage staff initiative dubbed Stairwell Challenge which saw each participating staff raise money towards the programme.Additionally, the company made donations towards education of needy students during the 2017 Starehe Founders Day Celebration in Nairobi. On health, the company ran a vigorous

Healthy Living Campaign that aimed at sensitizing company staff on benefits of living a healthy lifestyle. Indeed, it was through this initiative that staff raised funds towards the Kajiado Township Primary School feeding programme. Other initiatives included support to the Cerebral Palsy Society of Kenya and participation in the Association of Kenya Insurers Medical Camp in Githunguri, Kiambu County.

REGULATORY ENVIRONMENT IN KENYA The Insurance Act has undergone various revisions in the year 2017 to keep abreast with the changing environment.

The changes were majorly on harmonizing the risk-based capital provisions within the Act and creation of perpetual licenses for insurance companies.

The Insurance Regulatory Authority (IRA) also issued the following guidelines to assist in the risk-based supervision: • The Insurance (Valuation of Technical Provisions for General Business) Guidelines 2017.

• The Insurance (Investments Management) Guidelines, 2017 • The Insurance (Capital Adequacy) Guidelines, 2017

REGULATORY ENVIRONMENT

The Insurance (Amendment) Act 2016 took effect on 13 January 2017 and the Act was amended to operationalize risk-based solvency requirements that were introduced in the Finance Act, 2013.

THE STATUTE LAW (MISCELLANEOUS AMENDMENTS)

ACT, 2017

The Insurance Act was amended by changing the date when the insurance companies were expected to fully comply with the Risk-Based Capital Requirement. The date has been moved

from 30 June 2018 to 30 June 2020.

THE INSURANCE (AMENDMENT) ACT 2017 AND THE INSURANCE (AMENDMENT) REGULATIONS 2017

The Insurance Act was amended to create perpetual licenses for Insurance companies and did away with the annual application for insurance licenses.

“The company has a long-term education financial aid program where students from poor backgrounds across the counties are considered for sponsorship. The company walks with the student the entire journey from Form 1 admission until they graduate from the university and eventual job placement.”P. N. Gethi

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

15

CHAIRMAN’S STATEMENT (CONT’D)

REGIONAL MARKET There were Regulatory Changes in Tanzania as outlined below:

A) THE MISCELLANEOUS AMENDMENTS ACT (NO. 2) OF 2017

In June 2017, the Tanzanian Parliament passed the Written Laws (Miscellaneous Amendments Act (No. 2) of 2017, which amended the Insurance Act, with respect to foreign ownership of insurance brokers, the mechanics of payment (and minimums) for insurance premiums and the requirement to obtain insurance only through Tanzanian insurers.

OWNERSHIP AND PAYMENT OF BROKERS

The changes require insurance brokers to be at least two thirds (over 66 percent) owned and controlled by Tanzanian citizens. This is a 100 percent increase from the previous local participation requirement (of one third (above 33 percent).

Further, customers will have to pay insurers all premiums directly, even when they are using brokers. Brokers will only be entitled to receive their commissions directly from the insurers (instead of taking them out of premiums from customers) and there are heavy penalties for contravening this.

MINIMUM INSURANCE PREMIUMS

The amendments enable the Commissioner of Insurance to set minimum rates of premiums payable for different classes of insurance by, publishing orders in the Government Gazette.

REQUIREMENT TO OBTAIN INSURANCE ONLY THROUGH TANZANIAN INSURERS

Insurance cover for a Tanzanian resident person or company may only be placed with a Tanzanian registered insurer. The exception to this, where classes of insurance are not available from a Tanzanian registered insurer, is now even further curtailed. The changes make it clear that all ground transport insurance, marine insurance and air cargo insurance covers for Tanzanian imports must be effected by a Tanzanian insurer.

B) CIRCULAR LETTER NO.055/2017 (CONDITIONS FOR DEALING WITH FOREIGN REINSURERS AND REINSURANCE BROKERS)

The circular issued by Commissioner of Insurance specifically seeks to address market challenges resulting

from externalisation (fronting) of insurance business outside the country through reinsurance. It particularly prohibits the externalization of risks at 100 percent, externalisation of long term insurance business in the country and also prohibits co-insurance with sister or parent companies based in other jurisdictions.

The circular also requires insurers to diversify the reinsurers used and ensure the reinsurers have a rating of B+ or better from independent reputable rating agency. Further, the insurance companies are required to retain competent reinsurance staff.

The circular came into effect on 1 January 2018.

All the above regulatory changes have a direct impact in the company and the Group conducts business.

BUSINESS PERFORMANCE IN TANZANIA

Tanzania has sustained relatively high economic growth over the last decade, averaging 6 percent to 7 percent a year.

The growth in the insurance market has been aligned to the reported growth in Gross Domestic Product. In 2018, the general insurance market is expected to grow in double digits based on the historical trend.

During the year under review, the following legislations came into effect:

• Cash before cover – This requires clients to pay their premiums directly to the insurers

• Accreditation of foreign Reinsurance. – This call for foreign reinsurers seeking to transact business in Tanzania to have an accreditation letter from Tanzania Insurance Regulatory Authority.

These changes aim to ensure that a sound business environment is realized.

In terms of financial performance, Heritage Insurance Company Tanzania Limited gross written premium decreased by 26 percent over the previous year primarily due to regulatory changes, loss of large corporate clients and other market conditions. The net earned premium decreased by 19 percent over 2016. During the year, the Company had a reasonable claims experience and recorded an overall net claims ratio of 47 percent (net claims over net earned premium) in line with the

16Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

budget and previous year loss. Operating expenses remained marginally higher at 17 percent compared to the international benchmark of 10 percent of gross written premium.

The Company continues to focus on prudently reducing the cost base and on improving the operational cost ratios. Interest & dividend incomes at Tshs 2,089 million were 6 percent higher than the previous year due mainly to an increase in bank deposits from Tshs 19,680 million to Tshs 24,234 million.

Fair value gain on investment was Tshs 293 million compared to a loss of Tshs 587 million in 2016.

Unrealized exchange loss of TZS 22 Million and realized exchange gains of TZS 417 million has also been recorded as at the end of December 2017.

The underwriting profit decreased by 51 percent to TShs 696.8 million in 2017 from TShs 1,409 million in 2016. The profit before tax at TShs 1,677 million is 23 percent lower compared with profit before tax of TShs 4,331 million in 2016.

Besides the drop in business at the top line, the bottom line results were significantly affected by a one-off bad debt provision of a disputed claim recovery worth Tshs 1,189 million. During the year the company paid an interim dividend of Tshs 4 billion. With total Assets of Tshs 56.6 billion and a strong relationship with reputable Reinsurers, the Company remains both strong and dynamic.

The Heritage Insurance Company Tanzania strives to ensure success for the benefits of all our stakeholders by providing efficient service to its loyal clients and enhancing shareholders value.

The Company will continue to focus on its core market segment of large corporate clients alongside while making concerted efforts to develop and strengthen business relationships with Tier II, Tier III brokers and retail channel partners to broaden its client base.

The positive impact of various Government projects and the focus on industrialization will have a positive impact for the Company.

The Company is expecting to derive substantive growth from Aviation, Engineering, Marine business segments and other retail business especially motor segment.

The success of our business derives from our stakeholders: Employees, Clients, Brokers, Agents, Reinsures, Business partners, Regulators and Shareholders.

COMPANY OF CHOICE

Heritage Insurance Company Kenya Limited is an equal opportunity employer. The company provides equal employment opportunities to all employees or job applicants and does not discriminate in any way because of gender, race, colour, religion, national origin, sex, physical or mental disability, or age.

The company encourages staff development by offering both Professional and Internal training opportunities.Our objectives in appointment are to recruit the person who is most suited to the particular job based on his relevant abilities, qualifications, experience and skills for the post. Recruitment and selection decisions will always be made on the basis of merit making our company the most attractive place to work.

Heritage Insurance Company Limited is committed to ensuring the best possible environment for the employees. Safeguarding and promoting their welfare is our highest priority.

We aim to recruit staff that share and understand our commitment, and to ensure that no job applicant is treated unfairly by reason of a protected characteristic as defined under the Employment Act.

DEALING WITH FRAUD

Fraud is one of the biggest challenges facing the insurance industry. The industry estimates generally put fraud at about 10 percent of the property or casualty insurance industry’s incurred losses and loss adjustment expenses each year, although the figure can fluctuate based on the line of business, economic conditions and other factors.

Fraudulent claims are particularly prevalent in motor and medical claims. It is difficult to tell the exact magnitude of the menace.

The industry lobby body, the Association of Kenya Insurers (AKI) is developing a data sharing platform that should help industry players share information freely to assist stakeholders to understand customer trends.

CHAIRMAN’S STATEMENT (CONT’D)BUSINESS PERFORMANCE IN TANZANIA (CONT’D)

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

17

PRODUCTS AND CHANNELS Heritage Insurance Company Kenya Limited provides short term insurance products and prides on its superb history of prompt claims payment.

This has earned us major awards for Outstanding Insurance Underwriter in Claims Settlement as nominated by members of the Association of Insurance Brokers of Kenya.

We are also rated AA by Global Rating Company (GRC), for amongst other reasons, our high claims paying ability. This is one of the highest international ratings ever given to recognize a Kenyan insurer!

As Heritage Insurance Company, we are developing systems and processes to meet the modern demands of the ever enlightened customers.

This, therefore, means investing in the expansion of our distribution channels and networks making it easier for our customers to have access to services at their own convenience.

As a result, we have gained cumulative experience in understanding our customers’ needs and preferences and have been largely successful in providing innovative solutions that meet their needs.

APPRECIATION

I would like to take this opportunity to sincerely thank the Board of Directors for their unrelenting support and guidance throughout the year.

Similarly, to our valued business partners, brokers, agents and clients who have remained with us even in the most turbulent of times, we thank you and reiterate our unbreakable promise to service. As I conclude, I wish to thank the management and staff for your dedication and commitment to serve our clients. Together, we will maintain our Brand as the trusted leader in insurance in the East African region.

Peter Gethi,ChairmanDate: 28 March 2018

CHAIRMAN’S STATEMENT (CONT’D)

18Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

TRADE CREDIT INSURANCE

because some risksare worth taking

GROSS WRITTEN PREMIUMS

GROSSPREMIUMS

(Kshs.)

TOTAL ASSETS UNDERWRITING RESULTS

GROUP

COMPANY

Kenya

5.9 B

Tanzania

1.7 B

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.02013 2014 2015 2016 2017

6.0 6.

24.

0

5.2 5.

3

5.9

3.5

7.5 7.

6

7.6

1 0

2 0

30

40

50

60

70

80 5 .

00

10

8.0

6.0

4.0

2.0

1.0

0.02013 2014 2015 2016 2017

9.9

9.1

6.1 6.

6 7.2

8.9

4.7

9.8 10

.2

11.3

1 0

2 0

40

60 7

80 2

10 .

.

00

0.6

0.5

0.4

0.3

0.2

0.1

0.02013 2014 2015 2016 2017

0.33

0.25

0.20 0.

22

0.40

0.26

0.31

0.28

0.48

0.30

0

01

0 2

0

0 3 5 2

04

4

0 5 0

06

00

Heritage Insurance Company Kenya Limited is among the top 10 short term insurance underwriters in the industry by premium volumes. The Company has put in place some rigorous underwriting guidelines to ensure that we have continuously returned underwriting results from the operations of the Company over the years. In addition, the Company continuously evaluates its processes and procedures to ensure the operations are done in the most efficient manner, to serve the clients in the most satisfactory manner. Today we are among the best in service delivery.

FIN

AN

CIA

LH

IGH

TLIG

HTS

20Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

GROSS WRITTEN PREMIUMS

GROSSPREMIUMS

(Kshs.)

TOTAL ASSETS UNDERWRITING RESULTS

GROUP

COMPANY

Kenya

5.9 B

Tanzania

1.7 B

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.02013 2014 2015 2016 2017

6.0 6.

24.

0

5.2 5.

3

5.9

3.5

7.5 7.

6

7.6

1 0

2 0

30

40

50

60

70

80 5 .

00

10

8.0

6.0

4.0

2.0

1.0

0.02013 2014 2015 2016 2017

9.9

9.1

6.1 6.

6 7.2

8.9

4.7

9.8 10

.2

11.3

1 0

2 0

40

60 7

80 2

10 .

.

00

0.6

0.5

0.4

0.3

0.2

0.1

0.02013 2014 2015 2016 2017

0.33

0.25

0.20 0.

22

0.40

0.26

0.31

0.28

0.48

0.30

0

01

0 2

0

0 3 5 2

04

4

0 5 0

06

00

Heritage Insurance is an equal opportunity employer. The Company strives to attract and retain a highly skilled and competent staff who in turn serves our clients in the most professional way. Out of the 179 members of staff employed by Heritage Kenya as at 31 December 2017, 105 are male and 74 are female.

1

3

2

BOARD OF DIRECTORS

4

22Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

7

26

1 Peter GethiChairman 4 Gayling May

Director

7 Stuart WenmanDirector

2 Godfrey KioiManaging Director 5 Mike Du Toit

Director

3 Rachel Mbai Director (Appointed 30 Aug. 2017) 6 Catherine Mitchem

Director (Appointed 17 Nov. 2017)

4

5

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

23

MANAGEMENTTEAM

1 2 3

6

1 G. Kioi

Managing Director

4 S. Chege

Head of Retail Business

2 B. N. Hiuhu (Mrs.)

Director (Underwriting & Claims)

3 A. P. Ngunjiri

Director (Medical)

4 5

7

9

8

10

7 L. Magambo

General Manager (Finance)

10 I.Kamau

Senior Manager (ICT)

8 B. Irungu

Senior Manager (Claims)

5 J. Maluki (Ms.)

Senior Manager (Medical) 9 B. Maina

Senior Manager (Underwriting)

6 D. Mathenge

Senior Manager (Finance)

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

25

AGRICULTURAL INSURANCE

because growth and progress drive everything

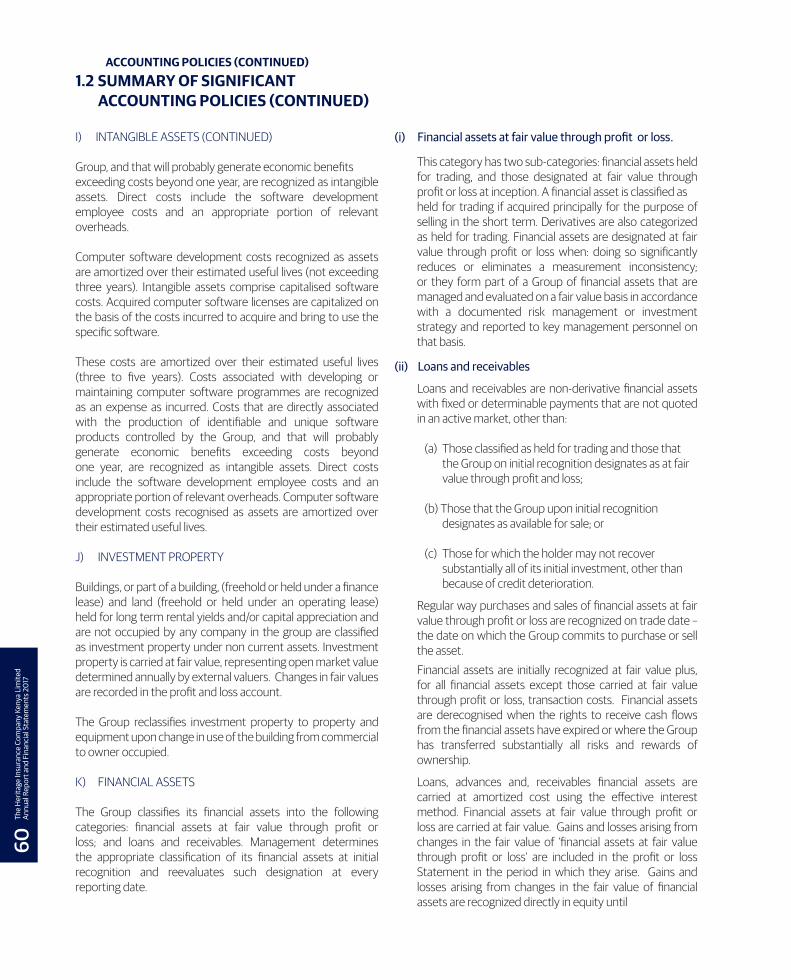

1. INTRODUCTION

The Heritage Insurance Company Kenya Limited Corporate Governance Framework comprises the Board of Directors, Committees of the Board, Management and Operations Committees, as well as policies, procedures and systems which together govern the management of the business. The company continuously embraces the principles of good corporate governance to ensure that its business remains sustainable, relevant and profitable. The Board of Directors and Management have embraced the principles of integrity, accountability and transparency in directing and running the affairs of the company.

The Corporate Governance Framework also guides the relationship between Heritage Insurance Company Kenya Limited its parent shareholder, Liberty Kenya Holdings Ltd, as well as its relations with other member companies of the Liberty Africa Group.

2. BOARD OF DIRECTORS

The Mandate of the Heritage Insurance Company Board of Directors is to implement principles of good corporate governance, determine the strategic direction of the company and ensure sustainability of the business. The Board of Directors is therefore responsible for implementing the Strategic Plan through oversight, enhanced shareholder value, company growth, profitability, financial reporting, accountability and safeguarding of company assets.In order to achieve this efficiently, the Board has delegated various responsibilities to various committees of the Board and Management Committees, while the mandate to oversee the running of the business has been conferred to the Managing Director. There are three committees of the board, namely: The Directors Affairs Committee, Audit and Risk Committee and the Investment Committee.

The Board of Directors is constituted of six non-executive directors and the Managing Director and holds meetings at least once every quarter.

In 2017, the Board of Directors held meetings as follows:

Member 02.03.2017 25.05.2017 30.08.2017 17.11.2017 11.12.2017

Peter N Gethi P P P P P

Godfrey Kioi P P P P P

Gayling R May P P P P P

Stuart Wenman P P P P P

Mike du Toit P P P P P

Claire W Mwangi * 1 P P P N/A N/A

Sonal Sejpal * 2 P A P P N/A

Rachel Mbai * 3

Catherine Mitchem * 4

-

-

--

P-

P

-

P

P

*1 Resigned on 14 June 2017 *2 Resigned on 20 November 2017

*3 Joined the Board on 30 August 2017 *4 Joined the Board on 17 November 2017P - Present A - Absent with apologies N/A - Resigned

CORPORATEGOVERNANCE REPORT

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

27

CORPORATE GOVERNANCE REPORT (CONT’D)

3. THE DIRECTORS’ AFFAIRS COMMITTEE

This Committee is established by the directors of Liberty Kenya Holdings Limited. The mandate of this committee is to supervise the management of key human resources of all its subsidiaries. This includes the appointment and management of executives and review of remuneration policies.

4. THE AUDIT AND RISK COMMITTEE (ARC)

The mandate of this committee is to oversee the implementation of effective policies, procedures and internal controls.

The ARC also sets and reviews the company’s risk management strategy, while enforcing compliance with internal and regulatory provisions.

This committee also reviews the scope of work, skills of the Internal Audit function and provides guidance in the resolution of audit findings. The ARC reinforces best practice in Corporate Governance through the implementation of its mandate.

The Audit and Risk committee is charged with approving the company’s financial statements, and acts as the liaison with the External Auditors. In this regard, the ARC provides oversight and assurance for financial reporting.

The Audit and Risk Committee is constituted of four non-executive directors, and holds meetings every quarter:

In the year 2017, the Audit and Risk Committee held meetings as follows:

Director 28.02.2017

23.05.2017

28.08.2017

14.11.2017

G R May P P P P

M L du Toit P P P P

S Sejpal A P P N/A

S C Wenman P P P P

P - Present A - Absent with apologies N/A - Resigned

5. THE INVESTMENT COMMITTEE

The objective of the Investment Committee is to oversee the design of the company’s investment strategy and to monitor its implementation. The committee monitors performance of the company’s investment portfolio, as administered by professional asset managers in accordance with the Board Investment Strategy, and reviews compliance of the investment

managers with benchmarks and performance standards.The committee is constituted of three non-executive directors, the Managing Director and representatives from the Finance Department and holds quarterly meetings.

In year 2017, the Investment Committee held meetings as follows:

Director 01.02.2017

24.05.2017

29.08.2017

15.11.2017

M.L . du Toit P P P P

S.C. Wenman P P P P

C.W. Mwangi * A A N/A N/A

G.M. Kioi P P P P

P - Present A - Absent with apologies N/A - Resigned

6. MANAGEMENT AND OPERATIONS COMMITTEES

Three Management and Operations Committees have been constituted to facilitate effective implementation of the Strategic Plan and efficient Company operations. They include:

6.1 THE EXECUTIVE COMMITTEE (EXCO)

The mandate of ExCo is to oversee strategic and operational matters of the company, as well as all its relations with the Liberty Group. The objective of this committee is to enhance coordination and communication across the business units, and carry out review of company performance and implementation of the Strategic Plan. This committee meets weekly, and also holds monthly Mission Status Review (MSR) forums to monitor implementation of the Strategic Plan.

The members of ExCo are;

• Managing Director• Director – Medical• Director – Operations• General Manager – Finance and Administration• General Manager – Risk and Compliance• Senior Manager – ICT• Senior Manager – Human Resources• Head of Retail Business• Head of Corporate Business

28Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

CORPORATE GOVERNANCE REPORT (CONT’D)6. MANAGEMENT AND OPERATIONS COMMITTEES(CONT’D)

6.2 THE CREDIT MANAGEMENT COMMITTEE

The mandate of the Credit Management committee is to ensure full implementation of the Credit Policy, as well as providing policy guidance and oversight in credit management.

It is chaired by the General Manager-Finance and Administration, and is constituted by members whose functions have the greatest impact in debt management and credit control. Its core responsibilities are:

• To ensure compliance with the credit management policy;• To ensure that all money owed to the company is

promptly collected in accordance with credit terms;• To take appropriate measures in dealing with defaulters;

and• To recommend to the Board, through the Managing

Director and Audit and Risk Committee, provision for doubtful debts and write off of uncollectible debts.

L. Magambo ChairmanL. Wachira SecretaryG.M. Kioi Member B.N.G. Hiuhu Member F. Muikamba Member A.P. Ngunjiri Member A. Njiru Member S. Chege Member S. Githinji Member

6.3 THE HUMAN RESOURCES COMMITTEE

The objectives of this committee are as follows:

• To develop policies on terms and conditions of service, performance management and staff remuneration in line with best market practice

• To ensure compliance with legislation regarding human capital management

• To develop and review the code of ethics and evaluate cases of unethical behavior

The members of this committee are the Managing Director, General Manager – Finance and Administration, Director – Medical, and the Senior Manager – Human Resources.

The committee meets bi-monthly or as deemed necessary.

7. THE OPERATIONS COMMITTEE

The company has implemented an enterprise risk management framework and upholds internal controls designed to enhance compliance, integrity and reliability of financial data.This framework is also supported by policies, procedures and segregation of duty, which ensure accountability and safeguarding of company assets.

The effectiveness of the risk management and internal control environment is monitored regularly through the internal audit function and annual review by external auditors.

As part of risk governance, internal control and compliance oversight, the company has established an Operating Company (OpCo) Committee.

The objective of this committee is to monitor key risk indicators and to set the tone in management of operational, market, insurance and compliance risks. This committee holds monthly meetings.

The members of the OpCo are:

G.M Kioi ChairmanM. Kivuitu MemberB.N.G. Hiuhu MemberA. Ngunjiri MemberL. Magambo MemberJ. Kinoti MemberI. Kaviti Member

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

29

CORPORATESOCIALINVESTMENT

1.

2.

3.

4.

STUDENT SPONSORSHIP PROGRAMME - 7

Members of the Heritage Corporate Social Investment committee with one of the student under the sponsorship programme when they paid her a visit at Kyeni Girls High School in Embu County. Currently, the programme has enrolled over 50 students from across the country in secondary and university institutions.

DIABETES AWARENESS - 3

Members of staff take part in a diabetes awareness campaign walk organised by the Kenya Diabetes Management Information Centre. The company donated Ksh.100,000

HEALTHY DIET - 1

Heritage Managing Director Mr. Godfrey Kioi (centre) leads members of staff in launching an internal staff campaign on healthy living during “HAPPY DAY”

MARKING NELSON MANDELA DAY - 6

Heritage Insurance and Liberty Life Kenya CSI patrons Albert Ngunjiri and Kivuitu Musili present a sponsorship cheque to teachers and students of Kajiado Township Primary School in marking the 2017 Nelson Mandela Day. The funds will go towards the school feeding programme for all the students in the school.

30Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

5.

6.

7.

MEDICAL CAMP - 4

The company in partnership with the Association of Kenya Insurers (AKI) organised a public medical camp in Gatanga Kiambu County targeting members of the public as part of Heritage CSI initiative.

STAIRWELL CHALLENGE - 5

Members of staff from Heritage Insurance, Liberty Life and Stanlib sign commemorative t-shirts after successfully taking part in a stairwell challenge at Liberty House. The initiative involved staff taking stairs from ground floor to the rooftop with each trip raising funds towards school feeding programme while promoting healthy living.

WALKING FOR A CAUSE -2

A group of staff from Heritage express their delight after successfully finishing a 20 km walk in support of the Celebral Palsy Society of Kenya.Heritage actively supports the society’s campaigns to create awareness and advocacy for the rights of persons afflicted by celebral palsy in Kenya.

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

31

STATEMENT OF DIRECTORS’ RESPONSIBILITIESThe Directors are responsible for the preparation and presentation of the consolidated and separate financial statements of The Heritage Insurance Company Kenya Limited set out on pages 39 to 103 which comprise the Group and Company statements of financial position as at 31 December 2017, the statements of profit or loss, statements of other comprehensive income, statements of changes in equity and statements of cash flows for the Group and Company for the year then ended, and the notes to the financial statements which include a summary of significant accounting policies and other explanatory information.

The Directors responsibilities include: determining that the basis of accounting described in Accounting policy 1.2 is an acceptable basis for preparing and presenting the financial statements in the circumstances, preparation and presentation of financial statements in accordance with International Financial Reporting Standards and in the manner required by the Kenyan Companies Act, 2015 and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatements, whether due to fraud or error.

Under the Kenyan Companies Act, 2015, the Directors are required to prepare financial statements for each financial year that give a true and fair view of the financial position of the Group and Company as at the end of the financial year and of the profit or loss of the Group and company for that year. It also requires the Directors to ensure the company keeps proper accounting records that disclose with reasonable accuracy the financial position of the Group and the company.

The Directors accept responsibility for the annual financial statements, which have been prepared using appropriate accounting policies supported by reasonable and prudent judgements and estimates, in conformity with International Financial Reporting Standards and in the manner required by the Kenyan Companies Act, 2015. The Directors are of the opinion that the financial statements give a true and fair view of the financial position of the Group’s and Company’s profit or loss.

The Directors further accept responsibility for the maintenance of accounting records that may be relied upon in the preparation of financial statements, as well as adequate systems of internal financial control.The Directors have made an assessment of the Group and the Company’s ability to continue as a going concern and have no reason to believe the Group and the Company will not be a going concern for at least the next twelve months from the date of this statement.

APPROVAL OF THE FINANCIAL STATEMENTSThe financial statements, as indicated above, were approved and authorized for issue by the Board of Directors on 28 March 2018.

P.N. Gethi G.M. KioiDate: 28 March 2018

32Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

MOTOR INSURANCE

because we believeyou deserve peace of mind

INDEPENDENT AUDITORS’ REPORT TO THE SHAREHOLDERSREPORT ON THE AUDIT OF THE CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS

OPINION

We have audited the consolidated and separate financial statements of The Heritage Insurance Company Kenya Limited (the Group and Company ) set out on pages 39 to 103 which comprise the Group and Company statements of financial position as at 31 December 2017, Group and Company statements of profit or loss, Group and Company statements of other comprehensive income, Group and Company statements of changes in equity and Group and Company statements of cash flows for the year then ended, and notes to the consolidated and separate financial statements, including a summary of significant accounting policies and other explanatory information.

In our opinion, the accompanying consolidated and separate financial statements give a true and fair view of the consolidated and separate financial position of The Heritage Insurance Company Kenya Limited as at 31 December 2017, and of the consolidated and separate financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards and in the manner required by Kenyan Companies Act, 2015.

BASIS FOR OPINION

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the consolidated and separate Financial Statements section of our report. We are independent of the Group and Company in accordance with the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants (IESBA Code) together with the ethical requirements that are relevant to our audit of the financial statements in Kenya and we have fulfilled our other ethical responsibilities in accordance with these requirements and the IESBA Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

KEY AUDIT MATTERS

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated and separate financial statements of the current period. These matters were addressed in the context of our audit of the consolidated and separate financial statements as a whole, and in forming our opinion, and we do not provide a separate opinion on these matters.34

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS (CONT’D)REPORT ON THE AUDIT OF THE CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS (CONT’D)KEY AUDIT MATTERS (CONT’D)

INSURANCE CONTRACT LIABILITIES

See accounting policy note 1.2e) and disclosure note 25 - Insurance contract liabilities

The key audit matter How the matter was addressed

Insurance contract liabilities constitute about 37% of the Group’s total liabilities. Valuation of these liabilities is highly judgemental and requires a number of assumptions to be made that have high estimation uncertainty.

This is particularly the case for those liabilities that are recognized in respect of claims that have occurred but have not yet been reported to the Group. Small changes in the assumptions used to value the liabilities, particularly those relating to the amount and timing of future claims, can lead to material impacts on the valuation of insurance liabilities..

The key assumptions that drive the reserving calculations include graduated development factors, loss ratios, inflation assumptions and claims expense assumptions.

The valuation of insurance contract liabilities depends on the accuracy of data about the volume, amount and pattern of cur-rent and historical claims since they are often used to form expectations about future claims.

If the data used in calculating insurance liabilities, or for forming judgements over key assumptions, is not complete and accurate then material impacts on the valuation of insurance liabilities may arise. Consequently, we have determined the valuation of insur-ance contract liabilities to be a key audit matter.

Our audit procedures in this area included among others:

• Evaluating and testing of key controls around the claims handling and reserve setting processes of the Group;

• Checking for any unrecorded liabilities at the end of the period;

• Checking samples of claims reserves by comparing the estimated amount of the reserve to appropriate docu-mentation, such as reports from loss adjusters;

• Re-performing reconciliations between the data record-ed in the financial systems and the data used in the actu-arial reserving calculations;

• Using our actuarial specialists to review the reserving methodology applied and analytically reviewing the valu-ation results presented and movements since the pre-vious year-end. We focused on understanding the meth-odologies applied and examining areas of judgement such as changes in valuation assumptions; and

• We also considered the validity of management’s liability adequacy testing by assessing the reasonableness of the projected cash flows and challenging the assumptions adopted in the context of company and industry experi-ence data and specific product features.

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

35

The key audit matter How the matter was addressed

The recognition of premium revenue, determination of un-earned premiums and estimation of provisions for uncollected premiums receivables involves significant judgment.

There are inherent risks in the valuation of reinsurance assets and insurance receivables (Note 35 (c)).

These balances require judgement to be applied by the Compa-ny for their valuation and their processing requires manual ad-justments to be made.

Due to the above factors, we considered premium income and receivables to be a key audit matter.

Our audit procedures in this area included, among others:

• Understanding the terms of the reinsurance programmes in place and conducting relevant substantive procedures and substantive analytical procedures to assess the rea-sonableness of the reinsurance assets relative to gross provisions;

• Inspection of management’s aged analysis for recoveries as at 31 December 2017;

• Evaluation and testing of key controls over the processes designed to record and monitor premium income and insurance and reinsurance receivables;

• Testing of the manual adjustments on a sample basis by tracing back to supporting documentation; and

• Considering credit ratings for reinsurers, facultative and brokerage entities.

See accounting policy notes:

• 1.2 (f) (i)) recognition and measurement of premium income• 1.2 (f) (vi) receivables and payables related to insurance contracts and investment contracts• 1.2 (k) impairment of financial assets

See notes to the financial statements:

• 35 (c) Management of insurance and financial risk (Credit risk)• 2 Gross earned premiums

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS (CONT’D)REPORT ON THE AUDIT OF THE CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS (CONT’D)KEY AUDIT MATTERS (CONT’D)

PREMIUM INCOME AND RECEIVABLES

36Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

The key audit matter How the matter was addressed

Many financial reporting controls depend on the correct functioning of operational and fi-nancial Information Technology (IT) systems, for example interfaces between the operat-ing systems and financial reporting systems, or automated controls that prevent or detect inaccurate or incomplete transfers of financial information.

If these systems or controls fail, a significant risk of error in reported financial information can arise from the failure to transfer data ap-propriately between systems or inappropriate changes being made to financial data or sys-tems.

This is an area requiring particular audit atten-tion in our audit due to the complexity of the IT infrastructure and legacy systems which re-quire manual inputs, relative to more automat-ed processes.

In this area our audit procedures included,among others:

• Testing general IT controls around system access and change management and testing controls over computer operations within specific applications which are required to be operating correctly to mitigate the risk of misstatement in the fi-nancial statements;

• With the support of our own IT specialists, we tested these controls through ex-amining the process for approving changes to the systems, and assessing the restrictions placed on access to core systems through testing the permissions and responsibilities of those given that access.; and

• Where we identify the need to perform additional procedures, place reliance on manual compensating controls, such as reconciliation between systems and other information sources or performing additional testing, such as extending the size of our sample sizes, to obtain sufficient appropriate audit evidence over the financial statement balances that were impacted.

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS (CONT’D)REPORT ON THE AUDIT OF THE CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS (CONT’D)KEY AUDIT MATTERS (CONT’D)

INFORMATION TECHNOLOGY SYSTEMS AND CONTROLS

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS (CONT’D)REPORT ON THE AUDIT OF THE CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS (CONT’D)

OTHER INFORMATION

The Directors are responsible for the other information. The other information obtained at the date of this aduitor’s report is information included in the Annual Report and Financial Statements, but does not include consolidated and separate financial statements and our auditors report thereon.

Our opinion on the consolidated and separate financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

37

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS (CONT’D)REPORT ON THE AUDIT OF THE CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS (CONT’D)

OTHER INFORMATION

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed on the other information obtained prior to the date of this auditors’ report, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

RESPONSIBILITIES OF DIRECTORS FOR THE FINANCIAL STATEMENTS

As stated on page 30, the Directors are responsible for the preparation of the financial statements that give a true and fair view in accordance with International Financial Reporting Standards and in the manner required by the Kenyan Companies Act, 2015 and for such internal control, as the Directors determine is necessary to enable the preparation of consolidated and separate financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated and separate financial statements, the Directors are responsible for assessing the group’s and company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the Directors either intend to liquidate the Company or to cease operations, or have no realistic alternative but to do so.

The Directors are responsible for overseeing the Company’s financial reporting process.

AUDITORS’ RESPONSIBILITIES FOR THE AUDIT OF THE CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS

Our objectives are to obtain reasonable assurance about whether the financial statements of the consolidated and separate as a whole are free from material misstatement, whether due to fraud or error and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group’s and Company’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the Directors.

38Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS (CONT’D)REPORT ON THE AUDIT OF THE CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS (CONT’D)

• Conclude on the appropriateness of the Director’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt

on the Group’s and Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated and separate financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors’ report. However, future events or conditions may cause the Group and/or Company to cease to continue as a going concern.

• Evaluate the overall presentation, structure, and content of the consolidated and separate financial statements, including the disclosures, and whether the consolidated and separate financial statements represent the underlying transactions and events in a manner that achieves a fair presentation.

• Obtain sufficient appropriate audit evidence regarding the financial information of the entities within the group to express an opinion on the consolidated and separate financial statements. We are responsible for the direction, suspension, and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with Directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

From the matters communicated with the Director’s, we determine those matters that were of most significance in the audit of the consolidated and separate financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditors’ report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

REPORT ON OTHER LEGAL AND REGULATORY REQUIREMENTS

As required by the Kenyan Companies Act, 2015 we report to you, based on our audit, that:• In our opinion, the information given in the report of the directors on page 7 is consistent with financial statements.• Our opinion is unqualified.

The Engagement Partner responsible for the audit resulting in this independent auditors’ report is CPA Alexander Mbai P/2172

KPMG Kenya8th Floor, ABC TowersWaiyaki WayP O Box 4061200100 Nairobi GPODate: 28 March 2018

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

39

LADIES FIRST CAR INSURANCE

because your prizedpossessions matter

FINANCIAL STATEMENTS 2017

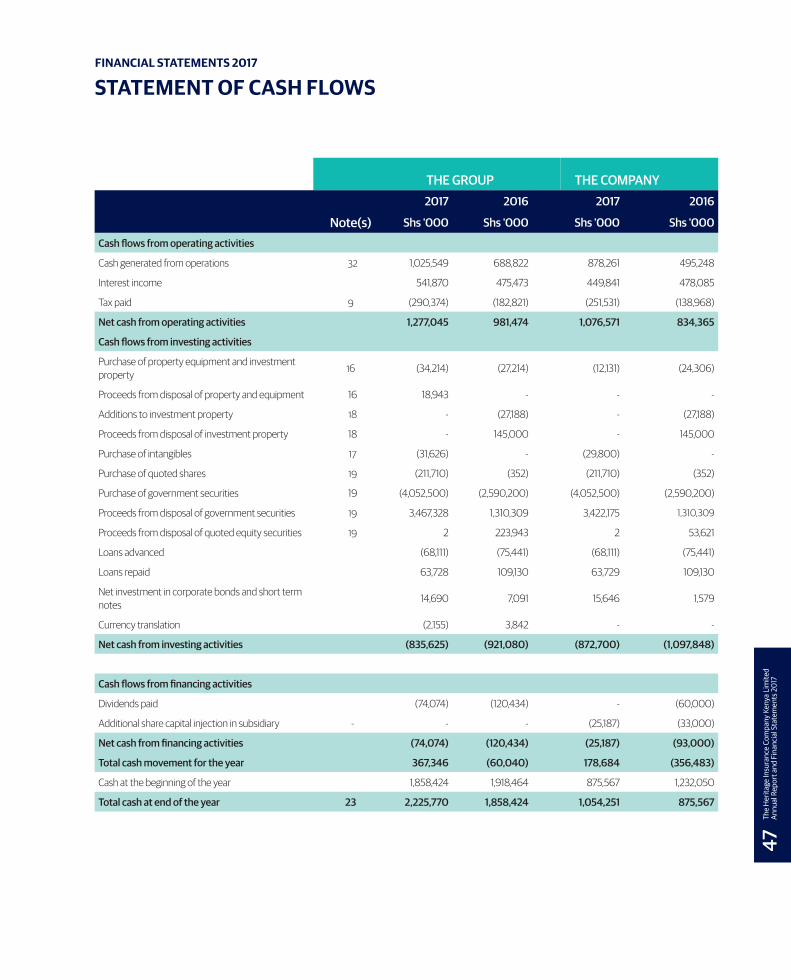

STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 2017

THE GROUP THE COMPANY

2017 2016 2017 2016

Note(s) Shs '000 Shs '000 Shs '000 Shs '000

Gross earned premiums 2 7,584,902 7,519,324 5,606,220 5,206,092

Less: reinsurance premium ceded (3,933,831) (3,762,092) (2,508,219) (2,143,667)

Net earned premiums 3,651,071 3,757,232 3,098,001 3,062,425

Commissions earned 834,634 776,942 648,476 570,333

Investment income 3 567,561 462,848 561,042 478,085

Gain/(loss) on sale of subsidiary 4 (10,549) - 49,615 -

Other income/(loss) 5 32,173 17,268 15,056 5,765

1,423,819 1,257,058 1,274,189 1,054,183

Net income 5,074,890 5,014,290 4,372,190 4,116,608

Claims and policyholder benefits 6 3,466,013 3,329,367 2,710,775 2,586,027

Less: amounts recoverable from re insurers (1,705,130) (1,657,550) (1,209,415) (1,230,725)

Net insurance benefits and claims 1,760,883 1,671,817 1,501,360 1,355,302

Operating and other expenses 7 1,790,058 1,696,549 1,425,477 1,422,194

Commissions payable 844,948 863,589 674,371 634,035

Total expenses and commissions 2,635,006 2,560,138 2,099,848 2,056,229

Result of operating activities 679,001 782,335 770,982 705,077

Profit before income tax 679,001 782,335 770,982 705,077

Income tax expenses 9 (220,258) (258,088) (193,892) (206,885)

Profit for the year 458,743 524,247 577,090 498,192

Profit attributable to:

Owners of the Company 437,961 481,993 577,090 498,192

Non controlling interests 20,782 42,254 - -

458,743 524,247 577,090 498,192

The accounting policies on pages 47 to 61 and the notes on pages 61 to 103 form an integral part of the financial statements 2017.

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

41

FINANCIAL STATEMENTS 2017

STATEMENT OF OTHER COMPREHENSIVE INCOME

THE GROUP THE COMPANY

2017 2016 2017 2016

Note(s) Shs '000 Shs '000 Shs '000 Shs '000

Profit for the year 458,743 524,247 577,090 498,192

Other comprehensive income:

Items that may be reclassified to profit or loss:

Foreign currency translation differences 13 (b) (17,013) (20,517) - -

Total other comprehensive income (17,013) (20,517) - -

Total comprehensive income for the year 441,730 503,730 577,090 498,192

Total comprehensive income attributable to:

Owners of the parent 426,154 464,589 577,090 498,192

Non controlling interest 15 15,576 39,141 - -

441,730 503,730 577,090 498,192

The accounting policies on pages 47 to 61 and the notes on pages 61 to 103 form an integral part of the financial statements 2017.

42Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

FINANCIAL STATEMENTS 2017

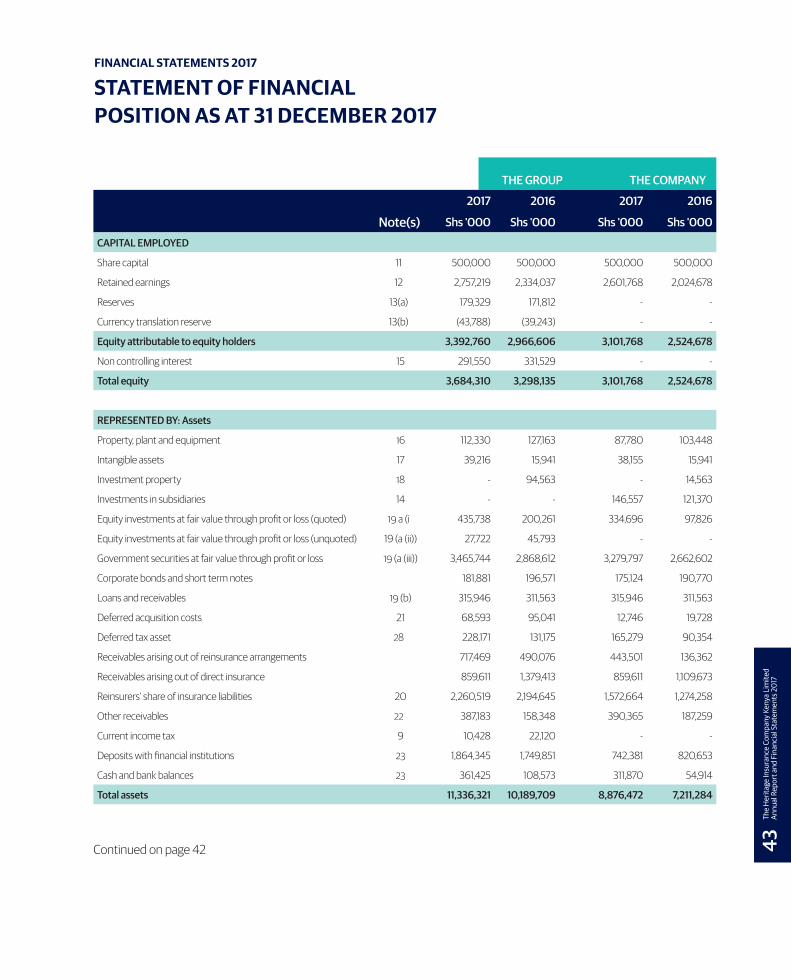

STATEMENT OF FINANCIALPOSITION AS AT 31 DECEMBER 2017

THE GROUP THE COMPANY

2017 2016 2017 2016

Note(s) Shs '000 Shs '000 Shs '000 Shs '000

CAPITAL EMPLOYED

Share capital 11 500,000 500,000 500,000 500,000

Retained earnings 12 2,757,219 2,334,037 2,601,768 2,024,678

Reserves 13(a) 179,329 171,812 - -

Currency translation reserve 13(b) (43,788) (39,243) - -

Equity attributable to equity holders 3,392,760 2,966,606 3,101,768 2,524,678

Non controlling interest 15 291,550 331,529 - -

Total equity 3,684,310 3,298,135 3,101,768 2,524,678

REPRESENTED BY: Assets

Property, plant and equipment 16 112,330 127,163 87,780 103,448

Intangible assets 17 39,216 15,941 38,155 15,941

Investment property 18 - 94,563 - 14,563

Investments in subsidiaries 14 - - 146,557 121,370

Equity investments at fair value through profit or loss (quoted) 19 a (i 435,738 200,261 334,696 97,826

Equity investments at fair value through profit or loss (unquoted) 19 (a (ii)) 27,722 45,793 - -

Government securities at fair value through profit or loss 19 (a (iii)) 3,465,744 2,868,612 3,279,797 2,662,602

Corporate bonds and short term notes 181,881 196,571 175,124 190,770

Loans and receivables 19 (b) 315,946 311,563 315,946 311,563

Deferred acquisition costs 21 68,593 95,041 12,746 19,728

Deferred tax asset 28 228,171 131,175 165,279 90,354

Receivables arising out of reinsurance arrangements 717,469 490,076 443,501 136,362

Receivables arising out of direct insurance 859,611 1,379,413 859,611 1,109,673

Reinsurers’ share of insurance liabilities 20 2,260,519 2,194,645 1,572,664 1,274,258

Other receivables 22 387,183 158,348 390,365 187,259

Current income tax 9 10,428 22,120 - -

Deposits with financial institutions 23 1,864,345 1,749,851 742,381 820,653

Cash and bank balances 23 361,425 108,573 311,870 54,914

Total assets 11,336,321 10,189,709 8,876,472 7,211,284

Continued on page 42

The

Her

itage

Insu

ranc

e Co

mpa

ny K

enya

Lim

ited

Annu

al R

epor

t and

Fin

anci

al S

tate

men

ts 2

017

43

FINANCIAL STATEMENTS 2017

STATEMENT OF FINANCIALPOSITION AS AT 31 DECEMBER 2017 CONTINUED

THE GROUP THE COMPANY

2017 2016 2017 2016

Note(s) Shs '000 Shs '000 Shs '000 Shs '000

Liabilities

Insurance contract liabilities 25 2,823,722 2,652,724 2,182,858 2,048,629

Unearned premium 27 2,918,386 2,926,838 2,355,765 2,018,889

Deferred commission income 21 59,594 87,318 - -

Deferred income tax 28 - 1,719 - -

Current income tax 36,511 19,604 36,511 19,225

Creditors arising from direct insurance 585,119 449,402 546,310 449,408

Creditors arising from reinsurance arrangements 755,146 540,791 484,578 -

Amounts due to related companies 29 10,429 9,042 10,429 13,741

Other payables 29 463,104 204,136 158,253 136,714

Total liabilities 7,652,011 6,891,574 5,774,704 4,686,606

Total net assets 3,684,310 3,298,135 3,101,768 2,524,678

The annual report and financial statements 2017 and the notes on pages 39 to 103, were approved and authorised for issue by the board on the 28 March 2017 and were signed on its behalf by:

P.N. Gethi G.R. May G.M. Kioi

The accounting policies on pages 47 to 61 and the notes on pages 61 to 103 form an integral part of the financial statements 2017.

44Th

e H

erita

ge In

sura

nce

Com

pany

Ken

ya L

imite

d An

nual

Rep

ort a

nd F

inan

cial

Sta

tem

ents

20

17

FINANCIAL STATEMENTS 2017