Embed Size (px)

Citation preview

The Impact of Cross-listing on the Cost of Equity Capital: The Case of

American Depository Receipts (ADRs) and Global Depository Receipts

(GDRs)*

Oksana Kim

The University of Melbourne Department of Accounting and Business Information Systems

Abstract

The study contributes to the cross-listing literature and examines the impact of cross-listing via an American Depository Receipt (ADR) or a Global Depository Receipt (GDR) program on the cost of equity capital. The study covers a global sample of firms that were cross-listed as ADRs on the NYSE, NASDAQ and AMEX, or GDRs on the London Stock Exchange (LSE). Using the implied cost of capital models that are based on the [1] realized accounting earnings (O’Hanlon and Steele 2000 - OHS) and [2] analysts’ predictions (Easton et al. 2002 - ETSS) and asset-pricing models (Fama and French 1993), the study finds that the cost of capital declines for both ADRs and GDRs. This result holds across both methodological approaches to estimating the cost of capital. Consistent with this decline being due to information risk reduction, we find some evidence that it varies as a function of the quality of the disclosed information. The findings of the study will enhance our understanding of why firms chose to cross-list as ADRs or GDRs, provide insights into the impact of information risk on the cost of capital and have practical implications for exchanges that consider accommodating depository receipts programs, such as Dubai, Singapore, and Hong Kong. Keywords: American Depository Receipts, Global Depository Receipts, cost of equity capital, information risk, cross-listing.

* We thank the participants of the workshops at the University of Technology Sydney and the University of New South Wales for their helpful comments and suggestions.

2

1. INTRODUCTION The study investigates the impact of cross-listing via American Depository Receipts (ADRs)

or Global Depository Receipts (GDRs) on cost of equity capital. While ADRs, a more

traditional cross-listing mechanism, were extensively examined in the empirical cross-listing

literature, the GDRs, which is a more recent globalization phenomenon, received limited

attention. The two cross-listing mechanisms are expected to result in cost of capital decline

through a number of avenues. One of them is the reduction in information risk of firms that

choose to cross-list, as they become a subject to more stringent mandatory disclosure

requirements enforced by the respective standard setting regulatory bodies. In case of ADRs it

is the Securities and Exchanges Commission (SEC), while in case of the GDRs listed on the

London Stock Exchange’s (LSE) Main Market it is the United Kingdom Listing Authority

(UKLA)2 that is a regulatory body for all regulated markets of the European Union.

The study has a twofold motivation and will make a number of contributions to both the

cross-listing literature and the literature examining the impact of information risk on cost of

capital. First, prior studies did not examine properties of GDRs alone or in comparison to

ADRs. GDR programs are fundamentally different from ADR programs in a number of ways

and therefore generalizing findings of ADR-based empirical studies on GDRs may not be

appropriate. As of 2006, the capital raising activity via GDRs far exceeded that of ADRs (JP

Morgan 2008). If the total Depository Receipts market constituted a stock exchange of its

own, it would have the world’s 10th largest market capitalization (Bank of New York 2008).

The market would be far ahead of the Australian and Swiss markets in terms of liquidity and

well ahead of the Toronto Stock Exchange and the Hong Kong Stock Exchange in terms of

trading volume, for instance. The share of GDRs in the total Depository Receipts (DR) market

was 26 percent as of 2005, reached 44 percent as of 2007 and is expected to increase (Bank of

New York 2008). Given the growing economic significance of GDRs, it is important to

understand whether the alternative depository receipts programs such as GDRs provides

benefits in the form of a reduced cost of capital compared to ADRs that represent a more

traditional cross-listing tool.

2 Formerly known as the Securities and Investments Board Ltd, currently also known as the UK Financial Services Authority (FSA).

3

The motivation of this study is to provide empirical evidence on the alternative programs,

GDRs, alone and in comparison to the more traditional cross-listing mechanism - ADRs. The

findings of the study will have important practical implications for firms intending to cross-

list via an ADR or a GDR program, as well as for stock exchanges that have been actively

promoting themselves as a new cross-listing destination in an attempt to enter the cross-listing

market, for example Dubai, Singapore, Hong Kong, etc.

Second, the study contributes to the empirical literature examining the association between

information risk and cost of capital. Among the studies that have established a theoretical

association between the information risk and the cost of equity capital are those of Lambert,

Leuz and Verrecchia (2007), Easley and O’Hara (2004), and others. While a strong theoretical

link between the information risk and the cost of capital is well established in the literature,

the findings of the empirical work that attempted to test this prediction in cross-listing settings

are mixed. Using realized returns methodology Errunza and Miller (2000) documented

economically significant cost of capital decline – around 42 percent. Employing a different

methodology - the implied cost of capital models – Hail and Leuz (2009) documented a

modest cost of capital decline for exchange-listed ADRs, while increase in cost of capital for

the Rule 144A private placement programs. The motivation for this study is to provide new

empirical evidence on the impact of changes in the information environment as a result of

cross-listing on the cost of capital, given the mixed results of extant literature. Provided that

the requirements of the SEC in relation to ADRs and those of UKLA in relation to GDRs

differ in terms of the quantity and quality of the disclosed information, the two samples of

ADR and GDR cross-listed firms offer a powerful experiment for testing the rank order effect

of the theory of information risk on the cost of capital.

Next, the study makes a contribution to the accounting literature that examines the association

between the level of disclosure and cost of capital. The findings from this literature have been

mixed (Botosan, 1997; Botosan and Plumlee 2002). One of the reasons for the mixed results

of extant literature is that the studies have examined the association in the levels of the two

variables and were primarily based on voluntary disclosure practice of the US-registered firms

where the disclosure environment under the US GAAP regime is rich anyway (Leuz and

Verrecchia 2000). In addition, market participants recognize that voluntary commitment does

not necessarily imply enhanced reporting in the future and may be reversed any time (Leuz

and Verrecchia 2000). In this study we propose to construct experimental settings that allow

4

tests for the association between the changes in the level of disclosure and cost of equity

capital as a result of a mandatory disclosure increase. This will represent a more powerful test

of the impact of improved disclosure on cost of capital3.

The final contribution of the study is in the improved research design. The potential

explanation for the mixed findings of prior cross-listing literature is both the low power of

empirical tests due to limitations of the research design and sampling technique and failure to

control for potential endogeneity. Recognizing this, we adopt several innovations. First, the

study controls for the self-selection bias by using the ADR and GDR cross-listed firms as

their own control. This avoids the matching procedure used in prior studies that compared

cost of capital of all existing ADRs and non-ADRs4. Second, when comparing the magnitude

of changes in cost of capital of ADRs versus GDRs we use a two-stage estimation procedure

that addresses a potential self-selection bias issue and attempts to account for a number of

characteristics that might drive a firm’s decision to list as an ADR or a GDR.

Another potential explanation for the mixed findings of prior studies is inappropriate and

noisy sample construction. Prior studies used the term “ADR” and “cross-listed”

interchangeably, while in fact far not all ADRs (and GDRs) are cross-listed firms. It is often

the case that one cross-listed firm enters an ADR/GDR sample several times when a company

changed a name, was acquired or was restructured, for instance. Besides, there are multiple

cases when ADR-listed firms changed cross-listing programs and/or switched to a GDR

listing (and vice versa), or prior to an ADR/GDR listing they had been directly listed on the

exchanges that required extensive disclosure of accounting information. Assigning cross-

listed firms to a correct sub sample is crucial to the study given small sample sizes of ADRs

and GDRs. Therefore the manual background check for each ever existing ADR and GDR

3 Larcker and Rusticus (2010) discuss problems with estimating the association between voluntary disclosure and cost of capital. They argue that while the earlier studies treated the disclosure as exogenous, the relationship in fact suffers from endogeneity issue. It is possible that firms with lower disclosure level have higher cost of capital and hence the association between the cost of capital and the disclosure level is negative, provided the disclosure level is a priced factor. But if such firms decide to disclose more (voluntary disclosure) and do not succeed, the observed association will be positive. This may explain mixed findings of the studies such as Botosan (1997). In the present study this is not an issue, as cross-listed firms are subject to mandatory disclosure and do not have much discretion over the extent and content of the reported information. 4 As argued by Stulz (1999), the problem with the interpretation of results based on a matching procedure is that the theory does not make a direct prediction about how changes in cost of capital for ADRs should differ from non-ADRs. Instead, the theory helps making predictions in regard to the changes in cost of capital for the same firms after a certain event that is expected to result in such changes.

5

program is essential5. In addition, some ADR and GDR-listed firms never list on their

domestic markets and hence never become cross-listed. Such firms should not be treated as

cross-listed firms and should be excluded from the ADR/GDR sample.

The study pays specific attention to the institutional differences and the pre- and post-listing

disclosure requirements of ADRs and GDRs that were largely overlooked in prior literature.

For example, prior literature that mentioned existence of GDRs as a LSE listing tool argued

that GDRs were not a subject to enhanced disclosure requirements and hence were not

expected to experience positive changes in the information environment upon cross-listing

(Abdallah 2008). While the argument is applicable to the GDRs listed on the unregulated

Professional Securities Market (PSE) and the Alternative Investment Market (AIM) of the

LSE, it is not applicable to the GDRs listed on the Main Market of the LSE that are the focus

of the present study. The Main Market (MM) of the LSE is the European Union (EU)

regulated market that puts in place stringent disclosure requirements for all companies listed

on it. Although being exempt from a number of reporting obligations that the native (directly

listed) UK firms are subject to, the GDR programs listed on the MM have been a subject to

more rigorous disclosure requirements compared to their domestic markets. The institutional

details and the disclosure requirements for the existing LSE markets are disclosed in details in

Section 2.

Our findings indicate that cost of capital declines for both ADRs and GDRs and the result

holds across both methodological approaches to estimating cost of capital. There is, however,

only week evidence in support to the prediction that the magnitude of changes in cost of

capital varies as a function of disclosed information.

The remainder of the paper is organized as follows. Section 2 provides background details on

ADRs and GDRs, Section 3 is dedicated to the related research and hypotheses development.

Section 4 discusses data collection process and the issues associated with the manual

background check, Section 5 describes the research design. Section 6 discusses the results of

empirical tests and Section 7 concludes.

5 Section 4 elaborates on the striking findings of the manual background check for each ADR and GDR program that ever existed and provides evidence on how the composition of the ADRs and GDRs sample changes as a result of the background verification compared to if a simple matching procedure is used.

6

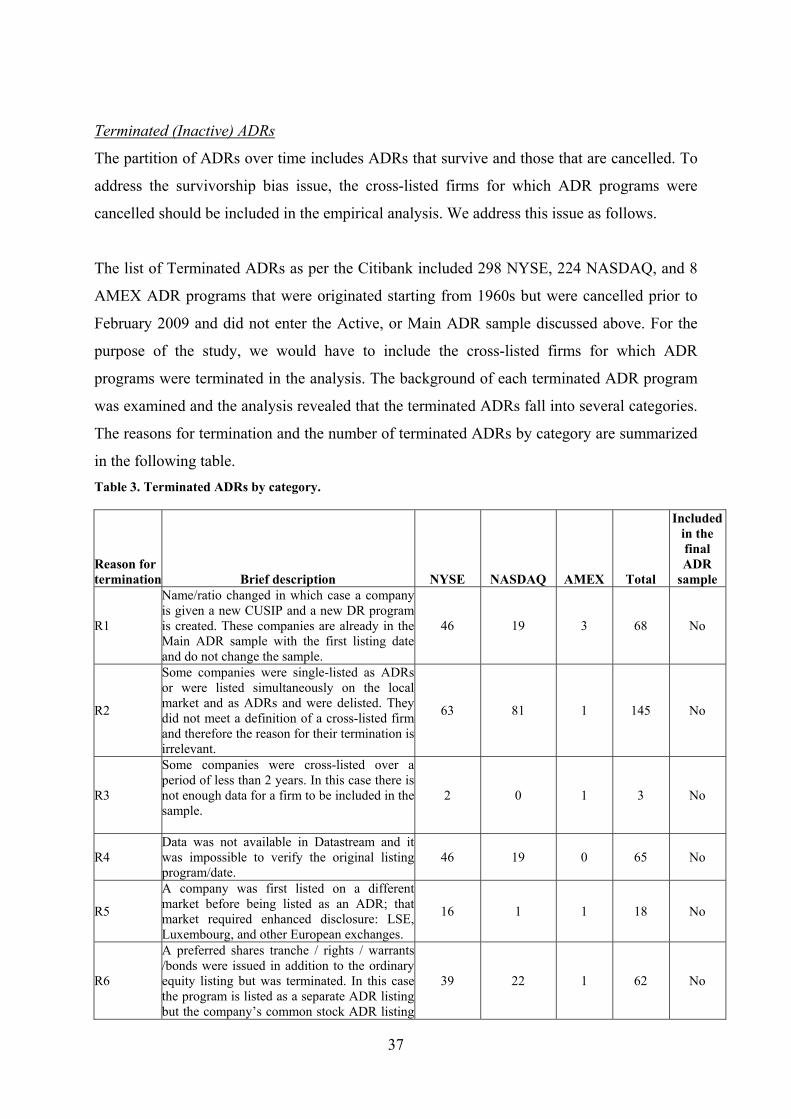

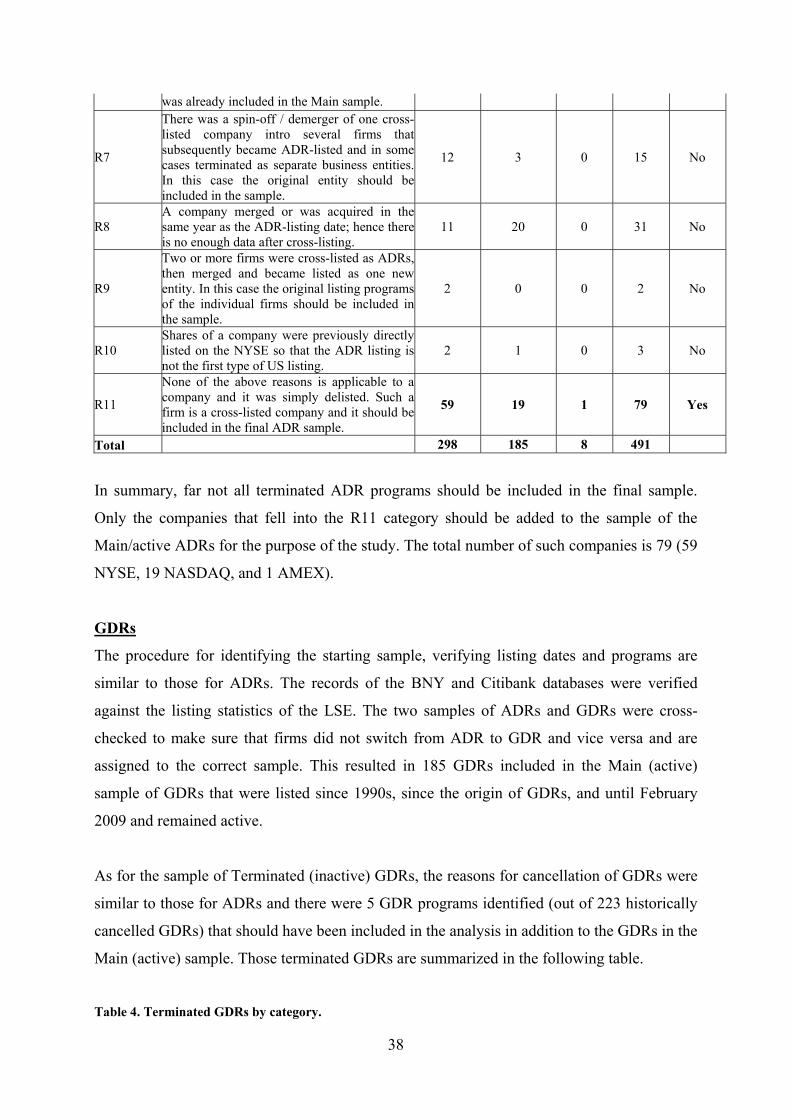

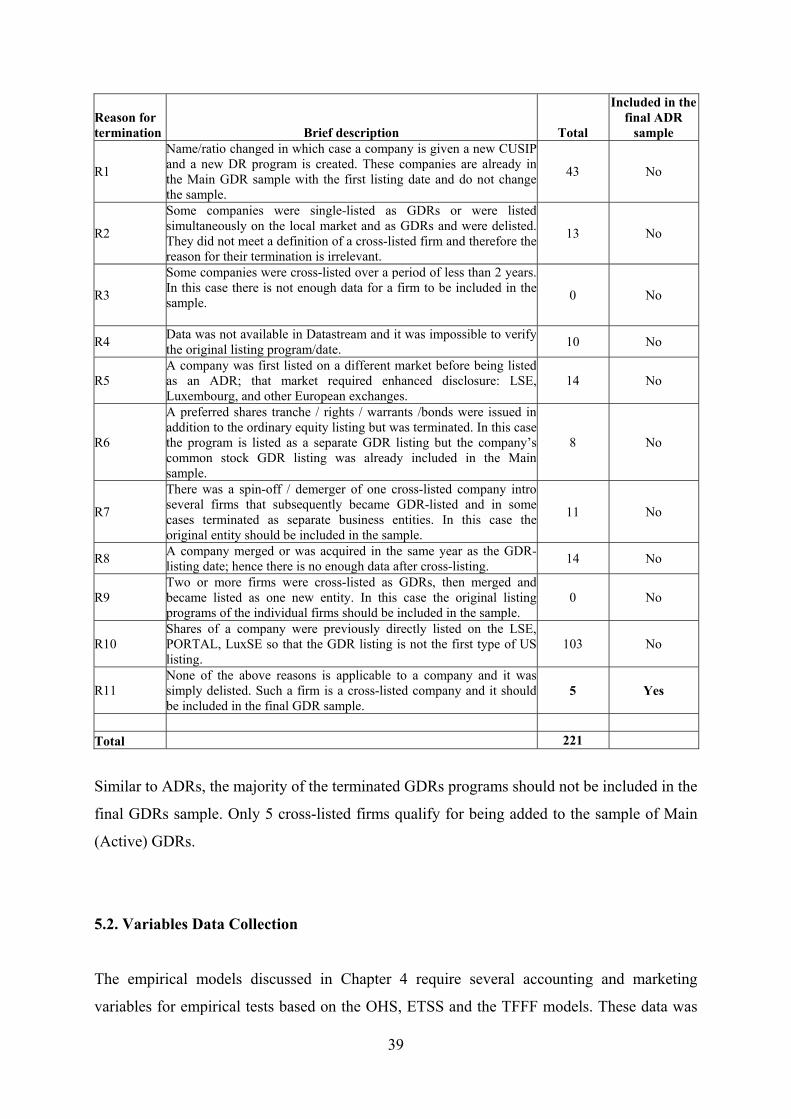

2. DEPOSITORY RECEIPTS PROGRAMS: HISTORY, TRENDS AND INSITUTIONAL DETAILS

2.1. HISTORY AND TRADING MECHANISM

As documented by JP Morgan (2003), the history of the first depository receipt program goes

back to 1920s. The UK-based retail company “Selfridge Provincial Stores Ltd.” decided to

expand its shareholding base and aimed to start selling its shares to the US investors. As the

same time, the US investors expressed their interest in buying the company’s shares; however

the awkward settlement procedures complicated the process. For instance, the potential US

buyers would have to pass through the list of registered holders in England in order to buy the

shares (Deutsche Bank 2003). At the same time, if a US investor further decided to sell the

shares to other US investors through the NYSE, he would fail to do so because the new

investor would have to be registered in the UK as well. Hence, there was a clear need to

establish the mechanism that would allow overcoming those barriers (Deutsche Bank 2003;

Mondevisione 2009).

A US bank, Morgan Guarantee Trust (the predecessor of the J.P. Morgan) solved the problem

by holding the Selfridge’s shares on its name in the UK and at the same time issuing

promissory notes to the US investors through its US branch. The notes were freely tradable on

the NYSE, as they were registered in the US, and had no limitations on purchase and

transferability (JP Morgan 2003). The mechanism proved to be a successful tool and

following the Selfridge’s practice, a few other companies expressed their desire to open the

same programs. The promissory notes issued by the Guarantee Trust became known as

“American Depository receipts” and were a predecessor of today’s ADRs (JP Morgan 2003).

The stock market crush in 1929 and the following periods of Great Depression in 1930s

resulted in lack of investment resources and low demand for foreign issuers’ securities. With

stock markets recovering from the financial crisis, the World War II resulted in certain

restrictions imposed on the capital movement (Mondevisione 2009). The DR programs no

longer existed until the US economy partially recovered and in 1950’s the new era for the DR

programs began with SEC’s introduction of the ADR programs registration in the US market

(Deutsche Bank 2003). In 1960-1970s the ADR programs were primarily in high demand by

7

the leading hi-tech and car manufacturing companies from Japan6 and the mining companies

from South Africa7. More companies from the developed markets joined the ADR market in

1980s (primarily from Australia and Great Britain).

The cross-listing boom started in 1990s primarily due to the relaxation of the ADR

registration requirements accompanied by the development of trading and communication

technology. The globalization process resulted in the growing desire from the US investors to

diversify their portfolios and invest in foreign companies’ stocks (Karoliy 1998)8. The ADR

mechanism that was substantially less costly than the direct listing of shares in the US gave

rise to the corresponding growing offer of foreign equities to the US investors. Finally, the

companies from emerging markets (Latin America, Middle East, Eastern Europe, and Asia)

joined the ADRs market primarily in mid-late 1990s and have continued their cross-listing via

the ADR programs until the present moment9.

The growing ability of emerging markets’ companies to offer their stocks overseas (not

limited by the US market) due to the gradual removal of trade barriers and the overall

relaxation of the capital movement was met with the foreign, non-US (global) investors,

demand for their securities (Mondevisione 2009). This gave rise to the DR program that

represents an alternative to the ADR programs, namely Global Depository Receipts (GDRs).

Initially it was expected that Luxembourg Stock Exchange (LuxSE) would be the primary

exchange for GDRs due to its well-established historic linkage to the Eurobond market and

direct settlement procedures through Euroclear and Clearstream electronic systems

(Mondevisione 2009). However, the London Stock Exchange (LSE) was the first exchange

that provided a convenient regulatory approach and established trading of GDRs through the

International Order Book (IOB) with high liquidity and global investor access (Russian IPO

2010). Therefore the LSE and not Luxembourg occupied the niche of GDR business

(Mondovisione, 2009). The first GDR program was registered on the LSE in 1994 but other

exchanges have been accommodating a few new GDR programs per year. Luxembourg

5 Sony, Panasonic, TDK, Toyota were listed as ADRs on the NYSE back in 1973. 7 AngloGold Ashanti, Gold Fields, Harmony Gold Mining were listed as ADRs on the NYSE in early 1970s. 8 The example would be a relaxation of the requirement for institutional investors to hold privately placed securities for two years before trading them. 9 The example of the cost efficiency of ADRs over the direct listing is absence of brokerage fees, lower accounting and legal costs, and a low chance of the trade failure in case of ADRs, compared to the direct listing (Karoliy 1998).

8

remains the second largest GDR destination after the LSE, followed by Dubai, Singapore, and

Hong Kong. The LSE, however, is the clear leader in attracting GDRs by providing special

services to firms intending to cross-list as GDRs and maintaining comprehensive database on

GDR trends, history, and analysis (London Stock Exchange 2009).

GDRs target investors from all over the world and are done primarily by the companies from

emerging (developing) markets, while ADRs have been and remain the major investment tool

for the US investors (Bank of New York 2006). Both ADRs and GDRs represent a certificate,

an underlying number of shares, and the creation and cancellation mechanisms are very

similar for them. There is an effective exchange mechanism in place between a local

custodian bank based in the domestic market of an ADR/GDR-listed firm, and a foreign

depository bank that represents a firm overseas10. When an international investor wishes to

invest in the ADR/GDRs, its broker contacts a foreign depository bank with a request to

deliver a certain number of securities. The depository bank then contacts the local custodian

bank that purchases the required number of shares from the local market, holds them and

gives instructions to the depository bank to issue a certain number of certificates representing

the number of underlying shares. The depository bank then issues DRs on the name of the

international investor. The cancellation of DRs is a reverse mechanism. Such a dual exchange

mechanism establishes a price linkage between the two markets. Therefore the liquidity of the

DRs should be the same as liquidity of underlying shares and there are no arbitrage

opportunities expected, as the DR certificates are simply multiple of common shares. In

practice, however, due to state restrictions that put a cap on the tradability of DRs on foreign

markets, the DRs may be of lower liquidity than their underlying shares (Russian IPO 2010).

Despite the similarities in purpose and mechanism of establishing a program, ADRs and

GDRs differ in terms of the disclosure requirements set up by the respective listing authorities

– SEC in case of ADRs and UKLA (FSA) in case of GDRs. The institutional details of ADRs

and GDRs are discussed separately.

2.2. ADRs: REGULATORY STRUCTURE AND INSITUTIONAL DETAILS

2.2.1. Regulatory Structure

10 The four major financial institutions that have had a proven success of working with GDRs are the Bank of New York Mellon, the Citibank, the JP Morgan Chase, and the Deutsche Bank.

9

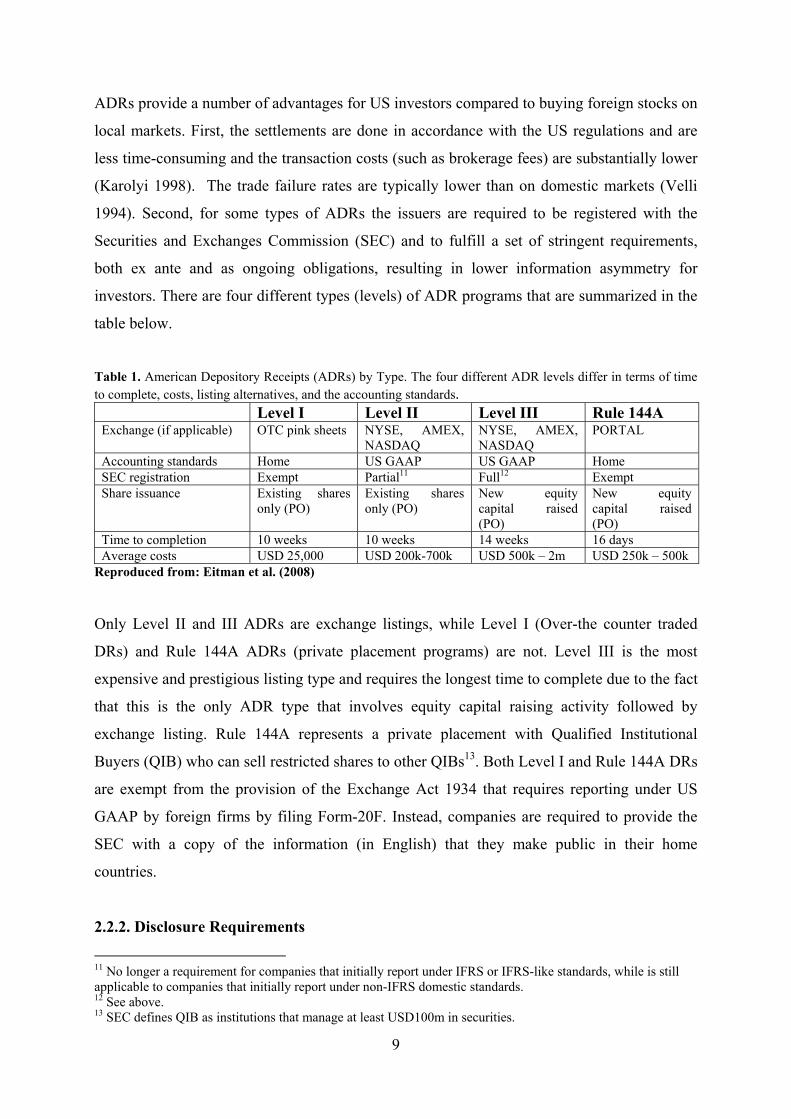

ADRs provide a number of advantages for US investors compared to buying foreign stocks on

local markets. First, the settlements are done in accordance with the US regulations and are

less time-consuming and the transaction costs (such as brokerage fees) are substantially lower

(Karolyi 1998). The trade failure rates are typically lower than on domestic markets (Velli

1994). Second, for some types of ADRs the issuers are required to be registered with the

Securities and Exchanges Commission (SEC) and to fulfill a set of stringent requirements,

both ex ante and as ongoing obligations, resulting in lower information asymmetry for

investors. There are four different types (levels) of ADR programs that are summarized in the

table below.

Table 1. American Depository Receipts (ADRs) by Type. The four different ADR levels differ in terms of time to complete, costs, listing alternatives, and the accounting standards. Level I Level II Level III Rule 144A Exchange (if applicable) OTC pink sheets NYSE, AMEX,

NASDAQ NYSE, AMEX, NASDAQ

PORTAL

Accounting standards Home US GAAP US GAAP Home SEC registration Exempt Partial11 Full12 Exempt Share issuance Existing shares

only (PO) Existing shares only (PO)

New equity capital raised (PO)

New equity capital raised (PO)

Time to completion 10 weeks 10 weeks 14 weeks 16 days Average costs USD 25,000 USD 200k-700k USD 500k – 2m USD 250k – 500k

Reproduced from: Eitman et al. (2008)

Only Level II and III ADRs are exchange listings, while Level I (Over-the counter traded

DRs) and Rule 144A ADRs (private placement programs) are not. Level III is the most

expensive and prestigious listing type and requires the longest time to complete due to the fact

that this is the only ADR type that involves equity capital raising activity followed by

exchange listing. Rule 144A represents a private placement with Qualified Institutional

Buyers (QIB) who can sell restricted shares to other QIBs13. Both Level I and Rule 144A DRs

are exempt from the provision of the Exchange Act 1934 that requires reporting under US

GAAP by foreign firms by filing Form-20F. Instead, companies are required to provide the

SEC with a copy of the information (in English) that they make public in their home

countries.

2.2.2. Disclosure Requirements

11 No longer a requirement for companies that initially report under IFRS or IFRS-like standards, while is still applicable to companies that initially report under non-IFRS domestic standards. 12 See above. 13 SEC defines QIB as institutions that manage at least USD100m in securities.

10

ADR Level II cross-listed firms are required to file Form 20-F annually and Form 6-K

quarterly after cross-listing. Those forms require reconciliation of material differences in

companies’ financial statements (major balance sheet and income statement items) to the US

GAAP. In addition to this, ADR Level III firms (capital raising firms) must fully reconcile

their financial statements to the US GAAP and submit Form F-1 (registration of securities

publicly offered to the US investors through IPO) and Form 8-K (disclosure of material

information made available to the home market’s shareholders). Thus, Level II and III ADRs

are associated with the extended and most rigorous disclosure requirements.

Level II and III ADRs can be listed on the NYSE, NASDAQ, and AMEX and are clearly

subject to more stringent disclosure requirements than Level I ADRs and Rule 144A private

placement programs. This study focuses on Level II and Level III ADRs, while Level I and

Rule 144A programs are not covered due to the fact that the disclosure requirements for them

are low and are not expected to result in improvement in firms’ information environment

upon cross-listing14.

Prior to 1983 there were so called unsponsored ADRs in place that were originated by

depositories in response to the investors’ demand and did not require a formal agreement with

the issuer. The number of such programs was small; they were not subject to enhanced

disclosure requirements upon cross-listing and no longer exist. Therefore the unsponsored

ADRs are not covered in the present study.

2.3. GDRs: REGULATORY STRUCTURE AND INSITUTIONAL DETAILS

2.3.1. Regulatory Structure

The study focuses on the Main Market LSE-listed GDRs and does not cover GDRs listed on

the LuxSE and other exchanges due to the fact that, first, the LSE is the world’s largest GDR

market in terms of market capitalization and liquidity (London Stock exchange 2009) and,

second, the cross-sectional variety of companies trading as GDRs through the LSE’s

14 Potentially Level I and Rule 144A programs could serve as a controlling sample for the exchange-listed Level II and III ADRs due to differential disclosure requirements – low for the former group of programs and extensive for the latter group. However, this would lead to the same trap of using a matching procedure used in prior studies that is viewed as a limitation in the present study due to the self-selection bias issues. Instead, the study attempts to control for this weakness in methodology by using the samples of the same cross-listed firms as their own control and therefore Level I and Rule 144A are not examined.

11

International Order Book (IOB) far exceeds that of the next largest GDR destination – the

LuxSE. To compare, as of 2009 there were over 270 securities from 46 countries trading on

the IOB service as GDRs (Russian IPO 2010), while the majority, 88 percent, of the LuxSE

GDRs were represented by companies from India and Taiwan (Bank of New York 2009).

The structure of the LSE GDRs closely parallels that of ADRs. There are Level I OTC-traded

GDRs that are not subject to any enhanced disclosure requirements. Level II and Level III

GDRs are exchange-listed programs. The companies that chose the LSE as their GDR-listing

destination has a choice of listing on the Main Market, the Professional Securities Market

(PSM), and the Alternative Investment Market (AIM). The AIM and the PSE are designed for

listing by small and mid-cap firms with high growth potential. The PSE is a relatively new

market and is the least liquid of all the LSE markets (London Stock Exchange 2009). Both

markets are not EU regulated markets. There are very few GDRs listed on the PSE and AIM,

compared to the Main Market, which is the most highly regulated market. The reason for this

is that the LSE discourages foreign entities from listing GDRs on the AIM due to insufficient

regulatory framework (Russian IPO 2010).

The UKLA (FSA) is the regulatory body for the Main Market. It reviews and approves

companies’ listing applications and prospectuses and grants a listing status to successful

applicants. The rules governing the admission of securities to trade on regulated markets and

the continuing obligations are set out in the Listing Rules, the Prospectus Rules, and the

Transparency and Disclosure Rules. The LSE, however, is responsible for trade admission

and makes a decision about which market a company qualifies to be admitted to (JP Morgan

2008). To be admitted to the trade on the Main Market, for instance, a company should have a

market capitalization of at least GBP 700 000, have underlying shares that are fully

transferable, and 25 percent of the GDRs must be in public hands.

Similarly to the Rule 144 for ADRs, there is a private placement program for GDRs that

represents a selective process of targeting a small number of QIBs. This is generally known as

a Regulation S (Reg S) offering. At the same time, a company may choose to include both the

US and non-US (global) QIBs into the pool by issuing a US tranche under the Rule 144A that

does not require a formal registration with the SEC and doesn’t lead to the enhanced

disclosure under US GAAP. In this case the GDR program is called a Bifurcated GDR.

12

2.3.2. Disclosure Requirements

While the trading mechanism is similar for ADRs and GDRs, the reporting and disclosure

requirements differ in terms of quantity, quality, and frequency of the disclosed information.

The European nations have been going through the unionization process, and so did their

markets. The development of a single trade market system with a regulatory system that

would apply to all member states of the European Union (EU) have resulted in bringing the

regulated markets of Europe in compliance with the EU Directives (FSA 2010). While each

regulated European market has its own national listing authority (UKLA in the United

Kingdom), the transparency and disclosure requirements set by the EU Directives apply to all

the companies listed on those regulated markets. The GDRs listed on the Main Market of the

LSE therefore must comply with the minimum disclosure requirements set up by the EU and

additionally with the specific requirements set up by the UKLA and the LSE (FSA 2009).

In contrast to the ADRs for which the disclosure requirements have remained relatively

unchanged historically (in terms of the frequency and the extent of the disclosed information,

filing the forms, reporting GAAP, etc.), the disclosure requirements for GDRs have

experienced substantial changes starting from the first year of GDRs registration, 1994, until

the present day. The changes primarily concern the accounting standards in accordance to

which GDRs were to disclose information and report. Historically, prior to 2005 the GDRs

listed either on the Main Market, PSE or AIM, were allowed to show the financial

information in the prospectus, as well as ongoing obligations, based on their national GAAP.

However, the Main Market LSE GDRs disclosed the major items of the balance sheet and the

income statement in accordance with the International Accounting Standards (IAS) prior to

2001 and in accordance with the International Financial Reporting Standards (IFRS) after

2001. In addition, the financial statements were to be audited annually in accordance with the

International Standards on Auditing (ISA). Any departure from the IAS and ISA would have

to be explained and the UKLA had discretion to decide whether or not the disclosed

information was in compliance with its requirements set up for the securities listed on the

Main Market.15 The GDRs listed on the PSE and AIM were exempt from such requirements

15 The UKLA guidance on the Depository Receipts (2000) cites: “The UK Listing Authority may enquire as to whether accounting principles which are consistent with IAS have been applied and as to the standing of the

13

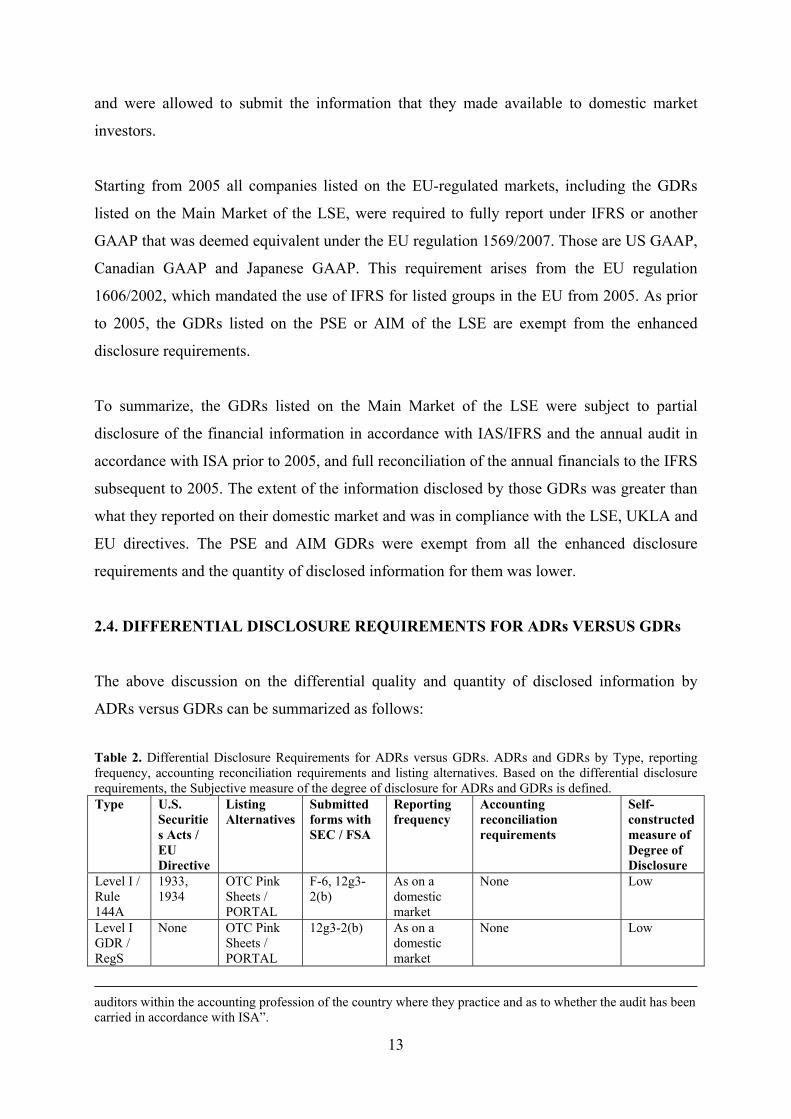

and were allowed to submit the information that they made available to domestic market

investors.

Starting from 2005 all companies listed on the EU-regulated markets, including the GDRs

listed on the Main Market of the LSE, were required to fully report under IFRS or another

GAAP that was deemed equivalent under the EU regulation 1569/2007. Those are US GAAP,

Canadian GAAP and Japanese GAAP. This requirement arises from the EU regulation

1606/2002, which mandated the use of IFRS for listed groups in the EU from 2005. As prior

to 2005, the GDRs listed on the PSE or AIM of the LSE are exempt from the enhanced

disclosure requirements.

To summarize, the GDRs listed on the Main Market of the LSE were subject to partial

disclosure of the financial information in accordance with IAS/IFRS and the annual audit in

accordance with ISA prior to 2005, and full reconciliation of the annual financials to the IFRS

subsequent to 2005. The extent of the information disclosed by those GDRs was greater than

what they reported on their domestic market and was in compliance with the LSE, UKLA and

EU directives. The PSE and AIM GDRs were exempt from all the enhanced disclosure

requirements and the quantity of disclosed information for them was lower.

2.4. DIFFERENTIAL DISCLOSURE REQUIREMENTS FOR ADRs VERSUS GDRs

The above discussion on the differential quality and quantity of disclosed information by

ADRs versus GDRs can be summarized as follows:

Table 2. Differential Disclosure Requirements for ADRs versus GDRs. ADRs and GDRs by Type, reporting frequency, accounting reconciliation requirements and listing alternatives. Based on the differential disclosure requirements, the Subjective measure of the degree of disclosure for ADRs and GDRs is defined. Type U.S.

Securities Acts / EU Directive

Listing Alternatives

Submitted forms with SEC / FSA

Reporting frequency

Accounting reconciliation requirements

Self-constructed measure of Degree of Disclosure

Level I / Rule 144A

1933, 1934

OTC Pink Sheets / PORTAL

F-6, 12g3-2(b)

As on a domestic market

None Low

Level I GDR / RegS

None OTC Pink Sheets / PORTAL

12g3-2(b) As on a domestic market

None Low

auditors within the accounting profession of the country where they practice and as to whether the audit has been carried in accordance with ISA”.

14

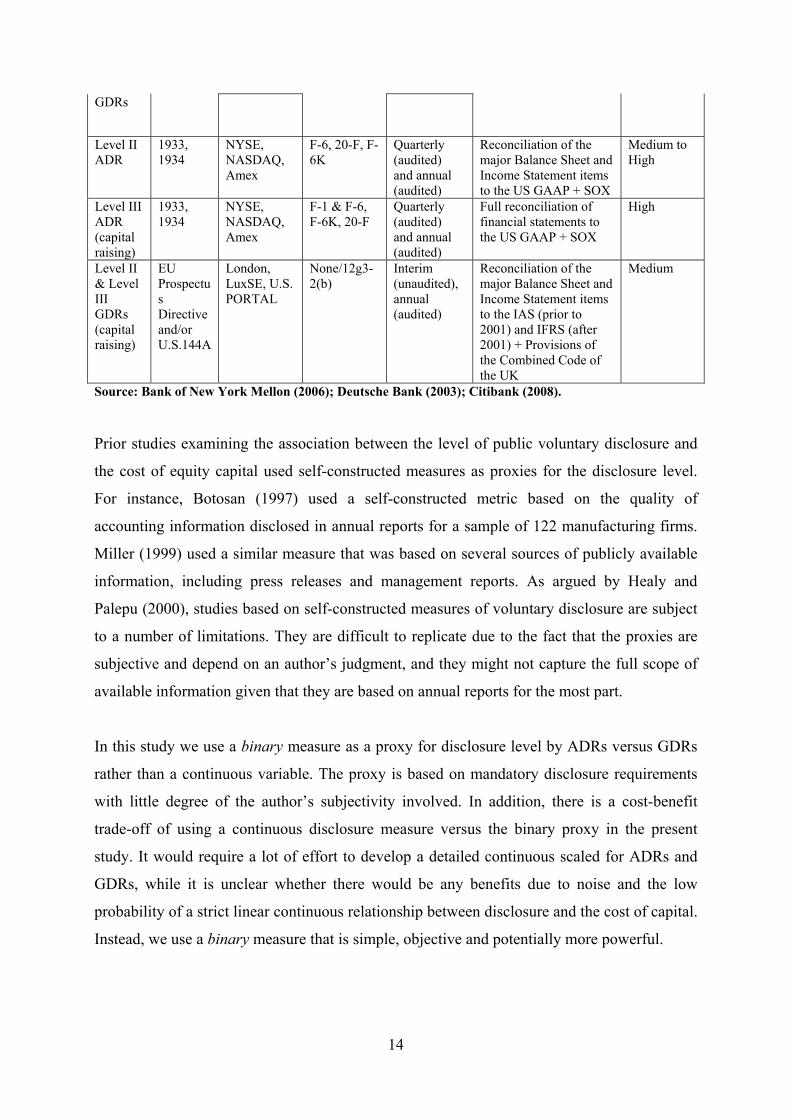

GDRs

Level II ADR

1933, 1934

NYSE, NASDAQ, Amex

F-6, 20-F, F-6K

Quarterly (audited) and annual (audited)

Reconciliation of the major Balance Sheet and Income Statement items to the US GAAP + SOX

Medium to High

Level III ADR (capital raising)

1933, 1934

NYSE, NASDAQ, Amex

F-1 & F-6, F-6K, 20-F

Quarterly (audited) and annual (audited)

Full reconciliation of financial statements to the US GAAP + SOX

High

Level II & Level III GDRs (capital raising)

EU Prospectus Directive and/or U.S.144A

London, LuxSE, U.S. PORTAL

None/12g3-2(b)

Interim (unaudited), annual (audited)

Reconciliation of the major Balance Sheet and Income Statement items to the IAS (prior to 2001) and IFRS (after 2001) + Provisions of the Combined Code of the UK

Medium

Source: Bank of New York Mellon (2006); Deutsche Bank (2003); Citibank (2008).

Prior studies examining the association between the level of public voluntary disclosure and

the cost of equity capital used self-constructed measures as proxies for the disclosure level.

For instance, Botosan (1997) used a self-constructed metric based on the quality of

accounting information disclosed in annual reports for a sample of 122 manufacturing firms.

Miller (1999) used a similar measure that was based on several sources of publicly available

information, including press releases and management reports. As argued by Healy and

Palepu (2000), studies based on self-constructed measures of voluntary disclosure are subject

to a number of limitations. They are difficult to replicate due to the fact that the proxies are

subjective and depend on an author’s judgment, and they might not capture the full scope of

available information given that they are based on annual reports for the most part.

In this study we use a binary measure as a proxy for disclosure level by ADRs versus GDRs

rather than a continuous variable. The proxy is based on mandatory disclosure requirements

with little degree of the author’s subjectivity involved. In addition, there is a cost-benefit

trade-off of using a continuous disclosure measure versus the binary proxy in the present

study. It would require a lot of effort to develop a detailed continuous scaled for ADRs and

GDRs, while it is unclear whether there would be any benefits due to noise and the low

probability of a strict linear continuous relationship between disclosure and the cost of capital.

Instead, we use a binary measure that is simple, objective and potentially more powerful.

15

We classify ADRs and GDRs in accordance with subjective binary measure proxying for

overall Degree of Disclosure (final column of Table 2). Based on the accounting

reconciliation requirements, quantity of disclosed information and the reporting frequency

summarized in Table 2, the degree of disclosure is high for level III capital raising ADRs, is

medium for Level II and III GDRs and is medium-to-high for level II ADRs16. Overall, the

quality of the disclosed information is higher for ADRs compared to GDRs due to more

rigorous disclosure requirements put in place by the SEC compared to those of UKLA. The

quantity of the disclosed information should be higher for ADRs, too, given the higher

reporting frequency and the fact that GDRs are exempt from preparing a number of

statements and forms ADRs must submit. For instance, GDR-listed firms do not have to

include the forecast information in the prospectus and in later reports, don’t have to prepare

the working capital statement, do not file pro-forma financial statements in case of significant

changes in business, etc. In addition, their interim financials do not have to be audited. To

summarize, the anticipated improvements in the information environment of cross-listed firms

are higher for ADRs, compared to GDRs. The argument is further developed in Section 3.

3. HYPOTHESES DEVELOPMENT

3.1. Related Research

While a firm’s cost of capital is crucial to its decisions, there is still no consensus in the

theoretical and empirical literature as to whether information risk is priced. A number of

theoretical studies provide support for the view that firms’ information environment affect

expected returns. That is, firm-specific information is a priced factor. Economic theory

suggests that there are two channels through which information risk can affect expected

returns (cost of capital) – the diversification and the adverse selection path. The first stream of

research focuses on the incomplete information argument (Merton 1987) and the second

stream builds on the asymmetric information explanation (Easley and O’Hara 2004).

The investor recognition explanation in the study by Merton (1987) represents the first stream

of related research. Merton examined how stocks are priced in equilibrium when the

information about existing stocks is incomplete, i.e. investors are unaware about existence of

16 The classification is in line with that of Bank of New York Mellon (2008). One point to make here is that the presented disclosure requirements that are in place at cross-listing destinations should be treated as minimum mandatory disclosure requirements, as even under mandatory reporting regime some firms might choose to disclose more information voluntarily.

16

some stocks. He argues that incomplete information results in the under-diversification

problem. As a result, some firms will be recognized by relatively few investors and will

experience lower demand for their securities. Such firms should offer compensation to other

investors in the form of higher returns and will have higher cost of capital as a result.

More recently Easley and O’Hara (2004) developed a model showing that firms with higher

proportion of private versus public information have higher expected returns. They argue that

informed investors are better able to change their portfolios when the new information

becomes available. Uninformed investors end up holding more stocks with bad news, for

which they require compensation. The information risk they face cannot be diversified away

and is therefore priced. Overall, the difference in composition of information, public versus

private, should affect cost of capital. Other studies have also showed a theoretical link

between firms’ information environment and cost of equity capital but used a different

approach, e.g. Leuz and Verrecchia (2004).

The theoretical predictions on the positive association between information risk and cost of

capital have been empirically tested using different characteristics for firm-specific proxies

for information environment. Using the level of voluntary disclosure by firms as a proxy for

information environment, Botosan and Plumlee (2002) documented negative association

between the level of disclosure and cost of capital. Francis et al. (2004) used seven attributes

of earnings that they believed were a premier-source of firm-specific information and reached

a similar conclusion. The findings of Francis et al. (2005) who focused on the accrual quality

and Barth and Landsman (2003) who used value relevance as firm-specific information

attributes are in line with the predictions of Easley and O’Hara (2004), too. Finally,

Bhattacharya et al. (2003) and Francis et al. (2005) provided evidence on the negative

association between country-level measures of disclosure and cost of equity capital of firms

domiciled outside the US.

A number of theoretical and empirical studies found only partial support to the predicted

positive association between information risk and cost of capital. Lambert et al. (2007) built a

model that is consistent with the Capital Asset Pricing Model (CAPM) and includes multiple

securities whose cash flows are correlated. They demonstrated that the information risk can

affect required returns directly through the market participants’ assessment of the covariance

of firms’ cash flows with those of the market, and indirectly through firms’ decisions.

17

Accordingly, information risk affects firms’ beta and not the required returns, and if the beta

is measured with error, the information risk might appear to be a priced factor. They extended

their analysis to a model with multiple securities and demonstrated that as the number of

market participants (investors) increases, the information risk is more likely to be diversified

away.

The more recent study by Hughes, Liu and Liu (2007) builds on Easley and O’Hara (2004)

and shows that in a large economy model with the asymmetric information, the risk premium

is determined by the market betas and factor risk premiums. After controlling for beta in the

cross-section, information asymmetry does not affect required returns. To summarize, the

findings of the theoretical information risk studies, with some exception, provide support to

the positive association between the information risk and the cost of capital.

3.2. Testable predictions

The review of the theoretical and empirical literature on information risk suggests that

investors require higher rates of return when information is incomplete (investor recognition

hypothesis, Merton 1987) or is asymmetric (adverse selection problem, Easley and O’Hara

2004).

Easley and O’Hara argue that for two stocks that are otherwise identical, the stock with a

higher proportion of private and less public information will have larger expected returns.

This occurs when uninformed investors are unable to infer information from prices and treat

stocks with greater proportion of private information as riskier. These investors, however, are

still better off holding stocks with little public information rather than holding no stocks at all

(Easley and O’Hara 2004, Proposition 6). In this case information structure of each individual

stock will define how it is priced in equilibrium. The authors show that converting private

information into public will decrease expected returns, as uninformed investors have a better

change to invest in “good” stocks when information environment improves.

The mechanisms through which companies can increase the proportion of public versus

private information is by increasing the quantity and quality of the public (accounting)

information through enhanced disclosure or, alternatively, by improving properties of

analysts’ forecasts such as following and accuracy (Easley and O’Hara 2004). Each path will

result in increase in proportion of public versus private information. The shift will lead to the

18

decline in cost of capital, as predicted by the model. The argument is directly applicable to

our first prediction.

When firms choose to cross-list, the quantity and quality of publicly available information

substantially increases. Consistent with Easley and O’Hara (2004), two significant sources of

improvement in information environment for cross-listed firms are public (accounting)

disclosure and analysts’ forecasts (accuracy and following). The increase in the first source,

public (accounting) disclosure, is due the following.

Upon cross-listing both ADRs and GDRs become subject to more rigorous reporting

compared to that on their domestic markets. They have to report more frequently and must

disclose additional information by filing a number of forms. This additionally reported

information must be disclosed regardless of its content and despite the fact that omitting it

may be a preferred strategy. This suggests increase in quantity of disclosed information. Next,

ADRs and GDRs must prepare financial reports in accordance with US GAAP and IAS/IFRS,

respectively, and the audit of their reports must be conducted in accordance with the

International Standards on Auditing (ISA). Prior studies found that the US GAAP and IFRS

are overall more informative and comprehensive than other local GAAPs (Leuz and

Verrecchia 2000; Ashbaugh 2001). The superior value-relevance and timeliness of the US

GAAP and IFRS compared to other national accounting standards is also well documented in

the literature (Bath et al. 2008). Based on the findings of the prior literature, the quality of

disclosed information for ADRs and GDRs is expected to improve after cross-listing, too.

As for the second component of information environment, analysts’ forecasts, the theory

suggests several paths through which the properties of analysts’ forecasts are expected to

improve as a result of improved disclosure. Hope (2003) argues that better enforcement of

accounting disclosure standards makes firms’ reporting more transparent and less uncertain

for analysts encouraging them to follow firms more actively. The increase in analysts’

following in this case is a result of the improved disclosure and lower cost of following a firm

(Lang et al. 2003). Provided that after cross-listing ADRs and GDRs become subject to

stringent disclosure with better enforcement mechanism of the SEC and UKLA, respectively,

this path suggests that analysts’ following should improve for both ADRs and GDRs.

Alternatively, analysts might follow firms more actively in response to increased investors’

demand. When the information asymmetry declines as a result of improved disclosure,

19

investors’ transaction costs decline and their demand for securities rises (Amihud and

Mendelson 1986). Positive changes in analysts’ following for ADRs and GDRs through this

avenue are plausible, too, provided that the firms disclose more and better quality information

when offering their securities via cross-listing.

Improvement in accuracy of analysts’ forecasts is expected to occur due to improved

communication of information by firms as a result of improved disclosure. Hope (2003)

suggests that annual reports help analysts understand firms’ reporting practices at a broad

level, while notes to the reports with additionally disclosed information assist them in

assessing firms’ future prospective in order to make forecasts more accurately. Therefore

better quality disclosure is expected to be positively associated with accuracy of forecasts.

Alternatively, the increased competition among analysts when the demand from investors

rises should encourage them to produce better quality forecasts due to the fact that each

additional analyst reduces others’ marker share (Lys and Soo 1995). Each theoretical path is

relevant to the discussion on ADRs and GDRs suggesting that accuracy of forecasts should

improve for them.

The empirical findings do not strongly support the theoretical predictions on the positive

changes in analysts’ following and accuracy. On one hand, it is well documented that overall

analysts contribute to a firm’s information environment either through increased following,

improved accuracy of forecasts, or both. For example, Hope (2003) examined the association

between the firm-level disclosure, level of enforcement, analysts’ following and accuracy for

firms domiciled in 22 countries. He documented positive association between disclosure and

analysts’ following and between the level of enforcement of accounting standards and

accuracy of analysts’ forecasts. Findings of Lang et al. (2003) who examined changes in

information environment for ADR-listed firms are in line with those of Hope (2003).

The findings of the study by Lang and Lundholm (1996) and a more recent study by Abdallah

(2008) provide conflicting evidence on the changes in properties of analysts’ forecasts as a

result of better disclosure. Lang and Lundholm (1996) showed that for the sample of US firms

the ratings of annual report disclosure as measured by the Association for Investment

Management and Research (AIMR) are not associated with forecast accuracy and analyst

following. The predicted positive association is only observed when various information

20

sources including annual reports, media coverage and investor relations, are aggregated to

form the total public information score. In cross-listing settings Abdallah (2008) documented

that the improvement in analysts’ following is in fact more pronounced for firms that cross-

list through programs with lower disclosure requirement, such as private placement programs

traded through PORTAL, and that there is no improvement in quality of analysts’ forecasts

(accuracy) observed for ADRs listed on both regulated and unregulated markets in the US and

the UK. The results of the study by Abdallah are robust to various partitioning of firms and

provide strong evidence that analysts’ following and accuracy may experience changes in

different direction as a result of cross-listing and do not necessarily improve when disclosure

improves.

The discussion suggests that information environment of firms that cross-list as ADRs or

GDRs is expected to improve, either through changes in only one component of the

information environment (public disclosure) or both (public disclosure and analysts’

forecasts). Based on the above, our first hypothesis is stated as follows:

H1: Ceteris paribus, the cost of capital of ADR-listed firms and GDR-listed firms declines in

the post-listing period.

The requirements of the SEC for ADR-listed firms with regard to the extent of disclosure are

higher than those prescribed by UKLA for GDR-listed firms in a number of aspects. The

quality of disclosed information is expected to be higher for ADRs because GDRs are exempt

from a number of reporting requirements both when preparing a prospectus and as ongoing

obligations. The quantity of the disclosed information is expected to be higher for ADRs, too.

First, the reporting frequency is lower for GDRs, as they are required to publish interim and

annual reports, while ADR-listed firms report quarterly and annually. Second, the number of

forms and reports that GDRs have to submit is not as high as for ADRs. For example, GDRs

are exempt from preparing the working capital statement and do not have to prepare

additional statements when changes in business occur, etc. Therefore based on the first

component of information environment – public disclosure - alone, the magnitude of changes

in cost of capital is expected to be greater for ADRs compared to GDRs17.

17 The argument is built on the post-listing disclosure requirements in the US and UK markets. One possibility is that the origins of cross-listed firms and their disclosure level on a domestic market prior to cross-listing should also be considered when changes in public disclosure are assessed. This would require estimating the pre-listing

21

As for the second component of information environment, properties of analysts’ forecasts, it

is unclear whether the changes in following and accuracy should be more pronounced for

ADRs or GDRs. On one hand, greater positive changes in the quantity and quality of

disclosed information shall manifest in greater analysts’ following due to lower cost of

processing information, as well as in the improved accuracy of analysts’ forecasts for ADRs

rather than GDRs (Lang et al. 2003). On the other hand, GDRs attract global investors and are

aimed at a more diverse pool of market participants and therefore the increase in analysts’

following should be more pronounced for them and not for ADRs, as analysts are expected to

respond to a higher demand from investors by increased following (Merton 1987). Greater

competition and following, in turn, can lead to greater accuracy of analysts’ forecasts for

GDRs, as each additional following of a company by analysts reduces others’ market share

(Lys and Soo, 1995).

Based on the above discussion, while it is intuitive that the first component of firms’

information environment - public disclosure – should experience more positive changes in

case of ADRs, it is not entirely clear how the changes in properties of analysts’ forecasts

should differ between ADRs and GDRs. Therefore the differential impact of cross-listing via

ADRs versus GDRs on cost of capital is ultimately an empirical question. On the assumption

that public disclosure component is a greater contributor to the information risk reduction

than properties of analysts’ forecasts, we assume:

H2: Ceteris paribus, the magnitude of decrease in the cost of capital in the pre-post listing

period is greater for ADR-listed firms than for GDR-listed firms.

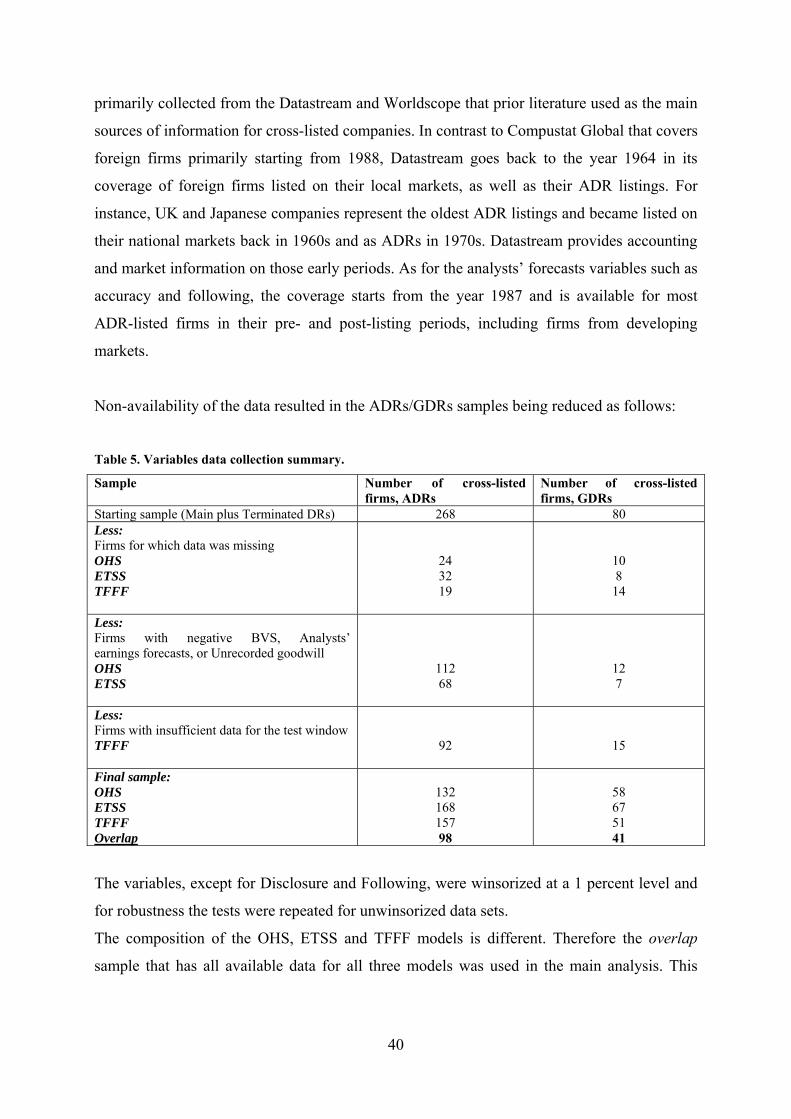

4. RESEARCH DESIGN AND METHODOLOGY

4.1. Cost of equity capital estimation – overview of existing approaches

Prior literature employed two distinct approaches to estimation of the cost of equity capital:

the approach based on calculating implied cost of capital and the approach based on realized

disclosure level for each cross-listed firm, which is hardly possible because it suggests analysing financial report of each firm and self-constructing a disclosure index. Instead, this study follows the argument of prior cross-listing works that suggest focusing on the post-listing requirements that are at place at cross-listing destinations because in assessing changes in risk associated with cross-listing investors heavily rely on those requirements.

22

returns. Realized returns as a proxy for cost of capital have been extensively used in prior

studies in various settings, including cross-listing, and represent a more traditional

methodology than the implied cost of capital models (Miller 1999; Errunza and Miller 2000).

Realized returns require large sample sizes and are a noisy measure of cost of capital, as

information surprises do not always cancel over time and may have substantial variances on

the individual stock level (Botosan and Plumlee 2005). They are, however, not subject to the

measurement errors due to bias in analysts’ forecasts, for instance, and have fewer restrictions

on variables than implied cost of capital models are subject to (Francis et al. 2004).

The models that are based on realized returns employed by prior empirical studies are the

Capital Asset Pricing Model (CAPM) and the Three Factor Fama and French model (TFFF).

The present study employs the three-factor model of Fama and French (TFFF) to examine

changes in cross-listed firms’ returns after cross-listing. We do not use a portfolio-based

approach and instead run a pooled regression based on a 24-month window prior to and after

cross-listing for each firm, a [48 X N] design, where N is the number of cross-listed firms in

the ADRs/GDRs sub samples. The present study employs the univariate, the CAPM and the

three-factor Fama and French (TFFF) models as the primary asset-pricing tests. The general

form of the estimated regressions is:

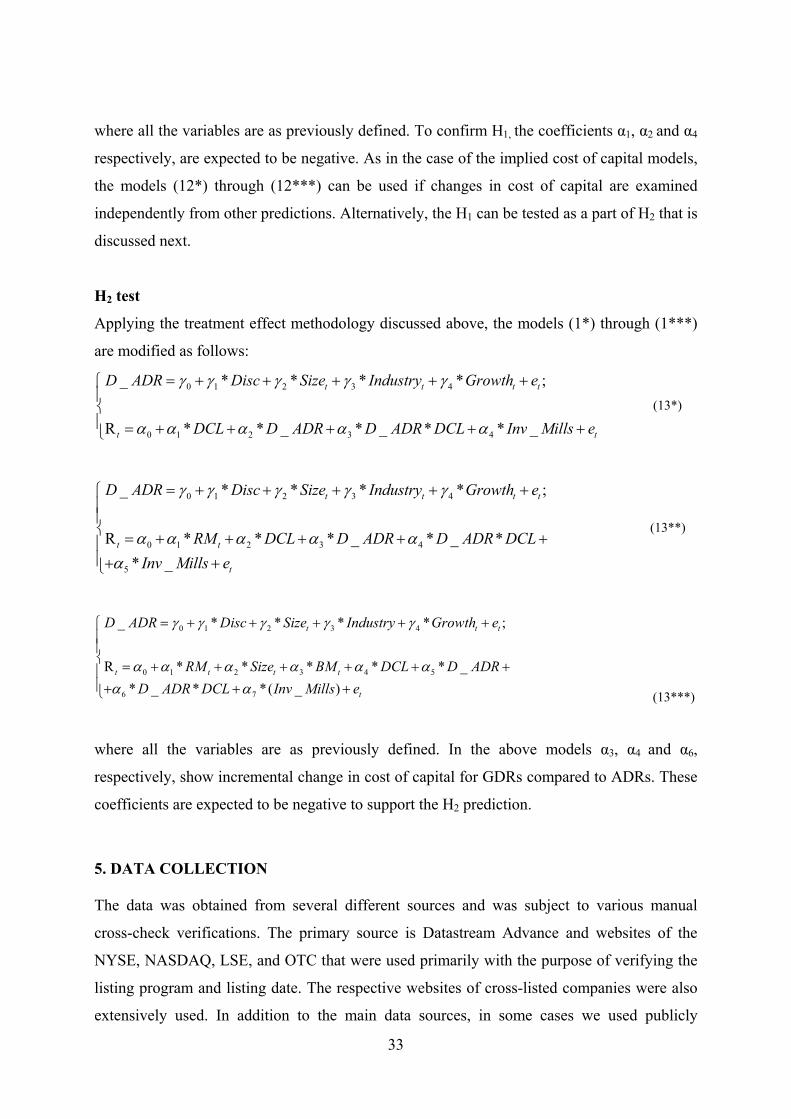

tt eR 0 (1*)

ttt eRMR *10 (1**)

ttttt eBMSizeRMR 3210 ** (1***)

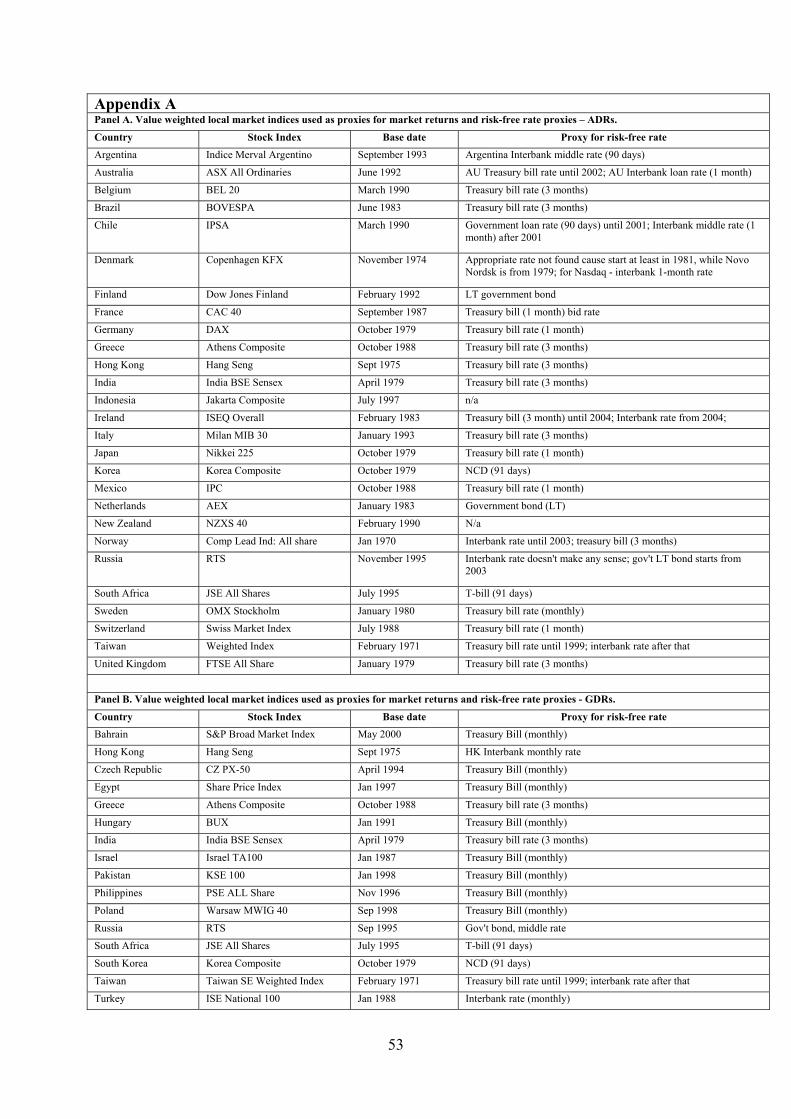

where Rt are monthly-based realized returns measured 24 months prior to and 24 months after

a listing month for each firm. RMt are the excess monthly market returns measured as the

difference between market returns and a proxy for a country-specific risk-free rate as at the

end of each month. Local market indices represent value-weighted indices for each country

for a certain period18. Following prior literature, we used short-term governmental bonds /

treasury bills as a proxy for a risk-free rate. Where this was unavailable we used a short-term

interbank rate summarized in Appendix A. If neither was available, cross-listed firms were

18 Given the fact that there are a large number of various market indices available in Datastream for each country, I followed Datastream methodology and collected information on the local market indices that are used by Datastream research team for calculation of the market beta for different countries.

23

excluded from the sample19. Sizet is a market value of equity, and BMt is a book-to-market

value of equity measured at the end of each period20.

The implied cost of capital methodology provides an alternative to the realized returns tests

and is relatively new. Those models suggest reverse-engineering valuation models in order to

obtain the cost of capital estimates. They are based on the dividend capitalization model

(Botosan 1997), residual income valuation model (O’Hanlon and Steele 2000; Claus and

Thomas 2001; ETSS 2002), and abnormal growth in earnings model (Gode and Mohanram

2003). There were attempts to validate those measures of cost of capital by [1] examining

correlation of the cost of capital with the ex-ante firm-specific risk proxies such as beta,

leverage, firm size, etc. (Gode and Mohanran 2003) and by [2] examining correlation between

the cost of capital and realized returns (Easton and Monahan 2005). The conclusions of those

studies are that the two approaches to estimation of cost of equity capital do not produce

consistent results (Easton 2006). Among the potential reasons for inconsistency are bias in

analysts’ forecasts used in the models, noise in realized returns due to information surprises,

and others21. Given the imperfection of existing approaches to estimate cost of capital, the

study adopts both methods.

Implied cost of capital models provide advantage over realized returns tests in that they allow

explicitly separating cash flows (growth) from the cost of capital effects (Hail and Leuz

2009). Therefore accurate estimation of the growth rate is essential, yet studies have used

different approaches to estimating growth beyond the forecast horizon. Gebhardt, Lee and

Swaminathan (GLS 2001) and Claus and Thomas (CT 2001), for instance, make assumptions

19 The analysis resulted in excluding Russia from the CAPM and TFFF estimation due to the fact that the first governmental bonds were originated in 2003 and the only available interest rate for 1990s – 2003 was the interbank short-term lending rate. However, the rate was changing in accordance with no particular trend and for some months it exceeded 100% due to the poor economic condition of the country and hyper inflation. Next, Argentina had only interbank lending rate available which was used as a risk-free proxy for all the Argentinean firms in the sample. The Australian treasury bills rate was truncated in 2002 and the only available rate after that period was a one-month interbank loan rate. The correlation between the two rates in the pre-2002 period was 88% and it was decided to use the interbank rate as a risk-free proxy for the 2002-2008 periods. Finally, Denmark which was represented by only 1 firm, was excluded from the sample due to the fact there were no interest rates available prior to 1981, while its Novo Nordisk was listed in 1979. 20 A 24-month pre- and post window is used to ensure a higher statistical power. For robustness, a shorter 12-month window is used as an additional analysis. In the main analysis the pooled regression is used, while for robustness a firm-specific test is performed. 21 The more recent stream of literature has focused on improving the accounting-based valuation models by, for instance, explicitly correcting for the analysts’ bias (Guy et al. 2005, Gode and Mohanran 2008).However, the approach is yet to be validated. Correcting for bias in analysts’ forecasts is not of interest for this study.

24

about the growth rate22 before proceeding to cost of capital estimation, while O’Hanlon and

Steele (OHS 2000) and ETSS (2002) estimate a growth rate and a cost of capital

simultaneously as implied by data. As demonstrated by Easton (2006), cost of capital

estimates are sensitive to assumptions about a growth rate23. The estimates derived from the

OHS and ETSS models are viewed as superior to those of GLS and CT due to the fact that,

first, they allow avoiding making an assumption about the growth rate that may lead to

incorrect inferences; second, they allow estimating cost of capital for a portfolio of stocks that

is required by the research design of the study.

The model of ETSS (2002) is a regression-based model that allows simultaneous estimation

of the implied cost of capital and the growth rate implied by the market prices, book values

and earnings forecast data. However, as pointed out by Easton and Sommers (2007), the

methodology of obtaining the implied cost of capital based on the analysts’ forecasts has its

limitations. The estimation requires the firms to have positive earnings forecasts, several years

of consecutive data and is based on the assumption that analysts’ forecasts are good proxies

for market expectations. The requirements put substantial limitations on the size of the ADRs

and GDRs samples that are small anyway.

The model by O’Hanlon and Steele (2000) is similar to that of ETSS (2002) and also suggests

simultaneous estimation of the implied rate of return and a growth rate; however their model

is based on reported rather than forecasted earnings. This approach avoids the forecasts bias

problem discussed above, while making no assumptions about the growth rate in abnormal

earnings. We therefore adopt the model derived by O’Hanlon and Steele (2000) as the main

model of the study and further discuss the details of the estimation technique. The ETSS

model is used as the second model to validate the findings. The two models are discussed

separately.

22 GLS approach is to forecast earnings explicitly for the next three years and to forecast earnings beyond that horizon implicitly, that is by mean reverting the period t+3 ROE to the median industry ROE. Easton (2009) points out (and provides an examples of) to why mean-reverting to the industry median assumption is not feasible. For example, in the IT sector the median numbers can be driven by the big firms such as Microsoft and are not representative of the whole population of IT companies. 23 Easton (2006) performed a comparison of estimates of the implied rate of return obtained from the models used in the several mentioned studies and came up with the conclusion that the assumption about the growth rate beyond the forecasted horizon is critical to the analysis of cost of capital and may lead to incorrect inferences, as making explicit assumptions about the growth rate suggests making implicit assumptions about the required rate of return itself. He suggests that the simultaneous estimation technique used by ETSS (2002) is superior to other studies.

25

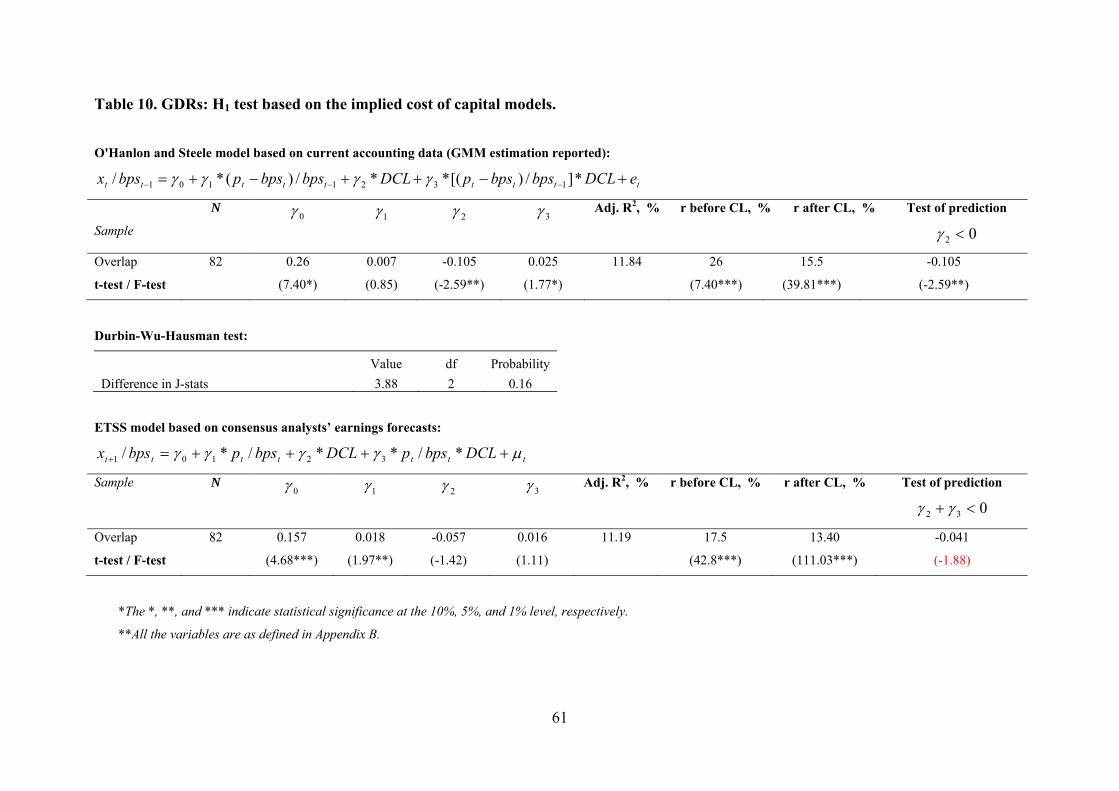

O’Hanlon and Steele (2000)

The derivation of the model by O’Hanlon and Steele is based on the linear valuation equation

of Ohlson (1995) that allows presenting an unrecorded goodwill (URG), as measured by the

difference between a price (pt) and a book value of equity (bpst), as a function of accounting

earnings (xt) and a prior period book value of equity (bpst-1)24:

1 2 1t t t t tp bps x bps e (2)

where the book value of equity and the earnings are measured as at fiscal year end and the

price is measured around the earnings announcement day. Since the announcement days for

ADRs and GDRs (especially prior to cross-listing when companies report under their local

GAAP and to local investors) are not known, we use the prices as at fiscal year end under the

assumption that all available information is incorporated in those prices. Besides, given the

fact that after cross-listing firms report both to local investors using local GAAP, which

usually occurs earlier than reporting to foreign investors using IFRS/US GAAP, it is unclear

which earnings announcement dates should be used to obtain the price, as local earnings

announcement (and other announcements made on a local market) may introduce noise and

the reaction to the release of IFRS (for GDRs) and US GAAP (for ADRs) earnings will be

biased as a result.

Next, deflation of the equation (2) by the opening book value of equity, bpst-1, leads to the

following regression:

1 2 1 1/ *( ) /t t t t tURG bps x bps e (3)

where the estimated cost of equity capital, r, is measured as the negative ratio of the intercept

and the slope: 12 / r . The authors point out that the ratio of the two variables measured

with error will depart from normality and its moments will not exist (Geary 1930). Therefore

the model (3) would have to be rearranged so that the cost of capital estimation is based on a

parameter, not a ratio, estimate. They suggest rearranging both sides of the equation (3):

1 1 2 1/ * /t t t t tx bps URG bps e (4)

In the above “reverse” model (4) the cost of capital is no longer a ratio of two variables and is

just an intercept. The slope is equal to (1-g2), where g is the growth in abnormal earnings rate.

24 The derivation of the equation (2) is omitted here; please refer to O’Hanlon and Steele (2000) for details.

26

O’Hanlon and Steele (2000) and later Easton and Sommers (2007) use equation (4) for the

cost of capital estimation.

The suggested by O’Hanlon and Steele rearrangement in the final empirical model has some

practical estimation issues. The problem with estimating the “reverse” regression (4) is that it

is the case that the reversal suggested by O’Hanlon and Steele does not eliminate the

econometric problem completely but rather transforms it into a different form. After reversal,

in model (4) the URG becomes correlated with the error term and hence the coefficients based

on a simple OLS estimation may be biased. As such, there is an issue as to whether use a

“normal” regression (3) to estimate cost of capital, which would be more justified provided

that it is (3) and not (4) that is derived from the linear value relevant information equation of

Ohlson (1995), or to use the “reverse” regression (4) that was validated in prior studies.

There are two potential solutions to the problem, each representing a trade off. First, instead

of using the equation (4), we need to go back to the equation (3) and estimate it with a non-

linear restriction on the coefficients in the following form:

1 1 1 1/ * *( ) /t t t t tURG bps r x bps e (5)

Tthe properties of r in this case may be poor due to a small sample size of ADRs and GDRs.

Alternatively, as is done in the present study, we can use equation (4) that O’Hanlon and

Steele used as their final model after correcting for correlation between the independent

variable and the error term. The correction can be done by using the Generalized Methods of

Moments (GMM), for instance, which requires findings an instrumental variable that would

be correlated with the independent variable, URG, but uncorrelated with the error term.

Finding an instrumental variable (IV) represents a challenge for a researcher, and unless there

are successful IV “candidates” for which valid economic justifications exist, a simple OLS

model may be preferred (Larcker and Rusticus 2010). Using semi-endogenous instruments

that are weakly correlated with an error term would also make properties of estimated

coefficients poorer compared to a simple OLS estimation (Francis and Lennox 2008; Larcker

and Rusticus 2010). Therefore it is essential to test for the validity of the chosen instruments

when running the GMM estimation, as is done in the present study. For robustness, a simple

OLS estimation is performed.

27

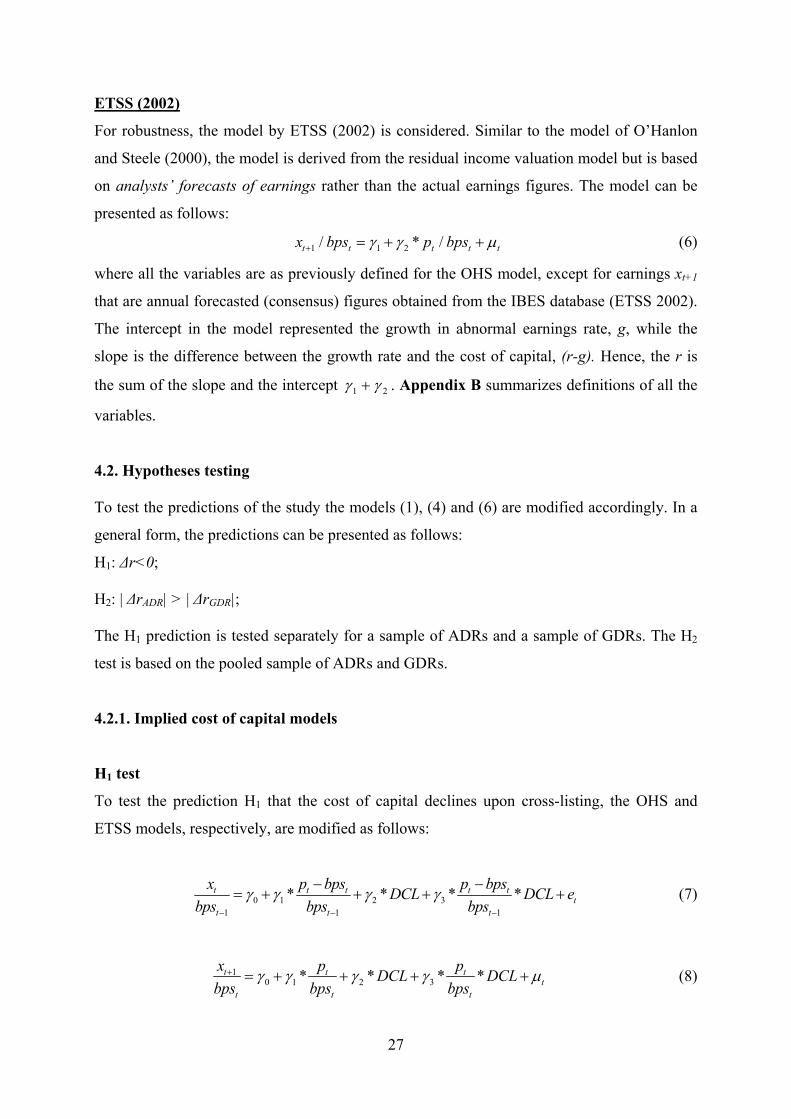

ETSS (2002)

For robustness, the model by ETSS (2002) is considered. Similar to the model of O’Hanlon

and Steele (2000), the model is derived from the residual income valuation model but is based

on analysts’ forecasts of earnings rather than the actual earnings figures. The model can be

presented as follows:

1 1 2/ * /t t t t tx bps p bps (6)

where all the variables are as previously defined for the OHS model, except for earnings xt+1

that are annual forecasted (consensus) figures obtained from the IBES database (ETSS 2002).

The intercept in the model represented the growth in abnormal earnings rate, g, while the

slope is the difference between the growth rate and the cost of capital, (r-g). Hence, the r is

the sum of the slope and the intercept 21 . Appendix B summarizes definitions of all the

variables.

4.2. Hypotheses testing

To test the predictions of the study the models (1), (4) and (6) are modified accordingly. In a

general form, the predictions can be presented as follows:

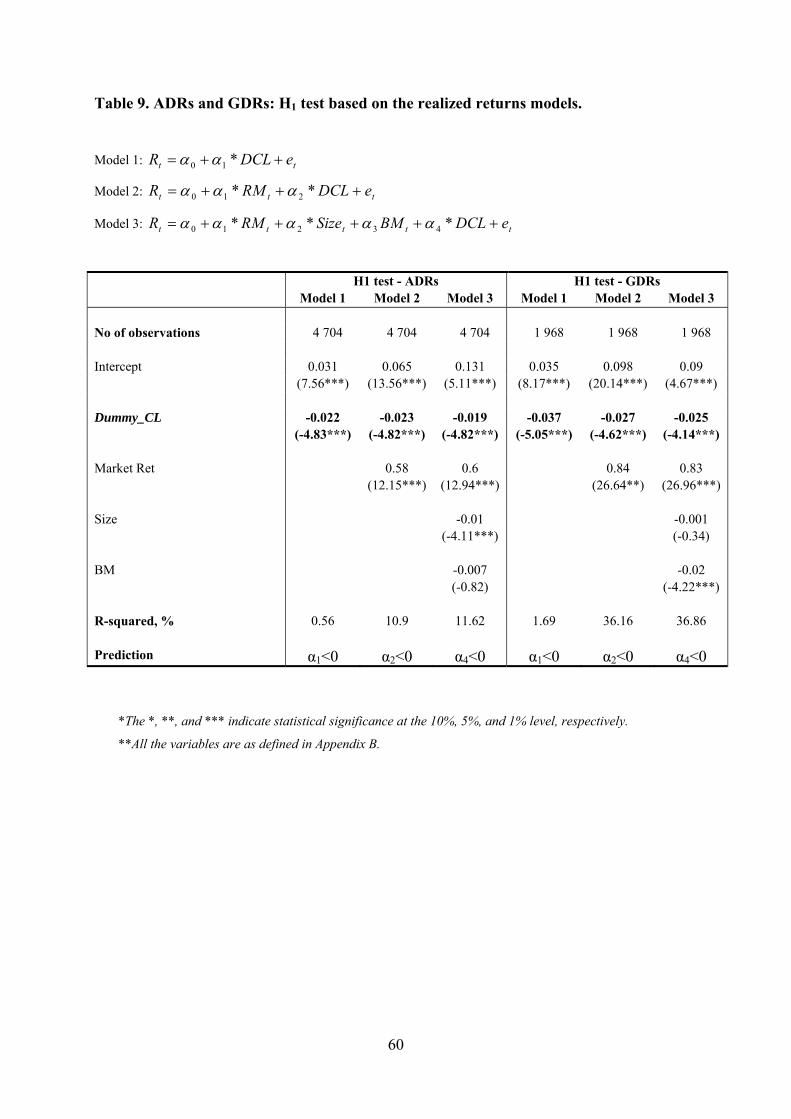

H1: Δr<0;

H2: | ΔrADR| > | ΔrGDR|;

The H1 prediction is tested separately for a sample of ADRs and a sample of GDRs. The H2

test is based on the pooled sample of ADRs and GDRs.

4.2.1. Implied cost of capital models

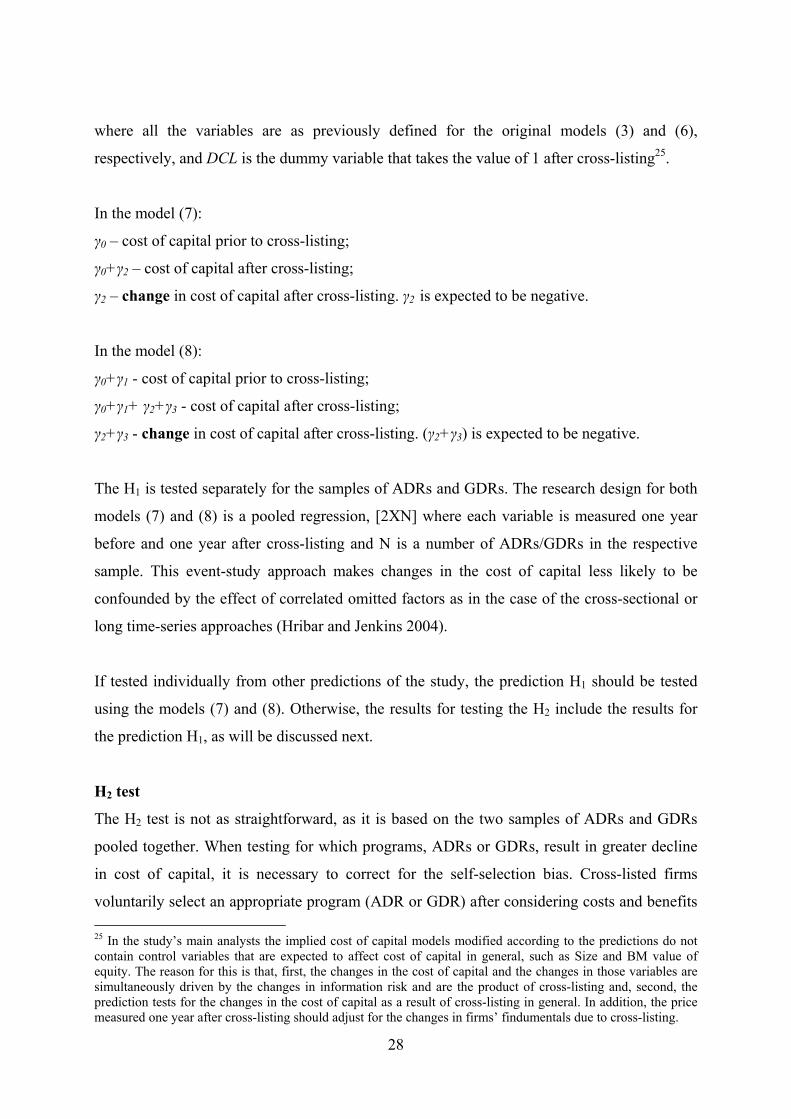

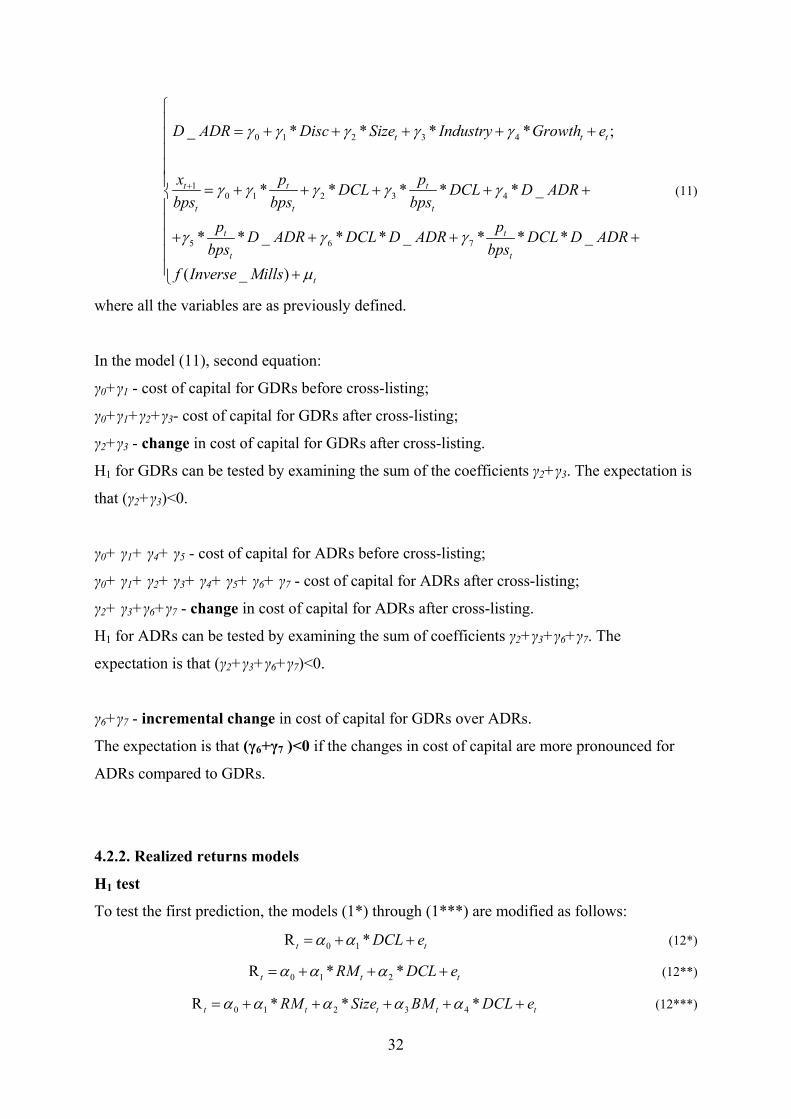

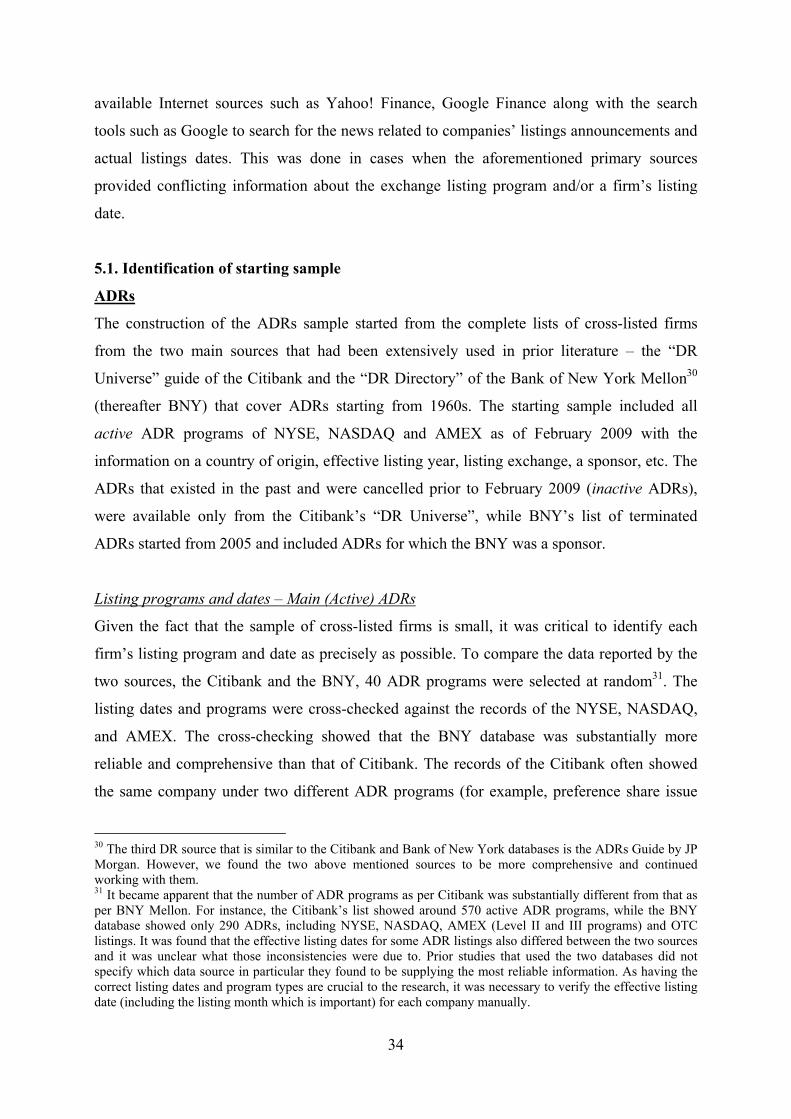

H1 test

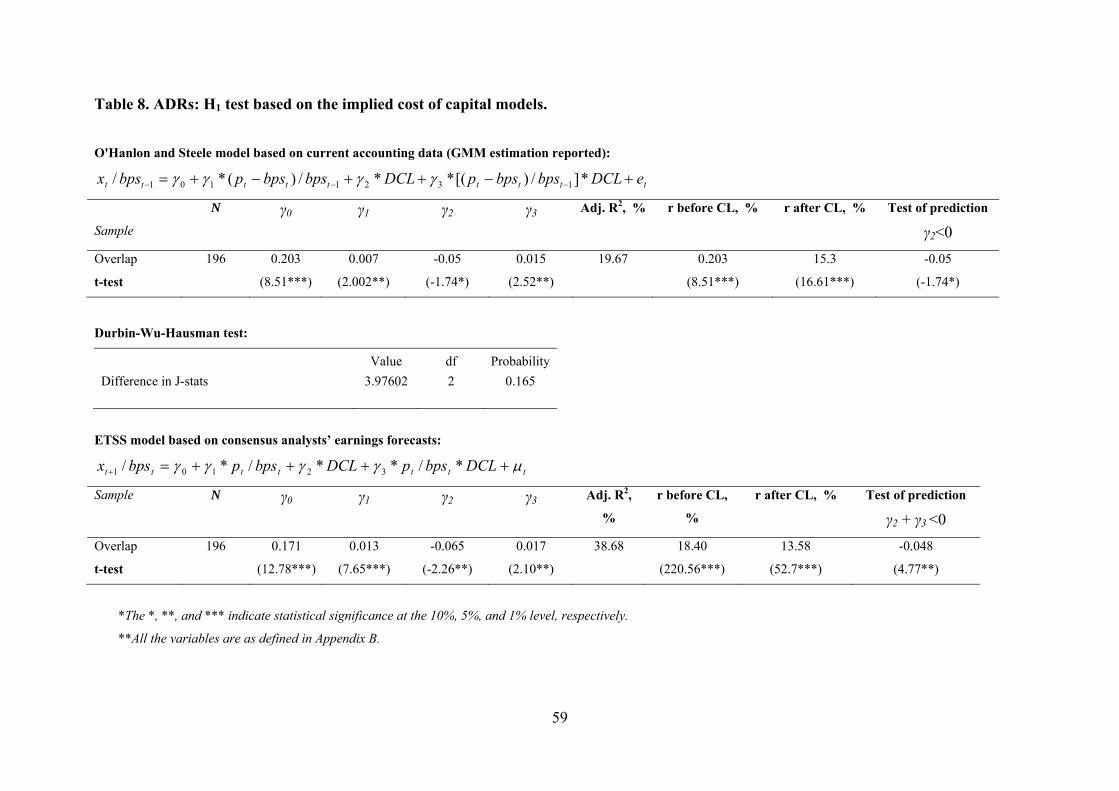

To test the prediction H1 that the cost of capital declines upon cross-listing, the OHS and

ETSS models, respectively, are modified as follows:

0 1 2 31 1 1

* * * *t t t t tt

t t t

x p bps p bpsDCL DCL e

bps bps bps

(7)

10 1 2 3* * * *t t t

tt t t

x p pDCL DCL

bps bps bps (8)

28

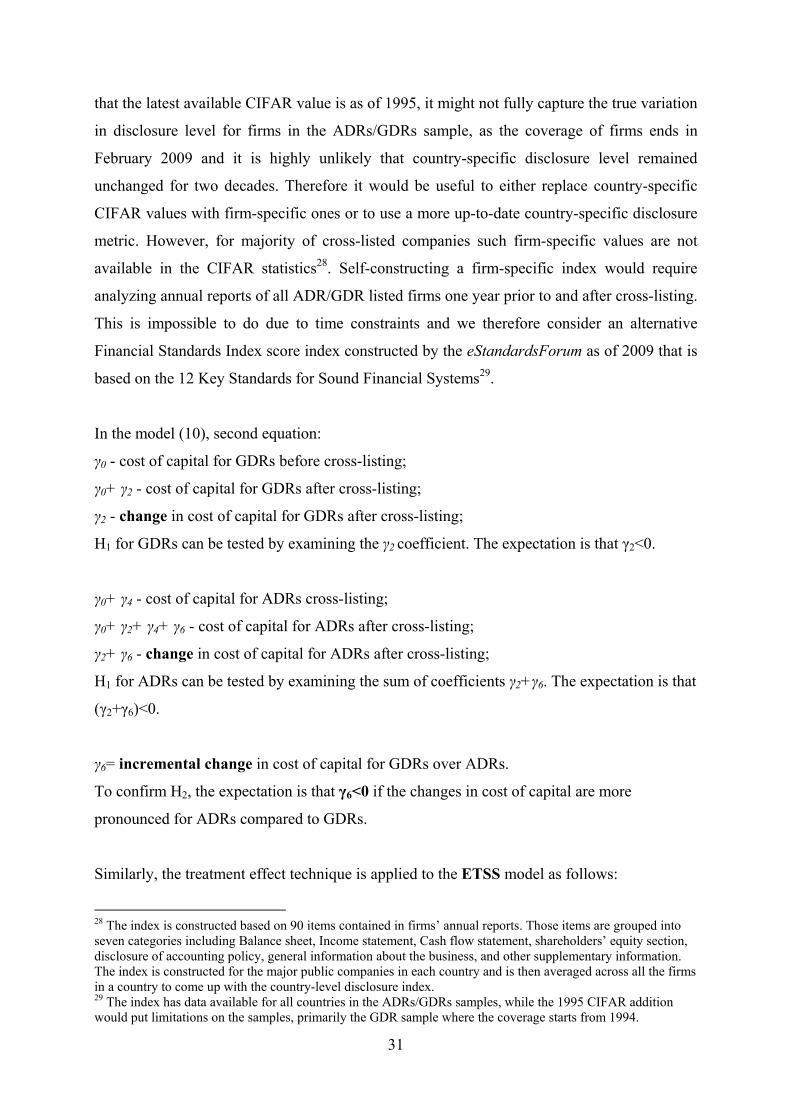

where all the variables are as previously defined for the original models (3) and (6),

respectively, and DCL is the dummy variable that takes the value of 1 after cross-listing25.

In the model (7):

γ0 – cost of capital prior to cross-listing;

γ0+γ2 – cost of capital after cross-listing;

γ2 – change in cost of capital after cross-listing. γ2 is expected to be negative.

In the model (8):

γ0+γ1 - cost of capital prior to cross-listing;

γ0+γ1+ γ2+γ3 - cost of capital after cross-listing;

γ2+γ3 - change in cost of capital after cross-listing. (γ2+γ3) is expected to be negative.

The H1 is tested separately for the samples of ADRs and GDRs. The research design for both

models (7) and (8) is a pooled regression, [2XN] where each variable is measured one year

before and one year after cross-listing and N is a number of ADRs/GDRs in the respective

sample. This event-study approach makes changes in the cost of capital less likely to be

confounded by the effect of correlated omitted factors as in the case of the cross-sectional or

long time-series approaches (Hribar and Jenkins 2004).

If tested individually from other predictions of the study, the prediction H1 should be tested

using the models (7) and (8). Otherwise, the results for testing the H2 include the results for

the prediction H1, as will be discussed next.

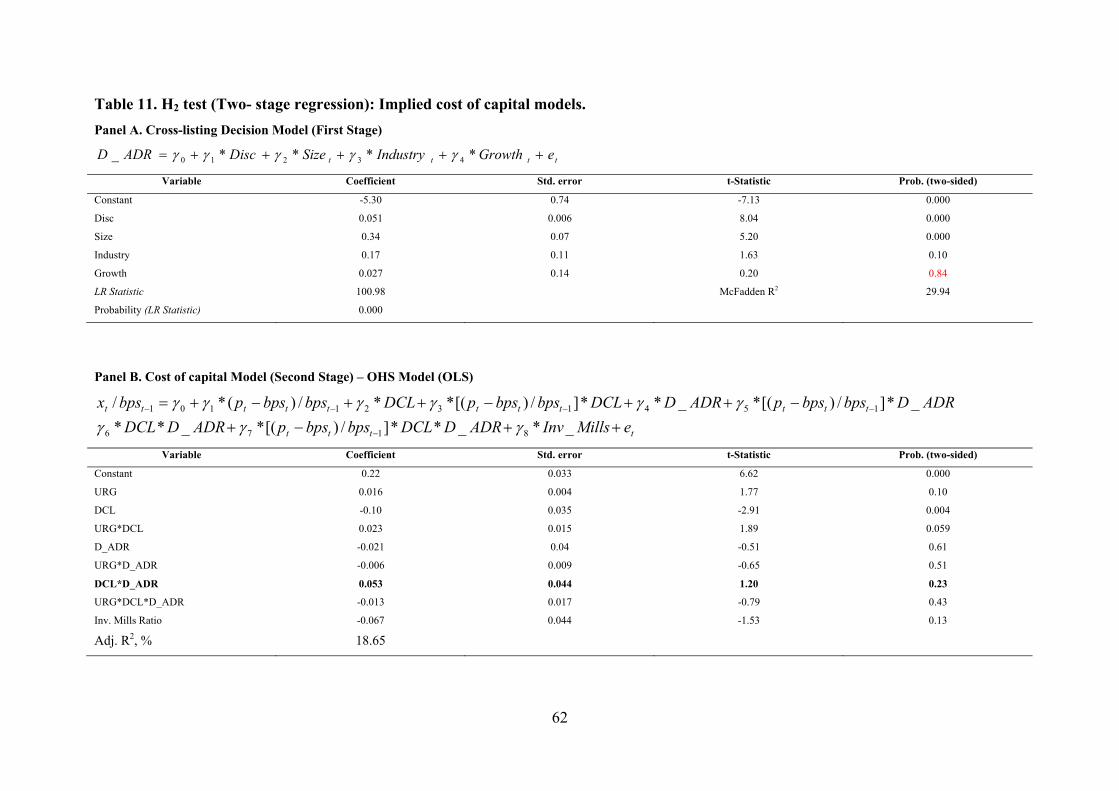

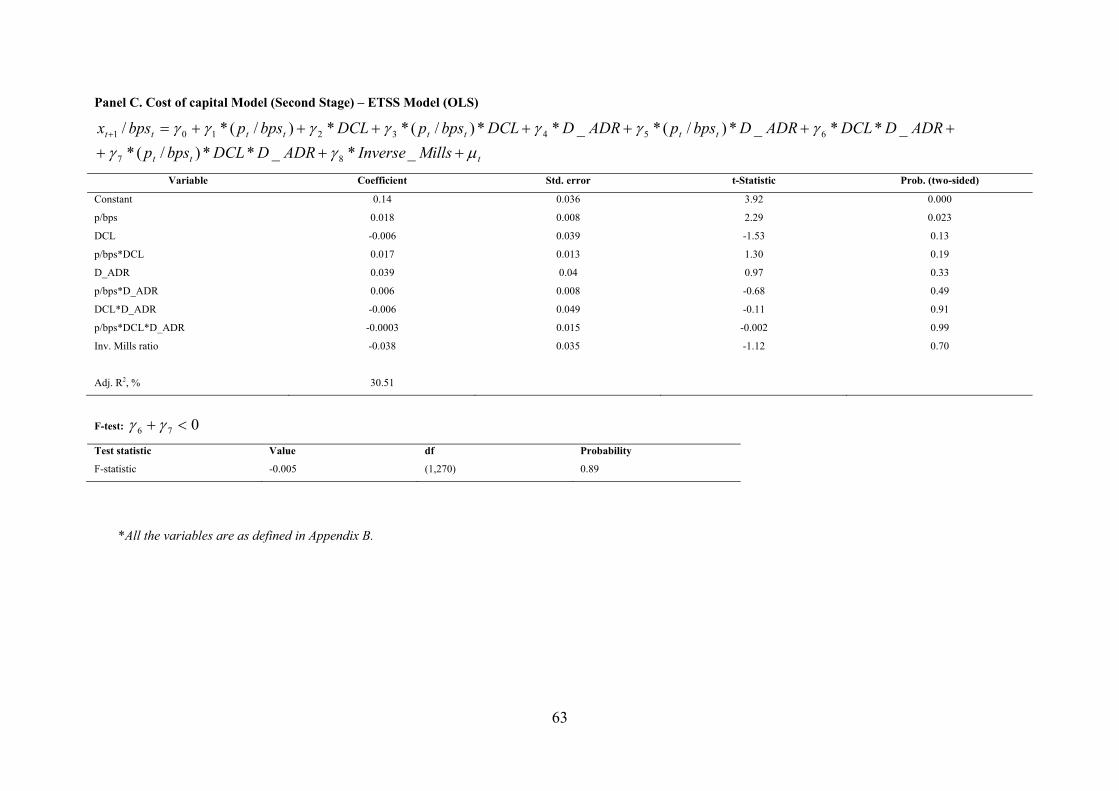

H2 test

The H2 test is not as straightforward, as it is based on the two samples of ADRs and GDRs

pooled together. When testing for which programs, ADRs or GDRs, result in greater decline

in cost of capital, it is necessary to correct for the self-selection bias. Cross-listed firms

voluntarily select an appropriate program (ADR or GDR) after considering costs and benefits

25 In the study’s main analysts the implied cost of capital models modified according to the predictions do not contain control variables that are expected to affect cost of capital in general, such as Size and BM value of equity. The reason for this is that, first, the changes in the cost of capital and the changes in those variables are simultaneously driven by the changes in information risk and are the product of cross-listing and, second, the prediction tests for the changes in the cost of capital as a result of cross-listing in general. In addition, the price measured one year after cross-listing should adjust for the changes in firms’ findumentals due to cross-listing.

29

of their decision. There are a number of characteristics that might drive firms’ decisions to list

as ADRs rather than GDRs. Prior literature identifies several of them. Size is an important

factor and larger firms with greater liquidity demand, for instance, may choose the US

destination rather than the UK (Bianconi and Tan 2008). The Disclosure level on a domestic

market may drive firms’ decision in favor of ADRs or GDRs, as additional disclosure is

costly and time-consuming, and as a result firms with poorer disclosure may choose GDRs to

minimize their costs (Francis et al. 2005). Next, companies may choose a cross-listing

destination based on where their industry peers list. An example would be the high-tech firms

concentrated on the NASDAQ. Finally, the business cycles are important, as firms with

higher growth may choose a destination that provides better realization for such growth

opportunities.

The above discussion suggests that standard OLS estimation where the differential changes in

cost of capital of ADRs versus GDRs are measured by the simple dummy variable will

produce biased results. To address the issue, we adopt an empirical approach used in prior

literature. The approach suggests the estimation of a “treatment effect” model that allows

controlling for the self-selection bias that ADR and GDR-listed firms may be subject to (see

Leuz and Verrecchia 2000; Bianconni and Tan 2008). The model requires estimation of the

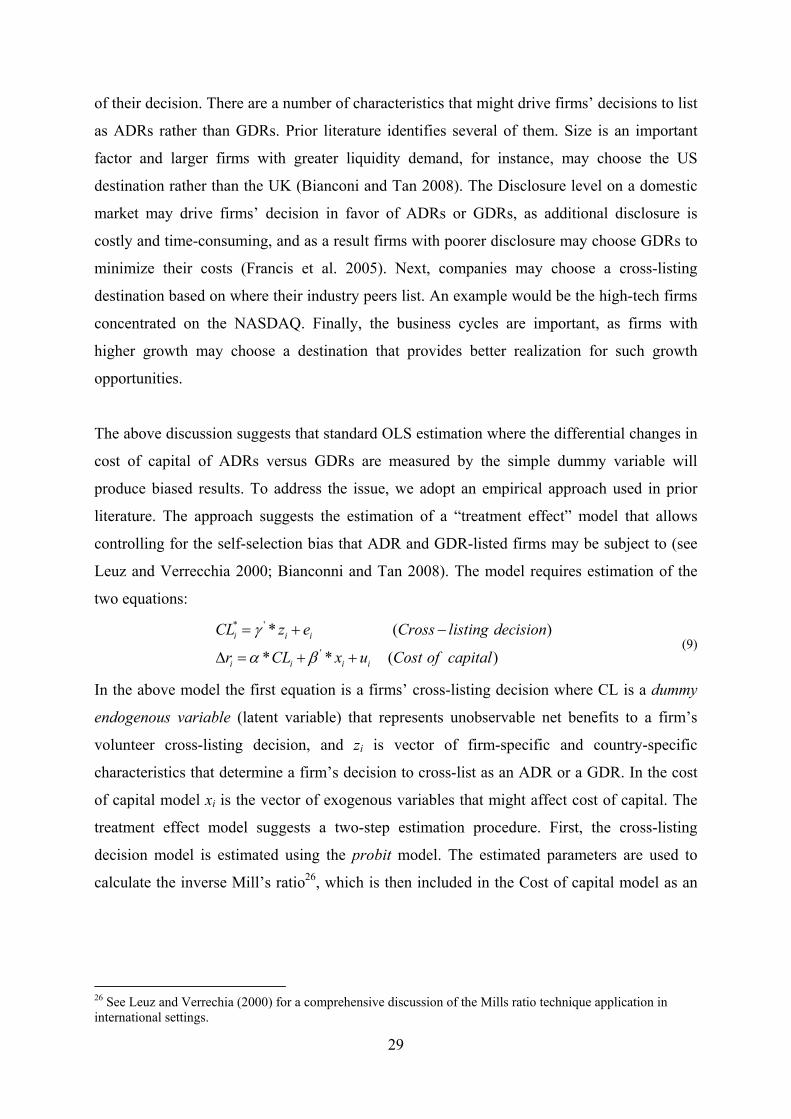

two equations:

* '

'

* ( )

* * ( )

i i i

i i i i

CL z e Cross listing decision

r CL x u Cost of capital

(9)

In the above model the first equation is a firms’ cross-listing decision where CL is a dummy

endogenous variable (latent variable) that represents unobservable net benefits to a firm’s

volunteer cross-listing decision, and zi is vector of firm-specific and country-specific

characteristics that determine a firm’s decision to cross-list as an ADR or a GDR. In the cost

of capital model xi is the vector of exogenous variables that might affect cost of capital. The

treatment effect model suggests a two-step estimation procedure. First, the cross-listing

decision model is estimated using the probit model. The estimated parameters are used to

calculate the inverse Mill’s ratio26, which is then included in the Cost of capital model as an

26 See Leuz and Verrechia (2000) for a comprehensive discussion of the Mills ratio technique application in international settings.

30

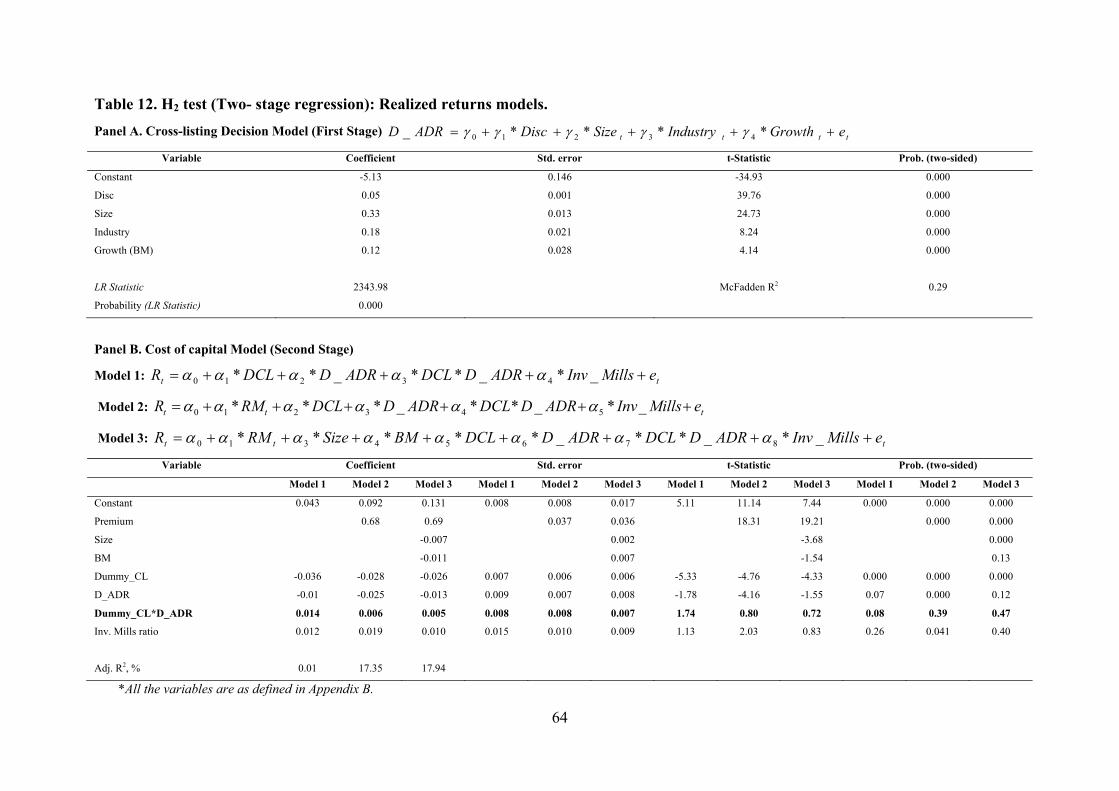

additional explanatory variable (see Maddala 1983). The above model for testing H2 based on

the original OHS model becomes a system of two equations27:

0 1 2 3 4

0 1 2 3 41 1 1

5 6 71 1

_ * * * * ;

* * * * * _

* * _ * * _ * * * _

( _ )

t t t

t t t t t

t t t

t t t t

t t