Embed Size (px)

Citation preview

ISSN: 2289-4519 Page 21

International Journal of Accounting & Business Management

www.ftms.edu.my/journals/index.php/journals/ijabm

Vol. 6 (No.1), April, 2018

ISSN: 2289-4519 DOI:10.24924/ijabm/2018.04/v6.iss1.21.38

This work is licensed under a

Creative Commons Attribution 4.0 International License.

Research Paper

THE IMPACT OF OWNERSHIP STRUCTURE ON FIRM PERFORMANCE: A STUDY ON BOMBAY STOCK EXCHANGE IN INDIA

Sahibzada Muhammad Hamza

Lecturer

School of Accounting and Business Management

FTMS College, Malaysia

Siti Suziyati Suman BSc(Hons) Accounting & Finance Student

Lords Ashcroft Business School

Anglia Ruskin University, UK

ABSTRACT

The purpose of this study is to examine the impact of ownership structures on firm performance in India. Textiles, oil marketing and distribution, movies and entertainment industries were studied through 50 companies registered in Bombay stock exchange within the span of 2011 -2015 and total observations of 250 firms-years. The independent variable is managerial, concentrate, institutional and foreign ownership while the dependent variable is Return on Assets. The research employed Descriptive Statistics, Pearson correlation coefficient and multiple linear regressions for gauging the impact of the independent variables on the dependent variable. Simple convenience sampling technique is used to select the sample size and E-view software was adopted to generate the data for analysis. The findings show that concentrate ownership has a significant positive impact on Return on Assets. While managerial and institutional ownership have positive insignificant impact on ROA. Lastly, foreign ownership is found to have a negative insignificant impact on ROA. Furthermore, it is recommended that future researchers are encourage different industries with the same framework to investigate the impact which might be different due to the difference in the nature of the industry. While another framework with more different ownership structure options can be designed and test to see more aligned results. This Study will eventually benefit the textiles, oil marketing and distribution and movies and entertainment sectors r to deal with their ownership structure in future. It also helps to guide them in determining the costs, improving the relationship in organization within the firms and make a good understanding on how the ownership structure would bring influence on the firm performance.

Key Terms: Structure, Managerial ownership, Concentrates ownership, Institutional ownership,

Foreign ownership, Firm Performance, ROA, and BSE

ISSN: 2289-4519 Page 22

1. INTRODUCTION

The purpose of this research is to examine the impact of ownership structures on firm

performance in Indian textile, oil marketing and distribution and movies and entertainment

sector registered in Bombay stock exchange. Ownership structure is an important factor which

affects a firm’s movement especially its health (Zeitun & Tian, 2007). Berle and Mean (1932)

are the pioneers of studying ownership structure which they conducted in United States

corporate law where they hypothesize that an inverse correlation should be observed between

the diffuseness of shareholdings and firm performance. From the conflicts of interest between

controllers and managers, it was concluded that with increasing ownership diffusion, the

authority of the shareholders to control management is minimized (Berle & Mean, 1932).

Previous studies in India has been done by Singh and Gaur (2009) on corporate

sector, Srivastava (2011) on actively listed company constitute the bulk of trading and Nazir

and Malhotra (2016) on corporate governance. While globally the studies in this topic done by

Gedajlovic and Shapiro (2002) on financial performance of Japanese corporations; Grant and

Kirchmaier (2004) in Europe corporate governance industry; Karaca and Ekşi (2012)in

manufacturing industry on the Istanbul stock exchange. Mostly researches has been done in

corporate governance sector and the common variables used are ROI, ROE and ROA (Kaur &

Gill, 2008; Srivastava, 2011;Nazir & Malhotra, 2016).

The interest conflict between a firm’s managers and owners influence the decision

made by themselves which leave impacts on company performances. Undeniable, when the

control of a company is separate from its ownership, agents either managers may not generally

act to the best interest of its shareholders (Bonazzi & Islam, 2006). Moreover, the issue of

ownership structure on firm performance within any company has become a serious discussion

in corporate governance for decades as the problem of “separation of ownership from control”

always arises within organization in different types of ownership structures (Srivastava, 2011).

Adding to it, ownership structure has been always dictated by other country-level

corporate governance characteristics such as stock market development and the state

intervention with the regulations natures (Porta et al., 1998).A firm with the different

ownership structure will not have the same level of efficiency, where the high concentrate

companies can be more efficient in which the concentration may alleviate the interest conflicts

among agents (Ramli, 2010).While in poorly performing firms, the directors may be assumed

doing a poor job in overseeing management and have less opportunity to be the directors at

other firms (Kaplan & Reishus, 1990). This is why ownership matters to be discuss.

By conducting this research, it can add a new element in contributions to the previous

literature on firm's’ performance and ownership structure. The study also beneficial for

corporate, textiles, oil marketing and distribution and movies and entertainment sectors since

the issue in ownership structure are mostly addressed to them especially in managing

ownership and its control within the growing firms surround them and may also help the

company Board of Director to deal with their ownership structure in future. It also helps to

guide them in determining the costs, improving the relationship of the organization within the

firms. Indirectly this research information can help the firms in textiles, oil marketing and

distribution and movies and entertainment sectors to have a good understanding how the

ownership structure would bring influence on the firm performance.

Research Objectives:

To identify and examine the impact of institutional ownership on ROA

To identify and examine the impact of managerial ownership on ROA

To identify and examine the impact of concentrated ownership on ROA

ISSN: 2289-4519 Page 23

To identify and examine the impact of foreign ownership on ROA

2. LITERATURE REVIEW

Jensen and Meckling (1976) defined ownership structure as capital commitments,

which involves inside investors (supervisors) and outside investors (debt and equity holder).

Bansal (2005), demonstrated that the committee of investors and shareholders (proprietors) is

made up of individual peoples, groups and institutions whose have different goals, interests,

investment horizons and capabilities. Abel & Okafor (2010) defines ownership structure as the

percentage of share held by managers (managerial ownership), institutions (institutional

ownership), government (state ownership), foreign investors (foreign ownership), and family

(family ownership).

Numerous theoretical models and frameworks have been developed in order to

identify the relationship and the impacts of ownership structures trend towards firm

performances. Most common theoretical adopted was the Agency Theory which is created by

Jensen and Meckling (1976). This theory emphasises on the separation of firm management

and ownership. The theory was born as the consequences of conflict of interest between agents

(shareholders and managers) and due to problem in separation of firm management and

ownership (Abdul Jamal et al, 2013). Secondly, Stewardship theory was introduced by

Donaldson and Davis (1991) to understand the existing relationships between ownership and

management of the company. This theory arises as an important counterweight to Agency

Theory (Pastoriza, 2008). While Transaction cost theory was initially developed by Coase

(1937) to discuss how the costs of engaging in an action by an organization affect its behavior.

Modern corporations generally have easy access to finance; but their shareholders are more

dependent on the managers (Volonte, 2012). Lastly, Property Rights Theory developed by

Coase (1960) stresses that property rights give the freedom to decision maker and control its

financial performance. Referring to Alchian and Demsetz (1973), the ownership of property

rights didn’t set specifically only for certain groups which can be owned privately, government

and even by society (Shleifer & Vishny (1997).

Table 1: Summary of theories on Ownership Structure

Theories Description Sources

Theory of the

firm

Theory of market in which firms are crucial actors Coase (1937)

Agency Theory Explain the relationship between principal and agents Jensen and

Meckling

(1976)

Principal agent

theory

Emphasis the conflict between shareholders and the

management

William

(1963)

Stewardship

theory

Understanding the existing relationship between

ownership and management within the firm

Donaldson

and Davis

(1991)

Property rights

theory

Specification of individual rights determines how

costs and rewards will be allocated for the

participants in all organization

Coase (1960)

Transaction cost

theory

Discuss how the cost of engaging in action by an

organization affects its behavior

Coase (1937)

ISSN: 2289-4519 Page 24

Several researches were conducted previously in India to examined the ownership

structure impacts on firms performance such as likeNazir and Malhotra (2016) did on

corporate governance, Singh and Gaur (2009) did study on corporate sector, Srivastava (2011)

on actively listed company constitute the bulk of trading, Kumar (n.d) did on corporate

governance, Singh and Singh (2016) study on cement industry, Haldar and Rao (n.d) make

research by analyzing firms traded on Bombay Stock Exchange, Balasubramanian and Anand

(2013) study about ownership trends in corporate. Mostly researches has been done in

corporate sector and the common variables used are ROI, ROE, ROA, concentrate and

managerial ownership (Kaur & Gill, 2008; Srivastava, 2011; Nazir a& Malhotra, 2016).

Globally there are numerous studies conducted on the topic. Some notable amongst

them are mentioned; Lazaretou and Kapopoulos (2006), conduct study to investigate if there’s

a strong evidence to support the notion that variation across firms in observed ownership

structures impacts in systematic variations in observed firm performance. Demsetz and

Villalonga (2001) by using endogenous variable and two types of ownership structure which

reflect on different group of shareholders with conflicting interests. The findings suggest that a

more concentrated ownership structure positively relates to higher. Chen (2012) makes a

research to investigate the effect of ownership structure on firm performance on Non-financial

Listed Companies in Scandinavian. Furthermore, Radice (1971) prove that owner-controlled

firms tend to have higher profit rates and growth rates. Wahla, Shah and Hussain (2012) make

a research to analyze the significant relationship of Ownership Structure with Firm

Performance in non-financial companies listed at Karachi Stock Exchange with a period of

2008 to 2010. Wei et al., (2014) make a research to determine the relationship between

ownership structure and firm performance in Malaysia in trading and services sector. They

conduct the research by testing dependent variables like firm age, firm size, leverage, return on

assets (ROA), return on equity (ROE) and Tobin’s Q; and independent variable which are

managerial ownership structure and Non-managerial ownership structure. This study includes

of testing 70 companies in treading and services sector which listen in in Bursa Malaysia

within the year from 2008-2012 (5 years). The finding concludes that the firm size, leverage

and Tobin’s Q have significant relationship with ownership structure of the company. Zakaria,

Purhanudin and Palllanimally (2014) conduct a study to examine the impact of ownership

structure on firm performance of the Malaysian listed Trading and Services firms. Phung and

Mishra (2015) conduct a study to examine the effect of ownership structure on firm

performance, for firms listed on Vietnamese stock exchanges, using 2744 firm-year

observations covered from year 2007 to 2012.

Figure 1: Conceptual Framework

Concentrate

Ownership

Institutional

Ownership

Foreign

Ownership

Managerial

Ownership

ROA

ISSN: 2289-4519 Page 25

Investors are large institutional investors such as banks, insurance companies,

investment companies (Bush, 1998). The institutional ownership is gauged through the ratio of

shareholding held by institutions to the total number of shares (Fazlzadeh et al., 2011;

Nuryanah & Islam, 2011). Cornett et al (2003) found that large stockholders and institutional

investors have become increasingly active in corporate governance, especially in

underperforming firms. Bethel et al. (1998) find that block share purchases by institutional

investors are most likely in highly diversified firms with poor profitability.Cornet et al. (2003)

has proven that there's a significant positive relationship between institutional ownership and

corporate performance especially in the organizations' working income (operating cash flow)

and the ownership percentages and institutional stockholder number. The total share or stock

hold by institutional ownership within the firm has high influence on ROA. The increases of

independent directors percentage would aligning the interests conflict between managers and

shareholders which reduce the conflicts and resulting in higher ROA (Cornett et al 2003).

H1: There is a positive significant impact of Institutional ownership on ROA.

Li and Sun (2014) defined managerial ownership as the ratio of equity owned by

directors. The diffuseness of shareholdings of today Modern Corporation decides the

detachment of ownership and control, that’s why it causes a conflict of interest problem,

occurs among the management and the shareholders which may leave consequences into firm

performance (Berle and Means, 1932).This can be observed from Morck, Shleifer and Vishny

(1988) and McConnell and Servaes (1990) studies that the relationship between managerial

ownership and firm performance should be focused. However, Demsetz (1983) state that an

expanded level of insider ownership can diminish corporate performance.

H2: There is a positive significant impact of managerial ownership on ROA.

Ownership concentration is the ownership share (votes) of the largest owner in

percentage (Pathirawasam, 2013). Hill and Snell (1998) found good relationship between

ownership structure and firm performance which is measured by using profitability.

Concentrated firms will encourage innovation as a strategy to increased firm value rather than

diversification strategy because it will make the manager tied along with the interest objective

(Zakaria, Purhanudin & Palanimally, 2014).Hill and Snell (1998) got that there’s a good

relationship between ownership structure and firm performance which is measured by using

profitability. Then Claessens, Djankov & Pohl (1997) prove that ownership concentration has a

strong positive relationship with the profitability. They conclude that the firm with high

concentrated generated higher profitability and market value. Mitton (2002) also found the

same finding where the high concentrated company has a better stock market performance

during the economic crisis of Asian. Furthermore, by reducing the monitoring costs, ownership

concentration will help in improving the firm performance (Shleifer and Vishny, 1986).

H3: There is a positive significant impact of concentrate ownership on ROA.

Foreign ownership is found in the increasing output, employment and wages of target

firms in respect to residential procured firms (Wang and Wang, 2014). Along with this its

directly can influence the company performance. Barbosa, Natalia & Louri (2003) state no

evidence shows that multinational corporations are performing well than the domestic

corporations in Greece and Portugal which is measured by ROA. Li and Jeong-Bon (2004)

point out that foreign ownership generated higher ROA and ROE compared to domestic

ownership.Furthermore, the presence of foreign ownership improves the comparative cost

advantage of firms(Micco, Panizza, & Yañez, 2004).

H4: There is a positive significant impact of foreign ownership on ROA.

ISSN: 2289-4519 Page 26

3. RESEARCH DESIGN AND METHODOLOGY

The research design adapted for this study is explanatory research design to test the

causal relationship between the independent and dependent variable. Quantitative secondary

data has been collected for the defined variables to examine the topic. To examine the

hypotheses, companies from three sectors (textiles, oil marketing and distribution; movies and

entertainment) which are publicly listed in Bombay Stock Exchange has been chosen within

the time span of 2011-2015. 50 total companies were being selected for the sample by using

convenient sampling technique. The companies were chosen based on availability of data in

the annual reports. Thus the study would take data from the published annual reports which are

accessible in the company’s official website. For the ethical issue, as this was a secondary

research the copyright and legal access to the owner’s works will be applied to avoid

misconduct in this research and the proper citation of the real facts using Harvard Referencing

is provided. Then E-views employed software to analyze the Correlation analysis and the

Multiple Regression analysis as this research used convenience sampling technique to collect

the data.

4. RESULT AND DISUCSSION

Descriptive statistics

Table 2: Descriptive Means and Standard Deviation

N Min Max Mean Std. Deviation

Concentration ownership 250 373.43 2308 15.03 299.84

Foreign ownership 250 156.73 2926.78 15.34 397.21

Institutional ownership 250 1016 8666746 15.77 109.48

Managerial ownership 250 1879 31087 43.87 217.20

As shown at the Table 2, the average mean for the independent variable Concentration

Ownership is 15.03 with the standard deviation of 299.84. This indicates that the 15% of

ownership is concentration ownership from the selected sample of the Australian Mining

Industry. Secondly, the average mean for the independent variable Foreign Ownership is 15.34

with the standard deviation of 397.21. This indicates that the 15% of ownership is foreign

ownership from the selected sample of the Australian Mining Industry. Furthermore, the

average mean for the independent variable Institutional Ownership is 15.77 with the standard

deviation of 109.48. This indicates that the 15% of ownership is Institutional ownership from

the selected sample of the Australian Mining Industry. Lastly, the average mean for the

independent variable Managerial Ownership is 43.87 with the standard deviation of 217.20.

This indicates that the 43% of ownership is Managerial ownership from the selected sample of

the Australian Mining Industry

ISSN: 2289-4519 Page 27

Correlation Analysis

Table 3: Correlation analysis

ROA Concentrate

ownership

Foreign

ownership

Institutional

ownership

Managerial

ownership

ROA 1

Concentrate ownership 0.058047 1

Foreign ownership 0.213627** 0.299852 1

Institutional ownership -0.31784 -0.49633** -0.365772** 1

Managerial ownership 0.172379** -0.094291 0.167839** 0.016401 1

According to Table 3 above, Concentrate ownership (independent variable) has a

positive insignificant relationship with ROA (dependent variable) with a Pearson Correlation

value of 0.05 and probability value of 0.36. This research findings are similar with the findings

of AL-Najjar (2015); Gedajlovic and Shapiro (2002); Zakaria, Purhanuddin and Palanimally

(2014) and Raji (2012). While opposite findings have found by Claessens and Djankov (1999);

Din and Javid (2011) and Kiruri, (2013) which argue that as the number of block holder

increase within the company, the company performance fall while if the number decrease the

performance rises. Foreign Ownership (independent variable) has a positive significant

relationship with ROA (dependent variable) with a Pearson Correlation value of 0.21 and

probability value of 0.00. The result of this study is similar to the results concluded by

Mang’unyi (2011) and Kiruri (2013) finding which concludes that higher foreign ownership in

a company leads to higher profitability while lower foreign ownership leads to lower

performance. However, Aburime (n.d) and Lee (2008) have concluded contradicting findings.

Institutional Ownership (independent variable) has a positive insignificant

relationship with ROA (dependent variable) with a Pearson Correlation value of -0.31 and

probability value of 0.61. Duggal and Millar (1999) and Faccio and Lasfer (2000)also found

similar findings from their study.However, this result is contradicted with Nesbitt (1994);

Smith (1996) and AL-Najjar (2015) findings. Mao (2015) also concludes that institutional

investors have more incentives and more competencies to involve in monitoring management

therefore enhancing firm performance. Managerial Ownership (independent variable) has a

positive significant relationship with ROA (dependent variable) with a Pearson Correlation

value of 0.17 and probability value of 0.00. Moreover, the findings of this study are similar

toMorck, Shleifer and Vishny (1988); Cheung, Fung and Tsai (2008) and Shleifer and Vishny

(1986). Opposite findings found by Wahla, Shah and Hussain (2015); and Ruan, Tian and Ma

(2011).

Table 4: Summary of correlation analysis results

Variables Results

Concentrate ownership Positive insignificant correlated with ROA

Foreign ownership Positive significant correlated with ROA

Institutional ownership Negative insignificant correlated with ROA

Managerial ownership Positive significant correlated with ROA

Multiple Regression Analysis

Table 5: Model fitness

Model R-squared Adj. R-squared F-Significance Durbin-Watson Statistics

1 0.531 0.392 0 1.522

ISSN: 2289-4519 Page 28

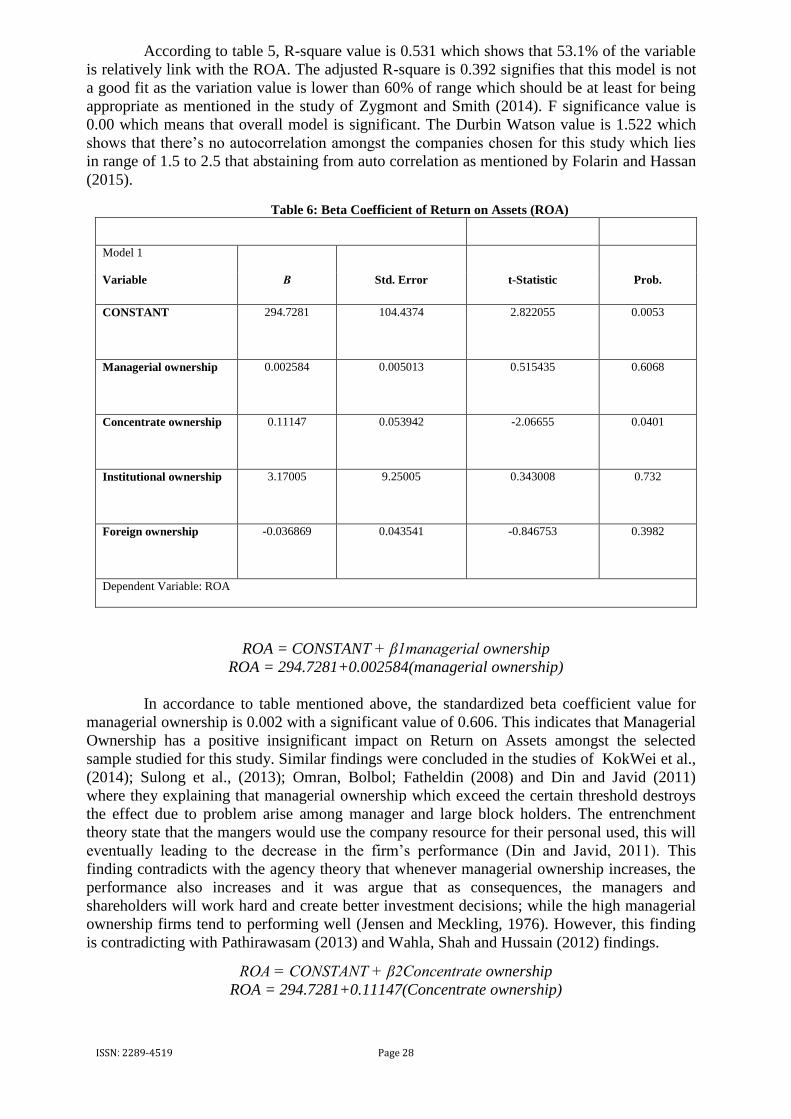

According to table 5, R-square value is 0.531 which shows that 53.1% of the variable

is relatively link with the ROA. The adjusted R-square is 0.392 signifies that this model is not

a good fit as the variation value is lower than 60% of range which should be at least for being

appropriate as mentioned in the study of Zygmont and Smith (2014). F significance value is

0.00 which means that overall model is significant. The Durbin Watson value is 1.522 which

shows that there’s no autocorrelation amongst the companies chosen for this study which lies

in range of 1.5 to 2.5 that abstaining from auto correlation as mentioned by Folarin and Hassan

(2015).

Table 6: Beta Coefficient of Return on Assets (ROA)

Model 1

Variable Β Std. Error t-Statistic Prob.

CONSTANT 294.7281 104.4374 2.822055 0.0053

Managerial ownership 0.002584 0.005013

0.515435 0.6068

Concentrate ownership 0.11147

0.053942

-2.06655 0.0401

Institutional ownership 3.17005 9.25005 0.343008 0.732

Foreign ownership -0.036869 0.043541 -0.846753 0.3982

Dependent Variable: ROA

ROA = CONSTANT + β1managerial ownership

ROA = 294.7281+0.002584(managerial ownership)

In accordance to table mentioned above, the standardized beta coefficient value for

managerial ownership is 0.002 with a significant value of 0.606. This indicates that Managerial

Ownership has a positive insignificant impact on Return on Assets amongst the selected

sample studied for this study. Similar findings were concluded in the studies of KokWei et al.,

(2014); Sulong et al., (2013); Omran, Bolbol; Fatheldin (2008) and Din and Javid (2011)

where they explaining that managerial ownership which exceed the certain threshold destroys

the effect due to problem arise among manager and large block holders. The entrenchment

theory state that the mangers would use the company resource for their personal used, this will

eventually leading to the decrease in the firm’s performance (Din and Javid, 2011). This

finding contradicts with the agency theory that whenever managerial ownership increases, the

performance also increases and it was argue that as consequences, the managers and

shareholders will work hard and create better investment decisions; while the high managerial

ownership firms tend to performing well (Jensen and Meckling, 1976). However, this finding

is contradicting with Pathirawasam (2013) and Wahla, Shah and Hussain (2012) findings.

ROA = CONSTANT + β2Concentrate ownership

ROA = 294.7281+0.11147(Concentrate ownership)

ISSN: 2289-4519 Page 29

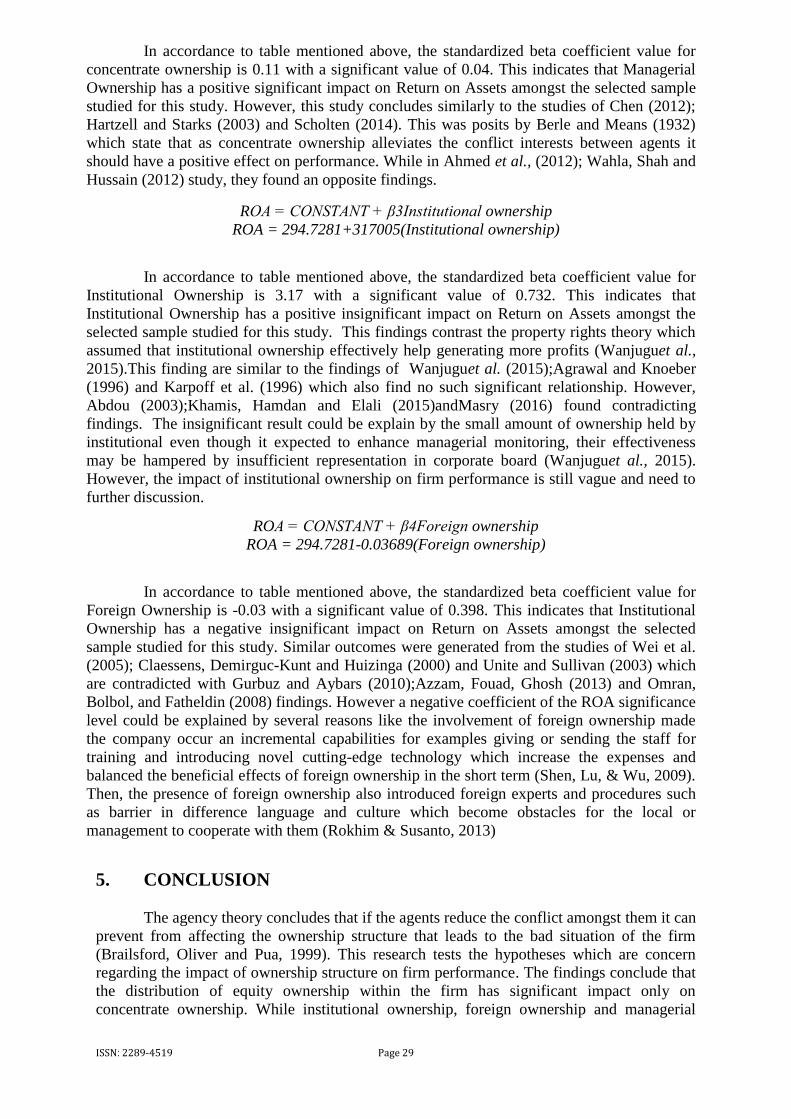

In accordance to table mentioned above, the standardized beta coefficient value for

concentrate ownership is 0.11 with a significant value of 0.04. This indicates that Managerial

Ownership has a positive significant impact on Return on Assets amongst the selected sample

studied for this study. However, this study concludes similarly to the studies of Chen (2012);

Hartzell and Starks (2003) and Scholten (2014). This was posits by Berle and Means (1932)

which state that as concentrate ownership alleviates the conflict interests between agents it

should have a positive effect on performance. While in Ahmed et al., (2012); Wahla, Shah and

Hussain (2012) study, they found an opposite findings.

ROA = CONSTANT + β3Institutional ownership

ROA = 294.7281+317005(Institutional ownership)

In accordance to table mentioned above, the standardized beta coefficient value for

Institutional Ownership is 3.17 with a significant value of 0.732. This indicates that

Institutional Ownership has a positive insignificant impact on Return on Assets amongst the

selected sample studied for this study. This findings contrast the property rights theory which

assumed that institutional ownership effectively help generating more profits (Wanjuguet al.,

2015).This finding are similar to the findings of Wanjuguet al. (2015);Agrawal and Knoeber

(1996) and Karpoff et al. (1996) which also find no such significant relationship. However,

Abdou (2003);Khamis, Hamdan and Elali (2015)andMasry (2016) found contradicting

findings. The insignificant result could be explain by the small amount of ownership held by

institutional even though it expected to enhance managerial monitoring, their effectiveness

may be hampered by insufficient representation in corporate board (Wanjuguet al., 2015).

However, the impact of institutional ownership on firm performance is still vague and need to

further discussion.

ROA = CONSTANT + β4Foreign ownership

ROA = 294.7281-0.03689(Foreign ownership)

In accordance to table mentioned above, the standardized beta coefficient value for

Foreign Ownership is -0.03 with a significant value of 0.398. This indicates that Institutional

Ownership has a negative insignificant impact on Return on Assets amongst the selected

sample studied for this study. Similar outcomes were generated from the studies of Wei et al.

(2005); Claessens, Demirguc-Kunt and Huizinga (2000) and Unite and Sullivan (2003) which

are contradicted with Gurbuz and Aybars (2010);Azzam, Fouad, Ghosh (2013) and Omran,

Bolbol, and Fatheldin (2008) findings. However a negative coefficient of the ROA significance

level could be explained by several reasons like the involvement of foreign ownership made

the company occur an incremental capabilities for examples giving or sending the staff for

training and introducing novel cutting-edge technology which increase the expenses and

balanced the beneficial effects of foreign ownership in the short term (Shen, Lu, & Wu, 2009).

Then, the presence of foreign ownership also introduced foreign experts and procedures such

as barrier in difference language and culture which become obstacles for the local or

management to cooperate with them (Rokhim & Susanto, 2013)

5. CONCLUSION

The agency theory concludes that if the agents reduce the conflict amongst them it can

prevent from affecting the ownership structure that leads to the bad situation of the firm

(Brailsford, Oliver and Pua, 1999). This research tests the hypotheses which are concern

regarding the impact of ownership structure on firm performance. The findings conclude that

the distribution of equity ownership within the firm has significant impact only on

concentrate ownership. While institutional ownership, foreign ownership and managerial

ISSN: 2289-4519 Page 30

ownership makes no contribution to the profitability of selected sample companies in

Bombay stock exchange (BSE). The lack of consensus from empirical research isn't

surprising because performance depend on the ownership pattern applied and sometimes

relying on the national institutional (Gitundu et al., 2016).

The study provides a heading light for the future researchers to investigate different

variables that aren’t adopted in this study. There many other else variables such as return on

investment, Tobin Q, return on equity, size and leverage which can be used to investigate and

discover various factors of ownership structure which affecting the company’s performance

that registered in Bombay Stock Exchange. Moreover, in future research the managerial,

institutional and foreign ownership which is found insignificant in this study can be readopted.

Then the future researcher also recommend to use larger sample size since this research has

only used 50 listed companies in 3 sectors of Bombay Stock Exchange like study done by

Kaopoulos and Lazaretou (2006) where their study covers all sectors of Greek economy.

This study facing several limitations such as the study only covers three sectors of

BSE which cannot be a representative for the entire economies. However the most highlighted

limitation in this study is the availability of the data because the ownership structure data are

quietly limited in India as it was developing country. Next, the impact that has been intended

to be measured in short term which might not reflects the perfect outcomes as maybe the

performance of the companies could be impacted in long term. Moreover, the limited time

limitation has much influence this research scope which insufficient time to discover entire

sectors and the spending times on collecting data where only ROA independent variable that

used to measure the profitability. Lastly, a minimal sample size was selected due to non-

availability of financial data for the companies registered in BSE.

The further researchers are encouraged to conduct a research with more wide

approach by conducting research which covers entire sectors and countries to check the

similarity that found in this research. Furthermore, a comparative study also can be made in

order to checking the deviation and ownership structure behavior in different industries.

Therefore the future researchers are advised to use different industries with the same

framework to investigate the impact which might be different due to the difference in the

nature of the industry. While another framework with more different ownership structure

options can be designed and test to see more aligned results. Future researchers are

recommending taking larger sample size as this study only used 50 selected firms. The result

will be more accurate and better if the sample size is increase. Besides that future researchers

advise to lengthen the period of sample size by using more than 5 years. Lastly, future

researchers are encouraged to expand the coverage of the sample in various countries since

different country will have different result

REFERENCES

Applied studies, 10(5).

Abdul Jamal, A. A., Geetha, C., Mohidin, R., Abdul Karim, M.R., Lim, T.S. and Ch’ng, V., 2013.

Capital Structure Decisions: Evidence from Large Capitalized Companies in Malaysia.

Interdisciplinary Journal of Contemporary Research in Business, [ejournal] 5(5). Available at:

ijcrb.webs.com [Accessed 30 Oct 2016]

Abel, E. E & Okafor, F. O. (2010). Local corporate ownership and capital structure decisions in

Nigeria: A developing country perspective. Corporate Governance, 10(3), 249-260.

Aburime, U.T. (n.d). IMPACT OF OWNERSHIP STRUCTURE ON BANK PROFITABILITY IN

NIGERIA. [Online] Available on:

ISSN: 2289-4519 Page 31

http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.383.7848&rep=rep1&type=pdf

[Retrieved 27/03/2016].

Agrawal, A., and C.R. Knoeber, 1996. Firm performance and mechanisms to control agency problems

between managers and shareholders. Journal of Financial and Quantitative Analysis 31, 377-

397.

Ahmed, K,.Sehrish, S., Saleem, F., Yasir, M. and Shehzad, F. (2012). IMPACT OF

CONCENTRATED OWNERSHIP ON FIRM PERFORMANCE (EVIDENCE FROM

KARACHI STOCK EXCHANGE). Available on: http://journalarchieves23.webs.com/201-

210.pdf [Accessed 16/09/2016].

Alchian, A. A. & H. Demsetz. (1973), ‘The Property Rights Paradigm,’ Journal of Economic History

33, 16-27.

Alipour M, Amjadi H (2011). “The Effect of Ownership Structure on Corporate Performance of

Listed Companies in Tehran Stock Exchange: An Empirical Evidence of Iran” J. Bus. Soc. Sci.

2(13):955.

Alireza F, Hendi AT, Mahboubi K (2011). The Examination of the Effect of Ownership Structure on

Firm Performance in Listed Firms of Tehran Stock Exchange” J. Bus. Manage. 6(3):249-266.

Al-Najjar, D. (2015). The Effect of Institutional Ownership on Firm Performance: Evidence from

Jordanian Listed Firms. Available on: http://dx.doi.org/10.5539/ijef.v7n12p97 [Accessed

18/07/2016].

Available on: http://down.cenet.org.cn/upfile/34/200742395443169.pdf [Accessed on 17th March,

2016]

Azzam, I., Fouad, J., & Ghosh, D. K. (2013). Foreign ownership and financial performance: evidence

from Egypt. International Journal of Business, 18(3), 232

Balasubramanian, N. and Anand, R.V. (2013). Ownership Trends in Corporate India 2001 – 2011

Evidence and Implications. [Online] available on:

http://www.iimb.ernet.in/research/sites/default/files/WP%20No.%20419_0.pdf [Retrieved

08/11/2016].

Bansal, C.L. (2005). Corporate governance – law practice and procedures with case studies. New

Delhi: Taxmann Allied Service (P) Ltd. 2 -11, 163, 234.

Barbosa, Natalia, and Louri, H. (2003). Corporate Performance: Does Ownership Matter? A

Comparison of Foreign- and Domestic-Owned Firms in Greece and Portugal, Review of

Industrial Organization 27/1: 73- 102.54 | P a g e 63 | P a g e

Barton, F., Bradbrook., G. and Broome, G. (2015). Digital Accessibility: A brief landscaping.

[Online]. Available at: http://www.citizensonline.org.uk/wpcontent/uploads/digital-

accessibility-reporta-pdf.pdf [Accessed 18/07/2016].

Bathula, H. (2008). Board Characteristics and Firm Performance: Evidence from New Zealand.

[Online]. Available on:

http://aut.researchgateway.ac.nz/bitstream/handle/10292/376/BathulaH.pdf?sequence=4

[Retrieved 27/03/2016].

Berle, A. and Means, G. (1932). The Modern Corporation and Private Property. New York, NY:

Macmillan.

Bethel, J., J. Liebiskind, and T. Opler, 1998. Block share purchases and corporate performance.

Journal of Finance 53, 605-635.

Bonazzi, L. and Islam, S.M. (2006). "Agency theory and corporate governance: A study of the

effectiveness of board in their monitoring of the CEO", Journal of Modelling in Management.

ISSN: 2289-4519 Page 32

Available on: http://www.emeraldinsight.com/doi/abs/10.1108/17465660710733022

[Accessed 18/07/2016].

Brailsford, T.J., Oliver, B.R. and Pua, S.L. (1999). Theory and evidence on the relationship between

ownership structure and capital structure. Available on:

file:///C:/Users/1541029BJ/Downloads/brailsford.pdf [Accessed 16/09/2016].

Bush, B. J. (1998). "The Influence of Institutional Investors on Myopic R&D Investment Behavior",

Accounting Review, 73(July): 305-334.

Chen, L (2012). The Effect of Ownership Structure on Firm Performance. Pp.3-59. Available on:

http://pure.au.dk/portal/files/48424135/The_Effect_of_Ownership_Structure_on_Fi

rm_Performance_Chen_Luzhen_2012.pdf [Accessed on 16th March, 2016]

Cheung, W., Fung, S. and Tsai, S.C. (2008). The Impacts of Managerial and Institutional Ownerships

on Firm Performance: The Role of Stock Price Informativeness and Corporate Governance.

Available on:

http://umir.umac.mo/jspui/bitstream/123456789/14715/1/3872_0_IO_PriceInformativeness_C

OC_Final_20081213.pdf [Accessed 16/09/2016].

Claessens, S. And Djankov, S. (1999). Ownership Concentration and Corporate Performance in the

Czech Republic. Available on:

http://home.cergeei.cz/hanousek/jel_survey/Table%204/Claessens%20and%20Djankov%20(1

999).pdf (Accessed 23/03/2016).

Claessens, S., Demirguc-Kunt, A. & Huizinga, H. (2001). How does foreign entry affect domestic

banking markets? Available on:

http://siteresources.worldbank.org/DEC/Resources/847971114437274304/final.pdf [Accessed

18/07/2016].

Claessens, S., Djankov, S. and Pohl, G. (1997). Ownership and Corporate Governance: Evidence from

the Czech Republic. Available on:

https://www.researchgate.net/publication/23721971_Ownership_and_Corporate_Governance_

Evidence_from_the_Czech_Republic [Accessed 29/08/2016].

COASE, R. H. (1960) The Problem of Social Cost, in idem, (1988). The Firm, the Market and the

Law. Chicago: University of Chicago Press.

Coase, R.H. (1937). The Nature of the Firm. Available on:

http://www3.nccu.edu.tw/~jsfeng/CPEC11.pdf [Accessed 19/11/2016]

Coase, R.H. (1937). The Nature of the Firm. Available on:

http://www3.nccu.edu.tw/~jsfeng/CPEC11.pdf [Accessed 19/11/2016]

Cornett, M., Marcus, A.J., Saunders, A. and Tehranian, H. (2007). The impact of institutional

ownership on corporate operating performance. [Online] available on:

https://www2.bc.edu/alan-marcus/papers/JBF_2007.pdf [Retrieved 08/11/2016].

Davis, J.H., Schoorman, F.D., & Donaldson, L. 1997. Academy of Management Review, 22: 20-47.

Demsetz, H. and B. Villalonga (2001), “Ownership Structure and Corporate Performance”, Journal of

Corporate Finance, 7, 209-233.

Din, S. and Javid, A.Y. (2011). Impact of Managerial Ownership on Financial Policies and the Firm’s

Performance: Evidence Pakistani Manufacturing Firms. Available Online at

https://mpra.ub.uni-muenchen.de/37560/ [Accessed 26/03/2016].

Donaldson, L. and Davis, J. H. (1994) Boards and company performance - research challenges the

conventional wisdom, Corporate Governance: An International Review, 2(3), 151-160.

ISSN: 2289-4519 Page 33

Donaldson, L., & Davis, J. H. (1991). Stewardship Theory or Agency Theory: CEO Governance and

Shareholder Returns. [Online]. Available on:

https://pdfs.semanticscholar.org/b226/d681d20fb646b147ecb3f452fb5de2269cb7.pdf

[Accessed 20/11/2016].

Driffiled, N. and Mahambare, V. (2005). How Ownership Structure Affects Capital Structure and

Firm Performance? Recent evidence from East Asia. Available on:

http://www.fep.up.pt/conferences/earie2005/cd_rom/Session%20VII/VII.A/Driffield%20.pdf

[Accessed 24/08/2016].

Duggal, R., Millar, J.A. (1999). Institutional ownership and firm performance: The ease of bidder

returns. Journal of Corporate Finance 5, 103-117.

Eisenhardt, K.M. (1989) “Agency Theory: An Assessment and Review”. Academy of Management

Review, Vol. 14, pp. 57-74

Faccio, M., Lasfer, M.A. (2000). Do occupational pension funds monitor companies in which they

hold large stakes? Journal of Corporate Finance 6, 71-110.

Fazlzadeh, A., Hendi, A. T., &Mahboubi, K. (2011). The examination of the effect of ownership

structure on firm performance in listed firms of Tehran stock exchange based on the type of the

industry. Interactional Journal of Business and Management, 6(3), 249–267.

Folarin, T. O. and Hassan, Z., 2015. Effects of Technology On Customer Retention: A study on Tesco

Malaysia. International Journals, [online] 1(1). Available at:

http://www.ftms.edu.my/journals/images/Document/IJABM/April2015/12Effects%20of%20T

echnology%20on%20Customer%20Retention.pdf [Accessed 18/09/2016].

GEDAJLOVIC, E & SHAPIRO, D.M (2002). OWNERSHIP STRUCTURE AND FIRM

PROFITABILITY IN JAPAN. [Online] Available on:

http://www.sfu.ca/~erg/research/japan411f.pdf [Accessed 26/03/2016].

Gitundu, E. W., Kiprop, S.K., Kibet, L.K., and Kisaka, S.E. (2016). The influence of ownership

structure on financial performance of privatized companies in Kenya. [Online]. Available on:

DOI: 10.5897/AJBM2015.7949 [Accessed 20/11/2016].

Grant, J. and Kirchmaier, T. (2004). Corporate Ownership Structure and Performance in Europe.

Pp.4-21. Available on:

http://eprints.lse.ac.uk/19960/1/Corporate_Ownership_Structure_and_Performance_in_Europe

.pdf [Accessed on 16th March, 2016]

Gurbuz, A. O., &Aybars, A. (2010). The impact of foreign ownership on firm performance, evidence

from an emerging market: Turkey. American Journal of Economics and Business

Administration, 2(4), 350.

Haldar, A. &Roa, S.V.D. (2010). Empirical Study on Ownership Structure and Firm Performance.

[Online] available on: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2185860

[Retrieved 08/11/2016].

HARTZELL, J. C., and STARKS, L. T. (2003). “Institutional investors and executive compensation”,

Journal of Finance, 58(6), pp. 2351-2374

Hill, C. W., & Snell, S. A. (1988). External Control, Corporate Strategy, and Firm Performance in

Research Intensive Industries. Strategic Management Journal, 9(6), 577-590.

Himmelberg, C.P., Hubbard, R.G. and Palia, D. (1999), Understanding the Determinants of

Managerial Ownership and the Link Between Ownership and Performance, Journal of

Financial Economics 53, 353–384.

Hu, Y & Zhou, X (2006). Managerial Ownership Matters for Firm Performance: Evidence from

China. [Online]. Available on:

ISSN: 2289-4519 Page 34

http://www.cicfconf.org/past/cicf2006/cicf2006paper/20060201085218.pdf [Accessed

03/04/2016].

Jensen, M.C. and Meckling, W. (1976) “Theory of the Firm: Managerial Behavior, Agency Costs and

Ownership Structure”. Journal of Financial Economics, Vol. 3, pp.305-360

Kaplan, S.N., and Reishus, D. (1990). Outside directorship and corporate performance. Journal of

Financial Economics 27, 389-410.

Kapopoulos, P. and Lazaretou, S (2006). CORPORATE OWNERSHIP STRUCTURE AND FIRM

PERFORMANCE: EVIDENCE FROM GREEK FIRMS. Pp. 7-20. [Online]

Karaca, S.S and Eksi, I.H. (2012). The Relationship between Ownership Structure and Firm

Performance: An Empirical Analysis over Istanbul Stock Exchange (ISE) Listed Companies.

[Online]. Available on: URL: http://dx.doi.org/10.5539/ibr.v5n1p172 [Accessed 18/07/2016].

Karpoff, J.M., P.H. Malatesta, and R.A. Walkling, 1996. Corporate governance and shareholder

initiatives: Empirical evidence. Journal of Financial Economics 42, 365395.

Khamis, R., Hamdan, A.M. and Elali, W. (2015). The Relationship between Ownership Structure

Dimensions and Corporate Performance: Evidence from Bahrain. Available on:

http://ro.uow.edu.au/cgi/viewcontent.cgi?article=1629&context=aabfj [Accessed 16/09/2016].

Kiruri, R. M. (2013). The effects of ownership structure on bank profitability in Kenya. European

Journal of Management Sciences and Economics, 1(2), 116127.

Kok Wei, C., Sew Fong, C., Carrie, C. and Chi Yan, T. (2014). OWNERSHIP STRUCTURE AND

FIRM PERFORMANCE IN MALAYSIA: IN TRADING SERVICES SECTOR. Pp.4-99.

Available on: http://eprints.utar.edu.my/1287/1/BF20141005622.pdf [Accessed on 16th

March, 2016].

Kortelainen, P (2007). The Effect of Family Ownership on Firm Performance: Empirical Evidence

from Norway. [Online] Available on:

http://www.doria.fi/bitstream/handle/10024/30738/TMP.objres.546.pdf? [Accessed

26/03/2016]

Kumar, J. (n.d). Does Ownership Structure Influence Firm Value? Evidence from India. [Online]

available on:

http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.203.1673&rep=rep1&type=pdf

[Retrieved 08/11/2016].

La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert Vishny, 1998, Law and

finance, Journal of Political Economy 106, 1113-1155.

Lee, S (2008). Ownership Structure and Financial Performance: Evidence from Panel Data of South

Korea. DEPARTMENT OF ECONOMICS WORKING PAPER SERIES, Pp. 13-26. [Online]

Available on:

http://www.peri.umass.edu/fileadmin/pdf/UMNS_Workshop/NewSchool2008/Lee S.pdf

[Accessed on 17th March, 2016]

Li, J. and Jeong-Bon K.V. (2004). Foreign Equity Ownership and Information Asymmetry: Evidence

from Japan. Journal of International Financial Management and Accounting. Available on:

http://onlinelibrary.wiley.com/doi/10.1111/j.1467646X.2004.00107.x/abstract [Accessed

07/09/2016]

Li, X., and Sun, S.T., (2014). Managerial Ownership and Firm Performance: Evidence From the 2003

Tax Cut. Available on:

file:///C:/Users/1438545BJ/Downloads/ManagerialOwnershipAndFirmPerformanc_preview.pd

f [Accessed 18/07/2016].

ISSN: 2289-4519 Page 35

Lieber, R.L. (1990). Available on:

http://muscle.ucsd.edu/More_HTML/papers/pdf/Lieber_JOR_1990.pdf [accessed 24/08/2016].

Manawugde, A. and De Zoysa, A. (2013).THE STRUCTURE OF CORPORATE OWNERSHIP

AND FIRM PERFORMANCE: SRI LANKAN EVIDENCE. Corporate Ownership & Control

/ Volume 11, Issue 1, pp. 725-731. Retrieved. http://www98.griffith.edu.au/dspace/bitstrea

m/handle/10072/60707/94047_1.pdf [Accessed on 17th March, 2016]

Mang’unyi, E.E. (2011). Ownership Structure and Corporate Governance and Its Effects on

Performance: A Case of Selected Banks in Kenya. Available on:

http://www.sciedupress.com/journal/index.php/ijba/article/viewFile/342/153 [Accessed

16/09/2016].

Mao, L. (2015). State Ownership, Institutional Ownership and Relationship with Firm Performance:

Evidence from Chinese Public Listed Firms. Available at: http://essay.utwente.nl/67339/

[Accessed 24/08/2016].

Masry, M. (2016). The Impact of Institutional Ownership on the Performance of Companies Listed In

the Egyptian Stock Market. Available on: http://www.iosrjournals.org/iosr-jef/papers/Vol7-

Issue1/Version3/B07130515.pdf [Accessed 16/09/2016].

Micco, A., Panizza, U. and Yañez, M. (2004). Bank Ownership and Performance. IDB Working Paper

No. 429. Available on: http://dx.doi.org/10.2139/ssrn.1818718 [Accessed 07/09/2016].

Mishari A, Faisal A, Hesham A (2012). “The Influence of Institutional and Government Ownership

on Firm Performance: Evidence from Kuwait” Int. Bus. Res. 5 (10):192-200.

Mitton, T. (2002). A cross-firm analysis of the impact of corporate governance on the East Asian

financial crisis. Journal Finance Economy. 64:215.

Mohd, S.N.A., and Kallamu, B.S. (2014). Ownership structure, Independent Chair and Firm

Performance. [Online] Available on: http://www.pertanika.upm.edu.my/ [Accessed

20/03/2016].

Morck, R., Shleifer, A. and R. Vishny (1988), “Management Ownership and Market Valuation: An

Empirical Analysis”, Journal of Financial Economics, 20, 293-315.

Nazir, N. & r Malhotra, A. (2016). The Effect of Ownership Structure on Firm Profitability in India:

A Panel Data Approach. [Online] available on:

http://ccsenet.org/journal/index.php/ijef/article/view/57711/32199 [Retrieved 08/11/2016].

Nesbitt, S.L. (1994). Long-term rewards from shareholder activism: A study of ‘CalPERS effect’.

Journal of Applied Corporate Finance 6, 75-80.

Nuryanah, S., & Islam, S. M. N. (2011). Corporate governance and performance : Evidence from an

emerging market. Malaysian Accounting Review, 10(1), 17–42.

Omran, M.M., Bolbol, A., &Fatheldin, A. (2008). Corporate Governance and Firm Performance in

Arab Equity Markets: Does Ownership Concentration Matter? International Review of Law

and Economics, 28, 32-45.

Ongore, V., K’Obonyo, P.O. and Ogutu, M. (2011). “Implications of Firm Ownership Identity and

Managerial Discretion on Financial Performance: Empirical Evidence from Nairobi Stock

Exchange” Int. J. Hum. Soc. Sci. 1:187-195.

Pastoriza, D. and Ariño, M.A. (2008). WHEN AGENTS BECOME STEWARDS: INTRODUCING

LEARNING IN THE STEWARDSHIP THEORY [Online]. Available on:

http://www.iese.edu/en/files/6_40618.pdf [Retrieved 27/03/2016].

Pathirawasam, C. (2013). INTERNAL FACTORS WHICH DETERMINE FINANCIAL

PERFORMANCE OF FIRMS: WITH SPECIAL REFERENCE TO OWNERSHIP

ISSN: 2289-4519 Page 36

CONCENTRATION. [Online] Available on: http://www.slu.cz/opf/cz/informace/acta-

academica-karviniensia/casopisyaak/aakrocnik-2013/docs-2-2013/Pathirawasam.pdf

[Accessed on 17th March, 2016].

PERFORMANCE: EVIDENCE FROM THE MALAYSIAN ACE MARKET. [Online] available on:

http://www.theibfr2.com/RePEc/ibf/acttax/at-v5n1-2013/AT-V5N12013-7.pdf [Retrieved

08/11/2016].

Pervan, M., Pervan, I. and Todoric, M. (2012). “Firm Ownership and Performance: Evidence for

Croatian Listed Firms” World Acad. Sci. Eng. Tech. 6:1-28

Phung, D. N., and Mishra, A. V. (2016) Ownership Structure and Firm Performance: Evidence from

Vietnamese Listed Firms. Australian Economic Papers, 55: 63–98. doi: 10.1111/1467-

8454.12056. [Accessed on 17th March, 2016]

RAJI, I (2012). EFFECTS OF OWNERSHIP STRUCTURE ON THE PERFORMANCE OF LISTED

COMPANIES ON THE GHANA STOCK EXCHANGE. Pp.9-49. [Online] Available on:

http://ir.knust.edu.gh/bitstream/123456789/4929/1/Ibrahim%20Raji.pdf [Accessed on 17th

March, 2016].

Ramli. N.M. (2010). Ownership Structure and Dividend Policy: Evidence from Malaysian

Companies. Available on:

http://www.irbrp.com/static/documents/February/2010/16.Nathasa.pdf [Accessed 28/04/2016].

Rokhim, R &Susanto, A.P (2013). The Increase of Foreign Ownership and its Impact on the

Performance, Competition and Risk in the Indonesian Banking Industry. Asian Journal of

Business and Accounting 6(2). [Online]. Available on:

http://ajba.um.edu.my/filebank/published_article/6003/AJBA_5.pdf [Accessed 30/03/2016].

Ruan, W., Tian, G & Ma, S. (2011). Managerial Ownership, Capital Structure and Firm Value:

Evidence from China’s Civilian-run Firms, Australasian Accounting, Business and Finance

Journal, 5(3), 2011, 73-92. Available at: http://ro.uow.edu.au/aabfj/vol5/iss3/6 [Accessed

15/04/2016].

Saravia, J. and Chen, J. (2008). The Theory of Corporate Governance: A Transaction Cost Economics

- Firm Lifecycle Approach. [Online]. Available on:

https://mail.sssup.it/~l.marengo/ENEFfinal/Saravia.pdf [Accessed 18/07/2016].

Scholten, M. (2014). Ownership structure and firm performance: Evidence from the Netherlands.

Available on: http://essay.utwente.nl/65381/1/scholten_BA_MB.pdf (Accessed 23/03/2016).

Shen, C. H., Lu, C. H., & Wu, M. W. (2009). Impact of foreign bank entry on the performance of

Chinese banks. China & World Economy, 17(3), 102-121.

Shleifer Hall, Inc. Beaver, W.H. (1989)., A. and Vishny, R. W. (1997), A Survey of Corporate

Governance, Journal of Finance 52(2)(June): 737-77.

Shleifer, A., and Vishny, R. (1986). "Large shareholders and corporate control", Journal of Political

Economy 95, 461–488

Singh, B. & Singh, M. (2016). Impact of Capital Structure on Firm's Profitability: A Study of selected

listed Cement Companies in India. [Online] available on:

http://www.pbr.co.in/January2016/6.pdf [Retrieved 08/11/2016].

Singh, D. A., & Gaur, A. S. (2009). Business group affiliation, firm governance, and firm

performance: Evidence from China and India. Corporate Governance: An International

Review, 17(4), 411–425. doi:10.1111/j.1467-8683.2009.00750.x [Accessed 03/04/2016].

Smith, M. (1996). Shareholder activism by institutional investors: Evidence from CalPERS. Journal

of Finance 51, 227-252.

ISSN: 2289-4519 Page 37

Srivastava, A. (2011). Ownership Structure and Corporate Performance: Evidence from India.

International Journal of Humanities and Social Science, pp.23-26. Available on:

Http://www.researchgate.net/profile/Aman_Srivastava6/publication/266866976_Ownership_St

ructure_and_Corporate_Performance_Evidence_from_India/links/554190cf2718618dcb8d0.pd

f [Accessed on 16th March, 2016]

Sulong, Z., Gardner, J.C., Hussin, A.H., Sanusi, Z.M. and McGowan, C.B. (2013). MANAGERIAL

OWNERSHIP, LEVERAGE AND AUDIT QUALITY IMPACT ON FIRM

Tian L, Estrin S (2008). “Retained State Shareholding in Chinese PLCs: Does Government

Ownership Reduce Corporate Value?” J. Commun. Econ. 36:74-89

Trien L, Chizema A (2011). “State Ownership and Firm Performance: Evidence from the Chinese

Listed Firms” Org. Mkt. Emer. Econ. 2:7290

Unite, A.A and Sullivan, M.J. (2003). The effect of foreign entry and ownership structure on the

Philippine domestic banking market: Journal of Banking & Finance 27 (2003) 2323-2345.

[Online]. Available on:

http://ebook.nscpolteksby.ac.id/files/Ebook/Journal/2015/Banking%20and%20Finance/Vol.%2

027/Volume%2027%20Issue%2012/The%20effect%20of%20foreign%20entry%20and%20ow

nership%20structure%20on%20the%20Philippine%20domestic%20banking%20market.pdf

[Accessed 18/07/2016].

Uwuigbe U, Olusanmi O (2012). “An Empirical Examination of the Relationship between Ownership

Structure and the Performance of Firms in Nigeria” Int. Bus. Res. 5(1):208-215.

Volonté, C. (2012). Foundations of Corporate Governance. Available on:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1991135 [Accessed 08/05/2916].

Wahla, K.U.R., Shah, S.Z.A. and Hussain, Z. (2012) Impact of Ownership Structure on Firm

Performance: Evidence from Non-Financial Listed Companies at Karachi Stock Exchange.

International Research Journal of Finance and Economics, 84(1), 613.

Wang, J. and Wang, X. (2014). Benefits of Foreign Ownership: Evidence from Foreign Direct

Investment in China. [Online]. Available on:

http://www.dallasfed.org/assets/documents/institute/wpapers/2014/0191.pdf [Accessed

18/07/2016].

Wanjugu, G.E., Kangogo, K.L., Kibet, K.S. and Kisaka, S.E. (2015). THE INFLUENCE OF

OWNERSHIP STRUCTURE AND CORPORATE GOVERNANCE REFORMS ON

PROFITABILITY AND MARKET VALUE OF PRIVATIZED COMPANIES IN KENYA.

[Online]. Available on: http://ijecm.co.uk/wpcontent/uploads/2015/12/31221.pdf [Retrieved

27/03/2016].

Wei Z, Xie F, Zhang S (2005). “Ownership Structure and Firm Value in China’s Privatized Firms:

1991-2001” J. Fin. Quant. Anal. 40:87-108.

Williamson, O. E. (1988). “Corporate Finance and Corporate Governance.” Journal of Finance (July):

567-91.

Zakaria, Z., Purhanuddin, N. and Palanimally, Y.R. (2014). OWNERSHIP STRUCTURE AND

FIRM PERFORMANCE: EVIDENCE FROM MALAYSIAN TRADING AND SERVICES

SECTOR. [Online]. Available on: URL: http://www.ejbss.com/recent.aspx [Retrieved

27/03/2016].

Zeitun, R. and Tian, G. G. (2007) “Does Ownership Affect a Firm’s Performance and Default Risk in

Jordan?” Corporate Governance 7 (1), 66-82.

Zygmont, C. and Smith, M. R., 2014. Robust factor analysis in the presence of normality violations,

missing data, and outliers: Empirical questions and possible solutions. The Quantitative

ISSN: 2289-4519 Page 38

Methods for Psychology, [online] 10(1). Available at:

http://www.tqmp.org/RegularArticles/vol10-1/p040/p040.pdf [Accessed on 21/07/2016].

IJABM is a FTMS Publishing Journal