Embed Size (px)

Citation preview

1

THE IMPACT OF TAXES ON LOCATION DECISIONS

Martin Thomsena, Robert Ullmann

a and Christoph Watrin

a

a School of Business Administration and Economics, Institute of Accounting and Taxation,

University of Muenster, Germany

May 2013

Abstract

In this study, we investigate whether taxes influence the location of real business activities.

To this end, we identify a natural experiment in the German tax regime and find that lower tax

rates in a particular region are associated with firms paying higher wages in that region.

Moreover, our findings show that firms adapt to changes in tax rates over time by making

decisions about locating their workforce that are consistent with the hypothesis of tax-induced

income shifting. We conclude that the frequently employed argument that business income

shifting is undertaken primarily through accounting changes does not necessarily hold; thus,

in addition to reducing the income of domestic firms, unfavorable changes in the tax system

may also reduce domestic investment and curtail real business activity.

2

THE IMPACT OF TAXES ON LOCATION DECISIONS

1. Introduction

Although it is well established in accounting research that profits are shifted on the

merits to low tax jurisdictions to minimize consolidated tax rates, the exact channels of in-

come shifting are not yet well understood. An in-depth understanding of these channels is

important, however, because policy makers should be aware of all of the effects that are em-

bodied in changes in tax systems — particularly in light of increasing global tax rate competi-

tion. Consequently, Shevlin et al. (2012), among others, have recently called for further re-

search into the exact channels of how income shifting is implemented in multinational enter-

prises because such research would be particularly relevant if it were possible “[…] to […]

test whether firms are shifting real operations or relying on accounting-based methods of

income shifting.” In this study, we investigate specifically whether tax rates influence loca-

tion decisions.

It has often been argued that accounting methods are used to shift income between

countries with different tax rates because of the relatively low cost of this strategy (e.g., Har-

ris 1993; Klassen et al. 1993; Shackelford and Shevlin 2001; Devereux and Maffini 2007;

Huizinga and Laeven 2008).1 However, the tangible overall business activity of a country

might be unaffected by cross-border tax rate differentials — or even increase as a conse-

quence of the higher investment potential for domestic firms caused by lower consolidated tax

rates. Of course, revenue-maximizing policy makers understand that most developed coun-

tries rely considerably more on personal income taxes than on business taxes. Thus, in gen-

eral, shifting business income based on accounting decisions might be negligible in terms of a

country’s tax revenue if the individual incomes of the country’s residents remain largely un-

1 Income shifting via accounting decisions means contracting and includes setting transfer prices, debt, or

licensing intangible property.

3

changed (i.e., if the tangible business activity of a country was unchanged) or if the initial

shifting of business income might be offset by the subsequently higher potential for tangible

investment by domestic firms. In such an environment, policy makers — contrary to intuition

— might not have an incentive to engage in global competition with respect to business tax

rates or may, in fact, encourage a decrease in tax rates in nearby foreign countries for their

own country’s advantage. In this light, policy makers must understand the exact channels of

income shifting that multinational enterprises employ.

Despite its importance, research on the exact channels of income shifting is hindered

by data availability. As a consequence, most available research merely investigates whether

income shifting occurs on its merits — without isolating the means of income shifting (for an

overview, see Shackelford and Shevlin 2001 and Devereux and Maffini 2007). The prior liter-

ature focuses specifically on accounting decisions that result in income shifting, such as

changes in transfer pricing (e.g., Newberry and Dhaliwal 2001; Mills and Newberry 2004;

Blouin et al. 2012) and selective location of debt (e.g., Froot and Hines 1995; Newberry and

Dhaliwal 2001) or intangibles (Dischinger and Riedel 2011; Karkinsky and Riedel 2012). The

body of research on altering tangible business activity as a means of shifting business income

is considerably smaller because of limited data availability (Shevlin et al. 2012). Against this

background, our research design takes advantage of a peculiarity in the German tax system:

for purposes of the so-called "trade tax", each local municipality determines its own individu-

al rate, and there were 12,266 municipalities in Germany in 2007. Firms are liable for trade

tax in a municipality if they have a permanent establishment therein. When a given firm has

permanent establishments in more than one municipality, formulary apportionment is used to

allocate the trade tax base to the relevant municipalities, and wages paid in a municipality are

used as the allocation key. Thus, to shift income to a municipality with a favorable trade tax

rate, a transfer of personnel (more specifically, of wages paid) and a change of tangible opera-

4

tions are inevitable. Conversely, accounting changes have no effect on the allocation of a

firm’s trade tax base between municipalities.

We note that wages paid are a particularly well-suited proxy for investigating tax-

induced location decisions for several reasons. First, wages paid can be measured with mini-

mal error. Most particularly, wage taxes in Germany are levied directly at the source firm, so

data are not estimated or rounded. Moreover, the data are explicitly audited by tax authorities.

Second, wages paid cannot realistically be shifted without actual changes in headcount, i.e.,

without changes in location decisions.2 Finally, wages paid are a better proxy for tangible

business activity than other measures that are also often discussed as allocation keys in formu-

lary apportionment, such as sales or total assets. Sales can be manipulated without difficulty

by adjusting intra-group trades, and total assets are generally subject to considerable discre-

tion for accounting purposes, such as in the assessment of their fair value.

We acknowledge that there are tax regimes that use formulary apportionment in other

countries (e.g., state tax in the U.S.). However, regarding research on location decisions, the

German trade tax has several notable advantages. First, the wording and application of the

trade tax law is exactly the same for each municipality; thus, variation in the trade taxation

regimes between municipalities is solely derived from differences in the trade tax rates. Fur-

thermore, tax audits are conducted at the level of the firm; thus, the total trade tax base is not

affected by its allocation among municipalities. Second, wages paid affect only the allocation

of the trade tax base, and other taxes are not affected. Third, other tax laws (e.g., corporate

tax, labor tax, value added tax) and non-tax laws (including labor laws) are largely identical

2 We note that tax planning based on accounting decisions would theoretically also be possible by simply in-

creasing the wages of employees in municipalities with low trade tax levy rates. However, wages (and ancil-

lary wage costs) are in fact paid out in full to a third party (i.e., employees) and are thus full expenses from

the perspectives of the firm and the entire consolidated group (a slightly different rationale might hold in the

case of the employment of family members or close friends, but these rare and arguably negligible cases are

not addressed here). Moreover, given Germany’s strong labor laws, increases in wages cannot generally be

reversed in the future; thus, such a strategy would be almost prohibitively inflexible. In sum, the strategy of

purposefully increasing the wages of selected individuals for purposes of a firm’s trade tax planning is not an

economically sensible strategy and is even anecdotally unheard of.

5

between municipalities because the relevant laws are created on a national level and national

courts are in place that specialize in different areas of laws to guarantee homogenous applica-

tion (e.g., one national court for tax law, one national court for labor law, and the supreme

court). Fourth, trade taxes are economically relevant to the firm. Roughly speaking, trade tax-

es account for approximately 40 % of the corporate income tax burden and approximately

30 % of the income tax burdens of other types of business entities (e.g., for sole proprietor-

ships). Fifth, there are many municipalities in Germany, and trade tax rates vary between 0 %

and 31.0 %, which indicates that considerable variation can be found in the data. Sixth, gen-

eral institutional factors, such as the stability of the government (central and local), function-

ality of public authorities, infrastructure, availability of finance, unemployment support, and

antitrust regulations, are similar throughout Germany. Finally, because of Germany’s relative-

ly small geographic dimensions, any unobservable variables — such as tax-paying mentality

— are likely more similar in our data than in cross-border studies (e.g., Klassen and Laplante

2012b) or compared to within-country studies in geographically larger and culturally more

heterogeneous countries, such as China (e.g., Shevlin et al. 2012) or the U.S. (e.g., Gupta and

Mills 2002).

We obtained access to a confidential dataset from the German fiscal authorities that

includes full trade-tax returns for all German-based commercial firms for the years 2001,

2004 and 2007 (5,116,719 firms). Our main set of tests focuses on the subset of firms that

have permanent establishments in more than one municipality. In our cross-sectional analysis,

we find that a greater share of total wages paid on the firm level is allocated to permanent

establishments in municipalities with relatively low trade tax rates. We also report that firms

with greater incentives to shift trade tax bases between municipalities (proxied by a higher tax

rate differential between the maximum trade tax rate and the minimum trade tax rate within a

firm) indeed exhibit relatively more income shifting with respect to these “extreme” munici-

6

palities. Following this cross-sectional analysis, in a panel analysis, we analyze how changes

in trade tax rates impact firms’ behavior over time and find evidence that firms react to

changes in trade tax rates with changes in location.

This study connects to three major research issues in international taxation. First, it fits

directly into the growing body of research on cross-border business income shifting in multi-

national enterprises. Such research is vital because global tax rate competition is increasing

the pressure on the tax revenues of developed countries. Second, in the U.S., multistate-level

research has been conducted to a notable extent in the past that has been aimed at investigat-

ing cross-state income shifting under a formulary apportionment regime. However, data avail-

ability is a key concern in this respect. The unique data and setting that are the focus of this

study offer a deeper understanding of the behavior of firms under formulary apportionment

between regions within one country that might be transferred to the U.S. context, although

allocation keys and further details might differ. Finally, the EU continues to debate a common

consolidated corporate tax base, which considers a joint tax base computation scheme for all

EU firms and an allocation of resulting tax revenue to member countries based on formulary

apportionment. Admittedly, this project has moved slowly because of the considerable politi-

cal disputes among member countries. However, there appears to be a common understanding

that the arm’s length standard that is currently applied has its flaws — some that are rather

serious to the public finances of certain EU member countries — and that formulary appor-

tionment might have the potential to increase the efficiency and effectiveness of tax systems

in the EU.

We contribute to the available literature on multinational enterprise income shifting by

exploiting a unique data set in a well-defined natural experiment at the firm level to show that

taxes impact location decisions. Our analysis arguably does not suffer from self-selection bias

because we have obtained data on all commercial firms in Germany. Furthermore, we use

7

genuine tax data; therefore, no estimation of any tax effects from accounting data is neces-

sary. Given these factors, we present a distinctive analysis of the effects of taxes on the be-

havior of firms.

The remainder of this paper is organized as follows. Section 2 provides a short over-

view of the institutional details of the German trade tax system. We review the empirical lit-

erature in Section 3 and subsequently develop hypotheses in Section 4. Section 5 describes the

data and the research design. We present our results and discuss robustness tests in Section 6,

and conclusions and summary comments are provided in Section 7.

8

2. Institutional Details of the German Trade Tax System

Politically, the Federal Republic of Germany has 16 states, and each state has several

districts (there are a total of 470 districts). Each district is subdivided into municipalities

(12,266 municipalities overall). Trade taxes collected are available to the municipalities di-

rectly and represent a major source of their public financing. Every municipality has the right

to set its trade tax rate independently but must apply the same national trade tax code and may

only collect taxes from firms that have a permanent establishment in its geographic area. Con-

sequently, competition is fierce among municipal governments to attract firms to establish

facilities in their municipalities.

From an empirical point of view, economically important municipalities — such as

Munich or Cologne — have higher trade tax rates (approximately 19.7 %) than lesser-known

municipalities that are mostly located in rural areas (some have tax rates as low as 0 % to at-

tract businesses).3 Consequently, there is a variety of trade tax rates in Germany (in our sam-

ple, between 0 % and 31.0 %, with a mean of 14.3 %). With the addition of general corporate

income taxes, the total corporate tax burden is approximately 35 % to 40 %, on average, dur-

ing our sample period; the individual income tax burden for high-income individuals amounts

to approximately 45 % (including the trade tax). Thus, the trade tax is an economically rele-

vant factor in firm decisions.

With respect to its legal application, the trade tax base is generally derived directly

from financial accounting income (with certain specific adaptations for trade tax purposes). It

is computed and audited on the firm level (in a single-firm financial statement tax audit).

When a firm has permanent establishments in more than one municipality, the firm-level trade

3 To calculate the trade tax rate, we compute the following: trade tax rate = trade tax levy rate / (trade tax levy

rate + 2000 %). This computation correctly considers the marginal statutory basic federal rate in our sample

period of 5 % (paragraph 11 of section 2 of the trade tax code) and the fact that the trade tax is deductible

from its own tax base (known as the circularity problem with German trade tax). Trade tax levy rates in our

sample period vary between 0 % and 900 %, with a mean of approximately 333 %.

9

tax base is allocated in a formulary apportionment regime with respect to the different munic-

ipalities, and trade taxes are paid directly to the municipalities accordingly. The sole alloca-

tion key in this regard is wages paid.4 Ceteris paribus, the allocation of wages paid between

municipalities has no direct impact on the financial statement of a firm, whereas a potential

decrease in the trade tax indirectly impacts net income. If a firm has only one permanent es-

tablishment, wages paid are irrelevant in the calculation of the trade tax burden.

As a result, when considering individual firms with permanent establishments in more

than one municipality, income shifting for trade tax purposes is only possible by changing

locations. In particular, changes in transfer prices on transactions between several permanent

establishments or the deliberate allocation of debt and intangible property has no impact on

the allocation of the trade tax base among the firm’s permanent establishments. Consequently,

the German trade tax system offers a unique natural experiment to analyze the effect of tax

rates (or tax rate changes) on location decisions.

4 We note that there are rare and exceptional cases, such as for firms with wind power stations (which general-

ly have limited permanent personnel) in which allocations are based on both wages paid (30 % weight) and

the value of property, plants, and equipment (70 % weight).

10

3. Literature Review

3.1 Overview

We investigate whether firms alter their “real” business activity — i.e., the allocation

of tangible resources — in response to tax incentives. Consistent with Gunny (2010), we dif-

ferentiate between two major channels of income shifting, which we denote as accounting

decisions and location decisions. Accounting decisions are broadly defined as any accounting

choice within generally accepted accounting principles (GAAP) that aims at “hiding” true

economic results (Dechow and Skinner 2000). In particular, we include transfer-pricing

changes because they are technically accounting decisions. Moreover, we include matters

such as changes in the financing structure (e.g., the tax-optimal allocation of debt) or in the

location of intangible property. We argue that these changes to business activity are relatively

easy to implement and reverse — compared, for instance, to the establishment of new facto-

ries and the relocation of employees — and are thus considered accounting decisions. Other

matters are included when they fulfill those requirements. On the contrary, a firm might gen-

erally decide to decrease its tax burden by location decisions, which we define as changing

the structure or timing of the firm’s tangible operations. Location decisions include reallocat-

ing factory equipment, such as machinery, or of personnel.

We first briefly discuss research on income shifting on its own merits and its determi-

nants; however, we refer to a review of the available literature in this area to avoid unneces-

sary repetition. Most research falls into this relatively broad category. Subsequently, we dis-

cuss the two threads of research that focus specifically on the effect of accounting decisions

on income shifting and, alternatively, on the effect of location decisions on income shifting

separately.

11

3.2 Income shifting on the merits

It is well documented that firms react to tax incentives by shifting income across juris-

dictions (for a detailed overview, see Shackelford and Shevlin 2001 and Devereux and Maf-

fini 2007). The consolidated tax burden decreases when income is shifted from a high-tax

jurisdiction to a low-tax jurisdiction. Because this shifting also generally leads to a decrease in

the tax base in a firm’s domestic country, policy makers in well-developed countries (with

relatively high tax rates) have become increasingly concerned about the possible tax revenue

losses that income shifting might evoke (Klassen and Laplante 2012b).

The first studies to investigate the cross-border income shifting of multinational firms

were Harris 1993 and Klassen et al. 1993. Both studies investigated whether tax rate differ-

ences between the parent company and its subsidiaries leads to income-shifting incentives.

Huizinga and Laeven 2008 were the first to investigate the extent and effect of tax rate differ-

entials on cross-border income shifting specifically between the subsidiaries of a multination-

al firm (rather than between a parent firm and subsidiaries). They find that income shifting

can also be observed between different subsidiaries and that this income shifting is ultimately

comparable to that between a parent firm and its subsidiaries.

Income shifting on the merits within one specific jurisdiction was investigated by

Gramlich et al. 2004, who relied on the specific Japanese setting of so-called keiretsu groups.5

A benefit of keiretsu groups is the possibility of effortlessly shifting income among member

firms. Using this setting, Gramlich et al. 2004 demonstrate that tax-induced income shifting

can be observed because high-tax-rate keiretsu group firms shift income to relatively low-tax-

rate firms in the same keiretsu group.

5 Keiretsu groups are diversified groups of manufacturing and trading firms that share the same financial insti-

tutions and adopt coordinated business strategies. They represent a significant portion of Japan’s economy.

12

Consistent with most recent research, Klassen and Laplante 2012b examine the long-

term cross-border income shifting of U.S. multinational firms. By considering two full dec-

ades of data, they investigate how income shifting behavior has changed over time and report

that income shifting has increased significantly — mainly because of declining regulatory

costs. Along the same lines, a previous study by Grubert 2003 has generally shown a negative

association between income shifting and the costs of income shifting. With increased globali-

zation, income shifting thus appears to be an ever-increasing phenomenon.

3.3 Accounting decisions

Previous research regarding the impact of accounting decisions on income shifting fo-

cuses largely on transfer prices, financing structures, and the location of intangible property.

Arguably one of the most important means of shifting income is the purposeful adjustment of

transfer prices on intra-firm trades. Intra-firm trading is economically relevant in magnitude

and constitutes approximately 40 % and 20 % of the U.S. and worldwide trading volumes,

respectively (Tang 2002). Transfer pricing changes might be particularly easy to implement

when cross-border transactions already exist because they must only be readjusted. Some ear-

lier studies in this area concentrate on the specific techniques that are used to shift income

from one jurisdiction to another (Newberry and Dhaliwal 2001; Mills and Newberry 2004).

For example, the types of balance sheet items most suitable for to set transfer prices in a tax

optimal manner have been investigated.

Other studies concentrate on the possible conflicts surrounding transfer price setting

for minimizing income tax and pursuing other firm goals (some of which might also be tax

related). In this context, Blouin et al. 2012 are the first to consider the conflict between trans-

fer prices and customs duties (‘all tax’). The authors mainly argue that high transfer prices on

goods delivered from low-tax jurisdictions to high-tax jurisdictions might minimize income

tax payments while concurrently evoking high customs duties — and vice versa. They find

13

that when income taxes and customs duties cannot be optimized simultaneously, considera-

tions involving the planning of customs duties outweigh income tax considerations. An eco-

nomically similar conflicting situation theoretically arises when transfer prices compete

against internal performance measures, such as schemes of internal management accounting

(Baldenius et al. 2004, Tang 2002).

Research on financing structures generally investigates whether firms shift debt into

high-tax jurisdictions to deduct interest payments and save taxes. To investigate this research

question on the merits, previous research has relied on tax reforms, such as the 1986 Ameri-

can tax reform, in which the tax benefits of foreign debt were decreased because of the intro-

duction of a foreign tax credit limitation. Newberry 1998 shows that this regulation leads

firms to reduce their domestic debt and issue more equity. This finding is consistent with that

of Collins and Shackelford 1992, who also report that U.S. firms issue more (preferred) stock

in reaction to the tax reform. Froot and Hines 1995 find that debt is reduced as a reaction to

the tax reform but cannot confirm the use of more equity. In addition to the rather isolated

effect of firms' reducing U.S. debt holdings, it has also been reported that the American tax

reform of 1986 in fact resulted in a shift of debt to low-tax foreign subsidiaries (Smith 1997;

Newberry and Dhaliwal 2001).

With a specific focus on the magnitude of income shifting from financing structure

decisions, Desai et al. 2004 compute that a 10 % increase in the tax rate is associated with

2.8 % more debt. Using European samples, Mintz and Weichenrieder 2005, Huizinga et al.

2008, Buettner et al. 2012 and Buettner and Wamser 2013 compute similar elasticities.

Regarding the allocation of intangible property, Dischinger and Riedel 2011 find that

in a setting of multinational firms domiciled in Europe, subsidiaries subject to relatively low

tax rates have more investments in intangible properties compared to subsidiaries subject to

relatively high tax rates. Similar results can also be shown more specifically for patents

14

(Karkinsky and Riedel 2012). These findings are consistent with the hypothesis that differ-

ences in tax rates lead to an allocation of intangible property such that license fees are deduct-

ible in high-tax jurisdictions and subject to taxation in low-tax jurisdictions.

We finally note that research on the repatriation of U.S. domestic firms connects to

research on income shifting by means of accounting decisions (see for example Altshuler and

Newlon 1993; Altshuler et al. 1995; Desai et al. 2001; Altshuler and Newlon 2003; Altshuler

and Grubert 2003; Krull 2004; Clausing 2005; Blouin and Krull 2009; Albring et al. 2011).

Thus, in a recent study, Klassen and Laplante 2012a investigate the impact of both reinvest-

ment-related incentives and incentives that stem from financial reporting income shifting

(similarly also: Collins et al. 1998; Newberry and Dhaliwal 2001; Mills and Newberry 2004).

Regarding the latter, in particular, they find that firms with higher financial reporting-related

incentives for earnings management are more aggressive in income shifting compared to other

firms. Desai et al. 2012 find that U.S. multinational enterprises use trade credits to allocate

capital from foreign low-tax jurisdictions to the U.S, which is arguably in response to the re-

patriation taxation regime.

3.4 Location decisions

Research has also begun to investigate the effects of tax incentives on the location of

tangible business activity. Because of data limitations in this field, such work must depend

considerably more on surveys, highly aggregated data or specific circumstances than the re-

search discussed above. We intend to add to this line of research by using a rather broad da-

taset (all commercial firms in Germany) with access to in-depth information (on the level of

the firm and to permanent establishments).

Single 1999 surveys 66 tax executives of major U.S.-based multinational firms in the

manufacturing industry to evaluate the importance of location-specific factors. In this study,

15

only five of the 29 factors are tax related, and all five tax factors ranked among the lower half

in importance for the location decision. Hence, she finds evidence that tax effects are of lim-

ited importance to location decision changes or that “tax might just follow business”. In a

more recent study, Graham et al. 2011 conduct a considerably larger survey of nearly 600 tax

executives and note that 44 percent of the respondents consider the deferral of tax expenses

that are reported in financial statements to be relevant for their decision to reinvest foreign

earnings outside of the U.S. Based on this finding, Graham et al. 2011 argue that possibly

(and legally) avoiding or deferring the recording of income tax expenses for financial ac-

counting is an important consideration in undertaking real investment. Because such a possi-

bility arises from foreign business activity, these findings indicate that financial accounting

for tax purposes has an impact on firms’ location decisions.

Research considering multiple states within one country often relates to tangible busi-

ness activity because tax bases are generally allocated based on formula apportionments with

allocation keys that are affected by location decisions. In their overview article, Shackelford

and Shevlin 2001 point out that multistate research has the advantage that non-tax factors are

more homogenous between states than between countries (although state tax regimes may

fundamentally differ). As a result, the multistate research arena provides an attractive setting

for empirical tests of the mechanisms used in jurisdictional tax planning. However, most of

the studies on multistate taxation (e.g., Klassen and Shackelford, 1998 and Lightner, 1999)

have conducted such tests with macro data aggregated at the state level. Firm-level data are

rarely available and cover only specific circumstances when they are available.

In the U.S., the formulary apportionment method is generally applied, with the alloca-

tion key being based on the portion of property, wages, and sales in each state6. Whereas

property and wages are considered to be factors indicating tangible business activity in the

6 State taxation schemes in the U.S. vary in the weights assigned to different factors; 13 states use equally

weighted formulas, 23 states double-weight sales and six states weight sales more than 50%.

16

definition in which it is used here, sales might at least partly be affected by accounting deci-

sions, such as transfer pricing. Apart from the exact allocation keys, the system is ultimately

similar to the German trade tax system (for details refer to Chapter 2). In this regard, Gupta

and Mills 2002 report that corporations doing business in several U.S. state jurisdictions with

different tax treatments have both greater incentive and more opportunities to shift income.

Specifically, a firm’s effective state tax rate generally decreases with the number of states in

which it files tax returns and firms use so-called sales factor apportionments to reduce effec-

tive tax rates, which confirms our conjecture that sales might be most influenced by non-

location decisions. Their findings are consistent with the previous work of Klassen and

Shackelford 1998 and Boucher 1993, who similarly report that the sales apportionment factor

lends itself most to state tax avoidance opportunities because it can be manipulated through

legal changes and accounting adaptations. Petroni and Shackelford 1995 and Petroni and

Shackelford 1999 conduct research at the firm level in U.S. multistate taxation and find that

state tax rates have a significant effect on the behavior of property-casualty insurers.

Other countries also provide valuable research opportunities for multiregional re-

search. Using a Canadian dataset from 1983-1991, Klassen and Shackelford 1998 report that

firms use a rather specific form of tax avoidance: manufactured shipments and their cross-

state taxation. Their results are consistent with firms strategically structuring their shipments

to reduce sales reported to states with relatively high reliance on the sales for taxation. Most

recently, Shevlin et al. 2012 investigate the effects of local tax incentives in Chinese sub-

national jurisdictions on income-shifting by Chinese national firms. In China, the central gov-

ernment has structured a set of regional tax incentives (e.g., economic zones, high-tech devel-

opment zones). Using hand-collected data (the final sample contains 320 firms), Shevlin et al.

2012 present evidence that income shifting towards low-tax regions within China occurs. Re-

grettably, with the data set at hand, they ultimately cannot distinguish whether the income

17

shifting is based primarily on accounting decisions (e.g., via transfer pricing adaptions) or on

changes in tangible operations.

Finally, archival literature exists regarding settings that allow investigations of loca-

tion decisions between multiple countries (see, for instance, Hines Jr 1997; Devereux and

Griffith 1998; De Mooij and Ederveen 2003; Buettner and Ruf 2007). Boskin and Gale 1987

find that a tax rate decrease (or a tax benefit) is associated with increased foreign direct in-

vestments. Similarly, Grubert and Mutti 2000 find that average effective tax rates have a sig-

nificant effect on the choice of investment location and also on the amount of capital invested.

We note that most of the literature on cross-border location decisions focuses on foreign di-

rect investments (Hanlon and Heitzman 2010). Most studies in this area confirm that the tax

rate in the subsidiary’s country is an important factor when considering investments (e.g.,

Hartman 1985; Grubert and Mutti 1991; Hines and Rice 1994; Swenson 2001). We note that

the German Federal Reserve Bank makes available a dataset pertaining to the foreign direct

investments of domestic German firms with foreign subsidiaries and of foreign firms invest-

ing in Germany (MiDi database). Research using this specific database has generally reported

that tax rates affect firms’ investment decisions (Weichenrieder 2009, Ruf and Weichenrieder

2012). Ultimately, cross-border research on location decisions faces the issue of considerable

heterogeneity between countries (which is greater than between regions within one country).

18

4. Hypotheses Development

4.1 Trade tax rates and tax base allocation to facilities (cross-sectional analysis)

Changes in real operations are complex, and many non-tax factors are to be consid-

ered, including, but not limited to, local infrastructure, labor supply, (business) culture, eco-

nomic and political risk, geographic distance to customers, and costs of capital in segmented

global capital markets. Based on this observation, it has been argued that when different tax

rates apply in different locations, firms typically do not alter their location decisions in re-

sponse to this tax incentive but instead use accruals manipulation to shift income to low-tax

jurisdictions (e.g., Harris 1993; Klassen et al. 1993; Huizinga and Laeven 2008).

In this context, Shevlin et al. 2012 explicitly interpret their findings to mean that in-

come shifting in China through accounting decisions is more likely than reallocating real op-

erations and that lower local tax rates are not automatically associated with greater levels of

real investment. Ultimately, however, Shevlin et al. 2012 acknowledge that it is impossible

for them to clearly distinguish between accruals manipulation and changes in real operations

because they “[…] do not have data on the assets located within each subsidiary of the con-

solidated group”. Similar to Shevlin et al. 2012, we focus on one country with tax rate varia-

tion across regions, which has the advantage that country-specific institutional factors are

largely similar, particularly in well-developed and (relatively) geographically small countries,

such as Germany. Germany also provides considerable variation in its municipal trade tax

rates (i.e., ranging from 0 % to 31.0 %).

For the sake of simplicity and comprehensibility, we derive our hypotheses based on a

hypothetical firm A. Firm A is in no way representative or even realistic, but this method al-

lows for a straightforward discussion of the expected effects in our setting. We assume the

following initial situation: firm A has total wages paid that amount to $6,000 and are paid to

19

personnel in two facilities in two different municipalities. These municipalities are exactly

alike in all parameters. In this case, an average firm A should be indifferent about where to

locate its assets and personnel; thus, it should allocate personnel equally between facility 1

and facility 2 (each $3,000).

Figure 1: Example Initial Situation.

We continue our example and change only the tax rates for one of the hypothetical

municipalities. Firm A now faces a tax rate of 25% in facility 1 and a tax rate of 15% in facili-

ty 2. As a consequence, firm A has a tax incentive to allocate relatively more wages paid to

facility 2 than to facility 1. The allocation of wages paid might be as follows:

Figure 2: Example for H1a.

If we were to apply our example strictly and without transaction costs, to minimize its

tax burden under the German trade tax regime, firm A would, ceteris paribus, shift all person-

nel to facility 2. However, because of non-tax factors in real location decisions (e.g., geo-

graphic distance to valuable customers in municipality 1), this extreme result does not occur.

We note at this point that no decrease in tax burden would result from a mere accounting allo-

cation of income to facility 1 or facility 2. Technically, we hypothesize the following (all hy-

potheses in the alternative form):

Tax Rates Wages Paid

t0 t0

Facility 1 25% $3,000

Facility 2 25% $3,000Firm A

Tax Rates Wages Paid

t0 t0

Facility 1 25% $1,000

Facility 2 15% $5,000Firm A

20

H1a: The wages paid with respect to a particular facility are higher if the trade tax rate is

lower and vice versa.

Exploring this argument further, ceteris paribus, an incentive to shift income within a

firm is greater if the tax rate differential between the lowest and highest tax rates applicable to

any facility is higher. In our example, assume two different cases:

Figure 3: Example for H1b.

Firm A would naturally have a greater tax incentive to shift income from facility 1 to

facility 2 in case 1 than in case 2. Thus, the net benefit of reallocating employees would be

larger in case 1. We thus hypothesize the following:

H1b: The larger the trade tax rate differential of a firm (∆intra-period(Tax Rates)), the larger its

wages paid differential will be (∆intra-period(Wages Paid)) and vice versa.

Tax Rates Wages Paid

Case 1 t0 t0

Facility 1 25% $1,000

Facility 2 15% $5,000

∆ intraperiod 10 -$4,000

Case 2 t0 t0

Facility 1 25% $2,000

Facility 2 20% $4,000

∆ intraperiod 5 -$2,000

Firm A

Firm A

21

4.2 Changes in trade tax rates and tax base allocations to facilities over time

(panel analysis)

Despite treating data as cross-sectional in H1a and H1b, the available data in fact have

a panel structure. Thus, we investigate in the following how firms react to changing trade tax

rates over time. Consider the two cases in the continued example:

Figure 4: Example for H2a.

When considering only facility 2 in case 1, the firm faces a decrease in local tax rates

from 20 % to 15 % over time. Consequently, ceteris paribus, the firm might shift personnel

into the facility (wages paid increase from $4,000 to $5,000), with a corresponding decrease

in facility 1 (wages paid decrease from $2,000 to $1,000). Alternatively, considering case 2,

in which facility 2 faces a more distinct decrease in local tax rates from 20 % to 10 %, the

effects should be even stronger. Vice versa, an increase in tax rates at facility 1 should have

the economically opposite effect in both cases. We hypothesize the following:

Case 1 t0 t1 t0 t1

Facility 1 25% 25% $2,000 $1,000

∆ interperiod

Facility 2 20% 15% $4,000 $5,000

∆ interperiod

Case 2 t0 t1 t0 t1

Facility 1 25% 25% $2,000 $500

∆ interperiod

Facility 2 20% 10% $4,000 $5,500

∆ interperiod

Firm A0 not considered in H2a

-10 $1,500

Tax Rates Wages Paid

0 not considered in H2aFirm A

-5 $1,000

22

H2a: The larger the increase in the trade tax rate for a particular facility over time

(∆inter-period(Tax Rates)), the larger the decrease in wages paid of that facility over time

will be (∆inter-period(Wages Paid)) and vice versa.

23

5. Sample Selection and Research Design

5.1 Sample selection

We use a unique dataset from the German fiscal authorities. The dataset contains con-

fidential tax return data for the full population of all German commercial firms that were sub-

ject to trade tax in 20017, 2004, and 2007. This dataset includes data from corporations, part-

nerships and single entrepreneurs. Data are available at the level of single tax payers (single

firms) but excludes any identifying information. We merge this confidential dataset with a

regional dataset to insert economic variables on the district level into our analyses.

Our sample selection criteria are described in Table 2. We begin with the full popula-

tion of German firms liable for trade tax and their complete annual trade tax return infor-

mation. Our initial sample contains 5,116,719 firms with 9,720,291 facility-years. We exclude

firms that do not contain cases of trade tax allocation by means of formulary apportionment

(i.e., firms without a permanent establishment in more than one municipality), which reduces

our sample to 278,918 firms (2,012,817 facility-years). We exclude firms with missing values

for trade tax levy rates or missing identifying municipality codes (23,064 firms excluded).

Additionally, we limit our investigation to firms turning a profit, i.e., we exclude loss firms

and firms with loss carryforwards as reported on their tax returns (92,972 firms excluded).

Moreover, we eliminate all firms for which trade tax base allocation is not conducted with

regard to wages paid (976 firms excluded)8. Finally, we exclude all firms in which the sum of

total wages paid for a firm is equal to zero (19,830 firms excluded). Our resulting main sam-

ple thus consists of 617,262 facility-years from 142,076 firms.

(Insert Table 2 about here)

7 We convert 2001 values, which are in the currency Deutsche Mark, to the Euro by dividing the Deutsche

Mark values by the relevant factor 1.95583. 8 Refer to Footnote 4 for a discussion. By eliminating these firms, we ensure that only tangible income shifting

firms are investigated.

24

For inter-periodic analyses, we must further ensure that a specific firm can be followed over

time. Therefore, we exclude all firms that exist in only one of the three sample periods (i.e.,

only in 2001, 2004 or 2007),9 which reduces our sample to 21,589 firms (199,575 firm-years).

5.2 Research design

5.2.1 Trade tax rates and the tax base allocation to facilities (cross-sectional analysis)

To implement the intra-periodic approach for H1a, we treat our dataset as cross-

sectional and estimate equation (1a) using OLS10

:

where is wages paid for each facility of firm i in municipality j, scaled by total wages

paid for each firm i.11

is the trade tax rate of municipality j in which the facility is

domiciled (with the trade tax levy rate being linearly transformable to the trade tax rate, as

discussed in Section 2) scaled by the weighted average trade tax rate of firm i.12

We then con-

trol for firm-level variation. The matrix includes one non-dichotomous varia-

ble ( of each firm) and four firm-specific dummy variables:

, , , and We further control for

regional factors using a variety of macroeconomic variables. The matrix

includes the following three different municipality-specific varia-

9 There are several reasons why firms exist in only one of the three sample periods, including bankruptcy,

termination of business, establishment after 2004, or a changed tax ID. 10

A description of all variables used in this manuscript can be found in Table 1 11

If a firm has more than one permanent establishment in the same municipality, these permanent establish-

ments are consolidated and considered as one joint facility. The reason for this is straightforward. Within one

municipality, the trade tax rate for every facility is equal at all points in time. Thus, when investigating the

shifting behavior of a firm, we are interested in how many wage earners are allocated toward a specific mu-

nicipality (thus a specific trade tax rate) on the firm level. Thus, different permanent establishments of one

firm in only one specific municipality are a formal distinction of German tax law, which is not relevant to our

economic analysis at this point. 12

We scale the tax rate for each facility by the weighted average tax rate of the firm because firms face differ-

ent average levels of trade tax. Under these circumstances, tax-induced incentives on the level of an individu-

al municipality impact firms and scaling controls for this effect differently.

25

bles: , and . The matrix

includes more than 15 district-specific variables:

,

,

, , and , where k is the

anonymized district identifier. We anticipate that a higher trade tax rate is associated with

lower total wages paid for a particular facility; thus, consistent with H1a, we predict < 0.

In H1b, we ask whether firms with large trade tax rate differentials (i.e., a large differential

between the highest trade tax rate and the lowest trade tax rate within one firm) shift more

tangible operations into the extremal municipalities compared to firms with small trade tax

rate differentials. Thus, we estimate equation (1b) as the following:

where is the difference in the wages paid between the facility with the highest

and the facility with the lowest trade tax levy rate within one firm i scaled by total wages paid

for each firm i. We create four equally sized bins of trade tax rate differentials (i.e., the differ-

ences between the maximum and the minimum of TaxRatei for a single firm i within one par-

ticular year). Firms with a trade tax rate differential in the lowest quartile of the sample (i.e.,

firms with relatively small tax-induced shifting incentives) fall into the first , labeled Diff. Tax

Rate 0-25%, and so forth for the other three bins. The municipality-and district-level controls

from equation (1a) are computed as the differential between the facility with the highest trade

tax rate and the facility with the lowest trade tax rate. Considering H1b, we expect that the

26

significance and level of personnel located in facilities in low-tax municipalities will be high-

er in a bin that has higher incentives in terms of shifting income ( < < 0).

5.2.2 Changes in trade tax rates and tax base allocations to facilities over time (panel analysis)

The second part of our analysis investigates how firms react to varying tax rates over

time. To test H2a, i.e., whether firms react to time-varying trade tax rates with tangible

changes in business activity (i.e., in our study, through personnel shifting), we employ the

following equation (2a):

where is the first difference of total wages paid between periodt and periodt-1 for

each facility of firm i, both scaled by total wages paid of each firm i of the particular year.13

We create four equally sized upward and downward bins of the first difference of the

TaxRatej,t between periodt and periodt-1 for each municipality j, both periods scaled by the

weighted average trade tax rate of the firm i of the particular year. Firms with a upward

(downward) first difference in the lowest quartile of the sample fall into the first bin, labeled

, and so forth for the other three bins.

All control variables discussed above are likewise included as first difference variables.14

We

13

More precisely, period t and t-1 means 2007, 2004, and 2001. 14

In so doing, we control for the fact that the change in personnel shifting might also be caused by a change in

the unemployment rate from 2001 to 2004, for example, and not by the change of the trade tax levy rate.

27

expect that a higher positive (negative) first difference in the tax rate from one period to an-

other is associated with a higher negative (positive) first difference in total wages paid for a

particular facility. Therefore, consistent with H2a, we predict that < < 0 and

< < 0.

28

6. Empirical Results

6.1 Descriptives

Table 3 shows the descriptive statistics for the main and control variables in our regres-

sion models, which are on a firm, municipality or district level. The mean of , which

is defined as the wages paid for each facility of a firm i in municipality j scaled by the total

wages paid by each firm i, is 0.31. Our main variable of interest, which is the trade

tax rate of the municipality j in which the facility is domiciled scaled by the weighted average

trade tax rate of firm i, has a mean of 1.11.15

Municipalities and districts are naturally heterogeneous (to some extent). In particular,

the number of inhabitants per municipality shows notable variation, with the minimum being

five inhabitants (for the municipality of Wiedenborstel) and the maximum being 3.4 million

inhabitants (for the municipality of Berlin). In terms of economic indicators, the average GDP

in EUR per inhabitant ranges between 13,085 (in the Sudwestpfalz district) and 86,728 (in the

Munich district), with a mean of approximately 27,872, whereas the unemployment rate var-

ies between 2.2% (in the Eichstätt district) and 22% (in the Demmin district), with a mean of

approximately 7.88 %.

(Insert Table 3 about here)

Pairwise correlations between selected variables are shown in Table 4. The correlation

matrix shows that the independent variables in our regression are generally not strongly corre-

lated, which indicates limited multicollinearity issues. More specifically, the Pearson correla-

tions are mostly less than 50 %. However, the total No. of Inhabitants appears to be correlat-

ed strongly with variables such as Real Property Tax B, Size of District, Average Purchase

Price Land, GDP per Inhabitant, and Tourism - Beds.

15

Data confidentiality prohibits the publication of certain parameters (e.g., minimum, maximum) for certain

variables.

29

(Insert Table 4 about here)

6.2 Hypotheses testing

We report four different models for each hypothesis, with models differing in the extent

to which control variables are included. Model 1 includes only the treatment variable

TaxRatej and four firm controls. To isolate the effect of trade tax rates on location decisions,

we control for several municipality and district characteristics in further models. Control vari-

ables at the municipality and district levels allow us to control for the general economic envi-

ronment of a certain region, which in turn allows us to control for the remaining heterogenei-

ties between locations within Germany that might explain differences in wages in a given

facility on their own. Therefore, in model 2, we add selected municipality-level controls.

Model 3 further includes district-level controls on an aggregated level. For instance, the vari-

able MovingInj is incorporated into our regression only as a total, instead of separating it fur-

ther into different age groups (e.g., under 18 and between 18 and 25). Finally, model 4 in-

cludes district controls on a disaggregated level and a full set of district-fixed effects (i.e., 470

different district indicator variables). All models include industry-fixed effects.

(Insert Table 5 about here)

Consistent with H1a, we observe in Table 5 that wages paid are higher in facilities with

lower trade tax rates, and the coefficients of TaxRatej are significantly negative in all four

models. This finding suggests that firms with facilities in more than one municipality use lo-

cation decisions (reallocation of personnel) to save trade taxes; thus, the location decisions of

firms are indeed altered in response to tax incentives.

To control for the economic reasonableness of our results, we form certain expecta-

tions with regard to the control variables (as indicated by the predicted sign). For instance, we

30

find a positive and significant sign for Inhabitants, which is expected because the number of

inhabitants in a municipality indicates a large labor market, which in turn might indicate high-

er wages paid per facility within that respective location; that is, we expect larger facilities in

municipalities with larger labor markets. The control variable Real Property Tax A, which is a

special tax for agricultural activity in a given municipality, shows an expected negative asso-

ciation with wages paid because it is a proxy for more rural characteristics in a particular mu-

nicipality. We note that further control variables have significant association with Wageij, but

we do not interpret these variables in detail.

Considering H1b (Table 6), we expect that the significance and the level of personnel

located in facilities in low-tax municipalities will be higher in a bin with greater incentives in

terms of shifting income.

(Insert Table 6 about here)

Indeed, we find that firms react more when they exhibit higher trade tax differentials.

Considering models 1 and 2, which include firm- and municipality-level controls, respective-

ly, we find that the coefficients on the treatment variable bins are insignificant except for the

bin with the highest tax incentives (Diff. Tax Rate 75-100) for which the coefficient is signif-

icantly negative, which is as expected. In model 3, in which we further include aggregated

district control variables, we observe that differences in real activities between facilities ap-

pear to be induced by the level of trade tax rate differentials. Technically, the coefficient and

the corresponding T-value increase in absolute value step-by-step with each bin. Model 4,

with disaggregated district controls and also district-fixed effects, validates this finding. We

interpret this finding to mean that small trade tax rate differentials do not significantly moti-

vate firms to shift personnel because the costs of personnel shifting most likely are high com-

pared to the corresponding tax benefits. Conversely, if the trade tax rate differential is large,

31

firms appear to recognize an advantage in shifting personnel to tax-favored facilities; there-

fore, the tax savings seem to outweigh the costs of shifting.

Considering the control effects for the sake of discussion, the variable Diff. Unem-

ployment Rate shows a predicted negative sign, which indicates that a relatively higher unem-

ployment (rate) means that the labor market has more oversupply and, ceteris paribus, average

wages per employee might be lower, which in turn predicts lower wages per facility. Addi-

tionally, the coefficients of the control variables Diff. GDP per Inhabitants and Diff. Average

Purchase Price Land, which are both proxies for the economic strength of a district, are sig-

nificantly positive. This finding may be interpreted to indicate that wages paid are higher in

more economically attractive districts.

In contrast with the tests for hypotheses H1a and H1b, which are intra-periodic anal-

yses, we test in H2a whether firms react to trade tax rate changes over time (inter-periodic

analysis, Table 7). Thus, we use a slightly adjusted first-difference model. Similar to H1b, we

now create four upward and four downward bins of trade tax rate changes. Firms with a trade

tax rate upward (downward) change in the lowest quartile of the sample. Thus, firms with

relatively small tax-induced shifting incentives fall into the first bin, labeled ∆ Tax Rate up 0 -

25 (∆ Tax Rate down 0 - 25); the process is similar for the remaining bins.

In Table 7, Panel A, we present results for the association between changes in wages

paid and tax rate changes for the 2001-2004 period (short time horizon). We observe that

firms appear to react more to tax rate decreases than to tax rate increases, which indicates that

an upward tax rate change is only associated with a reduction in the workforce (away from the

respective facility) if the tax rate change is in the highest quartile. Downward tax rate changes

appear to have a greater effect in inducing firms to shift personnel; the relevant coefficients

and T-values increase in absolute value step-by-step with each downward bin, which persists

over all four models.

32

Panel B of Table 7 reports the findings from our investigation of tax rate changes from

2001 to 2007 (a long time horizon) in which we generally find that firms react more strongly

if they have more time to adapt to tax rate changes. Technically, both upward and downward

tax rate changes are associated with significant changes in wages paid over the longer time

horizon with the expected coefficients. We interpret this to mean that location decisions are

indeed shifted but only at a relatively slow pace, which contrasts the quick pace of shifting

through accounting decisions that can be implemented quickly through transfer pricing or the

allocation of debt. Shifting personnel is relatively complex to implement (and reverse) and

must therefore be carefully considered and is thus more time-consuming.

(Insert Table 7 about here)

33

6.3 Robustness tests

We conduct several sets of robustness tests to evaluate our reported results. We first

determine the reliability of our results by clustering on a district level. Moreover, we use addi-

tional models (i.e., including further variations of the available control variables) to validate

our results. In these untabulated results, we find that all our results are economically and sta-

tistically stable.

Secondly, to further strengthen the support for our findings with respect to H1b, we re-

run the regression by replacing the dummy bins with the actual tax rate differential (Table 8).

is the difference between the maximum and the minimum of TaxRatei for a

single firm i within one particular year scaled by the weighted average trade tax rate of firm i.

We find in all four models that firms with relatively higher tax rate differentials between mu-

nicipalities with the highest trade tax rate and the lowest trade tax rate have relatively more

employees located in facilities with the lowest firm-specific tax rate (

). Thus, firms appear to react to greater incentives for income

shifting by changing their real activities.

(Insert Table 8 about here)

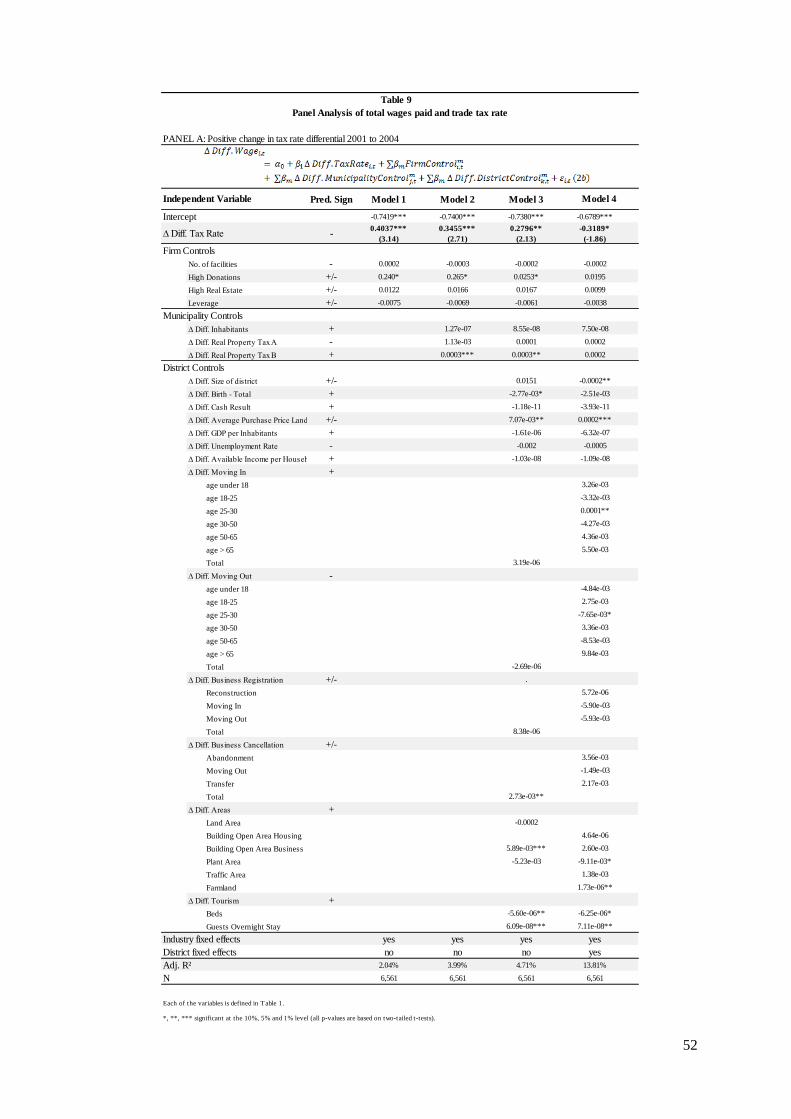

Third, to validate our findings regarding the inter-periodic analyses in H2a, we con-

duct additional tests based on the previous research design (Table 9). In addition to the tax

rates of a given facility, the tax rate differential between a given firm's facilities at the highest

and lowest tax rates may vary over time when either the firm’s highest and/or lowest trade tax

rate changes:16

16

For our analysis, we only include cases in which the municipalities with the highest and lowest trade tax rates

of a given firm remain unchanged over time. Thus, if a medium-ranked trade tax rate changes so much be-

tween the first and second periods that the municipality becomes one of the firm’s extremal trade tax rate

municipalities (minimum or maximum), the respective firm is excluded.

34

Figure 5: Example for Inter-periodic Robustness Test.

For firm A, the trade tax rate differential in the first period is ∆intra-period, which equals

5. Because of a decrease in the minimum trade tax rate (here, a decrease from 20 % to 15 %

for facility 2), the trade tax rate differential increases between the first and second periods

(∆intra-period: 10). The same effect would occur with an increase in the maximum trade tax rate

for firm A with facility 1 (not considered in the example). We expect that firms would react to

such a change over time (∆inter-period: 10 - 5 = 5) with tangible income shifting. Based on such

arguments, in the second period, there is a greater incentive to shift personnel to facility 2.

Consequently, in the second period, we expect that the wages paid are relatively higher in

facility 2 compared to period 1. As a result, the difference in wages paid between the two fa-

cilities (∆inter-period: -$2,000) is expected to increase between the first period (∆intra-period: -

$2,000) and the second period (∆intra-period: -$4,000). Moreover, the larger the change over

time (case 1: ∆inter-period = 5; case 2: ∆inter-period = 15), the larger the difference in wages paid

over time will be (case 1: ∆inter-period = -$2,000; case 2: ∆inter-period = -$3,000). However, in our

dataset, we do not find this effect directly for the small time horizon (i.e., tax rate differentials

increase from 2001 to 2004, as shown in Table 9, Panel A). In only one of the four models

Case 1 t0 t1 t0 t1

Facility 1 25% 25% $2,000 $1,000

Facility 2 20% 15% $4,000 $5,000

∆ intraperiod 5 10 -$2,000 -$4,000

∆ interperiod

Case 2 t0 t1 t0 t1

Facility 1 25% 25% $2,000 $500

Facility 2 20% 5% $4,000 $5,500

∆ intraperiod 5 20 -$2,000 -$5,000

∆ interperiod

Firm A

15 -$3,000

Tax Rates Wages Paid

Firm A

5 -$2,000

35

(Model 4) do we observe that the larger the positive change in the trade tax rate differential of

a firm over time (∆inter-period), the larger the change is in the differential in wages paid. All

other models show the opposite effect. In further investigating the longer time horizon (Table

9, Panel B), we also do not find the expected results.

(Insert Table 9 about here)

Finally, following exactly the same argument, the trade tax differential of a firm might

also decrease over time (leading to a relative decrease in tax incentives with respect to tangi-

ble decisions, untabulated). We find that firms do not react (in a statistically significant man-

ner) to this decreasing tax rate differential.

36

7. Conclusion

We investigate the impact of taxes on location decisions for a full sample of all com-

mercial firms in Germany (5,116,719 firms) during the 2001-2007 period. To specifically

observe the location decisions of a firm, we use the peculiarity of the German trade tax regime

in which formulary apportionment is used to allocate the tax base for the different facilities of

a firm that are faced with different tax rates at the municipality level. In this respect, wages

paid at a facility are used as the sole allocation key. Contrary to location decisions, accounting

choices do not impact the allocation of a tax base in these cases and are thus excluded as an

explanation. The trade tax scheme applied has considerable variation in tax rates across

12,266 German municipalities, and the trade tax rate is economically relevant to German

firms, which provides us with a valuable natural experiment from which we can derive mean-

ingful findings about the behavior of multinational enterprises.

We report three distinct main findings. First, we find that tax rates are associated with

the allocation of wages paid between the facilities of a firm (i.e., the location of employees) in

a manner that is consistent with our hypothesis of the tax-induced effects on location deci-

sions. Second, when tax rates vary over time, firms appear to react by transferring personnel

to facilities in municipalities with lower tax rates, and this effect increases with the length of

the time period. Third, the greater the tax incentives of a firm, the greater the reaction as

shown in tangible business activity changes with respect to the relevant tax incentives will be.

Overall, we conclude that taxes thus notably impact a firm’s location decisions.

This paper contributes to the ongoing debate about the channels of income shifting.

Income shifting might be based primarily or even solely on accounting decisions (e.g., via

transfer pricing, location of debt, and the location of intangible property) or might also be

based on changes in tangible operations. Our findings suggest that tax rates can induce firms

37

to alter their location decisions. We conclude that the relevance of tax rates for location deci-

sions may thus have been underestimated.

38

References

Albring, Susan M., Lillian F. Mills and Kaye J. Newberry (2011). Do Debt Constraints Influence

Firms' Sensitivity to a Temporary Tax Holiday on Repatriations? Journal of the American

Taxation Association 33(2): S. 1-27.

Altshuler, Rosanne and Harry Grubert (2003). Repatriation taxes, repatriation strategies and multina-

tional financial policy. Journal of Public Economics 87(1): S. 73-107.

Altshuler, Rosanne and T. S. Newlon (2003). The Effects of U.S. Tax Policy on the Income Repatria-

tion Patterns of U.S. Multinational Coporations, in: A. GIOVANNINI, R. G. HUBBARD and J.

SLEMROD, Studies in International Taxation, University of Chicago Press, Chicago, 77-115.

Altshuler, Rosanne, T. S. Newlon and W. C. Randolph (1995). Do Repatriation Taxes Matter? Evi-

dence from the Tax Returns of U.S. Multinationals, in: MARTIN FELDSTEIN, JAMES R. HINES

and R. G. HUBBARD, The Effects of Taxation on Multinational Corporations, University of

Chicago Press, Chicago, 253-272.

Altshuler, Rosanne and T. Scott Newlon (1993). The Effects of U.S. Tax Policy on the Income Repat-

riation Patterns of U.S. Multinational Corporations. Studies in International Taxation. ALBER-

TO GIOVANNINI, R. GLENN HUBBARD and JOEL SLEMROD, University of Chicago Press.

Baldenius, Tim, Nahum D. Melumad and Stefan Reichelstein (2004). Integrating Managerial and Tax

Objectives in Transfer Pricing. Accounting Review 79(3): S. 591-615.

Blouin, Jennifer and Linda Krull (2009). Bringing It Home: A Study of the Incentives Surrounding the

Repatriation of Foreign Earnings Under the American Jobs Creation Act of 2004. Journal of

Accounting Research 47(4): S. 1027-1059.

Blouin, Jennifer L., Leslie A. Robinson and Jeri K. Seidman (2012). Coordination of Transfer Prices

on Intrafirm Trade, available at:

Boskin, M. J. and W. G. Gale (1987). New Results of the Effects of Tax Policy on the International

Location of Investment, in: MARTIN FELDSTEIN, The Effects of Taxation on Capital Accumu-

lation, University of Chicago Press, Chicago, 201-219.

Boucher, Karen J. (1993). Multistate corporate tax-saving strategies. Journal of State Taxation 12: S.

23-57.

Buettner, Thiess, Michael Overesch, Ulrich Schreiber and Georg Wamser (2012). The Impact of Thin-

Capitalization Rules on Multinationals' Financing and Investment Decisions. Journal of Public

Economics 96(11-12): S. 930-938.

39

Buettner, Thiess, Nadine Riedel and Marco Runkel (2008). Strategic Consolidation Under Formula

Apportionment, available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1313028, 1-

35.

Buettner, Thiess and Martin Ruf (2007). Tax Incentives and the Location of FDI: Evidence from a

Panel of German Multinationals. International Tax and Public Finance 14(2): S. 151-164.

Buettner, Thiess and Georg Wamser (2013). Internal debt and multinationals' profit shifting - empiri-

cal evidence from panel data. National Tax Journal: S. erscheint demnächst.

Clausing, Kimberly A. (2005). Tax Holidays (and Other Escapes) in the American Jobs Creation Act.

National Tax Journal 58(3): S. 331-346.

Collins, Julie H. and Douglas A. Shackelford (1992). Foreign Tax Credit Limitations and Preferred

Stock Issuances. Journal of Accounting Research 30(3): S. 103-124.

Collins, Julie, Deen Kemsley and Mark Lang (1998). Cross-Jurisdictional Income Shifting and Earn-

ings Valuation. Journal of Accounting Research 36(2): S. 209-229.

De Mooij, Ruud A. and Sjef Ederveen (2003). Taxation and Foreign Direct Investment: A Synthesis of

Empirical Research. International Tax and Public Finance 10(6): S. 673-693.

Dechow, Patricia M. and Douglas J. Skinner (2000). Earnings Management: Reconciling the Views of

Accounting Academics, Practitioners, and Regulators. Accounting Horizons 14(2): S. 235-

250.

Desai, Mihir A., C. Fritz Foley and James R. Hines, Jr. (2004). A Multinational Perspective on Capital

Structure Choice and Internal Capital Markets. Journal of Finance 59(6): S. 2451-2487.

Desai, Mihir A., C. Fritz Foley and James R. Hines, Jr. (2012). Trade Credit and Taxes, available at:

http://www.nber.org/papers/w18107.pdf?new_window=1

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2066404, 1-31.

Desai, Mihir A., C. Fritz Foley and Jr James R. Hines (2001). Repatriation Taxes and Dividend Distor-

tions. National Tax Journal 54(4): S. 829-851.

Devereux, Michael P. and Rachel Griffith (1998). Taxes and the location of production: Evidence

from a panel of US multinationals. Journal of Public Economics 68(3): S. 335.

Devereux, Michael P. and Giorgia Maffini (2007). The Impact of Taxation on the Location of Capital,

Firms and Profit: A Survey of Empirical Evidence, available at:

http://www.sbs.ox.ac.uk/centres/tax/Documents/working_papers/WP0702.pdf, 1-53.

40

Dischinger, Matthias and Nadine Riedel (2011). Corporate taxes and the location of intangible assets

within multinational firms. Journal of Public Economics 95(7/8): S. 691-707.

Froot, K, A. and J. R. Hines (1995). Interest Allocation Rules, Financing Patterns, and the Operations

of U.S. Multinationals. The Effects of Taxation on Multinational Corporations. M. FELDSTEIN,

J. R. HINES and R. G. HUBBARD. Chicago, University of Chicago Press: 277-307.

Graham, John R., Michelle Hanlon and Terry Shevlin (2011). Real Effects of Accounting Rules: Evi-

dence from Multinational Firms’ Investment Location and Profit Repatriation Decisions.

Journal of Accounting Research 49(1): S. 137-185.

Gramlich, Jeffrey D., Piman Limpaphayom and S. Ghon Rhee (2004). Taxes, keiretsu affiliation, and

income shifting. Journal of Accounting and Economics 37(2): S. 203-228.

Grubert, Harry (2003). Intangible Income, Intercompany Transactions, Income Shifting, and the

Choice of Location. National Tax Journal 56(1): S. 221-242.

Grubert, Harry and John Mutti (1991). TAXES, TARIFFS AND TRANSFER PRICING IN MULTI-

NATIONAL CORPORATE DECISION MAKING. Review of Economics & Statistics 73(2):

S. 285.

Grubert, Harry and John Mutti (2000). Do Taxes Influence Where U.S. Corporations Invest? National

Tax Journal 53(4): S. 825-839.

Gunny, Katherine A. (2010). The Relation Between Earnings Management Using Real Activities Ma-

nipulation and Future Performance: Evidence from Meeting Earnings Benchmarks. Contem-

porary Accounting Research 27(3): S. 855-888.

Gupta, Sanjay and Lillian F. Mills (2002). Corporate multistate tax planning: benefits of multiple ju-

risdictions. Journal of Accounting and Economics 33(1): S. 117-139.

Hanlon, Michelle and Shane Heitzman (2010). A review of tax research. Journal of Accounting and

Economics 50(2-3): S. 127-178.

Harris, David G. (1993). The Impact of U.S. Tax Law Revision on Multinational Corporations' Capital

Location and Income-Shifting Decisions. Journal of Accounting Research 31(3): S. 111-140.

Hartman, David G. (1985). TAX POLICY AND FOREIGN DIRECT INVESTMENT. Journal of Pub-

lic Economics 26(1): S. 107-121.

Hines Jr, James R. (1997). Tax policy and the activities of multinational corporations. Fiscal Policy:

Lessons from Economic Research. A. AUERBACH. Cambridge, MIT Press: 401–445.

Hines, Jr James R. and Eric M. Rice (1994). FISCAL PARADISE: FOREIGN TAX HAVENS AND

AMERICAN BUSINESS. Quarterly Journal of Economics 109(1): S. 149-182.

41

Huizinga, Harry and Luc Laeven (2008). International profit shifting within multinationals: A multi-

country perspective. Journal of Public Economics 92(5–6): S. 1164-1182.

Huizinga, Harry, Luc Laeven and Gaetan Nicodeme (2008). Capital Structure and International Debt

Shifting. Journal of Financial Economics 88(1): S. 80-118.

Karkinsky, Tom and Nadine Riedel (2012). Corporate Taxation and the Choice of Patent Location

within Multinational Firms. Journal of International Economics 88(1): S. 176-185.

Klassen, Kenneth J. and Stacie Kelley Laplante (2012a). Are U.S. Multinational Corporations Becom-

ing More Aggressive Income Shifters? Journal of Accounting Research 50(5): S. 1245-1285.

Klassen, Kenneth J. and Stacie Kelley Laplante (2012b). The Effect of Foreign Reinvestment and Fi-

nancial Reporting Incentives on Cross-Jurisdictional Income Shifting. Contemporary Ac-

counting Research 29(3): S. 928-955.

Klassen, Kenneth J. and Douglas A. Shackelford (1998). State and provincial corporate tax planning:

income shifting and sales apportionment factor management. Journal of Accounting and Eco-

nomics 25(3): S. 385-406.

Klassen, Kenneth, Mark Lang and Mark Wolfson (1993). Geographic Income Shifting by Multina-

tional Corporations in Response to Tax Rate Changes. Journal of Accounting Research 31(3):

S. 141-173.

Krull, Linda K. (2004). Permanently Reinvested Foreign Earnings, Taxes, and Earnings Management.

Accounting Review 79(3): S. 745-767.

Mills, Lillian F. and Kaye J. Newberry (2004). Do Foreign Multinationals' Tax Incentives Influence

Their U.S. Income Reporting and Debt Policy? National Tax Journal 57(1): S. 89-107.

Mintz, Jack and Alfons J. Weichenrieder (2005). Taxation and the Financial Structure of German Out-

bound FDI, available at: 1-24.

Newberry, Kaye J. (1998). Foreign Tax Credit Limitations and Capital Structure Decisions. Journal of

Accounting Research 36(1): S. 157-166.

Newberry, Kaye J. and Dan S. Dhaliwal (2001). Cross-Jurisdiction Income Shifting by U.S. Multina-

tionals: Evidence from International Bond Offerings. Journal of Accounting Research 39(3):

S. 643-662.

Oestreicher, Andreas and Melanie Klett (2011). Impact of Taxation on Company Decisions under

Seperate Accounting and Formula Apportionment, available at: 1-27.

42

Shackelford, Douglas and Terry Shevlin (2001). Empircal Tax Research in Accounting. Journal of

Accounting & Economics 31(1-3): S. 321-387.

Shevlin, Terry, Tanya Y. H. Tang and Ryan J. Wilson (2012). Domestic Income Shifting by Chinese

Listed Firms. Journal of the American Taxation Association 34(1): S. 1-29.

Single, Louise E. (1999). Tax Holidays and Firms' Subsidiary Location Decisions. Journal of the

American Taxation Association 21(2): S. 17-34.

Smith, James K. (1997). The Effect of the Tax Reform Act of 1986 on the Capital Structure of Foreign

Subsidiaries. Journal of the American Taxation Association 19(2): S. 1-18.

Swenson, Deborah L. (2001). Transaction Type and the Effect of Taxes on the Distribution of Foreign

Direct Investment in the United States. International taxation and multinational activity.

JAMES R. HINES, JR. Chicago and London, University of Chicago Press: 89-108.

Tang, R. (2002). Current Trends and Corporate Cases in Transfer Pricing, in: Quorum Books, West-

port, Conn./London,

43

Wages Total total wages paid of each firm i

Wages wages paid for each facility of a firm i in municipality j, scaled by total wages paid of each firm i