Embed Size (px)

Citation preview

The Impact of Thin-film PV on the Cost of SolarEnergy

Bert Haskell- Director of Product Development

The Impact of Thin-film PV on the Cost of SolarEnergy

Bert Haskell- Director of Product Development

Confidential HelioVolt Corp © 20082

About HelioVoltAbout HelioVolt

Founded: 2001

Location: Austin, TX

Employees: 80+ (160 expected by end of 2008)

Technology: Revolutionary method for manufacturing high-efficiency CIGS PV circuits

Recently completed $101M Private Equity Financing Round

Building commercial production facility in Austin

Confidential HelioVolt Corp © 20083

Energy Generation and the Terawatt (TW) ChallengeEnergy Generation and the Terawatt (TW) Challenge

Humanity uses 12 TW of power today• 1 TW = 1,000 GW (Gigawatts)

World will need 15 TW by 2012

Only 5 known sources of energy are available on a TW scale*• Fossil fuels: Coal, oil, gas• Nuclear fuels• Solar

Only inherently distributed solution No fuel cost

*Prof. Nathan Lewis,

http://nsl.caltech.edu/

Confidential HelioVolt Corp © 20084

Sun – Our Free Fuel!Sun – Our Free Fuel!

The earth receives more energy from the sun in just over one hour than the world uses in an entire year

Confidential HelioVolt Corp © 20085

Regional PV-Generation per installed kWpRegional PV-Generation per installed kWp

Confidential HelioVolt Corp © 20086

Worldwide PV Market by RegionWorldwide PV Market by Region

2005 2006 2007E 2008E 2009E 2010E 2011E 2012E0

2,000

4,000

6,000

8,000

10,000

12,000

CanadaUSASpainPortugalOthersLuxemburgKoreaJapanItalyGreeceGermanyFranceChinaAustralia

Source: Credit Suisse company compiled data

Confidential HelioVolt Corp © 20087

US RPS GoalsUS RPS Goals

Cumulative in MW 2007 2010 2017 2020 CA 380 850 3,740 4,950 NY 115 250 940 1,200 NJ 35 130 620 1,000U.S. TX 15 30 80 100(per RPS) IL 10 80 350 950 PA 5 30 570 850 NM 255 370 680 800 AZ 15 50 430 700Total U.S. 1,020 2,200 9,900 14,400

Source: Lazzard Freres

Confidential HelioVolt Corp © 20088

Source: Christopher O’Brien of Sharp Solar at EESI climate change meeting 2005

Example of successful long term solar incentivesExample of successful long term solar incentives

Confidential HelioVolt Corp © 20089

Confidential HelioVolt Corp © 200810

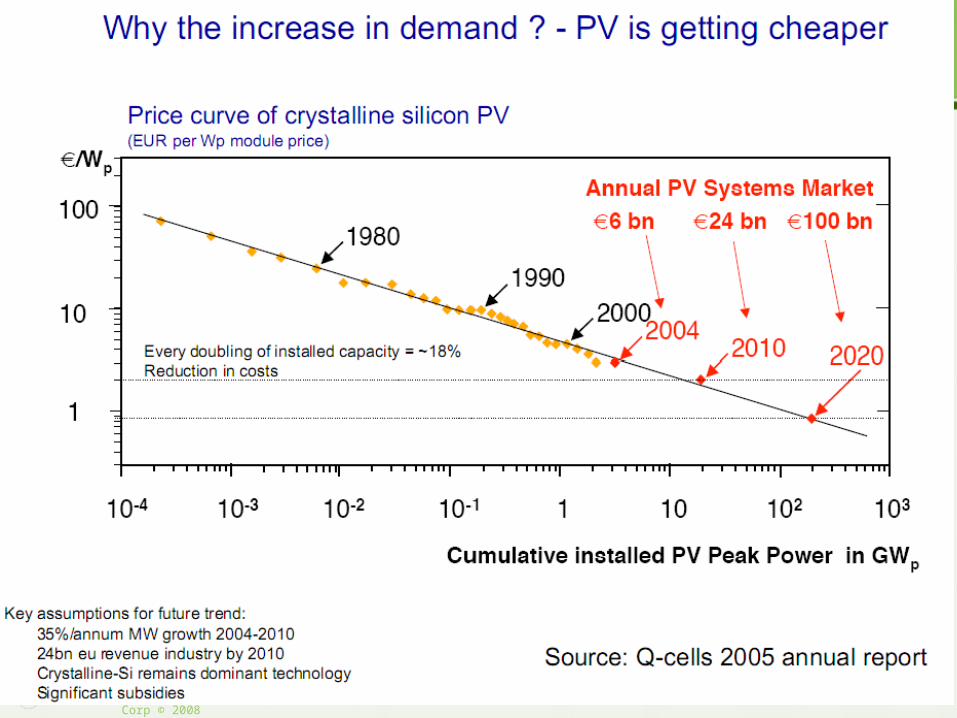

Projected $/watt trendsProjected $/watt trends

2005 2006 2007E 2008E 2009E 2010E 2011E 2012E0

10

20

30

40

50

60

70

80

90

100

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

An

nu

al S

ola

r In

sta

llati

on

s (

GW

)/S

ola

r In

du

str

y R

ev

en

ue

($

,bb

)

WW

We

igh

ted

Av

era

ge

Sy

ste

m A

SP

($

/wa

tt)

Source: Credit Suisse company compiled data

Confidential HelioVolt Corp © 200811

Confidential HelioVolt Corp © 200812

Polysilicon

Wafer Solar Cell Solar Panel SystemIngotPolysilicon

Value Chain Cost DistributionValue Chain Cost Distribution

20%30%

50%

2006 US Solar System Cost Allocation by Category

Confidential HelioVolt Corp © 200813

Inefficiencies in Today’s Value ChainInefficiencies in Today’s Value Chain

15 – 20 + % margins at each step in the value chain

Raw silicon Wafer mfg Cell Module assembly

Inverters System Eng Installation$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$

$

$

$

$

$

Thin Film Advantage

Building Integrated PV

Advantage

US PV System Price $/w ~ $7.50

Confidential HelioVolt Corp © 200814

Confidential HelioVolt Corp © 200815

Solar Product AvailabilitySolar Product Availability

Crystalline Silicon ~ 18% conversion efficiency

Multi-crystalline Silicon ~ 14 - 16%

Amorphous Silicon ~ 6-8%

• Flexible and rigid

Cadmium Telluride ~ 8-9%

• First Solar capturing significant market share for central power applications

CIS/CIGS ~11-12%

• New commercial availability entering the market in 2008

90% of current market

10% of current marketbut fastest growing segment

Confidential HelioVolt Corp © 200816

Advantages of thin film PVAdvantages of thin film PV

Efficient and high performing materials• Direct bandgap semiconductors• Better energy output – kWh/KW • CIGS record at 19%+ conversion efficiency

Significantly reduced costs• Less material usage

Not affected by silicon supply shortages• Potential for improving costs throughout value

chain

Better aesthetics

Roadmap of glass-to-glass and flexible substrate

Confidential HelioVolt Corp © 200817

Solar TodaySolar Today

Google HQ - Solar Project

Solar farm in Amstein, Germany

Utility Scale Commercial Systems

Confidential HelioVolt Corp © 200818

Solar Tomorrow: Building Integrated Photovoltaics Solar Tomorrow: Building Integrated Photovoltaics

Power Buildings will become multi-$T market• BIPV is the fastest growing sector of PV• Building Integration leverages available surface area, installation

costs, and proximity to loads

Revolutionary products through efficient, durable thin-film solar cells embedded into traditional building materials • Current products unsuitable and not cost effective

Confidential HelioVolt Corp © 200819

BIPV ApplicationsBIPV Applications

Roofing

• Most common BIPV application today

Sunshades

• Energy conservation and reduced building operating costs

• Cooling load mitigation and glare control

• Easiest retrofit for PV

Overhead glazing (canopies, skylights, atriums)

Curtain wall / Facades

Confidential HelioVolt Corp © 200820

24h-Energy Profile

0:0

0

6:0

0

12:0

0

18:0

0

24:0

0

Ele

ctr

ica

l E

ne

rgy

[a

rb. u

nit

s]

Low Tariff Low TariffHigh Tariff

Electricity supplied by Utility

Fed-InEnergy

Solar Energy

Energy consumption of building

Electricity supplied by Utility

Source: RWE Energie AG and RSS GmbH

Example: Correlation between Daily PV Power Production and Energy Consumption of an Office Building in SpainExample: Correlation between Daily PV Power Production and Energy Consumption of an Office Building in Spain

Confidential HelioVolt Corp © 200821

Broad Challenge for CollaborationBroad Challenge for Collaboration

–BIPV

World’s Highest Performance, Lowest Cost, & Most Versatile

Solar Power Platform

![Thin film and thin wafer PV: challenges for BIPV applications [PV 2009]](https://img.pdfslide.net/doc/110x75/558559fdd8b42a54608b50df/thin-film-and-thin-wafer-pv-challenges-for-bipv-applications-pv-2009.jpg)