Embed Size (px)

Citation preview

Determining the best strategies for your financial future begins with education. Information is a powerful ally—knowledge may be the most valuable financial tool. And the earlier you learn to develop sound money habits, the more at ease you will be when making important financial decisions. To prepare yourself to take advantage of life’s opportunities (and also hedge your bets against unforeseen difficulties), you’ll want to be on sound financial footing. Lifetime rewards can come from learning the best financial techniques including: organizing your finances, spending what you can afford, saving for a rainy day, obtain-ing career training and teaching children and youth how to handle money responsibly.

Use credit wiselySaving & investingMarriage & moneyFinancial tips & tweaks

People helpingpeopleMoolah managementHelp for students

INSIDE

The importance of teaching

R E S P O N S I B I L I T YR E S P O N S I B I L I T Y

ClassroomConnectionsDESERET NEWS

The importance of teaching

A brief history of the piggy bank According to legend, the piggy bank came into being in about the 15th century. �e origin of the word apparently evolved from the Old English word “pygg,” which was a type of inexpensive orange clay used to manufacture a broad variety of household items, including small plates or kitchen jars that people used to hold their change. Penny boxes or money boxes were also a common place to store coins. �eory has it that over following centuries the “pygg jar” evolved into the “pygg bank,” actually taking on the characteristics and color of pigs. Once the meaning of pygg had evolved from the actual material into the shape of the animal, other materials were put into use, including glass and plastic. Original pyggy banks had to be broken to retrieve the coins, but today, most piggy banks come with a removable plug underneath for removal of the money. Introducing children to the piggy bank is a great way to begin shaping their understanding of how to save and how to spend responsibly.

financial

2 T E A C H I N G F I N A N C I A L R E S P O N S I B I L I T Y

The American credit union movement began in New England 100 years ago. Those credit unions began as a social movement designed to help people live better lives through access to essential financial services. Early credit union pioneers identified a need for a cooperative source of fairly priced credit at a time when it was not available for average consumers. Throughout its history, the credit union movement has remained true to these philosophical, yet pragmatic, roots. Mountain America Credit Union has been serving Utah communities for more than 75 years. We’re governed by a volunteer board of directors, consisting of credit union members elected by credit union members. This is one of the very important ways we’re different from other financial institutions. Another significant way we’re different is that we’re a financial cooperative. We give back to members through higher savings rates, lower loan rates and new, improved services. Because credit unions focus on serving members, we have a long history of consistently ranking higher than banks and thrifts in the annual American Banker/Gallup opinion poll. And today, when so many other financial institutions are struggling in a weakened economy, credit unions are strong because they stay true to their original purpose—people helping people.

Huntsman Cancer Research Receives Three-Point Challenge Donation Mountain America Credit Union supports deserving charitable causes that are important to the communities where our members live. To this end the credit union has partnered with the Utah Jazz and Huntsman Cancer Founda-tion to help fight cancer. During the Utah Jazz’s 2009–2010 season, the credit union donated $50 to the Huntsman Cancer Foundation for every three-point shot made by Utah Jazz players. The team completed the season with 439 three-pointers, bringing Mountain America’s total contribution to $21,950. “All of us have been touched by cancer in some way, either through our own experience or that of someone we know and love. Moun-tain America Credit Union is proud to partner with the Utah Jazz and the Huntsman Cancer Foundation in finding a cure for cancer. With every three-point shot that the Jazz makes, we are a little closer to our goal,” said Sterling Nielsen, Mountain America’s president and CEO. Nielsen presented the check to Robert P. Haight, executive vice president of the Hunts-man Cancer Foundation, during halftime of the Jazz’s final regular season home game. “The Huntsman Cancer Foundation was honored this past Jazz year to be the benefi-ciary of the three-point challenge. We wish to thank Mountain America and its members for their generous donation to cancer research. Huntsman Cancer Institute is a world leader in cancer care and research, and this contribu-tion will be used to continue the world-class care and research for which HCI has become known,” Haight said. The Huntsman Cancer Foundation’s office is located at 500 Huntsman Way in Salt Lake City. For more information about the foundation, visit www.huntsmancancerfoundation.org or call 801-584-5800.

Robert P. Haight, executive vice president of the Huntsman

Cancer Foundation (left), received the donation from

Sterling Nielsen, president and CEO of Mountain America (right).

2Mountain AmericaM O N E Y T I P S

WEEK CR

ED

ITA P R I L

Why should you join a credit union? 1.

2.3.

4.5.

6.

7.

Credit unions are focused on people. Credit unions operate by a “people helping people” philosophy that is hard to find at many other financial institutions.

Credit unions exist to serve people—including people of modest means.

Financial education is available to all members. Credit unions help members become better-educated consumers of financial services.

As not-for-profit institutions, credit unions typically o�er better rates on credit cards.

As a member of a credit union, no matter how much money you have on deposit, you have an equal voice in how your credit union is run.

Superior service, convenience and technology. Credit union members receive the service convenience of today’s technology through mobile and online banking.

Many credit unions can put you in business with a small business loan.

People helping people — the credit union philosophy

M o u n t a i n a M e r i c a s u p p o r t s c o M M u n i t y c a u s e s

Why should you join a credit union?

3

Consider the way most children see the world around them. When they're hungry, food appears on the table. When they're bored, they push a button and they're watching the Cartoon Network or they flick a switch that turns on the computer.

For children, it seems everything is in their immediate grasp. It's not surprising they may not appreciate what it takes to get that TV or why a new bike doesn't fit in the family budget this month. Here are a few active ways to teach children about money.

Children five years and older:

* Play counting games with money. Use coins and dollar bills to play adding and subtracting games.

* Role-play. Set up toys in a "toy store." Take turns playing the customer and the clerk exchang-ing various amounts of money. When your child is the clerk, hand over too much money so he or she counts the money back to you.

Fun ways to learnabout money

MONEY TIPS

Consider the way most children see the world around them. When they’re hungry, food appears on the table. When they’re bored, they push a button and they’re watching the Cartoon Network or they flick a switch that turns on the computer. For children, it seems everything is in their immediate grasp. It’s not surprising that they may not appreciate what it takes to get that TV or why a new bike doesn’t fit in the family budget this month. Here are a few active ways to teach children about money.

Children five years and older:

Play counting games with money. Use coins and dollar bills to play adding and subtracting games.

Role-play. Set up toys in a "toy store." Take turns playing the customer and the clerk exchanging various amounts of money. When your child is the clerk, hand over too much money so he or she counts the money back to you.

Children 10 years and older:

Include children on shopping trips to teach them what things cost and smart shopping techniques. Have them help compare product qualities, prices, return policies and warranties.

Children 15 years and older:

Play a version of "Let's Pretend," focusing on how much money it takes to run a household. Start by saying, "Let's pretend you're 19 years old and living on your own. You work full time at the local grocery store and earn $8.25 an hour; that's $330 a week and $1,320 a month—but really $1,120 once taxes come out."

Figure costs for rent, food, utilities and other monthly expenses. As a start, review the family'smonthly utility bills to show how much things like cable TV and heating the house cost. �en subtract monthly expenses from the $1,120 monthly earnings. Discuss ways to cut costs--fewer takeout dinners or fewer long-distance phone calls to friends.

It's never too early to teach children the value of money. And remember Mountain America Credit Union has a variety of youth savings accounts that can help them reach all their money goals.

D

Learn valuable money skills

3

EvElopiNG fiNANCiAl liTErACy is a lifetime process. if you’re lucky, you start learning at a young

age, beginning with your first piggy bank. later you may move on to a savings account; as you mature, open a checking account; and then perhaps have a debit and credit card after high school. Each step of the way toward successful adult financial responsibil-ity requires development of your money smarts and the ability to make good choices. To help our youth start on the right track, Mountain America Credit Union has partnered with The Deseret News and its Newspapers in Education program, the National Endowment for Financial Education and the Jump$tart Coalition for Personal Financial Literacy. This helps bring financial knowledge and effective training programs to schools in our community. Utah’s high school students are required to pass a general financial literacy course in order to graduate, and Mountain America Credit union is devoted to supporting educators in the classroom by assisting with instruction, helping by providing financial training materials and by continually encouraging students through offering special accounts and providing information on our youth website at www.youth.macu.com. In addition, we work with Newspapers in Education to support the Connect 123 program that brings current financial information to students every week in their classrooms.

FIN

AN

CIA

L R

ESPO

NSIB

ILIT

Y

MOUNTAIN AMERICA CREDIT UNIONDESERET NEWS

H E L P I N G Y O U T H S

4 T E A C H I N G F I N A N C I A L R E S P O N S I B I L I T Y4

T I P S F O R P A R E N T S

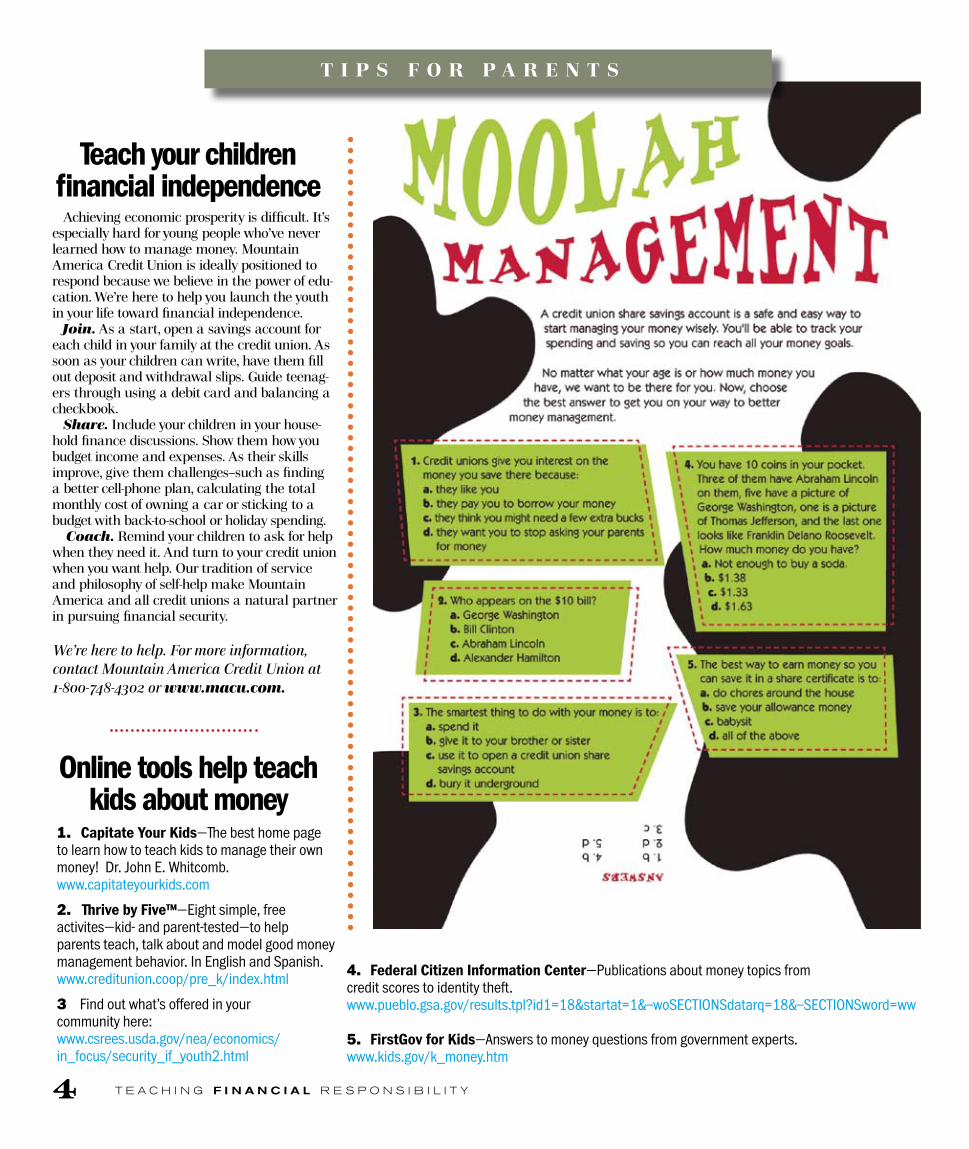

Achieving economic prosperity is difficult. It’s especially hard for young people who’ve never learned how to manage money. Mountain America Credit Union is ideally positioned to respond because we believe in the power of edu-cation. We’re here to help you launch the youth in your life toward financial independence. Join. As a start, open a savings account for each child in your family at the credit union. As soon as your children can write, have them fill out deposit and withdrawal slips. Guide teenag-ers through using a debit card and balancing a checkbook. Share. Include your children in your house-hold finance discussions. Show them how you budget income and expenses. As their skills improve, give them challenges—such as finding a better cell-phone plan, calculating the total monthly cost of owning a car or sticking to a budget with back-to-school or holiday spending. Coach. Remind your children to ask for help when they need it. And turn to your credit union when you want help. Our tradition of service and philosophy of self-help make Mountain America and all credit unions a natural partner in pursuing financial security.

We’re here to help. For more information, contact Mountain America Credit Union at 1-800-748-4302 or www.macu.com.

Teach your children financial independence

Online tools help teach kids about money

1. Capitate Your Kids—The best home page to learn how to teach kids to manage their own money! Dr. John E. Whitcomb. www.capitateyourkids.com

2. Thrive by Five™—Eight simple, free activites—kid- and parent-tested—to help parents teach, talk about and model good money management behavior. In English and Spanish. www.creditunion.coop/pre_k/index.html

3 Find out what’s offered in your community here:www.csrees.usda.gov/nea/economics/ in_focus/security_if_youth2.html

4. Federal Citizen Information Center—Publications about money topics from credit scores to identity theft. www.pueblo.gsa.gov/results.tpl?id1=18&startat=1&--woSECTIONSdatarq=18&--SECTIONSword=ww

5. FirstGov for Kids—Answers to money questions from government experts. www.kids.gov/k_money.htm

5

HELPING STUDENTS

MOUNTAIN AMERICA CREDIT UNIONDESERET NEWS

Three students win $2,000 scholarships

OUNTAIN AMERICA CREDIT UNION offers the education loans that will help students finance their education. With many lenders leaving the student loan industry, we have

continued offering private student loans because we believe it is valu-able for our members to have the ability to further their educations. In fact, Mountain America was the first credit union in Utah to offer private student loans to students who did not qualify for traditional college financing. In May 2007, we introduced our Education Line of Credit to a few schools in Utah. Now that number has grown to over 200 schools throughout Utah, Arizona, New Mexico and Nevada, and the portfolio has grown to more than $25 million in just three years. The Education Line of Credit is a great solution for those students who need financing to fill the remaining gap after reaching their federal loan maximum limits; who are attending a trade school such as cosmetology, aesthetics, massage therapy and other nontraditional schools; or for schools that do not offer federal loans. The Education Line of Credit offers a competitive variable inter-est rate, with low monthly, interest-only payments while the student is in school. There are no origination fees or prepayment penalties to worry about. To apply a student can simply go to their closest Mountain America branch, call our Service Center at 1-800-748-4302 (option 2) or go to www.macu.com. The student will receive a deci-sion within 24 hours, and the typical processing turnaround time for funding is seven business days from start to finish. We will work with your school to obtain the School Certification and disburse the funds directly to the school. Six months after either graduation or withdrawing from school, the Education Line of Credit will convert to the Education Repayment Loan, with low monthly payments and a competitive fixed inter-est rate. It offers a repayment plan of 12 months per $1,000, with a maximum of up to ten years to repay so payments stay low. The Edu-cation Repayment Loan is also a great way for students with previous private student loan debt to consolidate their nonfederal loans into

one loan payment. Mountain America strives to be a leader in the student loan industry so we can provide students and schools with a quality product and with quality personal service. Our mission is to continue to help students finance their education so they can achieve their dreams.

NE OF THE AvENUES to help achieve financial success is education. Supporting higher education has been one of Mountain America’s community sponsorships for many

years. In 1992 after the untimely death of Paul R. Ball, the credit union’s vice president of Human Resources, the company introduced its annual scholarship program, which was named in his honor. Each year three scholarships are awarded. The applicants are judged on a combination of academic performance, special skills, commu-nity service and their future plans. Post secondary education and training costs continue to increase every year. The College Board¹ estimates that the cost of one year’s tuition and fees² for 2009 were $7,020–$11,582 for a public four-year college; $26,273 for a private college; and $2,544 for a public two-year college. The College Board has introduced a new Net Price Calculator that can be used to help develop a personal cost estimate for the col-lege a student plans to attend. Go to www.collegeboard.com/npc. Mountain America awarded three students $2,000 each for the 2010 Paul R. Ball Memorial Scholarship. Credit Union president and CEO, Sterling Nielsen, noted that, “Mountain America is a strong sup-porter of education. We are proud to be able to offer scholarships to deserving students pursuing higher education. We congratulate this year’s Paul Ball Scholarship winners.” Staci Harris, Trevor Johnson and Danielle Wynn were selected by the scholarship committee to receive the awards. Harris is a master’s student at Westminster College, with a goal of working in the FBI’s Behavioral Analysis Unit. Johnson, a continuing student at Utah State University, plans to go on to medical school after he receives his bachelor’s degree. Wynn is also striving to become a doctor. A freshman recently ac-cepted into Southern Utah University’s Rural Health Scholars pro-gram, she’s excited to begin a new phase in her life. “Thank you for helping me make my goals and dreams a reality,” Wynn wrote in a letter to Mountain America.

Scholarshipopportunities

1The College Board is a not-for-profit membership association whose mission is to connect students to college success and opportunity. Price and aid figures are from the College Board’s Trends in College Pricing 2009, Trends in Student Aid 2009 and Education Pays 2007. 2Board and room not included in estimate.

At left, an excited Trevor Johnson displays his award with branch manager Josh Harbinson of Roosevelt.

Not pictured: Staci Harris.

Danielle Wynn received her scholarship award from Cedar City branch manager, Cathy Stucki.

A leader in the student loan industry

O M

6 T E A C H I N G F I N A N C I A L R E S P O N S I B I L I T Y 7

WHAT’S YOUR INVESTMENT STYLE?by Matthew ClarkVice President−Financial ServicesMountain America Credit Union

The word “style” describes how people dress, wear their hair and even walk and talk. But style also plays a role in how you invest money. Identifying and adopting an investment style that’s a good fit is the first step toward secur-ing your financial future. Choosing an investment style allows you to

take a planned approach to investing. By selecting a style that’s in sync with your financial situation and then choosing investments according to that style, you boost your chances of getting what you want out of your investment program.

Here are some basic distinctions:Growth: Investors using a growth style put their money into secu-rities, typically stocks, that are growing in earnings. These stocks are growing, or are expected to grow, faster than the stock market average. The growth investor aims for big gains over the long term, but also faces risks as growth-oriented companies go through their ups and downs. In fact, short-term losses can be substantial and severe during down cycles.

Value: In the value style, investors look for stocks that are com-paratively low-priced, but the price doesn’t accurately reflect the company’s potential and current assets. Thus, value investors are betting that the company’s stock will rise again to reflect its true value.

Income: Investors using an income style choose securities that produce regular but modest earnings. Some examples include government-issued bonds or money market mutual funds. Income investments don’t bring as much potential for gain as growth investments, but they also carry less risk for loss. Income investors aim for fairly stable earnings over time.

Blended: The blended style combines both growth and income investments. This helps strike a balance between the potential for gain and the risk of loss.

Your investment style depends on your goals, resources and your risk tolerance. Other factors to consider are your age, financial goals and investment time frame. If you still have a few decades before retirement, you’ll have ample opportunity to regain whatever short-term losses you might incur. Thus, a growth investment style may serve you well. But if retirement is a few years away, or you’ll be sending a child to college in five years, you can’t afford to take a severe hit. You’d be better off with a less risky income investment style. Whatever your style, Mountain America Credit Union has savings and retirement vehicles that can help you get closer to your goals−safely. Use your credit union options to accumulate the funds necessary to make other investments, with style.

SAVING & INVESTING

MOUNTAIN AMERICA CREDIT UNIONDESERET NEWS MOUNTAIN AMERICA CREDIT UNIONDESERET NEWS

Effective savings practices made easy

Matthew Clark

SO, WHAT’S 65 CENTS? Cards can be used just about anywhere, some only at a specific place No payo� deadline Monthly minimun payments vary, based on the balance Usually has the highest rate of these four types of credit

Typically used for large puchases, such as a car or an appliance Loan term can vary from a few months to many years Monthly payment amounts are o�en set for the length of the loan Usually has a lower rate than a credit card

Used for tuition and other college expenses Depending on your income level, some loan programs let you delay making payments until you graduate Loan term is usually up to 10 years, depending on the amount borrowed Monthly payment amounts are usually set annually, when interest rates are adjusted Usually has a lower interest rate than an installment loan May provide an income tax break on interest paid to the lender

Used specifically for a loan to purchase a home Usually repaid over 15-30 years Monthly payments may be set for the life of the loan, or changed more frequently, depending on the type of interest rate Usually has a lower interest rate than an installment loan May provide an income tax break on interest paid to the lender

Mountain AmericaM O N E Y T I P S

B I G M O N E Y

Credit card

JohnSue

20-4040-65

2025

$1,000/year$1,000/year

$20,000$25,000

$338,472$ 78,984

8%8%

Installmentloan

Student loan

Mortgage

PERSON

Banks, credit unions, stores and gas stations

Banks, credit unions, auto dealers and otherfinancial institutions

Banks, credit unions and the federalgovernment

Banks and credit unions

AGES TOTAL SAVEDYEARSSAVED RATE

INTEREST TOTAL AT AGE 65AMOUNT

BY T

HE N

UM

BER

S

It’s easy to postpone starting to save for a later day, but a solid plan is key to success. By following some basic guide-lines, you’re more likely to achieve financial security.

Pay yourself firstUse automated transfers to get in the habit of saving. Money will be transferred from your account without your seeing it, which makes you less likely to miss it. Simply com-plete a form authorizing Mountain America to receive a portion of every paycheck and deposit it directly into your savings account.

Save 10% of your paycheckThe general rule of thumb is to save about 10% of each paycheck. If that seems too high, try 5% and work your way up to saving 10% of your earnings. Add 1% every year you get a raise until you reach 10%.

Know yourselfExamine your goals to determine which savings plan will work best for you. For example, don’t invest all your money in an aggressive stock or mutual fund if you’re conservative with your money. If you’re saving for retirement, select a plan that will fit your financial needs down the road.

Realize that age mattersAlways take into consideration how much time you have to save for your goal. If you are a recent college graduate, you have several decades to ride out the highs and lows of the market and can take advantage of more high-risk investments. If you’re only a few years from retirement, you might not have the time cushion to afford to be too aggressive.

See the benefit of compound interestThe simplest way you can invest your mon-ey is to leave it alone and let it “compound” over time. You earn interest not only on what you save, but also on the dividends generated. The earlier and more you save, the more your money will grow.

Use dollar-cost averagingThis is the process of routinely investing a set amount of money over time, rather than all in one lump sum. It’s a convenient savings method, particularly for begin-ning investors. For example, each month transfer $25 or $50 from your share draft account directly into an investment vehicle such as a traditional or Roth IRA. You reduce your overall risk from market fluc-tuations because your money buys more shares when the price of a share is down, and your money buys fewer shares when the price of a share is up. Bottom line: You’ve reduced your investment risk.

The sooner, the bigger You know you should put money away now for the future. The sooner you start, the bigger your savings stack will be. But few people realize how easy it is to get started and how the dramatic the effect of compounding interest can be. If you put away $1,000 a year for 10 years, then let it earn a 6% annual percentage yield for 20 more years, you’ll have more money than if you wait for 10 years and then save $1,000 for 20 years. Mountain America has savings accounts, including regular savings, share certifi-cates and IRAs. Our rates will get your money working for you now so you won’t have to work so hard for it later. Give us a call today at 1-800-748-4302. The sooner you start, the bigger your stack will be when you need it.

Investor challenges in a changing market

With all the ups and downs in the financial markets, it’s hard for investors to know what to do and when. How do investors typically respond to change?

React to what happens. Unfortunately, some investors react in ways that are counter to their best interests. When the stock market declines, some people sell stocks. When the market moves sharply higher, people fear they may miss out on a good thing and buy stocks. A buy high, sell low strategy won’t improve a portfolio.

Anticipate and act. The ideal strategy for successful investing or attempting to get in at the lows and out at the peaks is a good one . . . but only if you happen to know in advance where interest rates are headed, what unemployment will be in the future and who will win the next election. Changes in markets and the economy are nearly impossible to anticipate.

Sit on the sidelines. Some investors avoid the pain associated with market vola-tility and sit tight with cash in their pockets. This strategy provides small long-term returns after inflation.

So what’s an investor to do? Know where you want to be and when, and implement a plan to get there based on goals and tolerance for short-term volatility. Diversify, and then stick with your plan.

3

{ D O THE M ATH }

{ D O THE M ATH }

Saving &investing

What if the account earned 10% interest instead of 5%? You’d double your money in 7.2 years.

Now let’s say you have $500 and you want to double it in 4 years. What interest rate will you need? Divide 72 by the 4 years and you’ll need to earn 18% interest.

Mountain AmericaM O N E Y T I P S

J A N U A R Y

WEEK

Rule of 72 Want to know how long it will take to double your money? Use the Rule of 72 to find out. Just divide 72 by the interest rate. For example, if you have $100 and put it into a savings account earning 5% interest, it would take 14.4 years to turn that $100 into $200.

MONEY TIPS

Grab a calculator. Add up what you spend on so-called “little things” that end up being budget-busters:

If you spend 65 cents a day—every day of the week—on soda, that adds up to $237 a year.

If you spend $2.00 a day—every weekday—on music downloads, that’s $520 a year.

If you spend $3.00 a day—every day of the week—for going over your texting limit, that’s $1,095 a year.

If you spend $5.00 a day—every week-day—on fast food, that’s $1,300 a year.

8 T E A C H I N G F I N A N C I A L R E S P O N S I B I L I T Y

2Mountain AmericaM O N E Y T I P S

WEEK

Manage your credit cards

CR

ED

IT

A P R I L

rEdiT is BorroW-iNG money or purchasing goods

with the promise to pay for them at a later date or over time. Charge accounts at banks and other institutions are available to people who establish a history of repaying their debts fully or promptly. 2009/2010 Credit CARD Act changes cards for young adults You’ve probably already seen changes in the world of credit cards or at least noticed all the disclosure notices appearing with your credit card bills. The first phase of the Credit CARD Act of 2009 went into effect that year. The majority of the Act went into effect February 2010. Among those changes effective in February are many that will affect people younger than age 21. In short, these changes limit the marketing and issuing of credit cards to young adults. Here are the details:

Anyone younger than 21 years of age must be an authorized user on a parent’s account. To have their own card, individuals must show proof of adequate income to pay card debts, or have an adult co-signer.

Prescreened offers to consumers under 21 are banned.

Card companies are banned from offering free gifts for completion of an applica-tion on or near a college campus and at college-sponsored activities/events.

Colleges, universities and alumni associations must disclose details of contracts they sign that allow credit card marketers access to student and alumni contact info.

Card issuers must file reports annually with the Federal Reserve Board listing all business/marketing/promotional deals with schools. These reports must detail the terms and conditions, list schools by name and identify how much the issuer is paying the school.

A “Sense of Congress” provision is included in the CARD Act recommending that colleges offer credit card and debt education sessions during new student orien-tation. So check your statements and read the notices your credit card company sends.

If you have specific questions, call Mountain America Credit Union at 1-800-748-4302.

You can be guaranteed that one thing hasn’t changed . . . getting the best choice of a credit card at Mountain America Credit Union.

CCREDITUse wisely by Teressa Rich

Assistant Vice President— Consumer LoansMountain America Credit Union

Under the pressure of job insecurity and wide-spread unemployment, U.S. consumers have actually

reduced their collective credit card debt. Yet to-tal U.S. credit card debt still exceeds $888 billion. New Credit Card Accountability, Responsibility and Disclosure (CARD) Act protections require card issuers to communicate better and disclose rates and other information more clearly. This should make it easier for consumers to moni-tor what they owe. But new regulations can’t prevent people from having poor debt manage-ment habits.

Here’s some advice for controlling credit card use:

Teressa Rich

Actively manage your account. Open and examine your credit card statements promptly. Look for unauthorized use, of course, but also look for announcements from the issuer. Under the new rules, you must have 45 days notice of a change in your card’s terms, such as an interest rate increase. If you choose to “opt out” of the change, you no longer will be able to add new charges to your card and will want time to get a replacement while you pay off the old balance.

Keep your credit score healthy. This number between 300 and 850 is a measure of your trustworthiness as a borrower. The higher your score, the easier it is to get a loan and, often, the more favorable the interest rate. The most important ways to maintain and improve your credit score are by paying all your bills on time and not taking on excessive debt.

Watch your card balance-to-limit ratio. It’s OK to occasionally “max out” your credit card for impor-tant purchases, as long as you can pay it off in a few months. But over the long term, try to keep your total credit card debt to a reasonable 10% to 20% of your total credit limit.

Understand the overlimit option. The CARD Act allows you to choose what you want your card issuer to do when you try to go over your card’s credit limit. If you “opt in,” you can go over the limit for a fee. If you “opt out,” your attempt to go over the limit will be declined.

9

COLLEGE studEnts

MOUNTAIN AMERICA CREDIT UNIONDESERET NEWS

2Mountain AmericaM O N E Y T I P S

WEEK How to handle roommate financesCR

ED

IT

A P R I L

tips for parents of college students

those students new to a college environ-ment will embark on many new experiences—including financial independence. Here are some tips for parents to help kids prepare for what’s in store:Explain how credit works. If your son applies for a credit card at a campus table promotion, he could get a credit line he may not be able to afford and may not know how to manage. A credit card is not free money; it’s a means of putting off paying for purchases until a later date. Accompany him to the credit union for the best rates on credit cards and consider urging him to use a debit card instead.

Create a spending plan. Write down all college expenses such as tuition, books, room and board, toiletries, entertainment and so forth. Determine which expenses you’ll be paying and those your child will be paying.

Come to a no-bail-out agreement. If your daughter ends up charging more than she can afford, or runs out of money before the end of the month, your first reaction may be to send money and bail her out. Don’t do it. If she needs to figure out a way to get out of debt, such as working or staying home on week-ends, chances are good she won’t make the same mistake twice.

going to college? You don’t have to leave your credit union

Are you leaving town to attend college? You might think that means you need to leave Mountain America Credit Union be-hind, but we’d hate to see you go. Once you join a credit union, you’re a member for life−no mat-ter where life takes you. So even if you’re leaving the state to go to school, you can stay with us. We’re here to help you with all your financial needs. And with today’s technology, staying in contact with us and using credit union services is easier than ever. Visit us at www.macu.com for more information.

Use your student ID/activity card to see athletic events, etc.

Cook for yourself and pack a lunch whenever possible.

Shop at used clothing stores and thrift shops.

Watch the matinee instead of the evening show and seek out theaters offering student discounts.

Use public transportation or ride a bike. Hey, it eliminates speed-ing and parking tickets.

Brew yourself a cup of coffee in the morning instead of paying $3 for a latte.

Visit parks, zoos and museums for inexpensive entertainment.

Buy used books, CDs and furniture.

Use discipline. Before splurging on items such as expensive shoes, hold off for a week or two and decide if they are something you really need.

Most important, join Mountain America Credit Union. We offer low-interest loans and charge fewer and lower fees than banks to help our college students stretch their dollars to the max.

Don’t let the excitement of living with friends and having your first apartment cause you to overlook financial particulars that come with having roommates. While you and your roommates may share the same love for Facebook and MySpace, you may find you’re polar opposites when it comes to attitudes about spending and money. By laying some ground rules, you can help guarantee that all parties meet their obligations, despite differences in financial habits. Bills. Where will the money come from? Find out before signing a lease if the roommate-to-be will be reliable when it comes to paying bills. The lease. Make each roommate sign it so each person shares the responsibility if there’s a problem or if someone decides to move out before the lease is up. Utilities. Unlike the lease, utility bills usually carry only one roommate’s name. In the company’s eyes, that person is responsible for making full and prompt payment. To spread the risk, each roommate should put a bill in his or her name. If need be, make a payment with individual, prorated checks—divide the whole bill among roommates.

Ideas to stretch those college dollars

Let’s face it, even with all the ramen noodle variations out there, a person can eat only so many. Here are some tips to maximize your resources during your college years:

Food. Will you limit shared costs for household supplies, like toilet paper and dishwasher detergent? Or can you agree about how to share other staples, like milk? Chores. Will one person always get stuck unloading the dishwasher or cleaning the bathrooms? This kind of issue is a common source of friction among roommates.

Not sure where to start? Use your browser to search for “roommate agreement forms,” many of which are comprehensive and easy to use.

2Mountain AmericaM O N E Y T I P S

WEEK How to handle roommate financesCR

ED

IT

A P R I L

10 T E A C H I N G F I N A N C I A L R E S P O N S I B I L I T Y

G E t t I n G M A R R I E d

efore you tie the knot, it’s best to tie up any financial loose ends. sit down with your future spouse and talk about your financial situation—where you

are now and where you want to be in six months, one year, a decade and beyond.

starting your financial life together

Say “I DO” with MatriMoney Wedding RegistryChoosing the perfect wedding registry has never been easier. Mountain America’s MatriMoney Wedding Registry lets wedding guests give you the gift of cash so you can get the gifts you really need without the hassle of returning items or signing up for multiple registries.

Spend your cash gifts where and when you want.

Conveniently access your cash gifts with your new Visa® Debit Card.

Receive a starter packet that includes helpful tips and registry cards.

Family and friends can visit our website (www.macu.com) and give their gifts using a major credit card.

MatriMoneyWEDDING REGISTRY

MatriMoneyWEDDING REGISTRY

Say “I DO” with

With MatriMoney from

Mountain America, you won’t

have to worry about returning

gifts or registering at multiple

stores. MatriMoney allows

your wedding guests to easily

give you the gift of cash online,

so you can spend your money

where you want, on the things

you really need. Sign up today!

www.macu.com1-800-748-4302

Discussing these topics may be uncomfortable,

but, in the end, communi-cation is key to avoiding

conflicts over money. Once you’ve determined

your financial plan and goals, Mountain

America’s full range of products and services

can help you put them into action.

When getting married, there are a number of financial decisions you need to make as a couple:

Are you going to have individual checking accounts or a joint one?

How much of each of your incomes is going to be used for normal household expenses, such as utilities and rent?

Who is going to be responsible for actually writing the checks or making the online payments for monthly bills?

What are your long- and short-term financial goals?

What is your attitude toward using credit cards?

How frequently are you going to purchase big-ticket items like a new car?

What is your comfort level with spending and debt?

What is your risk tolerance for investments?

What are each of your retirement plans?

Four money mistakes every couple should avoid Money can wreck a relationship. In fact, how they spend, save and account for money is one of the leading sources of friction between couples. In virtually every study, money ranks as the first or second most argued-about topic for twosomes of all types.

Try To avoid These common misTakes:extremism. Work on changing your ways if you’re on either end of the spectrum from shopaholic to cheapskate. It’s a lot easier to have a meeting of the minds when both partners practice moderation.

secrecy. Don’t hide your spending from your partner. Once you lose your part-ner’s trust, it’ll be an uphill battle to win it back.

assigning blame. If both partners stay involved, one can’t blame the other for the household’s money troubles.

Using money as a weapon. Spending to get back at your partner won’t solve your relationship issues, it will just make you unhappy and broke.

Ultimately, experts note that peaceful coexistence is possible if couples agree on three things: to live within their means, to take care of the future and to still be willing to have fun with their money.

B

This educational section from Deseret News Newspapers in Education department was under the direction of Brenda Smith with layout and design by Lou Ann Reineke. Assistance was provided by Louisa Ingalls, Mountain America Credit Union community involvement supervisor.

Mountain America Credit Union has 63 branches in four states and offers a variety of financial products and services for consumers and businesses. With roots dating back to the 1930s, Mountain America Credit Union is a tradition for many members. Today the credit union serves more than 343,000 members and has over $2.8 billion in assets. Mountain America Credit Union has been honored four times as one of “Utah’s Best Companies to Work For” by Utah Business magazine. Visit www.macu.com for more information.

Credits

F I N A N C I A L T I P S A N D T W E A K SFO

LLOW

TH

ESE T

IPS

MOUNTAIN AMERICA CREDIT UNIONDESERET NEWS

�ese nine ways make one big di�erence—better service to credit union members:

1. Democratic control 2. Member service3. Generous in giving back to members4. Building financial stability 5. Easy to become a member6. Ongoing education 7. Cooperate with other cooperatives8. Social responsibility

Help reduce your exposure to fraud

It’s important to protect your financial information. Here are a few tips to help you keep tabs on your money and identity:

1. Track the balances on your financial accounts. If there is dramatic or unexpected change in an account this could be a warning signal 2. It’s OK to hang up the phone when strangers call and ask for any type of personal information. 3. Be wary of using toll free numbers sent to you. Call your local credit union branch on your own to check on your account status.4. Don’t open e-mails unless you KNOW the source. Mountain America Credit Union never asks for personal account information on the phone.5. If an ATM captures your credit or debit cards, call your financial institution immediately to report it and arrange for a replacement card.6. Don’t talk to strangers hanging out by an ATM, and never approach an ATM when people are lingering about.

Open and voluntary membership

Eight ways credit unions are different

Help reduce your exposure to fraud it’s important to protect your financial information. Here are a few tips to help you keep tabs on your money and identity:

Track the balances on your financial accounts. If there is dramatic or unexpected change in an account this could be a warning signal.

It’s OK to hang up the phone when strangers call and ask for any type of personal information.

Be wary of using toll-free numbers sent to you. Call your local credit union branch on your own to check on your account status.

Don’t open e-mails unless you KNOW the source. Mountain America Credit Union never asks for personal account infor-mation on the phone.

If an ATM captures your credit or debit cards, call your financial institution immediately to report it and arrange for a replacement card.

Don’t talk to strangers hanging out by an ATM, and never approach an ATM when people are lingering about.

Pay for purchases by cash, check or debit card—not with a credit card.

Make a shopping list and only buy what’s on it. Put financial goals in writing so you have something to “save” for.

Get rid of department store credit cards; carry one major credit card for emergencies.

Record every dollar you spend and your feelings about each purchase.

Avoid discount warehouses; allocate a certain amount of cash to spend if you do shop at one.

Avoid catalog ordering and watching TV shopping channels.

Take a walk or exercise when the urge to shop comes on.

Find a money mentor; look for a friend or colleague who spends and saves wisely and ask for advice.

If you feel out of control, you probably are. Seek counseling or a support group.

Five resolutions to trim spending and reduce stress

These five tips will help you trim spending, beef up savings and reduce stress:Pay it off. Pay off your credit cards to save money.

Conserve. Small changes can yield big savings.

Grab a calculator. Add up what you spend on small budget-busters.

Tune it up. Regularly service your automobile—prevent costly repairs.

Transfer it. Pay yourself first—set up automatic transfers into your savings account.

do the poor economy and ballooning grocery prices have you ready to forgo food? While you can’t change the economy, you can save money on your grocery bills. “One way to save is by using basic buying strategies that apply to everyone,” says

George Barany, director of financial education for the Consumer Federation of America, Washington, D.C., and for the Youth Saves program at America Saves.

try these grocery shopping strategies:Compare unit price—Take note of the price per pound or ounce for a particular food.

Check out what’s on sale—Make sure to be flexible with your recipes.

Clip coupons—Coupons can save you up to $25 a month when used on groceries.

Shop multiple stores—Prices vary from store to store, so you can save by shopping at two or three.

Shop local—Farmers markets are a great way to save money, buy fresh food and, well, meet the farmers.

Plan your trips to the store—If you shop for groceries once a week with a list, you’ll most likely spend less time and money.

Be wary of bulk buys—If you buy too much, your “savings” will end up in the garbage. If you do purchase larger quantities of meat—such as hamburger or chicken—divide it into portions needed for meals and freeze.

To prevent shopping binges:

On the money with food

11

These eight ways make one big difference− better service to credit union members:

M O U N T A I N A M E R I C A V I S A® C A R D S

A SMART IDEA

GOOD THRU

Rates as low as 8.25% APR*

No Annual Fee

No Balance Transfer Fees

Rewards Program

MyStyle Customized Cards

www.macu.com*Annual Percentage Rate. Loans subject to credit approval.

Having a Visa® Card from

Mountain America doesn’t

automatically make you a

financial expert. But you

just may feel like one.

APPLY TODAY AT YOUR NEAREST BRANCH!