Embed Size (px)

Citation preview

THE INDIAN HIGH SCHOOL, DUBAI

ACCOUNTANCY GRADE 11 MARKS DISTRIBUTION & MONTHLY PLAN

2017-2018

FIRST TERM

MONTH NAME OF CHAPTERS

April Introduction to Accounting ( Theory )

Accounting- objectives, advantages and limitations, types of

accounting information; users of accounting information and their needs.

Basic accounting terms: business transaction, account, capital,

drawings, liability (internal & external, long term & short term)

asset ( tangible & intangible, fixed, current, liquid and fictitious) receipts (capital & revenue), expenditure (capital,

revenue & deferred), expense, income, profits, gains and

losses, purchases, sales, stock, debtors, bills receivable, Creditors, bills payable, goods, cost, vouchers, discount - trade

and cash.

(Explanation for the terms beyond the text but the

questions to be asked only from syllabus)

07

April-May

Recording of Business Transactions.

Rules of debit and credit: for assets, liabilities, capital, revenue

and expenses. Origin of transactions- source documents (invoice, cash memo,

pay in slip, cheque), preparation of vouchers - cash (debit &

credit) and non-cash (transfer).

- Accounting Equation - Accounting equation: analysis of transactions using

accounting equation, including Balance Sheet.

- Journal, - Books of original entry: format and recording -Journal.

(Including VAT and CST)

- Ledger - Ledger - format, posting from journal, cash book and

other special purpose books, balancing

- of accounts.

- Trial Balance. - objectives and preparation (Only One Method)

06

09

06

06

May-June

-Cash Book

Simple Cash Book(only cash column) and Cash Book with

Bank Column (With Journal Proper)

Petty Cash Book

All Subsidiary Books- Purchases Book, Purchase Returns Book Sales Book, Sales

returns Book and Journal Proper.

(Columnar format is compulsory)(Including Journal

Entries)

06

10

June

Bank Reconciliation Statement

( Exclude Adjusted cash book) Need and preparation.

(Only first two cases: Cash book and Passbook

favorable) Theory Base of Accounting.(Theory)

Fundamental accounting assumptions: going concern,

consistency, and accrual. Accounting principles: Business entity, money measurement,

accounting period, full Disclosure, materiality, prudence, cost

concept, matching concept and dual aspect. Double entry

system. Basis of accounting - cash basis and accrual basis.

Accounting standards: concept & objectives.

Total 50

SUGGESTED QUESTION PAPER DESIGN (FIRST TERM)

S.NO.

TYPOLOGY OF QUESTIONS

VSA 1 Mark

VSA II 2 Marks

SA I 3 Marks

SA II 4 Marks

LA I 6 Marks

MARKS %

1. Remembering 2 1 12 25

2. Understanding 2 1 1 13 25

3. Application 1 1 1 10 20

4. HOT

(Analysis and

synthesis)

1 1 10 20

5. Evaluation 1 1 5 10

Total 2x1=2 2x2=4 4x3=12 2x4=8 4x6=24 50(14) 100

The topics which are not included in the first term (50 Marks) Test..

Bank Reconciliation statement

Theory base of Accounting

Accounting standards

Bases of Accounting—Cash basis and accrual basis

SECOND TERM

MONTH NAME OF CHAPTERS

Introduction to Accounting ( Theory )

Theory Base of Accounting. ( Theory )

Source document (Theory) Recording of Business Transactions.

- Accounting Equation

- Journal and Ledger

-Cash Book and Petty Cash Book, Subsidiary Books- Purchases Book, Purchase Returns Book, Sales Book, Sales returns Book

and Journal Proper.

Bank Reconciliation statement

07

07

03

05

07

10

06

Sept

Bank Reconciliation Statement

(Two cases: Cash book and Passbook Unfavorable)

(Excluded Adjusted BRS)

Depreciation (Excluding Dep. Provision accounting and

Disposal accounting)

concept, need and factors affecting depreciation; methods of

computation of depreciation: straight line method, written down

15

Sept - Oct

Oct

Dec

value method (excluding change in method and provision for

depreciation account)

Provisions and reserves. (Theory )

Provisions and reserves: concept, objectives and difference

between provisions and reserves; types of reserves- revenue

reserve, capital reserve, general reserve, specific reserves and secret reserves

Rectification of errors

Errors: types-errors of omission, commission, principles, and compensating errors Their effect on Trial Balance.

Detection and rectification of errors; preparation of suspense

account (All one sided errors to be rectified by using

Suspense Account)

Bills of Exchange

Bills of exchange and promissory note definition, features, parties, specimen and distinction.

Important terms : term of bill ,due date, days of grace, date of

maturity, bill at sight, bill after date, discounting of bill, endorsement of bill, bill sent for collection, dishonor of bill,

noting of bill , retirement and renewal of a bill, Accounting

treatment of bill transactions;

(Promissory note term not to be used in sums, promissory

note only theory, Format with dates, In exam sums to be

asked either in drawer or drawee’s book)

Final Accounts without Adjustments

Objective and importance.

Balance Sheet: need, grouping, marshalling of assets and liabilities.

Preparation of Trading and Profit and Loss Account and

Balance Sheet of sole proprietorship ( without adjustments)

Small sums – finding opening stock and closing stock and gross profit – missing information

Second Term Exam

03

12

15

10

TOTAL( Theory 20 + Sums 80 marks ) 100

SECOND TERM

SUGGESTED QUESTION PAPER DESIGN (BLUE PRINT)

S.N

O.

TYPOLOGY OF

QUESTIONS

VSA

1 Mark

SA I

3 Marks

SA II

4 Marks

LA I

6 Marks

LA II

8 Marks

MARKS %

1. Remembering 1 1 3 25 25

2. Understanding 1 1 2 1 25 25

3. Application 4 1 20 20

4. HOT

(Analysis and

synthesis)

2 1 1 1 20 20

5. Evaluation 2 2 10 10

Total 5x1=5 5x3=15 5x4=20 6x6=36 3x8=24 90(24) 100

THIRD TERM

MONTH NAME OF CHAPTERS

Dec - Jan

Jan - Feb 2018

Final Accounts with Adjustments

Preparation of Trading and Profit and Loss Account and Balance Sheet of sole proprietorship( with adjustments )

Adjustments in preparation of financial statements : with

respect to closing stock, outstanding expenses, prepaid expenses, accrued income, income received in advance,

depreciation, bad debts, provision for doubtful debts, provision

for discount on debtors, manager's commission, abnormal loss,

goods taken for personal use and goods distributed as free sample .(Excluding Adjustments of Errors, Maximum four

adjustments including closing stock, One Implied

adjustment)(Bad debts and provision in format)(Treatment

for goods destroyed or free samples??)

Single Entry System Incomplete records: use and limitations.

Ascertainment of profit/loss by statement of affairs method

Not for Profit Organization

Not-for-profit organizations: concept.

Receipts and payment account: features. Income and expenditure account: features. preparation of

income and expenditure account and balance sheet from the

given receipt and payment account with additional information.

Adjustments in a question should not exceed 3 or 4 in number, restricted to subscriptions, consumption of consumables and

sale of assets/ old material.

(ii) Entrance/ admission fees and general donations are to be treated as revenue receipts.

(Treatment of Legacy to be skipped from exam questions)

(No Fund Based accounting)(No Subscription Account)

(iii) Trading Account of incidental activities is not to be prepared

Comprehensive project – 10 marks

Tally will be tested in Unit test ( February) for 10 marks.

ANNUAL EXAMINATION MARKS DISTRIBUTION - 2017

GRADE 11 – ACCOUNTANCY.

Chapters Sums Theory

1 Introduction to Accounting Chapter 1& 2 5

2 Theory Base of Accounting Chapter 3,4 &7 7

3 Recording Of Business Transactions.

Accounting Equations

Journal

5

4

Subsidiary Books

Bank Reconciliation Statement

6 6

5 Depreciation

Provisions and Reserves

8

3

6 Bills of Exchange 10

7

.

Rectification of Errors 9

8 Financial Statements - Comprehensive Sum

(Max.6 adjustments including closing stock).

(pls. refer to current year syllabus)

11

9 Not for profit Organization : ( Opening B/S, I E a/c

and Closing B/S) ( No fund based adjustments and

No ledger accounts )

10

10 Single Entry Book Keeping

Statement of affairs method

6

Total 75marks 15marks 90

11 Project 10

Theory Questions from theory lessons only 100

Type of questions and Marks Distribution

MCQ /

VSA

1 mark

SA I

3 Marks

S A II

4 Marks

L A II

6

Marks

LA III

8 Marks

TOTAL

No of

questions

5 5 4 5 3 22

Total 5 15 16 30 24 90

SUGGESTED QUESTION PAPER DESIGN

S.N

O.

TYPOLOGY OF

QUESTIONS

VSA

1Mark

SA I

3 Marks

SA II

4 Marks

LA I

6 Marks

LA II

8 Marks

MARKS %

1. Remembering 2 2 2 22 25

2. Understanding 1 2 1 23 25

3. Application 3 1 1 1 18 20

4. HOT

(Analysis and

synthesis)

2 1 1 18 20

5. Evaluation 1 1 9 10

Total 5x1=5 5x3=15 4x4=16 5x6=30 3x8=24 90(22) 100

GRADE 11 ACCOUNTANCY PROJECT

GUIDELINES TO STUDENTS FOR MAKING COMPREHENSIVE PROJECT IN

ACCOUNTANCY

Students are required to carefully observe the following, before starting the Accountancy

Project work:- 1. Write an explanatory note about a business situation stating the capital introduced by a

Sole Trader followed by various business transactions during a given period of time.

(Please refer to the attached model Summary of a Business and Grade 11 Accounts Text

Book)

2. Record the above mentioned transactions by passing Journal entries. (Columns must be

drawn neatly and narrations must be written completely.)

3. Relevant Ledger Accounts in proper format are to be made by posting the Journal

entries.

4. Prepare Trial Balance.

5. Trading and Profit & Loss a/c is to be prepared, followed by Balance Sheet

6. Conclude the project by making an observation about the Gross profit and Net Profit

made by the firm.

7. The entire project is to be hand written.

8. The duly completed and spiral bound Project file must be produced at the time of Viva

Voce Exam to get the approval signature of the Examiner. The project file should be

safely kept by the students so that it can be a valuable guidance for gr 12 Accountancy

Project.

9. Use only plain white sheets (A4 size) for preparing the project

10. Please maintain the project very neat and tidy.

11. It is always desirable to prepare the project individually.

12. Refrain from blindly copying from other students projects as the Examiner can verify the

authenticity of your project by asking relevant questions during viva voce and the

examiner reserves the right to reject it and deny marks, if found unauthentic.

13. For clearing any queries, please feel free to contact your concerned Accounts

Teacher/Lead Teacher/HOD.

14. Submit the duly completed projects well before the stipulated date, as late submission

may cause deduction of marks.

15. Marks awarded- Project File: 6 marks, Viva Voce: 4 Marks

Issued by the Dept. of Commerce .

(A model Project)

THE BUSINESS HISTORY OF A SOLE PROPRIETOR

Kiran is an enterprising young man who is a graduate in commerce. When he was a

student, he had always cherished the dream of becoming a ‘businessman who serves the

people’ rather than acting as a money making machine. One day he discussed his wish

with his father Mr. Kumar, who is a philosophy professor at the University level. Mr.

Kumar was very glad to hear this new kind of proposal of linking human values in

business.

Mr. Kumar gifted a sum of `12,00,000 to his son by giving cash for `30,000 and the

remaining by a cheque to start the business and advised him to avail a bank Loan for the

remaining amount. Kiran approached his friend’s father Mr. Gulatti who is a garment

wholesale dealer. According to his advice Kiran decided to start a garment retail shop in

the nearby town. Total capital required to start the business was estimated to be at

`15,00,000. A small show room was taken at a monthly rent of `2,000. Two employees

were appointed respectively to deal with customers and to maintain the accounts. The

agreed salaries were `8,000 and `10,000 respectively per month.

Cloths purchased were converted to garments by the inmates of a nearby Orphanage who

were given special training in this field. These employees were given a total wages of

`550,000, by means of issuing cheques during the year.

Showcases were bought for `300,000, Sales Counter for `80,000, Cash counting machine

for `12,000. Other furniture was bought for `120,000. Textile goods for `180,000 were

purchased from the wholesale market. The payment of all these were done by issuing

cheques. Further credit purchases were done from Mr. Gulatti for `600,000.

Kiran approached the Manager of The State Bank of India and arranged for a loan of

`300,000 on the security of the assets he acquired. During the first year, his other

business transactions are summarized as follows:-

Cash Sales `170,000, Credit sales `15,80,000

Bills Receivable received from debtors `20,000

Bills payable accepted from creditors `90,000, Cheque issued to Creditors `450,000

Electricity bill `20,000 and other Sundry expenses of `24,000 were paid in cash

Cheques received from debtors `980,000

Discount allowed `12,000 and received `8,000

Interest on loan paid `30,000, Rent outstanding for the current year was `2,000.

Salaries were paid fully by issuing cheques. Closing stock was valued at `20,000.

During the year garments worth `15,000 were distributed to the Orphanage as charity.

Further garments worth `6,000 were withdrawn for personal use.

The Financial Position of the business can be presented by preparing the Journal, Ledger,

Trial Balance, Trading and Profit &Loss Account and Balance Sheet.

ACCOUNTING RECORDS OF THE SOLEPROPRIETORSHIP BUSINESS OF

SHRI KIRAN

BOOK OF ORIGINAL ENTRIES (JOURNAL)

PARTICULARS DR CR

1.

2

3

4

5

6

7

8

9

10

Cash a/c Dr.

Bank a/c Dr.

To Capital

(Being capital brought in)

Wages a/c Dr.

To Bank

(Being wages paid in cheque)

Office Furniture a/c Dr.

To Bank

( Being sundry office furniture bought)

Purchases a/c Dr.

To Bank

To Creditors

(Being goods purchased )

Bank a/c Dr.

To Bank Loan

( Being Bank loan taken)

Cash Dr.

Sundry Debtors a/c Dr

To Sales

( Being goods sold for cash and credit basis)

B/R a/c Dr.

To Sundry Debtors

(Being B/r drawn)

Sundry creditors a/c Dr.

To B/P a/c

(Being B/P accepted)

Sundry Creditors a/c Dr.

To Bank

To Discount a/c

(Being cheque issued to creditors and discount

earned)

Electricity expenses a/c Dr.

Sundry Expenses a/c Dr.

To Cash

30,000

11,70,000

550,000

512,000

780,000

300,000

1,70,000

15,80,000

20,000

90,000

458,000

20,000

24,000

12,00,000

550,000

512,000

180,000

600,000

300,000

17,50,000

20,000

90,000

450,000

8,000

44,000

11.

12.

13.

14

15

( Being expenses paid in cash)

Bank a/c Dr.

Discount allowed a/c Dr.

To Sundry debtors a/c

( Being Cheque received and discount allowed

to Debtors)

Interest on Loan a/c Dr.

To Bank

(Being interest paid)

Rent a/c Dr.

To cash

To O/s Rent

( Being rent paid and outstanding)

Salaries a/c Dr.

To Bank

( Being salaries paid)

Drawings a/c Dr.

Charity a/c Dr.

To Purchases

( Being goods withdrawn for personal use and

distributed as charity

980,000

12,000

30,000

24,000

216,000

6,000

15,000

992,000

30,000

22,000

2,000

216,000

21,000

PRINCIPAL BOOK (LEDGER)

LEDGER ACCOUNTS

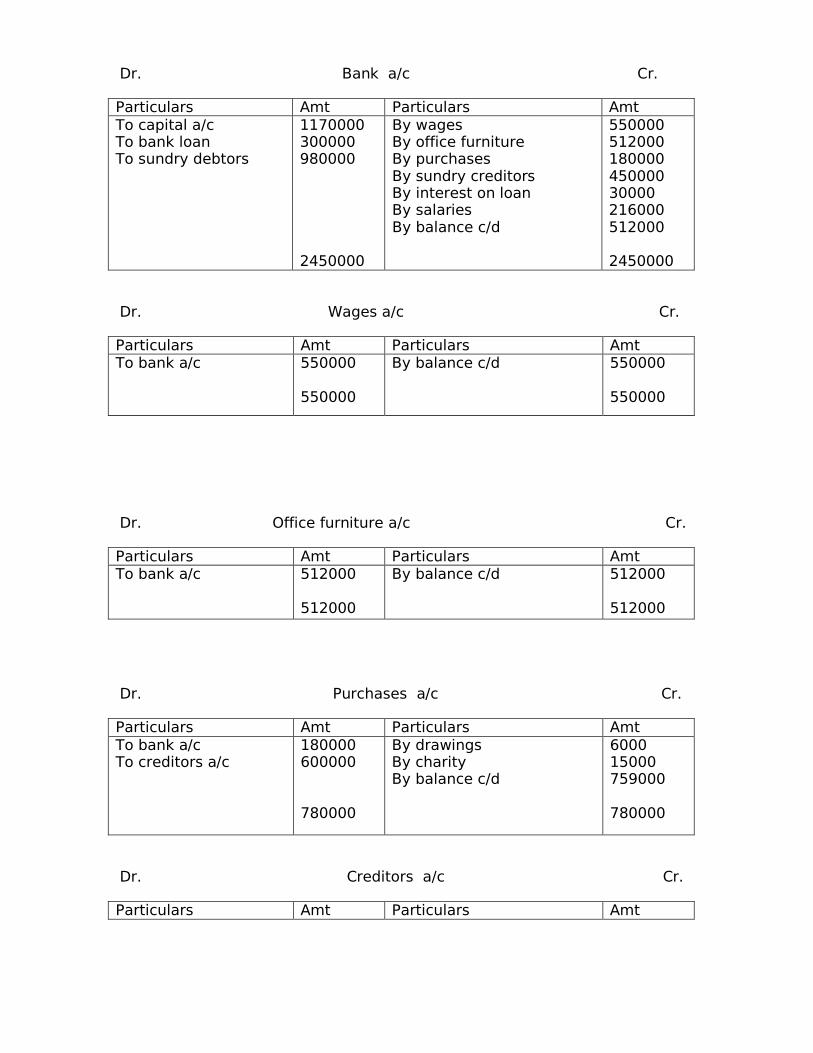

Dr. Cash a/c Cr.

Particulars Amt Particulars Amt To Capital a/c To Sales a/c

30000 170000 200000

By electricity expenses By sundry expenses By rent a/c By balance c/d

20000 24000 22000 134000 200000

Dr. Capital a/c Cr.

Particulars Amt Particulars Amt To Balance c/d 1200000

1200000

By Cash a/c By Bank a/c

3000 1170000 1200000

Dr. Bank a/c Cr.

Particulars Amt Particulars Amt To capital a/c To bank loan To sundry debtors

1170000 300000 980000 2450000

By wages By office furniture By purchases By sundry creditors By interest on loan By salaries By balance c/d

550000 512000 180000 450000 30000 216000 512000 2450000

Dr. Wages a/c Cr.

Particulars Amt Particulars Amt To bank a/c 550000

550000

By balance c/d 550000 550000

Dr. Office furniture a/c Cr.

Particulars Amt Particulars Amt To bank a/c 512000

512000

By balance c/d 512000 512000

Dr. Purchases a/c Cr.

Particulars Amt Particulars Amt To bank a/c To creditors a/c

180000 600000 780000

By drawings By charity By balance c/d

6000 15000 759000 780000

Dr. Creditors a/c Cr.

Particulars Amt Particulars Amt

To bills payable a/c To bank a/c To discount received a/c To balance c/d

90000 450000 8000 52000 600000

By purchases 600000 600000

Dr. Bank Loan a/c Cr.

Particulars Amt Particulars Amt To balance c/d 300000

300000

By bank 300000 300000

Dr. Sundry Debtors a/c Cr.

Particulars Amt Particulars Amt To sales a/c 1580000

1580000

By bank a/c By discount allowed a/c By bills receivable a/c By balance c/d

980000 12000 20000 568000 1580000

Dr. Sales a/c Cr.

Particulars Amt Particulars Amt To balance b/d 1750000

1750000

By cash a/c By sundry debtors a/c

170000 1580000 1750000

Dr. Bills Receivable a/c Cr.

Particulars Amt Particulars Amt To sundry debtors a/c 20000

20000

By balance c/d 20000 20000

Dr. Bills payable a/c Cr.

Particulars Amt Particulars Amt To balance c/d 90000

90000

By sundry creditors 90000 90000

Dr. Discount received a/c Cr.

Particulars Amt Particulars Amt To balance c/d 8000

8000

By sundry creditors a/c 80000 80000

Dr. Electricity expenses a/c Cr.

Particulars Amt Particulars Amt To cash a/c 20000

20000

By balance c/d 20000 20000

Dr. Sundry expenses a/c Cr.

Particulars Amt Particulars Amt To cash a/c 24000

24000

By balance c/d 24000 24000

Dr. Discount allowed a/c Cr.

Particulars Amt Particulars Amt To sundry debtors a/c 12000

12000

By balance c/d 12000 12000

Dr. Interest on loan a/c Cr.

Particulars Amt Particulars Amt To bank a/c 30000

30000

By balance c/d 30000 30000

Dr. Rent a/c Cr.

Particulars Amt Particulars Amt To cash a/c To outstanding rent a/c

22000 2000 24000

By balance c/d 24000 24000

Dr. Salaries a/c Cr.

Particulars Amt Particulars Amt To bank a/c 216000

216000

By balance c/d 216000 216000

Dr. Drawings a/c Cr.

Particulars Amt Particulars Amt To purchases a/c 6000

6000

By balance c/d 6000 6000

Dr. Charity a/c Cr.

Particulars Amt Particulars Amt To purchases a/c 15000

15000

By balance c/d 15000 15000

Dr. Outstanding rent a/c Cr.

Particulars Amt Particulars Amt To balance c/d 2000

2000

By rent a/c 2000 2000

TRIAL BALANCE as on 31-3- 2017

Particulars Debit (`) Credit (`) Cash a/c Capital a/c Bank a/c Wages a/c Office furniture a/c Purchases a/c Creditors a/c Bank loan a/c Sundry debtors a/c Sales a/c Bills Receivable a/c Bills payable a/c Discount Received a/c Electricity expenses a/c Sundry expenses a/c Discount allowed a/c

134 000

512 000 550 000 512 000 759 000

568 000

20 000

20 000 24 000 12 000

12 00 000

52 000 3 00 000

175 000

90 000 8 000

Interest on loan a/c Rent a/c Salaries a/c Drawings a/c Charity a/c Outstanding rent a/c

30 000 24 000

2 16 000 6 000

15 000

34, 20, 000

2 000

34 ,20, 000

Liabilities Amount Assets Amount Capital 1200000 (-)Drawings (6000) 1194000 (+)Net Profit 128000 Creditors Bank Loan Bills Payable Outstanding Rent

1322000 52000

300000 90000 2000

1766000

Cash Bank Office Furniture Sundry Debtors Bills Receivables Closing Stock

134000 512000 512000 568000 20000 20000

1766000

Particulars Amount(Rs) Particulars Amount(Rs) To Purchases To Wages To Gross Profit To Electricity Expenses To Sundry Expenses To Discount Allowed To Interest on Loan To Rent To Salaries To Charity To Net Profit

759000 550000 461000

1770000

20000 24000 12000 30000 24000

216000 15000

128000

469000

By Sales By Closing Stock By Gross Profit By Discount Received

1750000 20000

1770000

461000 8000

469000

Trading and Profit and Loss a/c for the year ending 31-3 2017

Balance Sheet as on 31-12-2017

Cr.

INDIAN HIGH SCHOOL-DUBAI

HOT QUESTIONS – GRADE 11 – 2017

ACCOUNTANCY

Chapter: Journal Entry

Q.1: Krishna is a whole sale trader dealing in distribution of grocery items. He is also

engaged in the philanthropic work in the society. He is connected to one of the

Organisation who takes care of the orphans and disabled people.

Journalise the following transactions in the books of Krishna for the month of April 2016

also Identify the values. Company has No refund scheme.

1) On 31st March 2017 his books of account showed the following balances.

Balance sheet (31-3-2017)

Liabilities Amount Assets Amount

Capital - 25000 Cash in Hand 430

Add: Additional capital -

4000

Cash at Bank 2500

Less Drawings - 9000 20000 Accounts Receivables 7670

Accounts Payable 5600 Closing stock 9000

Machinery 6000

25600 25600

2) Sold goods to James for 10000 allowing her 10% T.D. and 10% C.D. She paid

25% of the amount is cash at the time of purchase. After that she found half of the

goods are not as per the sample so she returned it.

3) Krishna has decided to send food grains to orphanage on his birthday worth Rs

20,000 (Cost Price Rs 15000)

Answer:

1) Cash in hand A/C Dr. 430

Cash at Bank A/C Dr. 2500

Accounts Receivables A/C Dr 7670

Closing Stock A/C Dr 9000

Machinery A/C Dr 6000

Drawing A/C Dr. 9000

To Accounts Payable 5600

To Capital A/C 29000

2) (A) Cash A/C Dr. 2025

Cash Discount A/C Dr. 225

James A/C Dr. 6750

To Sales A/C 9000

Sales Return A/c Dr. 4500

To James A/C 4500

James A/C Dr. (6750- 4500) 2250

To sales A/C 2250

3) Charity A/c Dr. 15000

To Goods given as charity 15000

*Values: Generous and Kind

Social Responsibility

Chapter: Accounting Equation

Question 1: Complete the gaps in the following table after considering additional

information.

Sr.No Assets Liabilities Capital

1 150000 ? ?

2 ? 17200 ?

3 ? ? 100000

Additional information

1. Started a business on 1st April 2016 with opening capital of 50000,

drawings 15000, additional capital 25000 and profit 65000.

2. The firm has machinery for 50000, furniture 50000, stock 10000,

investment 15000

3. Firm has creditors 10000, bills payable 5000, loan from bank 10000

Answer:

Sr.No Assets Liabilities Capital

1 150000 25000 125000

2 125000 17200 107800

3 125000 25000 100000

Question 2: Why there should be equality in accounting equation. Justify with

example

Answer: Double entry system (one effect debit and another effect credit)

Ex: any transaction of journal entry

* Knowledge & Understanding: Accounting rules of debit credit and Principles of

accounting

Analysis: Breaking down in components as per the required entries.

Evaluation: From the given information (Internal criteria) finding out the values.

Creating: Create journal proper and accounting equation in a proper format.

CHAPTER

SUBSIDIARY BOOKS

1. ABC ltd, a trading firm, purchased goods from RKR co. Though the goods were not as

per their order, ABC Ltd. failed to carry out inspection on receiving goods and send the

stock to the warehouse. the quality difference was noticed on a later date and ABC

approached RKR to return these goods. RKR offered a discount of Rs. 5000 if the firm

retained the goods. The firm accepted the offer and RKR send a credit note for the

amount. in your opinion, what entries should be recorded by RKR Co. and why? Domain : Analysis, Evaluation

2. A wholesaler sold 55 items to a retailerat a price of Rs. 200 each, less trade discount.

The value of sale recorded after deducting trade discount was Rs. 8800. The retailer

subsequently returned 12 out of 55 items. What should be the amount recorded on credit

note? Who will be sending the credit note to whom?

Domain : Analysis, Evaluation

CHAPTER

CASH BOOK

1. Prepare Cash Book with Cash and Bank Column from the following details:

2017

Jan.1 Cash at office `123, and bank overdraft `2575

Jan.2 Cash Sales `1,570.

Jan.3 Deposited into bank `1,500.

Jan.5 Mohan settled his account for ` 750 by giving a cheque for `730.

Jan.7 Mohan’s cheque deposited into bank

Jan.10 Bought goods for `450 and paid by cheque.

Jan.13 Purchased stationery for `75.

Jan.18 Mohan’s cheque returned dishonoured.

Jan.20 Received a cheque for ` 1,500 from Prabhu which is deposited into bank.

Jan.25 Withdrew for office use ` 475.

Jan.31 paid salary by cheque `1,000 and rent in cash `150.

(i) In which side of the cash book will the overdraft in the beginning of the

month be recorded?

(ii) Did the bank overdraft amount reduce at the end of the month?

(iii)Give your suggestions to convert the overdraft balance to bank deposit?

(Analysis, synthesis, Creating)

2. Prepare Analytical Petty Cash book with the help of imaginary figures.

(Creating)

CHAPTER

BANK RECONCILIATION STATEMENT

Bank Reconciliation Statement

Pass Book

Date Particulars withdrawals Deposits Dr/Cr bal Balance

1.1.14

3.1.14

5.1.14

6.1.14

10.1.14

31.1.14

By balance

To self

To Farha & co

By cash

By dividend

To Bankcharges

6,000

5,000

250

4,500

10,000

Cr

Dr

Dr

Cr

Cr

Dr

50,000

44,000

39,000

43,500

53,500

53,250

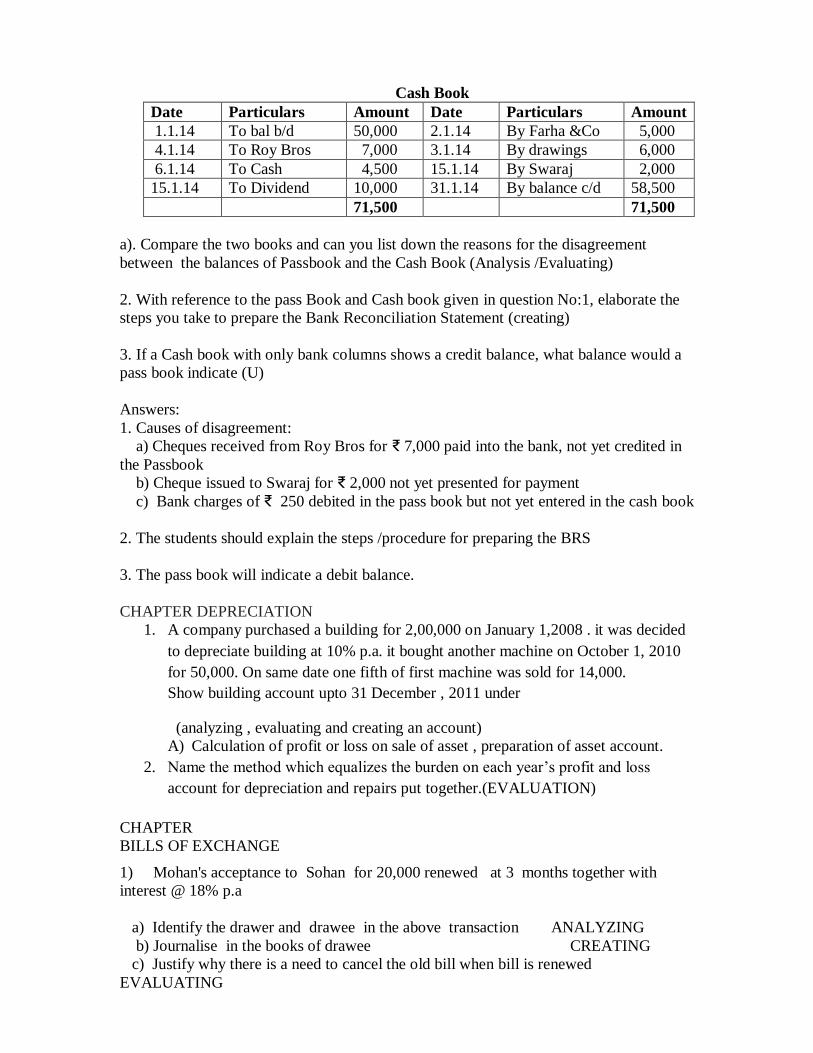

Cash Book

Date Particulars Amount Date Particulars Amount

1.1.14 To bal b/d 50,000 2.1.14 By Farha &Co 5,000

4.1.14 To Roy Bros 7,000 3.1.14 By drawings 6,000

6.1.14 To Cash 4,500 15.1.14 By Swaraj 2,000

15.1.14 To Dividend 10,000 31.1.14 By balance c/d 58,500

71,500 71,500

a). Compare the two books and can you list down the reasons for the disagreement

between the balances of Passbook and the Cash Book (Analysis /Evaluating)

2. With reference to the pass Book and Cash book given in question No:1, elaborate the

steps you take to prepare the Bank Reconciliation Statement (creating)

3. If a Cash book with only bank columns shows a credit balance, what balance would a

pass book indicate (U)

Answers:

1. Causes of disagreement:

a) Cheques received from Roy Bros for ₹ 7,000 paid into the bank, not yet credited in

the Passbook

b) Cheque issued to Swaraj for ₹ 2,000 not yet presented for payment

c) Bank charges of ₹ 250 debited in the pass book but not yet entered in the cash book

2. The students should explain the steps /procedure for preparing the BRS

3. The pass book will indicate a debit balance.

CHAPTER DEPRECIATION

1. A company purchased a building for 2,00,000 on January 1,2008 . it was decided

to depreciate building at 10% p.a. it bought another machine on October 1, 2010

for 50,000. On same date one fifth of first machine was sold for 14,000.

Show building account upto 31 December , 2011 under

(analyzing , evaluating and creating an account)

A) Calculation of profit or loss on sale of asset , preparation of asset account.

2. Name the method which equalizes the burden on each year’s profit and loss

account for depreciation and repairs put together.(EVALUATION)

CHAPTER

BILLS OF EXCHANGE

1) Mohan's acceptance to Sohan for 20,000 renewed at 3 months together with

interest @ 18% p.a

a) Identify the drawer and drawee in the above transaction ANALYZING

b) Journalise in the books of drawee CREATING

c) Justify why there is a need to cancel the old bill when bill is renewed

EVALUATING

ANS MOHAN --DRAWEE , SOHAN --- DRAWER

2) FILL IN THE BLANKS :

Shyam Dr 6000

To Bills Payable ------------

To ------------------ 100

(Being the bill accepted in full payment of the claim)

Bills Payable A/c Dr ------------

-------------------------- Dr 100

Noting charges A/C Dr --------------

To------------- 6150

(Being the bill dishonoured ,noting charges paid)

Write the journal entry in case noting charges are not paid

(ANALYSING , EVALUATING , CREATING)

Rectification of Errors.

1. Rectify the following journal entries and state whether these errors cause disagreement

of the Trial Balance (A/E)

a) A cheque from A for ₹ 150 has been correctly entered in the Cash book, but has

been posted to the credit of A as ₹ 100.

b) Goods returned to the firm by B amounting to ₹ 80 had been recorded in the Sales

Return Book, but the entry had not been posted to the Personal A/c

2. Read the transaction, examine the journal entry recorded. by your accountant

(Analyzing)

a) Wages paid for the installation of machinery ₹ 350

b) Credit sales to Kumar ₹ 3,950.

Do you agree with the entries recorded in the Journal? (Evaluating)

If you disagree, how can you elaborate on the reason? (Creating)

JOURNAL ENTRIES

Particulars L.F Debit Credit

Wages A/c Dr

To Cash A/c

350

350

Kumar’s A/c Dr

To Sales A/c

3,590

3,590

Answers:

1)

Particulars L.F Debit Credit

Suspense A/c Dr

To A’s A/c

(Being A’s A/c credited short now rectified)

50

50

Suspense A/c Dr

To B’s A/c

(Being B’s A/c omitted to be posted now rectified)

80

80

Both the transactions cause the disagreement of the Trial Balance.

2. No I disagree. Errors have been made while recording the transactions in the journal.

Reasons for disagreement.

a) Wages paid for the installation of machinery debited to wages account

b) Credit sales to Kumar for ₹ 3,950 recorded as ₹ 3590.

CHAPTER

FINAL ACCOUNTS

1. Point whether the following transactions are capital expenditure or revenue

expenditure and also explain the treatment of these transactions in the final

accounts:

i) Payment of wages amounting to `2,50,000 for construction of building.

ii) Renewal fee of license `200.

iii) Distribution of free goods costing `40,000 to introduce the goods in the

market.

iv) Cost of furnishing the newly constructed building `20,000.

(ANALYSING)

2. A manager is entitled to a commission of 10% on net profit before charging such

commission. Net profit before charging such commission is `1, 00,000. Find out

the commission payable to manager and show how it will be treated in final

accounts. (APPLICATION)

CHAPTER SINGLE ENTRY SYSTEM OF ACCOUNTING

1. Mr. sharma is doing a small trading business in stationary items. He is not

maintaining proper books of accounts as it is expensive. At the beginning of the

year he had cash in hand ` 20,000; Furniture – `30,000; debtors – `6,000;

computer – `11,000.

When he started his business on 1st January 2012 he had borrowed from his friend

`15,000. Interest @ 5% p.a.is unpaid for the current year.

At the end of the year, he had cash in hand `25,000; furniture – `30,000; debtors-

`7,000; computer – `11,000.

One of the debtor became insolvent. The amount due from him was `2,000. 60

paise in rupee was recovered from his official receiver as final dividend.

Which system of accounting is suitable for Mr. sharma’s business? Give reasons?

(Evaluating)

Calculate profit or loss for the year ended on 31st December 2016.

(Creating)

2. Compare Single entry system of accounting and double entry system of

accounting .

3. How can you prove that double entry system of accounting is better than single

entry system of accounting? (Evaluating)

Not -For Profit Organisation

1. How would you present the following case while preparing the final accounts of a Non

profit organization for the year 2012

a) subscription received during the year 2012 –

2011 ₹ 40

2012 ₹ 2,050

2013 ₹ 60

There are 500 members each paying an annual subscription of ₹ 5, ₹ 50 are still in

arrears for the

year 2011. ( A/E)

2. Calculate the stationery consumed and show how you will present deal them while

preparing

the final accounts for the year 2012

1/1/2012 31/12/2012

Stock of stationery ₹ 300 ₹ 50

Creditors for stationery ₹ 200 ₹ 130

Advance paid for stationery ₹ 20 ₹ 30

Amount paid for stationery during 2012 ₹ 1,080 (A/E)

Answers:

1) Subscription income ₹ 2,500

2) Stationery consumed ₹ 1,250

Faculty Members of the Morning Shift

Dr Girija GKrishnan HOD

Lead Teachers

Mrs Mary John --ACCOUNTS

Mrs Roshini Elezabeth Alex ---BUSINESS STUDIES

Mrs Ancy Ann Varghese ---- Entrepreneurship

Mrs Arshiya -----Marketing

Mrs Priya Godvani ----- Salesmanship

Teachers

Mrs Vidhi Ahuja

Mrs Rakhee Nandakumar

Mrs Prashanti.V

Mrs Savitha Roy Thattil

Mrs Preetha Balajiprasad

Mrs Renette James

Mrs Upma Sharma

Mrs Sreeranjini Sunilkumar

Dr Richa vij

Mrs Anupama Murthy

Mrs Saritha Simon

Mrs Hema Takkar

Faculty Members of the Afternoon Shift

Dr. David Thomas

Mr. Leslie Saldanha

Mrs. Parveen

Mrs. Minimol

Mrs. Saraswathi

Dr. Renju Elizabeth

Lead Teachers

Mrs. Zayeda Ashraf --ACCOUNTS

Mrs Shisa Nair --- BUSINESS STUDIES

Mr.D Chandrasekaran ---- Entrepreneurship

Mrs. Kinjal Shah -----Marketing

Mrs. Srijaya V ----- Salesmanship

HOD

Paulson Thomas