Embed Size (px)

Citation preview

i

THE INFLUENCE OF NPL, NIM and ROA TOWARD EARNING

PER SHARE (EPS) OF COMMERCIAL BANK IN INDONESIA

(A case study of PT. Bank Central Asia Tbk period 2007 - 2016)

By:

Billy Thenu

ID: 014201400025

A Skripsi presented to the

Faculty of Business President University

In partial fulfillment of the requirements for

Bachelor Degree in Management

May 2018

ii

PANEL OF EXAMINERS

APPROVAL SHEET

The Panel of Examiners declare that the skripsi entitled “THE

INFLUENCE OF NPL, NIM & ROA TOWARD EARNING PER

SHARE (EPS) OF COMMERCIAL BANK IN INDONESIA (A case

study of PT. Bank Central Asia Tbk. period 2007-2016)” that was

submitted by Billy Thenu majoring in Management from the Faculty of

Business was assessed and approved to have passed the Oral Examinations

on 22 May 2018

Purwanto S.T., M.M.

Chair-Panel of Examiner

Liswandi S.Pd,M.M.,Ph.D

Examiner 2

Pandu Adi Cakranegara S.E, M.Sc. FI,MBA

Examiner 3

iii

DECLARATION OF ORIGINALITY

I declare that this skripsi, entitled “THE INFLUENCE OF

NPL, NIM AND ROA TOWARD EARNING PER SHARE

(EPS) OF COMMERCIAL BANK IN INDONESIA (A case

study of PT. Bank Central Asia Tbk. period 2007-2016)” is,

to the best of my knowledge and belief, an original piece of work

that has not been submitted, either in a whole or in a part, to

another university to obtain a degree.

Cikarang, Indonesia, 1 May 2018

Billy Thenu

iv

ABSTRACT

Nowaday, the presence of bank is increasingly important in daily life. This research

was conducted to assess the influence of non-performing loans, net interest margin and

return on assets toward earning per share of PT. Bank Central Asia, Tbk.period 2007 -

2016.This research based on the Financial Statement of PT. Bank Central Asia Tbk

period 2007-2016 quarterly. Data analysis technique used is multiple linear regression

and test hypotheses using t-statistic for testing the partial regression coefficient and F-

statistics to test the effect with a significance level 5%. It also tested the classical

assumption that included tests of normality, multicollinearity test, test of

heteroscedasticity and autocorrelation test. The results indicate that Non-Performing

Loans, Net Interest Margin and Return on Asset have significant positive effect towards

the Earning Per Share in PT. Bank Central Asia Tbk. Predictive ability of three

variables to EPS in this research 65.3% while the remaining 34.7% affected by other

factors not included in the research model.

Keywords: Non-Performing Loan (NPL), Net Interest Margin, Return on Assets

(ROA), Earning per Share (EPS), Financial Ratio.

v

ACKNOWLEDGEMENT

First of all, the researcher would like praise to God for his blessings, the researcher

could finish this research as a requirement to obtain a Bachelor Degree. In this preface,

the researcher would like to express sincere gratitude to:

1. Researcher’s family who always help and support me to complete this skripsi.

Without their help and support I might not be able to complete this skripsi.

2. Mr. Purwanto ST., M.M as researcher thesis advisor who have taught and guide

me to complete this thesis.

3. Researcher’s friends that can’t be mentioned one by one and those who

indirectly contribute in this research, thank you very much..

The researcher is fully aware that this thesis is far away from perfection, but hopefully

this thesis can give positive contribution to the readers and provide information for

people who need it. The researcher hope this thesis can give positive contribution to

the readers.

vi

TABLE OF CONTENTS

PANEL OF EXAMINERS ..................................................................... i

APPROVAL SHEET ............................................................................ ii

DECLARATION OF ORIGINALITY................................................iii

ABSTRACT .......................................................................................... iv

ACKNOWLEDGEMENT .................................................................... v

TABLE OF CONTENTS ..................................................................... vi

LIST OF TABLES ............................................................................... ix

LIST OF FIGURES............................................................................... x

LIST OF EQUATION .......................................................................... xi

LIST OF ACRONYMS ....................................................................... xii

CHAPTER I INTRODUCTION .......................................................... 1

1.1. Background of the Study .......................................................... 1

1.2. Problem Identification .............................................................. 3

1.3 Statement of Problem ................................................................... 3

1.4. Research Objective ...................................................................... 3

1.5. Definition of Terms ....................................................................... 4

1.6 Scope and Limitation .................................................................... 5

1.7 Benefit of the study ...................................................................... 5

1.7.1 For Academic ........................................................................ 5

1.7.2 For the Organization ............................................................. 5

1.7.3 For Future Researcher ........................................................... 5

CHAPTER II LITERATURE REVIEW ............................................. 6

vii

2.1 Theoretical Review .................................................................. 6

2.1.1 Non-Performing Loan ........................................................... 6

2.1.2 Net Interest Margin ............................................................... 7

2.1.3 Return on Assets ................................................................... 7

2.1.4 Earnings per Share ................................................................ 8

2.2 The relationship between NPL, NIM and ROA to EPS ............ 8

2.2.1 The relationship between NPL to EPS .................................. 8

2.2.2. Relationship between ROA and NIM to EPS ........................ 9

2.3 Bank....................................................................................... 10

2.4 Analysis Method of financial statements ................................ 11

2.5 Method of Ratio Analysis ...................................................... 12

2.6 Financial ratios ....................................................................... 13

2.6 Previous Research ................................................................. 14

2.7 Theoretical Framework ............................................................... 16

2.8 Hypothesis ............................................................................. 17

CHAPTER III METHODOLOGY .................................................... 18

3.1. Research Design..................................................................... 18

3.2. Research Framework .............................................................. 19

3.3 Research Instrument ............................................................... 20

3.3.1 Type and source of data ...................................................... 20

3.3.2 Data Collection Method ...................................................... 21

3.3.3 Data Analysis Method .......................................................... 21

3.4. Sampling Design .................................................................... 22

3.5. Testing the Hypothesis and Data Analysis ............................. 23

3.5.1 Multiple Regression Analysis ............................................. 23

3.5.2 Classical Assumption Test .................................................. 24

3.5.3 Measuring the Variability of the Regression Model ............ 28

3.5.4 Testing the Hypothesis ........................................................ 29

CHAPTER IV ANALYSIS AND INTERPRETATION ................... 32

viii

4.1. PT. Bank Central Asia Tbk. Company Profile ........................ 32

4.2. Data Analysis .............................................................................. 33

4.2.1 Description of each variable ...................................................... 33

4.2.2 Descriptive Statistical Analysis .............................................. 35

4.2.3 Classical Assumption Test Result .......................................... 37

1. Normality Test ............................................................................ 37

2. Autocorrelation Test ................................................................... 38

3. Multicollinearity Test ................................................................. 39

4.2.3 Multiple Regression Analysis ............................................. 41

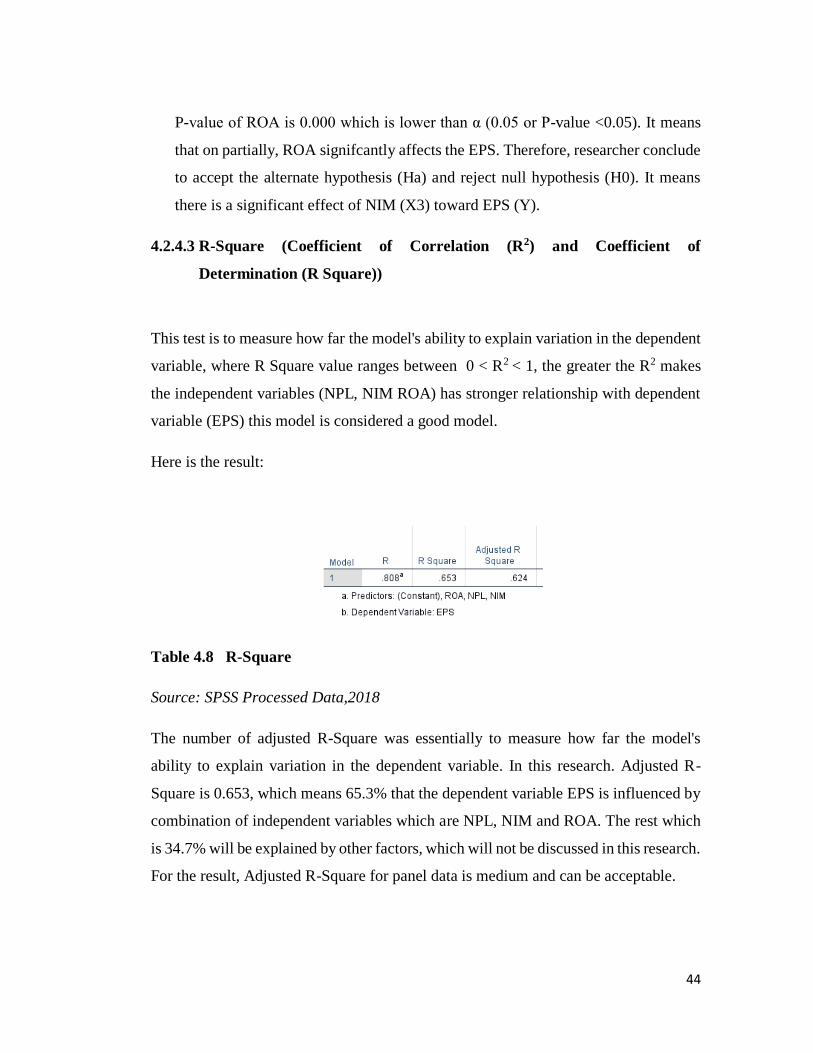

4.2.4 Goodness or Fit Test ........................................................... 42

4.3. Interpretation of Results ......................................................... 45

4.3.1 The influence of Non-Performing Loan (NPL) towards

Earning Per Share (EPS) ................................................................. 45

4.3.2 The influence of NIM towards EPS..................................... 45

4.3.3 The influence of ROA towards EPS .................................... 45

4.3.4 The influence of NPL, NIM & ROA towards EPS. ............. 46

CHAPTER V CONCLUSION AND RECOMMENDATION .......... 47

5.1. Conclusion................................................................................. 47

5.2 Recommendation ....................................................................... 47

BIBLIOGRAPHY ............................................................................... 49

APPENDIX .......................................................................................... 56

ix

LIST OF TABLES

Table 4.1 Bank Central Asia financial highlight…………………….. 33

Table 4.2 Component ratio of each variable………………………….. 34

Table 4.3 Descriptive Statistic………………………………………... 37

Table 4.4 Autocorrelation Test……………………………………….. 39

Table 4.5 Multicollinearity Test……………………………………… 40

Table 4.6 Coefficients………………………………………………... 42

Table 4.7 F-Test………………………………………………………. 43

Table 4.8 R-Square………………………………………………….... 45

x

LIST OF FIGURES

Figure 2.1 Theoretical Framework…………………………………….. 18

Figure 3.1 Research Framework………………………………………. 21

Figure 4.1 Normal P-Plot of Regression Standardized Residual……… 38

Figure 4.2 Histogram………………………………………………….. 39

Figure 4.3 Scatterplot…………………………………………………...41

xi

LIST OF EQUATION

Equation 1 Non-Performing Loan………………………….. 7

Equation 2 Net Interest Margin…………………………….. 8

Equation 3 Return On Asset……………………………….. 9

Equation 4 Earning Per Share ……………………………... 10

Equation 5 Multiple Linear Regression Model…………….. 24

Equation 6 Variance Inflation Factor Model ………………… 26

Equation 7 Durbin-Watson D-Test ………………………….. 27

Equation 8 Coefficient of Determination……………………. 29

Equation 9 Coefficient of Correlation ……………………….. 30

Equation 10 F-Test…………………………………………….. 31

Equation 11 T-Test…………………………………………….. 32

xii

LIST OF ACRONYMS

NPL : Non-Performing Loan

NIM : Net Interest Margin

ROA : Return On Asset

EPS : Earning per Share`

1

CHAPTER 1

INTRODUCTION

1.1. Background of the Study

Bank holds important role in every country economy. Since many sectors are rely on

banking industry support such as agriculture, farm, construction, trade, real estate and

other sector. In addition, banking industry provide investor instrument to channel their

fund or in other word provide investment instrument. Bank financial statement provide

key metric for their stakeholder especially investor.

Essentially, banking can be translated as the business activity of accepting and

preserving money by depositor, and then lending out this money in order to earn a

profit (Goyal, 2014). To be more specific, banking is vital economic infrastructures,

which perform three main functions: accepting deposits, lending money and money

transfer services.

Broadly speaking bank plays an important role in economy. Modern financial set-up

contributes to economic improvement and consequently lead to the increasing living

standards as it is put on numerous contribution to the remainder economy in present

day. Bank specialize in function to ensure borrowers fulfill their obligations related to

the credit. There is a tendency a more developed country capital market's dominantly

supplying financial products and services relative supplied by the bank (Bollard, 2011).

Since decades, the banking industry in Indonesia has made tremendous progress in the

country. This is due to the Indonesian government’s deregulation of the banking

industry commenced in June 1983 (Low, 1997).The changes are technology innovation

and financial services deregulation (Mihaljek, 2009).

2

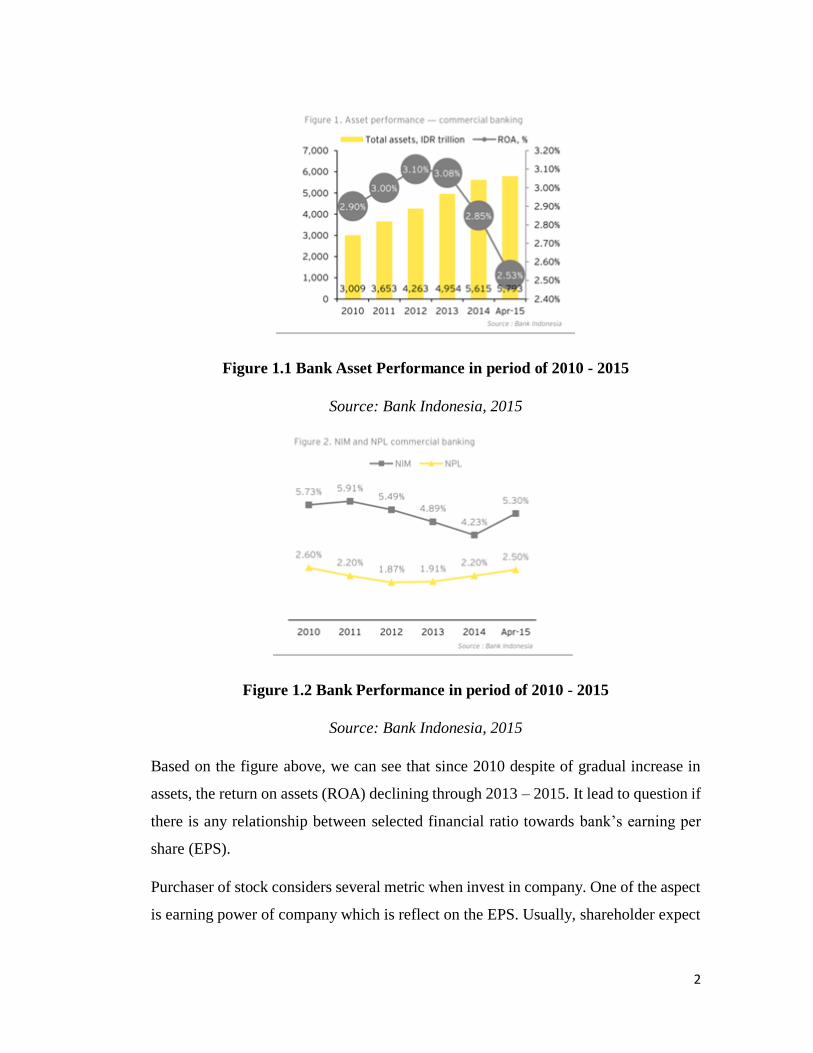

Figure 1.1 Bank Asset Performance in period of 2010 - 2015

Source: Bank Indonesia, 2015

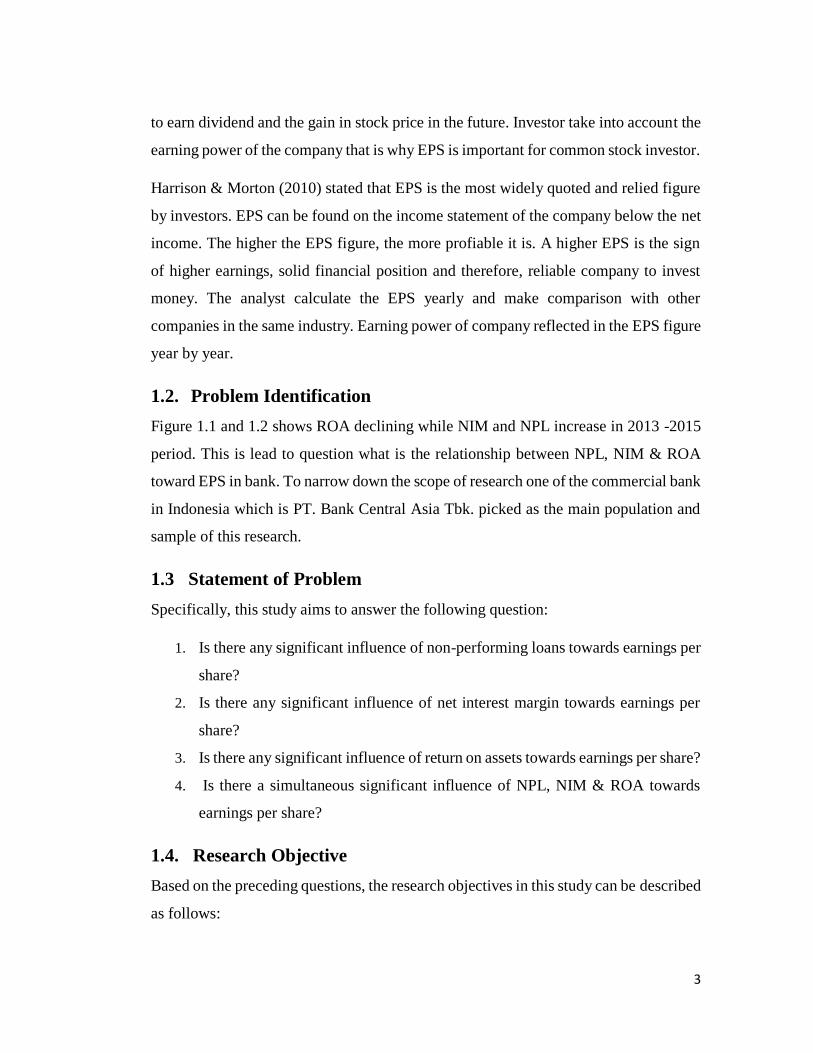

Figure 1.2 Bank Performance in period of 2010 - 2015

Source: Bank Indonesia, 2015

Based on the figure above, we can see that since 2010 despite of gradual increase in

assets, the return on assets (ROA) declining through 2013 – 2015. It lead to question if

there is any relationship between selected financial ratio towards bank’s earning per

share (EPS).

Purchaser of stock considers several metric when invest in company. One of the aspect

is earning power of company which is reflect on the EPS. Usually, shareholder expect

3

to earn dividend and the gain in stock price in the future. Investor take into account the

earning power of the company that is why EPS is important for common stock investor.

Harrison & Morton (2010) stated that EPS is the most widely quoted and relied figure

by investors. EPS can be found on the income statement of the company below the net

income. The higher the EPS figure, the more profiable it is. A higher EPS is the sign

of higher earnings, solid financial position and therefore, reliable company to invest

money. The analyst calculate the EPS yearly and make comparison with other

companies in the same industry. Earning power of company reflected in the EPS figure

year by year.

1.2. Problem Identification

Figure 1.1 and 1.2 shows ROA declining while NIM and NPL increase in 2013 -2015

period. This is lead to question what is the relationship between NPL, NIM & ROA

toward EPS in bank. To narrow down the scope of research one of the commercial bank

in Indonesia which is PT. Bank Central Asia Tbk. picked as the main population and

sample of this research.

1.3 Statement of Problem

Specifically, this study aims to answer the following question:

1. Is there any significant influence of non-performing loans towards earnings per

share?

2. Is there any significant influence of net interest margin towards earnings per

share?

3. Is there any significant influence of return on assets towards earnings per share?

4. Is there a simultaneous significant influence of NPL, NIM & ROA towards

earnings per share?

1.4. Research Objective

Based on the preceding questions, the research objectives in this study can be described

as follows:

4

1. To determine if there's significant influence of non-performing loans toward

the earnings per share.

2. To determine if there's significant influence of net interest margin toward the

earnings per share.

3. To determine if there's significant influence of return on asset toward the

earnings per share.

4. To determine if there's a significant simultaneous influence of NPL, NIM and

ROA toward the earnings per share.

1.5. Definition of Terms

Some terms used in this research are as follow:

1. Bank: A financial institution acting as a receiver of deposits from the public

and lend them for investment purpose (Josh, 2012).

2. Bank Capital: funds kept by banks from the depositors and published in the

balance sheet in order to cover depositors and creditors against loss. (Olalekan,

2013).

3. Commercial Bank: common type of bank that is mainly handle loans and

deposits and having access to financial market (Kugiel, 2009).

4. Non-Performing Loans: is a loan that is default or close to being in default.

Generally, this loans become non-performing after being default for 3 months

(90 days) depend on the contract (Aziz, 2009).

5. Net Interest Margin: a metric that examines how successful a company's

funding decisions are compared to its debt situation (Evans, 2014). Is one the

indicators that can assess the profitability. NIM is a ratio that used to examine

their activity of asset productivity in order to get an interest.

6. Earnings Per Share: profit attributable to equity owned divided by number of

ordinary shares.

7. Return On Assets: is a metric to measure a company’s ability to generate

earnings from investment activities.

5

1.6 Scope and Limitation

This study is limited to the scope of biggest bank by total assets in Indonesia. The

author chose PT. Bank Central Asia Tbk because it is the largest bank by total asset

and public non-government companies. In other word not owned by government. The

financial ratio is limited to NPL, NIM, ROA & EPS.

1.7 Benefit of the study

This research has objectives to be achieved in academic research community,

organization and other researchers. The following below are the benefit of this

research:

1.7.1 For Academic

To give the contribution to the academic study and other. This research give an insight

that the theory studied by students will have application in the real working world. It

would be better for academic institution to have various approach on teaching theory

by combination with this study.

This will definitely help students to solve problems and not focused on proposed theory

without observing the real business condition.

1.7.2 For the Organization

It provide company information about their positioning and historical data as a

benchmarking for company to perform better than before.

1.7.3 For Future Researcher

Because this research is for partial fulfilment of the requirement for Bachelor Degree

and also by doing this research the researcher can apply the theory that obtained during

study process into the real market environment. There are more knowledge about NPL,

NIM, ROA and Earnings Per Share (EPS). The researcher gains knowledge &

motivation in higher education institution. This knowledge will be useful in the future

to be applied in when entering workplace.

6

CHAPTER II

LITERATURE REVIEW

2.1 Theoretical Review

Since this paper about financial ratios relation correspond to profitability which is

important for the business shareholders which is the investor, the value maximization

theory is comprised. Value maximization theory as mentioned in this paper states the

one objective of a firm’s existence is to maximize profits in the short run and maximize

shareholders wealth in the long run (Friedman, 1970). The theory said that all the

organization activities primary goal is to profit even though there are charitable

activities included in the company activities. The value maximization theory point-out

shareholder's wealth maximization including financial claimant maximization such as

debt and warrant holders. Therefore, EPS which is a profitability metric which may

influenced by NPL, NIM and ROA are one of the important metric the investor count

on when decide to invest in a company.

2.1.1 Non-Performing Loan

IMF (2004) stated non-performing loans is any loan already exceeds its maturity date

and part of the loan is still outstanding. The specific definition is dependent upon the

loan’s particular terms.

According to Riyadi (2004), the credit risk is a risk that appears if a lenders unable to

return the fund that borrows along with the interest. The level of credit can be

formulated as follows:

(Equation 1)

Non-Performing Loan = Total NPL x 100%

Total Loan

7

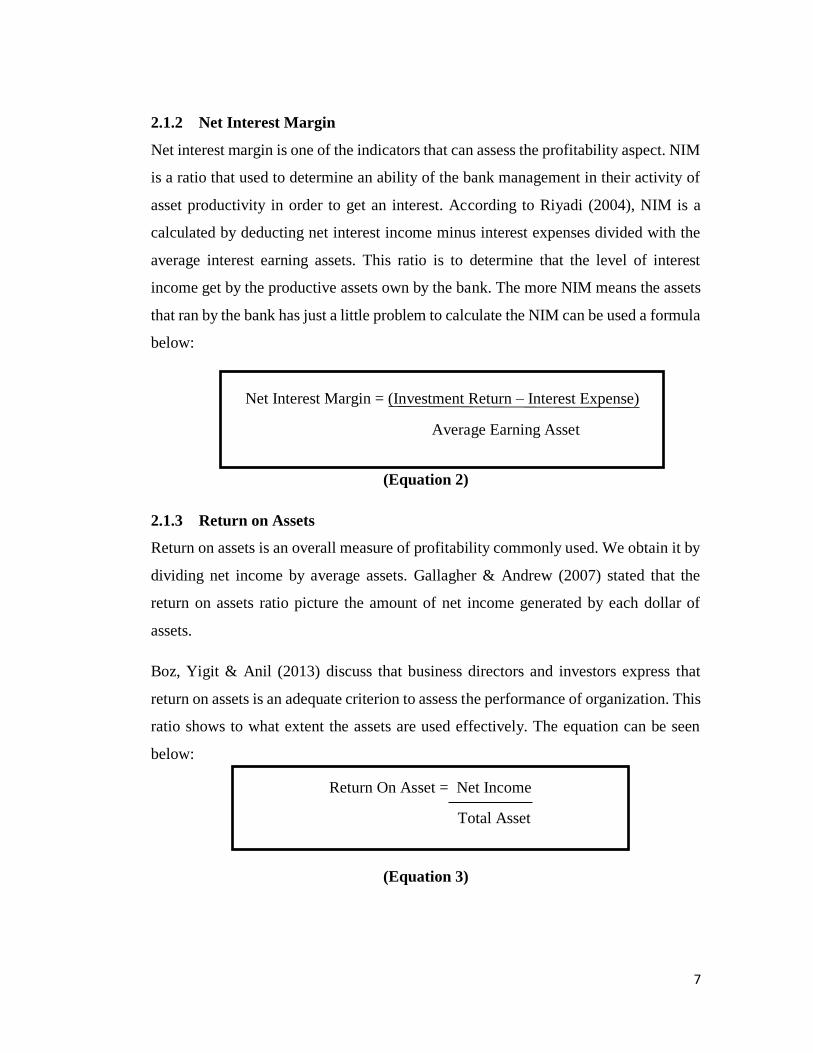

2.1.2 Net Interest Margin

Net interest margin is one of the indicators that can assess the profitability aspect. NIM

is a ratio that used to determine an ability of the bank management in their activity of

asset productivity in order to get an interest. According to Riyadi (2004), NIM is a

calculated by deducting net interest income minus interest expenses divided with the

average interest earning assets. This ratio is to determine that the level of interest

income get by the productive assets own by the bank. The more NIM means the assets

that ran by the bank has just a little problem to calculate the NIM can be used a formula

below:

(Equation 2)

2.1.3 Return on Assets

Return on assets is an overall measure of profitability commonly used. We obtain it by

dividing net income by average assets. Gallagher & Andrew (2007) stated that the

return on assets ratio picture the amount of net income generated by each dollar of

assets.

Boz, Yigit & Anil (2013) discuss that business directors and investors express that

return on assets is an adequate criterion to assess the performance of organization. This

ratio shows to what extent the assets are used effectively. The equation can be seen

below:

(Equation 3)

Net Interest Margin = (Investment Return – Interest Expense)

Average Earning Asset

Return On Asset = Net Income

Total Asset

8

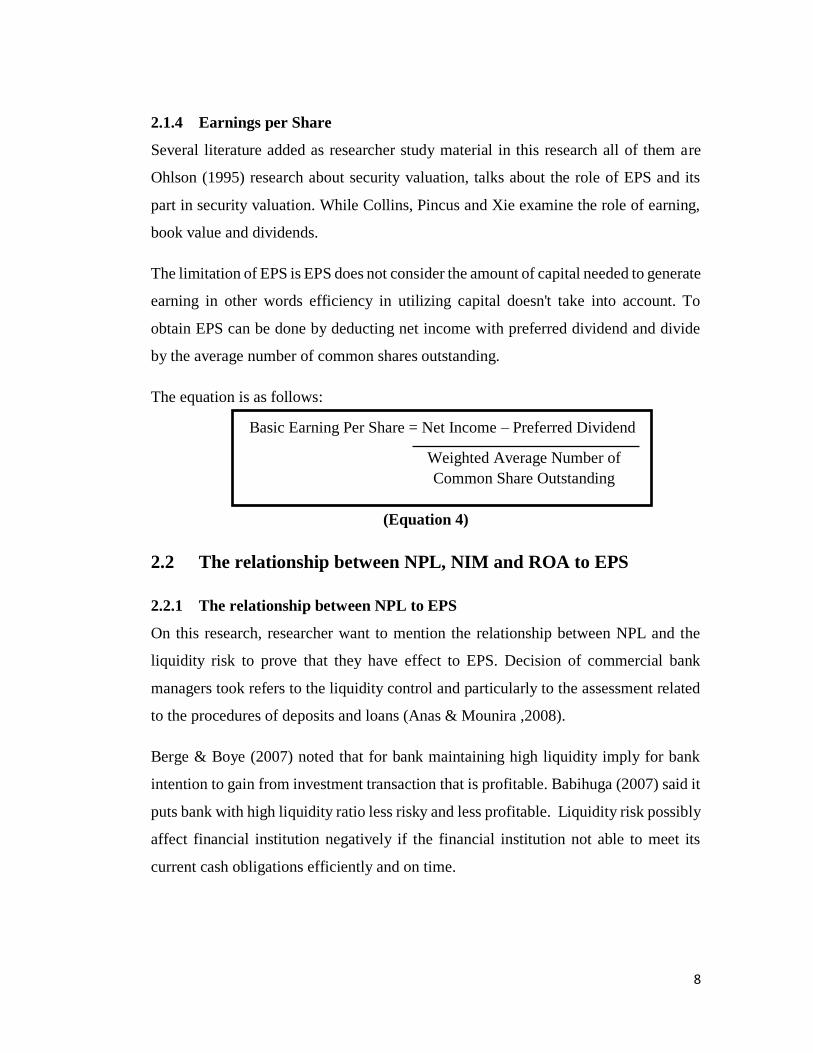

2.1.4 Earnings per Share

Several literature added as researcher study material in this research all of them are

Ohlson (1995) research about security valuation, talks about the role of EPS and its

part in security valuation. While Collins, Pincus and Xie examine the role of earning,

book value and dividends.

The limitation of EPS is EPS does not consider the amount of capital needed to generate

earning in other words efficiency in utilizing capital doesn't take into account. To

obtain EPS can be done by deducting net income with preferred dividend and divide

by the average number of common shares outstanding.

The equation is as follows:

(Equation 4)

2.2 The relationship between NPL, NIM and ROA to EPS

2.2.1 The relationship between NPL to EPS

On this research, researcher want to mention the relationship between NPL and the

liquidity risk to prove that they have effect to EPS. Decision of commercial bank

managers took refers to the liquidity control and particularly to the assessment related

to the procedures of deposits and loans (Anas & Mounira ,2008).

Berge & Boye (2007) noted that for bank maintaining high liquidity imply for bank

intention to gain from investment transaction that is profitable. Babihuga (2007) said it

puts bank with high liquidity ratio less risky and less profitable. Liquidity risk possibly

affect financial institution negatively if the financial institution not able to meet its

current cash obligations efficiently and on time.

Basic Earning Per Share = Net Income – Preferred Dividend

Weighted Average Number of

Common Share Outstanding

9

Lynch (2007), stated that financial institution as well as banker put substantial concern

in cash adequacy for clearing responsibilities on time. Liquidity risk could happen if

the management unable to mitigate risk and plan in finding cash sources. Liquidity risk

occurs when there is a sudden rush in liability withdrawals resulting in a bank to

liquidate assets to meet the demand (Eakins, 2008). Maintaining cash reserves while at

the same time increase investment to maximize earnings (Brigham & Ehrhardt, 2005).

It concluded that NPL and EPS have a negative relationship because NPL belongs to

Liquidity ratio in bank.

2.2.2. Relationship between ROA and NIM to EPS

Both of ROA and NIM are belong to profitability ratios. EPS is a good indicator of the

profitability and it is used measures of profitability (Ratios, 2012). Hence, ROA and

NIM have close relationship with EPS.

ROA shows investors what earning had been generated from invested capital (assets).

ROA for public banks can range significantly and might be pretty dependent on the

industry. This is why when using ROA as a comparative measure, it is best to compare

it towards the ROA of comparable bank. The ROA is a better gauge than simple EPS

of how bank is deploying its capital to build a profitable business. The higher ROA,

the more wealth the bank is creating for its shareholders and the better return they can

expect from their investment (Streissguth, 2014). The bank's ROA should be compared

to that of its competitors and other banks, whereas EPS is better used as a gauge of

whether the shares themselves are sometimes over or undervalued. If ROA increase in

the number, it will be a positive influence to EPS.

Based on the model developed by Ho & Saunders (1981), bank uncertainty derived

from asynchronous and random coming of deposits and loans. Typically, bank choose

the most beneficial loans and deposits increase / reduction. It mitigates the unused

demand of deposits or loans supply. Maximization of NIM in these models is the basic

assumption in bank behavior for these models.

10

2.3 Bank

A bank is a licensed order by a government to accept money from depositor, act as an

intermediary in financial transactions, clear checks, lend money and offer other

financial services to its clients. Jeanne Gobat (2012) explained some functions of a

bank include making loans, creating money and transmitting monetary policy. Her

explanations will be listed below.

Making Loans

When people make some deposits to a bank, the bank may be used the money as long-

term loans. That money which is the shorter-term deposits is used by banks to make

longer - term goals.

Creating Money

Banks also involved in creation of money. Bank have to maintain reserve and not lend

out, some portion of their deposits.

Transmitting Monetary Policy

Banks has important role in the monetary policy transmission for achieving economic

growth without inflation. Bank safety and soundness are a major public concern, one

of the government’s critical tools and government regulations were designed to limit

bank failures and the panic they can cause. Every bank tries to avoid the exposure risks

like credit risk, market risk and overall solvency risk. That is where regulations are

designed for.

In general, any company either bank or non-bank in a certain period will do reporting

its financial activity. Information about the company's financial processes, company

performance, cash flow and any information referring to the activities of financial

statements received from the company's financial statements. According to Bachtiar

(2014) the financial statements will present most of the data on the economic activities

of public companies that investors and other parties need. According to PSAK financial

statements are reports that illustrate the financial impact of transactions and other

11

events classified in several major groups according to their economic characteristics.

Based on the previous sentence it can be said that the financial statements are reports

that present the company's economic activities derived from transactions and other

events classified in groups that are expected to provide information or a better picture

of the prospects and risks of the company to investors and other parties who appeal.

2.4 Analysis Method of financial statements

According to Kashmir (2014) analysis of financial report needs to be done. Financial

statements become more useful so it can be understood by various parties.

For owners and management, the main purpose of financial statement analysis is to

know the current financial position of the company. By knowing the position of

financial statements, after the analysis of financial statements in depth, will look,

whether the company can achieve the target that has been planned previously or not.

The results of this financial statement analysis will also tell information about the

weaknesses and strengths of the company. By understanding this, management can

improve or cover-up those weaknesses. Then the strength of the company must be

maintained or even improved.

There are two kind of financial statements technique analysis commonly used

according to Kashmir (2014), namely:

a. Vertical Analysis (Static)

Vertical analysis is an analysis performed on only one financial reporting period.

Analysis is conducted between existing posts, in one period. Information obtained only

for one period only and unknown progress from period to period.

b. Horizontal analysis (Dynamic)

Horizontal analysis is an analysis performed by comparing the financial statements for

several periods. From the results of this analysis will see the development of the

company from one period to another. Then, in addition to the methods used above,

12

there are also other financial statement analysis, here are some analysis that can be

done.

1) Trend Analysis

Trend Analysis or tendency is an analysis of financial statements that are usually

expressed in certain percentages. This analysis is conducted from period to period

so it will be seen whether the company experienced a change that is up, down, or

fixed, and how big the change is calculated in percentage.

2) Fund Source and Use of Fund Analysis

Analysis of sources and use of funds is an analysis conducted to determine the

sources of corporate funds and the use of funds in a period. This analysis is also to

determine the amount of working capital and the causes of changes in working

capital of a company within a period.

3) Source Analysis and Cash Usage

Analysis of sources and use of cash is an analysis used to determine the source of

the company's cash and use of cash in a period. In addition, also to determine the

causes - the change in the amount of cash in a certain period.

2.5 Method of Ratio Analysis

Ratio analysis is an analysis used to determine the relationship that exist in one

financial statement or between the balance sheet financial statements and income

statement.

a) Gross Profit Analysis

Gross profit analysis is an analysis used to determine the amount of gross profit

from period to period. Then also to find out the causes of the change in gross profit

between periods.

13

b) Break Even Point Analysis

Break-even point analysis. The purpose of this analysis is to find out on what

conditions the sale of the product is done and the company does not lose. The

usefulness of this analysis is to determine the amount of profit at different levels of

sales.

2.6 Financial ratios

The definition of financial ratios according to James C Van Horne (2014) is an index

that relates two accounting numbers and is obtained by dividing one number by

another. Financial ratios are used to evaluate the company's financial condition and

overall performance. From the results of this financial ratio will be seen the health

condition of the company concerned. The company's financial ratios can help us to

identify some of the weaknesses and strengths of the company. With this financial ratio

we can make two ways of comparison, ie by comparing the ratio between time and we

can also compare the ratio of companies with other companies (Keown, et al, 2011).

So we can conclude the financial ratios is an analytical method obtained by dividing a

number by another number contained in the balance sheet or income statement

individually or in combination of both reports are used to know and evaluate the

financial condition and performance of the company concerned.

Forms of financial ratios:

According to Dendawijaya (2005) form of financial ratio are as follows:

1. Liquidity Ratio

Dendawijaya (2005), stated liquidity ratios used in regular basis in assessing bank

performance such as cash ratio, required amount of reserve, loan to deposit ratio, loan

to asset ratio, net call liabilities ratio. The liquidity ratio analysis performed to analyse

the bank's ability to meet its short-term liabilities or matured liabilities.

14

2. Solvency Ratio

Dendawijaya (2005), elaborate solvency ratio is the bank's ability to fulfill its long-

term liability or the capability of banks to meet obligations in the event of bank

liquidation. In addition, it is used to specify the ratio between the extent (amount) of

funds received from various debts (short-term and long-term) as well as different

external resources by the number of investment in various kind of assets owned by the

bank. The ratios are capital adequacy ratio, debt to equity ratio, long term debt to assets

ratio.

3. Profitability Ratio

It is a tool to analyze or measure the level of business efficiency and profitability.

Further, it is used to measure bank soundness. Profitability ratios are usually sought

reciprocal relationship between posts contained in the income statement of banks with

accounts on bank balance sheets in order to obtain various indications. The analysis of

rentability ratio of a bank, among others are ROA, ROE, net profit margin, operational

cost ratio (Dendawijaya, 2005).

2.6 Previous Research

1. Sam (2012) conducted a research entitled "Analysis of effect of LDR, NPL and

ROA to the CAR of the Regional Development Bank in Indonesia period 2007

– 2011". It is mainly about the effect of non-performing loan, return on assets

and loan to deposit ratio toward capital adequacy ratio. Data used in this

research based on Bank Indonesia published report period 2007 to 2012. Data

used in this research was normally distributed. Empirical evidence shown loan

to deposit ratio, non-performing loan, Return on assets to have influence toward

capital adequacy ratio of regional development bank in Indonesia over period

2007 – 2011 at level of significance less than 5% and together LDR, NPL and

ROA to have influence toward CAR.

15

2. Mahamat (2012), conducted. a research entitled "Analysis of Influence of

BOPO, NPL, NIM and CAR on PT. Bank Negara Indonesia (persero) Tbk.

Period 2006-2013" . This research was conducted to assess the influence of

operating revenue to operating expense ratio (BOPO), non-performing loan, net

interest margin and capital adequacy ratio toward loan to deposit ratio. This

research based on PT. Bank Negara Indonesia Tbk. period 2006-2013 quarterly

report. The results indicate that operating revenue to operating expense have no

significant effect towards LDR in PT. Bank Negara Indonesia, Tbk. The

variable NPL, NIM and CAR significantly has positive effect on the LDR.

Predictive ability of three variables to EPS in this research of 90.3% while the

remaining 9.7% affected by other factors not included in the research model.

3. Karim, Chan & Hassan (2010), conducted a research entitled "Bank Efficiency

and Non-Performing Loans. Evidence from Malaysia and Singapore". The

intent of this study is to analyze the connection among NPL and bank efficiency

in Malaysia and Singapore. The author use stochastic cost frontier with

assumption of normal-gamma efficiency distribution model proposed. The

outcomes imply that there is no significant distinction in cost efficiency

between bank in Singapore and Malaysia even though banks in Singapore

shows higher average cost efficiency. Likewise, lower cost efficiency will

increase non-performing loans. The result support the terrible management

hypothesis proposed that bad management inside the banking institutions

results in bad loans quality and then escalates the level of non-appearing loans.

4. Bhatt & Sumangala (2012), conducted a research entitled "Impact of Earnings

Per Share on Market Value of an Equity Share : an Empirical Study in Indian

Capital Market". Equity valuation is a central question which the academicians

and researchers in the field of capital markets are looking to address through

different perspective. At the same time, the stock trading practitioner have been

working through different clues. The most important variable affecting market

value of equity share is earning. Usually when a successful company starts build

16

up reserve they also look for expanding its scale of operation to increase its

earnings. Once a company starts earning attractive sum, the equity share will

have more and more thus increase its earnings. Then the equity share will have

more demand resulting increase in market value of equity attractive sum, the

equity share will have more and more demand which will result in increase in

market value of the equity. This paper attempt to study the impact of EPS on

the market value of an equity share in the India.

5. Mayasari & Setiawan (2013), conducted a research entitled "Capital Ratios on

Regional Development Banks". PDN partially has positive significant influence

toward CAR, LDR, IPR, NPL, FBIR and NIM partially have positive but not

significant influence toward CAR. APB and IRR partially have negative

significant influence toward CAR, OER and ROA partially have negative

insignificant influence to CAR. Policies related to APB, based on research

results APB has a negative impact on CAR and that have the most impact. All

independent variables have significant influence simultaneously toward CAR.

6. Seetharaman & Raj (2013), conducted a research entitled "An Empirical Study

on the Impact of Earnings per Share on Stock Prices of Listed Bank in

Malaysia". An impact of an announcement of EPS on stock prices had been the

interest of stakeholder. It is since EPS is one of the investment tools to evaluate

a company’s performance either in the short or long term. EPS can be used to

measure the financial performance and company prospect. In this research

finding, it can be concluded that there is a very strong positive correlation

between public bank EPS and that there is a significant impact of earnings

announcement on public bank stock prices.

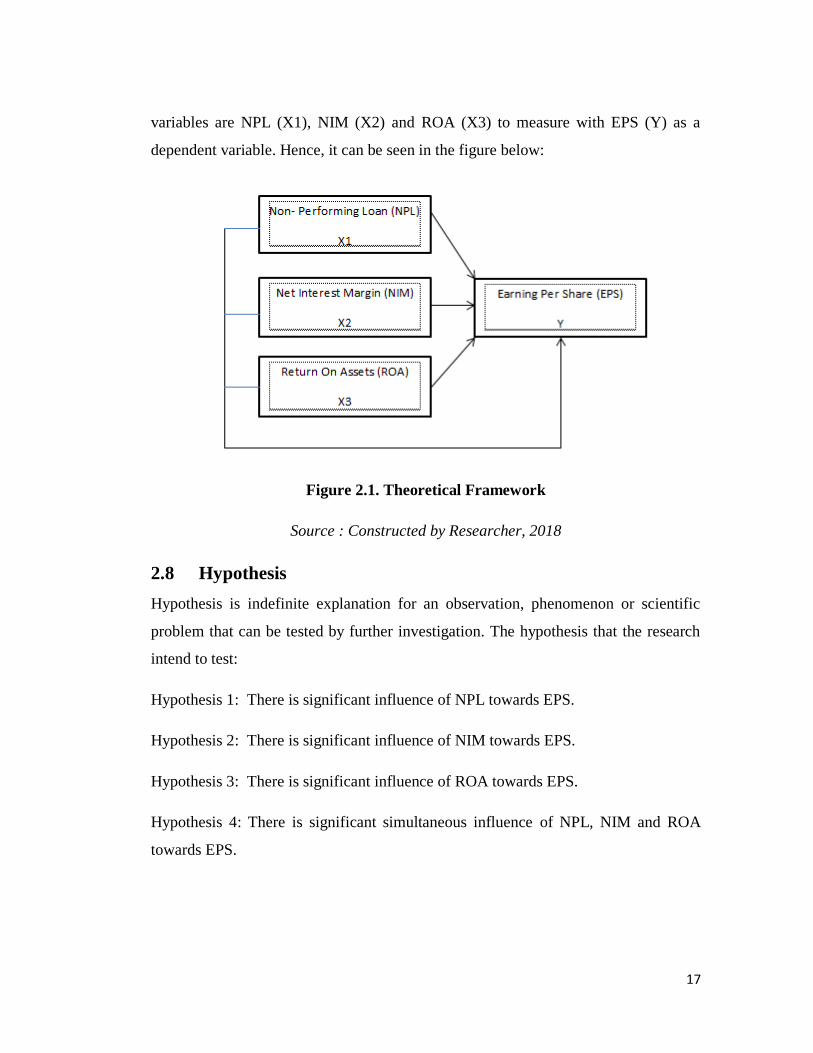

2.7 Theoretical Framework

Based on the model theoretical review above and previous study, so this research use

three independent variables to measure the dependent variable. The independent

17

variables are NPL (X1), NIM (X2) and ROA (X3) to measure with EPS (Y) as a

dependent variable. Hence, it can be seen in the figure below:

Figure 2.1. Theoretical Framework

Source : Constructed by Researcher, 2018

2.8 Hypothesis

Hypothesis is indefinite explanation for an observation, phenomenon or scientific

problem that can be tested by further investigation. The hypothesis that the research

intend to test:

Hypothesis 1: There is significant influence of NPL towards EPS.

Hypothesis 2: There is significant influence of NIM towards EPS.

Hypothesis 3: There is significant influence of ROA towards EPS.

Hypothesis 4: There is significant simultaneous influence of NPL, NIM and ROA

towards EPS.

18

CHAPTER III

METHODOLOGY

3.1. Research Design

According to Render (2006), in doing scientific research there are two methods, those

are qualitative and quantitative approach. The differences between qualitative and

quantitative are the type of data, research process, instrument in collecting data and the

purpose of research.

1. Qualitative method usually gathered observation, interviews, can be from

written evidence and case studies. It is more about attribute value.

2. Quantitative method entails only a few respondents, utilizes open-ended

questionnaires, great for answering how and why questions.

Quantitative observations are made using mathematical tools and measurements. The

results can be scrutinized and any other person trying to quantitatively examine the

same mode ought to turn up to be with the identical outcomes. In quantitative method

portions of data that can be counted mathematically, it also includes accrued via

surveys from huge numbers of respondents selected randomly and it is analysed using

statistical methods best used to answer what, when and who questions. The researcher

make use of quantitative method in undertaking this studies.

Render (2006), stated that the essence of quantitative analysis is the process of

manipulating raw data into significant information. Quantitative approach is

predetermined and use large number of respondent. Per se, analysis must be objective

and valid. The sample size for a survey is calculated using formulas to determine how

large a sample size might be needed from a given population to attain findings with an

acceptable degree of accuracy. Typically, researchers are trying to find sample sizes

19

which yield findings with at least a 95% confidence interval, margin error of 5 percent.

The surveys are designed to produce a smaller margin of error.

Therefore, in this study the writer uses the quantitative method with Factor Analysis

and Multiple Regressions Analysis to answer the research questions. Quantitative

method will be used because of the objective of this research is to appoint mathematical

models, theories and/or hypotheses relating phenomena. Mujis (2011), stated that in

the social sciences, quantitative research refers to give an explanation of phenomena

by collecting numerical data that are analysed using mathematically based methods

(especially statistics).

According to research objective in this research which is to explain effect of

independent variable (variable used to predict) to dependent variable (variable to be

predicted) which are the analysis of relationship among NPL, NIM & ROA toward

EPS.

Using quantitative research method, data can be easily converted into number and

analyzed through mathematical expression. Quantitative research shows the

relationship between independent variables and the dependent variable.

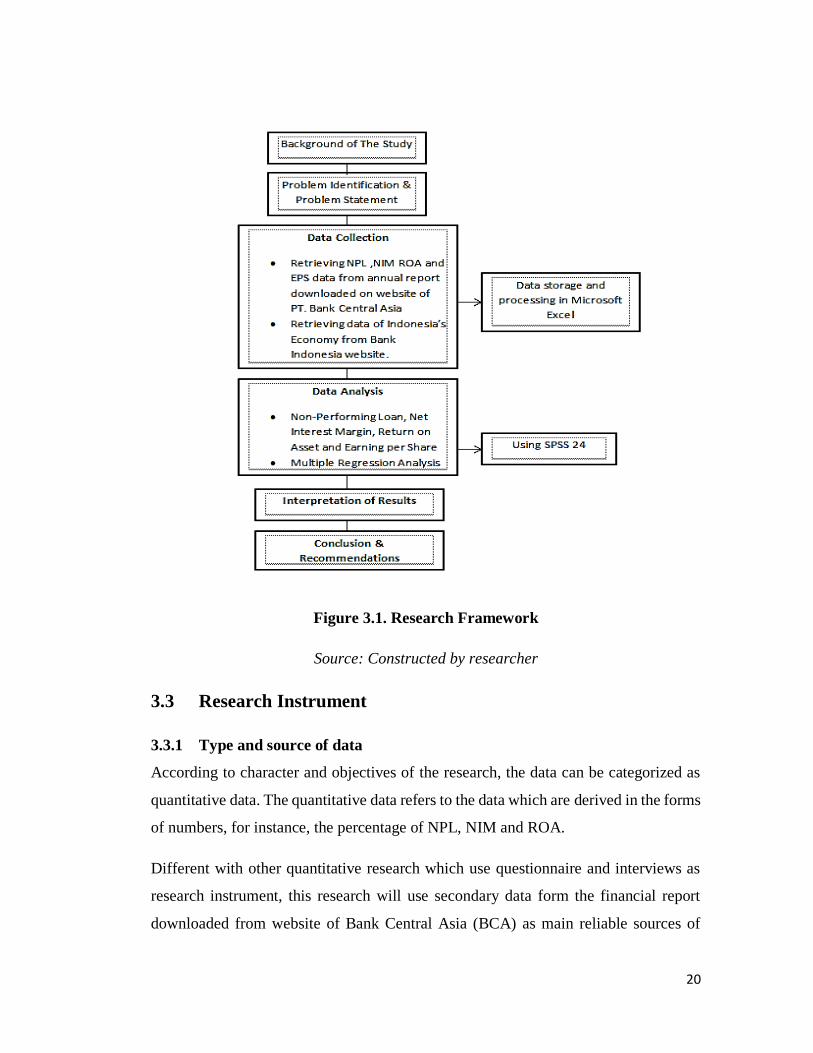

3.2. Research Framework

This research specifically investigates the influence of NPL, NIM and ROA toward

EPS on Bank Central Asia. Before conducting this research, the researcher had to find

out the information and overview about Bank Central Asia.

20

Figure 3.1. Research Framework

Source: Constructed by researcher

3.3 Research Instrument

3.3.1 Type and source of data

According to character and objectives of the research, the data can be categorized as

quantitative data. The quantitative data refers to the data which are derived in the forms

of numbers, for instance, the percentage of NPL, NIM and ROA.

Different with other quantitative research which use questionnaire and interviews as

research instrument, this research will use secondary data form the financial report

downloaded from website of Bank Central Asia (BCA) as main reliable sources of

21

information. According to the sources, the data that the researcher preferred to use is

secondary data. Secondary data is not originated by the investigator who doing this

research itself, but basically it obtains the source from someone else’s record. Such

data are cheaper and more quickly to obtain than the primary data and also may be

available when the primary data cannot be obtained at all (Render, Stair & Hanna,

2006).

According to (Malhotra & Peterson, 1996), secondary data is collected from some

purpose other than problem at hand”. Actually, secondary data is used for exploratory

study, but more formalised studies are typically structured which clearly stated

hypothesis or investigate questions which are known as descriptive studies.

3.3.2 Data Collection Method

Lind & Wathen (2010) states that collection of data should be systematic because if the

data is not systematic, it will be inhibit the writer to accomplish this research. The

writer used secondary data to do this research; the data was collected from several

reliable Indonesian institution source which is Bank of Indonesia.

Indonesia’s economic data from 2009-2013 taken from the official website of Bank

Indonesia which controls all of the banking system and operating system and operating

business in Indonesia. This website provided full information about overview of

Indonesia’s Economy every year.

NPL, NIM, ROA and EPS data from year 2007 - 2016 was taken from public non-

government bank official website which is PT. Bank Central Asia, Tbk.

3.3.3 Data Analysis Method

Because there are three (3) variables in this research that three of X (independent

variable) correlated to one Y (dependent variable). Multiple Regression will be used to

analyze the data. Regression analysis is a technique for modelling and analyzing

variables, when focus is on the relationship between a dependent variable and one or

more independent variables (Lind & Wathen, 2010). Moreover, multiple regression

22

analysis enables the researcher to understand how the value of the dependent variable

changes when any one of the independent variables is varied, while the other

independent variables are held fixed (Render, Stair & Hanna, 2006)

Multiple Regression is widely used for predicting and forecasting but also to

understand which among the independent variables are related to the dependent

variable, and to explore the forms of these relationships (Levine, Krehbiel and

Berenson, 2009). So, in order to find correlation between variables researched, the

author will use multiple regression method.

For the process of analyzing the data, the researcher will use SPSS 24 for statistic

purpose and Microsoft Excel software. It makes the calculation can be done easily by

this software. For making the report or book of this research, Microsoft Word was used

to make diagram and framework.

3.4. Sampling Design

Sampling Design is part of statistical methodology that related in taking a portion of

the population. If a sampling is done correctly, statistical analysis can be used to

generalize whole population (Sekaran, Bougie, 2010).

a. Population

Population includes each element from the set of observation. The population of

this research is largest public non-government owned by total assets. Banks in

Indonesia which is the population is also a sample used only for Bank Central Asia

(BCA) ,which is as main population.

b. Sample

Sample consists only observation drawn from the population. From this research

the sample is taking from the annual of time based on the financial statement of

Bank Central Asia (BCA). The sample that used come from the quarterly report of

financial statement released, with the period from 2007-2016.

23

3.5. Testing the Hypothesis and Data Analysis

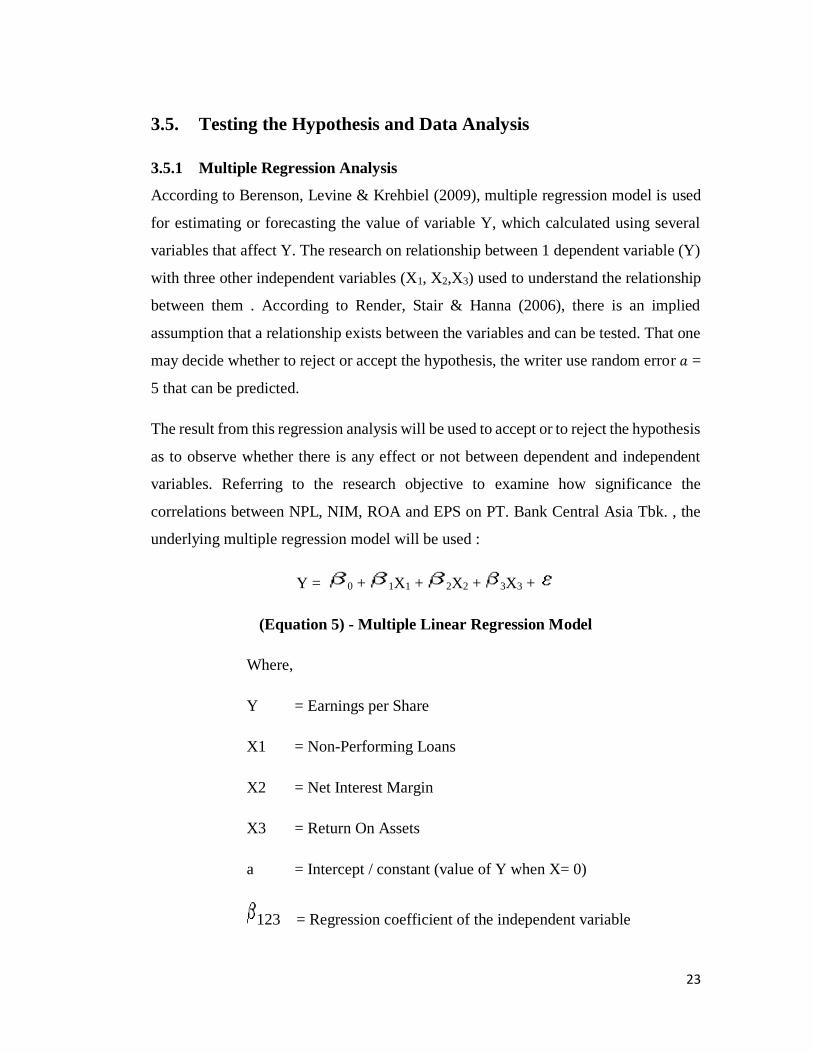

3.5.1 Multiple Regression Analysis

According to Berenson, Levine & Krehbiel (2009), multiple regression model is used

for estimating or forecasting the value of variable Y, which calculated using several

variables that affect Y. The research on relationship between 1 dependent variable (Y)

with three other independent variables (X1, X2,X3) used to understand the relationship

between them . According to Render, Stair & Hanna (2006), there is an implied

assumption that a relationship exists between the variables and can be tested. That one

may decide whether to reject or accept the hypothesis, the writer use random error 𝑎 =

5 that can be predicted.

The result from this regression analysis will be used to accept or to reject the hypothesis

as to observe whether there is any effect or not between dependent and independent

variables. Referring to the research objective to examine how significance the

correlations between NPL, NIM, ROA and EPS on PT. Bank Central Asia Tbk. , the

underlying multiple regression model will be used :

Y = 0 + 1X1 + 2X2 + 3X3 +

(Equation 5) - Multiple Linear Regression Model

Where,

Y = Earnings per Share

X1 = Non-Performing Loans

X2 = Net Interest Margin

X3 = Return On Assets

a = Intercept / constant (value of Y when X= 0)

123 = Regression coefficient of the independent variable

24

= Random Error

However, in order to finish the regression model to see the correlation between the

variables, there are some tests including measuring the regression model to test the

validity of the data which are normality test & classic assumption tests.

3.5.2 Classical Assumption Test

The estimation method used in this research is the Ordinary Least Square (OLS)

method. Least Square method determines a regression equation by minimizing the sum

of the squares of the vertical distance between the actual Y values and the predicted

values of Y (Lind & Wathen, 2010). This method is chosen because it is the most

powerful and popular methods of regression analysis. Moreover, it is also simpler

mathematically. The use of this mathematic has to meet several assumptions to make

sure that the data collected are valid and reliable distribution (Levine, Krehbiel and

Berenson, 2009).

1. Normality Test

It's far assumed in a multiple of regression that residuals (predicted minus observed

values) are distributed normally. This test can be achieved with the aid of producing

histograms for the residual as well as normal probability plots, if you want to look into

the distribution of the residual values (Render, Stair & Hanna, 2006).

The normality test also can be done by using SPSS statistical software and can be

viewed in the graph of normal probability plot that is a graphical device to study the

shape of the probability density function. Normal probability plot is used to assess how

well empirical data approximates a particular theoretical (Levine, Krehbiel and

Berenson, 2009). In this case a linear relationship distribution; the data can also be

plotted on the probability scale by plotting the cumulative probabilities of the data

under the assumed distribution against their expected probabilities.

25

2. Multicollinearity Test

Multicollinearity is the correlation among the independent variables which makes it

difficult to make conclusion about the individual regression coefficients and their

individual effects on the dependents variables. Another reason for avoiding correlated

independent variable is they may lead to false results in the hypothesis test for the

individual independent variables. In practice, it is nearly impossible to select the

independent variables that are completely unrelated or not correlated in some degree

(Lind & Wathen, 2010). Multicollinearity problems arise if there is perfect relationship

or certainly among the few independent variables or all variables in the model. In cases

of serious multicollinearity, regression coefficients are no longer showing pure effect

on independent variables in the model. Multicollinearity does not affect the multiple

regression equation’s ability to predict the dependent variable. However, it might show

unexpected results on the relationship between each independent variables and the

dependent variable (Levine , Krehbiel and Berenson, 2009)

If Multicollinearity shows in a multiple regression model, the model is still good for

prediction, but the interpretation of individual coefficient is not valid. There are many

methods to detect the presence of multicollinearity, in this research the writer would

like to do a test on the variables with the measurement of the Variance Inflation Factor

(VIF) (Lind & Wathen, 2010).

𝑉𝐼𝐹𝑘 =1

1 − 𝑅𝑘2

(Equation 6) Variance Inflation Factor model

The term 𝑅𝑘2 refers to the coefficient of determination, where the selected independent

variable Is used as a dependent variable and the remaining independent variables are

used as independent variables. A VIF greater than 10 is considered unsatisfactory,

indicating that the independent variable should be removed from the analysis. When

VIF is under 10 , it means that there is no multicollinearity problem aroused (Lind &

Wathen, 2010)

26

3. Autocorrelation Test (The Durbin - Watson statistic)

Autocorrelation is the correlation (relationship) between members of a time series of

observations (as in time series data) or space (as in cross sectional data). Since the basic

assumption of the regression model is the independence of errors, a good regression

model is one that has no correlation problem. If autocorrelation happens in the

regression model, the sample will not show variance of the population (Lind & Wathen,

2010).

Although estimates are still linear and unbiased there are no longer best of efficient.

The standard errors become so wide that confidence interval will be larger. As a

consequence, the result of regression model t-test and F-test may give inaccurate result

which cannot be used to predict the value of dependent variable toward particular

independent variable (Levine, Krehbiel and. Berenson,2009).

In this research, because the data collected are quarterly data from 2007 - 2016 on PT.

Bank Central Asia Tbk. financial statement, it is necessary for the researcher to

determine whether the autocorrelation is present in order to decide the validity of the

data collected. To detect whether there is autocorrelation, the writer would like to use

Durbin-Watson D-Test.

(Equation 7) Durbin - Watson D-test Formula

Where: 𝑒i = residual at the time period I.

27

According to Keller (2009), in order to test the positive autocorrelation at significance

𝑎, sample n and k number of independent variables, the test statistic d is compared to

lower and upper critical values (dL,a and d𝑈, 𝑎) :

a. If (4 - d) < d𝐿, 𝑎 there is statistical evidence that the error terms are negatively

autocorrelated.

b. If (4-d) > d𝑈, 𝑎 there is statistical evidence that the error terms are not negatively

correlated.

c. If d𝐿, 𝑎 < (4- d) < d𝑈, 𝑎 : the test is inconclusive.

A good regression model should have no presence of autocorrelation to validate the

result of t-test and F-test to predict the value of dependent variable toward particular

independent variable (Keller, 2009).

4. Heteroscedasticity Test

Heteroscedasticity occurs when the variance of errors is constant. When the dispersion

of term's probability distribution is not constant, heteroscedasticity likely exists.

Heteroscedasticity often arises in the analysis of cross sectional data and time series

data (Lind & Wathen, 2010).

If heteroscedasticity exist in the regression model, the variance and standard error will

tend to increase as the t value will not get lower than the actual t value. The

consequences are the t- test and F-test will be inaccurate and fail to reject the null

hypotheses (Levine, Krehbiel and Berenson, 2009).

A simple test for heteroscedasticity is to plot the standardized residuals (on vertical

axis) against the dependent variable (horizontal axis). If no heteroscedasticity occurs,

the plot will appear to spread randomly. If a systematic pattern (wave, straight, narrow,

widen) appears in the scatter plot then heteroscedasticity exists (Levine, Krehbiel and

Berenson, 2009).

28

3.5.3 Measuring the Variability of the Regression Model

A regression equation can be developed for any variables X and Y, even random

numbers. There are two ways to know that the model is actually helpful in predicting

Y based on X :

a. Coefficient of Determination (𝑹𝟐)

In multiple regression model, the coefficient of multiple determination (𝑟2) represents

the proportion of variant in Y that can be defined by the independent variables X1 and

X2 in the multiple regression equation. The coefficient of determination is a summary

measure that tells how well the sample regression line fits the data (Levine, Krehbiel

and Berenson, 2009). Statistically, it measures how many percentage variation of Y

variable explained by the repressors jointly. The 𝑟2 value can range from a low of 0 to

a high 1 0 ≤ 𝑟2 ≤ 1).

𝑟2 = SSR

SST

(Equation 8) Coefficient of Multiple Determination

Where : SSR= Regression Sum of Squares

SST = Total Sum of Squares

a. If 𝑟2 = 0 , indicating that X explains 0% of the variability in Y

b. If 𝑟2 = 1, indicating that every point in the sample were on the regression line

(meaning all errors are 0). In other words, 100% of the variability in Y could be

explained by the regression equation. In developing regression equation, a good

model will have and 𝑅2 value close to 1.

2. Coefficient of Correlation (R)

Coefficient of Correlation measures the extent of association between Y and X

variables (Levine, Krehbiel and Berenson, 2009). In other words, it expresses the level

29

of strength of the linear relationship. The coefficient of correlation can be computed

directly from the coefficients of determination as follows:

r = ±√𝑟2

Or from the sample data:

(Equation 9) Formula of Coefficient of Correlation

The result of r can be stated at any number between +1 and -1. The value of r is the

square root of 𝑟2. It is negative if the slope is negative and it is positive if the slope is

positive.

3.5.4 Testing the Hypothesis

1. Testing the Model for Significance

A statistical test (F- test and T-test) is performed to determine if there is a linear

relationship between X and Y. The null hypothesis is that there is no linear relationship

between the two variables (i.e. β = 0) and the alternate hypothesis is that there is a linear

relationship (i.e. β ≠ 0) .If the null hypothesis rejected, we have proven that a linear

relationship does exist.

a. F-test

The F-test determines whether or not there is a relationship between set of independent

variables & dependent variable simultaneously. And F-test is used to test statistically

the null hypothesis that there is no linear relationship between the X and Y variables

(i.e.β=0). Lind & Wathen states that If the significance level for the F-test is low

30

(significance level α used is 0.05), we reject H0 and conclude there is a linear

relationship and vice versa.

H0:β1 = β2 = β3 = 0, if significant F>0.05, accept H0

Ha: at least there is one β ≠ 0, if significant F < 0.05, reject H0

(Equation 10) Formula of F-test

Where:

F = Statistic test for F distribution

𝑅2 = coefficient of determination

k = Number of independent variables in the model

n = Number of sample period

b. T-Test

The T - Test is applied to determine the partial relationship between each independent

variable (coefficient) and the dependent variable. The null hypothesis is that the

coefficient of X (i.e. the slope of the line) is 0. Lind & Wathen states that If the

significance level for the T - Test is low (significance level 𝑎 used is 0.05), we reject

H0 and conclude there is a linear relationship and vice versa.

H0 : X = 0 ,if Significant T > 0.05, accept H0

Ha: X ≠ 0 , if Significant T < 0.05, reject H0

31

We use correlation coefficient (r) to measure the strength of the relationship between

two numerical variables, the test for the existence of correlation is using t-test.

(Equation 11) Formula of T-test

x̄ = sample mean

μ0 = population mean

s = sample standard deviation

n = sample size

2. Testing the Partial Correlation

Correlation test is conducted to find out the correlation between one independent

variable partially to the dependent variable. The result can be shown in the Pearson

correlation table. The positive sign gives information on the increase of the values of

one variable relative to the increase value of another variable and vice versa (Levine,

Krehbiel and Berenson, 2009).

32

CHAPTER IV

ANALYSIS AND INTERPRETATION

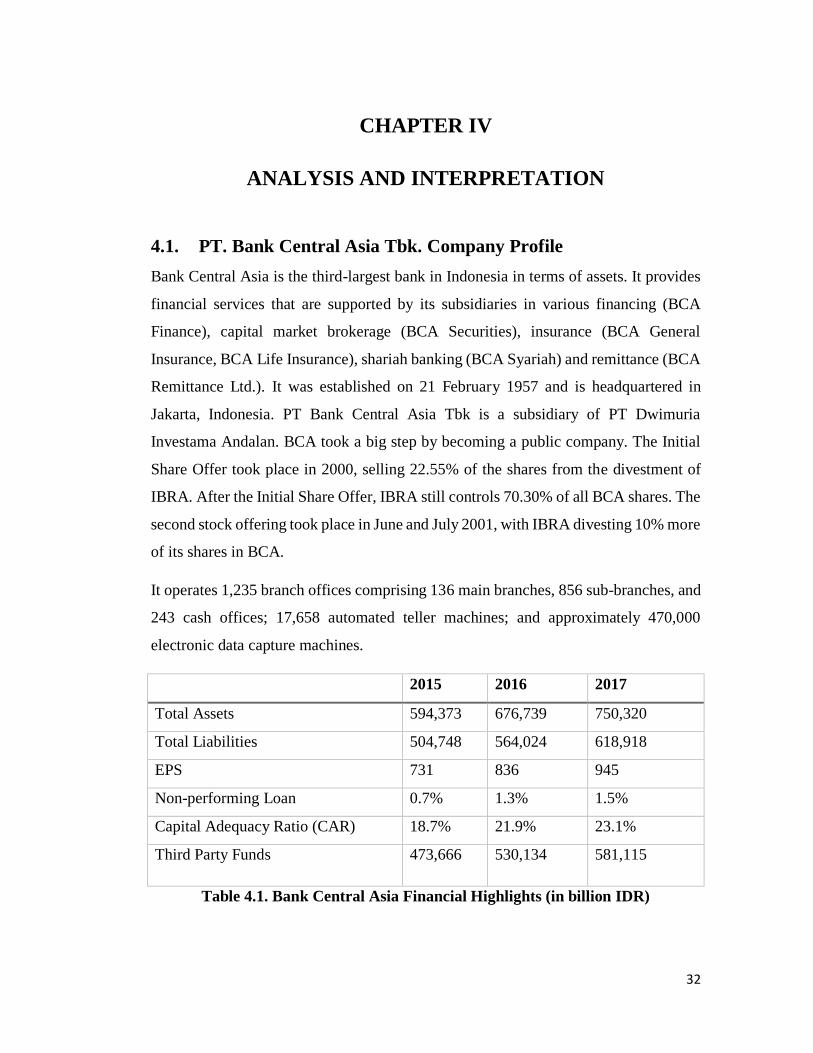

4.1. PT. Bank Central Asia Tbk. Company Profile

Bank Central Asia is the third-largest bank in Indonesia in terms of assets. It provides

financial services that are supported by its subsidiaries in various financing (BCA

Finance), capital market brokerage (BCA Securities), insurance (BCA General

Insurance, BCA Life Insurance), shariah banking (BCA Syariah) and remittance (BCA

Remittance Ltd.). It was established on 21 February 1957 and is headquartered in

Jakarta, Indonesia. PT Bank Central Asia Tbk is a subsidiary of PT Dwimuria

Investama Andalan. BCA took a big step by becoming a public company. The Initial

Share Offer took place in 2000, selling 22.55% of the shares from the divestment of

IBRA. After the Initial Share Offer, IBRA still controls 70.30% of all BCA shares. The

second stock offering took place in June and July 2001, with IBRA divesting 10% more

of its shares in BCA.

It operates 1,235 branch offices comprising 136 main branches, 856 sub-branches, and

243 cash offices; 17,658 automated teller machines; and approximately 470,000

electronic data capture machines.

2015 2016 2017

Total Assets 594,373 676,739 750,320

Total Liabilities 504,748 564,024 618,918

EPS 731 836 945

Non-performing Loan 0.7% 1.3% 1.5%

Capital Adequacy Ratio (CAR) 18.7% 21.9% 23.1%

Third Party Funds 473,666 530,134 581,115

Table 4.1. Bank Central Asia Financial Highlights (in billion IDR)

33

Source: Annual Report of Bank Central Asia, 2017

4.2. Data Analysis

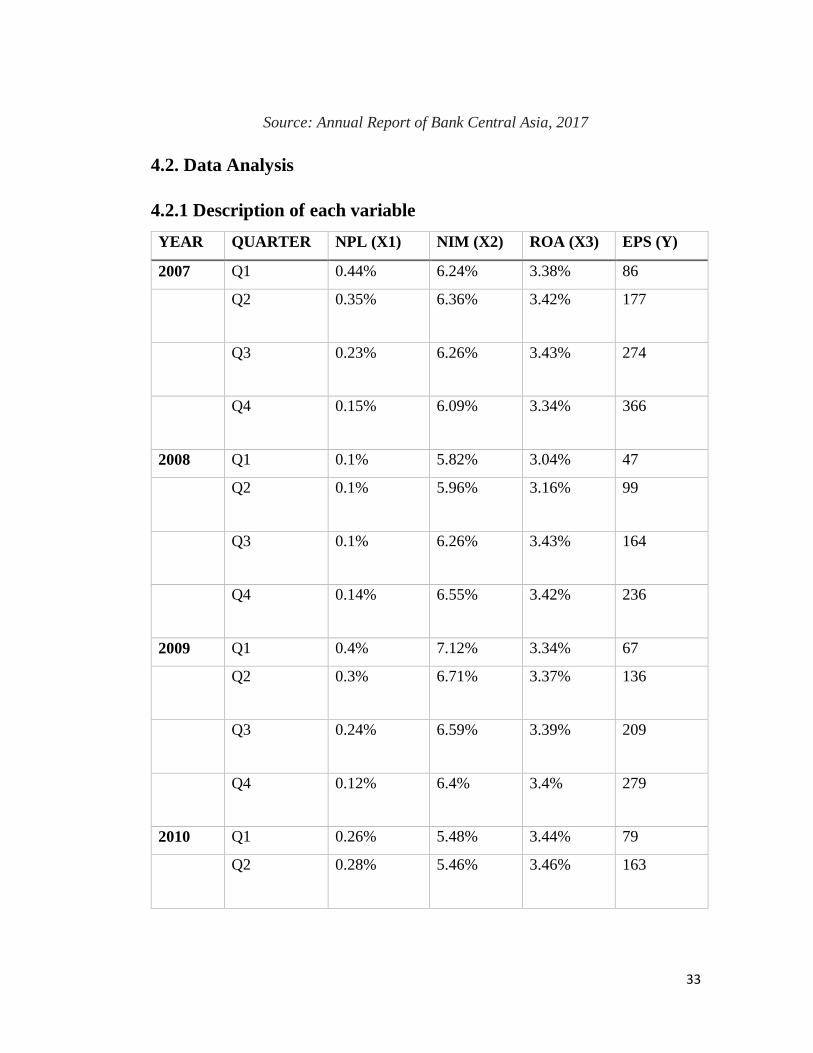

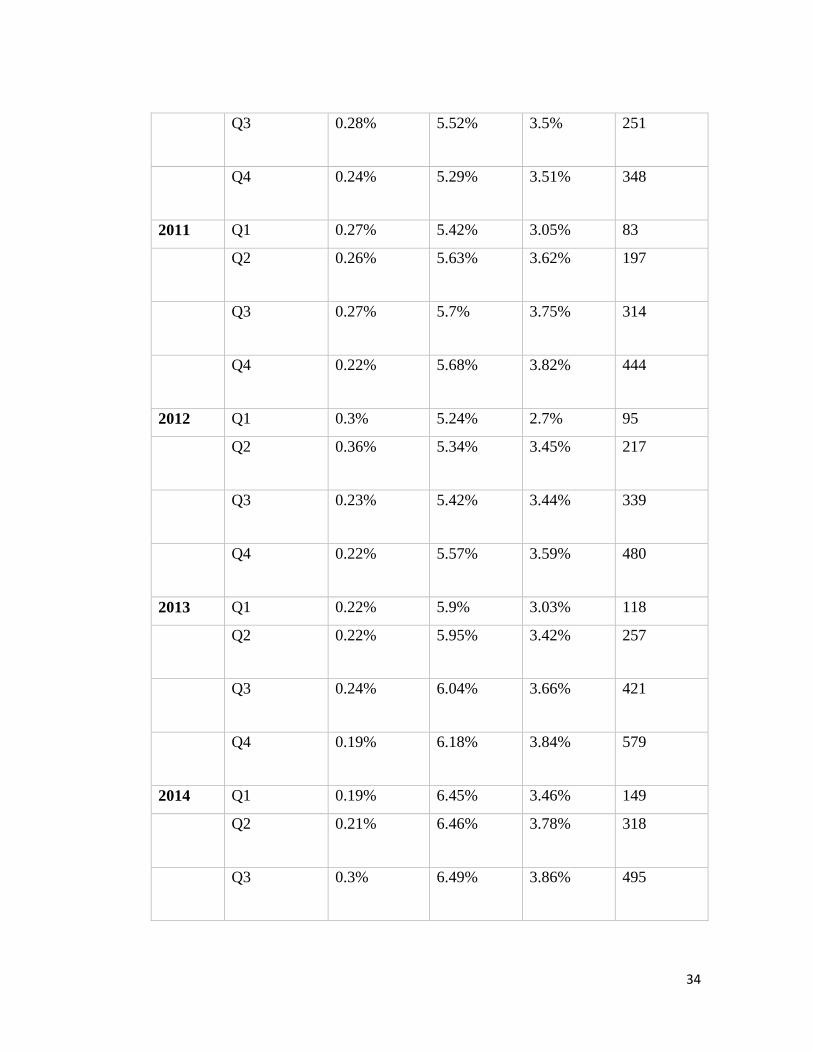

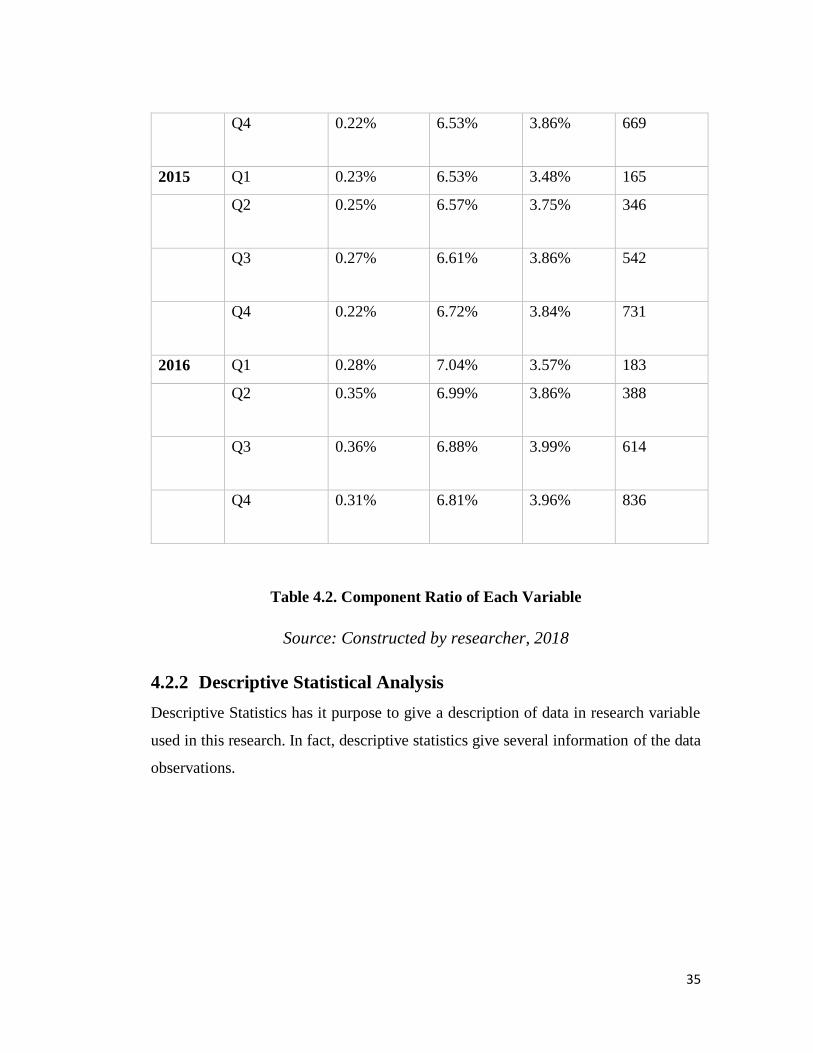

4.2.1 Description of each variable

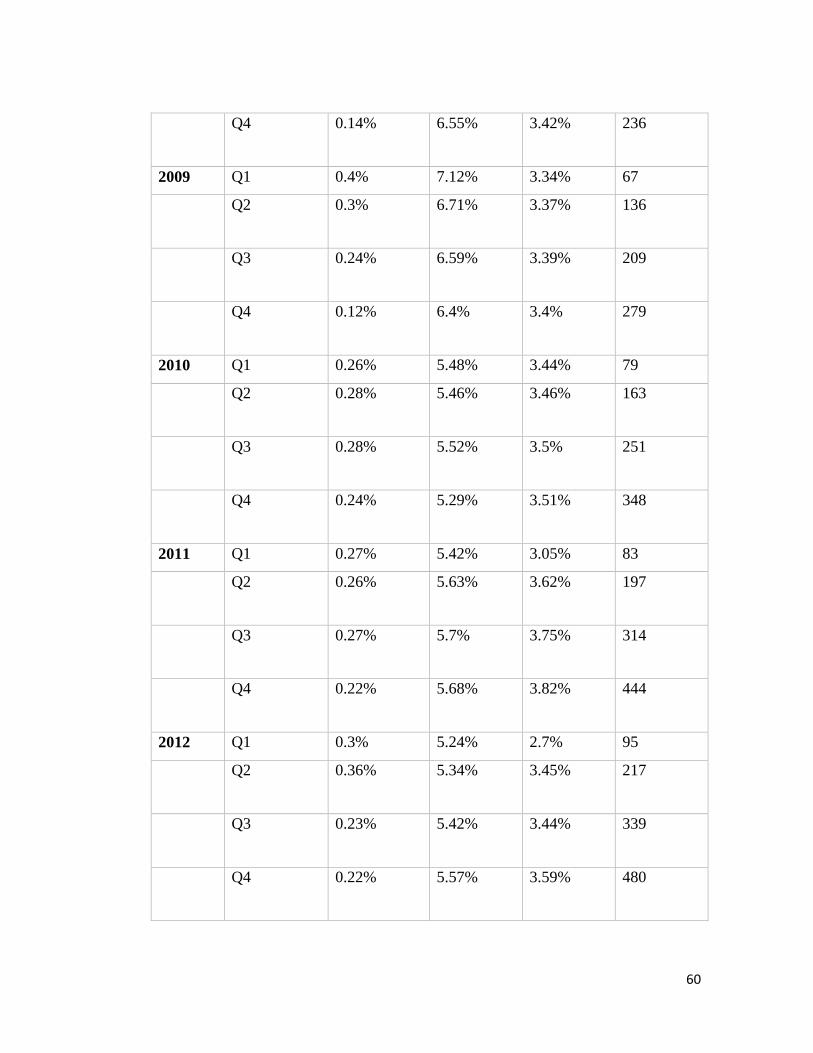

YEAR QUARTER NPL (X1) NIM (X2) ROA (X3) EPS (Y)

2007 Q1 0.44% 6.24% 3.38% 86

Q2 0.35% 6.36% 3.42% 177

Q3 0.23% 6.26% 3.43% 274

Q4 0.15% 6.09% 3.34% 366

2008 Q1 0.1% 5.82% 3.04% 47

Q2 0.1% 5.96% 3.16% 99

Q3 0.1% 6.26% 3.43% 164

Q4 0.14% 6.55% 3.42% 236

2009 Q1 0.4% 7.12% 3.34% 67

Q2 0.3% 6.71% 3.37% 136

Q3 0.24% 6.59% 3.39% 209

Q4 0.12% 6.4% 3.4% 279

2010 Q1 0.26% 5.48% 3.44% 79

Q2 0.28% 5.46% 3.46% 163

34

Q3 0.28% 5.52% 3.5% 251

Q4 0.24% 5.29% 3.51% 348

2011 Q1 0.27% 5.42% 3.05% 83

Q2 0.26% 5.63% 3.62% 197

Q3 0.27% 5.7% 3.75% 314

Q4 0.22% 5.68% 3.82% 444

2012 Q1 0.3% 5.24% 2.7% 95

Q2 0.36% 5.34% 3.45% 217

Q3 0.23% 5.42% 3.44% 339

Q4 0.22% 5.57% 3.59% 480

2013 Q1 0.22% 5.9% 3.03% 118

Q2 0.22% 5.95% 3.42% 257

Q3 0.24% 6.04% 3.66% 421

Q4 0.19% 6.18% 3.84% 579

2014 Q1 0.19% 6.45% 3.46% 149

Q2 0.21% 6.46% 3.78% 318

Q3 0.3% 6.49% 3.86% 495

35

Q4 0.22% 6.53% 3.86% 669

2015 Q1 0.23% 6.53% 3.48% 165

Q2 0.25% 6.57% 3.75% 346

Q3 0.27% 6.61% 3.86% 542

Q4 0.22% 6.72% 3.84% 731

2016 Q1 0.28% 7.04% 3.57% 183

Q2 0.35% 6.99% 3.86% 388

Q3 0.36% 6.88% 3.99% 614

Q4 0.31% 6.81% 3.96% 836

Table 4.2. Component Ratio of Each Variable

Source: Constructed by researcher, 2018

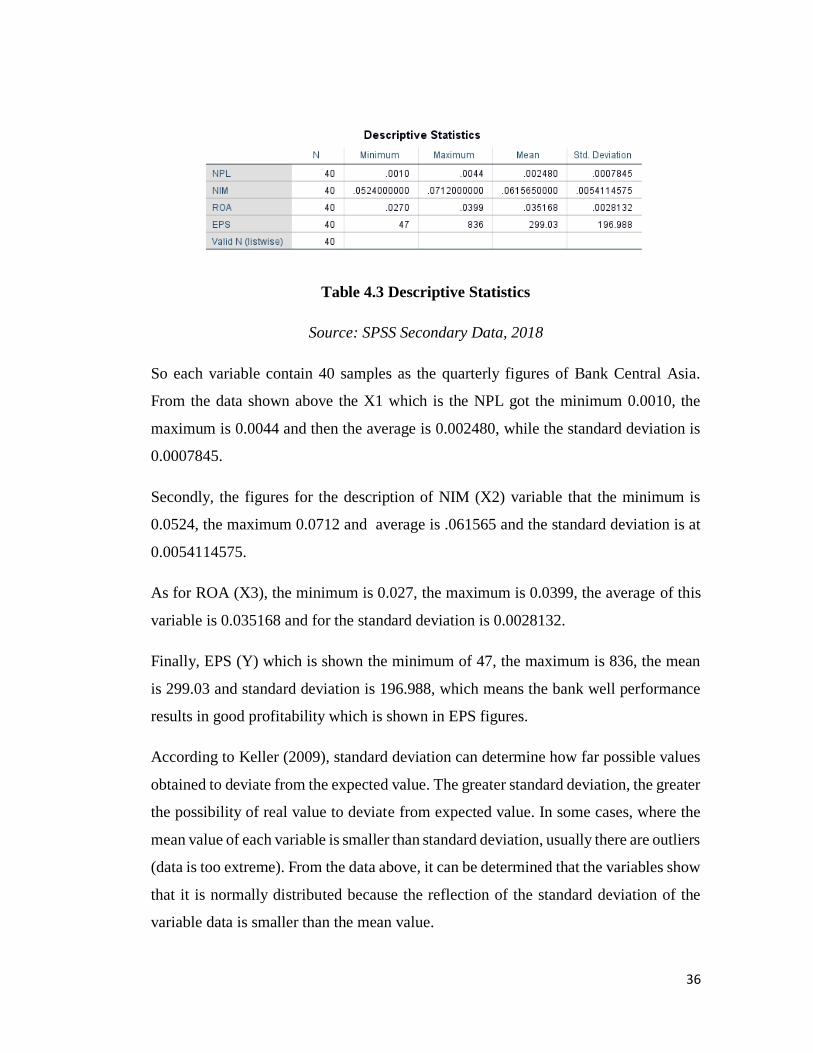

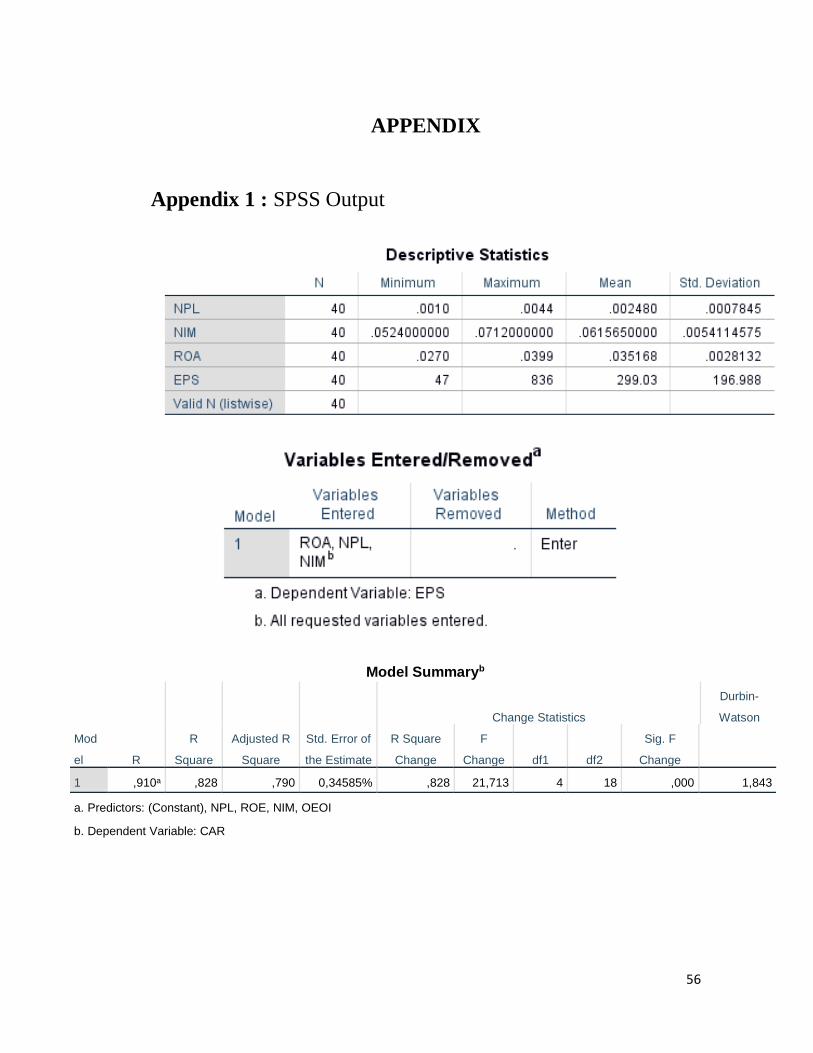

4.2.2 Descriptive Statistical Analysis

Descriptive Statistics has it purpose to give a description of data in research variable

used in this research. In fact, descriptive statistics give several information of the data

observations.

36

Table 4.3 Descriptive Statistics

Source: SPSS Secondary Data, 2018

So each variable contain 40 samples as the quarterly figures of Bank Central Asia.

From the data shown above the X1 which is the NPL got the minimum 0.0010, the

maximum is 0.0044 and then the average is 0.002480, while the standard deviation is

0.0007845.

Secondly, the figures for the description of NIM (X2) variable that the minimum is

0.0524, the maximum 0.0712 and average is .061565 and the standard deviation is at

0.0054114575.

As for ROA (X3), the minimum is 0.027, the maximum is 0.0399, the average of this

variable is 0.035168 and for the standard deviation is 0.0028132.

Finally, EPS (Y) which is shown the minimum of 47, the maximum is 836, the mean

is 299.03 and standard deviation is 196.988, which means the bank well performance

results in good profitability which is shown in EPS figures.

According to Keller (2009), standard deviation can determine how far possible values

obtained to deviate from the expected value. The greater standard deviation, the greater

the possibility of real value to deviate from expected value. In some cases, where the

mean value of each variable is smaller than standard deviation, usually there are outliers

(data is too extreme). From the data above, it can be determined that the variables show

that it is normally distributed because the reflection of the standard deviation of the

variable data is smaller than the mean value.

37

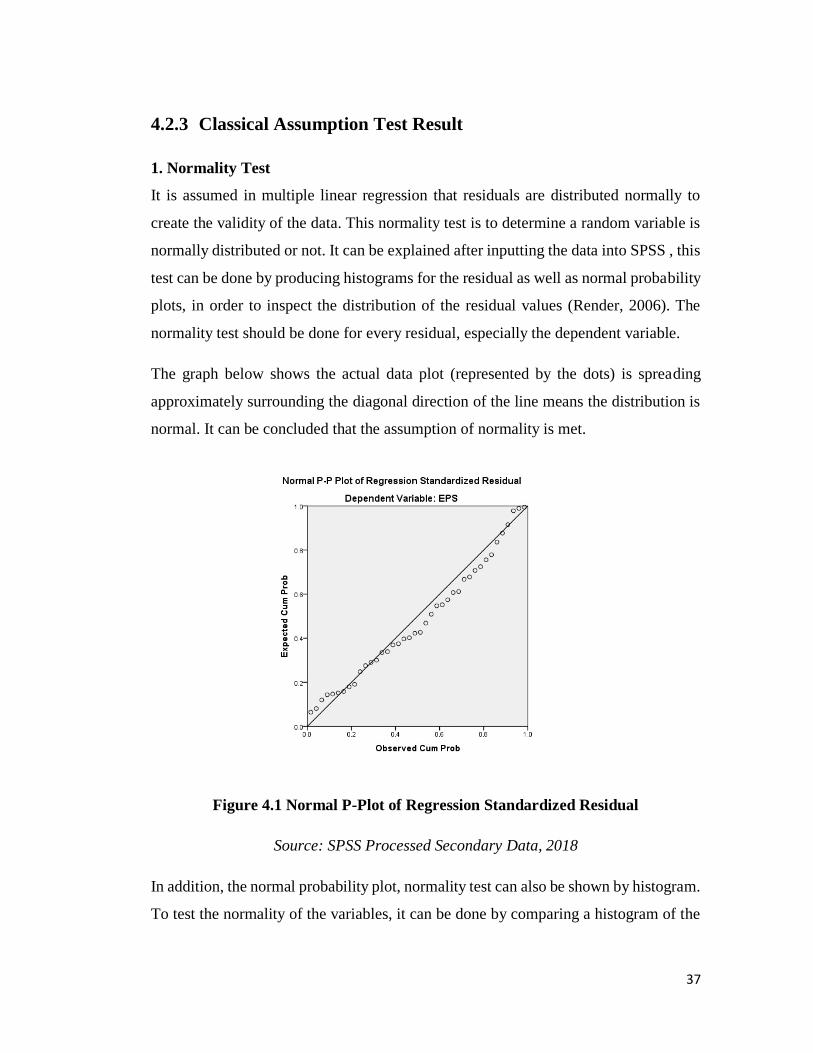

4.2.3 Classical Assumption Test Result

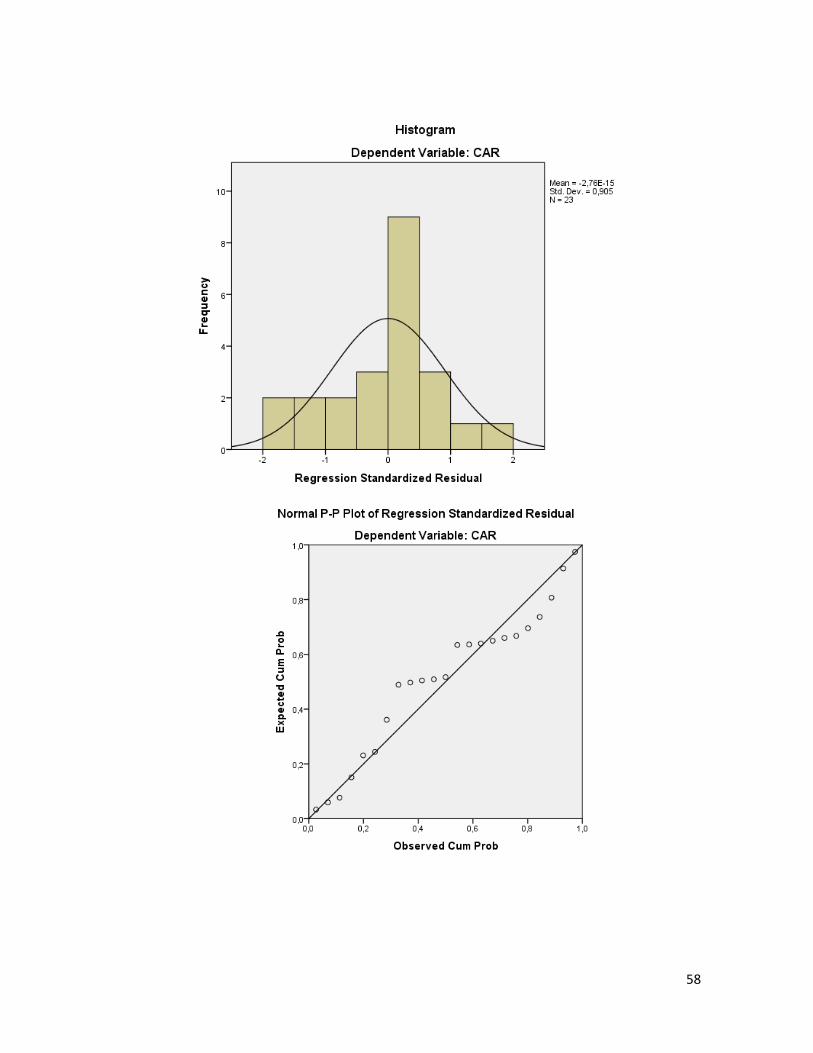

1. Normality Test

It is assumed in multiple linear regression that residuals are distributed normally to

create the validity of the data. This normality test is to determine a random variable is

normally distributed or not. It can be explained after inputting the data into SPSS , this

test can be done by producing histograms for the residual as well as normal probability

plots, in order to inspect the distribution of the residual values (Render, 2006). The

normality test should be done for every residual, especially the dependent variable.

The graph below shows the actual data plot (represented by the dots) is spreading

approximately surrounding the diagonal direction of the line means the distribution is

normal. It can be concluded that the assumption of normality is met.

Figure 4.1 Normal P-Plot of Regression Standardized Residual

Source: SPSS Processed Secondary Data, 2018

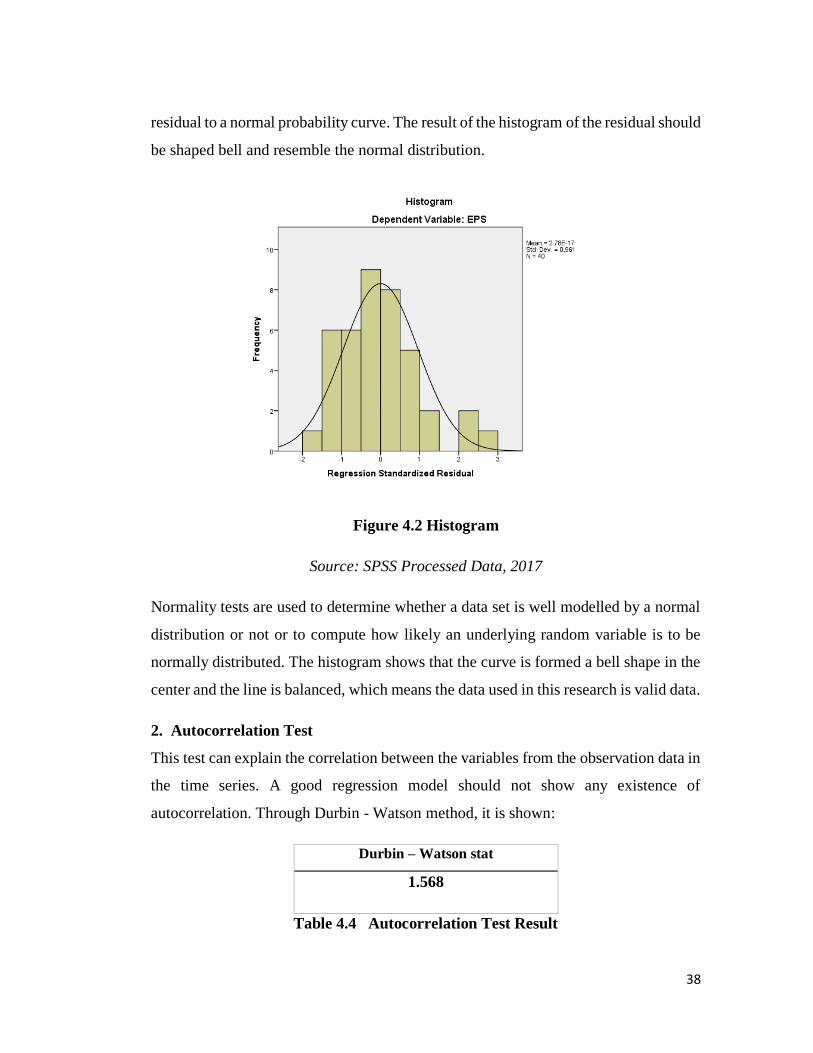

In addition, the normal probability plot, normality test can also be shown by histogram.

To test the normality of the variables, it can be done by comparing a histogram of the

38

residual to a normal probability curve. The result of the histogram of the residual should

be shaped bell and resemble the normal distribution.

Figure 4.2 Histogram

Source: SPSS Processed Data, 2017

Normality tests are used to determine whether a data set is well modelled by a normal

distribution or not or to compute how likely an underlying random variable is to be

normally distributed. The histogram shows that the curve is formed a bell shape in the

center and the line is balanced, which means the data used in this research is valid data.

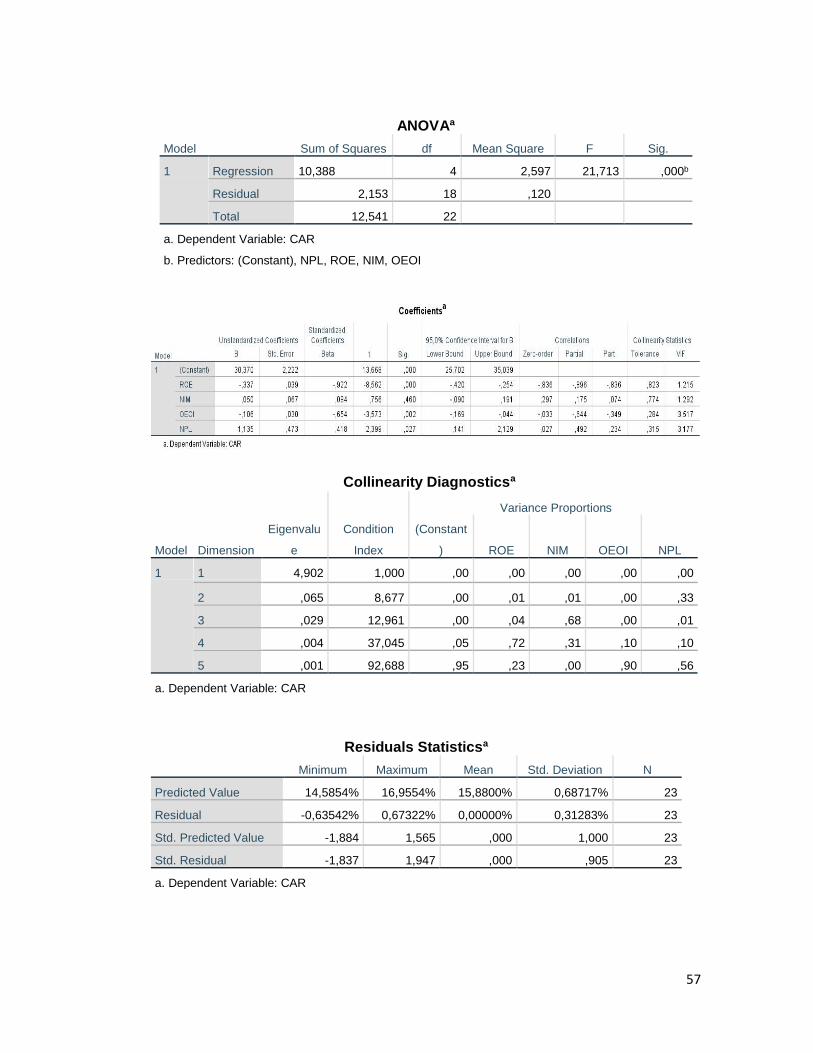

2. Autocorrelation Test

This test can explain the correlation between the variables from the observation data in

the time series. A good regression model should not show any existence of

autocorrelation. Through Durbin - Watson method, it is shown:

Durbin – Watson stat

1.568

Table 4.4 Autocorrelation Test Result

39

Source: SPSS Processed Data,2017

The value of Durbin - Watson in this model is 1.568. Which is the test is acceptable

and free from autocorrelation problem.

3. Multicollinearity Test

The multicollinearity in the regression model can be assumed if there is a perfect linear

relationship between a few or all of the independent variables in the model. One method

of measuring multicollinearity is the Variance Inflation Factor (VIF) for each

independent variable. According to Barry Render , Ralph Stair and Michael Hanna

(2006), a variable has high collinearity (multicollinearity) if it has VIF value more than

10 or it has tolerance tend to approach 0. A good regression model should not have

correlation between independent variables. Similarly, multicollinearity test aims to

determine whether there is perfect relationship or very high among the independent

variables in the regression model.

The multicollinearity test was conducted by SPSS software:

Table 4.5 Multicollinearity Test Result

Source: SPSS Processed Secondary Data, 2018

Good regression model should not happen correlation between the independent

variable. Multicollinearity problem will happen if the level of VIF more than 10 or if

the tolerance value less than 0.1. From the table above all the independent variables got

40

tolerance value above 0.1 and VIF is far below 10, so the result there is no

multicollinearity problem.

3. Heteroscedasticity Test

Heteroscedasticity test of the regression model is to measure that whether the

disturbance variance is constant, or homogenous, across observation. The result of the

test can be seen by looking at the distribution of residual values toward the predicted

values in the scatterplot. If the distribution spread randomly and does not make any

systematic such as increasing or decreasing pattern, then the heteroscedasticity

assumption is fulfilled.

Figure 4.2. Scatterplot

Source: SPSS Processed Secondary Data, 2018

From the scatterplot graph above, it can be concluded that this is heteroscedasticity in

nature because the plots are spreading throughout the figures are very clear. However,

the graph also shows a random dispersion around zero. It means that the T-test and F-

41

test are accurate and valid, and this regression model is eligible to predict the EPS based

on the independent variables.

4.2.3 Multiple Regression Analysis

In the multiple regression this research test the hypothesis by using the T-test, F-Test

and R Square. All the variables using in this regression model such as NPL, NIM &

ROA as the independent variable and for the dependent variable EPS.

Table 4.6 Coefficients

Source: SPSS Processed Secondary Data, 2018

Based on table above the multiple regression equation becomes as follow:

EPS = -1583.999 - 305.621NPL - 18.715NIM + 589.760ROA + e

From the data above the multiple regression can be explained:

1. Coefficient Variable NPL= -305.621 means that in every 1 unit increase of NPL

will cause the decrease of EPS by 305.621, with the assumption that

independent variables are constant.

2. Coefficient variable NIM = -18.715 means that in every 1 unit increase of NIM

will cause the decrease of EPS by 18.715, with assumption that independent

variables are constant.

3. Coefficient variable ROA = 589.760 means that in every 1 unit increase of ROA

will cause the increase of EPS bt 589.760, with assumption that independent

variables are constant.

42

From the explanation of multiple regression above, then researcher will be testing

the hypothesis both partially and simultaneously.

4.2.4 Goodness or Fit Test

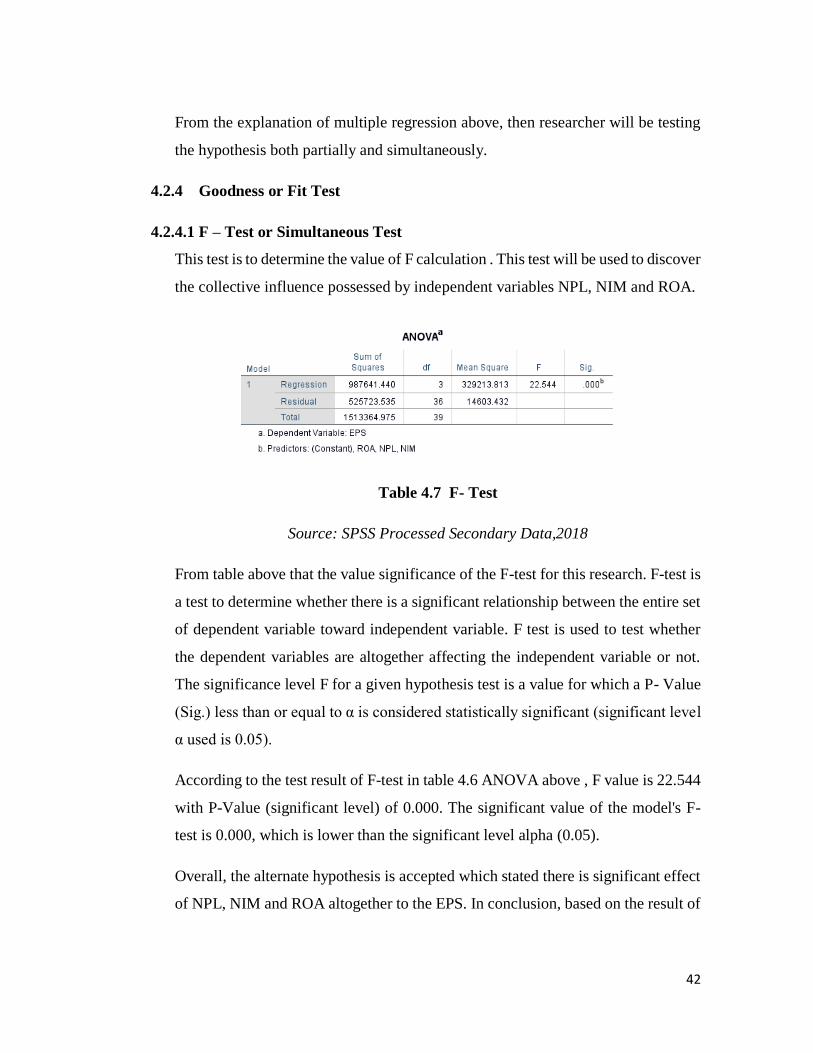

4.2.4.1 F – Test or Simultaneous Test

This test is to determine the value of F calculation . This test will be used to discover

the collective influence possessed by independent variables NPL, NIM and ROA.

Table 4.7 F- Test

Source: SPSS Processed Secondary Data,2018

From table above that the value significance of the F-test for this research. F-test is

a test to determine whether there is a significant relationship between the entire set

of dependent variable toward independent variable. F test is used to test whether

the dependent variables are altogether affecting the independent variable or not.

The significance level F for a given hypothesis test is a value for which a P- Value

(Sig.) less than or equal to α is considered statistically significant (significant level

α used is 0.05).

According to the test result of F-test in table 4.6 ANOVA above , F value is 22.544

with P-Value (significant level) of 0.000. The significant value of the model's F-

test is 0.000, which is lower than the significant level alpha (0.05).

Overall, the alternate hypothesis is accepted which stated there is significant effect

of NPL, NIM and ROA altogether to the EPS. In conclusion, based on the result of

43

F-test, it can be stated there is altogether effect of NPL,NIM and ROA to the EPS

of PT. Bank Central Asia Tbk (BCA) during 10 years from 2007 to 2016.

4.2.4.2 T - test

Based on the table 4.5 Coefficients above can be explained that the partial test or T

–test is used to measure the influence of each independent variable toward the

dependent variable. If the level of signifcance is 0.05, the Ha will be accepted. And

if the level of significance more than 0.05 the H0 will be accepted. The hypothesis

for T-test can be shown below:

T-test is used to analyze the partial relationship between each of independent

variables (coefficient) to the dependent variable. The significance level T for a

given hypothesis test is a value for which a P-value (sig.) less than or equal to α is

probability value, if the level of significant lower than 0.05 or 5% so the hypothesis

is accept or significant, just the opposite if the value of significant higher than 0.05

or 5% so the hypothesis will be reject or does not significant.

a. Non – Performing Loans (NPL)

According to the table 4.5 coefficient above, p-value of t-statistics 0.23 > 0.05. It

means that NPL does not have a significant effect to the EPS. Thus, researcher

reject the alternate hypothesis (Ha) and accept null hypothesis (H0). It means there

is no significant impact of NPL (X1) toward EPS (Y).

b. Net Interest Margin (NIM)

P-value (sig.) of NIM is 0.622 which is higher than α. It means that NIM doesn't

significantly affect the EPS. Therefore, researcher conclude to reject the null

hypothesis (H0) and accept alternate hypothesis (Ha). It means there is no

significant effect of NIM (X2) toward EPS (Y).

c. Return on Assets (ROA)

44

P-value of ROA is 0.000 which is lower than α (0.05 or P-value <0.05). It means

that on partially, ROA signifcantly affects the EPS. Therefore, researcher conclude

to accept the alternate hypothesis (Ha) and reject null hypothesis (H0). It means

there is a significant effect of NIM (X3) toward EPS (Y).

4.2.4.3 R-Square (Coefficient of Correlation (R2) and Coefficient of

Determination (R Square))

This test is to measure how far the model's ability to explain variation in the dependent

variable, where R Square value ranges between 0 < R2 < 1, the greater the R2 makes

the independent variables (NPL, NIM ROA) has stronger relationship with dependent

variable (EPS) this model is considered a good model.

Here is the result:

Table 4.8 R-Square

Source: SPSS Processed Data,2018

The number of adjusted R-Square was essentially to measure how far the model's

ability to explain variation in the dependent variable. In this research. Adjusted R-

Square is 0.653, which means 65.3% that the dependent variable EPS is influenced by

combination of independent variables which are NPL, NIM and ROA. The rest which

is 34.7% will be explained by other factors, which will not be discussed in this research.

For the result, Adjusted R-Square for panel data is medium and can be acceptable.

45

4.3. Interpretation of Results

The data that input in SPSS based on the quarterly period of PT. Bank Central Asia

Tbk. Starting 2007 –2016. From the data analysis above which already done by

research using SPSS about NPL, NIM and ROA as the independent variables towards