Embed Size (px)

Citation preview

Chapter 14

The It o Integral

Thefollowing chaptersdealwith StochasticDifferentialEquationsin Finance. References:

1. B. Oksendal,StochasticDifferentialEquations, Springer-Verlag,1995

2. J.Hull, Options,FuturesandotherDerivativeSecurities,PrenticeHall, 1993.

14.1 Brownian Motion

(SeeFig. 13.3.)�����������

is given,alwaysin thebackground,evenwhennot explicitly mentioned.Brownian motion, � �� �������������������� ��! " , hasthefollowing properties:

1. � ���#�$%�'& Technically,! (*)+�,& � �-�'�.�/�$%�102$43

,

2. � �� . is a continuousfunctionof ,

3. If�5$6 87,9� �:;9=<><><19� 8?

, thentheincrements

� �� : �@ � �A 87BC��<B<C<D� � �� E?��@ � �A 8?#F :

areindependent,normal,and

! GH� � �A JILK : M@ � �A JIN-OP$=�'�! G�� � �A EILK : Q@ � �A EINEOAR�$S .I�K : @� .IT<

14.2 First Variation

Quadraticvariationis a measureof volatility. First we will considerfirst variation, U,V ��WP , of afunction

W��� ..

153

154

t

t

1

2t

f(t)

T

Figure14.1:ExamplefunctionW��� .

.

For thefunctionpicturedin Fig. 14.1,thefirst variationover theinterval��������O

is givenby:

U,V�� 7�� ��� ��WD�$4� W/�A :�@ W����#EO @ � W/�A R �@ W��� :�EO � W���� /@ W��� R EO$

�� �7W��A�� .�� � ����

�� �J@ W��-�A E��� �

��� �W����� J��# L<

$��7�� W��A�A J � � �<

Thus,first variationmeasuresthetotalamountof upanddown motionof thepath.

Thegeneraldefinitionof first variationis asfollows:

Definition 14.1(First Variation) Let � $ )B 7 � : �C<B<C<��� ? 0 bea partition of��������O

, i.e.,

��$S 7 9� : 9=<><><19 ? $��2<Themeshof thepartitionis definedto be

��� � ��� $ "!$#I&% 7��(' ' '�� ?#F : �� I K : @� I +<We thendefine

U,V � 7)� ��� ��WD�$ *,+� -(- ./-(- � 7? F :0I1% 7 � W/�A EI K : M@ W/�A JIN � <

SupposeW

isdifferentiable.ThentheMeanValueTheoremimpliesthatin eachsubinterval� JI � JI K : O

,thereis apoint

32Isuchthat

W��� .I K :+�@ W��� JI �$=W � �� 2I C�� .I K :�@ .IN <

CHAPTER14. TheIto Integral 155

Then ?#F :0I&% 7 � W/�A JILK : M@ W/�A EIN � $

? F :0I&% 7 � W � �� 2I � �� .I�K : @ EIN+�

and

U,V � 7)� ��� ��WD�$ * +� - - ./- - � 7?#F :0I&% 7 � W � �� 2I � �� JILK : @ JIN

$��7 � W��-�A J � � �<

14.3 Quadratic Variation

Definition 14.2(Quadratic Variation) Thequadraticvariationof afunctionW

onaninterval����� ��O

is� W�� � � $ * + -(- . -(- � 7

? F :0I1% 7 � W �A EI K :+�@ W �� JIN � R <

Remark 14.1(Quadratic Variation of DifferentiableFunctions) IfW

isdifferentiable,then�EW��B��� Q$

�, because ? F :0

I1% 7 � W �� JI K :��@ W �� JIN � R $? F :0I&% 7 � W�� �A 2I � R �A EI K :�@� JIN R

9 ��� � ��� <? F :0I1% 7 � W � �A 2I � R �A EI K :�@� JIN

and

�8W��>��� 9 * +� - - ./- - � 7 ��� � ��� < * +� - - ./- - � 7? F :0I&% 7 � W � �� 2I � R �� JI K :�@ JIN

$ * +� - - ./- - � 7 ��� � �����7 � W � �� J � R �

$=�'<

Theorem 3.44� � �>���2�$�� �

or moreprecisely, ! ( ) ��� ��& � � �.< ���/��C���; $ �50;$43 <In particular, thepathsof Brownianmotionarenot differentiable.

156

Proof: (Outline)Let � $ )B 87#� �: �><><><�� -? 0bea partitionof

����� � O. To simplify notation,set � I*$

� �A ILK : �@ � �A I . Definethesamplequadratic variation

� . $?#F :0I1% 7 � RI <

Then� . @ �S$ ? F :0

I1% 7 � � RI @ �� .I�K : @� .I EOJ<We wantto show that *,+� -(- ./-(- � 7 � � . @ � $6��<Consideranindividualsummand

� RI @ �� JI K :�@ JIN�$ � � �� .I K :LQ@ � �� .IBJO R @S�� JI K :�@ .IBC<

Thishasexpectation0, so

! G � � . @ � $%! G ? F :0I&% 7 � � RI @ �� .I�K : @ .I>EO $%�'<

For ���$�� , theterms� R� @ �� � K : @� � and � RI @ �� I K : @ I

areindependent,so

� !>� � . @ �2�$ ? F :0I1%�7 � !+� � RI @ �A EI K :�@ .I>EO

$? F :0I1%�7 ! G�� ���I @� ��� JI K :�@� .IB � RI 6�� .I K :�@� JIN R O

$? F :0I1%�7 �����A I K : @� I R @� �� I K : @ I R �A I K : @ I R O

(if � is normalwith mean0 andvariance� R , then! G � ��� �$�� ��� )

$� ? F :0I1%�7 �� I K : @� I R

9� � � � � �? F :0I�% 7 �� JI K : @ JIC

$ � � � � � �;<Thuswe have

! GH� � . @ �2�$%�'�� !�C� � . @ �2�9� ��� � ��� <(�;<

CHAPTER14. TheIto Integral 157

As ��� � ��� � � , � !B� � . @ �2����, so *,+� -(- ./-(- � 7 � � . @ �2�$6��<

Remark 14.2(Differential Representation) We know that! G���� � �� .I K : �@ � �� JIN� R @ �� JI K : @� JI EO $%��<

We showedabove that

� !C� � � �A JI K : M@ � �� .I . R @ �� JI K : @� .IBJOD$� �� .I K : @ .I> R <When

�� I�K : @ I is small,

�A ILK : @ I Ris verysmall,andwehave theapproximateequation

� � �� JI K : Q@ � �� JI R�� EI K : @� JIT�

whichwe canwrite informally as � � �� .�� � �� .�$ �# L<

14.4 Quadratic Variation asAbsoluteVolatility

Onany time interval� � : ��� R O , we cansampletheBrownianmotionat times� : $ E7*9� : 96<><B< 9 8? $�� R

andcomputethesquaredsampleabsolutevolatility

3� R @ � :? F :0I&% 7 � � �A JILK : �@ � �A JIN� R <

This is approximatelyequalto3� R @ � : � � � �>��� R M@ � � �C� � : JO�$ � R @ � :� R @ � : $ 3 <

As we increasethe numberof samplepoints,this approximationbecomesexact. In otherwords,Brownianmotionhasabsolutevolatility 1.

Furthermore,considertheequation

� � �>��� �$�� $��73 � L� ����� ��<

This saysthat quadraticvariation for Brownian motion accumulatesat rate 1 at all timesalongalmosteverypath.

158

14.5 Construction of the It o Integral

The integrator is Brownian motion � �� . � � �, with associatedfiltration

� �A J+�� � �, andthe

following properties:

1. � 9� .$�� everysetin� � � is alsoin

� �A J,

2. � �� . is� �� J

-measurable,��

,

3. For 9� : 9=<><><19 8?

, theincrements� �A : M@ � �A E+� � �� R �@ � �� : +�C<B<C<�� � �� 8?1�@ � �� 8? F : areindependentof

� �� ..

The integrand is� �A J � � �

, where

1.� �A J

is� �� .

-measurable�

(i.e.,�

is adapted)

2.�

is square-integrable:

! G��7� R �� .�� �� �S� ���2<

We wantto definetheIt o Integral:

!D�� .�$��7

� ��� �� � ��� � �� �'<

Remark 14.3(Integral w.r.t. a differentiable function) IfW��� .

is a differentiablefunction, thenwecandefine ��

7� ��� ��8W������$ � �

7 � ��� �W��A��� ��� <This won’t work whenthe integratoris Brownianmotion, becausethe pathsof Brownianmotionarenotdifferentiable.

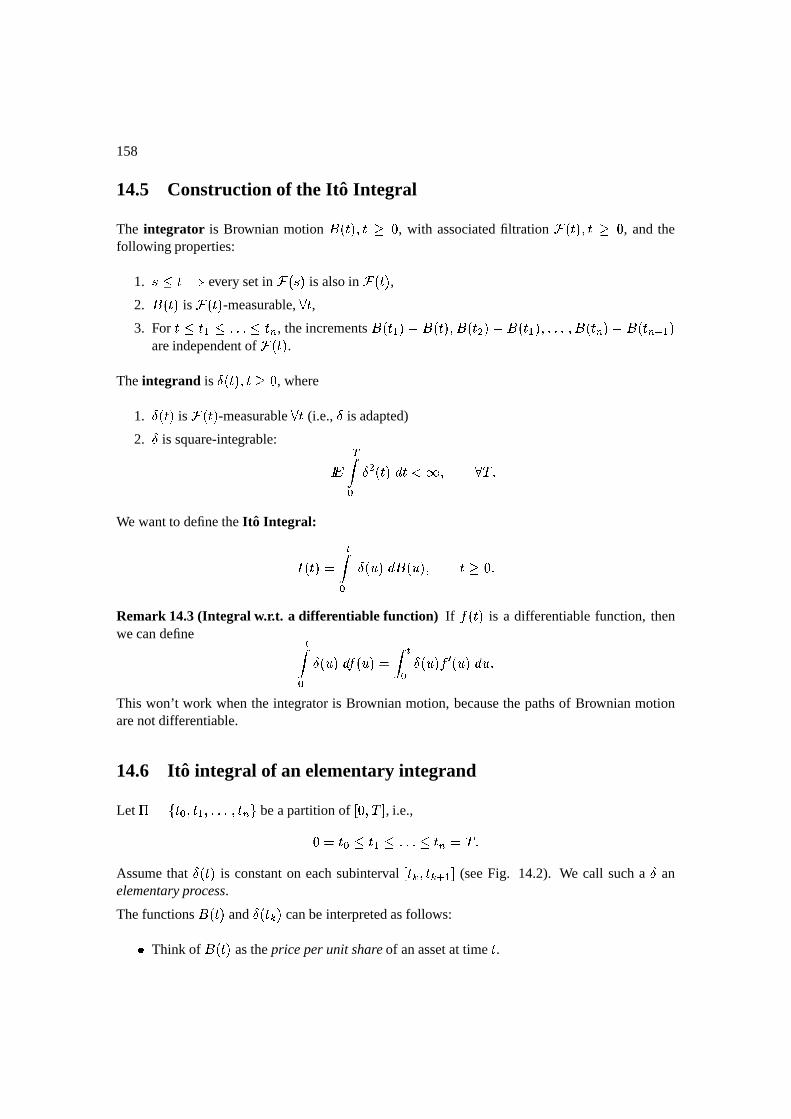

14.6 It o integral of an elementaryintegrand

Let � $ )C 7 � : �><><><'� ? 0 beapartitionof���'����O

, i.e.,

��$S E7*9� :29=<><><19 E? $��2<Assumethat

� �� .is constanton eachsubinterval

� .I1� JILK : O(seeFig. 14.2). We call sucha

�an

elementaryprocess.

Thefunctions� �� J and� �A I

canbeinterpretedasfollows:

Think of � �� J asthepriceperunit shareof anassetat time .

CHAPTER14. TheIto Integral 159

t )δ(

t )δ(δ( ) δ( t )=t

)tδ(

0=t0t t t = T2 3 4t1

0

δ( t )= 1

δ( t )= 2

δ( t )= 3

Figure14.2:Anelementaryfunction�.

Think of E7#� :+�C<B<>< � 8?

asthetradingdatesfor theasset. Think of

� �A JI>asthenumberof sharesof theassetacquiredat tradingdate

JIandhelduntil

tradingdate .I K :

.

ThentheIto integral! �� .

canbeinterpretedasthegainfromtradingat time ; thisgainis givenby:

! �A J�$������ �����

� �� 87> � � �� .�@ � �� 87>� ��� �%�� 7� �% 7 OJ� � 9� �9 :

� �� 87> � � �� : �@ � �� E7>EO � �� : +� � �A J�@ � �� : EOJ� : 9� �9� R� �� 7 � � �� : �@ � �� 7 EO � �� : � � �A R �@ � �� : EO � �A R � � �A EM@ � �A R EO � R 9 9 �� <

In general,if EI 9 9 JI K :

,

! �� .�$I+F :0� % 7 � �� � C� � �� � K : M@ � �� � EO� � �A JICC� � �� .�@ � �� JINEOJ<

14.7 Propertiesof the It o integral of an elementaryprocess

AdaptednessFor each �N! �� .

is���� .

-measurable.

Linearity If

!D�� J�$��7� ��� �� � ����+� ���A E�$ ��

7�� ��� /� � ��� then ! �A J������� J $ � �

7 � � ��� �� � �����/� � ���

160

t tttl+1l k k+1

s t

. . . . .

Figure14.3:Showing� and

in differentpartitions.

and �!D�� J $ � �

7�� ��� �� � ��� <

Martingale!D�� J

is a martingale.

We prove themartingalepropertyfor theelementaryprocesscase.

Theorem 7.45(Martingale Property)

!D�� J�$I F :0� % 7 � �� � +� � �� � K : �@ � �� � EO � �� .IBC� � �� .�@ � �A JINEOE� JI 9� �9 EILK :

is a martingale.

Proof: Let�S9 � 9

be given. We treat the moredifficult casethat � and

are in differentsubintervals,i.e., therearepartitionpoints

��and

Isuchthat �

��� ��+�� ��-K : Oand

� � I � I K : O(See

Fig. 14.3).

Write

!P�� . $�JF :0� % 7 � �� � +� � �� � K : �@ � �� � JO � �� ��� � � �� ��8K : �@ � �A ���EO I+F :0� % � K : � �� � +� � �� � K : �@ � �A � 8O � �A EIN+� � �� .�@ � �� .I EO

We computeconditionalexpectations:

! G�� �JF :0� %�7 � �� � B� � �� � K : Q@ � �� � ����� � � � � $

�JF :0� % 7 � �� � >� � �� � K : �@ � �A � <

! G�� � �� � C� � �� � K : �@ � �� � E ���� � � � 5$ � �A � ��! GH� � �� � K : � � � � -O @ � �� � �$ � �A � � � � � �@ � �� � EO

CHAPTER14. TheIto Integral 161

Thesefirst two termsaddup to! � � . Weshow thatthethird andfourth termsarezero.

! G�� I+F :0� % � K : � �A � >� � �� � K : �@ � �� � . ���� � � � � $

I+F :0� % � K : ! G � ! G � � �� � B� � �� � K : Q@ � �� � ���� � �� � ���� � � �

$I F :0� % �8K : ! G

���� �A � Q� ! G � � �� � K : � � �� � EO @ � �� � �� ��� �% 7 ���� � � � ���

! G � � �� .I >� � �� .�@ � �A JIN ���� � � � $=! G���� �� .IC ��! G�� � �� J � � �� JIB8O @ � �A JIN�� ��� �%�7 ���� � � � � �

Theorem 7.46(It o Isometry)

! G !TR �A J $=! G � �7 � R � ���� � <

Proof: To simplify notation,assume �$S JI

, so

! �A J�$I0� %�7 � �� � C� � �� � K : �@ � �� � � � � ���� O

Each� � hasexpectation0, anddifferent � � areindependent.

! R �A J�$�� I0� % 7 � �A � � ��

R

$I0� % 7 � R �� � � R� 0 � � � � ��

� � �� � �

�� � <

Sincethecrosstermshave expectationzero,

! G !1RB�A J�$I0� % 7 ! G�� � R �� � � R� O

$I0� % 7 ! G � � R �� � ! G � � � �� � K :��@ � �� � . R ���� � �� �

$I0� % 7 ! G � RN�� � >�� � K : @� �

$=! GI0� % 7

� ��� �� � � R ��� �� �

$=! G � �7 � R#��� ���

162

0=t0t t t = T2 3 4t1

path of path of

δδ4

Figure14.4:Approximatinga general processbyanelementaryprocess�� , over

��������O.

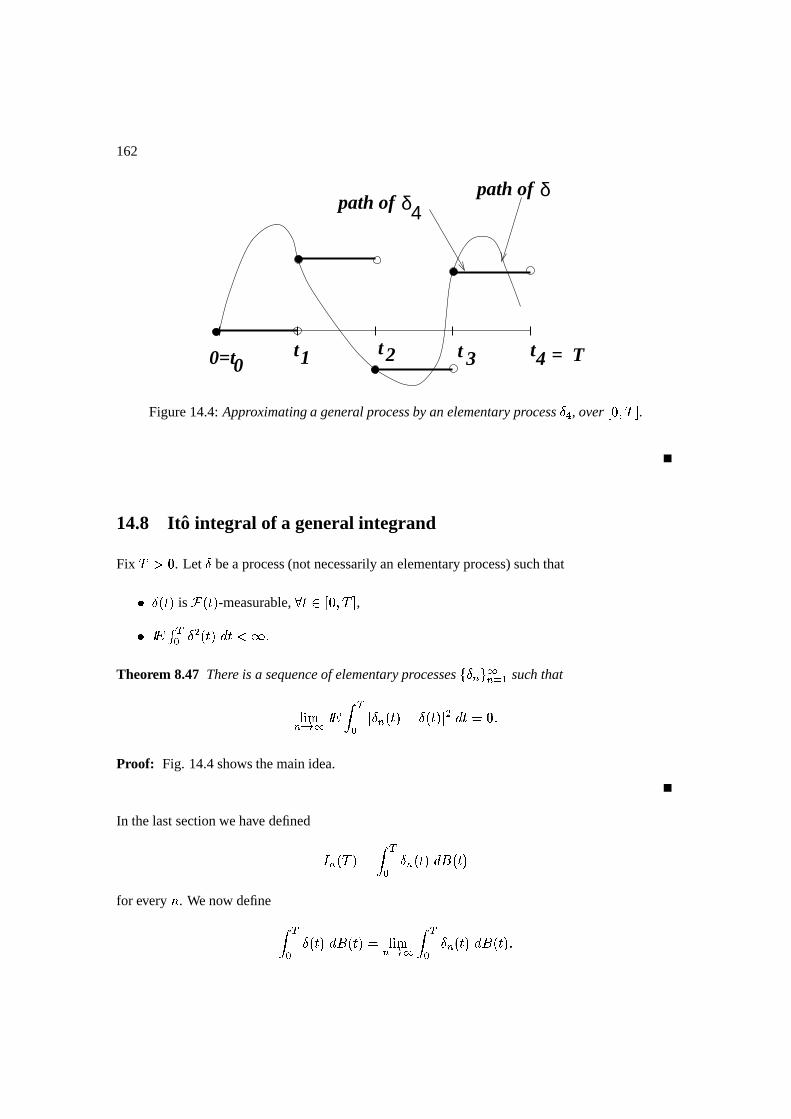

14.8 It o integral of a generalintegrand

Fix�����

. Let�

bea process(not necessarilyanelementaryprocess)suchthat

� �A Jis� �� .

-measurable,�� � � ��� ��O

,

! G�� �7 � R �� .�� �� �S<Theorem 8.47 There is a sequenceof elementaryprocesses

) � ?�0��? % :such that

* +� ? � � ! G � �7 � � ? �A J�@ � �A J � R �# �$=��<

Proof: Fig. 14.4showsthemainidea.

In thelastsectionwehave defined

!�? ���2�$ � �7 � ?P�� .�� � �A E

for every � . Wenow define

� �7 � �A J�� � �� .�$ *,+� ? � � � �

7 � ? �� .�� � �� . <

CHAPTER14. TheIto Integral 163

Theonly difficulty with thisapproachis thatwe needto makesuretheabove limit exists. Suppose� and � arelargepositiveintegers.Then

� ! � ! ? � � Q@ ! � � � $=! G � � �7 � � ? �A EM@ � � �� .EO�� � �� .�� R

(Ito Isometry:)$ ! G � �

7 � � ? �� JM@ � � �� .EO R � $ ! G � �

7 � � � ? �A EM@ � �� J � � � �A EQ@ � � �� J � O R �# ���� �� R 9� � R � � R � �9� #! G � �

7 � � ?D�� .�@ � �� J � R � �� ! G� �7 � � � �� J�@ � �� . � R � ��

which is small.Thisguaranteesthatthesequence) !�? � � L0 �? % :

hasa limit.

14.9 Propertiesof the (general)It o integral

!D�� J�$ � �7 � ������ � � ��+<

Here�

is any adapted,square-integrableprocess.

Adaptedness.For each ,! �A J

is� �� .

-measurable.

Linearity . If

!D�� J�$��7� ��� �� � ����+� ���A E�$ ��

7 � ��� /� � ��� then ! �A J������� J $ � �

7 � � ��� �� � �����/� � ��� and �

!D�� J�$ � �7�� ��� �� � ��� +<

Martingale.!D�� .

is amartingale.

Continuity.!D�� .

is acontinuousfunctionof theupperlimit of integration .

It o Isometry.! G ! R �� .�$6! G � �7 � R � ���� �

.

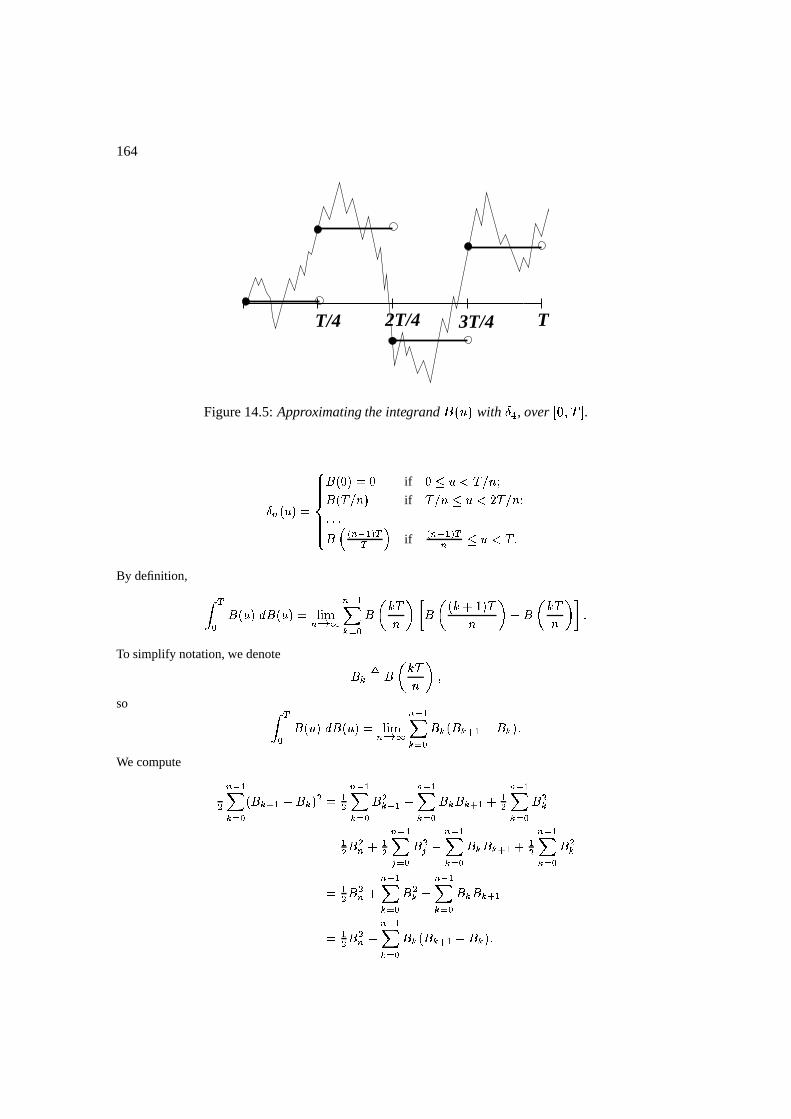

Example14.1() ConsidertheIto integral ���� ��������� ��������We approximatetheintegrandasshown in Fig. 14.5

164

T/4 2T/4 3T/4 T

Figure14.5:Approximatingtheintegrand � ��� with�� , over

� ��� ��O.

��� � ����������� ����� � � ��� �

if��� �� ��� ��

� ��� � if��� �� ����� ��� ����� � ��� ������� � if� � �!�"� � � ��� �

By definition,

� � � � ��� �� � ���$#&%&'�)(+* ���!�0,.- � 0/21 43 � 5/ � 17698 � 3+: 5/;1 <3 �To simplify notation,wedenote

,>=� ?/�1 3A@so � � ��� ��� �� � ���B#&%&'�C(+* � �!�0,D- � , �� ,.E � : , � �We compute �F ���!�0,.- � � ,DE � : , � F � �F ���!�0,D- � F,DE � :

� �!�0,D- � , ,.E � 6 �F � �!�0,D- � F,� �F F� 6 �F �G�H�0IJ- � FI :

�����0,D- � , ,.E � 6 �F �����0,D- � F,� �F F� 6

� �!�0,D- � F, :�G�!�0,D- � , ,DE �

� �F F� :� �!�0,D- � , �� ,.E � : , � �

CHAPTER14. TheIto Integral 165

Therefore, �G�!�0,D- � , � ,DE � : , ��� �F F� : �F �G�!�0,.- � � ,DE � : , � F @or equivalently�����0,.- � 5/21 3 � ?/ � 1 6<8 � 34: /�1 3 � �F F � � : �F � �!�0,D- � � 5/ � 1 698 � 3 / 1 3 F �Let

(� andusethedefinitionof quadraticvariationto get� � ���� ��� ���� � � �F F � � : �F �

Remark 14.4(Reasonfor the:R � term) If

Wis differentiablewith

W����#/$6�, then

� �7 W���� ��8W���� M$ � �

7 W/� ��W��-��� �� �$ :R W R ���� ����

�7

$ :R W R ���2+<

In contrast,for Brownianmotion,we have� �7 � ��� � � �����$ :

R � R ���;�@ :R � <The extra term

:R � comesfrom thenonzeroquadraticvariationof Brownian motion. It hasto be

there,because ! G � �7 � ������ � ��� $6� (Ito integral is a martingale)

but ! G :R � R ���2Q$ :R �;<

14.10 Quadratic variation of an It o integral

Theorem 10.48(Quadratic variation of It o integral) Let

!D�� J�$ � �7 � ������ � � ��+<

Then� ! �C�� .�$ � �

7 � RN��� �� � <

166

Thisholdsevenif�

is notanelementaryprocess.Thequadraticvariationformulasaysthatat eachtime

�, the instantaneousabsolutevolatility of

!is

� R ��� . This is the absolutevolatility of the

Brownianmotionscaledby thesizeof theposition(i.e.� �� J

) in theBrownianmotion. Informally,wecanwrite thequadraticvariationformulain differentialform asfollows:�T! �� .�� !D�� . $ � R �� .��# L<Comparethiswith � � �� .�� � �� .�$ �# L<Proof: (For anelementaryprocess

�). Let � $ )> -7 �� : �><><><��� 8?'0

bethepartitionfor�, i.e.,

� �� . $� �� JIB

for JI*9 �9� .I�K :

. To simplify notation,assume /$6 8?

. We have

�8! �>�� E�$? F :0I1%�7 � �8! �C�� .I K : Q@ �8! �>�� .I EO1<

Let uscompute�8! �C�� JI K :�M@ �8! �B�� JI>

. Let� $ ) � 7B� � :>�><><><'� � � 0 bea partition

JI2$ � 7*9 � : 9=<><>< 9 � � $ JI K : <Then

!D� � � K : M@ ! � � � �$� ��� �� � � �� JI>�� � ����

$ � �� .IC � � � � � K :+�@ � � � � EO �

so

�E! �C�A JILK : �@ �8! �B�� JI �$ � F :0� % 7 � !D� � � K : @ !D� � � EO R

$ � R �� .I> � F :0� % 7 � � � � � K : �@ � � � � JO R

��� � ��� ���@ @�@�@'@T� � R �� JI>>�� .I�K : @ .I +<

It followsthat

�8! �B�� J�$? F :0I&% 7 � R �A EIN>�� .I K : @ EIN

$?#F :0I&% 7

��� � �� �

� R#��� �� �

� � � � � � �@8@�@'@'@ @ �� �7 � RB� ���� � <

Chapter 15

It o’s Formula

15.1 It o’s formula for oneBrownian motion

We wanta rule to “dif ferentiate”expressionsof the formW�� � �� J� , where

W/����is a differentiable

function.If � �� . werealsodifferentiable,thentheordinarychain rule wouldgive�� W�� � �� J�M$=W � � � �A J � � �� J+�whichcouldbewritten in differentialnotationas

�EW/� � �� .�$=W � � � �� J � � �A E�� $=W��8� � �� J�� � �� JHowever, � �� . is notdifferentiable,andin particularhasnonzeroquadraticvariation,sothecorrectformulahasanextra term,namely,

�8W�� � �A J $6W��-� � �� .�� � �A E :R W�� �-� � �� .� �# ��� ���

� �� � � �� � <

This is Ito’s formulain differential form. Integratingthis,weobtainIto’s formulain integral form:

W�� � �A J�@ W�� � ���#� ��� �� � 7�

$ � �7 W��8� � ��� �� � ��� :

R� �7 W�� �8� � ������ � <

Remark 15.1(Differential vs. Integral Forms) Themathematicallymeaningfulform of Ito’sfor-mulais Ito’s formulain integral form:

W�� � �A J�@ W�� � ���#�$� �7 W��8� � ��� �� � ��� :

R� �7 W�� �8� � ������ � <

167

168

This is becausewe have solid definitionsfor both integralsappearingon the right-handside. Thefirst, � �

7 W � � � � ���� � ��� is anIto integral, definedin thepreviouschapter. Thesecond,

� �7 W�� �8� � � ���� � �

is aRiemannintegral, thetypeusedin freshmancalculus.

For paperandpencilcomputations,themoreconvenientform of Ito’s rule is Ito’s formulain differ-ential form: �8W�� � �� J $6W � � � �� .�� � �� . :

R W � � � � �� .��� �<Thereis anintuitivemeaningbut nosoliddefinitionfor theterms

�8W�� � �� J�+��� � �� . and�

appearingin this formula.This formulabecomesmathematicallyrespectableonly afterwe integrateit.

15.2 Derivation of It o’s formula

ConsiderW � �� $ :

R � R , sothat W��8� � �$ � � W�� �8� ���$ 3#<

Let��I � � I K :

benumbers.Taylor’s formulaimplies

W�� ��ILK : �@ W�� ��IN�$ ����ILK : @ � IN�W��A� � IC� :R ����ILK : @ ��IB�R�W��(�8� � IC+<

In thiscase,Taylor’s formulato secondorderis exactbecauseW

is aquadratic function.

In thegeneralcase,theaboveequationis only approximate,andtheerroris of theorderof� ��ILK : @

� I �. Thetotalerrorwill have limit zeroin thelaststepof thefollowing argument.

Fix�����

andlet � $ )> E7#� : �><><C< �� E?�0 bea partitionof� �'����O

. UsingTaylor’s formula,wewrite:

W � � � � �@ W � � � � �$ :R � R � � @ :

R � R � � $? F :0I&% 7 ��W�� � �� JI K : �/@ W/� � �� .IB�EO

$?#F :0I&% 7 � � �� JILK : �@ � �� JINEOBW��8� � �� JI �

:R? F :0I�% 7 � � �� JILK : �@ � �� JINEO R W��(�A� � �� .IB�

$?#F :0I&% 7 � �� JIN � � �� JILK : �@ � �� .I JO

:R?#F :0I&% 7 � � �� .I�K : M@ � �� .I JO R <

CHAPTER15. Ito’sFormula 169

We let ��� � ��� � � to obtain

W�� � ���2��@ W�� � ���#�$ � �7 � ������ � ����/ :

R � � �C� �2� � � ��$ � �

7 W��8� � ��� ��� � � ��� :R� �7 W��(�A� � ������ � � �:

�� <

This is Ito’s formulain integral form for thespecialcaseW�� �� $ :

R � R <

15.3 GeometricBrownian motion

Definition 15.1(GeometricBrownian Motion) GeometricBrownianmotionis� �� J�$ � ��� ��)#���� � � �� ./ ��� @ :R � R � *�

where�

and � � � areconstant.

DefineW/�A �� � �$ � �-� ��)#���� � � � � @ :

R � R � � �so

� �� .�$=W��� �� � �� .+<Then

W � $ � � @ :R � R � W ��W��,$ � W ��W����*$ � R W�<

Accordingto Ito’s formula,� � �� JQ$ �-W��� L� � �� J$=W � �# W � � � :R W ��� � � � �� ��� �

� �$ � � @ :R � R �W � � � W � � :

R � R W �# $ � � �� .�� � � � �� J�� � �� .

Thus,GeometricBrownianmotionin differential form is� � �� JQ$ � � �� .�� � � � �� J�� � �� .+�andGeometricBrownianmotionin integral form is

� �� .�$ � �-� � � �7 � � � ���� � � �

7 � � ��� /� � � �� <

170

15.4 Quadratic variation of geometricBrownian motion

In theintegral form of GeometricBrownianmotion,

� �� J $ � � � � � �7 � � ��� �� � � �

7 � � � ���� � ��� �theRiemannintegral

U �� .�$� �7 � � ��� ���

is differentiablewith U � �A JM$ � � �� J. This termhaszeroquadraticvariation.TheIto integral

� �� .�$ � �7 � � ��� /� � � ��

is notdifferentiable.It hasquadraticvariation

� � � �A J $ � �7 � R � R ������ � <

Thusthequadraticvariationof�

is givenby thequadraticvariationof�

. In differentialnotation,wewrite � � �� .�� � �� J $ � � � �A J�� � � � �� J�� � �� J� R $ � R � R �A J��

15.5 Volatility of GeometricBrownian motion

Fix��9 � : 9 � R . Let � $ )> 87#�B<C<B<�� E?'0

bea partitionof�(� : ��� R O . Thesquaredabsolutesample

volatility of�

on� � : ��� R O is

3� R @ �Q:? F :0I&% 7 � � �� JI K :��@ � �� .I>EO R � 3� R @ �Q:

� ��� �

R � R � ���� �� � R � R � � :

As� R�� � :

, the above approximationbecomesexact. In otherwords,the instantaneousrelativevolatility of

�is � R . This is usuallycalledsimply thevolatility of

�.

15.6 First derivation of the Black-Scholesformula

Wealth of an investor. An investorbeginswith nonrandominitial wealth � 7 andat eachtime ,

holds ��� .

sharesof stock.Stockis modelledby a geometricBrownianmotion:

� � �� JQ$ � � �A J�� � � � �� J�� � �� J <

CHAPTER15. Ito’sFormula 171

��� .

can be random,but mustbe adapted.The investorfinanceshis investingby borrowing orlendingat interestrate � .Let � �� J denotethewealthof theinvestorat time

. Then� � �� JQ$ � �A J�� � �� .� � � � �� . @ � �� . � �� .EO �# $

��A J � � � �� . � � � � �� J�� � �A EEO � � � �� J�@ � �� J � �� JJO)� $ � � �� J � �

�� J � �� J � � @ � � ��� �Riskpremium

� ��A E � �� J � � � �� J+<

Valueof an option. ConsideranEuropeanoptionwhichpays� � � ���2 attime�

. Let � �� �� � denotethe valueof this option at time

if the stockprice is

� �� . $ �. In otherwords,the valueof the

optionateachtime � � ��� ��O

is� �� �� � �� .�+<

Thedifferentialof thisvalueis� � �� L� � �A J $ � � � � � �$� � :R � ��� � � � �

$ � � � � � � � � � � � � � � O :R � ��� � R � R � $�� � � � � � � :

R � R � R � ����� �# � � � � � �A hedgingportfolio startswith someinitial wealth � 7 andinvestssothat thewealth � �A E at eachtime tracks � �A �� � �� J� . We saw abovethat� � �� JQ$4� � �

�� � @ � � O � � � � � � � <

To ensurethat � �� J�$ � �� L� � �A J for all , weequatecoefficientsin theirdifferentials.Equatingthe� � coefficients,weobtainthe � -hedgingrule:

��� J $ � � �� �� � �� . <

Equatingthe�#

coefficients,weobtain:

� � � � � � :R � R � R � ��� $ � �

�� � @ � � <

But wehaveset �$ � � , andweareseekingto cause� to agreewith � . Makingthesesubstitutions,

weobtain� � � � � � :

R � R � R � ��� $ � � � � � � @ � � �(where � $ � �A �� � �� E� and

� $ � �� .) whichsimplifiesto

� � � � � � :R � R � R � ��� $ � � <

In conclusion,weshouldlet � bethesolutionto theBlack-Scholespartial differentialequation

� � �A � � � � � � � �A � � :R � R � R � ��� �� � �� $ � � �� � ��

satisfyingtheterminalcondition� ���2� � $ � � � +<

If aninvestorstartswith � 7 $ � �-��� � ���# andusesthehedge��� .�$ � � �� �� � �� . , thenhewill have

� �� J�$ � �� L� � �� J for all , andin particular, � ���2Q$ � � � ��� � .

172

15.7 Mean and varianceof the Cox-Ingersoll-Rossprocess

TheCox-Ingersoll-Rossmodelfor interestratesis

� � �� .�$ � � ��@ �� �A J � � ��� � �� J�� � �A E+�

where��� � � � � � and � ��� arepositiveconstants.In integral form, thisequationis

� �� E�$ � �-�#� � � �7 ��� @ �

� ��� � � � � �7 � � � ���� � ��� <

We applyIto’s formulato compute� � R �� . . This is

� W � � �� J� , whereW ���� $ � R

. We obtain� � R �A J�$��EW/� � �A J�$6W��8� � �� J��� � �� .� :R W�� ��� � �A E��� � �� .�� � �� .

$ � �� . � � ��� @ �� �� . �# ��� � �A J�� � �� . � � � ��@ �

� �� .��# ��� � �� J�� � �� . R$� ��� � �� J�� @� �

�� R �� J�� � � ���� �� J�� � �� . � R � �� .��#

$ � ���� � R � �� .��# Q@ ��� R �� J��# � ��� � �� J�� � �A E

The meanof � �A J . Theintegral form of theCIR equationis

� �� E�$ � �-�#� � � �7 ��� @ �

� ��� � � � � �7 � � � ���� � ��� <

Takingexpectationsandrememberingthattheexpectationof anIto integral is zero,we obtain

! G � �� . $ � ��� � � � �7 ��� @ �

! G � ��� � � � <Differentiationyields �� ! G � �� J�$ �P����@ �

! G � �� .� $ ����@ � � ! G � �� J+�which impliesthat �� ����� � ! G � �� . � $���� � � � � ! G � �A J� �� ! G � �� . $ ���� � ��� <Integrationyields � �� � ! G � �� JQ@ � ��� $ ��� � �

7 � ���� � � $ �� ��� �� � @ 3>+<We solvefor

! G � �� J : ! G � �� J�$�� � F �� � / � ���#/@ �� 3 <

If � ��� Q$�� , then! G � �� JQ$�� for every

. If � ��� �$�� , then � �� . exhibits meanreversion:

* +� � � � ! G � �� J�$�� <

CHAPTER15. Ito’sFormula 173

Varianceof � �� . . Theintegral form of theequationderivedearlierfor� � R �� . is

� R �� . $ � R � � =� � �/ � R � �7 � ��� �� � @� �

� � �7 � R ��� �� � � � � �

7 � �� ������ � ��� <Takingexpectations,weobtain

! G � R �� . $ � R � � %� ��� � R � �7 ! G � ��� �� @� �

� � �7 ! G � R � ���� � <

Differentiationyields �� ! G � R �� J $ � ���/ � R ! G � �� J @ ��! G � R �� J+�

which impliesthat �� � R �� � ! G � R �� J�$ � R �� � � � � ! G � R �A J� �� ! G � R �� J $�� R �� � � ���/ � R ! G � �� .+<

Using the formula alreadyderived for! G � �� J andintegratingthe last equation,after considerable

algebraweobtain

! G � R �A J�$� � R � � R � R�

R / � ��� Q@ �� 3 � � R� � �� � � F �� � / � ��� @ �� 3 R � R� � � F R �� � � R� � / �

� @ � ���# 3 � F R �� � <

� ! � �A J $=! G � R �� J�@S� ! G � �� J� R$ � � R � � R / � ��� Q@ �� 3 � R� � � F �� � � R� � / �

� @ � ���# 3 � F R �� � <

15.8 Multidimensional Brownian Motion

Definition 15.2(�-dimensionalBrownian Motion) A

�-dimensionalBrownianMotion is a pro-

cess� �� .�$ � � : �� . �><B<C<'� � � �� .

with thefollowing properties:

Each� I��� E is a one-dimensionalBrownianmotion; If

� �$ � , thentheprocesses���A J

and � � �� J areindependent.

Associatedwith a�-dimensionalBrownianmotion,wehave afiltration

) � �A E 0suchthat

For each , therandomvector � �� J is

� �A E-measurable;

For each 9 : 96<B<><19 ?

, thevectorincrements

� �� �: Q@ � �� J+�B<C<B<�� � �� 8?T�@ � �� 8? F : areindependentof

� �� ..

174

15.9 Cross-variations of Brownian motions

Becauseeachcomponent��is aone-dimensionalBrownianmotion,wehavetheinformalequation� �

��� .�� �

��� J�$ �# L<

However, wehave:

Theorem 9.49 If� �$ � , � �

��� .�� � � �� J�$=�

Proof: Let � $ )B 87#�><B<C< � 8?�0bea partitionof

���'����O. For

� �$ � , definethesamplecrossvariationof �

�and � � on

� �'����Oto be

� . $? F :0I1% 7 � �

��� JI K :��@ �

��� JIB8O1� � � �� .I K :��@ � � �� JINEO#<

Theincrementsappearingon theright-handsideof theabove equationareall independentof oneanotherandall have meanzero.Therefore,

! G � . $6��<We compute� ! � � . . First notethat

� R. $? F :0I&% 7 � � �

�� .I�K : Q@ ���� JI R � � � �� JILK : �@ � � �� .IN R

? F :0� � I � � ��A � K : �@ � �

�� � JON� � � �� � K : �@ � � �� � JO <>� � ��� .I�K : M@ �

��� .ICEO1� � � �A JILK : �@ � � �� .I>8O

All the incrementsappearingin the sumof crosstermsare independentof oneanotherandhavemeanzero.Therefore,

� ! C� � . �$%! G � R.$%! G

? F :0I1% 7 � �

��� JI K :��@ �

��� JINEO R � � � �A EI K : �@ � � �� JIBEO R <

But� �

��� .I K : Q@ �

��� EINEO R

and� � � �� .I K :LM@ � � �� JI>EO R areindependentof oneanother, andeachhas

expectation�� .I�K : @� .I

. It followsthat

� !>� � . �$? F :0I1% 7 �A JI K :�@� JI R 9 � � � � �

? F :0I1% 7 �� JI K :�@ .IB�$ ��� � ��� < �;<

As ��� � ��� � � , we have � !B� � . ��� , so� . convergesto theconstant

! G � . $=� .

CHAPTER15. Ito’sFormula 175

15.10 Multi-dimensional It o formula

To keepthenotationassimpleaspossible,we write the Ito formulafor two processesdrivenby atwo-dimensionalBrownianmotion. Theformulageneralizesto anynumberof processesdrivenbya Brownianmotionof anynumber(notnecessarilythesamenumber)of dimensions.

Let � and � beprocessesof theform

� �� J�$ � ��� � � �7�� ��� �� � � �

7 � :�: ������ � : � �� � �7 � : R ��� �� � R � ��+�

� �� .�$ � �-�#� � �7�� ������ � � �

7 � R : ��� �� � : ��� � � �7 � RR ��� �� � R ��� +<

Suchprocesses,consistingof a nonrandominitial condition,plusa Riemannintegral, plusoneormoreIto integrals,arecalledsemimartingales. The integrands� ���� � � ��� � and

��� ��� canbeany

adaptedprocesses.Theadaptednessof theintegrandsguaranteesthat � and � arealsoadapted.Indifferentialnotation,wewrite � � $ � � � � :�: � � :/ � : R � � R �� � $ � �# � � R : � � : � R�R � � R <Giventhesetwo semimartingales� and � , thequadraticandcrossvariationsare:

� � � � $ � � � � � :: � � : � : R � � R R �$ �NR:�: � � : � � :� ��� �� �

� :: � : R � � : � � R� � � �7 �NR: R � � R � � R� ��� �

� �$ � � R:�: � R: R R � �� � � � $ � � � � � R : � � : � RR � � R R$ � � RR : � RRR R � ��� � � � $ � � � � � :: � � : � : R � � R >� � � � R : � � : � RR � � R $ � � :�: � R : � : R � RR �� Let

W��� L� � ���1bea functionof threevariables,andlet � �A E and � �� . besemimartingales.Thenwe

have thecorrespondingIto formula:�8W��� L� � ���1 $ W � � W � � � W�� � � :R ��W ��� � � � � W � � � � � � �W�� � � � � O <

In integral form, with � and � asdecribedearlierandwith all thevariablesfilled in, thisequationis W��� �� � �� J+� � �A JQ@ W������ � ���#+� � ���

$ � �7 � W � � W � � W�� :

R � � R:: � R: R W ��� � � :: � R : � : R � RR W � � :R � � RR : � RRR �W���� O � �

� �7 � � :: W � � R : W � O � � : � �

7 � � : R W � � RR W � O � � R �where

W $=W���� � � ����+� � ��� , for� � � � ) 3#� T0 , �

�� $ �

�� ���� , and �

�$ �

�� ��

.