Embed Size (px)

Citation preview

THE KERALA STATE FINANCIAL ENTERPRISES LIMITEDCorporate Office, “Bhadratha”, Thrissur – 680 020

From Dy.Gen.Manager (P&HR), H.O. Thrissur.

To All Units

Our Ref: 4130/T Your Ref:

Date: 15-01-2013Promotion test for the year 2012 updated hand book of schemes is ready for reference which is available in the company’s website.

Sd/-DY.GEN.MANAGER(P&HR)

THE KERALA STATE FINANCIAL ENTERPRISES LIMITED Corporate Office, “Bhadratha”, Thrissur – 680 020.

( For private circulation only)

Hand book of schemes as on 31.12.2012

Index

SI No. Particulars

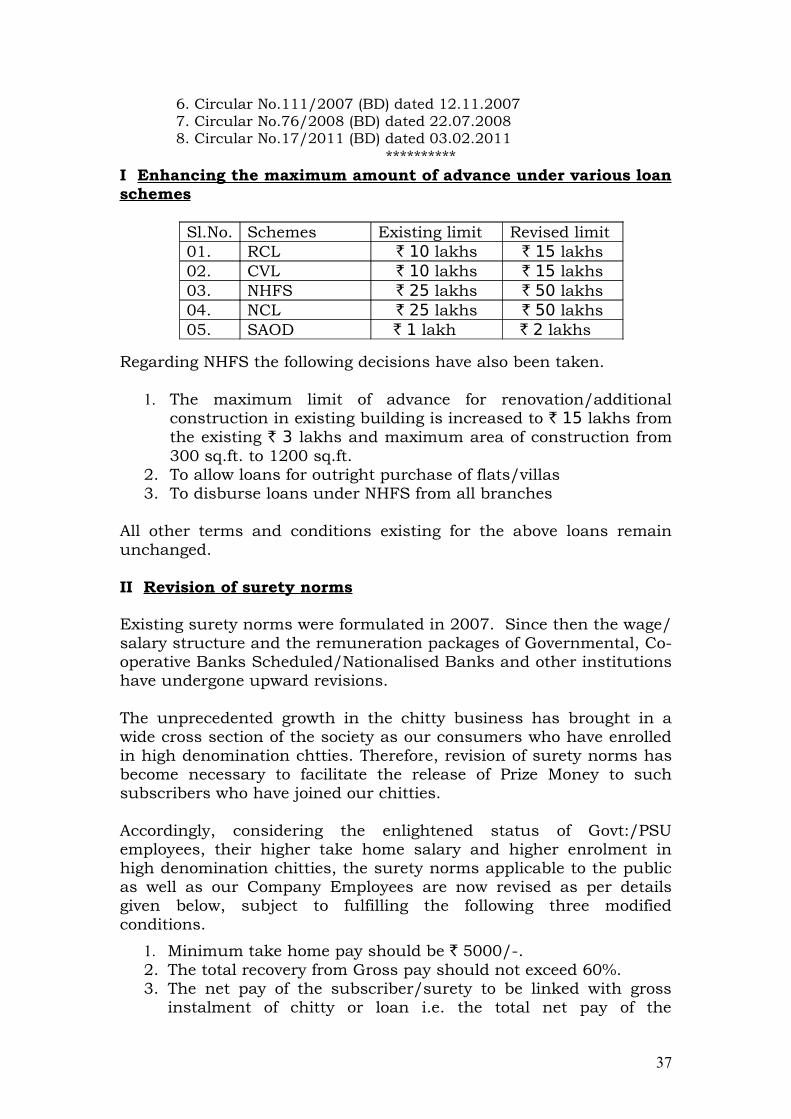

1. Schemes at a glance ................................................................................................ 2. Interest Rate of Different types of FD.s and its interest rates on premature

closure ..................................................................................................................... 3. Flexy trade loan ................................................................................................. 4. Sugama Akshaya Overdraft for Company employees ....................................... 5. Special car loan .................................................................................................... 6. Reliable customer loan ...................................................................................... 7. Gold loan and Gold Security Scheme ..................................................................

8. Acceptance of property as security ................................................................... 9. Property Security at a Glance and its valuation ........................................................ 10. Personal surety norms (English) .......................................................................... 11. Personal surety norms at a glance ........................................................................... 12. Personal surety in short .......................................................................................... 13. Acceptance of flats as securities .............................................................................. 14. Acceptance and sanction powers at a various levels............................................. 15. Procedure for selection of canvassing agent and commission applicable .............. 16. General information regarding various types of fees to be collected from

subscribers/loanees ................................................................................................ 17. Service Tax .......................................................................................................... 18. Personal surety norms (Instructions in Malayalam) ........................................ 19. Property security (Instructions in Malayalam) .................................................... 20. Financial documents and gold security (Instructions in Malayalam) ......................

2

KSFE SCHEMES AT A GLANCE AS ON 31-12-2012Sl.No. Product Particulars Rate of Interest Remarks1.

Chittya) Interest for advance payment of prize

moneyb) Due date of prize money: Date of next

auctionc) Period of interest to be charged for

advance payment of prize money: Up to the date of next auction (excluding next auction date) or up to 30th day (including) from the date of prizing whichever is earlier.

d) R.R. Interest in prized chittiese) Interest on Non-prized chitties

Interest on Non-prized chitties registered w.e.f.02-01-2013

Interest on prized chitties started before 1.11.2002

Started after 1.11.2002[

15% simple

12%simple9% simple

12% simple

12% simple14% simple

Cir.No.51/2010 dt. 12-11-2010

Cir.No.125/08 dt.31.12.2008

CirNo.143/05 dt. 28.9.2005

Cir.No.74/2012 dt.29-12-2012cir.No.143/05 dt.28.9.2005 [

2. N.C.L. a) For Regular Loaneesb) For defaulters

c) Maximum period of interest tobe charged: Up to the date of next auction or date of payment of prize money whichever is earlier

d) Maximum NCL amount (irrespective of number of tickets) that can be allowed to an individual: Rs. 50 Lakhs

15 %17%Monthly diminishing.Note. Ist interest is to be charged up to the due date of chitty instal-ment in cases where chitty date is a later date than NCL. Cir No.3/2003

No.51/2010 dt.12.11.10w.e.f.15.11.2010Cir.No.83/09dt7.10.09 Cir.No. 125/08 dt. 31.12.08

Cir.No.13/2012Dt. 29-03-2012

3. P.B.Loan

a) For regular customersb) For defaultersc) Interest to be collected at the time of

closing: Only up to the date of next auction or payment of prize money whichever is earlier

14.5% simple16.5% simple

Cir No.51/10 dt.12.11.10 w.e.f 15.11.10Cir.No.48/07Cir.No.136/06 Cir.No.125/08 dt. 31.12.08

4. Consu-mer/ Vehi-cle Loan

Repayment period: 12-- 60 monthsa) For regular loaneeb) For defaultersc) Repayment period of electronic and

computer items: 36 monthsd) Concession to staff: 3% (Up to an

advance amount of R.100000/-)Maximum Loan amount per person Rs. 15 Lakhs

15%17.%simple

Cir No.51/10 dt.12.11.10 w.e.f 15.11.10Cir.No.2/11 dt.06-01-11

5. Spl.Car Loan for Public

Repayment period 6– 60 monthsa) Rate of interest upto 35 months

b) Rate of interest above 35 months

c) Penal interest for defaulters

14%monthly diminishing16%monthly diminishing 1.5% per month on EMI

Cir No.47/11dt.06.08.11w.e.f 10.08.11

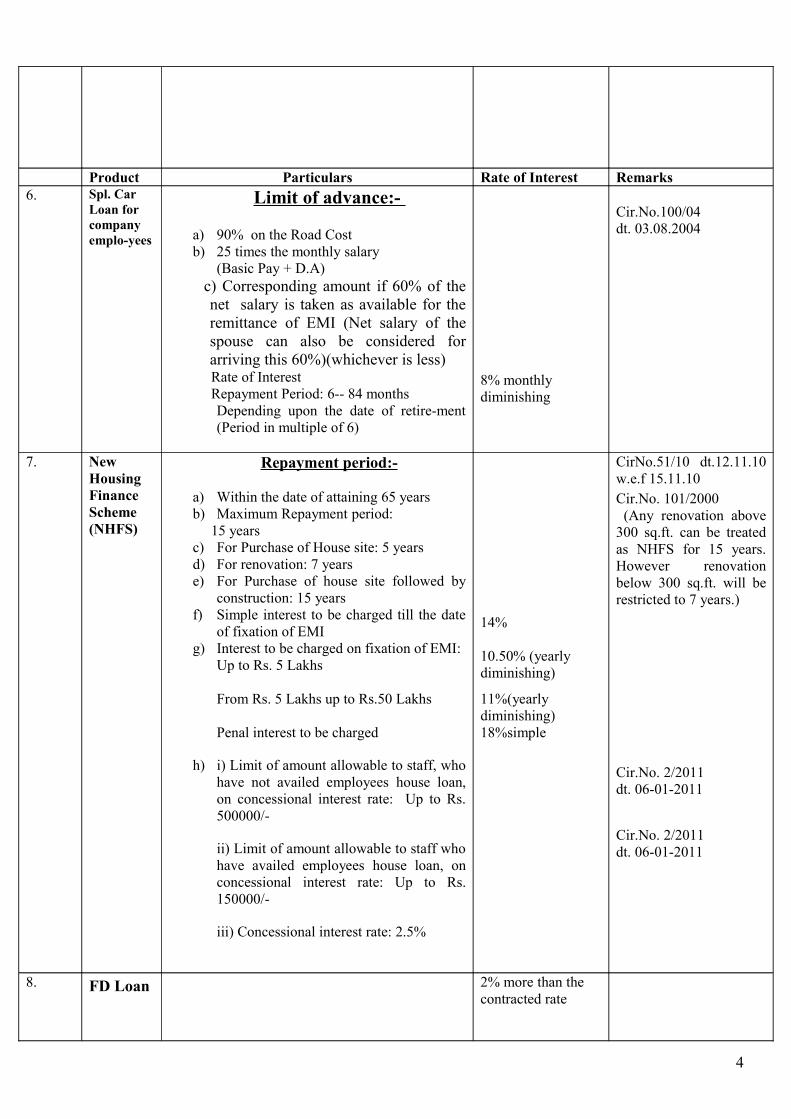

3

Product Particulars Rate of Interest Remarks6. Spl. Car

Loan for company emplo-yees

Limit of advance:-

a) 90% on the Road Cost b) 25 times the monthly salary

(Basic Pay + D.A) c) Corresponding amount if 60% of the

net salary is taken as available for the remittance of EMI (Net salary of the spouse can also be considered for arriving this 60%)(whichever is less)

Rate of Interest Repayment Period: 6-- 84 months

Depending upon the date of retire-ment (Period in multiple of 6)

8% monthly diminishing

Cir.No.100/04 dt. 03.08.2004

7. New Housing Finance Scheme(NHFS)

Repayment period:-

a) Within the date of attaining 65 yearsb) Maximum Repayment period: 15 yearsc) For Purchase of House site: 5 yearsd) For renovation: 7 yearse) For Purchase of house site followed by

construction: 15 yearsf) Simple interest to be charged till the date

of fixation of EMI g) Interest to be charged on fixation of EMI:

Up to Rs. 5 Lakhs

From Rs. 5 Lakhs up to Rs.50 Lakhs

Penal interest to be charged

h) i) Limit of amount allowable to staff, who have not availed employees house loan, on concessional interest rate: Up to Rs. 500000/-

ii) Limit of amount allowable to staff who have availed employees house loan, on concessional interest rate: Up to Rs. 150000/-

iii) Concessional interest rate: 2.5%

14%

10.50% (yearly diminishing)

11%(yearly diminishing)18%simple

CirNo.51/10 dt.12.11.10 w.e.f 15.11.10Cir.No. 101/2000 (Any renovation above 300 sq.ft. can be treated as NHFS for 15 years. However renovation below 300 sq.ft. will be restricted to 7 years.)

Cir.No. 2/2011 dt. 06-01-2011

Cir.No. 2/2011 dt. 06-01-2011

8. FD Loan 2% more than the contracted rate

4

Product Particulars Rate of Interest Remarks9. Sugama

Deposit5.5% simple interest w.e.f.1.5.05

Cir. No.64/0510. Sugama

Akshaya O.D.

a. For regular customersMaximum loan amount Rs. 2 Lakhs

b) For defaulters

15% simple(on daily product basis) 17%

Cir No.47/11 dt.06.08.11 w.e.f 10-08-11

11. Sugama Akshaya OD(Staff)

a. Regular customersb) For defaulters

11% simple15% simple

Cir.No.103//09w.e.f. 01.12.09Cir.No.76/07

12. Gold Loan

Upto and including Rs.10000 Above 10000/- & upto and inclu- ding Rs.2500000/-

Interest should be remitted every month. If interest not remitted within 30 days, penal interest @ 2% per month on the interest.

Admissible amount per gram Purity Gold Loan&Gold security (Vide cir. No. 66/2012 BD dt. 23.11.2012)18 carat 1850 19 carat and above 225019 carat and above(Spl.cases) 2350(Special cases include reliable and reputed customers assessed by unit Head as well as jewellery bearing BIS hall mark symbol having purity of 19 carats and above. The gold loan advances sanctioned under special cases should invariably be at the discretion of Unit Heads – Cir No. 66/2012 dt. 23-11-2012 effective 26-11-2012) ___________________________Loan can be renewed remitting the interest at any time, limiting the whole period of loan to a max. of one year _______________________________It should be ensured that the advance (Advance should not exceed 82% of the prevailing market rate) + interest in any gold loan/gold security account, at any point of time should not exceed 85% of the prevai-ling market value. If so, immediate action should be initiated to realize the dues through auction sale.------------------------------------------Total advance made in one day (to a particular customer from a particular Branch) would be aggregated for determining the applicable rate

12% simple

14% simple

No appraiser fee need be charged in cases where the same gold loan packet is repledged.Max. Gold loan admissible : 25 lakhs (at a time in one account.)No.of advan-ces that could be given to a particular person in a working day from a Branch: 3 Nos.If exceed 3 s/to specific approval of Branch ManagerCir Nos.36/09, 85/08. 42/09,87/00, 129/07,34/08,126/04.65/08,36/08,

Cir No.11/12 dt.13-3-12w.e.f.1-3-12

5

of interest and recovery of minimum charges___________________________

13.RCL

RCL Repayment perioda) For Public Upto 25000 - 36 months Above 25000 – 48 monthsb) For staff : 48 months Interest rate:

Maximum loan amount per person Rs. 15 lakhs Penal interest

Concession to staff : 3% (Upto 100000 or 10 times of net salary whichever is less)

13.5%yearly diminishing 18% simple

Cir No.97/09 dt.17.11.09 w.e.f 18.11.09

Cir. No.47/2011 dt.06-08-11

14 Trade Finance

Repayment period : 12 – 60 a) For regular loaneeb) For defaultersMaximum limit of loan: Rs.100000/-. Loan limit for Stamp Vendors:Rs. 30000/-For lottery Agents: Rs.10000/-

15% simple18% simple

Cir No.47/11 dt.6-8-11 (w.e.f.10-8-11)

15. Flexy Trade Loan

15% diminishing (on quarterly product basis)

Cir No.47/11 dt.6-8-11 (w.e.f.10-8-11)

16. Western Union

Should be produced I.D.Proof of the party Cir No. 130/04 dt. 10.9.2004

17. Manga-lya Loan for CompanyEmplo-yees

a. Eligibility: Permanent employees who have minimum future service of one

yearb) Minimum required net salary:-

Assistants and above: Rs.5000/-, Peons : Rs.3000/-, PTS: Rs.1700

c) Maximum loan amount Rs. 150000 or 10 times of net salary whichever is less.

d) Period of Loan: Maximum period: 48 months or upto retirement whichever is less

e) Rate of interest:f) Penal interest

Security: Self surety

Cost of fund (current rate as on 17.7.06) 8% simple24% simple

Cir.No. 80/2006 dt. 17.7.2006

18. Vidyadhanam Loan Scheme Maximum loan amount Rs. 10 Lakhs

Interest 13.5% simpleEWS category 12%(4% subsidy given

Cir.No.57/2011Dt. 7-5-2011

6

by Govt.)19. KSFE Haritham –85% of the article to be

paidInterest 14% simple Cir.No.62/2012

Dt. 05-11-12

20. Open and CSDT For Sr.citizen Short Term Deposit and others

(These rates are applicable for all fresh deposits /renewals)

Cir No.56/11 dt.5-9-11 w.e.f 7-9-11

Period Rate of interest Cir.No.83/09dt7.10.09

30 – 60 4.75 Cir No.47/11 dt. 6-8-11w.e.f. 10-8-11

61 – 90 5.75% Cir No. 8/06 Dt.23.1.0691—180 6.25%181–364 7.00%

21. FD from Public

Rate of interest Remarks

Particu-lars

Sr.citizen Other than Sr. citizen

Retired KSFE employees

Open FD transfer From chitty including spl. campaigns 10.50% 10.50 % 10.00% 10.25% 11.00% 11.00%

(These rates are applicable for all fresh deposits/renewals)(Maximum period 3 years)

Cir 56/11 dt.5-9-11 w.e.f.7-9-11

Product Rate of Interest Remarks22.

CSDT

Particu-lars(One year and above)

Spl.Camp- other chitties aigns

Max. period: up to the termina-tion of the chitty Cir. No.45/07

Cir 56/11 dt.5-9-11 w.e.f.7-9-11

Sr.citi-zen

Other than Sr. citizen

10.50 10.50% 10.50 % 10.50%

(These rates are applicable for all fresh deposits/

renewals)

7

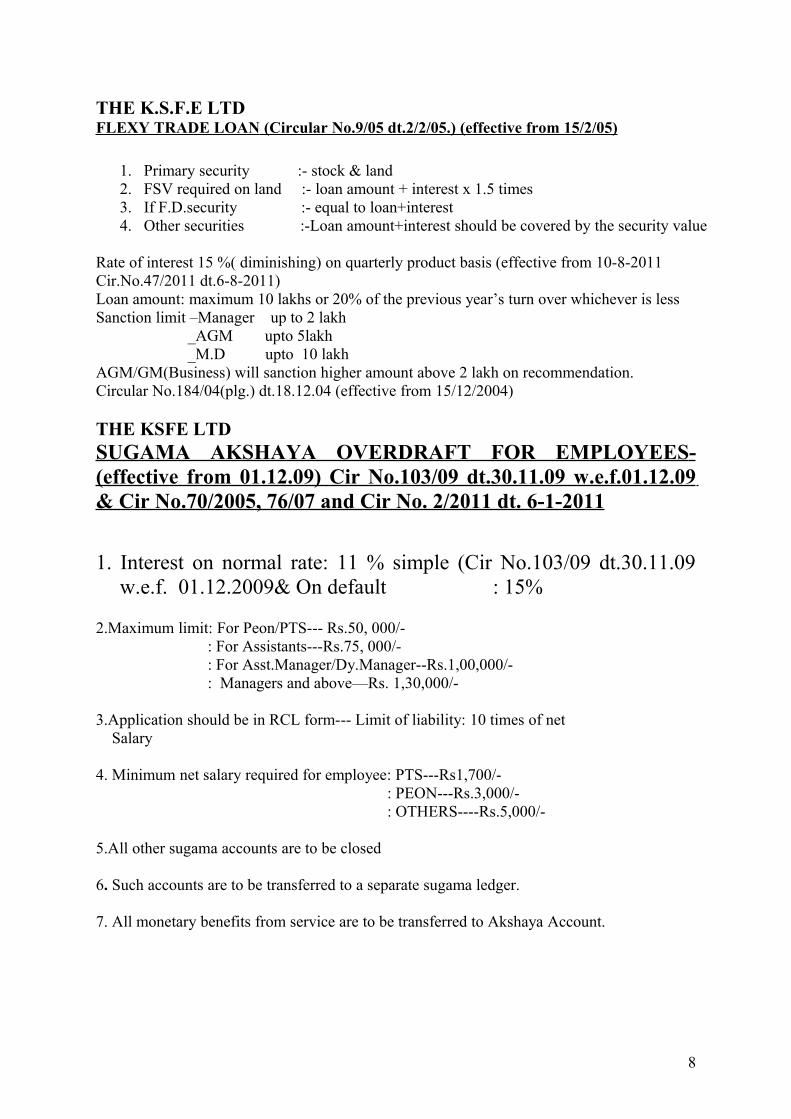

THE K.S.F.E LTDFLEXY TRADE LOAN (Circular No.9/05 dt.2/2/05.) (effective from 15/2/05)

1. Primary security :- stock & land2. FSV required on land :- loan amount + interest x 1.5 times3. If F.D.security :- equal to loan+interest4. Other securities :-Loan amount+interest should be covered by the security value

Rate of interest 15 %( diminishing) on quarterly product basis (effective from 10-8-2011 Cir.No.47/2011 dt.6-8-2011)Loan amount: maximum 10 lakhs or 20% of the previous year’s turn over whichever is lessSanction limit –Manager up to 2 lakh _AGM upto 5lakh _M.D upto 10 lakhAGM/GM(Business) will sanction higher amount above 2 lakh on recommendation.Circular No.184/04(plg.) dt.18.12.04 (effective from 15/12/2004)

THE KSFE LTDSUGAMA AKSHAYA OVERDRAFT FOR EMPLOYEES - (effective from 01.12.09) Cir No.103/09 dt.30.11.09 w.e.f.01.12.09 & Cir No.70/2005, 76/07 and Cir No. 2/2011 dt. 6-1-2011

1. Interest on normal rate: 11 % simple (Cir No.103/09 dt.30.11.09 w.e.f. 01.12.2009& On default : 15%

2.Maximum limit: For Peon/PTS--- Rs.50, 000/- : For Assistants---Rs.75, 000/- : For Asst.Manager/Dy.Manager--Rs.1,00,000/-

: Managers and above—Rs. 1,30,000/-

3.Application should be in RCL form--- Limit of liability: 10 times of net Salary

4. Minimum net salary required for employee: PTS---Rs1,700/- : PEON---Rs.3,000/- : OTHERS----Rs.5,000/-

5.All other sugama accounts are to be closed

6. Such accounts are to be transferred to a separate sugama ledger.

7. All monetary benefits from service are to be transferred to Akshaya Account.

8

KSFE LTD. HO., THRISSUR. Special car Loan (General) at a glance as on 18.11.09 Cir No.97/09 dt.17.11.09 w.e.f. 18.11.09 and CirNo.48/2004 (plg.) dt.5.5.04

1. Application – Free of cost.2. Agreement – on stamp paper worth Rs.100/-3. No administration fee and stamp and paper charges

4. Eligibility – Salaried persons – Net monthly pay exceeding Rs.10000/- (Husband and wife) – One Unit

5. Self employed professional/ business-men(I.T. Payees) having an average annual total income exceeding Rs. 2 Lakhs for the last 3 years.

6. Income tax assessees also includes persons employed in Private/ Public Institutions (which are not in approved list) provided such employees are having own residential building in Kerala.

7. Salaried employees includes Central/State Govt. and other approved Insitutions.

8. Identity – Professional – Copy of certificate issued by the concerned professional body – others : Election I.D. etc.

9. Age – repayment is to be limited to the date of retirement. In sthe case of professional upto 65 years.

10 Limit of advance –(a) 85% of the road cost (b) 30 times the combined net salary (c) Corresponding loan amount if 45% of the combined net salary is taken as available for remittance of EMI.

11.In the case of income tax assessees - (a) 1 ½ times of the average annual total income of the past 3 years based on IT return (b) corresponding loan amount if 25% of the average monthly total income is taken as available for remittance of EMI.

12.Fixation of instalment - as per EMI table13.Customers targeted under the scheme being from the elite group with

adequate repaying capacity, the vehicle purchased under this scheme is the prime security. No other collateral security is required provided the Unit Head should satisfy the repaying capacity and credit worthiness of the loan applicant. In addition the customer should give 5 undated singed account payee local cheques from his bank account, 4 cheques for quarterly EMI amounts and the 5th one without mentioning the amount. The drawees name “KSFE” in all five cheques and the amount in the first four cheques should be got filled by the loanee leaving the date on all the cheques and the amount in the 5th cheque unfilled

14.Pass Book of the related account should be verified and copy of the front page of the pass book should be attested . The signature of the drawer should also be verified

9

15.Lien should be noted in the R.C.Book. Duplicate key should also be collected and kept in safe custody. Copy of the relevant pages of the R.C. Book duly attested by the Unit Head, should be kept with the file.

16.Collateral security should not be insisted if the loanee is prepared to give LIC policy / Bank guarantee / FD receipts covering full amount.

17.Alternatively if the security offered is company FD, Double the amount of the FD can be sanctioned as loan subject to the condition that loan granted should not exceed 85% on the road cost of the vehicle. 18.In addition to the FD receipt, 5 post dated cheques should also be collected

as detailed above.19.Spouse should join in the agreement.20.Repayment period - Maximum 60 months – Minimum 6 months.21.Rate upto 35 months 14% - Exceeding 35 months 16% (Cir. 47/2011 dt. 6-8-11)22.Due date: Loan disbursed between 1st to 15th - 4th of subsequent month. 16th

to 31 - 21st of the subsequent month.23.Default interest 18% simple24.Monthly repayment – By EMI25. Procedure for submission and scrutiny of application, disbursement of loan

–same as in the case of CVL – However a separate form of Agreement has been designed for special car loan.

26.Agreement No. – CVL Agreement in chronological order can be assigned.27.A few pages may be set apart in the current personal ledger of CVL.28.Accounting -- same as CVL29.Delegation - Upto 5 lakhs – Manager - Above 5 lakhs - HO Business

through Regional Manager.30.Margin Money – Difference between on the road cost (Invoice price +

Registration charges + Insurance premium + Road Tax) and the loan amount.

31.Payment to the dealer – Through CVL Voucher – Cheques towards Insurance proposal to the Insurance Company.

32.Attested copy of insurance certificate is to be with us after verifying that the hypothecation in favour of KSFE is noted.

33.Lumpsum remittance is possible34.Premature closure is possible. If the premature closure is on the due date,

loan amount outstanding as per personal ledger is to be collected. If it is not due date next EMI instalment along with the principal outstanding after above EMI should be collected.

10

Reliable customer loan As on 9.10.09 (Cir.No.184/04.dt.18.12.04, 84/05 dt.2.6.05, 157/05 dt. 8.11.05, and 83/09 dt.7.10.09, 97/2009 dt.17.11.09. Effective from 18.11.09 and 47/2011 dt. 6-8-2011 w.e.f. 10-8-2011.1. a) Staff : 48months

b) Rate of interest : 13.5% (yearly dimi.) w.e.f.10-08-2011

c) penal interest : 18% simple d) Up to Rs25000/- : 36 months (For Public Cir. No.3/03 dt.2.1.03) e) Above Rs25000/- : 48months

f) Power delegated to sanction RCL (Cir.No.13/2012 dt. 29-3-2012)

UptoRs.200000/- : Manager UptoRs.400000/- : Regional Manager (on property security and

financial Documents Up to Rs.7,50,000/- : DGM (B & O) & GM (B) Above Rs.7.50 Lakhs : Board to Rs. 15.00 Lakhs 2. a) Estimated market Double the amount of Future liability(in the case Value of Property) b) F.D.Security : Equal amount of future liability

3.Loan for staff:Company employees need not remit registration fee. They can avail loan up to Rs.2,00,000/-or 10 times of net salary which ever is less under the RCL scheme on self-guarantee. They are allowed, concession of 3% in interest rate for a maximum loan of Rs.1,00,000/-

4. Number of loan, which can be availed under RCL:At a time there should be only one live RCL in the company in the name of a customer. (To ensure this the covering abstract should be sent to H.O and Clearance obtained before releasing the loan).

5. There are no separate security norms for RCL. The various types of Security norms given under the chitty scheme are applicable for RCL also.

Gold loan and gold security scheme –At a glance- Different rates of interest etc. as on 18.11.09(Cir No.97/09 dt.17.11.09 w.e.f. 18.11.09 48/09 dt.20.06.09 83/09 dt.07.10.09, 47/2011 dt. 6-8-2011, 11/2012 dt. 13/03/2012

I). Gold Loan Schemea. Up to and including 10,000 : 12% simpleb. Above Rs. 10,000 and Up to & including Rs.25,00,000 : 14% simplec. Penal interest on default interest should be remitted every month, if not remitted, penal

interest @ 2% per month on interest.d. A minimum interest of Rs.25/- should be charged for all gold loans over Rs. 5000/-e. The total advances made in one day (to particular customer from a branch) would be

aggregated for the fixation of applicable rate of interest and recovery of minimum charges.

f. The No. of advances that could be given to a particular person in a working day from a branch should not exceed 3 in the ordinary course. If more than 3 advances has to be given to a particular person in a working day from a branch, the same should be with the

11

specific approval of the branch manager concerned Cir. No.85/2008 dt.27.8.08, 48/2009 dt. 20.6.2009

g. Maximum gold loan admissible: 25 lakhs(at a time in one account)h. Maximum amount that can be secured under gold security: no ceilingi. Loan exceeding Rs. 3 Lakhs upto Rs. 10 Lakhs will have to approved by the Branch

Manager. Loan above Rs. 10 Lakhs will have to approved by AGM (Region) after 2nd

appraisal.

2) Admissible amount per gram(Cir. No. 66/2012 BD dt. 23-11-2012) purity Gold loan & Gold security

18 carat 1850 19 caret and above 2250

19 caret and above (special cases) 2350(Special cases include reliable and reputed customers assessed by Unit Head as well as jewellary bearing BIS hallmark symbol having purity of 19 carats and above. The gold loan advances sanctioned under special cases should be invariably be at the discretion of Unit Heads. (Cir. no.66/2012 dt.23-11-2012 effective from 26-11-2012)

3) It should be ensured that the advance + interest in any Gold Loan/Gold security account, at any point of time should not exceed 85% of the prevailing market value. If so, immediate action should be initiated to realize the dues through auction sale. Advance portion should not exceed 82% of the market value.

4) (A) Gold loan-maximum period to which loanee can maintain his account alive will be 6 months with facility to renew another six months after remitting interest on loan. (Cir. No. 48/2009 dt. 20-06-2009)

4. (B) Loan amount may be disbursed in cash upto Rs. 3 lakhs only. For advance amount higher than Rs. 3 lakhs only cheque payment or payment through RTGS is allowed. Payments partly in cash or partly in cheque are not allowed.

4. (C) The changes in interest vide Cir. No. 47/2011 will be applicable to Company employees also. However they will get regular concession at the rate of 2.5% for a loan amount upto Rs. 50,000/-.

5) Appraiser charges and other charges

Gold loan gold securitya) Appraiser charges at the 0.2% of the loan 0.2% of the amount time of pledging gold amount subject to to be secured subject Maximum Rs.100/- to maximumRs.100

b) Partial redemption of 0.1% of the redeemed principal 0.1% of the redeemed the pledged gold ornaments subject to maximum Rs.50 principal subject to Under gold loan maximum Rs50/- Scheme/gold security

c) Availing addl.loan 0.2% of the addl.loan 0.2 of the addl. liabilityunder gold loan scheme/ sanctioned subject to to be charged subject toadditional liability under G.S maximum Rs.100/- maximum Rs.100/-

12

d) Loan above Rs. 10 Lakhs should be appraised by 2nd appraiser. Additional Appraisor charges at the present rate 2% subject to maximum Rs. 100/- + Rs. 50/- towards TA may be paid to the 2nd

appraiser.

e) Auction sale of pledged expenses actually incurred Rs.125 per auctiongold ornaments is to be deducted from the Auction proceeds

Note:-Payment of appraiser charge and limits thereof:-Under both schemes (Gold loan and gold security) appraiser charge is to be paid at a uniform rate of 0.2% of the loan amount / amount secured / released / exchanged subject to a maximum of Rs.100/- per case.

The maximum limit of monthly appraiser charges that can be paid to an appraiser (inclusive of transfer to Sugama) is Rs.15000/- (vide circular No. 72/2009 dt. 7.9.2009). This ceiling of Rs.15000/- envisaged is including appraiser charges due on appraisal of gold ornaments accepted as security also. This limit of Rs. 15000/- need not be considered for 2nd appraiser. The limit of amount to be transferred monthly to sugama is Rs. 10% of the appraiser charge collected under both scheme subject to a maximum of Rs. 1500/-. The monthly amount exceeding Rs.15000/- is to be transferred to General Fund kept in R.O. Consequent to the amendment, the maximum monthly limit of amount that can be drawn an appraiser as appraiser charge after crediting 10% in sugama account is Rs. 13500/-.6) Partial redemption of pledged gold ornaments under gold security/gold loanFacility for partial redemption of pledged gold ornaments available under gold security scheme is also extended to gold loan scheme on repayment of proportionate loan amount along with the accrued interest on the entire loan till the date of partial redemption. Under both scheme those who remit 25% or more of the original loan outstanding /original amount secured along with accrued interest on the entire loan till the date, are eligible for partial redemption of pledged gold ornaments and this facility is limited to maximum of four times.

7) Facility for availing additional gold loan /securing additional liability Circular No.126/2004dt.21.8.04

a) 2 nd and subsequent charges in the original branch /primary branch Additional loan on the gold pledged /creation of additional charge on gold security (unencumbered portion) can be allowed in accordance with the value fixed on gold under pledge; provided, such accounts are to be properly linked.

b) In other branches In the case of gold security additional charge to another branch can be created in accordance with the value fixed on gold under pledge limiting such charges to two times. Such accounts shall be properly linked.

Extract of circular nos.36/08 dt.1.4.08 and circular no.65/08 dt.23.6.08:1. Enhancement of fidelity cover:- The minimum fidelity insurance guarantee limit of gold appraiser is enhanced to Rs.50,000/-from the existing limit of Rs 5,000/- or equivalent security deposit /fixed deposit or any other financial security in the name of appraiser based on the following business level

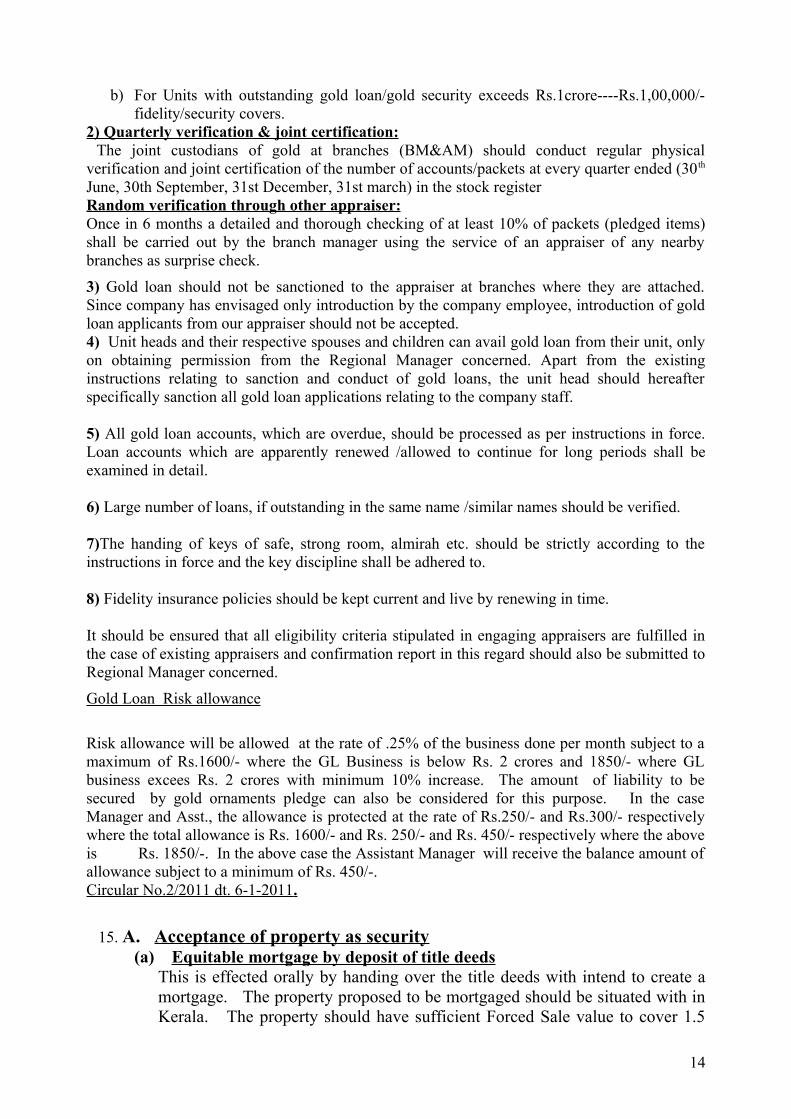

a) For Units with outstanding gold loan/gold security less than Rs.1crore --- Rs, 50,000/- fidelity/security cover.

13

b) For Units with outstanding gold loan/gold security exceeds Rs.1crore----Rs.1,00,000/-fidelity/security covers.

2) Quarterly verification & joint certification: The joint custodians of gold at branches (BM&AM) should conduct regular physical verification and joint certification of the number of accounts/packets at every quarter ended (30th

June, 30th September, 31st December, 31st march) in the stock registerRandom verification through other appraiser:Once in 6 months a detailed and thorough checking of at least 10% of packets (pledged items) shall be carried out by the branch manager using the service of an appraiser of any nearby branches as surprise check.

3) Gold loan should not be sanctioned to the appraiser at branches where they are attached. Since company has envisaged only introduction by the company employee, introduction of gold loan applicants from our appraiser should not be accepted.4) Unit heads and their respective spouses and children can avail gold loan from their unit, only on obtaining permission from the Regional Manager concerned. Apart from the existing instructions relating to sanction and conduct of gold loans, the unit head should hereafter specifically sanction all gold loan applications relating to the company staff.

5) All gold loan accounts, which are overdue, should be processed as per instructions in force. Loan accounts which are apparently renewed /allowed to continue for long periods shall be examined in detail.

6) Large number of loans, if outstanding in the same name /similar names should be verified.

7)The handing of keys of safe, strong room, almirah etc. should be strictly according to the instructions in force and the key discipline shall be adhered to.

8) Fidelity insurance policies should be kept current and live by renewing in time.

It should be ensured that all eligibility criteria stipulated in engaging appraisers are fulfilled in the case of existing appraisers and confirmation report in this regard should also be submitted to Regional Manager concerned.

Gold Loan Risk allowance

Risk allowance will be allowed at the rate of .25% of the business done per month subject to a maximum of Rs.1600/- where the GL Business is below Rs. 2 crores and 1850/- where GL business excees Rs. 2 crores with minimum 10% increase. The amount of liability to be secured by gold ornaments pledge can also be considered for this purpose. In the case Manager and Asst., the allowance is protected at the rate of Rs.250/- and Rs.300/- respectively where the total allowance is Rs. 1600/- and Rs. 250/- and Rs. 450/- respectively where the above is Rs. 1850/-. In the above case the Assistant Manager will receive the balance amount of allowance subject to a minimum of Rs. 450/-.Circular No.2/2011 dt. 6-1-2011 .

15. A. Acceptance of property as security(a) Equitable mortgage by deposit of title deeds

This is effected orally by handing over the title deeds with intend to create a mortgage. The property proposed to be mortgaged should be situated with in Kerala. The property should have sufficient Forced Sale value to cover 1.5

14

time of the future liability in the prized chitty. The Forces Sale Value is 75% of the estimated market value. The property offered may be in the name of the subscriber or any other person. The property can be accepted as security only if the first charge thereon is in favour of the Company. For this purpose, an application in Form prop.1 along with the relevant title deeds and an affidavit in Form prop 2 should be obtained. The affidavit should be duly attested by an advocate in stamp paper worth Rs.25/-. If the subscriber himself is not the mortgagor of the property, the application in Form prop.1 should be signed by the subscriber as well as by the mortgagor. The important points to be noted while accepting immovable property as security are as follows:

(i) All original documents pertaining to the property proposed to be mortgaged as security including prior documents should invariably be produced along with the application. However, if prime document is more than 13 years old, production of prior documents in original can be dispensed with provided a photocopy of the prior document or registration copy is produced. If prime document is less than 13 years old, all the original prior documents executed during the last 13 years and immediate prior deed shall invariably be insisted upon either for keeping in custody or for perusal and recording its production if other properties are also involved in such prior documents.

(ii) In case of patta issued under the Kerala Land Assignment Act and the Rules made there under, the order of assignment on registry should also be got produced besides the original patta and scrutinized to see whether there is any condition restricting any alienation etc.

(iii) In the case of patta issued under the Kerala Land Ceiling Rules, it should be ensured that the Rules governing restriction of alienation are not violated.

(iv) In case where purchase certificate issued under KLR Act is alone produced by way of title deed, document relating to assignment of verumpattom right to the holder should be obtained besides the purchase certificate. In case of verumpattom assignment is claimed to have been orally made, the following precautions must be taken.The applicant should produce certified copy of the proceedings leading to the issue of purchase certificate.The party must swear to an affidavit stating that he has got exclusive right over the property involved in such purchase certificate.

(v) If the property was encumbered by way of a registered mortgage, registered release deed discharging the liability should be obtained.

(vi) Property in which any minor has got interest will not be accepted as security.

(vii) In case the executants of the assignment deed in favour of the applicant is a Power of Attorney holder, then verify:a) Whether the Power of Attorney is registered.b) Whether the principal has given specific authority to assign the

property.

15

Ordinarily, registered Power of Attorney (in specific) alone can be approved of. If the Power of Attorney is not one given for consideration, it should be confirmed from the principal that it is not revoked. If the Power of Attorney received from foreign countries attested by embassy officials are not in stamp paper, the same shall be got impounded by the concerned district authorities.

(i) If the party is offering property covered by a partition deed, the party should be directed to produce the original partition deed for depositing with us.

(ii) If the original partition deed is in the possession of one share holder who keeps the same for the benefit of other share holders also, then the person depositing the same should get consent from the other share holders. Such consent must be in writing, attested by a Notary public.

(iii) If the party is producing the duplicate copy of the partition deed, it has to be ensured by referring to the endorsement made in the stamp paper purchased for the duplicate copy that the duplicate is actually set apart to him and handed over to him at the time of execution of original partition.

(iv) In case the applicant obtained the property under a WILL, death certificate of the testator shall be obtained.

(v) If the property offered by the applicant is devolved on him on the death of his predecessor, it should be ascertained whether there is any other heir who is also entitled to the property, by causing production of a heir ship certificate.

(vi) The production of Thandaper account along with the application for acceptance of property security shall not be insisted upon.

(vii) To insist on ‘Non-kudikidappu Certificate’ from the village office in respect of landed property below 5 cents in rural areas and 3 cents in corporations/ Municipalities in case of future liabilities in chitties.

(viii) In respect of all loans to insist on personal surety of one individual in addition to landed property below 5 cents irrespective of the locality wherein it lies. This is in addition to the ‘Non-kudikidappu Certificate’ from the village office.

(i) Work at the BranchOn receipt of the property document noted above the branch should verify the adequacy of the title of the property and if find acceptable photocopy of the entire documents should be forwarded to Panel Advocate attached to the branch for his opinion on the adequacy of title of the property to the mortgagor. The originals of the documents should be retained with the branch for safe custody. The panel Advocate should scrutinise the documents meticulously and tender his definite opinion regarding title of the property. If, during the course of scrutiny, the Advocates feel that any additional documents /records are required to establish the title, he should inform the Manager of the same and the Manager will, in turn, collect the same from the party. The panel Advocates are expected to be present in the Branch Office for the scrutiny of the property documents. If the documents are found acceptable as per the opinion of the panel Advocate, arrangements have to be made for the valuation of the property as per the procedure prescribed. If the

16

documents are not found acceptable, the same can be rejected at branch level. Further, if the additional documents required to be produced for establishing the title over the property are not produced the application is liable for rejection at branch level. The Managers are also free to express dissent , if any, on the opinion tendered by the panel Advocate in the above matters subject of course that such dissents are substantiated with reasons. However the property documents based on the opinion of the panel Advocate found acceptable to the Unit Head and the liability upto Rs. 10 lakhs, the Unit Head can accept the same. If the liability exceeds Rs.10 lakhs the entire documents received and scrutinized at branch level may be forwarded to the Regional Office with recommendations/remarks of the Unit Head along with the scrutiny note in the prescribed form, report of panel Advocates and committee valuation report etc. for the decision/sanction of the Regional Manager. Valuation of the property where the liability ranges up to Rs. 2 lakhs, is to be done as per the procedure prescribed (Branch Manager). For liabilitiy above 2 lakhs to 5 lakhs Branch Manager and an independent approved valuer. If the property is not within a radius of 15 kms.the Manager in whose juridiction the property is located should value the property (Nearest Manager). For the liability above Rs. 5 lakhs Committee comprising 2 officers of the Comapany and an approved valuer. Manager where the chitty has been floated and the 2nd Manager will be of the Branch or Regional Office under whose jurisdiction the property is located. The 2nd Officer of the Committee will be decided by the R.O. concerned. With the introduction of the Committee, approach for the valuation of properties offered as security of above 2 lakhs, and the existing requirement of double valuation in cases of liabilities exceeding Rs. 5 lakhs are discontinued. The committee should arrive its decisions through consensus. In cases where the liability exceeds Rs.200000/- but does not exceeds 500000/-, the Manager of the Branch can arrange such valuation without seeking the sanction from the R.O. If the liability exceeds Rs.500000/-, the Manager of the Branch where the chitty was floted should intimate that fact to the Regional Office for arranging the 2nd Officer for valuation.

(ii) Work at the Regional Office levelA legal cell in the Regional Office will scrutinize the documents, panel Advocates’ opinion, valuation reports etc. received from the branches and record the result of their scrutiny in the space provided in the scrutiny report form. A legal cell consisting of Senior Manager (Business) and two or more staff trained in the matter of scrutiny of property security documents will be constituted in the Regional Office for processing the security documents received from the units. The file should then be submitted to the Regional Manager for his decision/ sanction. The opinion of the PTLA will also be obtained by the Legal Cell/Regional Manager.

17

If the future liability is Rs. 15 lakhs or below such files can be sanctioned by the Senior Manager of Business of the R.O. concerned. If it exceeds Rs. 15 lakhs file should definitely be passed by the AGM (Region).

The decision/sanction of the AGM should then be communicated to the Branch. The sanction order from the Regional Office should necessarily contain the value of the property accepted by the AGM and the details of committee valuation. If the liability is not within his limit, he will forward the same to the appropriate authority with his comments/recommendations. On receiving the sanction order from the Regional Office, the Branch should arrange for getting equitable/registered Mortgage executed in favour of the Company in strict compliance of the directions in the sanction order of Regional Office. The Branch should also arrange to obtain E.C. covering the date of execution of mortgage and other documents required to be produced.

(iii) General instructions for acceptance of property as security 1. Second and subsequent charges over the property already under

mortgage to the Company.

The powers to accept the property already under mortgage to the company, for second and subsequent time is delegated to the branch Managers subject to the following terms and conditions.

a. The aggregate liability for which property is accepted as security should be with in the norms/rules prescribed by the Company and the same should not exceed the limit for which the valuation adopted by the AGM.

b. The number of additional charges should be limited strictly in accordance with the instructions i.e., four charges including the 1st equitable mortgage.

c) Revaluation of the property already under mortgage to company should be made only after obtaining written sanction from the Regional Office. Unless 3 years are elapsed after the first valuation, revaluation will be permitted only in the following circumstances.

(i) Improvements/additional construction in the property which will add the value of the property.

(ii) A total development of the area due to additional infrastructure facilities.

(iii) Revaluation report should be forwarded to AGM and his acceptance of the report obtained before reckoning the value for the purpose of security.

d) If the total liability exceeds Rs.10 lakhs the second/additional charge created at the Branch level should be intimated to the AGM for necessary recording in the original file.

e) While creating second/additional charge, an up to date encumbrance certificate in respect of the property including the date on which additional charge is created, should be obtained, along with up to date land/building tax receipt, application, affidavit etc. Possession certificate need not be insisted upon while creating the second and subsequent charges.

18

f) It should be specifically ensured that the subscribers/loanees should not have any defaults/overdue in the Chitties/Loan accounts for which property is already under mortgage.

2. Protection of women from domestic Violence Act 2005 – Legal impact to be considered when property is accepted as securityOn 20th October 2006, protection of women from Domestic violence Act 2005 came in to force in our country. As per the provision of the Act, the wife has got residential right in the housing property of the husband. Even as per 8,89 of Transfer of Property Act, there is such a right available to the wife and these provisions will have serious legal impact as far as acceptance of property security and creation of mortgages are concerned. Considering the legal aspect of the above while the property belonging to the husband is being accepted as security for the chitty prize money and for all types of loans, wife should be invariably be made a party to the mortgage. Hence, when landed properties are accepted as security, mortgagor’s wife has invariably to be made a party to the mortgage hereafter. It is further clarified that in the case of purchase of residential buildings, flats etc. by the husband under the Housing finance scheme spouse should also be made a party to the legal agreement and mortgage proceedings. In the light of the above following amendments to the procedure may be ensured.

i) Wife should also sign the document register along with the husband, mortgagor.

ii) Prop.2 shall be a joint affidavit.iii) Wife should also sign in the Prop 5 along with the husband, mortgagor.

3. Valuation of the property and other related instructions ::(i) Valuation of the property in cases where the liability ranges up to Rs.2 lakhs is

to be done as per procedure in vogue( Branch Manager). For liability from Rs. 2,00,001 to 5 lakhs Branch Manager and an independent approved valuer. If the property is not within a radius of 15 Kms, the Manager in whose jurisdiction the property is located should value the property (Nearest Manager). Liability above Rs.5 lakhs Committee comprising 2 officers of the Company and an approved valuer. Manager where the chitty has been floated and the 2nd Manager will be of the Branch or Regional Office under whose jurisdiction the property is located. The second officer of the committee will be decided by the R.O. concerned. With the introduction of the committee, approach for the valuation of properties offered as security of above 2 lakhs, the existing requirement of double valuation in cases of liabilities exceeding Rs.5 lakhs are discontinued. The committee should arrive its decisions through consensus. Additional fee to be collected for approved valuer up to a value of Rs.5 lakhs is Rs.500/- and above Rs. 5 lakhs is Rs.750/-. Maximum liability that can be secured by single property for an individual or a proprietor is limited to Rs.1.50 crore. Maximum liability that can be considered for a firm or corporate body is Rs.2 crores. This should be done with utmost discretion. 75% can be considered as forced sale value. Forced Sale Value should be

19

atleast 150% of the future liability. Valuation report should be submitted with in 7 days. (ii) The valuation report should be prepared in the prescribed form.(iii) In case of dispute in the value of the property offered as security for liability in

chitties, it shall be referred to Registrar for arbitration under section 64 of the Chit Fund Act 1982

4. Creation of additional charge on the property The Company will not accept landed property as security by way of additional

charge for the liability of a person other than the subscribers and the mortgagors in the 1st mortgage. However, acceptance of property as additional charge for liabilities of persons standing in fiduciary relation (i.e. father and son/daughter, Brothers, Sisters, Son-in-laws, Daughter-in-laws etc.) to the mortgagor can be considered on merit of each case by the AGM provided a Registered Mortgage is prepared to be created.

5. Acceptance of Company’s property, Cardamom Estate, Rubber, Coffee, tea, coconut plantations, paddy fields

(i) Not to accept the properties belonging to Companies as securities. (This provision has been relaxed subsequently which can be seen as separate clause)

(ii) Not to accept Cardamom estate as security.(iii) The maximum Estimated Market Value of Rubber/Coffee/Tea/Coconut

plantations should be below Rs.2.25 lakhs per acre provided there is direct access to the security property through a tar road. (Coconut plantations are to be valued according to the yield and health of the trees).

(iv) Paddy fields (wetlands) having road access, tractorable and two crop (irrippu) will fetch a maximum Estimated Market Value of Rs.1 lakh per acre. Managers should avoid accepting paddy fields other than referred above as security

(v) Managers should forward the files in respect of additional charges on properties already under mortgage to Company for the sanction of the AGM in the case of plantations mentioned above.

6. Production of Land acquisition certificate

The loanee/subscriber/mortgagor should be insisted to produce ‘Land acquisition non-proceding certificate’ from the village office. A separate certificate need not be insisted upon if the same information is included in any other certificate, like Possession & Enjoyment Certificate , location Certificate and Location sketch etc.

7. Formalities to be observed at the time of creation of equitable mortgage by deposit of title deeds

(i) The creation of equitable mortgage takes place when the mortgagor calls at our office and formally hands over the document to the Manager/Officer in charge of the office in the absence of Manager with the intention of creating the mortgage. After accepting the property as security, the mortgagor should be insisted to be present in the office on a specific day for creation of equitable mortgage for which a communication is to be sent. As an evidence of the mortgagor’s presence in our office and with a view to avert a possible plea of

20

alibi, the mortgagor shall be required to affix his signature in the document register of the Branch amidst the usual entries therein for the day on which he was present in the office. The document register of the Branch shall have to be maintained up to date at all times so that the mortgagor’s signature can be obtained amidst various entries in the chronological order in the register. The signature in the document register shall be obtained after the following endorsement, disregarding the boundaries of various columns in the register.

(ii) Endorsement to be made in the document register at the time of equitable mortgage“I /we have deposited today the original documents No.(…….….) in respect of landed property of ……………………cents with all improvements therein comprised in Sy.No ……..…of ………………..Village…………….……Taluk with intent to create a mortgage by deposit of title deeds for the liability of Rs……in ……held by me/ ………in …………branch of K.S.F.E.Ltd.”

(Signature of the Mortgagor with date)

This endorsement has to be made in the document register of the Branch in which the equitable mortgage is created even in cases of mortgage for the liability to the branches situated in un-notified areas. Company had, vide Circular 70/2010(BD) dt. 28-12-2010 conveyed the G.O. (P) NO. 252/2010/TD dt. 02-11-2010 which had made necessary changes under section 58 (f) of the TP Act 1882 making all Panchayaths, Municipalities and Corporations in the State of Kerala as notified area. The endorsement in the Document Register in the case of letter of continuities shall be in the following lines:

(iii) Endorsement to be made in the Document Register in the case of letter of continuities“You may continue to hold the property documents already deposited by me/us on ……….……as security for additional liability of Rs……..…in……………held by ……….…..in…………….……….Branch.

(Signature of the Mortgagor/s with date)

Before execution of the mortgage as above, the branch has to confirm the identity of the mortgagor so as to avoid impersonation of the mortgagor. After acceptance of the property as security, the mortgagor should be intimated by Registered post with A/D to be present in the branch where the mortgage is to be created.

8. Effecting of payment in cases where equitable mortgage is madePayment can be effected on or after the date on which the statement is recorded in the register in Form prop.4 by the Manager and Assistant Manager/Deputy Manager and after obtaining EC covering the date on which the mortgagor called at the branch office and signed the endorsement in the document register as explained above. Form prop 4 is the register of Memorandum of title deeds deposited by the mortgagor(s) with intent to create equitable mortgage/letter of continuity. The register is designed with a view

21

to accommodate letter of continuity created on the same property on future dates. The columns in the register are self explanatory leaving no room for any doubt regarding recording of the mortgages. It should be specifically noted that the recording of Memorandum of title deeds deposit has to be made on the date subsequent to mortgagors presence in the office and signing the endorsement in the document register. A letter of admission of the mortgage in Form prop.5 should also be obtained on the date on which the Memorandum of deposit of title deed is recorded in the register in Form prop.4, by the Manager of the Branch where the liability exists. This letter shall be submitted in duplicate, a copy of which is to be given back to the subscriber duly acknowledging the deposit of documents.

In the register separate space is provided for entering the particulars of liabilities for which additional charges on property are created by way of letters of continuity. Entries in this space have to be made as and when letters of continuity are created as per the procedure/norms in vogue. This will facilitate easy verification and confirmation of the number of times letters of continuity have been created and the particulars of liabilities for which they are in existence etc. the endorsement in respect of a letter of continuity shall be in the following lines.

“Letter of continuity No……………. dated……………..liability of Rs…………… towards chitty/CVL/NCL No………… held by ……………………………………….”

Assistant Manager/ Deputy Manager. Manager

9. Limiting the No. of parties in first mortgageLimiting the number of parties in the 1st mortgage: Under the present procedure the liability of any number of subscribers/loanees can be charged on a single property while creating equitable mortgage subject of course to the limits prescribed for charging each item of liability. Statistics reveal that the incidence of default and problems of proceeding against the security property is more in cases of group financing than in the case of single advances. It is therefore decided to limit the number of subscribers/loanees who can join in the equitable mortgage to a maximum of four including the mortgagor. But, at the interest of customer satisfaction spouse’s liability can be allowed to be charged as letter of continuity instead of the present practice of insisting registered mortgage when she/he is not a party in the equitable mortgage, subject of course to the condition that the maximum number of charges that can be created on a property continues to be four including the equitable mortgage.

10. When the party offers settlement deedIf the party is offering settlement deed we have to verify whether any life interest has been created (Life interest means interest in the property which

22

determines on the termination of life. Eg. Right to live in the building of the property till death). While creating mortgage, the persons having life interest should also join the mortgage.

11. When the party offers partition deedWe have to ensure the following while accepting the partition deed.

(i) If the party is offering property covered by a partition deed, the party should be directed to produce the original partition deed for depositing with us.

(ii) If the original partition deed is in the possession of one share holder who keeps the same for the benefit of other share holders also, then the person depositing the same should get consent from the other share holders. Such consent must be in writing, attested by a Notary public.

12. When the party offers duplicate copy of Regd. deed along with partition deedIf the party is producing the duplicate copy registered along with the partition deed, it has to be ensured by referring to the endorsement made therein the stamp paper purchased for the duplicate copy that the duplicate is actually set apart to him and handed over to him at the time of execution of original partition. There may be cases where a particular sharer to whom a particular property is set apart in the partition deed , will be required to oblige certain condition. In such cases a release deed discharging such obligation should be ensured.

13. While accepting the WILL Usually partition occurs when the title holder dies intestate. While accepting the “WILL” the following precautions have to be taken.

(i) Cause production of death certificate of the testator unless the “WILL” is probated. However probate of Will is run away with from 14-03-1997

(ii) A declaration (in stamp paper of Rs.25/- attested by an advocate) shall be obtained from all the heirs to the effect that they approve of the “WILL” and have no objection what so ever with regard to the genuineness of the “WILL” .

14. Purchase Certificate/ Kraya Certificate If the property is held on ‘verum pattam’ tenure then in order to perfect his

title, the holder has to obtain a purchase certificate issued by the land tribunal. As per the Land Reforms Act the Jenmam right of such properties as held on ‘verum pattam’ tenure got vested with the government and it is that right which is being purchased by the holder after paying the appropriate price to the government. In cases where purchase certificate issued under K.L.R.Act is alone produced by way of title deed, document relating to assignment verum pattam right to the holder should be obtained besides the purchase certificate. In case the verum pattam assignment is claimed to have been orally made, the following precaution must be taken.

(i) The applicant should produce certified copy of the proceedings leading to the issue of purchase certificate.

23

(ii) The party must swear to an affidavit stating that he has got exclusive right over the property involved in such purchase certificate.

15. If the property was encumbered by way of Regd. Mortgage If the property was encumbered by way of a registered mortgage, registered release deed discharging the liability should be obtained. In appropriate case registered receipt can also be entertained.

16. In the case of executant of the assignment deed in favour of the applicant is a power of attorney holder.In case the executant of the assignment deed in favour of the applicant is a Power of Attorney holder, then verify.

(i) whether the Power of Attorney is registered(ii) whether the principal has given specific authority to assign the property.Ordinarily registered Power of Attorney (in specific) alone can be approved of. However in exceptional cases Power of Attorney executed specifically for executing mortgage in K.S.F.E and attested by a Notary public duly confirmed shall also be considered. If the Power of Attorney is not one given for consideration. It should be confirmed from the principal that it is not revoked. If the Power of Attorney received from foreign countries attested by embassy officials are not in stamp paper the same shall be got impounded by the concerned district authorities.

17. If the property offered by the applicant is devolved on him on the death of his predecessorIf the property offered by the applicant is devolved on him on the death of his predecessor, it should be ascertained whether there is any other heir who is also entitled to the property, by causing production of a heir ship certificate.For ascertaining the clear and marketable title of the property, we have to verify the revenue records and the encumbrance certificate. Along with the property documents, we used to obtain following revenue records from the parties.

(i) Possession Certificate(ii) Basic tax receipt(iii) Location certificate(iv) Location Sketch

18. Discrepancy in the Sy. No. of the property & accessibility to the property is through another person’s property.Generally survey number of the property as well as the extent shown in the revenue records should tally with the survey number and extent of the property in the schedule of property documents. If any discrepancy in the same is seen, a clarification shall be obtained from the village office. If the property security is comprised of building then we may also obtain Building Tax receipt. The accessibility of the property can be under stood from the Location Sketch and certificate. Incidentally it is pointed out that if the accessibility to the property is through another person’s property either the

24

said property shall be mortgaged to the Company or registered right along with demarcated sketch of the pathway from V.O. shall be obtained from the party for considering acceptance of security. Each case of discrepancy have to be dealt with in its own facts and circumstances.

19. Tenure of the propertyThe tenure means the mode or system or the action or fact of holding land or tenements. In all the property documents, a column is provided for tenure of property. The tenure can be Jenmam, Kanam, Pandaravaha, and Verumpattom. The purchase certificate is needed only for verumpattom property as the Jenmam right is vested with the government by virtue of S.72 of Kerala Land Reforms Act. Ownership of a verumpattom property has two components.

(i) verumpattom right(ii) Jenmam rightSince Jenmam right is vested with government as aforementioned, it has to be purchased from the government in order to make the title absolute. The Jenmam right is so purchased from the government is evidenced in the purchase certificate issued by the Land Tribunal. For all practical purpose persons holding Kanam and pandaravaha property can be considered to have absolute title to the property.

Rented out building (i) If the entire area of land offered as security is occupied by the building which

has been rented out, such property is not normally acceptable. However, if the rent of the let out building is substantial to cover the monthly instalment and interest in the case of Chitty loan, the R.M. may at his discretion consider accepting the property as security after obtaining Power of Attorney from the Land lord (Mortgagor) and consent from the Tenants subject of course to the condition that the value of the rented out buildings shall not be assessed at par with similar buildings occupied by owners themselves.

(ii) If only a portion of the land offered as security is occupied by the building, such property can be accepted based on the value of the remaining part of the land subject to satisfying the condition of free and fair accessibility to the property from the Public Road.

20. Property valuation Fee and Fee Payable to Panel Advocate.Property valuation Fee must be collected in all cases except NHFS. Valuation fee to be collected from customers is 1% of the chitty sala / loan amount, subject to a minimum of Rs.350/- and a maximum of Rs.1350/- Fee payable to the panel Advocate is Rs.350/- per file(Cir.No.42/2010(B) dt. 20-8-10). Additional fee to be collected for approved valuer in cases where value of the property exceeds Rs.2,00,000/- up to Rs.5,00,000/- is Rs.500/- Above Rs.5,00,000/- is Rs.750/- Documentation charges to be collected is 0.20% of the sala subject to minimum Rs.50/-, and maximum Rs.200/- Points to be noted.

25

(i) Identification of the property with boundaries.(ii) The extent of property whether it is wet land or garden land or building

site, survey number, boundaries, village, taluk and district.(iii) Improvements in the property.:

(a) Nature of improvements such as fruit bearing trees, timber trees, the age of fruit bearing trees etc.

(b) The annual gross income and the net income.(c) In the case of buildings, the building number, the plinth area, whether

it has concrete roofing or tiled roofing, the quality and quantity of timber used, the approximate age of the building, the depreciation to be allowed, the rent it may fetch, and also the approximate value of the building, whether it is residential if so, whether occupied by the owner, if let out what is the rent.

(iv) The location of the property and accessibility whether it faces any public road, the importance of the locality, if situated by a lane whether vehicles will pass through the lane.

(v) The present Estimated Market Value of the building showing separately the site value.

(vi) Recent sales, if any, of adjacent properties.(vii) The minimum price it may fetch as Estimated Market Value.(viii)Any other relevant fact/ information about the property valued, which is

likely to be useful for arriving at a decision regarding the value of the property, should also be furnished.

21. Modified property circular (at a Glance) Cir.No.95/07 & 103/07, 76/08 As on 1.2.2009

(i) Valuation of the property in cases where the liability ranges up to Rs.2 lakhs is to be done as per procedure in vogue (by Branch Manager)

(ii) Liability from Rs.2,00,001 to 5 lakhs- Branch Manager and an independent approved valuer. If the property is not within a radius of 15 kms., the manager in whose jurisdiction the property is located should value the property (ie. Nearest Manager)

(iii) Liability above Rs.5 lakhs, committee comprising 2 Officers of the Company and an approved valuer. Manager where the chitty has been floated and the 2nd Manager will be of the Branch or Regional Office under whose jurisdiction the property is located. The 2nd Officer of the Committee will be decided by the R.O. concerned.

(iv) With the introduction of the Committee, approach for the valuation of properties offered as security of above 2 lakhs and the existing requirement of double valuation in cases of liabilities exceeding Rs.5 lakhs are discontinued.

(v) The committee should arrive its decisions consensus(vi) Additional Fee to be collected for approved valuer.

a) If the value of the property is up to Rs.5 lakhs - Rs.500/- b) If the value of the property is above Rs.5 lakhs - Rs.750/-

(vii) Maximum liability that can be secured by a single property for an individual or a proprietor is limited to Rs.1.50 crore.

26

(viii) Maximum liability that can be secured by a Firm or Corporate Body Rs.2 Crore

(ix) Maximum liability admissible in the case of properties used for industrial purposes and where there are chances of labour related issues (This should be done with utmost care) Rs. 15 Lakhs

(x) 75% of the market value can be considered as Forced Sale Value and the Forced Sale Value should be atleast 150% of the future liability for security purpose.

(xi) valuation report should be submitted within 7 days.

Initial property valuation fee and fee payable to Advocatea) Valuation fee to be collected from customers : 1% of the chitty sala/loan

amount subject to a minimum of Rs.350/- and maximum of Rs.1350/- (Rs.750+600)

b) Fee payable to Advocate : Rs.350/- (Per file)(Cir. No. 42/2010 BD dt. 20.8.2010)

Estimated Market Value of the property required for each schemes1. Chitty & NCL : Forced Sale Value should be atleast150%

of the future liability2. Consumer/Vehicle Loan : Amount equal to advance plus interest as

per repayment schedule3. T.F.S : 2 times of the future liability4. R.C.L : 2 times of the future liability 5. NHFS ,HMS : 1.3 times of the loan amount

1. Personal Surety Norms A prized subscriber/Loanee may offer personal sureties as security for the payment of future instalments. The personal sureties offered should have the required salary/gross taxable income as specified in the norms.

General conditions 1. Persons acceptable as sureties/guarantors to our various schemes.

The Company accepts the following persons as sureties /guarantors to our schemes:

(i) Employees of Central/State Governments/ Quasi-Government

(iii) Employees of Central/State Government Undertakings.

(iv) Employees of Government and Aided Schools, Plus Two Schools and Colleges and other institutions approved for the purpose including reputed Companies/ firms and scheduled Banks.

(v) Employees of Local Bodies.

27

(vi) Employees of certain Co-operative Institutions according to their “Financial `classification/ gradation” i.e. Class II and above (as detailed in Cir.No.39/99 dt.16.03.1999)

2. Persons accepted as sureties should be :

(i) Residents of and working in Kerala State.

(ii) They should be permanent/officiating full time employees.

(iii) They should not be defaulters in any of our schemes in the capacity of principal debtor or surety/guarantor, in any of our branches.

(iv) They should have at least six months service left for retirement after

termination of the chitty/advance agreement (there are exceptions)

3. Classification of employees :- Employees in whose case salary recovery can be effected towards our schemes are categorized as Salary Recovery Enforceable Group (SREG) and others as Salary Recovery Non-Enforceable Group (SRNEG)

4. Number of sureties/guarantors permitted :- Except under self/single, surety/ guarantor norms, generally, not less than two sureties and not more than 5 sureties will be accepted as security. In these cases the requirement of 6 months service after termination of the chitty is not compulsory in respect of 2 sureties) Salary includes Basic Pay + DA + PP + IR, if any. Minimum take home pay should be Rs. 5000/-.

5. Maximum recovery from salary (including loan instalment) should not exceed 60%of the gross salary. The net pay and the subscriber/surety to be linked with gross instalment of chitty/loan i.e. total net pay of subscriber/sureties together should cover the gorss monthly instalment of chitty/loan.

6. Deduction from salary by way of court attachment or compulsory co-operative recovery should not be present. (If the co-operative recovery is not compulsory, this fact should be mentioned in the salary Certificate). Salary certificates with co-operative recovery may be accepted by the Manager applying his discretion.

7. If the application for acceptance as surety /guarantor can not be furnished in the prescribed format, the details required may be given in the letter head of the Institution concerned which should bear the signature and seal of the drawing Officer. Also the signature of the employee must be attested by the Drawing Officer.

8. In the case of gazetted Officers attested copies of their payslips should also be produced and their signature attested by the immediate superior officer.

9. The genuineness of the loanee and the guarantors will be verified and confirmed as per procedure prescribed by the Company for this purpose.

28

10. Aided school teachers who were in service as on 14.07.97 are eligible for protection and hence such teachers can be accepted as surety/guarantor to our various schemes under SREG without insisting for certificate regarding protection from the Head Master concerned.

11. If the surety guarantor has existing liability, 50% of such liability will be added together with new l iability

Norms for fixing liability

(i) SREG/SRNEG CASES : Score marks and stipulation of 10 & 8 times of the gross salary (Basic+D.A.+Personal Pay) can be considered for fixing liability limit. Likewise in the case of I.T. Category, 50% of their gross taxable income can be considered for fixing the liability. If both type of securities are offered simultaneously, the liability permissible on SREG and SRNEG will be calculated first, and then calculate the liability permissible on Income Tax. Both permissi.ble amounts will be added together and the liability limit fixed accordingly.

(ii) Self surety : Upto Rs.2,00,000/- (In addition to the stipulation of 10 or 8 times of the gross salary (Basisc Pay+D.A+Personal Pay) and 50% of gross taxable income in the case of I.T. category, score marks may also be considered up to Rs.3,00,000/- ) For covering liabilities above Rs. 2 lakhs credit scoring is necessary. The limit of 10 or 8 times of the gross salary for SREG/SRNEG and 50% of the gross taxable income in the case of I.T.category, as the case may be, is applicable in all cases.

(iii) Single surety if subscriber or loanee is an employee: Upto Rs.5,00,000/- (In addition to the stipulation of 10 or 8 times of the gross salary (B.P.+D.A.+P.P.) and 50%of the gross taxable income in the case of I.T. category, score marks may also be considered up to Rs.500000/-). For covering the liabilities above Rs.200000/- credit scoring is necessary. The limit of 10 or 8 times of the gross salary for SREG/SRNEG and 50% of the gross taxable income in the case of I.T. category, as the case may be, is applicable in all cases. Rs. 4 Lakhs on the basis of salary certificate of subscriber/loanee/surety @ Rs. 2 Lakhs each and Rs. 1 Lakh under the basis of score sheet.

(iv) Single surety with unemployed subscriber : (a) If the surety is Up to Rs.200000/- subject to the stipulation of 10 or 8 times

of the gross salary. (Even if the party deserves score marks, the limit of liability prescribed will stand unchanged.)

(v) Multiple surety : Upto Rs.10 Lakhs subject to the stipulation of 10 or 8 times

of the gross salary in the case of SREG / SRNEG and 50% of gross taxable income in the case of I.T. category. Score marks are not applicable in the case of Multiple surety. Only class III and above category employees shall be accepted for future liability if it exceeds Rs. 5 Lakhs. For the liability of above 5 lakhs number of sureties may be minimum 3 (H.O. Lr. No. 12401 dt. 07-04-2012).

29

Other conditions.(i) Weightage for spouse’s income will be given only if he/she is covered under

SREG/ SRNEG/ I.T. category. In order to be eligible for score marks under “owning immovable properties, the borrower has to have the property in his/her own name or should be joint owner.

(ii) Valuation of the immovable properties is by means of a self-declaration by the applicant. However in case where the self declared property value is Rs.2 lakhs, photocopies of tax receipts (building/land) has to be produced. Cases where valuation exceeds Rs.2 lakhs, photocopy of original title deeds has to be produced.

(iii) Qualifying score : 50 marks

Credit scoring criteria (General – other than SREG/SRNEG) 2) The upper cap on the eligibility limit of General Category

(Other than SREG/SRNEG) shall be 50% of the declared gross taxable income as proved by I.T. returns, Form No.16 and latest salary certificate subject to an upper limit Rs.3 lakhs for self surety, Rs.5 lakhs for single surety if subscriber/loanee is an employee and Rs. 2 lakhs if subscriber/loanee is not an employee and Rs.10 lakhs for multiple sureties.

3) While accepting subscribers under general categories, 5 Nos. of cheques have to be collected as security.

4) Special stipulations for subscribers coming under the criteria 6-b in the credit scoring sheet (i.e., those with minimum annual income Rs.48,000/- which was confirmed by Manager)

(a) Qualifying score marks will be 35%

(b) Maximum amount under self surety irrespective of the score shall be Rs. 24,000/-

(c) Maximum amount under single surety (provided surety is also of the same category that is with minimum annual income Rs.48,000/- ) irrespective of the score shall be Rs.36,000/-

(d) Maximum amount under multiple surety (provided surety is also of the same category that is with minimum annual income Rs.48000/-) irrespective of the score shall be Rs.48,000/-

(e) If the surety under single /multiple surety for a subscriber happens to be a

person in the SREG/SRNEG or in the General Category, subscriber’s limit will be reckoned as Rs.24,000/-

30

(f) Applicants belonging to the General Category (Other than SREG/SRNEG) in order to score, marks against the following criteria, will have to submit documentary evidence.(i) Income of the applicant: Income tax returns (For the last 3 years),

Form 16 and latest salary slip /certificate.( If income tax return is accepted as security, such person should produce original acknowledgement receipt received from I.T. Department along with photo copy thereof. The photocopy of the original acknowledgement receipt will be returned after affixing a seal overleaf to the effect that “accepted for liability of Rs……..in chitty No……in ……………Branch.

(ii) Spouse income : Photocopy of income tax returns, form 16 and latest salary slip

(iii) Immovable property : For valuation up to 2 lakhs : photo copy of the tax receipt (Building/land) has to be produced.

(iv) Valuation in excess of Rs.2 lakhs would require submission of photocopies of original title deeds.(Valuation irrespective of the amount will be by means of self declaration by the applicant. The property has to be either in the name of the applicant or he/she should be a joint owner.)

(v) Banking habit : Photo copy of passbook(vi) Weightage for spouse income would be given only if he/she is

covered either under SREG/SRNEG category or should be an I.T. payee.

(vii) Qualifying score : 40%

(viii) The new set of norms i.e., acceptance of sureties under general category other than SREG/SRNEG is applicable to chittty only for the time being.

Note:-1. Stipulation of 10 times/8 times means that SREG & SRNEG employees are allowed to have a liability of 10 times and 8 times respectively of their wages (B.P+D.A+ P.P)

2. Score marks : Subscribers / Loanees / Guarantors will be given score marks considering their taxable gross income , property owned , status, family set-up, age etc. If they score minimum qualifying marks and above , they will be allowed to create liability according to the limits prescribed.

31

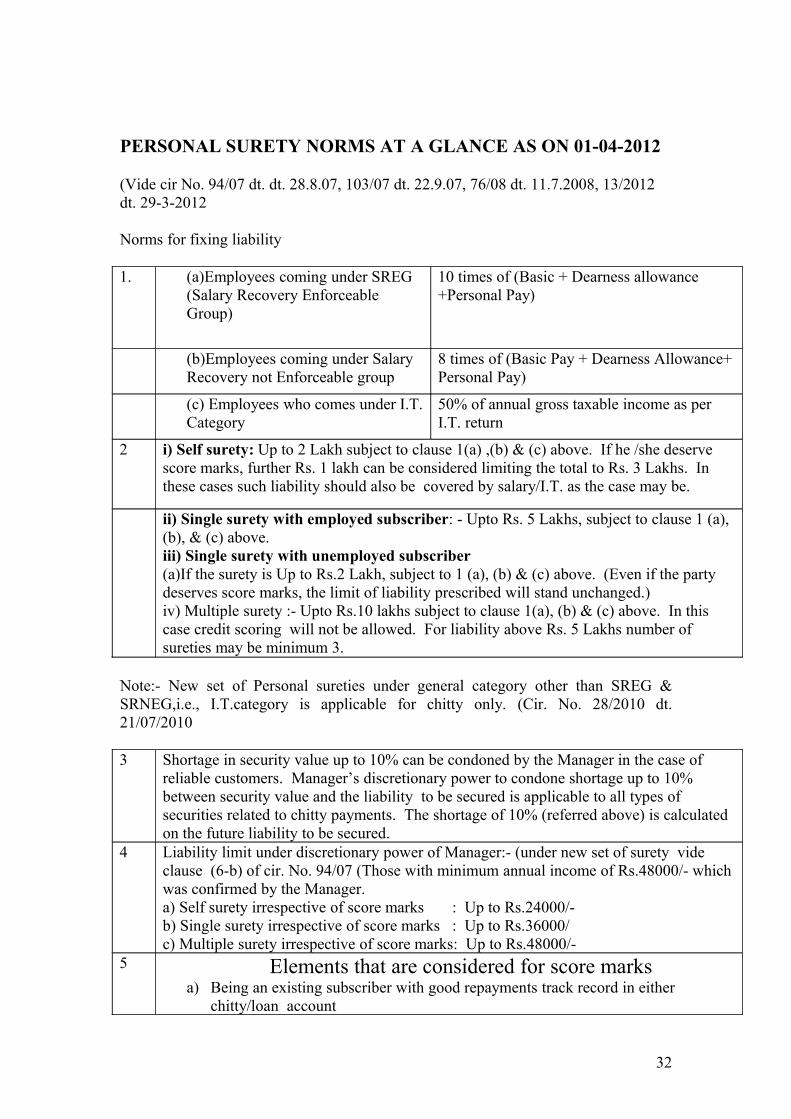

PERSONAL SURETY NORMS AT A GLANCE AS ON 01-04-2012

(Vide cir No. 94/07 dt. dt. 28.8.07, 103/07 dt. 22.9.07, 76/08 dt. 11.7.2008, 13/2012 dt. 29-3-2012

Norms for fixing liability

1. (a)Employees coming under SREG (Salary Recovery Enforceable Group)

10 times of (Basic + Dearness allowance +Personal Pay)

(b)Employees coming under Salary Recovery not Enforceable group

8 times of (Basic Pay + Dearness Allowance+ Personal Pay)

(c) Employees who comes under I.T. Category

50% of annual gross taxable income as perI.T. return

2 i) Self surety: Up to 2 Lakh subject to clause 1(a) ,(b) & (c) above. If he /she deserve score marks, further Rs. 1 lakh can be considered limiting the total to Rs. 3 Lakhs. In these cases such liability should also be covered by salary/I.T. as the case may be.

ii) Single surety with employed subscriber: - Upto Rs. 5 Lakhs, subject to clause 1 (a), (b), & (c) above. iii) Single surety with unemployed subscriber(a)If the surety is Up to Rs.2 Lakh, subject to 1 (a), (b) & (c) above. (Even if the party deserves score marks, the limit of liability prescribed will stand unchanged.)iv) Multiple surety :- Upto Rs.10 lakhs subject to clause 1(a), (b) & (c) above. In this case credit scoring will not be allowed. For liability above Rs. 5 Lakhs number of sureties may be minimum 3.

Note:- New set of Personal sureties under general category other than SREG & SRNEG,i.e., I.T.category is applicable for chitty only. (Cir. No. 28/2010 dt. 21/07/2010

3 Shortage in security value up to 10% can be condoned by the Manager in the case of reliable customers. Manager’s discretionary power to condone shortage up to 10% between security value and the liability to be secured is applicable to all types of securities related to chitty payments. The shortage of 10% (referred above) is calculated on the future liability to be secured.