Embed Size (px)

Citation preview

Pensions in the UK receive generous tax reliefs, but there are some limitations. The Lifetime Allowance (LTA) is the maximum value of benefits which can be taken from registered pension schemes without incurring a special tax charge – known as the Lifetime Allowance tax charge.

The Lifetime Allowance

The LTA is currently £1,030,000. However it has changed frequently since it was introduced in 2006 as shown below. The intention is it will increase in line with the Consumer Prices Index from 2018 onwards.

The Lifetime Allowance and Benefit Crystallisation EventsTechnical Factsheet

For financial adviser use only - not for retail customers

£1.75m£1.8m £1.8m

£1.5m £1.5m

£1.25m £1.25m

£1m £1m £1.03m

£1.65m£1.6m

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Lifetime Allowance test

A test is carried out each time benefits are taken from a registered pension scheme to check if the LTA has been exceeded.

The special tax charge

If the value of benefits exceeds 100% of the LTA, a lifetime allowance tax charge will be payable on the excess. This is currently 55% if the excess is taken as a lump sum. If the excess remains in the pension wrapper, an immediate tax charge of 25% is due and normal rules apply to any future pension withdrawals which are taxed as income under the Pay As You Earn system.

Protection

When the LTA was introduced in 2006 the Government allowed people to apply for two types of protection – known as primary and enhanced protection – to enable people to protect their pension fund from the lifetime allowance charge. Further types of protection have been introduced as the LTA was reduced in 2012, 2014 and 2016. In essence, protection provides entitlement to a special personal lifetime allowance and means a member will pay no, or a lower, lifetime allowance tax charge than if they used the standard LTA.

Individuals with protection should have a certificate from HMRC detailing their personal arrangement.

Age 75

If an individual doesn’t take their benefits until after age 75, then all uncrystallised funds are tested at age 75. When the individual takes their pension benefits in future (eg at age 80) there is no further check against the lifetime allowance. The only Benefit Crystallisation Event (BCE) that can occur after an individual’s 75th birthday is where a scheme pension in payments is increased beyond the permitted margin, through BCE3.

1

2

3

4

5

5a

5b

5c

5d

6

7

8

9

Benefit Crystallisation Events

Each time benefits are taken from a registered pension scheme a test is carried out to ensure the LTA hasn’t been exceeded, these are known as Benefit Crystallisation Events (BCEs) as shown below.

An individual dies before age 75 and remaining uncrystallised funds are designated for dependant’s or nominee’s flexi-access drawdown*

Individual moves funds to provide a drawdown pension

The value of the amount moved into drawdown

Individual becomes entitled to a scheme pension before age 75 20 times the pension paid in the first year

An increase in a scheme pension exceeds a certain level 20 times the excess pension increase

Individual becomes entitled to a lifetime annuity

The value used to buy the annuity (less any amounts previously crystallised under BCE1 if funds are coming from a drawdown arrangement)

An individual reaches age 75 and has not taken all of their benefits under a defined benefit scheme

20 times the pension, plus any separate lump sum, as if these benefits were taken at age 75

An individual with drawdown pension funds reaches age 75

The value of the drawdown less any amounts previously crystallised under BCE1

An individual reaches age 75 with uncrystallised funds in a money purchase arrangement

The value of the uncrystallised funds

The value of the amount moved into drawdown

An individual dies before age 75 and remaining uncrystallised funds are used to buy a dependant’s or nominee’s annuity*

The value used to buy the annuity

Payment of a relevant lump sum before age 75 (eg tax-free lump sum) The amount of the lump sum

Payment of a lump sum death benefit where individual dies before age 75

The amount of the death benefit

Transfer to a Qualifying Recognised Overseas Pension Scheme (QROPS)

The amount transferred (less any amounts previously crystallised under BCE1 if funds are coming from a drawdown arrangement)

Any other event prescribed in regulations. Currently includes certain payments made (arrears after death, pension errors)

Depends on event

BCE What and when Amount measured against LTA

*Needs to be within 2 years of Scheme Administrator being informed of death.

BCE 4

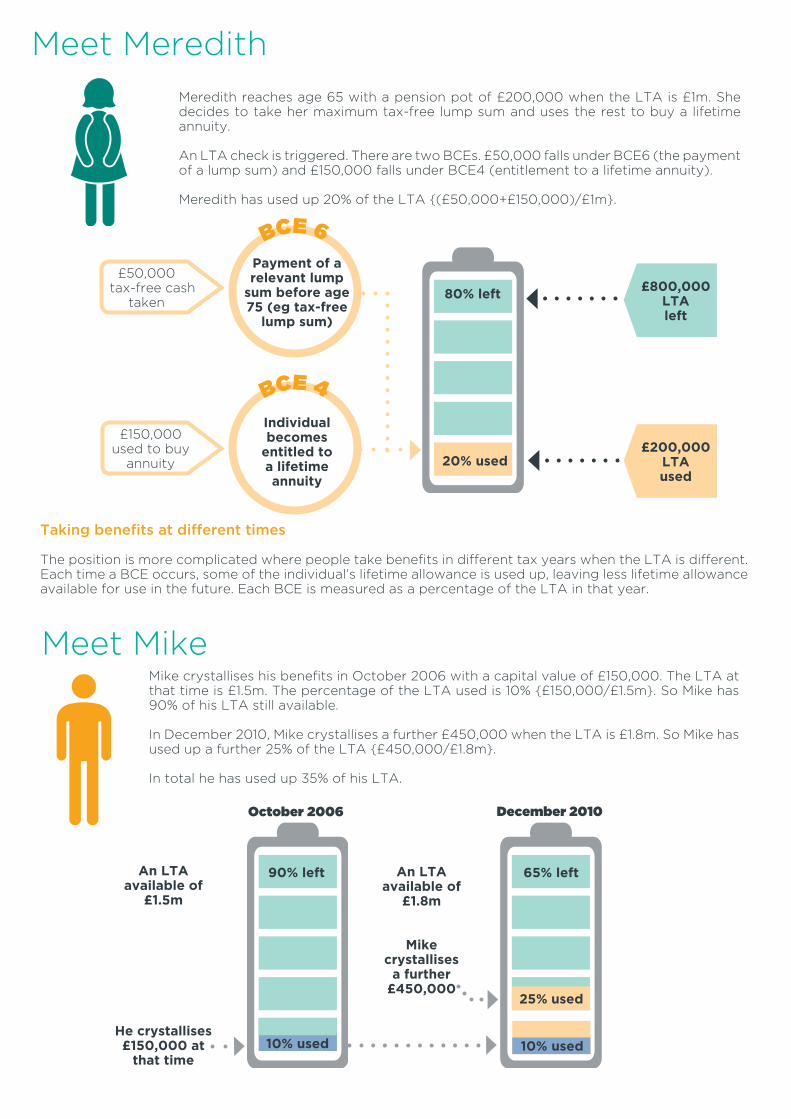

Meet Meredith

Meet Mike

Meredith reaches age 65 with a pension pot of £200,000 when the LTA is £1m. She decides to take her maximum tax-free lump sum and uses the rest to buy a lifetime annuity.

An LTA check is triggered. There are two BCEs. £50,000 falls under BCE6 (the payment of a lump sum) and £150,000 falls under BCE4 (entitlement to a lifetime annuity).

Meredith has used up 20% of the LTA {(£50,000+£150,000)/£1m}.

£800,000LTA left

£200,000LTA used

£50,000 tax-free cash

taken

£150,000 used to buy

annuity

Taking benefits at different times

The position is more complicated where people take benefits in different tax years when the LTA is different. Each time a BCE occurs, some of the individual’s lifetime allowance is used up, leaving less lifetime allowance available for use in the future. Each BCE is measured as a percentage of the LTA in that year.

Mike crystallises his benefits in October 2006 with a capital value of £150,000. The LTA at that time is £1.5m. The percentage of the LTA used is 10% {£150,000/£1.5m}. So Mike has 90% of his LTA still available.

In December 2010, Mike crystallises a further £450,000 when the LTA is £1.8m. So Mike has used up a further 25% of the LTA {£450,000/£1.8m}.

In total he has used up 35% of his LTA.

An LTA available of

£1.5m

An LTA available of

£1.8m

Mike crystallises

a further £450,000

10% used

25% used

BCE 6

90% left 65% left

He crystallises £150,000 at

that time

Payment of a relevant lump

sum before age 75 (eg tax-free

lump sum)

Individual becomes

entitled to a lifetime annuity

20% used

80% left

October 2006 December 2010

10% used

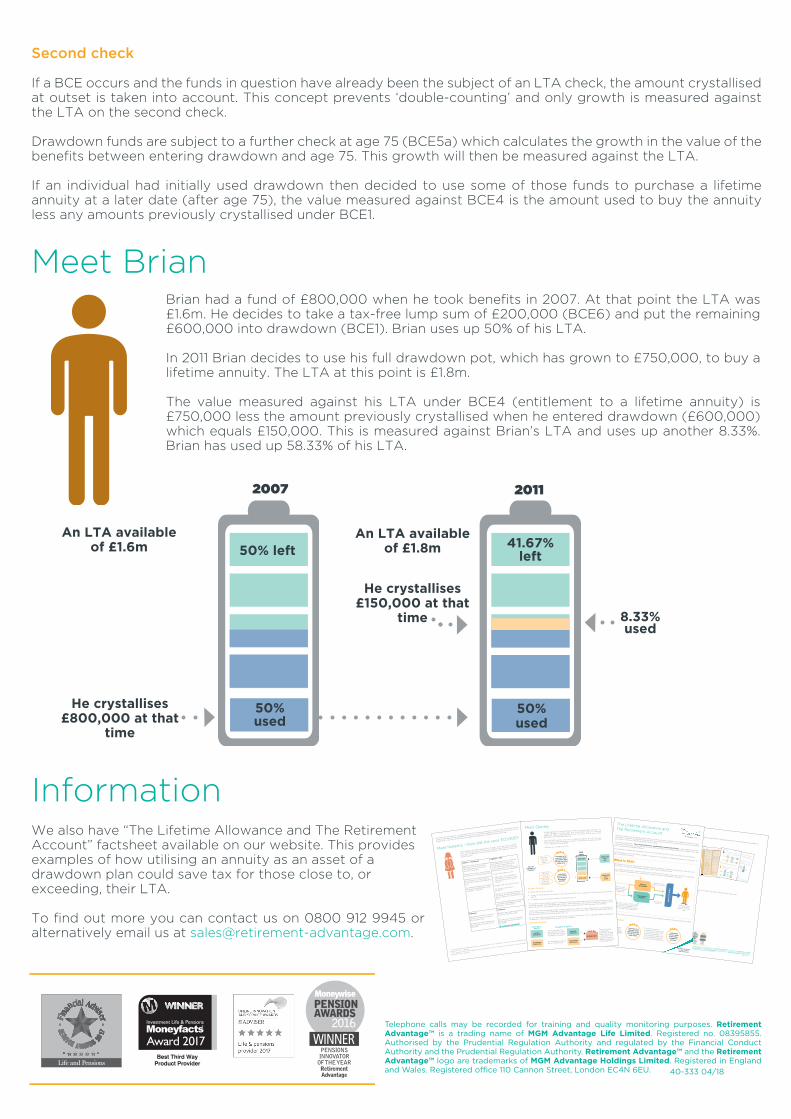

Second check

If a BCE occurs and the funds in question have already been the subject of an LTA check, the amount crystallised at outset is taken into account. This concept prevents ‘double-counting’ and only growth is measured against the LTA on the second check.

Drawdown funds are subject to a further check at age 75 (BCE5a) which calculates the growth in the value of the benefits between entering drawdown and age 75. This growth will then be measured against the LTA.

If an individual had initially used drawdown then decided to use some of those funds to purchase a lifetime annuity at a later date (after age 75), the value measured against BCE4 is the amount used to buy the annuity less any amounts previously crystallised under BCE1.

Meet BrianBrian had a fund of £800,000 when he took benefits in 2007. At that point the LTA was £1.6m. He decides to take a tax-free lump sum of £200,000 (BCE6) and put the remaining £600,000 into drawdown (BCE1). Brian uses up 50% of his LTA.

In 2011 Brian decides to use his full drawdown pot, which has grown to £750,000, to buy a lifetime annuity. The LTA at this point is £1.8m.

The value measured against his LTA under BCE4 (entitlement to a lifetime annuity) is £750,000 less the amount previously crystallised when he entered drawdown (£600,000) which equals £150,000. This is measured against Brian’s LTA and uses up another 8.33%. Brian has used up 58.33% of his LTA.

An LTA available of £1.8m

He crystallises £150,000 at that

time 8.33% used

50% left 41.67% left

2007 2011

50% used

50% used

An LTA available of £1.6m

He crystallises £800,000 at that

time

Telephone calls may be recorded for training and quality monitoring purposes. Retirement Advantage™ is a trading name of MGM Advantage Life Limited. Registered no. 08395855. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Retirement Advantage™ and the Retirement Advantage™ logo are trademarks of MGM Advantage Holdings Limited. Registered in England and Wales. Registered office 110 Cannon Street, London EC4N 6EU. 40-333 04/18

We also have “The Lifetime Allowance and The Retirement Account” factsheet available on our website. This provides examples of how utilising an annuity as an asset of a drawdown plan could save tax for those close to, or exceeding, their LTA.

To find out more you can contact us on 0800 912 9945 or alternatively email us at [email protected].

InformationFor those who are close to, or exceeding, their LTA, utilising an annuity as an asset of the drawdown may be

useful. It obviously gives a guaranteed lifetime income, with the flexibility to reinvest any income which isn’t

needed. But it may also minimise any tax charge in comparison to a traditional drawdown plan.

Meet Natasha, who had a pension pot of £1.6m which she took at age 63.

Her LTA was also £1.6m so she used up 100% of this. She took a tax-free

lump sum of £400,000. From the remaining £1.2m she needs an income of

£20,000 a year.

Meet Natasha - How did she save £121,000?

Option 1 – Drawdown

Natasha invests £1.2m in drawdown,

taking an income of £20,000 a

year. She achieves investment

growth of 5% a year.

At age 75 her fund is worth £1.82m

The growth in her fund is £620,000.

Natasha is due a lifetime allowance

tax charge on this full amount as

she has previously used 100% of her

LTA.

Tax charge at 55% (assuming funds

withdrawn and Natasha is a 40%

tax payer) = £341,000*.

Option 2 – TRA

Natasha invests £1.2m in TRA. She

uses £400,000 via an annuity

to provide her required income

of £20,000 (with a 20-year

income guarantee). The remaining

£800,000 is invested in drawdown.

At age 75 her TRA is worth –

• £400,000 – (12 x £20,000) =

£160,000 for the annuity; plus

• Her drawdown is now worth

£1.44m.

Giving a total TRA value of £1.6m.

The growth in her fund is

£400,000.

Natasha is due a lifetime allowance

tax charge on this full amount as

she has previously used 100% of her

LTA.

Tax charge at 55% (assuming funds

withdrawn and Natasha is a 40%

tax payer) = £220,000**.

Summary:

Natasha has a lifetime income of

£20,000 a year, as long as her

funds support that.

She pays tax (lifetime allowance

tax charge plus income tax) of

£341,000.

Summary:

Natasha has a guaranteed lifetime

income of £20,000 a year.

She pays tax (lifetime allowance

tax charge plus income tax) of

£220,000.

A saving of £121,000!

*This is made up of a 25% lifetime allowance tax charge (£620,000 x 25% = £155,000) + 40% income tax on the remaining fund

(£465,000 x 40% = £186,000).

**This is made up of a 25% lifetime allowance tax charge (£400,000 x 25% = £100,000) + 40% income tax on the remaining fund

(£300,000 x 40% = £120,000).

Contact usTo find out more you can contact us on 0800 912 9945 or alternatively email us at

Telephone calls may be recorded for training and quality monitoring purposes. Retirement Advantage™ is a trading name of MGM Advantage Life Limited.

Registered no. 08395855. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential

Regulation Authority. Retirement Advantage™ and the Retirement Advantage™ logo are trademarks of MGM Advantage Holdings Limited. Registered in

England and Wales. Registered o�ce 110 Cannon Street, London EC4N 6EU.

40-334 03/17

We also have “The Lifetime Allowance and Benefit Crystallisation Events” technical factsheet available on

our website.

Information

Pensions in the UK receive generous tax reliefs, but there are some limitations. The Lifetime Allowance is the maximum value of benefits which can be taken from registered pension schemes without incurring a special tax charge – known as the Lifetime Allowance tax charge.The Lifetime AllowanceThe Lifetime Allowance (LTA) is currently £1m. However it has changed frequently since it was introduced in 2006 as shown below. The intention is it will increase in line with the Consumer Prices Index from 2018 onwards.

The Lifetime Allowance and Benefit Crystallisation EventsTechnical Factsheet

For financial adviser use only - not for retail customers

£1.75m£1.8m £1.8m

£1.5m £1.5m

£1.25m £1.25m

£1m £1m

£1.65m£1.6m£1.5m

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Lifetime Allowance testA test is carried out each time benefits are taken from a registered pension scheme to check if the LTA has been exceeded.

The special tax chargeIf the value of benefits exceeds 100% of the LTA, a lifetime allowance tax charge will be payable on the excess. This is currently 55% if the excess is taken as a lump sum. If the excess remains in the pension wrapper, an immediate tax charge of 25% is due and normal rules apply to any future pension withdrawals which are taxed as income under the Pay As You Earn system.Protection

When the LTA was introduced in 2006 the Government allowed people to apply for two types of protection – known as primary and enhanced protection – to enable people to protect their pension fund from the lifetime allowance charge. Further types of protection have been introduced as the LTA was reduced in 2012, 2014 and 2016. In essence, protection provides entitlement to a special personal lifetime allowance and means a member will pay no, or a lower, lifetime allowance tax charge than if they used the standard LTA.Individuals with protection should have a certificate from HMRC detailing their personal arrangement.Age 75

If an individual doesn’t take their benefits until after age 75, then all uncrystallised funds are tested at age 75. When the individual takes their pension benefits in future (eg at age 80) there is no further check against the lifetime allowance.

Benefit Crystallisation EventsEach time benefits are taken from a registered pension scheme a test is carried out to ensure the LTA hasn’t

been exceeded, these are known as Benefit Crystallisation events (BCEs) as shown below.

1

2

34

5

5a5b5c

5d

6

78

9

An individual dies before age 75 and remaining uncrystallised funds are designated for dependant’s or nominee’s flexi-access drawdown*

Individual moves funds to provide a drawdown pension The value of the amount moved into drawdown

Individual becomes entitled to a scheme pension before age 75 20 times the pension paid in the first year

An increase in a scheme pension exceeds a certain level 20 times the excess pension increase

Individual becomes entitled to a lifetime annuityThe value used to buy the annuity (less any amounts previously crystallised under BCE1 if funds are coming from a drawdown arrangement)

An individual reaches age 75 and has not taken all of their benefits under a defined benefit scheme

20 times the pension, plus any separate lump sum, as if these benefits were taken at age 75

An individual with drawdown pension funds reaches age 75The value of the drawdown less any amounts previously crystallised under BCE1

An individual reaches age 75 with uncrystallised funds in a money purchase arrangement The value of the uncrystallised funds

The value of the amount moved into drawdownAn individual dies before age 75 and remaining uncrystallised funds are used to buy a dependant’s or nominee’s annuity*

The value used to buy the annuity

Payment of a relevant lump sum before age 75 (eg tax-free lump sum) The amount of the lump sum

Payment of a lump sum death benefit where individual dies before age 75 The amount of the death benefit

Transfer to a Qualifying Recognised Overseas Pension Scheme (QROPS)

The amount transferred (less any amounts previously crystallised under BCE1 if funds are coming from a drawdown arrangement)Any other event prescribed in regulations. Currently includes certain payments made (arrears after death, pension errors)Depends on event

BCE What and whenAmount measured against LTA

*Needs to be within 2 years of Scheme Administrator being informed of death.

Second check If a BCE occurs and the funds in question have already been the subject of an LTA check, the amount crystallised

at outset are taken into account. This concept prevents ‘double-counting’ and only any growth is measured

against the LTA on the second check.

Drawdown funds are subject to a further check at age 75 (BCE5a) which calculates the growth in the value of the

benefits between entering drawdown and age 75. This growth will then be measured against the LTA.

If an individual had initially used drawdown then decided to use some of those funds to purchase a lifetime

annuity at a later date, the value measured against BCE4 is the amount used to buy the annuity less any amounts

previously crystallised under BCE1.Meet BrianBrian had a fund of £800,000 when he took benefits in 2007. At that point the LTA

was £1.6m. He decides to take tax-free cash of £200,000 (BCE6) and put the remaining

£600,000 into drawdown (BCE1). Brian uses up 50% of his LTA.

In 2011 Brian decides to use his full drawdown pot, which has grown to £750,000, to buy a

lifetime annuity. The LTA at this point is £1.8m.

The value measured against his LTA under BCE4 (entitlement to a lifetime annuity) is

£750,000 less the amount previously crystallised when he entered drawdown (£600,000)

which equals £150,000. This is measured against Brian’s LTA and uses up another 8.33%*.

Brian has used up 58.33% of his LTA.

An LTA available of £1.8million

*He crystallises £150,000 at that time

8.33% used

50% left

41.67% left

2007

2011

50% used

50% used

An LTA available of £1.6million

He crystallises £800,000 at that time

Contact usTo find out more you can contact us on 0800 912 9945 or alternatively email us at

Telephone calls may be recorded for training and quality monitoring purposes. Retirement

Advantage™ is a trading name of MGM Advantage Life Limited. Registered no. 08395855.

Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct

Authority and the Prudential Regulation Authority. Retirement Advantage™ and the Retirement

Advantage™ logo are trademarks of MGM Advantage Holdings Limited. Registered in England

and Wales. Registered o�ce 110 Cannon Street, London EC4N 6EU.40-333 02/17

BCE 4

Meet Meredith

Meet Mike

Meredith reaches age 65 with a pension pot of £200,000 when the LTA is £1million.

She decides to take her maximum tax-free lump sum and uses the rest to buy a lifetime

annuity.An LTA check is triggered. There are two BCEs. £50,000 falls under BCE6 (the payment

of a lump sum) and £150,000 falls under BCE4 (entitlement to a lifetime annuity).

Meredith has used up 20% of the LTA {(£50,000+£150,000)/£1m}.

£800,000LTA left

£200,000LTA used

£50,000 tax-free cash taken

£150,000 used to buy annuity

Taking benefits at di�erent timesThe position is more complicated where people take benefits in di�erent tax years when the LTA is di�erent.

Each time a BCE occurs, some of the individual’s lifetime allowance is used up, leaving less lifetime allowance

available for use in the future. Each BCE is measured as a percentage of the LTA in that year.Mike crystallises his benefits in October 2006 with a capital value of £150,000. The LTA at

that time is £1.5m. The percentage of the LTA used is 10% {£150,000/£1.5m}. So Mike has

90% of his LTA still available.In December 2010, Mike crystallises a further £450,000 when the LTA is £1.8m. So Mike has

used up a further 25% of the LTA {£450,000/£1.8m}.

In total he has used up 35% of his LTA.

An LTA available of £1.5millionAn LTA available of £1.8million

Mike crystallises a further £450,00010% used 25% used

BCE 6

90% left

65% left

He crystallises £150,000 at that time

Payment of a relevant lump sum before age 75 (eg tax-free lump sum)

Individual becomes entitled to a lifetime annuity 20% used

80% left

October 2006

December 2010

10% used

Pensions in the UK receive generous tax reliefs, but there are some limitations. The Lifetime Allowance (LTA) is

the maximum value of benefits which can be taken from registered pension schemes without incurring a special

tax charge – known as the lifetime allowance tax charge.Our technical factsheet – The Lifetime Allowance and Benefit Crystallisation Events – gives details of how the

LTA works and the tests carried out each time benefits are taken from a registered pension scheme which are

known as Benefit Crystallisation Events.This factsheet considers the interaction of the LTA with the Retirement Account, our unique hybrid solution.

As The Retirement Account (TRA) is legally a drawdown contract the LTA generally operates as it does for all

other drawdown contracts.

The Lifetime Allowance and The Retirement Account

What is TRA?The Retirement Account combines a Guaranteed Annuity, a Pension Drawdown facility and a Cash Account,

all held within a single tax-advantaged wrapper written under Drawdown rules.

Once a client transfers their pension pot(s) into The Retirement Account, they can choose to invest their

money in Pension Drawdown, buy a Guaranteed Annuity or use any combination of the two.

Guaranteed Annuity

PensionDrawdown

Cash A

ccount

Flexible income and access to cash

Guaranteed income

Secure more Guaranteed Annuity from Pension Drawdown

Client has total income flexibility and access to their cash

Redirect some or all of the guaranteed income and reinvest into Pension Drawdown. No

income tax and boost Pension Drawdown funds. Guaranteed income can restart at any time.

LTA check at outset

BCE 6Payment of a relevant lump sum before age 75 (eg tax-free lump sum)

BCE 1Individual moves funds to provide a drawdown pension

When an individual buys TRA, any tax-free lump sum taken is valued using BCE6.

The amount used to purchase the annuity and/or drawdown within TRA is valued using BCE1 - as TRA is legally a drawdown contract with the annuity an asset of that drawdown.

For financial adviser use only - not for retail customers

However, TRA is unique in that an annuity may be an asset of the drawdown and the following outlines how that

works.

Meet Stanley

£600,000LTA left

£400,000LTA used

£100,000 tax-free lump sum taken

£120,000 used to buy

annuity

£180,000 invested in drawdown

40% used

60% left

Stanley aged 65, invests £400,000 in TRA in October 2016 when the LTA

is £1m. He takes a tax-free lump sum of £100,000. With the remaining

£300,000, Stanley uses £120,000 to buy an annuity income and invests

£180,000 in the drawdown element.

The £100,000 tax-free lump sum is measured against the LTA through

BCE6, and the £300,000 used to invest in annuity and/or drawdown within

TRA is measured through BCE1.

Stanley uses up 40% of his LTA.

BCE 6Payment of a relevant lump

sum before age 75 (eg tax-free

lump sum)

BCE 1Individual

moves funds to provide a drawdown

pension

Second LTA check

A further check may be required –

• at age 75. This measures the growth in the value of the TRA, if any, between the individual entering TRA and

age 75.

• if a lifetime annuity is bought outside of TRA before age 75.

The valuation of most assets at age 75 is straightforward, being the market value of the asset. However for some

assets the valuation may be slightly more complex. TRA may hold an annuity as an asset. The valuation of the

annuity at age 75 is the original purchase price less the income paid up to the individual’s 75th birthday.

Continuing the above example, Stanley invested £400,000 in TRA in October 2016 when the LTA was £1m. He

took a tax-free lump sum of £100,000, used £120,000 to buy an annuity within TRA and invested £180,000 in

the drawdown element. He used up 40% of his LTA.

10 years later Stanley reaches age 75, and still has money invested within TRA. A valuation needs to take place

to determine if there has been any growth since he invested.

How does this work?

2016

An LTA available of

£1million

Annuity£120,000

Annuity£60,000

Drawdown£180,000

Drawdown£300,000

£360,000

This is valued as the

initial amount invested

(£120,000) less income

(£6,000 for 10 years) =

The drawdown fund has

grown to £300,000

Invested at age 65

Valuation at age 75

The initial value invested was £300,000, so that

means the growth

is £60,000. This is

measured against

Stanley’s remaining

LTA at that time.

TOTAL