Embed Size (px)

Citation preview

The Low-Cost OPEC Cycle:

The Big Elephant in the Room

Bassam Fattouh

PRESENTED AT THE BANK OF ENGLAND

Oxford Institute for Energy Studies

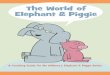

In 2015, Oil Demand Growth (particularly gasoline) Carried Bulk

of Adjustment

Global Oil Demand, y/y change,

thousand b/d

Source: IEA, Energy Aspects

Oil demand growth (driven in big part by low oil

prices) exceeded expectations in 2015 though it has

been slowing down in recent months

--

500

1,000

1,500

2,000

2,500

3,000

Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16

(600)

(400)

(200)

-

200

400

600

800

1,000

1,200

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Diesel Gasoline

Non-OECD Asian Gasoline and Diesel

Demand, y/y change, thousand b/d

Non-OECD Asia remains main source of growth;

But growth is no longer only about China or about

diesel; as Asian economies rebalance, gasoline (also

naphtha) have become the main driver of oil demand

growth

In 2016, Pass on the Baton to Non-OPEC Supply (Particularly US

Shale)

Despite efficiency gains, US shale has been

leading the way and has been the fastest to

respond to the decline in the oil price with growth

turning negative

1265

1035

881

583

44

-150

-318

-480

-681-578 -619

-1000

-500

0

500

1000

1500

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

2,500

3,000

12

Q1

12

Q2

12

Q3

12

Q4

13

Q1

13

Q2

13

Q3

13

Q4

14

Q1

14

Q2

14

Q3

14

Q4

15

Q1

15

Q2

15

Q3

15

Q4

16

Q1

16

Q2

16

Q3

North America South America FSU Europe

Asia-Pacific Middle East Africa

Non-OPEC Supply, y/y change, thousand b/d US Supply, y/y change, thousand b/d

After robust growth in the environment of high oil

prices, the y/y change in non-OPEC supply has

turned negative in almost every part of the world

Source: EIA, Energy Aspects

Middle East OPEC Supply Growth: the Elephant in the Room

Iranian oil Output, mb/dSaudi and Iraq output, y/y change, mb/d

OPEC has been major source of supply growth with

Iraq and Saudi Arabia alone adding more than 1.1 mb/d

in 2015 and more than 700,000 b/d in 2016 (Jan-

August)

In 2016, Iraq and Saudi Arabia were joined by Iran

which ramped up its output to pre-sanction levels

much faster than originally expected

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Iraq Saudi Arabia

2.50

2.70

2.90

3.10

3.30

3.50

3.70

3.90

Jan

-10

Au

g-1

0

Mar

-11

Oct

-11

May

-12

Dec

-12

Jul-

13

Feb

-14

Sep

-14

Ap

r-1

5

No

v-1

5

Jun-1

6

Source: OPEC, Energy Aspects

Saudi Oil Policy Based on Fundamental Principle: No Unilateral

Action to Balance the Market on Downside

Source: BP, OPEC

-

2000

4000

6000

8000

10000

12000

14000

Saudi Arabia Oil Production, mb/d Saudi Arabia production vs Quota (kb/d)

Saudi Arabia not willing to cut output unilaterally; shaped

by the mid 1980s events when its attempt to protect the

price resulted in loss of large volumes of production and

market share (and lower revenues)

In response to Venezuela’s increase in output in

the mid 1990s, Saudi Arabia increased its output

beyond its quota contributing to the oil price

collapse

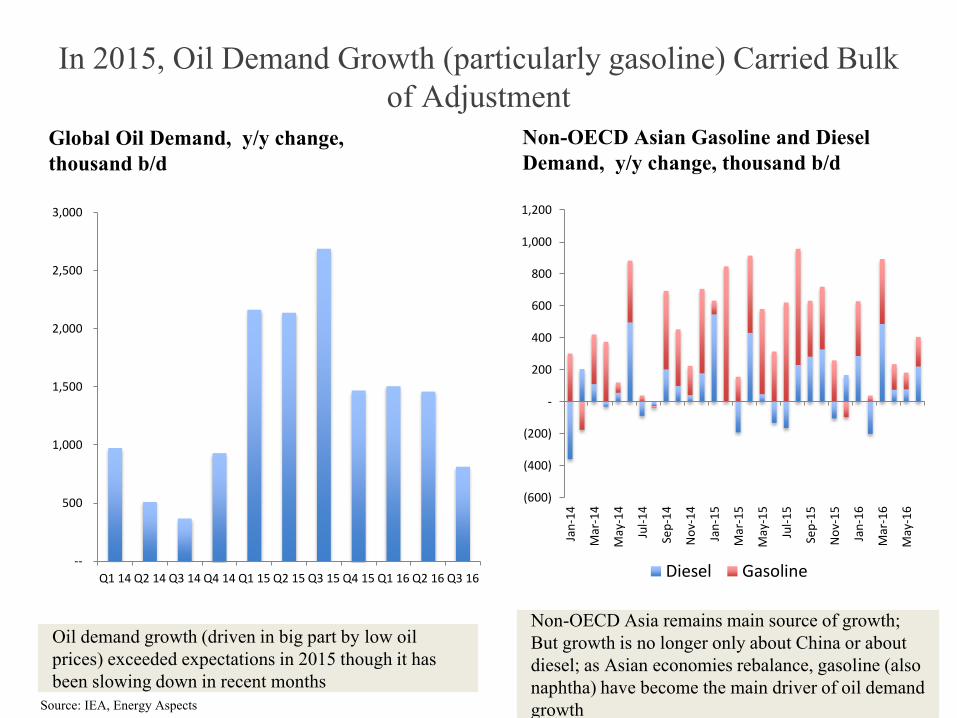

Saudi Output Policy Has Passed Through Various Phases Recently: Is

there a New Phase in the Making?

8

8.5

9

9.5

10

10.5

11

Jan

-10

Jun

-10

No

v-1

0

Ap

r-1

1

Sep

-11

Feb

-12

Jul-

12

De

c-1

2

May

-13

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-1

6

Saudi Arabia Oil Production, mb/d

Phase 1: Increase production to offset outages; Phase 2: Pursue a

market share strategy in the absence collective agreement on

output and in face of a structural shock and heightened

uncertainty; Phase 3 in making: Increase output and purse

cooperation; What are the potential drivers?

5000

5500

6000

6500

7000

7500

8000

8500

Jan

-10

Jun

-10

No

v-1

0

Ap

r-1

1

Sep

-11

Feb

-12

Jul-

12

De

c-1

2

May

-13

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-1

6

Saudi exports remain elevated and it seems there

is implicit policy of maintaining crude exports

above a certain level

Saudi Arabia Crude Oil Exports, thousand b/d

Recent Increase in Output Not Only Due To Swing in Summer Oil

Demand

-150

-100

-50

0

50

100

150

Jan14

Mar14

May14

Jul14

Sep14

Nov14

Jan15

Mar15

May15

Jul15

Sep15

Nov15

Jan16

Mar16

May16

Gasoline Diesel

Gasoline and Diesel Demand, thousand b/d

Products demand has weakened in recent months

particularly diesel reflecting an overall slower

economic growth

(250)

(200)

(150)

(100)

(50)

-

50

100

150

200

250

300

Jan14

Mar14

May14

Jul14

Sep14

Nov14

Jan15

Mar15

May15

Jul15

Sep15

Nov15

Jan16

Mar16

May16

Crude Burn, y/y change, thousand b/d

Crude burn compared to last year has also fallen

reflecting in part slower growth of electricity

demand and use of more gas in the power sector

Source: JODI

Saudi Arabia Also Competing in Products Markets

Saudi Arabia Refining Runs, mb/d

Saudi Arabia refining runs at record levels as the

new refineries ramp-up output

Exports of products (particularly diesel) have been

on the rise and Saudi Arabia is competing in

products market

Saudi Arabia Products Exports, mb/d

0

100

200

300

400

500

600

700

Jan

-10

Jun

-10

No

v-1

0

Ap

r-1

1

Sep

-11

Feb

-12

Jul-

12

De

c-1

2

May

-13

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-1

6

Gasoline Exports Diesel Exports Jet Exports

Source: JODI

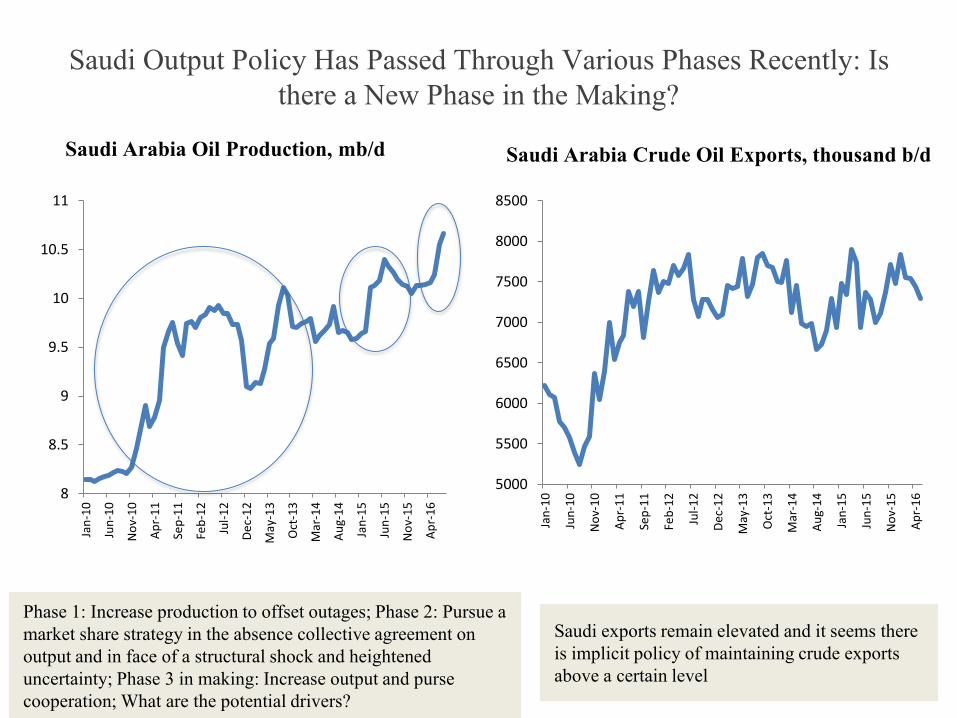

Phase 2: New Set of Structural Uncertainties

Under complete information about shale response in a

rising price environment, there is a single and efficient

solution to the game

Under uncertainty about US shale response, Saudi

Arabia is better-off to assume that shale supply curve

is elastic and not to cut production

Game Under Certainty

The contents of this paper are the author’s sole responsibility. They do not necessarily represent the viewsof the Oxford Institute for Energy Studies or any of its Members.

16

Figure 19: Game under uncertainty

Source: Fattouh et al. (2015).

The quest for market share

For now, Saudi Arabia’s output policy seems to focus on market share. There has been a debate

among economists about the intrinsic value of market share as an economic objective. It is possible to

identify three reasons as to why Saudi Arabia may wish to pursue market share. First, Saudi Arabia

holds 267 billion barrels of proven reserves, with a reserve-to-production ratio of more than 63 years.

Therefore, securing markets for its oil is a key long-term policy objective. In other words, while

revenue maximization constitutes a key policy objective, the time horizon over which revenues should

be maximized also matters. Second, when it is difficult to reach an agreement within OPEC on a

collective cut, Saudi Arabia can maintain or even increase its market share, pushing prices down and

reducing the revenues for all other oil producers in an attempt to get other producers to cooperate.

Third, pursuing market share can act as a deterrent strategy to squeeze high-cost competitors out of

the market. Also consistent with this strategy, Saudi Arabia can abandon its role as market stabilizer

in an over-supplied market, inducing more price volatility and sharper price movements. Increased

volatility, together with the perception that prices could fluctuate within a wide range, might cause

investors to reassess the risks in new energy projects. This would increase the value of the option to

wait and discourage investment in new oil projects.21

The loss of a key feedback mechanism

One of the distinguishing features of the current price fall is the low probability that the market

attaches to any form of cooperation between producers to clear the market. OPEC behaviour over

this cycle has been different from that seen in several previous cycles and this represents a structural

shift in the market adjustment mechanism. In 2008, the global financial crisis resulted in large drop in

oil demand. OPEC reacted to this temporary decline by sharply cutting output, which proved effective:

the V-shaped recovery of the global economy meant that oil demand quickly recovered and OPEC

was able to raise its output and meet the increase in demand. In 1998, the drop in demand due to the

Asian financial crisis and Venezuela’s drive to maximize production posed a major challenge for

OPEC. Both of these factors eventually reversed, with oil demand recovering as Asian economies

emerged from the financial crisis, and Venezuelan production declining after Chavez assumed power.

Although it took a long time for OPEC and non-OPEC members to reach an agreement on an output

cut, the 1998 crisis reasserted OPEC’s role in the market. In contrast, in 1986, the decline in demand,

the increase in non-OPEC supply, and lack of cohesion within OPEC resulted in a collapse of the

OPEC administered pricing system and the emergence of a new pricing structure in which OPEC’s

21 In 2015 the new Saudi Energy Minister Mr Al-Falih noted that ‘the past willingness of Saudi Arabia in particular to limit output

to defend high oil prices was a mistake that had only served to spur high-cost output elsewhere. Such a policy had offered high

cost producers an “insurance policy” of “$100 oil … a guarantee of no risk for investment.” ’

Game Under Uncertainty

Source: Fattouh, Sen, and Poudineh (2015), Oxford Review of Economic Policy

Limited Diversification and Heavy Reliance on Government Revenues

Oil share of government revenues, %

Data on Q1 real GDP growth showed that the economy expanded by 1.5 percent, year-on-year. Growth was mainly due to a positive contribution from the oil sector, while non-oil government GDP contracted for a second consecutive quarter, reflecting the impact of fiscal consolidation. GDP by kind of economic activity points to a general slowdown in most sectors within the non-oil economy.

3

Quarterly GDP Growth

Real GDP growth reached 1.5 percent in Q1 2016, slowing from 1.8 percent in the previous quarter.

The main contribution to GDP growth came from the oil sector, which rose by 5.1 percent, year-on-year.

Most sectors within the non-oil economy saw a slowdown in their growth rates during Q1, with annual growth turning negative in the construction, wholesale & retail, and utilities sectors.

August 2016

Oil Sector GDP Growth (year-on-year change)

Quarterly Real GDP Growth

Real GDP Growth by Kind of Economic Activity (year-on-year change)

-4

-2

0

2

4

6

8

10

12

2013Q1

Q3 2014Q1

Q3 2015Q1

Q3 2016Q1

Non-oil manufacturing ConstructionWholesale & retail TransportFinance Utilities

(p

erc

en

t)

-4

-2

0

2

4

6

8

2013Q1

Q3 2014Q1

Q3 2015Q1

Q3 2016Q1

Non-oil - gov (ppt) Non-oil - pvt. (ppt)Oil (ppt) Real GDP, % y/y

-10

-8

-6

-4

-2

0

2

4

6

8

10

2013Q1

Q3 2014Q1

Q3 2015Q1

Q3 2016Q1

Oil sector GDP Oil production

(p

erc

en

t)

Quarterly Real GDP Growth

Paradox: Vision 2030 is about moving away from oil

but oil revenues constitutes main source of

government revenues and are enabling factor to

transitioning to ‘vibrant’ economy

Fall in oil revenues has had a big on economy

especially on non-oil private sector which still relies

heavily on government spending

Source: Jadwa

Despite fiscal buffers, Saudi Economy Badly Hit By Low Oil Price

In June, the values for both non-oil exports and imports were down, month-on-month. The decline in imports in recent months reflects the slowdown in domestic economic activity so far in 2016. However, one upside from the recent decline in imports is an improvement in the Kingdom’s monthly non-oil trade balance.

7

Trade

Non-oil exports fell by $0.4 billion in June (-10 percent, year-on-year). Meanwhile imports declined at a faster pace, falling by $0.7 billion in June (-24 percent, year-on-year). One upside from the Kingdom’s recent trade performance is an improvement in the monthly non-oil trade balance, which has reached -$7.7 billion in June.

September 2016

Imports

Non-oil Exports

Monthly Non-oil Trade Balance

-40

-30

-20

-10

0

10

20

30

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Jun-14 Dec-14 Jun-15 Dec-15 Jun-16

non-oil exports % change, y/y (RHS)

(p

erc

en

t)

($

billio

n)

-30

-20

-10

0

10

20

30

10

11

12

13

14

15

16

Jun-14 Dec-14 Jun-15 Dec-15 Jun-16

Imports % change, y/y (RHS)

($

b

illio

n)

(p

erce

nt)

-12

-11

-10

-9

-8

-7

-6

Jun-14 Dec-14 Jun-15 Dec-15 Jun-16

($ b

illio

n)

Saudi Imports, $ billion and y/y change (%)

Saudi imports have declined sharply in the last few

months

The absence of any major events or news items related to listed companies, and a downward trend in oil prices towards the end of the month, saw the TASI fall by 3 percent, month-on-month, in August. Volumes also dipped during the month. We expect TASI activity to pick up in mid-September, after the Eid al-Adha break.

TASI

11

Stock Market

A dearth of news events

and a dip in oil prices, towards the end of the month, saw TASI decline by 3 percent month-on-month… ...with a number of regional markets also experiencing a similar decline. The impact was also seen in TASI market turnover,

which dipped to its lowest in exactly five years.

September 2016

Daily Average Stock Market Turnover

Comparative Stock Market Performance (monthly performance from 1st August 2016)

5,200

5,800

6,400

7,000

7,600

8,200

8,800

9,400

10,000

10,600

11,200

Aug-14 Feb-15 Aug-15 Feb-16 Aug-16

-4

-2

0

2

4

6

8

Qa

tar

Ch

ina

Bra

zil

Ge

rm

any

UK

MS

CI

EM

Ja

pa

n

Eg

yp

t

Du

bai

US

Ku

wa

it

Turkey

Ba

hra

in

Om

an

Ab

u D

ha

bi

TA

SI

(p

erce

nt)

0

2

4

6

8

10

12

Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

(S

R b

illi

on

)

Saudi Stock Market Index

Saudi stock market has lost more than half of its value

since the the fall in the oil price

Source: Jadwa

Phase 3: The Power of Signaling

01/09 /2016, 10:38Saudi energy minister hints at ef for t to rebalance oil market - FT.com

Page 1 of 6ht tp:/ /www.f t .com/cms/s/0/86 513a92- 5f9b- 11e6 - ae3f- 77baadeb1c93.html#axzz4Izmg4MER

Share Author alerts Print Clip Comments

August 11, 2016 9:30 am

Anjli Raval, Oil and Gas Correspondent

Saudi energy minister hints at effort torebalance oil market

©Reuters...

Speed the market rebalancing by seeking cooperation with other producers but OPEC output at

historical records; Help improve market sentiment and squeeze shorts out of the market; Serious

barriers remain for a deal in November (Iran-Saudi relations being only one among many barriers)

Source: Financial Times, Reuters

30/09 /2016, 08 :01OPEC agrees modest oil output curbs in f irst deal since 2008 | Reuters

Page 1 of 5ht tp:/ /www.reuters.com/ar t icle/us- opec- meet ing- idUSKCN11Y18K

COMMODITIES | Thu Sep 29, 2016 | 4:29pm EDT

OPEC agrees modest oil output curbs in firstdeal since 2008

OPEC deal bullish for U.S. shale 01:03

By Rania El Gamal , Alex Lawler and Vladimir Soldatkin | ALGIERS

OPEC agreed on Wednesday modest oil output cut s in the first such deal since 2008, with the

group's leader Saudi Arabia softening its stance on arch-rival Iran amid mounting pressure from

low oil prices.

"OPEC made an exceptional decision t oday ... After two and a half years, OPEC reached consensus

to manage the market," said Iranian Oil Minister Bijan Zanganeh, who had repeatedly clashed with

Saudi Arabia during previous meetings.

He and other ministers said the Organization of the Petroleum Exporting Countries would reduce

output to a range of 32.5-33.0 million barrels per day. OPEC estimates its current output at 33.24

million bpd.

ADVERTISING

1 Philippines' Duterte likens himsel f to

Hitler, wants to kill millions of drug

users

2 After military raid, India looks at more

ways to pressure Pakistan

3 NXP Semiconductors explores sale to

Qualcomm: sources

4 U.S. lawmakers may change

September 11 law after rejecting veto

5 Three Chinese fishermen killed in

confrontation with South Korea

coastguard

TRENDING STORIES

Business Markets World Politics Tech Commentary Breakingviews Money Life Pictures Video

EDITION: UNITED STATES

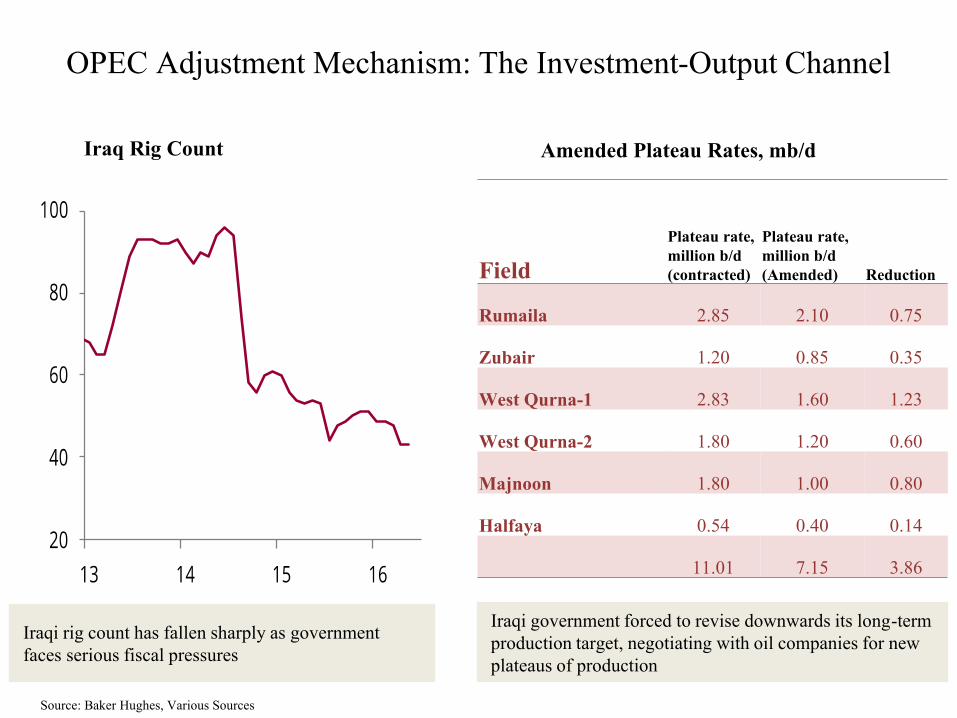

OPEC Adjustment Mechanism: The Investment-Output Channel

Iraq Rig Count

Iraqi rig count has fallen sharply as government

faces serious fiscal pressures

Iraqi government forced to revise downwards its long-term

production target, negotiating with oil companies for new

plateaus of production

Field

Plateau rate,

million b/d

(contracted)

Plateau rate,

million b/d

(Amended) Reduction

Rumaila 2.85 2.10 0.75

Zubair 1.20 0.85 0.35

West Qurna-1 2.83 1.60 1.23

West Qurna-2 1.80 1.20 0.60

Majnoon 1.80 1.00 0.80

Halfaya 0.54 0.40 0.14

11.01 7.15 3.86

Amended Plateau Rates, mb/d

Source: Baker Hughes, Various Sources

OPEC Adjustment Mechanism: The Fiscal Crisis-Output Disruption

Channel

Nigerian oil output, mb/d Venezuela oil output, mb/d

Attacks on oil infrastructure in the Niger Delta

intensifies as government’s ability to pay-off

militants weakens

Poor planning, lack of investment, fall in umber of

rigs, equipment theft, and payment delays to

service companies impacting Venezuela’s output

1

1.2

1.4

1.6

1.8

2

2.2

2.4

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

2

2.05

2.1

2.15

2.2

2.25

2.3

2.35

2.4

2.45

2.5

Jan

-10

Au

g-1

0

Mar

-11

Oct

-11

May

-12

Dec

-12

Jul-

13

Feb

-14

Sep

-14

Ap

r-1

5

No

v-1

5

Jun-1

6

Source: Energy Aspects

The Low-Cost OPEC Cycle

• OPEC adjustment mechanisms– Collective agreement on cuts (Long-time to achieve consensus especially when many producers have

aspirations to increase production; highly uncertain)

– Impact on investment and on output (Longer lags than high non-OPEC cost producers; in stable OPEC countries, drive to invest continues even in a low price environment; the drive to maximize output in an attempt to maximize short-term revenues)

– Fiscal crisis and output disruptions (highly unpredictable)

• OPEC current behavior represents a fundamental difference from some of the past cycles (absence of a key feedback mechanism to balance the market)

• Saudi oil policy shaped by multiple considerations (Internal: limited diversification; External: Nature of the shock; OPEC dynamics: Ability to forge a deal with other producers and implement it)

• As these factors change and/or as new information becomes available, Saudi oil policy will also change

• Potential shifts in Saudi oil policy and/or signals about these shifts will continue to shape oil market outcomes