Embed Size (px)

Citation preview

1

The Low Interest Rate Dilemma For Corporate InvestorsCarolina Cash Conference May 2012

Mike Betty, Senior Vice President, CTP; BB&T Florida Sales Manager

2

The Universally Accepted Response to the Global Cri sis:

3

The more appropriate response, according to some!!:

4

Topics for Discussion

� Discussion of the present state of corporate liquid ity – How did we get here?

� Corporate liquidity trends

� Facts related to the present state of corporate cas h

� What is driving the reluctance to invest

� Rationale for continued caution

� Rationale for optimism

� Today’s investment-related challenges for Treasurer s

� Investment policy best practices

5

The Present State of Corporate Liquidity

Macro causes:

• Crisis of confidence emanating from one of the wors t economic and

financial downturns since the Great Depression, wit h yields on 3-month

treasuries falling as low as .02% (a rate this low had not occurred since

January 1941)

• Employees at domestic and international firms have been cut at high

levels over the past three years (in a related surv ey, just 39% of US

companies expect to add employees in the next six m onths although

they are slightly more optimistic about U.S. econom ic growth - NABE

survey)

6

The Present State of Corporate Liquidity

Macro causes:

• The global pace of M&A has been reduced, not due to the dearth of

targets but largely due to continued economic uncer tainty

(only 31% of worldwide executives have plans to buy another

company over the next 12 months; down from 41% in t he 4th

quarter of 2011 – Ernst & Young survey)

• The number of global companies that desire continue d sale and spin-

off of their divisions and subsidiaries matches the amount of firms

that wish to acquire

• Capital expenditures budgets at many companies have been reduced

to forced replacement levels as opposed to enhancem ent levels – in

spite of cash availability and borrowing/line avail ability

7

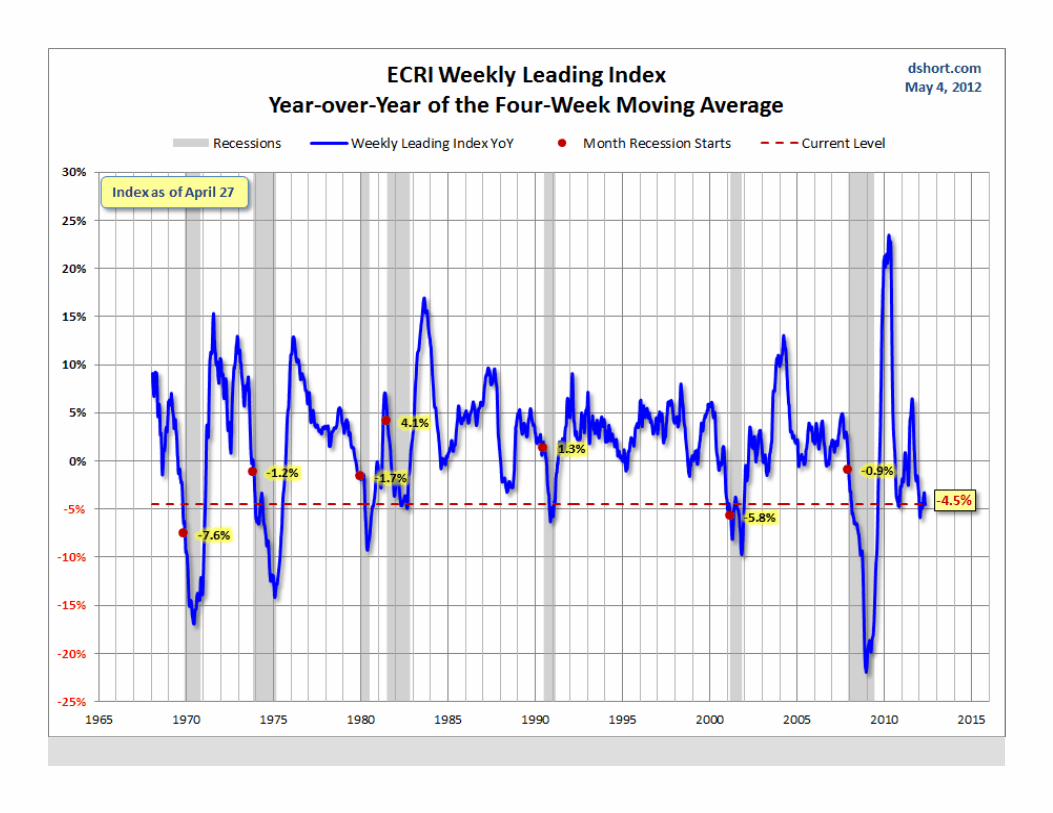

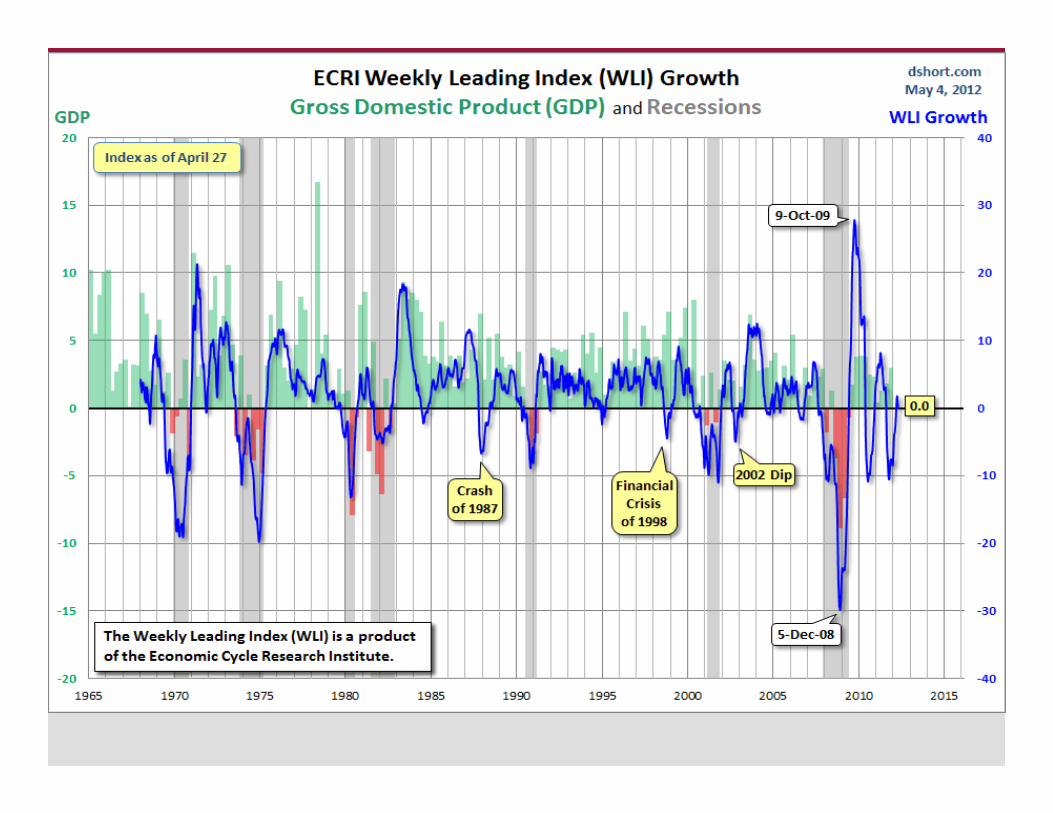

Economic Cycle Research Institute (ECRI)

� Publishes a weekly leading index (WLI) that utilize s a number of macroeconomic data points to forecast future eco nomic activity

� Designed to predict the direction of economic growt h in the next 6-9 months

� A significant decline of the WLI has been a leading indicator of six of the past seven recessions since the 1960’ s

8

Graph showing Corp. Cash Growth needed:

– R

Source:

9

10

Corporate liquidity trends

Due to unprecedented historical turmoil,that domestic and worldwide corporateliquidity levels are high does not come as alarge surprise, given the above; thesurprise is the magnitude of the increase:

11

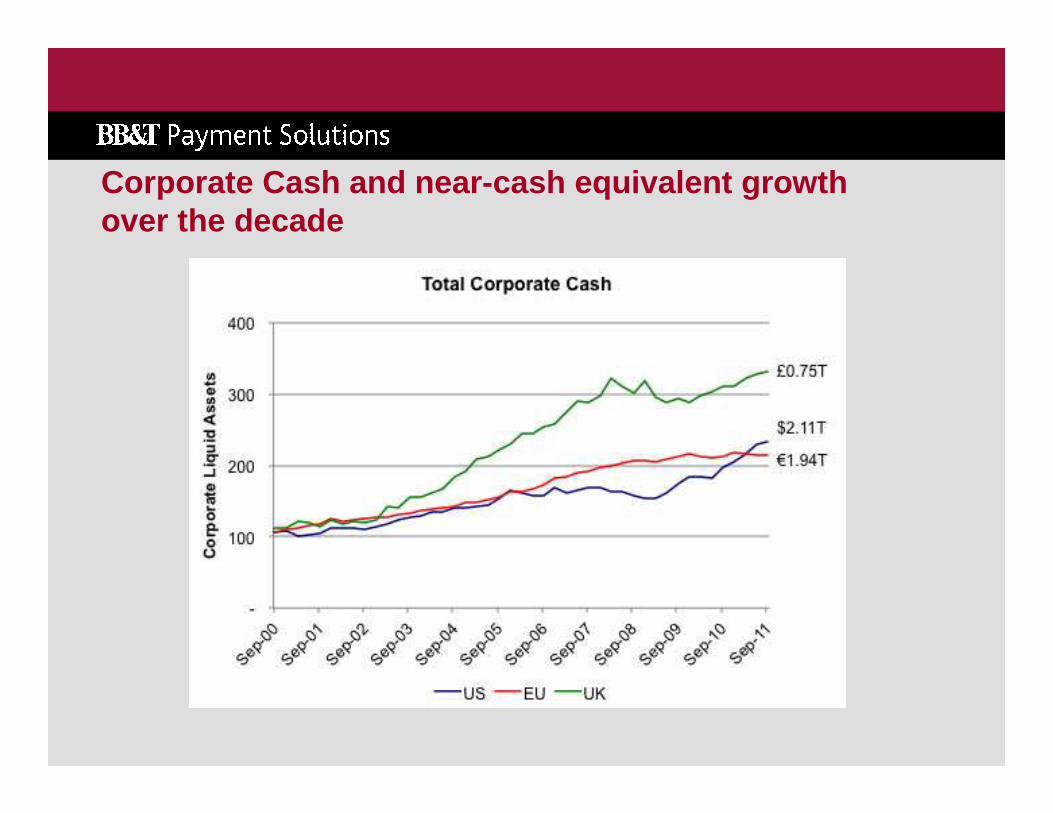

Corporate Cash and near-cash equivalent growth over the decade

12

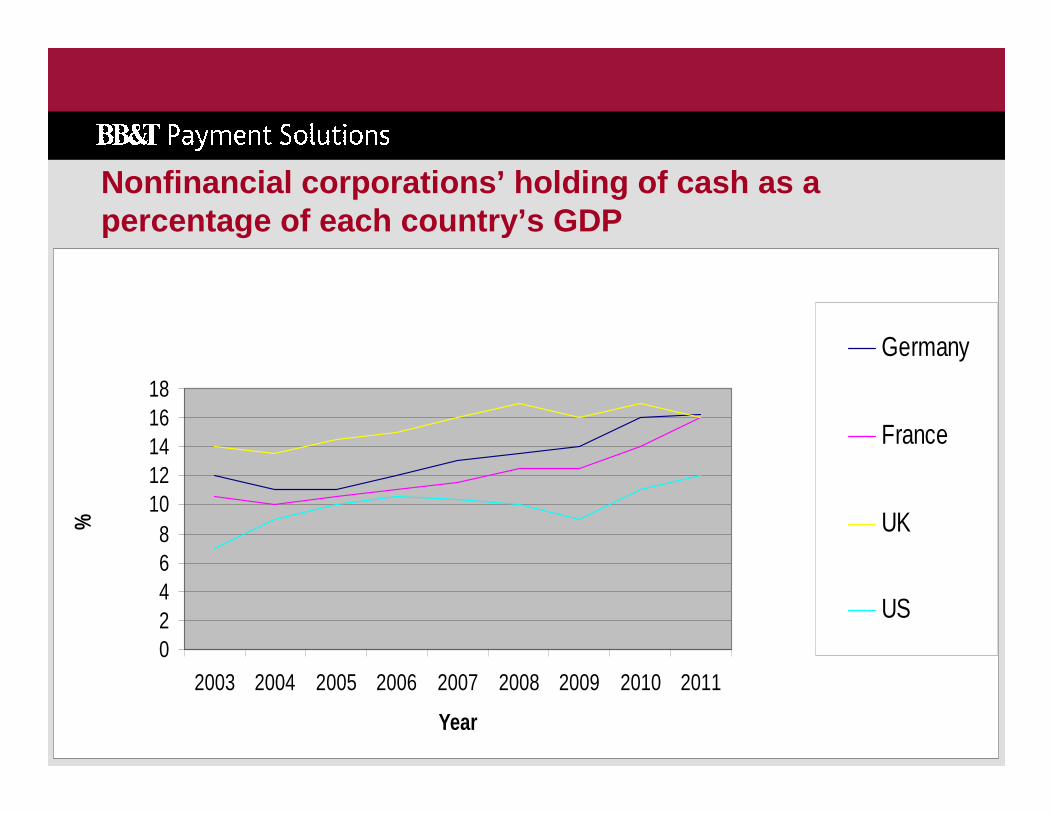

Nonfinancial corporations’ holding of cash as a percentage of each country’s GDP

02468

1012141618

2003 2004 2005 2006 2007 2008 2009 2010 2011

Year

%

Germany

France

UK

US

13

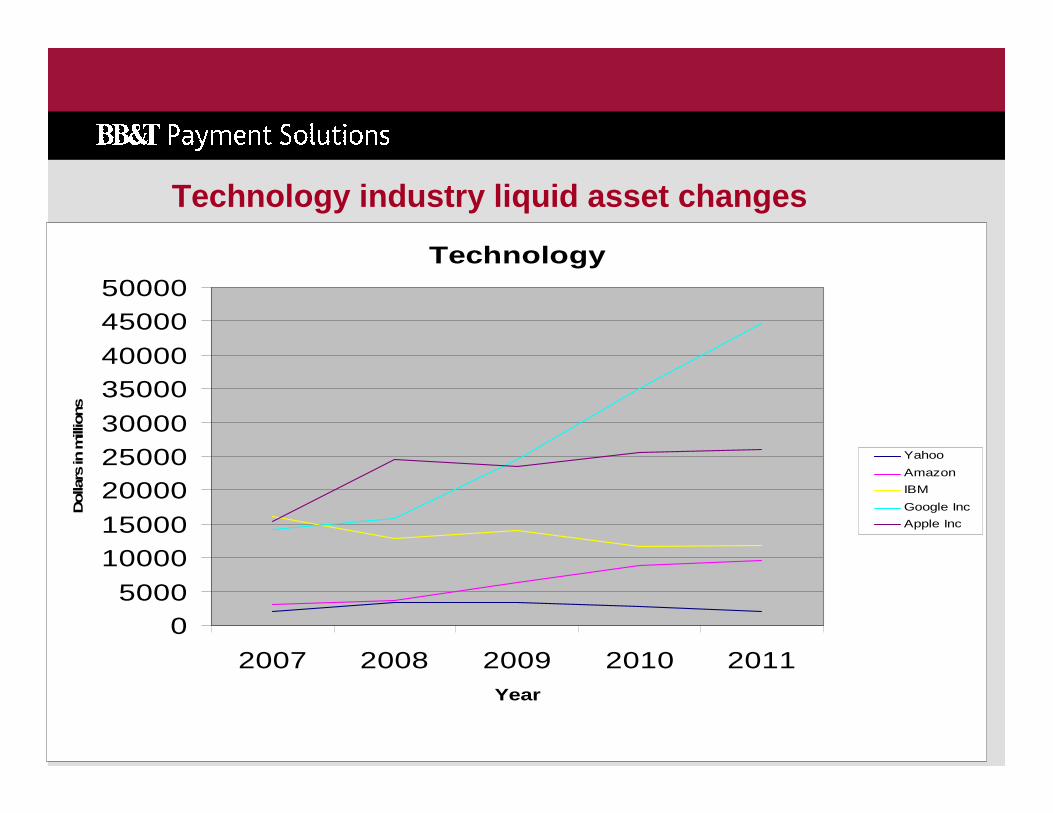

Technology industry liquid asset changes

Technology

05000

1000015000

200002500030000

3500040000

4500050000

2007 2008 2009 2010 2011Year

Dol

lars

in m

illion

s

Yahoo

Amazon

IBM

Google Inc

Apple Inc

14

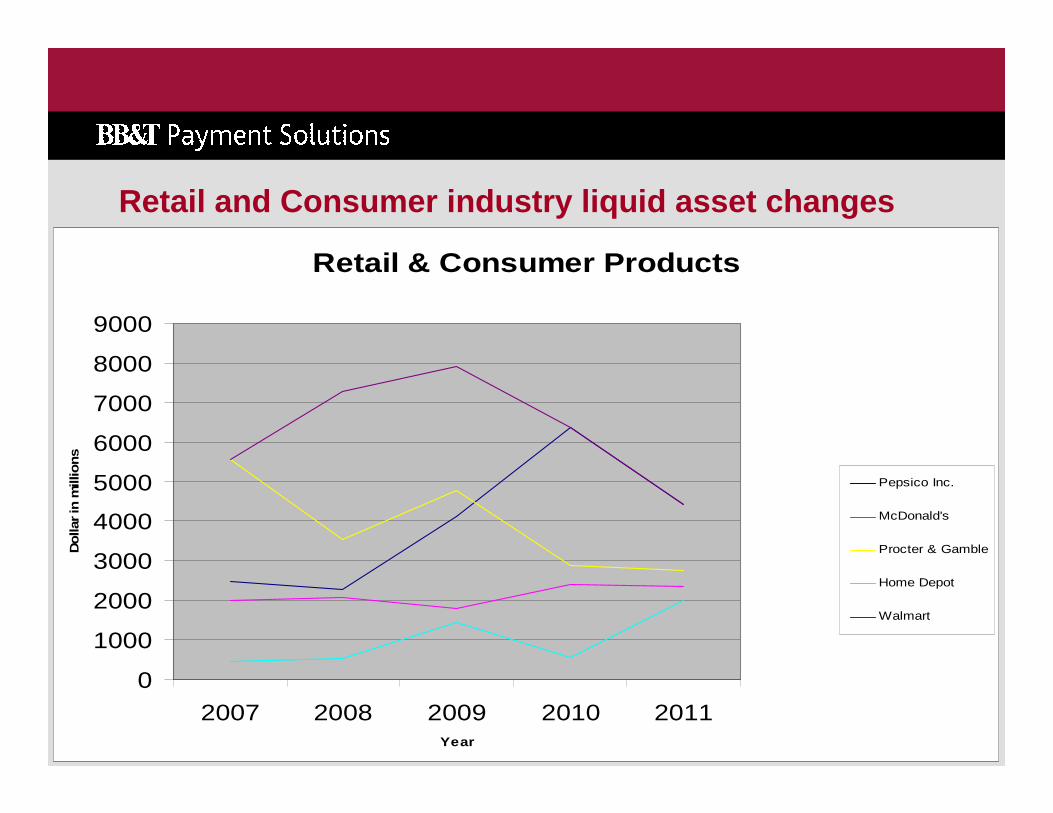

Retail and Consumer industry liquid asset changes

Retail & Consumer Products

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2007 2008 2009 2010 2011Year

Dol

lar i

n m

illio

ns

Pepsico Inc.

McDonald's

Procter & Gamble

Home Depot

Walmart

15

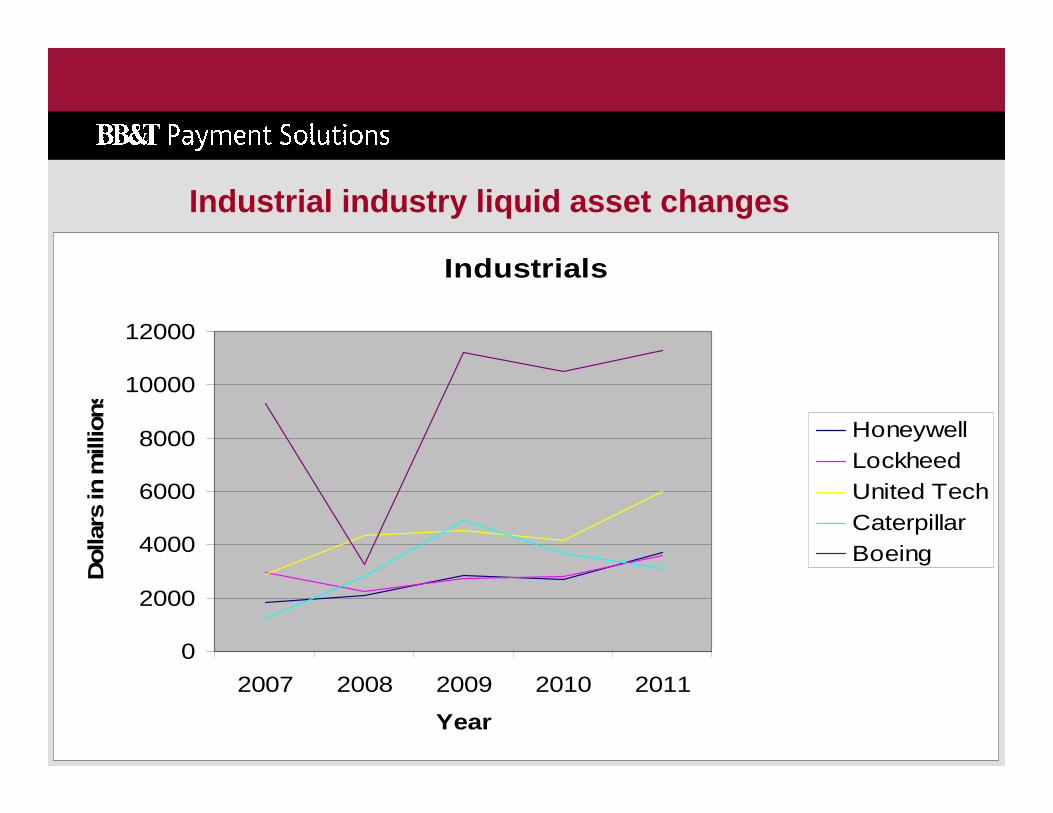

Industrial industry liquid asset changes

Industrials

0

2000

4000

6000

8000

10000

12000

2007 2008 2009 2010 2011

Year

Dol

lars

in m

illio

ns HoneywellLockheedUnited TechCaterpillarBoeing

16

Eurozone cash balances, compared to investment

0

5

10

15

20

25

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Year

% G

DP

Non FinancialCorp Holdings

Private Non-residentialInvestment

17

Facts related to the growth in corporate cash

– The latest data estimates that the cash pile is app roximately US$5.5 trillion: US$3.8 trillion in European non-fi nancial companies and US$1.7 trillion in US non-financial c ompanies.

– Corporate cash levels in the UK are nearly equal to half of its current annual GDP, and is at present, growing fast er than GDP levels

– Corporate cash levels in the U.S. and the Eurozone are growing faster than their respective GDP levels

– Over 40% of U.S. companies have raised their cash l evels in Q1 2012

– Companies in the S&P 500 have added $1.2 trillion i n cash since 2007, representing a 49% increase – Wall Street Jour nal

18

Facts related to the growth in corporate cash

� By contrast corporate business spending is up only 16% and overall hiring, only 5%, since 2007

� M&A in the first quarter of this year was the weake st for any quarter since 2003 (Bloomberg Data)

� More than half of the cash does not reside at the c orporate head office, but was sourced as overseas revenue an d remains overseas for various reasons, including unf avorable tax treatment for fund repatriation and regulatory constraints limiting the free flow of cash out of emerging mark ets.

� Corporate cash levels are at a record, and the oppo rtunity cost of not optimizing them for the intended corpor ate purpose are greater than ever

19

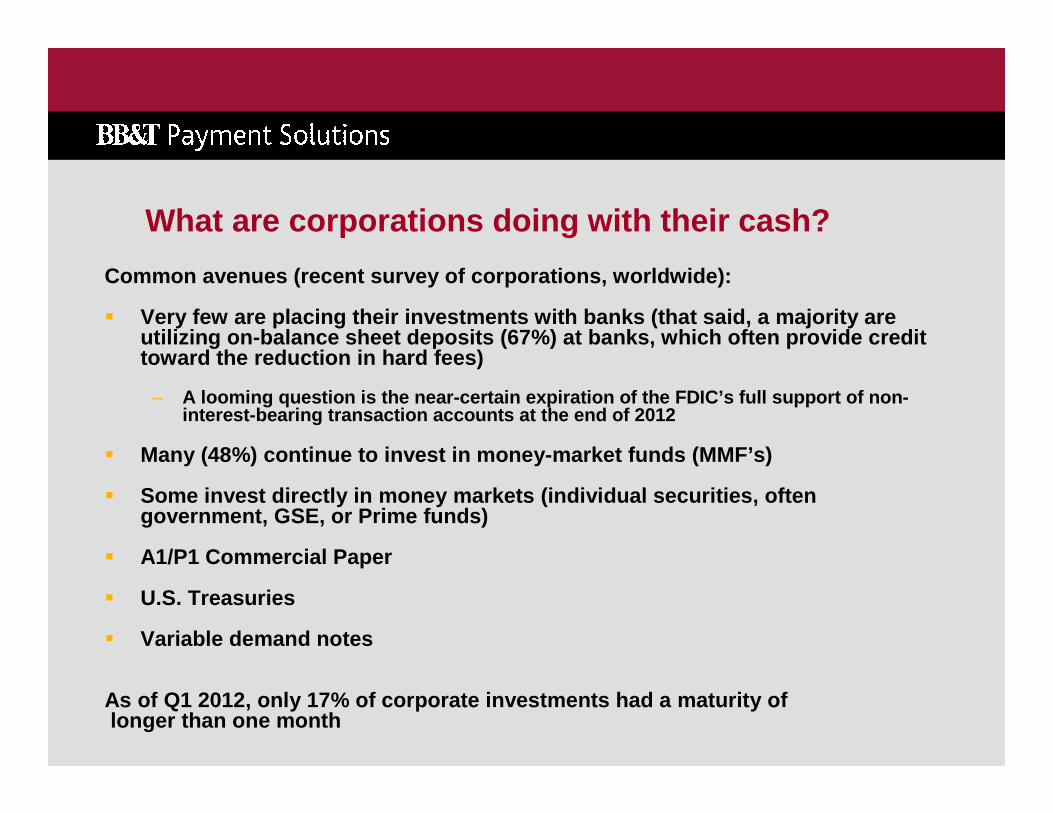

What are corporations doing with their cash?

Common avenues (recent survey of corporations, worl dwide):

� Very few are placing their investments with banks ( that said, a majority are utilizing on-balance sheet deposits (67%) at banks, which often provide credit toward the reduction in hard fees)

– A looming question is the near-certain expiration o f the FDIC’s full support of non-interest-bearing transaction accounts at the end of 2012

� Many (48%) continue to invest in money-market funds (MMF’s)

� Some invest directly in money markets (individual s ecurities, often government, GSE, or Prime funds)

� A1/P1 Commercial Paper

� U.S. Treasuries

� Variable demand notes

As of Q1 2012, only 17% of corporate investments ha d a maturity oflonger than one month

20

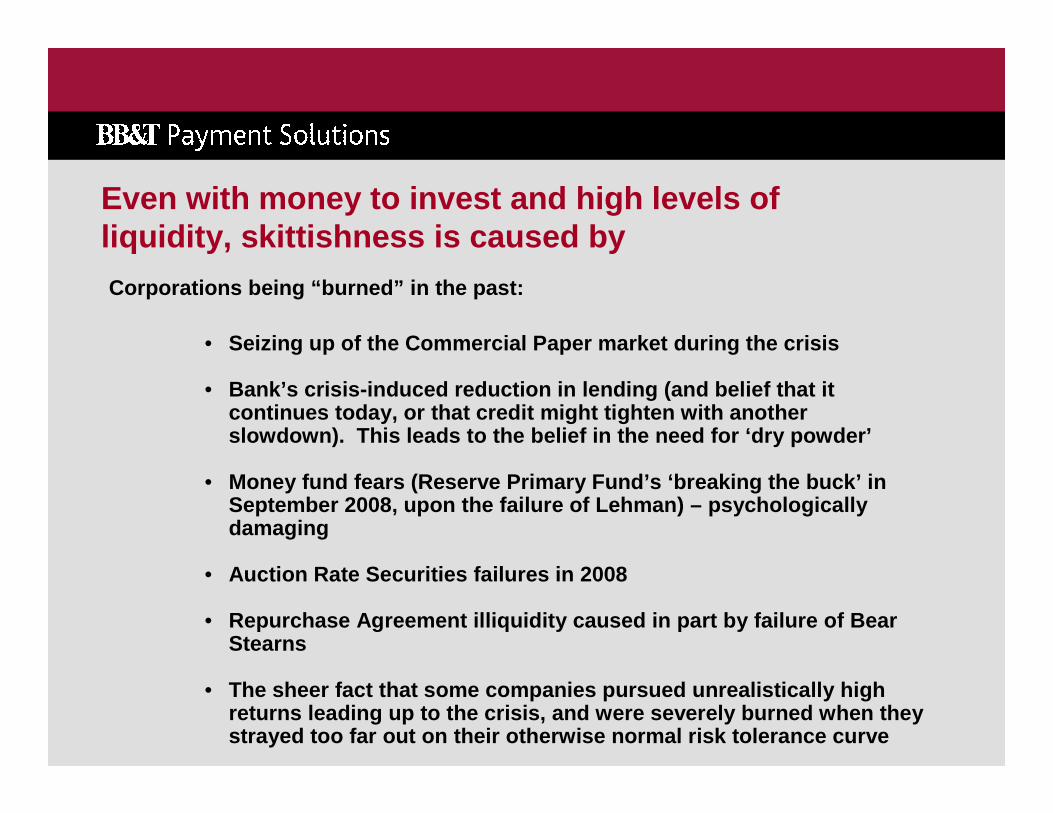

Even with money to invest and high levels of liquidity, skittishness is caused by

Corporations being “burned” in the past:

• Seizing up of the Commercial Paper market during th e crisis

• Bank’s crisis-induced reduction in lending (and bel ief that it continues today, or that credit might tighten with another slowdown). This leads to the belief in the need fo r ‘dry powder’

• Money fund fears (Reserve Primary Fund’s ‘breaking t he buck’ in September 2008, upon the failure of Lehman) – psycho logically damaging

• Auction Rate Securities failures in 2008

• Repurchase Agreement illiquidity caused in part by failure of Bear Stearns

• The sheer fact that some companies pursued unrealis tically high returns leading up to the crisis, and were severely burned when they strayed too far out on their otherwise normal risk tolerance curve

21

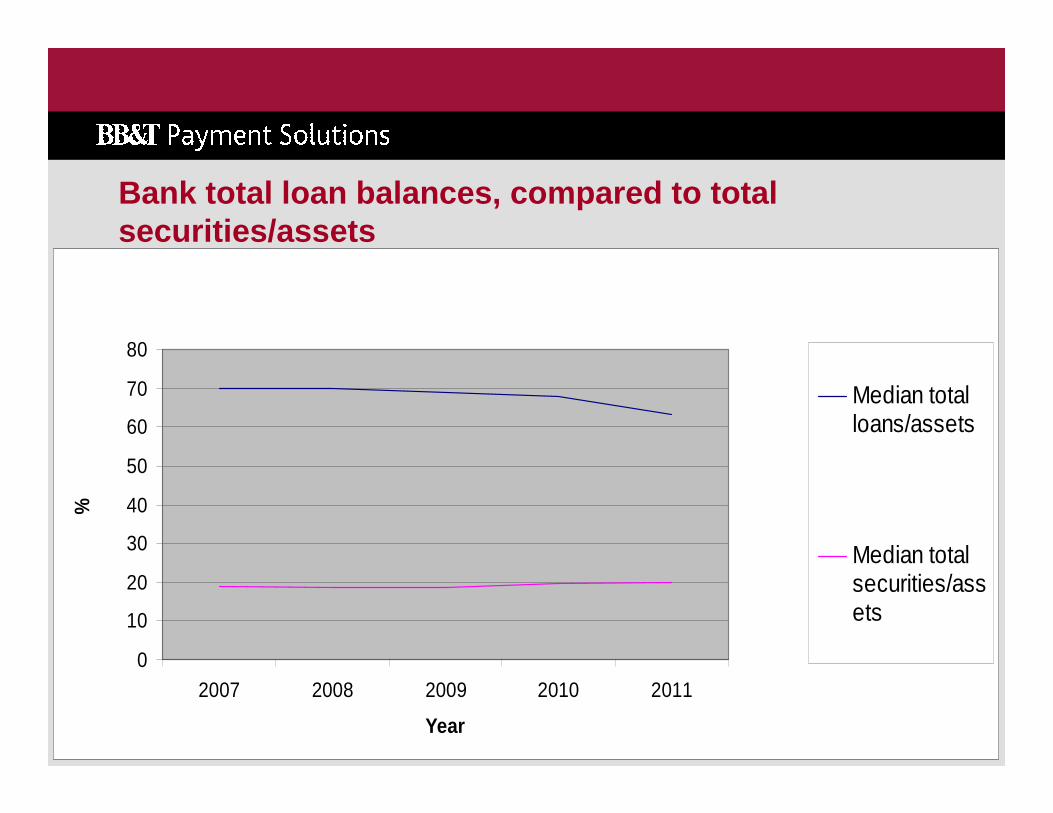

Bank total loan balances, compared to total securities/assets

0

10

20

30

40

50

60

70

80

2007 2008 2009 2010 2011

Year

%

Median totalloans/assets

Median totalsecurities/assets

22

Uncertainty is also being fueled by:

The Political Climate (both Washington and the Euro zone)

• Gridlock and vitriol that exists between Congress a nd the White House and inability to agree to a long-term plan on deficit reduction (and the size of the deficit itself)

• Uncertainty about taxation of business income in 20 12 and beyond

• Uncertainty regarding the appropriateness and ultim ate success of The Federal Reserve’s QE 1, QE 2 and Operation Twis t liquidity actions to spur the economy

• Concurrent uncertainty surrounding the initiation o f a possible QE 3 to further inject liquidity into the economy, follo wing the sunset of ‘Twist’ in June 2012

• Longer-term uncertainty with regard to the Fed’s pr onouncement that S/T interest rates will remain low through 2014

23

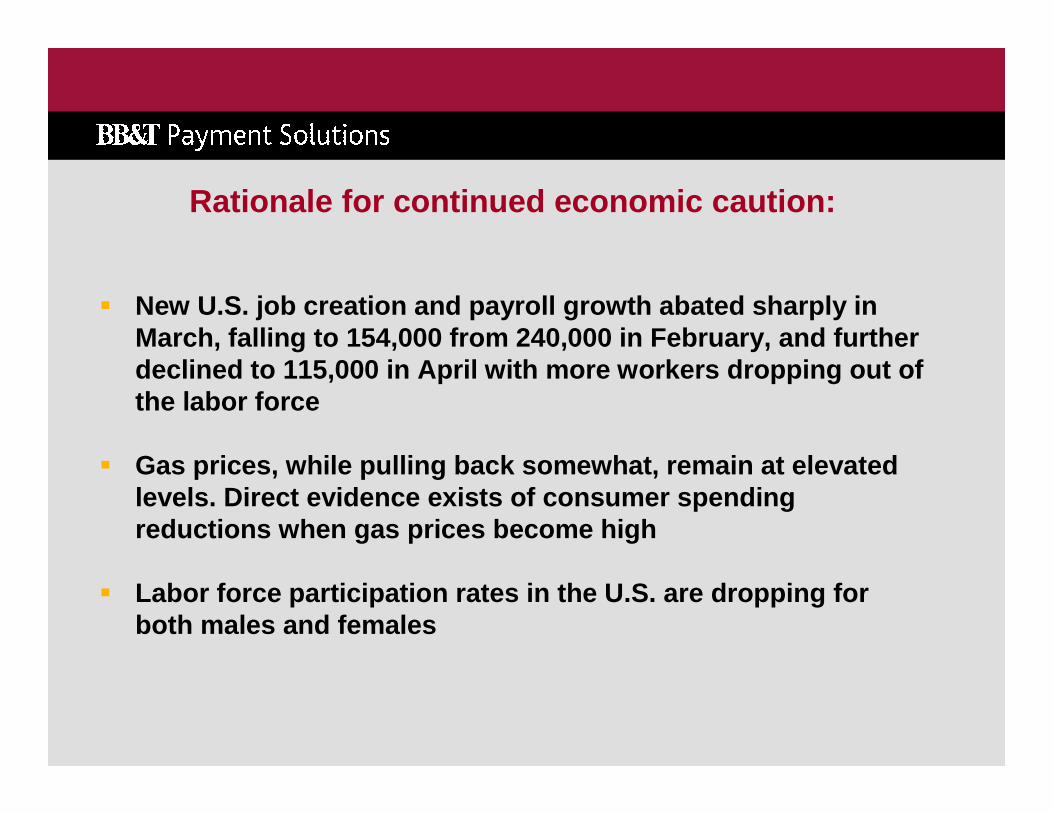

Rationale for continued economic caution:

� New U.S. job creation and payroll growth abated sha rply in March, falling to 154,000 from 240,000 in February, and further declined to 115,000 in April with more workers drop ping out of the labor force

� Gas prices, while pulling back somewhat, remain at elevated levels. Direct evidence exists of consumer spending reductions when gas prices become high

� Labor force participation rates in the U.S. are dro pping for both males and females

24

Rationale for continued economic caution:

� As mentioned, toxic and divisive policy climate in Washington and in much of the Eurozone, coupled with major ele ctoral changes/contests (China; France; Greece; Germany, U .S.; Russia)

� Continued economic slowdown in China off of histori c highs

� Significant Eurozone challenges:

– 17-Member Eurozone unemployment approaches 11%, the highest since the currency was introduced in 1999 ( as comparison, unemployment in March 2011 was 9.9%)

– Eurozone GDP growth is zero at present, with 8 of 1 7 Euro zone countries in recession

25

The Eurozone� In December, the European Central Bank (ECB) flooded banks

with more that 1 trillion euros ($1.31 trillion), returning interest rates to a record low 1%

� For the time being, this allayed fears of a disorderly breakup of the 17-nation currency union

� Hot spots, such as Spain, Italy, Greece and Portugal still remain, with sovereign and corporate downgrades and historic high bond yields continuing, which continues to highlight the financial challenges of some

� There is the belief that the healthy (Germany and France) will need to continue supporting the weaker countries for quite some time to support the financial firewall and to prevent a breakup of the Euro. France’s continued support is in doubt at present

� Ominously, a noted analyst has recently predicted that by 2013, there is a 75% chance that Greece will exit from the Euro – also the Troika publicly cancelled a recent visit to Greece, due to disagreements

26

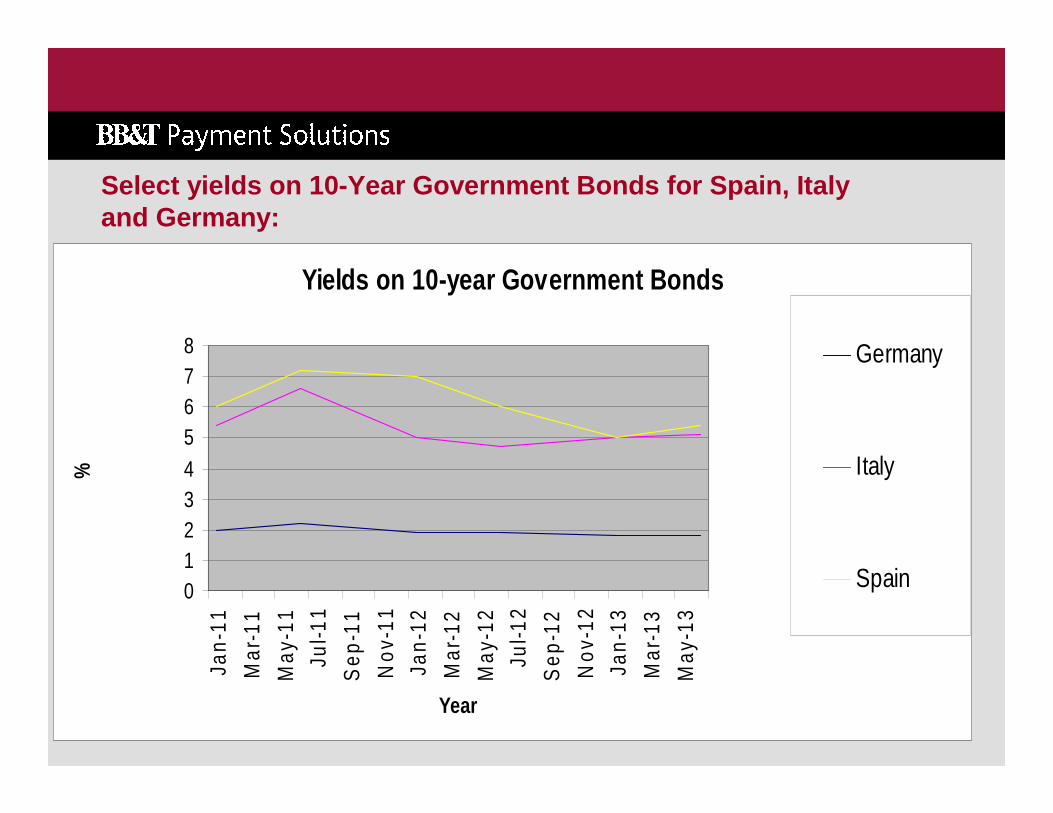

10-year Bond yields of select Eurozone countries (May 15, 2012):

– Greece: 29.40%

– Portugal: 11.42%

– Ireland: 8.21

– Spain: 6.28%

– Italy: 5.91%

– France: 2.83%

– Germany: 1.46%

By comparison,

– United States: 1.75%

– UK: 1.88%

27

Select yields on 10-Year Government Bonds for Spain , Italy and Germany:

Yields on 10-year Government Bonds

012345678

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep

-11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep

-12

Nov

-12

Jan-

13

Mar

-13

May

-13

Year

%

Germany

Italy

Spain

28

Euro/USD movement Thru mid-May 2012

29

Spain:

� Euro’s fourth largest economy, behind Germany, France and Italy (World Bank GDP)

� Of recent, confidence levels in Spain’s ability to weather the current crisis has continually eroded

� Overall unemployment presently stands at 25%, and approaching 50% for certain age groups

� Spain’s IBEX stock index is down over 30% YTD

� In late April, Spain became the 12th European nation to report at least two quarters of declining GDP (classic definition of recession)

� Reuters reports that the Spanish government expects its economy will contract by 1.7% in 2012

30

Rationale for optimism in the economy

� Ratio of liquid assets to short-term liabilities is the highest since 1954 (Federal Reserve)

� Consumer sentiment appears to be largely holding it s own (even with gas prices near highs) – (Univ. of Michigan)

� Consumer loan delinquencies fell across the board i n Q4 2011; the first time this has occurred in 8 years (American Bankers Assn.)

� Also in Q4 2011 total household financial obligatio ns fell to a 28-year low, when measured against disposable income (15.9%), In Q3 2007, the start of the recession/financial crisis, this ratio reach ed a record 18.9% (Federal Reserve)

� U.S manufacturing in April reached a four year high

� Productivity levels remain high and have trended hi gher

31

Rationale for optimism in the economy

� Arguably the secondary issue of importance in the U S economy –housing - seems to be showing signs of life, in pock ets, with positive housing starts and lower than expected for eclosures

� Surveys show that a far greater percentage of compa nies are receiving credit from banks than they were 18 month s ago

� In early May, Greece’s debt was actually upgraded b y Standard & Poors – in part, highlighting improved economic prog ress, in part highlighting the all to rapid pace that ‘swallows’ t he ability for ratings agencies to keep up

� According to a very recent Q2 survey, a majority of U.S. CFO’s expect the economy to expand in 2012, and anticipa te increases in hiring, higher revenues and profits

� Manufacturing in Germany is nearing historic high, due in large part to non Eurozone demand

32

Key Investment-related challenges/concerns facing corporate Treasurers today

� Of the most significant challenges faced by corpora te treasurers, and cash managers today, the ability to consistentl y and accurately forecast cash flow ranks at or near the top of the list

� Mentality of cash preservation, almost irrespective of yield

� Choices/decisioning in a highly uncertain macroecon omic and regulatory environment

� Finding the appropriate repositories for cash and m aintaining access to liquidity

� Transparency of investment type, counterparty, sove reign and liquidity risks cause many firms to default toward choosing the safest (near) risk-free investments with near zero to negative real returns – opportunity cost in and of itself

33

Key Investment-related challenges/concerns facing Treasurers today� Importantly, there is the increasing belief – backed by recent study

results - that cash investment policies and practice s need to be updated due to impending regulatory and other chang es

� Effective utilization of cash pooling structures to increase visibility and control of funds held with multiple banking par tners and/or in disparate countries/regions

� Understanding the impact and new leverage ratios re quired by Basel III global standards, - which I discuss in brief on the next page

� Understanding the impact of the impending regulator y changes including Dodd-Frank, particularly in areas such as SEC-driven pending changes in money market funds structures

� Following closely the developments in the Shadow Ba nking System,especially in light of recently-announced mark to m arket trading losses

34

Basel III potential impact

Basel III, what is it?

� Institutes minimum capital adequacy rules for banks � Phase in process, but with CCAR and other capital s ufficiency

‘tests’, banks clearly are already thinking about t his today in their mid- to long-term strategic plans

Why is this potentially material for investors?

� Under Basel III, stable corporate balances have the greatest value from a bank’s point of view

� “Discretionary” balances will attract lower returns since bank’s holding these deposits will have higher capi tal requirements to ensure sufficient liquidity in time s of stress

� This in time might lead to a reduction in return fo r discretionary balances, and might push treasurers t o search elsewhere for safe yield

35

Basel III

� Alternative investment products as an outgrowth of Basel III have been tested

– Products that pay bonus accruals of interest retroactively, for balances which stay within a certain range during a particular period

– Term products might be of lesser potential interest in this environment, for fear of being locked into an investment in a continuing volatile environment

36

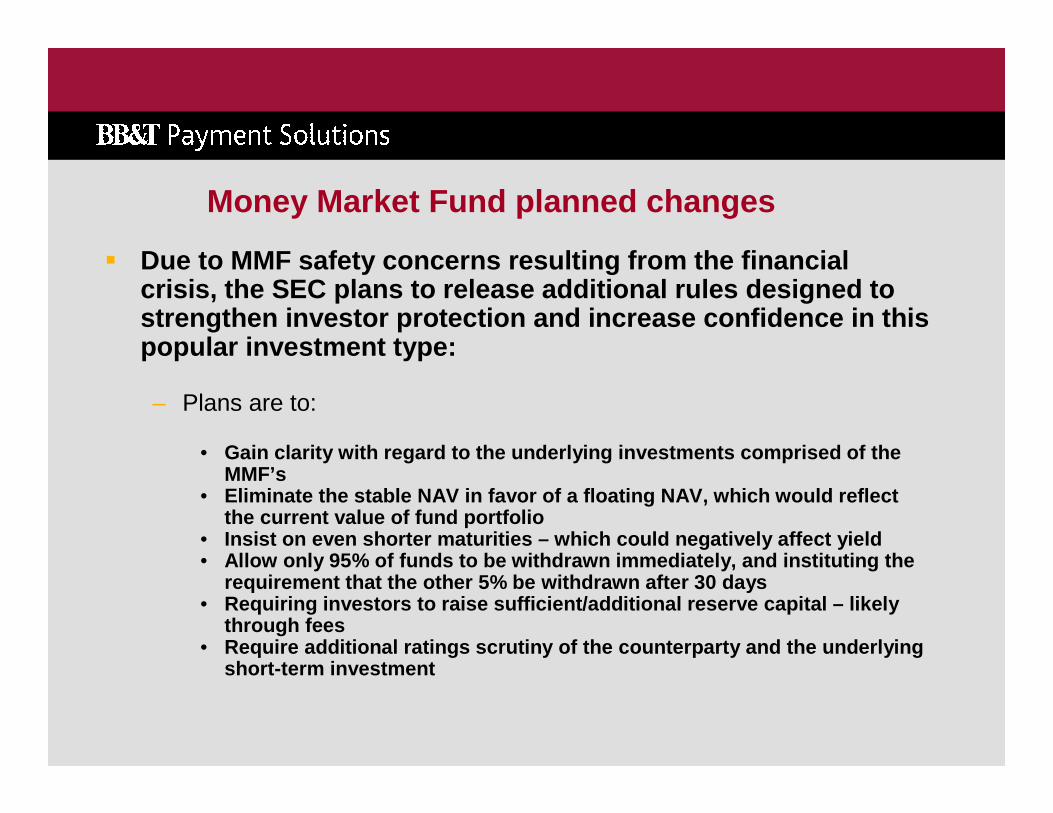

Money Market Fund planned changes

� Due to MMF safety concerns resulting from the finan cial crisis, the SEC plans to release additional rules d esigned to strengthen investor protection and increase confide nce in this popular investment type:

– Plans are to:

• Gain clarity with regard to the underlying investme nts comprised of the MMF’s

• Eliminate the stable NAV in favor of a floating NAV , which would reflect the current value of fund portfolio

• Insist on even shorter maturities – which could nega tively affect yield• Allow only 95% of funds to be withdrawn immediately , and instituting the

requirement that the other 5% be withdrawn after 30 days• Requiring investors to raise sufficient/additional reserve capital – likely

through fees• Require additional ratings scrutiny of the counterp arty and the underlying

short-term investment

37

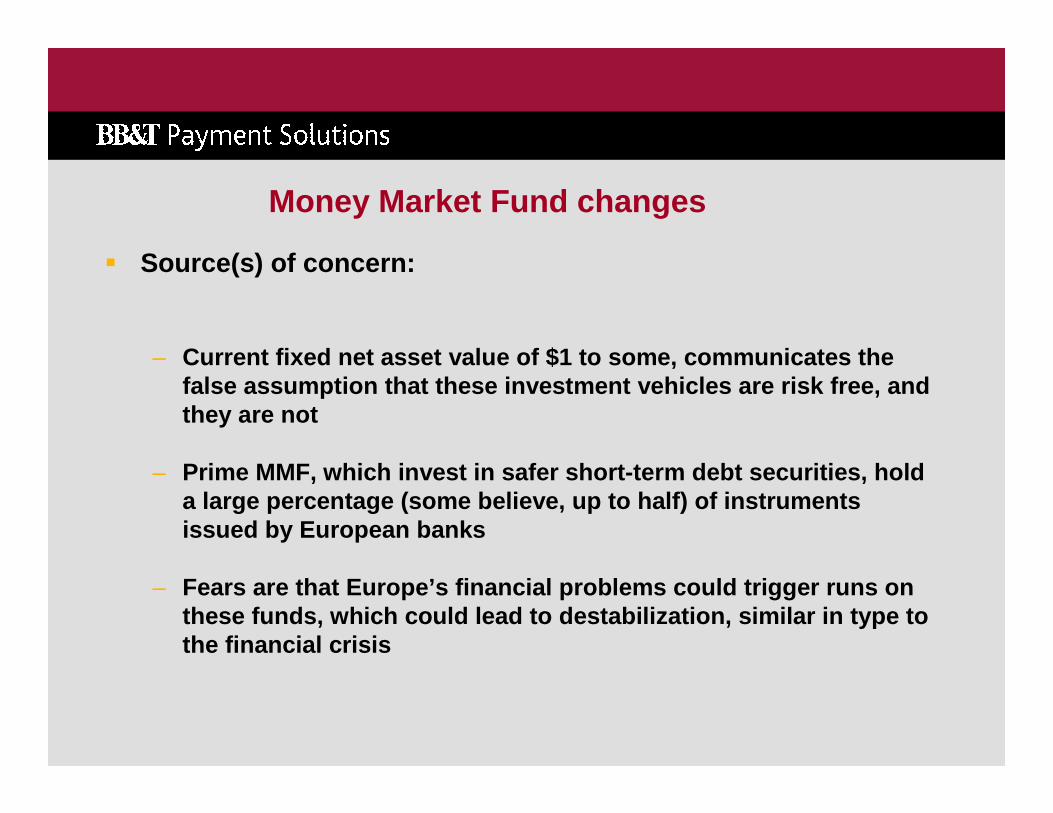

Money Market Fund changes

� Source(s) of concern:

– Current fixed net asset value of $1 to some, commun icates the false assumption that these investment vehicles are risk free, and they are not

– Prime MMF, which invest in safer short-term debt se curities, hold a large percentage (some believe, up to half) of in struments issued by European banks

– Fears are that Europe’s financial problems could tr igger runs on these funds, which could lead to destabilization, s imilar in type to the financial crisis

38

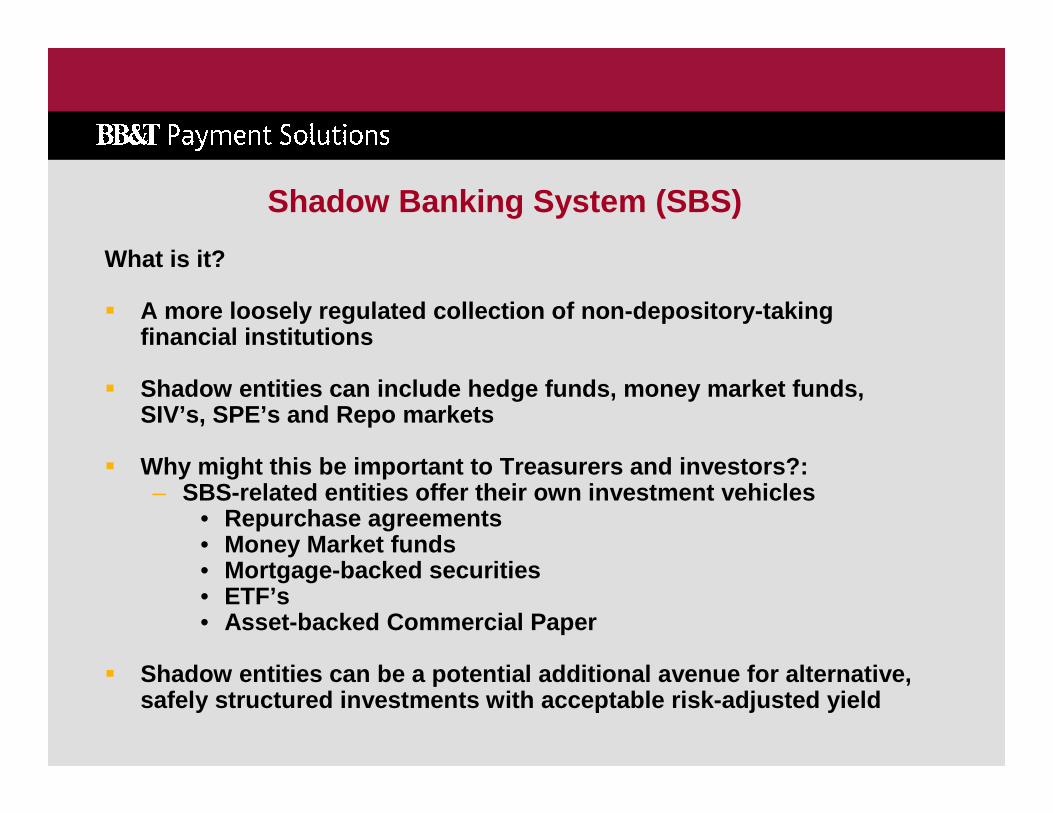

Shadow Banking System (SBS)

What is it?

� A more loosely regulated collection of non-deposito ry-taking financial institutions

� Shadow entities can include hedge funds, money mark et funds, SIV’s, SPE’s and Repo markets

� Why might this be important to Treasurers and inves tors?:– SBS-related entities offer their own investment veh icles

• Repurchase agreements• Money Market funds• Mortgage-backed securities• ETF’s• Asset-backed Commercial Paper

� Shadow entities can be a potential additional avenu e for alternative, safely structured investments with acceptable risk- adjusted yield

39

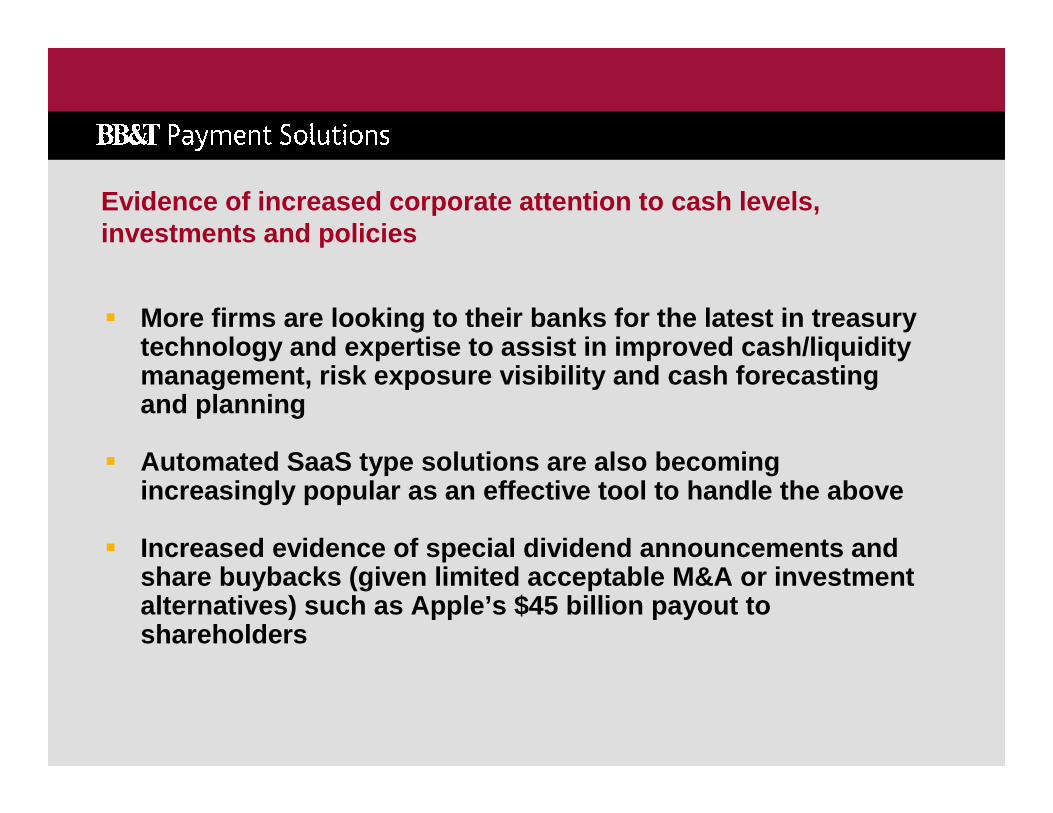

Evidence of increased corporate attention to cash l evels, investments and policies

� More firms are looking to their banks for the lates t in treasurytechnology and expertise to assist in improved cash /liquidity management, risk exposure visibility and cash forec asting and planning

� Automated SaaS type solutions are also becoming increasingly popular as an effective tool to handle the above

� Increased evidence of special dividend announcement s and share buybacks (given limited acceptable M&A or inv estment alternatives) such as Apple’s $45 billion payout to shareholders

40

Investment Policy Best Practices

� Companies that have not yet adopted a formal invest ment policy should craft one immediately

� Many corporations have had investment policies for years yet have failed to update or refresh to reflect the reality of the times

� When doing this, consult with the firm’s outside co nsultants and financial advisors (bankers, CPA’s), as needed

� Investment policies need to be carefully tailored t o appropriately balance the obvious trade-offs between the preserva tion of capital and return

� Investment policies, once formulated, need to be pe riodically reviewed on a more frequent, formalized basis, by m anagement

41

Investment policy best practices, continued

� Discussion with and approval by an independent boar d of directors (or a committee thereof) is crucial

� Finalized & approved investment policies should als o be communicated with the firm’s outside financial advi sors to better ensure that ongoing decisions are made in ac cordance with the policy

� Pay close attention to the quality of financial adv isors and themanner in which they are compensated (commission; success rate?)

� A tight fiduciary relationship with a FA ensures tr ansparency with respect to risk and accountability with respec t to performance

42

Investment policy best practices, continued

� Counterparty risk is more important than ever (OK t o invest with an entity that has a lower credit rating than you?)

� When making investment decision - either solo or wit h an FA - close attention needs to be paid to the actual stated mat urities and true liquidity of purchased securities, to ensure these are matched to working capital needs of the firm (historical Aucti on Rate debacle/MF Global)

� Reality of financial crisis and today is that ratin gs agencies’published ratings represent a ‘rear-window data’ poi nt with regard to safety and soundness, not a leading or concurrent d ata point

� Some believe that a permanent ‘buffer’ of liquid cas h should be kept as a hedge against a counter party or macroeconomic systemic shock, irrespective of chosen strategy?

43

Investment policy best practices, continued

� In the new ‘normal’ environment, investment manageme nt decisions need to be influenced by institutional AND sovereig n credit ratings

� Ask yourself, do hard and sometimes difficult conve rsations need to be held with counterparties in an effort to cull & rationalize, in order to gain additional control, based on ratings or ris k?

Importantly, investment management consideration is not solely relegated to operating entities:

� Often, M&A requires certain proceeds to be escrowed for a year or more, post closing

� While enormous due diligence usually accompanies th e M&A transaction itself, scant attention is paid to the credit worthiness of the escrow agent, the investment criteria/quality o r flexibility in movement of funds, if needed, due to safety concern s

44

Conclusion

The enormous increase in corporate cash, as highlig hted, andthe volatility of global market conditions during t he past fouryears has served as a catalyst for the birth of a n ew generationof treasury strategies, priorities and models. Incr eased economicuncertainty has made it extremely challenging for t reasurers toforecast short- and intermediate-term cash positions , therebyIncreasing the importance and value of liquidity.

As in any fiduciary relationship, but especially no w, the value oftrue partnership and agnostic consultative guidance betweencompanies and their advisors cannot be overestimate d.

45

Thank you!