Embed Size (px)

Citation preview

The Magic of Analytics John Wallhoff (CISA, CISM, CISSP)

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

The Magic of Analytics

…

when data comes

alive

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

The Magic of Analytics

…

when data

transforms into information, knowledge

and wisdom

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

The Magic of Analytics

…

when you can see beyond

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

The Magic of Analytics

…

now what is

your story?

The Magic of Analytics

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

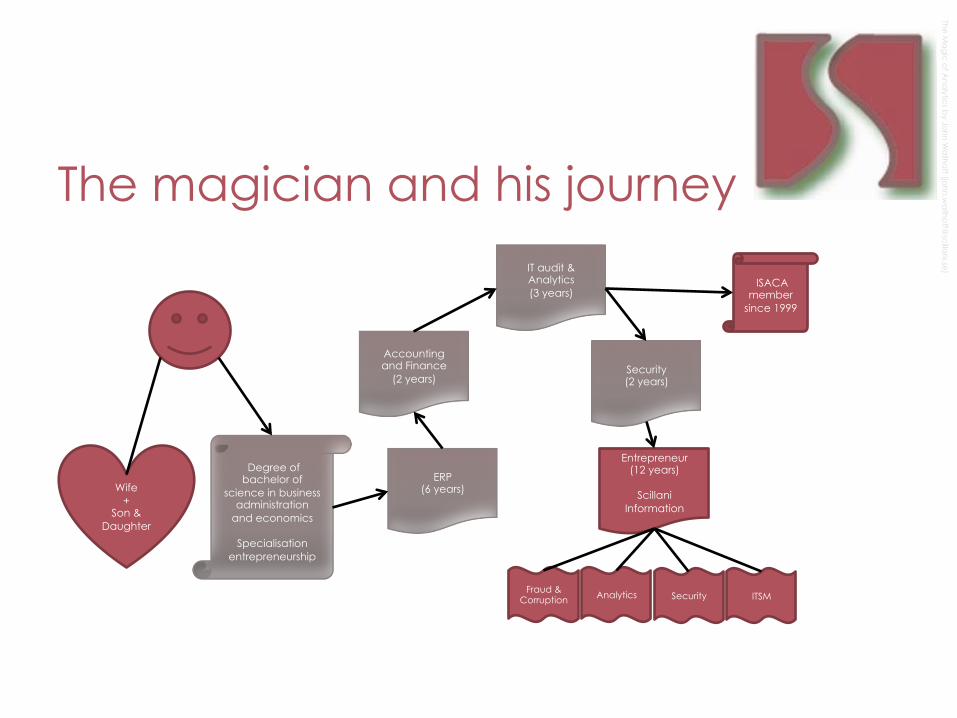

The magician and his journey

Wife

+ Son &

Daughter

Degree of bachelor of

science in business administration

and economics

Specialisation entrepreneurship

ERP (6 years)

Accounting and Finance

(2 years)

IT audit & Analytics (3 years)

Security (2 years)

Entrepreneur (12 years)

Scillani

Information

Fraud & Corruption Analytics Security ITSM

ISACA member

since 1999

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

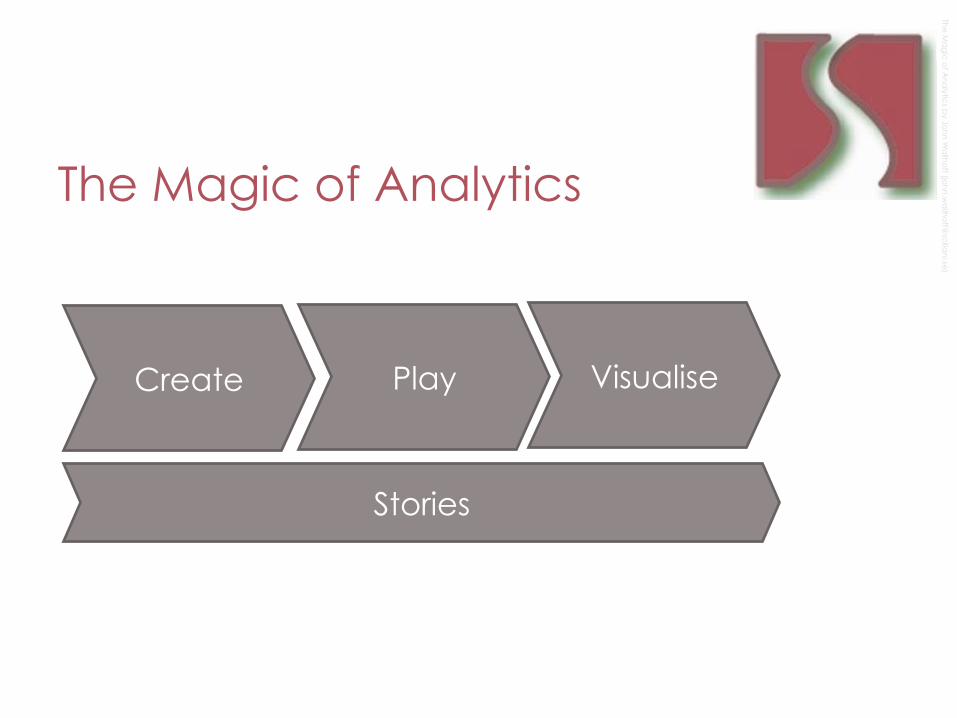

The Magic of Analytics

Create Play Visualise

Stories

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Create

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

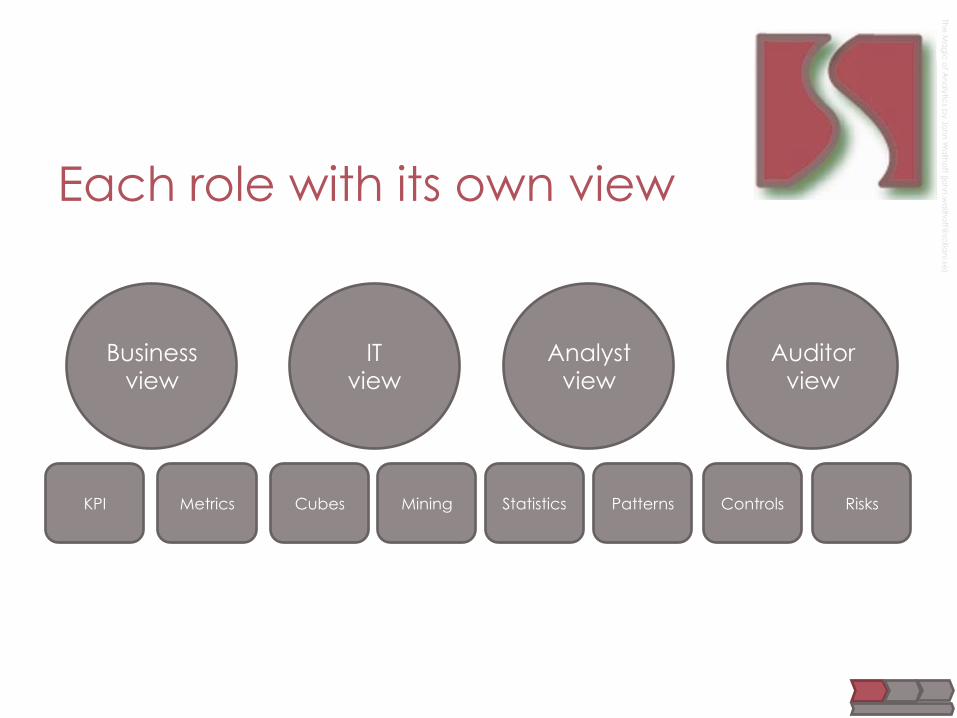

Each role with its own view

Business view

IT view

Analyst view

Auditor view

Metrics KPI Cubes Statistics Patterns Controls Risks Mining

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

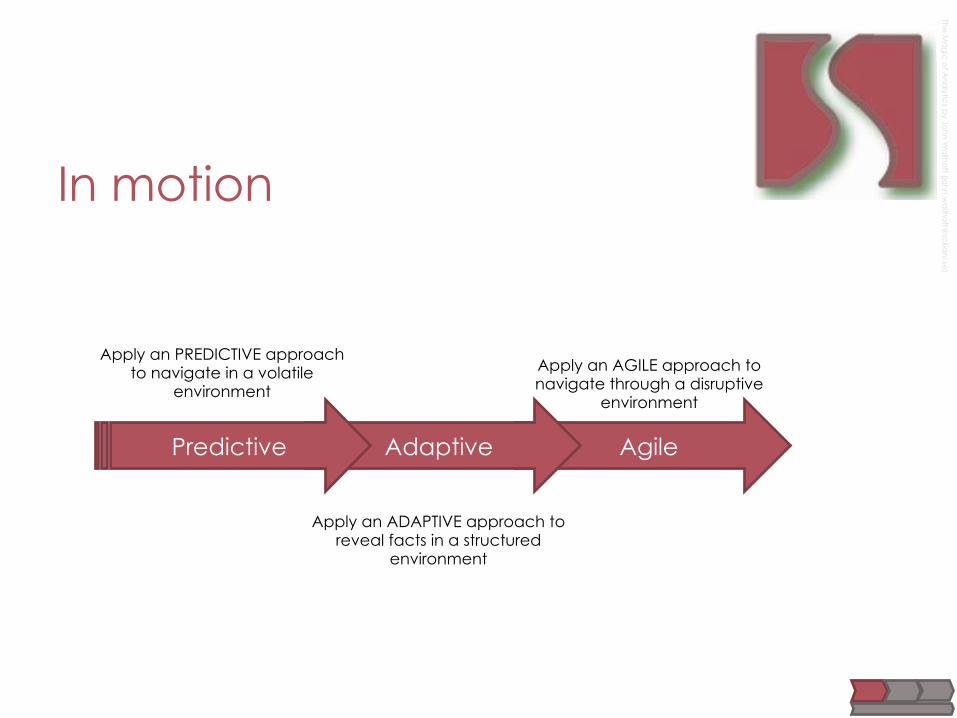

In motion

Agile

Apply an PREDICTIVE approach to navigate in a volatile

environment

Apply an ADAPTIVE approach to reveal facts in a structured

environment

Apply an AGILE approach to navigate through a disruptive

environment

Adaptive Predictive

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

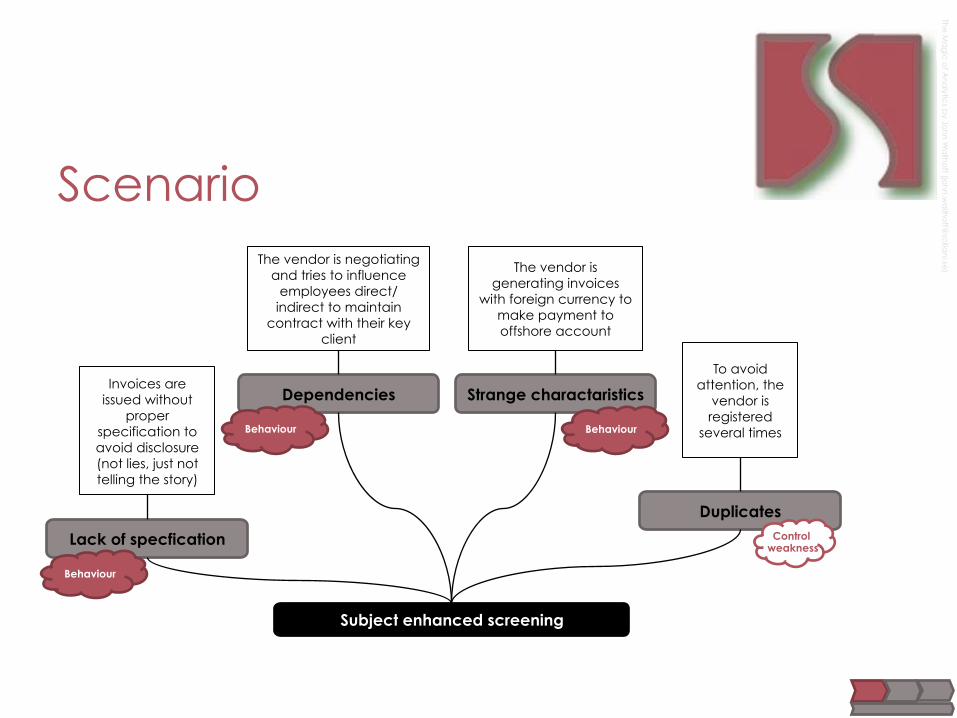

Scenario

Subject enhanced screening

Dependencies Strange charactaristics

Duplicates

Lack of specfication

The vendor is negotiating and tries to influence

employees direct/indirect to maintain

contract with their key client

Invoices are issued without

proper specification to avoid disclosure (not lies, just not telling the story)

The vendor is generating invoices

with foreign currency to make payment to offshore account

To avoid attention, the

vendor is registered

several times

Control weakness

Behaviour

Behaviour Behaviour

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

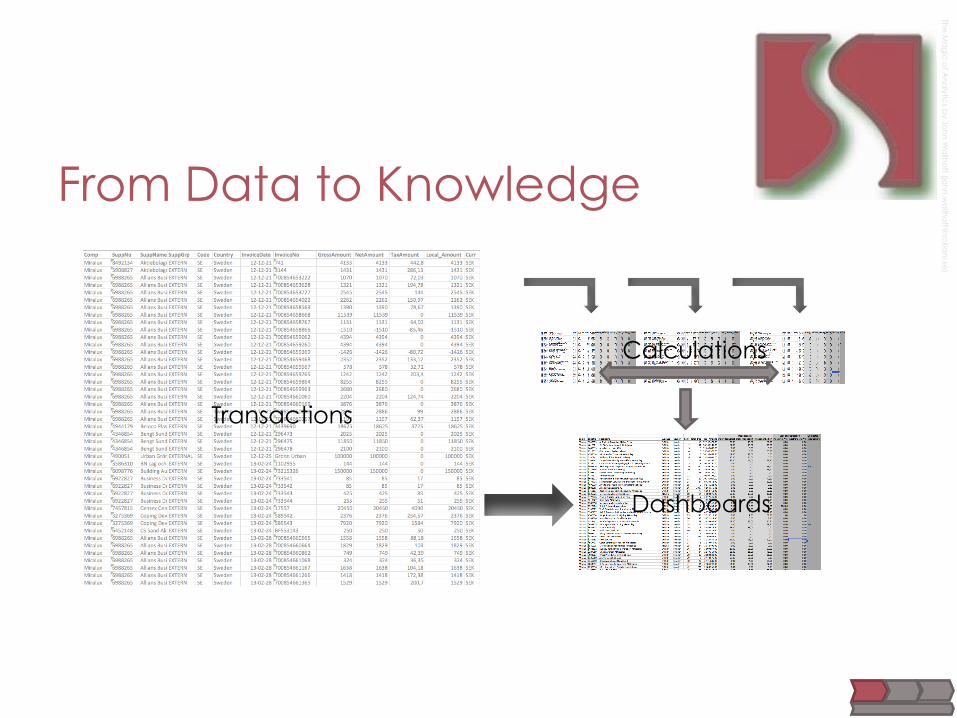

From Data to Knowledge

Transactions

Dashboards

Calculations

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

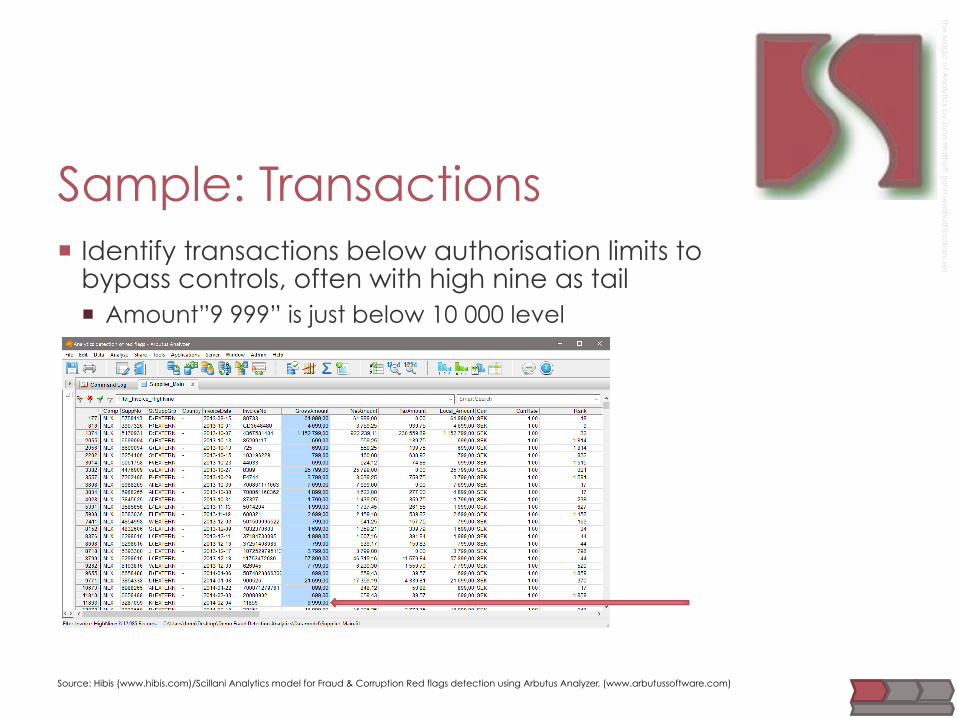

Sample: Transactions ¡ Identify transactions below authorisation limits to

bypass controls, often with high nine as tail ¡ Amount”9 999” is just below 10 000 level

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

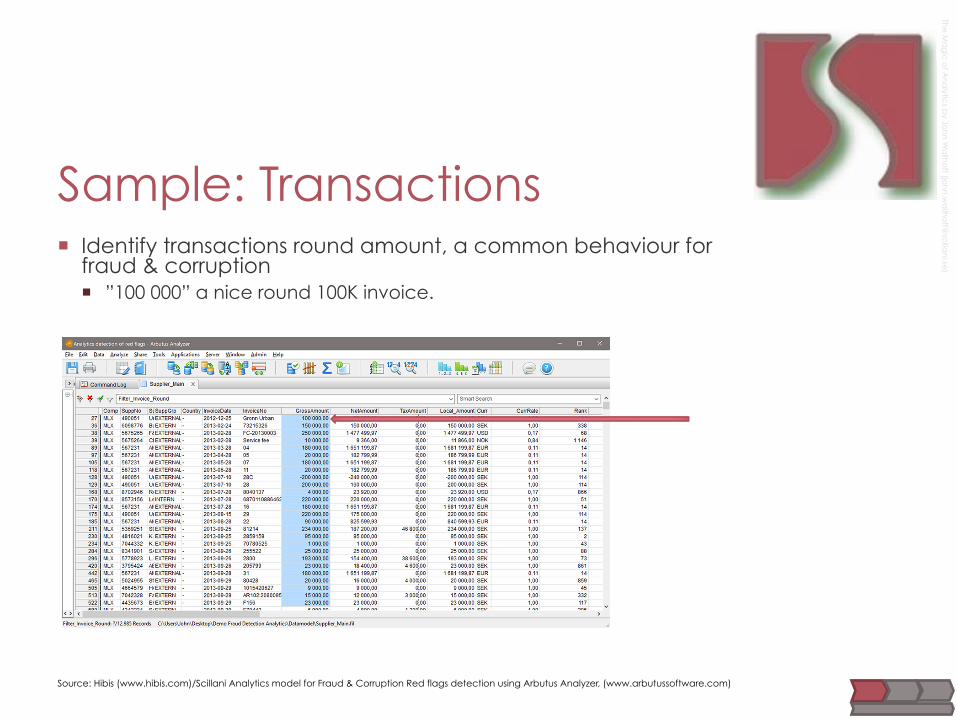

Source: Hibis (www.hibis.com)/Scillani Analytics model for Fraud & Corruption Red flags detection using Arbutus Analyzer, (www.arbutussoftware.com)

Sample: Transactions ¡ Identify transactions round amount, a common behaviour for

fraud & corruption ¡ ”100 000” a nice round 100K invoice.

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Source: Hibis (www.hibis.com)/Scillani Analytics model for Fraud & Corruption Red flags detection using Arbutus Analyzer, (www.arbutussoftware.com)

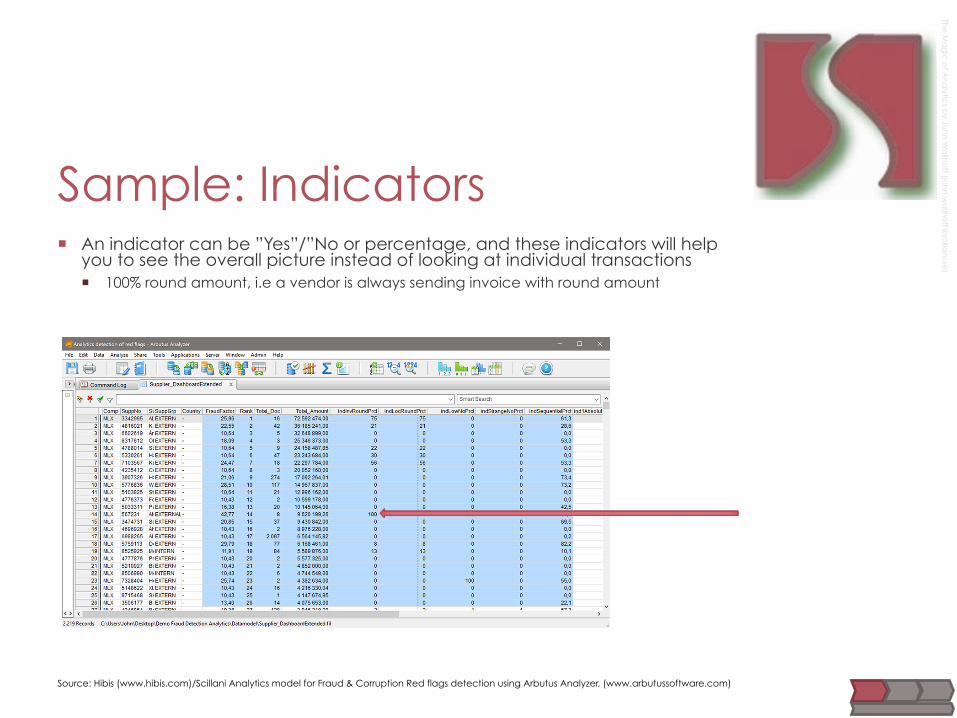

Sample: Indicators ¡ An indicator can be ”Yes”/”No or percentage, and these indicators will help

you to see the overall picture instead of looking at individual transactions ¡ 100% round amount, i.e a vendor is always sending invoice with round amount

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Source: Hibis (www.hibis.com)/Scillani Analytics model for Fraud & Corruption Red flags detection using Arbutus Analyzer, (www.arbutussoftware.com)

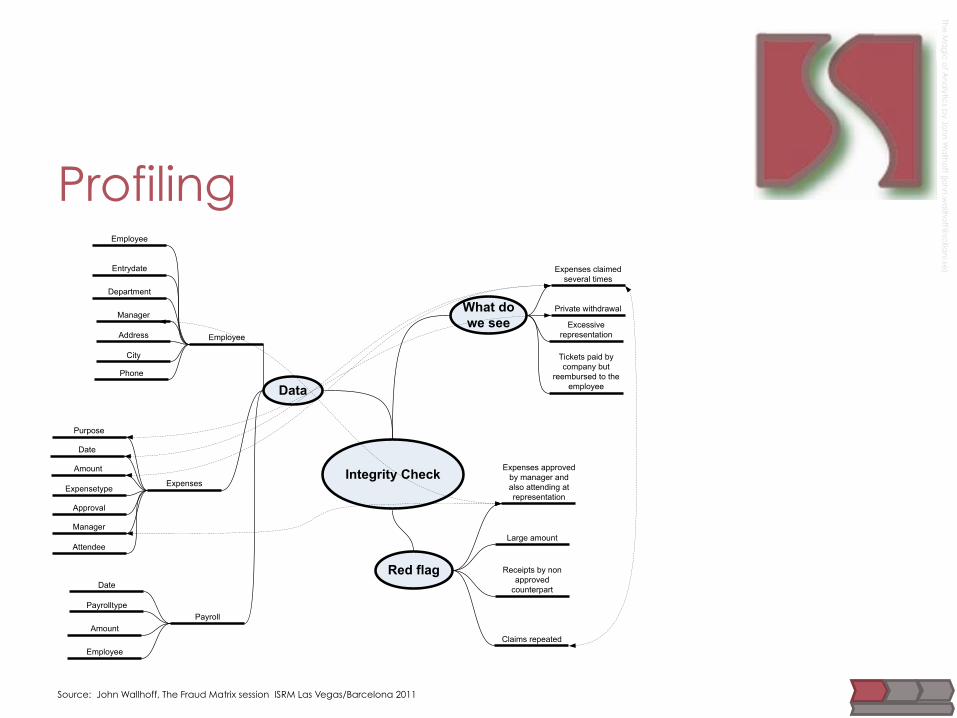

Profiling

Integrity Check

Data

Red flag

What do we see

Employee

Expenses

Payroll

Large amount

Expenses approved by manager and also attending at representation

Receipts by non approved

counterpart

Attendee

Manager

Approval

Expensetype

Amount

Date

Purpose

Claims repeatedEmployee

Date

Payrolltype

Amount

Employee

Entrydate

Department

Manager

Address

City

Phone

Expenses claimed several times

Private withdrawal

Excessive representation

Tickets paid by company but

reembursed to the employee

Source: John Wallhoff, The Fraud Matrix session ISRM Las Vegas/Barcelona 2011

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Storytelling Characteristics of a good story

¡ A single theme, clearly defined

¡ A well developed plot

¡ Style: vivid word pictures, pleasing sounds and rhythm

¡ Characterization

¡ Faithful to source

¡ Dramatic appeal

¡ Appropriateness to listeners

Source: Effective Storytelling, A manual for beginners by Barry McWilliams, http://www.eldrbarry.net/roos/eest.htm

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

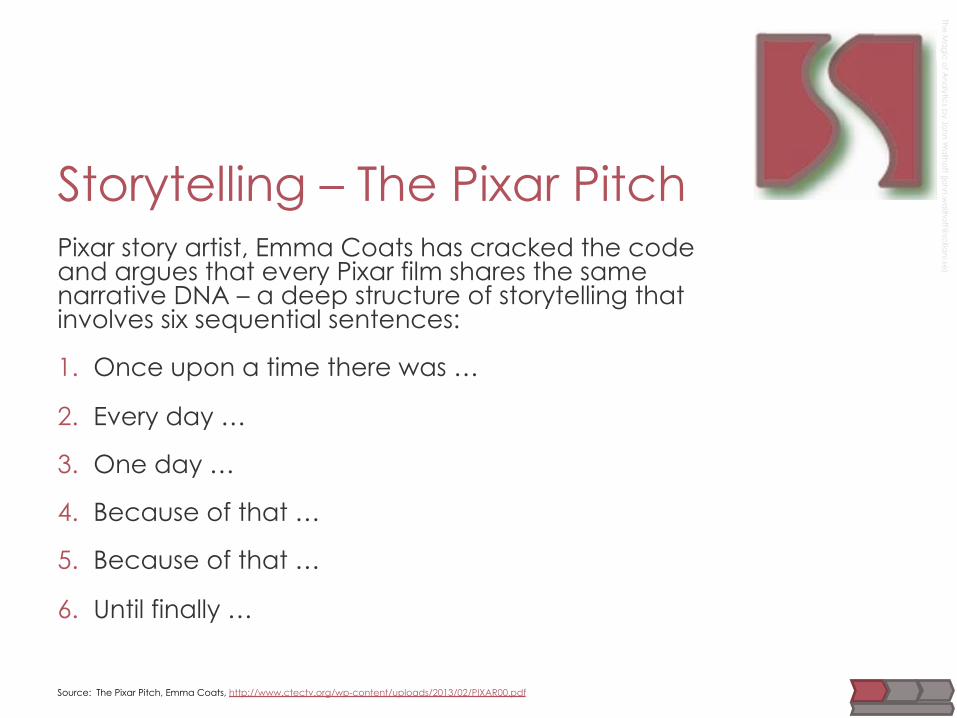

Storytelling – The Pixar Pitch Pixar story artist, Emma Coats has cracked the code and argues that every Pixar film shares the same narrative DNA – a deep structure of storytelling that involves six sequential sentences:

1. Once upon a time there was …

2. Every day …

3. One day …

4. Because of that …

5. Because of that …

6. Until finally …

Source: The Pixar Pitch, Emma Coats, http://www.ctectv.org/wp-content/uploads/2013/02/PIXAR00.pdf

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

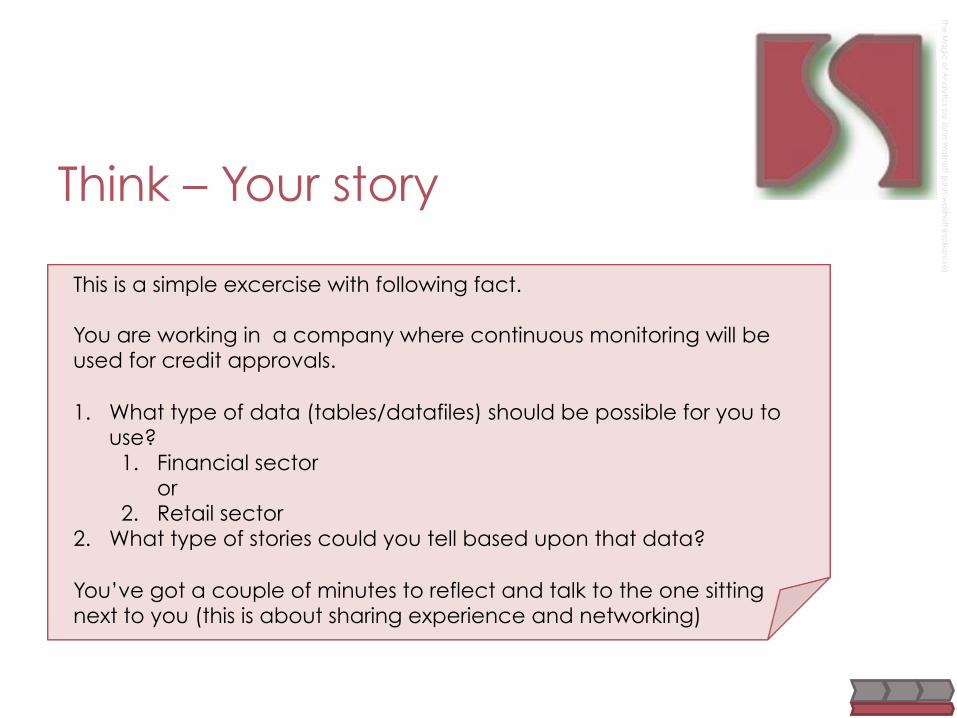

Think – Your story

This is a simple excercise with following fact. You are working in a company where continuous monitoring will be used for credit approvals. 1. What type of data (tables/datafiles) should be possible for you to

use? 1. Financial sector

or 2. Retail sector

2. What type of stories could you tell based upon that data? You’ve got a couple of minutes to reflect and talk to the one sitting next to you (this is about sharing experience and networking)

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Play

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

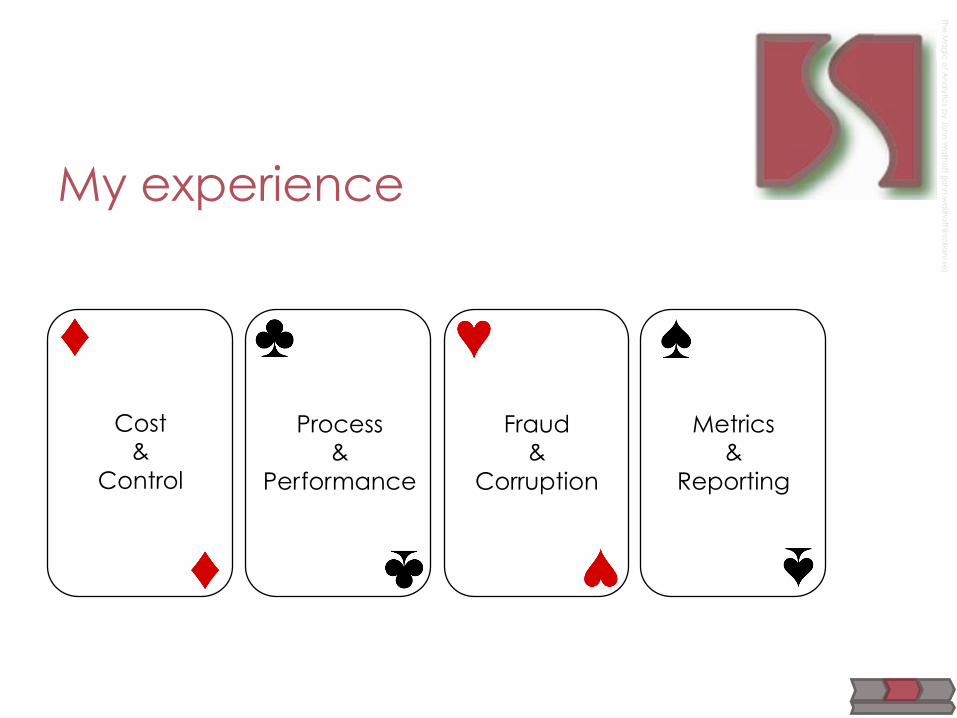

My experience

Cost &

Control

Process &

Performance

Fraud &

Corruption

Metrics &

Reporting

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

My experience - examples ¡ External Audit ¡ Accounts payables ¡ Accounts receivables ¡ Payroll ¡ Inventories ¡ General ledger ¡ Cash register data ¡ Aggreements vs invoice ¡ User accounts

¡ IT ¡ Server utilization

¡ Internal audit ¡ Expenses ¡ Payroll ¡ Logistics process ¡ Accounts payables ¡ General ledger ¡ Statistical sampling

(Agriculture-EU)

¡ Security/Privacy – IT ¡ Web server logfile ¡ Incidents

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

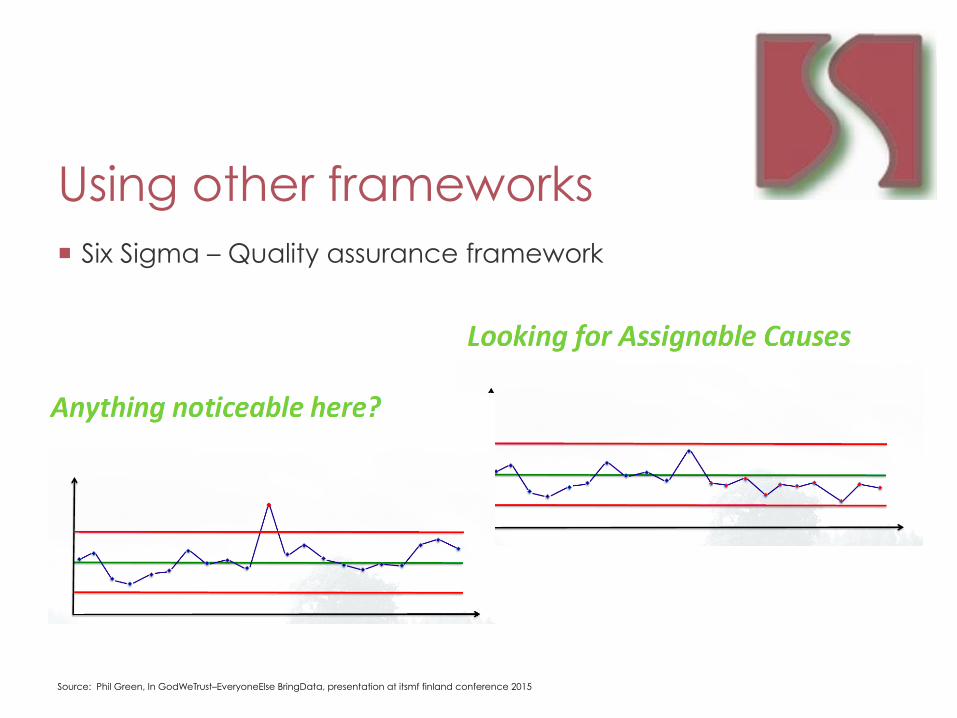

Using other frameworks ¡ Six Sigma – Quality assurance framework

Source: Phil Green, In GodWeTrust–EveryoneElse BringData, presentation at itsmf finland conference 2015

Strategies Approach

¡ Unstructured (Ad Hoc) ¡ Will only be used for one time

¡ Structured ¡ Will be used repeatedly

¡ Centralised ¡ Expert skills

¡ Monitoring ¡ Automation

Access to data

¡ Internally ¡ Are we able to access data

directly (our environment)

¡ Externally ¡ Do we need to request and

obtain data from someone else

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

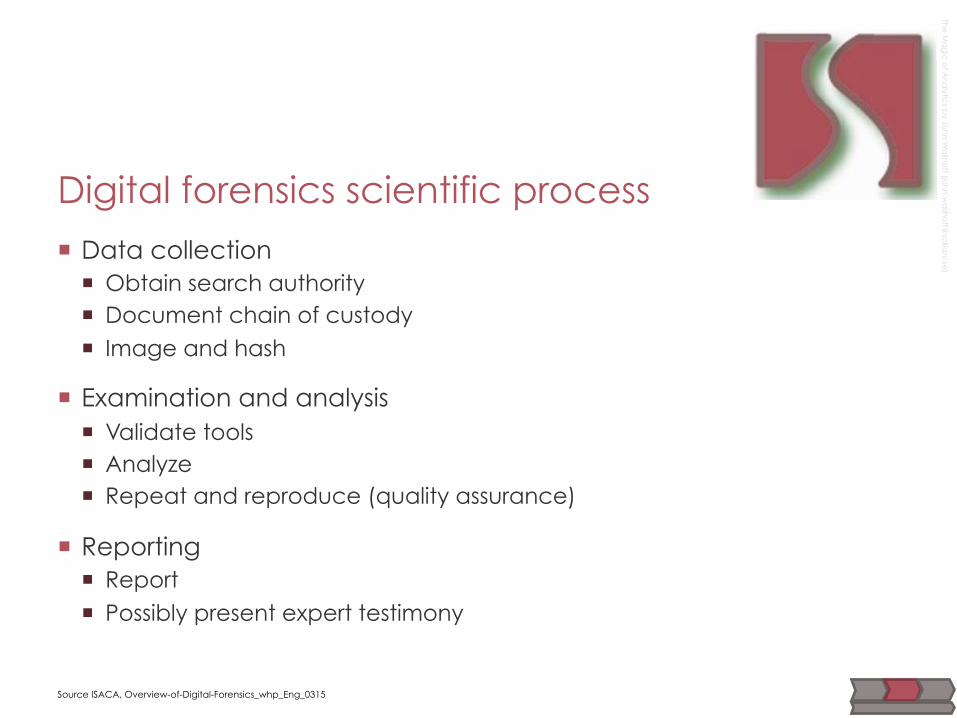

Digital forensics scientific process

¡ Data collection ¡ Obtain search authority ¡ Document chain of custody ¡ Image and hash

¡ Examination and analysis ¡ Validate tools ¡ Analyze ¡ Repeat and reproduce (quality assurance)

¡ Reporting ¡ Report ¡ Possibly present expert testimony

Source ISACA, Overview-of-Digital-Forensics_whp_Eng_0315

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

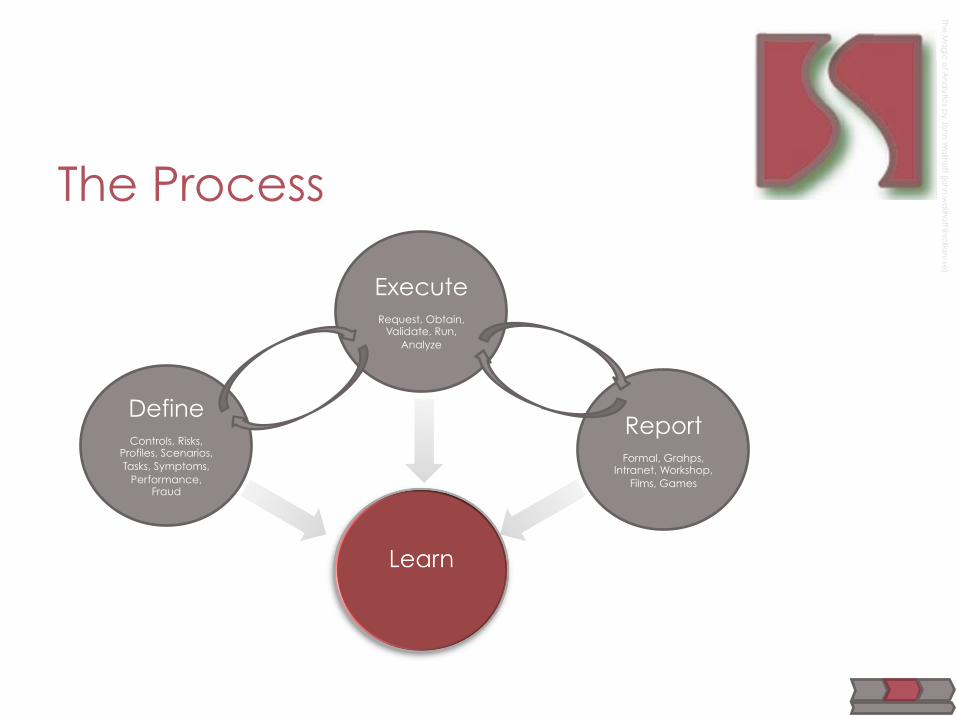

The Process

Define

Controls, Risks, Profiles, Scenarios, Tasks, Symptoms,

Performance, Fraud

Execute

Request, Obtain, Validate, Run,

Analyze

Report

Formal, Grahps, Intranet, Workshop,

Films, Games

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Use your imagination ¡ Controls

¡ Invoices with amount higher than approver is authorised to

¡ Risks ¡ Customers that have excceeded

credit limit

¡ Profiles ¡ Invoices with round amount that

is a start up

¡ Scenarios ¡ Unauthorised access to Financial

system in a certain month

¡ Tasks ¡ Investigate a privacy breach

¡ Symptoms ¡ Trend of problems related to

service/application/system

¡ Performance ¡ Weekly incident management

dashboard

¡ Fraud ¡ Red flags to indicate fraudulent

behaviour

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

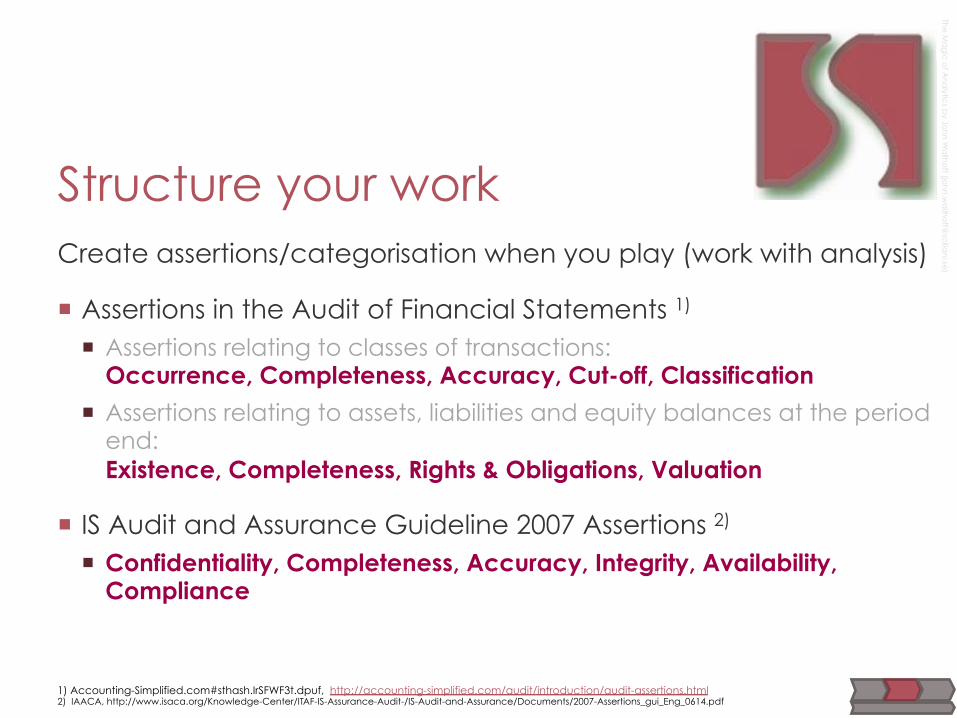

Structure your work Create assertions/categorisation when you play (work with analysis)

¡ Assertions in the Audit of Financial Statements 1)

¡ Assertions relating to classes of transactions: Occurrence, Completeness, Accuracy, Cut-off, Classification

¡ Assertions relating to assets, liabilities and equity balances at the period end: Existence, Completeness, Rights & Obligations, Valuation

¡ IS Audit and Assurance Guideline 2007 Assertions 2) ¡ Confidentiality, Completeness, Accuracy, Integrity, Availability,

Compliance

1) Accounting-Simplified.com#sthash.IrSFWF3t.dpuf, http://accounting-simplified.com/audit/introduction/audit-assertions.html 2) IAACA, http://www.isaca.org/Knowledge-Center/ITAF-IS-Assurance-Audit-/IS-Audit-and-Assurance/Documents/2007-Assertions_gui_Eng_0614.pdf

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

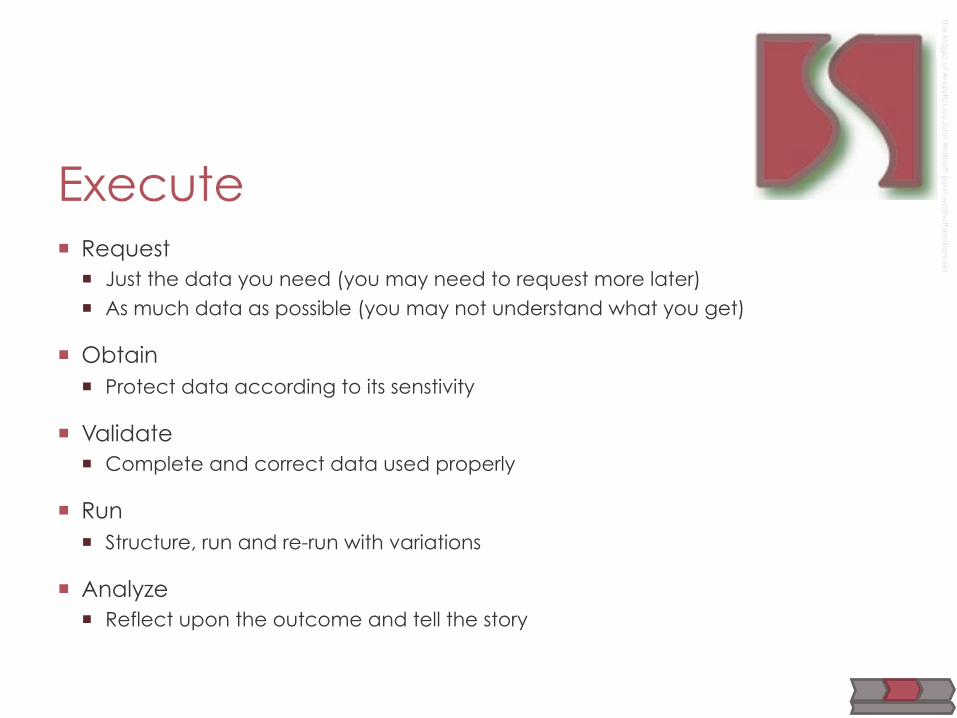

Execute ¡ Request

¡ Just the data you need (you may need to request more later) ¡ As much data as possible (you may not understand what you get)

¡ Obtain ¡ Protect data according to its senstivity

¡ Validate ¡ Complete and correct data used properly

¡ Run ¡ Structure, run and re-run with variations

¡ Analyze ¡ Reflect upon the outcome and tell the story

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Report ¡ Formal

¡ Report with summary and details

¡ Graphs ¡ Key findings to show progress

¡ Intranet ¡ Performance and metrics

¡ Workshop ¡ Discuss, learn and evolve

¡ Films ¡ Convert you ppt to movie clip and add comments/speaker

¡ Games ¡ Create interactivity based upon what you have discovered

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

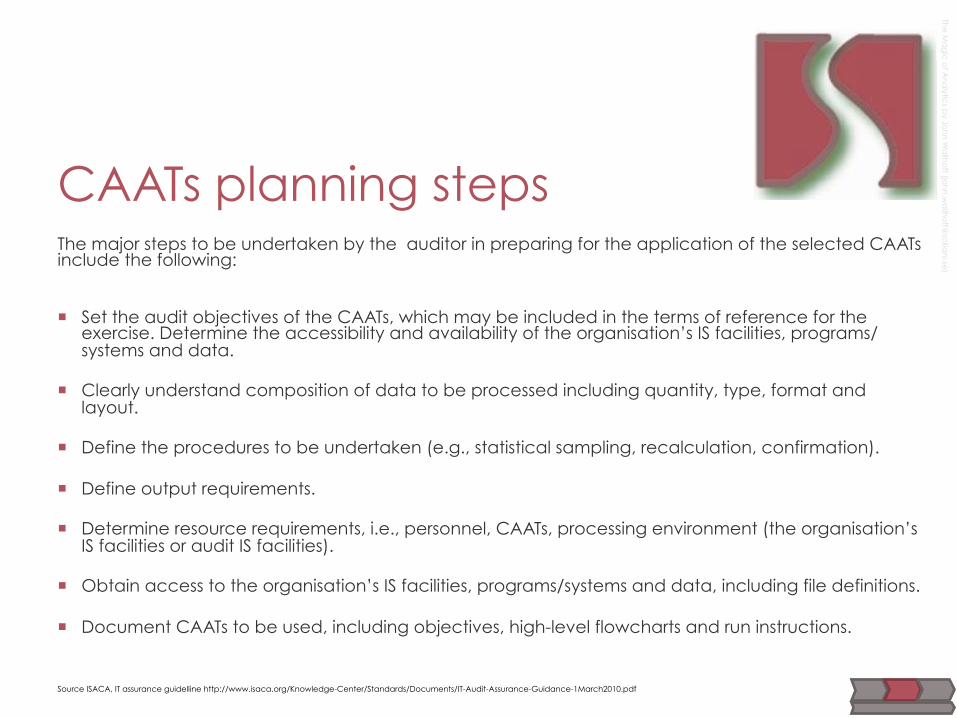

CAATs planning steps The major steps to be undertaken by the auditor in preparing for the application of the selected CAATs include the following:

¡ Set the audit objectives of the CAATs, which may be included in the terms of reference for the exercise. Determine the accessibility and availability of the organisation’s IS facilities, programs/systems and data.

¡ Clearly understand composition of data to be processed including quantity, type, format and layout.

¡ Define the procedures to be undertaken (e.g., statistical sampling, recalculation, confirmation).

¡ Define output requirements.

¡ Determine resource requirements, i.e., personnel, CAATs, processing environment (the organisation’s IS facilities or audit IS facilities).

¡ Obtain access to the organisation’s IS facilities, programs/systems and data, including file definitions.

¡ Document CAATs to be used, including objectives, high-level flowcharts and run instructions.

Source ISACA, IT assurance guidelline http://www.isaca.org/Knowledge-Center/Standards/Documents/IT-Audit-Assurance-Guidance-1March2010.pdf

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

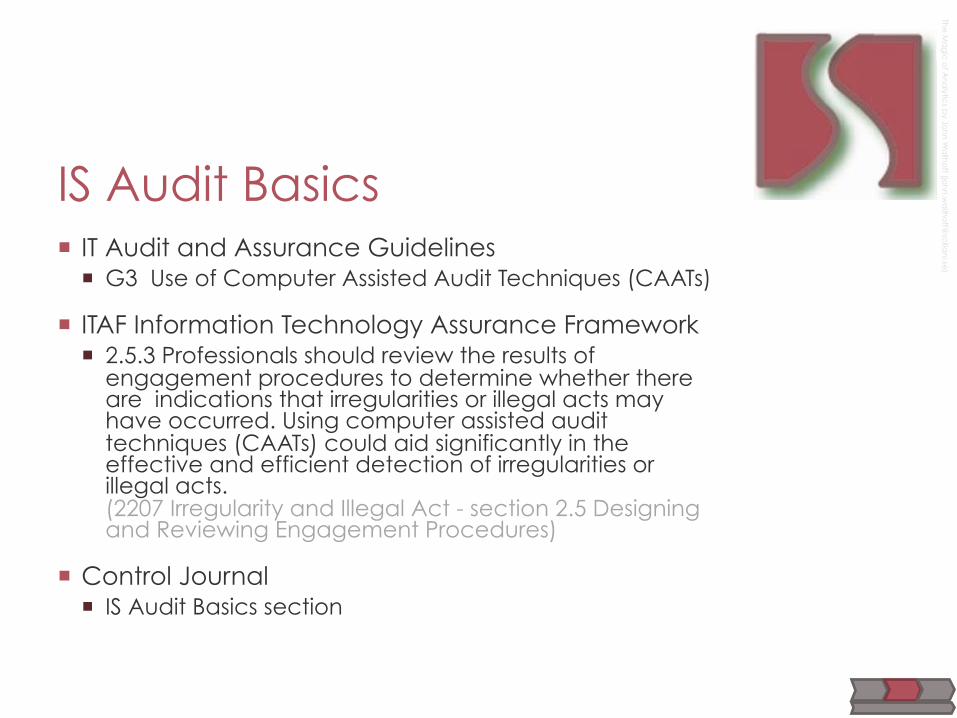

IS Audit Basics ¡ IT Audit and Assurance Guidelines

¡ G3 Use of Computer Assisted Audit Techniques (CAATs)

¡ ITAF Information Technology Assurance Framework ¡ 2.5.3 Professionals should review the results of

engagement procedures to determine whether there are indications that irregularities or illegal acts may have occurred. Using computer assisted audit techniques (CAATs) could aid significantly in the effective and efficient detection of irregularities or illegal acts. (2207 Irregularity and Illegal Act - section 2.5 Designing and Reviewing Engagement Procedures)

¡ Control Journal ¡ IS Audit Basics section

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

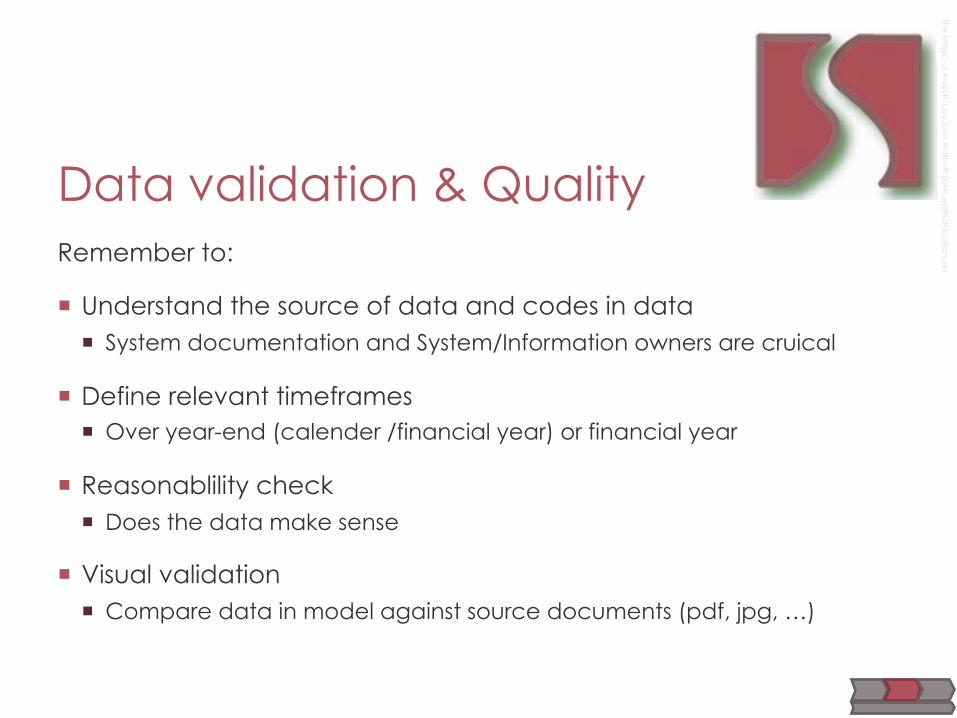

Data validation & Quality Remember to:

¡ Understand the source of data and codes in data ¡ System documentation and System/Information owners are cruical

¡ Define relevant timeframes ¡ Over year-end (calender /financial year) or financial year

¡ Reasonablility check ¡ Does the data make sense

¡ Visual validation ¡ Compare data in model against source documents (pdf, jpg, …)

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

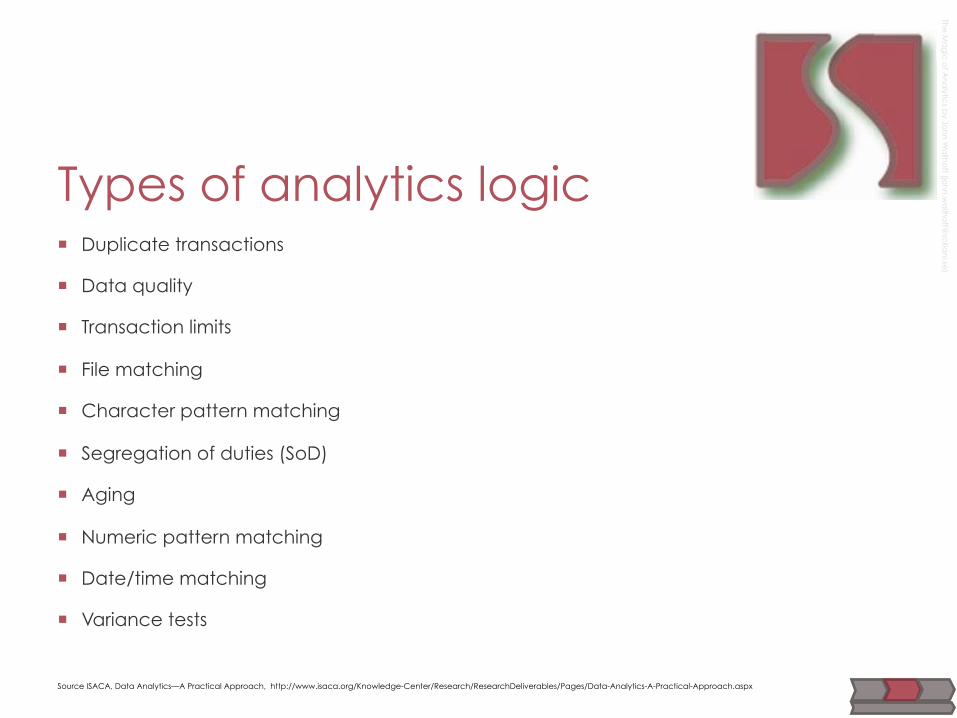

Types of analytics logic ¡ Duplicate transactions

¡ Data quality

¡ Transaction limits

¡ File matching

¡ Character pattern matching

¡ Segregation of duties (SoD)

¡ Aging

¡ Numeric pattern matching

¡ Date/time matching

¡ Variance tests

Source ISACA, Data Analytics—A Practical Approach, http://www.isaca.org/Knowledge-Center/Research/ResearchDeliverables/Pages/Data-Analytics-A-Practical-Approach.aspx

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

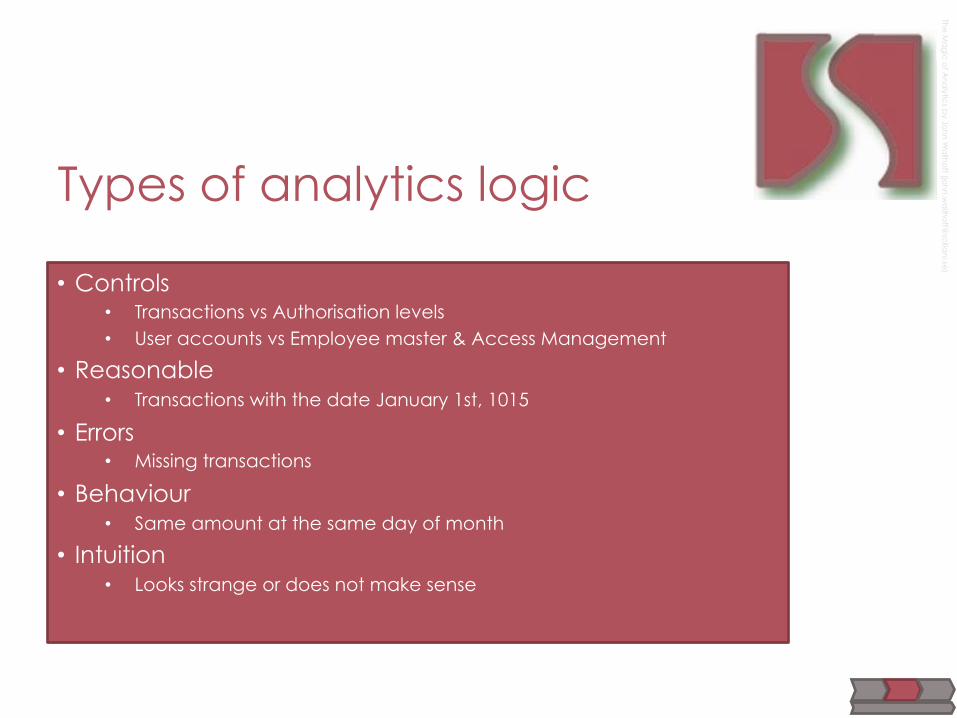

Types of analytics logic

• Controls • Transactions vs Authorisation levels • User accounts vs Employee master & Access Management

• Reasonable • Transactions with the date January 1st, 1015

• Errors • Missing transactions

• Behaviour • Same amount at the same day of month

• Intuition • Looks strange or does not make sense

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

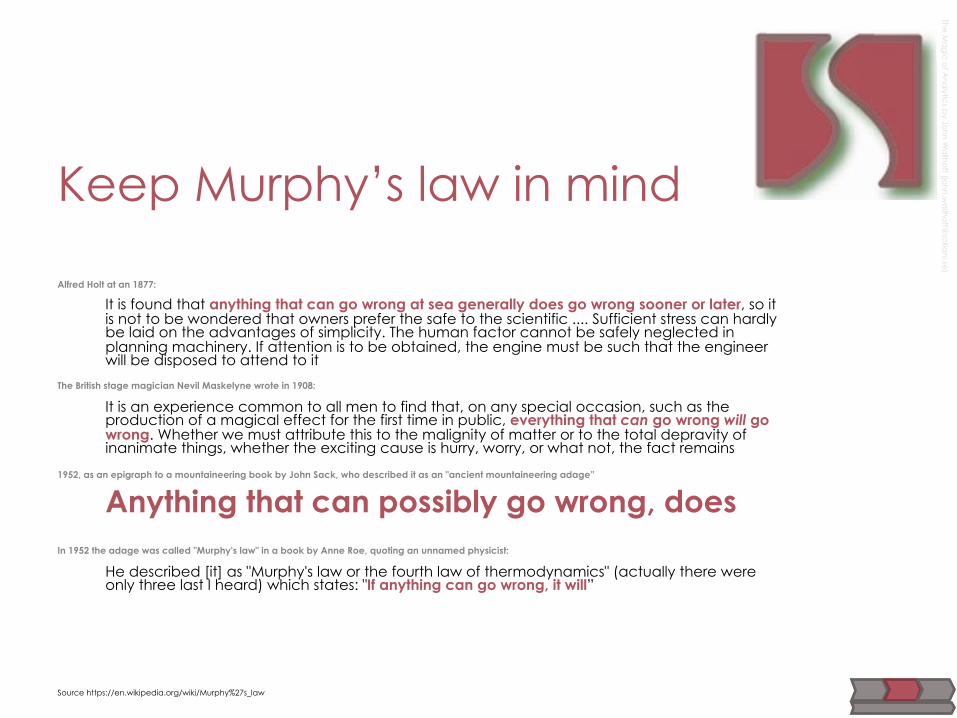

Keep Murphy’s law in mind

Alfred Holt at an 1877:

It is found that anything that can go wrong at sea generally does go wrong sooner or later, so it is not to be wondered that owners prefer the safe to the scientific .... Sufficient stress can hardly be laid on the advantages of simplicity. The human factor cannot be safely neglected in planning machinery. If attention is to be obtained, the engine must be such that the engineer will be disposed to attend to it

The British stage magician Nevil Maskelyne wrote in 1908:

It is an experience common to all men to find that, on any special occasion, such as the production of a magical effect for the first time in public, everything that can go wrong will go wrong. Whether we must attribute this to the malignity of matter or to the total depravity of inanimate things, whether the exciting cause is hurry, worry, or what not, the fact remains

1952, as an epigraph to a mountaineering book by John Sack, who described it as an "ancient mountaineering adage”

Anything that can possibly go wrong, does

In 1952 the adage was called "Murphy's law" in a book by Anne Roe, quoting an unnamed physicist:

He described [it] as "Murphy's law or the fourth law of thermodynamics" (actually there were only three last I heard) which states: "If anything can go wrong, it will”

Source https://en.wikipedia.org/wiki/Murphy%27s_law

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

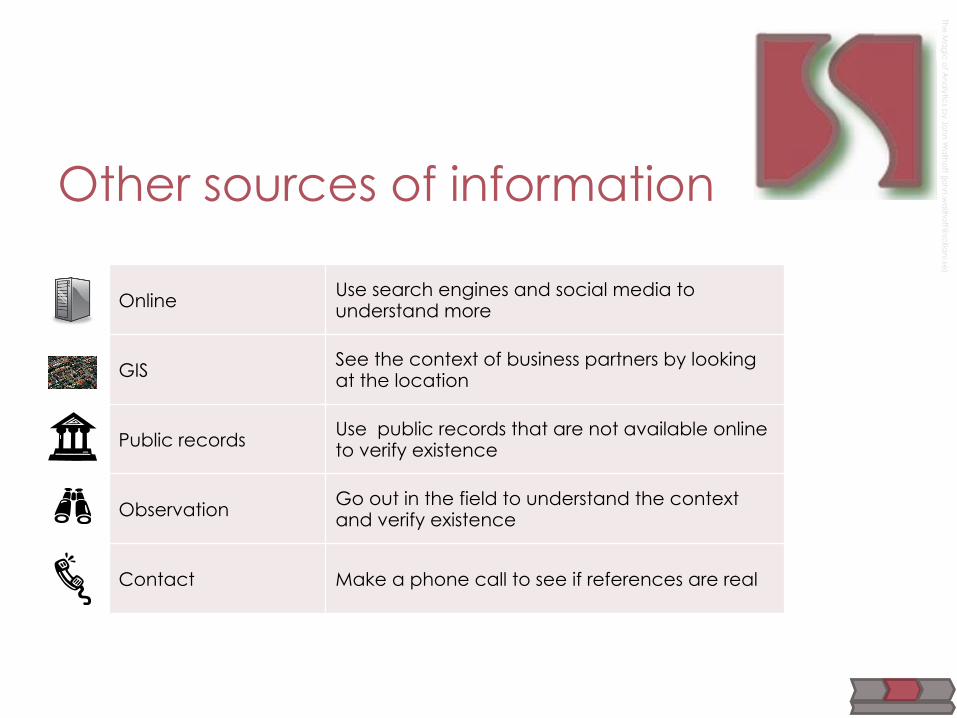

Other sources of information

Online Use search engines and social media to understand more

GIS See the context of business partners by looking at the location

Public records Use public records that are not available online to verify existence

Observation Go out in the field to understand the context and verify existence

Contact Make a phone call to see if references are real

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Think – Your story

This is a simple excercise with following questions: 1. You have just implemented the continuous monitoring solution for

credit limits. What could you do to transform it from a detective to predictive control ?

2. How can you integrate the output from Analytics to relevant processes?

You’ve got a couple of minutes to reflect and talk to the one sitting next to you (this is about sharing experience and networking)

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Visualise

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

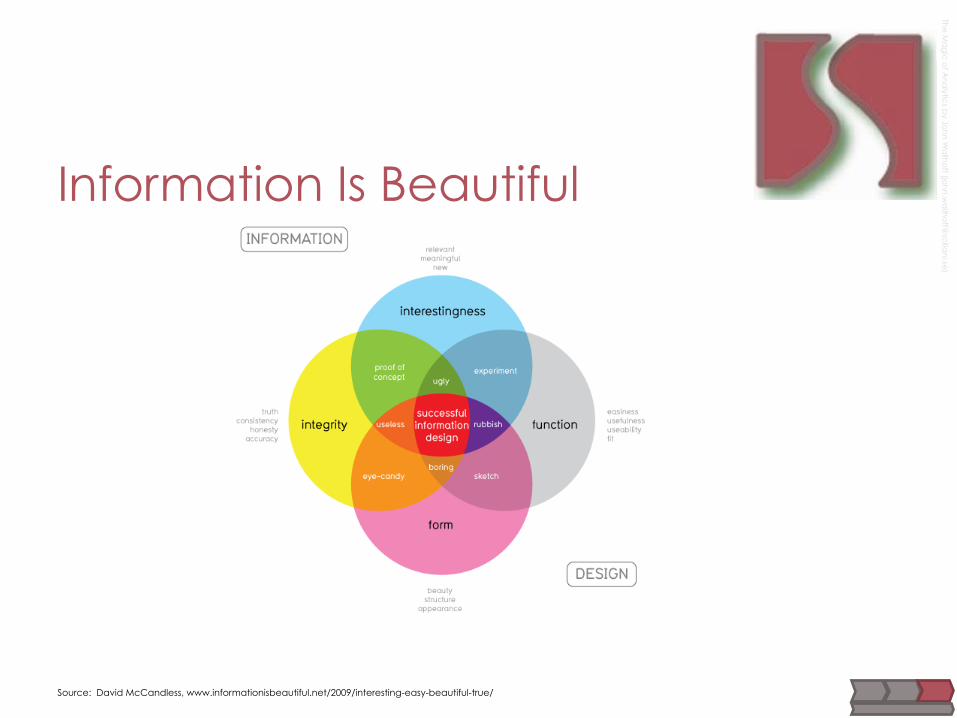

Information Is Beautiful

Source: David McCandless, www.informationisbeautiful.net/2009/interesting-easy-beautiful-true/

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

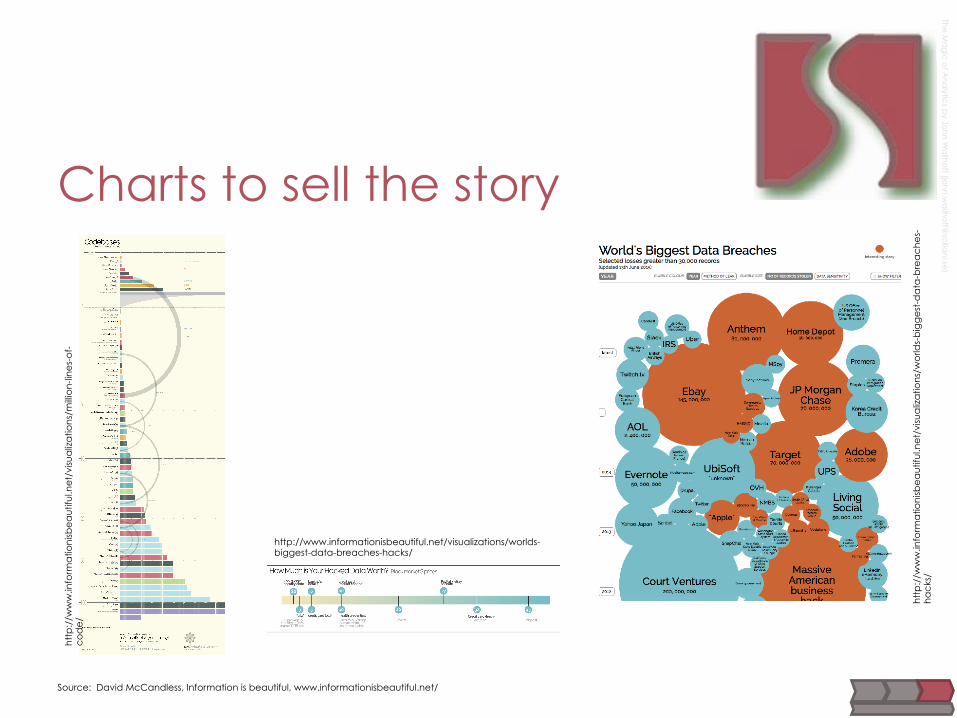

Charts to sell the story

Source: David McCandless, Information is beautiful, www.informationisbeautiful.net/

http://www.informationisbeautiful.net/visualizations/worlds-biggest-data-breaches-hacks/

htt

p:/

/ww

w.in

form

atio

nisb

ea

utif

ul.n

et/

visu

aliz

atio

ns/

mill

ion

-lin

es-

of-

co

de

/

htt

p:/

/ww

w.in

form

atio

nisb

ea

utif

ul.n

et/

visu

aliz

atio

ns/

wo

rlds-

big

ge

st-d

ata

-bre

ac

he

s-h

ac

ks/

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Infographics

Source: Google search on the word ”Inforgraphics”

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

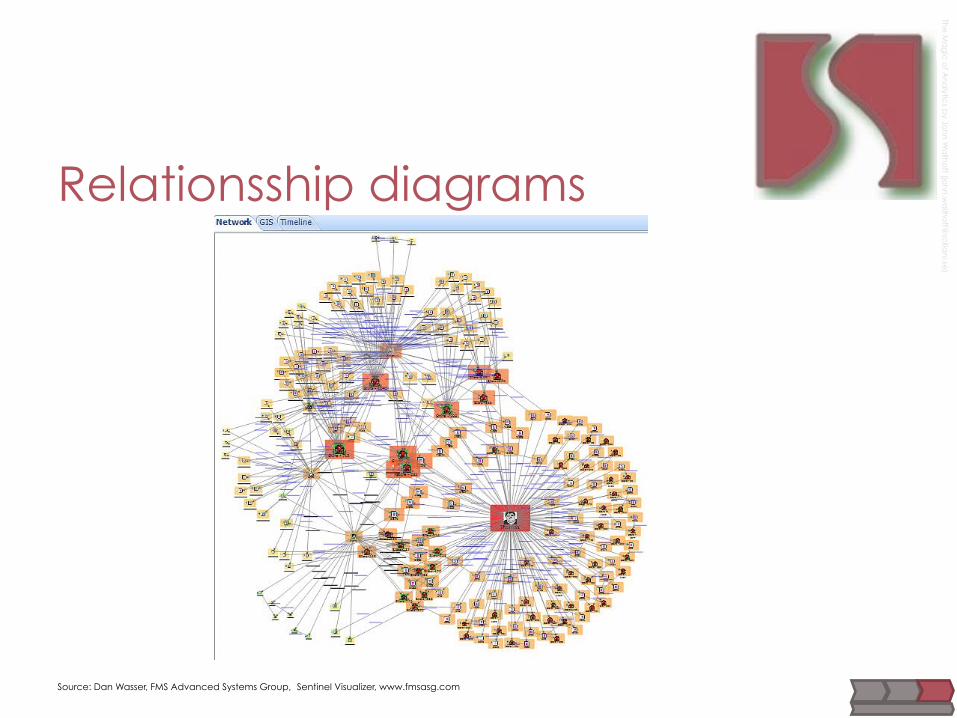

Relationsship diagrams

Source: Dan Wasser, FMS Advanced Systems Group, Sentinel Visualizer, www.fmsasg.com

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

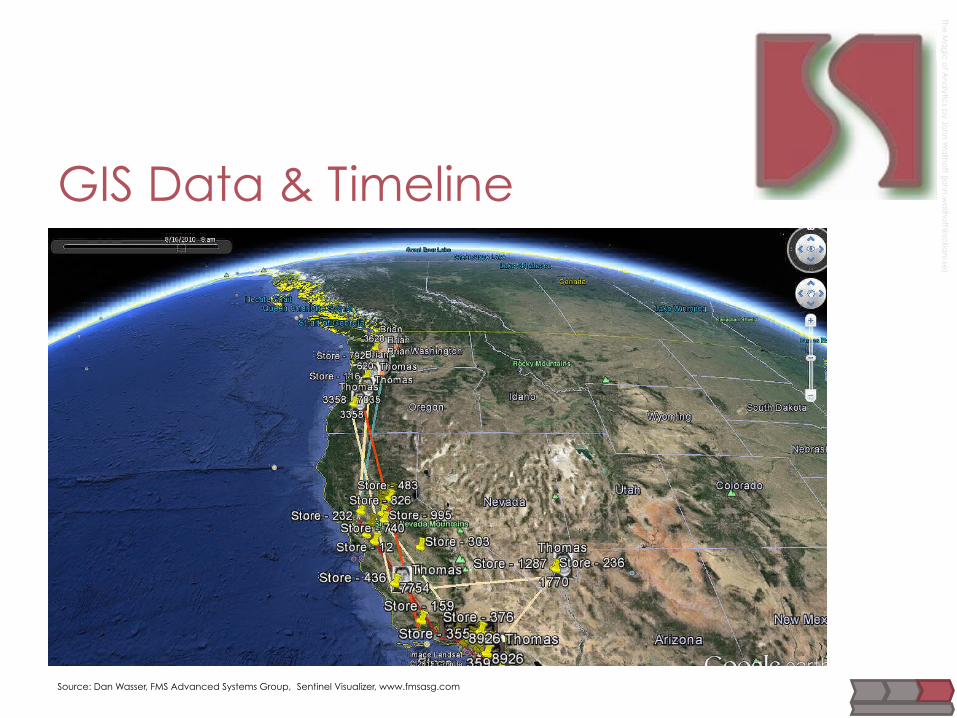

GIS Data & Timeline

Source: Dan Wasser, FMS Advanced Systems Group, Sentinel Visualizer, www.fmsasg.com

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

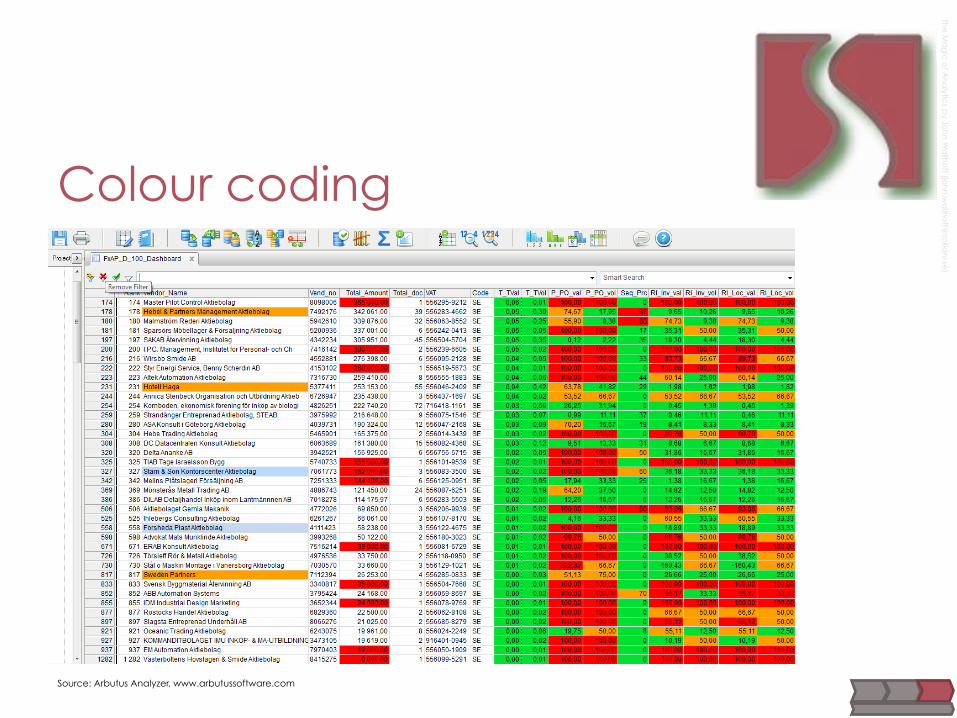

Colour coding

Source: Arbutus Analyzer, www.arbutussoftware.com

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Think – Your story

If you have implemented continuous monitoring in your organisation: 1. How do you use your results? 2. Are you communicating the results outside your department? 3. Have you enabled continuous improvements with your monitoring?

Share your experience with all of us!

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

Conclusions

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

The Magic of Analytics

…

is not about data -

it is about you

Definition - Analytics The field of data analysis. Analytics often involves studying past historical data to research potential trends, to analyze the effects of certain decisions or events, or to evaluate the performance of a given tool or scenario.

The goal of analytics is to improve the business by gaining knowledge which can be used to make improvements or changes.

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

See you again John Wallhoff (CISA, CISM, CISSP) Management consultant / Expert advisor Fraud & Corruption – Analytics - Information & Cyber security – IT Service Management

Scillani Information AB Ekgatan 6, SE 230 40 BARA, Sweden - Vestergade 16, DK 1456 COPENHAGEN, Denmark E-mail: [email protected] Linkedin: http://www.linkedin.com/pub/john-wallhoff/1/48b/a69 Skype: john.wallhoff Webb: www.scillani.se Mobile: +46 (0)707 743131 Phone: +46 (0)40 543131

The

Ma

gic

of A

na

lytics b

y Joh

n W

allh

off (jo

hn

.wa

llho

ff@sc

illan

i.se)

![Magic Quadrant for Business Intelligence and Analytics ... · Gartner Reprint 10:43:58]](https://img.pdfslide.net/doc/110x75/5fbff6451f09cb7ffe7677e3/magic-quadrant-for-business-intelligence-and-analytics-gartner-reprint-104358.jpg)