Embed Size (px)

Citation preview

1 31-03-2006 UvA Audit

The Management of Diversified Funding at theUniversiteit van Amsterdam

Dr. Sijbolt Noorda, president of the Universiteit van Amsterdam

2 31-03-2006 UvA Audit

1. Introduction

Purpose of our Business Process RedesignOur sizeThe funding of Dutch universitiesGovernment grant decompositionOur annual budgetOur internal devolution of budgetsOur devolved unitary modelA call for transparency

3 31-03-2006 UvA Audit

Purpose of our BPR

To align financial with academic responsibilities at all levels in the organisation

To gain better understanding of the true costs and cost drivers of our teaching and research

To enhance the transparency of internal budget allocation

4 31-03-2006 UvA Audit

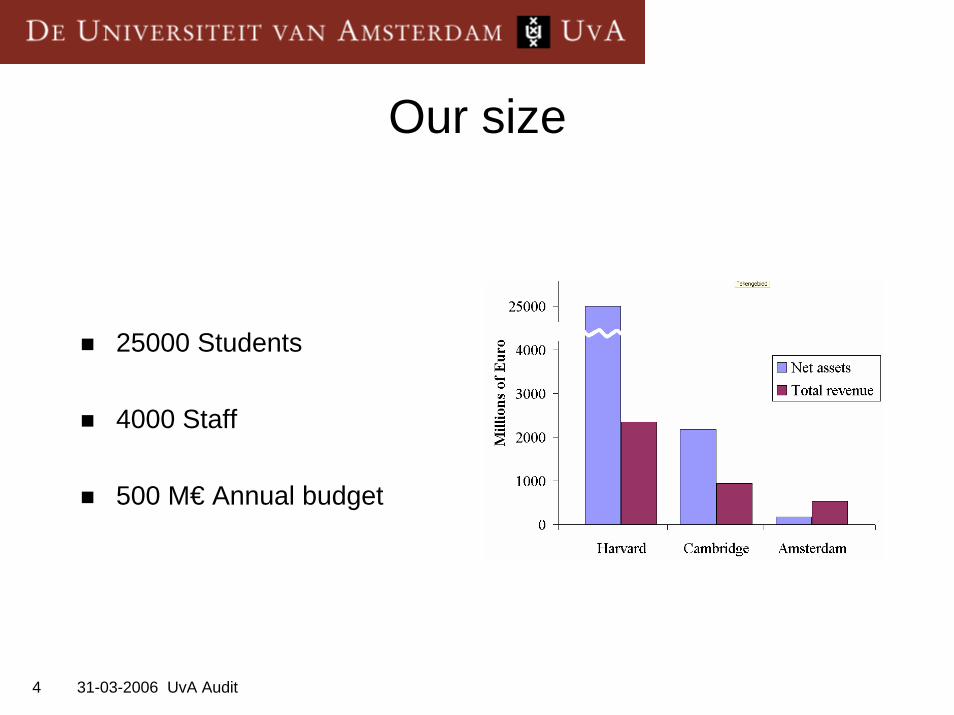

Our size

25000 Students

4000 Staff

500 M€ Annual budget

5 31-03-2006 UvA Audit

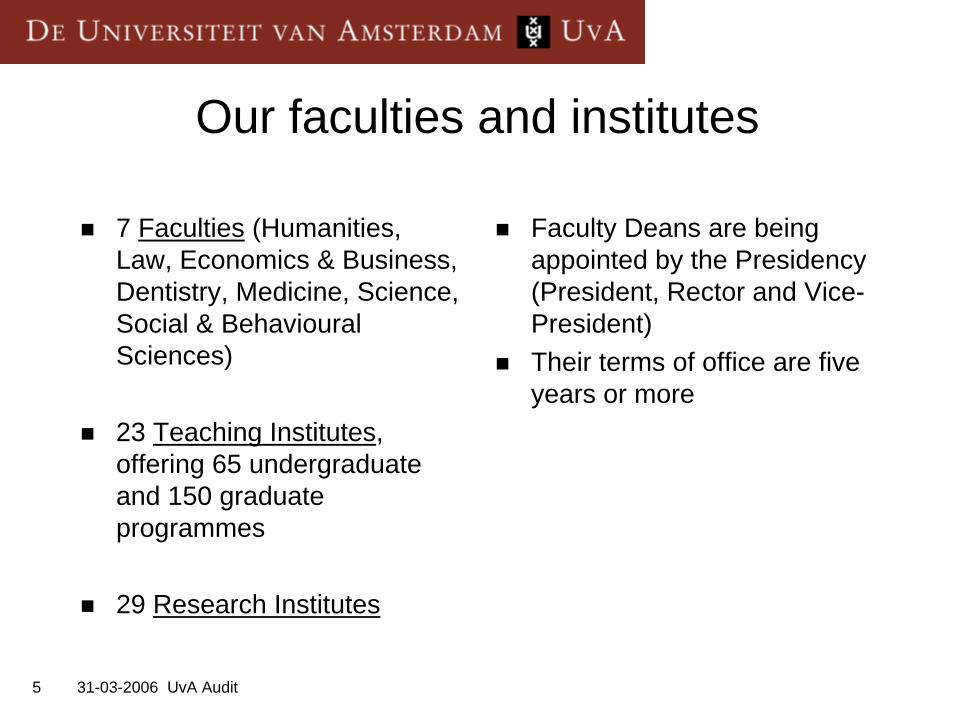

Our faculties and institutes

7 Faculties (Humanities, Law, Economics & Business, Dentistry, Medicine, Science, Social & Behavioural Sciences)

23 Teaching Institutes, offering 65 undergraduate and 150 graduate programmes

29 Research Institutes

Faculty Deans are being appointed by the Presidency(President, Rector and Vice-President)Their terms of office are five years or more

6 31-03-2006 UvA Audit

The funding of Dutch universities

Highly dependent on the State, as far as funding is concerned

Government:provides block grantand determines tuition feesbut does not regulate spending

No history of private estates and endowments

7 31-03-2006 UvA Audit

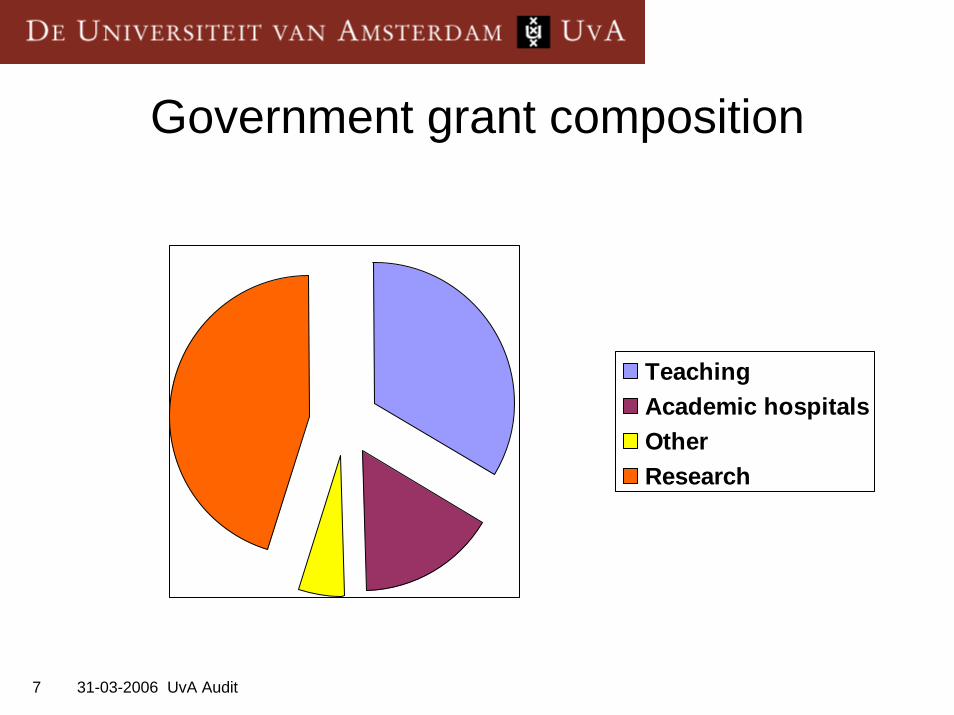

Government grant composition

TeachingAcademic hospitalsOtherResearch

8 31-03-2006 UvA Audit

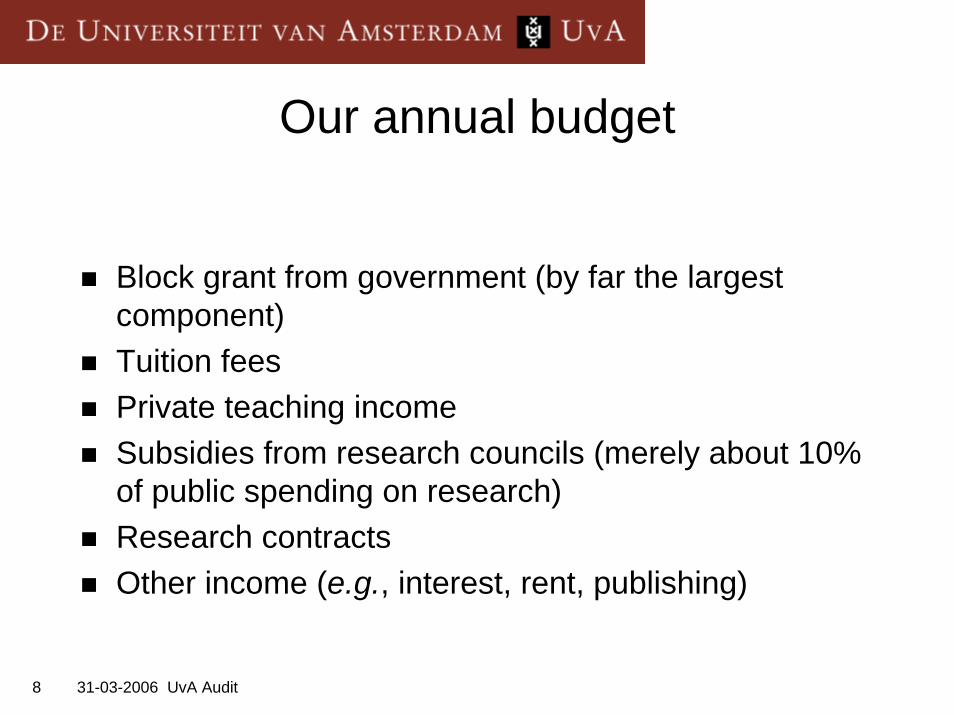

Our annual budget

Block grant from government (by far the largest component)Tuition feesPrivate teaching incomeSubsidies from research councils (merely about 10% of public spending on research)Research contractsOther income (e.g., interest, rent, publishing)

9 31-03-2006 UvA Audit

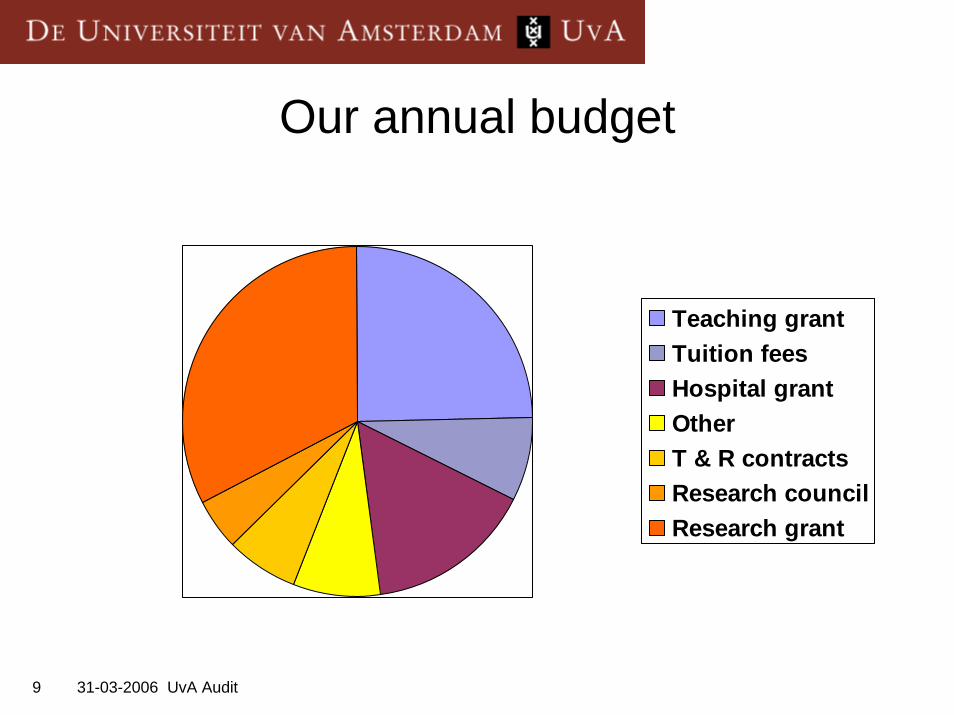

Our annual budget

Teaching grantTuition feesHospital grantOtherT & R contractsResearch councilResearch grant

10 31-03-2006 UvA Audit

Our internal devolution of budgets

Income from government grant and tuition fees should be allocated to faculties through transparentand cost conscious allocation formulae

Income from subsidies and contracts directly benefits the faculties, butthey are responsible for any project costs not covered by the subsidy or contract

All other income benefits the unit which generates it

11 31-03-2006 UvA Audit

Our devolved unitary model

Faculty deans enjoy autonomy in setting priorities and spending funds, relative to their success in research quality and in attracting students

The main purposes of central policies are:fostering good conditions for T&L and for researchsecuring the UvA ® brand nameanticipating long term trends and priorities in teaching and in research, and reflecting these in our budget allocation

12 31-03-2006 UvA Audit

A call for transparency

Surprisingly our block grant formula has of T and R compartments, but the DoE never asks about actual spending on T and RSo, like many, we didn’t know

But when budgets get tighter, questions may get asked andeveryone feels he’s getting too small a piece of the cake

13 31-03-2006 UvA Audit

2. A new budget allocation scheme

Principal cost driver of teachingDifferent subject weightsOther T&L cost driversT&L budget incentivesUvA teaching grant modelPrincipal cost “drivers” of researchUvA automatic research grant modelThe (implied) research strategy

14 31-03-2006 UvA Audit

Principal cost driver of teaching

Dutch universities have no authority of entry selection

So student volume is a truly external cost driver, measured by the number of ECTS credits generated (60/yr)

15 31-03-2006 UvA Audit

Different subjects weights

Delivery of the same quality of T&L does not require the same amount of €€ for all subjects

No reliable data on T&L cost per subject are available at UvA and in the Netherlands

Therefore we made use of recent HEFCE data on the relative cost of T&L per subject, and derived faculty averages on this basis

16 31-03-2006 UvA Audit

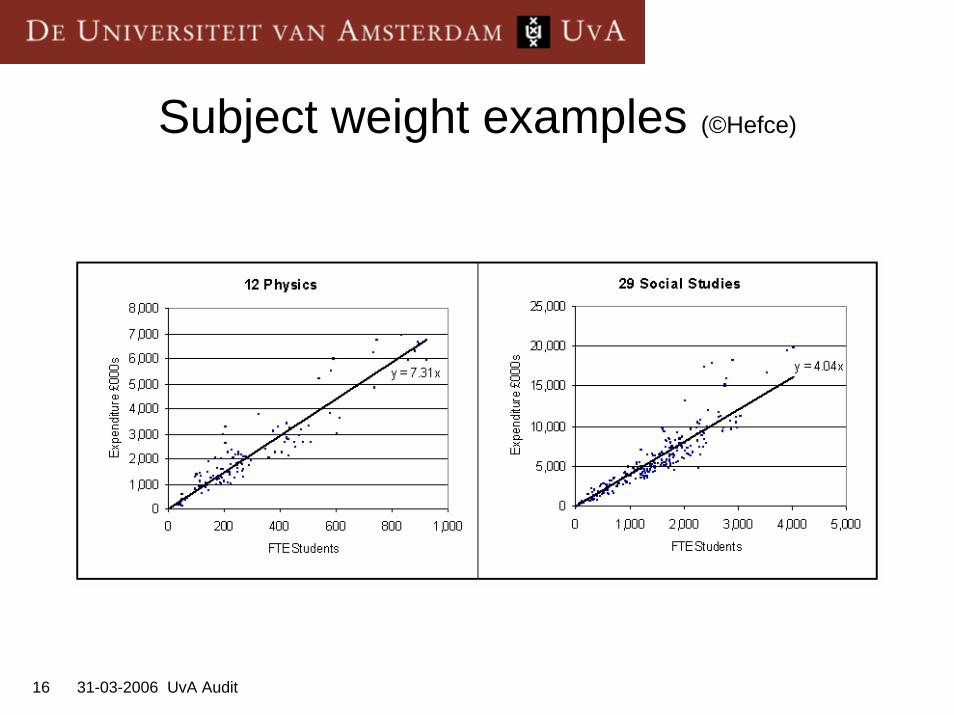

Subject weight examples (©Hefce)

17 31-03-2006 UvA Audit

Other T&L cost drivers

Surprisingly we conclude there are none

No evidence of economies of scalePerhaps some diseconomies at the lower end, but:these would imply perverse incentives

Only some intrinsically undersized groups such as minor languages might need a little extra support

18 31-03-2006 UvA Audit

T&L budget incentives

Internal debate showed that incentives were welcomed for:the teaching effort on behalf of those students who fail to generate creditsthe actual completion of a study programme in terms of master degrees awarded

So we provide these

19 31-03-2006 UvA Audit

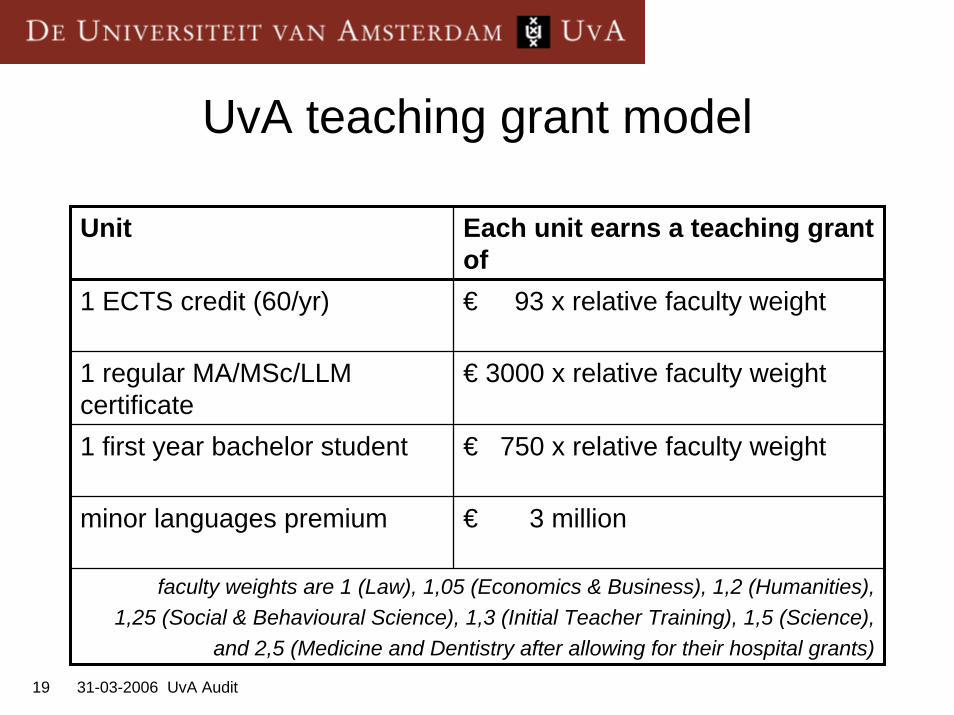

UvA teaching grant model

Unit Each unit earns a teaching grant of

1 ECTS credit (60/yr) € 93 x relative faculty weight

1 regular MA/MSc/LLM certificate

€ 3000 x relative faculty weight

1 first year bachelor student € 750 x relative faculty weight

minor languages premium € 3 million

faculty weights are 1 (Law), 1,05 (Economics & Business), 1,2 (Humanities), 1,25 (Social & Behavioural Science), 1,3 (Initial Teacher Training), 1,5 (Science),

and 2,5 (Medicine and Dentistry after allowing for their hospital grants)

20 31-03-2006 UvA Audit

Principal cost “driver” of research

Unlike teaching, research has almost no external cost driversException: the number of PhD degrees

However, we recognize:that academic teaching requires at least a proportionate amount of research;that faculties must be able to continue attracting research contracts and subsidies at present level

21 31-03-2006 UvA Audit

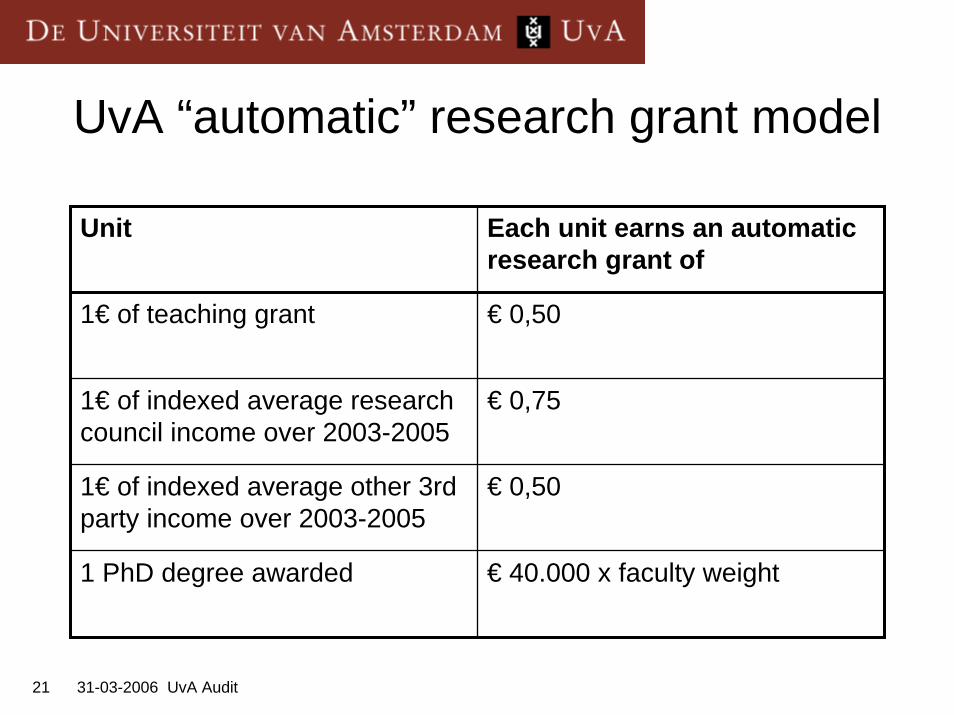

UvA “automatic” research grant model

Unit Each unit earns an automatic research grant of

1€ of teaching grant € 0,50

1€ of indexed average research council income over 2003-2005

€ 0,75

1€ of indexed average other 3rd party income over 2003-2005

€ 0,50

1 PhD degree awarded € 40.000 x faculty weight

22 31-03-2006 UvA Audit

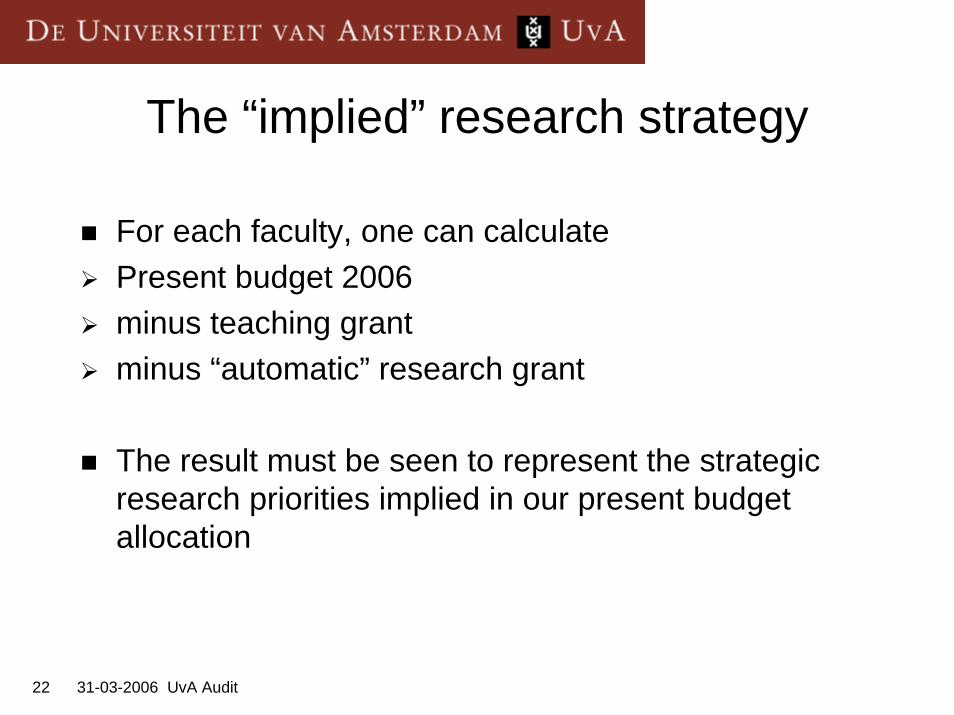

The “implied” research strategy

For each faculty, one can calculatePresent budget 2006minus teaching grantminus “automatic” research grant

The result must be seen to represent the strategic research priorities implied in our present budget allocation

23 31-03-2006 UvA Audit

The model at work on our 2006 budget

24 31-03-2006 UvA Audit

3. The business model environment

A level playing fieldSeparation of responsibilitiesNew deployment of SAP as a support structure

25 31-03-2006 UvA Audit

A level playing field

Two important conditions:i. all costs are full economic costs, calculated in a

uniform way throughout the universityii. faculties and units are held economically

responsible for their decisions

And a third:iii. the budget allocation formulae must be the (almost)

only source of devolved faculty income

26 31-03-2006 UvA Audit

Separation of responsibilities

At UvA we separate the responsibilities:for results from staff, and for teaching from research

Within faculties, teaching and research are organised in programmes hiring staff from departments

And services are rendered (on subscription) from shared service centres, such as Housing, IT, Records, Library

27 31-03-2006 UvA Audit

Supporting new deployment of SAP

Integration of personnel and financial records systems (in future also student & space records)

Labeling all costs as Teaching, Research, or Other (with internal labeling of some costs as Support) (not unlike UK TRAC development and US OMB A21 regulation)

Allocation of salary and standard overhead costs through actual or virtual time sheets

28 31-03-2006 UvA Audit

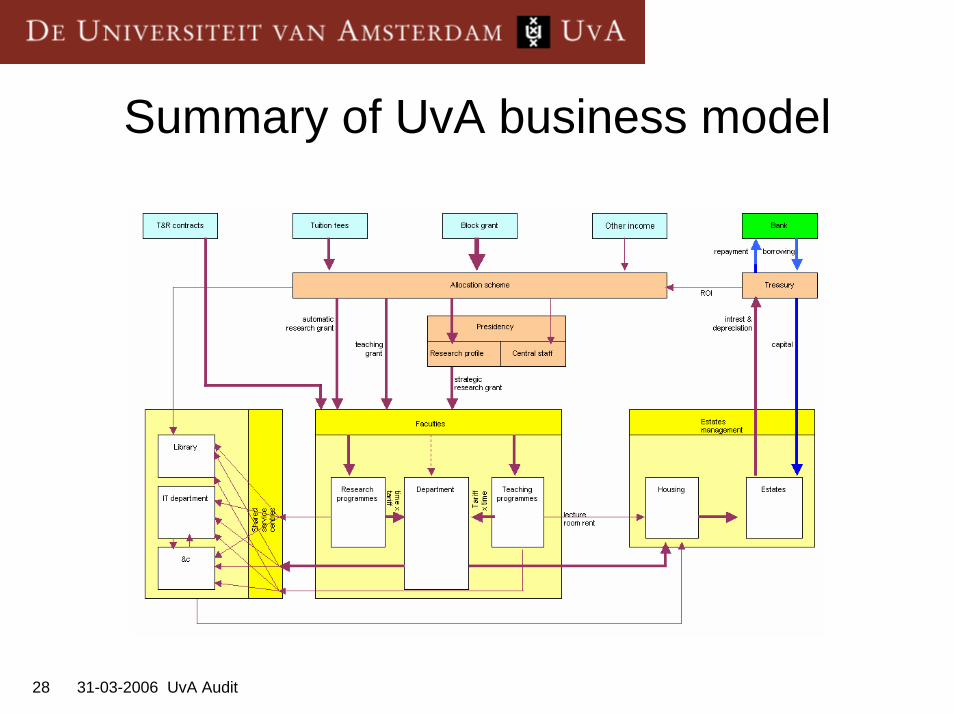

Summary of UvA business model