Embed Size (px)

Citation preview

8/14/2019 The Maps Are Being Redrawn

http://slidepdf.com/reader/full/the-maps-are-being-redrawn 1/3

9rorrP,uilding Betler Perf ormernce

COMMENTARY 83 MARCH 2OO5

THE MAPS ARE BEING REDRAWN'

"The world's biggest iceberg has crashed into an ice tongue protruding out of

Antarctica, breaking a portion off, the European Space Agency said."

"The B-15A iceberg, about the size of Luxembourg, in the past month hit the

Drygalski ice tongue, a feature marked on most maps of Antarctica, and broke

a five-kilometer- (three-mile-) long section off, ESA said on its Web site, using

satellite pictures to illustrate the damage."

"Maps of Antarctica need to be amended," ESA said."

wvwv.bloomberg.com, April 1 Bth 2005

Plexus Group's symbol for the hidden trading costs

has been the icebero. which leads us to use the

The force behind this movement is pressure to reduce

institutional trading costs. This pressure has three

driving forces: (1) modeling, derived from academic

work, (2) motivation, derived from pressing

institutional needs, and (3) methodology, to define,

implement and validate improvements to trading

practices.

Modeling

Jack Treynor and Andre Perold deserve credit for the

implementation shortfall (iceberg) approach. This is the

key insight, because it casts costs in the framework of a

cost:benefit model. The old paradigm considered costs

as something to be minimized. In effect, all other factors

other than broker behavior were assumed to be fixed and

unresponsive to trading strateEy and tactics. By linking

trading costs to performance, Perold recast the problem

from one of cost control to one of prudent spending to

achieve the investment goals. In addition, by creating an

all-inclusive cost measure, the door was opened to the

above geographical alteration as an

analogy to what's happening with the

U.S. stock exchanges. In one week

the NYSE announced a merger with

ARCA and the NASDAQ a purchase

of the lnstinet system. What has

caused this sudden flurry of exchange

mergers? We see two goals; further

reducing the cost of trading through the

technology along with accessing new

believe this is the next logical step in

'T'tz*##r??ss?gy ti*xreir; :xf"rtrpgf * **t'*s***re? FdY',$#

,S,tr#,€ #rpfl$ tr*S#*.#$s:psfd#*f arfff r**rx.#* fFa*

#{#c:g;ra#pfuy *f fft* #tr#fldd *f cs?w*s$setgr"

use of better

markets. We

response to

discovery ofhidden costs

the large but heretofore undiscoveredof trading: the iceberg. With this new

l\,4any thanks to Peter Haynes of TD Newcrest Securities, who brought the

iceberg news item to our attention and first developed the analogy to the

chanqes in the market.orces that have been active for decades

8/14/2019 The Maps Are Being Redrawn

http://slidepdf.com/reader/full/the-maps-are-being-redrawn 2/3

paradigm, it became possible to engineer changes to

improve trading results.

Motivation

The CFA Institute picked up on this same idea when they

defined Best Execution as the trading process most likely

to maximize the value of client portfolios.2 Once an

investment management firm truly internalizes theconnection between costs and performance, high-costtrading impediments become intolerable.

In recent years, institutional investors, led by -i./anguard

and Fidelity, have intensified pressure on the exchangesto develop more cost-effective solutions. The irresistible

iceberg of institutional trading needs broke the defense of

the entrenched interests.

Measu rement

In 1975, Cuneo and Wagner published an estimate ofround trip costs of 2.6% for information motivated trades.

This was in line with Demsetz's '1963 * the first we are

aware of - estimate and Krause and Stoll's 1972estimate. In Plexus' very first depiciion of an iceberg in

1992, the round trip costs were measured at2.B'h no

real change over 30 years.

Turning to the present, current Plexus client data shows

all-in round trip costs at an all time low of 1"5%. So it

appears at first blush that costs have been cut roughly in

half since the turn of the millennium, with the big

reductions starting to appear in 2003 as the effects ofdecimalization began to kick in.

Not so fast! As recently as 200'1, at the end of the Internet

frenzy, costs peaked out at 3.1% round trip, much higher

than current costs and higher than the cosl estimates ofthe 1960's and '70's. What this shows is that

economic/market prospects and

conditions play a major role in ,.,.,,,,,'-,:.. . ,,:.: .

determining the magnitude oftransaction costs. ln contrast, 1,,,,, 1, ;,: .: ..,,... : : :

the recent low costs are partly

due to the low volatility/low ...:, :.,,...,

: . : : :., ...

return exoectations of recentvears.

Another way of looking at this is to say that changes in

market structure and improved trading practices have

enabled us to hold costs constant in the face of massivegrowth in assets under management. Assuredly, both

the investing environment and the market structure are

much different than they were in the 70's and 80's.

Changes in the brokerage industry have led to much

lower liquidity costs as long as prices remain stable. But

as stability wavers, costs rise. Indeed, when adjusted for

momentum, the cost reduction shrinks. One well known

investment manager shared with us an intuition thattrading costs haven't fallen at all -- they've just moved

from one bucket (fixed commissions) to other buckets(impact and delay.) There's some truth to that insight,

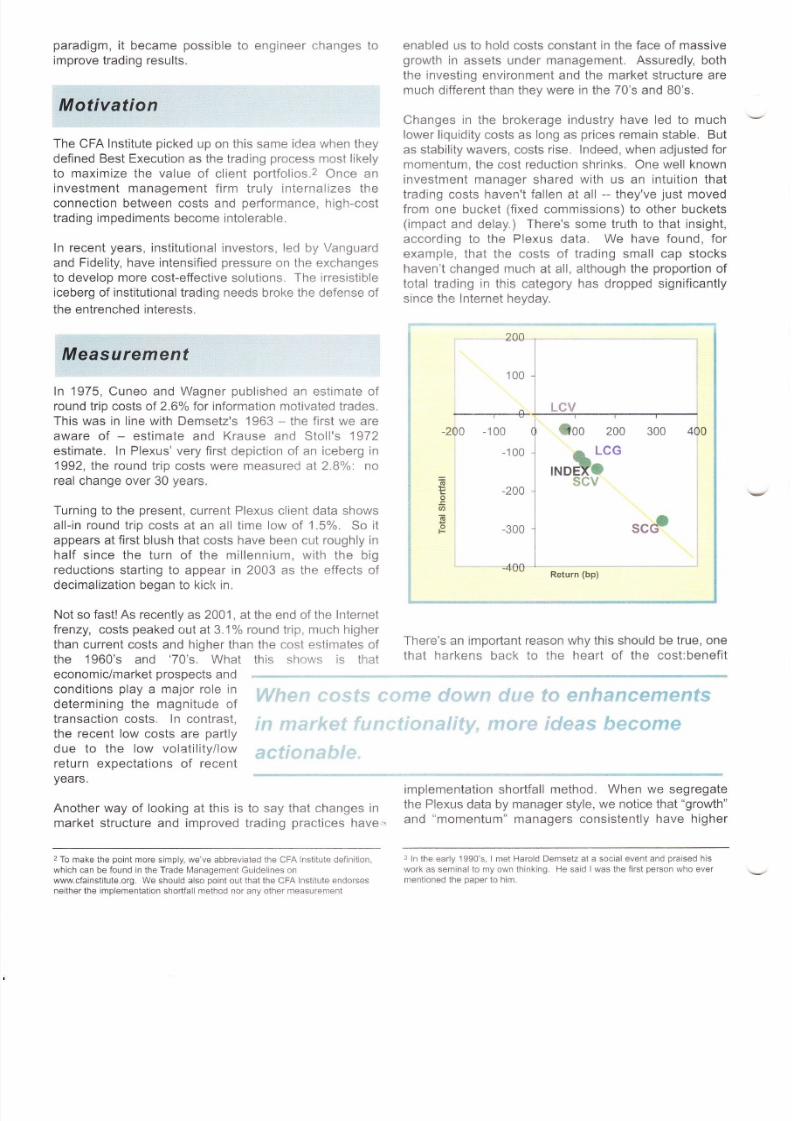

according to the Plexus data. We have found, forexample, that the costs of trading small cap stockshaven't changed much at all, although the proportion of

total trading in this category has dropped significantlysince the Internet heyday.

200

100

----r--+200 -100 &oo 200 300 400

-1 00

-200

-300

-400

e LCG

INDMS$evc

.E

: .cl.F SCGS

Return (bp)

There's an important reason why this should be true, one

that harkens back to the heart of the cost:benefit

...,',: .':.'.,.,..:.'::::ti:',. :1,:i''lii'lti;r-1,{.i{il'.i?l'::if':l$

,.. ,: :::';,:: ,1:',.a,.,.::":',a:::;::l .;';,..,.1:.;.',:: ::..,:::ill{;}:

ro"r"rt"ii".

.n"rnrll method. When we segregatethe Plexus data by manager style, we notice that "growth"

and "momentum" managers consistently have higher

*

i

"._*_*{

2 To make the point more simply, we've abbreviated the CFA Institute definition,

which can be found in the Trade l\4anagement Guidelines on

www.cfainstitute.org. We should also point out that the CFA Inst;tute endorses

neither the implementation shortfall method nor any other measurement

3 ln the early 1990's, I met Harold Demsetz at a social event and praised his

work as seminal to my own thinking. He said I was the first person who ever

mentioned the oaoer to him.

8/14/2019 The Maps Are Being Redrawn

http://slidepdf.com/reader/full/the-maps-are-being-redrawn 3/3

costs of trading than "value" or "contrarian" managers. In

Commentary 55 of May 1998, we measured trading costs

for large cap growth managers at 2.5 times the cost oflarge cap value managers. Small cap growth managers

spent twice the cost of small cap value managers.

The chart, reproduced from Commentary 55, graphs

trading costs by style against 30 day market adjusted

returns and draws two interesting conclusions: (1) the

dots representing costs vs. returns lie very close to a

straight line; and (2) the costs approached the experi-enced returns for each style. i.e. costs go up in lock step

with the information value.

We explained ". . . the value of the research dictates the

acceptable cost as managers filter out ideas with greater

expected cost, or stop trading when costs exceed idea

value. Either wav. manaqers overall are able to calibrate

costs to research value."

To summarize, in times of high expectations such as the

internet boom, transaction prices go up; in low expectation

times like 2002-2004, they go down. What we see here

is the returns expectations translated into an upper bound

on the cost of liquidity. This relationship of costs to

expectations seems to be a pointer to market efficiency,and goes a long way to explain why active management

net of costs looks like a zero-sum oame.

Lower Cosf Markets

It would be incorrect to conclude that the level ofexchange costs doesn't matter; it matters a great deal.

When costs come down due to enhancements in market

functionality, more ideas become actionable. Institutional

investors can profit from ideas that have smaller

expectations, to the benefit of investors. This is veryevident in the world of the high-turnover hedge funds,

who are able to trade for tinv returns at even tinier trade

costs.

Thus the changes in the markets and the coming titanic

struggle between NYSE/ARCA and NASDAQ/Instinet will

change the geography of the world of investing. Trading

of equities will merge with trading of bonds, options and

futures, opening new types of strategies that are too

difficult to execute now. We will redraw the map, and

investors will be the winners.

What will come of this in the future? Clearly both the

NYSE and NASDAQ are gathering resources for a titanic

clash. lt's hard to see who, if anyone, will ultimatelydominate. Any predictions are highly speculative, but

our guess would be a duopolistic standoff with both

systems surviving. We also predict continuing budding of

new trading technologies aimed at niche markets. Keeps

everybody on their toes.

Investors will be the clear winners, but the manner in

which investors win may be a

little more indirect than simplyfrom reduced trade costs. The

real gains will come from thenncnino rrn of new

investmentstrategies.

As the traditional barriers toprogress retreat, exchanges will

move on to the real work to be

done. The key to exchange improvement for institutional

investors lies, as always, in the enhancement of liquidity

and the strengthening of confidentiality. The major

challenge for the new consolidations will be to figure out

how information technology and high speed connectivity

can be used to promote these commanding institutional

needs.

However, connectivity won't solve all trading problems.

Ticking off orders against the book is fine when volatility

is low and the book is deep. However, high tech

solutions can traumatize when volatility is high,

momentum is strong and the book is thin. In those

situations hightouch markets show their merit, and find-

the-liquiciity services becorne more highly valued than

blazing speed. lf a headlong rush to high tech

connectivity destroys the high-touch capabilities of the

market, investors could be hurt.

Finally, don't expect the average cost of institutional

trading to remain low when a new boom drivesexpectations skyward. Transaction costs will still be top-

down driven by value expectations, not cost structures.

Plexus News *,;/.

Put this on your calendar! The Plexus Group 9th Client Conference is scheduled for September 18 - 20, 2005 at the :l:

Fairmont Turnberry Is/e Resort & Ctub (http://www.fairmont.com/turnberryisle/) 7:

,:,

![The Pythogorean Proposition Diagrams Redrawn [Clean]](https://img.pdfslide.net/doc/110x75/55cf990f550346d0339b51f6/the-pythogorean-proposition-diagrams-redrawn-clean.jpg)