Embed Size (px)

Citation preview

The Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

The Insured Annuity Concept

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

The Insured Annuity concept allows older clients to eliminate investment risk, earn a higher after-tax

income and guarantee the estate they leave behind.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Agenda – Insured Annuity

• Overview

- What it is

- Who it’s for

- How it works

• Case Study 1 – Increase income and preserve capital

• Case Study 2 – Maximizing an estate.

• Planning Considerations

• Conclusion

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

The Insured Annuity – What is it?

• Non-registered assets are placed in a Life Annuity with prescribed taxation.

• Life Insurance is purchased to replace the non-registered asset upon death.

• The tax free death benefit of Life Insurance combined with the tax advantages of Life Annuities increases income and the value of the estate

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Who’s it For?

• Clients over age 60

• Are concerned about

- Taxes

- Income

- Preservation of capital

- Leaving an estate

- Investment Risk

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Single Premium Immediate Annuities

• Income is 100% Guaranteed for the life of the annuitant.

• Annuity income will continue to a beneficiary for up to ten years if the annuitant dies prematurely.

• Beneficiary can elect to receive a commuted value instead of the payment stream.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

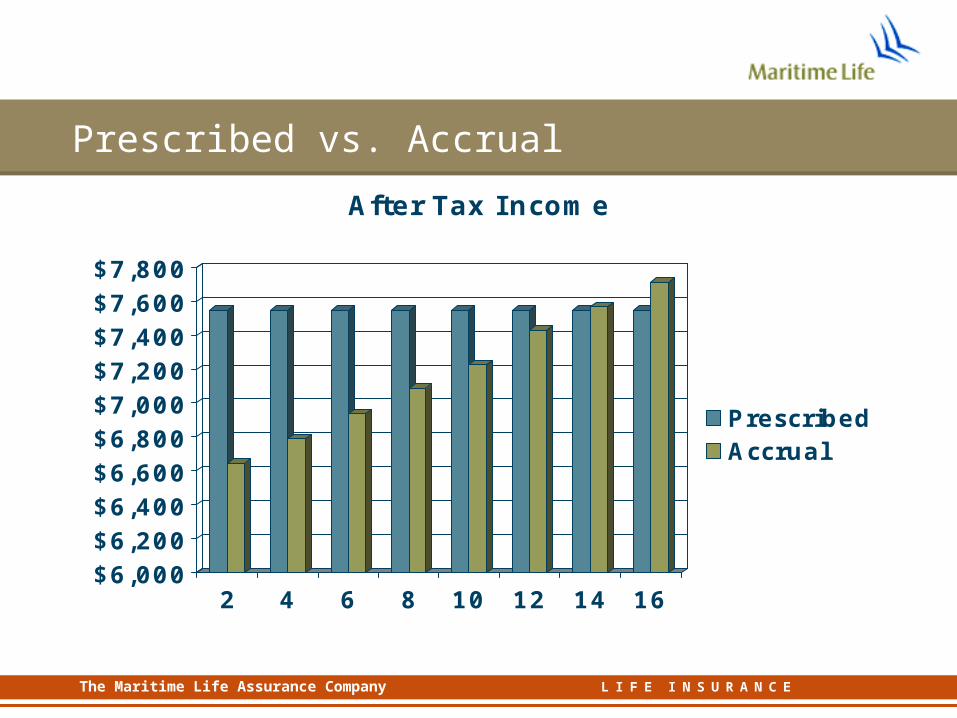

Prescribed vs. Accrual

$6,000$6,200$6,400$6,600$6,800$7,000$7,200$7,400$7,600$7,800

2 4 6 8 10 12 14 16

After Tax I ncome

PrescribedAccrual

The Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Case Study:Income and Capital Preservation

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Case Study

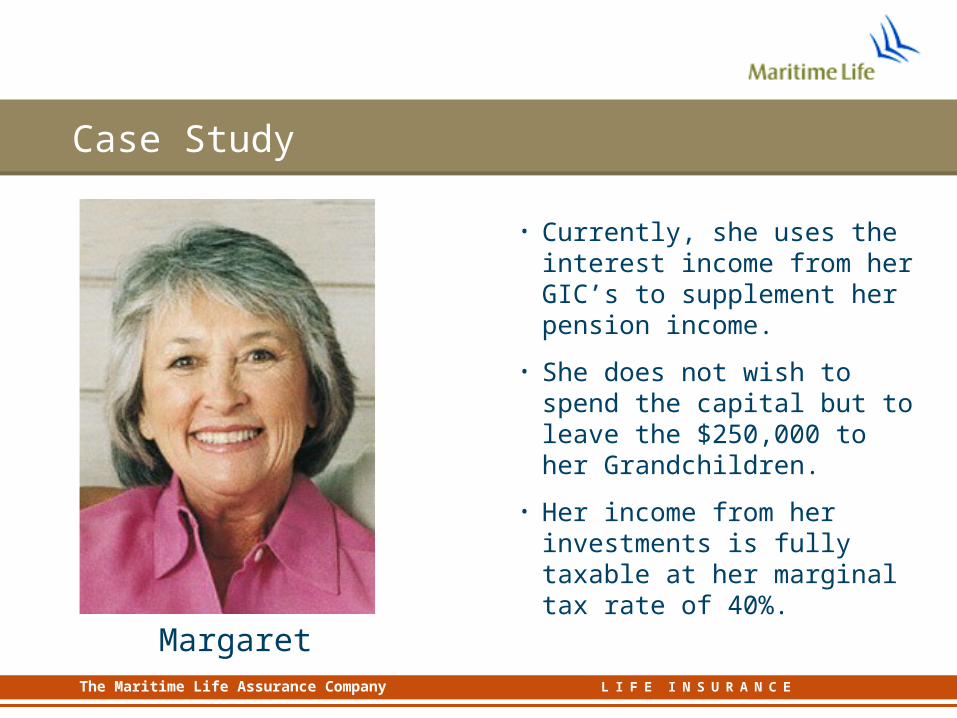

• Meet Margaret…

• 65 Years old

• Single.

• Retired and drawing income from her pensions.

• Very conservative - invests exclusively in fixed income.

• Has $250,000 in non-registered investments.

• Currently, she uses the interest income from her GIC’s to supplement her pension income.

• She does not wish to spend the capital but to leave the $250,000 to her Grandchildren.

• Her income from her investments is fully taxable at her marginal tax rate of 40%.

Margaret

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

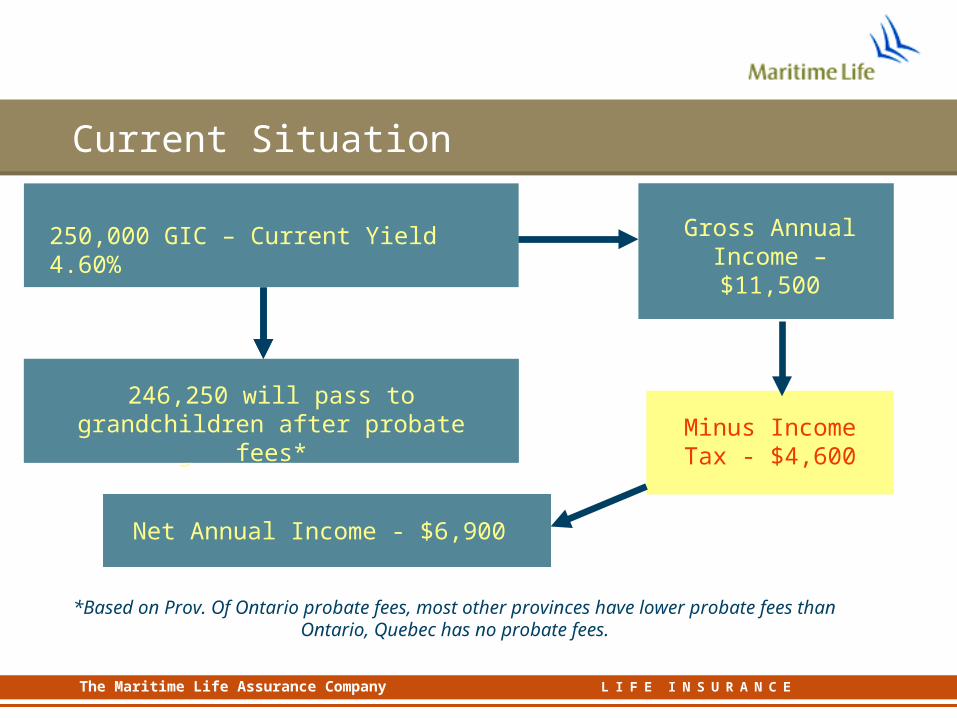

Current Situation

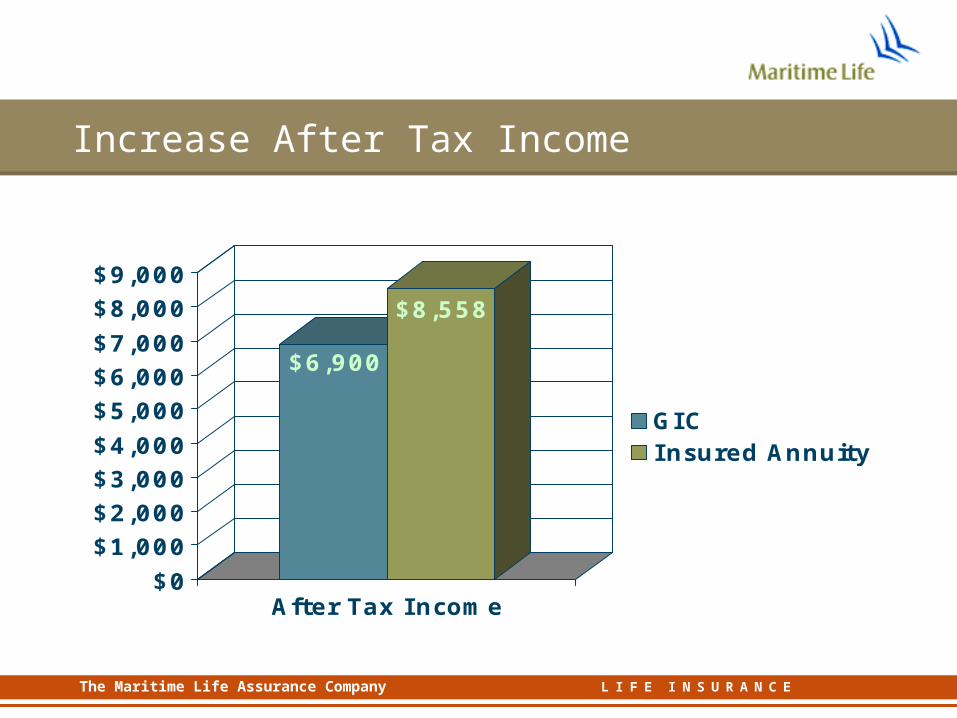

250,000 GIC – Current Yield 4.60% Gross Annual Income – $11,500

Minus Income Tax - $4,600

Net Annual Income - $6,900

$125,000 will pass through estate and then to grandchildren

246,250 will pass to grandchildren after probate fees*

*Based on Prov. Of Ontario probate fees, most other provinces have lower probate fees than Ontario, Quebec has no probate fees.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

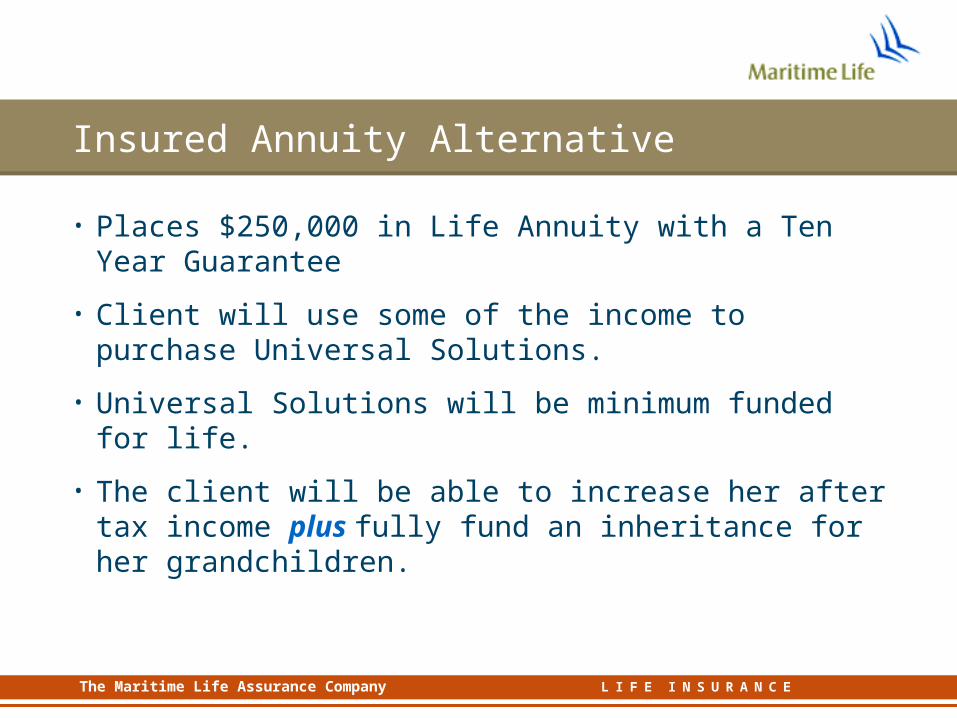

Insured Annuity Alternative

• Places $250,000 in Life Annuity with a Ten Year Guarantee

• Client will use some of the income to purchase Universal Solutions.

• Universal Solutions will be minimum funded for life.

• The client will be able to increase her after tax income plus fully fund an inheritance for her grandchildren.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

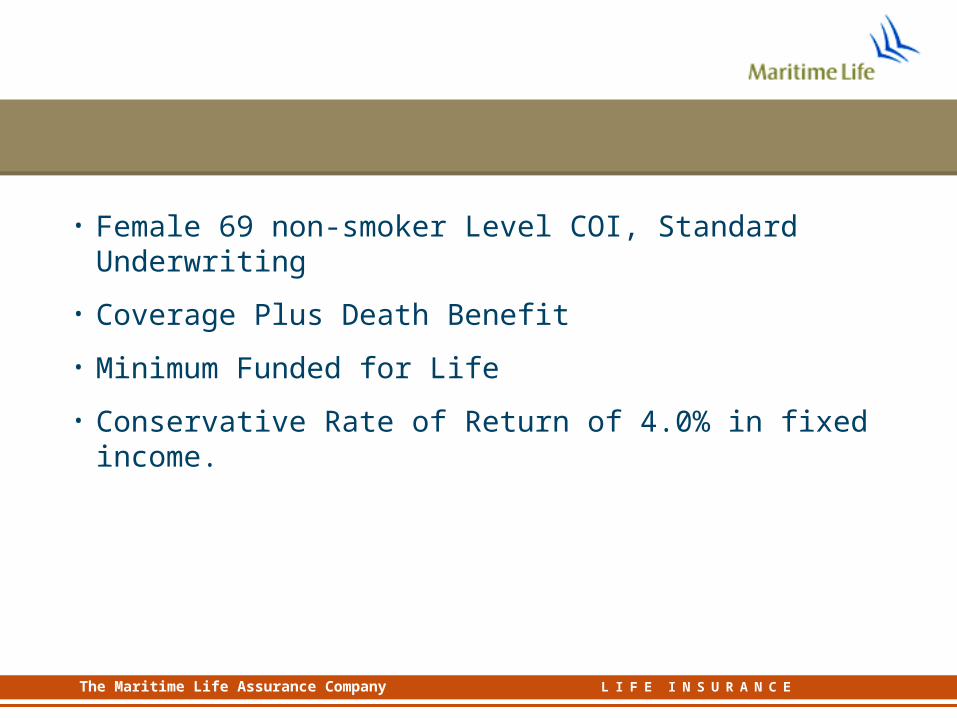

• Female 69 non-smoker Level COI, Standard Underwriting

• Coverage Plus Death Benefit

• Minimum Funded for Life

• Conservative Rate of Return of 4.0% in fixed income.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

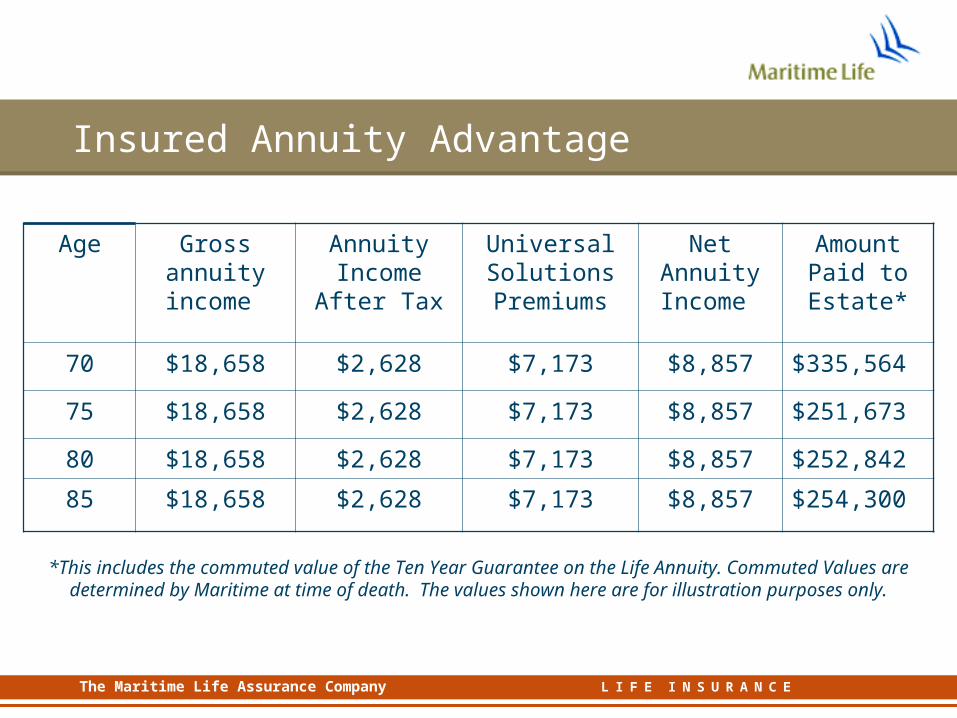

Insured Annuity Advantage

$250,00 Placed in Life 10 Annuity Gross Annual Income – $18,659

Minus Income Tax - $2,628

Net Annual Income - $8,858$7,173 used to

purchase UL

*$254,300 passes to grandchildren - no taxes, no probate fees

*$128,226 is based on death occurring at life expectancy: age 85 with coverage plus Universal Solutions with Level COI and a rate of return of 4.0%.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Insured Annuity Advantage

Age Gross annuity income

Annuity Income

After Tax

Universal Solutions Premiums

Net Annuity Income

Amount Paid to Estate*

70 $18,658 $2,628 $7,173 $8,857 $335,564

75 $18,658 $2,628 $7,173 $8,857 $251,673

80 $18,658 $2,628 $7,173 $8,857 $252,842

85 $18,658 $2,628 $7,173 $8,857 $254,300

*This includes the commuted value of the Ten Year Guarantee on the Life Annuity. Commuted Values are determined by Maritime at time of death. The values shown here are for illustration

purposes only.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Increase After Tax Income

$6,900

$8,558

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

After Tax Income

GICInsured Annuity

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Superior Estate Values

*Includes commuted value of ten year guarantee on annuity payments should death occur before the end of the guarantee period.

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

$550,000

66 70 74 78 82 86 90 94 98

Total paid out to estate*

Estate with GIC –

$246,250

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

The Ideal Solution

• Universal Solutions Offers:

- Level Guaranteed COI

- Attractive GIA options

- Wide Range of index options available

- Guaranteed Policy Fees

- Guaranteed MER’s

- Guaranteed availability of investment options

- Death Benefit Guarantee

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

The Ideal Solution con’t

• The Death Benefit Guarantee is of particular interest to Margaret:

- The purpose of the insurance is to leave an estate.

- Margaret is a very conservative investor, however:

- The Death Benefit Guarantee allows her to take advantage of higher returns of equity indexes

- Her estate can benefit from the upside of equity markets while being protected from downturns.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Conclusion

• Margaret was able to increase her after tax income from her investment.

• Leave a larger estate - fully guaranteed

• Using the security of the Death Benefit Guarantee, she can take advantage of Index Linked Accounts.

• Avoid probate fees.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

• Bob and Joan Hill

• Well into Retirement

• He is 75 and she is 74 years of age.

• Have more than enough retirement assets to last the rest of their lives.

• Wish to leave a sizable estate to their family.

• Very conservative investors.

• They are High Net Worth retirees.

• Top marginal tax bracket of 46%.

• They have $500,000 that they are confident they will not need for themselves.

• They would like to use these unsheltered funds to create an estate

Case Study

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

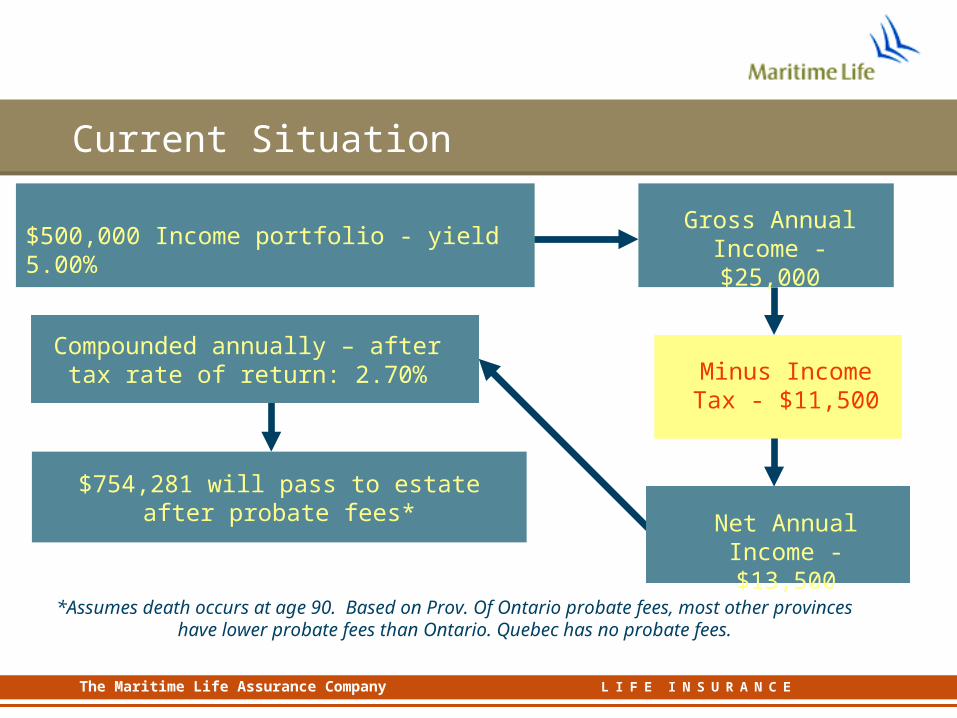

Current Situation

$500,000 Income portfolio - yield 5.00%

Minus Income Tax - $11,500

Gross Annual Income - $25,000

Net Annual Income - $13,500

$754,281 will pass to estate after probate fees*

*Assumes death occurs at age 90. Based on Prov. Of Ontario probate fees, most other provinces have lower probate fees than Ontario. Quebec has no probate fees.

Compounded annually – after tax rate of return: 2.70%

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

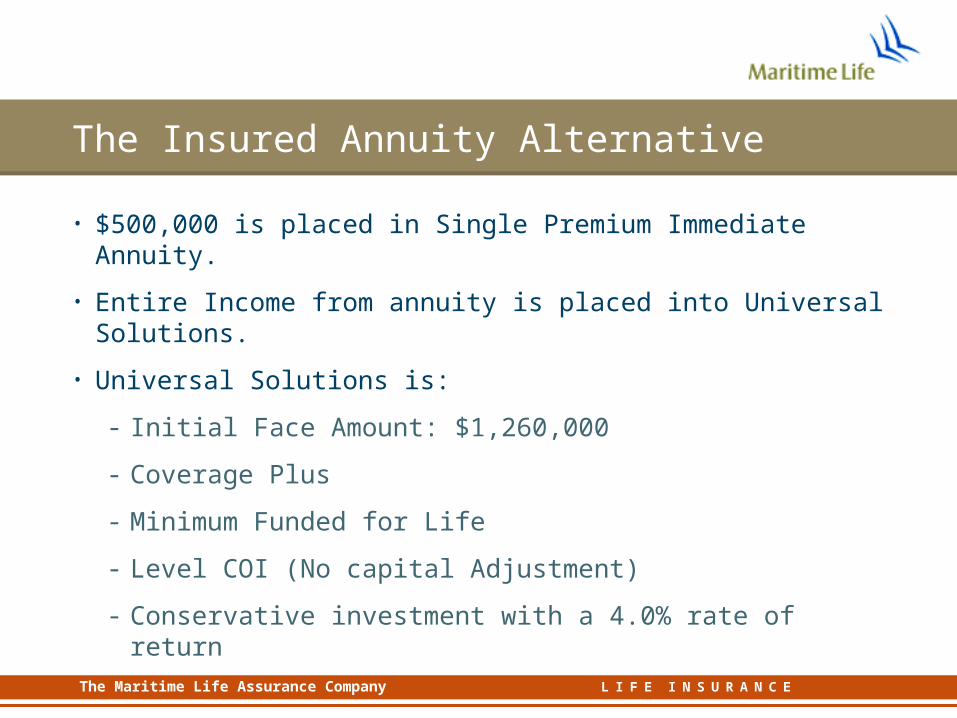

The Insured Annuity Alternative

• $500,000 is placed in Single Premium Immediate Annuity.

• Entire Income from annuity is placed into Universal Solutions.

• Universal Solutions is:

- Initial Face Amount: $1,260,000

- Coverage Plus

- Minimum Funded for Life

- Level COI (No capital Adjustment)

- Conservative investment with a 4.0% rate of return

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

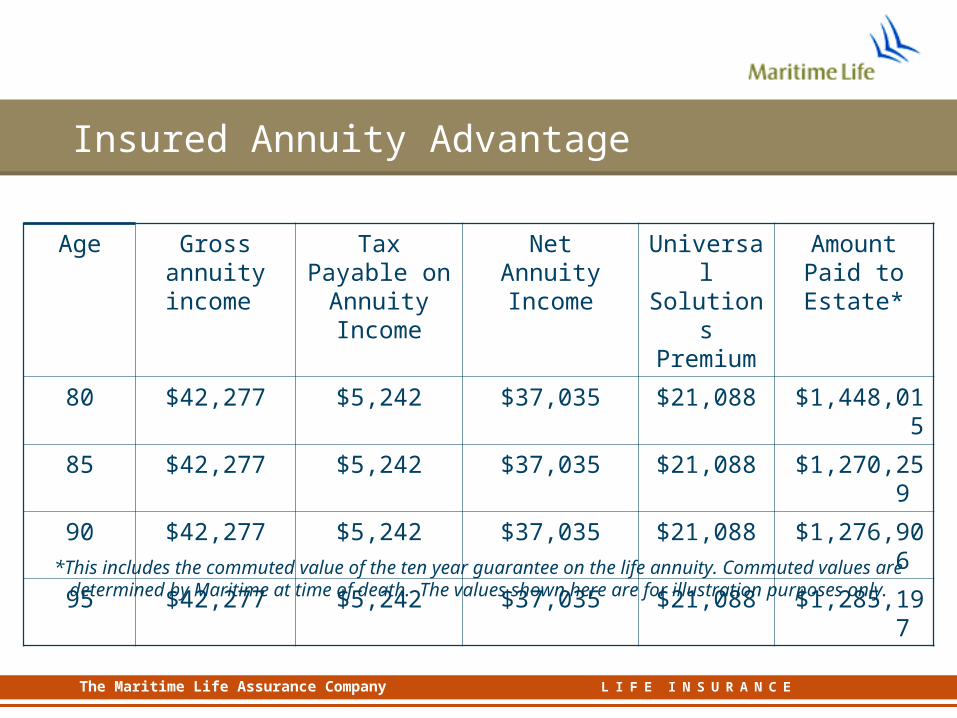

Insured Annuity Advantage

Age Gross annuity income

Tax Payable on Annuity

Income

Net Annuity Income

Universal Solutions Premium

Amount Paid to Estate*

80 $42,277 $5,242 $37,035 $21,088 $1,448,015

85 $42,277 $5,242 $37,035 $21,088 $1,270,259

90 $42,277 $5,242 $37,035 $21,088 $1,276,906

95 $42,277 $5,242 $37,035 $21,088 $1,285,197

*This includes the commuted value of the ten year guarantee on the life annuity. Commuted values are determined by Maritime at time of death. The values shown here are for illustration

purposes only.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Greater Estate Value

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

80 85 90 95

Insured Annuity Portfolio

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Conclusion

• Using the tax efficiencies of Universal Life contracts and single premium immediate annuities…

• The Hill’s were able to significantly improve the value of their estate by using the insured annuity concept.

• At age 90 their estate would be worth 31% more with the Insured Annuity concept.

• The Insured Annuity concept will bypass the expense and delay of probate.

The Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Planning Considerations

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Things to Consider

• Clients need to understand that an annuity will lock in their capital.

• Therefore, they need to make sure there is adequate liquidity

• If there is no income requirement and the objective is to maximize their estate, consider the Estate Creator with Universal Solutions.

The Maritime Life Assurance CompanyThe Maritime Life Assurance CompanyThe Maritime Life Assurance Company L I F E I N S U R A N C E

Special Quotes

• Term to 100 may be considered but would require a special quote if it is used within the Insured Annuity concept. Minimum case size – Premium of $15,000.

• If clients are over age 80 and it is a joint last to die case, annuities are available with a guarantee to age 90 on a special quote basis. This allows Prescribed Taxation.

• Special quote will be required for annuitants over age 80 with a guarantee period to age 90. Minimum case size $250,000.00

![Quality Assurance Program Description · NEI-06-14 Revision 98 [Nuclear Development] Quality Assurance Program Description v [Company Name] POLICY STATEMENT [Company Name] ([Company](https://img.pdfslide.net/doc/110x75/6008c971c812e421ad757625/quality-assurance-program-description-nei-06-14-revision-98-nuclear-development.jpg)