Embed Size (px)

Citation preview

JAPAN INTERNATIONAL COOPERATION AGENCY (JICA)

MINISTRY OF TRADE AND INDUSTRY (MOTI) THE REPUBLIC OF KENYA

THE MASTER PLAN STUDY FOR

KENYAN INDUSTRIAL DEVELOPMENT

(MAPSKID) IN

THE REPUBLIC OF KENYA

FINAL REPORT

ANNEX

JANUARY 2008

SANYU CONSULTANTS INC., JAPAN KRI INTERNATIONAL CORP., JAPAN

CONTENTS

Annex 1 List of Stakeholders.......................................................................................................... 1-1

Annex 2 List of Supporting Organisations...................................................................................... 2-1

Annex 3 Questionnaire for the Cluster Analysis............................................................................. 3-1

Annex 4 Related Organisations....................................................................................................... 4-1

Annex 5 Result of the Cluster Analysis .......................................................................................... 5-1

Annex 6 102 Companies in Kenya ................................................................................................. 6-1

Annex 7 Agro-industrial Maps ....................................................................................................... 7-1

Annex 8 Record of Workshops ....................................................................................................... 8-1

Annex 9 Record of Forums............................................................................................................. 9-1

Annex 10 Record of National Seminar ........................................................................................... 10-1

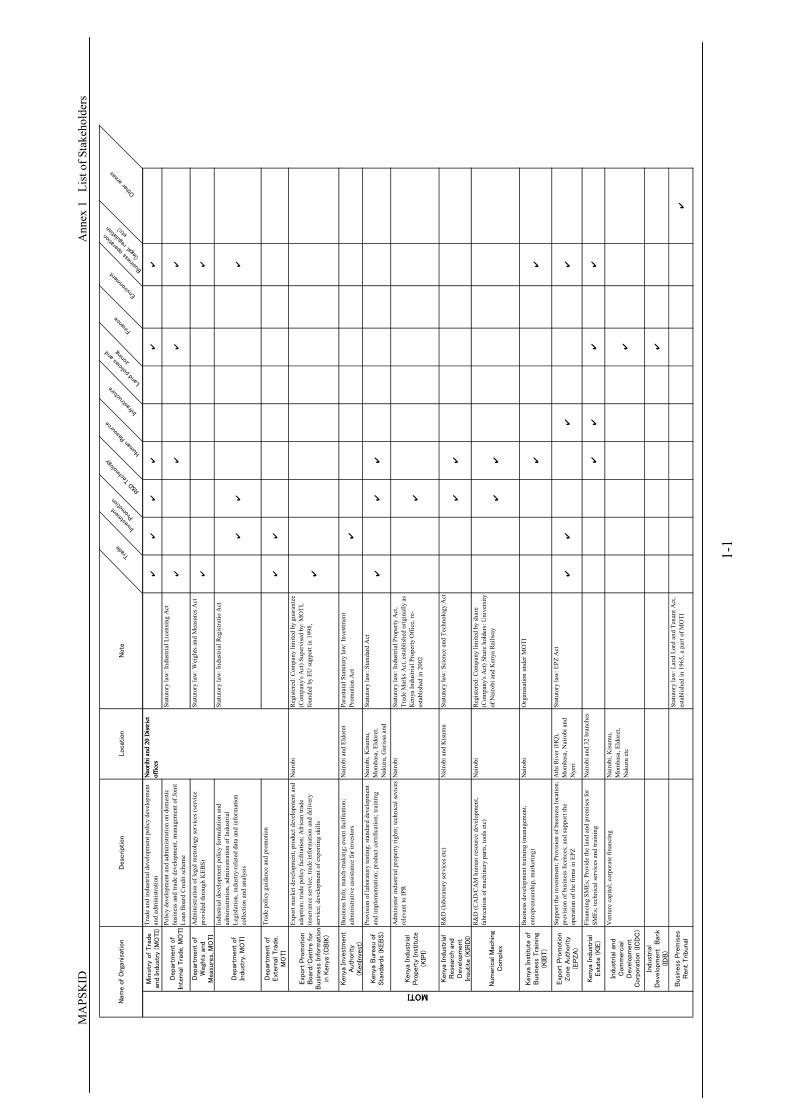

Annex 1 List of Stakeholders

MA

PSK

ID

Ann

ex 1

Li

st o

f Sta

keho

lder

s

1-

1

Desc

ript

ion

Loca

tion

Note

Trad

e

Inve

stm

ent

Prom

otio

n

R&D

Tech

nolo

gyHu

man

Res

ourc

e

Infra

stru

ctur

eLa

nd p

olic

ies

and

zonin

g

Fina

nce

Envir

onm

ent

Busin

ess

oper

atio

n

(lega

l, re

gulat

ion

etc)

Oth

er a

reas

Nam

e o

f O

rgan

isat

ion

Nao

ribi a

nd 2

0 D

istri

ctof

fices

MOTI

Min

istr

y of Tra

de

and

Indu

stry

(M

OTI)

Trad

e an

d in

dust

rial d

evel

opm

ent p

olic

y de

velo

pmen

tan

d ad

min

istra

tion

✔✔

✔✔

✔✔

Depar

tmen

t of

Inte

rnal

Tra

de, M

OTI

Polic

y de

velo

pmen

t and

adm

inis

tratio

n on

dom

estic

busi

ness

and

trad

e de

velo

pmen

t, m

anag

emen

t of J

oint

Loan

Boa

rd C

redi

t sch

eme

Stat

utor

y la

w: I

ndus

trial

Lic

ensi

ng A

ct✔

✔✔

✔

Depar

tmen

t of

Weg

hts

and

Meas

ure

s, M

OTI

Adm

inis

tratio

n of

lega

l met

rolo

gy se

rvic

es (s

ervi

cepr

ovid

ed th

roug

h K

EBS)

Stat

utor

y la

w: W

eigh

ts a

nd M

easu

res A

ct✔

✔

Depar

tmen

t of

Indust

ry, M

OTI

Indu

stria

l dev

elop

men

t pol

icy

form

ulat

ion

and

adm

inis

tratio

n, a

dmin

istra

tion

of In

dust

rial

Legi

slat

ion,

indu

stry

-rel

ated

dat

a an

d in

form

atio

nco

llect

ion

and

anal

ysis

Stat

utor

y la

w: I

ndus

trial

Reg

istra

tio A

ct

✔✔

✔

Depar

tmen

t of

Ext

ern

al T

rade,

MO

TI

Trad

e po

licy

guid

ance

and

pro

mot

ion

✔✔

Exp

ort

Pro

motion

Boar

d/C

ent

re f

orB

usi

nes

s In

form

atio

nin

Ken

ya (

CB

IK)

Expo

rt m

arke

t dev

elop

men

t; pr

oduc

t dev

elop

men

t and

adop

tion;

trad

e po

licy

faci

litat

ion;

Afr

ican

trad

ein

surr

ance

serv

ice;

trad

e in

form

atio

n an

d de

liver

yse

rvic

e; d

evel

opm

ent o

f exp

ortin

g sk

ills

Nai

robi

Regi

ster

ed: C

ompa

ny li

mite

d by

gua

rant

ee(C

ompa

ny's

Act

) Sup

ervi

sed

by: M

OTI

,fo

unde

d by

EU

supp

ort i

n 19

98,

✔

Kenya

Inv

est

men

tA

uthority

(KenI

nvest

)

Busi

ness

Info

; mat

ch-m

akin

g; e

vent

faci

litat

ion;

adm

inis

trativ

e as

sist

ance

for i

nves

tors

Nai

robi

and

Eld

oret

Para

stat

al S

tatu

tory

law

: Inv

estm

ent

Prom

otio

n A

ct✔

Ken

ya B

ure

au o

fSta

ndar

ds

(KEB

S)

Prov

isio

n of

labo

rato

ry te

stin

g; st

anda

rd d

evel

opm

ent

and

impl

emen

tatio

n; p

rodu

ct c

ertif

icat

ion;

trai

ning

Nai

robi

, Kis

umu,

Mom

basa

, Eld

oret

,N

akur

u, G

aris

sa a

ndN

i

Stat

utor

y la

w: S

tand

ard

Act

✔✔

✔

Kenya

Ind

ust

rial

Pro

per

ty Ins

titu

te(K

IPI)

Adm

inis

ter i

ndus

trial

pro

perty

righ

ts; t

echn

ical

sevi

ces

rele

vant

to IP

RN

airo

biSt

atut

ory

law

: Ind

ustri

al P

rope

rty A

ct,

Trad

e M

arks

Act

, est

ablis

hed

orig

inal

ly a

sK

enya

Indu

stria

l Pro

perty

Offi

ce, r

e-es

tabl

ishe

d in

200

2✔

Kenya

Ind

ust

rial

Rese

arch

and

Dev

elo

pment

Insu

tite

(KIR

DI)

R&D

(lab

orat

ory

serv

ices

etc

)N

airo

bi a

nd K

isum

uSt

atut

ory

law

: Sci

ence

and

Tec

hnol

ogy

Act

✔✔

Num

eric

al M

achin

gC

om

plex

R&D

(CA

D/C

AM

hum

an re

sour

ce d

evel

opm

ent,

fabr

icat

ion

of m

achi

nery

par

ts, t

ools

etc

)N

airo

biRe

gist

ered

: Com

pany

lim

ited

by sh

are

(Com

pany

's A

ct) S

hare

hol

ders

: Uni

vers

ityof

Nai

robi

and

Ken

ya R

ailw

ay✔

✔

Kenya

Ins

titu

te o

fB

usi

nes

s Tra

inin

g(K

IBT)

Busi

ness

dev

elop

men

t tra

inin

g (m

anag

emen

t,en

trepr

eneu

rshi

p, m

arke

ting)

Nai

robi

Org

anis

atio

n un

der M

OTI

✔✔

Exp

ort

Pro

motion

Zone

Auth

ority

(EPZA

)

Supp

ort t

he in

vest

men

t; Pr

ovis

ion

of b

usin

ess l

ocat

ion;

prov

isio

n of

bus

ines

s lic

ence

s; a

nd su

ppor

t the

oper

atio

n of

the

firm

s in

EPZ

Ath

i Riv

er (H

Q),

Mom

basa

, Nai

robi

and

Nye

ri

Stat

utor

y la

w: E

PZ A

ct

✔✔

✔✔

Kenya

Ind

ust

rial

Est

ate (KIE

)

Fina

ncin

g SM

Es; P

rovi

de th

e la

nd a

nd p

rem

ises

for

SMEs

; tec

hnic

al se

rvic

es a

nd tr

aini

ngN

airo

bi a

nd 3

2 br

anch

es✔

✔✔

✔

Indu

strial

and

Com

mer

cia

lD

evelo

pment

Corp

ora

tion (IC

DC

)

Ven

ture

cap

ital;

corp

orat

e fin

anci

ngN

airo

bi, K

isum

u,M

omba

sa, E

ldor

et,

Nak

uru

etc

✔

Indust

rial

Deve

lopm

ent

B

ank

(ID

B)

✔

Busi

ness

Pre

mis

es

Rent

Tribuna

l

Stat

utor

y la

w: L

and

Lord

and

Ten

ant A

ct,

esta

blis

hed

in 1

965,

a p

art o

f MO

TI✔

Nao

ribi a

nd 2

0 D

istri

ctof

fices

MOTI

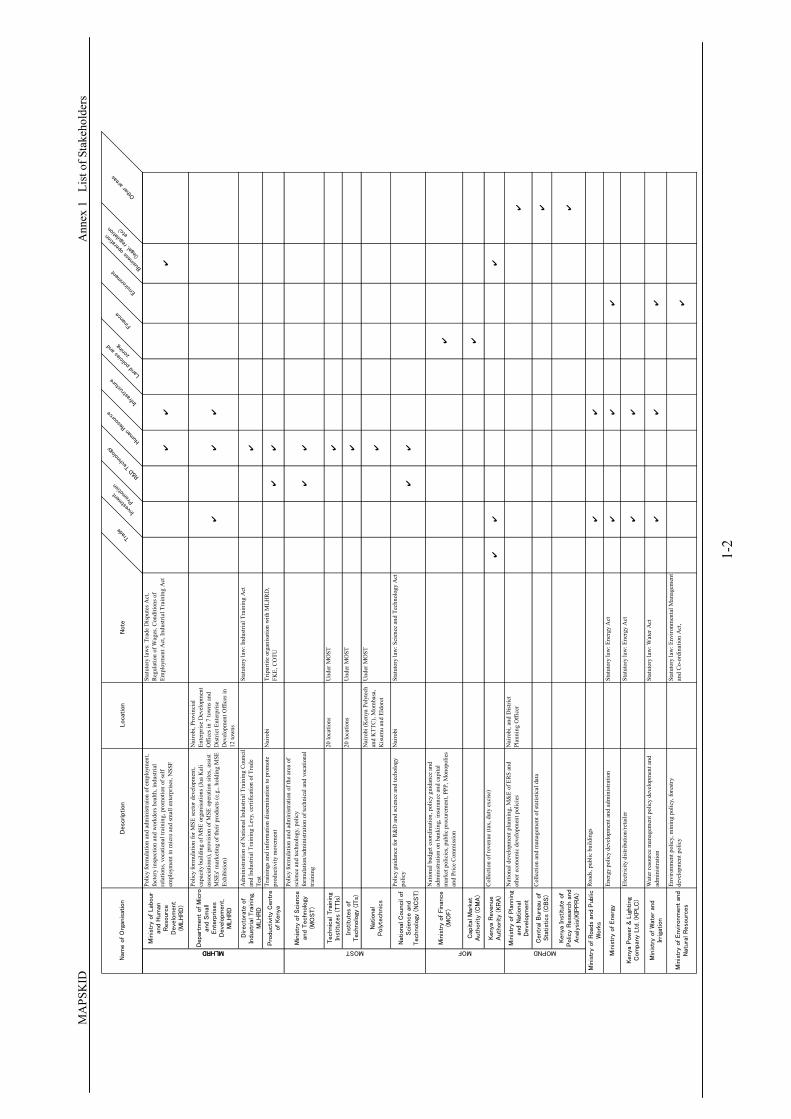

MA

PSK

ID

Ann

ex 1

Li

st o

f Sta

keho

lder

s

1-

2

Desc

ription

Locat

ion

Note

Trad

e

Inve

stm

ent

Prom

otion

R&D

Tech

nolo

gyHu

man

Res

ourc

e

Infra

stru

ctur

eLa

nd p

olic

ies

and

zonin

g

Fina

nce

Envir

onm

ent

Busin

ess

oper

atio

n

(lega

l, re

gulat

ion

etc)

Oth

er a

reas

Nam

e o

f O

rgan

isat

ion

MLHRD

Min

istr

y of Lab

our

and H

um

anR

eso

urc

eD

eve

lom

ent

(MLH

RD

)

Polic

y fo

rmul

atio

n an

d ad

min

istra

ion

of e

mpl

oym

ent,

fact

ory

insp

ectio

n an

d w

orkd

ers h

ealth

, ind

ustri

alre

latio

ns, v

ocat

iona

l tra

inin

g, p

rom

otio

n of

self

empl

oym

ent i

n m

icro

and

smal

l ent

erpr

ises

, NSS

F

Stat

utor

y la

ws:

Tra

de D

ispu

tes A

ct,

Regu

latio

n of

Wag

es, C

ondi

tions

of

Empl

oym

ent A

ct, I

ndus

trial

Tra

inin

g A

ct✔

✔✔

Depa

rtm

ent

of M

icro

and

Sm

all

Ente

rprise

sD

eve

lopm

ent,

MLH

RD

Polic

y fo

rmul

atio

n fo

r MSE

sect

or d

evel

opm

ent,

capa

city

bui

ldin

g of

MSE

org

anis

atio

ns (J

ua K

ali

asso

ciat

ions

), pr

ovis

ion

of M

SE o

pera

tion

site

s, as

sist

MSE

s' m

arke

ting

of th

eir p

rodu

cts (

e.g.

, hol

ding

MSE

Exhi

bisi

on)

Nai

robi

, Pro

vinc

ial

Ente

rpris

e D

evel

opm

ent

Offi

ces i

n 7

tow

ns a

ndD

istri

ct E

nter

pris

eD

evel

opm

ent O

ffice

s in

12 to

wns

✔✔

✔

Directo

rate

of

Indu

strial

Tra

inin

g,M

LH

RD

Adm

inis

tratio

n of

Nat

iona

l Ind

ustri

al T

rain

ing

Cou

ncil

and

Indu

stria

l Tra

inin

g Le

vy, c

ertif

icat

ion

of T

rade

Test

Stat

utor

y la

w: I

ndus

trial

Tra

inin

g A

ct✔

Pro

ductivi

ty C

entr

eof Kenya

Trai

ning

s and

info

rmat

ion

diss

emin

atio

n to

pro

mot

epr

oduc

tivity

mov

emen

tN

airo

biTr

ipar

tite

orga

nisa

tion

with

MLH

RD,

FKE,

CO

TU✔

✔

Min

istr

y of Scie

nce

and

Technolo

gy(M

OST)

Polic

y fo

rmul

atio

n an

d ad

min

istra

tion

of th

e ar

ea o

fsc

ienc

e an

d te

chno

logy

, pol

icy

form

ulat

ion/

adm

inis

tratio

n of

tech

nica

l and

voc

atio

nal

train

ing

✔✔

Technic

al T

rain

ing

Inst

itute

s (T

TIs

)

20 lo

catio

nsU

nder

MO

ST✔

Inst

itute

s of

Technolo

gy (IT

s)

20 lo

catio

nsU

nder

MO

ST✔

Nat

ional

Poly

technic

s

Nai

robi

(Ken

ya P

olyt

ech

and

KTT

C),

Mom

basa

,K

isum

u an

d El

dore

t

Und

er M

OST

✔

Nat

ional

Council

of

Scie

nce a

nd

Technolo

gy (

NC

ST)

Polic

y gu

idan

ce fo

r R&

D a

nd sc

ienc

e an

d te

chol

ogy

polic

yN

airo

biSt

atut

ory

law

: Sci

ence

and

Tec

hnol

ogy

Act

✔✔

Min

istr

y of

Fin

ance

(MO

F)

Nat

iona

l bud

get c

oord

inat

ion,

pol

icy

guid

ance

and

adm

inis

tratio

n on

ban

king

, ins

uran

ce a

nd c

apita

lm

arke

t pol

icie

s, pu

blic

pro

cure

men

t, PP

P, M

onop

olie

san

d Pr

ice

Com

mis

sion

✔

Cap

ital

Mar

ket

Aut

hority

(C

MA

)✔

Kenya

Reve

nue

Auth

ority

(KR

A)

Col

lect

ion

of re

venu

e (ta

x, d

uty

exci

se)

✔✔

✔

Min

istr

y of Pla

nnin

gan

d N

atio

nal

Deve

lopm

ent

Nat

iona

l dev

elop

men

t pla

nnin

g, M

&E

of E

RS a

ndot

her e

cono

mic

dev

elop

men

t pol

icie

sN

airo

bi, a

nd D

istri

ctPl

anni

ng O

ffice

r✔

Centr

al B

ure

au o

fSta

tist

ics

(CB

S)

Col

lect

ion

and

man

agem

ent o

f sta

tistic

al d

ata

✔

Kenya

Inst

itute

of

Polic

y R

ese

arch a

nd

Anal

ysis

(KIP

PR

A)

✔

Road

s, pu

blic

bui

ldin

gs✔

✔

Ener

gy p

olic

y de

velo

pmen

t and

adm

inis

tratio

nSt

atut

ory

law

: Ene

rgy

Act

✔✔

✔

Elec

trici

ty d

istri

butio

n/re

taile

rSt

atut

ory

law

: Ene

rgy

Act

✔✔

Wat

er re

sour

ce m

anag

emen

t pol

icy

deve

lopm

ent a

ndad

min

istra

tion

Stat

utor

y la

w: W

ater

Act

✔✔

✔

Envi

ronm

ent p

olic

y, m

inin

g po

licy,

fore

stry

deve

lopm

ent p

olic

ySt

atut

ory

law

: Env

ironm

enta

l Man

agem

ent

and

Co-

ordi

natio

n A

ct,

✔M

inis

try

of Envi

ronm

ent

and

Nat

ura

l R

eso

urc

es

Min

istr

y of R

oad

s an

d P

ublic

Work

s

Min

istr

y of Energ

y

Kenya

Pow

er

& L

ighting

Com

pan

y Ltd

. (K

PLC

)

MOPNDMOFMOSTMLHRD

Min

istr

y of

Wat

er

and

Irriga

tion

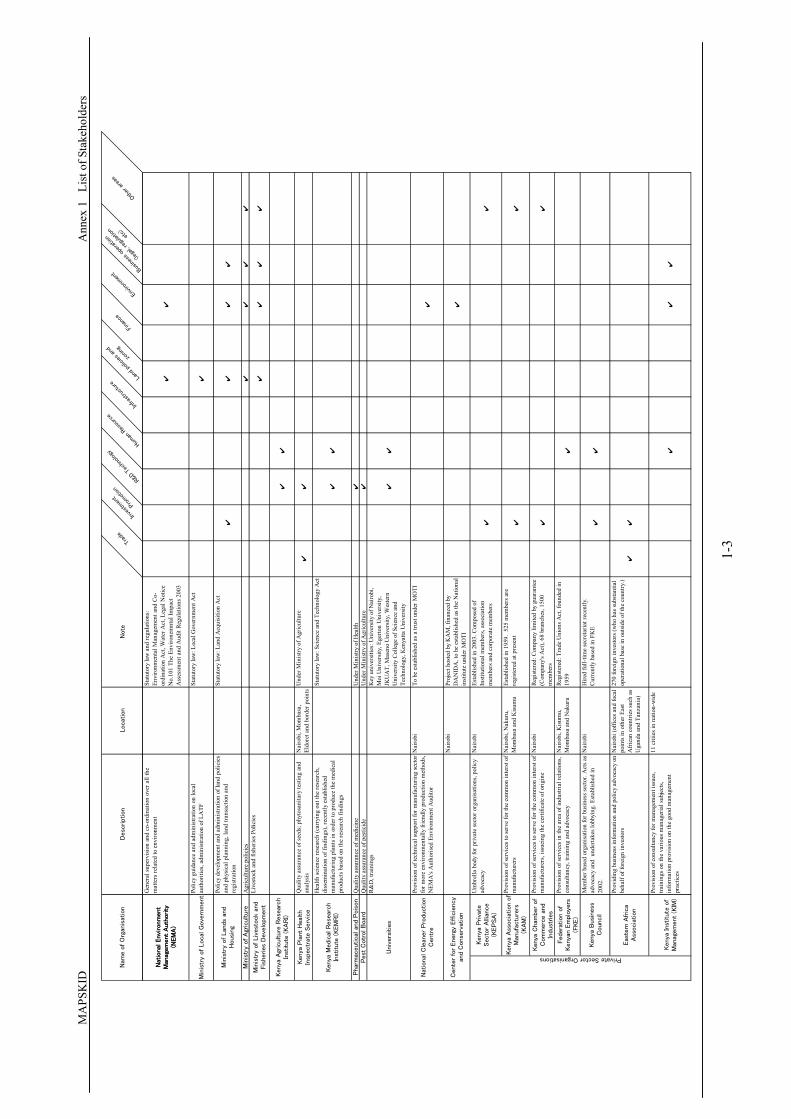

MA

PSK

ID

Ann

ex 1

Li

st o

f Sta

keho

lder

s

1-

3

Desc

ription

Loca

tion

Not

e

Trad

e

Inve

stm

ent

Prom

otio

n

R&D

Tech

nolo

gyHu

man

Res

ourc

e

Infra

stru

ctur

eLa

nd p

olic

ies

and

zonin

g

Fina

nce

Envir

onm

ent

Busin

ess

oper

atio

n

(lega

l, re

gulat

ion

etc)

Oth

er a

reas

Nat

iona

l Envi

ronm

ent

Man

agem

ent

Aut

hority

(NEM

A)

Nam

e of

Org

anis

atio

n

Gen

eral

supe

rvis

ion

and

co-o

rdin

atio

n ov

er a

ll th

em

atte

rs re

late

d to

env

ironm

ent

Stat

utor

y la

w a

nd re

gula

tions

:En

viro

nmen

tal M

anag

emen

t and

Co-

ordi

natio

n A

ct, W

ater

Act

, Leg

al N

otic

eN

o.10

1 Th

e En

viro

nem

ntal

Impa

ctA

sses

smen

t and

Aud

it Re

gula

tions

200

3

✔✔

Polic

y gu

idan

ce a

nd a

dmin

istra

tion

on lo

cal

auth

oriti

es, a

dmin

istra

tion

of L

ATF

Stat

utor

y la

w: L

ocal

Gov

ernm

ent A

ct✔

Polic

y de

velo

pmen

t and

adm

inis

tratio

n of

land

pol

icie

san

d ph

ysic

al p

lann

ing,

land

tran

sact

ion

and

regi

stra

tion

Stat

utor

y la

w: L

and

Acq

uisi

tion

Act

✔✔

✔✔

Agr

icul

ture

pol

icie

s✔

✔✔

✔Li

vest

ock

and

fishe

ries P

olic

ies

✔✔

✔✔

✔✔

Qua

lity

assu

ranc

e of

seed

s; p

hyto

sani

tary

test

ing

and

anal

ysis

Nai

robi

, Mom

basa

,El

dore

t and

bor

der p

oint

sU

nder

Min

istry

of A

gric

ultu

re✔

✔

Hea

lth sc

ienc

e re

sear

ch (c

arry

ing

out t

he re

sear

ch,

diss

emin

atio

n of

find

ings

), re

cent

ly e

stab

lishe

dm

anuf

actu

ring

plan

ts in

ord

er to

pro

duce

the

med

ical

prod

ucts

bas

ed o

n th

e re

sear

ch fi

ndin

gs

Stat

utor

y la

w: S

cien

ce a

nd T

echn

olog

y A

ct

✔✔

Qua

lity

assu

ranc

e of

med

icin

eU

nder

Min

istry

of H

ealth

✔Q

ualit

y as

sura

nce

of p

estic

ide

Und

er M

inis

try o

f Agr

icul

ture

✔R&

D, t

rain

ings

Key

uni

vers

ities

: Uni

vers

ity o

f Nai

robi

,M

oi U

nive

rsity

, Ege

rton

Uni

vers

ity,

JKU

AT,

Mas

eno

Uni

vers

ity, W

este

rnU

nive

rsity

Col

lege

of S

cien

ce a

ndTe

chno

logy

, Ken

yatta

Uni

vers

ity

✔✔

Prov

isio

n of

tech

nica

l sup

port

for m

anuf

actu

ring

sect

orfo

r mor

e en

viro

nmen

tally

frie

ndly

pro

duct

ion

met

hods

,N

EMA

's A

utho

rised

Env

ironm

ent A

udito

r

Nai

robi

To b

e es

tabl

ishe

d as

a tr

ust u

nder

MO

TI

✔

Nai

robi

Proj

ect h

oste

d by

KA

M, f

inan

ced

byD

AN

IDA

, to

be e

stab

lishe

d as

the

Nat

iona

lin

stitu

te u

nder

MO

TI✔

Ken

ya P

riva

teS

ecto

r A

llian

ce

(KEP

SA

)

Um

brel

la b

ody

for p

rivat

e se

ctor

org

anis

atio

ns, p

olic

yad

voca

cyN

airo

biEs

tabl

ishe

d in

200

3. C

ompo

sed

ofIn

stitu

tiona

l mem

bers

, ass

ocia

tion

mem

bers

and

cor

pora

te m

embe

rs✔

✔

Ken

ya A

ssoci

atio

n o

fM

anufa

ctu

rers

(KA

M)

Prov

isio

n of

serv

ices

to se

rve

for t

he c

omm

on in

ters

t of

man

ufac

ture

rsN

airo

bi, N

akur

u,M

omba

sa a

nd K

isum

uEs

tabl

ishe

d in

195

9. 5

25 m

embe

rs a

rere

gist

ered

at p

rese

nt✔

✔

Keny

a C

ham

ber

of

Com

mer

ce a

nd

Indus

trie

s

Prov

isio

n of

serv

ices

to se

rve

for t

he c

omm

on in

ters

t of

man

ufac

ture

rs, i

ssue

ing

the

certi

ficat

e of

orig

ine

Nai

robi

Regi

ster

ed: C

ompa

ny li

mite

d by

gua

rant

ee(C

ompa

ny's

Act

), 68

bra

nche

s, 15

00m

embe

rs✔

✔

Fed

erat

ion o

fKeny

an E

mpl

oyer

s(F

KE)

Prov

isio

n of

serv

ices

in th

e ar

ea o

f ind

ustri

al re

latio

ns,

cons

ulta

ncy,

trai

ning

and

adv

ocac

yN

airo

bi, K

isum

u,M

omba

sa a

nd N

akur

uRe

gist

ered

: Tra

de U

nion

s Act

, fou

nded

in19

59✔

Keny

a B

usi

ness

Cou

ncil

Mem

ber b

ased

org

anis

atio

n fo

r bus

ines

s sec

tor.

Act

s as

advo

cacy

and

und

erta

kes l

obby

ing.

Est

ablis

hed

in20

02.

Nai

robi

Hire

d fu

ll-tim

e se

cret

aria

t rec

ently

.C

urre

ntly

bas

ed in

FK

E✔

✔

Eas

tern

Afr

ica

Ass

oci

atio

n

Prov

idin

g bu

sine

ss in

form

atio

n an

d po

licy

advo

cacy

on

beha

lf of

fore

ign

inve

stor

sN

airo

bi (o

ffice

s and

foca

lpo

ints

in o

ther

Eas

tA

fric

an c

ount

ries s

uch

asU

gand

a an

d Ta

nzan

ia)

270

fore

ign

inve

stor

s (w

ho h

as su

bsta

ntia

lop

erat

iona

l bas

e in

out

side

of t

he c

ount

ry.)

✔✔

Keny

a In

stitut

e of

Man

agem

ent

(KIM

)

Prov

isio

n of

con

sulta

ncy

for m

anag

emen

t iss

ues,

train

ings

on

the

vario

us m

anag

eria

l sub

ject

s,in

form

atio

n pr

ovis

ion

on th

e go

od m

anag

emen

tpr

actic

es

11 c

itiie

s in

natio

n-w

ide

✔✔

✔

Nat

ional

Cle

aner

Pro

duction

Cent

re

Cen

ter

for

Ener

gy E

ffic

ienc

yan

d C

ons

erv

atio

n

Private Sector Organisations

Ken

ya M

edic

al R

ese

arch

Inst

itute

(KEM

RI)

Phar

mac

eutical

and

Poi

son

Pest

Cotr

ol B

oard

Uni

vers

itie

s

Min

istr

y of

Agr

icul

ture

Min

istr

y of

Liv

est

ock

and

Fis

heries

Deve

lopm

ent

Ken

ya A

gric

ultu

re R

ese

arch

Inst

itut

e (K

AR

I)

Ken

ya P

lant

Hea

lth

Insp

ectr

ate S

erv

ice

Nat

iona

l Envi

ronm

ent

Man

agem

ent

Aut

hority

(NEM

A)

Min

istr

y of Loc

al G

overn

ment

Min

istr

y of Lan

ds

and

Hous

ing

MA

PSK

ID

Ann

ex 1

Li

st o

f Sta

keho

lder

s

1-

4

Desc

ription

Locat

ion

Note

Trad

e

Inve

stm

ent

Prom

otio

n

R&D T

echn

olog

yHum

an R

esou

rce

Infra

stru

ctur

eLa

nd p

olic

ies

and

zonin

g

Fina

nce

Envir

onm

ent

Busin

ess

oper

atio

n

(lega

l, re

gulat

ion

etc)

Oth

er a

reas

Nam

e o

f O

rgan

isat

ion

Private SectorOrganisations

Inst

itute

of

Cert

ifie

dP

ubl

ic A

ccounta

nt

of

Kenya

(IC

PA

K)

Mem

ber o

rgan

isat

ion

of p

ract

icin

g C

PAs,

sem

i-st

atut

ory

body

for a

ccou

ntin

g, c

usto

dian

of t

he C

ode

ofEt

hic,

trai

ning

s and

pol

icy

advi

sory

rele

vant

toco

rpor

ate

sect

or re

gula

tions

Stat

utor

y la

w: A

ccou

tant

s Act

. It i

sm

anda

tory

to b

e a

mem

ber o

f IC

PAK

for

prac

ticin

g C

PAs (

2700

mem

bers

)✔

✔

Mar

keting

Socie

ty o

fKenya

(M

SK)

Mem

ber-

base

d or

gani

satio

n fo

r mar

ketin

gpr

actic

ione

rs, b

oth

indi

vidu

als a

nd c

orpo

rate

mem

bers

✔

Kenya

Ban

kers

'A

ssocia

tion

✔

Ass

ocia

tion o

f Kenya

Insu

rers

✔

Kenya

Moto

rIn

dust

ry A

ssoc

iation

(KM

I)

Lobb

ying

and

har

mon

isat

ion

of is

sues

rele

vant

for t

hem

embe

rsTh

e m

embe

rs in

clud

e as

sem

bler

s, su

pplie

rsof

par

ts, a

nd im

porte

rs/re

taile

rs. T

heor

gani

satio

n is

not

regi

ster

ed fo

rmal

ly.

✔

Kenya

Fis

hExp

ort

ers

and

Pro

cess

ors

Ass

ocia

tion

Qua

lity

cont

rol a

nd h

arm

onis

atio

n, tr

aini

ng fo

r qua

lity

cont

rol,

polic

y ad

voca

cy, r

esea

rche

s and

info

rmat

ion

shar

ing,

infr

astru

ctur

e de

velo

pmen

t for

fish

ing

Nai

robi

and

Kis

umu

MO

U w

ith th

e M

inis

try o

f Liv

estc

ok a

ndFi

sher

y✔

Kenya

IC

TK

EPSA

affi

liate

Com

pute

r S

ocie

ty o

fKenya

✔

Phar

mac

eutical

Socie

ty o

f Kenya

✔

Agr

ochem

ical

sA

ssocia

tion o

f Kenya

(KEN

YA

)✔

Petr

ole

um

Inst

itute

of Eas

t A

fric

a (P

IEA

)

Gro

up o

f com

pani

es in

pet

role

um a

nd p

etro

-rel

ated

indu

stry

for p

rom

otio

n of

pet

ro-r

elat

ed e

nter

pris

es in

Ken

ya✔

Com

merc

ial B

anks

✔M

icro

finan

ce

✔

Nai

robi S

tock

Exc

han

ge✔

Accounting

firm

s✔

PrivateSectorServicePrivate Sector Organisations

Private SectorOrganisations

Annex 2 List of Supporting Organisations

MA

PSK

ID

Ann

ex 2

Li

st o

f Sup

porti

ng O

rgan

isat

ions

2-

1

Ser

vices

Loc

atio

nN

ote

Mar

ketin

g

Mar

ket a

ndbu

sines

sin

form

atio

n Human Re

sour

ce

Deve

lopm

ent In

frast

ruct

ur e

R&D

TECH In

form

atio

n

Fina

nce

Man

agem

ent

Advis

ory

Adm

in Supp

ort

Oth

er serv

ices

Nam

e of Suppo

rtin

gIn

stitution

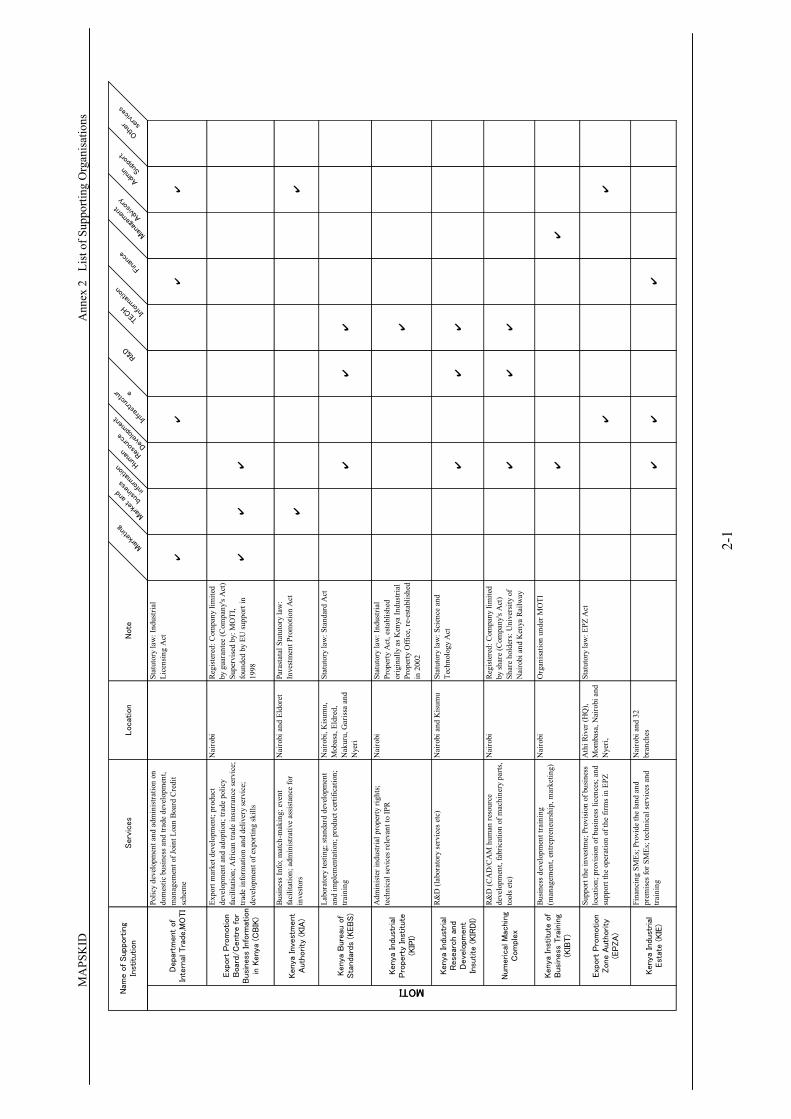

MOTI

Depa

rtm

ent

of

Inte

rnal

Tra

de,M

OTI

Polic

y de

velo

pmen

t and

adm

inis

tratio

n on

dom

estic

bus

ines

s and

trad

e de

velo

pmen

t,m

anag

emen

t of J

oint

Loa

n Bo

ard

Cre

dit

sche

me

Stat

utor

y la

w: I

ndus

trial

Lice

nsin

g A

ct

✔✔

✔✔

Exp

ort

Pro

motion

Boa

rd/C

entr

e fo

rB

usi

nes

s In

form

atio

nin

Keny

a (C

BIK

)

Expo

rt m

arke

t dev

elop

men

t; pr

oduc

tde

velo

pmen

t and

ado

ptio

n; tr

ade

polic

yfa

cilit

atio

n; A

fric

an tr

ade

insu

rran

ce se

rvic

e;tra

de in

form

atio

n an

d de

liver

y se

rvic

e;de

velo

pmen

t of e

xpor

ting

skill

s

Nai

robi

Regi

ster

ed: C

ompa

ny li

mite

dby

gua

rant

ee (C

ompa

ny's

Act

)Su

perv

ised

by:

MO

TI,

foun

ded

by E

U su

ppor

t in

1998

✔✔

✔

Kenya

Inv

est

ment

Aut

hor

ity

(KIA

)

Busi

ness

Info

; mat

ch-m

akin

g; e

vent

faci

litat

ion;

adm

inis

trativ

e as

sist

ance

for

inve

stor

s

Nai

robi

and

Eld

oret

Para

stat

al S

tatu

tory

law

:In

vest

men

t Pro

mot

ion

Act

✔✔

Ken

ya B

ureau

of

Sta

ndar

ds

(KEB

S)

Labo

rato

ry te

stin

g; st

anda

rd d

evel

opm

ent

and

impl

emen

tatio

n; p

rodu

ct c

ertif

icat

ion;

train

ing

Nai

robi

, Kis

umu,

Mob

asa,

Eld

red,

Nak

uru,

Gar

issa

and

Nye

ri

Stat

utor

y la

w: S

tand

ard

Act

✔✔

✔

Ken

ya Ind

ust

rial

Pro

pert

y In

stitute

(KIP

I)

Adm

inis

ter i

ndus

trial

pro

perty

righ

ts;

tech

nica

l sev

ices

rele

vant

to IP

RN

airo

biSt

atut

ory

law

: Ind

ustri

alPr

oper

ty A

ct, e

stab

lishe

dor

igin

ally

as K

enya

Indu

stria

lPr

oper

ty O

ffice

, re-

esta

blis

hed

in 2

002

✔

Ken

ya Ind

ust

rial

Res

ear

ch a

nd

Deve

lopm

ent

Insu

tite

(KIR

DI)

R&D

(lab

orat

ory

serv

ices

etc

)N

airo

bi a

nd K

isum

uSt

atut

ory

law

: Sci

ence

and

Tech

nolo

gy A

ct✔

✔✔

Num

eric

al M

achin

gC

om

plex

R&D

(CA

D/C

AM

hum

an re

sour

cede

velo

pmen

t, fa

bric

atio

n of

mac

hine

ry p

arts

,to

ols e

tc)

Nai

robi

Regi

ster

ed: C

ompa

ny li

mite

dby

shar

e (C

ompa

ny's

Act

)Sh

are

hold

ers:

Uni

vers

ity o

fN

airo

bi a

nd K

enya

Rai

lway

✔✔

✔

Kenya

Inst

itute

of

Busi

ness

Tra

inin

g(K

IBT)

Busi

ness

dev

elop

men

t tra

inin

g(m

anag

emen

t, en

trepr

eneu

rshi

p, m

arke

ting)

Nai

robi

Org

anis

atio

n un

der M

OTI

✔✔

Exp

ort

Pro

mot

ion

Zon

e A

uth

ority

(EPZA

)

Supp

ort t

he in

vest

me;

Pro

visi

on o

f bus

ines

slo

catio

n; p

rovi

sion

of b

usin

ess l

icen

ces;

and

supp

ort t

he o

pera

tion

of th

e fir

ms i

n EP

Z

Ath

i Riv

er (H

Q),

Mom

basa

, Nai

robi

and

Nye

ri,

Stat

utor

y la

w: E

PZ A

ct

✔

✔

Ken

ya Ind

ust

rial

Est

ate (KIE

)

Fina

ncin

g SM

Es; P

rovi

de th

e la

nd a

ndpr

emis

es fo

r SM

Es; t

echn

ical

serv

ices

and

train

ing

Nai

robi

and

32

bran

ches

✔✔

✔

MOTI

MA

PSK

ID

Ann

ex 2

Li

st o

f Sup

porti

ng O

rgan

isat

ions

2-

2

Serv

ices

Locat

ion

Note

Mar

ketin

g

Mar

ket a

ndbu

sines

sinf

orm

atio

n Hum

an Reso

urce

Deve

lopm

ent In

frast

ruct

ur e

R&D

TECH In

form

atio

n

Fina

nce

Man

agem

ent

Advis

ory

Adm

in Supp

ort

Oth

er serv

ices

Nam

e o

f Suppor

ting

Inst

itut

ion

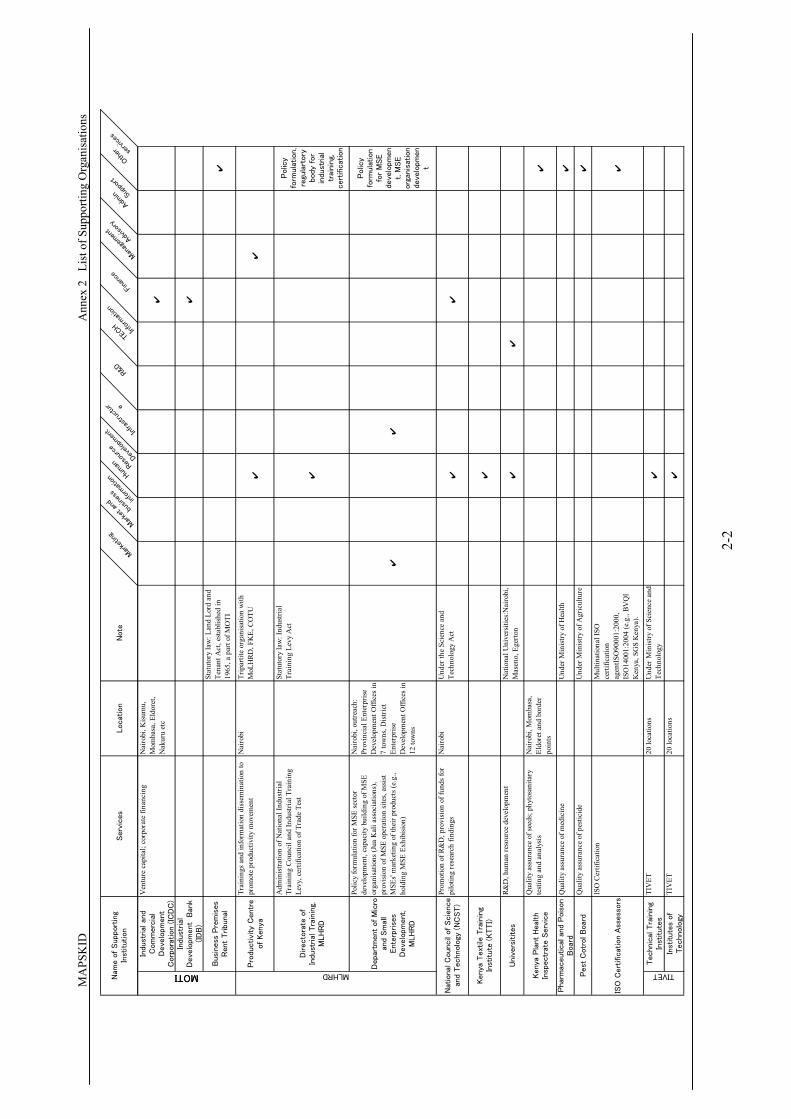

MOTIIn

dust

rial

and

Com

merc

ial

Deve

lopm

ent

Corp

orat

ion (IC

DC

)

Ven

ture

cap

ital;

corp

orat

e fin

anci

ngN

airo

bi, K

isum

u,M

omba

sa, E

ldor

et,

Nak

uru

etc

✔

Indust

rial

Deve

lopm

ent

Ban

k(ID

B)

✔

Bus

iness

Pre

mis

esR

ent

Tribunal

Stat

utor

y la

w: L

and

Lord

and

Tena

nt A

ct, e

stab

lishe

d in

1965

, a p

art o

f MO

TI✔

Pro

ductivi

ty C

entr

eof Ken

ya

Trai

ning

s and

info

rmat

ion

diss

emin

atio

n to

prom

ote

prod

uctiv

ity m

ovem

ent

Nai

robi

Trip

artit

e or

gani

satio

n w

ithM

oLH

RD, F

KE,

CO

TU✔

✔

Directo

rate

of

Indust

rial

Tra

inin

g,M

LH

RD

Adm

inis

tratio

n of

Nat

iona

l Ind

ustri

alTr

aini

ng C

ounc

il an

d In

dust

rial T

rain

ing

Levy

, cer

tific

atio

n of

Tra

de T

est

Stat

utor

y la

w: I

ndus

trial

Trai

ning

Lev

y A

ct

✔

Polic

yfo

rmula

tion,

regu

lart

ory

bod

y fo

rin

dust

rial

trai

nin

g,cer

tificat

ion

Depar

tment

of M

icro

and S

mal

lEnte

rprise

sD

eve

lopm

ent

,M

LH

RD

Polic

y fo

rmul

atio

n fo

r MSE

sect

orde

velo

pmen

t, ca

paci

ty b

uild

ing

of M

SEor

gani

satio

ns (J

ua K

ali a

ssoc

iatio

ns),

prov

isio

n of

MSE

ope

ratio

n si

tes,

assi

stM

SEs'

mar

ketin

g of

thei

r pro

duct

s (e.

g.,

hold

ing

MSE

Exh

ibis

ion)

Nai

robi

, out

reac

h:Pr

ovin

cial

Ent

erpr

ise

Dev

elop

men

t Offi

ces i

n7

tow

ns, D

istri

ctEn

terp

rise

Dev

elop

men

t Offi

ces i

n12

tow

ns

✔✔

Polic

yfo

rmul

atio

nfo

r M

SE

deve

lopm

en

t, M

SE

org

anis

atio

ndeve

lopm

en

t

Prom

otio

n of

R&

D, p

rovi

sion

of f

unds

for

pilo

ting

rese

arch

find

ings

Nai

robi

Und

er th

e Sc

ienc

e an

dTe

chno

logy

Act

✔✔

✔

R&D

, hum

an re

sour

ce d

evel

opm

ent

Nat

iona

l Uni

vers

ities

:Nai

robi

,M

asen

o, E

gerto

n✔

✔

Qua

lity

assu

ranc

e of

seed

s; p

hyto

sani

tary

test

ing

and

anal

ysis

Nai

robi

, Mom

basa

,El

dore

t and

bor

der

poin

ts✔

Qua

lity

assu

ranc

e of

med

icin

eU

nder

Min

istry

of H

ealth

✔

Qua

lity

assu

ranc

e of

pes

ticid

eU

nder

Min

istry

of A

gric

ultu

re✔

ISO

Cer

tific

atio

nM

ultin

atio

nal I

SOce

rtific

atio

nag

entIS

O90

001:

2000

,IS

O14

001:

2004

(e.g

., BV

QI

Ken

ya, S

GS

Ken

ya).

✔

Tec

hnic

al T

rain

ing

Inst

itute

s

TIV

ET20

loca

tions

Und

er M

inis

try o

f Sci

ence

and

Tech

nolo

gy✔

Inst

itute

s of

Technol

ogy

TIV

ET20

loca

tions

✔

Kenya

Pla

nt

Heal

thIn

spec

trat

e S

erv

ice

Phar

mac

eutical

and P

oiso

nB

oar

d

Pest

Cotr

ol B

oar

d

ISO

Cert

ific

atio

n A

ssess

ors

MOTI MLHRD

Nat

iona

l C

ounc

il of Scie

nce

and T

echnol

ogy

(N

CST)

Kenya

Text

ile T

rain

ing

Inst

itute

(KTTI)

Univ

ers

itites

TIVET

MA

PSK

ID

Ann

ex 2

Li

st o

f Sup

porti

ng O

rgan

isat

ions

2-

3

Serv

ices

Locat

ion

Note

Mar

ketin

g

Mar

ket a

ndbu

sines

sin

form

atio

n Hum

an Reso

urce

Deve

lopm

ent In

frast

ruct

ur e

R&D

TECH In

form

atio

n

Fina

nce

Man

agem

ent

Adviso

ry

Adm

in Supp

ort

Oth

er serv

ices

Nam

e o

f Suppor

ting

Inst

itution

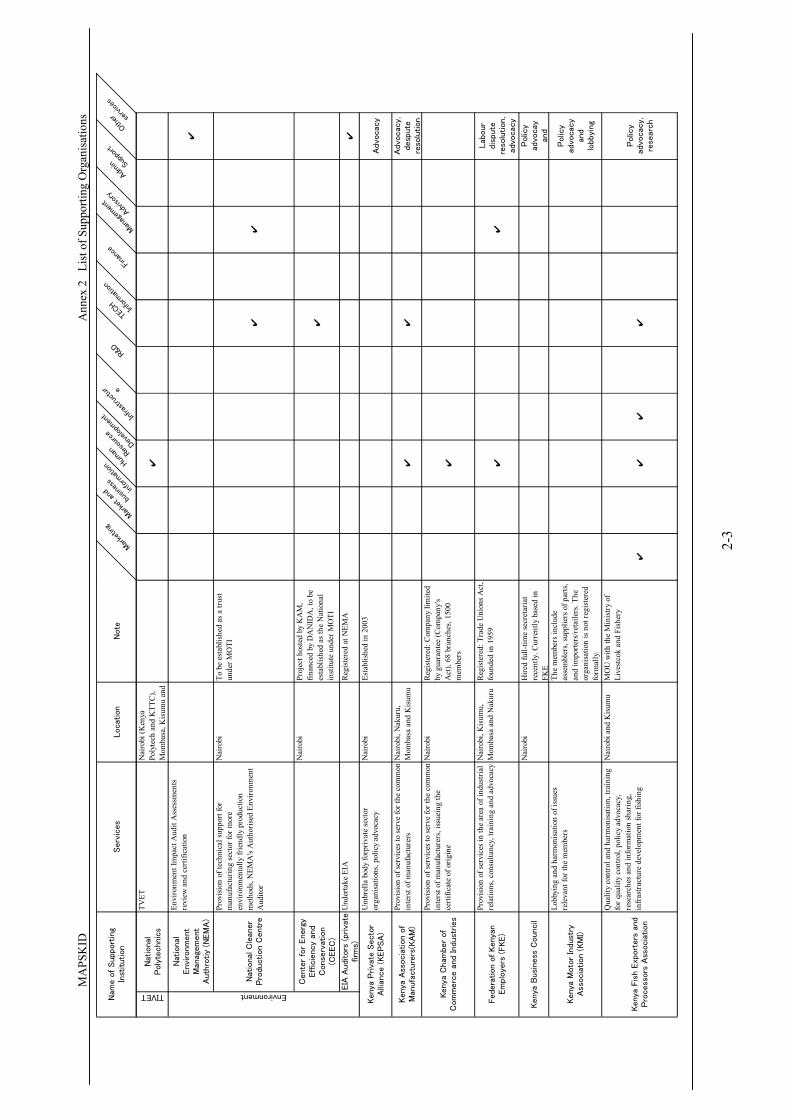

TIVET

Nat

ional

Pol

ytechnic

s

TVET

Nai

robi

(Ken

yaPo

lyte

ch a

nd K

TTC

),M

omba

sa, K

isum

u an

d✔

Nat

iona

lEnvi

ronm

ent

Man

agem

ent

Auth

rotiy

(NEM

A)

Envi

ronm

ent I

mpa

ct A

udit

Ass

essm

ents

revi

ew a

nd c

ertif

icat

ion

✔

Nat

ional

Cle

aner

Pro

duction

Centr

e

Prov

isio

n of

tech

nica

l sup

port

for

man

ufac

turin

g se

ctor

for m

ore

envi

ronm

enta

lly fr

iend

ly p

rodu

ctio

nm

etho

ds, N

EMA

's A

utho

rised

Env

ironm

ent

Aud

itor

Nai

robi

To b

e es

tabl

ishe

d as

a tr

ust

unde

r MO

TI

✔✔

Cent

er for

Ene

rgy

Effic

ienc

y an

dC

onse

rvat

ion

(CEEC

)

Nai

robi

Proj

ect h

oste

d by

KA

M,

finan

ced

by D

AN

IDA

, to

bees

tabl

ishe

d as

the

Nat

iona

lin

stitu

te u

nder

MO

TI✔

EIA

Auditor

s (p

riva

tefirm

s)U

nder

take

EIA

Regi

ster

ed a

t NEM

A✔

Um

brel

la b

ody

forp

rivat

e se

ctor

orga

nisa

tions

, pol

icy

advo

cacy

Nai

robi

Esta

blis

hed

in 2

003

Advo

cac

y

Prov

isio

n of

serv

ices

to se

rve

for t

he c

omm

onin

ters

t of m

anuf

actu

rers

Nai

robi

, Nak

uru,

Mom

basa

and

Kis

umu

✔✔

Advo

cac

y,desp

ute

reso

lution

Prov

isio

n of

serv

ices

to se

rve

for t

he c

omm

onin

ters

t of m

anuf

actu

rers

, iss

uein

g th

ece

rtific

ate

of o

rigin

e

Nai

robi

Regi

ster

ed: C

ompa

ny li

mite

dby

gua

rant

ee (C

ompa

ny's

Act

), 68

bra

nche

s, 15

00m

embe

rs✔

Prov

isio

n of

serv

ices

in th

e ar

ea o

f ind

ustri

alre

latio

ns, c

onsu

ltanc

y, tr

aini

ng a

nd a

dvoc

acy

Nai

robi

, Kis

umu,

Mom

basa

and

Nak

uru

Regi

ster

ed: T

rade

Uni

ons A

ct,

foun

ded

in 1

959

✔✔

Lab

our

dis

pute

reso

lution,

advo

cac

y

Nai

robi

Hire

d fu

ll-tim

e se

cret

aria

tre

cent

ly. C

urre

ntly

bas

ed in

FKE

Pol

icy

advo

cay

and

Lobb

ying

and

har

mon

isat

ion

of is

sues

rele

vant

for t

he m

embe

rsTh

e m

embe

rs in

clud

eas

sem

bler

s, su

pplie

rs o

f par

ts,

and

impo

rters

/reta

ilers

. The

orga

nisa

tion

is n

ot re

gist

ered

form

ally

.

Pol

icy

advo

cac

yan

dlo

bbyi

ng

Qua

lity

cont

rol a

nd h

arm

onis

atio

n, tr

aini

ngfo

r qua

lity

cont

rol,

polic

y ad

voca

cy,

rese

arch

es a

nd in

form

atio

n sh

arin

g,in

fras

truct

ure

deve

lopm

ent f

or fi

shin

g

Nai

robi

and

Kis

umu

MO

U w

ith th

e M

inis

try o

fLi

vest

cok

and

Fish

ery

✔✔

✔✔

Pol

icy

advo

cac

y,re

sear

ch

Kenya

Priva

te S

ecto

rA

llian

ce (

KEPSA

)

Kenya

Ass

ocia

tion

of

Man

ufa

ctu

rers

(KA

M)

Kenya

Cham

ber

ofC

omm

erc

e a

nd

Indust

ries

Federa

tion

of Kenya

nEm

plo

yers

(FKE)

Environment

Kenya

Busi

ness

Council

Ken

ya M

otor

Indust

ryA

ssoc

iation

(KM

I)

Kenya

Fis

h E

xpor

ters

and

Pro

cess

ors

Ass

ocia

tion

MA

PSK

ID

Ann

ex 2

Li

st o

f Sup

porti

ng O

rgan

isat

ions

2-

4

Serv

ices

Locat

ion

Note

Mar

ketin

g

Mar

ket a

ndbu

sines

sin

form

atio

n Human Re

sour

ce

Deve

lopm

ent In

frast

ruct

ur e

R&D

TECH In

form

atio

n

Fina

nce

Man

agem

ent

Adviso

ry

Admin Su

ppor

t

Oth

er serv

ices

Nam

e o

f Support

ing

Inst

itut

ion

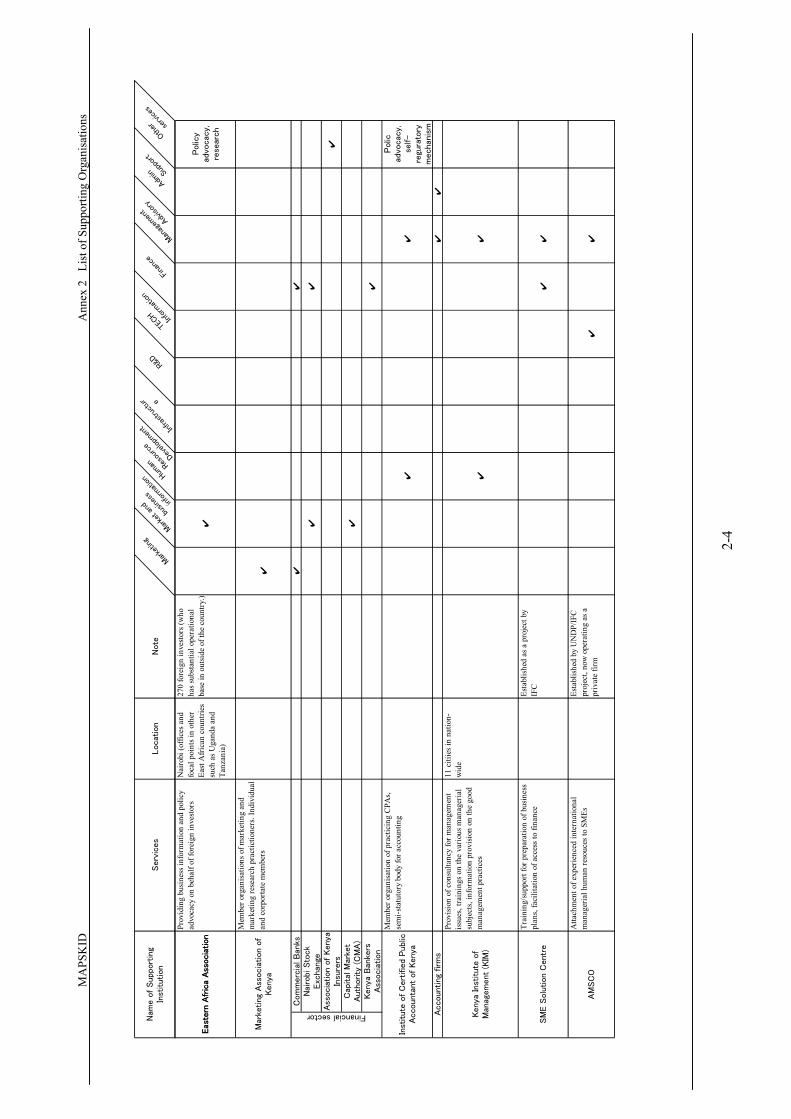

Eas

tern

Afr

ica

Ass

ocia

tion

Prov

idin

g bu

sine

ss in

form

atio

n an

d po

licy

advo

cacy

on

beha

lf of

fore

ign

inve

stor

sN

airo

bi (o

ffice

s and

foca

l poi

nts i

n ot

her

East

Afr

ican

cou

ntrie

ssu

ch a

s Uga

nda

and

Tanz

ania

)

270

fore

ign

inve

stor

s (w

hoha

s sub

stan

tial o

pera

tiona

lba

se in

out

side

of t

he c

ount

ry.)

✔P

olic

yad

vocac

y,re

sear

ch

Mem

ber o

rgan

isat

ions

of m

arke

ting

and

mar

ketin

g re

sear

ch p

ract

ictio

ners

. Ind

ivid

ual

and

corp

orta

te m

embe

rs✔

Com

merc

ial B

anks

✔✔

Nai

robi Sto

ck

Exc

han

ge✔

✔

Ass

ocia

tion o

f Kenya

Insu

rers

✔

Cap

ital

Mar

ket

Auth

ority

(C

MA

)✔

Kenya

Ban

kers

Ass

ocia

tion

✔

Mem

ber o

rgan

isat

ion

of p

ract

icin

g C

PAs,

sem

i-sta

tuto

ry b

ody

for a

ccou

ntin

g✔

✔

Polic

advo

cac

y,se

lf-

regu

rato

rym

echan

ism

✔✔

Prov

isio

n of

con

sulta

ncy

for m

anag

emen

tis

sues

, tra

inin

gs o

n th

e va

rious

man

ager

ial

subj

ects

, inf

orm

atio

n pr

ovis

ion

on th

e go

odm

anag

emen

t pra

ctic

es

11 c

itiie

s in

natio

n-w

ide

✔✔

Trai

ning

/sup

port

for p

repa

ratio

n of

bus

ines

spl

ans,

faci

litat

ion

of a

cces

s to

finan

ceEs

tabl

ishe

d as

a p

roje

ct b

yIF

C✔

✔

Atta

chm

ent o

f exp

erie

nced

inte

rnat

iona

lm

anag

eria

l hum

an re

souc

es to

SM

EsEs

tabl

ishe

d by

UN

DP/

IFC

proj

ect,

now

ope

ratin

g as

apr

ivat

e fir

m✔

✔

SM

E S

olu

tion C

entr

e

AM

SC

O

Inst

itute

of C

ert

ifie

d Publ

icA

ccounta

nt

of

Kenya

Mar

keting

Ass

ocia

tion o

fKenya

Kenya

Inst

itute

of

Man

agem

ent

(KIM

)

Accounting

firm

s

Eas

tern

Afr

ica

Ass

ocia

tion

Financial sector

Annex 3 Questionnaire for the Cluster Analysis

MAPSKID Annex 3 Questionnaire for the Cluster Analysis

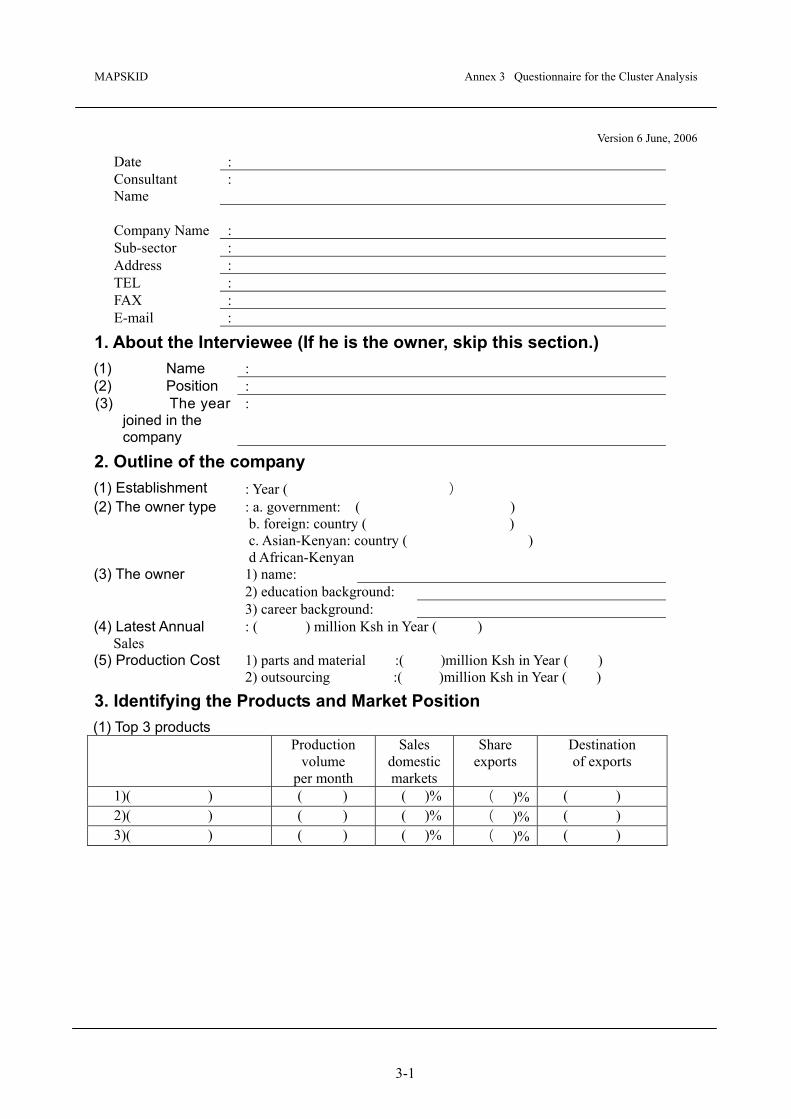

3-1

Version 6 June, 2006

Date : Consultant Name

:

Company Name : Sub-sector : Address : TEL : FAX : E-mail :

1. About the Interviewee (If he is the owner, skip this section.) (1) Name : (2) Position : (3) The year

joined in the company

:

2. Outline of the company (1) Establishment : Year ( ) (2) The owner type : a. government: ( )

b. foreign: country ( ) c. Asian-Kenyan: country ( ) d African-Kenyan

(3) The owner 1) name: 2) education background: 3) career background:

(4) Latest Annual Sales

: ( ) million Ksh in Year ( )

(5) Production Cost 1) parts and material :( )million Ksh in Year ( ) 2) outsourcing :( )million Ksh in Year ( )

3. Identifying the Products and Market Position (1) Top 3 products

Production volume

per month

Sales domestic markets

Share exports

Destination of exports

1)( ) ( ) ( )% ( )% ( ) 2)( ) ( ) ( )% ( )% ( ) 3)( ) ( ) ( )% ( )% ( )

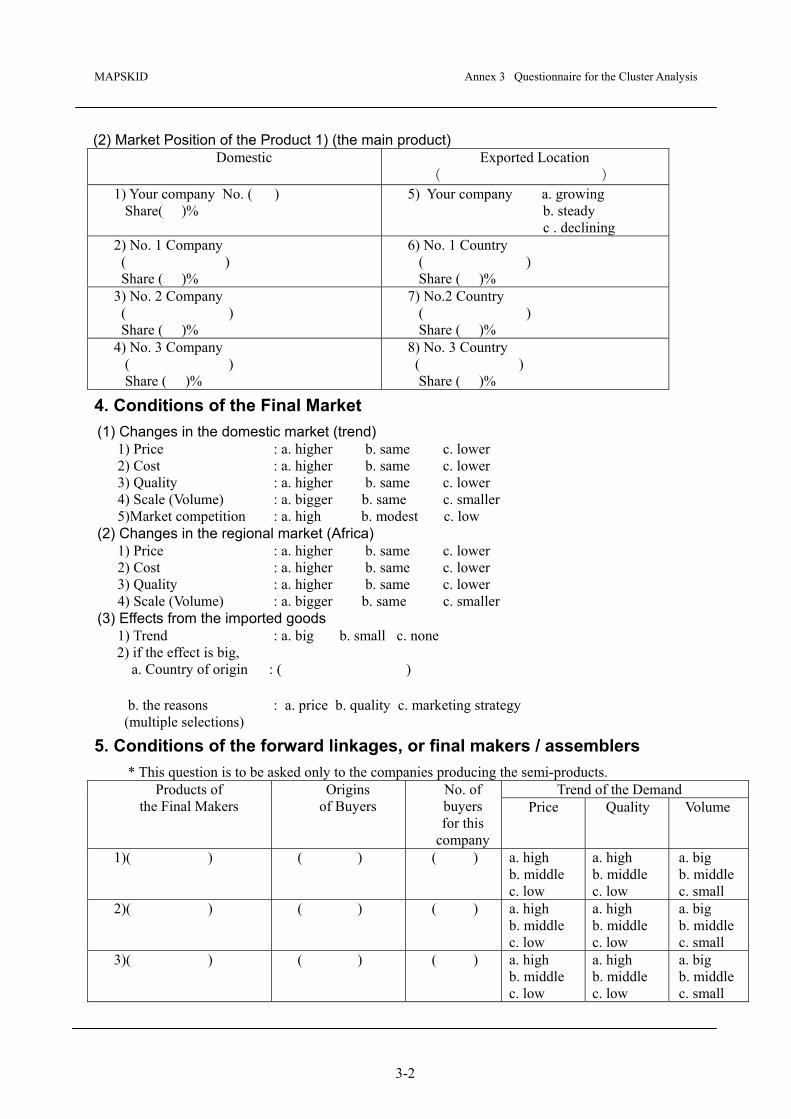

MAPSKID Annex 3 Questionnaire for the Cluster Analysis

3-2

(2) Market Position of the Product 1) (the main product) Domestic

Exported Location

( ) 1) Your company No. ( ) Share( )%

5) Your company a. growing b. steady c . declining

2) No. 1 Company ( ) Share ( )%

6) No. 1 Country ( ) Share ( )%

3) No. 2 Company ( ) Share ( )%

7) No.2 Country ( ) Share ( )%

4) No. 3 Company ( ) Share ( )%

8) No. 3 Country ( ) Share ( )%

4. Conditions of the Final Market (1) Changes in the domestic market (trend)

1) Price : a. higher b. same c. lower 2) Cost : a. higher b. same c. lower 3) Quality : a. higher b. same c. lower 4) Scale (Volume) : a. bigger b. same c. smaller 5)Market competition : a. high b. modest c. low

(2) Changes in the regional market (Africa) 1) Price : a. higher b. same c. lower 2) Cost : a. higher b. same c. lower 3) Quality : a. higher b. same c. lower 4) Scale (Volume) : a. bigger b. same c. smaller

(3) Effects from the imported goods 1) Trend : a. big b. small c. none

2) if the effect is big, a. Country of origin : ( )

b. the reasons (multiple selections)

: a. price b. quality c. marketing strategy

5. Conditions of the forward linkages, or final makers / assemblers * This question is to be asked only to the companies producing the semi-products.

Trend of the Demand Products of the Final Makers

Origins of Buyers

No. of buyers for this

company

Price Quality Volume

1)( ) ( ) ( ) a. high b. middle c. low

a. high b. middle c. low

a. big b. middle c. small

2)( ) ( ) ( ) a. high b. middle c. low

a. high b. middle c. low

a. big b. middle c. small

3)( ) ( ) ( ) a. high b. middle c. low

a. high b. middle c. low

a. big b. middle c. small

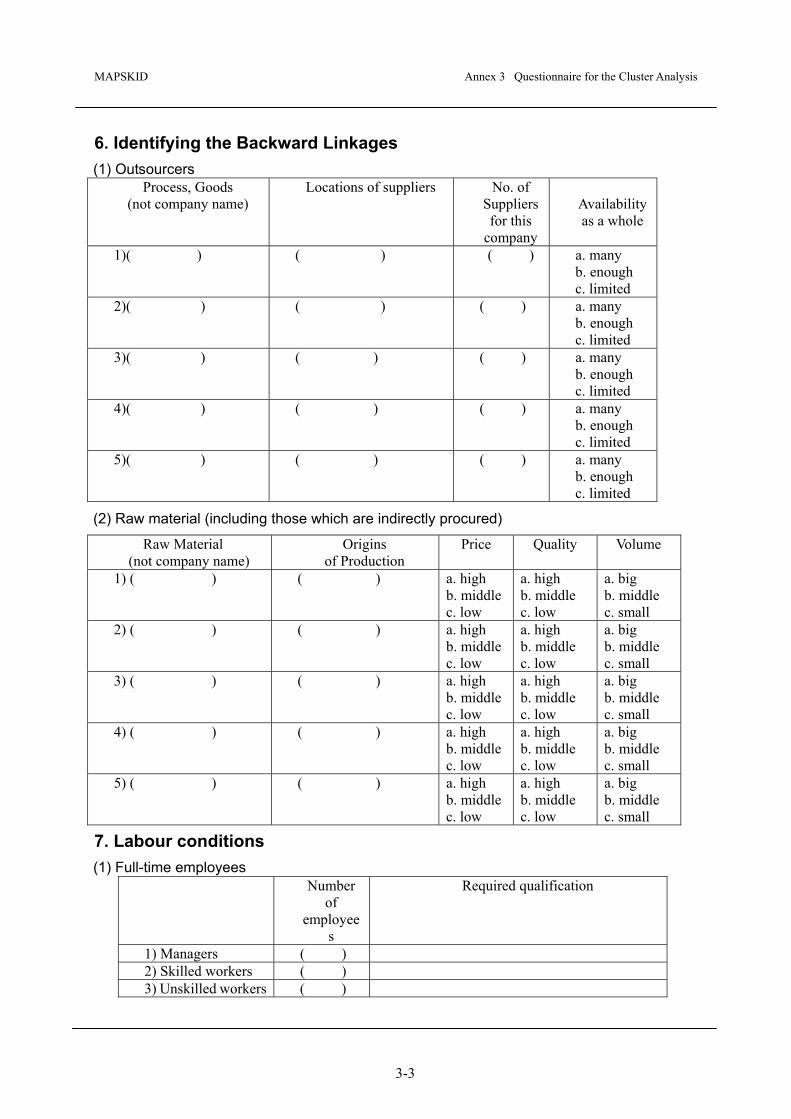

MAPSKID Annex 3 Questionnaire for the Cluster Analysis

3-3

6. Identifying the Backward Linkages (1) Outsourcers

Process, Goods (not company name)

Locations of suppliers No. of Suppliersfor this

company

Availability as a whole

1)( ) ( ) ( ) a. many b. enough c. limited

2)( ) ( ) ( ) a. many b. enough c. limited

3)( ) ( ) ( ) a. many b. enough c. limited

4)( ) ( ) ( ) a. many b. enough c. limited

5)( ) ( ) ( ) a. many b. enough c. limited

(2) Raw material (including those which are indirectly procured)

Raw Material (not company name)

Origins of Production

Price Quality Volume

1) ( ) ( ) a. high b. middlec. low

a. high b. middle c. low

a. big b. middle c. small

2) ( ) ( ) a. high b. middlec. low

a. high b. middle c. low

a. big b. middle c. small

3) ( ) ( ) a. high b. middlec. low

a. high b. middle c. low

a. big b. middle c. small

4) ( ) ( ) a. high b. middlec. low

a. high b. middle c. low

a. big b. middle c. small

5) ( ) ( ) a. high b. middlec. low

a. high b. middle c. low

a. big b. middle c. small

7. Labour conditions (1) Full-time employees

Number of

employees

Required qualification

1) Managers ( ) 2) Skilled workers ( ) 3) Unskilled workers ( )

MAPSKID Annex 3 Questionnaire for the Cluster Analysis

3-4

(2) Part-time employees Number of

employees Average duration of employment

per person per year 1) Skilled workers ( ) ( ) months 2) Unskilled workers ( ) ( ) months

(3) Average salary of full-time employees Full Time Part Time Skilled workers 1) ( ) Ksh/month 2) ( )Ksh/monthUnskilled workers 3) ( ) Ksh/month 4) ( )Ksh/month

8. Productivity Control (Include cost management and delivery management)

(1) Measurement index of productivity

a.Quantity ( ) b.Production speed ( ) c.ProductionCost ( ) d.Others( )

(2) Main method for productivity control

(3) Manual for production control : a. yes b. no

Facility Quantity

( ) ( )

( ) ( )

( ) ( )

( ) ( )

(4) Main production facility

( ) ( )

MAPSKID Annex 3 Questionnaire for the Cluster Analysis

3-5

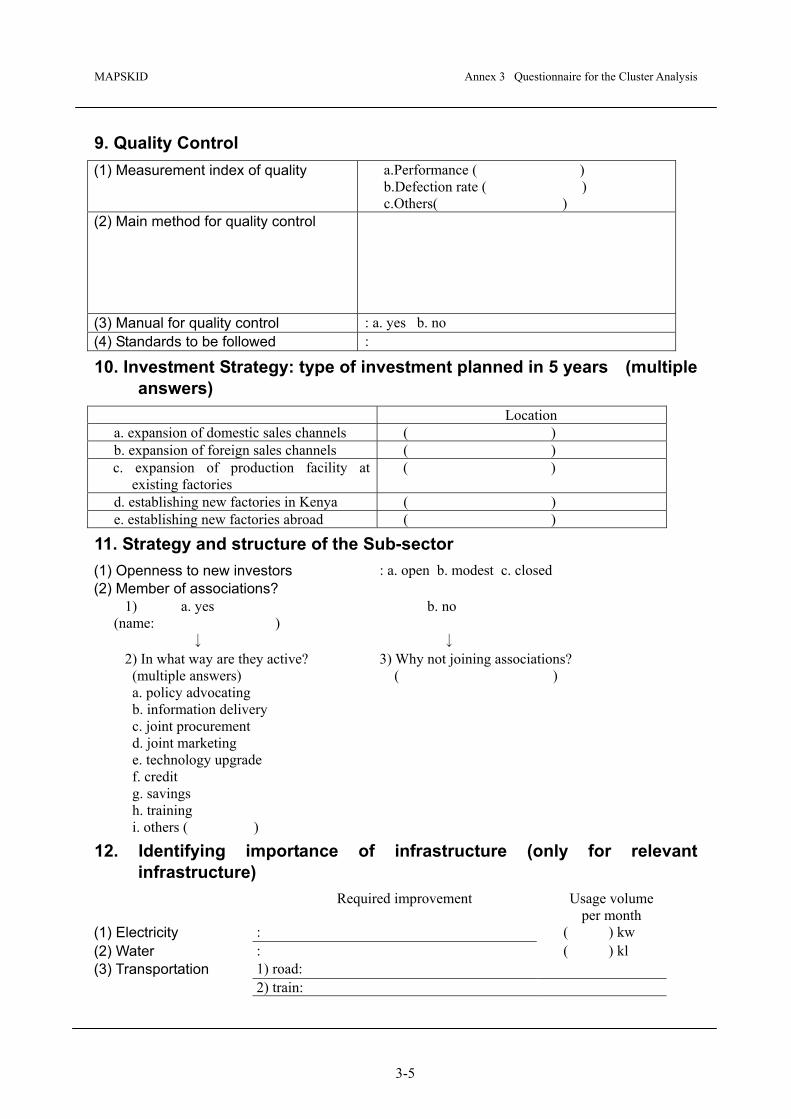

9. Quality Control (1) Measurement index of quality a.Performance ( )

b.Defection rate ( ) c.Others( )

(2) Main method for quality control

(3) Manual for quality control : a. yes b. no (4) Standards to be followed :

10. Investment Strategy: type of investment planned in 5 years (multiple answers)

Location a. expansion of domestic sales channels ( ) b. expansion of foreign sales channels ( ) c. expansion of production facility at

existing factories ( )

d. establishing new factories in Kenya ( ) e. establishing new factories abroad ( )

11. Strategy and structure of the Sub-sector (1) Openness to new investors : a. open b. modest c. closed (2) Member of associations?

1) a. yes (name: ) ↓

b. no ↓

2) In what way are they active? (multiple answers) a. policy advocating b. information delivery c. joint procurement d. joint marketing e. technology upgrade f. credit g. savings h. training i. others ( )

3) Why not joining associations? ( )

12. Identifying importance of infrastructure (only for relevant infrastructure)

Required improvement Usage volume per month

(1) Electricity : ( ) kw (2) Water : ( ) kl (3) Transportation 1) road:

2) train:

MAPSKID Annex 3 Questionnaire for the Cluster Analysis

3-6

3) air: 4) ship: 5) others:

(4)Telecommunication 1) telephone/fax: 2) Internet:

(5)Others ( )

MAPSKID Annex 3 Questionnaire for the Cluster Analysis

3-7

13. BDS Providers (1) What are the major difficulties or obstacles for your company? (multiple answers)

a. ( ) Severe market competition b. ( ) Lack of information for market expansion c. ( ) Lack of information for technological upgrading d. ( ) Obtaining better material/parts/components e. ( ) Keeping quality standards / upgrading productivity f. ( ) Labor issues and quality g. ( ) Cost increase of h. ( ) Tax / administrative system i. ( ) Insufficient infrastructures (Roads, Electricity, Water-supply, etc.) j. ( ) Others ( ) (2) How does your company try to

overcome the problems mentioned above? (multiple answers)

(3) Does your company require any improvement regarding this?

a. ( )

Information gathering by yourself ( )

b. ( )

Utilising consultants ( )

c. ( )

Obtaining loan ( )

d. ( )

Utilising outside training opportunities( )

e. ( )

Participating in exhibitions ( )

f. ( )

Making allies with other enterprises ( )

g. ( )

Utilising the services offered by the public institutions ( )

h. ( )

Utilising the services offered by the private institutions ( )

i. ( )

Others ( )

j. ( )

None→ Reason

14. Any requests to the government and the Study Team for industrial development?

Thank you very much

Annex 4 Related Organisations

MAPSKID Annex 4 Related Organisations

4-1

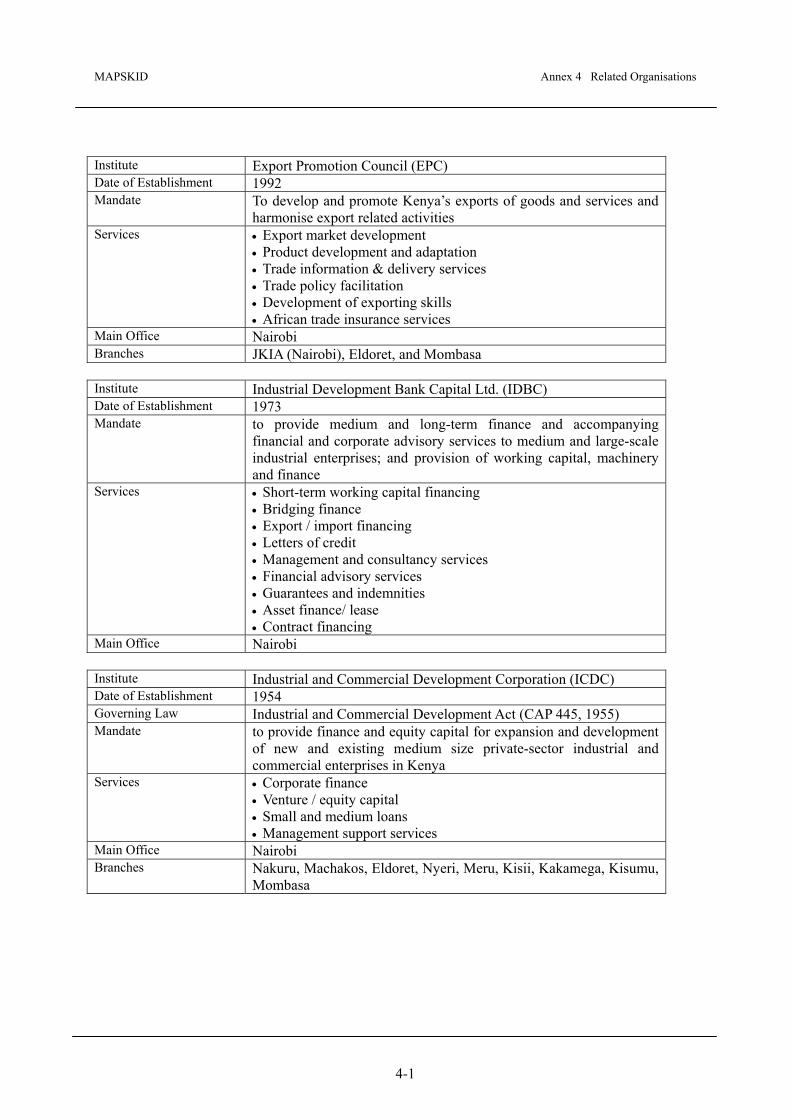

Institute Industrial Development Bank Capital Ltd. (IDBC) Date of Establishment 1973 Mandate to provide medium and long-term finance and accompanying

financial and corporate advisory services to medium and large-scale industrial enterprises; and provision of working capital, machinery and finance

Services • Short-term working capital financing • Bridging finance • Export / import financing • Letters of credit • Management and consultancy services • Financial advisory services • Guarantees and indemnities • Asset finance/ lease • Contract financing

Main Office Nairobi Institute Industrial and Commercial Development Corporation (ICDC) Date of Establishment 1954 Governing Law Industrial and Commercial Development Act (CAP 445, 1955) Mandate to provide finance and equity capital for expansion and development

of new and existing medium size private-sector industrial and commercial enterprises in Kenya

Services • Corporate finance • Venture / equity capital • Small and medium loans • Management support services

Main Office Nairobi Branches Nakuru, Machakos, Eldoret, Nyeri, Meru, Kisii, Kakamega, Kisumu,

Mombasa

Institute Export Promotion Council (EPC) Date of Establishment 1992 Mandate To develop and promote Kenya’s exports of goods and services and

harmonise export related activities Services • Export market development

• Product development and adaptation • Trade information & delivery services • Trade policy facilitation • Development of exporting skills • African trade insurance services

Main Office Nairobi Branches JKIA (Nairobi), Eldoret, and Mombasa

MAPSKID Annex 4 Related Organisations

4-2

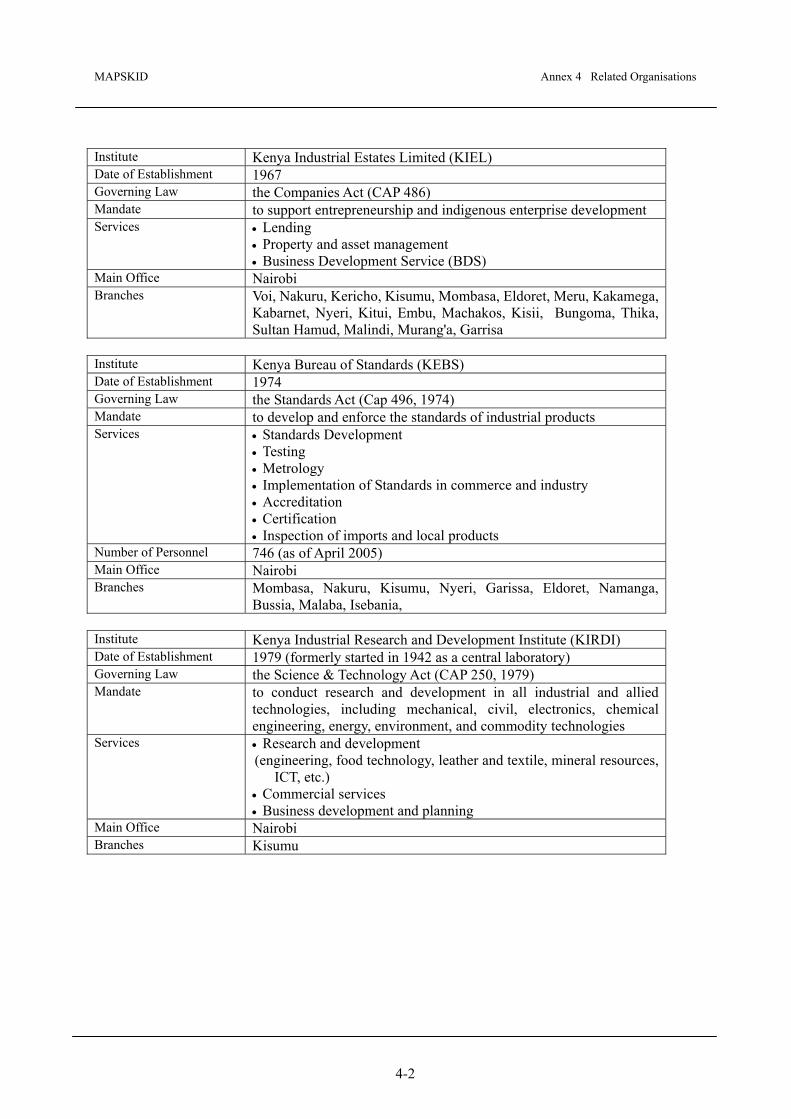

Institute Kenya Industrial Estates Limited (KIEL) Date of Establishment 1967 Governing Law the Companies Act (CAP 486) Mandate to support entrepreneurship and indigenous enterprise development Services • Lending

• Property and asset management • Business Development Service (BDS)

Main Office Nairobi Branches Voi, Nakuru, Kericho, Kisumu, Mombasa, Eldoret, Meru, Kakamega,

Kabarnet, Nyeri, Kitui, Embu, Machakos, Kisii, Bungoma, Thika, Sultan Hamud, Malindi, Murang'a, Garrisa

Institute Kenya Bureau of Standards (KEBS) Date of Establishment 1974 Governing Law the Standards Act (Cap 496, 1974) Mandate to develop and enforce the standards of industrial products Services • Standards Development

• Testing • Metrology • Implementation of Standards in commerce and industry • Accreditation • Certification • Inspection of imports and local products

Number of Personnel 746 (as of April 2005) Main Office Nairobi Branches Mombasa, Nakuru, Kisumu, Nyeri, Garissa, Eldoret, Namanga,

Bussia, Malaba, Isebania, Institute Kenya Industrial Research and Development Institute (KIRDI) Date of Establishment 1979 (formerly started in 1942 as a central laboratory) Governing Law the Science & Technology Act (CAP 250, 1979) Mandate to conduct research and development in all industrial and allied

technologies, including mechanical, civil, electronics, chemical engineering, energy, environment, and commodity technologies

Services • Research and development (engineering, food technology, leather and textile, mineral resources,

ICT, etc.) • Commercial services • Business development and planning

Main Office Nairobi Branches Kisumu

MAPSKID Annex 4 Related Organisations

4-3

Institute Kenya Investment Authority (KenInvest) Date of Establishment 2004 (Transformed from the Investment Promotion Centre,

established in 1986) Governing Law the Investment Promotion Act (No. 6 of 2004) Mandate to promote local and foreign investments in Kenya by providing

information on opportunities, policies, incentives, and procedures Services • Information on investing in Kenya.

• Assistance in the identification of investment opportunities • Identification of joint venture partners. • Appraisal and approval of investment projects • Assistance in timely acquisition of necessary licenses, clearances and permits

Main Office Nairobi Branches Eldoret Institute Numerical Machining Complex Ltd. (NMC) Date of Establishment 1994 (formerly started as a project in 1986) Mandate to manufacture metallic components and other industrial products Services • Manufacturing of mould, die, casting

• Manufacturing of metallic components • Training in CAD

Number of Personnel 57 (as of 2006) Main Office Nairobi Institute Kenya Industrial Property Institute (KIPI) Date of Establishment 2002 Governing Law The Industrial Property Act (Chapter 3 of 2001) Mandate to administer Industrial Property Rights (IPR); to provide

technological information and training in IPR; and to promote inventiveness and innovativeness

Services • Administer industrial property rights (i.e. patents, trade marks, utility models, and industrial designs)

• Providing technological information to the public • Provide training on industrial property.

Main Office Nairobi

MAPSKID Annex 4 Related Organisations

4-4

Institute Export Processing Zones Authority (EPZA) Date of Establishment 1990 Governing Law Export Processing Zones Act (CAP 517, 1990) Mandate to catalyse industrial and economic development through investments

in Economic Zones Services (i) Pre-investment services

• Provision of information and legal advice to investors • Granting of appropriate EPZ Enterprise licences, EPZ

Developer/operator Licences • Liaison with other government agencies for the issuance of

additional Licences (ii) Post-investment services • Approval of building plans within public zones and liaising with

local authorities in approving plans in the case of private zones • One stop facilitation of operating investors including customs and

immigration requirements • Industrial relations and dispute resolution for enterprises • Technical services in the area of waste management and

maintenance of acceptable environmental standards within public zones

• Management of public zones • Provision and maintenance of zone infrastructure • Facilitation of linkages between EPZ investors and providers of

goods and services in the domestic territory Main Office Athi River Branches Mombasa Institute Kenya Wine Agencies Ltd. (KWAL) Mandate to produce and distribute wines and spirits in Kenya and beyond Services Manufacturing of wines and spirits Main Office Nairobi Institute East Africa Portland Cement Company (EAPCC) Date of Establishment 1933 Mandate To manufacture and market quality cement and cement products to the

satisfaction of our customers Services Manufacturing of cements Main Office Athi River Institute Kenya National Trading Corporation Ltd. (KNTC) Date of Establishment 1965 Governing Law The State Corporations Act (CAP 466 in 1986) Mandate to distribute essential goods across the country Services Distribution of sugar, rice, wheat, maize, etc. Main Office Nairobi

MAPSKID Annex 4 Related Organisations

4-5

Institute Kenya Institute of Business Training (KIBT) Mandate to provide entrepreneurial development services to MSMEs Services • Training for the craft and diploma courses

• Training in short-term technical courses Number of Personnel 32 Main Office Nairobi Institute Kenya Industrial Training Institute (KITI) Date of Establishment 1965 Mandate To provide industrial and entrepreneurship skill training for

investment and employment creation Services • Training for the craft and diploma courses

• Training in short-term technical courses Number of Personnel 55 Main Office Nakuru

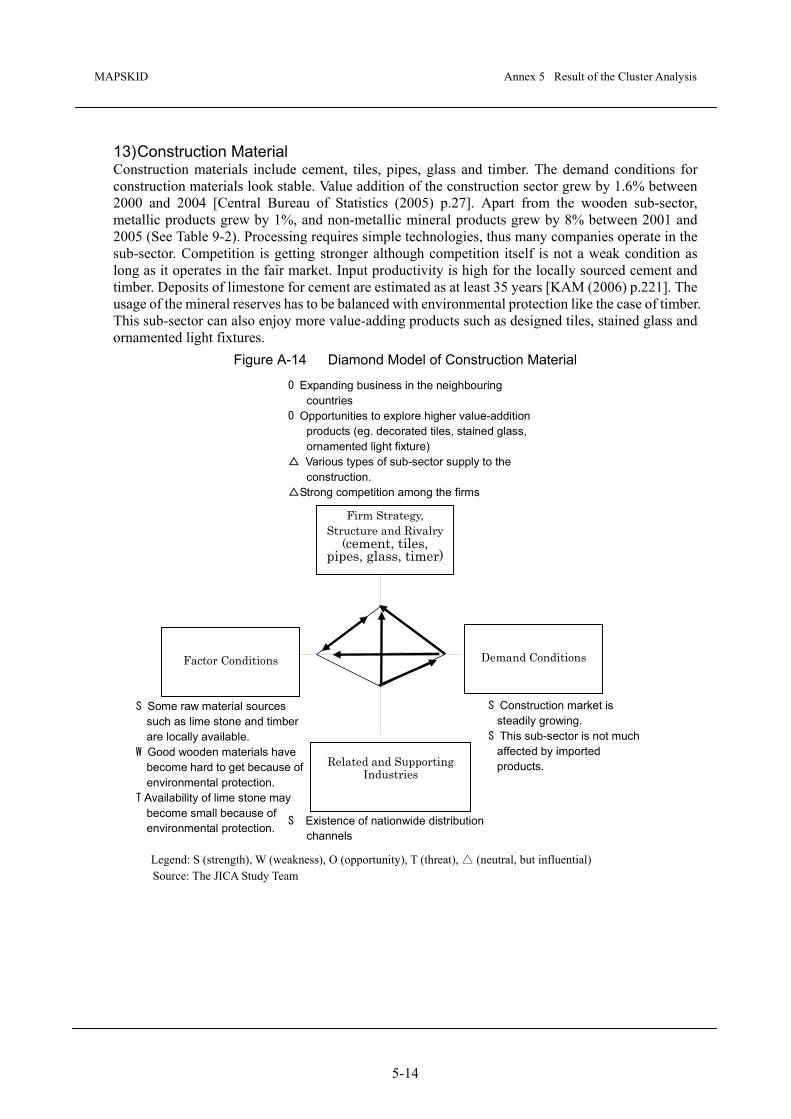

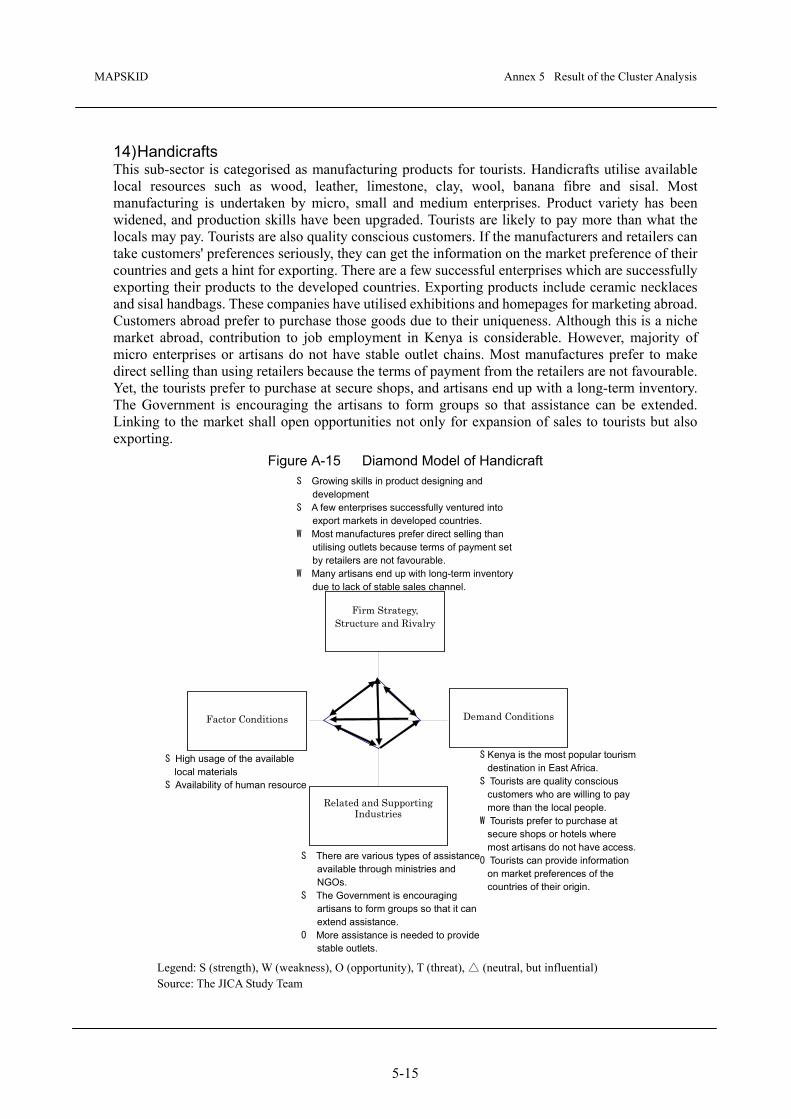

Annex 5 Result of the Cluster Analysis

MAPSKID Annex 5 Result of the Cluster Analysis

5-1

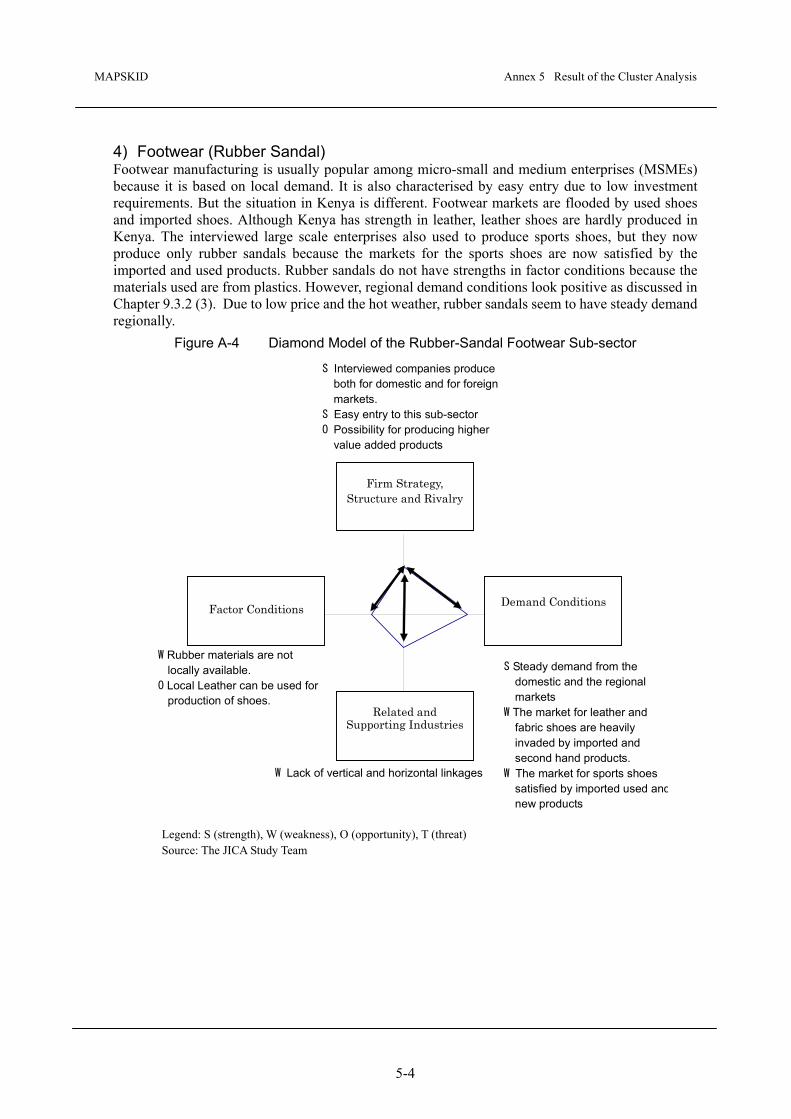

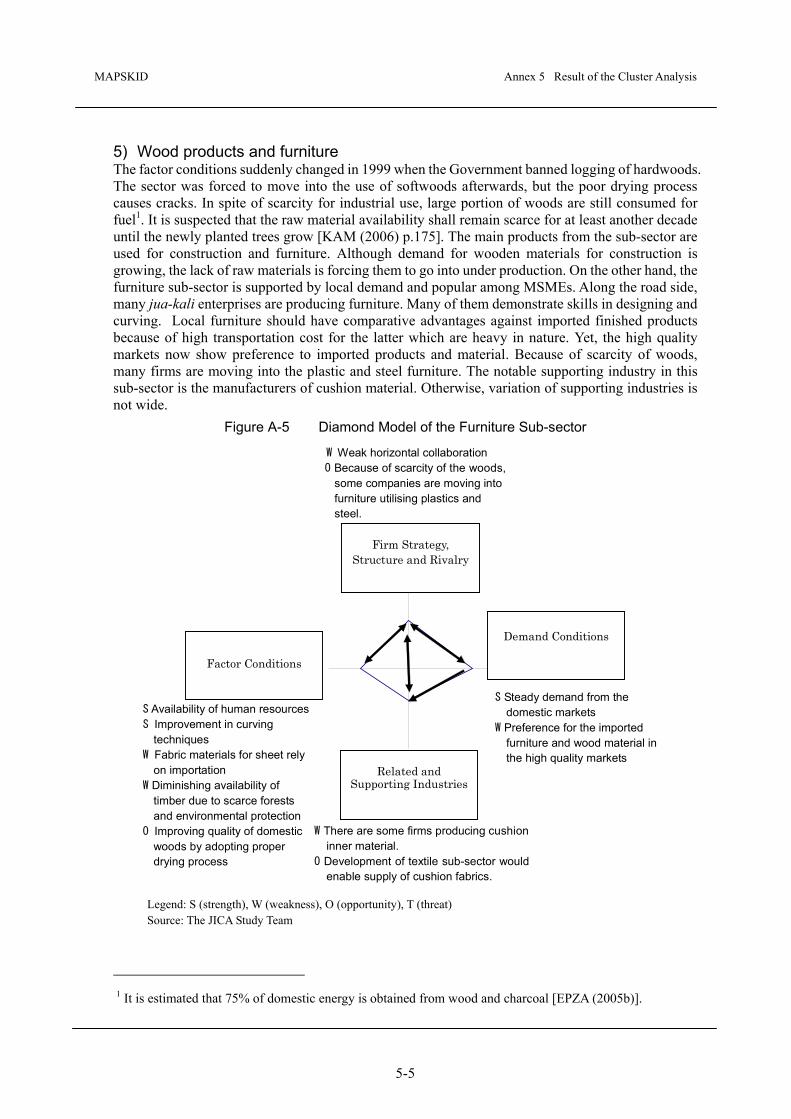

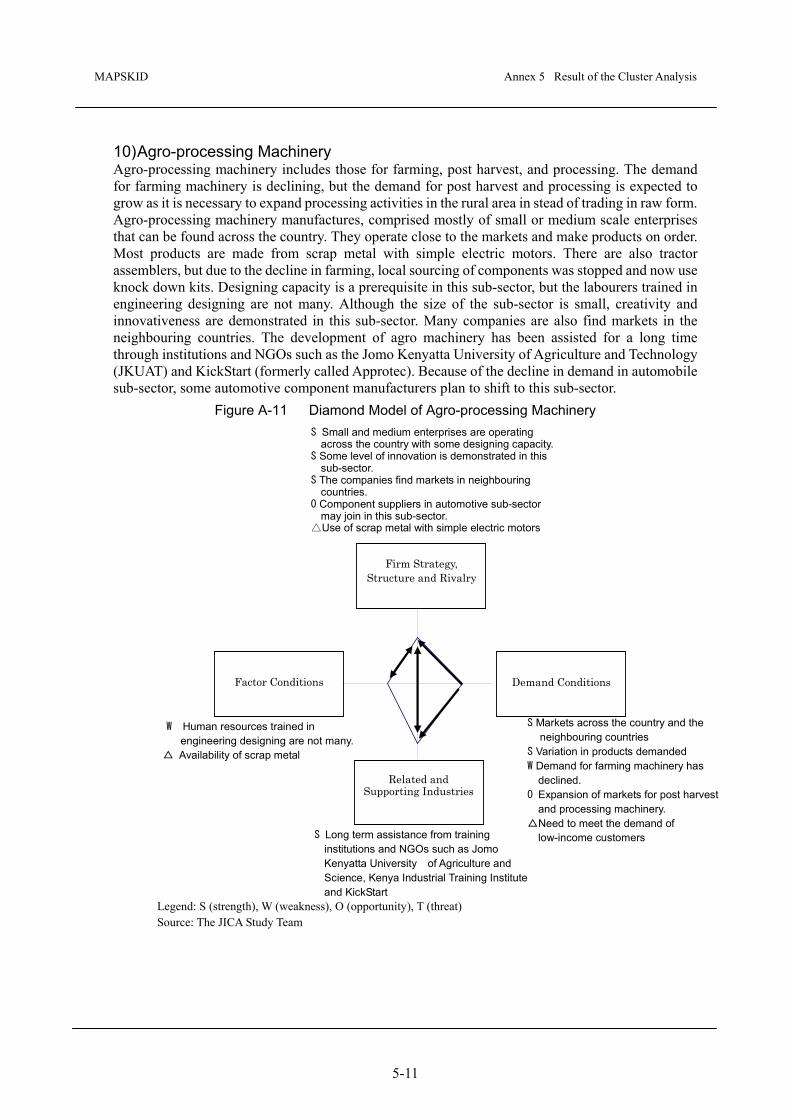

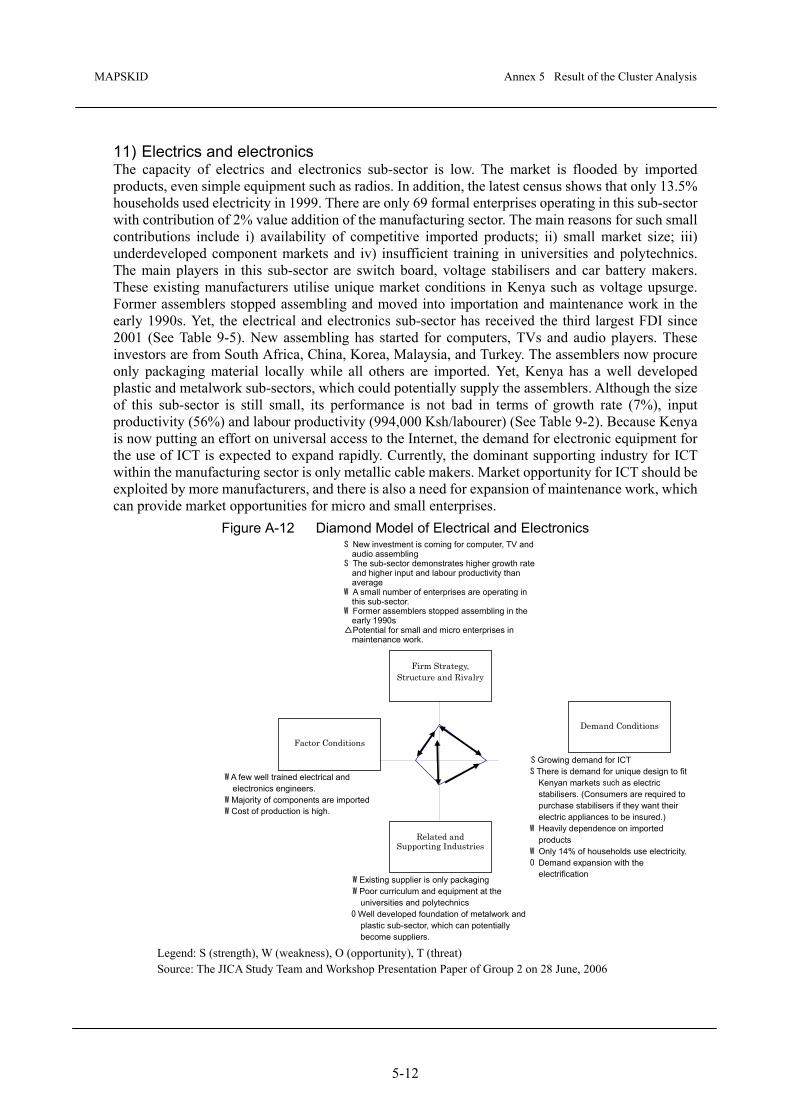

1) Food and beverage This sub-sector is showing the strongest potential in the diamond model analysis because of the favourable status of demand and factor conditions. The domestic demand for food and beverages is steadily growing, and products developed for the domestic market are also exportable to the neighbouring countries. While the domestic market prefers reasonably priced products, some export markets demand high quality products. Some companies undertake production of food and chemical by-products from the same agro-product. A popular example is cooking oil and soap. For such a large size and product diversification in demand, various types of manufacturers can enjoy operating in this sub-sector. Moreover, this sub-sector is most active across the country, utilising local resources. Although not all the visited companies rely on domestic materials, there is much more potential for exploiting domestic agro products. Backed by the growing market, enterprises show positive stance towards investment. Although competition from the imported products is getting severe for canned and bottled foods, which last longer, local enterprises are working in an effort to compete against them in price and quality. Potentialities of this sub-sector can also be observed through the width of supporting industries. Supporting industries among the sample enterprises include paper and plastic containers, bottle case, glue for paper labelling and ink for packaging. These supporting industries are enjoying growing demand conditions of the food processing sub-sector. On the other hand, the weakness of this sub-sector is low institutional collaboration between the farmers and the manufacturers. Supply volumes of raw products are not stable because farmers are switching into more productive income activities. Collaboration between the Ministry of Agriculture and the Ministry of Trade and Industry needs to be strengthened. Moreover, enterprises targeting at the export markets have to follow sanitary requirement such as "Good Manufacturing Practice", which motivates the enterprises to go into some level of automation.

Figure A-1 Diamond Model of the Food and Beverage Sub-sectors

Related and Supporting Industries

(paper and can containers, glue for labels, bottle case

and ink for packaging)

S Growing demand S Wide variation in quality demanded:

domestic demand takes preference to reasonably priced products while the markets abroad have demand for high quality products.