Embed Size (px)

Citation preview

ix

The Merger Control

Review

Law Business Research

Second Edition

Editor

Ilene Knable Gotts

The Merger ConTrol review

second edition

Reproduced with permission from Law Business Research Ltd.

This article was first published in The Merger Control Review,2nd edition (published in November 2011 – editor Ilene Knable Gotts).

For further information please email [email protected]

The Merger Control Review

seCond ediTion

editorilene Knable Gotts

Law Business Research Ltd

PuBLisheR Gideon Roberton

Business deveLoPMenT ManaGeR adam sargent

MaRKeTinG ManaGeRs nick Barette, Katherine Jablonowska

MaRKeTinG assisTanT Robin andrews

ediToRiaL assisTanT Lydia Gerges

PRoduCTion ManaGeR adam Myers

PRoduCTion ediToRs Joanne Morley, davet hyland

suBediToR Caroline Rawson

ediToR-in-Chief Callum Campbell

ManaGinG diReCToR Richard davey

Published in the united Kingdom by Law Business Research Ltd, London

87 Lancaster Road, London, W11 1QQ, uK© 2011 Law Business Research Ltd

© Copyright in individual chapters vests with the contributors no photocopying: copyright licences do not apply.

The information provided in this publication is general and may not apply in a specific situation. Legal advice should always be sought before taking any legal action based on the information provided. The publishers accept no responsibility for any acts

or omissions contained herein. although the information provided is accurate as of november 2011, be advised that this is a developing area.

enquiries concerning reproduction should be sent to Law Business Research, at the address above. enquiries concerning editorial content should be directed

to the Publisher – [email protected]

isBn 978-1-907606-22-9

Printed in Great Britain by encompass Print solutions, derbyshire

Tel: +44 870 897 3239

i

The publisher acknowledges and thanks the following law firms for their learned assistance throughout the preparation of this book:

aCCuRa advoKaTPaRTneRseLsKaB

advoKaTfiRMan CedeRQuisT KB

advoKaTsKo dRuZhesTvo andReev, sToYanov & TseKova in cooperation with sChoenheRR

aLi BudiaRdJo, nuGRoho, ReKsodiPuTRo

aLTius

andeRson MŌRi & ToMoTsune

andReas neoCLeous & Co LLC

BaRneRT eGeRMann iLLiGasCh ReChTsanWäLTe GMBh

BLaKe, CasseLs & GRaYdon LLP

BLaKe daWson

BRedin PRaT

CLiffoRd ChanCe LLP

CoCaLis & PsaRRas

CReeL, GaRCÍa-CuÉLLaR, aiZa Y enRÍQueZ, sC

CuaTReCasas, GonÇaLves PeReiRa

diLLon eusTaCe

edWaRd naThan sonnenBeRGs

eLiG, aTToRneYs-aT-LaW

aCKnoWLedGeMenTs

ii

Acknowledgements

houThoff BuRuMa

KinG & Wood

Lanna PeixoTo advoGados

LCs & PaRTneRs

LuThRa & LuThRa LaW offiCes

MaRvaL, o’faRReLL & MaiRaL

MoRavČeviĆ voJnoviĆ ZdRavKoviĆ in cooperation with sChoenheRR

MoTieKa & audZeviCius

nCTM

PeLifiLiP

PeLLeGRini & uRRuTia aBoGados

RosChieR aTToRneYs LTd

sChoenheRR

sLauGhTeR and MaY

sRs – soCiedade ReBeLo de sousa & advoGados assoCiados, RL

TaveRnieR TsChanZ

WaChTeLL, LiPTon, Rosen & KaTZ

Wda LeGaL, sC

WiesneR & asoCiados aBoGados

WonGPaRTneRshiP LLP

YuLChon, aTToRneYs aT LaW

v

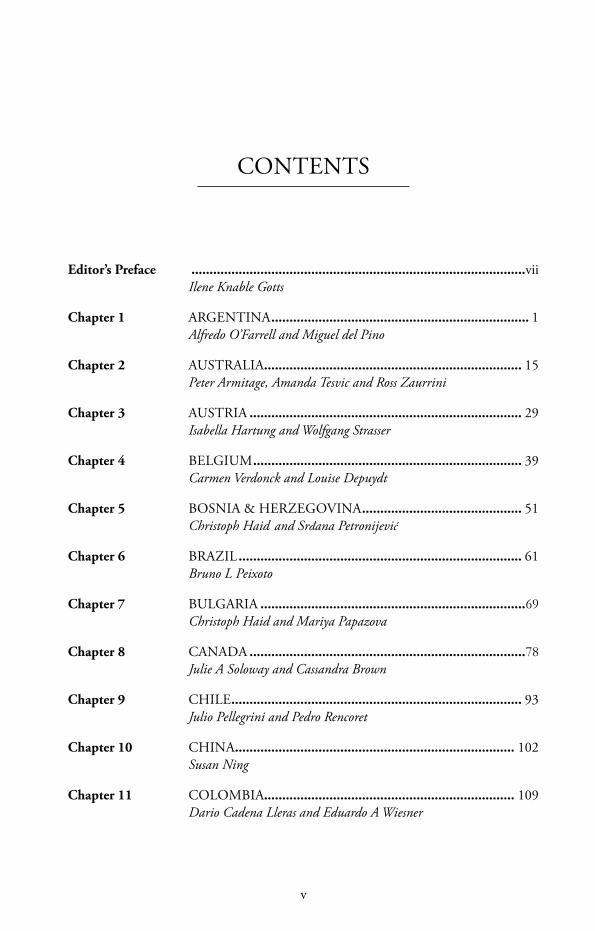

Editor’s Preface ��������������������������������������������������������������������������������������������viiIlene Knable Gotts

Chapter 1 aRGenTina ����������������������������������������������������������������������� 1Alfredo O’Farrell and Miguel del Pino

Chapter 2 ausTRaLia ����������������������������������������������������������������������� 15Peter Armitage, Amanda Tesvic and Ross Zaurrini

Chapter 3 ausTRia ��������������������������������������������������������������������������� 29Isabella Hartung and Wolfgang Strasser

Chapter 4 BeLGiuM �������������������������������������������������������������������������� 39Carmen Verdonck and Louise Depuydt

Chapter 5 Bosnia & heRZeGovina �������������������������������������������� 51Christoph Haid and Srđana Petronijević

Chapter 6 BRaZiL ������������������������������������������������������������������������������ 61Bruno L Peixoto

Chapter 7 BuLGaRia �������������������������������������������������������������������������69Christoph Haid and Mariya Papazova

Chapter 8 Canada ����������������������������������������������������������������������������78Julie A Soloway and Cassandra Brown

Chapter 9 ChiLe �������������������������������������������������������������������������������� 93Julio Pellegrini and Pedro Rencoret

Chapter 10 China ����������������������������������������������������������������������������� 102Susan Ning

Chapter 11 CoLoMBia��������������������������������������������������������������������� 109Dario Cadena Lleras and Eduardo A Wiesner

ConTenTs

vi

Contents

Chapter 12 CRoaTia ������������������������������������������������������������������������� 117Christoph Haid

Chapter 13 CYPRus ��������������������������������������������������������������������������� 125Elias Neocleous and Ramona Livera

Chapter 14 denMaRK ���������������������������������������������������������������������� 135Christina Heiberg-Grevy and Malene Gry-Jensen

Chapter 15 euRoPean union ������������������������������������������������������ 141Tony Reeves and Ashwin van Rooijen

Chapter 16 finLand ������������������������������������������������������������������������ 151Niko Hukkinen

Chapter 17 fRanCe �������������������������������������������������������������������������� 160Hugues Calvet and Olivier Billard

Chapter 18 GeRManY ���������������������������������������������������������������������� 175Marc Besen and Albrecht von Graevenitz

Chapter 19 GReeCe �������������������������������������������������������������������������� 184Alkiviades C A Psarras

Chapter 20 hunGaRY ���������������������������������������������������������������������� 193Christoph Haid and Anna Turi

Chapter 21 india ������������������������������������������������������������������������������ 203Rajiv K Luthra and G R Bhatia

Chapter 22 indonesia �������������������������������������������������������������������� 214Theodoor Bakker & Luky I Walalangi

Chapter 23 iReLand ������������������������������������������������������������������������ 225Lorcan Tiernan and Kate Price

Chapter 24 iTaLY ������������������������������������������������������������������������������� 237Luca Toffoletti and Emilio De Giorgi

Chapter 25 JaPan ������������������������������������������������������������������������������ 247 Yusuke Nakano, Vassili Moussis and Kentaro Hirayama

Chapter 26 KoRea ���������������������������������������������������������������������������� 257Sai Ree Yun, Seuk Joon Lee and Kyoung Yeon Kim

vii

Contents

Chapter 27 LiThuania �������������������������������������������������������������������� 265Giedrius Kolesnikovas, Emil Radzihovsky and Beata Kozubovska

Chapter 28 MexiCo �������������������������������������������������������������������������� 275Luis Gerardo García Santos Coy, José Ruíz López and Mauricio Serralde Rodríguez

Chapter 29 neTheRLands ������������������������������������������������������������� 286Berend Reuder and Weijer VerLoren van Themaat

Chapter 30 PoRTuGaL ��������������������������������������������������������������������� 295Gonçalo Anastácio and Maria João Duarte

Chapter 31 RoMania ����������������������������������������������������������������������� 305Carmen Peli, Carmen Korsinszki and Andra Gunescu

Chapter 32 seRBia ���������������������������������������������������������������������������� 317Christoph Haid and Srđana Petronijević

Chapter 33 sinGaPoRe ������������������������������������������������������������������� 328Ameera Ashraf

Chapter 34 souTh afRiCa ������������������������������������������������������������� 337Lee Mendelsohn

Chapter 35 sPain������������������������������������������������������������������������������� 350Cani Fernández, Andrew Ward and Albert Pereda

Chapter 36 sWeden ������������������������������������������������������������������������� 362Fredrik Lindblom and Amir Mohseni

Chapter 37 sWiTZeRLand �������������������������������������������������������������� 369Silvio Venturi and Pascal G Favre

Chapter 38 TaiWan �������������������������������������������������������������������������� 377Victor Chang, Margaret Huang and Christy Lin

Chapter 39 TuRKeY �������������������������������������������������������������������������� 388Gönenç Gürkaynak and K Korhan Yıldırım

Chapter 40 uKRaine ������������������������������������������������������������������������ 397Christoph Haid and Pavel Grushko

viii

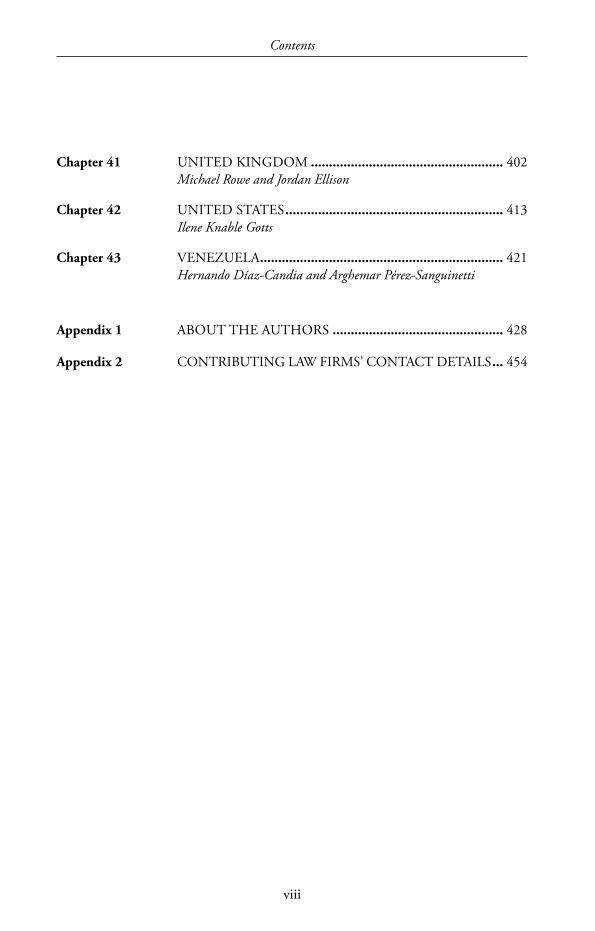

Chapter 41 uniTed KinGdoM ����������������������������������������������������� 402Michael Rowe and Jordan Ellison

Chapter 42 uniTed sTaTes ������������������������������������������������������������ 413Ilene Knable Gotts

Chapter 43 veneZueLa ������������������������������������������������������������������� 421Hernando Díaz-Candia and Arghemar Pérez-Sanguinetti

Appendix 1 aBouT The auThoRs ����������������������������������������������� 428

Appendix 2 ConTRiBuTinG LaW fiRMs’ ConTaCT deTaiLs ��� 454

Contents

ix

editor’s preface

perhaps one of the most successful exports from the United states has been the adoption of mandatory pre-merger competition notification regimes in jurisdictions throughout the world. although adoption of pre-merger notification requirements was initially slow – with a 13-year gap between the enactment of the United states’ Hart-scott-rodino act in 1976 and the adoption of the european community’s merger regulation in 1989 – such laws were implemented at a rapid pace in the 1990s, and many more were adopted and amended during the past decade. china and india have just implemented comprehensive pre-merger review laws, and although their entry into this forum is recent, it is likely that they will become significant constituencies for transaction parties to deal with when trying to close their transactions. indonesia also finally issued the government regulation that was needed to implement the merger control provisions of its antimonopoly Law. This book provides an overview of the process in jurisdictions as well as an indication of recent decisions, strategic considerations and likely upcoming developments in each of these. The intended readership of this book comprises both in-house and outside counsel who may be involved in the competition review of cross-border transactions.

as shown in further detail in the chapters, some common threads in institutional design underlie most of the merger review mandates, although there are some outliers as well as nuances that necessitate careful consideration when advising clients on a particular transaction. almost all jurisdictions either already vest exclusive authority to transactions in one agency or are moving in that direction (e.g., Brazil, france and the UK). The Us and china may end up being the outliers in this regard. Most jurisdictions provide for objective monetary size thresholds (e.g., the turnover of the parties, the size of the transaction) to determine whether a filing is required. Germany also provides for a de minimis exception for transactions occurring in markets with sales of less than €15 million. There are a few jurisdictions, however, that still use ‘market share’ indicia (e.g., colombia, Lithuania, portugal, spain, the United Kingdom). although a few merger notification jurisdictions remain ‘voluntary’ (e.g., australia, singapore, the United Kingdom, Venezuela), the vast majority impose mandatory notification requirements. almost all jurisdictions require that the notification process be concluded prior to completion (e.g., pre-merger, suspensory

Editor’s Preface

x

regimes), rather than permitting the transaction to close as long as notification is made prior to closing. some jurisdictions impose strict time frames by which the parties must file their notification. for instance, cyprus requires filing within one week of signing of the relevant documents and agreements; Brazil requires that the notification be made within 15 business days of execution of the agreements; and Hungary and romania have a 30-calendar-day time limit from entering into the agreement for filing the notification. Many jurisdictions have the ability to impose significant fines for failure to notify (e.g., the Netherlands, spain and turkey). some jurisdictions that mandate filings within specified periods after execution of the agreement also have the authority to impose fines for ‘late’ notifications (e.g., Bosnia and Herzegovina, serbia) for mandatory pre-merger review by federal antitrust authorities. Very little has changed in the Us process in the three decades since its implementation, but some aspects of the Us process have been adopted by other jurisdictions. for instance, canada has recently transformed its procedure to resemble the Us style of review, with a simplified initial filing, a 30-day period to issue a detailed information request and the waiting period tolled until the parties comply with the request. Germany and canada have adopted a procedure, similar to the Us, under which parties can ‘reset the clock’ by withdrawing and refiling the notification. offers to resolve competitive concerns are only considered by the Us after the more detailed investigation has been carried out. The Us, canadian and (although in other respects following the eU model) swedish authorities must go to court to block a transaction’s completion. Both jurisdictions can seek to challenge a completed merger, even if that transaction has already been reviewed pre-merger by the relevant authority, although in canada, such challenges must be brought within one year of closing, while in the Us there is no statute of limitations.

Most jurisdictions more closely resemble the european Union model. in these jurisdictions, pre-filing consultations are more common, parties can offer undertakings during the initial stage to resolve competitive concerns, and there is a set period during the second phase for providing additional information and the agency reaching a decision. in Japan, however, the Jftc announced in June 2011 that it would abolish the prior consultation procedure option. When combined with the inability to ‘stop the clock’ on the review periods, counsel may find it more challenging in transactions involving multiple filings to avoid the potential for the entry of conflicting remedies or even a prohibition decision at the end of a Jftc review.

The permissible role of third parties also varies across jurisdictions. in some jurisdictions (e.g., Japan) there is no explicit right of intervention by third parties, but the authorities can choose to allow it on a case-by-case basis. in contrast, in south africa, registered trade unions or representatives of employees are even to be provided with a redacted copy of the merger notification and have the right to participate in tribunal merger hearings and the tribunal will typically permit other third parties to participate. Bulgaria has announced a process by which transaction parties even consent to disclosure of their confidential information to third parties. in some jurisdictions (e.g., australia, the eU and Germany), third parties may file an objection against a clearance.

in almost all jurisdictions, once the authority approves the transaction, it cannot later challenge the transaction’s legality. other jurisdictions, such as croatia, are still aligning their threshold criteria and process with the eU model. There remain some jurisdictions even within the eU, however, that differ procedurally from the eU model. for instance, in austria the obligation to file can be triggered if only one of the involved

Editor’s Preface

xi

undertakings has sales in austria as long as both parties satisfy a minimum global turnover and have a sizeable combined turnover in austria.

it is becoming the norm in large cross-border transactions raising competition concerns for the Us, eU and canadian authorities to work closely with one another during the investigative stages, and even in determining remedies, minimising the potential of arriving at diverging outcomes. regional cooperation among some of the newer agencies has also become more common; for example, the argentinian authority has worked with that in Brazil, and Brazil’s cade has worked with chile and with portugal. competition authorities in Bosnia and Herzegovina, Bulgaria, croatia, Macedonia, serbia, Montenegro and slovenia similarly maintain close ties and cooperate on transactions. in transactions not requiring filings in multiple eU jurisdictions, Member states often keep each other informed during the course of an investigation. in addition, transactions not meeting the eU threshold can nevertheless be referred to the commission in appropriate circumstances. in 2009, the Us signed a memorandum of understanding with the russian competition authority to facilitate cooperation; china has ‘consulted’ with the Us and eU on some mergers and entered into a cooperation agreement with the Us authorities in 2011, and the Us has also announced plans to enter into a cooperation agreement with india.

Minority holdings and concern over ‘creeping acquisitions’, in which an industry may consolidate before the agencies become fully aware, seem to be gaining increased attention in many jurisdictions, such as australia. some jurisdictions will consider as reviewable acquisitions in which only 10 per cent interest or less is being acquired (e.g., serbia for certain financial and insurance mergers), although most jurisdictions have somewhat higher thresholds (e.g., Korea sets the threshold at 15 per cent of a public company and otherwise 20 per cent of a target; and russia, at any amount exceeding 20 per cent of the target). Jurisdictions will often require some measure of negative (e.g., veto) control rights, to the extent that it may give rise to de jure or de facto control (e.g., turkey).

Given the ability of most competition agencies with pre-merger notification laws to delay, and even block, a transaction, it is imperative to take each jurisdiction – small or large, new or mature – seriously. china, for instance, in 2009 blocked the coca-cola company’s proposed acquisition of china Huiyuan Juice Group Limited and imposed conditions on four mergers involving non-chinese domiciled firms. in Phonak/ReSound (a merger between a swiss undertaking and a danish undertaking, each with a German subsidiary), the German federal cartel office blocked the merger worldwide even though less than 10 per cent of each of the undertakings was attributable to Germany. Thus, it is critical from the outset for counsel to develop a comprehensive plan to determine how to navigate the jurisdictions requiring notification, even if the companies operate primarily outside some of the jurisdictions. This book should provide a useful starting point in this important aspect of any cross-border transaction being contemplated in the current enforcement environment.

Ilene Knable GottsWachtell, Lipton, rosen & KatzNew YorkNovember 2011

141

Chapter 15

EuropEan unionTony Reeves and Ashwin van Rooijen*

I INTRODUCTION

The European union (then the European Community) introduced its first merger control regime with the adoption in 1989 of the European Community Merger regulation (‘the ECMr’),1 in the context of the creation of a single market. There was a desire to create a central system of merger control at the level of the European Community, permitting the evaluation of the effect of mergers and acquisitions on competition in the single market on the basis of a common substantive test and with common procedures, regardless of the country of origin of the undertakings in question. in 2004, a new merger regulation replacing the 1989 regulation2 introduced procedural changes and a new substantive test of compatibility, with the aim of creating a more flexible and efficient regime. The 2004 European Community Merger regulation was renamed European union Merger regulation (‘the EuMr’) following the entry into force of the Treaty of Lisbon, on 1 December 2009.3

* Tony reeves is a partner and ashwin van rooijen is an associate at Clifford Chance LLp. The authors wish to acknowledge the contribution of Francesca Gizzi, a former associate at the firm, and Simon Baxter, a partner at Skadden, arps, Slate, Meagher & Flom LLp, in the preparation of this chapter.

1 See Council regulation 4064/89 of 21 December 1989 on the control of concentrations between undertakings, official Journal L 395 of 30 December 1989.

2 See Council regulation (EC) no 139/2004 of 20 January 2004 on the control of concentrations between undertakings, official Journal L 24 of 29 January 2004 and implementing Commission regulation (Commission regulation (EC) 802/2004), oJ L 133, 30 april 2004; as amended by Commission regulation (EC) 1033/2008 oJ L 279 of 22 october 2008.

3 The Lisbon Treaty amends both the Treaty on European union (the 1992 Maastricht Treaty) and the EC Treaty (the 1957 Treaty of rome). The EC Treaty has been superseded by the Treaty on the Functioning of the European union (TFEu) and all references to European Community

European Union

142

The EuMr requires that all ‘concentrations’ with an ‘Eu dimension’ must be notified to and approved by the European Commission (‘the Commission’) prior to completion.4

‘Concentrations’ for which notification under the EuMr is required involve lasting ‘changes in control’ resulting from mergers and acquisitions of the whole or parts of an undertaking. acquisitions are broadly defined to include all transfers of assets to which revenues are attributable (including potentially, for example, transfers of ip rights or of customers) as well as the formation and acquisition of control of certain joint ventures qualifying as ‘full-function’ joint ventures. Full-function joint ventures are joint ventures that perform, on a lasting basis, all the functions of an independent economic entity. a joint venture will qualify as full-function if: (1) it has sufficient assets, personnel and financial resources to operate its business activity independently; (2) it is allowed to conduct its own day-to-day commercial operations (subject to its shareholders’ decisive influence over its commercial strategy); (3) there are no substantial purchase or supply arrangements between the parents and the joint venture that would undermine its independent character; and (4) it is of sufficient length to cause it to be considered to bring about a lasting change in the structure of the undertakings concerned.

The concept of ‘change of control’ is very broad. it is sufficient that one party acquires ‘the possibility of exercising decisive influence’ over another company. For this possibility of decisive influence to be considered to have been acquired, a party must have the ability to veto strategic decisions affecting the business policy of the target (in particular, decisions relating to the budget, the business plan, major investments or the appointment of senior management). in contrast, veto rights that are normally accorded to minority shareholders in order to protect their financial interests as investors – such as the power to block changes in the company’s statutes, or to increase and decrease in its capital – are not viewed as conferring decisive influence.

a concentration is deemed to have an Eu dimension if the parties either: a have combined worldwide revenues of more than €5 billion, while each of at least

two of the merging parties realised more than €250 million revenues in the Eu; or

b have combined worldwide revenues of more than €2.5 billion, their combined revenues exceed €100 million in each of at least three Member States and in each of those three Member States, the revenues of each of at least two of the merging parties is more than €25 million; and the union-wide turnover of each of at least

and EC are replaced by European union and Eu. Thus, the ECMr becomes the EuMr and ‘concentrations with a Community dimension’ are ‘concentrations with a European union dimension’.

4 narrow exceptions exist: the EuMr excludes certain acquisitions by credit institutions holding securities on a temporary basis; certain acquisitions in the context of insolvency proceedings; certain acquisitions by financial holding companies; and intra-group restructurings. See article 3(5) EuMr.

European Union

143

two of the merging parties is more than €100 million, unless each of the merging parties obtains more than two-thirds of its Eu turnover in one Member State.5

The revenue taken into account is the revenue derived from the sale of products or the provision of services (excluding turnover taxes) in the preceding financial year, and in principle includes the turnover of the group to which the party belongs, except in the case of an acquired company or asset; revenue generated by a seller (as opposed to the sold business) are generally not taken into account. Certain serially or contemporaneously executed transactions that do not, individually, meet the revenue thresholds may nevertheless be deemed to have an Eu dimension if they are considered to be related.6 Detailed guidance on how the rules determining the Commission’s jurisdiction are to be interpreted and applied are provided in the Commission’s Consolidated Jurisdictional notice.7

Concentrations that do not have an ‘Eu dimension’ as defined by the Merger regulation may be subject to the notification requirements of the 26 out of 27 Eu Member States that have a merger control regime (Luxembourg being the exception). However, the Merger regulation provides for procedures whereby an Eu Member State or, if the transaction would be notifiable in at least three Member States, the parties may request that a concentration that does not have an Eu dimension be examined by the Commission (see below, Section iii).8

II YEAR IN REVIEW

The impact of the economic crisis continues to be reflected in the number of merger notifications to the Commission, with 251 notifications having been made between January and September 2011 – similar to the number of notifications in 2009 and 2010 (259 and 274, respectively) but down from a record 402 in 2007 and 356 in 2006. The Commission carried out six investigations in addition to issuing five phase ii decisions, which is in line with the number of phase ii investigations and decisions in previous years. in 2011, a total of seven merger notifications were withdrawn.

The Commission prohibited the merger between olympic air and aegean airlines – the first prohibition decision since 2007, when the Commission similarly prohibited another airline merger: RyanAir/Air Lingus.9 The Commission noted the likely difficulties in the olympic review early on, drawing parallels to the ryanair prohibition decision. in Olympic/Aegean, airport slots were numerous but competition from other airlines was unlikely to emerge, leaving the parties with a virtual monopoly position on several domestic routes. The Commission also found that ferry services between the Greek islands did not impose a sufficient competitive constraint on air travel services. The Commission

5 article 1 of the EuMr.6 recital 20 of the EuMr.7 Commission Consolidated Jurisdictional notice under Council regulation (EC) no. 139/2004

on the control of concentrations between undertakings, oJ 2008 C 95/01.8 See, respectively, articles 22 and 4(5) EuMr.9 Case no. CoMp/M.5434.

European Union

144

market tested but ultimately rejected three sets of remedies packages offered by the merging parties, including concessions with respect to access to their frequent flyer programmes and landing and take-off slots at athens and other airports. While ryanair resulted in a continuing court saga between the parties, the prohibition of the olympic/aegean merger was followed by an investigation by the Greek competition authority into whether olympic and aegean have colluded unlawfully since the failed merger attempt.

The Commission’s ‘first in’ or ‘priority’ rule saw one if its most striking demonstrations to date in the context of the two merger notifications in the hard disk sector – Western Digital/Hitachi10 and Seagate/Samsung.11 notified only one day ahead of Western Digital/Hitachi, the Seagate/Samsung review benefits from the priority rule at the expense of Western Digital/Hitachi. under the priority rule, the Commission’s review of Seagate/Samsung will disregard the subsequently notified Western Digital/Hitachi deal, yet in its review of Western Digital/Hitachi, the Commission will take into account the effects brought about by the Seagate/Samsung transaction. on 19 october, the Commission cleared the Seagate/Samsung merger unconditionally whereas by that time Western Digital had offered commitments that were still under review at the time of writing. perhaps due to the particularly striking circumstances of these two merger cases – not only were they notified one day apart, but Western Digital had engaged with the Commission informally before Samsung had done so, while the four companies involved in the two mergers together represent a substantial portion of the market for hard disks – commentators have questioned the fairness of a rule that has no formal basis in the EuMr. in the necessarily prospective analysis carried out by the Commission in any merger proceeding, in which the Commission’s investigative powers are designed to enable the Commission to predict the likely development of the competitive landscape as closely as possible, it may seem odd to entirely disregard the effects of another pending merger in the same market that is likely to be concluded shortly. Calls for reconsideration of the priority rule in favour of a parallel review system are unlikely to be answered in the short term, however.12

in two other transactions in the information technology field, namely Intel/McAfee13 – a merger between a manufacturer of computer processors and a developer of security software – and Cisco/Tandberg,14 which concerned a merger between two manufacturers of a variety of video conferencing products, the Commission accepted commitments aimed at facilitating interoperability with the merging parties’ products in the course of a phase i investigation. in response to concerns that the merger would result in reduced interoperability with the merging entity’s products by competitors, Cisco committed to transferring its intellectual property rights in the Tip protocol, necessary for interoperability with its video conferencing solutions, to a separate industry

10 Case no. CoMp/M.6203.11 Case no. CoMp/M.6214.12 Western Digital is understood to have appealed application of the priority rule in Western

Digital/Hitachi.13 Case no. CoMp/M.5984.14 Case no. CoMp/M.5669.

European Union

145

body, which would license the protocol to interested parties on fair, reasonable and non-discriminatory terms. in addition, Cisco committed to continuing to implement the Tip protocol and future versions thereof, as licensed by the independent industry body, in its own products. Hailed by Commission officials as a ‘model remedy’ in information technology, the commitments in Cisco/Tandberg can best be described as a combination of behavioural and structural remedies. on the one hand, the remedy package is structural in that intellectual property rights in a critical protocol for interoperability are in effect divested, thereby removing Cisco’s unilateral control over the protocol. Equally important, however, is the behavioural component of these commitments: notwithstanding divestment of the protocol to an independent industry body, availability of the Tip protocol would be useless if Cisco did not itself commit to continuing to implement it.

in January 2011, the Commission cleared the Intel/McAfee merger, a transaction of some significance in the information technology industry, after the parties had offered commitments aimed at ensuring interoperability between intel’s chipsets and rival security software products. rival security software developers were particularly concerned that close ‘hardware’ integration of intel’s chipsets with Mcafee’s security software would present an insurmountable advantage to competitors. in response to these concerns, the parties committed to providing interoperability information well ahead of the launch of new chipsets, allowing rivals sufficient time to adapt their security software products accordingly.

The effect of interoperability on competition often requires a complex analysis – as evidenced, for example, by the Commission’s 2004 Microsoft decision, which may be difficult to assess conclusively within the time constraints of a phase i investigation (see Section iii, infra). indeed, commentators have noted that in both Intel/McAfee and Cisco/Tandberg, it is conceivable that a phase ii investigation would have revealed that interoperability commitments were not in fact necessary.

III THE MERGER CONTROL REGIME

Qualifying transactions with an ‘Eu dimension’ under the EuMr (see above) must be notified – on the Form Co, as set out in the implementing regulation 802/200415 – to the Commission’s Directorate-General for Competition (‘DG Competition’) prior to their implementation and following the conclusion of the agreement, the announcement of a public bid or the acquisition of a controlling interest. notification may also be made where the undertakings demonstrate to the Commission a good faith intention to conclude an agreement (e.g., based on the existence of a draft agreement) or have publicly announced an intention to make a bid.

undertakings that fail to obtain Commission clearance before implementing their transaction in violation of the EuMr face fines of up to 10 per cent of the aggregate

15 See annex 1 of implementing Commission regulation (Commission regulation (EC) 802/2004), oJ L 133, 30.4.2004, available at http://eur-lex.europa.eu/LexuriServ/LexuriServ.do?uri=CELEX:32004r0802:En:noT.

European Union

146

worldwide turnover of the companies concerned, and penalty payments of up to 5 per cent of aggregate daily turnover of the companies concerned for each working day of the infringement, regardless of whether clearance is ultimately granted.

DG Competition conducts the review in two phases. The vast majority of transactions are cleared after phase i.

in phase i, the Commission has 25 working days from the day following its receipt of the notification in which to make its initial assessment. This period may be extended if remedies are offered (see below) or if a Member State requests that the transaction be referred to it.

at the end of the phase i, the Commission may decide that the transaction falls outside the scope of the EuMr; raises no serious doubts as to its compatibility with the internal market, (possibly after the parties have offered remedies – see below); or raises serious doubts as to its compatibility with the internal market and that proceedings should be initiated (resulting in the opening of a phase ii investigation).

in phase ii, the Commission has an additional 90 working days from the day following its phase i decision, in which to approve or prohibit the transaction. This period may be extended to 105 working days when the parties concerned offer, within 55 working days of the Commission’s decision to take the review to phase ii, commitments designed to render the concentration compatible with the internal market. The period may also be extended by 15 working days at the request of the parties, if that request is received within 15 working days after the Commission’s decision to initiate a phase ii review, or at any time during the review process, with the agreement of the Commission. This extension may, however, only occur once and extensions of phase ii may not exceed 20 working days in total.

The Commission must make a decision within binding time limits. if it fails to do so the concentration is deemed to be cleared. These time limits may be extended by the Commission if the parties submit an incomplete or incorrect notification or if DG Competition has to request further information by decision or order an inspection by decision.

immediately following the notification of a concentration or the opening of a phase ii investigation, the Commission publishes a notice in the official Journal of the European union, inviting third parties (customers and suppliers as well as competitors) to comment on the transaction (normally within 10 to 15 days). in addition, DG Competition customarily requests that third parties answer specific questions in the course of the investigation. Third parties may also voluntarily submit comments to DG Competition at any stage of the proceedings and may apply to be heard by DG Competition officials. in phase ii investigations, third parties who have an interest in the case may be granted access to DG Competition’s (non-confidential) files. it is important, therefore, that business secrets are clearly marked as such when notifications and any subsequent documents (e.g., draft undertakings) are submitted.

The Commission must determine whether a concentration is ‘compatible with the common market’. The Commission will assess a concentration by reference to the relevant product market or markets and the relevant geographic market or markets affected by

European Union

147

it.16 a transaction must be prohibited if it significantly impedes effective competition in the internal market, in particular as a result of the creation or strengthening of a dominant position (‘the SiEC test’).17 The test is intended to deal both with situations in which the merged firm may be dominant and with oligopolistic markets in which the merger may impede competition despite the merged entity’s market share falling below the dominance threshold.

Full function joint ventures are subject to a double substantive test: in addition to the SiEC test, the issue of whether the joint venture has as its object or effect the coordination of the competitive behaviour of its parents and whether, if so, the joint venture would generate countervailing efficiencies or promote technical progress and benefit consumers will be assessed under article 101 of the TFEu.

In assessing whether a transaction significantly impedes effective competition, the Commission will examine: whether the merger will eliminate competitive constraints on firms in the market, thus increasing their market power, without them having to resort to coordinating their behaviour (‘non-coordinated’ or ‘unilateral’ effects); and whether the merger will change the nature of competition in the market so that firms that were previously not coordinating their behaviour may now be significantly more likely to do so on a tacit basis, thus raising prices or otherwise harming competition (‘coordinated effects’).

a simplified procedure exists for the notification of transactions that clearly raise no substantive issues. in these cases, information only needs to be provided for certain sections of the Form Co. The Commission will issue a short-form decision within one month from the date of notification. The simplified procedure will apply to: (1) joint ventures with no, or minimal, actual or foreseen activities within the territory of the European Economic area (‘EEa’), (i.e., the turnover in the EEa of the joint venture or the contributed activities or both is less than €100 million in the EEa territory and the total value of assets transferred to the joint venture in the EEa is less than €100 million); (2) mergers or acquisitions of sole or joint control, provided that none of the parties to the concentration are engaged in business activities in the same product and geographical market, or in a product market that is upstream or downstream of a product market in which any other party to the concentration is engaged; and (3) mergers or acquisitions of sole or joint control where two or more of the parties are engaged in the same product and geographical market (horizontal relationships) but their combined market share is less than 15 per cent or where one or more of the parties are engaged in business activities in a product market that is upstream or downstream of a product market in which any other party is engaged (vertical relationships), provided that their individual or combined market share is not 25 per cent or more.

parties may offer remedies to meet specific competition objections and thereby obtain clearance of the transaction. remedies can be given in the first phase so as to avoid a second-phase investigation, or during the second phase. if remedies are offered in phase

16 See Commission notice on the definition of the relevant market for the purposes of Community competition law, official Journal C 372 of 9 December 1997.

17 a significant impediment to effective competition being maintained.

European Union

148

i, it is extended from 25 to 35 working days (to give DG Competition time to seek third party comments on the proposed undertakings). if remedies are offered in phase ii, it is extended from 90 to 105 working days, unless they are offered within 55 working days after the initiation of proceedings. as noted above, the Commission strongly favours structural over behavioural remedies. The Commission’s remedies notice sets out guidance on substantive and procedural considerations.18

under the EuMr the Commission has broad powers to investigate19 and to impose fines on persons or undertakings committing procedural or substantive infringements.20

The Commission may revoke a clearance decision where it is based on incorrect information for which one of the undertakings is responsible, where it has been obtained by deceit, or where the undertakings concerned commit a breach of an obligation attached to the decision.

Commission decisions can be appealed to the General Court on both procedural and substantive grounds. a further appeal on issues of law can be made to the Court of Justice of the European union.

IV OTHER STRATEGIC CONSIDERATIONS

The parties are strongly encouraged to contact DG Competition prior to submitting a formal notification. DG Competition has in the past been very cooperative in providing confidential guidance to parties in informal pre-notification contact. Such contact may be instrumental in avoiding a second-phase investigation, particularly if difficult issues are involved, as it effectively gives the Commission more time to examine the case. The

18 See Commission notice on remedies, official Journal C 267 of 22 october 2008.19 The Commission can request the provision of information, either by simple request or by

decision; it can conduct inspections of business premises during the course of which it can examine books and records, take copies, seal premises or books and records, and ask for explanations on facts or documents; and it can interview natural or legal persons who consent to be interviewed, to collect information relating to an investigation.

20 Fines not exceeding 1 per cent of the aggregate worldwide turnover of the undertaking concerned may be imposed where a person or undertaking, intentionally or negligently: supplies incorrect or misleading information in a notification; supplies incorrect information in response to a formal request by the Commission or fails to supply information in time; refuses or fails to supply complete information during investigations by the authorities of the Member States or the Commission; or breaks seals affixed by the Commission during its investigation. The Commission may impose fines of up to 10 per cent of the aggregate worldwide turnover of the undertakings concerned where the undertaking, intentionally or negligently: fails to notify a concentration in accordance with the EuMr prior to its implementation; puts a concentration into effect before expiry of the suspension period; puts a concentration into effect in breach of a prohibition decision or fails to comply with measures ordered following a prohibition decision; or fails to comply with an obligation attached to a Commission clearance decision or to a decision granting a derogation from the suspension period.

European Union

149

Commission has published guidance on this type of informal contact in its Best practices on the Conduct of EC Merger Control proceedings.

in addition, parties may ask for an exemption from some of the information requests in the notification during informal pre-notification contacts with DG Competition. The drafting will be considerably reduced where there are no major overlapping activities between the parties (less than 15 per cent combined market share) and where neither of them, individually, has a market share of 25 per cent or more in any relevant market in the Eu.

in advance of notifying the Commission, the parties may request that the Commission refer a concentration with an Eu dimension to be examined, in whole or in part, by a national competition authority (‘nCa’) on the basis that it may significantly affect competition in a distinct market within that Member State (article 4(4) EuMr). This will enable the parties to ensure that the transaction is investigated by the ‘best-placed’ authority; however, it does require the parties to highlight potential competition concerns in relevant national markets. The Commission must transmit this request to all Member States and the relevant Member State must express its agreement or disagreement within 15 working days of receipt of the request. provided that the Member State does not disagree; and the Commission agrees with the parties that competition might indeed be significantly affected in a distinct national market, the Commission may, within 25 working days of receipt of the request, refer the whole or part of the case to the relevant nCa, with a view to the application of that state’s national competition law.

in addition, the Commission may refer a notified concentration, in whole or in part, to the competent authorities of a Member State, at the request of the Member State concerned, in two circumstances:21 first, the Commission has a discretion as to whether to make such a referral when the concentration threatens to affect significantly competition in a distinct market within that Member State. Second, where a concentration affects competition within the requesting Member State in a distinct market that does not form a substantial part of the internal market, the Commission has no discretion but must refer the whole or part of the case relating to the distinct market concerned.

The parties to a concentration that has no Eu dimension, but is capable of being reviewed under the national competition laws of at least three Member States, may request the Commission to examine the concentration instead (article 4(5) EuMr). The request must be made before any notification to an nCa. The Commission must transmit the request to all Member States and any state competent to examine the concentration may, within 15 working days of receipt of the request, express its disagreement. if at least one Member State disagrees, the case will not be referred to the Commission. if no Member State disagrees the concentration is deemed to have a Eu dimension and must be notified in accordance with the EuMr.22

21 See article 9 of EuMr.22 See Form rS (Form for pre-notification referral requests) relating to the notification of a

concentration pursuant to Council regulation (EC) no. 139/2004 (annex to Commission regulation 802/2004, as amended by Commission regulation 1033/2008).

European Union

150

Finally, one or more Member States may request that a concentration having no Eu dimension is referred to the Commission for consideration under the EuMr, if it affects trade between Member States and threatens to significantly affect competition within the requesting Member States.23

V OUTLOOK AND CONCLUSIONS

in March 2011, Commissioner almunia announced that DG Competition would look into the potential ‘enforcement gap’ with respect to acquisitions of minority shareholdings. This assessment will likely result in some debate into how broadly the concept of ‘concentration’ is to be defined, and whether there is a need to close the perceived gap between the EuMr and articles 101 and 102 TFEu.

The continued global economic downturn led to another year of relatively few merger filings compared to earlier years, notably 2007 and 2008. This trend appears unlikely to change in the near future.

23 See article 22 EuMr.

428

Appendix 1

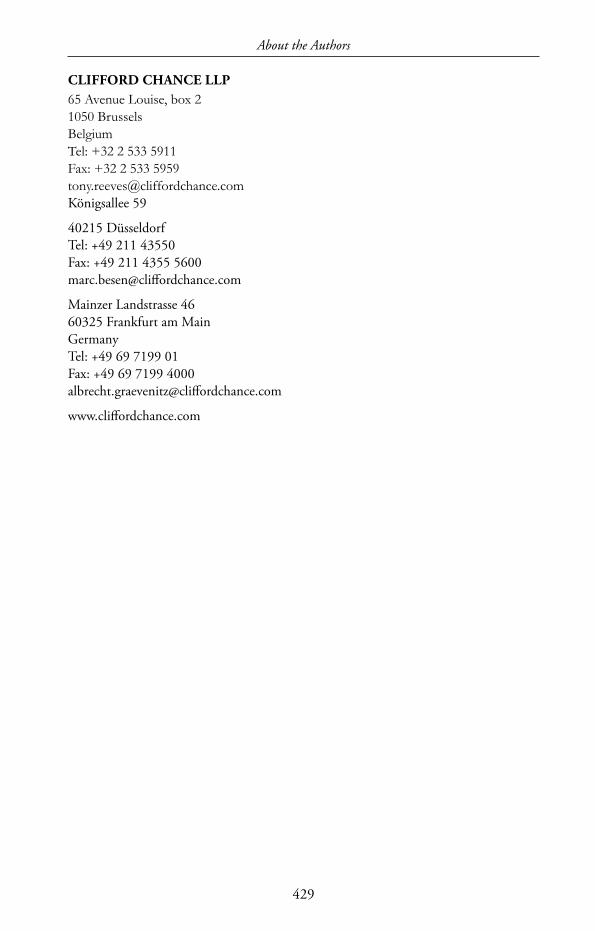

About the Authors

TONY REEVESClifford Chance LLPtony reeves is the managing partner of the brussels office of Clifford Chance LLP. he advises major corporations on eu and multi-jurisdictional competition law issues and specialises in merger notifications, abuse of market power, distribution and supply practices and compliance across a range of sectors. Mr reeves has been based in the brussels office since 1995 and is a member of the firm’s global cartel and merger taskforces. he speaks regularly at conferences such as Fordham, IbA, IbC, Chatham house and industry events. Mr reeves is recognised as a leading competition lawyer by Chambers, Legal 500, GCR, Who’s Who Legal, European Legal Experts and The Legal Media Group’s Guide to the World’s Leading Competition and Antitrust Lawyers. he has also been a non-governmental adviser to the International Competition Network (ICN).

ASHWIN VAN ROOIJEN

Clifford Chance LLPAshwin van rooijen an associate in the brussels office of Clifford Chance. he specialises in advising technology firms in mergers and behavioural antitrust matters as well as a wide variety of intellectual property issues. Mr van rooijen is a member of the brussels and New York bars.

About the Authors

429

CliffORd ChaNCE llP65 Avenue Louise, box 21050 BrusselsBelgiumTel: +32 2 533 5911Fax: +32 2 533 [email protected]önigsallee 59

40215 Düsseldorftel: +49 211 43550Fax: +49 211 4355 [email protected]

Mainzer Landstrasse 46 60325 Frankfurt am MainGermanytel: +49 69 7199 01Fax: +49 69 7199 [email protected]

www.cliffordchance.com