Embed Size (px)

Citation preview

The Microeconomic Strategy Project

A baseline assessment of the fishing and aquaculture industry

in the Western Cape

August 2004

Mohammed Karaan

Sanri Rossouw

Department of Agricultural Economics

Stellenbosch University

1

SUMMARY

The total value of the South African fishing industry amounted to R2.78 billion in 1999 and the

Western Cape accounted for about 90% of the industry. Demersal trawl contributes almost 50% to

the total value of the industry. The Western Cape exported fish with a total value of R2 418.4

million, representing 8.5% of total Western Cape exports and 73% of total South African fish

exports.

The South African fishing industry employs 38 311 people of which 90% are Black. The Western

Cape employs approximately 70% of the workers and about 71% of the gross remuneration is

earned in the Western Cape. The majority (90.6%) of workers in the fishing industry in the

commercial harbour towns of the Western Cape are Black. 76% of the Black workers are semi-

skilled.

Transformation in the fishing industry is primarily the result of a change in the number and size of

fishing rights allocated. Some 2 625 rights (or quotas) were allocated in 2001, of which at least 2

000 qualify as SMME’s. The Department of Environmental Affairs and Tourism estimates that an

average of 60% are majority PDI-owned (majority pdi-owned means 51% or more of the company

is owned by pdi’s). This large number of rights allocated to pdi’s or companies owned and

managed by pdi’s, resulted in a large increase in the flow of income to impoverished fishing

communities.

2

TABLE OF CONTENTS

Introduction………………………………………………………………………………………….4

A1. Catches, landings and value……………………………………………………...…………….6

A2. Imports and exports…………………………………………………………………………….7

A3. Income, employment and skills………………………………………………………………10

A4. The regulation of commercial fishing in South Africa ………………………………………19

B1. Abalone……………………………………………………………………………………….20

B2. Deep-sea and inshore hake……………………………………………………………………21

B3. Hake handline…………………………………………………………………………………22

B4. Hake longline…………………………………………………………………………………23

B5. Traditional commercial line…………………………………………………………………..24

B6. Midwater trawl………………………………………………………………………………..25

B7. Pelagic………………………………………………………………………………………...25

B8. South coast rock lobster………………………………………………………………………27

B9. Shark longline………………………………………………………………………………...28

B10. Squid…………………………………………………………………………………………28

B11. West coast rock lobster………………………………………………………………………29

B12. Tuna…………………………………………………………………………………………..30

B13. Seaweed………………………………………………………………………………………30

C Aquaculture…….……………………………………………………………………………….32

C1 Overview………………………….……………………………………………………………32

C2 Abalone………………………….……………………………………………………………..33

C3 Kelp……………………………….……………………………………………………………34

C4 Mussels…………………………….…………………………………………………………...34

C5 Oysters…………………………….……………………………………………………………35

C6 Seaweed…………………………….…………………………………………………………..35

C7 Trout………………………………….………………………………………………………...36

C8 Other……………………………………………………………………………………………36

D ??????????……………………………………………………………………………………….37

Bibliography…………………………………………………………………..……………….…..40

Annexure…………………………………………………………………………………………...42

3

LIST OF ABBREVIATIONS CAF Consultative Advisory Forum

ESS An Economic and Sectoral Study of the South Africa fishing industry

ICCAT International Commission for the Conservation of Atlantic Tunas

JSE Johannesburg Stock Exchange

MCM Marine and Coastal Management

MLRA Marine Living Resources Act

PDI Previously Disadvantaged Individuals

TAC Total Allowable Catch

TAE Total Applied Effort

4

INTRODUCTION

The value of the South African fishing industry was about R2.78 billion in 1999, and the Western

Cape accounts for some 90% of the industry. Fishing activity in the Western Cape is centered

predominantly along the West coast, that is from Simons Town to Saldanha. After fruit and wine,

beer and spirits, fish is the largest export product of the Western Cape with a total value of R2

418,4 million in 2002, representing 8.5% of total Western Cape exports. (Wesgro)

Besides the responsibility to ensure the sustainable utilisation of the living marine resources, the

government also needs to address the prevailing inequalities and dualism. The initial attempt of

intervention by allocating fishing rights to smaller, mostly black entrants at the cost of larger

historically white companies, resulted in many problems and legal challenges. Despite these

problems, the allocation of fishing rights are quite successful in empowering previously

disadvantaged individuals (pdi’s). Only 300 white-owned companies participated in the

commercial fishing industry during apartheid. Over the past three years rights were granted to 5

837 individuals and companies. Some 2 625 rights (or quotas) have been allocated in 2001, of

which at least 2 000 qualify as SMME’s. The Department of Environmental Affairs and Tourism

(hereafter referred to as the Department) estimates that an average of 60% are majority HDI owned

(majority hdi-owned means 51% or more of the company is owned by pdi’s). (Kleinschmidt,

2003). This large number of rights allocated to pdi’s or companies owned and managed by pdi’s,

resulted in a large increase in the flow of income to impoverished fishing communities. Also, the

allocation of rights to so many entities was achieved without compromising the long-term

sustainability of marine resources. (Transformation and the South African Fishing Industry, 2003)

Despite the significant progress made with transformation in the fishing industry, there is still

some way to go, especially considering the employment, income, skills distribution, and

livelihoods. This report describes the current status of the fishing industry, focusing on the

Western Cape, to provide a background for policy formulation.

No primary research was done for this report, but numerous secondary sources were consulted.

The most important source is a study by Rhodes University on behalf of MCM called “An

Economic and Sectoral Study of the South African Fishing Industry” (hereafter the ESS Report).

5

The report consist of three parts. Part A discusses general features of the fishing industry. Section

A2 provides statistics on catches, landings and values of the South African fishing industry and

section A3 discusses the trade statistics. Section A4 discusses employment and income statistics

for the country and the socio-economic contribution the fishing industry makes to commercial

harbour towns in the Western Cape. It also looks at different measures of transformation. Section

A5 briefly discusses the regulatory environment of the fishing industry. Part B provides a short

summary of the major fisheries active in the Western Cape. The fisheries discussed include

abalone, deep-sea and inshore hake trawl, hake handline, hake longline, traditional commercial

line fishery, midwater trawl fishery, pelagic, south coast rock lobster, shark longline, squid, west

coast rock lobster, tuna, seaweed and aquaculture. This section is largely a summary of the second

volume of the ESS Report. Section C provides and overview of the aquaculture industry in South

Africa with specific reference to abalone, kelp, mussels, oysters, seaweed, trout and eels.

6

PART A - INDUSTRY BACKGROUND

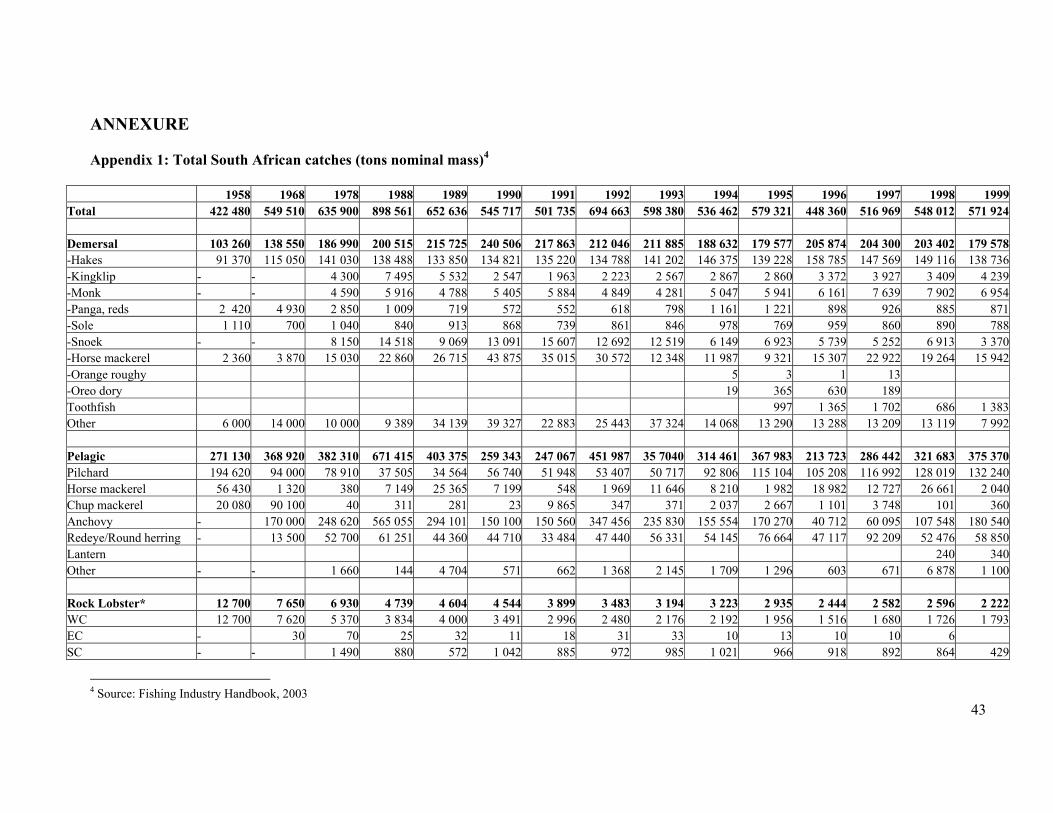

A1. Catches, landings and value1 Figures A1.1 and A1.2 show South African catches for the major fishery types: demersal, pelagic,

rock lobster, and line and small nets2. Total catch depends on the total allowable catch (TAC) or

total applied effort (TAE) determined for a specie or the abundance of the specie in the case where

no TAC/TAE is applicable. The TAC/TAE is determined after discussions between scientists who

conduct annual surveys to determine the stock levels, the government and various stakeholders in

the industry.

Figure A1.1: South Africa catches for the demersal and pelagic industries (tons nominal mass)

Source: Fishing Industry Handbook, 2003

Figure A1.2: South Africa catches for rock lobsters and line and small net industries (tons nominal mass)

Source: Fishing Industry Handbook, 2003 1 Source: Fishing Industry Handbook, 2003 2 Line and small net include species such as mullet, tuna, snoek, yellowtail and squid. See the annexure for a detailed table on South African catches.

0

100000

200000

300000

400000

500000

600000

700000

800000

1958

1968

1978

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Mas

s (T

ons)

Demersal Pelagic

0

5000

10000

15000

20000

25000

30000

35000

1958

1968

1978

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Mas

s (T

ons)

Rock Lobster* Line, small net

7

Table A1.1 provides information on South African catches, landings and value in 1999. The total

value of the South African fishing industry was R2.78 billion in 1999 and accounted for about

0.5% of total world production (Wesgro). Demersal trawl contributes almost 50% to the value of

the industry, followed by pelagic (19.5%) and line fish (11.4%). Oysters is the smallest industry

contributing less than 0.05% to the total value of the fishing industry.

In terms of mass almost 70% of landings is pelagic, but it contributes only 19.5% to the total value.

Demersal trawl contributes almost 50% to total value, but represents only 22.3% of total landings.

Fishery Catch Landings Value % of total

value (tons) (tons) (R'000)

Demersal: Offshore trawl 157 449 110 526 1 271 049 45.7 Demersal: Inshore trawl 15 150 10 492 86 873 3.1 Total demersal trawl 172 599 121 018 1 357 922 48.8 Purse Seine (Pelagic) 375 370 375 370 541 699 19.5 SC rock lobster 920 428 111 217 4 WC rock lobster 1 791 1 791 187 799 6.8 Crustacean Trawl 433 433 15 918 0.6 Line fish 24 094 24 094 316 701 11.4 Demersal longlining 7 273 6 611 85 659 3.1 Abalone 482 482 77 120 2.8 Miscellaneous 6 891 6 891 28 997 1 Oysters 55 55 1 342 0 Mariculture 2 631 2 631 47 134 1.7 Seaweed 2 202 2 202 10 425 0.4 Total 594 741 542 006 2 781 933 100 Table A1.1: South African catches, landings and values: 1999

Source: Fishing Industry Handbook, 2003

The Western Cape accounts for about 90% of the South African fishing industry (Wesgro).

A2. Imports and exports South Africa is a net-exporter of fish products and the main export destinations include European

countries like France, Germany and Belgium, African states like Angola, Zimbabwe and

Mozambique, and Canada, Australia, Hong Kong, Singapore and Taiwan (Wesgro).

8

Figure A2.1: South Africa fish trade in mass: 1999-2002

Source: Fishing Industry Handbook, 2003

Figure A2.2: South Africa fish trade in rands: 1999-2000

Source: Fishing Industry Handbook, 2003

South Africa imported fish with a total value of R496 million in 2002 and exported R3.3 billion.

Figure A2.2 indicates a clear upward trend in the value of exports, but this sharp increase may

largely be due to the weakening of the rand during that time. Figure A2.1 also shows an increasing

trend in the mass of fish exports, but not to the same extent as the growth in value (see figure

A2.2). Table A2.1 illustrates this point. The mass of fish exports increased with only 2% in 2001,

but the value increased with 30%. Also, the mass increased with only 8% in 2002, but the value

increased with 36%.

0

20

40

60

80

100

120

140

160

180

1999 2000 2001 2002

Mill

ions

Mas

s (k

g)

Import Export

0

500

1000

1500

2000

2500

3000

3500

1999 2000 2001 2002

Mill

ions

Ran

ds

Import Export

9

Import Export Mass (kg) Rands Mass (kg) Rands 1999-2000 14% 17% 14% 16% 2000-2001 17% 28% 2% 30% 2001-2002 -34% -6% 8% 36% Table A2.1: Growth in imports and exports: 2000-2002

Source: Fishing Industry Handbook, 2003

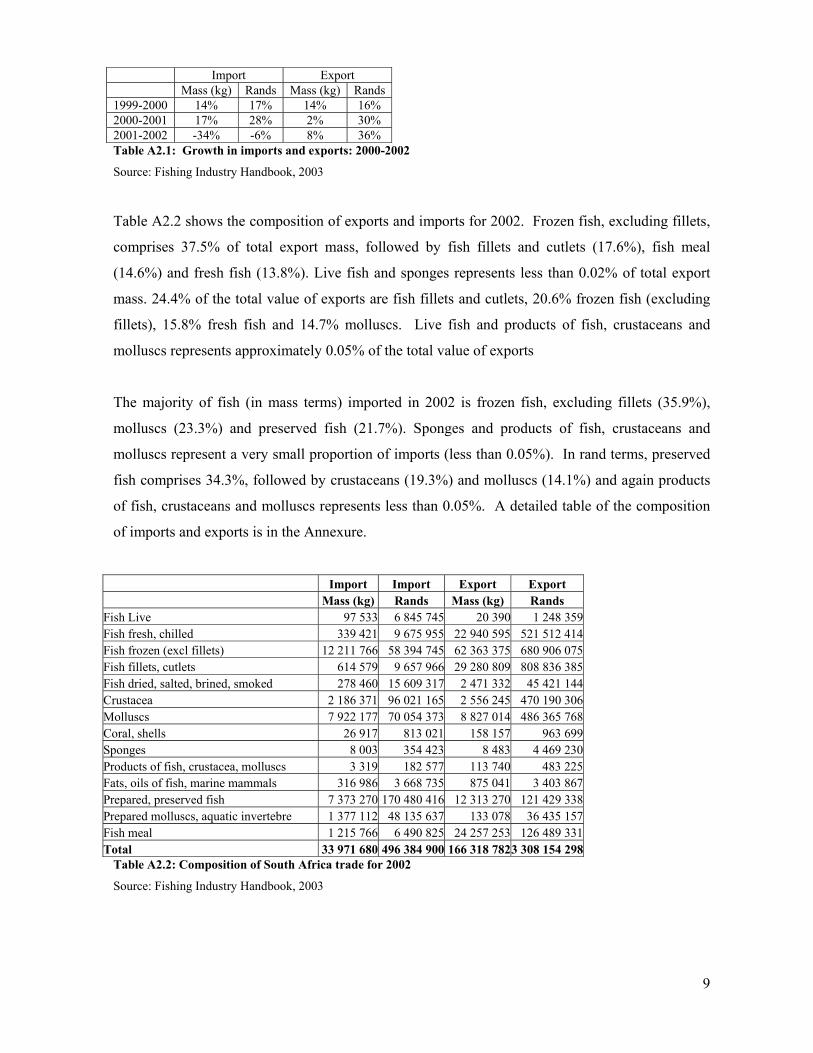

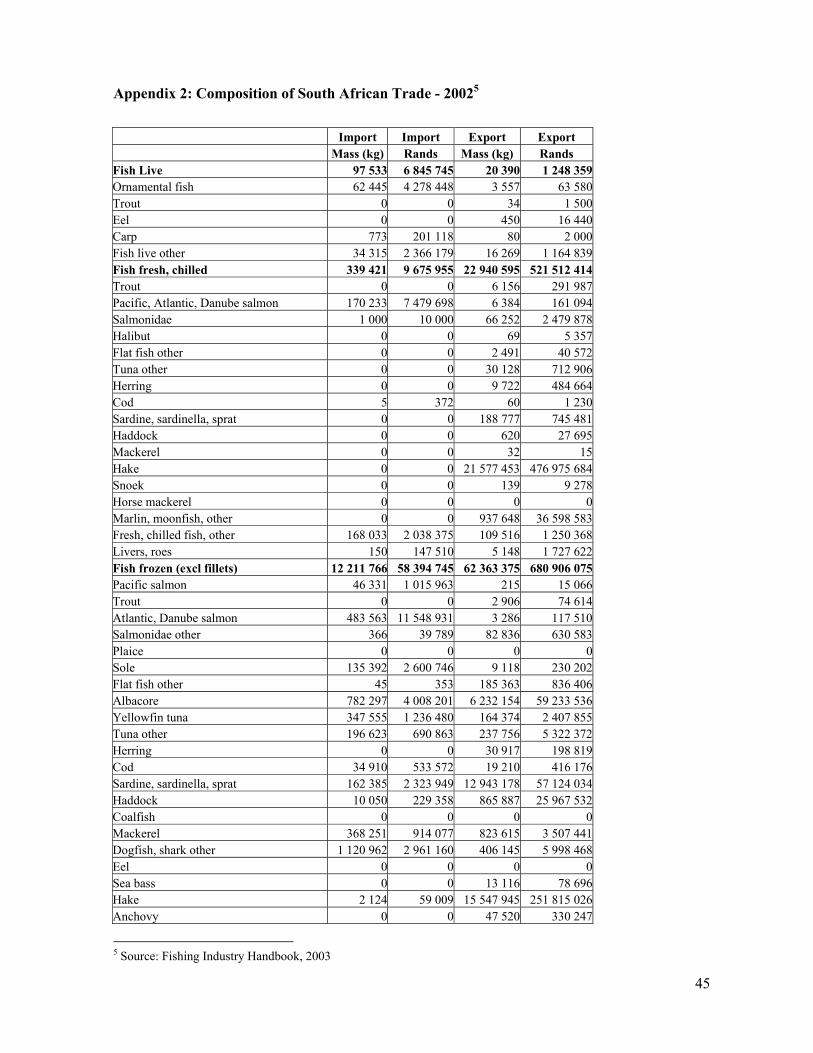

Table A2.2 shows the composition of exports and imports for 2002. Frozen fish, excluding fillets,

comprises 37.5% of total export mass, followed by fish fillets and cutlets (17.6%), fish meal

(14.6%) and fresh fish (13.8%). Live fish and sponges represents less than 0.02% of total export

mass. 24.4% of the total value of exports are fish fillets and cutlets, 20.6% frozen fish (excluding

fillets), 15.8% fresh fish and 14.7% molluscs. Live fish and products of fish, crustaceans and

molluscs represents approximately 0.05% of the total value of exports

The majority of fish (in mass terms) imported in 2002 is frozen fish, excluding fillets (35.9%),

molluscs (23.3%) and preserved fish (21.7%). Sponges and products of fish, crustaceans and

molluscs represent a very small proportion of imports (less than 0.05%). In rand terms, preserved

fish comprises 34.3%, followed by crustaceans (19.3%) and molluscs (14.1%) and again products

of fish, crustaceans and molluscs represents less than 0.05%. A detailed table of the composition

of imports and exports is in the Annexure.

Import Import Export Export Mass (kg) Rands Mass (kg) Rands Fish Live 97 533 6 845 745 20 390 1 248 359 Fish fresh, chilled 339 421 9 675 955 22 940 595 521 512 414 Fish frozen (excl fillets) 12 211 766 58 394 745 62 363 375 680 906 075 Fish fillets, cutlets 614 579 9 657 966 29 280 809 808 836 385 Fish dried, salted, brined, smoked 278 460 15 609 317 2 471 332 45 421 144 Crustacea 2 186 371 96 021 165 2 556 245 470 190 306 Molluscs 7 922 177 70 054 373 8 827 014 486 365 768 Coral, shells 26 917 813 021 158 157 963 699 Sponges 8 003 354 423 8 483 4 469 230 Products of fish, crustacea, molluscs 3 319 182 577 113 740 483 225 Fats, oils of fish, marine mammals 316 986 3 668 735 875 041 3 403 867 Prepared, preserved fish 7 373 270 170 480 416 12 313 270 121 429 338 Prepared molluscs, aquatic invertebre 1 377 112 48 135 637 133 078 36 435 157 Fish meal 1 215 766 6 490 825 24 257 253 126 489 331 Total 33 971 680 496 384 900 166 318 7823 308 154 298

Table A2.2: Composition of South Africa trade for 2002

Source: Fishing Industry Handbook, 2003

10

Fish products is the third largest export product of the Western Cape with a total value of R2 418,4

million, representing 8.5% of total Western Cape exports. (Wesgro)

A3. Income, employment and skills The Western Cape employs approximately 70% of the workers in the fishing industry and

approximately 71% of the employment income (gross remuneration) in the fishing industry is

earned in the Western Cape (see figures A3.1 and A3.2).

Figure A3.1: Total fishing industry employment Figure A3.2: Total fishing industry income

distribution between provinces distribution between provinces

Source: ESS Report (1), 2003 Source: ESS Report (1), 2003

The South African fishing industry employs 38 311 people, of which 90% are Black. Figure A3.3

shows the number of people for each race group, level of skills and sector within the fishing

industry. The majority of workers are semi-skilled and Black.

Figure A3.4 shows the percentage of black workers in each sector and the different levels of skills.

There is a clear relationship between the level of skills and the percentage of Black employees: the

higher the skill level the lower is the proportion of Black employees. For example, only 49.6% of

professionals or managers are Black whereas 98% of the unskilled workers are Black.

KZN2%

WC70%

NC1%

EC12%

Unspecified

15%KZN2%

WC71%

NC1%

EC11%

Unspecified

15%

11

Figure A3.3: The number of people employed in the South African fishing industry by race, by sector and by

skills level.

Source: ESS Report (1), 2003

Figure A3.4: The percentage black employment in the South African fishing industry by race, by sector and by

skills level

Source: ESS Report (1), 2003

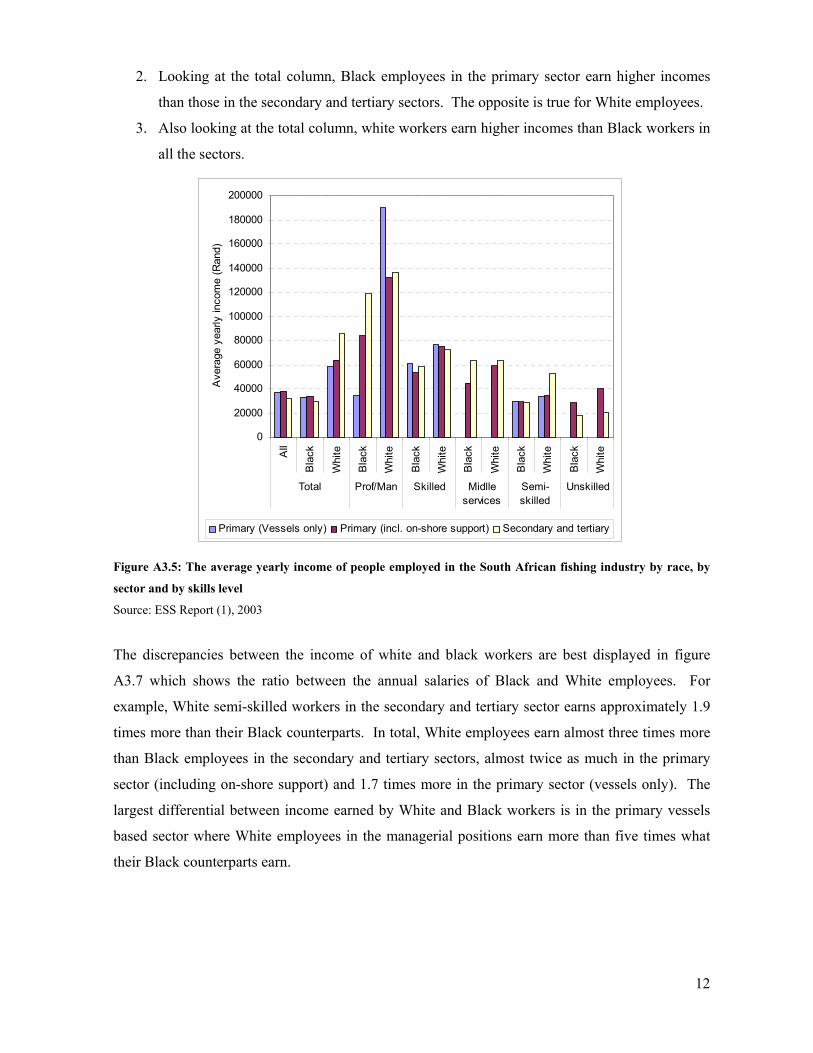

Figure A3.5 shows the average yearly income of people employed in the South African fishing

industry by race, by sector and by skills level. The following points are of importance:

1. Employees in the professional and managerial positions earn the highest average yearly

income, and as the skill level drops, the income earned also decline.

0

10

20

30

40

50

60

70

80

90

100

% Black employment

Primary 52.2 64.8 62.8 92.1 96

Secondary and tertiary 46.5 68 77.2 98.5 98.6

Fishing industry 49.6 65.1 71.9 94.5 98

Prof/Man Skilled Middle services

Semi-skilled

Unskilled

72 3

1377

1068

9769

828

218

200

2279

1237

155

92

1106

8

954

624

26160

184

193

91 328

97

7331

115

5343

34

0

2000

4000

6000

8000

10000

12000

Black White Black White Black White Black White Black White

Professional Skilled Middle services Semi-skilled Unskilled

Num

ber o

f peo

ple

empl

oyed

Primary (Vessels only) Primary (incl. on-shore support) Secondary and tertiary

12

2. Looking at the total column, Black employees in the primary sector earn higher incomes

than those in the secondary and tertiary sectors. The opposite is true for White employees.

3. Also looking at the total column, white workers earn higher incomes than Black workers in

all the sectors.

Figure A3.5: The average yearly income of people employed in the South African fishing industry by race, by

sector and by skills level

Source: ESS Report (1), 2003

The discrepancies between the income of white and black workers are best displayed in figure

A3.7 which shows the ratio between the annual salaries of Black and White employees. For

example, White semi-skilled workers in the secondary and tertiary sector earns approximately 1.9

times more than their Black counterparts. In total, White employees earn almost three times more

than Black employees in the secondary and tertiary sectors, almost twice as much in the primary

sector (including on-shore support) and 1.7 times more in the primary sector (vessels only). The

largest differential between income earned by White and Black workers is in the primary vessels

based sector where White employees in the managerial positions earn more than five times what

their Black counterparts earn.

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

All

Bla

ck

Whi

te

Bla

ck

Whi

te

Bla

ck

Whi

te

Bla

ck

Whi

te

Bla

ck

Whi

te

Bla

ck

Whi

te

Total Prof/Man Skilled Midlleservices

Semi-skilled

Unskilled

Ave

rage

yea

rly in

com

e (R

and)

Primary (Vessels only) Primary (incl. on-shore support) Secondary and tertiary

13

Figure A3.7: Ratio of White annual income to black annual income by sector and skills level.

Source: ESS Report (1), 2003

The discrepancy between the income earned by Black and White employees are true for all the

provinces as is indicated by figure A3.6. The Eastern Cape and Western Cape has the largest

differentials between Black and White earners. This does not necessarily imply greater

discrimination within these provinces, as the difference in income may be due to the skew skills

distribution. The figure also indicates that people in the Western Cape and KwaZulu-Natal earn

higher incomes than those in the Eastern Cape and Northern Cape.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Whi

te in

com

e : B

lack

inco

me

Primary (Vessels only) 1.7 5.5 1.3 1.2

Primary (incl. on-shoresupport)

1.9 1.6 1.4 1.3 1.2 1.4

Secondary and tertiary 2.9 1.2 1.2 1.0 1.9 1.1

Total Prof/Man Skilled Middle Services

Semi-skilled

Unskilled

14

Figure A3.6: Scatter plot of Black, White and aggregated yearly fishing industry incomes per province

Source: ESS Report (1), 2003

Socio-economic

The total population of the harbour towns in the Western Cape is 400 034 people of which 38.2%

are employed. (The extended labour force is 64.5% of the total population). The population

distribution in the harbour towns is 70.8% Black, 27.7% White and 1.5% unspecified. The

employment rates for Black and White people are 36% and 42.3% respectively.

Figure A3.7 shows the contribution the fishing industry makes to employment in the harbour

towns. The fishing industry employs 17.8% of all Black people employed and 2.2% of all White

people employed.

WC

NC

KZNEC

Unsp SAWC

NC

KZN ECUnsp SA

WC

NC

KZN

EC

Unsp

SA

0

10000

20000

30000

40000

50000

60000

70000

Ave

rage

Inco

me

All Black White

15

Figure A3.7: The number of people employed in the fishing industry and other industries in the commercial

harbour towns of the Western Cape

Source: ESS Report, 2003

Figure A3.8 shows the number of White and Black people for each level of skills employed in the

commercial harbour towns of the Western Cape. 14 414 of the 15 903 people (90.6%) employed

in the fishing industry in the harbour towns of the Western Cape are Black, and the remaining

9.4% are White. 10 935 (75.9%) of the Black people are semi-skilled and just over 1% are in

management positions. 630 (42.3%) of the White people are semi-skilled, 650 (43.7%) are skilled

and 9.4% are in management positions.

Figure A3.8: Number of people employed in the fishing industry in the commercial harbour towns in the

Western Cape by race and by skills level

Source: ESS Report (1), 2003

0

2000

4000

6000

8000

10000

12000

Num

ber o

f peo

ple

empl

oyed

Black 158 975 275 10935 2071

White 140 650 63 630 6

Professional Skilled Middle skilled Semi-skilled Unskilled

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Num

ber o

f peo

ple

empl

oyed

Fishing industry 14414 1489

Other 66771 65836 8066

Black White Unspecified

16

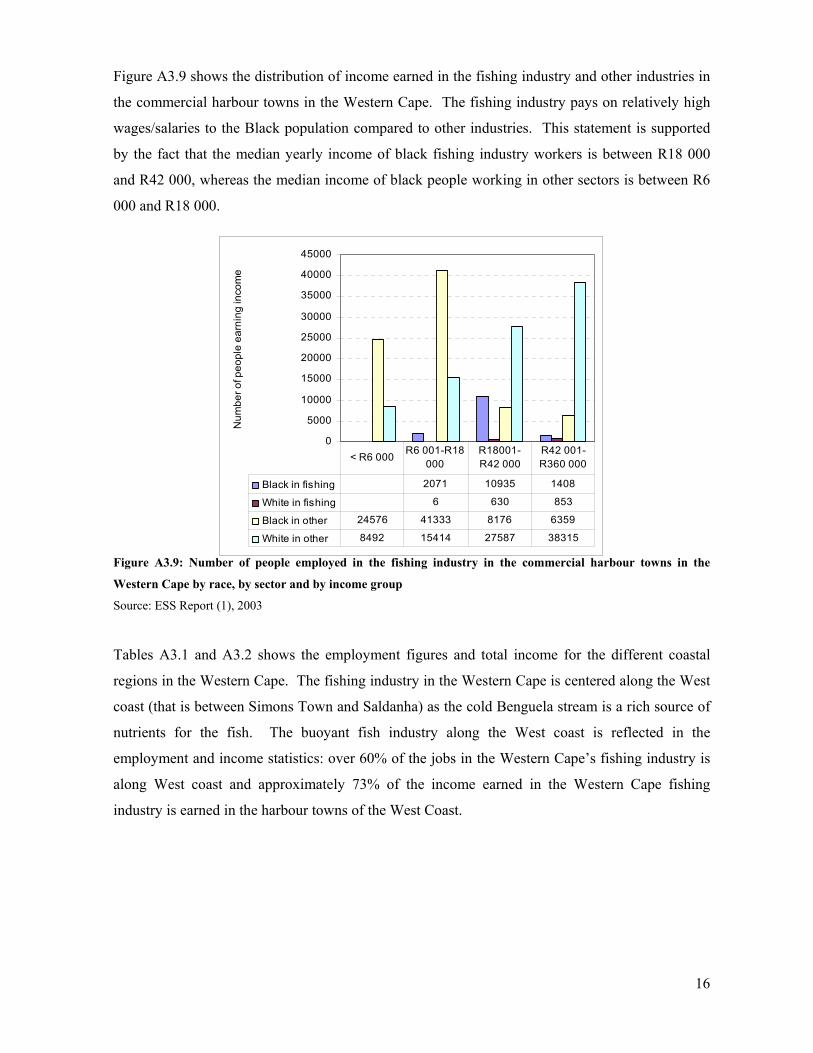

Figure A3.9 shows the distribution of income earned in the fishing industry and other industries in

the commercial harbour towns in the Western Cape. The fishing industry pays on relatively high

wages/salaries to the Black population compared to other industries. This statement is supported

by the fact that the median yearly income of black fishing industry workers is between R18 000

and R42 000, whereas the median income of black people working in other sectors is between R6

000 and R18 000.

Figure A3.9: Number of people employed in the fishing industry in the commercial harbour towns in the

Western Cape by race, by sector and by income group

Source: ESS Report (1), 2003

Tables A3.1 and A3.2 shows the employment figures and total income for the different coastal

regions in the Western Cape. The fishing industry in the Western Cape is centered along the West

coast (that is between Simons Town and Saldanha) as the cold Benguela stream is a rich source of

nutrients for the fish. The buoyant fish industry along the West coast is reflected in the

employment and income statistics: over 60% of the jobs in the Western Cape’s fishing industry is

along West coast and approximately 73% of the income earned in the Western Cape fishing

industry is earned in the harbour towns of the West Coast.

0

5000

10000

15000

20000

25000

30000

35000

40000

45000N

umbe

r of p

eopl

e ea

rnin

g in

com

e

Black in fishing 2071 10935 1408

White in fishing 6 630 853

Black in other 24576 41333 8176 6359

White in other 8492 15414 27587 38315

< R6 000R6 001-R18

000R18001-R42 000

R42 001-R360 000

17

Total Professional Skilled Middle skilled Semi-skilled Unskilled All Black White Full-time Part-timeFull-timePart-timeFull-timePart-timeFull-time Part-timeFull-timePart-time Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl WhWestern Cape 15 903 14 414 1 489 143 138 15 2 759 401 216 249 271 63 4 6 3512944 584336 989 21 082 4-North west coast 3 864 3 768 96 20 25 3 2 123 30 17 93 16 3 721 111 967 10 446 1 375 1-West coast 9 612 8 656 956 111 92 12 492 234 185 240 157 31 1 4 5611321 991223 449 1 697 3-South west coast 1 004 852 152 6 11 56 42 11 3 6 13 357 71 325 12 91 -South east coast 1 423 1 138 285 6 10 88 95 3 6 15 3 712 80 301 91 3 Table A3.1: The number of fishing industry employees by skills group, part-time or full-time employment and race by coastal regions in WC.

Source: ESS Report (1), 2003

Total Professional Skilled Middle skilled Semi-skilled Unskilled All Black White Full-time Part-time Full-time Part-time Full-time Part-time Full-time Part-time Full-time Part-time Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl Wh Bl WhBl WhWestern Cape564 132465 56498 568 17 130 20 388 252 45 97228 20611 38220 55617 7663 870 36 215 44810 740120 30614 70020 076 3617 196 72-North west 85 212 78 240 6 972 2 316 3 120 18 4 284 2 280 192 5 508 954 15 324 354 36 378 228 9 822 18 4 398 18-West coast 411 984366 47475 510 13 884 15 216 234 36 80418 87010 85420 19611 4481 962 36 176 112 7 290 66 19211 904 8 292 1812 618 54-South west 25 818 20 922 4 896 390 1 134 1 242 1 458 198 108 270 846 5 898 1 026 11 016 324 1 908 -South east 41 118 29 92811 190 540 918 3 642 5 598 138 252 540 108 18 114 2 070 6 720 2244 54 180

Table A3.2: Total income of fishing industry employees by skills group, part-time or full-time employment and race by coastal regions in WC

Source: ESS Report (1), 2003

North west coast West coast South west coast South east coast

Doringbaai Saldanha Kalk Bay Struisbaai

Lambert’s Bay Yzerfontein Strand Arniston

Elandsbaai Cape Town Gordon’s Bay Mossel Bay

Velddrif Hout Bay Kleinmond Knysna

St Helenabaai Kommetjie Hermanus Plettenberg Bay

Paternoster Simons Town Gansbaai

Table A3.3: Harbour towns for each coastal region in the Western Cape

Source: ESS Report (1), 2003

18

A large proportion of the workers are part-time employees (table A3.1). Many of the fisheries

have strong seasonal components resulting in 6 492 of the 15 903 employees (over 40% of total

employment) being part-time employed. The part-time workers earn 32.7% of total income (table

A3.2).

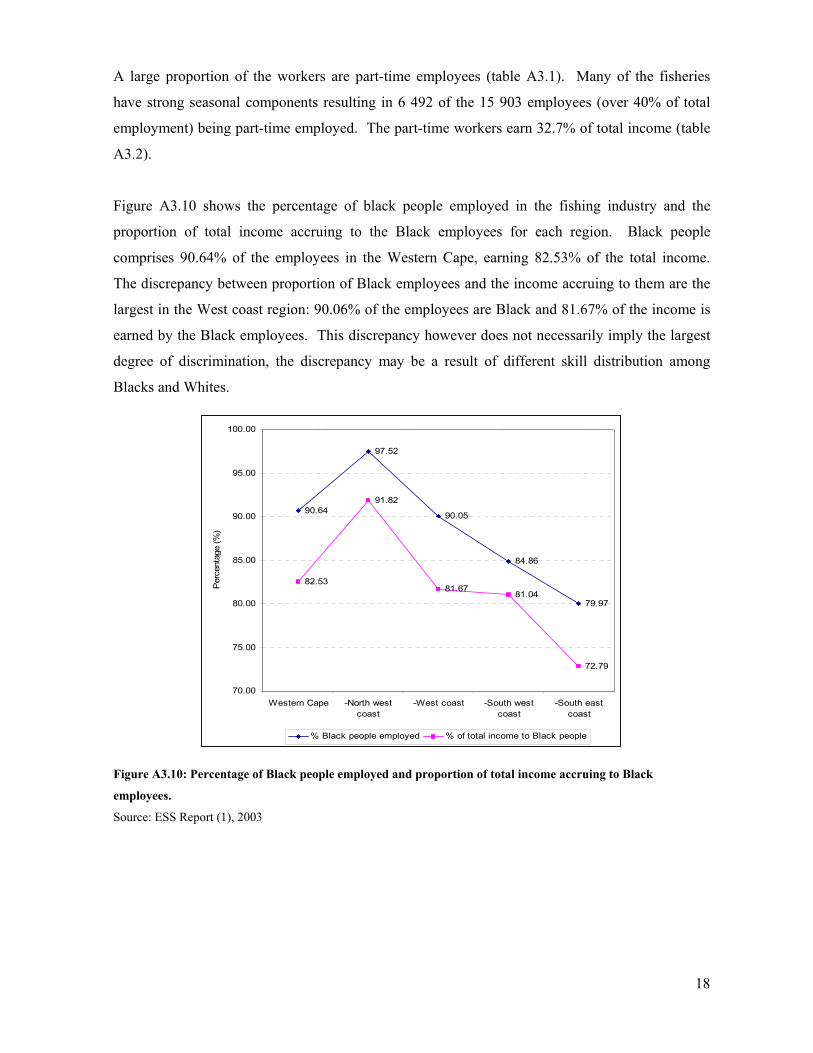

Figure A3.10 shows the percentage of black people employed in the fishing industry and the

proportion of total income accruing to the Black employees for each region. Black people

comprises 90.64% of the employees in the Western Cape, earning 82.53% of the total income.

The discrepancy between proportion of Black employees and the income accruing to them are the

largest in the West coast region: 90.06% of the employees are Black and 81.67% of the income is

earned by the Black employees. This discrepancy however does not necessarily imply the largest

degree of discrimination, the discrepancy may be a result of different skill distribution among

Blacks and Whites.

Figure A3.10: Percentage of Black people employed and proportion of total income accruing to Black

employees.

Source: ESS Report (1), 2003

90.64

97.52

90.05

84.86

79.97

82.53

91.82

81.6781.04

72.79

70.00

75.00

80.00

85.00

90.00

95.00

100.00

Western Cape -North westcoast

-West coast -South westcoast

-South eastcoast

Per

cent

age

(%)

% Black people employed % of total income to Black people

19

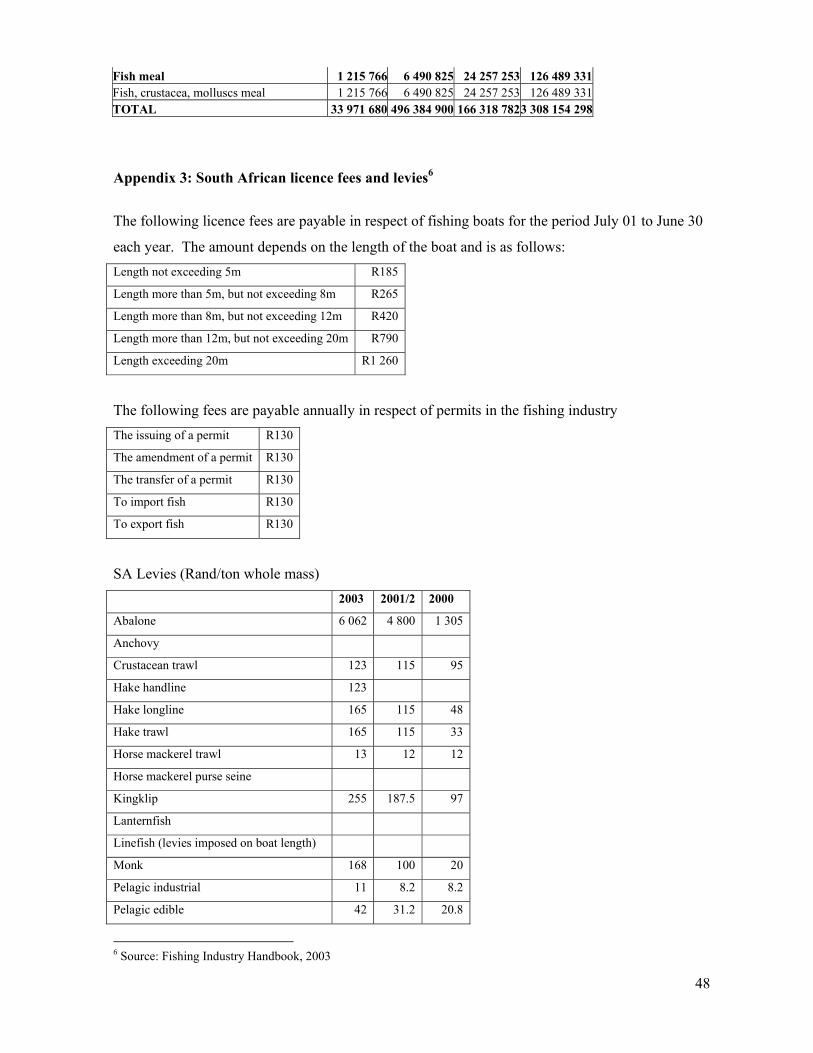

A4. The regulation of commercial fishing in South Africa The marine ecosystem is protected and governed by the Marine Living Resources Act (MLRA)

which was promulgated in 1998. The purpose of the Act is “To provide for the conservation of the

marine ecosystem, the long term sustainable utilisation of marine living resources and the orderly

access to exploitation, utilisation and protection of certain marine living resources; and for these

purposes to provide for the exercise of control over marine living resources in a fair and equitable

manner to the benefit of all the citizens of South Africa; and to provide for matters connected

therewith.” (ESS Report (1), 2003:76). Reaching these objectives is no easy task and the

Department experienced numerous problems ranging from administrative chaos resulting in long

delays in the allocation of fishing rights to repeated court appeals to the allocations made. Appeals

were made by those denying access to resources and by those who felt that too much had been

taken away from them. The Department lost a number of the appeals resulting in a loss of

confidence in the Department’s ability to implement the objectives of the MRLA.

A team, including contracted administrative and legal members, was put together to implement a

new plan for the 2001 application process. After wide spread consultation and communication

with companies, communities and other interested parties a new system of allocating fishing rights

in South Africa was put in place. With the new system medium-term rights (approximately for

four years) are allocated as opposed to one-year rights, application fees have increased, an

independent Rights Verification Unit check the details of the applicants, an advisory committee

(the Consultative Advisory Forum (CAF)) advises the Minister, and the process includes an

internal appeal period. The 2001 allocation process went fairly smoothly. Of the 3 574 potential

appellants, 1 501 lodged internal appeals and a few went directly to the court. The court ruled in

favour of the Department in all the appeals against the 2001 allocations. The greatest challenge

against the Department was that of Bato Star, a company owned by trade unions. They argued that

they should receive a greater share of the TAC since they are a wholly pdi-owned company. The

High Court in Cape Town ruled in favour of the applicant, but this judgement was overruled by the

South African Supreme Court. (Kleinschmidt, Sauer and Britz, 2003)

20

PART B – SECTORAL OVERVIEW

B1. Abalone Until 1968 there was no restrictions on the catches of abalone, but catches declined in the second

half of the 1960’s and government introduced the first quota’s in 1968 at 386 tons (meat mass).

These allocations were granted to six factories that were in production at the time. In 1983 they

made the quotas applicable to whole mass instead of meat mass and set the TAC at 660 tons. By

the early 1990’s the fishing industry consisted of two components, namely 50 licensed divers who

were each granted the right to harvest a small percentage of the TAC, and about six quota holders

who owned the receiving, processing and marketing rights to the bulk of the annual TAC. In the

1993/4 season a 10 ton community trust was introduced and allocated and in the 1995/6 season.

10% of the TAC was allocated to new entitlement holders. The TAC for the 1998/9 season was

820 tons of which 515 tons were allocated to the “traditional” commercial entities, 220 tons for

recreational take and 85 tons for subsistence allocation. (The recreational fishery no longer exists.)

The Department reduced the TAC from 430 tons to 282 tons in February 2004 and allocated the

following fishing rights, valid for ten years:

• Rights were allocated to 5 abalone fish processors.

• 200 divers received rights. An amount of 107 000kg was allocated to the divers. 74.5% of

the divers are pdi’s.

• 24 applicants for legal entity rights satisfied the criteria of the Department and received

quota’s. A total of 19 122 kg have been allocated to the 24 legal entities rights holders.

The 24 rights holders are highly transformed and are 66% or more pdi-owned and

managed.

• An amount of 58 374 kg has been set aside for appeals. (Department of Environmental

Affairs and Tourism, 2004)

The above allocation were made on the assumption that poaching will be reduced by 50% due to

increased compliance efforts. This assumption is however very optimistic and the CAF

recommended in September 2004 to reduce the TAC to 182 metric tonnes to ensure the sustainable

exploitation of abalone. The CAF also recommended that compliance issues should be given high

priority. Finally, the CAF recommended that the Department should consider completely closing

the abalone fishery. (CAF Meeting, 2004)

21

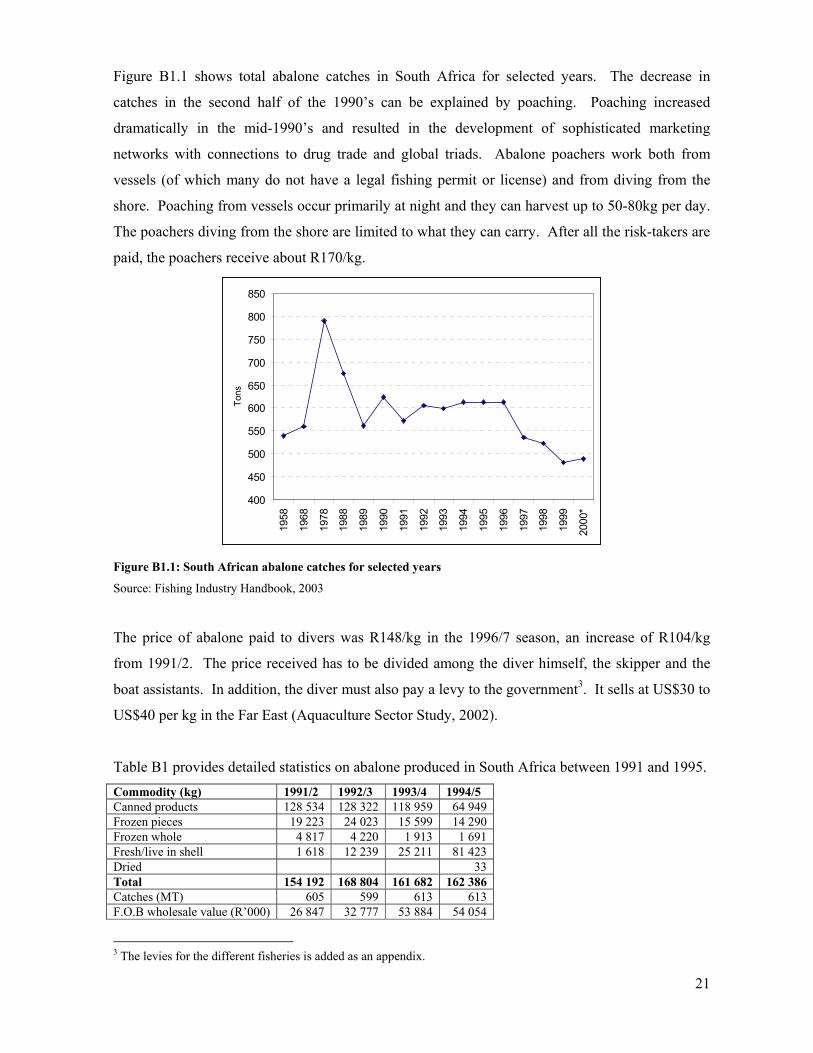

Figure B1.1 shows total abalone catches in South Africa for selected years. The decrease in

catches in the second half of the 1990’s can be explained by poaching. Poaching increased

dramatically in the mid-1990’s and resulted in the development of sophisticated marketing

networks with connections to drug trade and global triads. Abalone poachers work both from

vessels (of which many do not have a legal fishing permit or license) and from diving from the

shore. Poaching from vessels occur primarily at night and they can harvest up to 50-80kg per day.

The poachers diving from the shore are limited to what they can carry. After all the risk-takers are

paid, the poachers receive about R170/kg.

Figure B1.1: South African abalone catches for selected years

Source: Fishing Industry Handbook, 2003

The price of abalone paid to divers was R148/kg in the 1996/7 season, an increase of R104/kg

from 1991/2. The price received has to be divided among the diver himself, the skipper and the

boat assistants. In addition, the diver must also pay a levy to the government3. It sells at US$30 to

US$40 per kg in the Far East (Aquaculture Sector Study, 2002).

Table B1 provides detailed statistics on abalone produced in South Africa between 1991 and 1995. Commodity (kg) 1991/2 1992/3 1993/4 1994/5 Canned products 128 534 128 322 118 959 64 949 Frozen pieces 19 223 24 023 15 599 14 290 Frozen whole 4 817 4 220 1 913 1 691 Fresh/live in shell 1 618 12 239 25 211 81 423 Dried 33 Total 154 192 168 804 161 682 162 386 Catches (MT) 605 599 613 613 F.O.B wholesale value (R’000) 26 847 32 777 53 884 54 054

3 The levies for the different fisheries is added as an appendix.

400

450

500

550

600

650

700

750

800

85019

58

1968

1978

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

*

Tons

22

Table B1: Statistics for abalone produced in South Africa: 1991-1995

Source: ESS Report (2), 2003

B2. Deep-sea and inshore hake The first individual quota’s was introduced in 1979. In 1986 there were 7 participants in the

industry and this increased to 21 in 1992 and 56 in 2000. The increase between 1992 and 2000 is

in large a result of the Marine Living Resources Act that was promulgated in 1998. However, the

number of participants in the inshore industry has decreased over the past ten years.

In 2000, 33% of the deep-sea TAC was in the hands of previously disadvantaged individuals or

companies. The figures for the inshore trawl industry are 32% and 34% respectively. The three

largest companies in the industry are subsidiaries of JSE listed companies and the percentage

Black ownership may therefore be greater than the estimated figures given above. Employment in

the industry is formal and the majority of jobs (96.4%) in the deep-sea industry are permanent. In

2000, 92% of the 8 838 employees in the trawling industries was pdi’s and 40% of those were

women. The employees in the industry collectively earn approximately R428 million and 86% of

the payroll are paid to pdi’s. Centralised bargaining structures were introduced and salaries

depend on rank and the years of employment, and employees also earn commission that depends

on quantity and quality.

The demersal trawling industry is the largest and most valuable fishing industry in South Africa in

terms of capital investment, expenditure and product value. The industry accounts for

approximately 50% of the wealth generated by the marine industry with annual sales of R1.5

billion. The industry provides 75% of fresh and frozen seafood consumed by South Africans and

is therefore a very important link in South Africa’s food supply and security. Table B2 provide the

landings for the different demersal species from 1996 to 1999. Species 1996 1997 1998 1999 Hake 158 785 147 569 149 116 131 439 Sole 959 860 890 768 Kingklip 3 372 3 927 3 409 3 920 Monk 6 161 7 639 7 902 6 949 Horse mackerel 15 307 22 922 19 264 11 641 Other by-catch 19 925 19 387 20 917 13 452 TOTAL 206 505 202 304 201 498 168 169 Table B2: Total landings in metric tons for demersal species: 1996-1999 (Source: ESS Report (2), 2003)

23

B3. Hake handline 1998 handline catches is estimated at 2 500 to 3 000 tons and verifiable landings has increased to 4

500 tons. However, this figure is underreported and catches are probably around the TAC of 5 500

tons. A fisher needs a permit for handline hake. Under the old Act they could catch an unlimited

amount of fish per day, as long as they do not exceed the maximum of 10 hooks on a line. With

the promulgation of the MLRA in 1998, hake catches are restricted to a maximum of 5 hake per

day, but the ruling of the old Act remained in force. Currently there is uncertainty around the

status of the permits as the legislation in support of the MLRA is still in process.

About 2 400 fishers are directly or partly employed in the industry. Depending on the nature of the

vessel, fishers receive between R2.50 and R3.50 per kg. The handline industry is valued at

approximately R86 million (infrastructure mostly). Assuming a 5 550 ton catch, the total value of

the industry (catching, processing, freight, etc.) amounts to over R110 million.

Information on transformation in the hake handline industry is limited as the industry is not

formalised. Most operators are individual boat owners, many white people that are retrenched and

invested in their own boats. Few operators work through companies or closed corporations and

pdi’s involved in the industry are few. Black people are mostly employed on boats and their

income is irregular. Hake handline has a strong seasonality component (with catches peaking in

autumn and spring) and is dependant on weather conditions. Black workers move between boats

resulting in similar commission rates between boat owners and low social responsibility.

B4. Hake longline Longlining for dermersal species was only introduced in 1982 in South Africa and nine permits

were issued in 1983. Catches reached 5 000 tons kingklip and 1 500 tons hake during 1985 and

another six permits were issued. Kingklip catches increased to 11 370 tons in 1986, but decreased

sharply thereafter. Government introduced a 5 000 tons TAC in 1989, but stopped all demersal-

directed longlining by the end of 1990. It was only in 1994 that hake-directed longlining was

allowed again and the TAC was set at 4 000 tons for the 1994 and 1995 season and 4 400 tons for

the 1996 and 1997 seasons. After the experimental phase (1994 to 1998) the Minister allocated

permits for 6 400 tons to the experimental fisheries only, of which 6 192 tons of hake landed. In

2000, 5 250 tons was allocated initially and 4 750 tons was allocated later in the year as smaller

quota’s, mostly to new entrants. Of the initial 5 250 tons allocated, 5 256 landed and only 2 874

24

tons of the 4 750 tons later allocated was activated of which 1 774 tons landed. The allocations for

2000 were “rolled-over” to 2001. In 2000 there was 43 rights holders and 46 vessels.

Table B4 provides the number of longline landings by location for 1994 to 2001. The table shows

the geographical distribution of hake longline activity along the coast of the Western Cape. The

table also shows that hake longline landings occur predominantly in the Western Cape.

Port 1994 1995 1996 1997 1998 1999 2000 2001 Cape Town 135 71 252 401 75 178 186 70 Mossel Bay 58 28 129 60 46 261 84 28 Hout Bay 29 4 73 114 25 116 214 96 Plettenberg Bay 46 41 126 198 1 71 90 5 St Helena 16 8 22 26 2 51 156 42 Gansbaai 27 20 0 0 0 3 0 12 Kalk Baai 0 0 29 3 0 0 0 0 Knysna 0 0 0 15 1 7 0 0 Hermanus 0 10 9 0 0 1 0 0 Laaiplek 0 0 5 0 0 0 0 0 Lambert Bay 0 0 0 1 0 0 0 0 Saldanha 1 0 1 0 0 0 0 0 PE 9 0 65 73 105 179 117 39 Western Cape 321 182 711 891 255 867 847 292 Other 42 80 24 71 32 24 15 6 Total 363 262 735 962 287 891 862 298 Table B4: Number of hake longline landings by location since 1994

Source: ESS Report (2), 2003

According to the response received by the ESS report, pdi’s own 46% of the companies, 42% of

the rights are and 31% of the fishing fleet. Approximately 90% of people employed in small-scale

operations in the hake longline industry are Black and they earn 80% of total income.

B5. Traditional commercial line fisheries The Cape commercial line fishery is responsible for 95% of the South African linefish catch.

There are three sectors within the commercial line fishery namely the traditional commercial

sector, the tuna handline/pole sector and the hake handline sector. This section focuses on the

traditional species.

The levels of linefish (except snoek and yellow tail) deteriorated to dangerously low levels in the

1990’s due to poor management and enforcement and excess commercial effort in the 1980’s.

Commercial permits for line fishery was introduced in 1985. Despite heavily depleted stock at the

time, the industry survived by subsidising effort by external sources. In order to reduce cross-

subsidisation the MLRA does not allow part-time commercial activity and the Linefish

25

Management Protocol was developed in 1999 in which regulations are based on clearly defined

objectives. The Minister of the Department of Environmental Affairs and Tourism declared the

linefish resources in a state of crisis in December 2000 resulting in a reduction of the number of

vessels receiving rights. Currently there are concerns that this fishery is in jeopardy as certain

species are seriously depleted and will take a long time to recover. It has been proposed that rights

should be allocated to those depending on traditional linefish stocks for more than 75% of their

income. The recommended TAE for the traditional line fishery for 2005 is 3 450 crew and 756

vessels. (ESS Report (2), 2003 and CAF Meeting, 2004)

The ESS Report covered about 69% of the active commercial line fishers and estimated that 26%

of permit holders are pdi’s. Permit holders are mostly white men owning their own boats. Total

employment amount to 4 100 people of which 82% are pdi’s, earning 75% of the wages. There is

a substantial difference between the wages earned by white and pdi skippers (skilled labour). This

may be due to the fact that many white men operate their own boat.

B6. Midwater trawl Midwater trawl fishery targets horse mackerel. There is little information available on horse

mackerel as it is low-priority for research. It is believed that the stock is limited and TAC

estimates are only “Upper Precautionary Catch Limits” (ESS Report (2), 2003: 143). There is no

defined management plan for the industry though such is plan is needed to direct the nature of the

industry and the behaviour of the participants.

Horse mackerel was mostly caught by foreign fleets in the 1970’s, but these fleets withdrawn from

the South African waters in 1978 (the Japanese fleet withdrawn only in 1992). The absence of the

foreigners encouraged South African initiatives and the first quota’s for midwater trawl was

allocated in 1990 with the formation of the South African Midwater Trawling Association. The

quota’s was allocated to nine companies, allowing each vessel to catch 2 000 tons. There was a

steady increase in the number of right holders in the nineties and the number peaked at 18 in 1998

and 1999. There were 14 right holders in 2000 and 2001. There are a few new entrants, but

apparently they sell there allocations for between 50 cent (1997) and R1.20 (2001) per kg. Horse

mackerel does not contribute much to employment, as the few vessels targeting horse mackerel

employs about 70 people. All of the employees on the South African vessels are pdi’s.

26

Midwater trawling is capital intensive (as is suggested by the low employment figures) and have

low profit margins. Catching costs varies between R2.00 and R2.50 per kg and the landed price

varies between R2.50 and R3.20 per kg, leaving a profit of between R0 and 70 cents per kg. Horse

mackerel is directed at large volume low value African markets.

B7. Pelagic The pelagic industry started in South Africa in the Western Cape after the Second World War. 60

to 90 percent of the pelagic industry in South Africa consists of pilchard and anchovy. The ratio

between pilchard and anchovy landings, however fluctuated over the decades. Pilchard landings

averaged around 116 000 tons between 1951 and 1958 and peaked at 410 000 tons in 1962.

Thereafter catches dropped to below 100 000 tons until 1995 (except for 1968, 1972 and 1976).

The industry shifted its focus to anchovy in 1965 and anchovy landings reached almost 600 000

tons in 1988. At that time anchovy accounted for over 80% of total pelagic landings. Since then

anchovy landings reached a low of 40 000 tons in 1996. (ESS Report (2), 2003) However, 2001

and 2002 were booming years in the pelagic industry as total catch exceed half a million tons. In

2001 and 2002, 535 000 and 538 000 tons of small pelagic fish landed in South Africa

respectively. This increase is due to both an increase in pilchard and anchovy catches. The former

amounted to 261 000 tons in 2002, up from 192 000 tons in 2001. This increase reflect a shift

towards targeting pilchards, as well as the healthy state of the pilchard stock. Figure B7.1 shows

the total catches of pelagic fish for selected years. The fluctuations in total landings is due to the

large fluctuations in the abundance of the fish, which is a result of the short-livedness of pelagic

fish. (Kleinschmidt, 2003)

Figure B7.1: South African pelagic catches for selected years

Source: Fishing Industry Handbook, 2003

0

100000

200000

300000

400000

500000

600000

1958

1968

1978

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

*

Tons

Pilchard Mackerel Anchovy Redeye/Round herring

27

Numerous management restriction were introduced since 1951 and include a closed season, a

global quota and other restrictions on fleet hold capacity. In 1990 the government allocated an

average catch right of 4 000 tons to each boat, based on a TAC of 300 000 tons. The pilchard

allocations were granted to 12 companies in 1990, but in 2000 the number of rights holders

increased to 107. 48% of the 107 right holders are new entrants from previously disadvantaged

communities. The number of right holders for anchovy was 10 in 1990, but increased to 51 in

2000. The majority of the 41 new entrants are from previously disadvantage communities. These

transformations resulted in the establishment of a number of small companies.

The pilchard and anchovy species are well researched and stock management surveys are carried

out twice a year. The TAC for the next year is then based on survey results. One of the

characteristics of the pelagic industry is the large fluctuations in the TAC and this make small

companies extremely vulnerable. Another distinct characteristic of the pelagic industry is that all

fish landed has to be processed into another form. Pilchard is canned for human consumption

while anchovy and round-herring are used for fishmeal. The pelagic industry supports 8 fishmeal

plants, 6 canning factories, more than 40 bait packing facilities and 65 to 68 purse-seine vessels.

The industry employs 5 300 people on a full-time basis, 2 500 people on a part-time basis, 700

fishermen and 2 400 indirect jobs via support services (ESS Report (2), 2003 and Kleinschmidt,

2003). According to the ESS Report 19% of companies are owned by Whites, 28% by Blacks and

53% are unknown. Similarly, Whites own 21% of the rights, Blacks 26% and the 53% is

unknown. The ESS Report received employment data from 84.5% of the active vessels and

concluded that 92% of the 5 275 employees are pdi’s, earning 76% of the annual wages. 78% are

employed in the Western Cape.

B8. South coast rock lobster The fishery commenced in 1974 and foreign fleets participated until 1976. Catches and catch rates

collapsed between 1979 and 1981 resulting in a reduction of effort and consequently catches. This

allowed the stock to recover during the eighties. TAC was introduced at 450 tons (tail mass) in

1984 and was increased to 477 tons from the 1990/1 to 1993/4 seasons. The annual TAC was

gradually reduced to 365 tons in the 2000/1 season due to declining biomass. Despite declining

TAC, fishing effort has increased in recent years. The industry is now controlled by both TAC and

total applied effort (TAE). The quota holder must stop its activities when either of the quota’s are

filled. The recommended TAC for the 2004/2005 season is 382 tons, a 9% increase from the

28

previous season. This increase is in line with the cpue increase. It is recommended that the TAE

should increase from 2 038 sea-days to 2 089 sea-days (subject to change if vessels are

substituted). (ESS Report (2), 2003 and CAF Meeting, 2004)

The majority of the lobster products are exported to the US, Europe and the Far East and the price

depends on demand and supply conditions in the foreign country as well as the exchange rate.

Fees and levies are payable in the industry.

There were 13 fishing boats in the industry in the 2000/1 season and 19 rights holders.

Transformation in the industry is difficult as new entrants are dependent on the existing fishing

boats to activate their rights. The South coast rock lobster industry is capital-intensive and

requires large rights to be economical viable. Another problem is the declining biomass of

resources which make it difficult to allocate large quota’s. The rights of pdi’s are often sold to the

established companies. However, a few small new entrants managed to put their rights together

and bought a fishing vessel which is active in the industry. The ESS Report covered about 65% of

the fishery and found that Blacks own 69% of the rights and 79% of the fleet. 94% of the people

employed are Black, earning 86% of total income.

B9. Shark longline Sharks are mainly caught as a by-catch in other industries such as the deep-sea trawl hake industry.

The only shark directed fishery is the shark longline sector. There were 31 permit holders between

1991 and 1994, 35 in 1995 and 23 in 2001 to 2004 of which only 8 are active in the 2004 season.

No effort or catch quota’s are enforced. (ESS Report (2), 2003) The price of shark fins is rising

dramatically internationally and South African catches reached 300 tonnes in June 2004 and is

expected to reach 600 tons in December. So as a precautionary measure against increased effort,

the CAF recommends that the number of rights holders should be reduced to 10 vessels for 2005

(CAF Meeting, 2004).

The history of shark catches date back to 1934, but the fishery never received much attention as

there are too many other competing marine resources. Exports of shark products increased from

141.52 metric tons in 1990 to 248.36 metric tons in 1995. The rand value of exports was R378

545 in 1990 and R1 081 434 in 1995 (the exchange rate depreciated from R3.65/$ to R4.50/$

during this period). The main destinations of shark exports are Australia, Greece and Italy.

29

Total shark catches in 1994 was 2 044 tons and 1 724 tons in 1995. Prices ranged between

R430/ton (shark caught bay trawl) to R2 500/ton (line and longline catches). The total value of

sales was R 1 509 000 for 1994 and R1 298 000 for 1995. Shark fisheries are profitable in the way

it is operated currently, that is catching sharks as a by-catch or targeting sharks in the off-season of

the main activity.

Since sharks are mainly caught as a by-catch in other industries, there are no clear management

objectives for the exploitation of sharks (except for the limited number of permit holders).

However, the integration of the tuna and shark longline sectors are considered, since the two

fisheries use identical gear and have similar by-catches (ESS Report (2), 2003). A policy has been

drafted to consolidate all commercial large pelagic longline fisheries, thus commercial harvesting

fo pelagic shark longline will not be allowed after 31 December 2005 (CAF Meeting, 2004).

B10. Squid Chokka squid used to be caught for bait for sport linefishers, but in 1984 it was realised that squid

exports may be a profitable business. Squid are either caught by jigging or as a by-catch. The

latter makes out a very small proportion of total catch. The highest catch was reported in 1989 at 9

800 tons. The industry is managed by a closed season in October/November (four weeks), a

limited number of right holders (160 in 2000) and a total applied effort limit. Stock assessment is

annually done in September and the TAE is determined according to the results.

The fishery provides employment to roughly 2 500 people and generates more than R180 million

per year. The ESS Report found that 14% of company ownership are in the hands of pdi’s, 38% in

the hands of White people and the remaining 48% could not be determined (100% coverage of

active participants in the chokka squid industry). These figure translate into 16% if rights in the

hands of pdi’s and 36% owned by Whites. 91% of the people employed are pdi’s and they earn

80% of the total income (feedback received from 87.5% of the vessels and 12 squid

processing/packing facilities). The majority of the workforce are semi-skilled pdi’s, earning less

than R30 000 per year. The Western Cape employs 11% of the workforce in the chokka squid

industry.

B11. West coast rock lobster West coast rock lobster stocks are heavily depleted because of large unsustainable catches in the

first half of the twentieth century, and because of a slow-down in the somatic growth rate of

30

individual lobsters over the past 10 years. The Sea Fisheries Advisory Committee adopted a

resource management strategy in 1997 with the aim of increasing biomass with 20% between 1997

and 2006. A TAC was introduced in the early 1980’s. At that time utilisation stabilised at 3 500

to 4 000 tons per annum. With the slow-down in growth rates the TAC was gradually reduced in

the nineties, reaching a low of 1 500 tons in 1995 and 1996. The TAC for 2000 and 2001 was 1

614 tons. Other control strategies include a minimum size, a closed winter season and a daily bag

limit for recreational fishermen. The global TAC was 2 018 tons for the 2000/1 season of which

230 tons were for subsistence fishing, 174 tons for recreational fishing and the remaining 1 614

tons for commercial fishing. After consulting with the scientists the CAF recommends a TAC of 3

527 tons (320 tons for recreational take and 3 207 tons commercial sector) for the 2005 season, an

increase of 321 tons from the previous season. (ESS Report (2), 2003 and CAF Meeting, 2004)

The commercial industry employs 1 300 seasonal and full-time workers in the catching

component. There are currently 226 quota holders as opposed to the 39 holders in the late 1980’s.

199 of 226 holders are small quota holders (less than 10 tons) receiving 40% of the 1 614 tons

allocated, 18 are medium quota holders (10 to 40 tons) receiving 25% of the TAC, and 9 are large

quota holders (>40 tons), receiving 35% of the TAC. 58% of the small holders are pdi’s, 41% of

the medium holders and 76% of the large holders.

The processing component employs 2 800 people, but the factories operate below the optimum

level as a result of the reduction in TAC. At full capacity the factories can process up to 4 000

tons of TAC without any further capital investment. A further reduction in the TAC or changes in

the allocation of the TAC may result in job losses.

The ESS Report estimates that the west coast rock lobster industry provides employment for

approximately 4 400 people of which 95% of the employees are pdi’s, earning 87% of total

income. (These latter two figures are based on a 50% sample of the vessels and a 90% sample of

processing companies.)

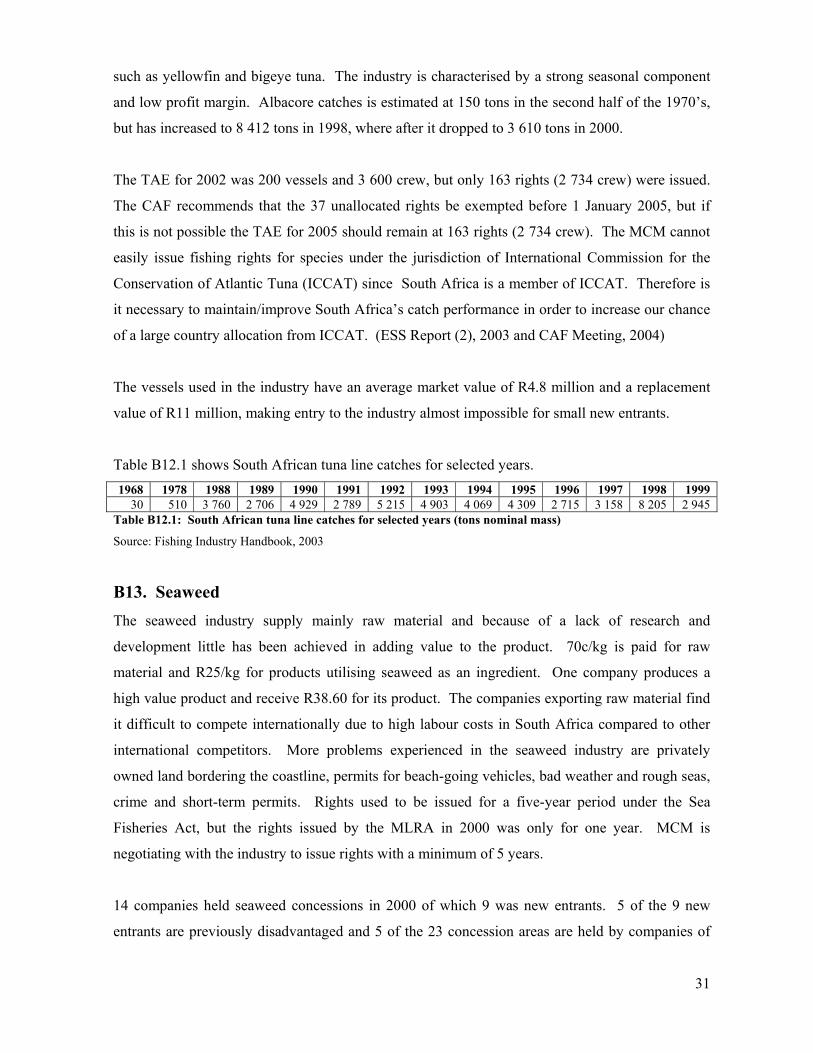

B12. Tuna Tuna was already discovered in 1860 in South African waters, but the commercial tuna industry

only started in 1960. Today there exists four distinct fisheries in the South African tuna fishery:

the tuna sport fishery, the baitboat fishery, the pelagic longline fishery and the foreign pelagic

longline fishery. The baitboat fishery targets albacore for canning and by-catch include species

31

such as yellowfin and bigeye tuna. The industry is characterised by a strong seasonal component

and low profit margin. Albacore catches is estimated at 150 tons in the second half of the 1970’s,

but has increased to 8 412 tons in 1998, where after it dropped to 3 610 tons in 2000.

The TAE for 2002 was 200 vessels and 3 600 crew, but only 163 rights (2 734 crew) were issued.

The CAF recommends that the 37 unallocated rights be exempted before 1 January 2005, but if

this is not possible the TAE for 2005 should remain at 163 rights (2 734 crew). The MCM cannot

easily issue fishing rights for species under the jurisdiction of International Commission for the

Conservation of Atlantic Tuna (ICCAT) since South Africa is a member of ICCAT. Therefore is

it necessary to maintain/improve South Africa’s catch performance in order to increase our chance

of a large country allocation from ICCAT. (ESS Report (2), 2003 and CAF Meeting, 2004)

The vessels used in the industry have an average market value of R4.8 million and a replacement

value of R11 million, making entry to the industry almost impossible for small new entrants.

Table B12.1 shows South African tuna line catches for selected years. 1968 1978 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

30 510 3 760 2 706 4 929 2 789 5 215 4 903 4 069 4 309 2 715 3 158 8 205 2 945 Table B12.1: South African tuna line catches for selected years (tons nominal mass)

Source: Fishing Industry Handbook, 2003

B13. Seaweed The seaweed industry supply mainly raw material and because of a lack of research and

development little has been achieved in adding value to the product. 70c/kg is paid for raw

material and R25/kg for products utilising seaweed as an ingredient. One company produces a

high value product and receive R38.60 for its product. The companies exporting raw material find

it difficult to compete internationally due to high labour costs in South Africa compared to other

international competitors. More problems experienced in the seaweed industry are privately

owned land bordering the coastline, permits for beach-going vehicles, bad weather and rough seas,

crime and short-term permits. Rights used to be issued for a five-year period under the Sea

Fisheries Act, but the rights issued by the MLRA in 2000 was only for one year. MCM is

negotiating with the industry to issue rights with a minimum of 5 years.

14 companies held seaweed concessions in 2000 of which 9 was new entrants. 5 of the 9 new

entrants are previously disadvantaged and 5 of the 23 concession areas are held by companies of

32

pdi’s – this represent 30% of the resources on a biomass basis. Pickers of seaweed are usually

Black females, while white males dominate the professional and managerial positions. Employees

are mostly employed on a permanent part-time or casual basis. The majority of the companies

offer some skills development programme to their employees. The ESS Report received feedback

from 11 of the 14 companies (79% coverage) and found that 40% of the seaweed concessions were

owned by White people, 20% by Black people and the remaining 40% by joint ventures or other

shareholding structures. The 11 companies and subcontractors employ 313 workers, of which 92%

are pdi’s earning 77% of total income. Beside the 313 formal employees the companies employ 1

450 casual workers during certain times of the year. All of these are pdi’s. The majority of

workers are unskilled earning less than R20 000 a year.

33

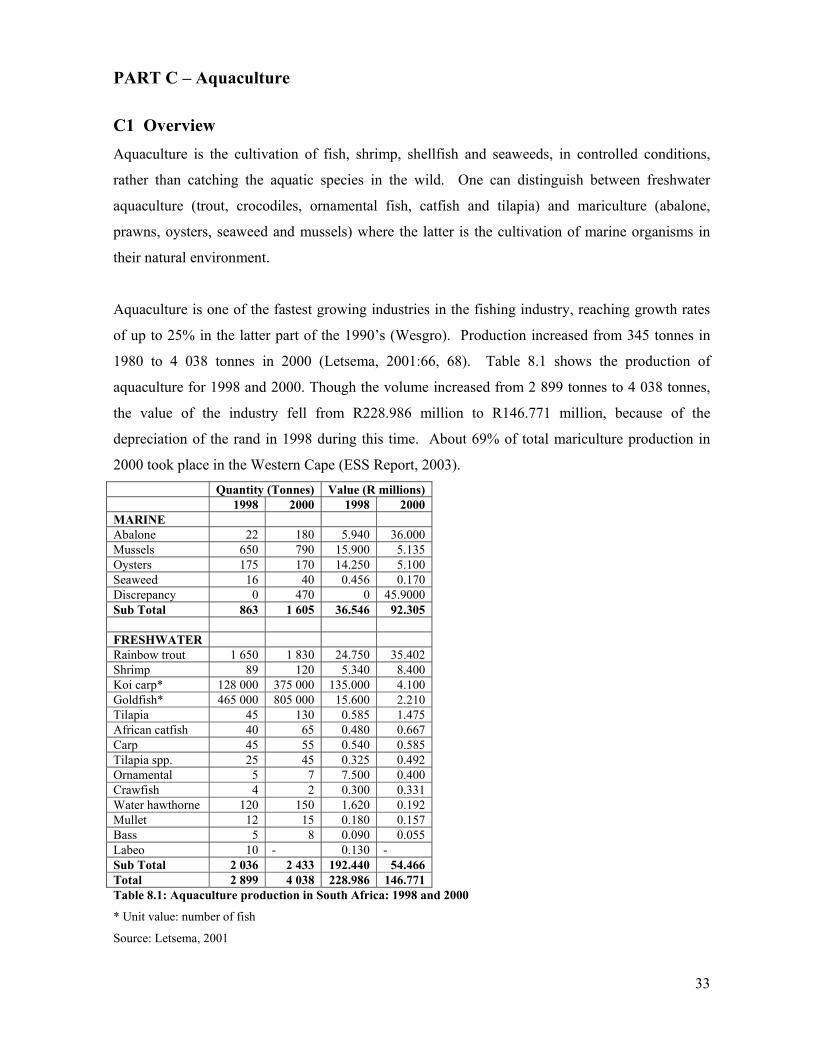

PART C – Aquaculture C1 Overview Aquaculture is the cultivation of fish, shrimp, shellfish and seaweeds, in controlled conditions,

rather than catching the aquatic species in the wild. One can distinguish between freshwater

aquaculture (trout, crocodiles, ornamental fish, catfish and tilapia) and mariculture (abalone,

prawns, oysters, seaweed and mussels) where the latter is the cultivation of marine organisms in

their natural environment.

Aquaculture is one of the fastest growing industries in the fishing industry, reaching growth rates

of up to 25% in the latter part of the 1990’s (Wesgro). Production increased from 345 tonnes in

1980 to 4 038 tonnes in 2000 (Letsema, 2001:66, 68). Table 8.1 shows the production of

aquaculture for 1998 and 2000. Though the volume increased from 2 899 tonnes to 4 038 tonnes,

the value of the industry fell from R228.986 million to R146.771 million, because of the

depreciation of the rand in 1998 during this time. About 69% of total mariculture production in

2000 took place in the Western Cape (ESS Report, 2003). Quantity (Tonnes) Value (R millions)

1998 2000 1998 2000 MARINE Abalone 22 180 5.940 36.000 Mussels 650 790 15.900 5.135 Oysters 175 170 14.250 5.100 Seaweed 16 40 0.456 0.170 Discrepancy 0 470 0 45.9000 Sub Total 863 1 605 36.546 92.305 FRESHWATER Rainbow trout 1 650 1 830 24.750 35.402 Shrimp 89 120 5.340 8.400 Koi carp* 128 000 375 000 135.000 4.100 Goldfish* 465 000 805 000 15.600 2.210 Tilapia 45 130 0.585 1.475 African catfish 40 65 0.480 0.667 Carp 45 55 0.540 0.585 Tilapia spp. 25 45 0.325 0.492 Ornamental 5 7 7.500 0.400 Crawfish 4 2 0.300 0.331 Water hawthorne 120 150 1.620 0.192 Mullet 12 15 0.180 0.157 Bass 5 8 0.090 0.055 Labeo 10 - 0.130 - Sub Total 2 036 2 433 192.440 54.466 Total 2 899 4 038 228.986 146.771 Table 8.1: Aquaculture production in South Africa: 1998 and 2000

* Unit value: number of fish

Source: Letsema, 2001

34

The mariculture industry in South Africa employed 678 people in 2000 of which the majority are

unskilled Black workers. Table 8.2 shows the employment statistics for the South African

mariculture industry in 2000. It is clear that White people are employed in the higher skilled jobs,

but this is a result of the nature of the mariculture industry at present. Running a fish farm requires

a relatively high level of technical skills and these skills are resident in the higher educated white

population. (ESS Report (2), 2003)

Total income earned in the mariculture industry amounted to R22.35 million in 2000. The average

monthly salary for professional staff, skilled workers, middle services, semi-skilled and unskilled

labourers were approximately R8 825, R5 170, R3 950, R2 300 and R1 500 respectively. The

difference in income earned between white and other population groups was 22.5% in the middle

services and semi-skilled groups and 57% in the skilled group (ESS Report (2), 2003: 302).

Sub-total Professional Skilled Middle services Semi-skilled Unskilled Total

Black White Black White Black White Black White Black White Black White Abalone 418 344 74 0 32 2 10 24 24 62 4 256 4 Oyster 132 115 17 0 15 0 0 0 2 15 0 100 0 Mussel 17 15 2 0 1 0 0 0 1 2 0 13 0

Seaweed 11 8 3 0 1 0 0 0 2 0 0 8 0 Finfish 2 2 0 0 0 0 0 0 0 0 0 2 0 Prawns 98 N/a 10 23 3 23 39 Total 678 59 35 56 106 422

Table 8.2: The employment structure of the South African mariculture industry in 2000

Source: ESS Report (2), 2003

C2 Abalone There are 15 commercial abalone farms in South Africa and more sites are investigated (Brink,

2003). A medium size farm produce around 35 tons per annum. Total farm production for 2002

was 500 tons, giving a gross production of R150 million (Aquaculture Sector Study, 2002).

Approximately 80% of total abalone production occurs in the Western Cape (Wesgro, 2004).

South African abalone is very popular in the Far East and main export destinations include China,

Hong Kong, Taiwan and Japan. SA exported 70 tons as canned product in 2003, and the rest

mainly as live abalone (Brink, 2003 and Gerber, 2004). H.midae (the specie cultivated in South

Africa) were sold for US$56-52 per kg on the Tokyo Central wholesale market in December 2003.

35

Key risks in abalone farming include water quality, mortalities and infestations. These risks are

minimised by good farm management which requires expertise in abalone farming. Site selection

is another important success factor. (Aquaculture Sector Study, 2002)

C3 Kelp Kelp is harvested by picking it up from the beach or shallow waters or by divers operating from

small vessels. A team operating on the beach consists of 6 to 8 people. The kelp is removed to a

location inland where it is dried and milled. The milled product is transported to Cape Town from

where it is exported to alginate plants abroad. The price for dried kelp was US$300 per ton in

2000. Kelp has numerous uses including food, paper, textiles, welding rods, pharmaceuticals,

fertilizer, animal feed, and food for abalone.

The kelp industry is managed by a system of concessions. These concessions are issued for short

periods and do not necessarily flow into each other resulting in kelp rotting on the beach. Another

problem making development projects difficult is the expertise required to market the product.

The world markets are highly erratic and new entrants with a lack marketing expertise should link

or collaborate with established businesses. (Aquaculture Sector Study, 2002)

C4 Mussels There are two mussel producers in South Africa. They produced approximately 1000 tons in 2003

of which 39% go back into the see for the next production cycle and the remaining 61% is

marketed in South Africa. The 61% is distributed as follows: 25% is marketed as fresh mussels,

5% is marketed directly, and 70% is delivered for processing. South Africa is a net importer of

mussels as only 45% of consumption in South Africa is produced locally. (Diza and Karaan,

2004)

Saldanha is very suitable for mussel farming, because the good water quality and the nutrient rich

Benguella current result in high mussel growth rates and good mussel quality. Saldanha also has a

large sheltered bay and the risk of red tides are low and well monitored. Despite these many

advantages of Saldanha, site selection remains an important factor for success. (Aquaculture

Sector Study, 2002) The Western Cape accounts for 85% (2 000 tons) of cultivated black mussel

production in South Africa (Wesgro, 2004).

36

There are several factors making it difficult for small farmers to enter the mussel industry. These

factors include:

• High start-up costs and asset specificity;

• Information constraints about technology, production techniques, marketing channels and

processing services;

• Variable size and quality of mussels making it difficult to penetrate niche markets.

(Aquaculture Sector Study, 2002)

C5 Oysters The oyster industry has proven to be profitable and expanded over the last few years. Production

was 175 metric tons in 1998 and increased to 250 metric tons in 2003. The value of production in

2003 was R1.6 million (Brink, 2003). The Western Cape produce 86% of total production of

cultivated oysters with an ex-farm income of R7 million (Wesgro, 2004). Oyster production is

clustered in the Knysna lagoon, but production also occurs at Saldanha Bay, St Helena Bay, Port

Nolloth and St Francis Bay. There are nine producers of which South Cape Oysters in Knysna is

the most successful producer. The marketing of oysters is limited to the local market as South

Africa is a net importer of oysters. The oyster industry is conducive to economic development and

empowerment (Aquaculture Sector Study, 2002).

C6 Seaweed The total seaweed industry in South Africa is valued at about R18 million and employed around

400 people in 1995 (Aquaculture Sector Study, 2002). Commercial production of seaweed started

in 1998 with a production of 16 metric tons. 48 tons were produced in 2003 with a value of

R0.265 million (Brink, 2003). Seaweed are collected for export and processing and is used as

food, food supplements or fertilizer.

The seaweed industry has the potential to provide work for the impoverished coastal communities

at the West Coast and to boost the local economy. The first community project was started in 1996

at St Helena Bay by the University of the Western Cape. Funds were obtained from the West

Coast Investment Initiative to write a business plan and register a private company. (Aquaculture

Sector Study, 2002)

37

C7 Trout Commercial production of trout already started in the 1960’s and increased from 1 000 metric tons

to 1 750 metric tons per annum. The 1 750 metric tons produced in 2003 is worth R44 million.

The industry is expected to grow by 2 to 3 percent per annum. Smaller producers have fallen away

through the years, leaving only the larger producers that benefit from economies of scale. 14 of

the 35 farms are located in the Western Cape, producing 450 tons trout. The trout produced is

either used as live fish for sport fishery or for food.

The trout industry provides about 220 direct jobs on the level of production and 200 indirect jobs

involved in processing. There are 8 processors, marketing their products almost exclusively to the

South African market. The trout industry is stable, despite competition form substitute imported

products such as Pacific and Atlantic salmon. (Brink, 2003)

The Division of Aquaculture of Stellenbosch University has helped to establish about 5 small

aquaculture farmers in the Western Cape, and there is enormous potential to establish more farms

in the Western Cape. Small scale aquaculture is very risky and the farms are vulnerable to, among

others, fluctuations in the interest rate as capital are usually borrowed funds, inflation as fish food

is very expensive, losses of fingerlings during transport and theft. The lack of technical and

business experience is another problem for small farmers. (Aquaculture Sector Study, 2002)

C8 Other Other species cultivated in South Africa include marron (freshwater lobster), Atlantic salmon, eels,

crocodiles and ornamental fish. The cultivation of these species are however still in the initial

phase. For example, there is only one producer of Atlantic salmon and the development of a

sustainable eel aquaculture sector is still in the planning phase. SA Eels Pty (Ltd) is planning to

develop four eel farms over the next two years in the Western Cape, Eastern Cape and

Mpumulanga. The total value of this production is estimated at R42 million and the project is

expected to create 60 permanent jobs and 160 indirect jobs in the processing sector.

38

PART D

SUMMARY OF FISHING IMBIZO’s by Minister Marthinus van Schalkwyk

Saldanha Bay, Hermanus & Woodstock August 2004

Undertakings by the Minister:

1. Access to the sea for all

2. Simplified application forms

3. Departmental officials will be trustworthy, transparent and monitored

4. Provisional lists will be published to verify that applicants are fishers

5. Training will be offered so all applicants understand the process of submission and

adjudication

6. Extension granted to successful lobster appeals till end September to catch males only

7. Long term rights will be considered with the next round of quotas

8. Cost of quota applications will be taken under consideration

Issues raised by Fishers:

1. The plight of line fishers who are increasingly marginalized

2. The dilemma of line fishers versus recreational fishers

3. A need to consider all fisheries as commercial vis a vis limited commercial and subsistence

4. The problem of retired or handicapped fishers who loose rights as a result

5. Similarly, the problems of fishers with rights who cannot fish due to e.g. illness but are

unable to transfer their rights albeit temporarily to assistants

6. Identification of real fishers on whom to confer rights, as opposed to opportunists who

attain rights at their expense

7. The need to co-manage resources with communities

8. Incessant call for transparency in the allocation and adjudication process

9. The viability of recreational line fish (i.e. 10 fish per person) is questionable

10. Permits do not take the viability of boats into consideration and the multi-specie allocation

per boat must be encouraged

11. The lack of women participation must be addressed and promoted with hard targets

39

12. The Department should make careful assessments of the type of boats used as Rubber boats

are in some instances more appropriate

13. Seasons should be set more strictly according to the biological requirements of species, not

merely administratively

14. African participation in Fishing remains neglected and under-represented

15. The restrictions placed on sale of linefish (recreational) by especially subsistence fishers

constrain the viability

16. Rights are allocated to boat owners which marginalizes the crew who are the real fishers,

but retain little rights

17. Quotas are linked to individuals linked to specific boats, and hence boat owners are placed

in a monopolistic position

18. A need to look more seriously into the availability of suitable infrastructure e.g. fish

markets, slipways and small processing

19. Longer term quotas are preferred

20. The need decentralise administrative measures such as applications, licensing, etc.

21. A general call to hold large corporates more responsible for BEE, catches and social

responsibility

22. Consideration be given to return to lobster rings because traps cause much mortality and

losses of especially juveniles

23. Some unions support corporates where they have their members, and not fishers.

24. Policing measures are more focused on smmes and not equally applied to large companies

25. Community members were in instances promised rewards when collaborating with

government in policing efforts, but these were not honoured

26. Some officials in the department are not adept at handling requests or honouring responses

27. Not all bogus applications are detected in the verification process

28. There is an impression that negotiations with large companies occur behind closed doors

29. Communities or fishers are often prompted into joint ventures but lack the necessary

business skills to contend at this level, and remain marginalized in decision-making and

business processes