Embed Size (px)

Citation preview

© App Annie & BIU 2015

The Mobile Gaming Landscape in Germany Gamescom Special Report

Table of Contents 1. Freemium Gaming Dominates

Germany’s App Economy

2. Google Play Drives Mobile Gaming in

Germany

3. Strategy and Casual Games Lead the

Way in Germany

4. The United States Leads Germany’s

Game Exports

USE RESTRICTIONS: The information, materials, data, images, graphics, and other components of this report ("Report") are copyrighted and owned or controlled by App Annie unless otherwise noted. Unauthorized use of the Report may violate copyright, trademark and/or other intellectual

property rights of App Annie and may give rise to a claim for damages and/or be a criminal offense. The Report may not be modified, copied, distributed, republished, uploaded, posted,

decompiled, or transmitted in any way, without the prior written consent of App Annie.

© App Annie & BIU 2015

Key characteristics of the mobile gaming

landscape in Germany

• Games are responsible for 75% of app store revenue in Germany’s app economy.

• Freemium is by far the dominant business model for games in Germany, contributing

around 95% of games revenue.

• In Germany’s mobile games market, Google Play continues to pull ahead of the iOS

App Store with a 60% share of games revenue and a 75% share in games

downloads.

• When compared to the rest of the world, mobile gamers in Germany spend large

amounts of money on Strategy and Casual games.

• In Q2 2015, approximately one third of the revenue earned by German companies’

mobile games came from the United States, making it the biggest market for German-

made mobile games.

• A major growth opportunity for German mobile game companies lies in Asia-Pacific’s

largest markets, where German-made games are currently underrepresented.

1. Freemium Gaming Dominates Germany’s App Economy

© App Annie & BIU 2015

Germany is the 7th largest market for combined

iOS App Store & Google Play revenue

0

25

50

75

100

Japan United

States

China South

Korea

United

Kingdom

Taiwan GermanyAustralia Canada France

Ind

exe

d R

eve

nu

e

Combined iOS App Store & Google Play Game Revenue, Q2 2015

• Germany is the second largest market for mobile gaming revenue in Europe, making it a

strong opportunity for growth and a leading candidate for game localization.

© App Annie & BIU 2015

0%

25%

50%

75%

100%

Q2 2013 Q2 2014 Q2 2015

Share

of A

pp

Sto

re R

eve

nue

Games Share of App Store Revenue, Germany

iOS App Store Google Play

Games drive revenue in Germany’s app economy

• Approximately 75% of combined iOS App Store and Google Play revenue in Germany

came from games in Q2 2015. This proportion is below the worldwide average.

• On Google Play, the contribution of games grew to reach almost 90% in Q2 2015.

• In contrast, the iOS App Store saw an increasing proportion of revenue from apps outside

games between Q2 2014 to Q2 2015.

© App Annie & BIU 2015

0% 25% 50% 75% 100%

South Korea

Japan

United States

Germany

United Kingdom

Worldwide

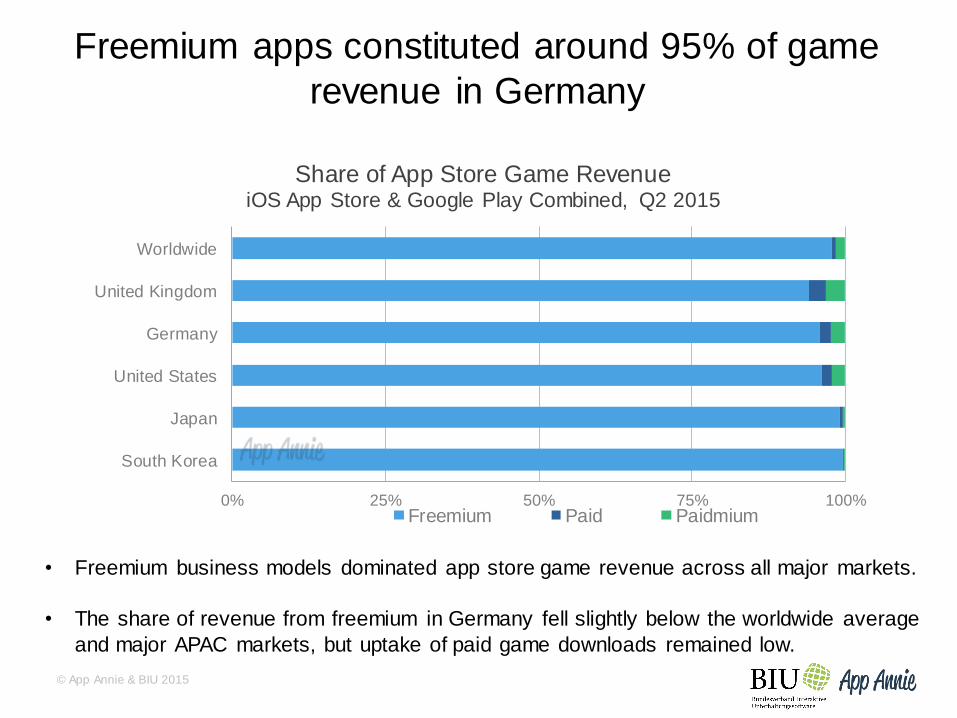

Share of App Store Game Revenue iOS App Store & Google Play Combined, Q2 2015

Freemium Paid Paidmium

Freemium apps constituted around 95% of game

revenue in Germany

• Freemium business models dominated app store game revenue across all major markets.

• The share of revenue from freemium in Germany fell slightly below the worldwide average

and major APAC markets, but uptake of paid game downloads remained low.

2. Google Play Drives Mobile Gaming in Germany

© App Annie & BIU 2015

0

50

100

150

200

Q2 2013 Q2 2014 Q2 2015

Ind

exe

d R

eve

nu

e

Quarterly Games Revenue, Germany

iOS App Store Google Play

Google Play game revenue in Germany

grew 5x over 2 years

• In Q2 2015, combined iOS App Store and Google Play game revenue in Germany was

approximately 2.2x larger than it was 2 years earlier.

• The gains in game revenue were primarily driven by Google Play, which accounted for

around 60% of game revenue from the two app stores in Q2 2015.

© App Annie & BIU 2015

0

50

100

150

200

250

Q2 2013 Q2 2014 Q2 2015

Ind

exe

d D

ow

nlo

ad

s

Quarterly Games Downloads, Germany

iOS App Store Google Play

Google Play accounted for around 75% of Q2

2015 game downloads in Germany

• Google Play’s share of downloads continued to grow over the last two years.

• It is therefore likely that Google Play will maintain or grow its lead in game revenue in the

medium-term future.

• However, the iOS App Store continued to monetize game downloads at a higher rate than

Google Play.

3. Strategy and Casual Games Lead the Way in Germany

© App Annie & BIU 2015

0%

25%

50%

75%

100%

Germany Worldwide

Sha

re o

f A

pp S

tore

Re

ve

nue

Google Play Games Revenue by Subcategory, Q2 2015

Other

Casual

Strategy

The Strategy and Casual subcategories

dominated games revenue in Germany

• The Strategy and Casual subcategories together contributed over half of Google Play game

revenue in Germany, led by Supercell’s Clash of Clans and Hay Day, respectively.

• Strategy was also the leading subcategory for iOS game revenue in Germany in Q2 2015.

© App Annie & BIU 2015

Top Games, iOS App Store & Google Play Combined

Germany, Q2 2015

Rank By Downloads By Revenue

Game Company Game Company

1 aa General Adaptive

Apps Clash of Clans Supercell

2 94% SCIMOB Hay Day Supercell

3 Clash of Clans Supercell Candy Crush Soda Saga King

4 Candy Crush Soda Saga King Candy Crush Saga King

5 QuizClash FEO Media Empire: Four Kingdoms Goodgame Studios

6 Subway Surfers Kiloo Game of War – Fire Age Machine Zone

7 Crossy Road HIPSTER WHALE Farm Heroes Saga King

8 Criminal Case Pretty Simple Castle Clash IGG

9 Candy Crush Saga King Clash of Kings Elex Technology

10 AlphaBetty Saga King Summoners War GAMEVIL

• International gaming heavyweights Supercell and King hold a strong grip on the revenue

charts, and their continued presence in the downloads charts bodes well continuing success.

• Despite only holding two places in downloads, strategy games held five places in revenue.

Strategy titles shown in blue

A game was considered a strategy title if its Google Play category was Strategy and at least one of its iOS categories was Strategy.

© App Annie & BIU 2015

Top Games Companies, iOS App Store & Google Play Combined

Germany, Q2 2015

Rank By Downloads Headquarters By Revenue Headquarters

1 General Adaptive Apps Supercell

2 King King

3 Electronic Arts Electronic Arts

4 Gameloft IGG

5 XPEC Elex Technology

6 SCIMOB GAMEVIL

7 Supercell Goodgame Studios

8 Doodle Mobile Kabam

9 TabTale Gameloft

10 Rovio Activision Blizzard

• Publishers from APAC feature prominently in the top revenue charts, driven primarily by

massively multiplayer online (MMO) real-time strategy and role-playing games such as

Castle Clash, Clash of Kings and Summoners War.

4. The United States Leads Germany’s Game Exports

© App Annie & BIU 2015

Top German Games Companies

iOS App Store & Google Play Combined, Q2

2015

Rank By Downloads By Revenue

1 Bertelsmann Goodgame Studios

2 FDG Entertainment Bertelsmann

3 LOTUM Wooga

4 Wooga InnoGames

5 Nenoff flaregames

6 Goodgame Studios XYRALITY

7 Tivola ProSeibenSat.1 Media

8 InnoGames LOTUM

9 HandyGames FDG Entertainment

10 Kamibox USM Games

• Bertelsmann’s strong performance in Q2 2015 was boosted by the release Jurassic

World™: The Game from subsidiary Ludia, demonstrating the value of strong IP in mobile

games.

• Publishers of strategy MMOs based in Germany such as Goodgame Studios, InnoGames

and flaregames found revenue success in the worldwide mobile gaming market.

© App Annie & BIU 2015

The US and Europe drive downloads of German apps

Combined iOS & Google Play Downloads Distribution German Companies, Q2 2015

Legend

All other countries

5% 10%

20%

• A high proportion of downloads for German companies are sourced from developed Western markets,

including the US, Germany and France. • Opportunities in rapidly rising Google Play-dominated markets such as Turkey have yet to be fully

capitalized on.

© App Annie & BIU 2015

Combined iOS & Google Play Revenue Distribution German Companies, Q2 2015

All other countries

Legend

10% 20%

35%

• While the US leads revenue generation for German publishers, relatively little revenue is sourced from

the huge mobile gaming markets in Japan, China and South Korea. • For those that can establish themselves, APAC markets may represent a huge opportunity for expansion,

particularly for publishers with experience in MMO genres that have proved popular in the region.

APAC is an untapped opportunity for German

companies

© App Annie & BIU 2015

• The share of revenue for German publishing coming from the US increased notably over

the past year, while the share sourced from Germany showed the greatest decline of any

country.

• As APAC-based publishers expand their influence to overseas markets like Germany,

German publishers will need effective internationalization strategies to compete in an

increasingly globalized mobile gaming market.

0%

25%

50%

75%

100%

Q2 2014 Q2 2015

Share

of A

pp

Sto

re R

eve

nue

Combined iOS App Store & Google Play Game Revenue, German Companies

Germany

Rest of World

United States

The US became increasingly important for German

publishers

© App Annie & BIU 2015

About App Annie

App Annie is the largest mobile app intelligence platform, providing developers and publishers with a 360 -degree view

of what they need to know to build, market and invest in their apps. App Annie is used by over 800,000 apps to track

their performance, and over 400,000 mobile app professionals - including 94 percent of the top 100 publishers - rely

on App Annie to inform their business decisions, including Electronic Arts, Google, LinkedIn, LINE, Microsoft, Nexon,

Nestle, Samsung, Tencent, Bandai Namco, Universal Studios and Dow Jones. App Annie is a privately held global

company headquartered in San Francisco with 12 global offices in cities including Amsterdam, Beijing, London, New

York, Seoul and Tokyo. The company has raised $94 million in funding from e.Ventures, Greycroft Partners, IDG

Capital Partners, Institutional Venture Partners and Sequoia Capital. For more information, please visit:

www.appannie.com or follow App Annie on Twitter: @AppAnnie.

About BIU The BIU is the German Entertainment Software Association for producers and providers of entertainment software in

Germany. The association and its 25 members represent over 85 % of the market for computer and video games in

Germany and are the main contact partner for political and social institutions, the media as well as the general public

when it comes to games. The association was established in 2005 and has its headquarters in Berlin.

Report methodology and updates are available here.

Thank you!

![Toy7 2007 Toys and Games Germany[1]](https://img.pdfslide.net/doc/110x75/5571ff7e49795991699d5f34/toy7-2007-toys-and-games-germany1.jpg)