Embed Size (px)

Citation preview

The Money Market

1

Copyright 2015 Diane Scott Docking

Copyright 2015 Diane Scott Docking 2

Learning Objectives

Define money markets Identify the major types of money market

securities Examine the process used to issue Treasury

securities

Copyright 2015 Diane Scott Docking 3

The Money Markets Defined

The term “money market” is a misnomer. Money (currency) is not actually traded in the

money markets. The securities in the money market are short

term with high liquidity; therefore, they are close to being money.

Copyright 2015 Diane Scott Docking 4

Money Market Securities’ Characteristics

Maturity of ___________________from their ________ date.

Large primary market focus Secondary market for securities

Money market securities are usually sold in large denominations.

They have low default risk.

Copyright 2015 Diane Scott Docking 5

Money Market Instruments

1. Treasury Bills

2. Federal Funds

3. Repurchase Agreements

4. Commercial Paper

5. Negotiable Certificates of Deposit

6. Banker’s Acceptance

7. Eurodollars

Copyright 2015 Diane Scott Docking 6

Treasury Bills

Issued by ________________ Virtually default risk free Interest earned is at state and local

government level. A _________security.

Does not make periodic interest payments.

http://www.treasurydirect.gov/indiv/products/prod_tbills_glance.htm

Copyright 2015 Diane Scott Docking 7

T-Bill Quote Example:

As of June 9, 2015:

Maturity Bid Asked Chg Asked Yield

12/11/2015 0.045 0.040 0.005 0.041

Quote is end of day 6/9/2015, assume 2 days to settle. Settle is = 6/11/2015 (do not count)…12/11/2015 is last trading day

(count). So 183 days to maturity.

http://online.wsj.com/mdc/public/page/2_3020-treasury.html?mod=wsj_mdc_additional_interestrates

Discount Rate Bond Equivalent Yield

Change from yesterday’s closing Asked Quote

Copyright 2015 Diane Scott Docking 8

Bid & Ask Facts

- what dealers will pay for security (or what investors can sell it for)

- what dealers will sell security for (or what investors can buy it for)

- is the dealers profit or markup Bid price Ask price Spread is in T-Bill market because market is so deep

Bid-ask quotes for T-bills are bid yields and ask yields- Bid yields Ask yields- As yields , prices

Copyright 2015 Diane Scott Docking

9

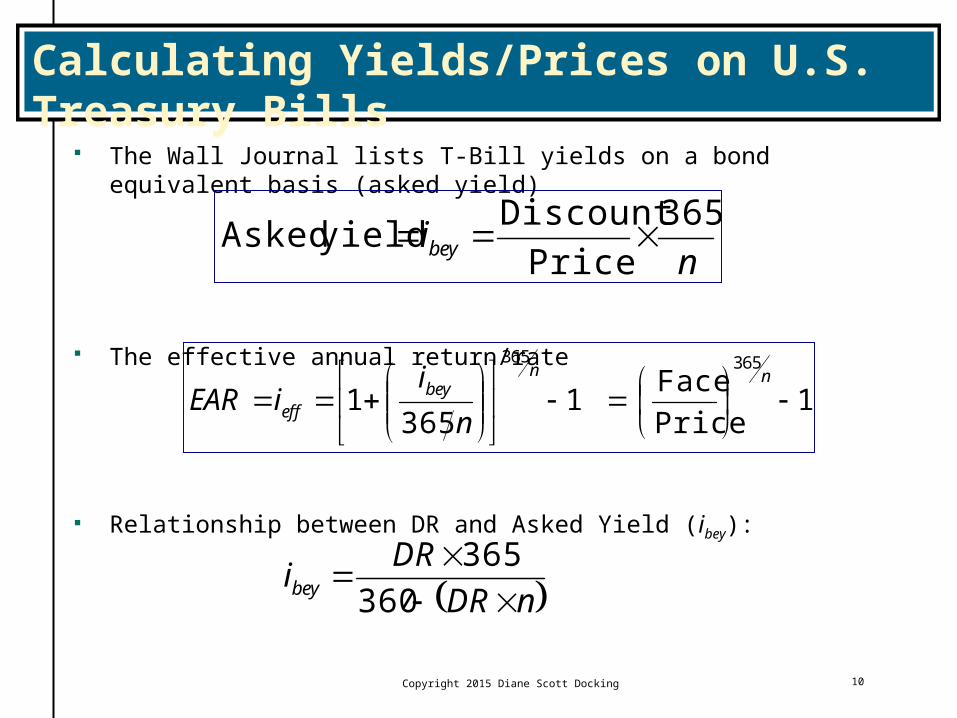

Calculating Yields/Prices on U.S. Treasury Bills

Treasury bills are priced on a discount rate basis, idy or DR, is:

maturity todays PriceFaceDiscount : where

360

Face

DiscountDR

n

ndyi

360 FaceDiscount :where

Discount FacePrice

nidy

Copyright 2015 Diane Scott Docking 10

Calculating Yields/Prices on U.S. Treasury Bills The Wall Journal lists T-Bill yields on a bond equivalent basis (asked yield)

The effective annual return/rate

Relationship between DR and Asked Yield (ibey):

nibey

365

Price

Discount yield Asked

1Price

Face1

3651

365365

nnbey

eff n

iiEAR

nDR

DRibey

360

365

Copyright 2015 Diane Scott Docking 11

Wall Street Journal Example:

Cost to buy $1,000,000 of T-bills:

Asked Yield calculation:

Effective Return calculation:

7$999,796.6

33.203 000,000,1Price

33.203$360

1830004. $1,000,000Discount

0.041%% 040563.000040563.183

365

999,796.67

203.33beyi

%040567.01999,796.67

1,000,000 183365

EAR%040567.01

183365

00040563.1

183365

EAR

Copyright 2015 Diane Scott Docking 12

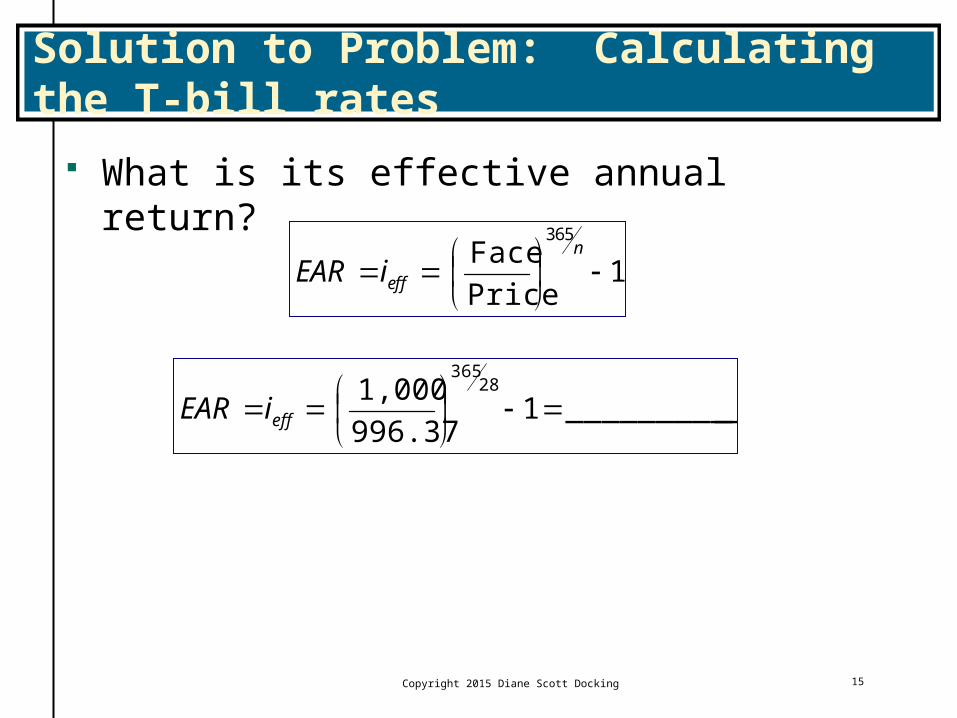

Problem: Calculating the T-bill rates

You pay $996.37 for a 28-day T-bill. It is worth $1,000 at maturity. What is its discount rate? Asked Yield? Effective Annual Return?

Copyright 2015 Diane Scott Docking 13

Solution to Problem: Calculating the T-bill rates

What is its discount rate?

where F = face, P = price, and n = days to maturity

nF

PFiDR dy

360

_________28

360

000,1

37.996000,1

dyiDR

Copyright 2015 Diane Scott Docking 14

Solution to Problem: Calculating the T-bill rates

What is its ask yield (or bond equivalent yield)?

where F = face, P = price, and n = days to maturity

___________28

365

37.996

37.996000,1

beyi

nP

PFibey

365

Copyright 2015 Diane Scott Docking 15

Solution to Problem: Calculating the T-bill rates

What is its effective annual return?

1Price

Face365

n

effiEAR

___________1996.37

1,000 28365

effiEAR

Copyright 2015 Diane Scott Docking 16

T-Bill Auction

All non-competitive bids accepted. Specify quantity only. Maximum bid . Price is the competitive auction yield price.

Noncompetitive Bidding

Copyright 2015 Diane Scott Docking17

T-Bill Auction

Specify price (as a yield %) and quantity desired. Minimum purchase $100 Single price auction used since 1998 Treasury accepts highest bids prices (lowest bid yields) Maximum amount sold to any one buyer is 35% of

offering amount

Competitive Bidding

Treasury Bill Offering

http://www.treasurydirect.gov/instit/annceresult/press/preanre/2014/A_20140123_4.pdf#page=1&zoom=auto,0,761Copyright 2015 Diane Scott Docking 18

Treasury Bill Auction Results

http://www.treasurydirect.gov/instit/annceresult/press/preanre/2014/R_20140127_2.pdfCopyright 2015 Diane Scott Docking 19

T-Bill rates vs. Inflation

Copyright 2015 Diane Scott Docking 20

Copyright 2015 Diane Scott Docking 21

Federal Funds

lending and borrowing Fed district bank debits and credits accounts for purchase

(borrowing) and sale (lending)• Fed Funds _______________________- this is a bank liability. • Fed Funds _____________ - this is a bank asset.

Usually $5 million or more Federal funds rate usually slightly higher than T-bill rate Fed Funds target vs. Actual FF rate Current FF target: http://www.frbdiscountwindow.org/

Effective FF rates: http://www.newyorkfed.org/markets/omo/dmm/fedfundsdata.cfm

360365

ffbey ii

Copyright 2015 Diane Scott Docking 22

Repurchase Agreements (Repo)

Repo Bank Financing – Source of funds – a bank liability “Security sold under agreement to repurchase” at given

price in future.

Reverse Repo Bank Investment/Loan – Use of funds – a bank asset “Security purchased under agreement to resell” at given

price in future.

Copyright 2015 Diane Scott Docking 23

Repurchase Agreements (cont.)

Negotiated market rate. Over telecommunications network Dealers and brokers used or direct placement No secondary market Rate is lower than the fed funds rate, since it is backed up by a

security.

Used by: Federal Reserve in open market operations. Government securities dealers to secure funds to invest in new

Treasury issues. Banks to secure funds to meet temporary liquidity needs as well as

lend funds when they have excess reserves.

Copyright 2015 Diane Scott Docking 24

Estimating Repo Rate

For Repurchase agreements:

Prepo= Repurchase price of security, which equals selling price plus interest

P0= Sales price of the security N=number of days to maturity

nx

P

PPrepo 360rateRepo

0

0

Copyright 2015 Diane Scott Docking 25

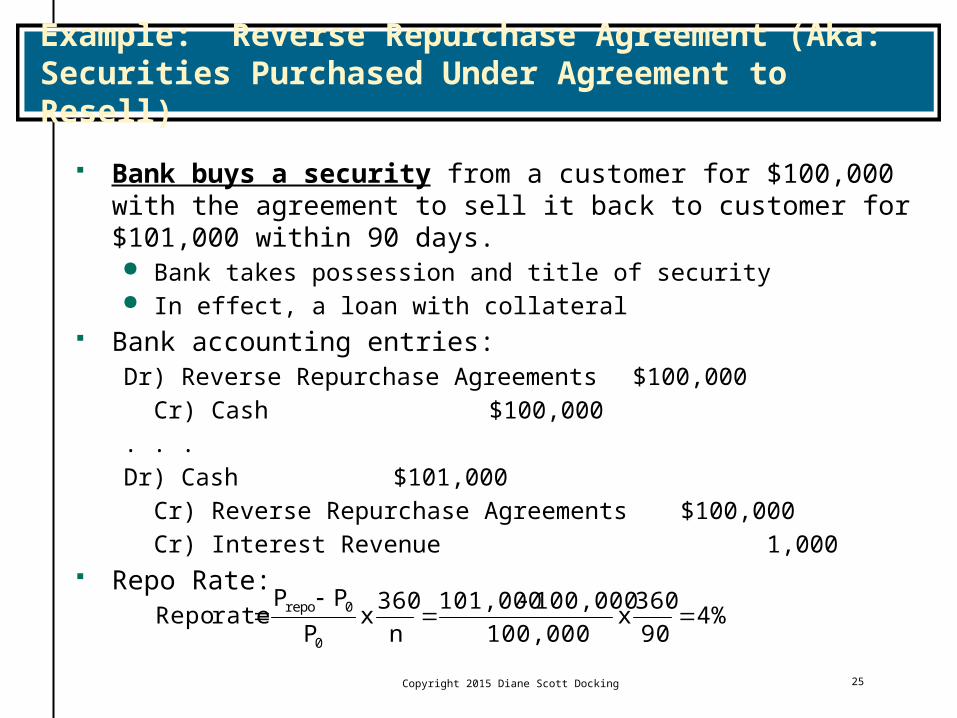

Example: Reverse Repurchase Agreement (Aka: Securities Purchased Under Agreement to Resell)

Bank buys a security from a customer for $100,000 with the agreement to sell it back to customer for $101,000 within 90 days. Bank takes possession and title of security In effect, a loan with collateral

Bank accounting entries:Dr) Reverse Repurchase Agreements $100,000

Cr) Cash $100,000

. . .

Dr) Cash $101,000

Cr) Reverse Repurchase Agreements $100,000

Cr) Interest Revenue 1,000 Repo Rate:

4%90

360x

100,000

100,000101,000

n

360x

P

PPrateRepo

0

0repo

Copyright 2015 Diane Scott Docking 26

Example: Repurchase Agreement (Aka: Securities Sold Under Agreement to RePurchase)

Bank sold its own security to a dealer/bank for $100,000 with the agreement to repurchase it within 90 days for $101,000. The value of the securities that the bank sold was $120,000. Bank releases possession and title of security In effect, a bank debt with security used collateral

Bank accounting entries:Dr) Cash $100,000

Cr) Repurchase Agreement $100,000

Dr) Securities Sold Under Repo $120,000

Cr) AFS Securities $120,000

…..

Dr) Repurchase Agreement $100,000

Dr) Interest Expense 1,000

Cr) Cash $101,000

Dr) AFS Securities $120,000

Cr) Securities Sold Under Repo $120,000

Copyright 2015 Diane Scott Docking 27

Repurchase Agreement (Aka: Securities Sold Under Agreement to RePurchase)

Bank sold its own security to a dealer/bank with the agreement to repurchase it within so many days (say 90 days).

Repo Rate:

4%90

360x

100,000

100,000101,000

n

360x

P

PPrateRepo

0

0Repo

Copyright 2015 Diane Scott Docking 28

Commercial Paper Alternative to bank loan Short-term debt instrument

• Initial maturities ____________ days • Usually ___________ days.

Used only by well-known and creditworthy firms• ________________• Credit ratings important

Minimum denominations of $100,000 Placement

• Directly by a sales force of the borrowing firm.• Indirectly through dealers.

Not a large secondary market (generally held to maturity) Sold at a discount from par – just like T-bills.

Commercial Paper Rates vs. Prime Rates

29Copyright 2015 Diane Scott Docking

Commercial Paper Outstanding

30Copyright 2015 Diane Scott Docking

Copyright 2015 Diane Scott Docking 31

Negotiable Certificates of Deposit

Development of the CD Market Issued by Citibank in 1961. Offset declining demand deposits as a source of funds.

CD Issuers Money center banks and large regional banks are the

primary issuers of domestic CDs

Copyright 2015 Diane Scott Docking 32

Negotiable Certificates of Deposit Characteristics of Negotiable CDs

Large denomination time deposit, less than six month's maturity.• minimum is ______ days• most are less than _________

Negotiable - may be sold and traded before maturity.• Primary market - denominations of at least $100,000. • Secondary market - $1 million or more.

Issued at face value with coupon rate.• Interest computed on a 360 day year.• Rate negotiated between buyer and seller.• Rates higher than on T-Bills

o higher credit risk, lower marketability and higher taxability.

Copyright 2015 Diane Scott Docking 33

Copyright 2015 Diane Scott Docking 34

Example 5-9 in text: Negotiable Certificates of Deposit

Q1: A bank has issued a 6-month (180 day), $1 million NCD with a 0.72% annual interest rate. How much will the NCD holder receive at maturity?

A:

maturity todays where

,360

n

niFaceFaceFV

600,003,1$

600,3000,000,1$

360

1800072.0000,000,1$000,000,1$

FV

Copyright 2015 Diane Scott Docking 35

Example 5-9 in text: Negotiable Certificates of Deposit

Q2: What is the Bond equivalent yield and the EAR?

A:

A.

%73.036036572.0, beyNCDi

360365

,, spNCDbeyNCD ii

1365

1

365

nbey

n

iEAR

%73135.01180365

0073.1

180365

EAR

Copyright 2015 Diane Scott Docking 36

Example 5-9 in text: Negotiable Certificates of Deposit

Q3: Immediately after the CD is issued, the secondary market price falls to $999,651. What is the new bey on the CD, the new EAR, and the new single-payment yield?

A: A:A: iNCD,sp = bey(360/365) = .008010 x 360/365 = 0.79003%

%8026.01180365

008010.1

180365

EAR

Copyright 2015 Diane Scott Docking 37

Example 1: Negotiable Certificates of Deposit

Q1: A bank has issued a 3-month (90 day), $1 million NCD with a 0.80% annual interest rate (current market rates). How much will the NCD holder receive at maturity?

A:

maturity todays where

,360

n

niFaceFaceFV

000,002,1$

000,2000,000,1$

360

900080.0000,000,1$000,000,1$

FV

Copyright 2015 Diane Scott Docking 38

Example 1: Negotiable Certificates of Deposit

Q2: What is the Bond equivalent yield and the EAR?

A:

A.

%8111.036036580.0, beyNCDi

360365

,, spNCDbeyNCD ii

1365

1

365

nbey

n

iEAR

%81358.0190365

008111.1

90365

EAR

Copyright 2015 Diane Scott Docking 39

Example 1: Negotiable Certificates of Deposit

Q3: Thirty days pass. Market rates are now 8.25%. What is the PV of the NCD?

A:

Copyright 2015 Diane Scott Docking 40

Bankers' Acceptances

1. Time draft1. Drafts are drawn on and/or accepted by commercial

bank.

2. Direct liability of bank.

2. Mostly relate to international trade.

3. Secondary market - dealer market.

4. Discounted in market to reflect yield.

5. Standard maturities of 30, 60, 90 days –270 days max.

Copyright 2015 Diane Scott Docking 41

Exhibit: Bankers Acceptance (see chart next page)

1) Importer (U.S.) places P.O. for goods.

2) Exporter (Japan) demands payment before shipment. So, Importer asks American Bank to issue a Letter of Credit.

3) American Bank presents LOC to Japanese Bank.

4) Japanese Bank notifies Exporter that they have a LOC and okay to ship.

5) Exporter ships goods.

6) Exporter sends shipping documents and Time Draft (like an invoice) to Japanese Bank.

7) Japanese Bank sends shipping documents and Time Draft to American Bank.

8) American Bank “stamps” Draft as “accepted” and a BA is created. American Bank will pay owner of BA (i.e. the Draft) so many $ in n-days.

9) American Bank returns BA to Japanese Bank who gives it to Exporter.

10) Exporter can sell BA at its current discounted PV or hold it until maturity.

11) At maturity of BA, Importer pays American Bank, who pays holder of BA.

Copyright 2015 Diane Scott Docking

42

Exhibit: (Bankers Acceptance)

1 Purchase Order

Shipment of Goods5

L/C3

Shipping Documents & Time DraftDraft Accepted (B/A Created)

7 Japanese Bank(Exporter’s Bank)

American Bank(Importer’s Bank)

Importer Exporter

2

L/C

(Le

tter

of C

redi

t) A

pplic

atio

n

4

L/C

Not

ifica

tion

6

Shi

ppin

g D

ocum

ents

& T

ime

Dra

ft

B/A sent to Japanese Bank9

10

B/A

sen

t to

Exp

orte

r w

ho k

eeps

or

sells

it

AB pays holderof B/A at maturity

11B/A created8

Banker’s Acceptance

Copyright 2015 Diane Scott Docking43

Copyright 2015 Diane Scott Docking 44

Eurodollars

Deposits of U.S. dollars in banks located outside the U.S. London interbank bid rate (LIBID)

• The rate paid by banks buying funds

London interbank offer rate (LIBOR)• The rate offered for sale of the funds (rate paid on ED)

Time deposits with fixed maturities Largest short term security market in the

world No reserve requirements at banks outside U.S.